agenda - j.p. morgan home · including capital structure, ... working capital and the cash...

TRANSCRIPT

AgendaAgenda

Optimizing Working CapitalOptimizing Working CapitalSeptember 24, 2014

SpeakersSpeakers

Cassio CalilInternational Corporate Client Banking J P MorganInternational Corporate Client Banking, J.P. Morgan

“Setting the Scene”

Calil manages the International Corporate Client Banking team for J.P. Morgan Commercial Banking. Prior to his current role, he was president of J.P. Morgan Asset management in Brazil, where he was responsible for accelerating the growth of institutional, retail and corporate clients. He holds a master’s degree in Economics from A li ’ M i U i i d b h l ’ d i E i f B il’ M k i U i iAustralia’s Macquarie University and a bachelor’s degree in Economics from Brazil’s Mackenzie University.

Fabian KhoshbakhtClient Solutions Specialist, J.P. Morgan

“The Importance of Working Capital”

Khoshbakht is a Client Solutions Specialist for J.P. Morgan Commercial Banking. Fabian has over 17 years of experience in the financial services industry, and he specializes in: working capital, treasury management, in-house banks, shared service centers, business process re-engineering, payables and receivables migration strategies, and account structuring and rationalization. He holds an MBA from Australia’s g g , gDeakin University.

Steven DelahuntTreasurer, Cabot Corporationp

“Cabot Overview and Working Capital Optimization Strategy”

Delahunt is Treasurer of Cabot Corporation. In this role, he is responsible for Cabot’s global treasury activities, including capital structure, capital markets issuance, interest rate and foreign exchange risk management, working capital management, treasury operations, cash flow forecasting, bank relationship management and global pension

2

p g , y p , g, p g g pand 401(k) plans. He holds a bachelor’s degree in Finance and an MBA from Boston University.

AgendaAgenda

Setting the Scene

Th I t f W ki C it l 1 The Importance of Working Capital

About Cabot Corporation and Cabot’s Working Capital Optimization Strategy

Where to From Here?

1

Where to From Here?

Participant Q&A

3

Setting the Scene

Operating performance for most firms has been relatively stable over time. However, financial risks have increased in pursuit of higher returns.

Setting the Scene

There is increasing scrutiny on financial performance that’s associated with managing working capital.

It can be difficult for companies to measure the effectiveness of working capitalIt can be difficult for companies to measure the effectiveness of working capital management relative to peers.

Although it does not appear on the income statement, working capital can amount to significant revenuesignificant revenue.

By improving working capital performance, corporations can free up cash and enhance their entire value chain.

TH

ES

CE

NE

SE

TT

ING

4

Working Capital Levels Are ImprovingWorking Capital Levels Are Improving

S&P 500¹ Balance Sheet 1999 S&P 500¹ Balance Sheet 2007 S&P 500¹ Balance Sheet 2014S&P 500¹ Balance Sheet – 1999Other Assets EquityA/R Other LiabilitiesInventory ST DebtCash A/P

S&P 500¹ Balance Sheet – 2007Other Assets EquityA/R Other LiabilitiesInventory ST DebtCash A/P

S&P 500¹ Balance Sheet – 2014Other Assets EquityA/R Other LiabilitiesInventory ST DebtCash A/P

$6.308bn $6.308bn 635

630 505

803 758

$8,312bn $8,312bn

$3,478bn $3,478bn

540

2,107

473522

463 6452,777

2,875

206

1,196

229429

167 302

$3,478bn $3,478bn

4,832

3,034

6,244

4,272

TH

ES

CE

NE

1,551

Asset Liabilities + Equity

Source: Bloomberg; J.P.Morgan

Asset Liabilities + Equity Asset Liabilities + Equity

SE

TT

ING ¹ Represents 345 companies from the S&P 500 constituents as of 7/25/14 that were publicly listed as of Dec 31, 1999; Excludes financials

