air transport and equipment market review & outlook for...

TRANSCRIPT

Slide 1

Dublin, January 17th 2017

Air transport and equipment market

Review & outlook for 2017

Slide 2

Disclaimer

This presentation was prepared by DVB Bank SE (“DVB”) exclusively for the benefit and internal use of the addressee mentioned on the cover page. Neither this

presentation nor any of its contents may be used by any other party or for any other purpose without the prior written consent of DVB. The oral commentary from DVB

accompanying this presentation is an integral part of the presentation and the presentation is not complete without such commentary.

This material is for distribution only under such circumstances as may be permitted by applicable law. It has no regard to the specific investment objectives, financial

situation or particular needs of any recipient. It is published solely for informational purposes and is not to be construed as a solicitation or an offer to buy or sell any

securities or related financial instruments. The contents of this presentation should not be treated as advice relating to legal, tax or investment matters.

No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it

intended to be a complete statement or summary of the securities, markets or developments referred to in the presentation. Any opinions expressed in this presentation

are subject to change without notice and DVB is not under any obligation to update or keep current the information contained herein or communicate any updates to the

addressee mentioned on the cover page. In particular, the information in this presentation reflects prevailing conditions and our views as of this date, all of which are

subject to change. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of information

available to us from public sources.

Furthermore, neither DVB nor any of its affiliates, directors, employees or agents accept any liability for any loss or damage arising out of the use of all or any part of this

presentation.

In the UK, DVB is regulated in the conduct of its investment business by the Financial Conduct Authority. In the United States of America, DVB acts through DVB Capital

Markets LLC, which is a broker dealer registered with the U.S. Securities and Exchange Commission and admitted by the Financial Industry Regulatory Authority to

conduct securities business in the U.S.

Forward looking statements:

Statements made in this presentation, other than statements of historical fact, are forward-looking statements that involve risks and uncertainties. These statements relate

to future aircraft deliveries, growths of the air transportation market and the aircraft leasing market. In some cases, forward-looking statements can be identified by

terminology such as “may”, “will”, “should”, “expect”, “anticipate”, “intend”, “plan”, “believe”, “estimate”, “potential”, “continue”, “outlook”, “could”, “target”, “project”, “seek”,

“may”, “assume”, the negative of these terms or other comparable terminology. Actual results, and actual events that occur, may differ materially from those projected in

any forward-looking statement as a result of certain risks and uncertainties.

You are cautioned not to place undue reliance on forward-looking statements, which speak only as of the date of this presentation and are based on information currently

and reasonably known to us. Except as required by law, we undertake no obligation to update or revise any forward-looking statements, whether as a result of new

information, future events or otherwise.

Slide 3

Four-cycle model – Background

The “Industry Cycle”

determines the demand for

seat (RPK) and cargo (FTK)

capacity. This “demand” can

be compared to the “supply”

side (ASK and AFTK) to

determine/project shortage

or surplus situations

The “Technology Cycle”

determines how competitive

an aircraft is. A more

competitive design (same

payload/range category) can

severely undermine value

and remarket ability (A340

vs. 777). A successor may

also impact the value curve

(“last of the line” effect)

Increasingly aircraft

transactions take place

between “financially driven”

parties (lessors, investors)

vs. the traditional “airline-to-

airline” model. The state of

the finance market conse-

quently is very important

For investors/financiers the

end-of-lease conditions are

increasingly important. Is the

aircraft under a FHA, Return

Conditions or does the lessor

have access to Maintenance

Reserves?

Avia

tio

n i

nd

us

try

Cyc

leTyp

e T

ec

hn

olo

gy C

yc

leA

/c M

ain

ten

an

ce

Cyc

leF

ina

nc

ing

Cyc

le

increasingly important for "mid live investors“ very high

peaked new generation gaining momentum

Slide 4

The global economic environment – Improving slightly

3.43.2

3.1

3.4

1.92.1

1.61.8

4.6

4.04.2

4.6

3.9

2.6

2.3

3.8

2014 2015 2016 2017

World output Output advanced economies Output emerging markets World trade volume

IMF – Macro-economic projections (Y-o-Y growth)

Source: IMF – World Economic Outlook October 2016

[%]

5

4

3

2

1

0

Slide 5

Towards an era of de-globalisation/protectionism?Global trade vs. global production

