aisch02

DESCRIPTION

dfTRANSCRIPT

2 – 1 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Systems TechniquesSystems Techniquesand Documentationand Documentation

Chapter 2Chapter 2

2 – 2 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Learning Objective 1Learning Objective 1

Characterize the use of systemsCharacterize the use of systems

techniques by auditors andtechniques by auditors and

systems development personnel.systems development personnel.

2 – 3 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

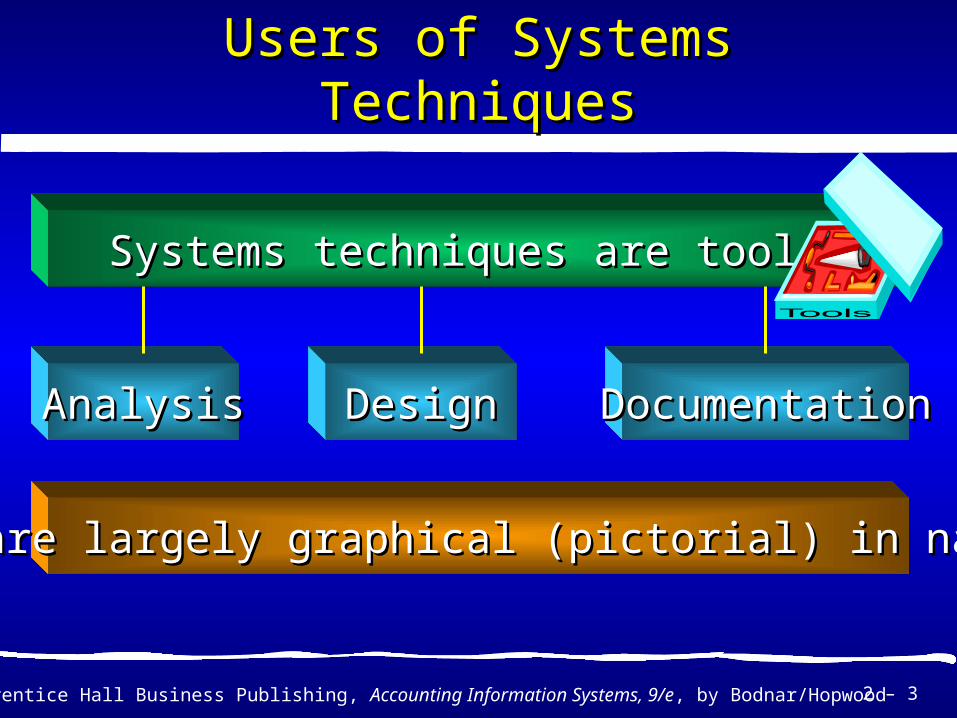

Users of Systems TechniquesUsers of Systems Techniques

Systems techniques are tools.Systems techniques are tools.

They are largely graphical (pictorial) in nature.They are largely graphical (pictorial) in nature.

AnalysisAnalysis DesignDesign DocumentationDocumentation

2 – 4 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Use of SystemsUse of SystemsTechniques in AuditingTechniques in Auditing

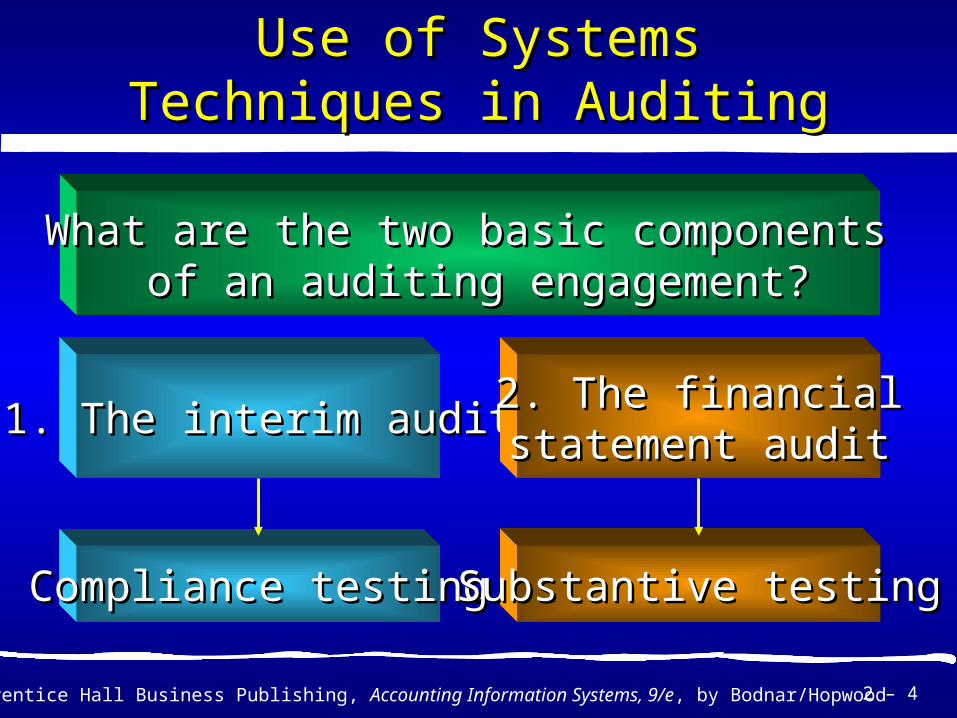

What are the two basic components What are the two basic components of an auditing engagement?of an auditing engagement?

1. The interim audit1. The interim audit

Compliance testingCompliance testing

2. The financial2. The financialstatement auditstatement audit

Substantive testingSubstantive testing

2 – 5 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Internal Control EvaluationInternal Control Evaluation

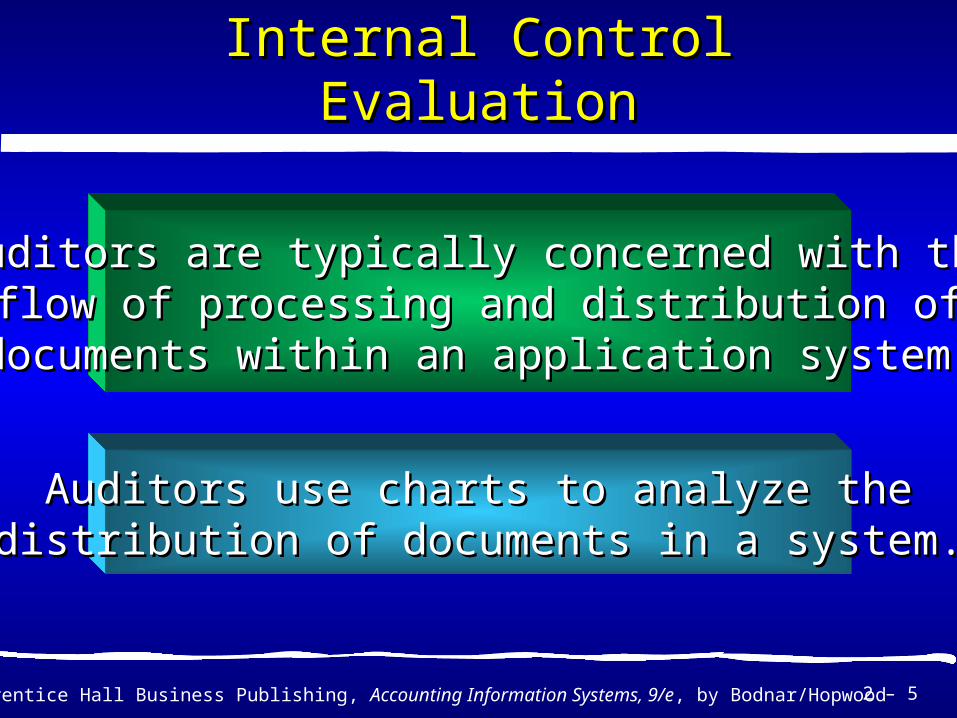

Auditors are typically concerned with theAuditors are typically concerned with theflow of processing and distribution offlow of processing and distribution of

documents within an application system.documents within an application system.

