agile financial times apr09

TRANSCRIPT

CCUUSSTTOOMMEERR IINNSSIIGGHHTT

SSOOLLUUTTIIOONN SSPPOOTTLLIIGGHHTT

Managing Liquidity

in Tough Times

Nyasha Makuvise

CEO, CBZ Holdings

Cash is King!

iDeal Liquidity

AgileFINANCIAL TIMES

April

2009

CCUUSSTTOOMMEERR SSPPOOTTLLIIGGHHTT

Leading Asset Management Company

Selects Agile FT

And here it is! Both Spring and our inaugural

issue that you behold at this moment!

We live in interesting times. A period in history

that will be studied for ages to come. There are

lessons to be learnt and for those who can

understand the opportunity within all the

adversity, it’s time to plan for a rewarding future

ahead.

We invite you to be inspired by the "lift of your driving dreams". This is

the time when we should take a relook at our systems and processes,

and prepare for the inevitable upswing ahead.

While an enormous spate of activity takes place round the clock at Agile

FT offices across the world in terms of research, product development

and innovation, we wanted to share some of it with you.

We share the joy that we feel in this initiative as it brings us closer to

you and allows us to chat with you - up close and personal. We invite

you to use this platform to share your own perspective, to reach out and

build partnerships within our community of clients, partners and

principals.

So go ahead and read a little, think a lot, get charged even more and

soar beyond glass ceilings and as you do, remember to drop us a

postcard (or an email will do) to let us know how we fared.

Be Agile!

Shefali Khera

Chief Marketing Officer

Write to us at [email protected]

CONTENTS

Editor’s Note

CUSTOMER INSIGHT

Optimal Insurance SelectsAGILIS 4

COVER STORY

Managing Liquidity inTough Times 6

NEWS

Global Update 9

INTERVIEW

Kalpesh Desai 10

SOLUTION SPOTLIGHT

Cash is King! 14

PARTNER SPOTLIGHT

Making Strides in WestAfrica 16

CUSTOMER SPOTLIGHT

Leading AssetManagement CompanySelects Agile FT 18

April 2009

4

What prompted the recent reorganisation and diversification

of the CBZ Holding Company based on client segments and

how has it impacted growth?

The primary motivation for the reorganisation and

diversification of CBZ Holdings Limited was the need to

provide clients with a ‘one-stop shopping experience’. This

meant providing a variety of services and products to clients

within a group. The generic financial services model in

Zimbabwe was that of a single service provider and we

endeavour to be unique in this area.

The intent of the innovation initiative was to provide clients

with many products and services within one group, but

through various subsidiaries. This is why we have a 360

degree icon as part of our corporate identity which is aptly

combined with the phrase “all round financial facilitator”.

The other objectives of our reorganisation were the

diversification of income streams, capital and shareholder

value preservation. Diversification of income streams

helped us reduce the shocks of major drops of income in

one line of business. On the other hand due to the hyper

inflationary conditions in the country, it was important to

preserve capital through acquisitions of value holding assets,

for e.g., real estate. We transformed the Zimbabwe dollar

‘trillions’ into land & buildings which held better value. This

helped us to preserve shareholder value and provide us with

steady income.

In what areas has the economic slowdown impacted CBZ

Holding Company, and how has the company maintained a

healthy position despite the economic slowdown?

The CBZ Group is largely a financial services company.

Lending is a major business, with interest income being the

main source of income.

Optimal

Insurance

Selects

AGILIS

Optimal Insurance Company (Pvt) Ltd, asubsidiary of one of Zimbabwe’s largest anddiversified financial services institution - CBZ

Holdings Limited - has shown its commitmentto improving service delivery to its clients by

recently acquiring the rights to implementAGILIS Core Insurance Software from Agile

Financial Technologies. The new system willallow Optimal Insurance to automate all its

existing operations and enable them to quicklycreate new insurance products thereby

reducing time-to-market.

AGILIS covers the entire spectrum ofoperations and finance management for aninsurer including product management and

distribution (policies), underwriting,reinsurance, claims and accounting. Available

with multi-language and multi-currency supportand consolidated financial information on multi-currency transactions, its well-defined workflow

covers all the steps of the insurance businessfrom a single view of the customer profile to

effective management with pre-configuredreports, including MIS.

On this occasion, Nyasha Makuvise, GroupCEO, CBZ Holding Company, shared his

insights on the company and industry, in anexclusive interview to Agile Financial Times.

Nyasha Makuvise, CEO, CBZ Holdings, signs the agreement with Kalpesh Desai, CEO,Agile Financial Technologies. Also see standing (from left to right) are RumbidzayiJakanani, Legal Advisor, CBZ; Munya Mateko, Regional Head - Africa, Agile FT; andTatyana Chernyshova, Business Development Manager, Agile FT.

CUSTOMER INSIGHT

The general economic slowdown and the hyper inflationary

conditions in Zimbabwe seriously and adversely affected the

core business of lending. As a result, financial profitability

was reduced significantly.

The other area that was affected was the stock market.

Within the group we have a stockbroker and an asset

management company. Their operations almost came to a

halt and reduced income flows for the group.

What is your outlook on the banking and financial services

industry in Zimbabwe?

Globally the banking and financial services is in bad shape.

Zimbabwe is, of course, no exception. However, I see a

bright future for our industry as we are poised for a

turnaround. This is mainly because we have been under

sanctions and were somehow insulated from the major

shocks that affected other markets.

As we come out of the isolation with the removal of

sanctions, business should start to improve. Lines of credit

availability should improve and trade will be facilitated. This

will benefit the industry; hence my optimism.

On the other hand, I do believe that some consolidation in

the industry will take place. This will be based on the need

to improve the capital strength of financial institutions.

Outside consolidation, I also believe that acquisitions,

particularly by larger foreign stronger financial institutions,

will take place. This will allow for financial strength and

stability.

Is the insurance business in Zimbabwe growing and what

are the opportunities for Optimal Insurance moving

forward?

Being a service industry the insurance sector has been

negatively affected by recession, mainly due to the political

climate in the country in the past couple of years. However,

we expect business to pick up after the recently pronounced

government of national unity.

