agency mbs prepayment model using neural networks

TRANSCRIPT

Machine Learning in Finance Workshop 2020

AGENCY MBS PREPAYMENT MODEL USING NEURAL

NETWORKS Jiawei “David” Zhang

MSCI

-

AGENCY MBS PREPAYMENT MODEL USING NEURAL NETWORKS

Columbia Bloomberg Machine Learning in Finance 2020

David Zhang

MSCI Securitized Products Research

© 2016 MSCI Inc. All rights reserved. Please refer to the disclaimer at the end of this document.

— GENERAL —

Zhang, PhD

ewYork

MANAGING DIRECTOR, HEAD OF

SECURITIZED PRODUCTS RESEARCH

212. 981. 7464

MSCII

Speaker

David Zhang is a Managing Director and Head of Securitized Products Research at MSCI. His

team is responsible for developing models and analytics to support investment analysis, risk

management, and regulatory compliance. Before joining MSCI, Dr Zhang was Managing

Director and head of Securitized Products modeling at Credit Suisse for more than a decade. At

Credit Suisse he was responsible for supporting risk, regulatory and client analytics as well as

sales/trading quantitative strategies. Dr Zhang’s group developed one of the most widely used

MBS models by fixed income institutional investors. Their work was consistently awarded top

ranking by various industry and client surveys, including Institutional Investor All-America

Research Team ranking in Agency prepayment. They also won the award for best paper by the

American Real Estate Society for research on effectiveness of government mortgage programs

The regulatory projects Dr Zhang lead at Credit Suisse included developing models for CCAR

and PPNR (Pre-Provision Net revenue), Dodd-Frank IHC (Intermediate Holding Company) and

related VaR, RWA and RBPL modeling, and FRTB (Fundamental Review of Trading

Book). Prior to Credit Suisse, Dr Zhang worked at FreddieMac, CIBC Oppenheimer, and

University of Chicago. He holds leadership positions at PRMIA (Professional Risk Management

International Association) and GCREC (Global Chinese Real Estate Congress). He is a frequent

speaker at industry and academic conferences, and his research on risk, financial modeling and

real estate has been published in many academic journals. Dr Zhang has a Ph.D. from Princeton

University.

3

SUMMARY: NEURAL NETWORKS AGENCY MBS PREPAYMENT MODEL

Why a machine learning model for Agency MBS? • Prepayment is a highly complex and non-linear process with many idiosyncratic risk factors, among the most

complex financial models

• Recent development in computational software and hardware enable us to make significant advancement in AI prepayment models

• Machine learning models have excelled in many areas, such as image recognition, natural language processing, fraud detection, etc.

What is the model and what have we learned?

• Deep neural network model applied to pool level agency MBS prepayment data, compared with MSCI1 (the

human model)

• Results show the deep learning model is able to capture very complex prepayment patterns and signals with

extremely high computational efficiency

— GENERAL — 4

MACHINE LEARNING IN FINANCE

• Consumer credit risk models via Machine-Learning Algorithms (Dr. Andrew Lo, 2010)

Using machine-learning model for consumer credit default and delinquency

Generalized classification and regression trees

Accurately forecasted credit events 3 to 12 months in advance

• Risk and risk management in credit card industry (Dr. Andrew Lo, 2016)

Analyzed very large dataset consisting of credit card data from six large banks.

Decision trees and random forests model perform better than logistic regression at short time horizon

• Deep learning for mortgage risk (Dr. Kay Giesechke, 2015-2018)

Using deep neural network to model mortgage prepayment, delinquency and foreclosure

Loan level data

Compared NNM with a logit model

— GENERAL — 5

MSCI •-

US Bond Market 2018 (42.4$Tn) Federal Agency

Securities Money Markets 1.05

Mortgage Related 9.66

US Bond Market 2007 (29.5$Tn}

Money Markets 1.79

AgencyMBS 5.80

US BOND MARKET

— GENERAL — 6

MODELING OBJECTIVE

Forecast prepayment rate for agency RMBS pools

SMM : Single Monthly Mortality Rate

CPR: Conditional Prepayment Rate

Agencies report last month’s prepayment speed on the 4th business day of each month.

Prepayment types:

─ Rate refinance

─ House turnover

─ Cash-out

─ Curtailment

─ Buyout

— GENERAL — 7

MORTGAGE PREPAYMENT MODELING: SCIENCE AND CRAFTSMANSHIP

Difficulties with mortgage prepayment modeling

• Large data sets: ~20-2000 G data, Agency MBS covers ~400,000 pools/100+mm loans performance over 20-30 years, pool/loan variables ~30-100

• Multiple, highly non-linear and interactive risk drivers (“layered risk”)

• Loan size vs. prepayment is function of moneyness

• Age vs. prepayment is function of past moneyness history

• Loan purpose (refi vs purchase) vs. prepayment is function of origination year

• ….

• Regime changes

• Mortgage credit and borrower risk appetite cycles, and business practice affect absolute level and risk drivers for prepayment/default

— GENERAL — 8

•

MSCII

• • • • • • •1•• . ,, ...

• • • .. ·- ..

I • • •

• • •

Agency MBS prepayment

• Complex behaviors

– 30–100 risk factors: rates, loan size, GEO, purpose, property, HPA….

– “layered risk”- non-linear interaction (e.g., loan size vs moneyness, purpose vs. origination year, ..)

– Regime changes: behavior, policy

– Statistical noises

• Large data set to model

– 400,000 pools/100m loans, 30yr

• Modelers as craftsman?

– Idiosyncratic modeler risk

Po

ol c

ou

nt

Mo

de

l C

PR

50

40

30

20

10

0

0 10 20 30 40 50 60 70 80

Actual CPR

Model CPR distribution

1,000

800

600

400

200

0

CPR range

90-100bps ITM FNCL 4s pool speeds

9

Architecture* Hidden

Input layer

r1 r .. :!'.1 = mox(A 1K I B,.,0) :!'.'... - mlll:'.(Ani' ,-i + Bn, 0)

Vilhtes ot hirJden lilyers ilrP. generilterJ hy Mtiviltion functions with previous layers as inputs, and weights and

biases as parameters

•Example of a Neural Network archite.cture Q Node

MSCII

Model training 1 Select a set of training data:

inputs togP.thP.r with correct/actual output

2 Pass training Al Model data through the network to obtain predicled output

T wea~ weiqttls tmcl biases using gradient function

Actual Output

3 reedforward pass: compare ilr.t ual Oll tp11t With pred i r.tP.rl output ilnd determinP. cost function based on the error rnlc::u I aterJ

Predicted MeP.ts Output Ctiteria? --~o•Y•••I

4 Backward propagation: oplirniLe weiqhls am.I I.Jiases (p,:H c1meler s) until some stopping condition has been met by passing the error si nal throu h the network usin radient function

