airports november 2011 - ibef · airports november 2011 . 2 contents ... • aviation sector growth...

TRANSCRIPT

1 1 For updated information, please visit www.ibef.org

Airports NOVEMBER

2011

2 2

Contents

Advantage India

Market overview and trends

Growth drivers

Success stories: Delhi, Mumbai

Opportunities

Useful information

For updated information, please visit www.ibef.org

Airports NOVEMBER

2011

3 3

Airports

For updated information, please visit www.ibef.org ADVANTAGE INDIA

Advantage India

NOVEMBER

2011

Advantage India

• Growth in passenger traffic likely to go up as incomes rise and more tourists flow in

• Freight traffic also likely to go up as

trade with the rest of the world increases

• Aviation sector growth accentuating need for maintenance, repair and overhaul

• Bright prospects due to location advantage and demand for new facilities

• USD7.5 billion worth of investments in airports infrastructure likely under the Eleventh Five Year Plan (2007-12)

• Growing private sector participation through public – private partnership

• Encouragement to private sector participation; relaxation of FDI norms

• Tax incentives for developers; liberalisation of the aviation sector – Open Sky Policy

No of operational airports: 82

2010

No of operational airports: 50

2000

Notes: FDI – Foreign direct investment, MRO – Maintenance, repair and overhaul

Growing demand Opportunities in MRO

Increasing investments Policy support

4 4

Contents

Advantage India

Market overview and trends

Growth drivers

Success stories: Delhi, Mumbai

Opportunities

Useful information

For updated information, please visit www.ibef.org

Airports NOVEMBER

2011

5 5 For updated information, please visit www.ibef.org MARKET OVERVIEW AND TRENDS

Evolution of the Indian aviation sector

Source: Airports Authority of India, Ministry of Statistics and Programme Implementation, Aranca Research

Notes: * data for FY10(P), ** data for financial year and not calendar year; FY – Indian financial year (April – March), mn km – million kilometers

Airports NOVEMBER

2011

→ India is the 9th largest civil aviation market in the world → India is ranked 4th in domestic passenger volumes (45.3 million*)

Scheduled airlines: distance flown (mn km)

Non-scheduled airlines in operation

Number of aircraft

Passenger handling capacity at airports

Number of operational airports 50

66 million

225

39

199**

82

235 million

735

123

710**

2000

2010

6 6 For updated information, please visit www.ibef.org

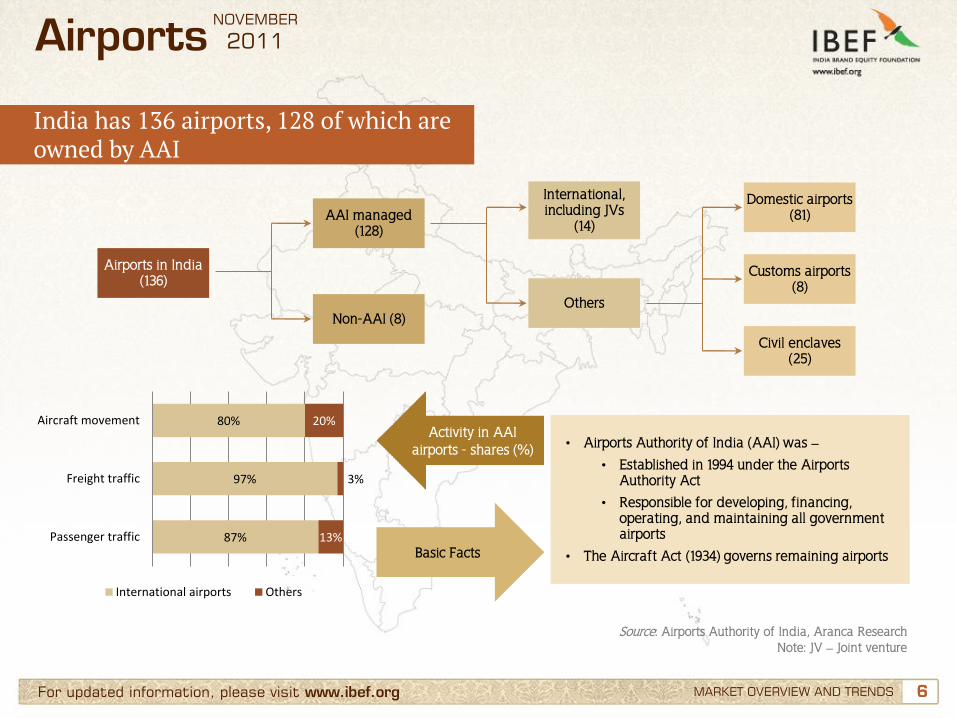

India has 136 airports, 128 of which are owned by AAI

Source: Airports Authority of India, Aranca Research Note: JV – Joint venture

MARKET OVERVIEW AND TRENDS

Airports NOVEMBER

2011

Airports in India (136)

