albert schoen

DESCRIPTION

TRANSCRIPT

Are Thematic Investments Sustainable?

Workshop 16TBLI Conference 2010, London

Workshop 16, TBLI LondonNovember 2010 - Page 2

Agenda

Moderator: Christian SCHÖN (Erste Asset Management)Introduction: EAM & Thematic Investments

Speaker 1: Andrea FERCH (LGT Capital Management)Thematic Investments and/or ESG Criteria? A Fund Selector‘s View

Speaker 2: Till JUNG (oekom research)Case Studies of Thematic Fund Holdings & their Responsibility Rating

Speaker 3: Wolfgang PINNER (VINIS)Can Sustainability Add Value To Thematic Investing?

moderated panel discussion and audience Q&A-session

Workshop 16, TBLI LondonNovember 2010 - Page 3

ERSTE-SPARINVEST KAG is mainly held by ERSTE GROUP BANK AG

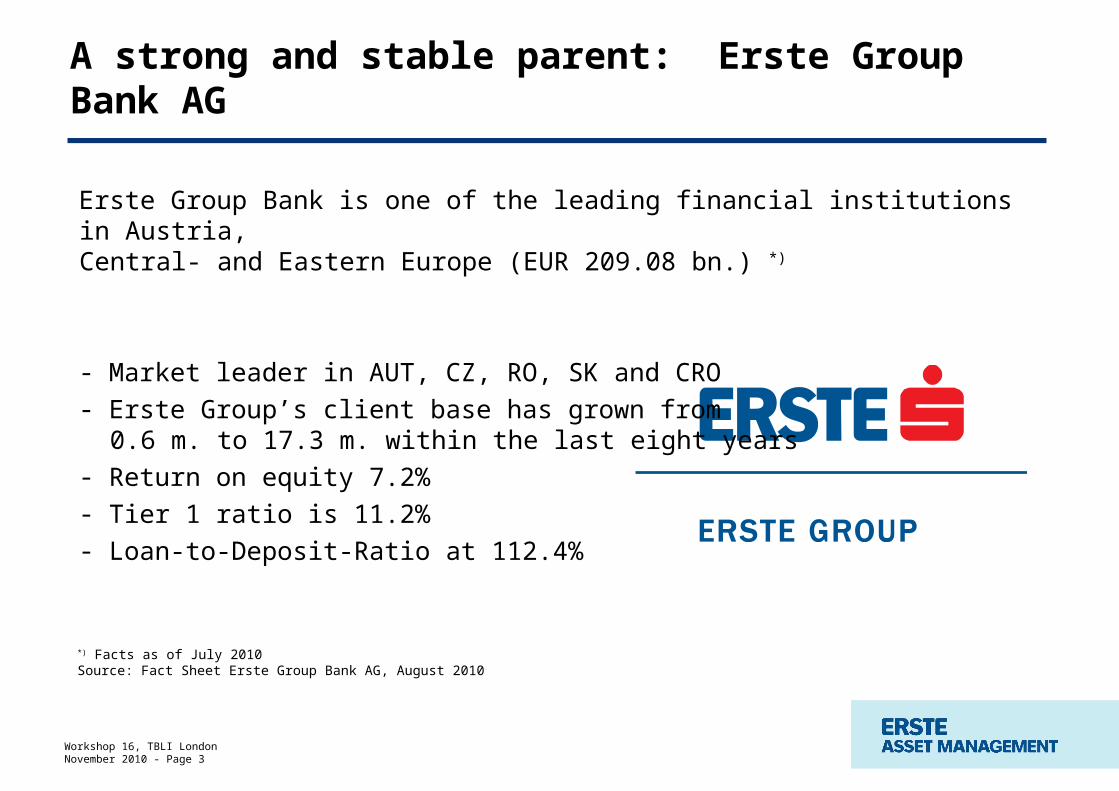

A strong and stable parent: Erste Group Bank AG

Erste Group Bank is one of the leading financial institutions in Austria, Central- and Eastern Europe (EUR 209.08 bn.) *)

- Market leader in AUT, CZ, RO, SK and CRO- Erste Group’s client base has grown from 0.6 m. to 17.3 m. within the last eight years - Return on equity 7.2%- Tier 1 ratio is 11.2% - Loan-to-Deposit-Ratio at 112.4%

*) Facts as of July 2010Source: Fact Sheet Erste Group Bank AG, August 2010

Workshop 16, TBLI LondonNovember 2010 - Page 4

Organizational chart of Erste Asset Management

Workshop 16, TBLI LondonNovember 2010 - Page 5

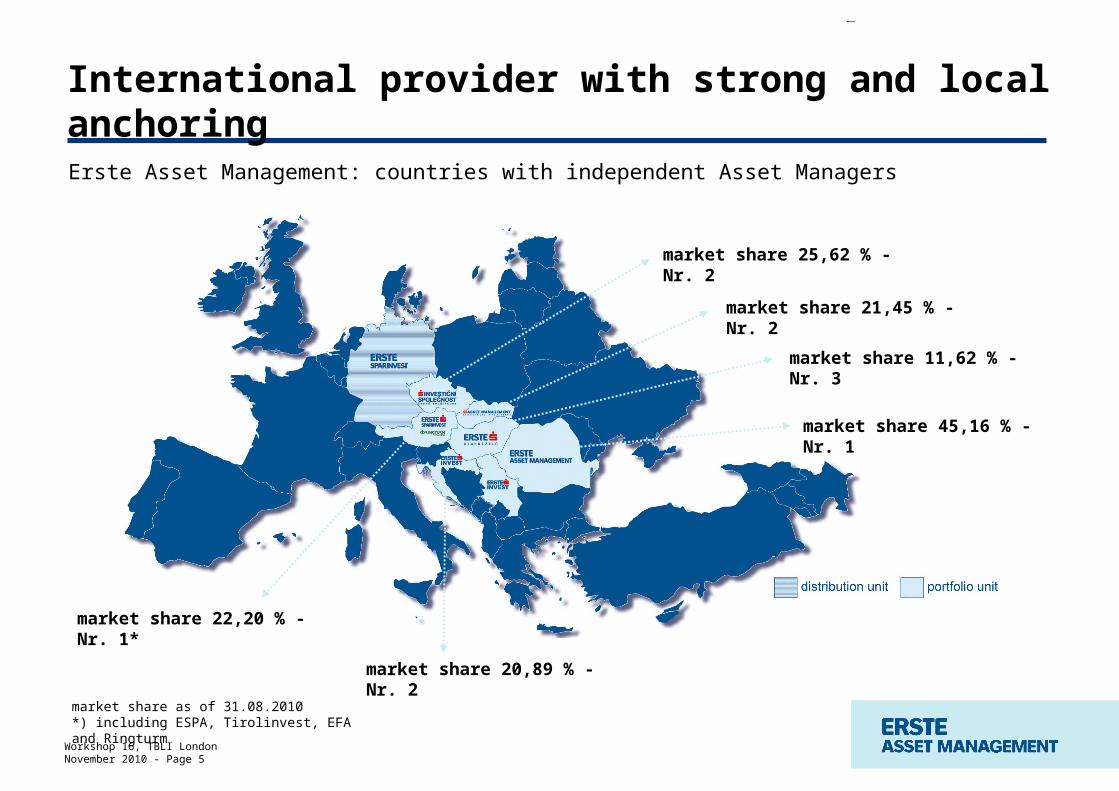

market share 22,20 % - Nr. 1*

market share 25,62 % - Nr. 2

market share 21,45 % - Nr. 2

market share 45,16 % - Nr. 1

market share 20,89 % - Nr. 2

market share 11,62 % - Nr. 3

market share as of 31.08.2010*) including ESPA, Tirolinvest, EFA and Ringturm

International provider with strong and local anchoring

Erste Asset Management: countries with independent Asset Managers

Workshop 16, TBLI LondonNovember 2010 - Page 6

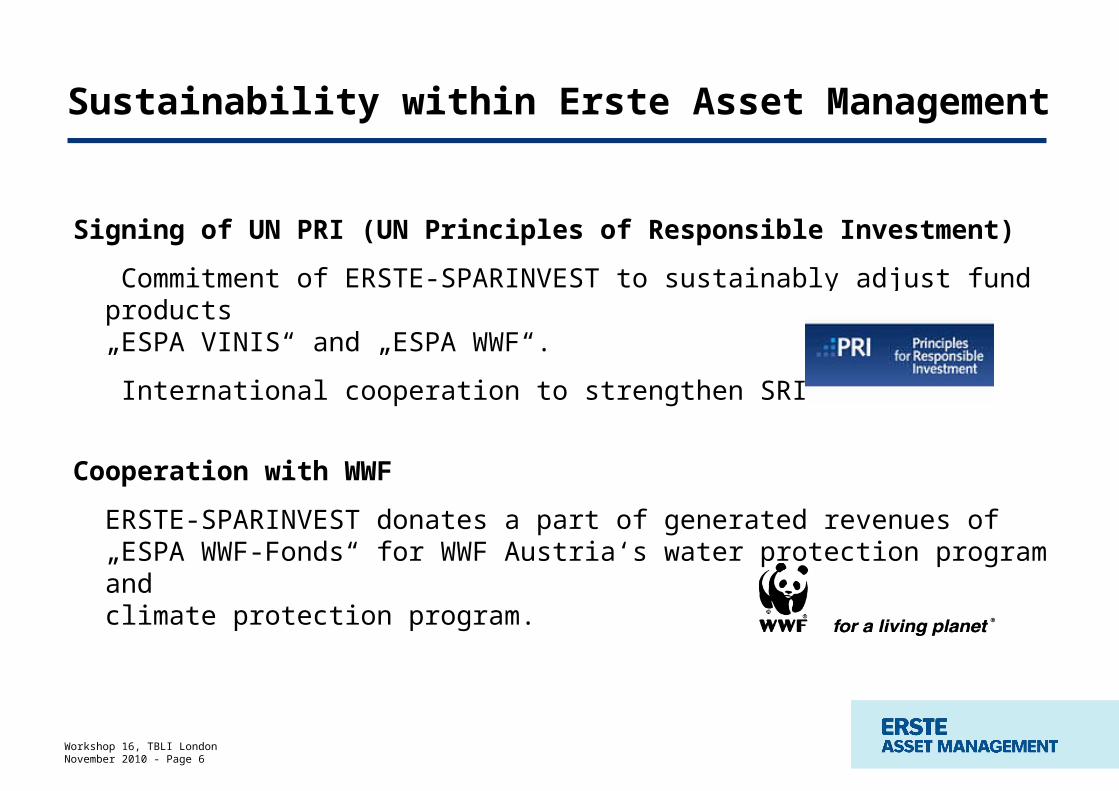

Signing of UN PRI (UN Principles of Responsible Investment)

Commitment of ERSTE-SPARINVEST to sustainably adjust fund products „ESPA VINIS“ and „ESPA WWF“.

International cooperation to strengthen SRI and ESG.

Cooperation with WWF

ERSTE-SPARINVEST donates a part of generated revenues of „ESPA WWF-Fonds“ for WWF Austria‘s water protection program and climate protection program.

