aluminium industry update and key challenges - … · aluminium industry update and key challenges...

TRANSCRIPT

Aluminium industry update and key challenges Alf Barrios, chief executive, Aluminium

20th CRU World Aluminium Conference 12 May 2015

©2014, Rio Tinto, All Rights Reserved

2

Aluminium contributes to a better life – driving long-term demand

Lower GHG emissions through lighter vehicles and buildings and through its recyclability

Bringing energy efficiency for cities and buildings in an energy constrained world

Preserving food and medicines through its unique barrier properties

©2015, Rio Tinto, All Rights Reserved

Source: CRU and Rio Tinto Source: Rio Tinto

3

Robust demand outlook

Primary Aluminium Demand (million tonnes)

Demand Growth (index)

14 17 19 21 24 27

51 20 24

26 26 26

27

47

34 41

45 47 50

54

98

0

20

40

60

80

100

120

2009

2010

2011

2012

2013

2014

2030

Rest of WorldChina

©2015, Rio Tinto, All Rights Reserved

Source: CRU and Rio Tinto

4

Fundamentals improving

Primary Aluminium Balance (million tonnes)

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Global Balance - actual

Global Balance - forecast

Global Balance - forecast range

China

RoW

©2015, Rio Tinto, All Rights Reserved

Source: LME, Platts and Metal Bulletin

Source: Platts and Metal Bulletin

5

Continued volatility near-term

0

50

100

150

200

250

300

350

400

450

500

550

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Europe (cash DPP)MidwestJapan

1,000

1,250

1,500

1,750

2,000

2,250

2,500

2,750

3,000

3,250

3,500

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

'All-In' average

LME Cash

Price ($US per tonne)

Market Premiums ($US per tonne)

©2015, Rio Tinto, All Rights Reserved

Source: China customs and Rio Tinto

6

Strong bauxite fundamentals

China Imports (million tonnes)

14 23

36 28

49

9

5

7

8 9

14

16

2

6

8

3

4

130

20

30

45 40

72

37

2009

2010

2011

2012

2013

2014

2025

Other

India & Malaysia

Australia

Indonesia

©2015, Rio Tinto, All Rights Reserved

7

Rio Tinto aluminium: clear focused strategy

First quartile smelters Tier one bauxite

Cash generation Market-paced growth Strategic focus

Low-cost, renewable energy portfolio Industry-leading bauxite position Competitive