5

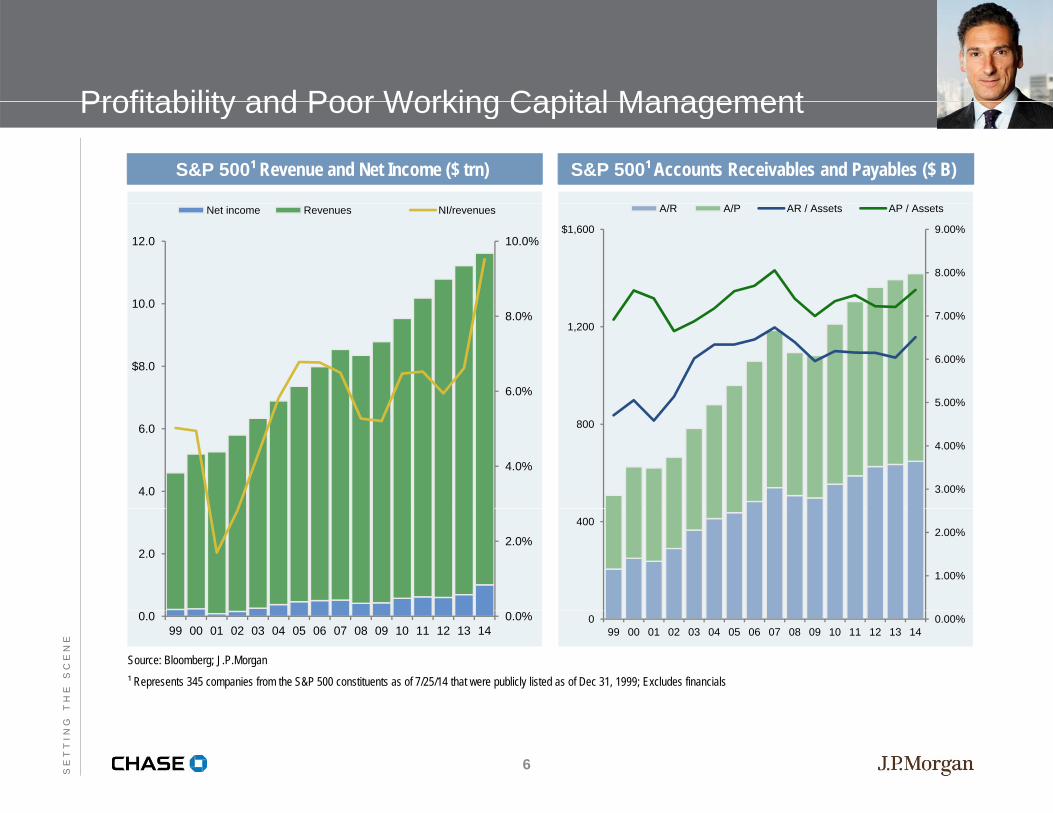

Profitability and Poor Working Capital ManagementProfitability and Poor Working Capital Management

S&P 500¹ Revenue and Net Income ($ trn) S&P 500¹ Accounts Receivables and Payables ($ B)

10.0%

10 0

12.0

Net income Revenues NI/revenues

8.00%

9.00%$1,600

A/R A/P AR / Assets AP / Assets

6.0%

8.0%

$8.0

10.0

5.00%

6.00%

7.00%1,200

4.0%

4.0

6.0

3.00%

4.00%

800

2.0%2.0

1.00%

2.00%400

TH

ES

CE

NE

0.0%0.099 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

0.00%099 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

Source: Bloomberg; J.P.Morgan

¹ Represents 345 companies from the S&P 500 constituents as of 7/25/14 that were publicly listed as of Dec 31, 1999; Excludes financials

SE

TT

ING

6

Working Capital and the Cash Conversion Cycle (CCC)

Days sales outstanding Days payables outstanding

Working Capital and the Cash Conversion Cycle (CCC)

Consumer Discretionary Consumer Staples

Accounts Receivables and Payables S&P 500¹ DSO vs. DPODays sales outstanding Days payables outstanding Consumer Discretionary Consumer Staples

