alliance pipeline · highlights 2016 financial results as strong as ever; 2017 q1 results exceed...

TRANSCRIPT

May 2, 2017

Alliance Pipeline

Update to Noteholders

1

Forward-Looking Information

Certain information contained in this presentation constitutes forward-

looking statements. The words “anticipate”, “expects” and “expected to”

and similar expressions are intended to identify such forward-looking

statements. Although Alliance believes that these statements are based on

information and assumptions which are current, reasonable and complete,

these statements are necessarily subject to a variety of risks and

uncertainties including, but not limited to, future operating performance,

regulation, economic conditions and fundamentals affecting the oil and gas

producing and marketing industries. Should one or more of these risks or

uncertainties materialize or fail to materialize, or should underlying

assumptions prove incorrect, actual results may vary materially from those

expected.

2

Alliance Overview

1.65 Bcf/d annual firm capacity from WCSB to Chicago

250 mmcf/d receipt capacity out of the Bakken

Robust maintenance program ensures next to new capability

Transporting approximately 140,000 bpd of NGLs

Ability to transport 1,150 Btu/cf commingled gas

Reliability over 99%

System Capability

3

D

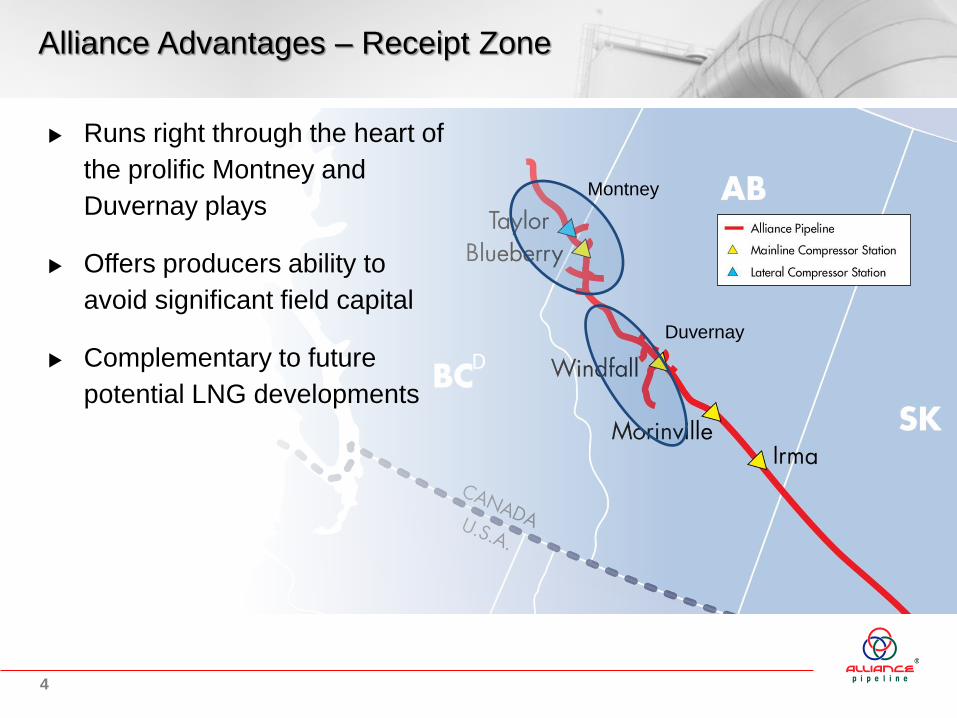

Alliance Advantages – Receipt Zone

Runs right through the heart of

the prolific Montney and

Duvernay plays

Offers producers ability to

avoid significant field capital

Complementary to future

potential LNG developments

4

Montney

Duvernay

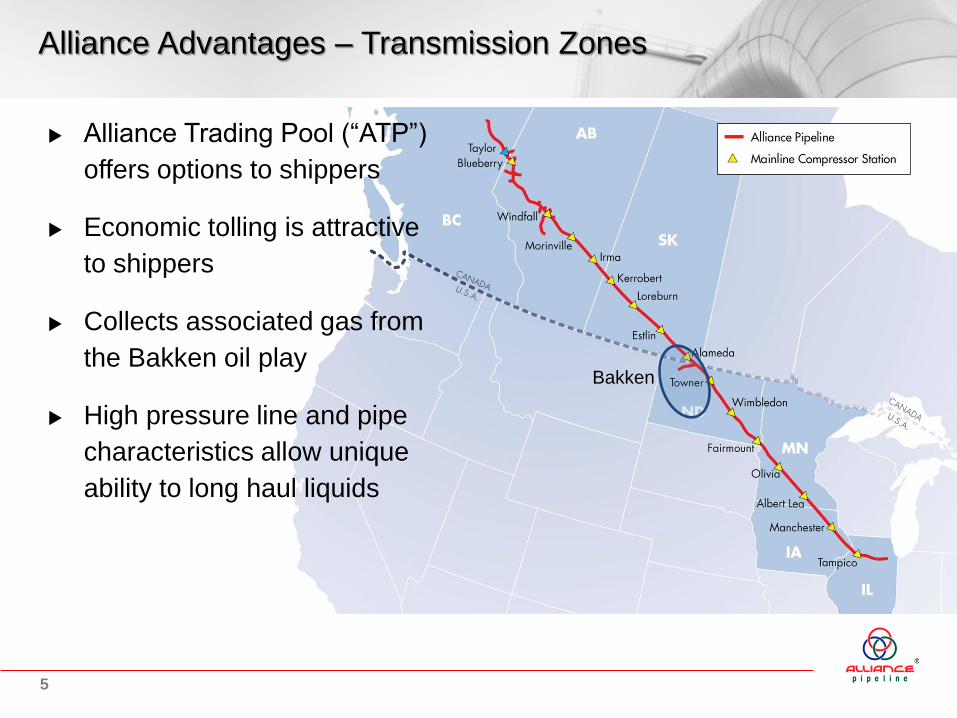

Alliance Advantages – Transmission Zones

Alliance Trading Pool (“ATP”)

offers options to shippers

Economic tolling is attractive

to shippers

Collects associated gas from

the Bakken oil play

High pressure line and pipe

characteristics allow unique

ability to long haul liquids

5

Bakken

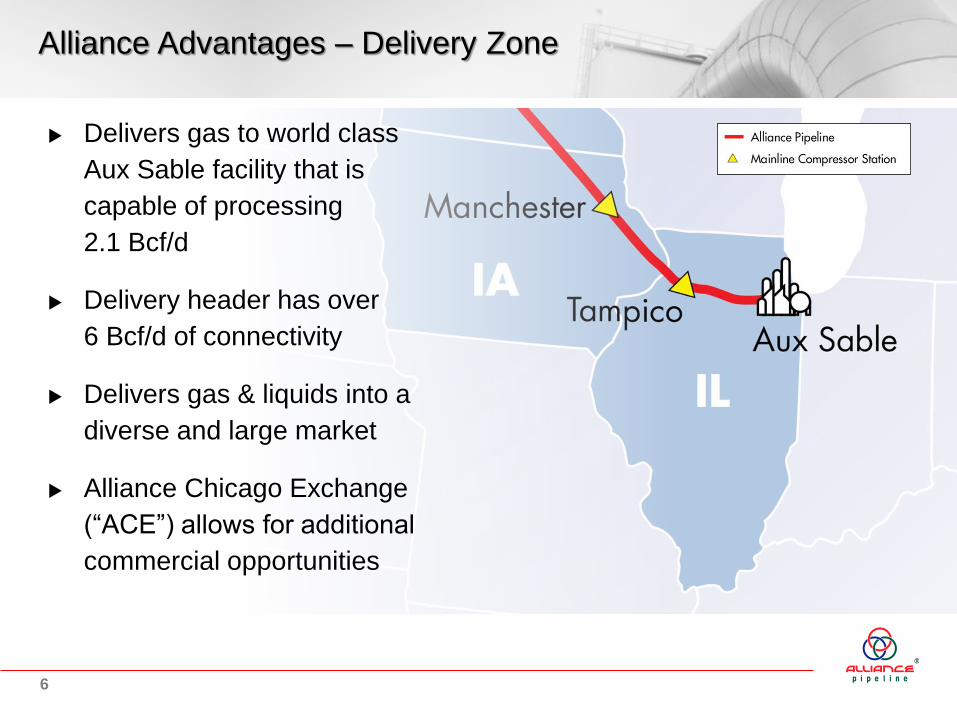

Alliance Advantages – Delivery Zone

Delivers gas to world class

Aux Sable facility that is

capable of processing

2.1 Bcf/d

Delivery header has over

6 Bcf/d of connectivity

Delivers gas & liquids into a

diverse and large market

Alliance Chicago Exchange

(“ACE”) allows for additional

commercial opportunities

6

Highlights

2016 financial results as strong as ever; 2017 Q1 results exceed budget

Alliance achieving revenues comparable to previous cost of service contracts

Corporate redesign and operational performance has led to significant permanent cost

