aja half year results - presentation - home page - astro ... group... · aja half year results -...

TRANSCRIPT

ASX/Media Release

24 February 2010

AJA HALF YEAR RESULTS - PRESENTATION

We attach the Presentation relating to Astro Japan Property Group’s Half Year Results to 31 December 2009.

ENDS Investor & Media Enquiries: Eric Lucas Ian Hay Senior Advisor Chief Financial Officer Phone: +61 2 8987 3900 (Australia) Phone: +61 2 8987 3902 +81 3 3238 1671 (Japan) About Astro Japan Property Group Astro Japan Property Group is a listed property group which invests in the Japan real estate market. It currently holds interests in a portfolio comprising 43 retail, office and residential properties. Asset management services in Japan are generally undertaken by Spring Investment Co., Ltd. AJA is a stapled entity comprising Astro Japan Property Trust (ARSN 112 799 854) and Astro Japan Property Group Limited (ABN 25 135 381 663). For further information please visit our website: www.astrojapanproperty.com.

AJA half year results to 31 December 2009

Eric Lucas, Senior Advisor

24 February 2010

DISCLAIMER

2

This publication is issued by the Astro Japan Property Group (“Astro Group”), comprising Babcock & Brown Japan Property Management Limited (ABN 94 111

874 563, AFSL 283142) (“Responsible Entity”) as responsible entity of the Astro Japan Property Trust (ARSN 112 799 854) (“AJT”) and Astro Japan Property

Group Limited (ABN 25 135 381 663) (“AJCo”).

The Astro Group and its directors, officers, employees and contractors do not accept, and expressly disclaim, any liability whatsoever for any loss howsoever

arising from any use of this publication or its contents.

This publication is not intended to constitute legal, tax or accounting advice or opinion. No representation or warranty, express or implied, is made as to the

accuracy, completeness or thoroughness of the content of the information contained in this publication. The recipient should consult with their own investment,

financial, taxation or other professional adviser as to the accuracy and application of the information contained herein and should conduct their own due

diligence and other enquiries in relation to such information.

The information contained in this publication does not constitute an offer of, or invitation to invest in or subscribe for, or a recommendation of, AJA stapled

securities.

The information contained in this publication constitutes general information only. The Responsible Entity is not licensed to provide financial product advice

(including personal financial product advice), and the information contained in this publication does not constitute financial product advice.

In providing this publication, the Astro Group has not considered the investment objectives, financial situation and particular needs of an investor. Before

making any investment decision with respect to AJA stapled securities, an investor should consider its own investment objectives, financial circumstances and

needs, and if necessary consult its investment, financial, taxation or other professional adviser.

This publication may include information forecasting or projecting future outcomes. Such outcomes may be affected by a wide range of influences outside of

the Astro Group‟s control. In respect of such forward-looking information, no representation or warranty is made by or on behalf of the Astro Group that any

projection, forecast, forward-looking statement, assumption or estimate contained in this publication should or will be achieved.

The Astro Group specifically prohibits the redistribution or reproduction of this material in whole or in part without the written permission of the Astro Group and

the Astro Group accepts no liability whatsoever for the actions of third parties in this respect.

Asset management services in Japan are generally undertaken by Spring Investment Co. Limited (“Spring”). Property level information contained in this

publication has been provided by Spring.

AGENDA

• Key points

• Financial results

• Portfolio overview and leasing activity

• Debt and FX hedging

• Events since 31 December 2009

• Outlook

• Appendices

3

Key Points

KEY POINTS

• Net operating profit after tax of A$26.7m, down approximately 17.7% on the prior corresponding period,

mainly due to a decline in net property income

• Net property income declined 15.6% on the prior corresponding period of which approximately 7.2%

represents the impact of the sale of Shinjuku Sanei in May 2009

• Excluding the sale of Shinjuku Sanei, net property income declined by approximately 8.4% on the prior

corresponding period, primarily due to a fall in office occupancy and office rental income

• Funds from operations (FF0)¹ of ¥2.0bn (A$25.1m) down ¥0.6bn (A$7.5m) relative to the prior

corresponding period of which approximately ¥0.3bn (A$3.8m) represents the impact of the sale of

Shinjuku Sanei

• Portfolio occupancy by area remains at 92.7% as at 31 December 2009 versus 94.0% as at 30 June 2009

• Portfolio debt service coverage ratio (DSCR)² remains strong at 3.5x

• Distribution of 3.50 cps for the period after retaining 2.13 cps for capital management purposes

• Full year distribution guidance of 7.00 cps

5

¹ FFO consists of operating cashflow excluding foreign exchange hedge income and Japanese withholding tax

² Portfolio DSCR is FFO divided by debt service costs

ACHIEVEMENTS DURING THE HALF YEAR

Debt

Definitive term sheet signed for a new five year, senior, non-recourse loan of ¥13.4bn (A$160m)

Loan will be used to refinance the five year term loan set to mature in March 2010, representing 16.3% of AJA‟s

total debt balance

Favourable margin payable of 195 bps, all-in margin cost of approximately 237 bps

Formal loan documentation currently being finalised with closing expected to take place in March

Discussions have commenced with current lender and other lender candidates regarding refinancing of loan

maturing in December 2010

Capital and distribution hedging

Successfully renegotiated positive changes to foreign exchange hedging terms including:

Waiver of counterparty‟s August 2009 option to terminate

Removal of the gearing ratio covenant

Amendment of the minimum securityholders‟ equity covenant reducing the threshold to A$250m (previously

A$458m)

As at 24 February 2010, at an FX rate of A$1.00 = ¥78.30, the hedging position is fully cash collateralised on a

mark to market basis. No further collateral can be called on the basis of mark to market movements

Counterparty has retained annual option to terminate in August. AJA is in constructive discussions with the

counterparty to manage the upcoming August 2010 termination option

6

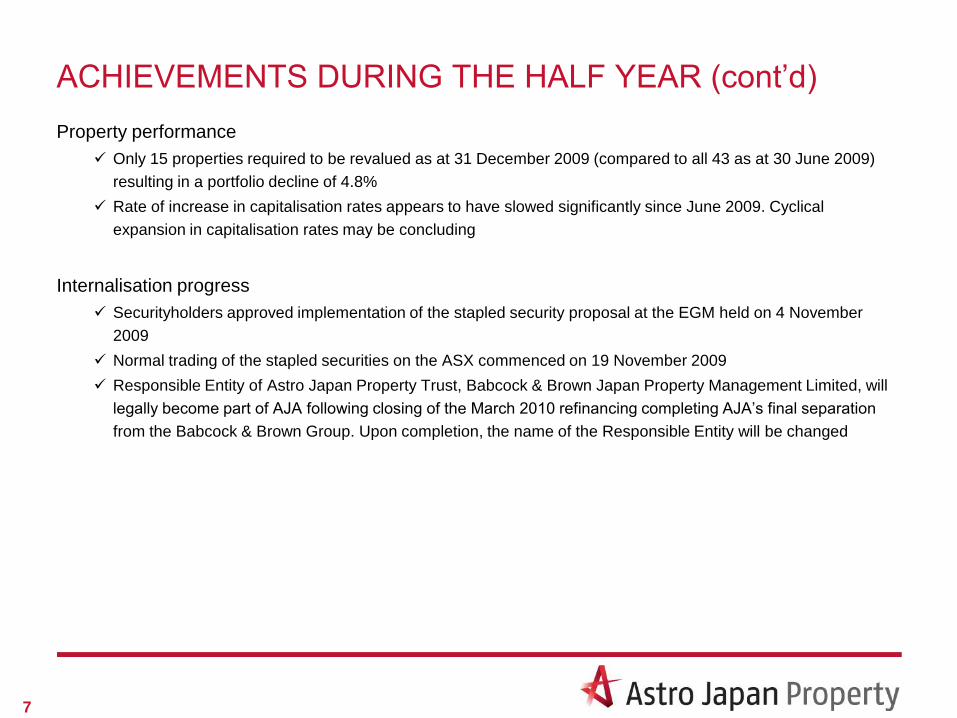

ACHIEVEMENTS DURING THE HALF YEAR (cont‟d)