The insurance market is a perception-driven market and

hence the recent political settlement creates an opportunity

for us to introduce new and improved products ahead of

competitors during the transition period. Competition in the

industry is based on service delivery and Optimal Insurance

hopes to capitalise on this transition period by being agile

and innovative on new products and services. The pre-

requisites for this are a robust and scalable technology

platform to complement the launch of new products, as well

as superior service delivery by improving document

turnaround.

Group synergies make Optimal Insurance strategically

positioned to significantly grow the bancassurance business.

The company is also looking forward to capturing

agricultural sector business through bancassurance.

A strong shareholder base increases stakeholder confidence

in the company, creating an opportunity for it to increase its

market share.

Do you believe that the current economic scenario will

throw up any significant challenges for CBZ Holding, and if

so, how do you plan to overcome them?

Indeed at no time in recent times has the term ‘global village’

relating to the world been so real. The general world

economic meltdown has affected Zimbabwe and indeed the

CBZ Group. This has mainly been through less borrowings,

hence diminishing opportunities to raise capital. Our main

focus is on lending, so if we cannot get lines of credit it

automatically translates to less business.

Developing economies are also largely commodity-driven.

The slowdown in the world economy reduces trade and

prices of commodities and this adversely affects financial

services.

I believe that this is the time to prepare for a better future,

so that when the good times come we are ready. This is one

of the reasons for focusing on putting the right technology

in place.

Why did you select Agile FT as your technology partner?

In our quest to provide superior service and delivery to our

clients, we needed a technology partner who understands

our business as well as we do. Agile FT met that need

perfectly.

In addition, the quality and experience of the Agile FT team

gives us a significantly high comfort level that the

implementation will go as planned, and that we will be able

to achieve our goals.

5

Competition in the industry is

based on service delivery and

Optimal Insurance hopes to

capitalise on this transition

period by being agile and

innovative on new

products and services.

CUSTOMER INSIGHT

Several banks globally have closed down over the past few months, the primary

reason for the failure of these banks being that their lending activity was much

higher than their deposits permitted. This mismatch between their assets and

deposits led to a shortage of funds for their operating activities. Another

significant reason for the downfall of these banks was the US sub-prime crisis,

which led to a dry up in the securities buyback markets resulting in a severe cash

crunch.

Banks form the backbone of an economy and when they are affected, the entire

economic activity of a country comes to a standstill. Worse, the domino effect

spills over the borders giving rise to the risk of contagion at a global level.

Obviously this is not a desirable situation and banks need to examine the reasons

for this and take concrete steps to ensure that a similar crisis does not recur.

Banking Risks

The traditional activity of a bank involves the business of borrowing (deposits)

and lending (loans). Profits are generated by the cost income arbitrage that a bank

incurs through deposits and loans respectively. Therefore, the primary risks that

a bank faces include credit risk and liquidity risk. The quantum of credit risk

primarily depends on the type of industry and the risks associated with the

industry, which would prevent the borrower from repaying the loans. Liquidity

risk arises out of the inability of the banks to honour their obligations due to

non-availability of liquid funds. This risk is inherent to the general banking

business, and arises out of due course of the banking business. The reason for

6

This article explores

the nature of the

banking business, the

different types of

risks involved in the

banking business,

identification,

measurement and

impact of liquidity

risk, and risk

management systems

that can be set up

to prevent a

liquidity crisis.

Managing Liquidity

in Tough Times

this is the manner in which banks conduct business.

Typically banks lend to customers on a long-term basis and

borrow on a short-term basis, such as from the financial

markets. Thus, they keep assets on their books for a longer

time and provide liquidity in the short term in case of

contingencies as well as to cater to the daily cash

requirements, with the assumption that the business will

continue to refinance itself.

Risk Management

There are a number of risk management systems that can be

used to identify, monitor and control risk:

Firstly, the bank needs to identify liquidity risk by classifying

its balance sheet into two classes:

� Sticky Assets

� Core Assets

Sticky assets refer to those assets that cannot be returned on

demand, For example, fixed assets like building and

computers. Core assets refer to those that can be liquidated

in case of an emergency. For instance, cash with the central

bank, and cash and deposits with peer banks. Clearly, a bank

cannot depend on sticky assets for a bailout in case of a

liquidity crisis. However, a bank can depend on the core

assets for generating cash in case of an emergency. These

core assets should be further classified into CASA (Current

account saving account), collateralized borrowings, long-

term loans and so on.

After classifying the assets, banks need to place risk weights

for each of these assets from highly liquid to less liquid and

illiquid.

Thereafter, banks should set up a maturity matrix for both

assets and liabilities, which helps ascertain the maximum

negative outflow within a period of three to six months.

This maturity matrix should be defined in terms of a cluster

of deterministic items and non-deterministic items.

Deterministic items are liabilities or assets with a fixed

maturity period, interest rate and amount (for example, a

bond with a fixed maturity period, coupon rate and amount).

Non-deterministic are assets or liabilities with unfixed

amounts, interest rates and maturity period (for example,

LIBOR-linked securities, callable bonds and put options).

Once the maturity matrix is set up, the banks should identify

and assess the liquidity attached to various assets and

liabilities on their balance sheets. Banks need to establish

scenarios at various levels (such as at the organizational level,

local bank system level and international level) and test how

these items are affected in a given situation. For example, at

an organizational level when a bank’s current accounts are

being called, deposits are being withdrawn; peer banks or

others hold and cannot offer liquidity, the question to be

asked is how will the bank generate cash for its operations?

At this point of time, the bank should be able to identify its

possible liquidity issues and therefore establish preventive

measures to steer clear of the same. These simulated

scenarios help a bank prepare for contingencies. Similarly,

situations or scenarios for the other levels can be simulated

and tweaked in accordance with the changing environment.

Once the scenarios are identified, banks should put them

through a stress test. Here banks would normally follow two

testing techniques:

� Historical Value at Risk: Historical Value at Risk can be

arrived at using normal distribution and events method

where-in the worst possible scenarios and events are

assumed to have taken place and then its effect on the

liquidity is calculated. Example of such events includes

failure of banks to borrow, dipping share prices etc.

