amendments to ias 1

TRANSCRIPT

Page of 1 29

Proposed Amendments to IAS 1 General Presentation and Disclosure Changes

CA Aditya Kumar S.

Prologue

An entity’s financial performance is reflected in its Financial Statements. Over a period of time, the contents of the Financial Statements have been amended to sync with the current business, economic, industrial, regulatory and other requirements. The IASB thought fit to revisit the Presentation and Disclosure aspects of the Financial Statements, and has recommended very significant changes to its form and content. The following document, gives an overview of what these amendments include.

The important presentation and disclosures are :

a. Providing form, content and structure of Balance Sheet and Income Statement.

b. It is now Statement of Profit or Loss and not Statement of Profit and Loss;

c. Complete change in the way Statement of Profit or Loss is prepared. To slice and dice information to main business activities. Each business activity will have it’s own revenue and costing details.

d. Classification of Expenses based on operating, investing and financing categories.

e. Suitable amendments to Statement of Cash Flows

f. Disclosure of Management Performance Measures and it’s reconciliation to totals and sub-totals in financial statements.

g. Changes in the definition of Materiality.

h. Changes in the rules of aggregation and disaggregation of information provided.

Page of 2 29

Statement of Profit or Loss 4 ................................................................................

Statement of Cash Flows 13 ..................................................................................

Other Comprehensive Income 15 ...........................................................................

Statement of Financial Position 16 .........................................................................

Management Performance Measures 17 ..................................................................

Unusual Income and Expenses 22 ..........................................................................

Materiality 24 ........................................................................................................

Indian Scenario 28................................................................................................

Page of 3 29

Statement of Profit or Loss

The Statement of Profit or Loss indicates the financial performance of an entity. This includes

the Revenue from Operations for the period, the related costs, the tax provisions on the net

profit (or loss) and the Earnings Per Share figure. In India, the structure of the structure is

defined under Division II of Schedule III to the Companies Act 2013 and the companies are

mandated to follow the structure indicated in the law. So, in the Indian context, there was very

little leeway for companies to decide on the structure, format and content and any violation on

this account would be regarded as non-compliance under section 129 of the Companies Act 2013

as the financials were not prepared in the manner prescribed. However, this position was quite

different under companies under IFRS regime, since the respective laws did not mandate such

format and structure and there was flexibility amongst the companies to adopt what was

essential for the business. See Table 1 for the difference between the current format and the

proposed format.

The significant changes that IAS 1 proposed to bring in is the following:

a. Classification of income and expenses as follows: a. Operating, b. Integral Associates and Joint Ventures, c. Investing, and d. Financing.

b. Disclosure of Operating Profit c. Splitting of profits or loss on consolidating of Associates and Joint Ventures between Integral

and Non-Integral Associates and Joint Ventures. d. Having specific sub-totals and totals and labelling them. e. Change in the definition of Materiality

Let’s analyse each of the new requirements.

Page of 4 29

Page of 5 29

Table 1: Difference between current and proposed format of Statement of Profit or Loss.

Current Format Proposed Format

I Revenue from Operations I Revenue

II Other Income II Operating Expense

III Total Revenue (I+II) Operating Profit or Loss

IV Expenses III Share of Profit or Loss of Integral Associates and Joint Ventures

Cost of Materials Consumed Operating Profit or Loss and Income and Expenses from Integral Associates and Joint Ventures

Purchases of Stock-in-Trade IV Share of Profit or Loss of non-integral Associates and Joint Ventures

Changes in Inventories of Finished Goods

V Income from Investments

Work-in-Progress and Stock-in-Trade

Profit or Loss before financing and income tax

Employee Benefits VI Interest Revenue from Cash and Cash Equivalents

Finance Cost VII Expenses from Financing Activities

Depreciation / Amortisation VIII Unwinding of discount on pension liabilities and provisions

Finance Costs Profit or Loss Before Tax

Other Expenses

V Total Expenses

VI Profit Before Tax

VII Current Tax

VIII Deferred Tax

Total Taxes

IX Profit / Loss from Discontinuing Operations

X Net Profit After Tax

XI Earnings Per Share

Classification of Expenses:

Operating Category: Excludes Income or Expenses classified in the other categories such as investing category or the financing category, and therefore includes all income and expenses from an entity’s main business activities. Operating category includes:

a. income and expenses from investments made in the course of an entity’s main business activities (including disposal gain / loss on sale of PPE); and

b. Income and expenses from financing activities and income and expenses from cash and cash equivalents if the entity provides financing to customers as a main business activity.

