alternative energy outlook for growth remains strong · alternative energy – outlook for growth...

TRANSCRIPT

Alternative Energy – Outlook for Growth Remains Strong

Keith Adams, Moderator Principal

Deloitte Transactions and Business Analytics LLP

Tom Kimbis Interim President and Chief Executive Officer

Solar Energy Industries Association

Peter L. Kelley Vice President, Public Affairs

American Wind Energy Association

U.S. Solar Market Overview

2016 Deloitte Energy Conference

Tom Kimbis

Solar Energy Industries Association (SEIA)

July 6, 2016 © 2016 Solar Energy Industries Association® 2

About SEIA

• U.S. National Trade Association for Solar Energy

• Founded in 1974

• 1,000 member companies from all 50 states

• Our Mission: Build a strong solar industry to power America

• Our Goal: 100 gigawatts of solar capacity by 2020

July 6, 2016 © 2016 Solar Energy Industries Association® 3

Solar Growth with the ITC

July 6, 2016 © 2016 Solar Energy Industries Association® 4

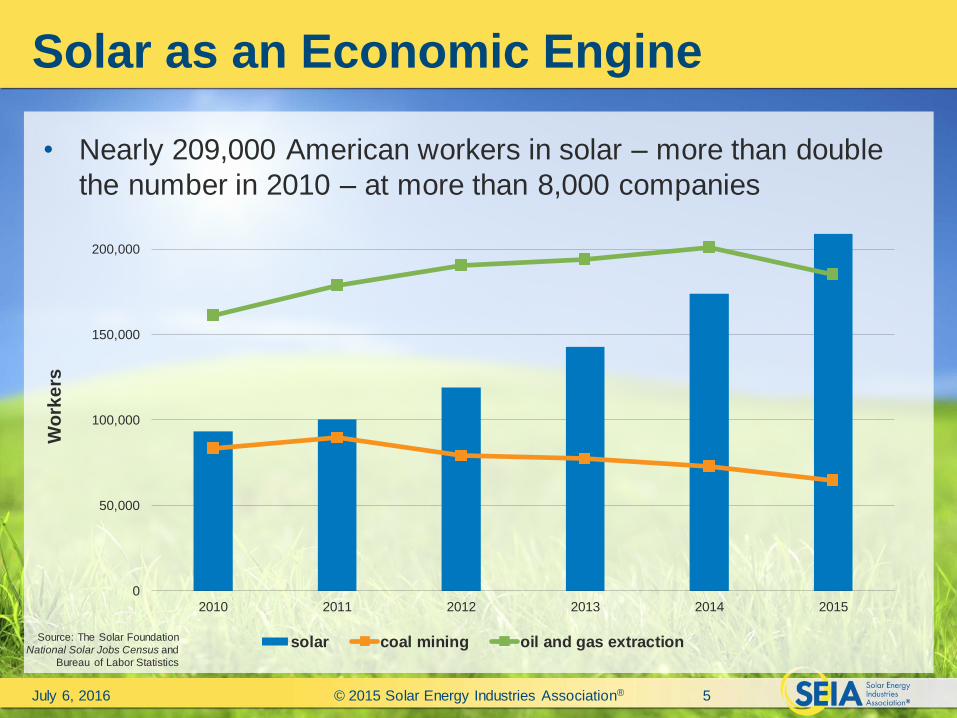

Solar as an Economic Engine

• Nearly 209,000 American workers in solar – more than double

the number in 2010 – at more than 8,000 companies

July 6, 2016 © 2015 Solar Energy Industries Association® 5

Source: The Solar Foundation

National Solar Jobs Census and

Bureau of Labor Statistics

0

50,000

100,000

150,000

200,000

2010 2011 2012 2013 2014 2015

Wo

rke

rs

solar coal mining oil and gas extraction

Growth in Solar led by Falling Prices

July 6, 2016 © 2016 Solar Energy Industries Association® 6

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

$-

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

2009 2010 2011 2012 2013 2014 2015

So

lar

PV

In

sta

llati

on

s (M

Wd

c)

Ble

nd

ed

Av

era

ge S

ola

r P

V P

rice (

$/w

att

)

Solar PV Installations Solar PV PricesSource: SEIA/GTM Research U.S. Solar Market Insight Q4 2015

greentechmedia.com/research/ussmi

Lawrence Berkeley National Laboratory, Tracking the Sun

U.S. Solar Market Through Q1 2016

• 7.5 GW of solar installed in 2015 – 19% growth in PV market over 2014

– Compound annual growth rate of 58% since 2010

• Over 29 GW of total solar capacity installed – Generates enough electricity to power 5.7 million homes

• Solar prices dropped 3% in 2015 from 2014 – Price drop accelerated in Q1 2016, down 12% y/y

– Prices have dropped over 70% since 2006

– Utility-Scale PPAs now signed for $0.03 - $0.05/kWh

• Solar has reached 1% of total US electric generation – Up from 0.1% just 5 years ago

– Expected to hit 3.5% by 2020

• In Q1 2016 reached 1 million solar installations – Will hit 2 million installs within just 2 years

July 6, 2016 © 2014 Solar Energy Industries Association® 7

Source: SEIA/GTM Research

U.S. Solar Market Insight

Solar PV Price Breakdown

July 6, 2016 © 2016 Solar Energy Industries Association® 8

$-

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

Residential Commercial Utility-Scale

$/w

att

-dc

Q1 2016 Quoted PV Prices

PV Module Inverter Electrical BOS Structural BOS Direct Labor Engineering and PII Supply Chain, Overhead, Margin

Soft Costs

(63% of residential

installation cost)

Source: SEIA/GTM Research

U.S. Solar Market Insight

U.S is a 50 state market

July 6, 2016 © 2016 Solar Energy Industries Association® 9

California, 11,987

North Carolina, 2,087

Arizona, 2,020

New Jersey, 1,631

Nevada, 1,041

Massachusetts, 1,037

New York, 638

Hawaii, 557

Colorado, 542

Texas, 537

Others, 3,519

2015 Year-End Cumulative Solar PV Capacity (MW-dc)

Source: SEIA/GTM Research

U.S. Solar Market Insight

Residential & Commercial (Distributed)