Source: CPB World Trade Monitor

20

15

10

5

0

-5

-10

-15

-20

-25

Ja

n-0

1

Ju

l-0

1

Ja

n-0

2

Ju

l-0

2

Ja

n-0

3

Ju

l-0

3

Ja

n-0

4

Ju

l-0

4

Ja

n-0

5

Ju

l-0

5

Ja

n-0

6

Ju

l-0

6

Ja

n-0

7

Ju

l-0

7

Ja

n-0

8

Ju

l-0

8

Ja

n-0

9

Ju

l-0

9

Ja

n-1

0

Ju

l-1

0

Ja

n-1

1

Ju

l-11

Ja

n-1

2

Ju

l-1

2

Ja

n-1

3

Ju

l-1

3

Ja

n-1

4

Ju

l-1

4

Ja

n-1

5

Ju

l-1

5

Ja

n-1

6

Ju

l-1

6

World industrial production volume (excl. construction) World merchandise world trade

[%]

Slide 6

0.3

0.5

1.0

1.3

0%

1%

1%

2%

2014 2015 2016 2017

1.5

1.0

0.5

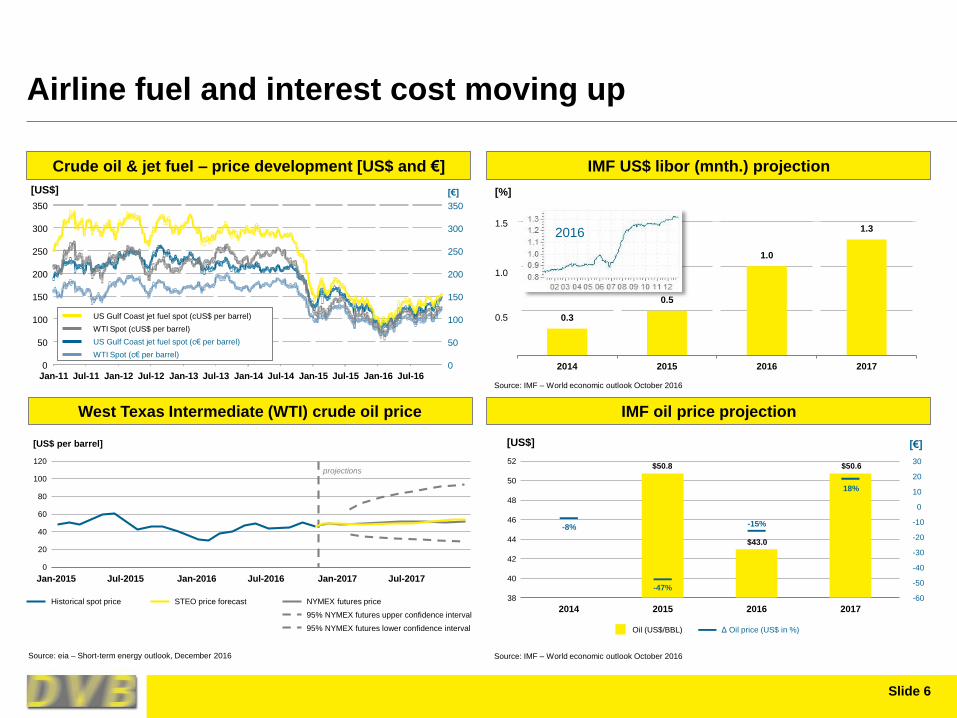

Airline fuel and interest cost moving up

Crude oil & jet fuel – price development [US$ and €]

Source: eia – Short-term energy outlook, December 2016

IMF US$ libor (mnth.) projection

West Texas Intermediate (WTI) crude oil price IMF oil price projection

0

50

100

150

200

250

300

350

0

50

100

150

200

250

300

350

Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16

[€][US$]

US Gulf Coast jet fuel spot (cUS$ per barrel)

WTI Spot (cUS$ per barrel)

US Gulf Coast jet fuel spot (c€ per barrel)

WTI Spot (c€ per barrel)

[US$ per barrel]

0

20

40

60

80

100

120

Jan-2015 Jul-2015 Jan-2016 Jul-2016 Jan-2017 Jul-2017

projections

STEO price forecast NYMEX futures priceHistorical spot price

95% NYMEX futures lower confidence interval

95% NYMEX futures upper confidence interval

Source: IMF – World economic outlook October 2016

2016

2014 2015 2016 2017

Oil (US$/BBL) Δ Oil price (US$ in %)

-8%

-47%

$50.8

-15%

$43.0

18%

$50.6

40

42

44

46

48

50

52

38 -60

-50

-40

-30

-20

-10

0

10

20

30

[US$]

[%]