Auditors use charts to analyze theAuditors use charts to analyze thedistribution of documents in a system.distribution of documents in a system.

2 – 6 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Compliance TestingCompliance Testing

Compliance testing requires an understandingCompliance testing requires an understandingof the controls that are to be tested.of the controls that are to be tested.

Auditors must have a basic understandingAuditors must have a basic understandingof systems techniques.of systems techniques.

– – input-process-output (IPO)input-process-output (IPO)– – hierarchy plus input-process-output (HIPO)hierarchy plus input-process-output (HIPO)

– – logical data flow diagrams (DFD)logical data flow diagrams (DFD)

2 – 7 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Working PapersWorking Papers

Required by professional standardsRequired by professional standards

These are the records kept by an auditorThese are the records kept by an auditorof the procedures and tests applied, theof the procedures and tests applied, theinformation obtained, and conclusionsinformation obtained, and conclusions

drawn during an audit engagement.drawn during an audit engagement.

2 – 8 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Working PapersWorking Papers

What are some of the systems techniquesWhat are some of the systems techniquesused by auditors to document and analyzeused by auditors to document and analyze

the content of working papers?the content of working papers?

– – internal control questionnairesinternal control questionnaires– – analytic flowcharts analytic flowcharts – – system flowchartssystem flowcharts

– – branching and decision tablesbranching and decision tables

2 – 9 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Use of Systems TechniquesUse of Systems Techniquesin Systems Developmentin Systems Development

What are the three phases of aWhat are the three phases of asystems development project?systems development project?

1. Systems analysis1. Systems analysis

2. Systems design2. Systems design

3. Systems implementation3. Systems implementation

2 – 10 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Systems AnalysisSystems Analysis

Much of a systems analyst’s job involvesMuch of a systems analyst’s job involvescollecting and organizing facts.collecting and organizing facts.

Systems techniques examples:Systems techniques examples:

InterviewingInterviewing

Document reviewsDocument reviews

ObservationsObservations

Matrix Matrix

2 – 11 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Systems DesignSystems Design

A blueprint must be formulatedA blueprint must be formulatedfor the complete system.for the complete system.

Input/output (matrix) analysisInput/output (matrix) analysis

Systems flowchartingSystems flowcharting

Data flow diagramsData flow diagrams

2 – 12 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Systems ImplementationSystems Implementation

Systems implementation involves theSystems implementation involves theactual carrying out of the design plan.actual carrying out of the design plan.

What systems techniques serveWhat systems techniques serveas a documentation tool?as a documentation tool?

Program flowchartsProgram flowcharts

Decision tablesDecision tables

2 – 13 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Learning Objective 2Learning Objective 2

Describe the use of flowchartingDescribe the use of flowcharting

techniques in the analysis oftechniques in the analysis of

information processing systems.information processing systems.

2 – 14 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Systems TechniquesSystems Techniques

What is a flowchart?What is a flowchart?

A flowchart is a symbolic diagramA flowchart is a symbolic diagramthat shows the data flow andthat shows the data flow and

sequence of operations in a system.sequence of operations in a system.

2 – 15 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Basic SymbolsBasic Symbols

Input/outputInput/output

ProcessProcess

AnnotationAnnotation

FlowlineFlowline

2 – 16 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Specialized Input/Output Specialized Input/Output SymbolsSymbols

PunchedPunchedcardcard

OnlineOnlinestoragestorage

MagneticMagneticdiskdisk

MagneticMagnetictapetape

PunchedPunchedtapetape

2 – 17 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Specialized Input/Output Specialized Input/Output SymbolsSymbols

DocumentDocument

ManualManualinputinput

DisplayDisplay

OfflineOfflinestoragestorage

CommunicationCommunicationlinklink

2 – 18 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Specialized Process SymbolsSpecialized Process Symbols

DecisionDecision

PredefinedPredefinedprocessprocess

PreparationPreparation

ManualManualoperationoperation

AuxiliaryAuxiliaryoperationoperation

MergeMerge

ExtractExtract

SortSortCollateCollate

2 – 19 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

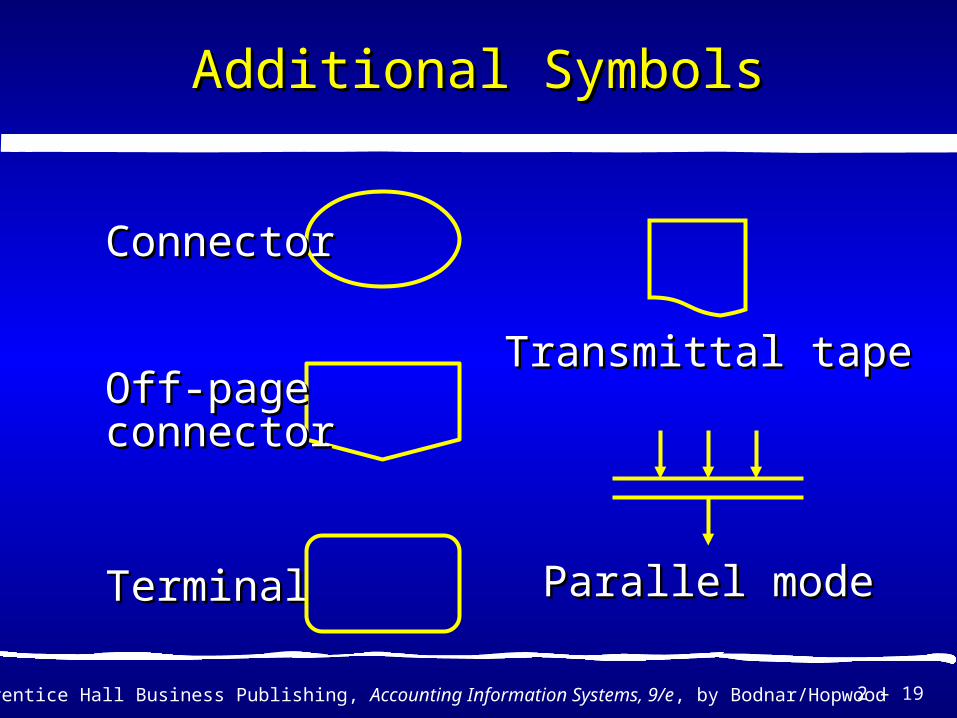

Additional SymbolsAdditional Symbols

Parallel modeParallel mode

Transmittal tapeTransmittal tape

ConnectorConnector

Off-pageOff-pageconnectorconnector

TerminalTerminal

2 – 20 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Symbol Use in FlowchartingSymbol Use in Flowcharting

Symbols are used in a flowchart toSymbols are used in a flowchart torepresent the functions of anrepresent the functions of an

information or other type of system.information or other type of system.

Normal direction of flow is fromNormal direction of flow is fromleft to right and top to bottom.left to right and top to bottom.

Open arrowheads should be usedOpen arrowheads should be usedon reverse-direction flowlines.on reverse-direction flowlines.