July 6, 2016 © 2016 Solar Energy Industries Association® 10

0

500

1,000

1,500

2,000

2,500

3,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E

Meg

aw

att

s

Yearly U.S. Solar Photovoltaic (PV) Installations

Residential (PV) Non-residential (PV) Source: SEIA/GTM Research

U.S. Solar Market Insight

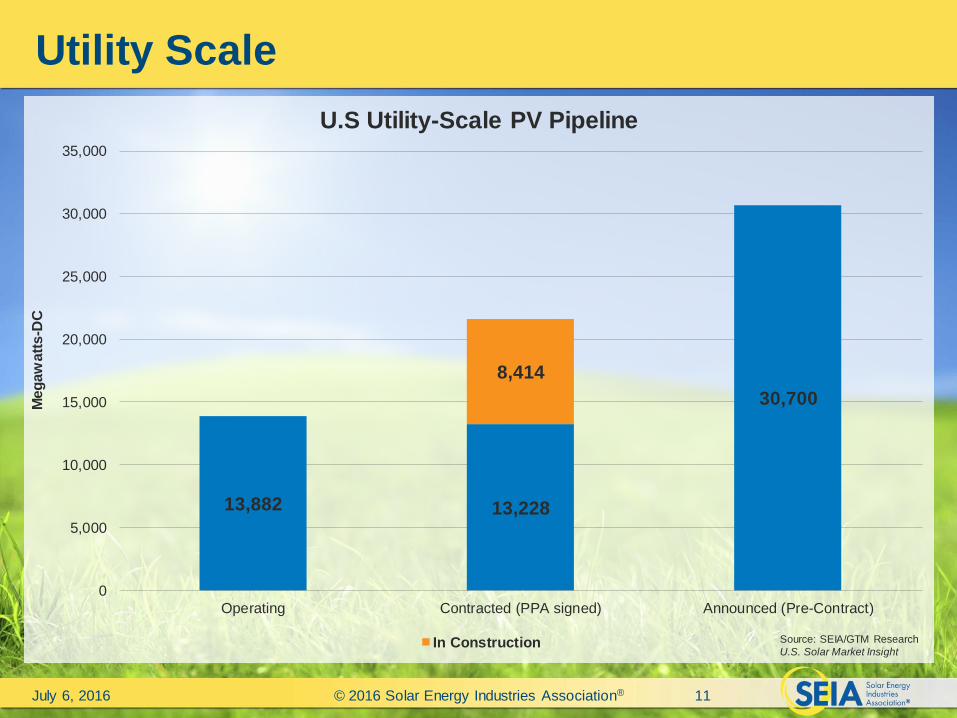

Utility Scale

July 6, 2016 © 2016 Solar Energy Industries Association® 11

13,882 13,228

30,700

8,414

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Operating Contracted (PPA signed) Announced (Pre-Contract)

