ambit gdp6

DESCRIPTION

Ambit GDP6TRANSCRIPT

Ambit Capital and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, investors should be aware that Ambit Capital may have a conflict of interest that could affect the objectivity of this report. Investors should not consider this report as the only factor in making their investment decision.

Please refer to the Disclaimers at the end of this Report.

AMBIT INSIGHTS 27 August 2014

DAILY

G&C 8.0-Quality at a reasonable price

Company name Weight (%) Rating FY15

P/E (x)

Bajaj Auto 4.5 BUY 17.3

Tata Motors 4.5 BUY 8.9

Bank of Baroda 4.5 BUY 7.2

ICICI Bank 4.5 BUY 16.3

I D F C 4.5 UR 11.3

Grasim Inds 4.5 NR 14.2

HCL Technologies 4.5 BUY 15.3

TCS 4.5 BUY 22.5

Coal India 4.5 BUY 13.3

NMDC 4.5 NR 9.5

Oil India 4.5 BUY 7.9

O N G C 4.5 BUY 10.6

Bharti Airtel 4.5 NR 27.6

Power Grid Corpn 4.5 BUY 12.4

McLeod Russel 2.3 NR 11.5

ING Vysya Bank 2.3 BUY 15.2

DCB Bank 2.3 NR 11.6

Castrol India 2.3 NR 34.4

TTK Prestige 2.3 BUY 39.0

Marico 2.3 BUY 29.4

Bharat Electron 2.3 BUY 13.8

Sadbhav Engg. 2.3 BUY 42.8

eClerx Services 2.3 NR 14.4

D B Corp 2.3 NR 16.5

Petronet LNG 2.3 SELL 18.6

Cadila Health. 2.3 NR 25.0

Oberoi Realty 2.3 BUY 16.3

Sobha Developer. 2.3 BUY 15.3

Vardhman Textile 2.3 NR 5.8

Torrent Power 2.3 BUY 12.7

Source: Bloomberg, Ambit Capital research

NR = Not Rated

UR = Under Review

Updates

Economy

FY16 GDP growth estimate of 6%

(Click here for detailed note)

Oil & Gas

Upstream companies subsidy burden to decline?

Power Grid Corporation (BUY)

Capitalisation momentum sustainable

Analyst Notes: Capital Goods: FII ban revoked in defence sector; BEL is the best defence play Tanuj Mukhija, CFA, +91 22 3043 3203

Continuing with its policy initiatives that encourage investment in Defence equipment manufacturing, the government revoked the FII ban in defence sector imposed on August 2013 alongside easing of FDI norms (now more than one domestic player can own the minimum 51% stake in a JV with a foreign firm). Over the last two months, the government had (a) put an end to the DPSU monopoly (56 aircraft AVRO project); (b) hiked the FDI limit to 49%; and (c) streamlined the licensing process. Domestic companies with technical capability, manufacturing base and financial strength are best placed to form JVs with global majors and capitalise on the US$106bn opportunity over FY14-19. Bharat Electronics (BUY, TP Rs2,082/share), a key beneficiary of new government policies, would maintain its market leadership in defence electronics industry owing to superior manufacturing base and increasing focus on (a) in-house R&D and (b) technology collaborations leading to 82% of sales from indigenized products. Source: Ambit Capital research

Analyst Notes: BFSI: Competition continues to intensify in home loans Pankaj Agarwal, CFA, +91 22 3043 3206

Yesterday, SBI cut its home loan rates by 5bps on loans <Rs7.5mn to 10.10% and by 15bps on loans >Rs7.5bn to 10.15%. This follows ICICI and HDFC reducing rates on high ticket size loans earlier this month in response to foreign banks becoming aggressive in high ticket size segment. With slowing corporate credit growth and better asset quality in mortgages, the segment has become fiercely competitive. This is visible in most banks offering home loans at base rate vs ~50bps premium 2 years back and the pricing differential between loans below Rs3mn and above Rs3mn disappearing vs 25-50bps premium 2 years back. With now banks being allowed to raise bonds with regulatory exemptions to fund home loans, competition should further intensify. Moreover, intense government scrutiny on corporate loans and thin tier-1, we expect most PSU banks to be more active in this segment going forward. Competitive intensity coupled with future regulatory changes on transparent and fair pricing for old borrowers and closing regulatory arbitrage between banks and NBFCs suggests a tough outlook for specialised mortgage lenders HDFC & LIC Hsg.

Ambit Capital and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, investors should be aware that Ambit Capital may have a conflict of interest that could affect the objectivity of this report. Investors should not consider this report as the only factor in making their investment decision.