Investing Category: This includes returns from investments, that is, income and expenses from assets that generate a return individually and largely independently of other resources held by the entity and also includes related incremental expenses.

Financing Category: These includes:

a. Income and expenses from cash and cash equivalents; b. Income and expenses on liabilities arising from financing activities; and c. Interest income and expenses one other liabilities, for example, the unwinding of discounts

on pension liabilities and provisions.

What is ‘main business activity’?

This ED does not define ‘main business activity’. Normally, it should be the business of the

entity. However, one of the indications given in ED is, in case of an entity which reports a

segment that constitutes a single business activity, this may indicate that this is a main business

activity. Therefore, this would be a case of management judgement as to what constitutes a

‘main business activity and it could differ from disclosures of operating segments, since the

criteria to determine the segments is clearly articulated in IFRS 8 ‘Operating Segments’. Such,

classification criteria is not available in IAS 1 proposed. Further, IAS 1 proposed, does not even

explicitly mention whether any management judgement involved in determining ‘main

business activity’ needs to be disclosed or not.

Page of 6 29

Can entities have multiple business activity and would that require separate analysis?

Yes, an entity may have multiple

business activity, which is residuary

i.e.,these are not investment or

financing category. In which case, an

entity has to analyse and present the

revenue and the operating

expenses, and the operating profit for

each ‘main business activity’. The

ED also gives an example of a car

manufacturer, who not only sells

cars but also arranges finance for its

customers. Then an entity has to

make an accounting policy choice as

follows:

a. Treat it as a operating category, as though the financing is integral to the main business of

selling the car and classify the income and expense accordingly, or

b. Treat this as income and expenses from financing activities and all income and expenses

from cash and cash equivalents therefore and exclude it from operating category.

Similarly, income and expenses from investments arise in the course of an entity’s main

business activity or is it an ancillary one is a matter of judgement. In general, investments are

likely to have been made in the course of an entity’s main business activity when investment

returns are an important indicator of operating performance. Examples of entities that invest

in the course of ‘main business activities’ may include:

a. Investment entities as defined by IFRS 10 Consolidated Financial Statements;

b. Investment property companies; and

c. Insurers.

Page of 7 29

Therefore, it is imperative to classify and disclose how the ‘main business activity’ is determined

and the yardstick used to determine it. This would also require detailed examination since the

results would be compared and reconciled with what is given in Statement of Cash Flows and

Operating Segment results as well. An entity will classify income and expenses from cash and

cash equivalents in the operating category when such entity invests in financial assets in the

course of its main business activities. It does not apply to an entity that invests only in non-

financial assets in the course of its main business activity.

An example of how a business with multiple business activity would have its Statement of Profit

or Loss is as follows: 1

The example given in the ED indicates that an entity can determine multiple ‘main business

activity’ and has to split its revenue and costs and disclose the Gross Profit form such activities

separately.

The totals and sub-totals given in ED is important and is mandatory to be followed.

How does this affect Segment Reporting?

The above classification may or may not be in sync with operating segments since that

disclosure is based on how the CODM reviews the financials and allocates the resources. Para 16

of IFRS 8 mentions “Information about other business activities and operating segments that are not

reportable shall be combined and disclosed in an ‘all other segments’ category separately from other

reconciling items in the reconciliations required by Para 28. The sources of the revenue included in

the ‘all other segments’ category shall be described.” Para 28(a) requires reconciliation of the total

of the reportable segments’ revenue to the entity’s revenue.

How should an entity give the details of the Cost of Goods Sold?

Hitherto, the Schedule III prescribed the minimum line items under Expenses which was

followed. The Para 68 of ED requires an entity to present the expenses either by nature or by

function, whichever provides the most useful information. Therefore, there is management

judgement as to why a particular classification was chosen. The operating expenses needs to be

classified either of the following basis:

December 2019 - IFRS Standards Exposure Draft ED/2019/7 Illustrative Examples1

Page of 8 29

a. Classification based on the nature i.e.,

the nature of expense method provides

information about operating expenses

arising from the inputs that are

consumed to accomplish an entity’s

activities such as expenses relating to

materials (raw materials), employee

benefits, depreciation / amortisation; or

b. Classification based on the function - i.e., Administrative Costs, Distribution Costs, etc., (See

beside picture. Refer IFRS Staff paper IASB Meeting Analysis of expenses by function and by

nature September 2017). The proposed version of IAS 1, does not specifically define what is

‘function’ and ‘nature,' but one has to gather its meaning through the context in which it is

explained.