Sustainability within Erste Asset Management

Workshop 16, TBLI LondonNovember 2010 - Page 7

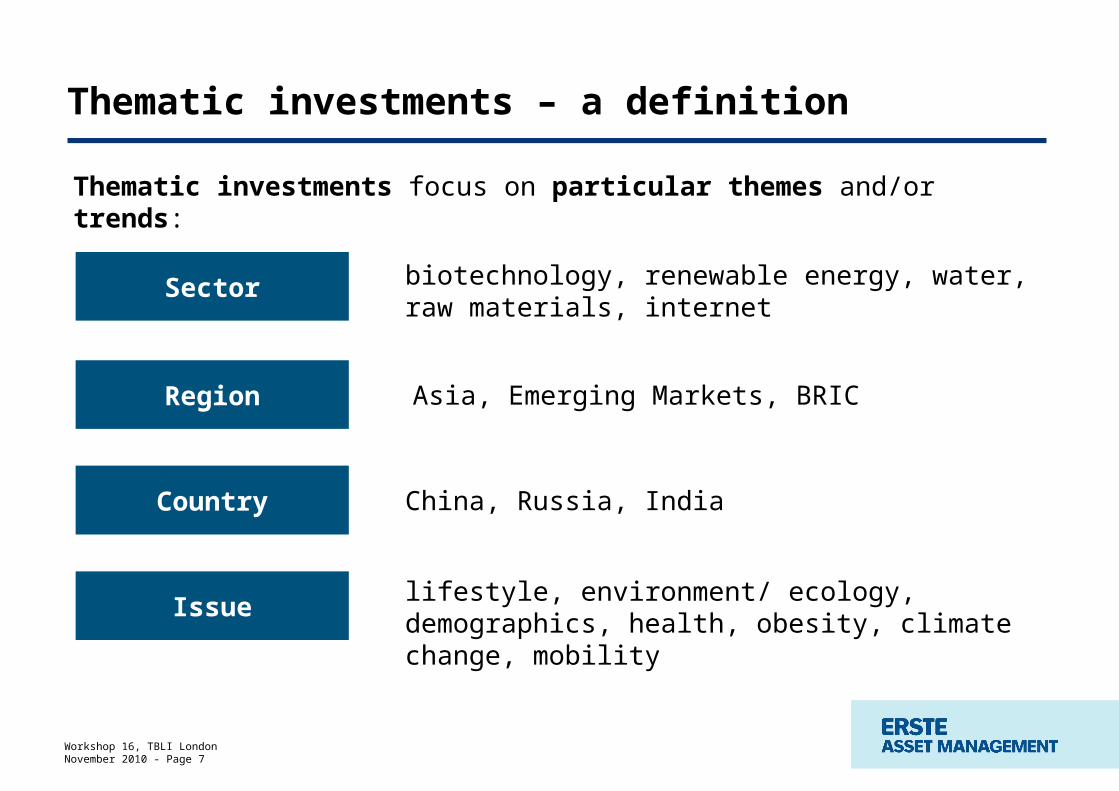

Thematic investments – a definition

China, Russia, India

Sector

Region

Country

Issue

Thematic investments focus on particular themes and/or trends:

biotechnology, renewable energy, water, raw materials, internet

Asia, Emerging Markets, BRIC

lifestyle, environment/ ecology, demographics, health, obesity, climate change, mobility

Workshop 16, TBLI LondonNovember 2010 - Page 8

corporate governance

brand name and reputation

ecological uncertainty

rising energy consumption

emphasis on human capital

trend towards ‘healthy living’

demographic development

publication and consideration of extra-financial data, strengthening of stakeholders

strengthening of customers over companies

strengthening of environmental awareness and the importance of environmental technologies

in search of alternative concepts

more consideration of employees’ interests

focus on production of foods and organic products

long-term concepts for an aging society

is p

rim

aril

y re

late

d t

o

company

individual

Thematic investments – sustainability trends

Workshop 16, TBLI LondonNovember 2010 - Page 9

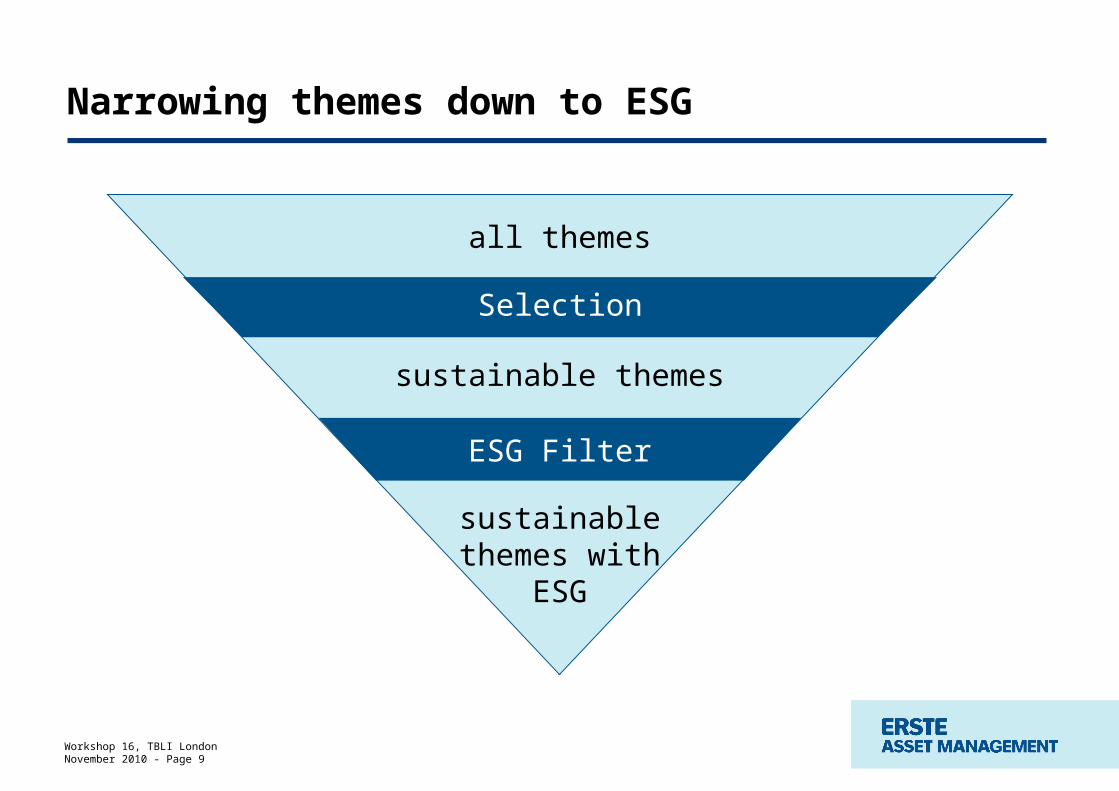

Narrowing themes down to ESG

sustainablethemes with

ESG

Selection

all themes

ESG Filter

sustainable themes

Workshop 16, TBLI LondonNovember 2010 - Page 10

Contact

Erste Asset Management GmbH

Institutional Distribution – International

Tel.: +43 50 100 19960

e-mail: [email protected]

www.erste-am.com

Workshop 16, TBLI LondonNovember 2010 - Page 11

Disclaimer

"This is an advertisement. Our languages of communication are German and English. The latest version of the Prospectus (and any changes thereto) has been published in the “Amtsblatt der Wiener Zeitung”, in accordance with the provisions of the Austrian Investmentfondsgesetz [Investment Funds Act]. Copies are available free of charge to interested parties at the registered offices of both Erste Asset Management GmbH and Erste Group Bank AG. The most recent publication date and details of any other collection offices are published on the Erste Asset Management GmbH website (www.erste-am.com). This document serves to provide additional information to our investors and reflects the knowledge of its authors at the time of going to press. Our analyses and conclusions are of a general nature and do not take into account the personal needs of our investors in terms of income, fiscal situation or attitude to risk. This is not a personal recommendation. It should be noted that past performance is not a reliable indicator of the future performance of a fund."

TBLI Conference London, 12 November, 2010

Thematic Investments and/or ESG Criteria –A Fund Selector’s View

1313

Source: LGT

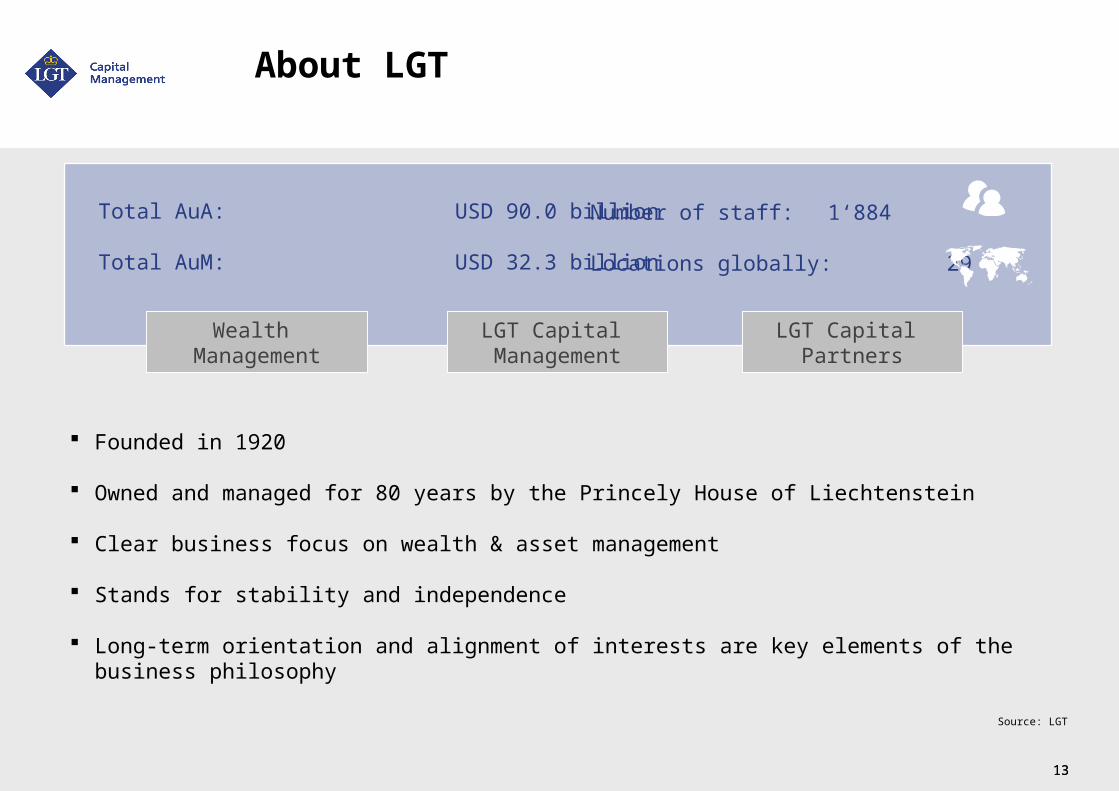

Founded in 1920

Owned and managed for 80 years by the Princely House of Liechtenstein

Clear business focus on wealth & asset management

Stands for stability and independence

Long-term orientation and alignment of interests are key elements of the business philosophy