AAI managed (128)

Non-AAI (8)

International, including JVs

(14)

Others

Civil enclaves (25)

Customs airports (8)

Domestic airports (81)

• Airports Authority of India (AAI) was –

• Established in 1994 under the Airports Authority Act

• Responsible for developing, financing, operating, and maintaining all government airports

• The Aircraft Act (1934) governs remaining airports

Activity in AAI airports - shares (%)

Basic Facts 87%

97%

80%

13%

3%

20%

Passenger traffic

Freight traffic

Aircraft movement

International airports Others

7 7 For updated information, please visit www.ibef.org

Six major airlines operate in the country

Note: All statistics are for the month of August 2011 as published by Directorate General of Civil Aviation

MARKET OVERVIEW AND TRENDS

Airports NOVEMBER

2011

Market Share (%) Flight Occupancy Rate (%)

26.3 (combined) 72.1 (Jet)

73.9 (Jet Lite)

18.8 75.9

18.7 73.2

17.4 72.8

13.4 66

5.3 65

8 8 For updated information, please visit www.ibef.org

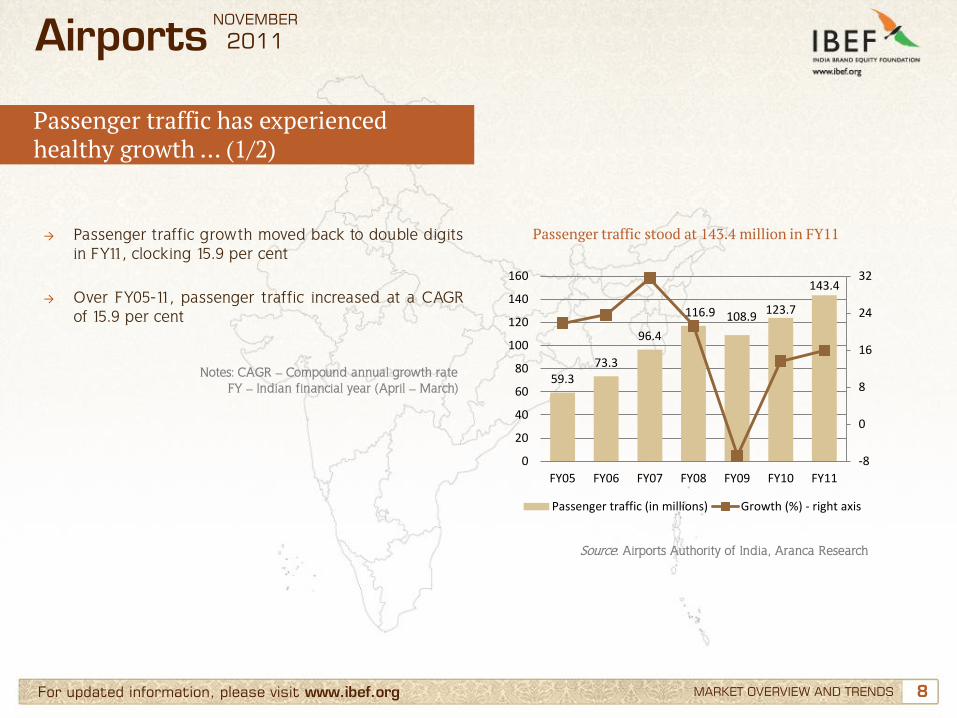

Passenger traffic has experienced healthy growth … (1/2)

MARKET OVERVIEW AND TRENDS

→ Passenger traffic growth moved back to double digits in FY11, clocking 15.9 per cent

→ Over FY05-11, passenger traffic increased at a CAGR

of 15.9 per cent

Passenger traffic stood at 143.4 million in FY11

Source: Airports Authority of India, Aranca Research

Notes: CAGR – Compound annual growth rate FY – Indian financial year (April – March)