Energy Financial ServicesHealth Care Materials & ProcessingN.A Producer DurablesTechnology Utilities

52 51 53 51 48 48 48 49 48 46 49 47 47 47 48 47

12%

9% 5% 12%

15%

30%

4%

9%

38% 10%

12%

6%

11%

4%

5%

'99 A/R

14 A/R

-57-50

-68

-54-64

-56 -51-59 -63

-56-64 -67

-72-61 -59 -54

28% 6% 5% 31% 10% 4%'99 A/P

24% 7% 16% 7% 13% 11% 8% 6%14 A/P

92 102 79 95 75 85 95 83 76 83 78 71 66 80 81 86

DSO/DPO ratio (%)

TH

ES

CE

NE

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 0% 20% 40% 60% 80% 100%

Source: Bloomberg; J.P.Morgan

¹ Represents 345 companies from the S&P 500 constituents as of 7/25/14 that were publicly listed as of Dec 31, 1999; Excludes financials

SE

TT

ING

7

Polling Question #1Polling Question #1

11

How important is working capital to your overall organizational strategy?

8

Working Capital Continues to Be a Global Priority for CFOs

Abilit t f t lt

for CFOs

Top Concerns for CFOs

Att ti d t i i lifi dAbility to forecast results

Working capital management

Maintaining morale/productivity

Attracting and retaining qualified employees

Paying down debt

during economic downturn

Cost-cutting

Cost of health care

Investing existing cash

Improving governance

Protection of intellectual property

L

Cost of health care

“Getting serious about working capital means making it an integral part of operational processes and the corporate i d d i i i i ”

“Getting serious about working capital means making it an integral part of operational processes and the corporate i d d i i i i ”

Protection of intellectual property

OR

KIN

GC

AP

ITA mindset and not treating it as a one-time exercise.”mindset and not treating it as a one-time exercise.”

“Working capital optimization usually has a less disruptive effect on the organization and employee morale.”“Working capital optimization usually has a less disruptive effect on the organization and employee morale.”

OR

TA

NC

EO

FW

O

“Working capital management and optimization can be embedded into corporate culture by providing workforce training, considering the impact in day-to-day strategic decision making.”

“Working capital management and optimization can be embedded into corporate culture by providing workforce training, considering the impact in day-to-day strategic decision making.”