Meg

aw

att

s-D

C

U.S Utility-Scale PV Pipeline

In Construction Source: SEIA/GTM Research

U.S. Solar Market Insight

Extending the ITC

• Extended at 30% through the end of 2019

– Drops to 26% in 2020 and 22% in 2021

– After 2021, Commercial credit drops to 10%, Residential

credit expires

• Commence Construction language added

– Projects must be placed in service before the end of 2023

July 6, 2016 © 2016 Solar Energy Industries Association® 12

Industry At Risk

July 6, 2016 © 2016 Solar Energy Industries Association® 13

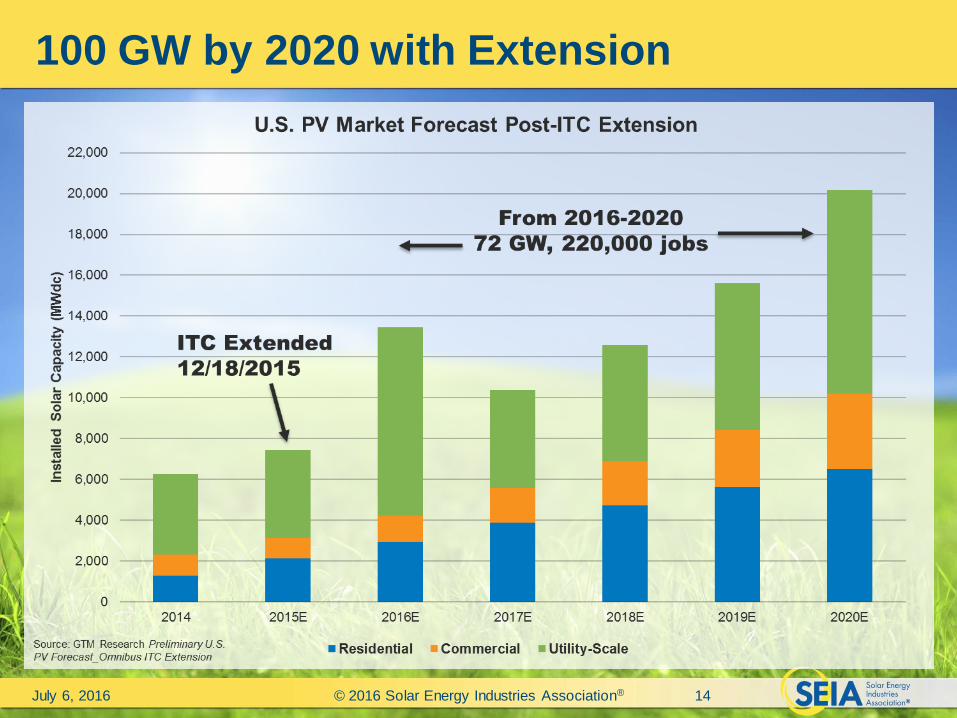

100 GW by 2020 with Extension

July 6, 2016 © 2016 Solar Energy Industries Association® 14

Net Metering

July 6, 2016 © 2016 Solar Energy Industries Association® 15

Net Metering

July 6, 2016 © 2016 Solar Energy Industries Association® 16

• Under current NEM rules, distributed generation solar

at grid parity in 20 states

Source: Shayle Kann, GTM Research

U.S. Solar Market Insight Conference

Keynote: The Future of Solar

Net Metering

July 6, 2016 © 2016 Solar Energy Industries Association® 17

• If export rate is cut in half, 0 states at grid parity

• Nevada outcome looms large, but not emblematic of

NEM policy nationally

Source: Shayle Kann, GTM Research U.S. Solar

Market Insight Conference Keynote: The Future of

Solar

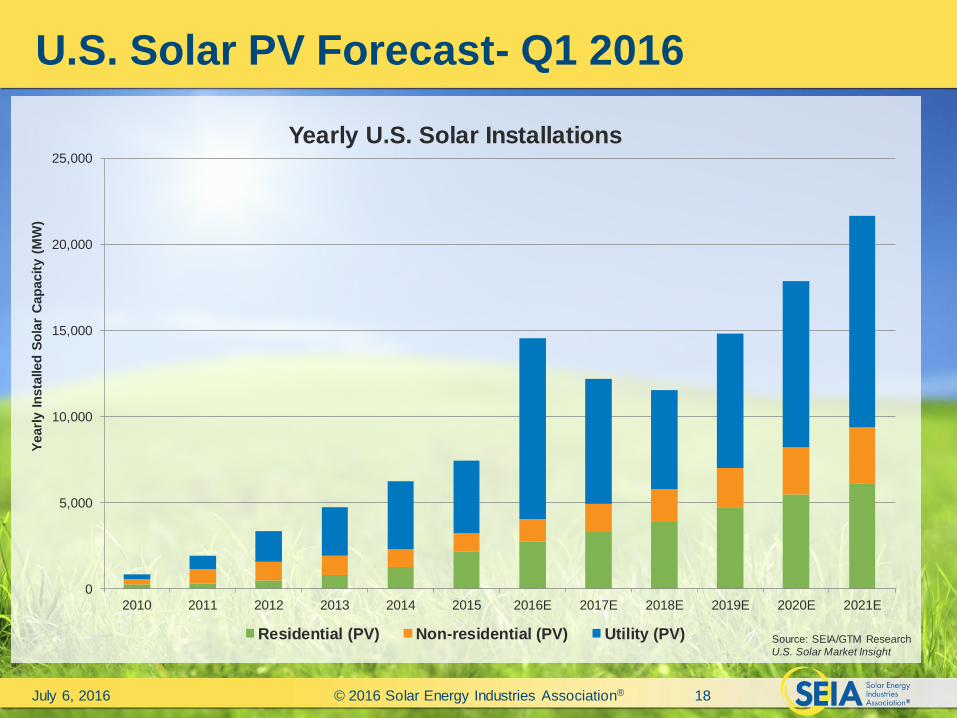

U.S. Solar PV Forecast- Q1 2016

July 6, 2016 © 2016 Solar Energy Industries Association® 18

0

5,000

10,000

15,000

20,000

25,000

2010 2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E 2020E 2021E

Yearl

y I

nsta

lled

So

lar

Cap

acit

y (

MW

)

Yearly U.S. Solar Installations

Residential (PV) Non-residential (PV) Utility (PV) Source: SEIA/GTM Research

U.S. Solar Market Insight

2016 and Beyond

• 14.5 GW of solar expected in 2016

– Nearly double the 2015 total

– Equal to half of the solar capacity online today

– Continue to see shift of 2016 utility-scale projects to

2017, 2018

• Developers add to massive project pipeline

– Build-out pressure decreases with extension

– Nearly 19 GW contracted BEFORE extension of ITC

• New States enter the mix

– Continued price declines, ITC Extension, Clean Power

Plan bring formerly marginal states into play

July 6, 2016 © 2016 Solar Energy Industries Association® 19

Source: SEIA/GTM Research

U.S. Solar Market Insight

Solar Moving Beyond Traditional Markets:

Distributed Generation

July 6, 2016 © 2016 Solar Energy Industries Association® 20

State2011-15 DG

MW

2016-2020 DG

MWDG Growth

1 California 3,880 13,234 9,353

2 New York 510 2,711 2,201

3 Massachusetts 937 2,256 1,319

4 Maryland 306 1,111 805

5 Connecticut 185 912 727

6 New Jersey 1,132 1,683 551

7 Texas 113 598 486

8 Florida 106 574 468

9 Minnesota 28 472 444

10 Vermont 55 399 345

Top 10 DG States by Absolute Growth

State2011-15 DG

MW

2016-2020 DG

MWDG % Growth

1 South Carolina 8 172 2097%

2 Minnesota 28 472 1579%

3 Indiana 9 130 1348%

4 Virginia 19 208 1003%

5 Michigan 15 151 936%

6 New Hampshire 23 222 868%

7 District of Columbia 15 136 796%

8 Delaware 32 271 752%

9 Illinois 22 180 731%

10 Vermont 55 399 632%

Top 10 DG States by % Growth

Source: SEIA/GTM Research Source: SEIA/GTM Research

U.S. Solar Market Insight

Solar Moving Beyond Traditional Markets:

Utility-Scale

July 6, 2016 © 2016 Solar Energy Industries Association® 21

State

2011-15

Utility-Scale

MW

2016-2020

Utility-Scale

MW

Utility-Scale

Growth

1 Texas 394 4,233 3,840

2 California 7,179 10,407 3,229

3 Utah 194 1,466 1,272

4 Nevada 777 1,978 1,201

5 Florida 21 1,173 1,152

6 Georgia 339 1,392 1,054

7 New Mexico 250 1,287 1,037

8 Oregon 26 1,042 1,016

9 Colorado 162 956 794

10 Virginia 2 750 748

Top 10 Utility-Scale States by Absolute Growth

State

2011-15

Utility-Scale

MW

2016-2020

Utility-Scale

MW

Utility-Scale

% Growth

1 Washington 0.0 142.4 -

2 Iowa 0.0 68.0 -

3 Louisiana 0.0 33.7 -

4 New Hampshire 0.0 12.5 -

5 Virginia 2.1 750.4 36414%

6 Minnesota 2.3 682.6 29578%

7 Michigan 1.3 333.5 26372%

8 South Carolina 3.7 525.2 14095%

9 Florida 20.9 1,173.0 5511%

10 Oregon 26.3 1,041.8 3861%

Top 10 Utility-Scale States by % Growth

Source: SEIA/GTM Research

Source: SEIA/GTM Research

U.S. Solar Market Insight

Other Issues to Watch

• 2016 Elections

• Access to Capital

• Workforce Development – Industry will double number of employees over 5 years

– Committed to hiring 50,000 veterans by 2020

• Technology Advances – Storage, Electric Vehicles, Continued Price Declines

• Grid Integration

– What does the grid of the future look like?