So, how would an entity decide which is the most appropriate classification, the proposed ED

prescribes the following tests to be done:

a. What drives the profitability?

b. Test of Business Model?

c. Industry Practice?

d. Others.

Page of 9 29

What about income from Investments, how are they classified?(Para 47 / B32 - B33)

Unless the entity’s main business itself is to invest and earn income, otherwise the income from this

head would include:

a. interest income,

b. fair value gains and losses,

c. dividends from equity investments,

d. gains and losses on disposal,

e. income and expenses on investment property,

f. income and expenses from speculative investments, such investments in artwork held for

capital appreciation,

g. share of profit or loss of non-integral associates and joint ventures;

h. Income and expenses from associates and joint ventures not accounted for using

the equity method.

Example:

a. Say A Ltd., has invested 25% in BC Ltd., It considers investments in BC Ltd., in its

consolidated financial statements as a JV using equity method. Further, BC Ltd., operations

are largely integrated to A Ltd., they also use A Ltd., brand and other IP Rights, and the JV

is basically to meet the regulatory requirements of FDI etc., In this case, BC Ltd., is integral

to the operations of A Ltd., and therefore, it’s profit or loss would not be included above, but

it is a separate line item in Statement of Profit and Loss Account.

Page of 10 29

Category Remarks

Integral Investments

These are Associates and Joint Ventures accounted for using the equity method that are integral to the main business activities of an entity and hence does not generate a return individually and largely independently of the other assets of the entity.

Non-Integral Investments

These are Associates and Joint Ventures accounted for using the equity method that are not integral to the main business activities of an entity and hence generate a return individually and largely independently of the other assets of the entity.

b. Further, the business of BC Ltd., is such that it is dependent on A Ltd., contribution largely;

but it has its own asset based out of which the income is generated. In which case, income

from BC Ltd., would be considered as ‘non-integral’ and the returns would be included in the

Statement of Profit and Loss Account.

c. Say A Ltd., has invested 30% in BC Ltd., and it considers BC Ltd., as a subsidiary (de-facto

control under IFRS 10), then income from BC Ltd., would qualify to be ‘integral’ since in the

consolidated financial statements, A Ltd., does not use equity method to consolidate the

results of BC Ltd., Then the returns on such investments would be included in the

Investment Activity of Statement of Profit or Loss.

d. Say A Ltd., has invested 20% in BC Ltd., But it is neither, a JV nor an Associate and neither

a subsidiary, it is just a passive investment, then this investment qualifies to be ‘integral’.

Then the returns on such investments would be included in the Investment Activity of

Statement of Profit or Loss.

What about income from Financing Activities, how are they classified? (Para 49(a) /

Para B34 - B37)

Financing activities are those involving the receipt or use of a resource from a provider of

finance with the expectation that:

a. the resource will be returned to the provider of finance; and

b. The provider of finance will be compensated through the payment of a finance charge that

is dependent on both the amount of the credit and its duration.

They include:

a. income and expenses from cash and cash equivalents;

b. income and expenses on liabilities arising on other liabilities (debentures, loans, notes,

bonds, lease liabilities, trade payables, fair value of gains and losses of liabilities

designated through profit or loss, dividends on issued shares classified as liabilities);

c. Net interest expense (income) on a net defined benefit liability (asset) under IAS 19 -

Employee Benefits;

d. Unwinding of the discount on a decommissioning, restoration or similar liability;

e. Unwinding of the discount on other long-term provisions;

Page of 11 29

f. Increase in the present value of the costs to sell a non-current asset (or disposal group)

held for sale arising from the passage of time (IFRS 5).

But excludes, income and expenses from cash and cash equivalents if the entity, in the course

of its main business activities, invests in financial assets that generate a return individually and

largely independently of other resources held by an entity i.e., main treasury operations. It also

excludes insurance finance income and expenses (covered under IFRS 17) and income and

expenses on liabilities arising from issued investment contracts with participation features

under IFRS 9.

Note: The ED is not explicit whether one should borrow the definition of ‘cash and cash equivalents’

from IAS 7. If yes, then interest income only from deposits which has original maturity of within

ninety days can only be considered as income from financing activity. Interest income from deposits

which are not classified as cash and cash equivalents will be classified under Investing activity.