Airports NOVEMBER

2011

59.3 73.3

96.4

116.9 108.9 123.7

143.4

-8

0

8

16

24

32

0

20

40

60

80

100

120

140

160

FY05 FY06 FY07 FY08 FY09 FY10 FY11

Passenger traffic (in millions) Growth (%) - right axis

9 9 For updated information, please visit www.ibef.org

Passenger traffic has experienced healthy growth … (2/2)

MARKET OVERVIEW AND TRENDS

→ Domestic passenger traffic expanded at 17.6 per cent CAGR over FY05–11

→ International passenger traffic rose 11.8 per cent over the same period

Growth in domestic passenger traffic has been robust

Source: Airports Authority of India , Aranca Research

Airports NOVEMBER

2011

39.9 51.0

70.6 87.1 77.3

89.4 105.5 19.4

22.3

25.8

29.8

31.6

34.4

37.9

-12

-6

0

6

12

18

24

30

36

42

0

20

40

60

80

100

120

140

160

FY05 FY06 FY07 FY08 FY09 FY10 FY11

Domestic (million,left axis) International (million,left axis)

Growth - domestic (%) Growth - international (%)

10 10 For updated information, please visit www.ibef.org

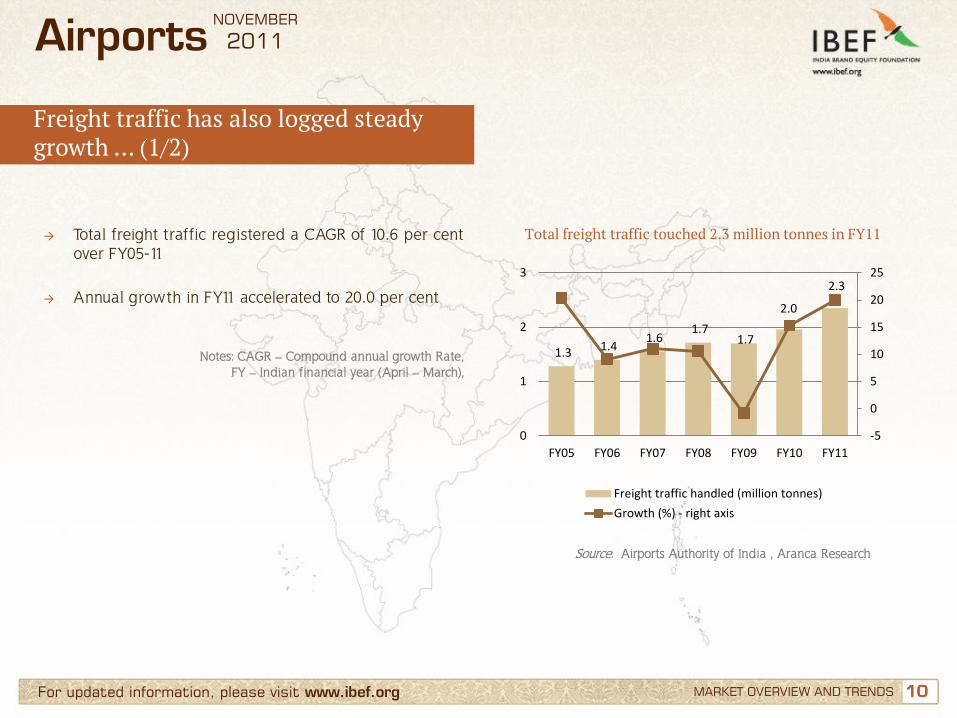

Freight traffic has also logged steady growth … (1/2)

MARKET OVERVIEW AND TRENDS

Airports NOVEMBER

2011

→ Total freight traffic registered a CAGR of 10.6 per cent over FY05-11

→ Annual growth in FY11 accelerated to 20.0 per cent

Total freight traffic touched 2.3 million tonnes in FY11

Source: Airports Authority of India , Aranca Research

Notes: CAGR – Compound annual growth Rate, FY – Indian financial year (April – March),

1.3 1.4 1.6

1.7 1.7

2.0

2.3

-5

0

5

10

15

20

25

0

1

2

3

FY05 FY06 FY07 FY08 FY09 FY10 FY11

Freight traffic handled (million tonnes)

Growth (%) - right axis

11 11 For updated information, please visit www.ibef.org

Freight traffic has also logged steady growth … (2/2)