2 – 21 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Symbol Usage IllustrationSymbol Usage Illustration

InvoiceInvoice

Normal Direction of FlowNormal Direction of Flow

ReviewReviewandand

approveapprove

ApprovedApprovedinvoiceinvoice

2 – 22 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

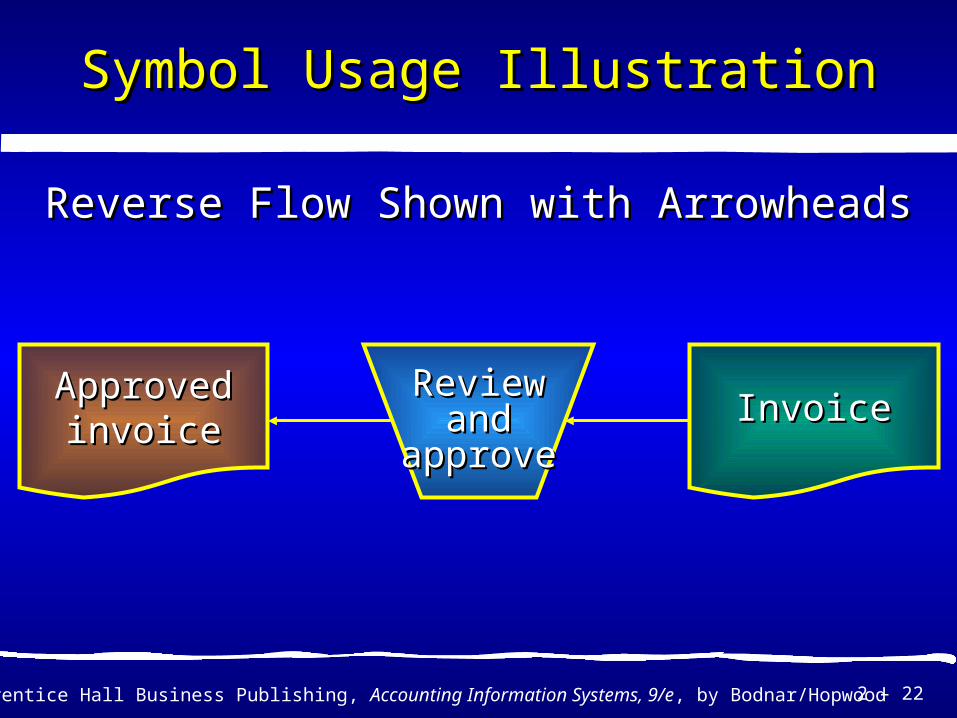

Symbol Usage IllustrationSymbol Usage Illustration

Reverse Flow Shown with ArrowheadsReverse Flow Shown with Arrowheads

InvoiceInvoiceReviewReview

andandapproveapprove

ApprovedApprovedinvoiceinvoice

2 – 23 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

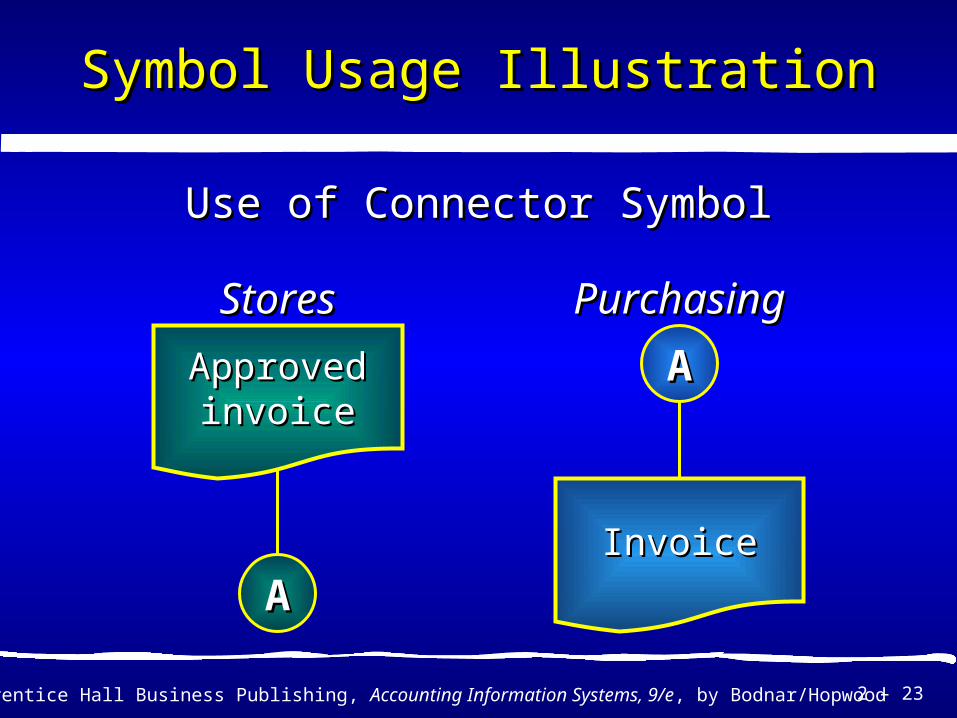

Symbol Usage IllustrationSymbol Usage Illustration

Use of Connector SymbolUse of Connector Symbol

ApprovedApprovedinvoiceinvoice

AA

StoresStores

InvoiceInvoice

AA

PurchasingPurchasing

2 – 24 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

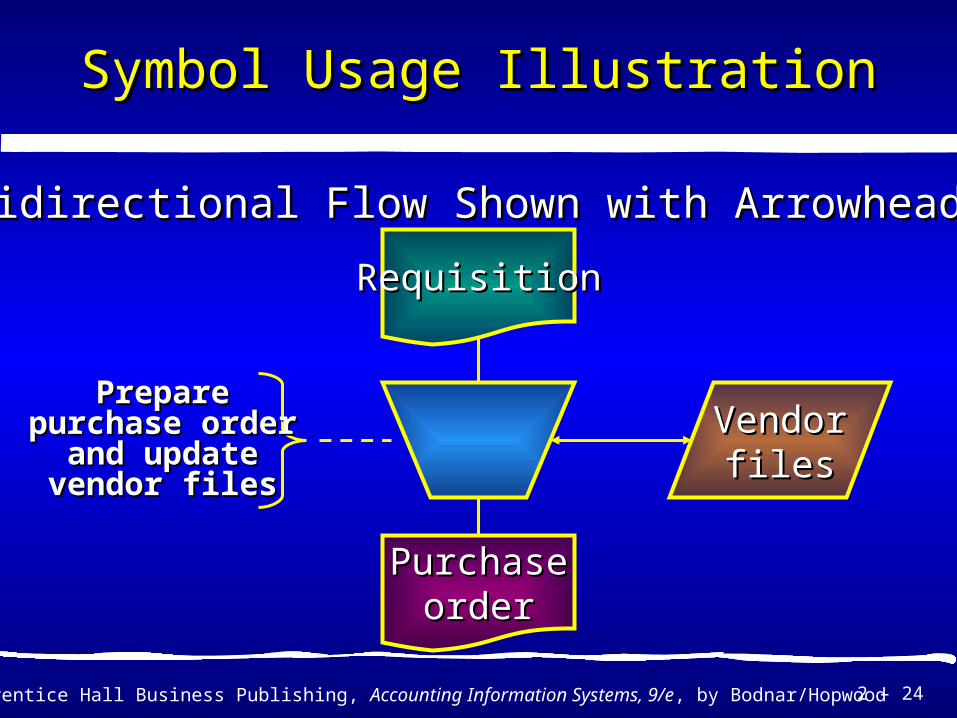

Symbol Usage IllustrationSymbol Usage Illustration

Bidirectional Flow Shown with ArrowheadsBidirectional Flow Shown with Arrowheads

RequisitionRequisition

VendorVendorfilesfiles

PreparePreparepurchase orderpurchase order

and updateand updatevendor filesvendor files

PurchasePurchaseorderorder

2 – 25 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Learning Objective 3Learning Objective 3

Define common systems techniques,

such as HIPO charts, systems

flowcharts, and logical

data flow diagrams.