reductions

Enhanced ability to profit from market opportunities by aligning operational capabilities with

suite of service offerings

Success with new services offering underpins more robust financial forecasts

Strong financial

results

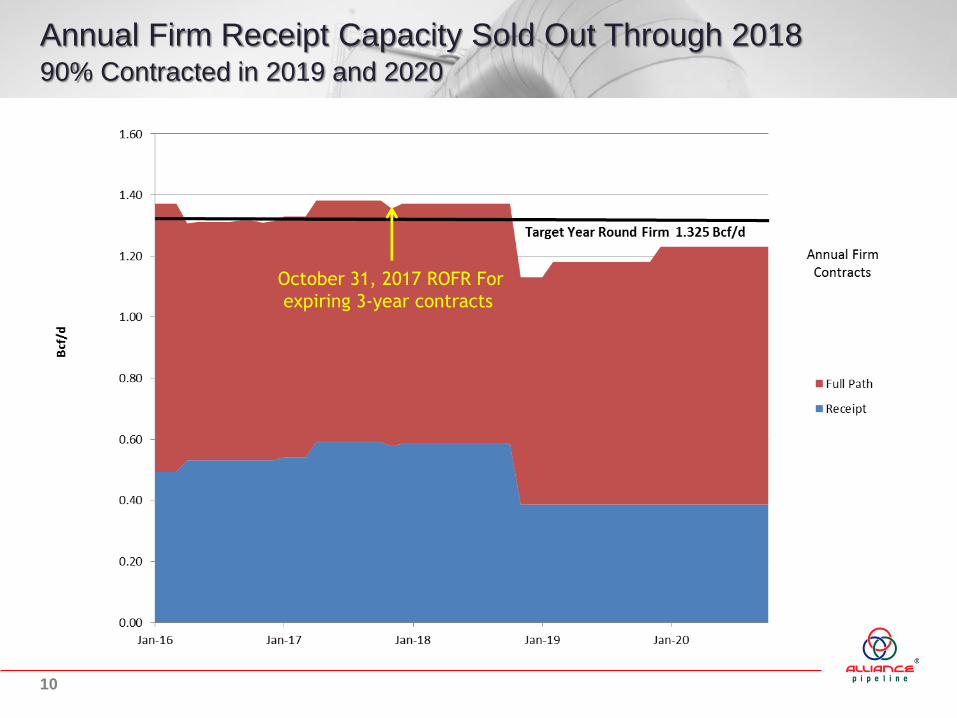

Sold out all firm annual receipt capacity through 2018 and 90% in 2019 and 2020

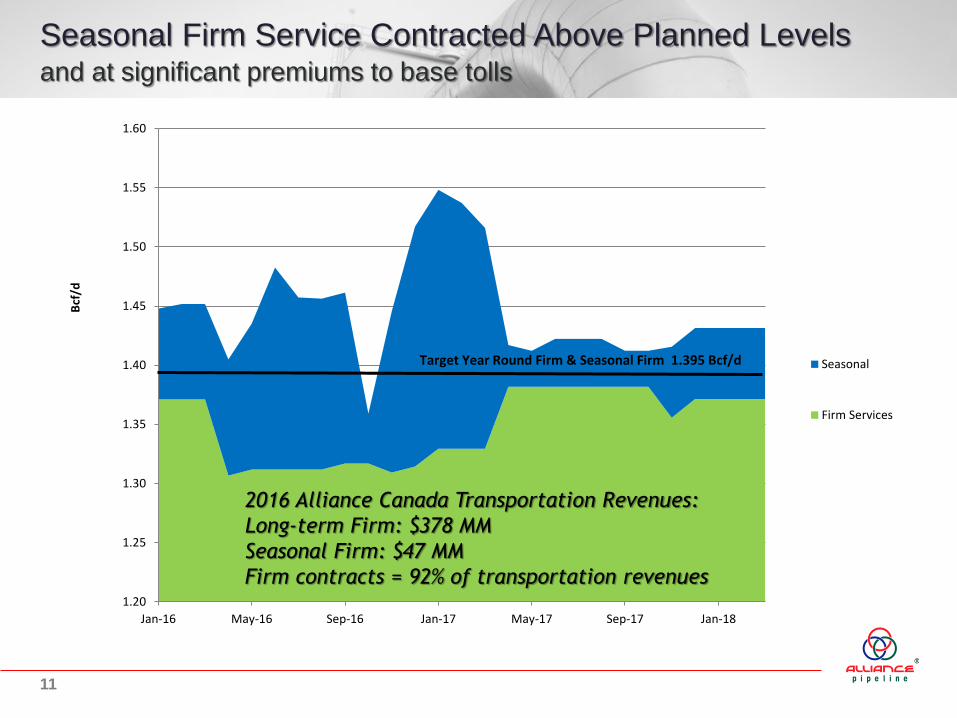

During 2016, Alliance sold all available seasonal firm capacity and successfully used short-

term firm and interruptible services to capture incremental producer demand for our

transportation service

Already contracted significant 2017/18 winter seasonal volumes at a significant premium to

our firm toll to creditworthy parties

Market optionality and operational capability have created significant interest in contract

extensions and possible system expansions

Substantial

demand for new

service offerings