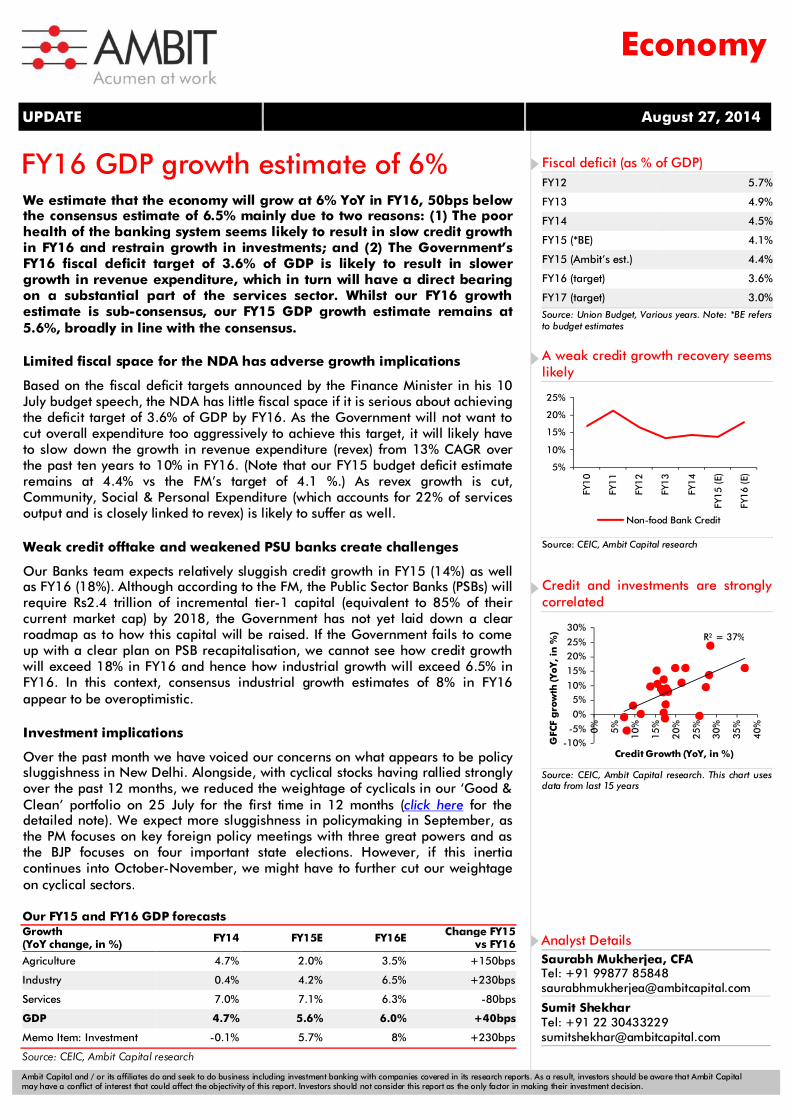

FY16 GDP growth estimate of 6% We estimate that the economy will grow at 6% YoY in FY16, 50bps below the consensus estimate of 6.5% mainly due to two reasons: (1) The poor health of the banking system seems likely to result in slow credit growth in FY16 and restrain growth in investments; and (2) The Government’s FY16 fiscal deficit target of 3.6% of GDP is likely to result in slower growth in revenue expenditure, which in turn will have a direct bearing on a substantial part of the services sector. Whilst our FY16 growth estimate is sub-consensus, our FY15 GDP growth estimate remains at 5.6%, broadly in line with the consensus.

Limited fiscal space for the NDA has adverse growth implications

Based on the fiscal deficit targets announced by the Finance Minister in his 10 July budget speech, the NDA has little fiscal space if it is serious about achieving the deficit target of 3.6% of GDP by FY16. As the Government will not want to cut overall expenditure too aggressively to achieve this target, it will likely have to slow down the growth in revenue expenditure (revex) from 13% CAGR over the past ten years to 10% in FY16. (Note that our FY15 budget deficit estimate remains at 4.4% vs the FM’s target of 4.1 %.) As revex growth is cut, Community, Social & Personal Expenditure (which accounts for 22% of services output and is closely linked to revex) is likely to suffer as well.

Weak credit offtake and weakened PSU banks create challenges

Our Banks team expects relatively sluggish credit growth in FY15 (14%) as well as FY16 (18%). Although according to the FM, the Public Sector Banks (PSBs) will require Rs2.4 trillion of incremental tier-1 capital (equivalent to 85% of their current market cap) by 2018, the Government has not yet laid down a clear roadmap as to how this capital will be raised. If the Government fails to come up with a clear plan on PSB recapitalisation, we cannot see how credit growth will exceed 18% in FY16 and hence how industrial growth will exceed 6.5% in FY16. In this context, consensus industrial growth estimates of 8% in FY16 appear to be overoptimistic.

Investment implications

Over the past month we have voiced our concerns on what appears to be policy sluggishness in New Delhi. Alongside, with cyclical stocks having rallied strongly over the past 12 months, we reduced the weightage of cyclicals in our ‘Good & Clean’ portfolio on 25 July for the first time in 12 months (click here for the detailed note). We expect more sluggishness in policymaking in September, as the PM focuses on key foreign policy meetings with three great powers and as the BJP focuses on four important state elections. However, if this inertia continues into October-November, we might have to further cut our weightage on cyclical sectors.

UPDATE August 27, 2014

Economy

Analyst Details Saurabh Mukherjea, CFA Tel: +91 99877 85848 [email protected]

Sumit Shekhar Tel: +91 22 30433229 [email protected]

Fiscal deficit (as % of GDP) FY12 5.7%

FY13 4.9%

FY14 4.5%

FY15 (*BE) 4.1%

FY15 (Ambit’s est.) 4.4%

FY16 (target) 3.6%

FY17 (target) 3.0%

Source: Union Budget, Various years. Note: *BE refers to budget estimates

A weak credit growth recovery seems likely

Source: CEIC, Ambit Capital research

Credit and investments are strongly correlated

Source: CEIC, Ambit Capital research. This chart uses data from last 15 years

5%

10%

15%

20%

25%

FY10

FY11

FY12

FY13

FY14

FY15 (E)

FY16 (E)

Non-food Bank Credit

-10%-5%

0%

5%10%

15%

20%25%

30%

0%

5%

10%

15%

20%

25%

30%

35%

40%

GFC

F g

row

th (Y

oY, i

n %

)

Credit Growth (YoY, in %)

Our FY15 and FY16 GDP forecasts Growth (YoY change, in %) FY14 FY15E FY16E Change FY15

vs FY16

Agriculture 4.7% 2.0% 3.5% +150bps

Industry 0.4% 4.2% 6.5% +230bps

Services 7.0% 7.1% 6.3% -80bps

GDP 4.7% 5.6% 6.0% +40bps

Memo Item: Investment -0.1% 5.7% 8% +230bps

Source: CEIC, Ambit Capital research

R² = 37%

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 27 August 2014

Oil & Gas Upstream companies subsidy burden to decline? Press reports suggest that Oil Ministry has proposed to the Government that (a) upstream companies and Government equally share FY15 subsidy burden of ~Rs980bn and (b) upstream companies be relieved of the subsidy burden to the extent of cess paid by them (~Rs100bn p.a.). If this proposal is accepted, it would imply a net crude realisation of US$70-75/bbl for ONGC and Oil India, significantly higher than US$41-47/bbl in FY14 and our assumption of US$58-60/bbl (in-line with historical trend). We however believe the proposal is unlikely to be accepted as it would imply that the Government has to bear Rs590bn in FY15 vs balance fuel subsidy provision of Rs225bn.

However, ONGC and Oil India stock prices currently factor in a perpetual net crude realisation that is ~US$5-10/bbl lower than the historical average (US$58-60/bbl) and a gas price of only US$5/mmbtu. Hence, we reiterate our BUY stance as decline in under-recovery burden and clarity on crude and gas realisation are likely to be key triggers for stock prices.

Event: Press reports suggest that Oil Ministry has proposed to the Government that upstream companies (ONGC, Oil India) and Government equally share (50% each) FY15 subsidy burden of ~Rs980bn. Further, Oil Ministry is suggesting that upstream companies be relieved of the subsidy burden to the extent of the Oil Industry Development (OID) cess paid by them. Government has levied OID cess on nominated fields of ONGC and Oil India, which amounts to Rs100bn p.a. Hence, Oil Ministry is proposing that Upstream companies bear Rs390bn as subsidy in FY15 (50% of Rs980bn less cess of Rs100bn), implying a net crude realisation of US$70-75/bbl. This is significantly higher than net crude realisation of US$41-47/bbl reported in FY14 and our assumption of US$58-60/bbl (in-line with historical trend). For every US$1/bbl higher net crude realisation, our valuation for ONGC and Oil India goes up by 1.4-1.7%.

Our view

We believe the Oil Ministry proposal is unlikely to be accepted as it is too aggressive and would imply that the Government has to bear Rs590bn in FY15. As per the fuel subsidy provision created for FY15 budget, the Government is left with only Rs225bn for FY15 (Rs573bn provision created for FY15 less Rs348bn already paid for FY14 subsidy provision).