2 – 26 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

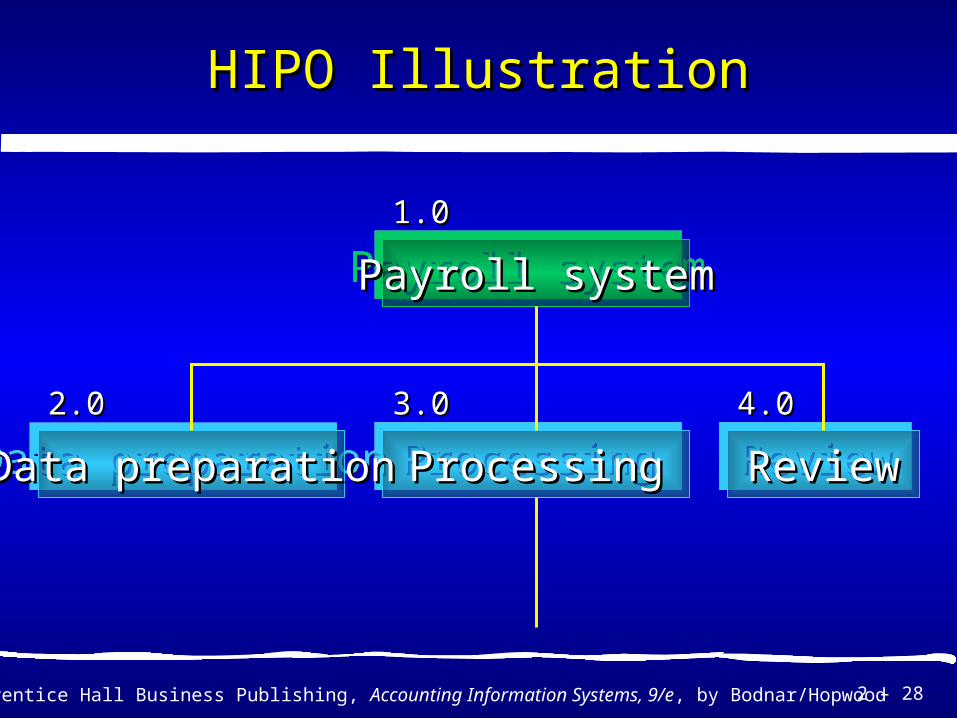

IPO and HIPO ChartsIPO and HIPO Charts

These charts are used primarily byThese charts are used primarily bysystems development personnel.systems development personnel.

At the most general level of analysis,At the most general level of analysis,only the basic input-process-outputonly the basic input-process-outputrelations in a system are of concern.relations in a system are of concern.

Additional processing detail is providedAdditional processing detail is providedby hierarchy plus input-process-output.by hierarchy plus input-process-output.

2 – 27 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

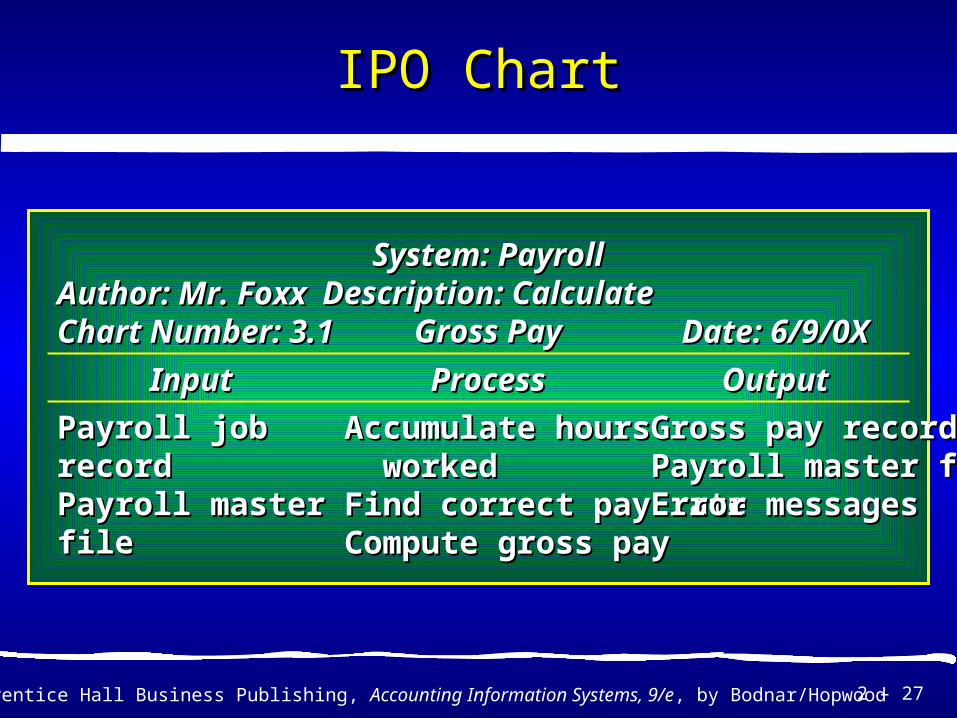

IPO ChartIPO Chart

Payroll job recordPayroll job recordPayroll master filePayroll master file

Accumulate hoursAccumulate hours workedworkedFind correct pay rateFind correct pay rateCompute gross payCompute gross pay

Gross pay recordsGross pay recordsPayroll master filePayroll master fileError messagesError messages

Author: Mr. FoxxAuthor: Mr. FoxxChart Number: 3.1Chart Number: 3.1

System: PayrollSystem: PayrollDescription: CalculateDescription: Calculate

Gross PayGross Pay Date: 6/9/0XDate: 6/9/0X

InputInput ProcessProcess OutputOutput

2 – 28 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

HIPO IllustrationHIPO Illustration

Payroll systemPayroll systemPayroll systemPayroll system

1.01.0

ProcessingProcessingProcessingProcessing

3.03.0

Data preparationData preparationData preparationData preparation

2.02.0

ReviewReviewReviewReview

4.04.0

2 – 29 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

HIPO IllustrationHIPO Illustration

CalculateCalculategross paygross payCalculateCalculategross paygross pay

CalculateCalculatenet paynet payCalculateCalculatenet paynet pay

3.13.1 3.23.2

Each numbered module would be detailed in an IPO chart.

AccumulateAccumulatehours workedhours worked

AccumulateAccumulatehours workedhours worked

3.113.11

Find correctFind correctpay ratepay rate

Find correctFind correctpay ratepay rate

3.123.12

ComputeComputegross paygross payComputeComputegross paygross pay

3.133.13

2 – 30 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Systems and Program Systems and Program FlowchartsFlowcharts

A A systems flowchartsystems flowchart identifies the overall identifies the overallor broad flow of operations in a system.or broad flow of operations in a system.

A A program flowchartprogram flowchart (block flowchart) (block flowchart)is more detailed concerningis more detailed concerning

individual processing functions.individual processing functions.