How are Foreign Exchange Gain or Losses accounted?

Hitherto, the gains or losses arising out of realisation or restatement of foreign currency

monetary items were shown under a single line item in the Statement of Profit or Loss.

However, now, the foreign exchange gain or losses have to be classified under their respective

activities i.e., operating, financing or investment activities.

How are fair value gains and losses on derivatives and hedging instruments classified?

In case of non-derivatives, classification will be based on depending on its nature i.e., operating, investing or

financing category.

Category Designated as Classification

Used for Risk Management

Hedging Instrument Classify in the category affected by the risk the entity is trying to manage, else investing category.

Used for Risk Management

Not designated as a Hedging Instrument

As above one investing category

Not used for Risk Management

Not Applicable Operating - if used in the main business activity or classify in Investment category.

Page of 12 29

Statement of Cash Flows

The Statement of Cash Flows is covered under IAS 7. This Statement presents the following:

a. Cash flow from operating activities;

b. Cash flow from investing activities;

c. Cash flow from financing activities.

Difference: What’s the difference between operating, investing and financing ‘categories’ vs. operating, investing

and financing ‘activities’ under IAS 7.

Method of Preparation

The cash flow from operating activities were either prepared using the direct method i.e.,

using the accounting records to extract the information relating to realisation from debtors

and payment to creditors , etc., the indirect method envisages using the income statement i.e.,

by adding back non-cash expenses / adjusting non-cash income to profit before tax and

making adjustments to the current assets and current liabilities. The indirect method is the

most widely used and acceptable method since it is easier to do, can be related to Statement of

Profit and Loss and meets the regulatory requirements as well.

Classification Per ED IAS 1 IAS 7

Operating Other than Investment and Financing Principal revenue-producing activities of the entity and other activities that are not investing or financing activities

Investment Includes returns from Investments from assets that generate a return individually and largely independent of other resources held by the entity.

Acquisition and Disposal of long-term assets and other investments not included in cash equivalents

Financing Income and Expenses from Cash and Cash equivalents, liabilities from financing activities and interest income and expenses on such liabilities.

Activities that result in changes in the size and composition of the contributed equity and borrowings of the entity.

Page of 13 29

So what has changed now under the ED?

The method of preparing the Statement of Cash Flow is largely the same, but certain aspects

have to be noted:

a. Considering the change in the components in Statement of Profit or Loss, the starting point to

start the cash flow statement will be from the operating profit. (Para 18(b) of IAS 7)

b. Cash flow from investments in integral and non-integral associates and joint ventures to be

presented separately. (Para 38 of IAS 7)

c. Reconsider how the dividend and interest will be reclassified based on the current proposed

changes.

The following table gives examples of the classification of certain items will vary between

Statement of Profit or Loss and Statement of Cash Flows.

Particulars Classification in Statement of Profit or Loss

Classification in Statement of Cash Flow

Profit or Loss on sale of Property Plant and Equipment (PPE)

Operating Investment

Profit or Loss on sale of Building which is rented out.

Operating / Investing Investment

Foreign Exchange Gain or Loss Operating / Investing / Financing Operating

Derivative losses Operating / Investing Operating

Interest Income Operating / Investment Operating

Profit or Loss on Sale of Investments in Associate / JV

Investment / Separate line item Investment

Disposal of Non-Current Assets held for sale

Separate line item Operating

Dividend Paid Operating / Financing Financing

Dividend Received Operating / Financing Investing

Page of 14 29

Other Comprehensive Income

There is no change in the current structure of Other Comprehensive Income, however

additional disclosures / modifications in the presentation are:

a. share of other comprehensive income of associates and joint ventures accounted for using the

equity method, presenting separately as integral and non-integral;

b. Other items of other comprehensive income classified by their nature i.e., those which are

permanently reported outside Statement of Profit or Loss and those which will be reported in

Statement of Profit or Loss in future.

Page of 15 29

Statement of Financial Position

This is also referred to as Balance Sheet, which presents the assets and liabilities as of a

particular date. The ED does not propose to make any changes to the structure of the Balance

Sheet, except for additional line items containing investments in integral or non-integral

associates and joint ventures, and, consequent new line items on introduction of IFRS 17.