AI agency MBS prepayment model

Deep neural network model

• Feed forward neural network – Applied successfully in many other fields

– Layers and nodes, hyper-parameters

– Ensemble techniques, bagging and boosting

• Competing vs. “human” /MSCI production model – Forecast accuracy

– New signals, new discoveries

– x100-1000 Efficiency gains: 3hrs vs. weeks/months

10

MSCII

CP

R

40

20

AI vs. “human” models: higher accuracy

8080

6060

0 0

CP

R

40

20

Au

g-0

3

Ma

r-0

4

Oc

t-0

4

Ma

y-0

5

De

c-0

5

Ju

l-0

6

Fe

b-0

7

Se

p-0

7

Ap

r-0

8

No

v-0

8

Ju

n-0

9

Ja

n-1

0

Au

g-1

0

Ma

r-1

1

Oc

t-1

1

Ma

y-1

2

De

c-1

2

Ju

l-1

3

Fe

b-1

4

Se

p-1

4

Ap

r-1

5

No

v-1

5

Au

g-0

3

Se

p-0

4

Oc

t-0

5

No

v-0

6

De

c-0

7

Ja

n-0

9

Fe

b-1

0

Ma

r-1

1

Ap

r-1

2

Ma

y-1

3

Ju

n-1

4

Ju

l-1

5

Au

g-1

6

Se

p-1

7

De

c-0

3

Ja

n-0

5

Fe

b-0

6

Ma

r-0

7

Ap

r-0

8

Ma

y-0

9

Ju

n-1

0

Ju

l-1

1

Au

g-1

2

Se

p-1

3

Oc

t-1

4

No

v-1

5

De

c-1

6

Ja

n-1

8

CA NY

Actual NNM CPR NNM Hmodel

• Higher modeling accuracy – Across cohorts and multiple dimensions of risk factors

– Highly adaptive to high dimensionality and non-linearity

11

-~-----------------------...

MSCII

...... ..... ......... _ ------

AI vs. “human” models: higher accuracy

FICO SATO

30 Actual

720 740 760 780 720 740 760 780

Pre-2008 Post-2008

0

10

20

30

40

50

60

CP

R

Actual

NNM

-1.5 -1 -0.5 0 0.5 1

CLTV

25 NNM

20

15

10

5

0

CP

R

Current loan size

CP

R

35

30

25

20

30 Actual Actual

25NNM NNM

20

CP

R15

10

5

0

15

10

5

0

50,000 100,000 150,000 200,000 250,000 300,000 350,000 55 65 75 85 95 105

12

-

MSCII

,, , ,,

---------------------_,

,, ,, ,,

,,,'

I , , , , ,, ,

AI vs. “human” models: higher accuracy

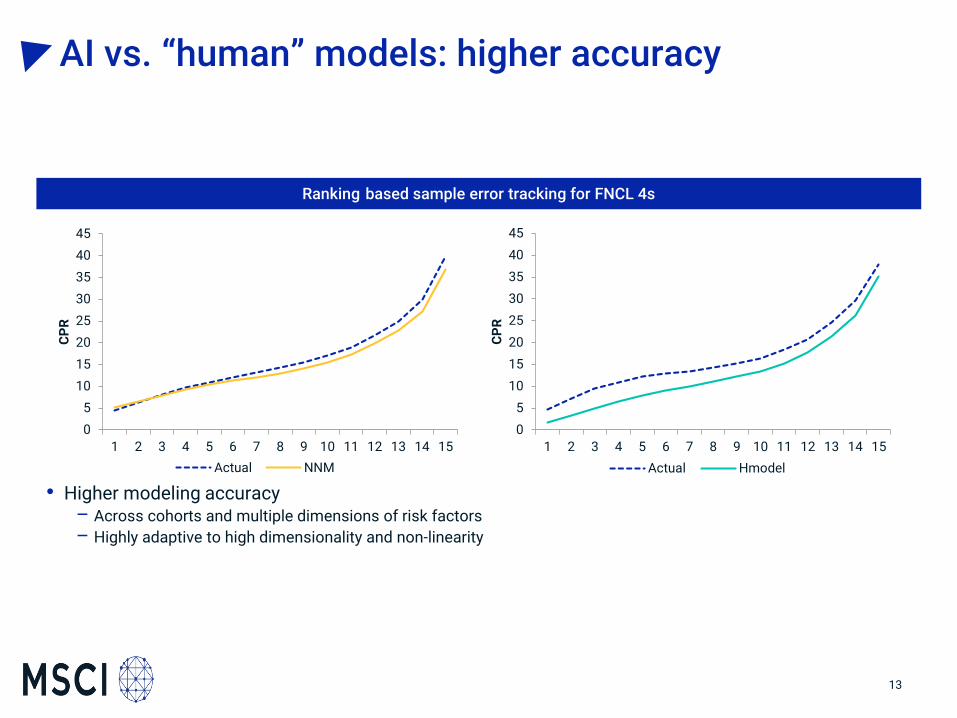

Ranking based sample error tracking for FNCL 4s

4545

4040

3535

3030

CP

R

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

CP

R 25

20

25

20

15

10

15

10

5 5

0 0

Actual NNM Actual Hmodel

• Higher modeling accuracy – Across cohorts and multiple dimensions of risk factors

– Highly adaptive to high dimensionality and non-linearity

13

MSCII

CP

R

AI vs. “human” models: higher accuracy

25 • “Media effect”

– When rates hit 20 historical low, new & lower coupons ramp

15 up faster

– Highly non-linear behavior and depends 10 on multiple risk factors

5

0

Ju

l-1

2

Se

p-1

2

No

v-1

2

Ja

n-1

3

Ma

r-1

3

Ma

y-1

3

Ju

l-1

3

Se

p-1

3

No

v-1

3

Au

g-1

2

Oc

t-1

2

De

c-1

2

Fe

b-1

3

Ap

r-1

3

Ju

n-1

3

Au

g-1

3

Oc

t-1

3

De

c-1

3

Ju

l-1

2

Se

p-1

2

No

v-1

2

Ja

n-1

3

Ma

r-1

3

Ma

y-1

3

Ju

l-1

3

Se

p-1

3

No

v-1

3

3.5 4 4.5

Actual NNM Hmodel

14

MSCII

AI vs. “human” models: new signals

60 1280

70 50 10

60

40 8 50

30

-10

0

-60

-40

-20

-10 0

10

20

30

40

30 6

0

20 4 8

0

20

10

0

10 2 10

12

0 0 0 0

14

0

16

0

20

0

24

0

CP

R

CP

R

CP

R

40

75k 100k 150k 200k 250k 300k 400k 500k

Incentive (bps)

75k 100k 150k 200k 300k 400k 500k 60 bps(LHS) -60 bps(RHS)

• Accuracy vs overfitting: loan size example – Understand sensitivities of risk drivers and economic rationale

– Apply regularization to penalize overfitting

6

15

MSCII

AI vs. “human” models: new signals

Model speeds for OTM 60bps vs loan size (in thousands) Housing turnover vs loan size and year*

12 0.80%

0.70% 10

0.60% 8

0.50%

6 0.40%

0.30% 4

0.20% 2

0.10%

0 0.00% 50 100 150 200 250 300 350 400 450 500 550

2005Yr 2012Yr <= 75k 76k-150k 151k-250k 251k-350k 351k+

• Is low loan balance still safe investment for extension risk?