TH

EIM

PO

Source: Deloitte CFO Signals 2012

9

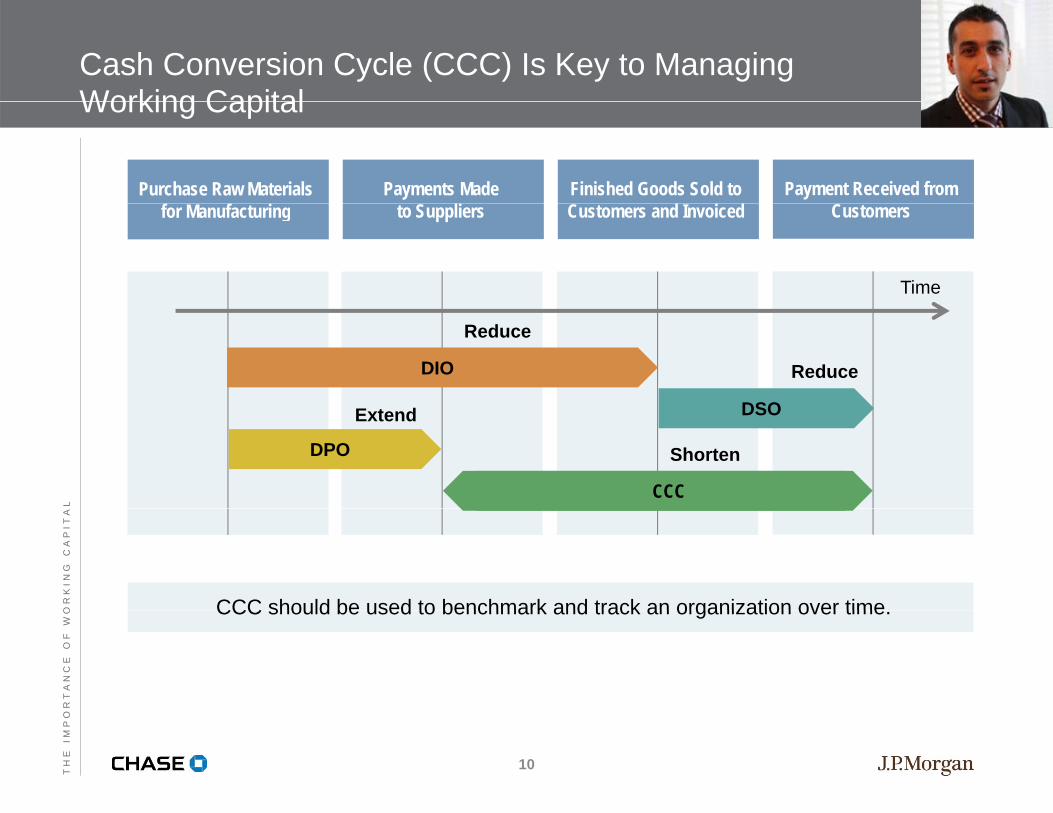

Cash Conversion Cycle (CCC) Is Key to Managing Working CapitalWorking Capital

Purchase Raw Materials Payments Made Finished Goods Sold to Payment Received from for Manufacturing to Suppliers Customers and Invoiced Customers

Time

DIO

DSO

Reduce

Reduce

L

DSO

DPO

CCC

Extend

Shorten

OR

KIN

GC

AP

ITA

CCC should be used to benchmark and track an organization over time

OR

TA

NC

EO

FW

O CCC should be used to benchmark and track an organization over time.

TH

EIM

PO

10

Polling Question #2Polling Question #2

11

How successful has your organization been in reducing days sales outstanding (DSO)?

11

US Working Capital Survey Results by IndustryUS—Working Capital Survey Results by Industry5

183

15

Computer & peripherals

Wireless telcom services

Opportunity cost too great to ignorePayables Payables

18

26

33

15

15

23

Diversified telecom services

Oil, gas & consumable fuels

H h ld d t prov

ing DPO remains flat for 2013

Continued improvements achieved post-recession unable to be sustained

33

94

57

30

85

52

Household products

Biotechnology

Containers & packaging

Im DPO has settled at 32 days

ReceivablesReceivables40

89

27

42

95

29

Electric utilities

Aerospace & defence

Media ning

DSO improved by half a percent since 2011—this follows several years of increases

Companies are efficiently managing credit

BE

RS

…

32

59

4

29

35

65

Gas utilities

Metals & mining

Diversified consumer servicesW

orse

n Companies are efficiently managing credit and collection processes

Inventory Inventory

CA

PIT

AL

NU

MB 4

615

74

Diversified consumer services

Internet software & services

DWC 2011 DWC 2012

Inventory increased by $56 billion in 2013

Inventory turnover remained flat

WO

RK

ING Source: REL 2013 US Working Capital Survey

12

Polling Question #3Polling Question #3

11

How successful has your organization been in reducing days payables outstanding (DPO)?

13

Europe Working Capital Survey Results by IndustryEurope—Working Capital Survey Results by Industry

12

9321Media

Life sciences tools & services

Opportunity cost too great to ignore

Payables Payables93

29

27

114

34

32

Life sciences tools & services

Food products

Automobiles

prov

ing

DPO fell to 43 days, from 45 days

Figures suggest pressure on supplier payments

28

39

40

32

45

46

Oil, gas & consumable fuels

Multi-utilities

IT services

Imp

Lowest levels in 10 years, at 47 days

V l b t t f

Receivables

50

78

44

46

48

73

Commercial services & supplies

Energy equipment & services

Beveragesng

Very large gap between top performers

and rest of companies

Inventory Inventory

BE

RS

…

86

37

15

40

79

31

Beverages

Semiconductors (including equipment)