Page of 16 29

Management Performance Measures

The Management Performance Measures (‘MPM’) are the

metrics that the Management prefers to communicate the

performance of their entity in public communication (apart

from the contents of the financial statements), which would provide

additional information to the stakeholders or readers of financial

statements. For example: A Management may discuss about EBITDA

(Earnings Before Interest, Tax, Depreciation and Amortisation), or ROCE (Return on Capital

Employed) or FOCF (Free Operating Cash Flows), etc., The Non-GAAP measures (also commonly

referred to as ‘Alternative Performance Measures (‘APM’)’ or ‘Key Performance Indicators (‘KPI’)

are quite different since they include information which are not part of the contents of the

financial statements. However, some of the Annual Reports have used APM as MPM also.

Regulators around the world (For Example: Guidelines on APM by European Securities and

Markets Authority [ESMA) in 2015, Statement on Non-Gaap Financial Measures issued by

International Organisation of Securities Commissions (IOSCO) in 2016, Regulatory Guide 230 -

Disclosing non-IFRS financial information 2011 by Australia) have issued various guidelines on

the use of financial APMs. However, these guidelines were applicable in respective jurisdictions

to whom the guidelines apply but not as part of financial statements. IAS 1 now brings in these

disclosures within the purview of financial statements and mandate the requirements relating to

its appropriateness, presentation and disclosure aspects.

The following are some of the sub-totals or totals from the financial statements not considered

as MPM:

a. Any total or sub-total of only income or expense; b. Gross Profit or Loss or similar sub-totals; c. Operating Profit or Loss before depreciation and amortisation; d. Profit or Loss from continuing operations; e. Profit or Loss Before Income Tax.

Any other information provided related to financial performance or financial position or cash flows etc., which cannot be directly related are MPM.

Page of 17 29

What is the disclosure requirement?

Hitherto, these metrics were just part of say Management Commentary, Director’s Report, etc.,

which did not cast an obligation on the Management to relate to the financial statements. The

Standard setters have felt that these numbers should be part of the financial statements and

should be reconciled to the sub-totals or totals in the financial statements.

Following is the extract of Annual Report of Covestro for the year 2019.

Page of 18 29

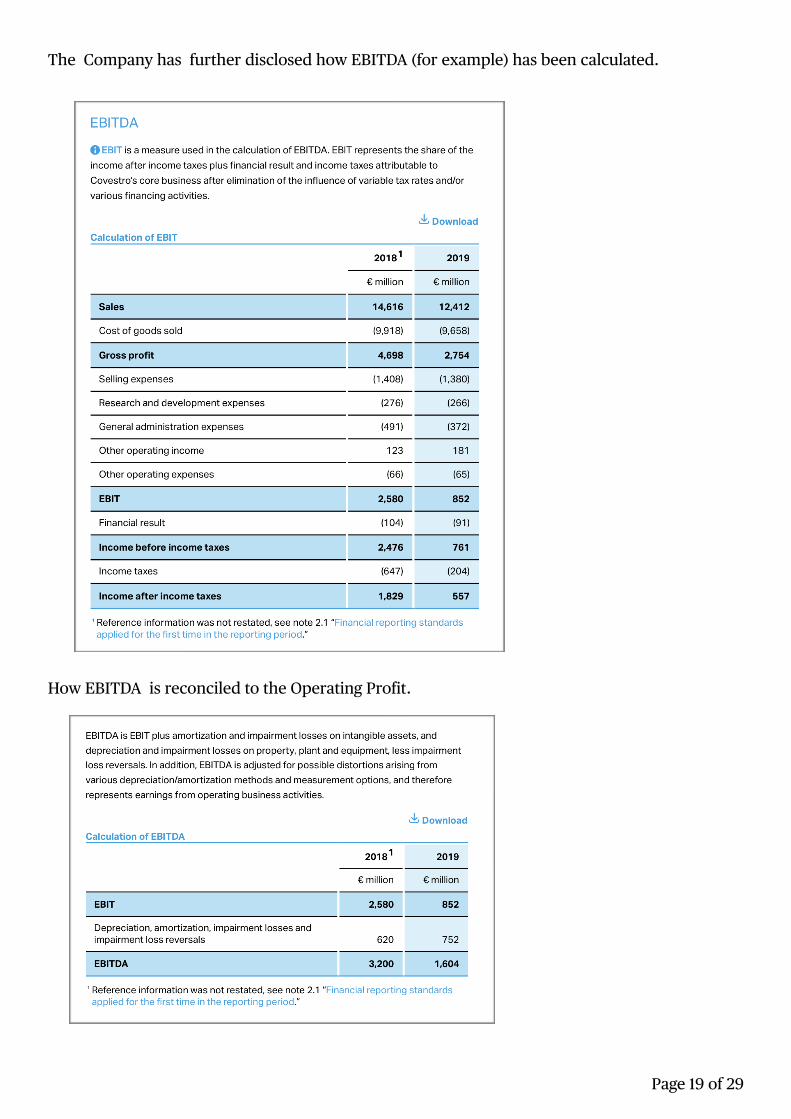

The Company has further disclosed how EBITDA (for example) has been calculated.