2 – 31 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

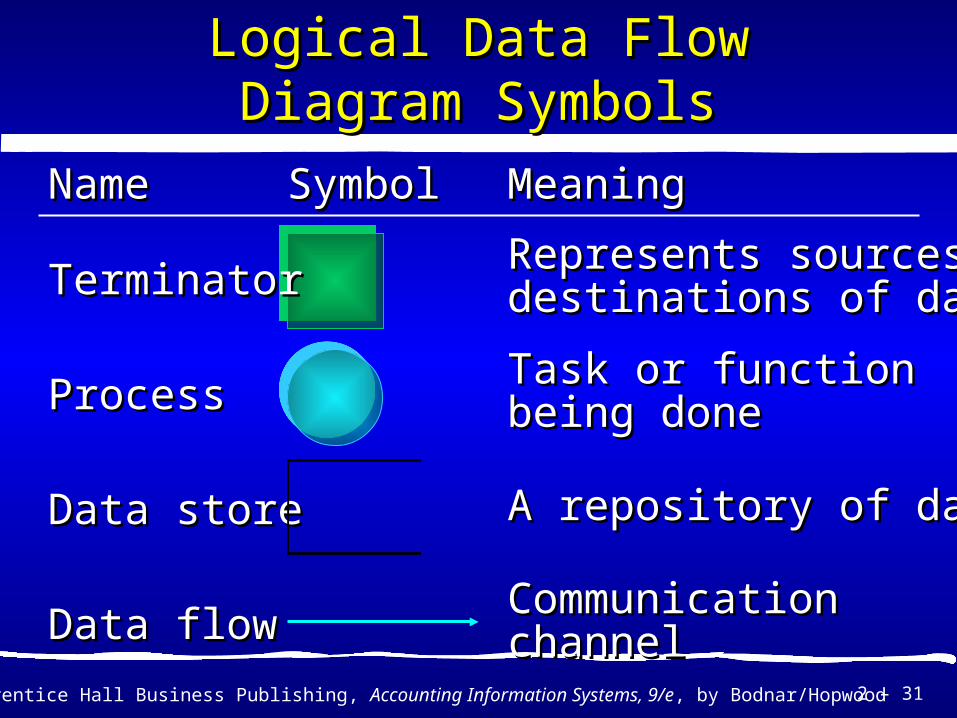

Logical Data FlowLogical Data FlowDiagram SymbolsDiagram Symbols

TerminatorTerminatorRepresents sources andRepresents sources anddestinations of datadestinations of data

ProcessProcessTask or functionTask or functionbeing donebeing done

Data storeData store A repository of dataA repository of data

Data flowData flowCommunicationCommunicationchannelchannel

NameName SymbolSymbol MeaningMeaning

2 – 32 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

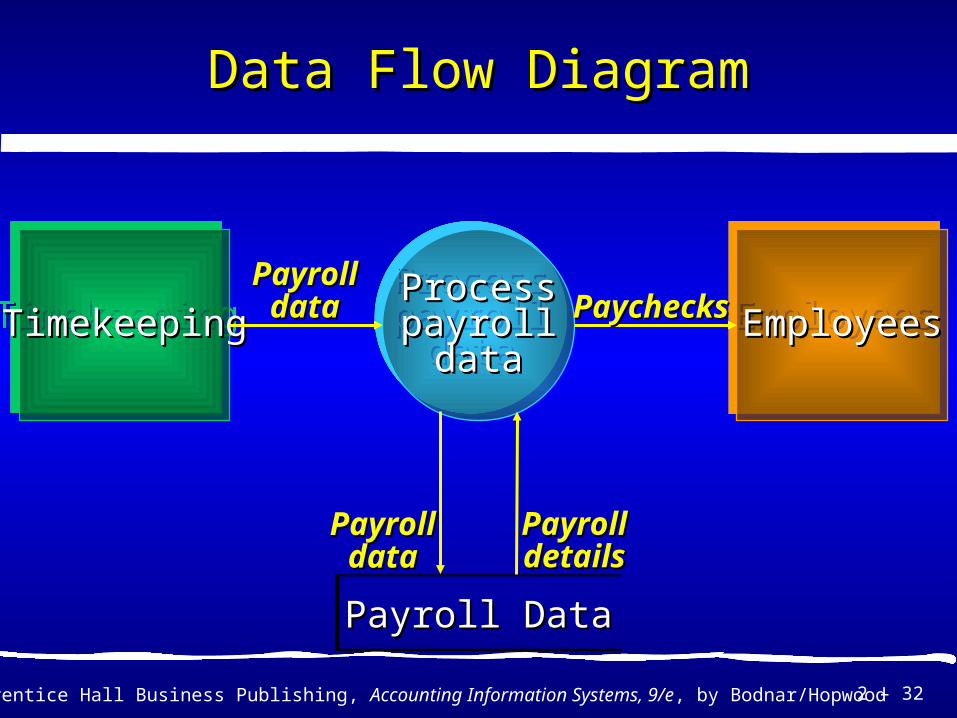

Data Flow DiagramData Flow Diagram

TimekeepingTimekeepingTimekeepingTimekeepingProcessProcesspayrollpayroll

datadata

ProcessProcesspayrollpayroll

datadata

PayrollPayrolldatadata EmployeesEmployeesEmployeesEmployeesPaychecksPaychecks

Payroll DataPayroll Data

PayrollPayrolldatadata

PayrollPayrolldetailsdetails

2 – 33 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

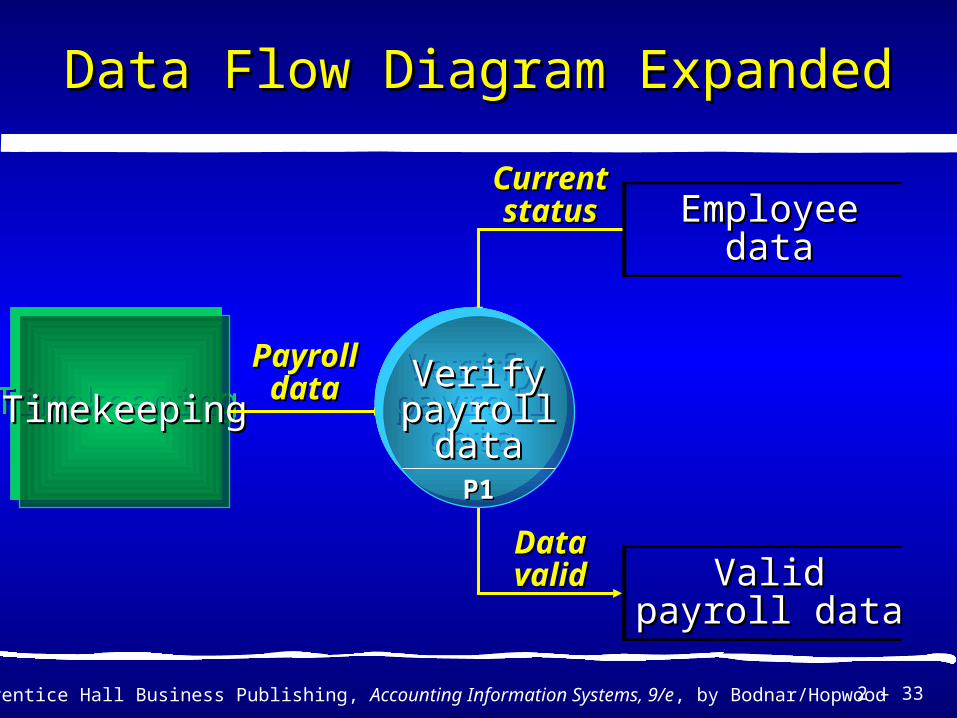

Data Flow Diagram ExpandedData Flow Diagram Expanded

TimekeepingTimekeepingTimekeepingTimekeeping

EmployeeEmployeedatadata

CurrentCurrentstatusstatus

ValidValidpayroll datapayroll data

DataDatavalidvalid

PayrollPayrolldatadata

VerifyVerifypayrollpayroll

datadata

VerifyVerifypayrollpayroll

datadataP1P1

2 – 34 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Data Flow Diagram ExpandedData Flow Diagram Expanded