Computers & peripheralsWor

seni

n Decrease of one day year-over-year, to

37 days

Heading to pre-recession levels

CA

PIT

AL

NU

MB 15

1511

9

Transportation infrastructure

Marine

DWC 2011 DWC 2012

WO

RK

ING Source: REL 2013 Europe Working Capital Survey

14

About Cabot CorporationAbout Cabot Corporation

NYSE: CBT

Founded in 1882

Global specialty chemicals and performance materials company

42 manufacturing sites in 21 countries

Core technical competencies in fine particles and surface modification

FY2013 sales: $3.5 billion

15

Discussion: Cabot’s Working Capital Optimization StrategyDiscussion: Cabot s Working Capital Optimization Strategy

11

St D l h t F bi Kh hb khtSteve Delahunt Fabian Khoshbakht

16

Polling Question #4Polling Question #4

11

How much working capital do you believe is locked up globally within organizations?

17

Optimizing Working Capital Is Not a One time ProcessOptimizing Working Capital Is Not a One-time Process

Strong Governance

Strong policy and procedures from executive managementDevelop management reports/dashboards to track and monitor compliance

P t ith i t l dit t

Scale Appropriately

Comprehensive end-to-end review of operationsEnsure accuracy of data to initiate remedies

Partner with an internal audit team

Set Performance Measures

Company, department, team and individual levelsDo not measure too broadly—be specific

Adjust Incentive Programs

Bonuses, incentives and commissions should be aligned to working capitalComponent linked to cash flow management should also be considered

Implementation and Roll Out

Define segments and identify rollout processBe aware of resistance—it will exist

OF

RO

MH

ER

E? Continuous

Process Management

Monitor and enhance processesRetool workforce with ability to continue to improve on metrics

WH

ER

ET

O

18

Considerations for a Successful Working Capital ProgramCapital Program

An Ongoing Approach to Working Capital Optimization

Senior Sponsorship Is Critical Identify a “champion” at the executive level to demonstrate to the organization the

priority attached to working capital by the executivespriority attached to working capital by the executives.

Be Inclusive Include corporate and local finance/functional teams (sales, accounting, accounts

payable accounts receivable procurement etc ) banking partners and ITpayable, accounts receivable, procurement, etc.), banking partners and IT.

Connect the Dots Education through a top-down approach (senior managers to employees) to understand

f “ ffthe meaning of “effective working capital” down to roles and responsibilities.

Create an Action Plan Establish practical and measurable plans that have accountability and target dates.

OF

RO

MH

ER

E?

Aim for Low-hanging Fruit Develop plans for subsidiaries, departments or countries where quick wins are possible. Leverage to show earnings potential for adoption within each area of focus

WH

ER

ET

O Leverage to show earnings potential for adoption within each area of focus.

19

Participant Q&AParticipant Q&A

To submit a question via the meeting room, please open up the Q&A panel, i i h b d li k h d b W ill ddtype your question in the text box and click the send button. We will address

as many questions as time permits.

20

© 2014 JPMorgan Chase & Co. All rights reserved. Chase, JPMorgan and JPMorgan Chase are marketing names for certain businesses of JPMorgan Chase & Co. and its subsidiaries worldwide (collectively, “JPMC”). The material contained herein is intended as a general market commentary. Opinions expressed herein are those of Chauncy Lennon, Fred Dedrick or Mike Mandina and may differ from those of other J.P. Morgan employees and affiliates. This information in no way constitutes J.P. Morgan research and should not be treated as such. Further, the views expressed herein may differ from that contained in J.P. Morgan research reports. The above information/statistics have been obtained from sources deemed to be reliable, but we do not guarantee their accuracy or completeness. None of this material or any of the other information provided in this seminar is intended to constitute an offer or solicitation for the purchase or sale of any financial product or service or the provision of any advice or recommendation, and JPMC is not acting as an advisor to any person or entity in giving this seminar or providing any such information. Please contact your own legal, accounting, tax, investment or other advisors as to the information provided and the suitability of any action or transaction arising therefrom.

21