agricultural trade today the eu position in the current

TRANSCRIPT

Willi Schulz-Greve European Commission DG Agriculture and Rural Development

Agricultural trade today – the EU position in the current market situation

European Economic and Social Committee Group III Seminar, Helsinki, 7 July 2015

Outline

• EU agri-food trade – current picture

• Latest development - Russian embargo

• actions to mitigate Russian embargo

• EU trade policy – future perspectives

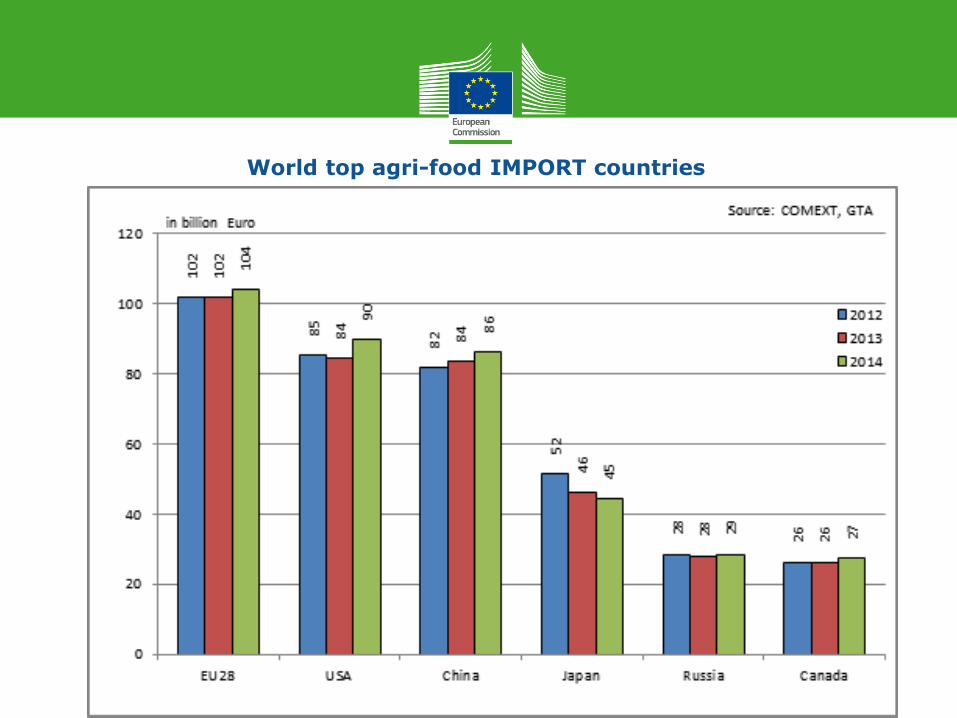