ValidValidpayroll datapayroll data

EmployeeEmployeedatadata

Net pay andNet pay anddeductionsdeductions

CalculateCalculatepaypay

CalculateCalculatepaypay

P2P2

Data toData toprocessprocess

EmployeesEmployeesEmployeesEmployeesPaychecksPaychecks

2 – 35 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

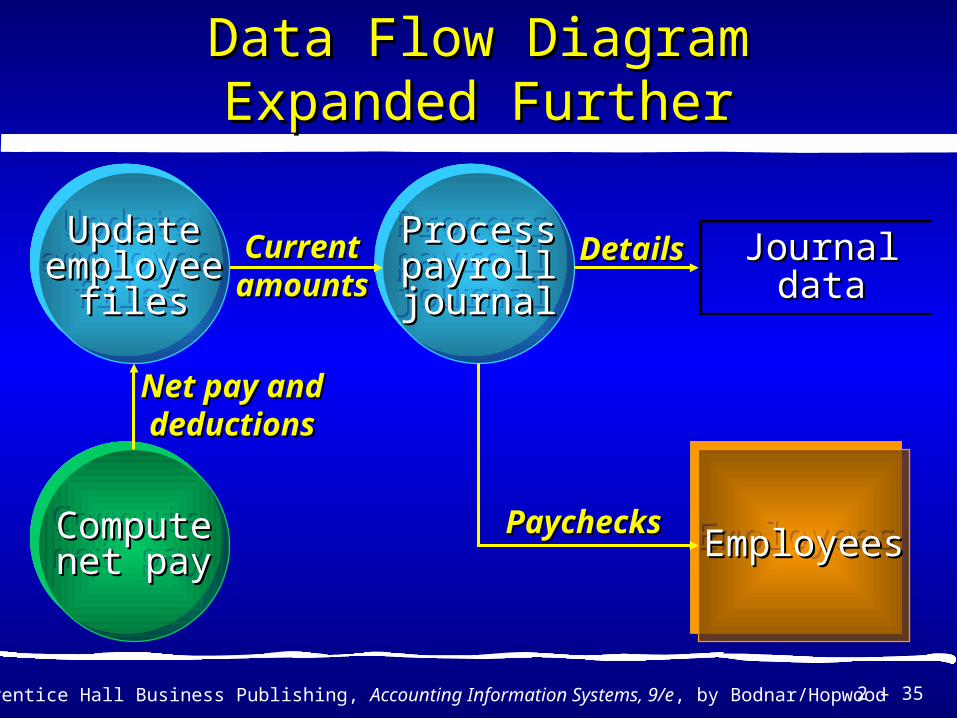

Data Flow DiagramData Flow DiagramExpanded FurtherExpanded Further

ComputeComputenet paynet payComputeComputenet paynet pay

ProcessProcesspayrollpayrolljournaljournal

ProcessProcesspayrollpayrolljournaljournal

CurrentCurrentamountsamounts

UpdateUpdateemployeeemployee

filesfiles

UpdateUpdateemployeeemployee

filesfiles

Net pay andNet pay anddeductionsdeductions

JournalJournaldatadata

DetailsDetails

EmployeesEmployeesEmployeesEmployeesPaychecksPaychecks

2 – 36 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Analytic, Document, and Forms Analytic, Document, and Forms Distribution FlowchartsDistribution Flowcharts

An An analytic flowchartanalytic flowchart is similar is similarto a systems flowchart in levelto a systems flowchart in level

of detail and technique.of detail and technique.

A A document flowchartdocument flowchart is similar to an is similar to ananalytic flowchart but contains lessanalytic flowchart but contains less

detail about the processing functionsdetail about the processing functionsof each entity shown on the chart.of each entity shown on the chart.

2 – 37 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Analytic, Document, and Forms Analytic, Document, and Forms Distribution FlowchartsDistribution Flowcharts

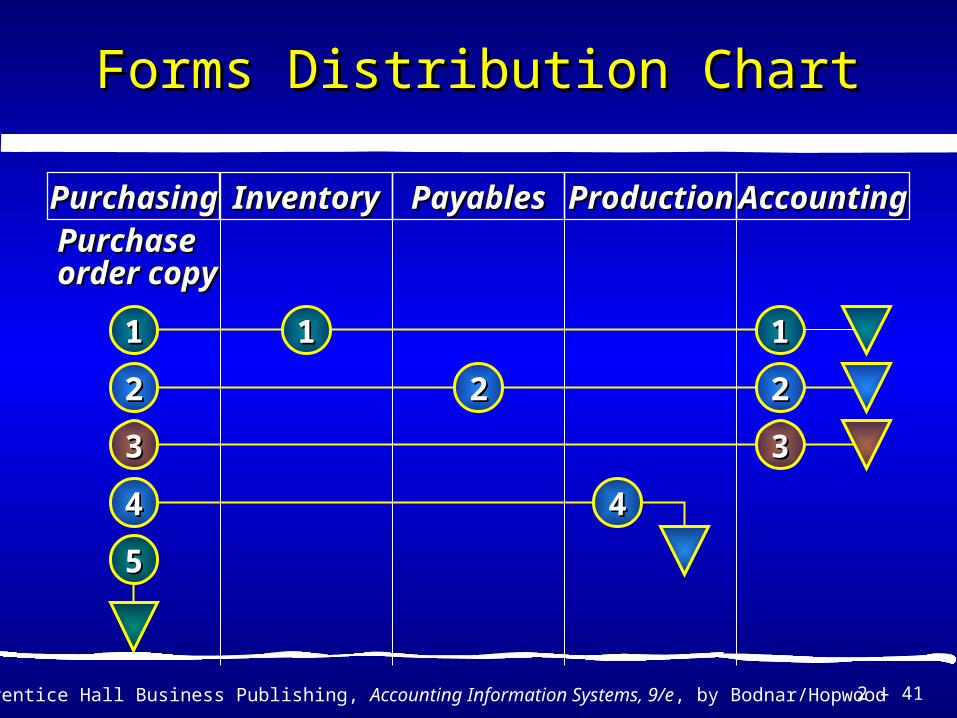

The The forms distribution chartforms distribution chart illustrates illustratesthe distribution of multiple copythe distribution of multiple copy

forms with an organization.forms with an organization.

ReceiveReceivePurchasePurchase

2 – 38 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Analytic FlowchartAnalytic Flowchart