WCSB long on gas – export options desired to lessen AECO dependence

Long term supply forecasts and Alberta-Chicago Basis favourable to long term Alliance utilization

Montney proving competitive to any play in North America: our shippers are in prominent areas

LNG exports from Canada’s west coast highly unlikely prior to 2022

Downstream connections allow Alliance shippers to be a competitive gas supply source to U.S.

LNG facilities

Robust

fundamentals

7

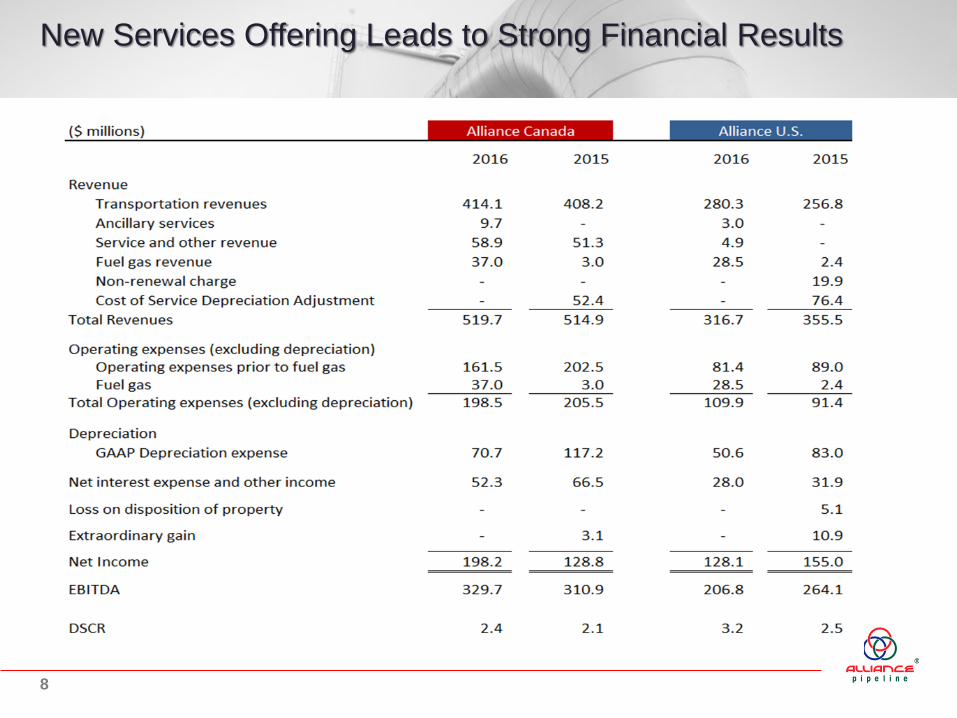

New Services Offering Leads to Strong Financial Results

8

Operational Excellence

In 2016, achieved highest compressor fleet availability in Alliance’s

history at 99.1%

Successfully completed the Regina Bypass project on time with full

revenue and cost recovery

– Also used window to install NGL scrubber at Blueberry, check valve in US

and complete all planned maintenance (safely completed 10,000 hours of

activity during the outage period)