� Balance Sheet Liquidity: Balance Sheet Liquidity puts to

test the bank’s ability to raise finance in a short period of

time. This assumes the shortest period within which

liquid assets can be sold in the market and funds can be

raised from market makers and brokers. In order to

make this possible, banks align the assets in accordance

with the level of their liquidity. Banks refer to the

balance sheet items in terms of the degree of their

liquidity. For example, a committed line from other

banks is considered as a percentage of short term

unsecured obligations. The higher the percentage, the

higher the liquidity.

Based on scenarios and testing techniques, banks can evolve

strategies to ensure that liquidity is available for daily

operations (the amount of negative outflow limits) and on a

long-term basis (align the deposit and asset side with the

long term goals).

Once the strategy is defined, the bank should set up a

Liquidity Continuity Plan (LCP) that can identify points of

cash limit breaches and measure how a bank can resolve the

situation. Banks should establish clearly documented

processes that explain the steps to be followed in case of a

liquidity contingency event.

The LCP should be made known to the large customers,

7

COVER STORY

Most banks and financial

institutions fail due to the

under-pricing of liquidity

risks, rather than a credit

risk due to aggressive selling.

creditors and stakeholders. In case a bank does not do

so, lack of information at the critical time can lead to a

crisis. Banking is a business of confidence and it is

critical that the same 'language' is spoken across various

levels. Lack of synchronisation between various levels

of management and stakeholders can further fuel the

crisis. Hence, it is critical to keep all stakeholders well-

informed.

Taken together, these steps should hold banks in good

stead while managing their liquidity risks proactively.

Conclusion

Liquidity risks have very long-standing effects, not only

for the bank, but for the country and economy as a

whole. Hence central governments of many countries

step in to bail out ailing banks in a liquidity crisis

scenario. However, banks should not use this as a

safety net and fall prey to the moral hazard it poses.

Liquidity risk negatively impacts both sides of a bank's

balance sheet, the assets and the liabilities. Assets are

affected, as bank's borrowers default in repayment of

loans resulting in a funds shortage. Similarly, liabilities

are impacted because depositors do not invest in a

bank that is facing a liquidity crisis.

Most banks and financial institutions fail due to the

under-pricing of liquidity risks, rather than a credit risk

due to aggressive selling. Regulators and the

government need to ensure that financial institutions

maintain a sufficient level of liquidity to meet sectoral

needs and sustain the level of liquidity in the market.

8

COVER STORY

LIQUIDITY RISKS

The recent fallout of major banks re-iterated the fact thatliquidity risk has a strong bearing on the world economy.

Structured Liquidity Risk (SLR) is defined as a riskundertaken in a conscious manner to generate cash andmaintain assets on a long-term basis. It is termed ‘structured’because it is well-known and it is undertaken in a plannedmanner. For example, banks need to pay taxes on a specificdate, and earmark a certain portion of their funds for this.

Contingent Liquidity Risk (CLR) is concerned with assetsand liabilities of a bank that typically have a long-term maturity,some examples of which include term deposits, offshoreproducts and guarantees. Although this is part of the dailybanking business, the possibility of these getting liquidatedprior to their maturity poses significant liquidity risk. Forexample, a term deposit with a maturity of five years may beliquidated by the depositor at the end of the third year.Similarly for offshore products like guarantees, if called uponat any point in time, the bank has to honour the financialobligations. When banks fail to honour their financialobligations, it can result in consequences like bad publicity, runon banks, breach of depositors trust, and degradation of thebank’s credit rating. Numerous situations of the same type cangive rise to shortage of funds. Such cases occur when there isa high amount of market volatility, which gives rise to marketliquidity risk.

Market Liquidity Risk (MLR) is the third type of risk andworks on the assumption that markets operate in a normalcondition and have sufficient liquidity levels. In case money isinsufficient in the market, it results in shortage of funds andeventually leads to a collapse of the financial system. Forexample, most banks undertake inter-bank lending andborrowing activities, which allows them to avail money to fulfiltheir financial needs. However, in case of the current financialcrisis the inter-bank lending markets had dried up and ashortage resulted in the markets getting tightened.

The market volatility was so high that the indigenous andendogenous risks led to a severe cash crunch in the market.For example, the mortgage-backed securities markets driedup completely and banks were unable to liquidate theirsecurities through re-pledging, which led to panic. Similarly,when banks could not raise finance to meet their contingentand structured liquidity requirements, rating institutions starteddowngrading their ratings. In addition, borrowers starteddemanding their loans. All these events had a cumulativeeffect on banks getting hit with substantial pressure from allstakeholders. Banks were unable to approach the market toraise finance through certificate of deposits, commercial paperor assets of similar classes, with Lehman Brothers being aclassic example that suffered the consequences of beingunable to create liquidity when required.

Liquidity risks have very

long-standing effects, not

only for the company, but

on the country and

economy as a whole.

9

NEWS

Leading UAE Banks to Convert State Deposits to

Capital: Leading UAE Banks such as Mashreq, RAK Bank,

NBAD, Emirates NBD have recently announced their

intention to convert federal government deposits into

regulatory capital. This is to improve asset quality and offset

the impact of global credit crisis on the domestic banking

industry. Most of these deposits will be converted to Tier 2

capital for effective risk mitigation.

Brazil Plans to Reduce Spending Due to Financial

Crisis: As a result of the financial crisis, revenues from tax

collections in Brazil recorded a significant fall. The

government is now taking measures to curb the impact of

lower inflow of funds. Guido Mantega, Finance Minister of

Brazil, announced a reduction in current expenditure and

tighter fiscal policies to reduce the mismatch between lower

tax collections and high fiscal expenditure.

Qatar Central Bank to Replace 1.2 Million ATM Cards:

Qatar Central Bank heads told all banks in the Gulf state to

change 1.2 million ATM cards with chip and pin technology

to smart chip cards technology within seven days. The aim

of this move is to offer greater protection to clients from

prospective hackers and ATM fraud. While it will enhance

security, it will also offer greater inter-operability .The banks

sent SMS messages to clients informing them about their

ATM card replacement move.