World top agri-food IMPORT countries

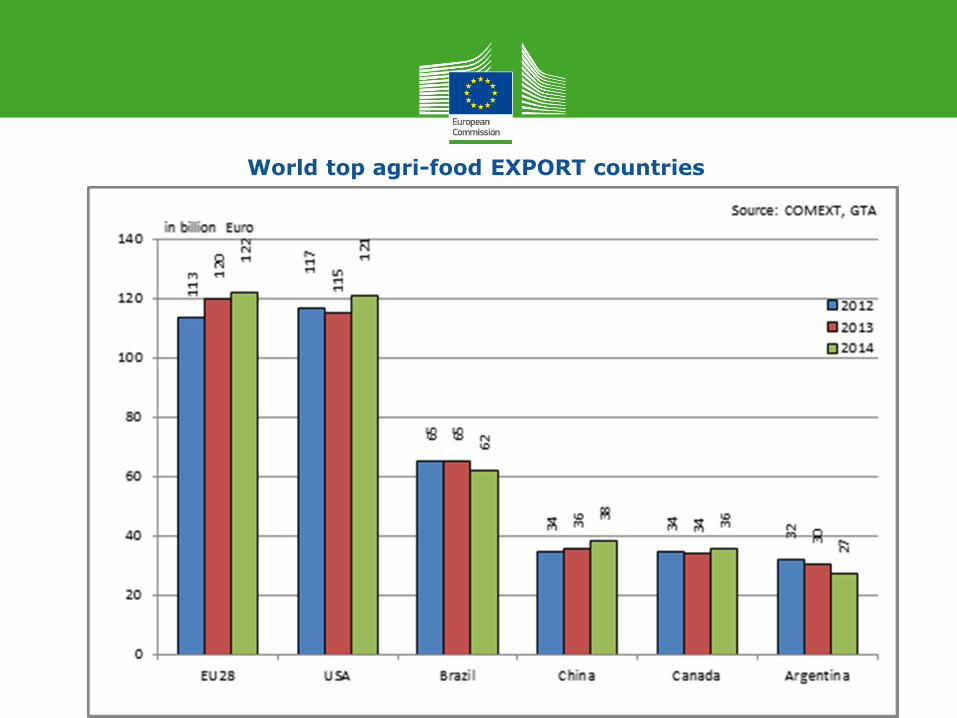

World top agri-food EXPORT countries

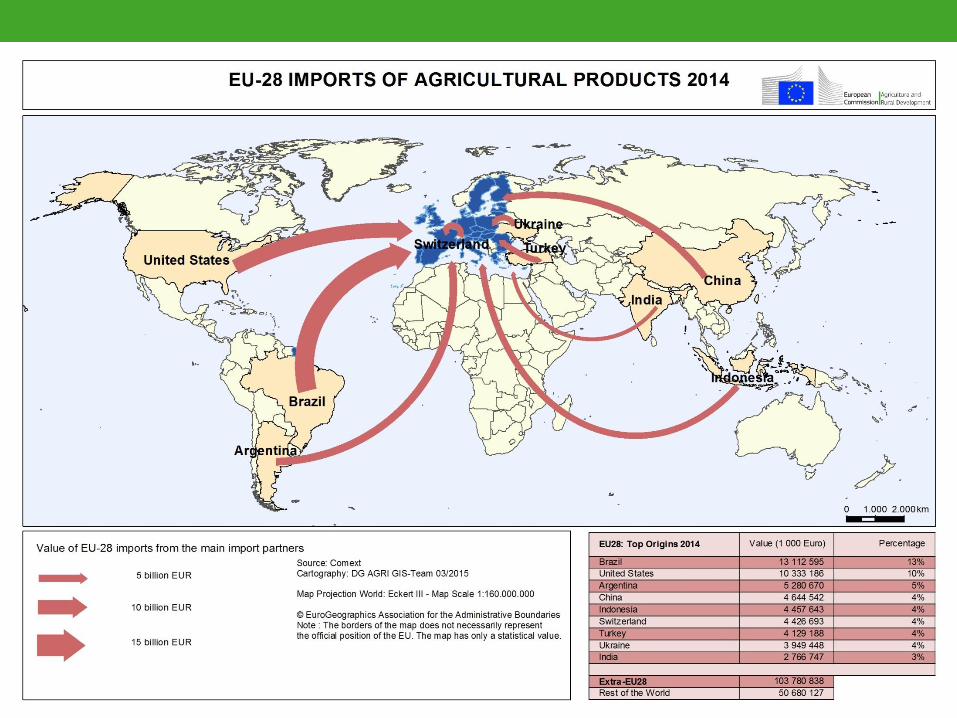

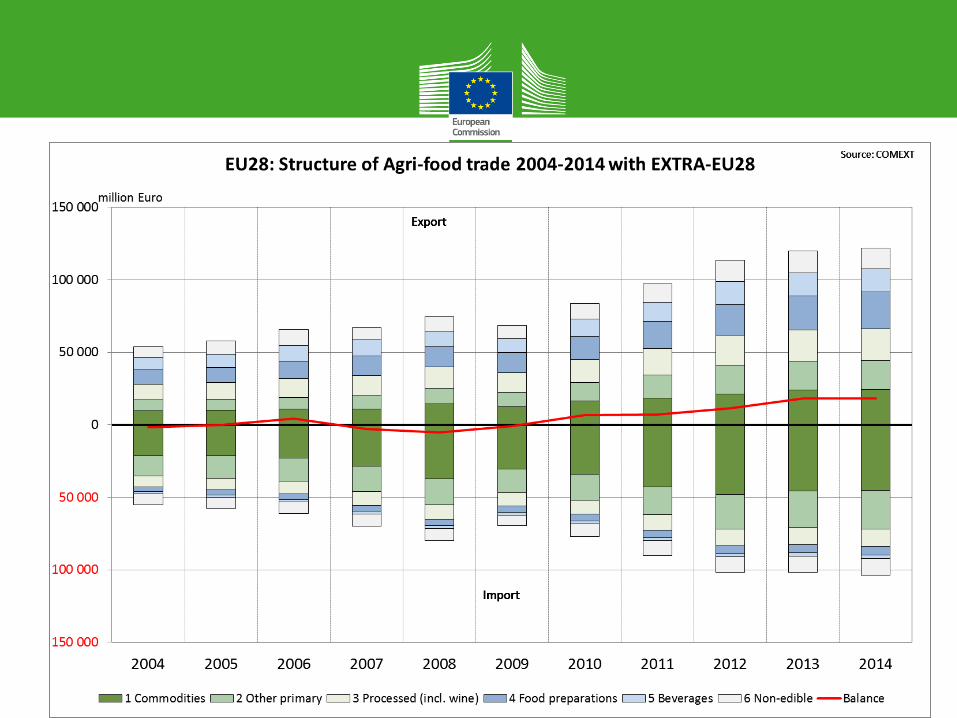

EU trade in agri-food products

• EU is leading importer and since 2013 leading exporter

• More than 7% of all EU exports are in agri-food

• The EU is competitive in a wide range of products

• The net surplus in agri-food exports in 2014 was €18 billion (all EU exports € 22 billion)