• Post-Clean Power Plan? – More ambitious plan needed to meet climate goals

July 6, 2016 © 2016 Solar Energy Industries Association® 22

Thank You

Tom Kimbis

Interim President

Solar Energy Industries Association (SEIA)

202-682-0556

July 6, 2016 © 2016 Solar Energy Industries Association® 23

Wind power: Low-cost, scalable, reliable

Peter L. Kelley

Vice President, Public Affairs

AWEA

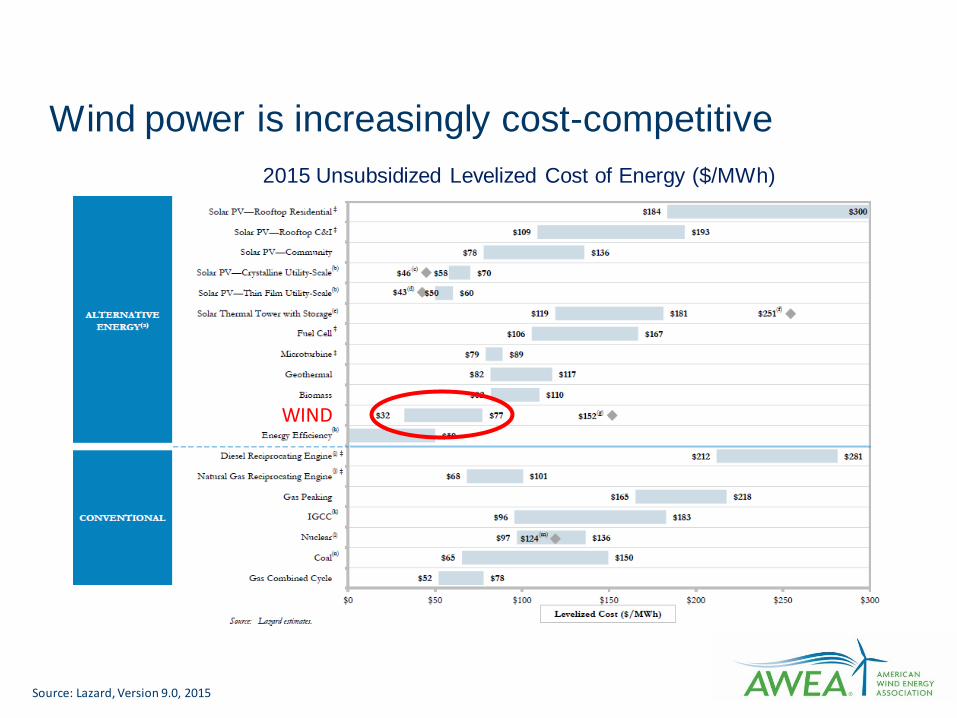

Low-cost solution

Wind power is increasingly cost-competitive

Source: Lazard, Version 9.0, 2015

2015 Unsubsidized Levelized Cost of Energy ($/MWh)

WIND