MARKET OVERVIEW AND TRENDS

Airports NOVEMBER

2011

→ Domestic freight traffic increased at 10.9 per cent CAGR over FY05-11

→ International freight traffic rose 10.4 per cent over the same period

International freight traffic was 64% of the total in FY11

Source: Airports Authority of India , Aranca Research

457 484 530 568 552 689 852

824

920 1,023 1,147 1,149 1,271

1,493

-5

0

5

10

15

20

25

0

500

1000

1500

2000

2500

FY05 FY06 FY07 FY08 FY09 FY10 FY11

International ('000 tonnes) Domestic ('000 tonnes)

Growth - domestic (%, right axis) Growth - international (%, right axis)

12 12 For updated information, please visit www.ibef.org

Growth in aviation has also led to higher aircraft movement … (1/2)

MARKET OVERVIEW AND TRENDS

→ Total aircraft movement recorded a CAGR of 11.7 per cent over FY05-11

→ Both international and domestic aircraft movement

have nearly doubled over this period

Total aircraft movement was 1.4 million in FY11

Source: Airports Authority of India , Aranca Research

Notes: CAGR – Compound annual growth rate FY – Indian financial year (April – March)

Airports NOVEMBER

2011

718 838

1,078

1,308 1,307 1,331 1,394

-5

0

5

10

15

20

25

30

0

200

400

600

800

1000

1200

1400

1600

FY05 FY06 FY07 FY08 FY09 FY10 FY11

Aircraft movement ('000) Growth (%) - right axis

13 13 For updated information, please visit www.ibef.org

Growth in aviation has also led to higher aircraft movement … (2/2)

MARKET OVERVIEW AND TRENDS

→ Domestic aircraft movement increased at 12.0 per cent CAGR over FY05-11

→ International aircraft movement expanded by 10.7 per

cent over the same period

Aircraft movement growth was sharpest over FY06–07

Source: Airports Authority of India , Aranca Research

Airports NOVEMBER

2011

554 647 862

1059

1036

1048 1093 163 191

216

249 270 282 300

-6

0

6

12

18

24

30

36

0

200

400

600

800

1000

1200

1400

1600

FY05 FY06 FY07 FY08 FY09 FY10 FY11

Domestic ('000, left axis) International ('000, left axis)

Growth - domestic (%) Growth - international (%)

14 14 For updated information, please visit www.ibef.org MARKET OVERVIEW AND TRENDS

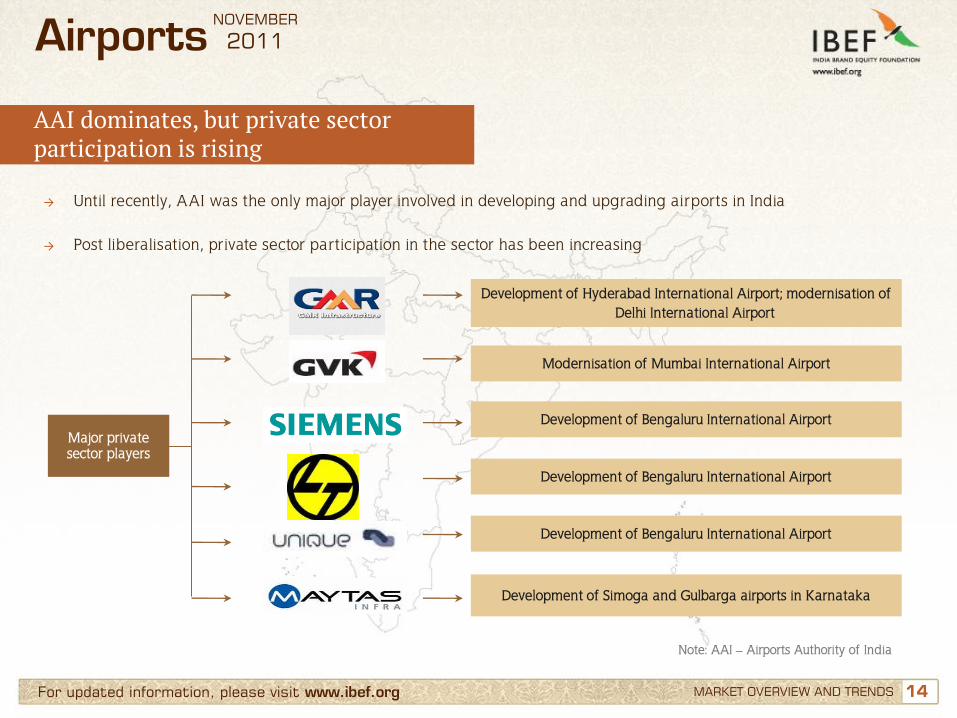

AAI dominates, but private sector participation is rising

Airports NOVEMBER

2011

→ Until recently, AAI was the only major player involved in developing and upgrading airports in India → Post liberalisation, private sector participation in the sector has been increasing