Shari’a Banks may Impose Fees to Issue Guarantees:

According to religious scholars, Shari'a banks should be

permitted to impose a fee for issuing guarantees as it

involves a transfer of risk to the bank. Supporting this,

Mohd Daud Bakar, advisor, Accounting and Auditing

Organisation for Islamic Financial Institutions (AAOIFI),

stated that the nature of transactions for guarantee issuance

has evolved from a family transaction (earlier guarantees

were issued between family members, whereas now they are

issued to unknown parties) to a financial product issued to

third parties. Similarly, opinions about imposing fees on

guarantees are undergoing a change and many banks have

already started charging fees for guarantee issuance.

Citigroup to Expand in South East Asia: Citigroup is

believed to be looking to open more branches in Thailand

and starting equity brokerage businesses in Malaysia,

Vietnam and Indonesia later this year, in an overall plan to

expand in Southeast Asia. This signifies that Citigroup,

which has been affected by huge losses in the United States

due to the real estate market collapse, is now banking on

Asia to bolster its business.

Yemen Plans to Approve Modified Investment Law:

Salah al-Attar, head of the General Investment Authority

(GIA) stated that the Yemen investment law was undergoing

modification. The modification involved a decrease in

income taxes charged on companies from 35% to between

15-20%, customs exemptions and the amendments of the

General Investment Authority’s board of directors (now

comprising 50% public sector employees, and remainder

from the private sector).

Indian Public Sector Banks Cut Rates: Indian banks

have begun reducing deposit and lending rates after the

Reserve Bank of India announced a 50 bps cut in repo and

reverse repo rates. Three public sector banks viz., Bank of

Baroda (PLR-12%, down 50bps), Union Bank of India

(PLR-12%, down 50bps) and United Bank of India (PLR-

12.5%, down 50bps) have reduced their rates. The rate cut is

expected to encourage banks to offer credit for productive

purposes at feasible interest rates. However, private sector

banks such as ICICI Bank and HDFC Bank have yet to

decide on the rate cut.

Global

Update

A quick review of industry news from

around the world.

10

The BFSI industry is in a challenged state today due to the

global financial crisis. Where do you see the industry going

from here?

Those who fail to learn from past failures are bound to

replicate it - the current state of the financial services sector

is a perfect example. As past experience fails to guide future

behaviour, banks and financial institutions across the globe

find themselves unable to understand what actually

happened. Overwhelmed by the sheer volume of lending

activity, many banks opened themselves up to tremendous

risk - for which they now are paying the price.

The current crisis facing the global financial services sector

can be attributed to the contracted liquidity in global credit

markets and banking systems triggered by the failure of

mortgage companies, investment firms and government

sponsored enterprises which had invested in subprime

mortgages. The crisis, which became more visible

Interview

Kalpesh Desai

CEO, Agile Financial Technologies

Kalpesh Desai, founder and CEO of AgileFinancial Technologies, envisioned the creation

of an unparalleled enterprise that would be atechnology partner to leading players in the

BFSI sector enabling business agility. Heformed Agile FT by acquiring and merging

strategic software products and technologycompanies in the space of software solutions,

technology services, BPO and KPO.

Kalpesh has over two decades of experiencein spearheading technology companies to

achieve and sustain a position of marketleadership and organic growth. He has earned

a reputation of creating and buildingsuccessful, scalable enterprises by defining

and converting corporate vision into strategicintent and coordinated action. A firm believer of

producing results through people, he hasattracted and retained talented people.

He brings a deep understanding of businesses having held multiple roles in

executive management, product development, operations management, sales and

marketing management.

INTERVIEW

throughout 2007 and 2008, has exposed persistent

weaknesses in the global financial system and regulatory

framework.

We believe that the domino effect of what happened to sub-

prime will now impact the prime markets. There will be

further write downs in the global financial industry, with

investment firms taking mark to market losses and banks

writing off non-performing assets over the next quarter due

to rise in unemployment, lay-offs and pressures due to

recession in the most economies. In the new economy,

nobody is isolated from the crisis and global liquidity

contraction is bound to put pressure on financial

institutions.

The BFSI sector as we know it has changed its outlook

significantly. Emerging markets will become the new

powerhouse considering that these economies have worked

under stretched circumstances already and are in a position

to adapt to change quickly. Most emerging economies have

also been more or less isolated from exposure to complex

financial instruments like derivatives and have been investing

in fundamental businesses.

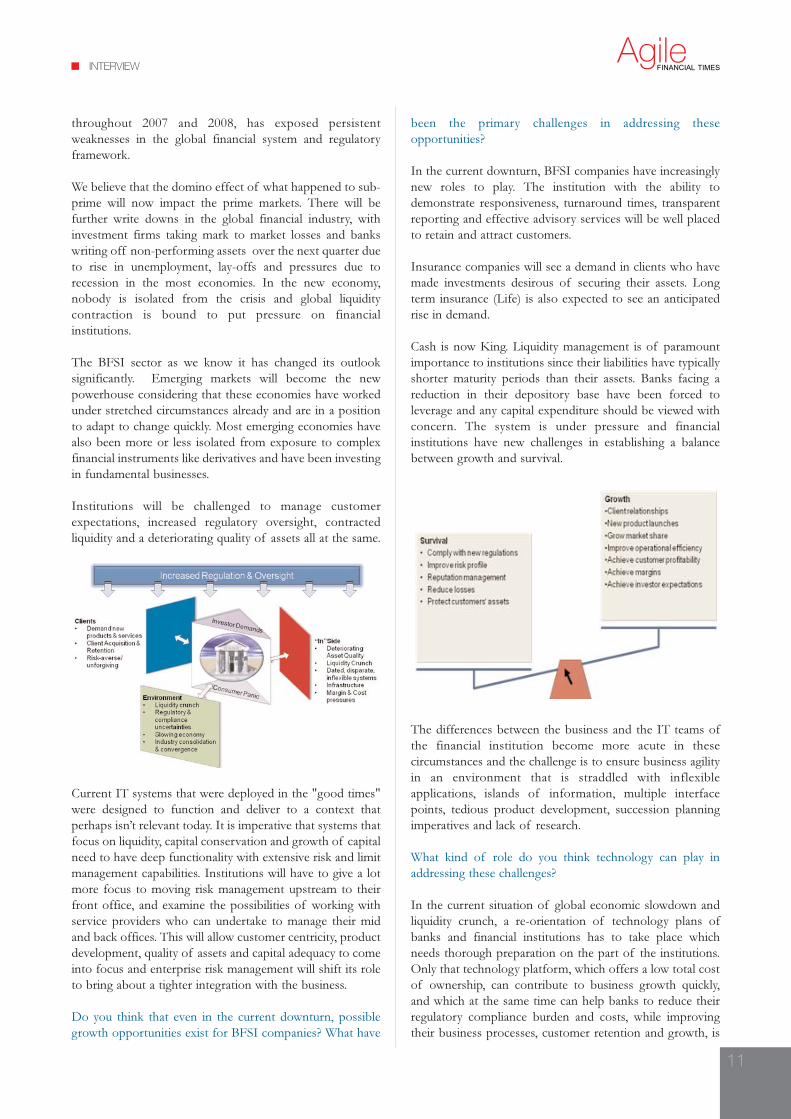

Institutions will be challenged to manage customer

expectations, increased regulatory oversight, contracted

liquidity and a deteriorating quality of assets all at the same.