Property performance

Only 15 properties required to be revalued as at 31 December 2009 (compared to all 43 as at 30 June 2009)

resulting in a portfolio decline of 4.8%

Rate of increase in capitalisation rates appears to have slowed significantly since June 2009. Cyclical

expansion in capitalisation rates may be concluding

Internalisation progress

Securityholders approved implementation of the stapled security proposal at the EGM held on 4 November

2009

Normal trading of the stapled securities on the ASX commenced on 19 November 2009

Responsible Entity of Astro Japan Property Trust, Babcock & Brown Japan Property Management Limited, will

legally become part of AJA following closing of the March 2010 refinancing completing AJA‟s final separation

from the Babcock & Brown Group. Upon completion, the name of the Responsible Entity will be changed

7

Financial Results

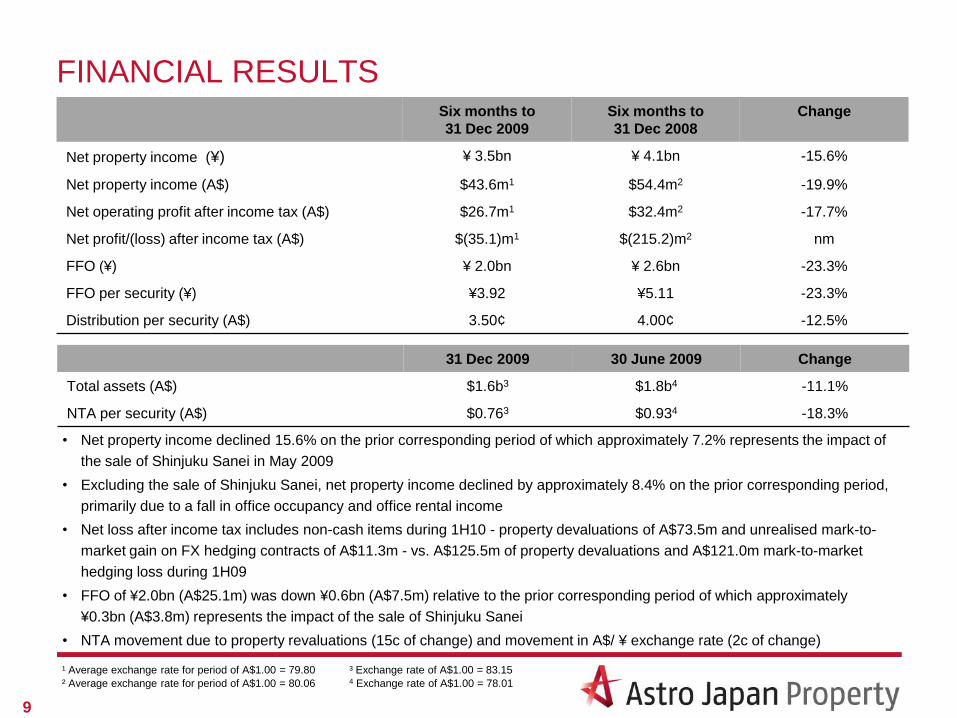

FINANCIAL RESULTSSix months to

31 Dec 2009

Six months to

31 Dec 2008

Change

Net property income (¥) ¥ 3.5bn ¥ 4.1bn -15.6%

Net property income (A$) $43.6m1 $54.4m2 -19.9%

Net operating profit after income tax (A$) $26.7m1 $32.4m2 -17.7%

Net profit/(loss) after income tax (A$) $(35.1)m1 $(215.2)m2 nm

FFO (¥) ¥ 2.0bn ¥ 2.6bn -23.3%

FFO per security (¥) ¥3.92 ¥5.11 -23.3%

Distribution per security (A$) 3.50¢ 4.00¢ -12.5%

9

¹ Average exchange rate for period of A$1.00 = 79.80 ³ Exchange rate of A$1.00 = 83.15

² Average exchange rate for period of A$1.00 = 80.06 4 Exchange rate of A$1.00 = 78.01

• Net property income declined 15.6% on the prior corresponding period of which approximately 7.2% represents the impact of

the sale of Shinjuku Sanei in May 2009

• Excluding the sale of Shinjuku Sanei, net property income declined by approximately 8.4% on the prior corresponding period,

primarily due to a fall in office occupancy and office rental income

• Net loss after income tax includes non-cash items during 1H10 - property devaluations of A$73.5m and unrealised mark-to-

market gain on FX hedging contracts of A$11.3m - vs. A$125.5m of property devaluations and A$121.0m mark-to-market

hedging loss during 1H09

• FFO of ¥2.0bn (A$25.1m) was down ¥0.6bn (A$7.5m) relative to the prior corresponding period of which approximately

¥0.3bn (A$3.8m) represents the impact of the sale of Shinjuku Sanei

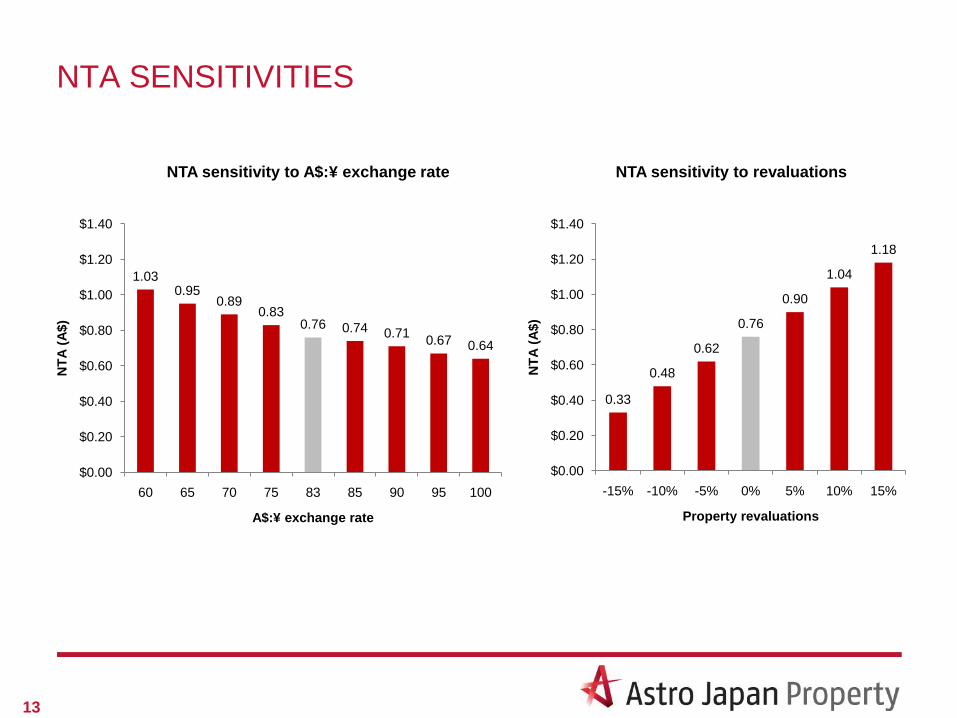

• NTA movement due to property revaluations (15c of change) and movement in A$/ ¥ exchange rate (2c of change)

31 Dec 2009 30 June 2009 Change

Total assets (A$) $1.6b3 $1.8b4 -11.1%

NTA per security (A$) $0.763 $0.934 -18.3%

MAIN COMPONENTS OF NET PROPERTY INCOME

DECLINE

10

• Rental income declined relative to the prior corresponding period reflecting the rise in office vacancies and a general

softening in market rents. Of the 8.9% decline in office rental income, Kokusai Nihombashi contributed 2.7%

• Occupancy levels declined relative to the prior corresponding period mainly due to a rise in office vacancies. Of the

14% decline in office occupancy levels, the vacancy of a sole tenanted office asset, Kokusai Nihombashi,

represented approximately 6% of the decline

• Occupancy in the retail segment has increased

Property revenue (¥ million)Six months to

31 Dec 2009

Six months to

31 Dec 2008

(ex. Shinjuku Sanei)