PreparePreparequotationquotationrequestsrequests

PreparePreparequotationquotationrequestsrequests

RequestsRequestsforfor

quotationquotation

RequestsRequestsforfor

quotationquotation

ApproveApprovevendorvendor

listlist

ApproveApprovevendorvendor

listlist

SelectSelectvendorsvendors

SelectSelectvendorsvendors

RequestsRequestsforfor

quotationquotation

RequestsRequestsforfor

quotationquotation

PurchasingPurchasing SuppliersSuppliers

QuotationsQuotationsQuotationsQuotations

2 – 39 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

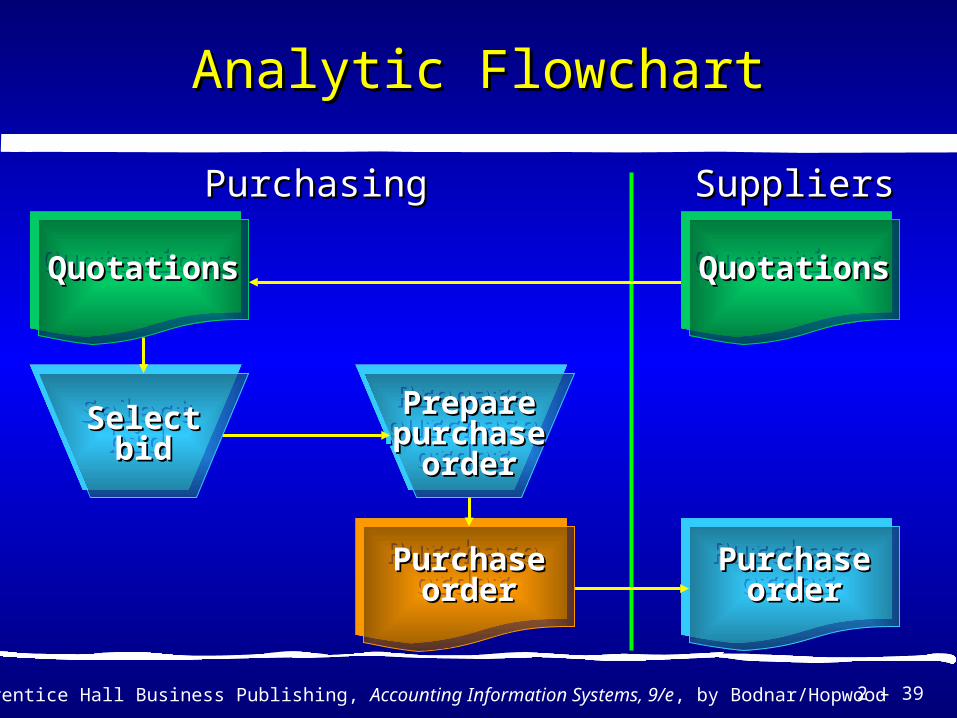

Analytic FlowchartAnalytic Flowchart

PurchasingPurchasing

PurchasePurchaseorderorder

PurchasePurchaseorderorder

SuppliersSuppliers

QuotationsQuotationsQuotationsQuotations

PreparePreparepurchasepurchase

orderorder

PreparePreparepurchasepurchase

orderorder

QuotationsQuotationsQuotationsQuotations

SelectSelectbidbid

SelectSelectbidbid

PurchasePurchaseorderorder

PurchasePurchaseorderorder

2 – 40 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Document FlowchartDocument Flowchart

2222

PurchasePurchaserequisitionrequisition

22

PurchasePurchaserequisitionrequisition

22

PurchasePurchaserequisitionrequisition

11

PurchasePurchaserequisitionrequisition

11

PurchasePurchaserequisitionrequisition

11

PurchasePurchaserequisitionrequisition

11

PurchasePurchaseorderorder

33

PurchasePurchaseorderorder

33 PurchasePurchaseorderorder

44

PurchasePurchaseorderorder

44PurchasePurchase

orderorder 55

PurchasePurchaseorderorder

55

To VendorTo Vendor

55554444

33332222

PurchasePurchaseorderorder

11

PurchasePurchaseorderorder

11

AccountsAccountsPayablePayable

Purchasing AgentPurchasing Agent ReceivingReceiving StoresStoresControllerController Vice President ManufacturingVice President Manufacturing

2 – 41 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Forms Distribution ChartForms Distribution Chart

PurchasingPurchasing InventoryInventory PayablesPayables ProductionProduction AccountingAccounting

PurchasePurchaseorder copyorder copy

22

33

44

55

11 11

22

44

11

22

33

2 – 42 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Analytical Flowcharting Analytical Flowcharting IllustrationIllustration

Symbol selectionSymbol selection System analysisSystem analysis

Drawing the flowchartDrawing the flowchart Sandwich ruleSandwich rule

Use of connector symbolUse of connector symbol Entity-column relationsEntity-column relations

2 – 43 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Narrative TechniquesNarrative Techniques

Narrative techniques are useful in theNarrative techniques are useful in thefact-finding stage of system analysis.fact-finding stage of system analysis.

What are some examples of narrative techniques?What are some examples of narrative techniques?

Open-ended and closed-ended questionnairesOpen-ended and closed-ended questionnaires

Document reviewsDocument reviews

2 – 44 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

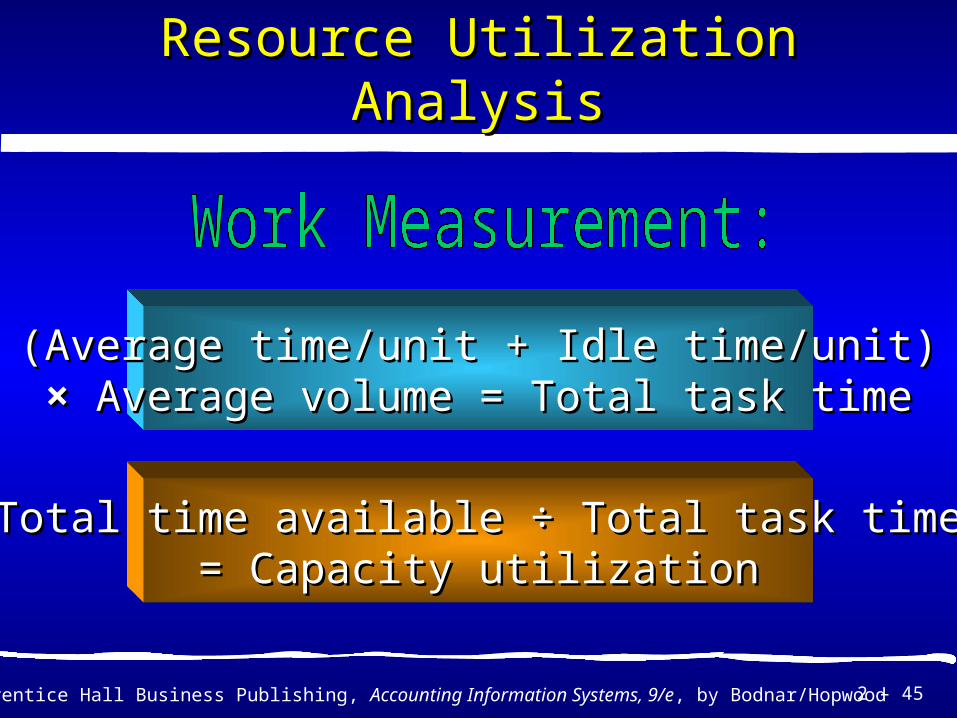

Resource Utilization AnalysisResource Utilization Analysis

Work measurement involves four basic steps.Work measurement involves four basic steps.

1. Identify the tasks.1. Identify the tasks.

2. Obtain time estimates for performing the tasks.2. Obtain time estimates for performing the tasks.

3. Adjust these time estimates.3. Adjust these time estimates.

4. Analyze requirements based on these data.4. Analyze requirements based on these data.

2 – 45 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Resource Utilization AnalysisResource Utilization Analysis

(Average time/unit + Idle time/unit)(Average time/unit + Idle time/unit)×× Average volume = Total task time Average volume = Total task time

Total time available ÷ Total task timeTotal time available ÷ Total task time= Capacity utilization= Capacity utilization