Current IT systems that were deployed in the "good times"

were designed to function and deliver to a context that

perhaps isn’t relevant today. It is imperative that systems that

focus on liquidity, capital conservation and growth of capital

need to have deep functionality with extensive risk and limit

management capabilities. Institutions will have to give a lot

more focus to moving risk management upstream to their

front office, and examine the possibilities of working with

service providers who can undertake to manage their mid

and back offices. This will allow customer centricity, product

development, quality of assets and capital adequacy to come

into focus and enterprise risk management will shift its role

to bring about a tighter integration with the business.

Do you think that even in the current downturn, possible

growth opportunities exist for BFSI companies? What have

been the primary challenges in addressing these

opportunities?

In the current downturn, BFSI companies have increasingly

new roles to play. The institution with the ability to

demonstrate responsiveness, turnaround times, transparent

reporting and effective advisory services will be well placed

to retain and attract customers.

Insurance companies will see a demand in clients who have

made investments desirous of securing their assets. Long

term insurance (Life) is also expected to see an anticipated

rise in demand.

Cash is now King. Liquidity management is of paramount

importance to institutions since their liabilities have typically

shorter maturity periods than their assets. Banks facing a

reduction in their depository base have been forced to

leverage and any capital expenditure should be viewed with

concern. The system is under pressure and financial

institutions have new challenges in establishing a balance

between growth and survival.

The differences between the business and the IT teams of

the financial institution become more acute in these

circumstances and the challenge is to ensure business agility

in an environment that is straddled with inflexible

applications, islands of information, multiple interface

points, tedious product development, succession planning

imperatives and lack of research.

What kind of role do you think technology can play in

addressing these challenges?

In the current situation of global economic slowdown and

liquidity crunch, a re-orientation of technology plans of

banks and financial institutions has to take place which

needs thorough preparation on the part of the institutions.

Only that technology platform, which offers a low total cost

of ownership, can contribute to business growth quickly,

and which at the same time can help banks to reduce their

regulatory compliance burden and costs, while improving

their business processes, customer retention and growth, is

11

INTERVIEW

likely to be considered in the short to medium term.

Given the enormity of the crisis, risk management

technology will be a key industry focus for the next three or

four years. While firms have invested significantly in their

risk infrastructure over the past 10 years, significant

investment and modifications to the existing infrastructure

will be made. To provide the chief risk officer with the

appropriate risk infrastructure, firms will augment their

Value at Risk (VaR) framework modeling to embrace

scenario analysis. Enterprise risk management platforms

will become the need of the hour as market, credit and

operational risk management become more essential in

running a modern financial institution.

Diversified financial groups will revamp the way to look at

customer centricity around their cash & liquidity

management, mortgage finance, wealth management, asset

management, broking and insurance services. Applications

with deep functionality in these areas and the ability to be

rapidly implemented will see more increasing demand.

Two other key technology initiatives will become

increasingly important as firms revamp their platforms.

First, normalising and validating data across the enterprise

will become critical. Grid, cluster and virtualization will

become more common within as institutions look at

consolidating their resources within a central processing

platform. Secondly, institutions will look for technology

partners who can service them holistically, instead of just

software product vendors or point service providers.

Margins for BFSI companies are under severe pressure

today. How do you think this will impact their technology

decisions?

Banks, both small and large, are under tremendous pressure

to tighten their financial belts. Consequently, they are

considering efficient ways of managing internal costs,

particularly with respect to their IT applications.

As capital markets firms recede, reorganise, and seek safe

harbours, IT spending and priorities are coming into focus.

Financial institutions, across the world, are considering their

competitive position, capital base, and growth prospects.

Platform enabled outsourcing services is emerging as the

definitive IT model for many banks as they strive to lower

operational costs to ensure a high return on investment.

This can be defined as the ability of an outsourcing vendor

to provide its services around functionality rich application

software platforms that are used for fulfillment and

dissemination. Platform enabled outsourcing is likely to

experience tremendous uptake in the coming months,

especially in the wake of the current credit crisis. Financial

institutions should, therefore, take advantage of the benefits

that can be sought from this model in order to stay ahead of

the competition and drive innovation.

Do you see any particular trend in terms of business

requirements from BFSI companies? Have you noticed any

significant change over the last 5 years?

An increasing number of financial institutions have been

using the software as a service (SaaS) model. The financial

services sector is one of the largest industry users of SaaS.

However, most of the current financial services SaaS

deployments are CRM applications. But in the wake of the

current market scenario, large asset managers and brokers

have been increasingly using certain types of non-CRM SaaS

offerings. In the risk and compliance space, there has been

an upswing for vendors offering hosted applications and

financial institutions willing to use such services. SaaS-

delivered risk and compliance applications include corporate

actions, approval mechanisms for complying with customer

regulations and anti-money laundering applications.

Many large institutions are increasingly using SaaS for wealth

management advisory functions; they take these on a need

basis from large clearing providers and wealth management

software providers. Such arrangements are a good fit for

institutions that have agent networks of 10,000 or more

financial advisors.

IT managers of financial institutions also face innumerable

challenges as business needs have been extremely defined,

and existing systems that have been loosely coupled together

are unable to cope with demands from business. Customers

have become very demanding on security issues. Informed

and tech-savvy customers expect financial institutions to

handle remote deposits, nationwide ATM and debit card

services, online banking and electronic bill payment from

multiple physical and digital locations. As a result, fraud

detection & prevention, regulatory compliance and ID &

data security issues have become as mission critical for the

CIO as managing the operations infrastructure.