• Growing opportunities on global markets

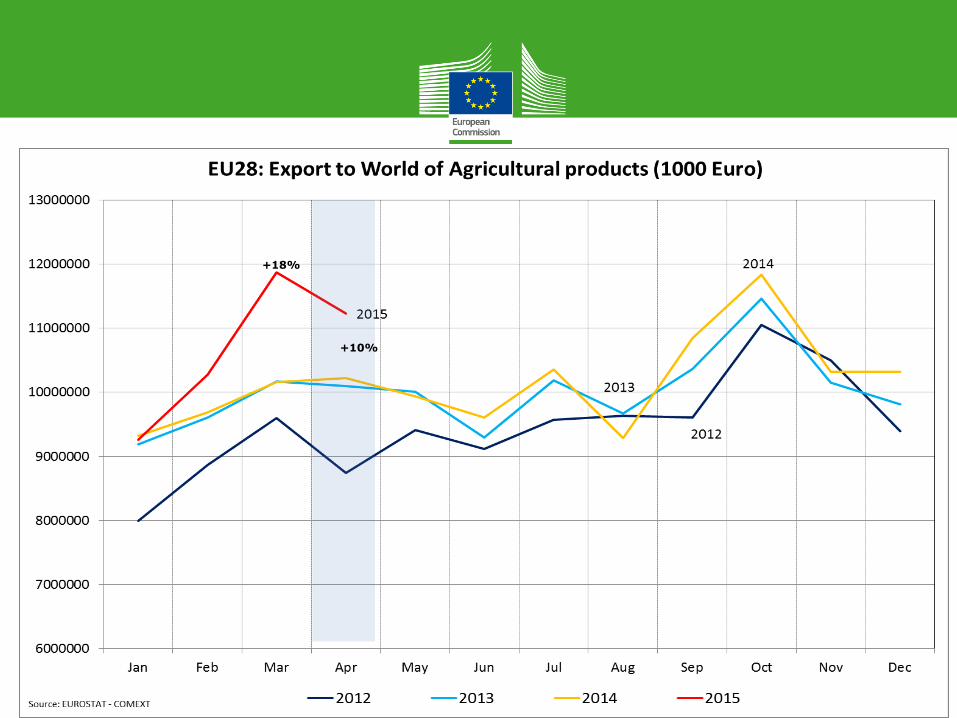

Latest Developments – Russian Embargo

+10%

+18%

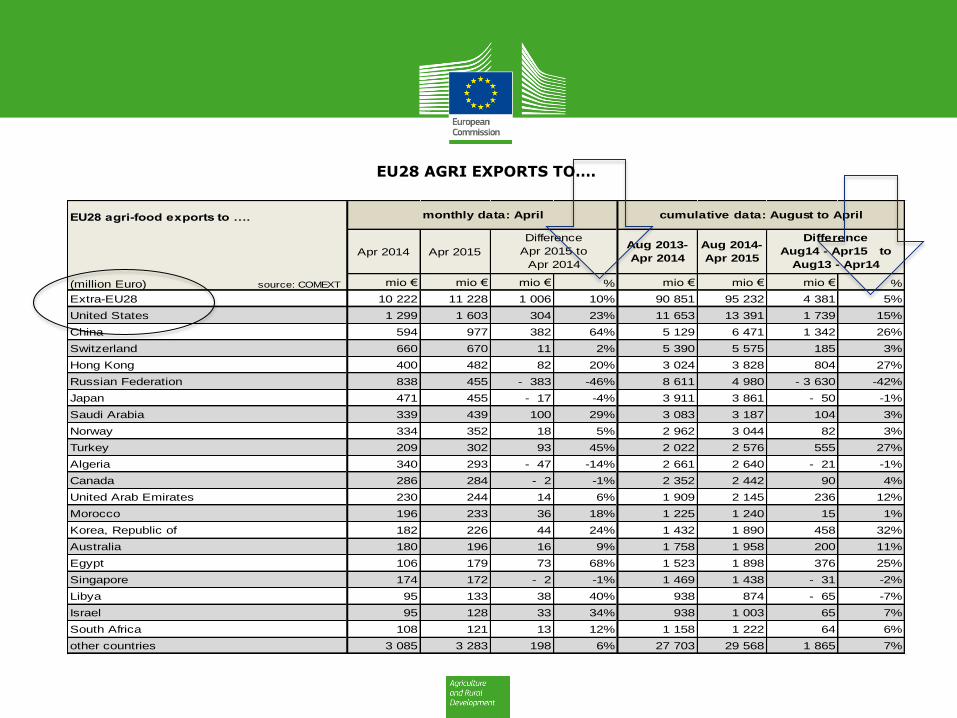

Apr 2014 Apr 2015Aug 2013-

Apr 2014

Aug 2014-

Apr 2015

mio € mio € mio € % mio € mio € mio € %

Extra-EU28 10 222 11 228 1 006 10% 90 851 95 232 4 381 5%

United States 1 299 1 603 304 23% 11 653 13 391 1 739 15%

China 594 977 382 64% 5 129 6 471 1 342 26%

Switzerland 660 670 11 2% 5 390 5 575 185 3%

Hong Kong 400 482 82 20% 3 024 3 828 804 27%

Russian Federation 838 455 - 383 -46% 8 611 4 980 - 3 630 -42%

Japan 471 455 - 17 -4% 3 911 3 861 - 50 -1%

Saudi Arabia 339 439 100 29% 3 083 3 187 104 3%

Norway 334 352 18 5% 2 962 3 044 82 3%

Turkey 209 302 93 45% 2 022 2 576 555 27%

Algeria 340 293 - 47 -14% 2 661 2 640 - 21 -1%

Canada 286 284 - 2 -1% 2 352 2 442 90 4%

United Arab Emirates 230 244 14 6% 1 909 2 145 236 12%

Morocco 196 233 36 18% 1 225 1 240 15 1%

Korea, Republic of 182 226 44 24% 1 432 1 890 458 32%

Australia 180 196 16 9% 1 758 1 958 200 11%

Egypt 106 179 73 68% 1 523 1 898 376 25%

Singapore 174 172 - 2 -1% 1 469 1 438 - 31 -2%

Libya 95 133 38 40% 938 874 - 65 -7%

Israel 95 128 33 34% 938 1 003 65 7%

South Africa 108 121 13 12% 1 158 1 222 64 6%

other countries 3 085 3 283 198 6% 27 703 29 568 1 865 7%

EU28 agri-food exports to ….