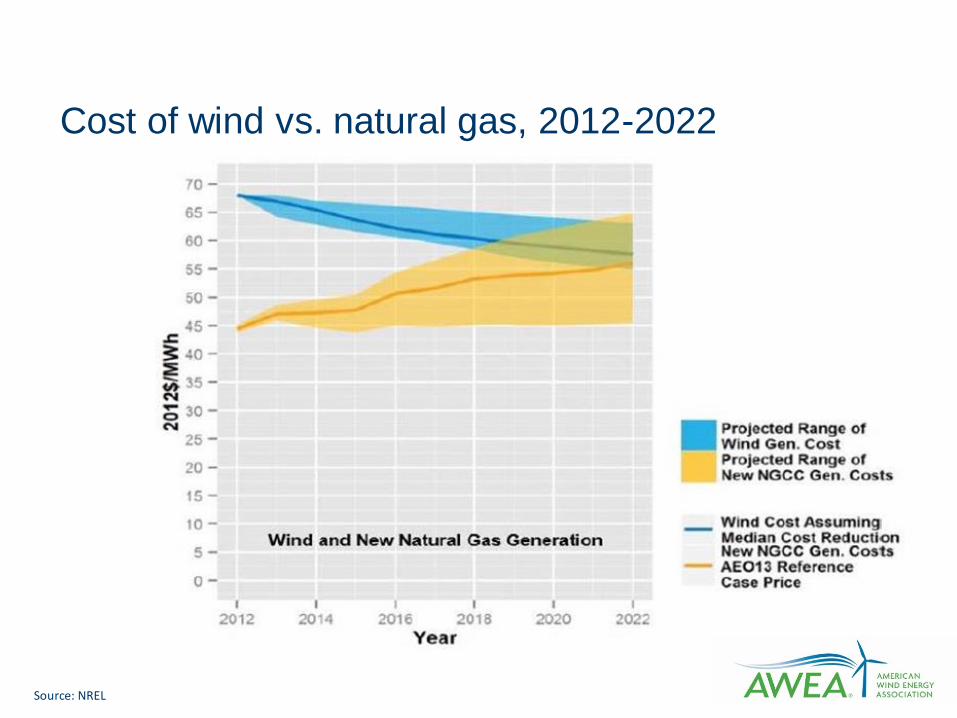

Cost of wind vs. natural gas, 2012-2022

Source: NREL

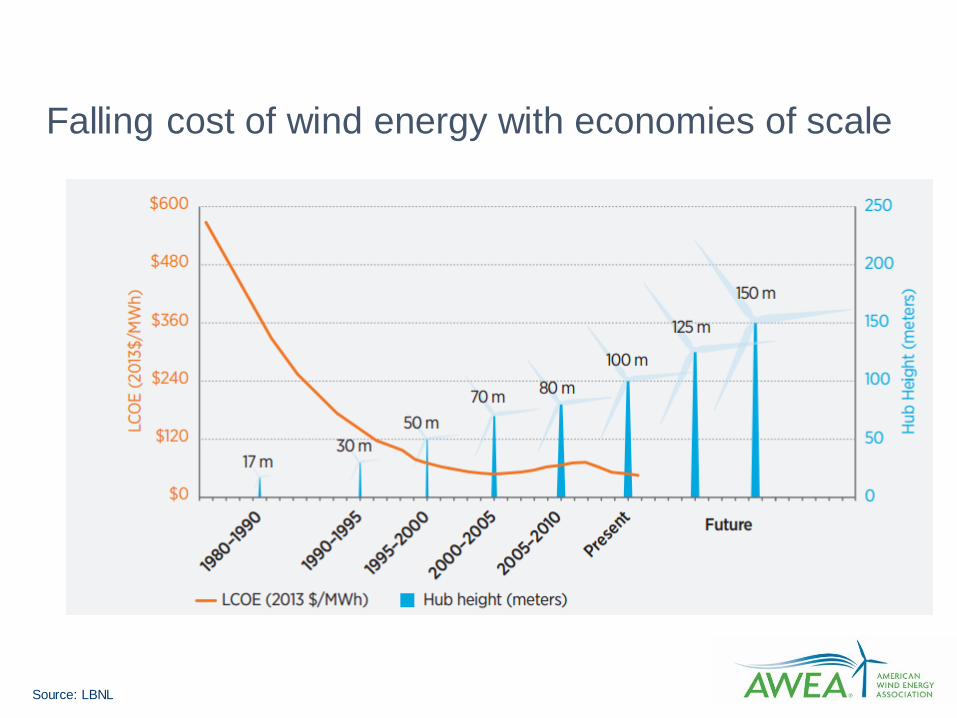

Source: LBNL

Falling cost of wind energy with economies of scale

More reasons for falling wind costs

• Policies now predictable

• Optimized siting

• Technology accessing higher winds

• More transmission to cities

• Data-driven O&M

• US manufacturing

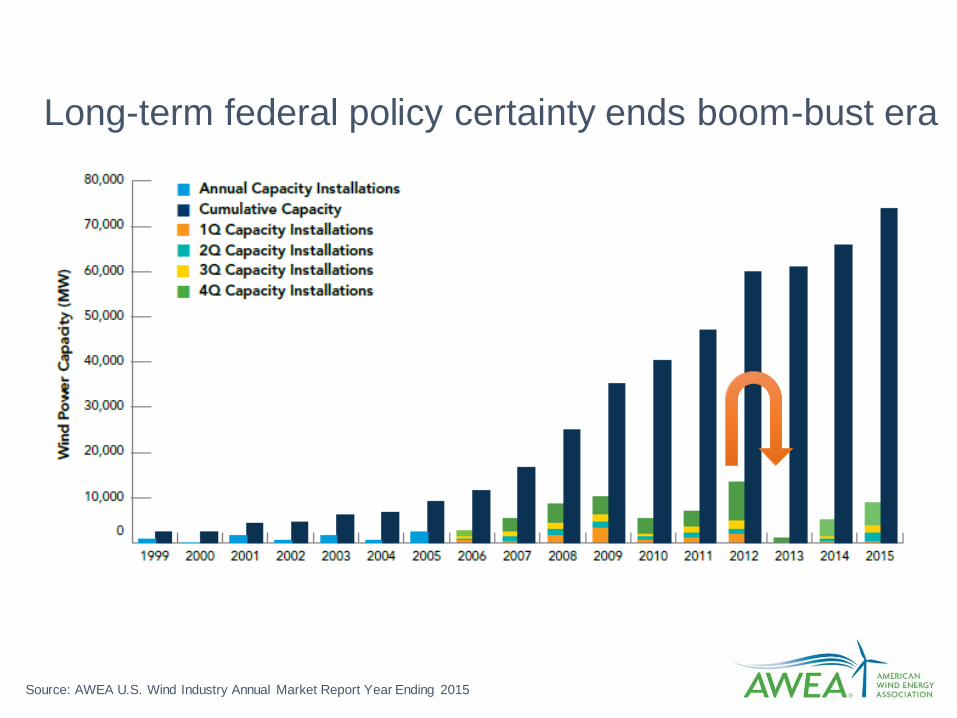

Long-term federal policy certainty ends boom-bust era

Source: AWEA U.S. Wind Industry Annual Market Report Year Ending 2015

New technology reaches higher winds in more regions