In the current economic scenario, financial institutions

worldwide are opting for SaaS to reduce IT costs and predict

their IT spending. Banks can reduce the total cost of

ownership (TCO) for IT by outsourcing the hosting of

applications. Through this, banks are able to significantly

reduce the implementation costs which otherwise would

have been higher for custom built solutions. Banks save on

12

Financial institutions, across the

world, are considering their

competitive position, capital

base, and growth prospects.

INTERVIEW

time and money as most of the risks of selecting and

implementing new applications are avoided.

The decision to implement SaaS for small and medium-sized

banks helps them to gain access to flexible software

applications that they traditionally have not been able to

obtain. SaaS enables banks to benefit from the highly

specialised applications at minimum cost and maintenance

fee. Smaller brokerages, fund managers and asset

management firms have a much easier time integrating data

from different applications with hosted services-oriented

applications than their larger counterparts. SaaS also

provides increased flexibility in responding to changes in

demand as well as seamless product enhancements, thereby

allowing financial institutions to concentrate on providing

better customer service to their customers.

Corporate clients can also benefit from SaaS. Financial

institutions offer online web-based cash management

service to corporate treasurers which can help them to

automate and consolidate their financial processes by having

complete access and control of their financial activities

through the bank’s online cash management tool.

The biggest obstacle to SaaS in large firms is integration -

integrating hosted Web services with back-end data storage

and legacy systems. Although SaaS offerings can integrate

with other programs, they operate more efficiently when the

data is in the SaaS provider’s data centre. Security is another

issue to be dealt with.

From Agile FT’s perspective, opportunities will span from

the smallest and the most cutting-edge, to the largest and the

most secure. During times of crisis, firms traditionally cut

back on IT spend, centralise development and operations to

cut down on redundancy and look to outsourcing to reduce

cost and thus focus on core deliverables. Our delivery model

will enable our clients reduce the cost of core technologies

(traditionally provided by larger vendors) and cut back on

newer, riskier technologies (traditionally provided by smaller

vendors).

CEO’s of financial institutions are taking the rein alongside

the Chief Information Officer since the need of the hour is

not just the technology required to run the business, but to

step into identifying what needs to be centralised,

outsourced and managed by an outsourcing service

provider. Thus a change of mindset is in the air - towards

the adoption of platform enabled services adoption.

We understand that a certain loss of control and having a

third party handle the IT infrastructure and the operations

can be a little un-nerving for any financial institution. Hence,

alongside the cost and time efficiencies and a pay-on-

consumption pricing model that is simple and attractive, we

differentiate our delivery model by basing the same on the

foundation of operational risk management, thus innovating

on how we deliver our software platform and operational

outsourcing services, and creating a differentiator for

ourselves.

What are your plans for Agile FT over the near-to-medium

term?

Agile Financial Technologies provides business enablement

services wrapped around its software products platform. We

service businesses of financial groups that focus on the

conservation or growth of capital. Our software products

run the core businesses of investment management firms,

finance companies and insurance companies. We have the

ability to provide financial institutions not just the software,

but managed services around their technology infrastructure

and the ability to take on the outsourced functions of mid

and back office operations. We have a distinctive advantage

by uniquely being able to provide an integrated offering.

Our focus in the near to medium term is to target emerging

markets in Latin America, Africa, Eastern & Central Europe,

Middle East, South Asia and some parts of APAC. We

identify and enable partners to operate as extensions of

Agile Financial Technologies and hence are able to garner

market information quickly and rapidly and delivery locally.

We are young, nimble and our agility is drawn from the years

of experience that the constituent companies that have now

become part of Agile Financial Technologies bring to the

table.

Our belief is that to better service our clients, we need to

think, act and behave like them. We treat clients with the

same deep respect that a financial institution would treat

theirs. We deploy systems and build products with a focus

on flexibility, adaptability to change, and most importantly

usability. Our outsourcing process inculcates the same

operational risk management parameters that an institution

would look at whilst deploying its own central processing

infrastructure.

With a delivery model that seeks to differentiate itself from

other service providers, and the ability to reach and service

clients whose needs are very, very different in the emerging

markets, we believe we will create a niche for ourselves in

this industry.

13

INTERVIEW

A change of mindset is in

the air - towards the

adoption of platform

enabled services adoption.

14

SOLUTION SPOTLIGHT

iDEAL LIQUIDITY

The two keys to good liquidity management are:

(a) to ensure that the regulatory norms of the country are

adequately met, and

(b) to ensure that treasury has a good technology system that

can help them model scenarios and track transactions on

a real-time basis.

iDEAL LIQUIDITY from Agile Financial Technologies is a

comprehensive straight through processing (STP) liquidity

management system that integrates the front office, mid

office, back office, banking and accounting processes of any

bank. It comprises iDEAL FINANCE, ALM and Risk

Management. iDEAL Finance helps banks in smoothly

managing multiple outstanding loans or borrowings and

generating future cash flows and MIS reports with minimal

manual intervention. The Asset and Liability management

(ALM) component manages exposure. The risk

management component is designed to manage net worth

by risk management, capital management and liquidity

management.

The solution covers the following base product classes, with

scalability to handle new product structures as the market

evolves:

� Commercial Papers

� Deposits

� Term Loans

� Floaters

� Non Convertible Debentures

The key features of iDEAL Finance are that it can manage

asset as well as liability products, supports multiple product

structures, supports fixed/floating loans, simple as well as

compounded interest payment, hybrid loans, options

Cash is King!

The success or failure of a financial institutionis determined by its ability to remain liquid and

yet prudently invest money and lend judiciouslyto make profits. Most financial services

companies borrow short and lend long, and atthe same time, must not remain too liquidbecause cash does not yield interest and

resultant profits. Many have failed in the pastbecause of irregular asset and liability

management practices.

A treasury function in a financial servicescompany is in charge of raising finance for

funding the business, taking care of short termcash management and managing liquidityrequired for operations. What the perfect

system must do, therefore, is take into accountthe complex transactions that a treasury offinancial services company performs in its

lending and record and track thesetransactions.