Change

Retail 2,300 2,542 -9.5%

Office 2,191 2,405 -8.9%

Residential 429 430 -0.2%

Total portfolio 4,920 5,377 -8.5%

Occupancy by area 31 Dec 200931 Dec 2008

(ex. Shinjuku Sanei)Change

Retail 97.6% 96.0% 1.7%

Office 79.1% 92.0% -14.0%

Residential 99.6% 99.8% -0.2%

Total portfolio 92.7% 95.3% -2.7%

OPERATING PERFORMANCE

11

36.0

46.3

54.4

43.6

0

10

20

30

40

50

60

Dec-06 Dec-07 Dec-08 Dec-09

A$

mil

lio

ns

Net Property Income

4.17

4.51

5.11

3.92

0.00

1.00

2.00

3.00

4.00

5.00

6.00

Dec-06 Dec-07 Dec-08 Dec-09

¥ p

er

secu

rity

FFO

NTA PER UNIT

Movement for half year ended 31 December 2009

12

*

0.02

0.76 0.05

0.14

0.93

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

NTA at 30/6/09 Impacts of FX FV of cap & dist hedges Revaluation of properties Closing NTA at 31/12/09

NT

A p

er secu

rity

NTA movement - A$ per security

FX 78.10

FX83.15

NTA SENSITIVITIES

13

0.33

0.48

0.62

0.76

0.90

1.04

1.18

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

-15% -10% -5% 0% 5% 10% 15%

NT

A (

A$)

Property revaluations

NTA sensitivity to revaluations

1.030.95

0.890.83

0.76 0.74 0.710.67 0.64

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

60 65 70 75 83 85 90 95 100

NT

A (

A$)

A$:¥ exchange rate

NTA sensitivity to A$:¥ exchange rate

Portfolio Overview and Leasing Activity

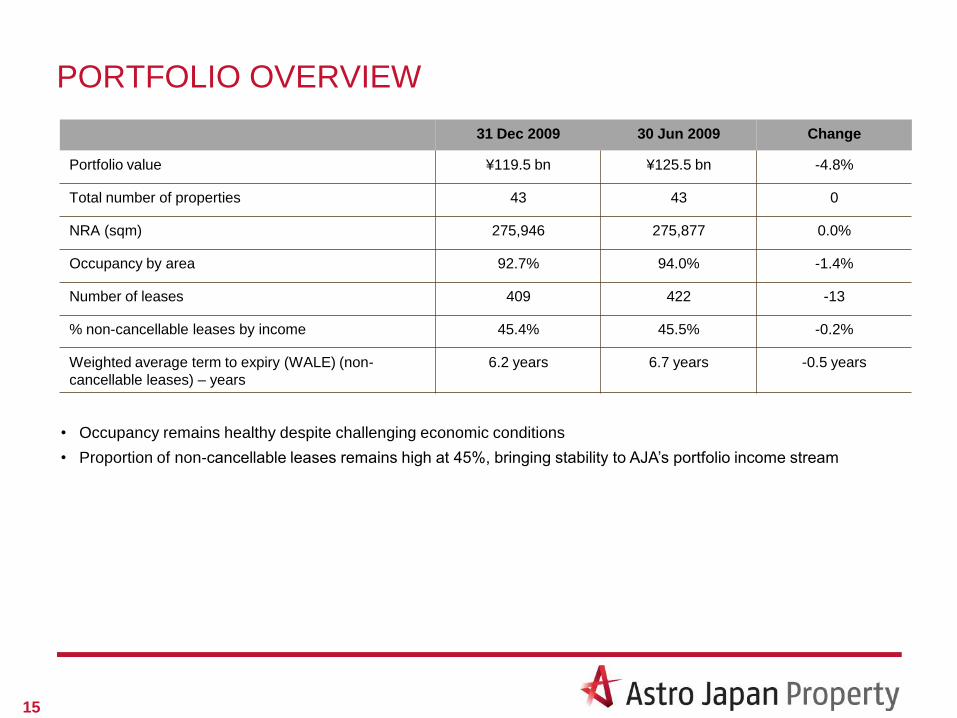

PORTFOLIO OVERVIEW

31 Dec 2009 30 Jun 2009 Change

Portfolio value ¥119.5 bn ¥125.5 bn -4.8%

Total number of properties 43 43 0

NRA (sqm) 275,946 275,877 0.0%

Occupancy by area 92.7% 94.0% -1.4%

Number of leases 409 422 -13

% non-cancellable leases by income 45.4% 45.5% -0.2%

Weighted average term to expiry (WALE) (non-

cancellable leases) – years

6.2 years 6.7 years -0.5 years

15

• Occupancy remains healthy despite challenging economic conditions

• Proportion of non-cancellable leases remains high at 45%, bringing stability to AJA‟s portfolio income stream

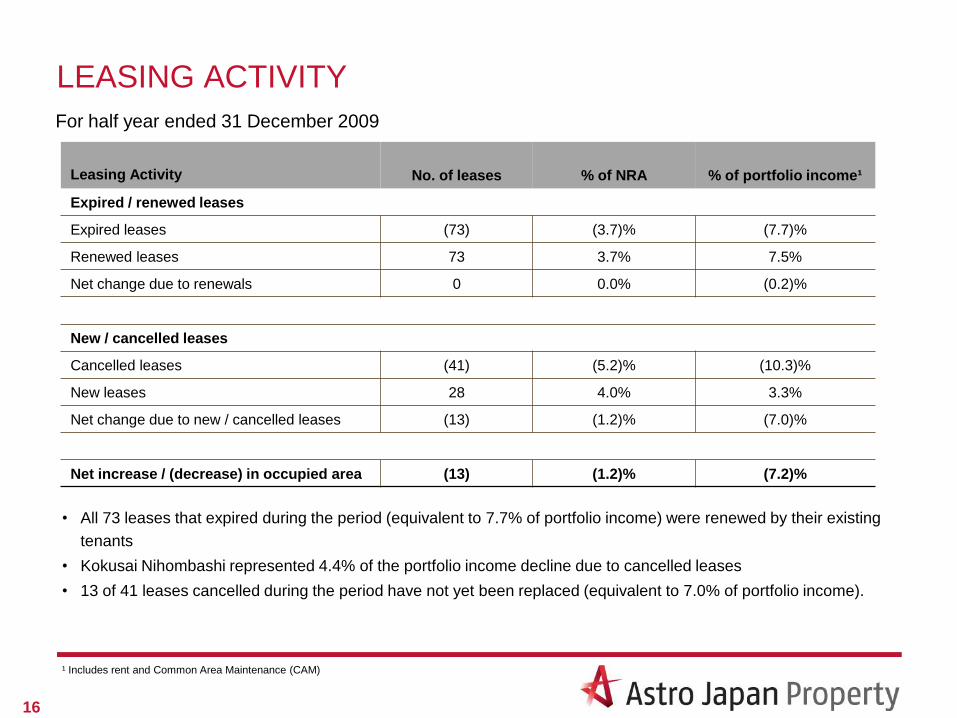

LEASING ACTIVITY

16

Leasing Activity No. of leases % of NRA % of portfolio income¹

Expired / renewed leases

Expired leases (73) (3.7)% (7.7)%

Renewed leases 73 3.7% 7.5%

Net change due to renewals 0 0.0% (0.2)%

New / cancelled leases

Cancelled leases (41) (5.2)% (10.3)%

New leases 28 4.0% 3.3%

Net change due to new / cancelled leases (13) (1.2)% (7.0)%

Net increase / (decrease) in occupied area (13) (1.2)% (7.2)%

For half year ended 31 December 2009

• All 73 leases that expired during the period (equivalent to 7.7% of portfolio income) were renewed by their existing

tenants

• Kokusai Nihombashi represented 4.4% of the portfolio income decline due to cancelled leases

• 13 of 41 leases cancelled during the period have not yet been replaced (equivalent to 7.0% of portfolio income).