Producers value the asset performance and lack of constraints/

bottlenecks on our system

– Consistently provide reliable transportation out of high activity production

areas

Our operational dependability and producers’ need for certainty on

production takeaway, has led producers to bid on seasonal and

short term firm rather than take chances with Interruptible

Transportation (“IT”)

9

Annual Firm Receipt Capacity Sold Out Through 2018 90% Contracted in 2019 and 2020

October 31, 2017 ROFR For

expiring 3-year contracts

10

Seasonal Firm Service Contracted Above Planned Levels and at significant premiums to base tolls

1.20

1.25

1.30

1.35

1.40

1.45

1.50

1.55

1.60

Jan-16 May-16 Sep-16 Jan-17 May-17 Sep-17 Jan-18

Bcf

/d

Seasonal

Firm Services

Target Year Round Firm & Seasonal Firm 1.395 Bcf/d

2016 Alliance Canada Transportation Revenues:

Long-term Firm: $378 MM

Seasonal Firm: $47 MM

Firm contracts = 92% of transportation revenues

11

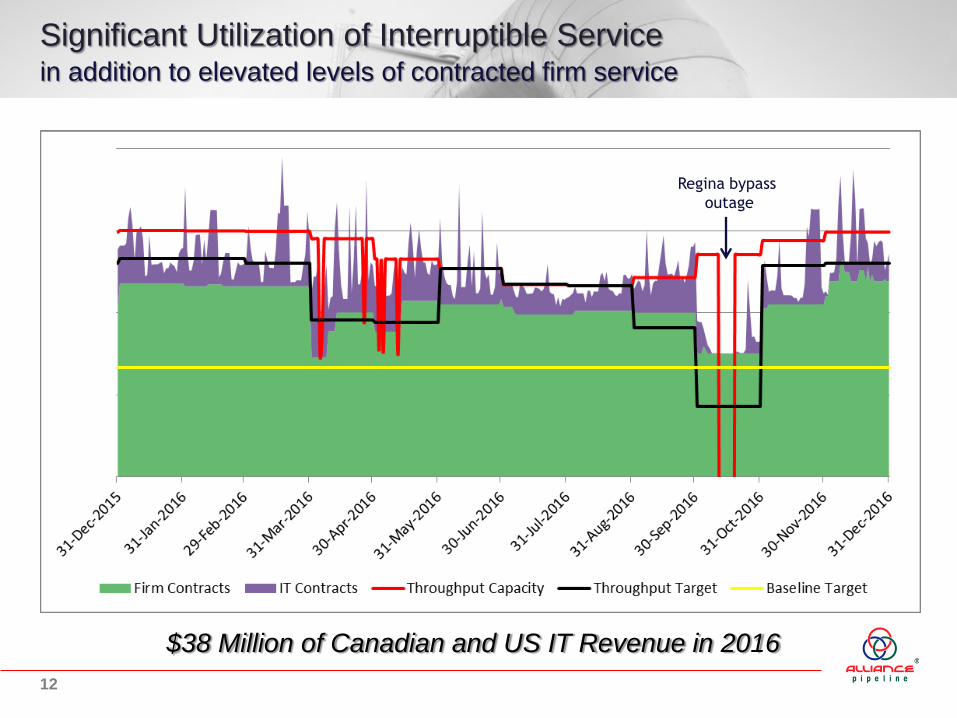

Significant Utilization of Interruptible Service in addition to elevated levels of contracted firm service