Major private sector players

Development of Hyderabad International Airport; modernisation of Delhi International Airport

Modernisation of Mumbai International Airport

Development of Bengaluru International Airport

Development of Bengaluru International Airport

Development of Bengaluru International Airport

Development of Simoga and Gulbarga airports in Karnataka

Note: AAI – Airports Authority of India

15 15 For updated information, please visit www.ibef.org MARKET OVERVIEW AND TRENDS

Notable trends in the airports sector

Airports NOVEMBER

2011

Note: FY – Indian financial year (April – March)

Increasing private sector participation

• Government policy to increase private sector participation

• Currently, there are 6 major private sector players

Greater use of non-scheduled airlines

• Rising business activity leading to higher demand for non-scheduled airlines

• 99 operators with combined fleet of 241 aircrafts in FY09

User development fees

• Increasing use of development fees by airport developers and operators

• Airport Development Fee: Delhi, Mumbai airports to fund expansion

• User Development Fee: Hyderabad, Bengaluru airports for maintenance

Focus on non-aeronautical revenue

• Indian airports emulating SEZ-aerotropolis model to enhance revenues; focus on revenues from retail, advertising, vehicle parking, etc.

• Absence of complementary meals in low-cost airlines have boosted the food and beverages retail segment at airports

16 16

Contents

Advantage India

Market overview and trends

Growth drivers

Success stories: Delhi, Mumbai

Opportunities

Useful information

For updated information, please visit www.ibef.org

Airports NOVEMBER

2011

17 17 For updated information, please visit www.ibef.org GROWTH DRIVERS

Strong demand and policy support driving investments

Airports NOVEMBER

2011

Strong

government

support

Growing demand

Inviting Resulting

in

Growing demand Increasing investments Policy support

More people travelling by air

Rise in business and tourist travellers

Strong growth in external

trade

Greater government focus on infrastructure

Increasing liberalisation,

Open Sky Policy

Policy sops, FDI encouragement

AAI driving large modernisation, development

projects

Increasing private sector

participation

Strong projected demand making returns attractive

18 18 For updated information, please visit www.ibef.org

Passenger traffic spikes up as demand for air travel soars

GROWTH DRIVERS

Airports NOVEMBER

2011

More Indians travelling by air

• Rise in per-capita income and a growing middle class

• Introduction of low cost airlines

Rising domestic and foreign tourists

• Improving tourism infrastructure

• Successful ad campaigns abroad

More business travellers as well

• India is one of the fastest growing economies

• Emergence of business hubs like Mumbai (Finance), Bangalore (IT), Chennai (IT), Delhi (Manufacturing, IT)

2,441 2,724 2,916 3,104 3,408

5

7

9

11

0

1000

2000

3000

2006 2007 2008 2009 2010E

Per-capita GDP (PPP, current USD)

Real GDP growth (%) - right axis

Travel and Tourism spending (USD billion)

Source: IMF, Aranca Research

Source: WTTC, Aranca Research

34

42 46 47

58

17 22 25 18 22

2006 2007 2008 2009 2010

Leisure travel and tourism spending

Business travel and tourism spending

CAGR 14.6 %

CAGR 6.6 %

Notes: IT – Information technology , E- estimate

GDP growth and per capita income

19 19 For updated information, please visit www.ibef.org

More passengers and rising trade aiding higher aircraft movement

GROWTH DRIVERS

Growth of exports and imports (USD billion)

Source: Ministry of Commerce, Aranca Research Notes: CAGR – Compound annual growth rate, FY11 data is for April-December

Airports NOVEMBER

2011

Growing trade benefits freight movement

• Over FY06-11,

• India’s exports expanded at a CAGR of 13.3 per cent

• Imports registered a 14.2 per cent CAGR

• Growing trade augurs well for airports as they handle about 30 per cent of India’s total trade (by value)

95 119

137

175 176

157 138 175

211

286 284

235

FY06 FY07 FY08 FY09 FY10 FY11

Exports Imports

Higher aircraft movement

Increasing airline operators

Rise in freight traffic

Growth in passenger traffic

Liberalised aviation policy

20 20 For updated information, please visit www.ibef.org

Policy support aiding growth in the airports sector

GROWTH DRIVERS

Airports NOVEMBER

2011

Notes: India currently has bilateral air service agreements with 104 countries. These include Brazil, 27 members of the EU, and China. In 2008 traffic rights were been enhanced with Mexico, Saudi Arabia, Netherlands , Qatar, Iran, Japan and Turkey