¹ Includes rent and Common Area Maintenance (CAM)

PORTFOLIO DIVERSIFICATION

17

Asset class diversification (by value) Geographic diversification (by value)

• Post property revaluations in December 2009:

- Retail increased to 47% from 46% at June 2009

- Office decreased to 44% from 46% at June 2009

- Residential increased marginally to 9% from 8% at June 2009

• Approximately 67% concentration of properties in Central and Greater Tokyo with asset and lease diversification

supporting stability of portfolio cashflows

Retail - 47% Office - 44% Residential - 9% Greater Tokyo - 41% Central Tokyo - 26% Greater Osaka - 22% Hokkaido - 4%

Okinawa - 2% Shizuoka - 2% Fukuoka - 2% Aichi - 1%

PROPERTY REVALUATIONS

• Fair value of all portfolio properties was independently reviewed at 31 December 2009

• All valuers used are also used by J-REITs

• Only 15 properties were required to be revalued as at 31 December 2009 (compared to all 43 as at 30

June 2009)

• Over the half year period, AJA‟s portfolio was devalued by 4.8% to ¥119.5bn (A$1.4bn)

• Devaluation for the period ended 31 December 2009 was ¥6.1 billion compared to 30 June 2009

devaluation of ¥19.2 billion, the latter reflecting full impact of „Lehman shock‟

• Weighted average capitalisation rate used by valuers for the portfolio moved from 5.5% (30 June 2009) to

5.6% (31 December 2009)

• Rate of increase in capitalisation rates appears to have slowed significantly since June 2009. Cyclical

expansion in capitalisation rates may be concluding

18

PORTFOLIO YIELD DATA AS AT 31 DECEMBER 2009

Asset class

Original NOI yield /

purchase price

Current NOI yield /

current book value

December 2009

Valuation cap rates¹

December 2009

Retail 5.3% 5.9% 5.8%

Office 5.0% 5.5% 5.2%

Residential 5.5% 7.2% 6.3%

Total 5.2% 5.8% 5.6%

19

¹ Cap rate used by valuers for NCF (Net operating income less leasing fees less capex)

Debt and FX Hedging

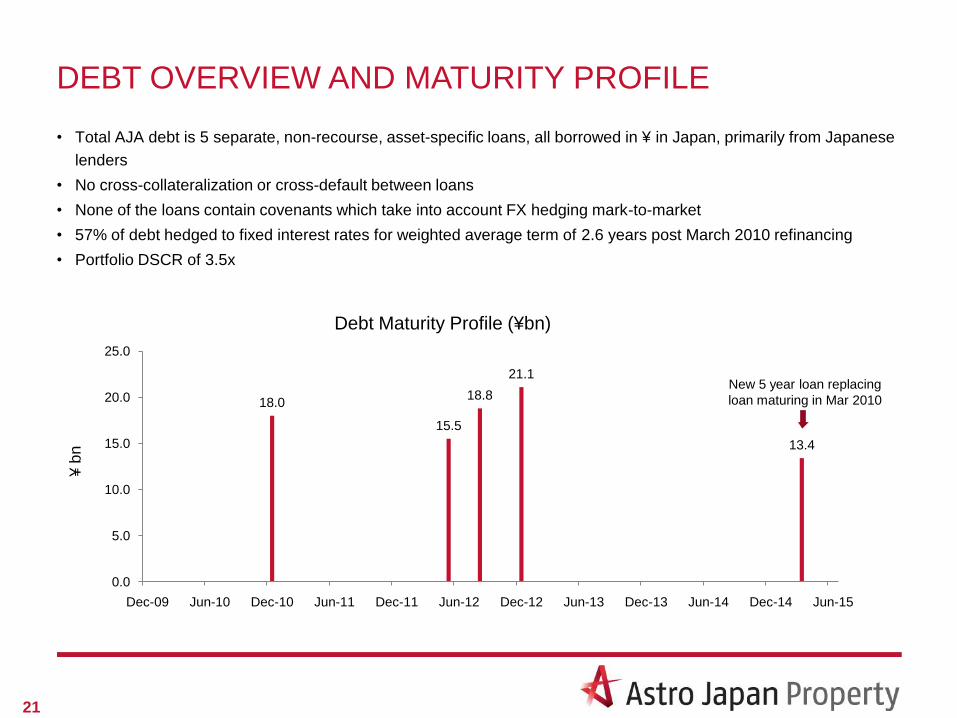

• Total AJA debt is 5 separate, non-recourse, asset-specific loans, all borrowed in ¥ in Japan, primarily from Japanese

lenders

• No cross-collateralization or cross-default between loans

• None of the loans contain covenants which take into account FX hedging mark-to-market

• 57% of debt hedged to fixed interest rates for weighted average term of 2.6 years post March 2010 refinancing

• Portfolio DSCR of 3.5x

21

Debt Maturity Profile (¥bn)

DEBT OVERVIEW AND MATURITY PROFILE

18.0

15.5

18.8

21.1

13.4

0.0

5.0

10.0

15.0

20.0

25.0

Dec-09 Jun-10 Dec-10 Jun-11 Dec-11 Jun-12 Dec-12 Jun-13 Dec-13 Jun-14 Dec-14 Jun-15

¥ b

n

New 5 year loan replacing

loan maturing in Mar 2010

• Definitive term sheet signed for a new, 5-year senior, non-recourse loan of ¥13.4bn (c. A$160m)

• Loan will be used to refinance the five year term loan set to mature in March 2010, representing 16.3% of AJA‟s total

debt balance

• Favourable margin payable of 195 bps, all-in margin cost of approximately 237 bps

• Formal loan documentation currently being finalised with closing expected to take place in March 2010

• AJA intends to contribute additional equity of ¥900m (c. A$11m) from existing cash resources to reduce leverage

• Equity will be injected into JPT Co., Ltd., the Japanese special purpose company borrowing the new loan, and

represents the difference between the amount being debt financed and the loan maturing

• Equity to pay loan costs and expenses will also be paid from existing cash resources

• Gearing across AJA‟s entire portfolio will be 72.6% post refinancing and equity injection

22

MARCH 2010 REFINANCING

Key terms of new loan

Lender: A Japanese commercial bank

Term: 5 years

Amount: ¥13.4 bn

Interest Margin: 195 bps

LTV Covenant: None

DSCR Covenant: Cashflow not to fall below 1.28 times a theoretical loan payment constant of 6.5% p.a .

applied to the outstanding loan balance

Amortization: ¥11.8m per quarter until October 2011 and then ¥148.4m per quarter until loan maturity

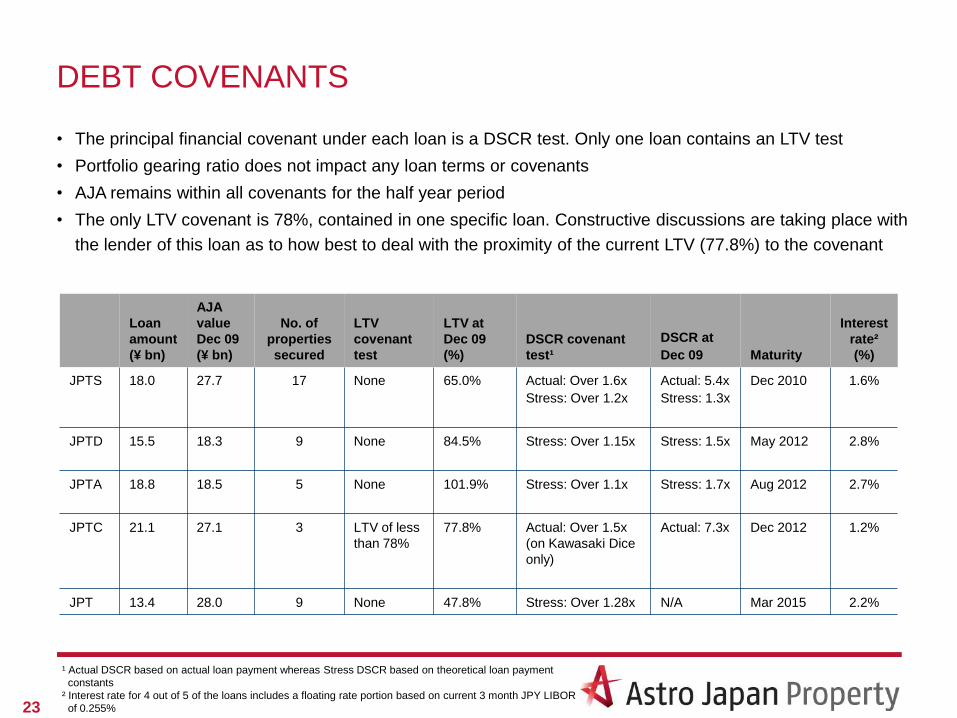

DEBT COVENANTS

23

• The principal financial covenant under each loan is a DSCR test. Only one loan contains an LTV test

• Portfolio gearing ratio does not impact any loan terms or covenants

• AJA remains within all covenants for the half year period

• The only LTV covenant is 78%, contained in one specific loan. Constructive discussions are taking place with

the lender of this loan as to how best to deal with the proximity of the current LTV (77.8%) to the covenant