$38 Million of Canadian and US IT Revenue in 2016

12

Regina bypass

outage

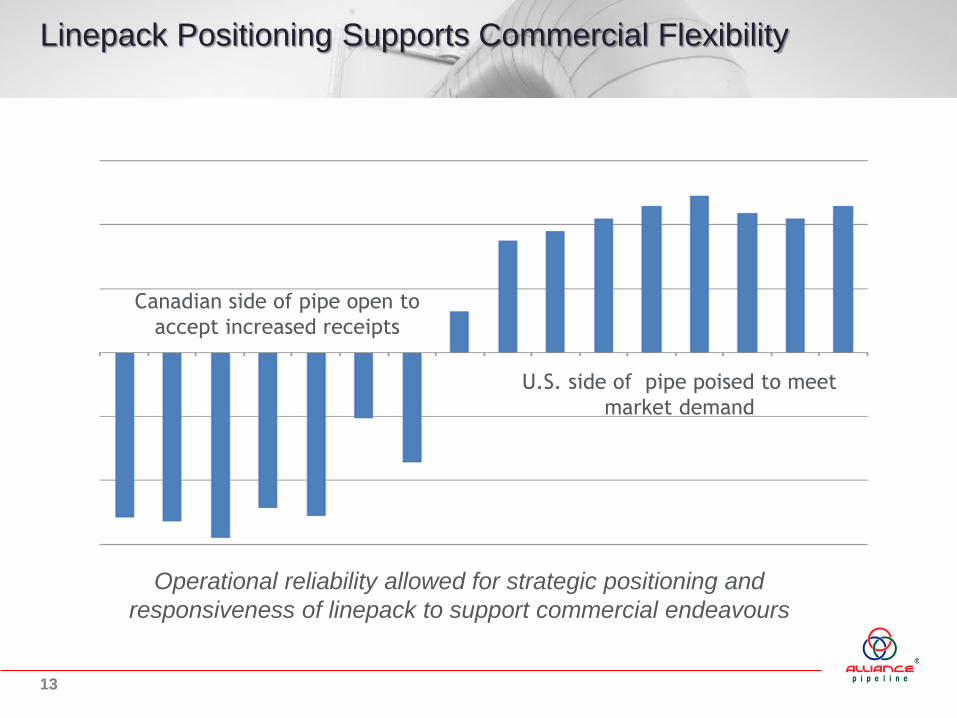

Linepack Positioning Supports Commercial Flexibility

Operational reliability allowed for strategic positioning and

responsiveness of linepack to support commercial endeavours

Canadian side of pipe open to

accept increased receipts

U.S. side of pipe poised to meet

market demand

13

Alliance Provides Economic Uplift for Producers

DELPHI ENERGY (February 2017 Corporate Presentation): “Secured firm service with

Alliance to access Chicago gas market for better pricing and fewer curtailments.” When

speaking of Alliance’s Full Path Service (“FFPS”): “Current temporary and permanent

assignments generate premiums over cost.”

FIRST ENERGY (August 24, 2016): “Alliance Pipeline system has captured a pricing premium

for the shippers/producers that are able to get gas onto this system.”

ENCANA CORPORATION (April 2017 Corporate Presentation): “Achieved liquids price

upgrade while minimizing midstream capex via Alliance pipeline.” Also: “Diversified pricing

exposure for liquids and natural gas in Chicago market.”

NATIONAL BANK (March 27, 2017): “At present, based on competitive pricing to Dawn and

pursuant to Rich Gas Premium agreements with Aux Sable at the end of Alliance, access to the

Chicago market continues to be attractive.”