– Sensitivity tests for the AI model indicate relationship between loan size and housing turnover has flipped after the recession

– This is verified by Black Knight’s proprietary data

* Source: Black Knight, used with permission 16

CONCLUSION

NN model vs. “Human Model”

• Accurate forecasts and successfully flag prepayment anomalies over the study period

• Accurate model large numbers of risk factors • Accurate model highly non-linear and interactive risk factors • Highly efficient modeling process - hundreds times of

increases in modeling efficiency • Was able to find/flag prepayment signals that eluded human

models

— GENERAL — 17

ACKNOWLEDGEMENT

Joy Zhang:

Executive Director, Securitized Product Research, MSCI

Jan Zhao:

Principal, Advanced Analytics, Ernst & Young

Fei Teng:

Senior Quantitative Analysts, Quantitative Advisory Services , Ernst & Young

Siyu Lin:

Senior Quantitative Analysts, Quantitative Advisory Services , Ernst & Young

Henry Li:

Executive Director, in Quantitative Advisory Services practice, Ernst & Young

— GENERAL — 18

Appendix

19

4: Agency MBS prepayment regimes since 2003

100

2003: historical l'ow

mortgage rates and

, refinancing wave ----FN 30 CPR/ Rate Incentive Bracket (Age= 10-30)

Mid 2004-,Mid 2006: Strong home price Mid 2007-2009: Severe

appreciation, (HPA), fast housing turnovet", high cash - home price depreciation

out refinancing and fast discount prepayment speed (HPD), low housing turnover,

2009: historical low mortgage

rates, but muted refinancing

_response.High premium coupons

prepay ever slower than, lower

premium coupons, because of 80 -----~--------------st------------ no cash out refinancing and

60 ct: Q. 0 40

20

0

Jan-03

MSCI •-

Aug-03 Mar-04

slow rate tet"m refinancing

Nov-04 Jun-05 Jan-06 Sep-06 Apr-07 Nov-07

Month

-(-50,-25) -(75,100) -(150,175)

- much tighter lending standard for

Jul-08 feb-09 Oct-09

MORTGAGE PREPAYMENT MODELING: SCIENCE AND CRAFTSMANSHIP

— GENERAL — 20

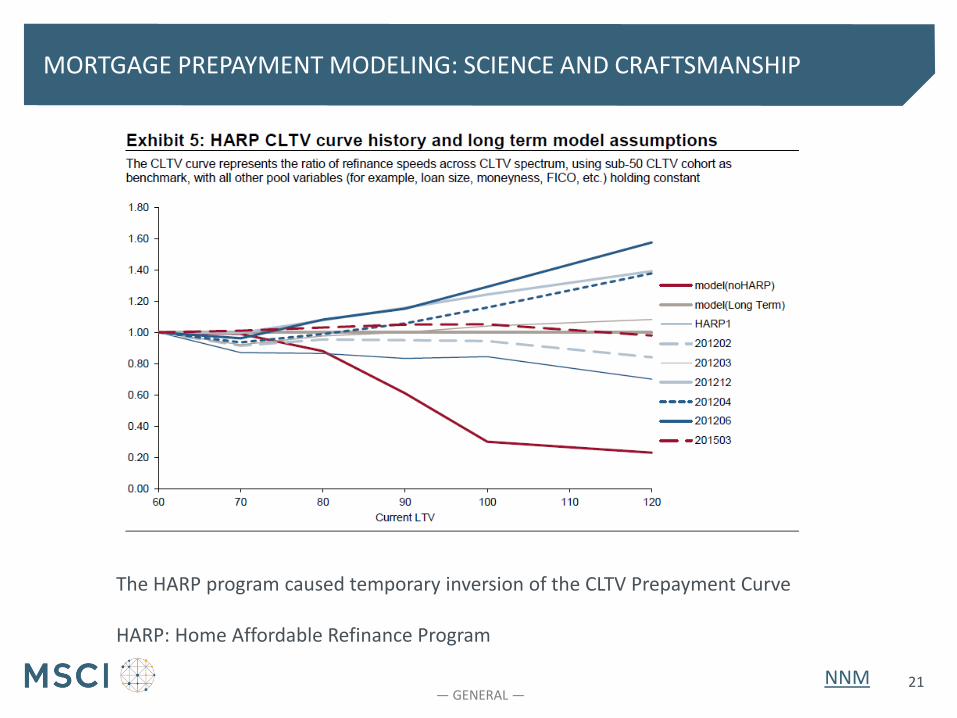

Exhibit 5: HARP CL TV curve history and long term model assumptions The CL TV curve represents the ratio of refinance speeds across CL TV spectrum, using sub-50 CL TV cohort as benchmark, with all other pool variables (for example, loan size, moneyness, FICO, etc.) holding constant

1.80

1.60

1.40

1.20

1.00

0.80

0.60

0.40

0.20

0.00 60

MSCI •-

70 80 90

Current LTV

-model(noHARP)

-model(Long Term)

--HARP1

- -201202

--201203

-201212

---•201204

-201206

~--------- - -201503

100 110 120

MORTGAGE PREPAYMENT MODELING: SCIENCE AND CRAFTSMANSHIP

The HARP program caused temporary inversion of the CLTV Prepayment Curve

HARP: Home Affordable Refinance Program

NNM 21 — GENERAL —

Q. u

100

80

60

40

20

0

40

30

!f 20 u

10

0

MSCI

V2002 Major Premium Coupons At 2003 Refi Wave In 2003 refi wave, nigher coupons prepay raster.

But in 2009 refi wave, higher coupons prepay lower e weake ccediLQi!J:Ual!!!!!J. f,.OQ!f..hd}!li ~rh~e:r..---===t~--'---------.....;::.,.. _________________ _

coupons was not much an issue in 2003's refi, but

rt become a big refi hurdle in 2009's refi.

Jan-03 Feb-03 Mar-03 Apr-03 May-03 Jun-03 Jul-03 Aug-03 Sep-03 Oct-03 Nov-03 Dec-03

Month

-5.5-6-6.5

V2008 Major Premium Coupons At 2009 Refi Wave

In 2003 refi wave,.,bigber cou oos rel'!!',,y.,fa.,,st,,e.,_c..,Be,,ut"-'-"inc,..--2.e.0,.,0..,9,_r._,e.:.,fi..,w"a"v_,.,e ___________________________ _

higher coupons prepay slower. The weaker credrt quality of higher coupons was not much an issue in 2003"s refi. but it become a big refi

hurdle in 2009's refi.

Jan-09 Feb-09 Mar-09 Apr-09 May-09 Jun-09 Jul-09 Aug-09 Sep-09 Oct-09

Month

-5.5-6-6.5

MORTGAGE PREPAYMENT MODELING: SCIENCE AND CRAFTSMANSHIP

— GENERAL — 22

35

30

25

.. C. 20 -u

15

1 0

5

0 "' "' ~ .. 9 0 0 0 a

.!.. I ' I

C: >, a. > Ill Ill (\) :::I

(l) 0 ..., :2i: ~ ...,

(/) z

FN30 6.0 V2004 CPR / Fico, (owner occ clsz=1 G0K-150 K oltv < 80)

■ Seasoned loan's FICO lending environment

■ :FICO beoomes less important after a few years' seasoning

IO I,() co <O <O r-- r-- r-- r-- r-- r- a:> co a 0 0 0 0 ~ 0 0 q 0 a a 0 0 0 0 0 ~ I .!.. I I I I

....!. > I .'.. I I I I ' ,c: >- a. > >- a. C: >- a. > C: (ti Ill Ill :::I (l) 0 (ti Ill :::I (l) 0 (ti (ti Ill :::I

(II 0 (\) (ti ..., :2i: ~ ...,

(/) z :2i: ~ ...,

(/) z ..., :a :!? ...,

(/J z ..., :a Ill 01 ,ti 1

■ Higher FICO prepays faster for new mortgages l--+-680-120 I ----> 720

MSCI •-

OJ a 0 0 0 9 a I I I ..!. ...!. >- a. > >, (ti QI 0 (\) <'O :,

:!? (/J z :i ~ ...,

MORTGAGE PREPAYMENT MODELING: SCIENCE AND CRAFTSMANSHIP

— GENERAL — 23

MORTGAGE PREPAYMENT MODELING: SCIENCE AND CRAFTSMANSHIP

Example of modeling: Assume ppm (pool, time) = f(X1, X2, X3,…. Xn) …

start by assuming separable risk factor: ppm= f1(x1)*f2(x2)…. Until (often) proven incorrect…

estimating f1(x1) by “building cohort”, by bucketing loans/pools for groups of x1, but similar x2, x3….