Loan

amount

(¥ bn)

AJA

value

Dec 09

(¥ bn)

No. of

properties

secured

LTV

covenant

test

LTV at

Dec 09

(%)

DSCR covenant

test¹

DSCR at

Dec 09 Maturity

Interest

rate²

(%)

JPTS 18.0 27.7 17 None 65.0% Actual: Over 1.6x

Stress: Over 1.2x

Actual: 5.4x

Stress: 1.3x

Dec 2010 1.6%

JPTD 15.5 18.3 9 None 84.5% Stress: Over 1.15x Stress: 1.5x May 2012 2.8%

JPTA 18.8 18.5 5 None 101.9% Stress: Over 1.1x Stress: 1.7x Aug 2012 2.7%

JPTC 21.1 27.1 3 LTV of less

than 78%

77.8% Actual: Over 1.5x

(on Kawasaki Dice

only)

Actual: 7.3x Dec 2012 1.2%

JPT 13.4 28.0 9 None 47.8% Stress: Over 1.28x N/A Mar 2015 2.2%

¹ Actual DSCR based on actual loan payment whereas Stress DSCR based on theoretical loan payment

constants

² Interest rate for 4 out of 5 of the loans includes a floating rate portion based on current 3 month JPY LIBOR

of 0.255%

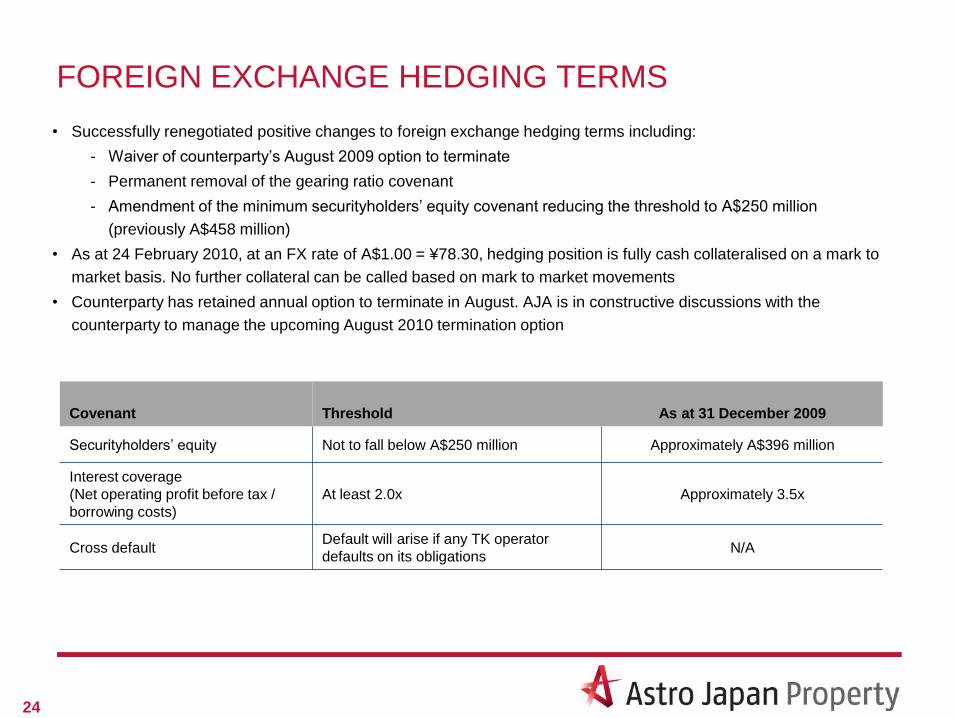

FOREIGN EXCHANGE HEDGING TERMS

• Successfully renegotiated positive changes to foreign exchange hedging terms including:

- Waiver of counterparty‟s August 2009 option to terminate

- Permanent removal of the gearing ratio covenant

- Amendment of the minimum securityholders‟ equity covenant reducing the threshold to A$250 million

(previously A$458 million)

• As at 24 February 2010, at an FX rate of A$1.00 = ¥78.30, hedging position is fully cash collateralised on a mark to

market basis. No further collateral can be called based on mark to market movements

• Counterparty has retained annual option to terminate in August. AJA is in constructive discussions with the

counterparty to manage the upcoming August 2010 termination option

24

Covenant Threshold As at 31 December 2009

Securityholders‟ equity Not to fall below A$250 million Approximately A$396 million

Interest coverage

(Net operating profit before tax /

borrowing costs)

At least 2.0x Approximately 3.5x

Cross defaultDefault will arise if any TK operator

defaults on its obligationsN/A

FOREIGN EXCHANGE HEDGING PROFILE

Capital Hedging

Settlement date

AJA receives

AUD

AJA pays

JPYExchange

rateInterest rate

spread

Aug 2011 14,724,649 1,500,000,000 101.9 6.19%

Aug 2012 20,614,509 2,100,000,000 101.9 6.01%

Aug 2013 16,687,936 1,700,000,000 101.9 5.86%

Aug 2014 22,577,795 2,300,000,000 101.9 5.69%

Aug 2015 24,541,082 2,500,000,000 101.9 5.52%

Aug 2016 14,724,649 1,500,000,000 101.9 5.39%

Distribution Hedging

Settlement dateExchange

rateJPY

Feb 2010 66.9 1,335,704,000

Aug 2010 68.8 1,339,291,000

Feb 2011 68.0 1,339,291,000

25

• Approximately 23.5% of net investment in Japanese properties

is hedged

• As at 31 December 2009, capital hedges were A$34.9m out-

of-the money (excluding collateral of ¥2.4bn) and distribution

hedges were A$6m in-the-money based on A$1.00 = ¥83.15

Events since 31 December 2009

PARTICIPATION IN ACQUISITION OF JOINT CAPITAL

PARTNERS

• AJA, through its 30% economic interest in its Japan asset manager, Spring Investment Co (Spring), will

participate in the acquisition of J-REIT management company, Joint Capital Partners (JCP)

• Spring is acquiring JCP in joint venture with Sekisui House Ltd, one of Japan‟s largest home builders

- Spring will take a 25% interest in the JV and Sekisui House will take a 75% interest

• JCP is the manager of Joint REIT, a Tokyo Stock Exchange listed J-REIT

• Joint REIT owns 53, mainly residential, assets with a book value of approximately ¥100 bn (A$1.25 bn)

• Details, including acquisition price, will remain confidential until the court administration of JCP‟s parent

company, Joint Corporation, is completed. The acquisition is expected to close in the first week of March

• AJA will contribute 30% of the capital to Spring‟s investment in JCP. The investment will have a minimal

impact on AJA‟s existing cash resources

• AJA‟s involvement marks the first time an Australian real estate company has held an interest in J-REIT

management

• AJA‟s participation is reflective of the opportunities now provided by AJA‟s economic interest in Spring.

These opportunities are expected to provide long term benefits to securityholders

27

OVERVIEW OF SEKISUI HOUSE

• Established on 1 August 1960, Sekisui House is one of Japan‟s leading homebuilders

• Sekisui House designs, prefabricates and builds steel, wooden and concrete houses and condominiums. It

is also involved in selling land, detached houses and condominiums. Its real estate operations include

leasing and managing houses, low-rise apartments and commercial and retail buildings

• Sekisui House has a market capitalisation of more than ¥500 billion (approximately A$6.2 billion) and a

credit rating of AA- (R&I)