FDI – Foreign direct investment, FIPB – Foreign Investment Promotion Board

Greater focus on infrastructure

• Infrastructure investment is a major focus area for the government

• Government of India (GOI) envisions airport infrastructure investment of USD7.5 billion under the Eleventh Five Year Plan (2007-12)

Liberalisation, Open Sky Policy

• GOI approved establishment of Greenfield airports under PPP mode in 2008

• New regulatory body (Airport Economic Regulatory Authority) set up in 2009

• Increased traffic rights under bilateral agreements with foreign countries

Encouragement to FDI • 100 per cent FDI under automatic route for Greenfield projects

• 100 per cent FDI for existing airports is also possible with an approval from FIPB

Taxes and other sops • 100 per cent tax exemption for airport projects for a period of 10 years

• Airport developers allowed to charge passengers development fees

21 21 For updated information, please visit www.ibef.org

AAI leads the way in airports infrastructure investment

GROWTH DRIVERS

Airports NOVEMBER

2011

Metro airports

• Work involves modernising and expansion; these include

• Chennai airport at a cost of USD376.7 million

• Kolkata airport at a cost of USD404.6 million

Non-metro airports

• Work covers upgrading and modernising; estimated cost is USD1 billion

• 35 airports including Ahmedabad, Amritsar, Bhopal, Jaipur, Pune and Goa

• 9 have already been completed

North East India

• Developing airports in Sikkim, Arunachal Pradesh and Nagaland

• Pakyong Airport (Sikkim) costing USD64.5 million to be completed by 2012

• Cheitu Airport (Nagaland), Itanagar Airport (Arunachal) in approval stage

22 22 For updated information, please visit www.ibef.org

Private sector investment in airports rising … (1/2)

GROWTH DRIVERS

→ Recourse to the Public Private Partnership (PPP) model has boosted private sector investments in airports

→ PPP route for five international airports (Delhi, Mumbai, Cochin, Hyderabad, Bengaluru) most noteworthy

Airports NOVEMBER

2011

• Increasing share of private sector in equity component of major airports –

• 74 per cent share in IGI Airport (Delhi); GMR is the largest shareholder (54 per cent)

• 74 per cent share in CSI Airport (Mumbai); GVK is the largest shareholder (50.5 per cent)

• 74 per cent share in RGI Airport (Hyderabad); GMR is the largest shareholder (63 per cent)

23 23 For updated information, please visit www.ibef.org GROWTH DRIVERS

Airports NOVEMBER

2011

Participation in international

airport projects

Terminal 3 construction in Delhi completed in 2010

Total cost

USD8 billion

Greenfield projects with private sector participation

PPP format likely to continue

USD2.6 billion of investments likely

Private sector investment in airports rising … (2/2)

Delhi (Modernisation,

Terminal 3)

Mumbai (Modernis-

ation)

Hyderabad

Bengaluru

Bijapur Airport

Shimoga Airport

Hassan Airport

Gulbarga Airport

24 24 For updated information, please visit www.ibef.org GROWTH DRIVERS

Foreign players are showing increasing interest in the sector

Airports NOVEMBER

2011

Major Foreign Players Airport Stake Description

Bid Services Division (Mauritius) Limited

Mumbai International Airport Pvt Ltd 13.5 International service, trading and distribution company

based in South Africa.

Airports Company South Africa Global

Mumbai International Airport Pvt Ltd

10 Operates and owns ten airports in South Africa.

Frankfurt Airport Services Worldwide

Delhi International Airport Pvt Ltd 10

Global airport operator that offers airport management services including terminal and traffic management, baggage and cargo handling, aviation

ground handling

Malaysia Airports Holdings Berhad

Delhi International Airport Pvt Ltd 10 Operates and manages 38 commercial airports in

Malaysia Hyderabad International Airport Pvt Ltd

11

25 25

Contents

Advantage India

Market overview and trends

Growth drivers

Success stories: Delhi, Mumbai

Opportunities

Useful information

For updated information, please visit www.ibef.org

Airports NOVEMBER

2011

26 26 For updated information, please visit www.ibef.org SUCCESS STORIES: DELHI, MUMBAI