(this further assumes quasi linear property of x2, x3…. Average(f2(x2) f3(x3)…)= f2(ave(x2))* f3(ave(x3))….

….. Checking overall fit after all Xn are fitted, adding extra variables to deal with non-linear and interactive variables… this often does not lead to convergence …

• Time consuming and non-standard approaches • Experience and step-by-step / regime-by-regime progress are valued

• Can new techniques of AI modeling provide the much needed disruption?

— GENERAL — 24

neural network model

Architecture*

Input layer

!:1 !n !'.1 = mllll(tl.1;! I 8 1,0) :!:'.,, - m111<(A11r·,-1 + 8 11, 0)

Values ot hidden layP.rs are ~enerated hy ar.tivation futtctiu11s with previous layers as inputs, and weights and

biases as parameters

•Exampfe of a Neural Network architecture Q Node

MSCI •-

Mode~ training 1 Select a set of training data:

inputs tog~thP.r with correct/actual output

2 Pass trail'linq Al Model data through the network to obtain predidet.l output

t Tweak weiqt1Ls i:mu Ltiases using gradient function

Actual Output

Predicted Output

F eedforwa rd pass: compare ac:tual outp11t with predicted out rut and dP.termine cost function based on the error calqtlnted

MeP.ts Criteria?

~Ye• ·I 4 Backward propagation: oµlfrnize weiqhls am.I uiases (par c1meter s)

until some stopping condition has been met by passing the error signal through the network using gradien function

FEED FORWARD NEURAL NETWORK

Network architecture:

Layers and nodes

Hyper-parameters Batch size, number of nodes, learning rate, max-norm constraint, dropout rate

Ensemble techniques: Bagging: minimum MSE of different realizations and neural networks Boosting: Fine tune a neural network via changing a few hyper-parameters

— GENERAL —

MSCI

~ C: ro E .g (I) a...

Data Size

Large NN

Med um NN

Sma

Traditional ML algorith Statisbcal Leaming ms I

GENERAL

TRADITIONAL VS.. DEEP MACHINE LEARNING

Identify problems

Set benchmarks

Train models Compare

performance Choose model

Optimize model

Deploy

Traditional learning algorithm Deep Learning

Pros Cons Pros Cons

Works better on smaller data

Hard to scale state-of-the-art for certain domains, such as computer vision and speech recognition.

require large amount of data.

Financially and computationally cheap

Lack of variability Perform very well on image, audio, and textual data, Easily updated with new data

Not suitable for classical machine learning problems.

Algorithms are easier to interpret, have more theories to back them up

Labor intensive model maintenance

Versatile architecture and low overhead maintenance

Computationally intensive to train, and they require much more expertise to tune

— —

X1 W1 y(t) y(l) y(2) y(3)

X2

X3 out w =

wi Wo x(t) x(l) x(2) x(3)

Xo ~ Xi

MSCI •-

NEURAL NETWORKS MODEL

Feed forward neural network (FNN)

the information moves in only forward direction from the input nodes to the output nodes. There are no cycles or loops in the network.;

Deep FNN consists of tens of layers and thousands of nodes; the simplest kind of FNN is logistic model

Feedforward Neural Network Recurrent Neural Network Logistic Model

Recurrent Neural Network (RNN)

A class of neural networks exploit the historical input sequences. Such inputs could be text, speech, time series, and anything else where the occurrence of an input in the sequence is dependent on the inputs that appeared before it

Motivation: Not all problems can be converted into one with fixed length inputs and outputs, such as text translation, speech recognition or time-series; predictions require a system to store and use context information

The input at time t include both the attributes at t and the intermediate values containing history at t-1.

— GENERAL —

BUILDING NEURAL NETWORK MODEL

EDA Feature selection

Build model

Performance Evaluation

1, sanity check 1,information value 1,error tracking 1. link weights 2. data cleansing 2.correlation matrix 2.sensitivity 2. hyper-parameters 3. data transformation 3.domain knowledge 3. transparency tool (deeplift)

Deep neural network fitting

2003-2018 30yr agency MBS data (~25G data)

30+ input variables: pool attributes, macro-economic variables

To reduce complexity, we added incentive, 1 regime indicators, and 1 policy indicator (HARP)

Cost function of RMS error of pool level prepayment

1 round of fitting can be completed in ~ 3 hours on a GPU machine

— GENERAL —

MODEL DRIVERS

WALA Weighted Average Loan Age

WAC Weighted Average Coupon

CLNSZ Current Average Loan Size

OLTV Original Loan to Value

Refi% Percentage of Refinanced Loans by UPB

SecHome% Percentage of Second Home Loans by UPB

MultiFamily% Percentage of Muti Family Loans by UPB

Investor% Percentage of Investor Loans by UPB

TPO% Percentage of Third party origination by UPB

AOL Original Average Loan Size

LNSZ_Q4 Max original loan size

LNSZ_Q3 Max original Loan Size - 3rd Quartile

LNSZ_Q1 Max original Loan Size - 1st Quartile

Geo_CA% Percentage of California Loans by UPB

Geo_FL% Percentage of Florida Loans by UPB

Geo_TX% Percentage of Taxas Loans by UPB

Geo_NY% Percentage of New York Loans by UPB

Geo_NE% Percentage of New England Region Loans by UPB

Geo_NO% Percentage of North Region Loans by UPB

Geo_SO% Percentage of South region Loans by UPB

Geo_PC% Percentage of Pacific region Loans by UPB

Geo_AT% Percentage of Atlantic region Loans by UPB

Geo_NONUS% Percentage of non-US region Loans by UPB

Seasonality Calendar month

Independent variables

Incentive WAC - Mortgage Rate(t)

Rolling Incentive Average Incentive ( 20month)

Loan size dispersion (LNSZ_Q3-LNSZ_Q1)/AOL

SATO Spread-at_origination = WAC - Mortgage Rate(0)

HPA House Price Appreciation ( HPI(t)/HPI(0)-1 )

HARP-able

1: IssueMonth <= Jun. 2009 and factor date between Mar. 2009

and Dec. 2011

2: IssueMonth <= Jun. 2009 and factor date > Dec. 2011

HARP-ed Refi% = 100 and OLTV > 80 and issueMonth > Jun. 2009

Underwritting standard 0: before 2008, 1: after 2008

cBal Current Balance

Prepayment speed Prepayment speed in SMM

Derived Variables

Weight

Dependent Variable

— GENERAL — 29

~ tn n -

• l> ri ,-+ C ~

z z ~

I-' 0 0

Aug-03

Apr-04

Dec-04

Aug-05

Apr-06

Dec-06

Aug-07

Apr-08

Dec-08

Aug-09

Apr-10

Dec-10

Aug-11

Apr-12

Dec-12

Aug-13

Apr-14

Dec-14

Aug-15

CPR I',.) w .i:,. V, 0-, -...J 0 0 0 0 0 0

AG

ENC

Y 30

YR U

NIV

ERSE SP

EEDS ER

RO

R TR

AC

KIN

G

• Train

ing D

ata: 20

03

– 20

15

Dec. R

and

om

samp

le 10

% p

oo

ls. •

Error trackin

g is generated

usin

g ou

t-of-th

e-samp

le po

ols.