(million Euro) source: COMEXT

Difference

Apr 2015 to

Apr 2014

Difference

Aug14 - Apr15 to

Aug13 - Apr14

monthly data: April cumulative data: August to April

EU28 AGRI EXPORTS TO….

Source: GTA

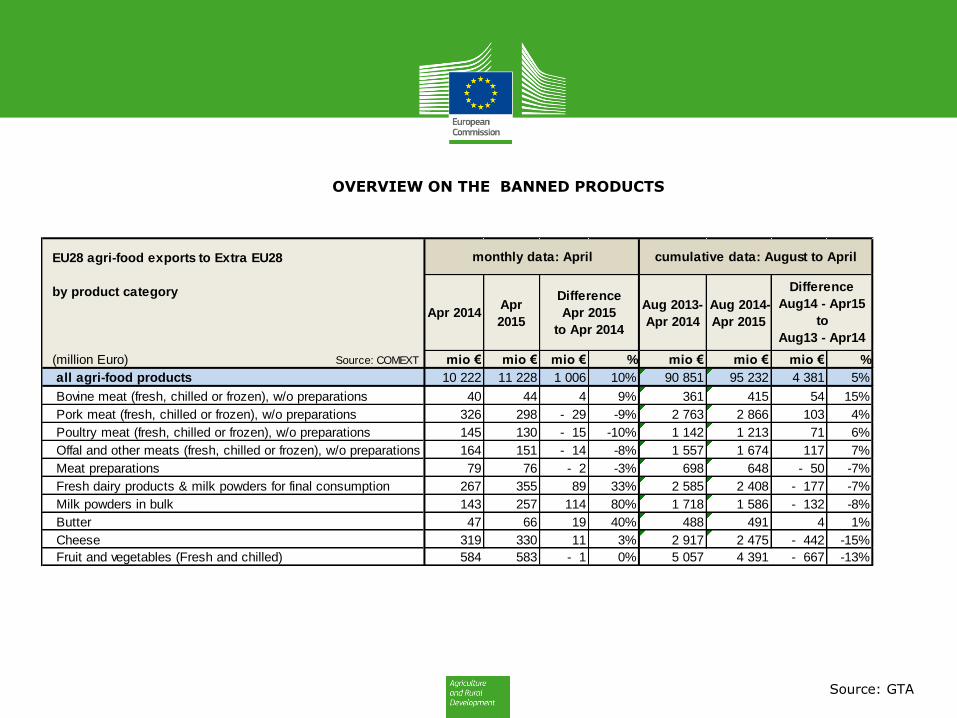

OVERVIEW ON THE BANNED PRODUCTS

Apr 2014Apr

2015

Aug 2013-

Apr 2014

Aug 2014-

Apr 2015

mio € mio € mio € % mio € mio € mio € %

all agri-food products 10 222 11 228 1 006 10% 90 851 95 232 4 381 5%

Bovine meat (fresh, chilled or frozen), w/o preparations 40 44 4 9% 361 415 54 15%

Pork meat (fresh, chilled or frozen), w/o preparations 326 298 - 29 -9% 2 763 2 866 103 4%

Poultry meat (fresh, chilled or frozen), w/o preparations 145 130 - 15 -10% 1 142 1 213 71 6%

Offal and other meats (fresh, chilled or frozen), w/o preparations 164 151 - 14 -8% 1 557 1 674 117 7%

Meat preparations 79 76 - 2 -3% 698 648 - 50 -7%

Fresh dairy products & milk powders for final consumption 267 355 89 33% 2 585 2 408 - 177 -7%