• Sekisui House entered the Australian residential market in 2009 and has announced plans for a significant

expansion of its Australian presence over time. Sales of dwellings owned by Sekisui House in Australia

have already commenced

28

Sekisui House Recent Financial Results

¥ billion 2007/1 2008/1 2009/1

Net sales 1,596.2 1,597.8 1,514.2

Operating income 111.6 109.7 74.0

Net income 62.7 60.4 11.5

Total assets 1,278.8 1,349.4 1,387.2

Net assets 798.3 771.0 754.1

Outlook

30

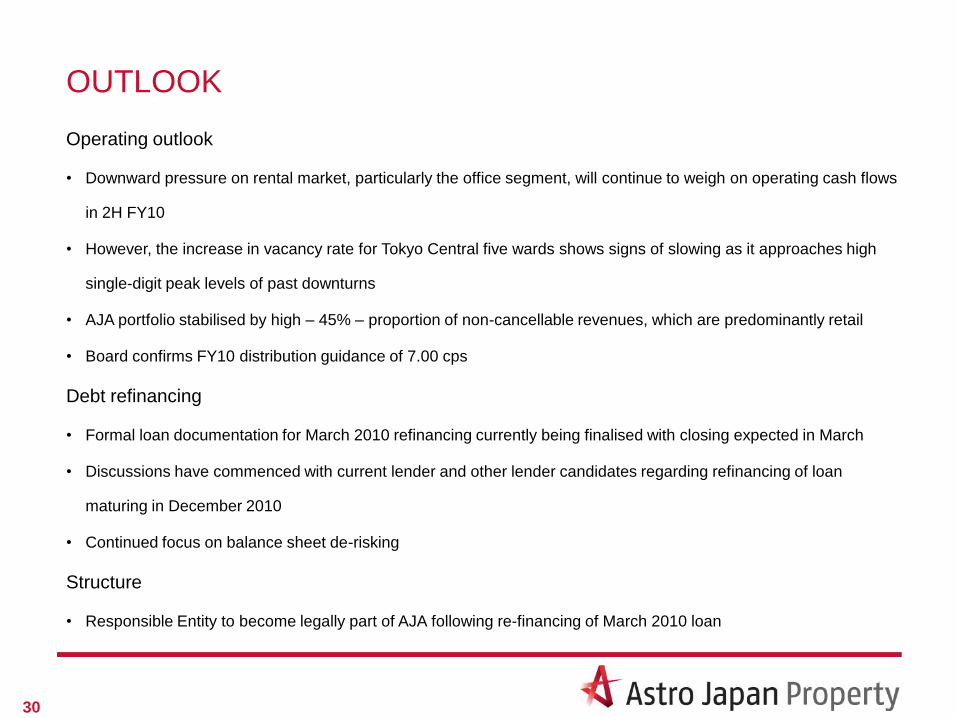

OUTLOOK

Operating outlook

• Downward pressure on rental market, particularly the office segment, will continue to weigh on operating cash flows

in 2H FY10

• However, the increase in vacancy rate for Tokyo Central five wards shows signs of slowing as it approaches high

single-digit peak levels of past downturns

• AJA portfolio stabilised by high – 45% – proportion of non-cancellable revenues, which are predominantly retail

• Board confirms FY10 distribution guidance of 7.00 cps

Debt refinancing

• Formal loan documentation for March 2010 refinancing currently being finalised with closing expected in March

• Discussions have commenced with current lender and other lender candidates regarding refinancing of loan

maturing in December 2010

• Continued focus on balance sheet de-risking

Structure

• Responsible Entity to become legally part of AJA following re-financing of March 2010 loan

Appendices

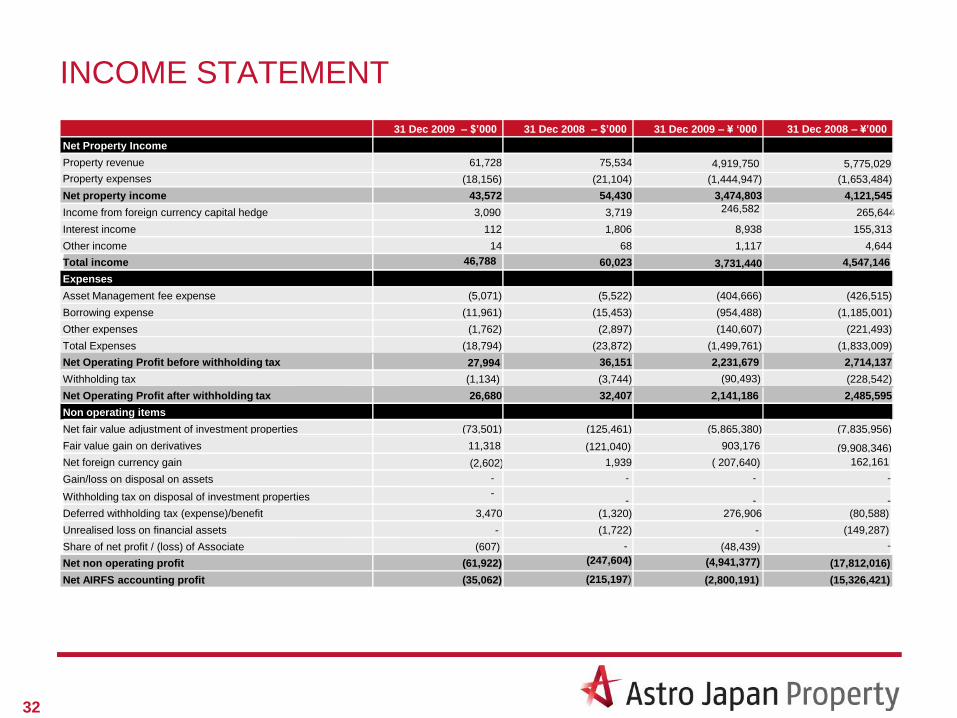

INCOME STATEMENT

32

31 Dec 2009 – $’000 31 Dec 2008 – $’000 31 Dec 2009 – ¥ ‘000 31 Dec 2008 – ¥’000

Net Property Income

Property revenue 61,728 75,534

(18,156) (21,104) (1,444,947) (1,653,484)

Net property income 43,572 54,430 3,474,803 4,121,545

Income from foreign currency capital hedge 3,090 3,719 265,644

Interest income 112 1,806 8,938 155,313

Other income 14 68 1,117 4,644

Total income 60,023 3,731,440 4,547,146

Expenses

Asset Management fee expense (5,071) (5,522) (404,666) (426,515)

Borrowing expense (11,961) (15,453) (954,488) (1,185,001)

Other expenses (1,762) (2,897) (140,607) (221,493)

Total Expenses (18,794) (23,872) (1,499,761) (1,833,009)

Net Operating Profit before withholding tax 36,151 2,231,679 2,714,137

Withholding tax (1,134) (3,744) (228,542)

Net Operating Profit after withholding tax 26,680 32,407 2,141,186 2,485,595

Non operating items

Net fair value adjustment of investment properties (73,501) (125,461) (5,865,380) (7,835,956)

Fair value gain on derivatives 11,318 (121,040) 903,176 (9,908,346)

Net foreign currency gain (2,602) 1,939 ( 207,640) 162,161

Gain/loss on disposal on assets

Withholding tax on disposal of investment properties

Deferred withholding tax (expense)/benefit 3,470 (1,320) 276,906 (80,588)

Unrealised loss on financial assets - (1,722) - (149,287)

Share of net profit / (loss) of Associate (607) (48,439)

Net non operating profit (61,922) (247,604) (4,941,377) (17,812,016)

Net AIRFS accounting profit (35,062) (2,800,191) (15,326,421)

5,775,029

-

4,919,750

246,582

Property expenses

(90,493)

- - -

-- -

-

-

-

46,788

27,994

(215,197)