The subsidy share of upstream companies has increased from 33% (Rs320bn) in FY09 to 48% (Rs670bn) in FY14. Though we expect FY15 under-recoveries to decline sharply to Rs870bn (from Rs1,398bn in FY14), we have assumed upstream companies still bear Rs520-540bn going forward, implying upstream PSUs would be allowed net crude realisation of ~US$58/bbl (in-line with historical average and as suggested by Kirit Parikh committee’s October 2013 report ).

Kirit Parikh committee formula for calculating upstream companies subsidy burden – implies net crude realisation of US$55-60/bbl

Crude Price Subsidy contribution (%) of upstream companies

Net crude realisation (FY15) as per formula (US$/bbl)

US$80/bbl 40% of crude price 48

US$90/bbl 40% of crude price + 0.25% for each US$1/bbl increase beyond US$80/bbl up to US$120/bbl

52

US$100/bbl 55

US$110/bbl 58

US$120/bbl 50% of crude price 60

Source: MOPNG, Ambit Capital research

POSITIVE Quick Insight Analysis Meeting Note News Impact

ONGC BUY Bloomberg Code: ONGC IN

CMP (Rs): 418

TP (Rs): 500

Mcap (Rs bn/US$ bn): 3,576/59.0

3M ADV (Rs mn/US$ mn): 3,101/51.2

Oil India BUY Bloomberg Code: OINL IN

CMP (Rs): 590

TP (Rs): 684

Mcap (Rs bn/US$ bn): 355/5.9

3M ADV (Rs mn/US$ mn): 299/4.9

Analysts

Dayanand Mittal, CFA [email protected] Tel: +91 22 3043 3202

Parita Ashar [email protected] Tel: +91 22 3043 3223

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 27 August 2014

For FY15-16, we assume that: (a) upstream PSUs would be allowed net crude realisation of ~US$58/bbl; and (b) OMCs would be allowed to earn a RoE of 10-13%. This would imply that upstream PSUs share 60% of FY15 and 95% of FY16 under-recovery burden whilst OMCs share 3-5% of FY15-FY16 burden. This would mean that the Government’s share of fuel subsidy burden falls to 37% in FY15 (down from 51% in FY14) and that the government doesn’t bear any fuel subsidy burden from FY16 onwards.

Subsidy sharing computation

FY12 FY13 FY14 FY15E FY16E Total Under-recovery (Rs bn) 1,386 1,704 1,398 871 571 Subsidy sharing (Rs bn)

Upstream PSUs 550 635 671 522 543 Government 835 1,058 707 322 0 OMCs 0 11 21 26 29

Subsidy sharing (%) Upstream PSUs 39.7% 37.3% 48.0% 60.0% 95.0% Government 60.3% 62.1% 50.5% 37.0% 0.0% OMCs 0.0% 0.6% 1.5% 3.0% 5.0%

Key Matrix ONGC net crude realisation (US$/bbl) 54.7 47.9 41.0 57.8 57.8 Oil India net crude realisation (US$/bbl) 59.8 53.6 47.1 57.4 57.9 BPCL RoE 5.0% 11.4% 21.6% 15.2% 14.6% HPCL RoE 1.3% 3.7% 7.9% 10.3% 12.8% IOCL RoE 7.2% 5.9% 10.6% 11.4% 11.0%

Source: Companies, Ambit Capital research

ONGC and Oil India- Best BUYs in the sector: We expect the Government to: (a) deregulate diesel prices in FY15 through the monthly price hike; and (b) take marginal price hikes in cooking fuel, which should result in under-recoveries declining by 50-60% to Rs871bn/Rs571bn in FY15/FY16, down from Rs1,381bn in FY14. Further, we expect the Government to provide clarity on net crude and gas realisation, which could drive the next leg of re-rating for upstream PSUs. However, ONGC / Oil India's share price factors in a perpetual net crude realisation that is ~US$5-10/bbl lower than the average (US$58-60/bbl) and a gas price of only US$5/mmbtu. Despite assuming that upstream PSUs bear 100% of the subsidy burden from FY16 onwards (vs 50% in FY14), their net crude realisation could rise to ~US$58-60/bbl (vs US$41-47 in FY14). ONGC is trading at 9.3x FY16 P/E (five-year average of 10.0x) and Oil India is trading at 7.1x FY16 P/E (five year average of 8.8x). Decline in under-recovery burden and clarity on crude and gas realisation are key triggers.

ONGC’s valuation sensitivity to net gas price realisation and net crude price realisation ( Rs)

Net crude price realisation (US$/bbl)

Net gas price realisation (US$/mmbtu)

45 50 55 58 60 65 4.2 343 378 411 433 447 482 5.0 373 408 442 463 477 512 6.0 411 446 479 500 514 549 7.0 448 483 517 538 552 587 8.0 486 521 554 575 589 624

Source: Ambit Capital research Note: Our base case is highlighted in grey shade and the assumptions factored in the CMP are highlighted in pink shade

Oil India’s valuation sensitivity to net gas price realisation and net crude price realisation ( Rs)

Net crude price realisation (US$/bbl)

Net gas price realisation (US$/mmbtu)

45 50 55 58 60 65 4.2 432 494 555 591 615 676 5.0 473 536 596 632 656 717 6.0 525 587 648 684 708 768 7.0 576 639 699 735 759 820 8.0 628 690 751 787 811 871

Source: Ambit Capital research; Note: Our base case is highlighted in grey shade and the assumptions factored in the CMP are highlighted in pink shade