Total AuA: USD 90.0 billion

Total AuM: USD 32.3 billion

Number of staff: 1‘884

Locations globally: 29

Wealth Management

LGT Capital Partners

LGT Capital Management

About LGT

1414

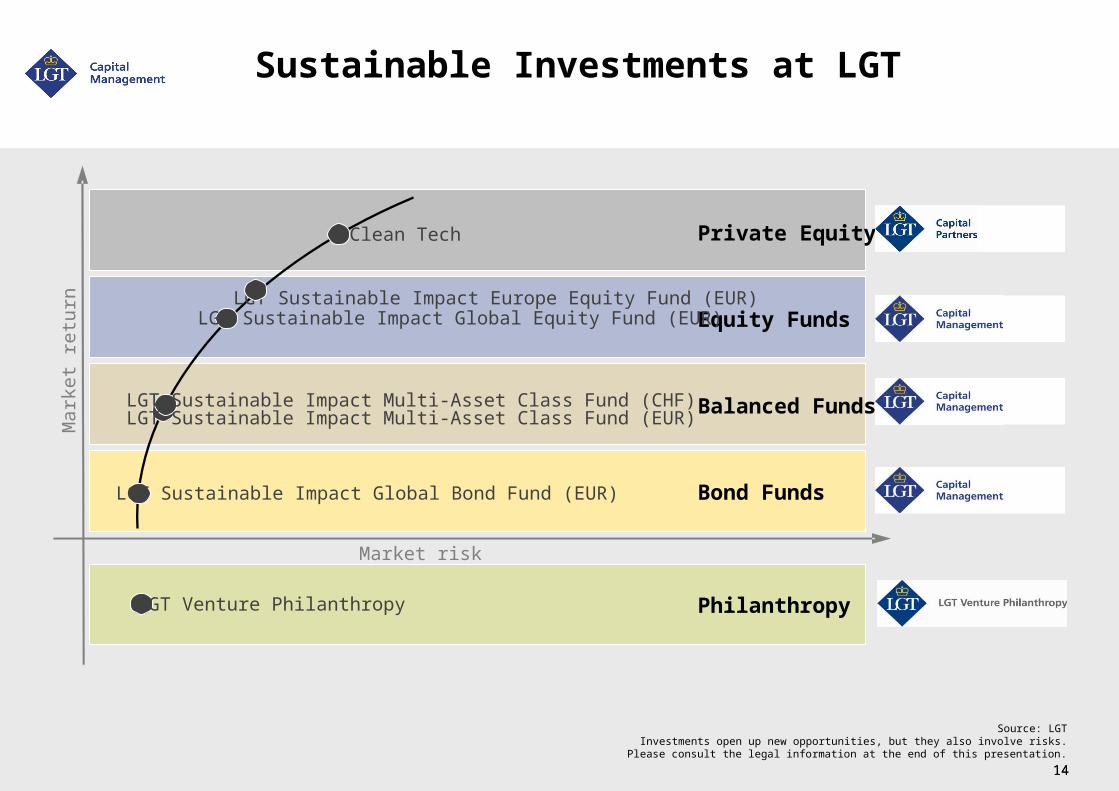

Sustainable Investments at LGTM

ark

et

retu

rn

Market risk

Private Equity

Equity Funds

Balanced Funds

Bond Funds

PhilanthropyLGT Venture Philanthropy

LGT Sustainable Impact Global Bond Fund (EUR)

LGT Sustainable Impact Global Equity Fund (EUR)

Clean Tech

LGT Sustainable Impact Multi-Asset Class Fund (CHF)LGT Sustainable Impact Multi-Asset Class Fund (EUR)

LGT Sustainable Impact Europe Equity Fund (EUR)

Source: LGTInvestments open up new opportunities, but they also involve risks.Please consult the legal information at the end of this presentation.

1515

We aim for thematic funds and ESG criteria!

Source: LGTInvestments open up new opportunities, but they also involve risks.Please consult the legal information at the end of this presentation.

Sustainable Multi-Asset Class Funds

Th

em

ati

c F

un

d S

ele

cti

on

Private Banking

Global sustainability trends offer investment opportunities

We want to take advantage of those trends

At the same time we want to support sustainable development and avoid the risks involved in non-sustainable activities

E S

G

+

1616

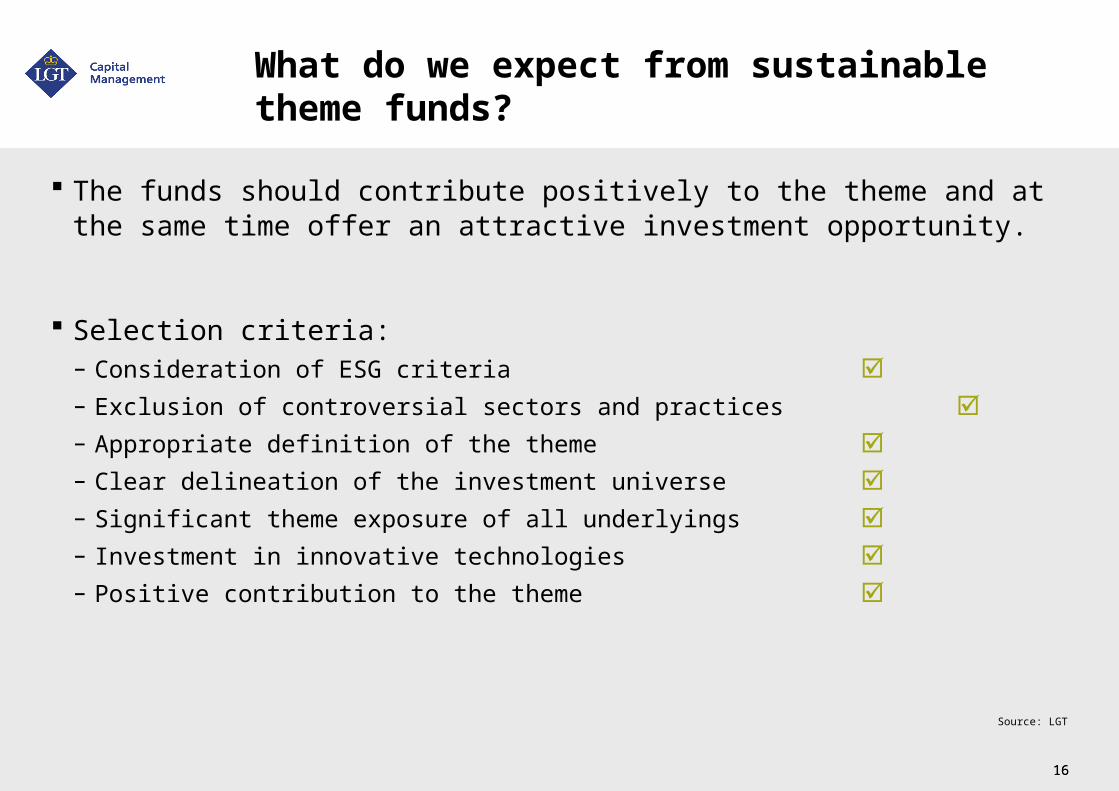

What do we expect from sustainable theme funds?

The funds should contribute positively to the theme and at the same time offer an attractive investment opportunity.

Selection criteria:– Consideration of ESG criteria – Exclusion of controversial sectors and practices – Appropriate definition of the theme – Clear delineation of the investment universe – Significant theme exposure of all underlyings – Investment in innovative technologies – Positive contribution to the theme

Source: LGT

1717

“Tick-box research” is not the way to go!

Possible Shortcomings No consideration of any ESG criteria

Investments in the weapon industry

Inclusion of bottled water producers

Investments with no reference to the water theme

Water exposure of the underlyings is insignificant

Focus on utilities

Investments in companies, which just profit from the theme

0!

Fund 1

Fund 2

Fund ...

Selection Criteria

---

- using the example of water funds -

Source: LGT

1818

Mission impossible?

Source: Internet

1919

Our goal is to find funds that come as close as possible to the “ideal” fund

It is vital for us that the investment philosophy of the funds adheresto the principles of sustainability (big picture!)

To find an appropriate fund, it is important to understand ...

how the managers approach the theme

what their understanding of sustainability is

how well-founded their investment decisions are

We evaluate all the above through intensive conversations with the managers.

Transparency+

Credibility

Source: LGT

2020

Lessons learned ... and still learning

When we consider ESG criteria, the number of funds is reduced significantly

However, we manage to find sustainable theme funds of good quality

Finding those funds requires a very thorough analysis

The sustainable theme fund segment is in a learning and development process

The trend is towards more sustainability

By engaging in a constructive dialogue with the providers we can support this trend

Source: LGT

2121

This document is intended solely for the recipient and may not be duplicated, distributed or published either in electronic or any other form without the prior written consent of LGT Group Foundation. This publication is for your information only and is not intended as an offer, solicitation of an offer, public advertisement or recommendation to buy or sell any investment or other specific product. Its content has been prepared by our staff and is based on sources of information we consider to be reliable. However, we cannot provide any undertaking or guarantee as to it being correct, complete and up to date. The circumstances and principles to which the information contained in this publication relates may change at any time. Once published, therefore, information shall not be understood as implying that no change has taken place since its publication or that it is still up to date. The information in this publication does not constitute an aid for decision-making in relation to financial, legal, tax or other consulting matters, nor should any investment or other decisions be made on the basis of this information alone. It is recommended that advice be obtained from a qualified expert. Investors should be aware that the value of investments can fall as well as rise. Positive performance in the past is therefore no guarantee of positive performance in the future. Forecasts are not a reliable indicator of future value developments. The risk of price and foreign currency losses and of fluctuations in return as a result of unfavorable exchange rate movements cannot be ruled out. There is a possibility that investors will not recover the full amount they initially invested. We disclaim without qualification all liability for any loss or damage of any kind, whether direct, indirect or consequential, which may be incurred through the use of this publication. This publication is not intended for persons subject to legislation that prohibits its distribution or makes its distribution contingent upon an approval. Any person coming into possession of this publication shall therefore be obliged to find out about any restrictions that may apply and to comply with them.

It is up to potential investors to obtain comprehensive information and appropriate advice in their home country, country of residence or country of domicile about the applicable legal requirements and any tax consequences, foreign currency restrictions or foreign exchange controls and any other aspects that are of relevance prior to any decision to subscribe to, purchase, own, exchange or redeem such investments, or enter into any other transaction in relation to same.

The securities and rights mentioned in this document may not be purchased or held by investors or for investors domiciled in the USA and/or with US citizenship, nor may such securities and rights be transferred to them.