14

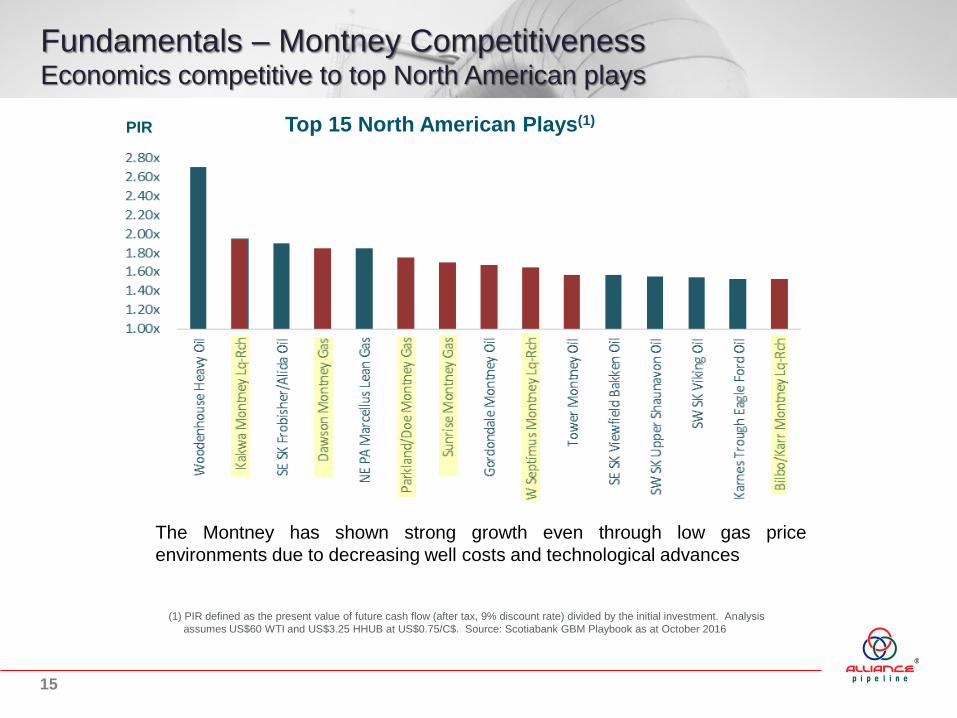

PIR Top 15 North American Plays(1)

The Montney has shown strong growth even through low gas price

environments due to decreasing well costs and technological advances

Fundamentals – Montney Competitiveness Economics competitive to top North American plays

(1) PIR defined as the present value of future cash flow (after tax, 9% discount rate) divided by the initial investment. Analysis

assumes US$60 WTI and US$3.25 HHUB at US$0.75/C$. Source: Scotiabank GBM Playbook as at October 2016

15

Fundamentals Montney economics continue to improve

Source: Encana as presented by TD Securities Inc, August 2016

16

Fundamentals Production growth around Alliance

Alliance Pipeline Ltd.

Nova Gas Transmission Ltd.

High-Producing Wells

A large majority of high producing wells

brought on in 2016 are within a 50 km

band around Alliance

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

$7.0

$8.0

$9.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

2008 2009 2010 2011 2012 2013 2014 2015 2016

$U

S/D

th

Bcf/d

NE BC/NW AB Production

Production Chicago-AECO Basis AECOSource: NEB, AER

Production in NE BC/NW AB (near Alliance receipt locations) has continued to grow over the past 8 years despite

declining pricing due to improving well economics and declining costs

However, Chicago-AECO basis (the spread captured in transporting from WCSB to Chicago) has remained relatively

level with the exception of the 2014 polar vortex spike and strengthening seen through 2016

17

Fundamentals US demand remains robust with export and industrial demand

Wood Mackenzie forecasts~16.5

Bcf/d of natural gas demand

growth in the Gulf of Mexico

region alone from 2015-2026

Alliance is well positioned to

provide low cost WCSB

production to US Midwest market

and onwards to other markets

including the Gulf Coast

Seven Generations has

contracted with Sabine Pass LNG

export facility to ship a minimum of

100 mmcf/d of gas transported on

Alliance and Natural Gas Pipeline

Company of America

Bcf/d

2 Bcf/d of US

Midwest demand

growth by 2025

18

Alliance is Well Connected to New Production Significant new receipt capacity since 2010

Alliance Canada is

connected to 53 natural

gas meter stations and

4 liquids receipt points

Since 2010, ~ 1.7 Bcf/d

of new receipt capacity

installed, with an

additional 323 MMcf/d

planned for the second

half of 2017

All receipt connections

were producer funded

Including planned

connections, will have

over 6 Bcf/d of receipt

capacity

19

Capacity on Alliance is Highly Valued

Some existing shippers have expressed interest in contract extensions

and/or obtaining incremental transportation capacity

– Due to Rights of First Refusals (“ROFRs”) on expiring firm capacity that

shippers must exercise by October 31, 2017, a contract extension strategy

will commence this fall

Prior to March 2017, new shippers had expressed interest in

contracting for firm service to Chicago

There are high levels of interest in contract extensions

and additional capacity on Alliance

20

Contract Extensions and Capacity Expansion

Alliance issued a press release on March 13, 2017

– Non-binding expressions of interest for new capacity

– Contract extensions from existing shippers required to underpin an expansion

High demand for Alliance transportation due to forecasted high production growth in