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 27 August 2014

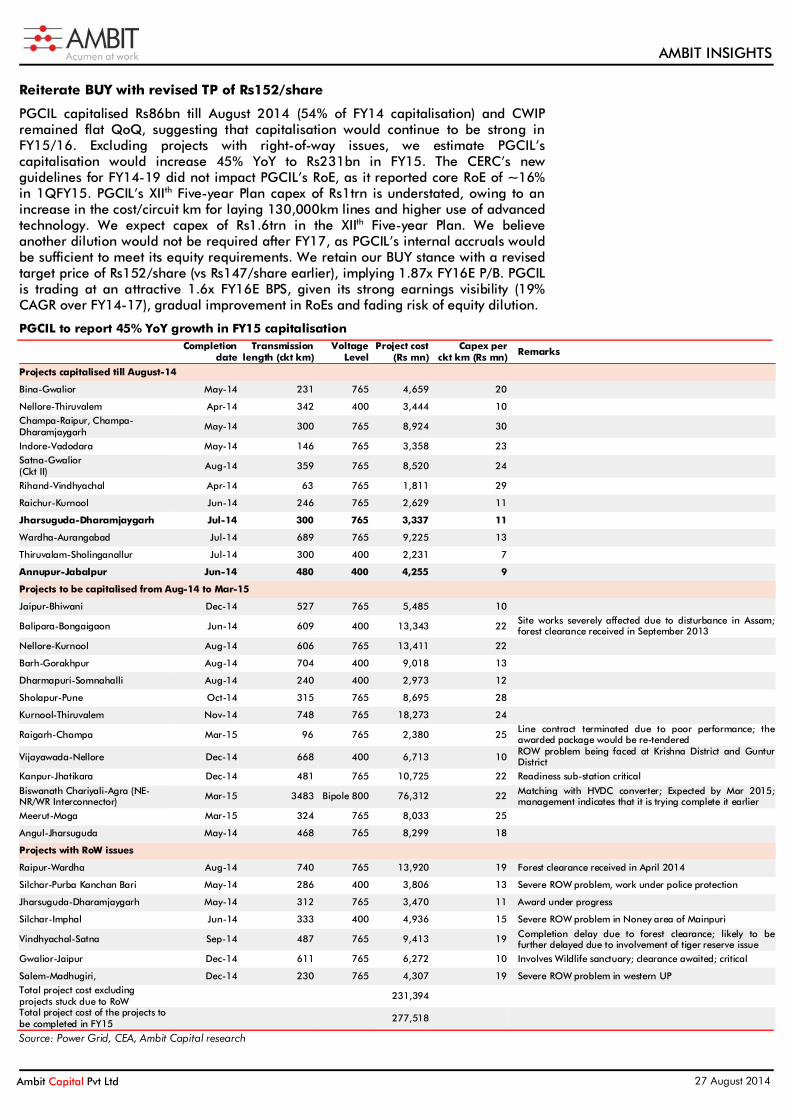

Power Grid Corporation Capitalisation momentum sustainable Power Grid’s execution of projects with right of way (RoW) issues (i.e. Jharsuguda–Dharamjaygarh worth ~Rs3.4bn and Annupur–Jabalpur worth ~Rs4.3bn) and resolution of RoW at the Angul-Jharsuguda project (worth ~Rs8.3bn) underpin an upgrade to our FY15 capitalisation estimate to Rs231bn (from Rs211bn earlier), which is higher than consensus’ estimate. The CERC’s new tariff guidelines for FY14-19 did not impact PGCIL’s RoE, as it reported core 1QFY15 RoE of ~16% on regulated equity. PGCIL’s XIIIth Five-year Plan capex of Rs1trn is understated, owing to an increase in the cost/circuit km for laying 130,000km lines and higher use of advanced technology; we expect Rs1.6trn capex in the XIIIth Five-year Plan. PGCIL would retain its monopoly, owing to its unmatched competitive advantages and the sharp decline in competitive intensity of tariff bid projects. Our revised TP of Rs152/share (vs Rs147/share earlier) implies 1.9x FY16E BPS alongside 19% earnings CAGR over FY14-17.

Upgrading FY15 capitalisation estimate to Rs231bn (higher than consensus)

We had highlighted in our note, ‘Investments to bear fruit’, that excluding projects with right of way issues, PGCIL would report a sharp 33% YoY rise in FY15 capitalisation to Rs211bn. PGCIL reported capitalisation of Rs48.7bn in 1QFY15 (up 65% YoY). PGCIL capitalised assets worth Rs85bn as on August 2014 (54% of total capitalisation in FY14), higher than our expectations, as it operationalised two projects with right of way issues: Jharsuguda–Dharamjaygarh worth ~Rs3.4bn and Annupur–Jabalpur worth ~Rs4.3bn. In addition, the right of way issue at the Angul-Jharsuguda 765kV transmission line worth ~Rs8.3bn has been resolved. Thus, we have upgraded our FY15 capitalisation estimate by Rs20.2bn to Rs231.4bn, higher than consensus. However, we have marginally cut our FY15/16E EPS estimates by ~1-2% led by: (1) lower transmission O&M cost escalation under the new CERC guidelines, (2) cut in consulting EBIT margin post the completion of the Myanmar project in 1QFY15, and (3) lower-than-expected 1QFY15 revenues in the telecommunications segment.

PGCIL’s capital expenditure for XIIIth Five-year Plan understated

PGCIL plans to add 130,000ckt km in the XIIIth Five-year Plan with an investment of ~Rs1 trillion vs Rs1.1 trillion in the XIIth Five-year Plan to add 107,00ckt km. We believe PGCIL’s capex requirement is understated due to an increase in the cost/ckt km and spend on advanced technology such as smart grids and gas-insulated sub-stations. We estimate PGCIL’s XIIIth Five-year Plan capex would be Rs1,664bn based on capacity addition of 121GW in the XIIIth Five-year Plan, higher than the Ministry of Power’s estimate of 93.4GW.

Competitive intensity fading in tariff bid projects

The number of bidders has materially declined in the last five projects to 3-4 from more than 10 bidders for the initial projects. The difference between the L1 and L2 bidder has declined to ~10%, except for the Unchahar TPS project, implying that the competition intensity has declined. PGCIL has unmatched competitive advantages such as its ability to raise low-cost debt and its strong execution skills that will enable it to retain its near monopoly in transmission.

BUY Quick Insight Analysis Meeting Note News Impact

Stock Information Bloomberg Code: PWGR IN

CMP (Rs): 132

TP (Rs): 152

Mcap (Rs bn/US$ mn): 685/11.3

3M ADV (Rs mn/US$ mn): 1,082/17.9

Stock Performance (%)

1M 3M 12M YTD

Absolute (3) 3 37 31

Rel. to Sensex (4) (4) (10) 6

Source: Bloomberg, Ambit Capital research

Ambit Estimates (Rs bn)

FY15 FY16 FY17

Capitalisation 231 227 237 Revenues 183 219 258 EPS (Rs) 10.4 12.2 14.4 Source: Bloomberg, Ambit Capital research

Analysts

Nitin Bhasin [email protected] Tel: +91 22 3043 3241

Tanuj Mukhija, CFA [email protected] Tel: +91 22 3043 3203

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 27 August 2014

Reiterate BUY with revised TP of Rs152/share

PGCIL capitalised Rs86bn till August 2014 (54% of FY14 capitalisation) and CWIP remained flat QoQ, suggesting that capitalisation would continue to be strong in FY15/16. Excluding projects with right-of-way issues, we estimate PGCIL’s capitalisation would increase 45% YoY to Rs231bn in FY15. The CERC’s new guidelines for FY14-19 did not impact PGCIL’s RoE, as it reported core RoE of ~16% in 1QFY15. PGCIL’s XIIth Five-year Plan capex of Rs1trn is understated, owing to an increase in the cost/circuit km for laying 130,000km lines and higher use of advanced technology. We expect capex of Rs1.6trn in the XIIth Five-year Plan. We believe another dilution would not be required after FY17, as PGCIL’s internal accruals would be sufficient to meet its equity requirements. We retain our BUY stance with a revised target price of Rs152/share (vs Rs147/share earlier), implying 1.87x FY16E P/B. PGCIL is trading at an attractive 1.6x FY16E BPS, given its strong earnings visibility (19% CAGR over FY14-17), gradual improvement in RoEs and fading risk of equity dilution.