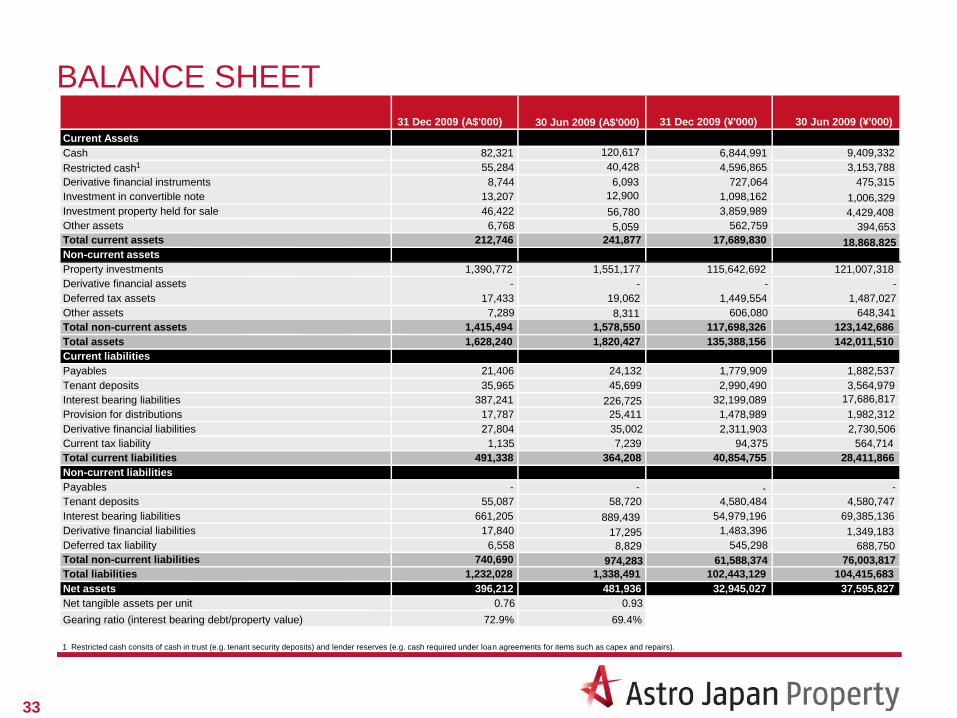

BALANCE SHEET

33

31 Dec 2009 (A$'000) 30 Jun 2009 (A$'000) 31 Dec 2009 (¥'000) 30 Jun 2009 (¥'000)

Current Assets

Cash 82,321 120,617 6,844,991 9,409,332

Restricted cash1 55,284 40,428 4,596,865 3,153,788

Derivative financial instruments 8,744 6,093 727,064 475,315

Investment in convertible note 13,207 12,900 1,098,162 1,006,329

Investment property held for sale 46,422 3,859,989 4,429,408

Other assets 6,768 5,059 562,759 394,653

Total current assets 212,746 241,877 17,689,830 18,868,825Non-current assets

Property investments 1,390,772 1,551,177 115,642,692 121,007,318

Derivative financial assets - - - -

Deferred tax assets 17,433 19,062 1,449,554 1,487,027

Other assets 7,289 8,311 606,080 648,341

Total non-current assets 1,415,494 1,578,550 117,698,326 123,142,686

Total assets 1,628,240 1,820,427 135,388,156 142,011,510

Current liabilities

Payables 21,406 24,132 1,779,909 1,882,537

Tenant deposits 35,965 45,699 2,990,490 3,564,979

Interest bearing liabilities 387,241 226,725 32,199,089 17,686,817

Provision for distributions 17,787 25,411 1,478,989 1,982,312

Derivative financial liabilities 27,804 35,002 2,311,903 2,730,506

Current tax liability 1,135 7,239 94,375 564,714

Total current liabilities 491,338 364,208 40,854,755 28,411,866

Non-current liabilities

Payables - - - -

Tenant deposits 55,087 58,720 4,580,484 4,580,747

Interest bearing liabilities 661,205 889,439 54,979,196 69,385,136

Derivative financial liabilities 17,840 17,295 1,483,396 1,349,183

Deferred tax liability 6,558 8,829 545,298 688,750

Total non-current liabilities 740,690 974,283 76,003,817

Total liabilities 1,232,028 1,338,491 102,443,129 104,415,683

Net assets 396,212 481,936 32,945,027 37,595,827

Net tangible assets per unit 0.76 0.93

Gearing ratio (interest bearing debt/property value) 72.9% 69.4%

1 Restricted cash consits of cash in trust (e.g. tenant security deposits) and lender reserves (e.g. cash required under loan agreements for items such as capex and repairs).

61,588,374

56,780

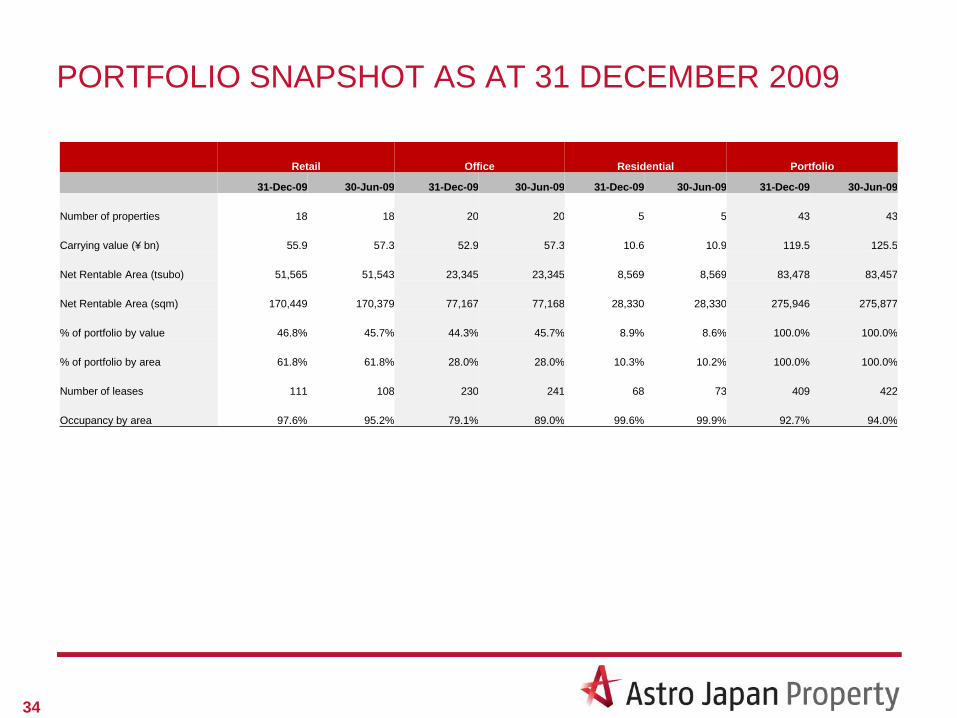

PORTFOLIO SNAPSHOT AS AT 31 DECEMBER 2009

34

Retail Office Residential Portfolio

31-Dec-09 30-Jun-09 31-Dec-09 30-Jun-09 31-Dec-09 30-Jun-09 31-Dec-09 30-Jun-09

Number of properties 18 18 20 20 5 5 43 43

Carrying value (¥ bn) 55.9 57.3 52.9 57.3 10.6 10.9 119.5 125.5

Net Rentable Area (tsubo) 51,565 51,543 23,345 23,345 8,569 8,569 83,478 83,457

Net Rentable Area (sqm) 170,449 170,379 77,167 77,168 28,330 28,330 275,946 275,877

% of portfolio by value 46.8% 45.7% 44.3% 45.7% 8.9% 8.6% 100.0% 100.0%

% of portfolio by area 61.8% 61.8% 28.0% 28.0% 10.3% 10.2% 100.0% 100.0%

Number of leases 111 108 230 241 68 73 409 422

Occupancy by area 97.6% 95.2% 79.1% 89.0% 99.6% 99.9% 92.7% 94.0%

PORTFOLIO SNAPSHOT AS AT 31 DECEMBER 2009

35

Carrying value Occupancy by area

31/12/2009

¥ billions % of portfolio Dec-09 Jun-09

Retail 55.9 46.8% 97.6% 95.2%

Office 52.9 44.3% 79.1% 89.0%

Residential 10.6 8.9% 99.6% 99.9%

Portfolio 119.5 100.0% 92.7% 94.0%

RETAIL

Kawasaki Dice 12.3 10.3% 99.3% 98.2%

Konan Home Centre 10.5 8.8% 100.0% 100.0%

Shinjuku Fuji 4.5 3.8% 100.0% 100.0%

Mukomachi Saty 4.2 3.5% 100.0% 100.0%

Shibuya Konami 2.4 2.0% 100.0% 100.0%

Ginowan 2.3 1.9% 67.4% 45.1%

Motomachi 2.3 1.9% 100.0% 100.0%

Susono 2.3 1.9% 100.0% 100.0%

Matsudo Nitori 2.2 1.8% 100.0% 100.0%

Tsudanuma 2.0 1.6% 100.0% 100.0%

Sapporo Co-op 1.9 1.6% 100.0% 100.0%

Sapporo Ai 1.7 1.4% 100.0% 100.0%

Harajuku Bell Pier 1.6 1.3% 85.5% 79.3%

Sapporo Toys R Us 1.6 1.3% 100.0% 100.0%

Round One Amagasaki 1.3 1.1% 100.0% 100.0%

Round One Nara 1.0 0.9% 100.0% 100.0%

Yoshikawa 1.0 0.8% 98.9% 86.0%

Kajicho Ekimae 0.9 0.8% 79.2% 79.2%

Retail sub total / average 55.9 46.8% 97.6% 95.2%

PORTFOLIO SNAPSHOT AS AT 31 DECEMBER 2009

(cont‟d)