How EBITDA is reconciled to the Operating Profit.

Page of 19 29

Example of Disclosure of Free Operating Cash Flows

Disclosure Requirements under the ED:

a. Note on why and how MPM communicates management's view of performance; b. Enlist the MPM; c. How is MPM calculated; d. How does MPM provide useful information about the entity's performance; e. Reconciliation between MPM and most directly comparable sub-total or total in financial statements;

f. Income Tax effect on the non-controlling interest for each item disclosed in the reconciliation, if applicable;

g. How was the income tax effect calculated?

Page of 20 29

What if the Management change the metrics?

If there is any change in the metrics, whether is on account of addition or deletion or modification of the existing ones, the management has to disclose the following:

a. Explain why the change was required; b. How is the change be more meaningful / useful; c. Give comparative information

Page of 21 29

Unusual Income and Expenses

The Statement of Profit or Loss indicates the performance during the year / period. However, there could be circumstances which could lead to transactions which are not recurring in nature or are say not in the

regular course of business. IFRS did not permit disclosure of such items as ‘extra-ordinary items’. Though, it did require disclosure material transactions which, by volume could be 'exceptional ones’. What’s the differentiating factor between ‘extra-ordinary’ and ‘exceptional’?

Extra-ordinary items are income or expenses that arise from events or transactions that are clearly distinct from the ordinary activities of the enterprise and, therefore, are not expected to recur frequently or regularly. For example, loss due to a natural calamity could be an extra-ordinary event, which is not expected to recur.

Exceptional items are those which do occur regularly but because of some reason, the volume or the value of the transaction is unusually very low or very high. For example, a company would have disposed of its fixed assets or written down its inventory to net realisable value which is way lower than the cost, etc.,

So, what is the change expected from ED?

ED defines ‘unusual income and expenses’ as 'Income and expenses with limited predictive value. Income and expenses have limited predictive value when it is reasonable to expect that income or expenses that are similar in type and amount will not arise for several future annual reporting periods’.

It appears that the term ‘Unusual Income and Expenses’ encompasses elements of both extra-ordinary and exceptional items, going with the following examples given in the ED:

a. Impairment loss recognised on account of a fire accident. This incident is not reasonably expected to recur in several annual reporting period, hence loss would be unusual;

b. Higher litigation costs incurred on a particular case. There could be other litigation costs, but in one reporting period, it seems to be higher, then it is unusual.

c. An entity which is making a series or string of acquisitions, acquisition cost may not be ‘unusual,' but one of a case could be so.

So, what is ‘unusual’ is a matter of professional judgement, at times. Income or expenses are classified as ‘unusual’ based on expectations about the future rather than past occurrences . Whether an item of income or expense is unusual in amount is determined by the range of outcomes reasonably expected to arise for that income or expense in several future annual reporting period. (Para B69 / B70 of ED.)

Page of 22 29

Other aspects to be considered:

a. Expectations of what could happen in future is a matter of judgement, hence the term used is ‘predictive’. What if an incident classified as ‘unusual’ repeats itself? For example, a fire accident. Then, would it mean that in the subsequent period it is ‘not unusual’ since it repeated. The ED only mentions whether it could have been predicted before, which is definitely not possible and hence in the second year also any loss due to fire accident would be treated as ‘unusual’.

b. When an income is classified as ‘unusual,' the related costs towards such ‘income’ would also be classified as ‘unusual’ only if such costs also meet the definition of ‘unusual income or expense’.

What is the disclosure requirement?

a. Amount of each item of unusual income or expense; b. Narrative description of the transaction or other events that give rise to this unusual income

or expense; c. Line item in Statement of Profit or Loss where this is included; d. Analysis of expense by nature or by function (whichever the entity has chosen in Statement

of Profit or Loss); e. If any MPM include such unusual income or expense, it shall disclose within the MPM

disclosure section.