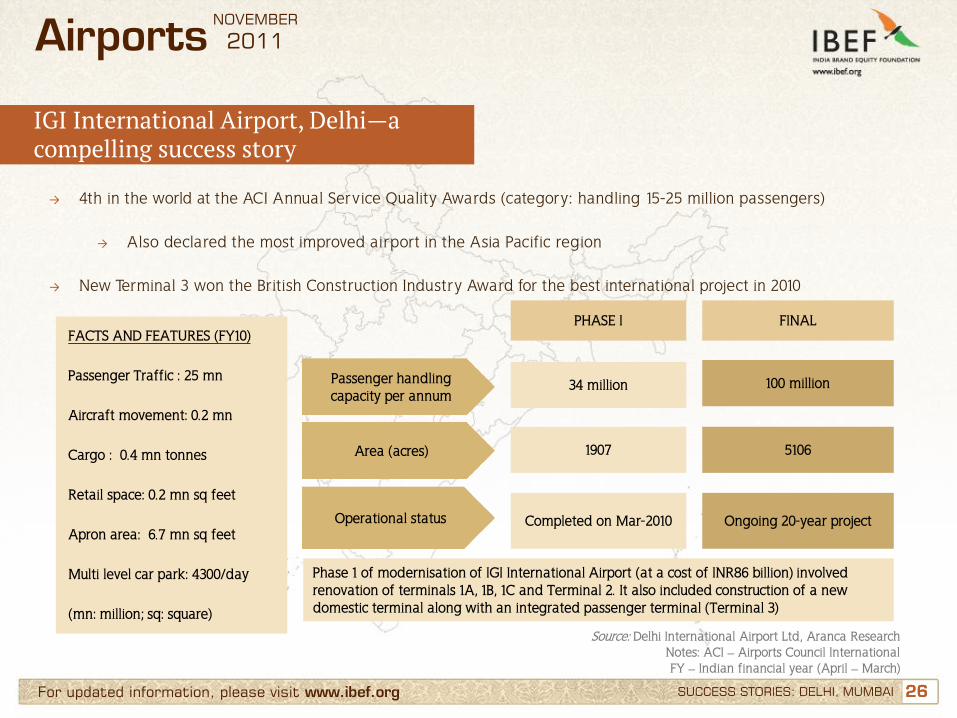

IGI International Airport, Delhi—a compelling success story

→ 4th in the world at the ACI Annual Service Quality Awards (category: handling 15-25 million passengers)

→ Also declared the most improved airport in the Asia Pacific region

→ New Terminal 3 won the British Construction Industry Award for the best international project in 2010

Source: Delhi International Airport Ltd, Aranca Research Notes: ACI – Airports Council International

FY – Indian financial year (April – March)

Airports NOVEMBER

2011

PHASE I

Operational status Completed on Mar-2010 Ongoing 20-year project

Area (acres) 1907 5106

Passenger handling capacity per annum

34 million 100 million

FINAL FACTS AND FEATURES (FY10)

Passenger Traffic : 25 mn

Aircraft movement: 0.2 mn

Cargo : 0.4 mn tonnes

Retail space: 0.2 mn sq feet

Apron area: 6.7 mn sq feet

Multi level car park: 4300/day

(mn: million; sq: square)

Phase 1 of modernisation of IGI International Airport (at a cost of INR86 billion) involved renovation of terminals 1A, 1B, 1C and Terminal 2. It also included construction of a new domestic terminal along with an integrated passenger terminal (Terminal 3)

27 27 For updated information, please visit www.ibef.org

CSI International Airport —harnessing the power of PPP

Airports NOVEMBER

2011

→ 1st in India for 2Q10 at the ACI Annual Service Quality Awards (category: handling > 15 million passengers)

→ Also ranked 4th in the world for 2Q10 in the 15-25 million passenger category

→ 23rd across all categories among a survey of 146 international airports in 2Q10

Passenger handling capacity per annum

Cargo handling capacity per annum

1 million tonnes

40 million

FACTS AND FEATURES

In FY10, CSI handled -

• Passenger traffic: 25.6 million

• Cargo movement: 0.5 million tonnes

• Modernisation of the Mumbai International Airport will entail investments worth INR70 billion over a period of 20 years

• Government of India to provide INR58 billion

• Parts of the project completed till now:

• Phase I (2008): New airport lounges, retail outlets, duty-free shops, temporary cargo facilities, and multilevel car parks

• Phase II (2010): Involved construction of a new terminal at Sahar, a parallel runway, and new cargo facilities