advantage

Key enablers

Industry-leading performance through the cycle Strategic goal

Alumina supply and security

Commercial excellence

©2015, Rio Tinto, All Rights Reserved

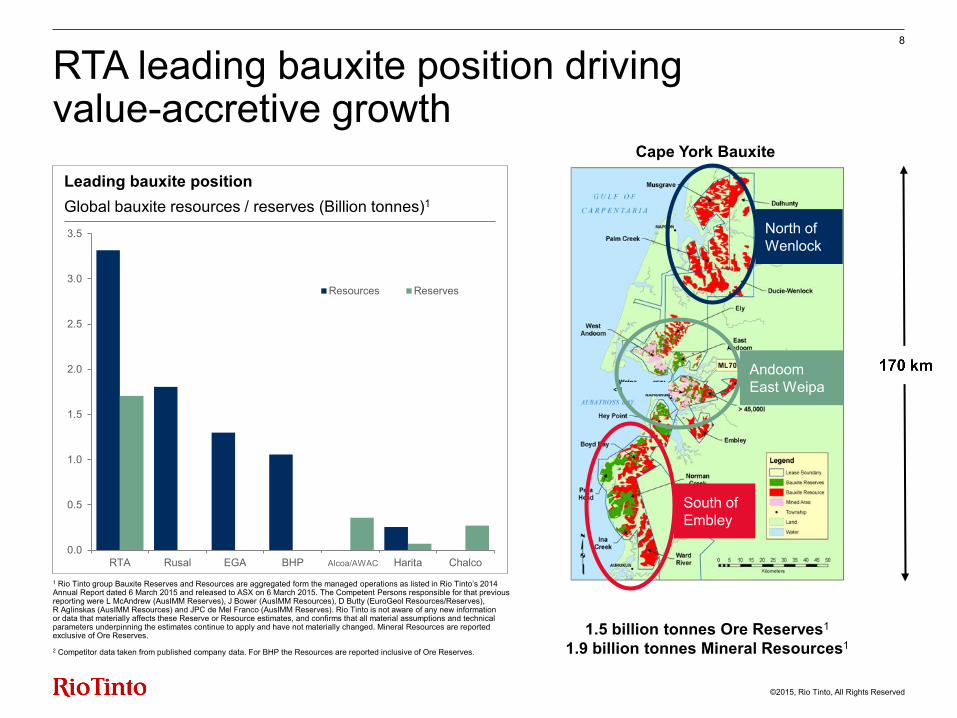

Leading bauxite position Global bauxite resources / reserves (Billion tonnes)1

1 Rio Tinto group Bauxite Reserves and Resources are aggregated form the managed operations as listed in Rio Tinto’s 2014 Annual Report dated 6 March 2015 and released to ASX on 6 March 2015. The Competent Persons responsible for that previous reporting were L McAndrew (AusIMM Reserves), J Bower (AusIMM Resources), D Butty (EuroGeol Resources/Reserves), R Aglinskas (AusIMM Resources) and JPC de Mel Franco (AusIMM Reserves). Rio Tinto is not aware of any new information or data that materially affects these Reserve or Resource estimates, and confirms that all material assumptions and technical parameters underpinning the estimates continue to apply and have not materially changed. Mineral Resources are reported exclusive of Ore Reserves.

2 Competitor data taken from published company data. For BHP the Resources are reported inclusive of Ore Reserves.

8

RTA leading bauxite position driving value-accretive growth

1.5 billion tonnes Ore Reserves1

1.9 billion tonnes Mineral Resources1

North of Wenlock

Andoom East Weipa

South of Embley

Cape York Bauxite

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

RTA Rusal EGA BHP Alcoa Harita Chalco

Resources Reserves

Alcoa/AWAC

©2015, Rio Tinto, All Rights Reserved

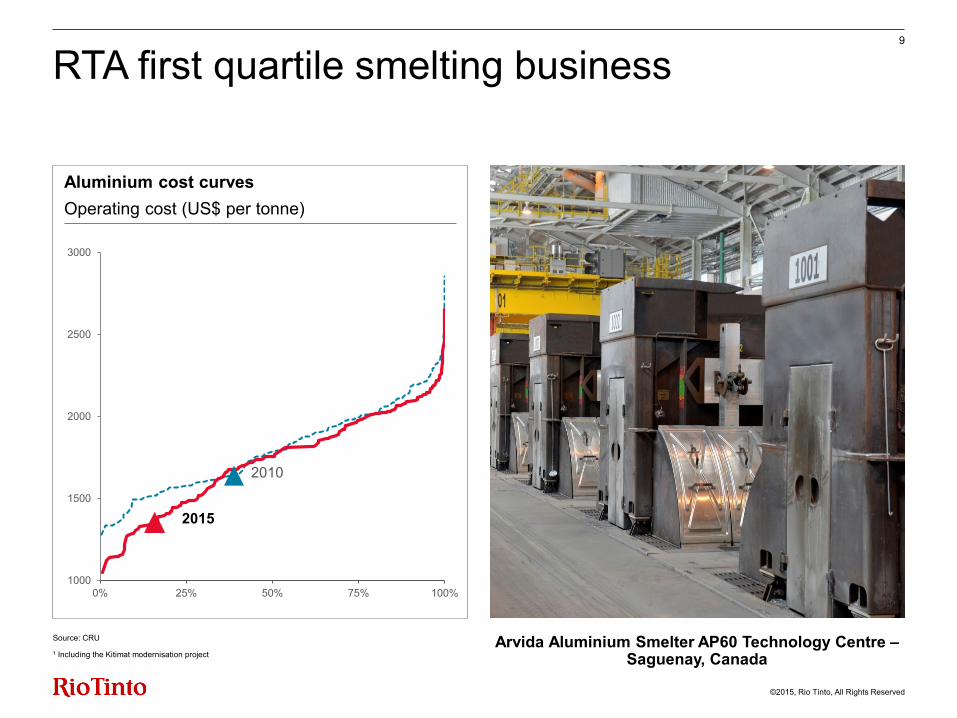

Aluminium cost curves Operating cost (US$ per tonne)

Source: CRU

1 Including the Kitimat modernisation project

9

RTA first quartile smelting business

Arvida Aluminium Smelter AP60 Technology Centre – Saguenay, Canada

1000

1500

2000

2500

3000

0% 25% 50% 75% 100%

2010

2015

©2015, Rio Tinto, All Rights Reserved

10

Rio Tinto: valued partner for the MENA aluminium industry • Offering support from mine to refining and smelting

− Technology − Secure, high-quality bauxite supply for increasing needs − Marketing and operational excellence

• Strong track record and commitment to regional social- economic development

Sohar, Oman