Legal information

2222

LGT Capital ManagementContact Details

LGT Capital Management Ltd.Schützenstrasse 68808 Pfäffikon Switzerland

Phone +41 55 415 92 11 Fax +41 55 415 92 30 E-Mail [email protected] www.lgt.com

Andrea FerchSenior Fund AnalystPhone +41 55 415 93 53 Fax +41 55 415 94 95 E-Mail [email protected]

2323

Picture description

"Artists Exploring the Austrian Alps", c. 1819

HEINRICH REINHOLD1788–1825Reinhold was born in Gera, near Leipzig, and studied in several places, including Vienna. Having spent a short period working for Napoleon, making engravings of his military triumphal marches, he joined the circle of artists around Josef Anton Koch, who encouraged him in his study of nature and, in particular, of the Alps.The painting was produced following Reinhold's study trip through the Alps in the summer of 1818 and shows a simplified mountain panorama featuring his fellow painters Johann Christoph Erhard and Ernst Welker, the latter accompanying him to Rome one year later.

© Collections of the Prince of Liechtenstein, Vaduz – ViennaLIECHTENSTEIN MUSEUM, Vienna. www.liechtensteinmuseum.at

2424

overview

Case Studies of Thematic Fund Holdings and

their Responsibility Rating

TBLI Conference,

12 November, 2010, London

1. oekom research background

2. oekom Corporate Rating

3. Case studies of thematic fund holdings

2525

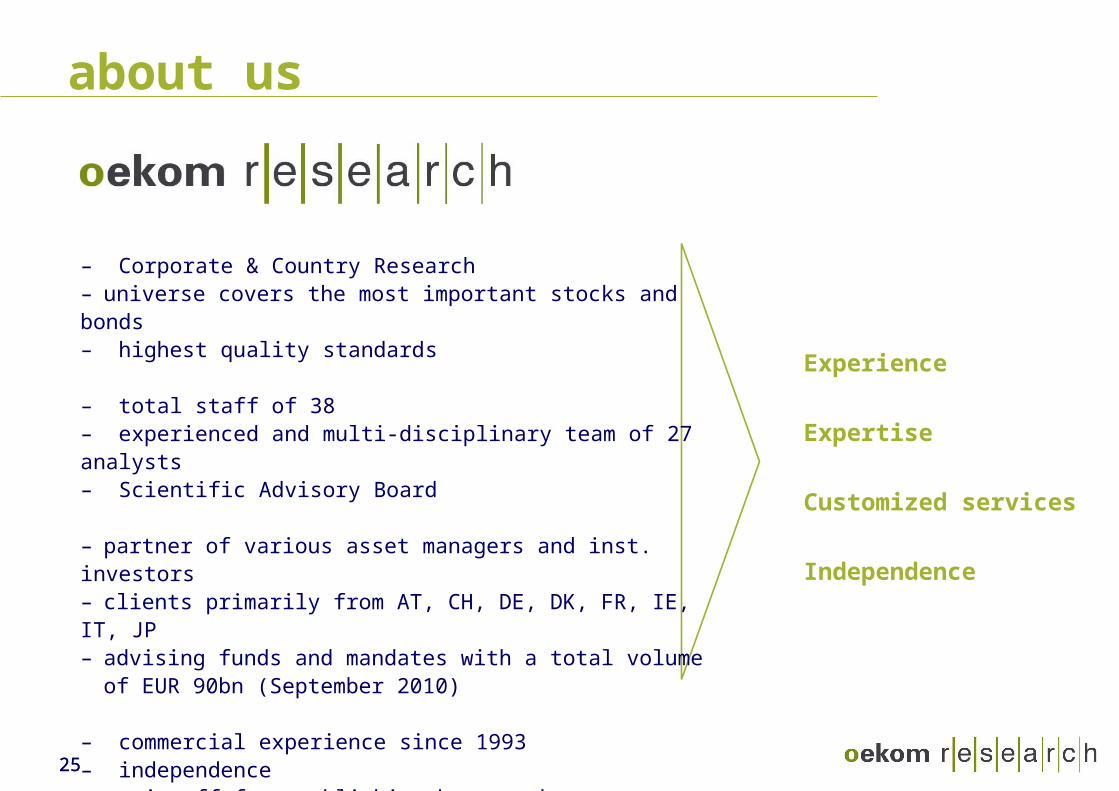

about us

Experience

Expertise

Customized services

Independence

– Corporate & Country Research– universe covers the most important stocks and bonds– highest quality standards

– total staff of 38– experienced and multi-disciplinary team of 27 analysts– Scientific Advisory Board

– partner of various asset managers and inst. investors– clients primarily from AT, CH, DE, DK, FR, IE, IT, JP– advising funds and mandates with a total volume

of EUR 90bn (September 2010)

– commercial experience since 1993– independence– spin-off from publishing house oekom

2626

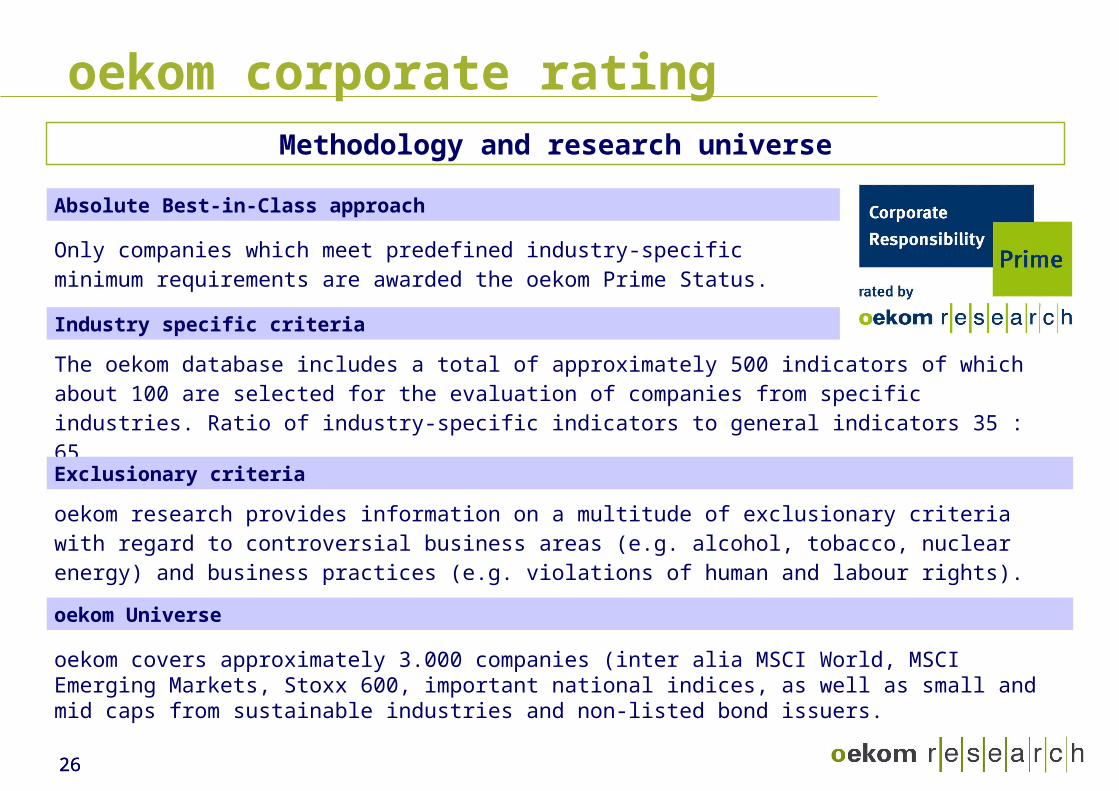

oekom corporate ratingMethodology and research universe

Absolute Best-in-Class approach

Only companies which meet predefined industry-specific minimum requirements are awarded the oekom Prime Status.

Industry specific criteria

The oekom database includes a total of approximately 500 indicators of which about 100 are selected for the evaluation of companies from specific industries. Ratio of industry-specific indicators to general indicators 35 : 65.

Exclusionary criteria

oekom research provides information on a multitude of exclusionary criteria with regard to controversial business areas (e.g. alcohol, tobacco, nuclear energy) and business practices (e.g. violations of human and labour rights).

oekom Universe

oekom covers approximately 3.000 companies (inter alia MSCI World, MSCI Emerging Markets, Stoxx 600, important national indices, as well as small and mid caps from sustainable industries and non-listed bond issuers.

2727

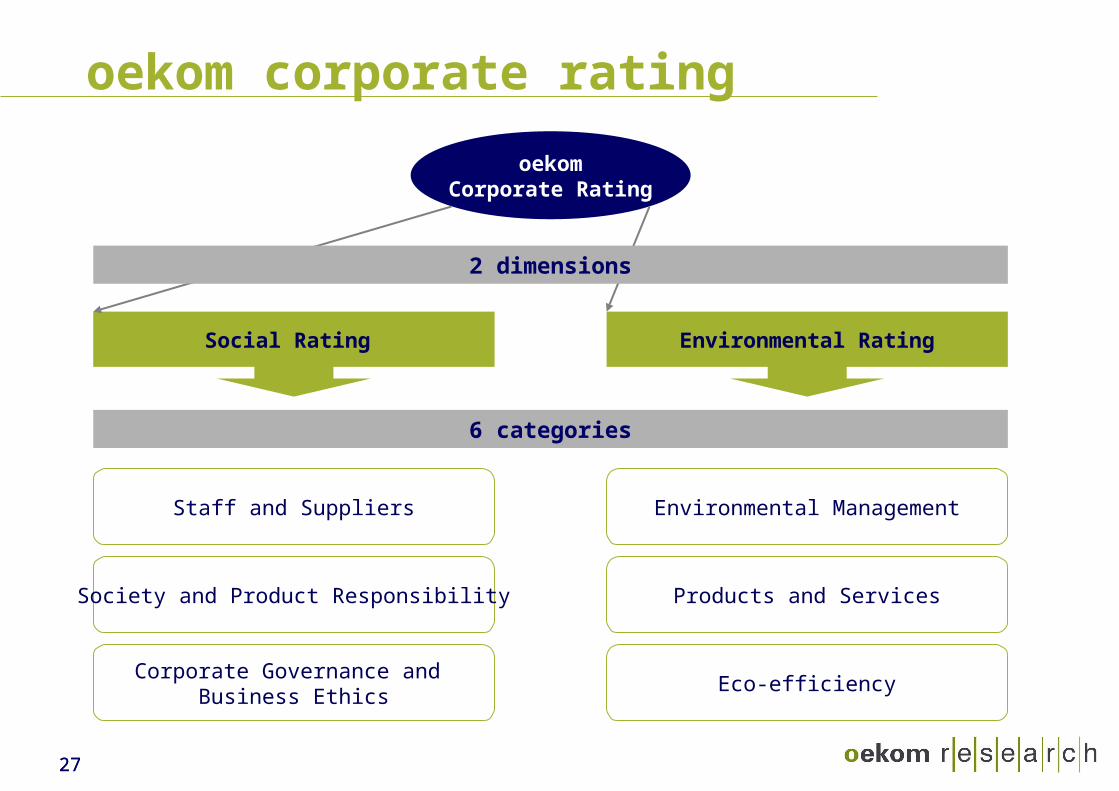

oekom corporate rating

oekomCorporate Rating

Environmental Rating

Environmental Management

Products and Services

Eco-efficiency

Social Rating

Staff and Suppliers

Society and Product Responsibility

Corporate Governance and Business Ethics

6 categories

2 dimensions

2828

oekom corporate rating

AbortionAlcoholBiocidesChlororganic Mass ProductsEmbryonic ResearchGamblingGMOsMilitaryNuclear PowerPornographyTobacco