— G

ENER

AL —

3

0

MSCI •-

er:: c.. u

---- Actual --NNM ---Hmodel

OUT-OF-SAMPLE FORECASTS

• True out-of-time and out-of-sample test. • Overall fitting is good in out-of-sample test • Missed the refi wave in second half of 2016

— GENERAL — 31

-----------

MSCI •-

MODEL RISK FACTORS C

PR

30

25

20

15

10

5

0

0

10

20

30

40

50

60

CP

R

-1.5 -1 -0.5 0 0.5 1

720 740 760 780 720 740 760 780

Pre-2008 Post-2008

FICO SATO Actual NNM

Actual NNM

30

35 25

30 20

25 C

PR

20

15

15

CP

R

10

5

10

5

0

50000 100000 150000 200000 250000 300000 350000

Current Loan Size

0

55 65 75

CLTV

85 95 105

Actual NNM Actual NNM

— GENERAL — 32

30

25

o::: 20 c.. u 15

10

5

0 0.4

MSCI •-

-~~-~ ... ...... ...... ---~"" ........

0.6 0.8

...... ......

1

...... ...... ..... ..... .... .... ....

-----Actual

--NNM

1.2 1.4

Rolling Incentive

1.6

MODEL BURNOUT

NNM and actual prepayment speeds against average incentive in prior 20 months

— GENERAL — 33

~ tn n -

n )>

n ""Cl ;;o

z z s

I I 3 0 a. (1)

z -<

Jun-09

Apr-10

Feb-11

Dec-11

Oct-12

Aug-13

Jun-14

Apr-15

Feb-16

Dec-16

Oct-17

Oct-0

Aug-0

Jun-OS

Apr-06

Feb-07

Dec-07

Oct-08

Aug-09

Jun-10

Apr-11

Feb-12

Dec-12

Oct-13

Aug-14

Jun-15

Apr-16

Feb-17

Dec-17

CPR ~ N W ~ ~ m ~ 00

0 0 0 0 0 0 0 0 0

MO

DEL P

OO

L VA

RIA

BLES V

S “HU

MA

N”M

OD

EL

NN

M an

d H

mo

del Erro

r Tracking again

st State Variab

les

NN

M accu

rately captu

red state

-level prep

aymen

t beh

aviors

— G

ENER

AL —

3

4

45

40

35

30

a:: 25 Cl. u 20

15

10

5

---- ------,,' _,

, , , ,

I I

I I

I ,

0-+-----~~-~----~~-~----~~-1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

----Actual -NNM

MSCI •-

45

40

35

30

a:: 25 Cl. u 20

15

10

5

0

,, , ,, ----

--..... --------,

------, , , ,

I , I

I I

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

----Actual -Hmodel

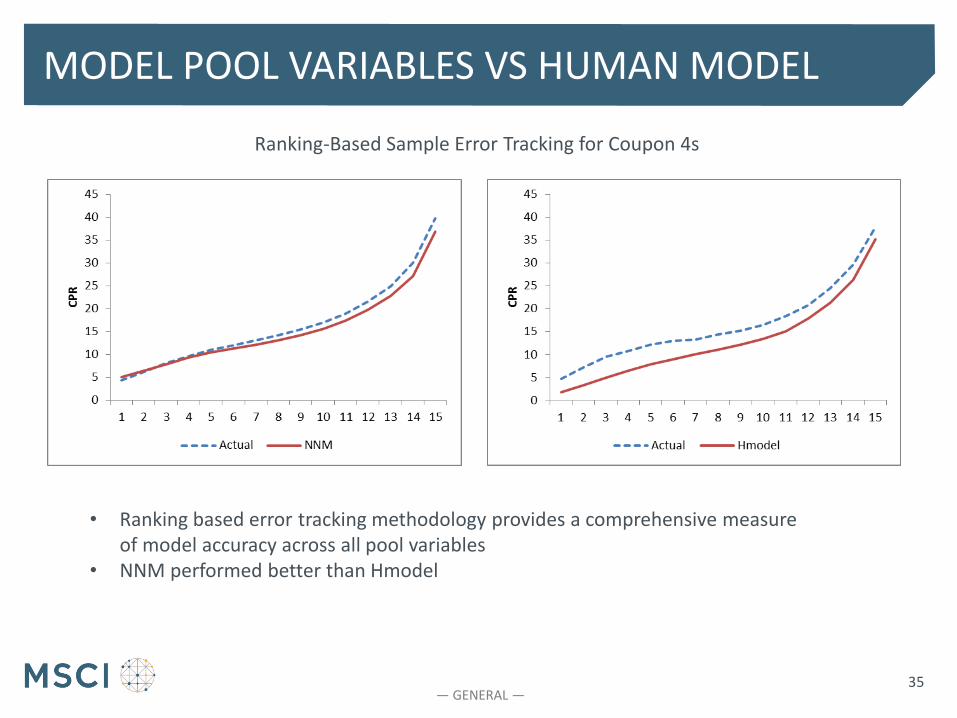

MODEL POOL VARIABLES VS HUMAN MODEL

Ranking-Based Sample Error Tracking for Coupon 4s

• Ranking based error tracking methodology provides a comprehensive measure of model accuracy across all pool variables

• NNM performed better than Hmodel

— GENERAL — 35

MSCI •-

50

40

50

40

o::: 30 Q..