Source: IMF – World economic outlook October 2016

[€]

Slide 7

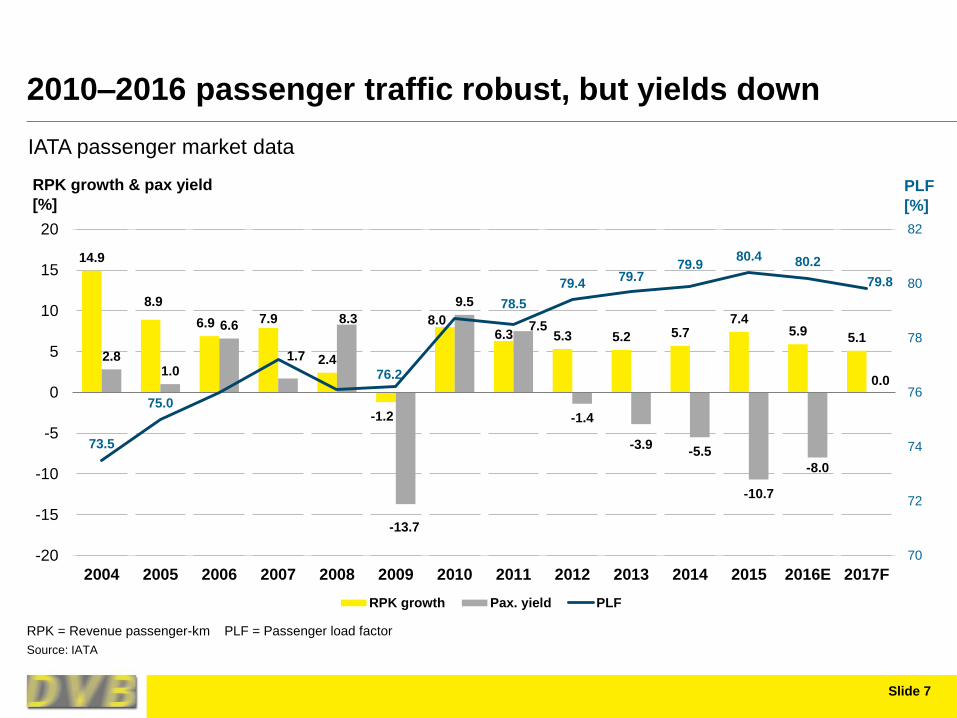

14.9

8.9

6.9 7.9

2.4

-1.2

8.06.3 5.3 5.2 5.7

7.45.9

5.1

2.81.0

6.6

1.7

8.3

-13.7

9.5

7.5

-1.4

-3.9-5.5

-10.7

-8.0

0.0

73.5

75.0

76.2

78.5

79.479.7

79.980.4 80.2

79.8

70

72

74

76

78

80

82

-20

-15

-10

-5

0

5

10

15

20

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017F

RPK growth Pax. yield PLF

2010–2016 passenger traffic robust, but yields down

Source: IATA

IATA passenger market data

[%]

RPK growth & pax yield

[%]

PLF

RPK = Revenue passenger-km PLF = Passenger load factor

Slide 8

11.6

2.3

6.3

4.7

-0.7

-8.8

19.4

0.4

-0.9

0.6

5.0

2.33.4

3.53.9

0.5

4.4 5.67.0

-15.2

14.4

0.8

-4.2 -4.9

-2.0

-17.4

-12.5

0.0

-20

-15

-10

-5

0

5

10

15

20

25

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017F

FTK growth Cargo yield

2011–2016 stagnant freight traffic – 2016 turn-around?

Source: IATA

IATA cargo market data

[%]

FTK = Freight tonne km

Slide 9

2016 YtD – Passenger traffic solid, freight recovering

Source: IATA Air passenger and freight analysis

10

8

6

4

2

0

-2

-4

-6

-8

Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Dec-16

Intra 2016

freight trend

YtD: 6.1%

YtD: 3.2%

RPK FTK

[%]

Traffic volumes

Slide 10

2016 – Peak in the profit cycle?