Wind resource potential at

110 meters

Wind resource potential at

turbine hub height of 80 meters

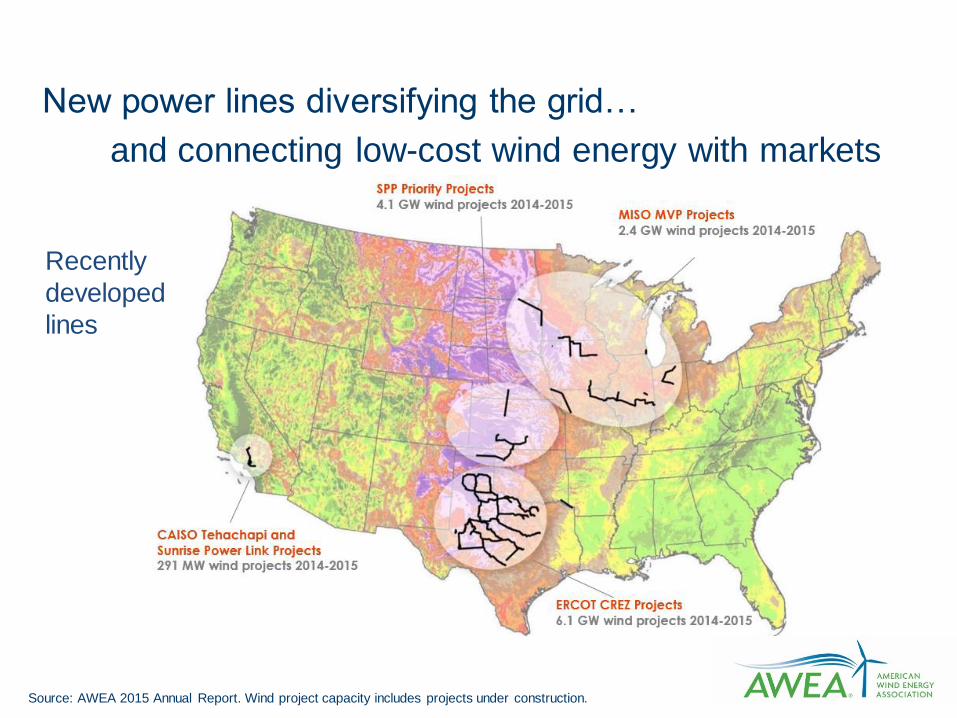

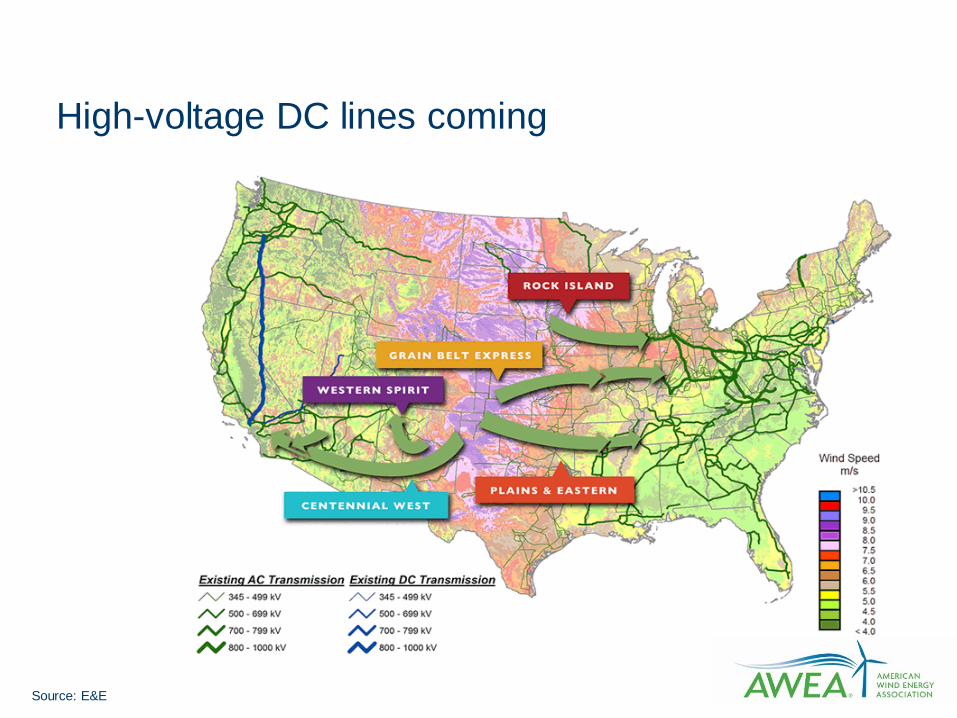

New power lines diversifying the grid…

and connecting low-cost wind energy with markets

Source: AWEA 2015 Annual Report. Wind project capacity includes projects under construction.

Recently

developed

lines

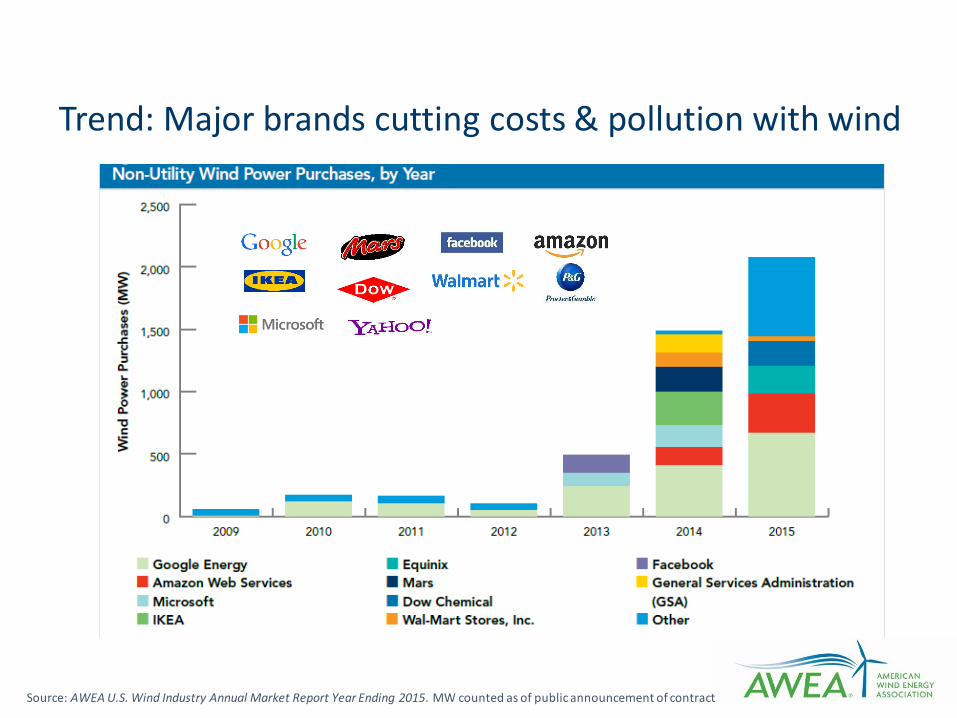

Trend: Major brands cutting costs & pollution with wind

Source: AWEA U.S. Wind Industry Annual Market Report Year Ending 2015. MW counted as of public announcement of contract