u 20

----Actual -NNM

1 4 7 1013 3 6 9 1215 2 5 8 1114 1 4 7 1013 3 6 9 1215 2 5 8 1114

3.5 4 3.5 4 3.5 4

Jun-13 Jun-16 Mar-18

----Actual -Hmodel

1 4 7 1013 3 6 9 1215 2 5 8 1114 1 4 7 1013 3 6 9 1215 2 5 8 1114

3.5 4 3.5 4 3.5 4

Jun-13 Jun-16 Mar-18

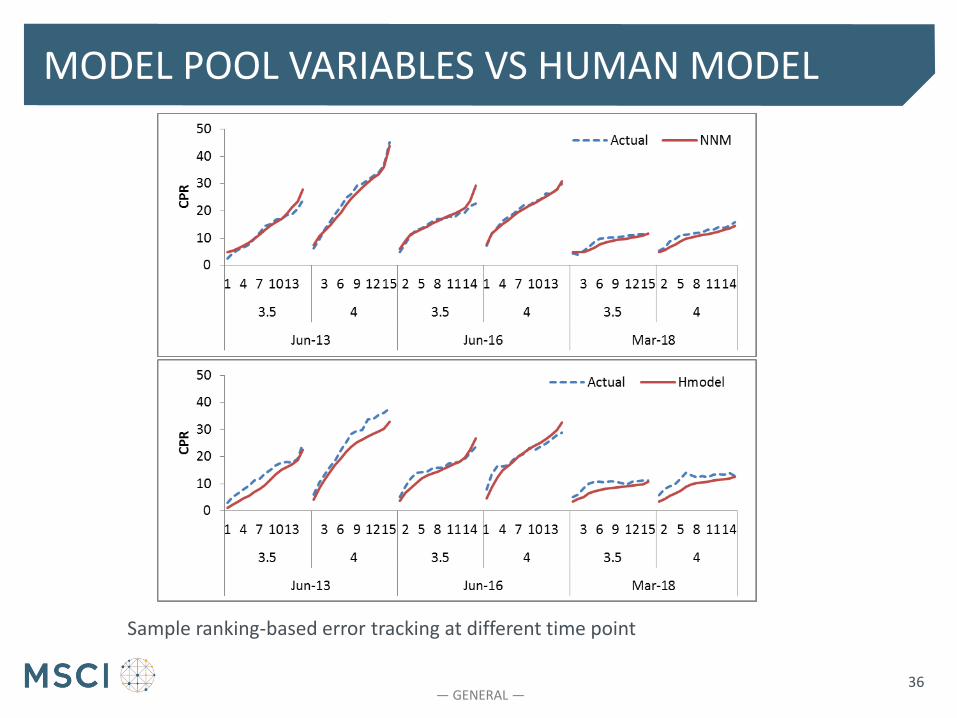

MODEL POOL VARIABLES VS HUMAN MODEL

Sample ranking-based error tracking at different time point

— GENERAL — 36

60

55 ' ' 50 ' '" ... -, 45 ';x:::J ~ ~ c.:: -Q. 40 ,

' u 35

30

25

20

60 80 9010 12 60 80 9010 12 60 80 9010 12

2012Q1 2012Q2 2012Q3 2012Q4

CLTV

----Actual NNM

MSCI •-

MODEL HARP EFFECTIVENESS

Error Tracking against HARP effectiveness across CLTV Cohorts

NNM is able to pick up the general trend of HARP effectiveness but missed the complexity of its revolution

Back 37

— GENERAL —

80

70

60

so f 40 u

30

20

10 l ...... ,.~~~~,,,t.,..... 0 ---t---.----.----.---.--.----.----.~~~~~~~--.----.---~

MSCI •-

-100 -40 -10 10 30 60 100 140 200

Incentive (bps)

~7Sk -100k-a-1SOk~200k

-300k-+-400k-SOOk

60 12

so 10

40 8

f 30 6 a: Cl.

u u

20 4

10 2

0 ---t-----.-~~~~--.---~--.-----+ 0

~ _c-.'4.-~'4.- r;:f- ~'4.- f::)'4.-_c-.'4.-r;:f-"\ ""\)-~ '"1-o '"I-<-, ,,_,o ~\)-~o

-60 bps(LHS} -.--60 bps(RHS}

MODEL SENSITIVITY

Model prepayment sensitivity to loan sizes and refinance Incentives

NNM captured the prepayment behavior for loan size

— GENERAL — 38

~ tn n -

w 0 -< :-, "Tl

X m a.. ~ 0 -, r-t-

C]Q QJ

C]Q m :::0 QJ r-t-m

Jan-10

Jun-10

Nov-10

Apr-11

Sep-11

Feb-12

Jul-12

Dec-12

May-13

Oct-13

Mar-14

Aug-14

Jan-15

Jun-15

Nov-15

Apr-16

Sep-16

Feb-17

Jul-17

Dec-17

May-18

w w .i:,. .i:,. V, V,

0 V, 0 V, 0 V,

w 0 < :"I 'Tl ~-c.. s 0 ""'II ,...

OQ Q)

OQ t1)

::a Q) ,... t1)

“MED

IA EFFEC

T”

Co

hort

Ob

servation R

angeC

PR

WA

LA

SA

TO

CL

TV

CL

NS

ZIncentive

FIC

OA

vg.UP

B(b

n)

FH

3.5

20

11

Jul.12

- Dec. 1

21

6.1

13

-577

212258

52

770

2.9

1

FH

4 2

010

No

v. 11

- Feb

. 12

13.9

15

378

201901

45

767

6.2

6

FH

3.5

20

11

Jul.20

12

- Dec. 1

22

1.9

12

-376

235847

50

770

4.0

4

FH

4 2

010

No

v. 11

- Feb

. 12

16.4

16

378

224734

45

765

8.6

6

FH

3.5

20

11

Jul.12

- Dec. 1

22

9.2

12

-266

216270

54

771

7.3

1

FH

4 2

010

No

v. 11

- Feb

. 12

15.3

15

11

70

208962

52

766

30.8

9

FH

3.5

20

11

Jul.12

- Dec. 1

24

6.1

12

-864

269298

46

773

9.5

8

FH

4 2

010

No

v. 11

- Feb

. 12

26.2

15

269

245496

44

767

23.0

2

Refi/T

PO

FH

20

11

3.5

vs 20

10

4 co

mp

arisons, acro

ss TP

O/R

etail and R

efi/Purchase co

mb

inations

Purchase/R

etail

Purchase/T

PO

Refi/R

etail

20

11

3.5

s and

20

10

4s p

repaym

ent sp

eeds

are com

pared

across lo

an attrib

utes, lo

an

pu

rpo

se and

origin

ation

chan

nel

3.5

s is mu

ch faster th

an 4

s given sim

ilar lo

an attrib

utes an

d in

centive

— G

ENER

AL —

3

9

~ tn n CPR

f-'> f-'> N N - 0 V, 0 V, 0 V,

~h Jul-12

Oct-12

Jan-13

' VJ Apr-13

)> V, ("') Jul-13 -C (l)

Oct-13

Sep-12

z Dec-12 z Mar-13 ~ .i:,.

Jun-13

Sep-13

Dec-13 I

Aug-12 3 0

Nov-12 Q. ~

.i:,. Feb-13 V,

May-13 I ""> "'~ Aug-13

Nov-13

CPR f-'> f-'> N N VJ

0 V, 0 V, 0 V, 0

--1

May-16 Sep-16

VJ Jan-17 ' V, )> May-17

("') - Sep-17 C (l)

Jan-18

Apr-16

z Aug-16

z Dec-16 ~ .i:,. Apr-17

Aug-17 Dec-17 Ai;ir-18

I Mar-16 3 0 Jul-16 Q. ~-, ~ Nov-16 s.

.i:,. V, Mar-17

Jul-17 ~i-Nov-17

Mar-18 ~, -..

MO

DEL “M

EDIA

EFFECT

”

20

12

Vin

tage in 2

01

2 refin

ance w

ave 2

01

5 V

intage in

20

16

refinan

ce wave

— G

ENER

AL —

4

0

~ tn n -

..., ...,.. N Nm ..... rvw.::..v,~" a,

! """" 0 • 0 • 0 • H I ::::f I ff I 11 I H 20160201 3 "' 20040401 3 "

20160301 §: ~ 20040801 §: r;'

20160401 ~ 8 20041201 0 ~ " 20050401 ,l ~

20160501 20050801

20160601 20051201

20160701 20060401 20060801

20160801 20061201

20160901 20070401

20161001 2oo7os01 20071201

20161101 20080401

20161201 20080801

20170101 20081201 20090401

20170201 20090801

20170301 20091201

20170401 20100401 20100801

20170501 20101201

20170601 20110401

20170701 20110801 20111201

20170801 20120401

20170901 20120801

20171001 20121201 20130401

20171101 20130801

20171201 20131201

20180101 20140401

20180201 20140801 20141201

20180301 201S0401

20180401 201S0801 20151201

I ! I I I i ~ ~ s: ► Q. i; Q ~ ;!; ;:; it &. -,:, -o r, n :::0 ;Q "0 "0

:,:, :,:,

MO

DEL ER

RO

R TR

AC

KIN

G

In-tim

e O

ut-o

f-samp

le (1

/20

03

-12

/20

15

)

1.