PGCIL to report 45% YoY growth in FY15 capitalisation

Completion

date Transmission

length (ckt km) Voltage

Level Project cost

(Rs mn) Capex per

ckt km (Rs mn) Remarks

Projects capitalised till August-14

Bina-Gwalior May-14 231 765 4,659 20

Nellore-Thiruvalem Apr-14 342 400 3,444 10

Champa-Raipur, Champa-Dharamjaygarh

May-14 300 765 8,924 30

Indore-Vadodara May-14 146 765 3,358 23

Satna-Gwalior (Ckt II)

Aug-14 359 765 8,520 24

Rihand-Vindhyachal Apr-14 63 765 1,811 29

Raichur-Kurnool Jun-14 246 765 2,629 11

Jharsuguda-Dharamjaygarh Jul-14 300 765 3,337 11 Wardha-Aurangabad Jul-14 689 765 9,225 13

Thiruvalam-Sholinganallur Jul-14 300 400 2,231 7

Annupur-Jabalpur Jun-14 480 400 4,255 9 Projects to be capitalised from Aug-14 to Mar-15

Jaipur-Bhiwani Dec-14 527 765 5,485 10

Balipara-Bongaigaon Jun-14 609 400 13,343 22 Site works severely affected due to disturbance in Assam; forest clearance received in September 2013

Nellore-Kurnool Aug-14 606 765 13,411 22 Barh-Gorakhpur Aug-14 704 400 9,018 13 Dharmapuri-Somnahalli Aug-14 240 400 2,973 12 Sholapur-Pune Oct-14 315 765 8,695 28 Kurnool-Thiruvalem Nov-14 748 765 18,273 24

Raigarh-Champa Mar-15 96 765 2,380 25 Line contract terminated due to poor performance; the awarded package would be re-tendered

Vijayawada-Nellore Dec-14 668 400 6,713 10 ROW problem being faced at Krishna District and Guntur District

Kanpur-Jhatikara Dec-14 481 765 10,725 22 Readiness sub-station critical

Biswanath Chariyali-Agra (NE-NR/WR Interconnector)

Mar-15 3483 Bipole 800 76,312 22 Matching with HVDC converter; Expected by Mar 2015; management indicates that it is trying complete it earlier

Meerut-Moga Mar-15 324 765 8,033 25

Angul-Jharsuguda May-14 468 765 8,299 18

Projects with RoW issues

Raipur-Wardha Aug-14 740 765 13,920 19 Forest clearance received in April 2014

Silchar-Purba Kanchan Bari May-14 286 400 3,806 13 Severe ROW problem, work under police protection

Jharsuguda-Dharamjaygarh May-14 312 765 3,470 11 Award under progress

Silchar-Imphal Jun-14 333 400 4,936 15 Severe ROW problem in Noney area of Mainpuri

Vindhyachal-Satna Sep-14 487 765 9,413 19 Completion delay due to forest clearance; likely to be further delayed due to involvement of tiger reserve issue

Gwalior-Jaipur Dec-14 611 765 6,272 10 Involves Wildlife sanctuary; clearance awaited; critical

Salem-Madhugiri, Dec-14 230 765 4,307 19 Severe ROW problem in western UP Total project cost excluding projects stuck due to RoW

231,394

Total project cost of the projects to be completed in FY15

277,518

Source: Power Grid, CEA, Ambit Capital research

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 27 August 2014

Change in assumptions (Rs bn)

Old estimates New estimates Change in Estimates

FY15E FY16E FY17E FY15E FY16E FY17E FY15E FY16E FY17E

Capital Expenditure 237.7 252.3 244.6 237.7 259.7 252.0 - 2.9 3.0

Capitalisation 211.6 220.1 229.9 231.4 226.8 236.8 9.3 3.0 3.0

Revenues 183.2 216.8 253.8 183.4 218.9 257.6 0.1 1.0 1.5

YoY growth (%) 20.3% 18.3% 17.1% 20.4% 19.4% 17.7% 13bps 106bps 59bps

Transmission Revenues 175.5 208.2 244.4 176.1 210.9 248.7 0.4 1.3 1.8

YoY growth (%) 22.6% 18.7% 17.4% 23.1% 19.8% 17.9% 44bps 108bps 59bps

Consultancy 4.4 4.9 5.4 4.4 4.9 5.4 - - -

Telecom 3.2 3.5 3.8 2.7 3.0 3.3 (13.6) (13.6) (13.6)

EBITDA 156.6 186.0 218.7 157.1 188.7 222.9 0.3 1.4 1.9

EBITDA margin 85.5% 85.8% 86.2% 85.6% 86.2% 86.5% 14bps 35bps 34bps

Net depreciation 46.4 55.3 65.2 47.8 57.6 68.0 3.2

4.1

4.3

Interest and financial charges 39.4 46.8 54.9 40.9 49.0 57.3 3.9 4.6 4.3

Average interest rate 8.3% 7.9% 7.6% 8.3% 8.0% 7.6% Other income 4.1 3.2 3.3 4.7 4.2 4.3 PBT before EO 75.0 87.1 101.9 73.0 86.4 101.8 (2.7) (0.8) (0.0)

Adjusted PAT 55.4 64.1 74.7 54.2 64.0 75.2 (2.3) (0.2) 0.6

EPS (Rs) 10.6 12.3 14.3 10.4 12.2 14.4 (2.3) (0.2) 0.6

RoE 15.2% 15.8% 16.4% 14.9% 15.9% 16.6% -31bps 4bps 17bps

Total Debt 935.7 1074.4 1189.2 949.5 1092.9 1212.6 Gross debt to equity 0.71 0.72 0.71 0.71 0.72 0.72 Gross block 1176.7 1396.8 1649.9 1196.4 1423.2 1683.3 1.7 1.9 2.0

Gross block YoY growth 21.9% 18.7% 18.1% 24.0% 19.0% 18.3% CFO 130.2 173.2 204.2 129.4 174.6 208.6 (0.6) 0.8 2.2

FCFF (107.5) (79.1) (40.4) -108.3 -85.1 (43.4) BVPS 73.2 81.8 91.9 72.8 81.4 91.6 -0.5 -0.5 -0.3

Source: Power Grid, CEA, Ambit Capital research

Relative valuation PGCIL vs global transmission players

PGCIL has a monopoly in inter-state grid transmission wherein its revenues and return on equity are regulated by the CERC. We have selected global peers for PGCIL based on two key parameters: regulated business model (leading to assured returns) and monopoly in power transmission. Based on the above criteria, we have identified Terna Spa (Italy) and Red Electrica (Spain) as true peers of PGCIL. PGCIL is trading at a 27%/47% discount to Terna/Red Electrica on one-year forward P/B. PGCIL is trading at a discount to Terna owing to lower RoEs and higher cost of equity (12.5% for PGCIL vs 10.6% for Terna).