Milk powders in bulk 143 257 114 80% 1 718 1 586 - 132 -8%

Butter 47 66 19 40% 488 491 4 1%

Cheese 319 330 11 3% 2 917 2 475 - 442 -15%

Fruit and vegetables (Fresh and chilled) 584 583 - 1 0% 5 057 4 391 - 667 -13%

EU28 agri-food exports to Extra EU28

by product category

(million Euro) Source: COMEXT

monthly data: April cumulative data: August to April

Difference

Apr 2015

to Apr 2014

Difference

Aug14 - Apr15

to

Aug13 - Apr14

Latest Developments – Russian Embargo

• Total EU agri-food exports increased

• Exports to Russia down by more than 40%

• Cheese, fruit and vegetables most affected

• Some Member States much stronger affected than others

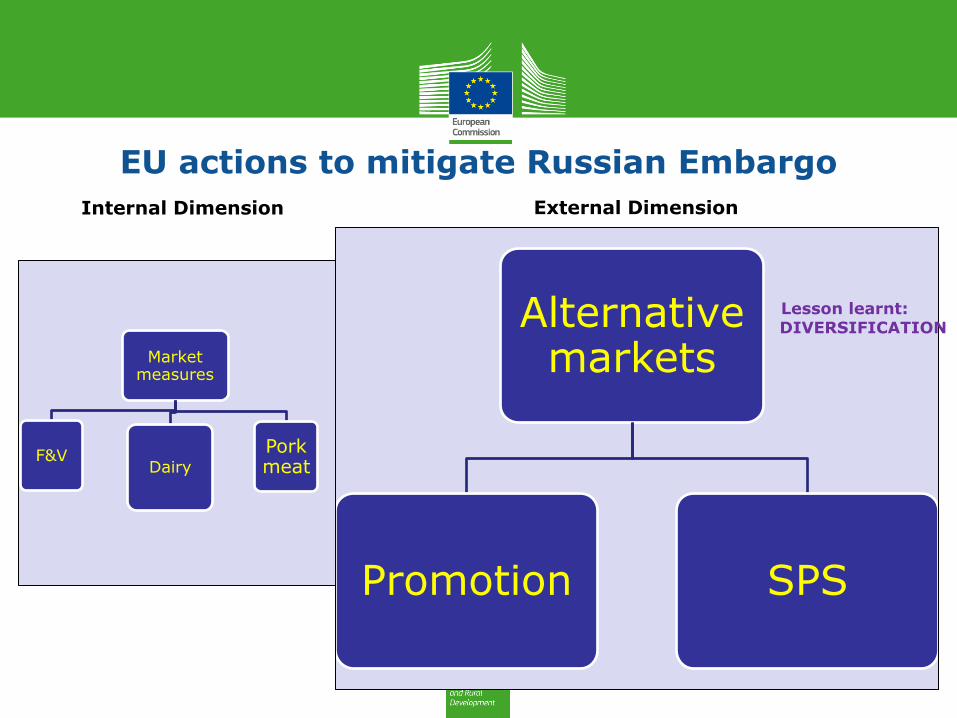

Internal Dimension

Alternative markets

Promotion SPS

External Dimension

Lesson learnt: DIVERSIFICATION

Market measures

F&V Dairy

Pork meat

EU actions to mitigate Russian Embargo

MARKET MEASURES

•FRUIT AND VEGETABLE MEASURES

•PRIVATE STORAGE FOR CERTAIN DAIRY PRODUCTS

•SPECIAL MILK PACKAGE FOR BALTIC COUNTRIES

•PRIVATE STORAGE FOR PORK MEAT

PROMOTION IN PRIORITY ALTERNATIVE MARKETS:

The reply to the Russian embargo in the current promotion system

The EC increased the budget by 30 million Euro and explored potential in new destinations, which resulted in:

•remarkable increase in applications!

•very steep increase in financing granted!

•proportion Third Countries vs. Internal Market almost reversed! - from around 1/3 previously to 60% now

•significant diversification of target destinations!