The system must also simultaneously keeptrack of the cash position and adequately

provide for the day-to-day operations of thetreasury and generate accurate and regular

MIS reports for the management. All this mustbe done in a scalable fashion applying themandated regulations that exist so that the

cash ratios are maintained.

(put/call), stubs, termination, transfer out, rollover and

adjustment entries as well as ad-hoc principal repayments

against outstanding contracts.

The system supports multiple currencies and can provide

dynamic generation of future cash-flows with an option to

override.

Most importantly, the software is flexible and easy to

configure and has built-in features that take care of event-

based charge definition (stamp duty, brokerage, taxes) and

charge on charge (taxes on brokerage, service tax).

iDEAL Finance for liquidity management allows treasurers

to transact in a real-time environment and generate

meaningful reports relating to their transactions. The system

has interfaces that allow upload, addition or modification of

benchmark values and also to upload/store beneficiary

positions for outstanding non-convertible debentures.

Managing Loans and Borrowings

This is a crucial function of the treasury. Using the iDEAL

Finance module, they can place and withdraw loans in full or

part as well as track multiple linked loans. The system allows

treasury function to generate and estimate future cash flows

as well which gives them a forecast in line with the liquidity

needs of the financial institution.

The system also has a settlement book that maintains

scheduled cash flow information. This allows marking cash

flow as principal redemption, interest payment or

brokerage payment as realised, redeemed either fully or

partially, capitalised interest, realised schedules/unscheduled

cash flows and calculate interest accrual and event based

charges.

Managing Banking & Accounting Transactions

The banking and accounting module helps in tracking

appropriation, payments and receipts and provides a

comprehensive and reconciled view of the accounts. The

accounting engine can also be configured to generate

vouchers and accounting statements as required.

Administering Users

iDEAL Finance allows for easy administration of users

through a centralised console. Every user has a secure and

unique login id to the system and access to the system is

defined based on his function, role, and authority in the

organisation.

Generating MIS Reports

iDEAL Finance has the ability to intuitively generate a

variety of reports that are required by different executives in

the management from time-to-time.

15

SOLUTION SPOTLIGHT

Asset Liability Management

The Asset Liability Management (ALM) solution fromAgile Financial Technologies is comprehensivelydesigned to manage intermediation risk and the networth of the institution by tracking risk, liquidity andcapital. It provides a complete and dynamic decisionframework of measuring, monitoring and managingliquidity and interest rate risks by uploading enterprise-wide asset and liability portfolios.

In the normal course of operations, financial institutionsare exposed to credit and market risk in view of theasset-liability transformation. They are required toperiodically determine their own interest rate onadvances and deposits, subject to the ceiling onmaximum rate of interest they can offer on deposits, on adynamic basis. Intense competition coupled withincreasing volatility in the interest rates brings intensepressure on banks and financial institutions to maintain agood balance among spreads, profitability and long-termviability.

The quest for profitability and sustenance exposes theseinstitutions to several major risks - categorised as creditrisk, market risk and operational risk - which emphasisesthe need to address these risks in a structured andcomprehensive manner.

It is important for financial institutions to base theirbusiness decisions on a dynamic and integrated riskmanagement system and processes driven by corporatestrategy. In this context, Agile FT’s ALM system isdesigned to serve as a central system for analysing,monitoring and simulating the balance sheet and aid inenterprise wide risk management.

The key features of the system include:

Comprehensive reporting and analysis.

Data management module for integration with legacydatabases and retrieval and processing of branch data.

Identifying funding gaps and estimating pre-payments.

Standard analysis for assets, liabilities and integratedALM analysis.

‘Interest Rate Sensitivity’ and ‘Net Interest Income’.

Facility to bucket non-performing assets as per theguidelines set by the regulator.

Enhanced risk management functionalities via analyticaltechniques like duration gap analysis and market valuecalculations.

Bade Aluko, Managing

Director, FASYL, shares his

thoughts with Agile Financial

Times:

What is the strategic rationale

of your partnership with

Agile FT?

Agile FT follows a proactive

approach while meeting

customer needs compared to

other partners who follow a reactive approach. They have a

high level of responsiveness to the company expectations as

well as the customer demands.

In addition, Agile FT provides a suite of products and

services that complement our current offerings and enables

us to meet customer requirements.

With the current economic scenario, what will be the impact

on partner relationships?

The current economic downturn is not going to significantly

change the role of partners. Partners with a long term view

survive an economic crisis as their prime focus is not only to

have quick profits, but to align goals with the partner

company in order to meet customer expectations.

Thus, I believe that short term partners will perish whereas

long term partners will continue to service the clients

effectively.

16

PARTNER SPOTLIGHT

Finance Application Systems Limited

www.fasylgroup.com

Finance Application Systems Limited (FASYL), a Nigeria-

based information technology company, was founded in

1998, and primarily offers specialist support services for

enterprise and finance applications & software systems

within areas of product sales, implementation, support and

training. In addition to this, FASYL also provides

consultancy services for the finance and telecom industries.

While the company’s operations extend across Asia, Africa,

Europe and the UK, its main focus is primarily pan-Africa.

FASYL also has offices at Mauritius (slated to become the

future group headquarters), Nigeria (to become a regional

office), Ghana, Sierra Leone, South Africa, UK and India.

The company, which currently has a staff strength of 120,

also plans to set up offices at Cote d’Ivoire, Kenya and

Angola in 2009.

Key Clients

FASYL’s clients include Union Bank of Nigeria, Access

Bank, Intercontinental Bank, Diamond Bank, Skye Bank,

Ecobank Group, Sierra Leone Commercial Bank, First

Securities Discount House Limited, NEXIM Bank, United

Bank of Africa, First Bank, Bank PHB, Fidelity Bank and

Spring Bank.

Making

Strides in

West Africa

A listing of key Agile FT partners from

West Africa

The financial services industry is undergoing a change; how

will this affect client requirements and buying decisions?

Banks are undergoing change due to the customer

demand for better and faster banking services. There is

significant competition amongst banks and hence they have

to rely on technology to gain a competitive edge. Customer

expectations are increasing manifold. The nature of services

demanded by banks is changing drastically from the manual

mode to a technological platform where banks are

competing to provide faster and improved service to its

clients. Similarly, the changing banking services are giving

rise to a need for newer and better technology platforms to

meet the changing customer needs.