Controversial

business areas

Animal TestingBusiness MalpracticeChild LabourControversial Environmental PracticesHuman Rights ViolationsLabour Rights Violations

Controversial

business practices

Client specific exclusionary criteria

2929

thematic fund approaches

Different investment approaches

funds often not limited to investments in their respective theme

sometimes no reference to any sustainability criteria (positive or negative)

“Problem solvers”

Small and mid caps from “sustainable industries” (e.g. renewable energy, recycling)

“Standard values”

Large caps which are (sometimes marginally)

involved in problem solving

“Profiteers”

Companies which profit from e.g. climate change or water scarcity but do not actively contribute to the solution of

the problem

3030

examples of investment strategies

Climate Change Fund:“… investing at least two thirds of its total non-cash assets in a well diversified portfolio of ... companies developing activities related to climate change such as alternative energies, water, waste and pollution, energy efficiency, low carbon players, industry transformers“

Water Fund:“… investments in securities of companies with activities in the water sector (utilities, waste water treatment, transportation, water desalination, treatment of waste products, equipment, services, irrigation and agriculture, nutrition, conditioning and distribution of water, hydropower, financing, etc.) ... may also invest a maximum of one third of the fund assets in equity securities and rights of companies that don't meet the above mentioned requirements regarding business sector ...“

Environment Fund:“… fund invests in ... companies with a large market capitalisation that have the best processes for ecological issues ... of their sector; or ... innovative companies with low or medium market capitalisation that develop new technologies for environmental protection“

3131

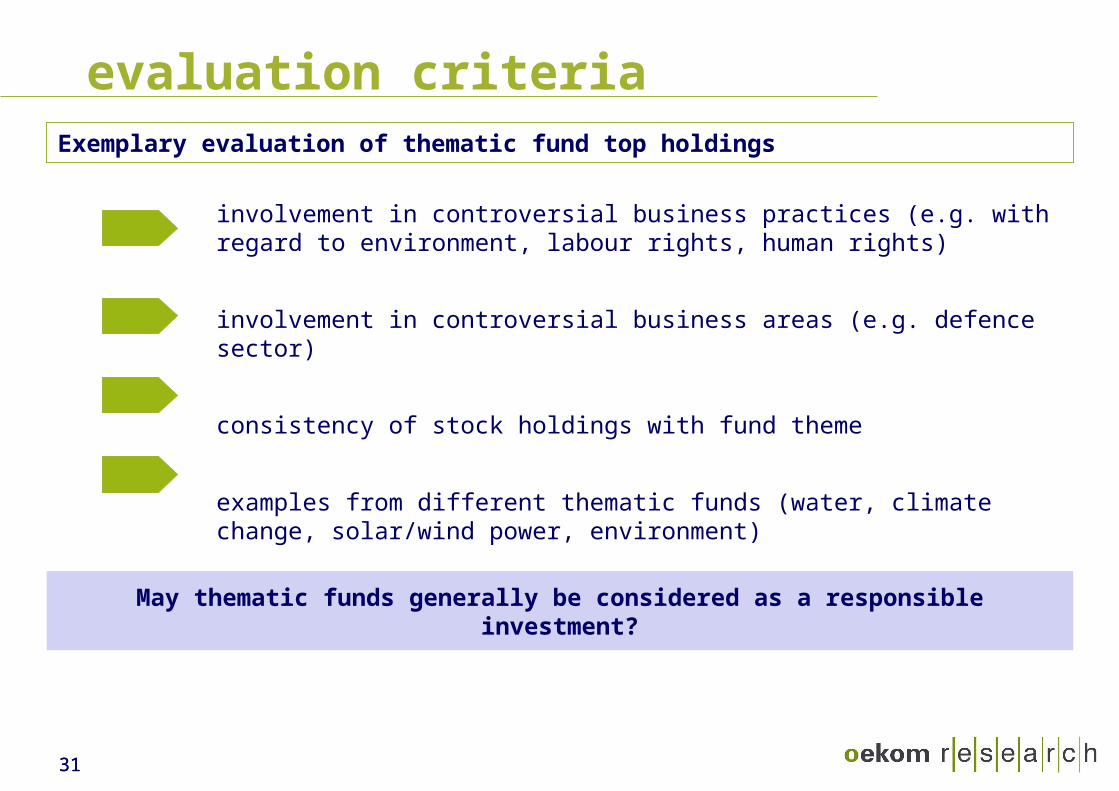

evaluation criteriaExemplary evaluation of thematic fund top holdings

involvement in controversial business practices (e.g. with regard to environment, labour rights, human rights)

involvement in controversial business areas (e.g. defence sector)

consistency of stock holdings with fund theme

examples from different thematic funds (water, climate change, solar/wind power, environment)

May thematic funds generally be considered as a responsible investment?