36

Carrying value Occupancy by area

31/12/2009

¥ billions % of portfolio Dec-09 Jun-09

OFFICE

JN 9.6 8.0% 81.9% 100.0%

Osaka No. 4 9.4 7.9% 94.9% 97.0%

Ginza Dowa 8.0 6.7% 83.6% 84.9%

Osaka No. 3 4.0 3.4% 83.0% 86.0%

Kokusai Nihombashi 3.9 3.2% 0.0% 100.0%

Yamashitachio 2.7 2.2% 100.0% 87.9%

Higashi Totsuka 2.0 1.6% 87.3% 87.3%

Takadanobaba 1.7 1.4% 79.4% 79.4%

Forest Kita Aoyama 1.6 1.4% 100.0% 100.0%

Sun Ace Tokugawa 1.4 1.2% 49.6% 58.5%

OS Tsukiji 1.4 1.2% 86.5% 100.0%

Prime Kanda 1.2 1.0% 71.4% 85.7%

Asakusa 1.2 1.0% 100.0% 100.0%

Prime Tsukiji 0.9 0.8% 71.4% 71.4%

Shiba Daimon 0.9 0.7% 28.7% 62.9%

Daikanyama Takara 0.7 0.6% 75.8% 100.0%

Yotsuya KD 0.7 0.6% 92.6% 79.1%

Akabane 0.7 0.6% 100.0% 100.0%

FT Nihombashi 0.6 0.5% 83.3% 83.3%

Sun No. 5 0.4 0.4% 100.0% 100.0%

Office sub total / average 52.9 44.3% 79.1% 89.0%

RESIDENTIAL

Tosabori 5.2 4.3% 100.0% 100.0%

Sekijomachi 2.7 2.2% 100.0% 100.0%

G-Clef Kamata 1.6 1.4% 100.0% 100.0%

Prime Stay Tsukiji 0.7 0.6% 90.1% 97.2%

Nishi-Kasai 0.5 0.4% 100.0% 100.0%

Residential sub total / average 10.6 8.9% 99.6% 99.9%

Total / average 119.5 100.0% 92.7% 94.0%

PORTFOLIO VALUATION SUMMARY

37

Carrying value Date Type of report

Direct Cap

Overall Cap

Rate

DCF

Discount

Rate

DCF Terminal

Cap Rate Method

31/12/2009

¥ billions % of portfolio % % %

Retail 55.9 46.8% 5.8% 5.6% 6.1%

Office 52.9 44.3% 5.2% 5.1% 5.5%

Residential 10.6 8.9% 6.3% 6.1% 6.5%

Portfolio 119.5 100.0% 5.6% 5.4% 5.9%

RETAIL

Kawasaki Dice 12.3 10.3% 30/11/2009 Full report 5.0% 4.7% 5.2% DCF

Konan Home Centre 10.5 8.8% 30/11/2009 Update report 6.1% 6.0% 6.3% DCF

Shinjuku Fuji 4.5 3.8% 30/11/2009 Update report 6.0% 5.2% 6.4% DCF

Mukomachi Saty 4.2 3.5% 30/11/2009 Update report 6.1% 5.9% 6.6% DCF

Shibuya Konami 2.4 2.0% 30/11/2009 Full report 4.9% 4.9% 5.4% DCF

Ginowan 2.3 1.9% 30/11/2009 Full report 6.6% 6.6% 7.1% DCF

Motomachi 2.3 1.9% 30/11/2009 Update report 5.5% 5.2% 5.6% DCF

Susono 2.3 1.9% 30/11/2009 Full report 6.3% 6.3% 6.8% DCF

Matsudo Nitori 2.2 1.8% 30/11/2009 Full report 5.5% 5.5% 5.8% DCF

Tsudanuma 2.0 1.6% 30/11/2009 Update report 6.2% 5.9% 6.4% DCF

Sapporo Co-op 1.9 1.6% 30/11/2009 Full report 6.6% 6.6% 7.1% DCF

Sapporo Ai 1.7 1.4% 30/11/2009 Update report 5.6% 5.6% 5.9% DCF

Harajuku Bell Pier 1.6 1.3% 30/11/2009 Update report 4.9% 4.7% 5.0% DCF

Sapporo Toys R Us 1.6 1.3% 30/11/2009 Update report 7.2% 6.7% 7.5% DCF

Round One Amagasaki 1.3 1.1% 30/11/2009 Update report 6.5% 6.2% 6.7% DCF

Round One Nara 1.0 0.9% 30/11/2009 Update report 6.8% 6.4% 7.0% DCF

Yoshikawa 1.0 0.8% 30/11/2009 Update report 6.7% 6.3% 6.8% 80:20 DCF & DC

Kajicho Ekimae 0.9 0.8% 30/11/2009 Update report 5.8% 5.4% 6.0% DCF

Retail sub total / average 55.9 46.8%

PORTFOLIO VALUATION SUMMARY (cont‟d)

38

Carrying value Date Type of report

Direct Cap

Overall Cap

Rate

DCF

Discount

Rate

DCF Terminal

Cap Rate Method

31/12/2009

¥ billions % of portfolio % % %

OFFICE

JN 9.6 8.0% 30/11/2009 Full report 4.9% 4.9% 5.2% DCF

Osaka No. 4 9.4 7.9% 30/11/2009 Update report 4.9% 4.9% 5.4% DCF

Ginza Dowa 8.0 6.7% 30/11/2009 Update report 4.9% 4.7% 5.1% DCF

Osaka No. 3 4.0 3.4% 30/11/2009 Update report 5.0% 5.0% 5.5% DCF

Kokusai Nihombashi 3.9 3.2% 30/11/2009 Update report 5.2% 4.8% 5.2% DCF

Yamashitachio 2.7 2.2% 30/11/2009 Update report 5.5% 5.5% 5.7% DCF

Higashi Totsuka 2.0 1.6% 30/11/2009 Update report 5.7% 6.2% 6.8% DCF

Takadanobaba 1.7 1.4% 30/11/2009 Update report 5.3% 5.3% 5.8% DCF

Forest Kita Aoyama 1.6 1.4% 30/11/2009 Update report 4.7% 4.7% 4.9% DCF

Sun Ace Tokugawa 1.4 1.2% 30/11/2009 Update report 7.3% 6.7% 7.3% DCF

OS Tsukiji 1.4 1.2% 30/11/2009 Update report 5.6% 5.4% 5.7% DCF

Prime Kanda 1.2 1.0% 30/11/2009 Update report 5.6% 5.5% 5.8% DCF

Asakusa 1.2 1.0% 30/11/2009 Update report 5.9% 5.5% 6.0% DCF

Prime Tsukiji 0.9 0.8% 30/11/2009 Update report 5.7% 5.5% 5.8% DCF

Shiba Daimon 0.9 0.7% 30/11/2009 Update report 5.5% 5.2% 5.6% DCF

Daikanyama Takara 0.7 0.6% 30/11/2009 Update report 5.6% 5.5% 5.8% DCF

Yotsuya KD 0.7 0.6% 30/11/2009 Update report 5.7% 5.4% 5.8% DCF

Akabane 0.7 0.6% 30/11/2009 Update report 5.9% 5.5% 5.9% DCF

FT Nihombashi 0.6 0.5% 30/11/2009 Update report 6.0% 5.6% 6.1% DCF

Sun No. 5 0.4 0.4% 30/11/2009 Update report 6.0% 5.6% 6.1% DCF

Office sub total / average 52.9 44.3%

RESIDENTIAL

Tosabori 5.2 4.3% 30/11/2009 Full report 6.4% 6.3% 6.6% DCF

Sekijomachi 2.7 2.2% 30/11/2009 Update report 6.1% 6.1% 6.5% DCF

G-Clef Kamata 1.6 1.4% 30/11/2009 Update report 6.0% 5.5% 6.3% DCF

Prime Stay Tsukiji 0.7 0.6% 30/11/2009 Update report 6.3% 6.1% 6.5% DCF

Nishi-Kasai 0.5 0.4% 30/11/2009 Update report 6.8% 6.1% 7.1% DCF

Residential sub total /

average 10.6 8.9%

Total / average 119.5 100.0%