PROMOTION IN PRIORITY ALTERNATIVE MARKETS–

New promotion policy (as of 1 December 2015)

- significant increase of the budget available for promotion

- expansion and diversification of the agricultural exports

SPS BARREERS REMOVAL

• Actions to reduce SPS barriers (priorities)

• Brazil: pork, dairy, bovine

• China: pork, dairy, bovine

• Chile: pork, F&V

• Colombia/Peru: pork, poultry, dairy

• India: pork, poultry, dairy

• Indonesia: F&V

• Mexico: pork, F&V

• Turkey: bovine, poultry, dairy, F&V

• US/Canada: bovine, dairy, F&V

• Vietnam: F&V

SPS FIRST RESULTS

• Turkey: bovine, poultry, dairy, F&V

• US/Canada: bovine, dairy, F&V

more than five fold increase in exports

BSE – bovine meat; pip fruit (Canada)

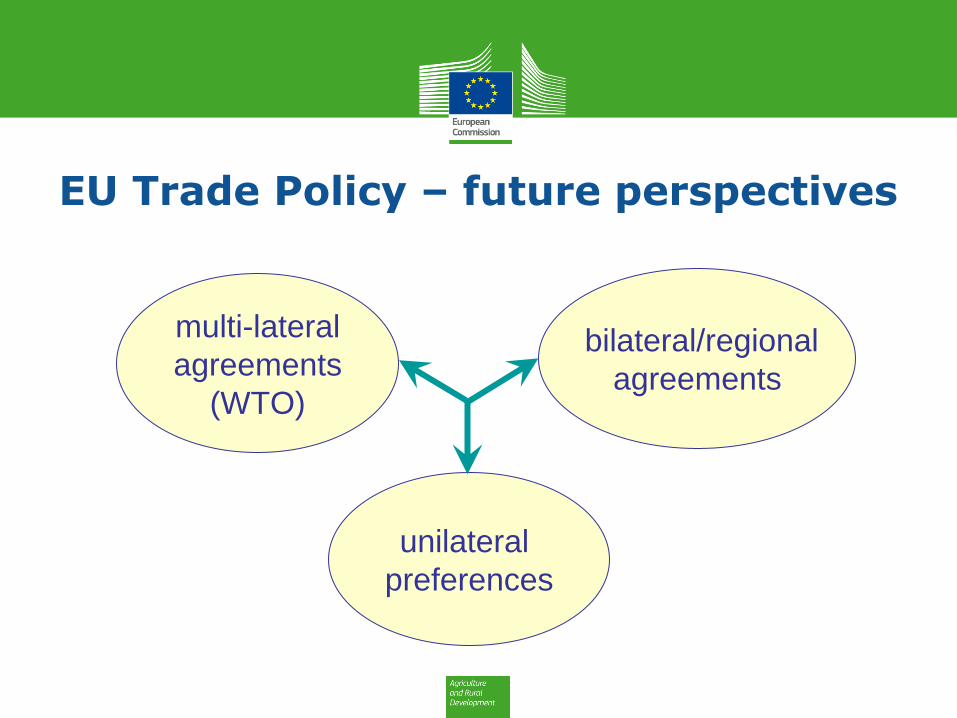

EU Trade Policy – future perspectives

unilateral

preferences

bilateral/regional

agreements

multi-lateral

agreements

(WTO)

Ukraine

Georgia

Ecuador

Moldova

SADC

Free Trade Agreements recently concluded

Singapore West Africa

Canada

Morocco

Col/Peru

Central America

EAC

India

Mercosur

Gulf countries

Bilateral and regional Negotiations launched or planned

Viet Nam

Malaysia

Thailand

Japan

USA

Norway

China GIs

Philippines Mexico

Tunisia

Iceland

Features of recent trade agreements

• “deep and comprehensive”

• ambitious objectives in market access negotiations

• still some sensitive products (tariff quotas)

• geographical indications

• SPS and other non-tariff issues – implementation of agreements

• sustainability chapters, environment, climate change, animal welfare, social standards …