3232

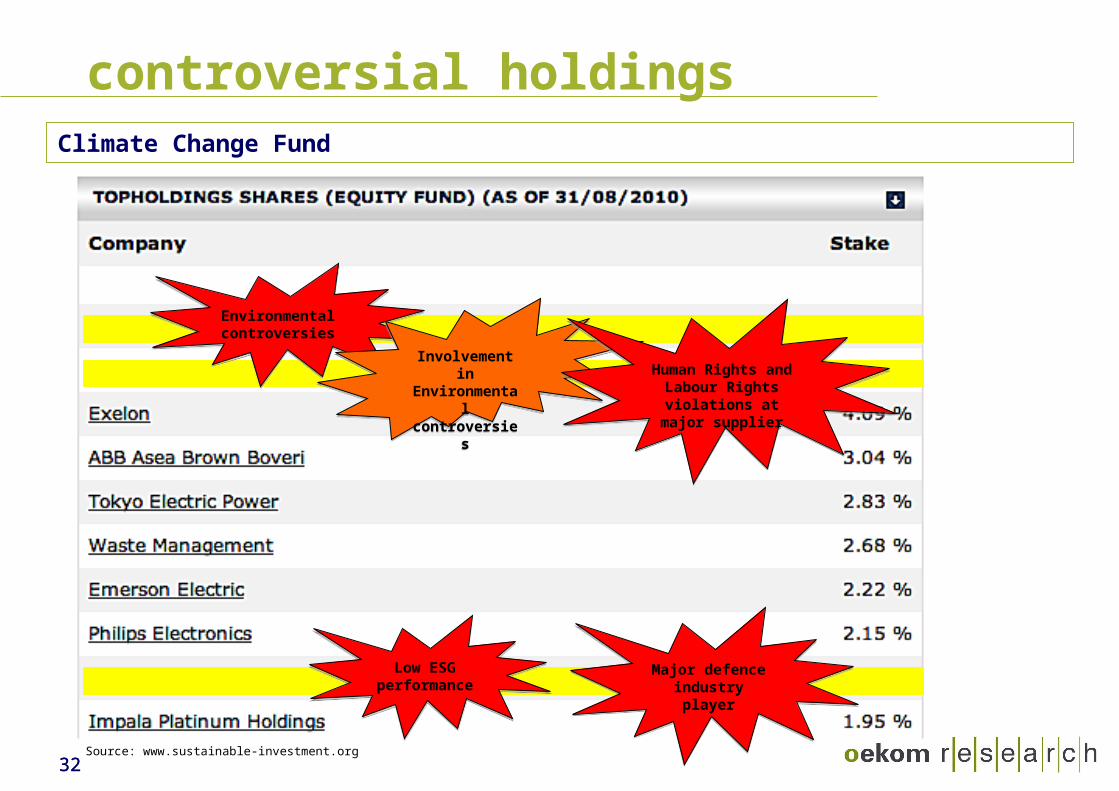

controversial holdingsClimate Change Fund

Low ESG performance

Low ESG performance

Environmental controversiesEnvironmental controversies

Involvement in Environmental controversies

Involvement in Environmental controversies

Human Rights and Labour Rights

violations at major supplier

Human Rights and Labour Rights

violations at major supplier

Source: www.sustainable-investment.org

Major defence industry playerMajor defence industry player

3333

controversial holdingsWater Fund

Source: www.sustainable-investment.org

Human Rights and Labour

Rights violations at major supplier

Human Rights and Labour

Rights violations at major supplier

Involvement in Environmental controversies

Involvement in Environmental controversies

3434

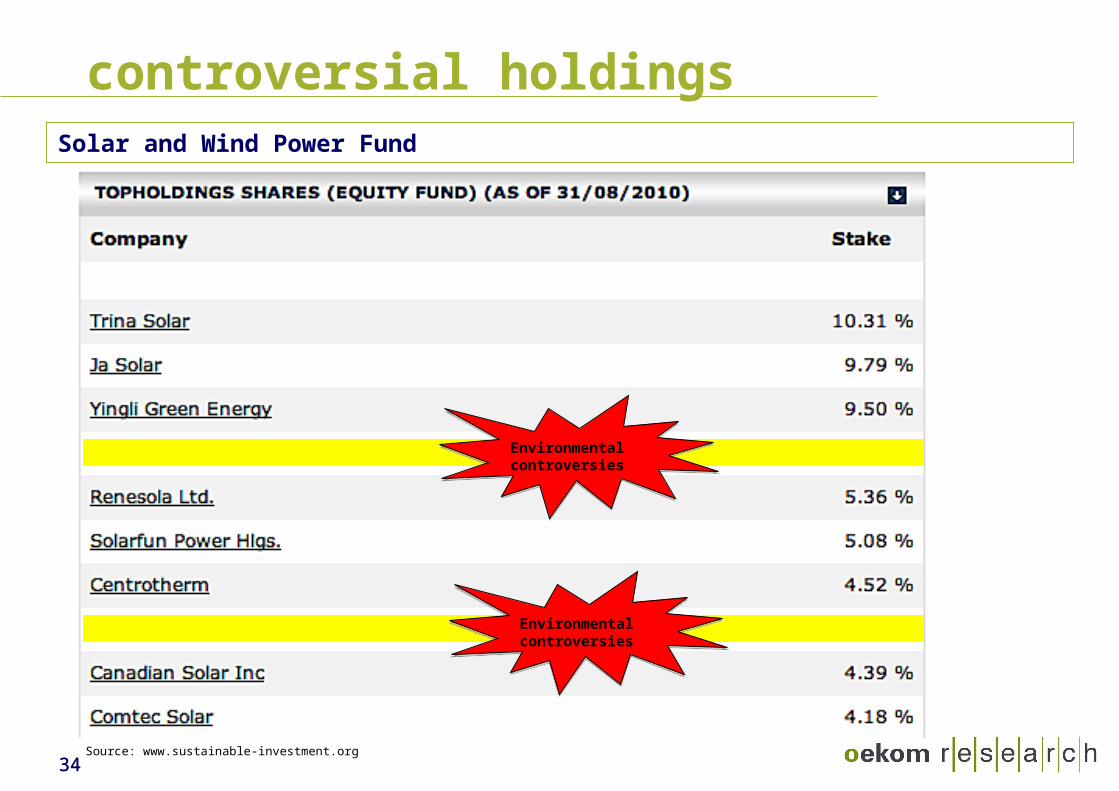

controversial holdingsSolar and Wind Power Fund

Source: www.sustainable-investment.org

Environmental controversiesEnvironmental controversies

Environmental controversiesEnvironmental controversies

3535

controversial holdingsEnvironment Fund

Source: www.sustainable-investment.org

Environmental controversies

Environmental controversies

Environmental controversies Environmental controversies

Human Rights and Labour Rights

violations

Human Rights and Labour Rights

violations

Environmental controversiesEnvironmental controversies

Human Rights

violations

Human Rights

violations

Environmental controversies Environmental controversies

3636

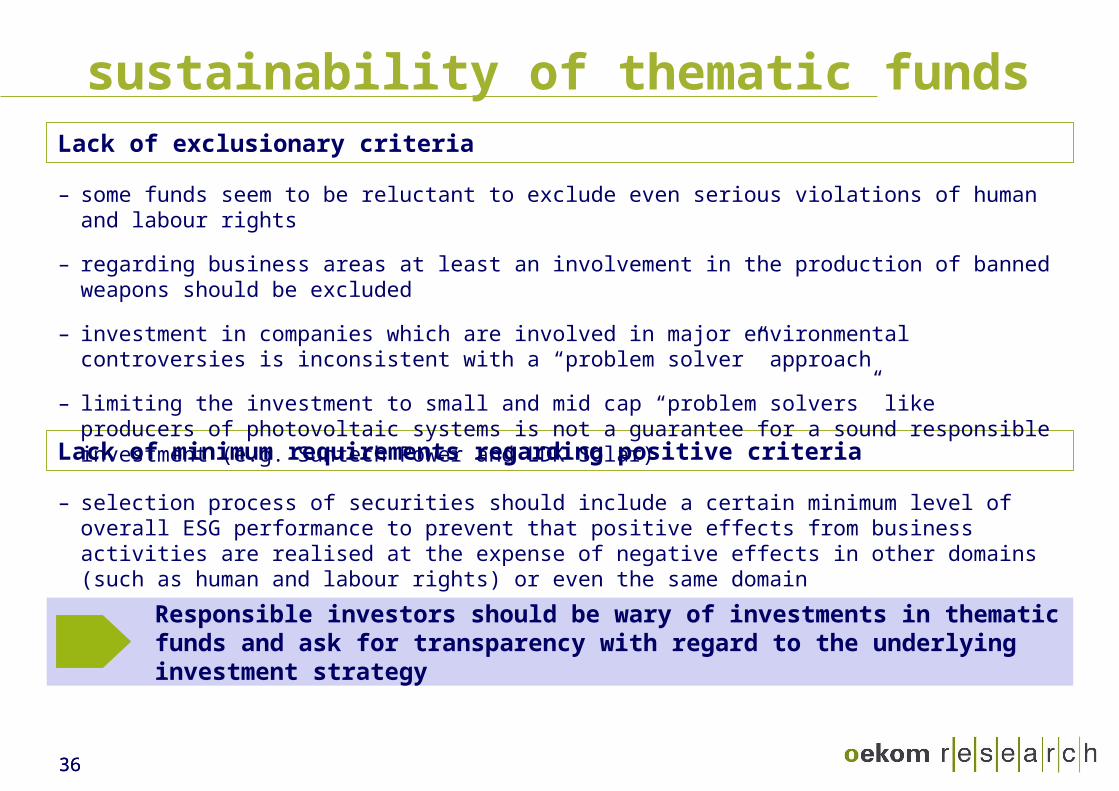

sustainability of thematic fundsLack of exclusionary criteria

Lack of minimum requirements regarding positive criteria

– some funds seem to be reluctant to exclude even serious violations of human and labour rights

– regarding business areas at least an involvement in the production of banned weapons should be excluded

– investment in companies which are involved in major environmental controversies is inconsistent with a “problem solver” approach

– limiting the investment to small and mid cap “problem solvers” like producers of photovoltaic systems is not a guarantee for a sound responsible investment (e.g. Suntech Power and LDK Solar)

– selection process of securities should include a certain minimum level of overall ESG performance to prevent that positive effects from business activities are realised at the expense of negative effects in other domains (such as human and labour rights) or even the same domain

Responsible investors should be wary of investments in thematic funds and ask for transparency with regard to the underlying investment strategy

3737

oekom research AGGoethestr. 28D-80336 Munich

Tel: +49/89/54 41 84-90Fax: +49/89/54 41 84-99

Email: [email protected]: www.oekom-research.com

contact

Can Sustainability Add Value To Thematic Investment?

Workshop 16TBLI Conference 2010, London

Wolfgang Pinner, MBA

Workshop 16, TBLI LondonNovember 2010 - Page 39

Agenda

EAM approach in thematic sustainability investment

Management tools in thematic sustainability investment

Value addition of sustainability in thematic investment

Workshop 16, TBLI LondonNovember 2010 - Page 40

EAM approach to thematic vs sustainability investment

Sustainability Thematic Thematic funds funds sustainability funds

- ESG driven yes no yes - Criteriology often no yes

- Investment focus total economy future trends future sustainability diversified approach focused approach trends, focused

approach- Investment universe broad narrow narrow- Sector coverage high low low

- Company growth (above) average high high (long-term)- Fund return target outperform high absolute high absolute

benchmark return return

- Tracking error/ volatility low/ medium high high

-

- Research specialised rating no rating agency specialised ratingagencies agencies (& committee)

- Sustainability based included possible sine qua nonthemes

I ESG

II Universe

III Performance

IV Research

Workshop 16, TBLI LondonNovember 2010 - Page 41

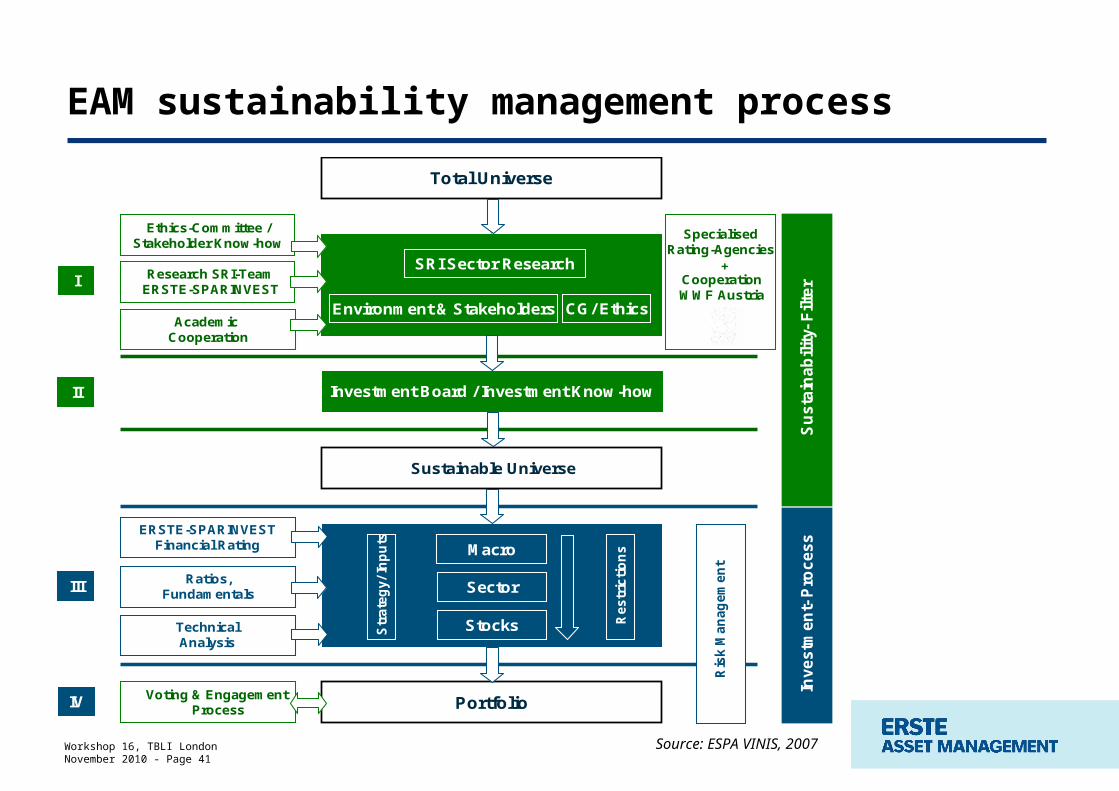

EAM sustainability management process

Source: ESPA VINIS, 2007

Total Universe

Sustainable Universe

Portfolio

Ratios, Fundamentals

Technical Analysis

Ethics-Committee / Stakeholder Know-how

SRI Sector Research

Environment & Stakeholders CG/ Ethics

Investment Board / Investment Know-how

Academic Cooperation

Su

sta

ina

bil

ity -F

ilte

r

ERSTE-SPARINVESTFinancial Rating

Voting & Engagement Process

Research SRI-Team ERSTE-SPARINVEST

Specialised Rating-Agencies

HOLD

Ris

k M

an

ag

em

en

t

Inve

stm

en

t -P

roc

ess

I

II

III

IV

Re

str

icti

on

s

Str

ate

gy/

Inp

uts

Sector

Macro

Stocks

Cooperation WWF Austria

+

Workshop 16, TBLI LondonNovember 2010 - Page 42

Thematic vs sustainability funds – performance track record and TE

TE ~12

TE ~4

VINIS STOCK GLOBAL T BM ESPA VINIS Stock Global -1D WWF STOCK UMWELT T (AT0000705678)

70,00

80,00

90,00

100,00

110,00

120,00

130,00

140,00

150,00

160,00

170,00

180,00

190,00

200,00

210,00

220,00

230,00

240,00

11.07.200309.12.2003

14.05.200413.10.2004

17.03.200519.08.2005

23.01.200627.06.2006

27.11.200603.05.2007

03.10.200707.03.2008

08.08.200814.01.2009

18.06.200913.11.2009

21.04.201020.09.2010

29.10.2010

Performance seit 11/07/2003ESPA VINIS STOCK GLOBAL 50,39%ESPA WWF STOCK UMWELT 39,75%MSCI World in EUR netdiv 28,74%