800

700

600

500

400

300

200

100

0

-1002000

Source: Airline Monitor; ICAO; for 2014/15/16 IATA

Op. income Net income Airline revenue Airline expenses

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E

701

718

35.3

35.6

[US$ mn]

World airline financial results

Slide 11

-0.8

0.3 0.9

7.3 7.50

20.3

35.5

-9.6

1.1

4.45.5

7.84

22.4

9.4

-15

-10

-5

0

5

10

15

20

25

30

35

40

Africa Latin America Middle East Asia/Pacific Europe North America Global

Net profit 2016F Net profit per passenger 2016F

2016 – Profitability mainly for North American Airlines

Source: IATA (Ec. performance December 2016)

[US$ bn]

IATA – Net airline profit – (post tax) per region

Slide 12

-5,6-4.1 -5.0

14.7

-26.1

-4.6

17.3

8.39.2 10.7

13.7

35.3 35.6

29.8

840

1,8732,033

2,421

1,420

652

1,354

2,561

2,331

3,534 3,551

2,3642,175

0

500

1000

1500

2000

2500

3000

3500

4000

-30

-20

-10

0

10

20

30

40

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017F

Net airline profit* Western built jet orders (civil operators)**

Airline profits driven by low fuel – Orders down 2015/16

Source: * IATA "Economic performance of the airline industry (December 2016), ** Ascend fleets (January 2017)

[US$ mn]

Net airline profits vs. commercial jet orders

[Number]

Slide 13

Lessor‘s share remains stagnant at high level (39%)

Source: Flightglobal/Ascend; West.B.Jets, all civil opserators

Lessor % in global jet fleet Lessor % in jets on order

45

40

35

30

25

20

15

10

5

01970 1975 1980 1985 1990 1995 2005 2010 20152000

39.1%

18.3%

[%]

Lessor share in global commercial jet fleet/orders

Slide 14

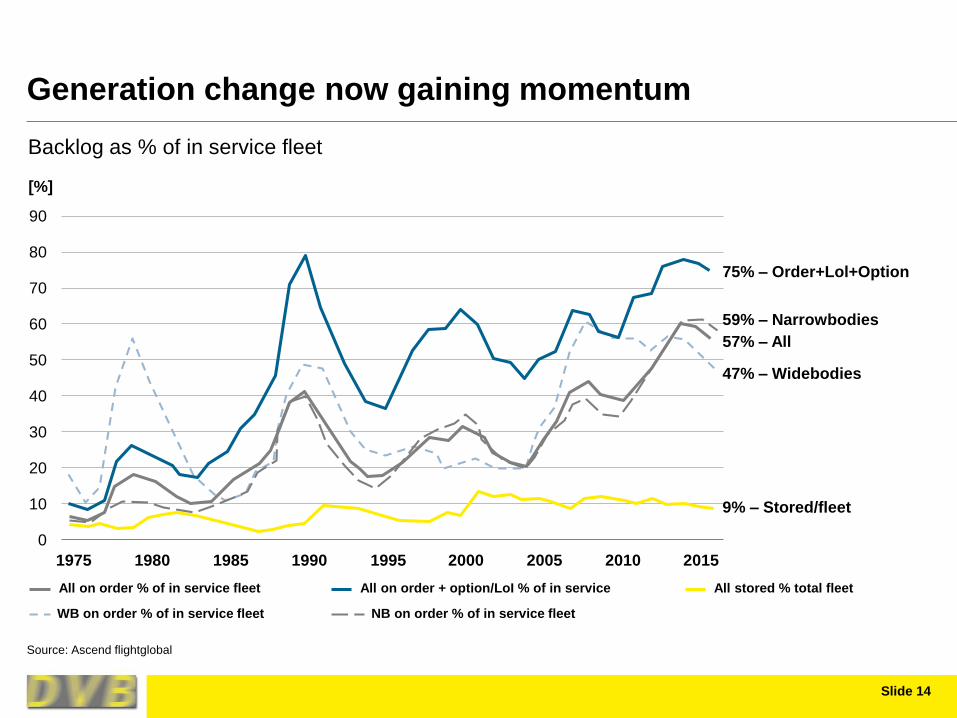

Generation change now gaining momentum

Source: Ascend flightglobal

90

80

70

60

50

40

30

20

10

0

1975

75% – Order+Lol+Option

59% – Narrowbodies

57% – All

47% – Widebodies

9% – Stored/fleet

1980 1985 1990 1995 2000 2005 2010 2015

All stored % total fleet

WB on order % of in service fleet

All on order % of in service fleet All on order + option/LoI % of in service

NB on order % of in service fleet

[%]