Page of 23 29

Materiality

Financial Statements are expected to fairly present the financial position and financial performance of an entity for a period of time. In the course of preparation of the financial statements due

care must be taken to ensure it is in compliance with the respective financial reporting framework, regulatory requirements, industry practices, etc., In the Indian context, The Framework for the Preparation and Presentation of Financial Statements issued by The Institute of Chartered Accountants of India mentions that ‘users are assumed to have a reasonable knowledge of business and economic activities and accounting and a willingness to study the information with reasonable diligence’. It is important how the information provided in the financial statements could impact the decision of the reader of the financial statements.

In September 2017, IASB also released a Practice Statement 2 ‘Making Materiality Judgements’ as part of a project to provide guidance on making materiality judgements and help others involved in the financial reporting to understand how a company makes materiality judgements in the preparation of financial statements. The objective of the Practice Statement is to promote a behavioural change in the way companies prepare their financial statements, encouraging a greater application of judgement. The Board also proposes to change 2

‘Significant Accounting Policies’ to ‘Material Accounting Policies’ with a requirement to clarify the threshold for disclosing information.

Old Definition New Definition

Material Omissions o r misstatements of items are material if they could, individually or collectively, influence the economic decisions that users make on the basis of the financial statements.

Information is material if omitting, misstating or obscuring it could reasonably be expected to influence decisions that primary users of general purpose financial statements make on the basis of those financial statements, which provide financial information about a specific reporting entity.

September 2017 IFRS Practice Statement - Project Summary and Feedback Statement - Making Materiality Judgements, Practice Statement 2.2

Page of 24 29

What is ‘obscuring information’ or ‘reasonably be expected…” phrases?

Obscuring information means to camouflage information in such a manner that it would be difficult to be identified or one should read ‘between the lines’ to understand the true meaning of the information provided. And IAS 1 has pushed the limit from its earlier definition of ‘influence the economic decision’ to ‘reasonably be expected to influence decision’ as well. Some companies would have provided the information, which can be viewed or identified as quickly as any other information available, because of the way it is presented, language used, part of a big paragraph wherein lot of efforts have to be put to understand, use of complex language or words, etc., For example:

a. If an information can be provided in a tabular format, which is reader friendly has been given in a paragraph which is difficult to comprehend.

b. Too many cross-references to a particular note, to deliberately confuse the reader;

c. Giving prominence to one set of information and not others.

d. Notes on the same topic, dispersed in too many places in the reporting pack.

e. Use of highly technical language or legal language, which a general reader may not be able to comprehend.

f. Providing superfluous information or irrelevant for the users.

So, the whole thing is ‘The key to making decisions about whether information is material is not to focus on the information in isolation. Rather, the question becomes one of whether the primary users to whom the financial report is directed are likely to want that information included in the report”. 3

It’s a pure judgemental call.

Disclosure on what is the threshold considered for materiality

Well, the IFRS practice statement does not specifically require any specific mention of materiality (unlike International Standards of Auditing where the auditors have to report on what materiality level has been chosen for the audit), it would be imperative for the users to know this information while reading the financial information. (personal view).

https://www2.deloitte.com/content/dam/Deloitte/ch/Documents/audit/ch-en-audit-thinking-allowed-materiality.pdf3

Page of 25 29

Materiality Vs. Relevance: At times what is ‘relevant’ for preparing the financial statements may not be ‘material’ enough. For example, in an assessment of whether a lease is a operating lease or a financial lease on a case to case basis is relevant for the purpose of preparing financials, but it does not mean that the entire decision making process of how it was evaluated , etc., are explained in a detailed manner. The financials may still provide a brief note on how these are evaluated using the information available, but should not be elaborate that other information, which is more important for the primary users of financials are shrouded within it.

The Practice Statements prescribes a four-step materiality process which is given herewith:

The four step approach is applied as follows:

a. Determine who the primary users of financial statements are and what information do they expect from it?

b. To decide how best such information can be presented and disclosed and ensure that it does not obscure the information they are looking out for.

c. Present the information in a meaningful manner

d. Review the information and it’s ‘relevance’ with other financial / GAAP or Non-GAAP information.