TE ~12

TE ~4

Workshop 16, TBLI LondonNovember 2010 - Page 43

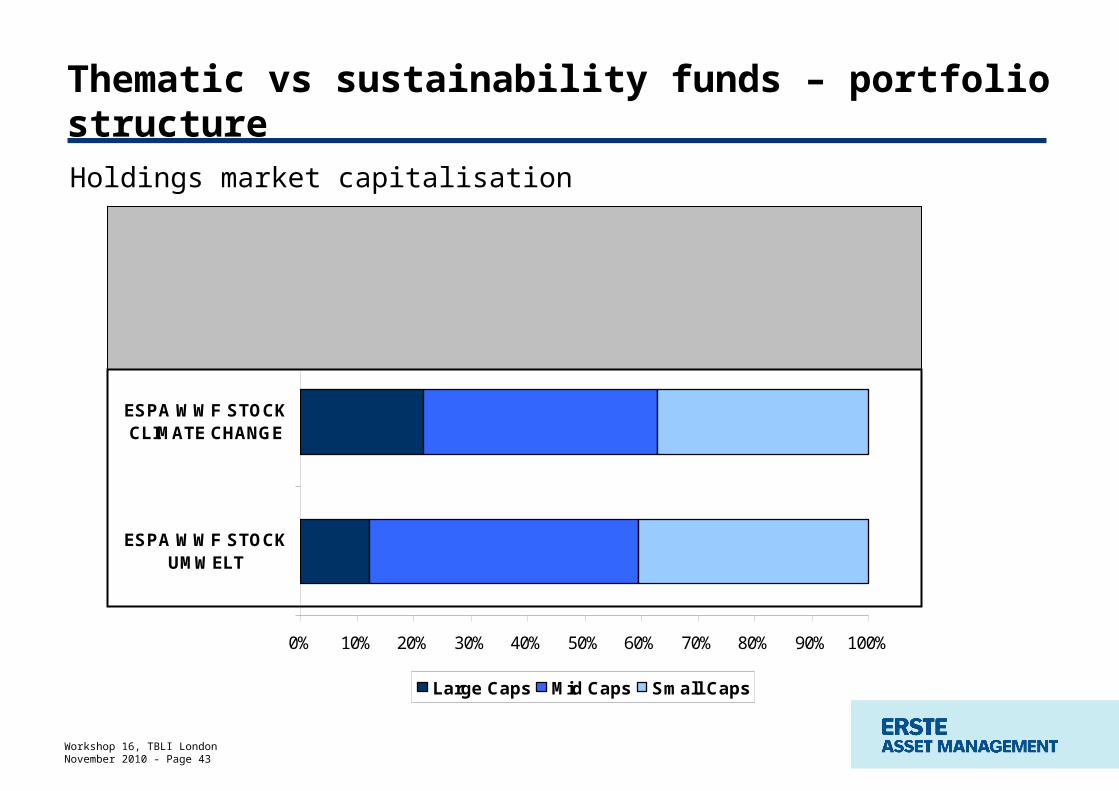

Holdings market capitalisation

Thematic vs sustainability funds – portfolio structure

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

ESPA WWF STOCKUMWELT

ESPA WWF STOCKCLIMATE CHANGE

ESPA VINIS STOCKGLOBAL

Large Caps Mid Caps Small Caps

Workshop 16, TBLI LondonNovember 2010 - Page 44

Agenda

EAM approach in thematic sustainability investment

Management tools in thematic sustainability investment

Value addition of sustainability in thematic investment

Workshop 16, TBLI LondonNovember 2010 - Page 45

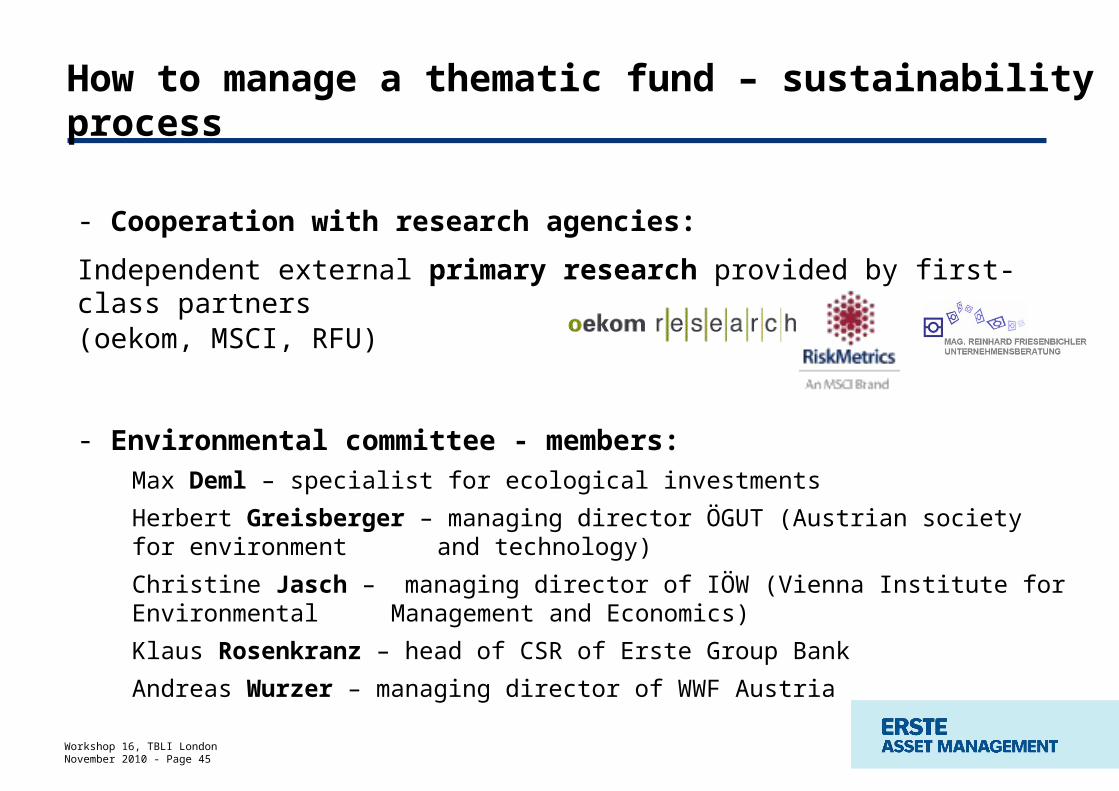

- Cooperation with research agencies:

Independent external primary research provided by first-class partners (oekom, MSCI, RFU)

- Environmental committee - members: Max Deml – specialist for ecological investments

Herbert Greisberger – managing director ÖGUT (Austrian society for environment and technology)

Christine Jasch – managing director of IÖW (Vienna Institute for Environmental Management and Economics)

Klaus Rosenkranz – head of CSR of Erste Group Bank

Andreas Wurzer – managing director of WWF Austria

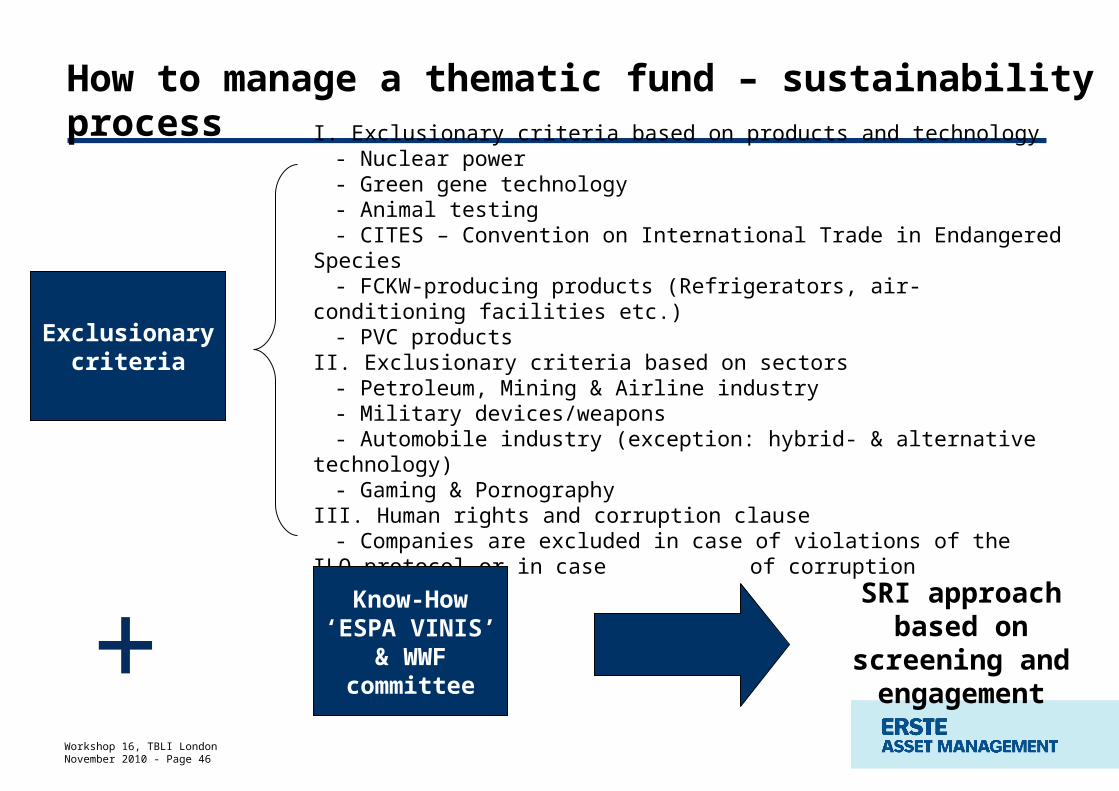

How to manage a thematic fund – sustainability process

Workshop 16, TBLI LondonNovember 2010 - Page 46

SRI approach based on screening and

engagement

Exclusionary criteria

I. Exclusionary criteria based on products and technology - Nuclear power- Green gene technology - Animal testing- CITES – Convention on International Trade in Endangered Species - FCKW-producing products (Refrigerators, air-conditioning facilities etc.)- PVC products

II. Exclusionary criteria based on sectors - Petroleum, Mining & Airline industry- Military devices/weapons- Automobile industry (exception: hybrid- & alternative technology)- Gaming & Pornography

III. Human rights and corruption clause- Companies are excluded in case of violations of the ILO-protocol or in case

of corruption

Know-How ‘ESPA VINIS’ &

WWF committee+

How to manage a thematic fund – sustainability process

Workshop 16, TBLI LondonNovember 2010 - Page 47

Cooperation with WWF through environmental committee(extract of list of discussed companies):

…

How to manage a thematic fund – sustainability process

Workshop 16, TBLI LondonNovember 2010 - Page 48

Total universe (2.000+

equities)

Global equities

SRI filterLevel I & II

FundamentalselectionLevel III

Portfolioconstruction

Level IV

MSCI World net.div.& ex-benchmark universe

Thematic universe (300 equities)

Fundamental analysisLiquidity analysis Thematic analysis(200 equities)

Fundportfolio

(70-100holdings)

How to manage a thematic fund – portfolio construction

Environmental committee

initiated by WWF

Workshop 16, TBLI LondonNovember 2010 - Page 49

Agenda

EAM approach in thematic sustainability investment

Management tools in thematic sustainability investment

Value addition of sustainability in thematic investment

Workshop 16, TBLI LondonNovember 2010 - Page 50

Thematic sustainability vs conventional thematic investments – characteristics of SRI