Scalable

Wind was biggest source of new electric power in 2015

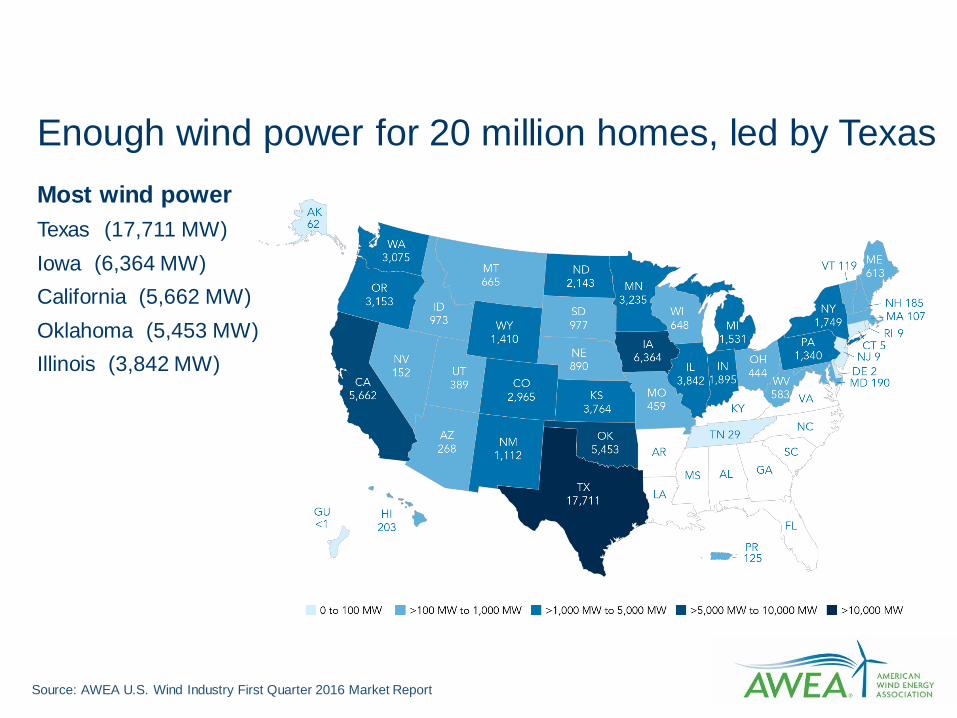

Enough wind power for 20 million homes, led by Texas

Most wind power

Texas (17,711 MW)

Iowa (6,364 MW)

California (5,662 MW)

Oklahoma (5,453 MW)

Illinois (3,842 MW)

Source: AWEA U.S. Wind Industry First Quarter 2016 Market Report

88,000 wind jobs today – growing to 360,000 in 2030

Source: AWEA U.S. Wind Industry Annual Market Report Year Ending 2015

Most wind jobs

Texas (24,001-25,000)

Oklahoma (7,001-8,000)

Iowa (6,001-7,000)

Colorado (6,001-7,000)

Kansas (5,001-6,000)