All attrib

utes statistics are very

close o

n Ju

ly and

Au

gust 2

01

6

except C

PR

. 2

. R

isk driver is m

issing, i.e., m

edia

effect or regim

e chan

ge

Ou

t-of-tim

e O

ut-o

f-samp

le (1

/20

16

-4/2

01

8)

— G

ENER

AL —

4

1

~ tn n -

;'~O ONAO'!OO

" "'6' -----,v 0,._,,AC"+COO

!!. .. ✓• ~ rl q, ,. o✓•

6''Y, rl q, o.,,_.o

rl :;,~ o.,,..,,

orl rl ~ o.,,

->o.,,. rl ~ o.,,

:..>4. rl ~ o.,,

->a ~ ~ o.,,..,,

rl~ o.,,_.o rl :>~ o.,,..,, ~

rl ~ o.,, .>~

rl v.,, o.,,:.>

rl ,l~ o.,, ~

rl ,l~ o.,,:.>

'Y, rl ~ o✓, d'o ~ :;,~ o✓•

d'orl rl ~ o✓,

d'o.,,. ~ ~ o✓•

d'q,. ~

)

/ vj ~v

j~

\ I

'I

~

f

I I ' ;:: ► ll

~ [ ,.., ,.., .,, .,, :,0 :,0

V /

)

J

~ I IL <

i f I . j f

! oo~~~~E~>

s. 20030801 ~ I I I I I "I I i M 20040101

• 20040601

20041101

20050401

20050901

20060201

20060701

20061201

20070501

20071001

20080301

20080801

20090101

20090601

20091101

20100401

20100901

20110201

20110701

20111201

20120501

20121001

20130301

20130801

20140101

20140601

20141101

20150401

20150901

20160201

20160701

I I f .:: >

i [ ,.., ,.., .,, .,, :,0 :,0

MO

DEL ER

RO

R TR

AC

KIN

G

In-tim

e O

ut-o

f-samp

le (1

/20

03

-10

/20

16

)

Ou

t-of-tim

e O

ut-o

f-samp

le (1

1/2

01

6-4

/20

18

)

— G

ENER

AL —

4

2

~ tn n -

I :::o, °" .. • • " " • • • H I ::::f j . . . j j i H "o,., ~ 20040601 ~ •

"0.t_,0 !i ~ 20041101 1! I~ .,0 "o,., i '§ 20050401 ~ 1'§

..-_,od 20050901 .>0 .,,., 20060201

"'>o.,,0 20060101

<'o " 20061201 .,_, 40 20070501 ~... ~~

d 0-£>,., 20080301 .,,.,_, 20080801

.>0 %,., 20090101

">o_,. 20090601

<'o ".t 20091101 ;,_, ~ 20100401

"o,.,_, " 20100901 d' rn~ ~ ~~

d 'b✓ 20111201 0 .,.,,., 20120501

~~ ~~ "'>,.,.,o 20130301

<'o " 20130801 "e. 0.to 20140101 d ;, ".tc90 20140601

d ?o✓ 20141101

".tc90 20150401 ::,i

~ ~ 2M50901

"d'4; 20160201 0,., 20160701

0 1 • -1,(

I If I I l ;:: l> f l> 2 ll ll &" & & ;:;r, nn -i::i ""Cl "Cl ~ :,:i,::, :,::,;o

MO

DEL ER

RO

R TR

AC

KIN

G

In-tim

e O

ut-o

f-samp

le (1

/20

03

-10

/20

16

)

Wh

en In

crease weigh

ts on

8

/20

16

– 10

/20

16

by 4

0 tim

es in

trainin

g: 1

. B

etter in th

e early stage o

f ou

t-of-tim

e test 2

. Sacrifice o

ther p

eriod

.

Ou

t-of-tim

e O

ut-o

f-samp

le (1

1/2

01

6-4

/20

18

)

— G

ENER

AL —

4

3

MSCI

Budcet Value • Coupon •

Aclllal CPR Model CPR

70 ..-------------------------------------

60 +-------------------------------------50-tt-------------------------------------

40 ------------------------------------------

30 +1-~1----------------,..----':'"'ll,,-r-----------

20 t--'V--bl5H~t::----------l~Ht-r-#--¼-----,1i------¼----,,.----k--

10 -l------¥~'1¥-!!ilic::,l-~+---------...:!l..,.~l!-....::l"'---\,,ey.

0 tt,Tmmmm"lffl'ITTTTTmTTmmmm....,'TfflTTTTTTffl"IT'mmmm'fflTTTTTTTmTTmmmm"lffl'ITTTTTfflTTfflTTmm....,TTTTTTTTTTmmmmmm'fflTTfflffmmm"f

Fac!O<Oale •

Budcet Value • Coupon •

Aclllal CPR Model CPR

12

8

6+-------------------------------------4

0+--------------~-----~------~------~------~ 20171101

Fac!O<Oale •

20171201 20180101 20180201 20180301 20180401

Values

--Actual CPR

-Model CPR

Values

--Actual CPR

-Model CPR

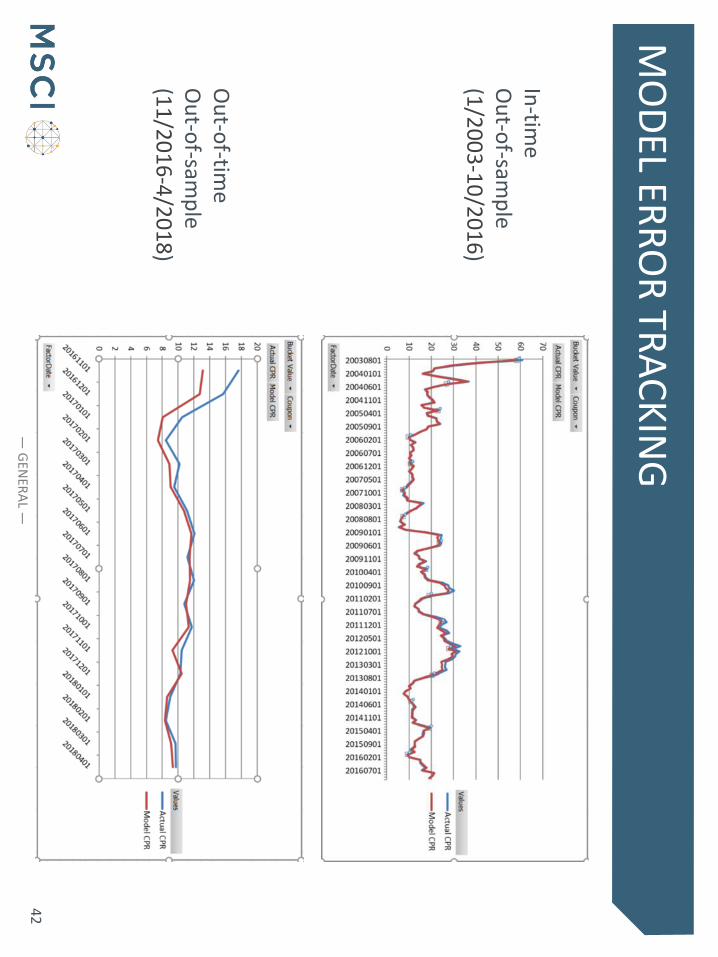

MODEL ERROR TRACKING

In-time Out-of-sample (1/2003-10/2017)

Out-of-time Out-of-sample (10/2017-4/2018)

— GENERAL — 44

MSCII

About MSCI

MSCI is a leading provider of critical decision support tools and services for the

global investment community. With over 45 years of expertise in research, data

and technology, we power better investment decisions by enabling clients to

understand and analyze key drivers of risk and return and confidently build

more effective portfolios. We create industry-leading research-enhanced

solutions that clients use to gain insight into and improve transparency across

the investment process. To learn more, please visit www.msci.com.