Backlog as % of in service fleet

Slide 15

The 2016 Numbers – Published net orders

Source: Press releases

A320CEO 46

A320NEO 561

NB: 607

A330CEO 41

A330NEO 42

A350 41

A380 0

WB: 124

731

Deliveries 688

Book/Bill 1,06

Cancellations 2016 218

Backlog 31/12 6874

Cancellation as % backlog 3.17%

737NG 16

737MAX 534

NB: 550

767 26

787 58

777CG 17

777X 0

747 17

WB: 118

668

Deliveries 748

Book/Bill 0,89

Cancellations 2016 180

Backlog 31/12 5715

Cancellation as % backlog 3.15%

Slide 16

231

785

136

540

405

80 51 64

32 23 129 21 10 7 2 18 10

500

1000

1500

2000

2500

3000

3500

4000

4500

Order Intake 2012 - 2016 (Western Jet, All Civil Ops.)Source : Ascend (data incl. "type swaps")

2012 2013 2014 2015 2016

Recent order intake per aircraft family

Source: Ascend (data incl. "type swaps")

Gross Orders

(incl. type

swaps) 2012 2013 2014 2015 2016

Backlog

31/12/16

A320CEOFam 278 435 496 146 231 653

A320NEOFam 407 830 1050 941 785 4992

737NG 217 469 265 234 136 837

737MAX 908 699 900 412 540 3605

E-Jets E1 69 203 69 126 40 185

E-Jets E2 0 150 60 57 5 272

787 36 181 49 99 80 700

A350 40 239 57 16 51 754

A330CEO 68 54 48 103 64 145

A330NEO 0 0 120 52 32 204

777 Current 75 55 54 38 23 134

777X 0 66 220 20 0 306

CSeries 15 25 61 0 129 353

CRJ 67 36 47 27 21 61

MRJ 100 0 26 32 10 233

767 22 2 4 49 7 70

A380 8 50 20 3 2 112

747 7 17 2 6 18 28

Others 14 23 3 3 1 15

2331 3534 3551 2364 2175 13659

Order intake 2012–2016 (western jet, all civil operators)

Slide 17

2016 – Equipment highlights & concerns

A320 family selling well and gaining market share vs. 737NEO. A319 marginalised and A321 taking increasing share of

orders. Significant number of A320CEO cancellations/type swaps.

737MAX selling well but slowly falling behind A320 family. Main difference seems the lack of a 737MAX10X (so far) to

compete against the A321NEO. Dilemma: a simple stretch or a more radical redesign (commonality?). 737MAX 7+ still at

risk of being marginalised. Cancellations/type swaps for 737NG.

E-Jets E2 still outsold by the E1, in particular by the 175-E1. Concerns about 175-E2 not meeting MTOW limits under US

Scope Clauses. E175-E1 the “fall-back” that MRJ may be missing, facing similar issues.

787 and A350 selling well by Twin Aisle standards with focus on 787-9 and A350-900. A350-800 “exit” and 787-8 heading in

same direction. 787-10 and A350-1000 not yet too convincing. Will a A350-”2000” be convincing as Airbus’ largest twin

aisle (apart from the struggling A380)?

A330CEO still doing well after having been given more range. A-300 still a credible aircraft. A330-800 seems to follow the

A350-800, -900 not a very convincing order-book yet.

777X order intake stalling but still time to bounce back. 777-300ER had to face the inevitable production cut. 777F the

leading long haul plane in this niche market.

CSeries had excellent 2016 in terms of – much needed – orders. Has to maintain momentum/profitability.

Will the MRJ be inspired by the recovery of the Cseries? Advanced plane but needs some credible orders.

747-8F got some crucial orders. 747-8I nearing the end. Program profitability impacted by Airforce One discounting?

A380 further in the danger-zone.

Slide 18

Outlook 2017 – Softening but no “doom & gloom“

According to IMF global economy heading for fragile continuation of the recovery. Event risk omni-present.

CPB data suggest de-globalisation (production growth > trade growth). Production technology (robotisation) and

protectionism? Long term risk!

Fuel slowly moving up, rising interest rates, labor cost increasing – airline profitability under pressure.

Ticket prices to increase, potentially reducing passenger traffic growth. Cargo recovering, beyond the Hanjin effect.

More order deferrals/cancellations in selected regions. Order slump to continue in 2017.

Programs that have not built strong backlog in 2013/14 may struggle to gain momentum.

Money remains plentiful, even without EXIM/ECA

Investors may be disappointed by residual value of selected twin aisle. No major impact expected yet of the last-of-the-line

effect, but… Big difference remarketability aircraft on lease or naked.

Will we see in 2017 :

‒ MAX 10 (yes)

‒ A350-2000 (no)

‒ CS500 (no)

‒ 777-10X (no)

‒ C919 making first flight (yes)

Slide 19

THANK YOU