PGCIL - Relative valuation vs global peers

Companies Mcap Revs

(US$ mn) Revenues EBITDA margin (%)

PAT margin (%)

RoE (%)

RoIC (%)

Net Debt: equity P/E (x) P/B (x)

US$ mn FY14 CAGR FY14-16 FY15 FY15 FY15 FY14 FY14 FY15E FY16E FY15E FY16E

PGCIL 11,333 2,583 16.9 85.1 29.7 14.6 6.2 2.17 13.0 10.9 1.9 1.6

Red Electrica 11,487 2,355 4.2 74.5 30.2 23.7 9.2 2.44 15.6 14.9 3.6 3.3

Terna Spa 10,506 2,450 4.3 76.6 26.7 17.0 4.9 2.41 15.7 14.9 2.6 2.5

Average 14.8 13.6 2.7 2.5

Source: Bloomberg, Company, Ambit Capital research; Note: Priced as on 27 August 2014

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 27 August 2014

PGCIL trading at a premium to domestic regulated business model companies

As mentioned earlier, PGCIL has a regulated business model, resulting in guaranteed RoEs of 15.5% on capitalisation of transmission assets. Whilst no power transmission companies are listed in India (excluding PGCIL), GAIL (a gas transmission company) and power generation companies such as NTPC and NHPC also have regulated business models. PGCIL is trading at a 46% premium to NTPC and a 137% premium to NHPC on one-year forward price to book, due to PGCIL’s higher RoEs. GAIL, a gas transmission company, also has a regulated business model. Based on the gas transmission guidelines designed by the Petroleum and Natural Gas Regulatory Board (PNGRB), GAIL is entitled to RoCEs of 12% on its capital investments. PGCIL is trading at a 19% premium to GAIL on account of higher revenue growth in FY14-16E and higher RoEs.

PGCIL - Relative valuation vs regulated players in India

Companies Mcap Rev

(US$mn) Revenues EBITDA margin (%)

PAT margin (%)

RoE (%)

RoIC (%)

Net Debt: equity P/E (x) P/B (x)

US$ mn FY13 CAGR FY14-16 FY15 FY15 FY15 FY14 FY14 FY15E FY16E FY15E FY16E

PGCIL 11,333 2,583 16.9 85.1 29.7 14.6 6.2 2.17 13.0 10.9 1.9 1.6

NTPC 19,225 13,071 6.2 22.8 12.0 11.0 7.3 0.65 12.0 11.0 1.3 1.2

NHPC 3,835 1,228 5.2 65.0 29.7 7.9 3.4 0.41 10.1 9.1 0.8 0.7

Gail 9,111 9,358 7.5 11.3 6.2 13.7 9.0 0.40 12.1 11.2 1.6 1.4

Average 11.8 10.5 1.3 1.2

Source: Bloomberg, Company, Ambit Capital research; Note: Priced as on 27 August 2014

Cross-cycle valuations PGCIL is trading at 1.9x FY15E BPS, 22% premium to its three-year average, due to higher visibility of FY15 capitalisation and the XIIIth Five-year Plan investment outlay. PGCIL has historically traded at a discount to its global peers such as Terna and Red Electrica owing to PGCIL’s lower RoEs. PGCIL’s P/B multiples declined sharply in 2HCY13, as the company announced the FPO plan, followed by a subsequent announcement for divestment by the Government. However, since then the valuations have recovered materially as not only company reported better capitalisation but the general market sentiment improved. We expect it to trade at marginally higher multiple from hereon as the QoQ capitalisation momentum continues.

PGCIL trading at a discount to its European peers on one-year forward P/B (x)

Source: Bloomberg, Ambit capital research

PGCIL trading 22% above its three-year average one-year forward P/B (x)

Source: Bloomberg, Ambit Capital research

0

1

2

3

4

Jun-

10

Sep-

10

Dec

-10

Mar

-11

Jun-

11

Sep-

11

Dec

-11

Mar

-12

Jun-

12

Sep-

12

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

PWGR IN REE SM TRN IM

1.0

1.2

1.4

1.6

1.8

2.0

2.2

Jun-

10Se

p-1

0D

ec-1

0M

ar-1

1Ju

n-11

Sep-

11

Dec

-11

Mar

-12

Jun-

12Se

p-1

2D

ec-1

2M

ar-1

3Ju

n-13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

1-year forward P/B average 1-year forward PB

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 27 August 2014

Increase in capitalization to capex ratio would lead to…

Source: Ambit Capital research, Company

….19% EPS CAGR over FY14-17 and uptick in RoE over FY14-17

Source: Ambit Capital research, Company

Key catalysts Higher-than-expected FY15 capitalisation: Capitalisation is the key driver for

PGCIL’s revenue and net profit, as the company earns regulated RoEs of 15.5% on the equity invested in transmission assets. We expect capitalisation of Rs644bn over FY14-17E which would lead to 18% revenue CAGR in FY14-17E. In our opinion, the key catalyst for PGCIL would be if the company meets/exceeds our capitalisation target of Rs231bn for FY15. Nearly 17% of PGCIL’s transmission projects worth Rs 46bn scheduled for completion in FY15 are delayed due to delays in forest clearance. We believe on-time execution of transmission projects would lead to higher revenues and higher operating cash flows.

Increase in XIIIth Five-year Plan capex by Ministry of Power (MoP): We believe that the Ministry of Power has underestimated the transmission capex for the XIIIth Five-year Plan. We expect PGCIL’s capex would be Rs1,664bn excluding the green energy investment, materially higher than the MoP estimate of ~Rs1,000bn. We believe XIIIth Five-year Plan’s capex upgrade would increase the earnings growth visibility for PGCIL.