45

MSCII

Contact us

AMERICAS EUROPE, MIDDLE EAST ASIA PACIFIC & AFRICA

Americas +1 888 588 4567 * Cape Town + 27 21 673 0100 China North 10800 852 1032 *

Atlanta + 1 404 551 3212 Frankfurt + 49 69 133 859 00 China South 10800 152 1032 *

Boston + 1 617 532 0920 Geneva + 41 22 817 9777 Hong Kong + 852 2844 9333

Chicago + 1 312 675 0545 London + 44 20 7618 2222 Mumbai + 91 22 6784 9160

Monterrey + 52 81 1253 4020 Milan + 39 02 5849 0415 Seoul 00798 8521 3392 *

New York + 1 212 804 3901 Paris 0800 91 59 17 * Singapore 800 852 3749 *

San Francisco + 1 415 836 8800 Sydney + 61 2 9033 9333

São Paulo + 55 11 3706 1360 Taipei 008 0112 7513 *

Toronto + 1 416 628 1007 Thailand 0018 0015 6207 7181 *

Tokyo +81 3 5290 1555

• = toll free

msci.com [email protected]

46

MSCII

Notice & disclaimer

This document and all of the information contained in it, including without limitation all text, data, graphs, charts (collectively, the “Information”) is the property of MSCI Inc. or its subsidiaries (collectively, “MSCI”), or MSCI’s licensors, direct or indirect suppliers or any third party involved in making or compiling any Information (collectively, with MSCI, the “Information Providers”) and is provided for informational purposes only. The Information may not be modified, reverse-engineered, reproduced or redisseminated in whole or in part without prior written permission from MSCI.

The Information may not be used to create derivative works or to verify or correct other data or information. For example (but without limitation), the Information may not be used to create indexes, databases, risk models, analytics, software, or in connection with the issuing, offering, sponsoring, managing or marketing of any securities, portfolios, financial products or other investment vehicles utilizing or based on, linked to, tracking or otherwise derived from the Information or any other MSCI data, information, products or services.

The user of the Information assumes the entire risk of any use it may make or permit to be made of the Information. NONE OF THE INFORMATION PROVIDERS MAKES ANY EXPRESS OR IMPLIED WARRANTIES OR REPRESENTATIONS WITH RESPECT TO THE INFORMATION (OR THE RESULTS TO BE OBTAINED BY THE USE THEREOF), AND TO THE MAXIMUM EXTENT PERMITTED BY APPLICABLE LAW, EACH INFORMATION PROVIDER EXPRESSLY DISCLAIMS ALL IMPLIED WARRANTIES (INCLUDING, WITHOUT LIMITATION, ANY IMPLIED WARRANTIES OF ORIGINALITY, ACCURACY, TIMELINESS, NON-INFRINGEMENT, COMPLETENESS, MERCHANTABILITY AND FITNESS FOR A PARTICULAR PURPOSE) WITH RESPECT TO ANY OF THE INFORMATION.

Without limiting any of the foregoing and to the maximum extent permitted by applicable law, in no event shall any Information Provider have any liability regarding any of the Information for any direct, indirect, special, punitive, consequential (including lost profits) or any other damages even if notified of the possibility of such damages. The foregoing shall not exclude or limit any liability that may not by applicable law be excluded or limited, including without limitation (as applicable), any liability for death or personal injury to the extent that such injury results from the negligence or willful default of itself, its servants, agents or sub-contractors.

Information containing any historical information, data or analysis should not be taken as an indication or guarantee of any future performance, analysis, forecast or prediction. Past performance does not guarantee future results.

The Information should not be relied on and is not a substitute for the skill, judgment and experience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. All Information is impersonal and not tailored to the needs of any person, entity or group of persons.

None of the Information constitutes an offer to sell (or a solicitation of an offer to buy), any security, financial product or other investment vehicle or any trading strategy.

It is not possible to invest directly in an index. Exposure to an asset class or trading strategy or other category represented by an index is only available through third party investable instruments (if any) based on that index. MSCI does not issue, sponsor, endorse, market, offer, review or otherwise express any opinion regarding any fund, ETF, derivative or other security, investment, financial product or trading strategy that is based on, linked to or seeks to provide an investment return related to the performance of any MSCI index (collectively, “Index Linked Investments”). MSCI makes no assurance that any Index Linked Investments will accurately track index performance or provide positive investment returns. MSCI Inc. is not an investment adviser or fiduciary and MSCI makes no representation regarding the advisability of investing in any Index Linked Investments.

Index returns do not represent the results of actual trading of investible assets/securities. MSCI maintains and calculates indexes, but does not manage actual assets. Index returns do not reflect payment of any sales charges or fees an investor may pay to purchase the securities underlying the index or Index Linked Investments. The imposition of these fees and charges would cause the performance of an Index Linked Investment to be different than the MSCI index performance.

The Information may contain back tested data. Back-tested performance is not actual performance, but is hypothetical. There are frequently material differences between back tested performance results and actual results subsequently achieved by any investment strategy.

Constituents of MSCI equity indexes are listed companies, which are included in or excluded from the indexes according to the application of the relevant index methodologies. Accordingly, constituents in MSCI equity indexes may include MSCI Inc., clients of MSCI or suppliers to MSCI. Inclusion of a security within an MSCI index is not a recommendation by MSCI to buy, sell, or hold such security, nor is it considered to be investment advice.

Data and information produced by various affiliates of MSCI Inc., including MSCI ESG Research LLC and Barra LLC, may be used in calculating certain MSCI indexes. More information can be found in the relevant index methodologies on www.msci.com.

MSCI receives compensation in connection with licensing its indexes to third parties. MSCI Inc.’s revenue includes fees based on assets in Index Linked Investments. Information can be found in MSCI Inc.’s company filings on the Investor Relations section of www.msci.com.

MSCI ESG Research LLC is a Registered Investment Adviser under the Investment Advisers Act of 1940 and a subsidiary of MSCI Inc. Except with respect to any applicable products or services from MSCI ESG Research, neither MSCI nor any of its products or services recommends, endorses, approves or otherwise expresses any opinion regarding any issuer, securities, financial products or instruments or trading strategies and MSCI’s products or services are not intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Issuers mentioned or included in any MSCI ESG Research materials may include MSCI Inc., clients of MSCI or suppliers to MSCI, and may also purchase research or other products or services from MSCI ESG Research. MSCI ESG Research materials, including materials utilized in any MSCI ESG Indexes or other products, have not been submitted to, nor received approval from, the United States Securities and Exchange Commission or any other regulatory body.

Any use of or access to products, services or information of MSCI requires a license from MSCI. MSCI, Barra, RiskMetrics, IPD and other MSCI brands and product names are the trademarks, service marks, or registered trademarks of MSCI or its subsidiaries in the United States and other jurisdictions. The Global Industry Classification Standard (GICS) was developed by and is the exclusive property of MSCI and Standard & Poor’s. “Global Industry Classification Standard (GICS)” is a service mark of MSCI and Standard & Poor’s.

47