Page of 26 29

General characteristics of materiality:

a. To identify who are ‘primary users’ and what would be their expectations from financial statements. They could be present and potential investors, lenders, creditors, government and regulatory authorities, employees, etc., This depends on case to case basis. What is expected is the company should be able to provide the possible information needs of these users of financial statements, regardless of the fact whether such information is available in public domain or not? Normally, companies can determine what are the expectations of the primary users through their interaction during investor meet, analyst meet, local corporate governance information needs, intimation of specific information to the stock exchanges / regulators on a periodical basis, local industry / economic requirements.

b. The IFRS also gives credence that the local laws and regulations could play a role in specific presentation and disclosure requirements as well. IFRS permits such information as required by the local or regulatory authorities to be provided in financials though it may not be material under IFRS, however such additional information should not obscure other material information.

c. Materiality should also factor in other specific topics including whether prior-period information needs to be provided and to what extent, to consider whether an error is material by applying the same consideration as in given in the identifying materiality, possible breach of covenants, to apply the same materiality factors for interim financial reporting period as well, etc., One has to go on case-to-case basis to determine the materiality aspect.

Qualitative and Quantitative Factors

Quantitative Factors: These are decided based on the monetary limits. When disclosing a specific total or sub-total in the financial statements, in becomes to decide on what would be the materiality limit considering the fact that the financial statements should not be containing trivial information or information which may not add any value (sheerly because of it’s volume). However, some of the items say related party transactions, key managerial personnel remuneration , etc., are required top e disclosed irrespective of the monetary limit. IAS 1 also gives examples of ‘unusual income or expenses’ which could quality to be one of the items to be disclosed under quantitative factors.

Qualitative Factors: These are those which cannot be quantified in terms of monetary value. But are very significant for the primary users of the financial statements. They include say, impact of COVID-19, Brexit, new regulatory requirements, potential loss of business, new business started by the company, outcome or status of specific litigations, etc.,

Page of 27 29

Indian Scenario

In India, the financial reporting framework for companies are quite different. For corporate entities, Companies (Accounting Standards) Rules 2006 and Companies (Indian Accounting Standards) Rules 2015, as amended over a period of time. For non-corporate entities, the Accounting Standards as issued by The Institute of Chartered Accountants of India will prevail. The Companies (Indian Accounting Standards) Rules, 2015 also called as ‘Ind AS’ came into force from the financial year 2016-2017.

Ind AS is converged to IFRS i.e., except for few carve outs to suit the Indian business / economic requirements. The numbering of the Standards, its content , etc., are based on IFRS. Any change in IFRS will also trigger consequent change to Ind AS, to ensure it is converged.

Firstly, the form, content and structure of the financial statements of the corporates are largely governed by Schedule III (Division 1 and Division 2) of the Companies Act 2013. Therefore, any amendment to the structure of the financial statements would also need amendment to the Companies Act accordingly.

Secondly, in case of MPM and other KPI, it is also important for regulators like SEBI and RBI also to step in give their direction like how other regulators are provided.

Third, there has to be a clarification on whether MPM is part of financial statements, what would be the role of auditors to audit and comment on them.

The Indian corporate world has successfully integrated Ind AS, and not to forget India was the first economy to adopt Ind AS 109 (avatar of IFRS 9) when the most advanced economies also pushed it by a year. Therefore, there would be no stone unturned by the corporates and the professionals to meet the new requirements of IAS 1, as and when it becomes applicable.

Page of 28 29

Page of 29 29

Disclaimer: The views expressed in this document should not be construed to be a professional advice or mandate or to solicit any professional work. The views expressed are strictly personal and does not represent the views of the firm where the author works. No action can be taken by any reader on the author based on the assertions given in this document. The author would not be liable for any action taken by anybody based on this document. The content of this books is the sole expression and opinion of the author, and not necessarily that of the organisation he represents. No warranties or guarantees are expressed or implied by the author herein. The author shall not be liable for any physical, psychological, emotional, financial or commercial damages, including, but not limited to, special, incidental, consequential or other damage. This document does not certify or guarantee completeness and accuracy of information mentioned. The document contains material sourced from various sources, which has been duly provided in the footnotes or any other place as appropriate. The author does not claim any intellectual property rights or ownership over such material or content and neither have or intended or attempted to express any comments / opinions on such contents whether it is relating to its completeness, accuracy, reliability or any other aspect, and have been used only as a reference source. The contents, including, the pictures / graphical images belong to the respective owners who created it. It is expected that the reader of the document shall be responsible for their own choices, actions and results. This document is intended to serve as an information or guidance about the subject matter dealt with. Author will not be responsible, if the reader is not able to obtain credible results. The author would advice the reader to take opinion / advice from a competent professional for any specific queries / issues / questions.