Source: Mumbai International Airport Ltd, Aranca Research Notes: ACI – Airports Council International

2Q10 – Second quarter of 2010

SUCCESS STORIES: DELHI, MUMBAI

28 28

Contents

Advantage India

Market overview and trends

Growth drivers

Success stories: Delhi, Mumbai

Opportunities

Useful information

For updated information, please visit www.ibef.org

Airports NOVEMBER

2011

29 29 For updated information, please visit www.ibef.org OPPORTUNITIES

Opportunities

Airports NOVEMBER

2011

• Indian aviation sector likely to see investments totalling USD150 billion

• GOI expects 64 per cent (of USD7.5 billion) investments in airports during 2007-12 to come from the private sector

• Success of PPP formats will raise investment in existing and greenfield airports

• Growing air traffic and fleet expansion accentuating the need for MRO facilities

• India has only one established third-party MRO currently

• Location advantage - No MRO facility within a 5-hour fly zone of India (nearest ones – West: Dubai; East: Singapore)

• Airport developers can now draw on wider revenue opportunities such as retail, advertising and vehicle parking

• Future operators will benefit from greater operational efficiency due to satellite based navigation systems like ‘Project Gagan’ which is in development phase

Policy support and demand growth unlocking large investment potential

Huge potential to develop India as an MRO hub

Leverage on non-aeronautical revenues, improved technology

Notes: ‘Project Gagan’ is directed towards transitioning from a ground-based navigation system to a satellite-based one. AAI and ISRO are jointly working on this. A Space Based Augmentation System (SABS) will be operational by 2013

MRO – Maintenance, repair and overhaul GOI – Government of India

PPP – Public Private Partnership

30 30

Contents

Advantage India

Market overview and trends

Growth drivers

Success stories: Delhi, Mumbai

Opportunities

Useful information

For updated information, please visit www.ibef.org

Airports NOVEMBER

2011

31 31 For updated information, please visit www.ibef.org USEFUL INFORMATION

Industry Associations

Airports Authority of India (AAI) Rajiv Gandhi Bhawan, Safdarjung Airport, New Delhi –110 003 Phone: 91 11 24632950 Directorate General of Civil Aviation (DGCA) Aurbindo Marg, Opp. Safdarjung Airport, New Delhi –110 003 Phone: 91 11 24622495 Fax: 91 11 24629221 E-mail: [email protected], [email protected]

Airports NOVEMBER

2011

32 32 For updated information, please visit www.ibef.org

Glossary

→ AAI: Airports Authority of India

→ ACI: Airport Council International

→ CAGR: Compound Annual Growth Rate

→ FDI: Foreign Direct Investment

→ FY: Indian Financial Year (April to March) → So FY10 implies April 2009 to March 2010

→ GOI: Government of India

→ INR: Indian Rupee

→ MRO: Maintenance, repair and overhaul

→ PPP: It could denote two things (mentioned in the presentation accordingly) –

→ Purchasing Power Parity (used in calculating per-capita GDP – slide 12, GROWTH DRIVERS) → Public Private Partnership (a type of joint venture between the public and private sectors)

→ USD: US Dollar

→ Conversion rate used: USD1= INR 48

→ Wherever applicable, numbers have been rounded off to the nearest whole number

USEFUL INFORMATION

Airports NOVEMBER

2011

33

India Brand Equity Foundation (IBEF) engaged Aranca to prepare this presentation and the same has been prepared by Aranca in consultation with IBEF. All rights reserved. All copyright in this presentation and related works is solely and exclusively owned by IBEF. The same may not be reproduced, wholly or in part in any material form (including photocopying or storing it in any medium by electronic means and whether or not transiently or incidentally to some other use of this presentation), modified or in any manner communicated to any third party except with the written approval of IBEF. This presentation is for information purposes only. While due care has been taken during the compilation of this

presentation to ensure that the information is accurate to the best of Aranca and IBEF’s knowledge and belief, the content is not to be construed in any manner whatsoever as a substitute for professional advice. Aranca and IBEF neither recommend nor endorse any specific products or services that may have been mentioned in this presentation and nor do they assume any liability or responsibility for the outcome of decisions taken as a result of any reliance placed on this presentation. Neither Aranca nor IBEF shall be liable for any direct or indirect damages that may arise due to any act or omission on the part of the user due to any reliance placed or guidance taken from any portion of this presentation.

Disclaimer

For updated information, please visit www.ibef.org DISCLAIMER

Airports NOVEMBER

2011