2 – 46 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

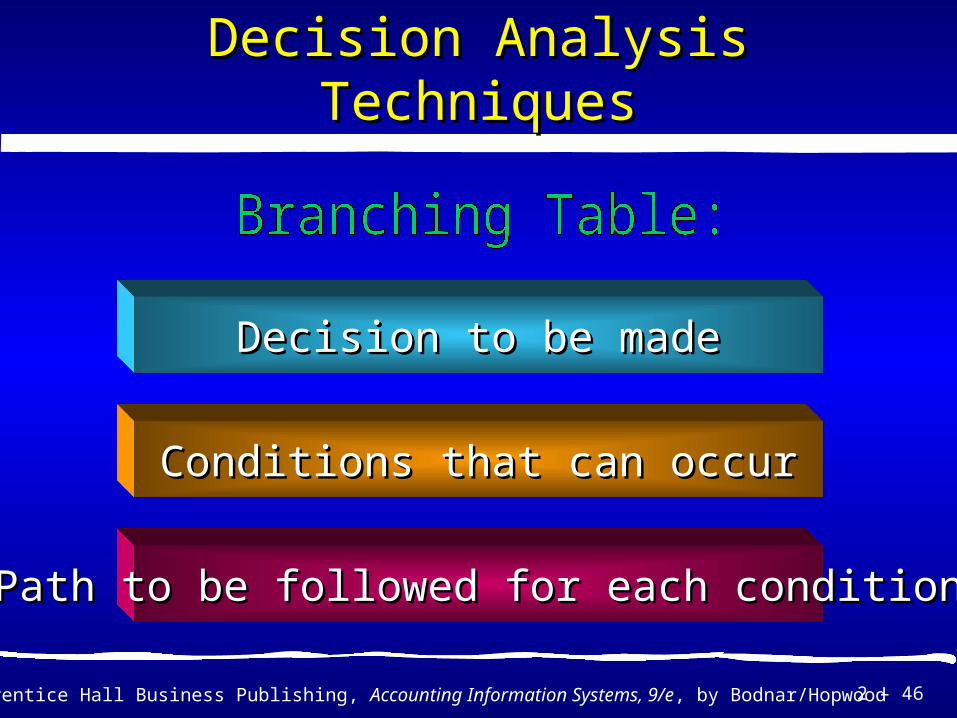

Decision Analysis TechniquesDecision Analysis Techniques

Decision to be madeDecision to be made

Conditions that can occurConditions that can occur

Path to be followed for each conditionPath to be followed for each condition

2 – 47 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

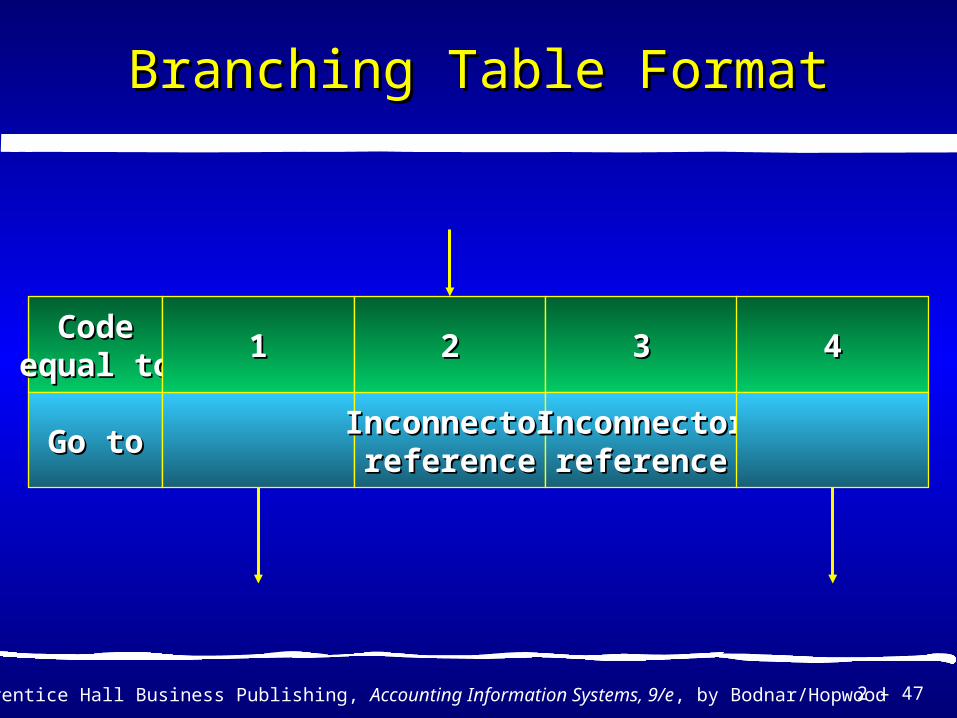

Branching Table FormatBranching Table Format

CodeCodeequal toequal to

Go toGo toInconnectorInconnector

referencereference

11 22 33

InconnectorInconnectorreferencereference

44

2 – 48 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

Decision Table FormatDecision Table Format

Condition stubCondition stub

Action stubAction stub

11 22 33 …… NN

If:If:

Then:Then:

Table TitleTable Title RulesRules

Condition entryCondition entry

Action entryAction entry

2 – 49 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

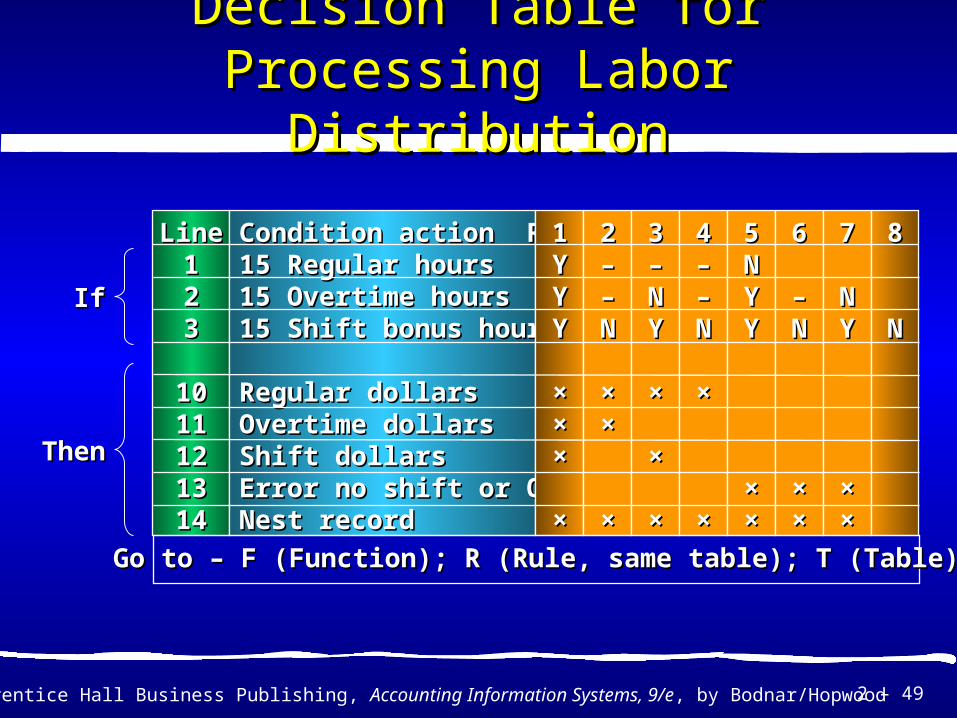

Decision Table forDecision Table forProcessing Labor DistributionProcessing Labor Distribution

LineLine112233

10101111121213131414

Condition action Rule Condition action Rule 15 Regular hours15 Regular hours15 Overtime hours15 Overtime hours15 Shift bonus hours15 Shift bonus hours

Regular dollarsRegular dollarsOvertime dollarsOvertime dollarsShift dollarsShift dollarsError no shift or OTError no shift or OTNest recordNest record

11YYYYYY

××××××

××

22––––NN

××××

××

33––NNYY

××

××

××

44––––NN

××

××

55NNYYYY

××××

66

––NN

××××

77

NNYY

××××

88

NNIfIf

ThenThen

Go to – F (Function); R (Rule, same table); T (Table)Go to – F (Function); R (Rule, same table); T (Table)

2 – 50 2004 Prentice Hall Business Publishing, Accounting Information Systems, 9/e, by Bodnar/Hopwood

End of Chapter End of Chapter 22