17

ExpertEdge Software & Systems Ltd

www.cwlgroup.com/ee

ExpertEdge Software & Systems Limited looks at Agile FT’s

iDEAL suite of investment & banking solutions. Its

business focus includes software development &

deployment, systems analysis, design & implementation and

smartcard applications. In-house expertise of providing

implementation, support and training was the key reason for

Agile FT to choose ExpertEdge to provide first level

support to its customers in Nigeria.

ExpertEdge Software & Systems Limited, headed by James

Agada, is the software subsidiary of the Computer

Warehouse Group, one of the fastest growing IT companies

in West Africa today.

Computer Warehouse Group (CWG), an information and

communication technology company, provides integrated

solutions to its clients. Apart from ExpertEdge, the group

consists of two more subsidiary companies:

Computer Warehouse Limited (provides supply and

maintenance of computer hardware and ancillary

equipment)

DCC Satellite & Networks Limited (offers VSAT,

metropolitan area network, wide area network, systems

integration and network monitoring and management

solutions).

The company also provides training to IT professionals

through its ExpertEdge Training Centre. The primary

industry verticals serviced by the company include banking

and telecom.

Key Clients

A partial list of key clients includes First Bank of Nigeria,

Union Bank of Nigeria, Nigeria Aviation Handling

Pacific Solution and Technologies

www.pacificsolutiontech.com

Pacific Solution is a system integrator founded with an

objective to provide solutions to West African countries.

The company provides hardware, security, software and

communication services to its clients. Pacific Solution is

essentially the information technology arm of the Budhrani

Group of companies, which has a global presence. The

company has offices in Nigeria, Ivory Coast, UAE (Dubai),

UK, Malaysia, Singapore, Indonesia and India. The key

industry verticals serviced include banking, insurance,

internet service providers, telecom operators, government

and corporates.

Key Clients

Pacific Solution’s clients include Sterling Bank, Royal United

Nigeria, Mikano International, Jubilee Brothers, Somotex

Nigeria, Critical Rescue International, Reliance Textile,

Millenium Furnitures, Hansbro Group, Park n Shop Retail,

MTN Nigeria, Multilinks Telecommunications, GLO

Mobile, Celtel, Lagos Metropolitan Area and

Transportation Authority, Nigerian Postal Service, Industrial

General Insurance, Linkage Assurance, Unic Insurance,

Michael Stevens Consulting and Standard Life Insurance.

Jeetu Hira, Head - Pacific Solution, speaks with Agile

Financial Times:

In what areas of business and technology do you share a

partnership with Agile Financial Technologies?

Pacific Solution and Technology is representing Agile FT for

their Insurance application. We are offering to the market

both, the product as well as the outsourced model of Agilis,

the Insurance suite from Agile FT comprising Life, Non-

Life, Health, Takaful, BancAssurance, Broker among others.

What is the key benefit of this partnership and how has it

impacted the way in which you service your clients?

There is a long standing relationship between the

management of Pacific Solution and Technology Limited

and that of Agile FT. We are bringing a blend of both, the

domain knowledge of Agile FT, and the geographic and the

vertical industry knowledge of Pacific Solution and

Technology.

PARTNER SPOTLIGHT

Company, African Petroleum, Adeniran Ogunsanya College

of Education, Ghana Telecom, British American Tobacco,

and Multilinks.

Besides Agile Financial Technologies, they work closely with

Infosys Technologies and Oracle.

18

CUSTOMER SPOTLIGHT

Leading Asset

Management

Company

Selects Agile FT

The Asset Management Company (AMC) offers investors a

well-rounded portfolio of products to meet varying investor

requirements and has a presence in 120+ cities across India.

A key business driver for the fund manager is the company’s

constant endeavour to launch innovative products and

provide proactive customer service to increase investor

value.

In line with this philosophy, the AMC wanted to automate

its asset management operations, achieve seamless

integration across the front, mid and back-office, offer a

comprehensive range of fund management products to suit

the investors’ needs and inclinations and provide exposure

to multiple asset classes like equity, bonds, mutual funds,

deposits, equity derivatives and interest rate derivatives as

also commodities like gold. More importantly, the fund

house also wanted to maintain a strict vigilance on limits and

exposures in line with its internal governance requirements

as well as in keeping with the norms of the securities

exchange regulator.

In this context, India’s top Asset Management Company

chose iDEAL Funds from Agile Financial Technologies to

manage its funds and investor portfolio. Apart from more

than adequately meeting the requirements of the fund

house, iDEAL Funds was also identified as a platform to

handle huge transaction volumes and cater to the large

investor base of the fund. In addition, the system integrated

with third-party price feed systems to provide valuation

across markets, and also with register and transfer (R&T)

platforms, business intelligence systems, equity straight-

through-processing and custodial files.

iDEAL Funds generates timely and key management reports

and has a biometric scanning security system for users. Most

importantly, the system has proved to be resilient and

scalable and hence supports the organisation’s expansion

and growth strategy.

One of the fastest growing and

largest mutual fund company in

India that is part of a large

Indian conglomerate chooses

iDeal Funds from Agile

Financial Technologies.

www.agile-ft.com

Views expressed in this publication do not necessarily represent the views of Agile FT and the information contained herein is only a brief synopsis of the issues discussed herein. Agile FT makes

no representation as regards the accuracy and completeness of the information contained herein and the same should not be construed as legal, business or technology advice. Agile FT, the authors and

publishers, shall not be responsible for any loss or damage caused to any person on account of errors or omissions.

Agile Financial Technologies

808-A, Business Central Towers

TECOM, Dubai Internet City

P.O. Box 503007

Dubai

United Arab Emirates

Tel: +971-4-4331825

Fax: +971-4-435-5709

Agile Financial Technologies Pvt Ltd

701-A, Prism Towers

Mindspace, Malad (West)

Mumbai 400064

India

Tel : +91-22-42501200

Fax: +91-22-42501234

Agile Financial Technologies Pte Ltd

20 Cecil Street, #14-01

Equity Plaza

Singapore 049705

Tel: +65-64388887

Fax: +65-64382436