0.68

0.69

0.70

0.71

0.72

0.73

0

50

100

150

200

250

300

FY13 FY14 FY15E FY16E FY17E

Capex (Rs bn)Capitalization (Rs bn)Debt-to-capital employed (x, RHS)

10%

12%

14%

16%

18%

0%

5%

10%

15%

20%

25%

30%

35%

FY13 FY14 FY15E FY16E FY17E

RoE (RHS) Net profit growth YoY

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 27 August 2014

Standalone income statement

Particulars (Rs bn) FY14 FY15E FY16E FY17E

Revenue 152.3 183.4 218.9 257.6

EBITDA 129.6 157.1 188.7 222.9

EBITDA margin 85.1% 85.6% 86.2% 86.5%

Net depreciation 40.0 47.8 57.6 68.0

Net interest 31.7 40.9 49.0 57.3

Other income 4.9 4.7 4.2 4.3

Provision for taxation 17.7 18.9 22.4 26.7

Consolidated Adjusted PAT 45.2 54.2 64.0 75.2

PAT margin 0.3 0.3 0.3 0.3

EPS (Diluted) Rs. 8.6 10.4 12.2 14.4

Source: Company, Ambit Capital research

Standalone balance sheet

Particulars (Rs bn) FY14 FY15E FY16E FY17E

Total Networth 345 381 426 479

Loans 795 950 1,093 1,213

Sources of funds 1,209 1,405 1,600 1,780

Gross Block 965 1,196 1,423 1,683

Net block 733 917 1,086 1,278

Capital work-in-progress 317 323 356 348

Construction stores and advances 176 176 176 176

Investments 10 10 10 10

Cash and bank balances 44 38 33 36

Current Liabilities 172 175 198 223

Net current assets (52) (46) (53) (57)

Source: Company, Ambit Capital research

Standalone cash flow statement

Particulars (Rs bn) FY14E FY15E FY16E FY17E

EBIT 89.6 109.2 131.1 154.9

Change in working capital 42.8 (10.8) 5.9 9.4

CFO 160.4 129.4 174.6 208.6

Purchase of fixed assets (304.0) (237.7) (259.7) (252.0)

CFI (299.1) (233.0) (255.5) (247.7)

CFF 102.8 97.2 76.2 41.9

Change In Cash (35.9) (6.4) (4.7) 2.8

Free cash flow (143.6) (108.3) (85.1) (43.4)

Source: Company, Ambit Capital research

Key ratios

Particulars FY14 FY15E FY16E FY17E

Net debt/Equity 2.2 2.4 2.5 2.5

ROCE 5.9% 6.2% 6.5% 6.8%

ROE (including other income) 14.9% 14.9% 15.9% 16.6%

BVPS 70 73 81 92

DPS (Rs) 2.6 2.8 3.1 3.6

P/E (x) 13.4 11.2 9.5 8.1

P/B (x) 2.0 1.8 1.6 1.4

Source: Company, Ambit Capital research

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 27 August 2014

Institutional Equities Team

Saurabh Mukherjea, CFA CEO, Institutional Equities (022) 30433174 [email protected]

Research

Analysts Industry Sectors Desk-Phone E-mail

Nitin Bhasin - Head of Research E&C / Infra / Cement / Industrials (022) 30433241 [email protected]

Aadesh Mehta Banking / Financial Services (022) 30433239 [email protected]

Achint Bhagat Cement / Infrastructure (022) 30433178 [email protected]

Aditya Khemka Healthcare (022) 30433272 [email protected]

Ashvin Shetty, CFA Automobile (022) 30433285 [email protected]

Bhargav Buddhadev Power Utilities / Capital Goods (022) 30433252 [email protected]

Dayanand Mittal, CFA Oil & Gas / Metals & Mining (022) 30433202 [email protected]

Deepesh Agarwal Power Utilities / Capital Goods (022) 30433275 [email protected] Gaurav Mehta, CFA Strategy / Derivatives Research (022) 30433255 [email protected]

Karan Khanna Strategy (022) 30433251 [email protected]

Krishnan ASV Real Estate (022) 30433205 [email protected]

Pankaj Agarwal, CFA Banking / Financial Services (022) 30433206 [email protected]

Paresh Dave Healthcare (022) 30433212 [email protected]

Parita Ashar Metals & Mining / Oil & Gas (022) 30433223 [email protected]

Pratik Singhania Retail (022) 30433264 [email protected]

Rakshit Ranjan, CFA Consumer / Retail (022) 30433201 [email protected]

Ravi Singh Banking / Financial Services (022) 30433181 [email protected]

Ritesh Gupta, CFA Midcaps – Chemical / Retail (022) 30433242 [email protected]

Ritesh Vaidya Consumer (022) 30433246 [email protected] Ritika Mankar Mukherjee, CFA Economy / Strategy (022) 30433175 [email protected]

Ritu Modi Automobile (022) 30433292 [email protected]

Sagar Rastogi Technology (022) 30433291 [email protected]

Sumit Shekhar Economy / Strategy (022) 30433229 [email protected]

Tanuj Mukhija, CFA E&C / Infra / Industrials (022) 30433203 [email protected]

Utsav Mehta Technology (022) 30433209 [email protected]

Sales

Name Regions Desk-Phone E-mail

Sarojini Ramachandran - Head of Sales UK +44 (0) 20 7614 8374 [email protected]

Deepak Sawhney India / Asia (022) 30433295 [email protected]

Dharmen Shah India / Asia (022) 30433289 [email protected]

Dipti Mehta India / USA (022) 30433053 [email protected]

Hitakshi Mehra India (022) 30433204 [email protected]

Nityam Shah, CFA USA / Europe (022) 30433259 [email protected]

Parees Purohit, CFA UK / USA (022) 30433169 [email protected]

Praveena Pattabiraman India / Asia (022) 30433268 [email protected]

Production

Sajid Merchant Production (022) 30433247 [email protected]

Sharoz G Hussain Production (022) 30433183 [email protected]

Joel Pereira Editor (022) 30433284 [email protected]

Nikhil Pillai Database (022) 30433265 [email protected]

E&C = Engineering & Construction

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 27 August 2014

Explanation of Investment Rating Investment Rating Expected return

(over 12-month period from date of initial rating)

Buy >5%

Sell <5%

Disclaimer

This report or any portion hereof may not be reprinted, sold or redistributed without the written consent of Ambit Capital. AMBIT Capital Research is disseminated and available primarily electronically, and, in some cases, in printed form.

Additional information on recommended securities is available on request.

Disclaimer 1. AMBIT Capital Private Limited (“AMBIT Capital”) and its affiliates are a full service, integrated investment banking, investment advisory and brokerage group. AMBIT Capital is a Stock Broker, Portfolio

Manager and Depository Participant registered with Securities and Exchange Board of India Limited (SEBI) and is regulated by SEBI 2. The recommendations, opinions and views contained in this Research Report reflect the views of the research analyst named on the Research Report and are based upon publicly available information

and rates of taxation at the time of publication, which are subject to change from time to time without any prior notice. 3. AMBIT Capital makes best endeavours to ensure that the research analyst(s) use current, reliable, comprehensive information and obtain such information from sources which the analyst(s) believes to

be reliable. However, such information has not been independently verified by AMBIT Capital and/or the analyst(s) and no representation or warranty, express or implied, is made as to the accuracy or completeness of any information obtained from third parties. The information or opinions are provided as at the date of this Research Report and are subject to change without notice.

4. If you are dissatisfied with the contents of this complimentary Research Report or with the terms of this Disclaimer, your sole and exclusive remedy is to stop using this Research Report and AMBIT Capital shall not be responsible and/ or liable in any manner.