State RPS laws generate demand for wind energy

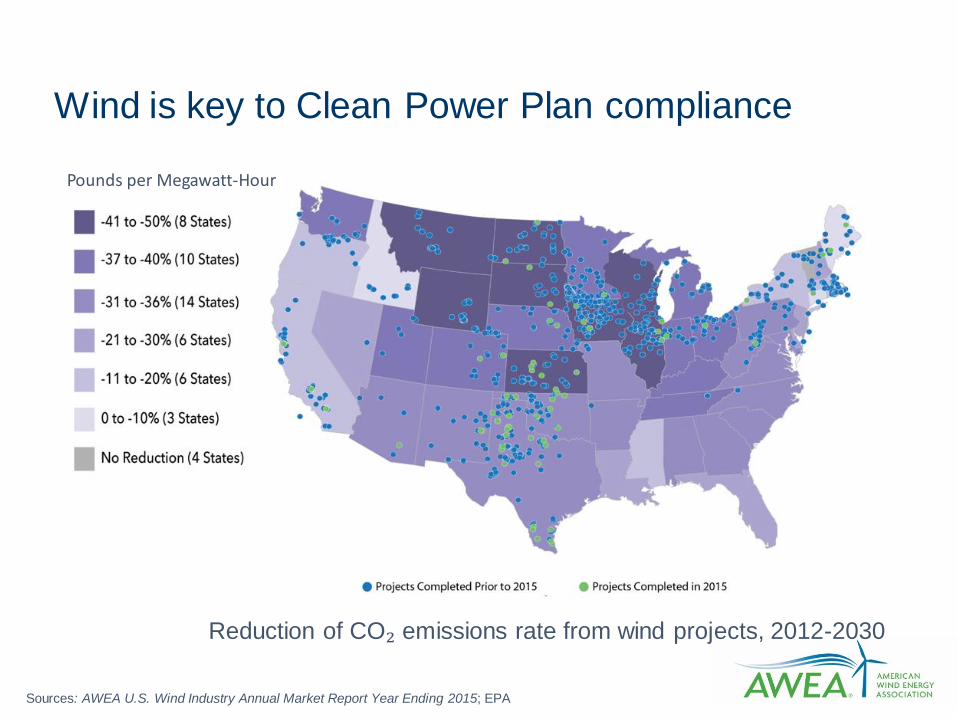

Wind is key to Clean Power Plan compliance

Reduction of CO₂ emissions rate from wind projects, 2012-2030

Pounds per Megawatt-Hour

Sources: AWEA U.S. Wind Industry Annual Market Report Year Ending 2015; EPA

Source: EIA; China Electricity Council, 2015

U.S. offshore wind energy: the new frontier

Grid reliability

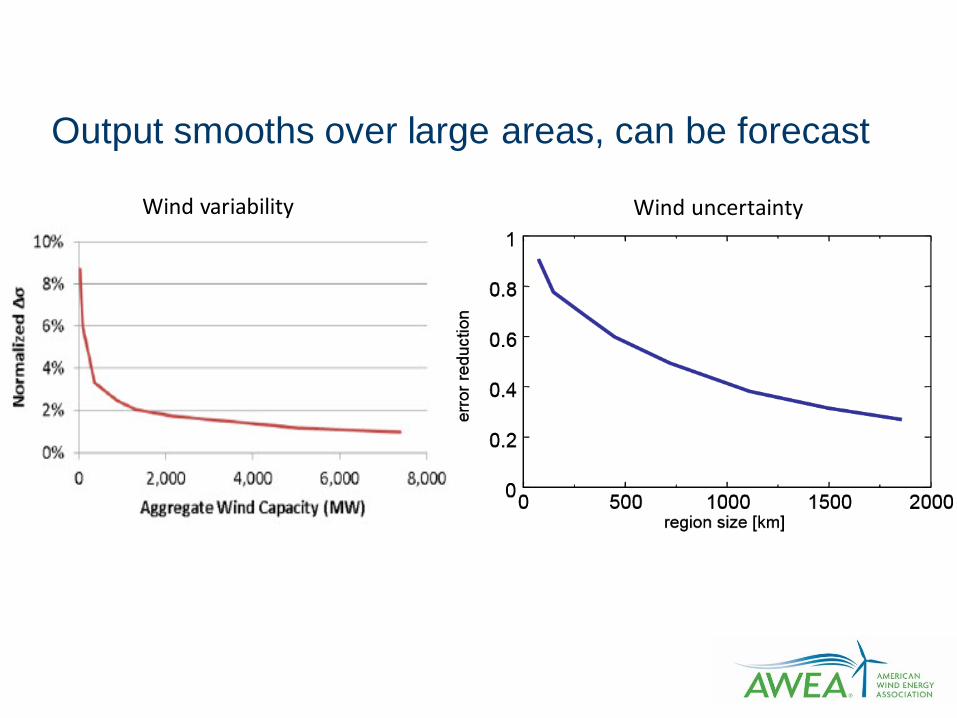

Variability & uncertainty nothing new for grid operators

Wind variability Wind uncertainty

Output smooths over large areas, can be forecast

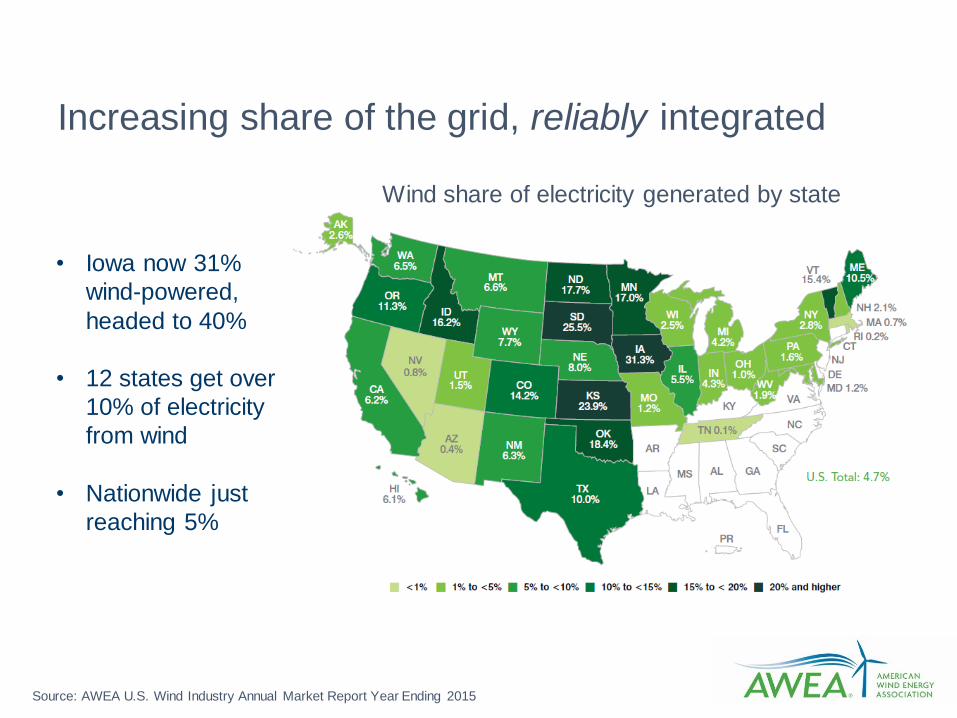

Increasing share of the grid, reliably integrated Wind share of electricity generated by state

Source: AWEA U.S. Wind Industry Annual Market Report Year Ending 2015

• Iowa now 31%

wind-powered,

headed to 40%

• 12 states get over

10% of electricity

from wind

• Nationwide just

reaching 5%

Source: E&E

High-voltage DC lines coming

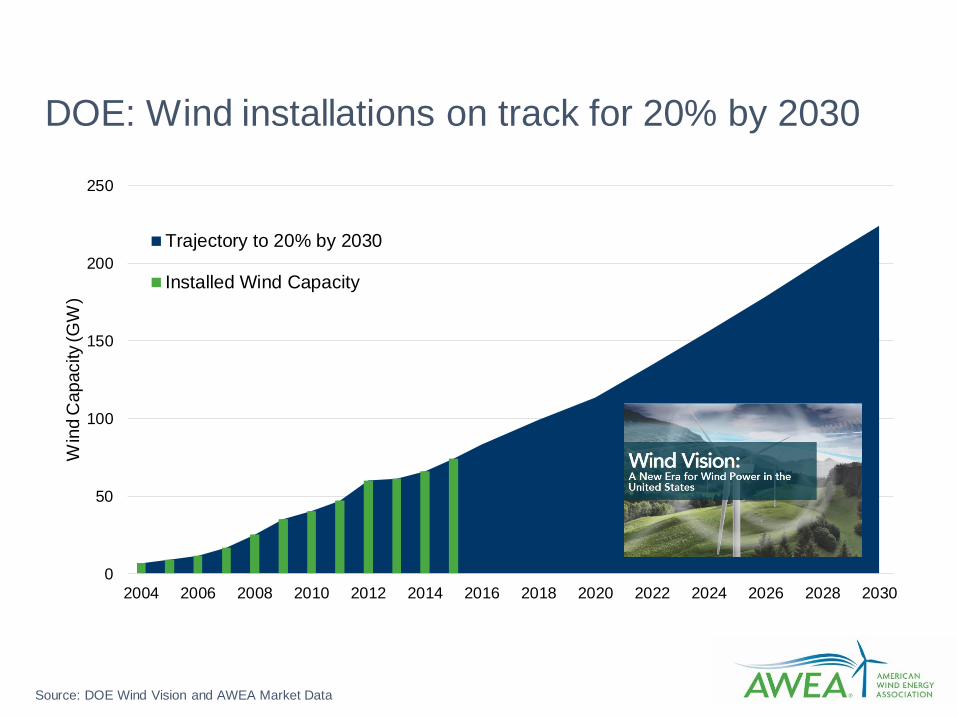

DOE: Wind installations on track for 20% by 2030

Source: DOE Wind Vision and AWEA Market Data

0

50

100

150

200

250

2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030

Win

d C

apacity (G

W)

Trajectory to 20% by 2030

Installed Wind Capacity

Questions?