Alliance catchment area, AECO pricing pressures and Alliance’s competitive tolls

The window for expressions of interest closed on April 7, 2017

– Process is ongoing but to date, more than 50 parties have signed

confidentiality agreements

Conducting a study to evaluate the commercial parameters of adding up to 500

mmcf/d in capacity through the addition of B Site compressor stations

If project economics are favourable, Alliance may conduct a binding open season

in late 2017

Financial structure to be addressed upon contractual commitments and

regulatory approvals

21

Summary

Alliance continues to deliver strong and sustainable financial results

– Competitive cost structure and transportation tolls

– Strong interest in seasonal and short-term firm over IT

– Current market favorable to contract renewals/extensions

Favourable fundamentals are supportive of continued financial success

– Reliable access to US Midwest with connectivity to reach other US markets

including the Gulf Coast

Substantial interest from existing and prospective shippers for

additional transportation take away

– Substantial indications of interest towards capacity expansion

– Many original shippers that missed out on December 1, 2015 contracting are

back utilizing Alliance

– Indicative of a large number of replacement shippers if ever required

22

Contacts

www.alliancepipeline.com

Keith Palmer Senior Vice President & CFO

Direct: (403) 517-6369

Email: [email protected]

Kevin Sundvall Treasurer

Direct: (403) 517-7711

Email: [email protected]

Terrance Kutryk President & CEO

Direct: (403) 517-6500

Email: [email protected]

23

Supplemental Information

24

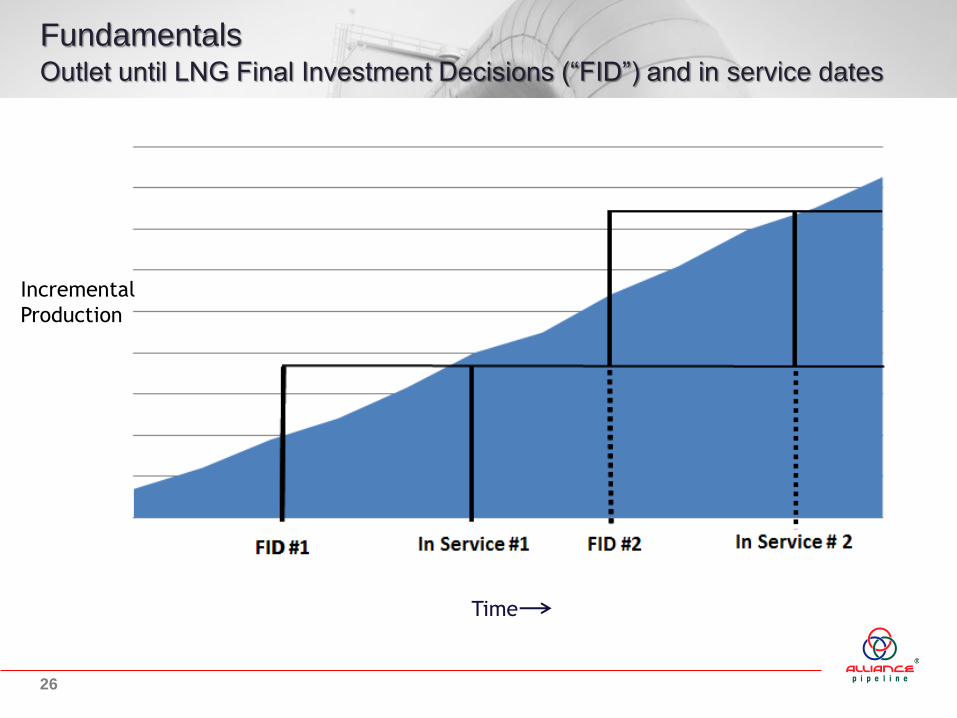

Fundamentals Immediate and economic bridge for LNG facilities

Alliance an existing, economic solution with immediate access

to market

Capital avoidance and predictable rich gas transportation through

2022 and beyond

First B.C. LNG projects still awaiting investment decisions

Optionality while LNG outcomes get sorted

Long-term market portfolio alternative for rich gas plays

Increasing exports from U.S. Gulf Coast

25

Fundamentals Outlet until LNG Final Investment Decisions (“FID”) and in service dates

Incremental

Production

Time

26

Fundamentals NGL transport up by 70% from 2010

Source: Company reports

0

10

20

30

40

50

2011 2012 2013 2014 2015 2016

Bar

rels

in m

illio

ns

NGL Transported Per Year

Ethane Propane Butane Condensate

27

Lender Protections Strong structural credit enhancements

Restrictive Covenant Package

– Restrictions on lines of business, disposals, and additional indebtedness

Liquidity and Structural Protections

– Debt Service Reserve Account for six months of scheduled principal and

interest payments

– Amortizing debt structure

Creditor Protections

– Intercreditor arrangement

– Security trustee and trust accounts (on all but equity accounts)

– Distribution restrictions

28