5. If this Research Report is received by any client of AMBIT Capital or its affiliate, the relationship of AMBIT Capital/its affiliate with such client will continue to be governed by the terms and conditions in place between AMBIT Capital/ such affiliate and the client.

6. This Research Report is issued for information only and should not be construed as an investment advice to any recipient to acquire, subscribe, purchase, sell, dispose of, retain any securities. Recipients should consider this Research Report as only a single factor in making any investment decisions. This Research Report is not an offer to sell or the solicitation of an offer to purchase or subscribe for any investment or as an official endorsement of any investment.

7. If 'Buy', 'Sell', or 'Hold' recommendation is made in this Research Report such recommendation or view or opinion expressed on investments in this Research Report is not intended to constitute investment advice and should not be intended or treated as a substitute for necessary review or validation or any professional advice. The views expressed in this Research Report are those of the research analyst which are subject to change and do not represent to be an authority on the subject. AMBIT Capital may or may not subscribe to any and/ or all the views expressed herein.

8. AMBIT Capital makes no guarantee, representation or warranty, express or implied; and accepts no responsibility or liability as to the accuracy or completeness or currentess of the information in this Research Report. AMBIT Capital or its affiliates do not accept any liability whatsoever for any direct or consequential loss howsoever arising, directly or indirectly, from any use of this Research Report.

9. Past performance is not necessarily a guide to evaluate future performance. 10. AMBIT Capital and/or its affiliates (as principal or on behalf of its/their clients) and their respective officers directors and employees may hold positions in any securities mentioned in this Research

Report (or in any related investment) and may from time to time add to or dispose of any such securities (or investment). Such positions in securities may be contrary to or inconsistent with this Research Report.

11. This Research Report should be read and relied upon at the sole discretion and risk of the recipient. 12. The value of any investment made at your discretion based on this Research Report or income therefrom may be affected by changes in economic, financial and/ or political factors and may go down as

well as up and you may not get back the full or the expected amount invested. Some securities and/ or investments involve substantial risk and are not suitable for all investors. 13. This Research Report is being supplied to you solely for your information and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, copied in whole

or in part, for any purpose. Neither this Research Report nor any copy of it may be taken or transmitted or distributed, directly or indirectly within India or into any other country including United States (to US Persons), Canada or Japan or to any resident thereof. The distribution of this Research Report in other jurisdictions may be strictly restricted and/ or prohibited by law or contract, and persons into whose possession this Research Report comes should inform themselves about such restriction and/ or prohibition, and observe any such restrictions and/ or prohibition.

14. Neither AMBIT Capital nor its affiliates or their respective directors, employees, agents or representatives, shall be responsible or liable in any manner, directly or indirectly, for views or opinions expressed in this Report or the contents or any errors or discrepancies herein or for any decisions or actions taken in reliance on the Report or inability to use or access our service or this Research Report or for any loss or damages whether direct or indirect, incidental, special or consequential including without limitation loss of revenue or profits that may arise from or in connection with the use of or reliance on this Research Report or inability to use or access our service or this Research Report.

Conflict of Interests 15. In the normal course of AMBIT Capital’s business circumstances may arise that could result in the interests of AMBIT Capital conflicting with the interests of clients or one client’s interests conflicting with

the interest of another client. AMBIT Capital makes best efforts to ensure that conflicts are identified and managed and that clients’ interests are protected. AMBIT Capital has policies and procedures in place to control the flow and use of non-public, price sensitive information and employees’ personal account trading. Where appropriate and reasonably achievable, AMBIT Capital segregates the activities of staff working in areas where conflicts of interest may arise. However, clients/potential clients of AMBIT Capital should be aware of these possible conflicts of interests and should make informed decisions in relation to AMBIT Capital’s services.

16. AMBIT Capital and/or its affiliates may from time to time have investment banking, investment advisory and other business relationships with companies covered in this Research Report and may receive compensation for the same. Research analysts provide important inputs into AMBIT Capital’s investment banking and other business selection processes.

17. AMBIT Capital and/or its affiliates may seek investment banking or other businesses from the companies covered in this Research Report and research analysts involved in preparing this Research Report may participate in the solicitation of such business.

18. In addition to the foregoing, the companies covered in this Research Report may be clients of AMBIT Capital where AMBIT Capital may be required, inter alia, to prepare and publish research reports covering such companies and AMBIT Capital may receive compensation from such companies in relation to such services. However, the views reflected in this Research Report are objective views, independent of AMBIT Capital’s relationship with such company.

19. In addition, AMBIT Capital may also act as a market maker or risk arbitrator or liquidity provider or may have assumed an underwriting commitment in the securities of companies covered in this Research Report (or in related investments) and may also be represented in the supervisory board or on any other committee of those companies.

Additional Disclaimer for U.S. Persons 20. The research report is solely a product of AMBIT Capital 21. AMBIT Capital is the employer of the research analyst(s) who has prepared the research report 22. Any subsequent transactions in securities discussed in the research reports should be effected through J.P.P. Euro-Securities, Inc. (“JPP”). 23. JPP does not accept or receive any compensation of any kind for the dissemination of the AMBIT Capital research reports. 24. The research analyst(s) preparing the research report is resident outside the United States and is/are not associated persons of any U.S. regulated broker-dealer and that therefore the analyst(s) is/are

not subject to supervision by a U.S. broker-dealer, and is/are not required to satisfy the regulatory licensing requirements of FINRA or required to otherwise comply with U.S. rules or regulations regarding, among other things, communications with a subject company, public appearances and trading securities held by a research analyst account.

Additional Disclaimer for Canadian Persons 25. AMBIT Capital is not registered in the Province of Ontario and /or Province of Québec to trade in securities nor is it registered in the Province of Ontario and /or Province of Québec to provide advice

with respect to securities. 26. AMBIT Capital's head office or principal place of business is located in India. 27. All or substantially all of AMBIT Capital's assets may be situated outside of Canada. 28. It may be difficult for enforcing legal rights against AMBIT Capital because of the above. 29. Name and address of AMBIT Capital's agent for service of process in the Province of Ontario is: Torys LLP, 79 Wellington St. W., 30th Floor, Box 270, TD South Tower, Toronto, Ontario M5K 1N2

Canada. 30. Name and address of AMBIT Capital's agent for service of process in the Province of Montréal is Torys Law Firm LLP, 1 Place Ville Marie, Suite 1919 Montréal, Québec H3B 2C3 Canada.

© Copyright 2014 AMBIT Capital Private Limited. All rights reserved.

Ambit Capital Pvt. Ltd. Ambit House, 3rd Floor 449, Senapati Bapat Marg, Lower Parel, Mumbai 400 013, India. Phone: +91-22-3043 3000 Fax: +91-22-3043 3100 CIN: U74140MH1997PTC107598 www.ambitcapital.com