Sustainability funds Thematic sustainability

funds

vs traditional funds vs thematic funds

- ‘diversification effect’ slightly negativenegative

- ‘small companies effect’ long-term positive long-term very positive

- ‘anticipation effect’ positive neutral

- ‘information effect’ positive neutral

- ‘positive selection effect’ positivepositive

Workshop 16, TBLI LondonNovember 2010 - Page 51

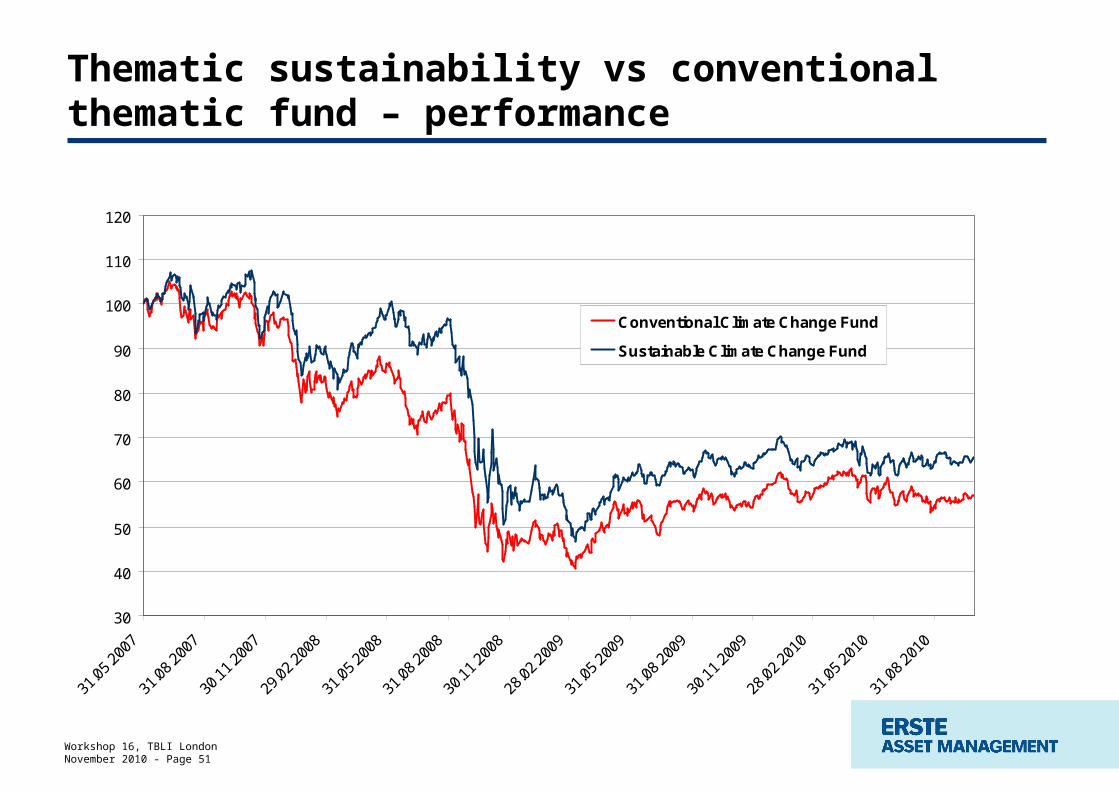

Thematic sustainability vs conventional thematic fund – performance

Sustainable Thematic Fund vs. Conventional Thematic Fund

30

40

50

60

70

80

90

100

110

120

31.0

5.20

07

31.0

8.20

07

30.1

1.20

07

29.0

2.20

08

31.0

5.20

08

31.0

8.20

08

30.1

1.20

08

28.0

2.20

09

31.0

5.20

09

31.0

8.20

09

30.1

1.20

09

28.0

2.20

10

31.0

5.20

10

31.0

8.20

10

Conventional Climate Change Fund

Sustainable Climate Change Fund

Workshop 16, TBLI LondonNovember 2010 - Page 52

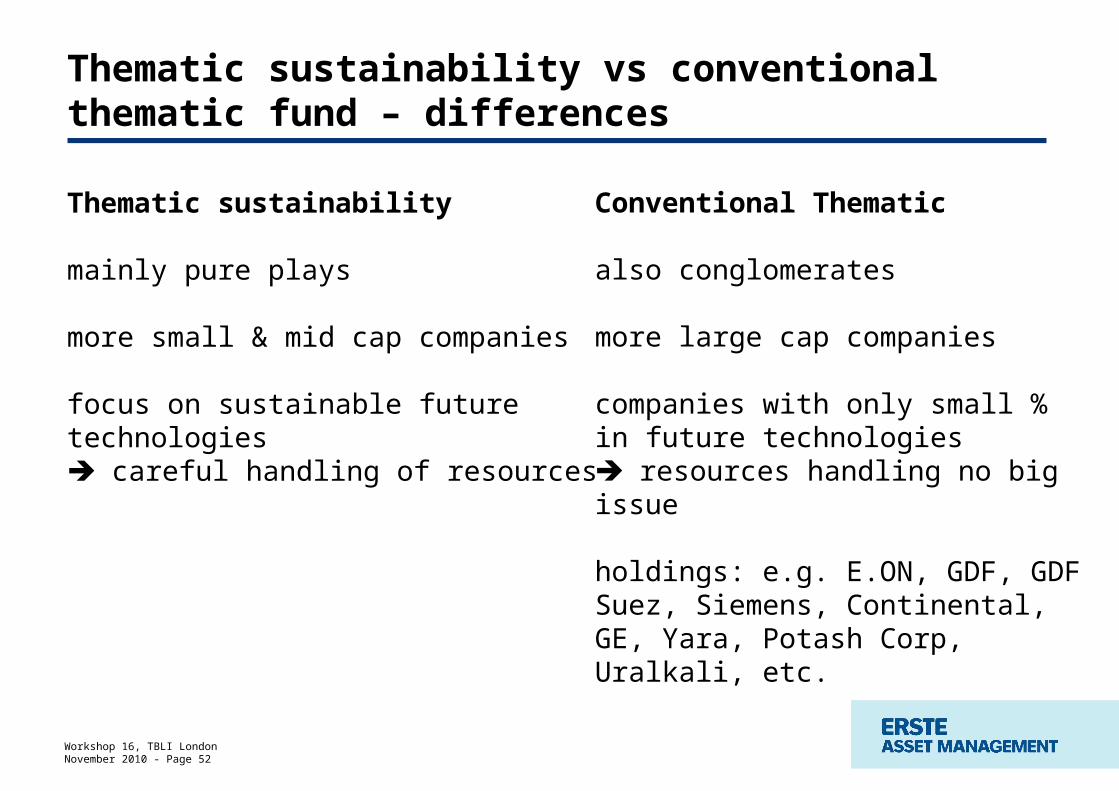

Thematic sustainability

mainly pure plays

more small & mid cap companies

focus on sustainable future technologies careful handling of resources

Thematic sustainability vs conventional thematic fund – differences

Conventional Thematic

also conglomerates

more large cap companies

companies with only small % in future technologies resources handling no big issue

holdings: e.g. E.ON, GDF, GDF Suez, Siemens, Continental, GE, Yara, Potash Corp, Uralkali, etc.

Workshop 16, TBLI LondonNovember 2010 - Page 53

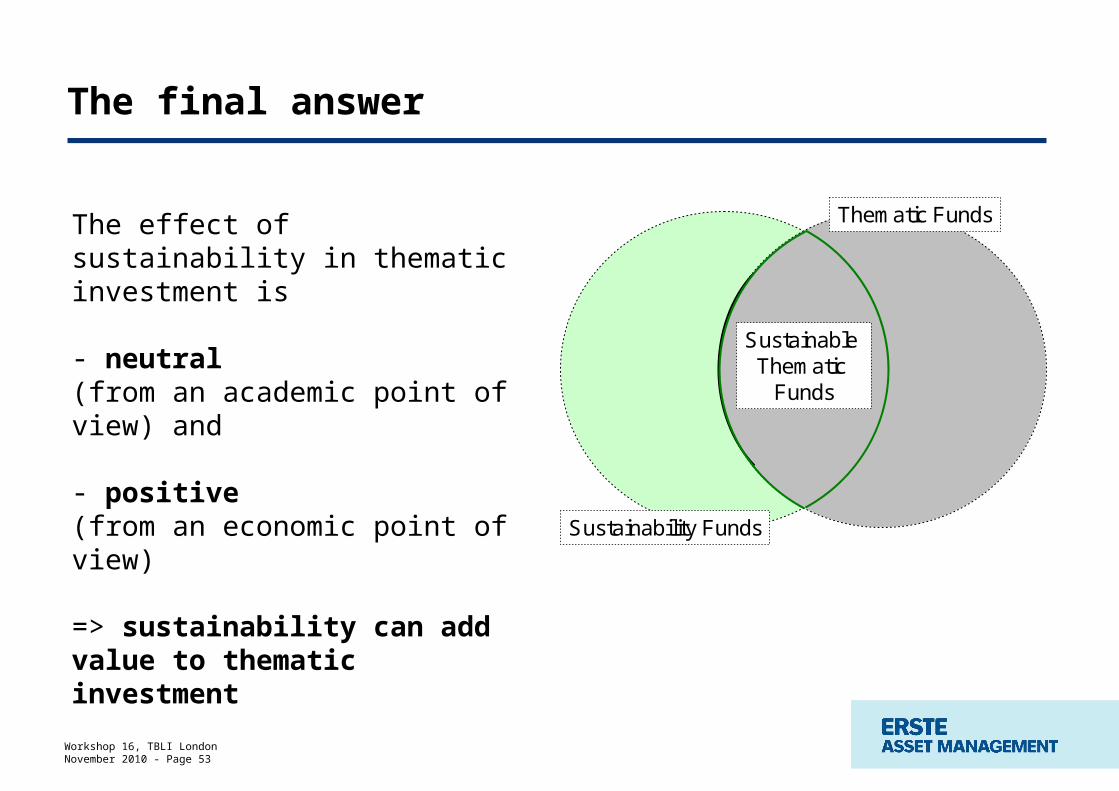

The final answer

The effect of sustainability in thematic investment is

- neutral (from an academic point of view) and - positive(from an economic point of view)

=> sustainability can add value to thematic investment

Sustainability Funds

Thematic Funds

SustainableThematic

Funds

Workshop 16, TBLI LondonNovember 2010 - Page 54

Disclaimer

"This is an advertisement. Our languages of communication are German and English. The latest version of the Prospectus (and any changes thereto) has been published in the “Amtsblatt der Wiener Zeitung”, in accordance with the provisions of the Austrian Investmentfondsgesetz [Investment Funds Act]. Copies are available free of charge to interested parties at the registered offices of both Erste Asset Management GmbH and Erste Group Bank AG. The most recent publication date and details of any other collection offices are published on the Erste Asset Management GmbH website (www.erste-am.com). This document serves to provide additional information to our investors and reflects the knowledge of its authors at the time of going to press. Our analyses and conclusions are of a general nature and do not take into account the personal needs of our investors in terms of income, fiscal situation or attitude to risk. This is not a personal recommendation. It should be noted that past performance is not a reliable indicator of the future performance of a fund."