afrox investor & analyst presentation half-year results 2016

TRANSCRIPT

2

1. Performance Summary

2. Performance Drivers

3. Afrox Financial Results Analysed

4. Turnaround Update

5. Key Project Update & Outlook

6. Appendices

Presentation Outline

3

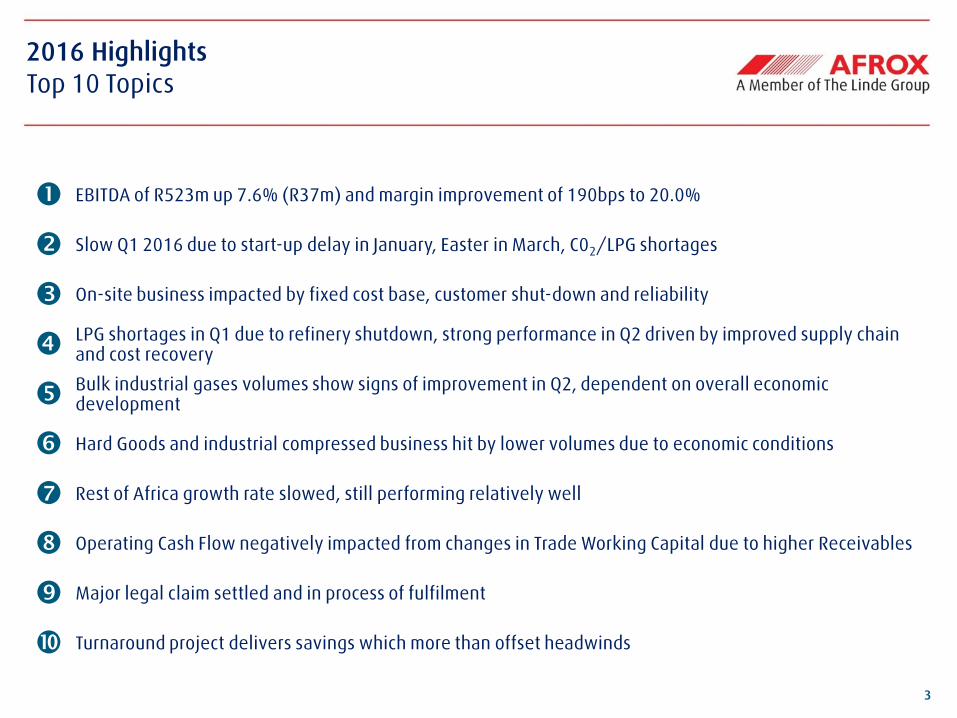

2016 Highlights

Top 10 Topics

EBITDA of R523m up 7.6% (R37m) and margin improvement of 190bps to 20.0%

Slow Q1 2016 due to start-up delay in January, Easter in March, C02/LPG shortages

On-site business impacted by fixed cost base, customer shut-down and reliability

LPG shortages in Q1 due to refinery shutdown, strong performance in Q2 driven by improved supply chain and cost recovery

Bulk industrial gases volumes show signs of improvement in Q2, dependent on overall economic development

Hard Goods and industrial compressed business hit by lower volumes due to economic conditions

Rest of Africa growth rate slowed, still performing relatively well

Operating Cash Flow negatively impacted from changes in Trade Working Capital due to higher Receivables

Major legal claim settled and in process of fulfilment

Turnaround project delivers savings which more than offset headwinds

4

31

25

28

22

8

6

8 8

2009 2010 2011 2012 2013 2014 2015 2016

SHEQ Performance

Significant MIR Reduction since 2009

¹ A MIR is an incident with a major outcome and consequences which represents a significant

non-compliance with Afrox's Safety, Security, Health, Environment and Quality (SHEQ) Policy

MIR Trend Comments

- MIRs¹ decreased by over 70% between

2013-2016 compared to the period 2009-2012

- Over 60% of the MIRs in 2016 are related to

security incidents

- Lost Time Injury (LTI) increased from 9 in 2015 to

11 in 2016 (YTD)

- 45% of the LTIs in 2016 are related to manual

handling

- Truck Severity level 1 and 2 decreased from 6 in

2015 to 2 in 2016 (YTD)

- Our SHEQ programmes are continuously

monitored and adapted to focus on improvement

in safe driving, manual handling and security

H1 2016

Performance Drivers

6

Progress Against Strategic Topics

By Business Segment

Prev. Latest

Atmospheric Gases Increase EBITDA from restructure

New CO2 sources

Increase asset utilisation and reliability

Go-to-market strategy

Growth in new applications

Price recovery 100% of cost inflation

LPG Leading margin management

Security of supply

Return on investment in cylinders

Go-to-market model relative to industrial gases

Ongoing focus on controlling illegal fillers and risk

Rest of Africa Reduce supply chain costs and increase customer supply security

Infrastructure in place for growth

Ensure critical mass per country and improvement in governance

Sales capability development

Hard Goods Optimise inventory

Right size fixed costs to throughput

Grow and defend volumes

Not started Work in progress Complete

7

Security of LPG Supply

¹ Bidvest Tanker Terminals (BTT), Richards Bay

- BTT¹ import commitment of 24 000 tons p/a with

ability to increase to 64 000 tons p/a according to

demand

- Additional investment in LPG bulk storage and

cylinders

- Logistics capability, vehicle and filling

infrastructure optimised

- Ability to support SA and Rest of Africa growth

- Management of import premium, resulting in full

cost recovery

8

Afrox Financial Results Analysed

9

Performance 30 June 2016

Highlights

¹ w/o positive effect from LPG market prices underlying revenue declined by –3%

ZARm H1 2015 H1 2016 YoY

Revenue 2 679 2 616 -2.3%¹

EBITDA 486 523 +7.6%

EBITDA margin 18.1% 20.0% +190bps

Operating cash flow 285 17 -94.0%

Headline EPS (cents) 37.4 76.5 +104.5%

Reported EPS (cents) 35.0 77.8 +122.3%

ROCE 16.6% 18.6% +200bps

- Market conditions and supply constraints impacted revenue development

- EBITDA growth in difficult trading conditions reflects benefits from restructuring initiatives

- Positive EBITDA margin development from restructuring

- Cash Flow reflects higher dividend, tax payments and increased Trade Working Capital

- ROCE improvement driven by higher profits and balance sheet optimisation

10

Business Performance

Lower revenues and reduction in GPADE due to volume decline

¹ Numbers shown on an adjusted basis with segments adjusted to align with how businesses are managed, & allocation of costs between businesses have been updated to better reflect

the split of operational costs | 2 GPADE is gross profit after distribution expenses

* Excluding change in market LPG prices

Atmospheric Gases LPG Hard Goods Rest of Africa

GPADE1,2

% Margin

Revenue1

2015 2016

1,050 1,044 862 852

2015 2016

400

336

2015 2016

367 384

2015 2016

366 335

2015 2016

163 185

2015 2016

148

114

2015 2016

163 162

2015 2016

-1% -1% -16% +5%

-8% +13%

-23% -1%

-3%*

34.8% 32.1% 18.8% 21.7% 37.1% 33.9% 44.4% 42.1%

11

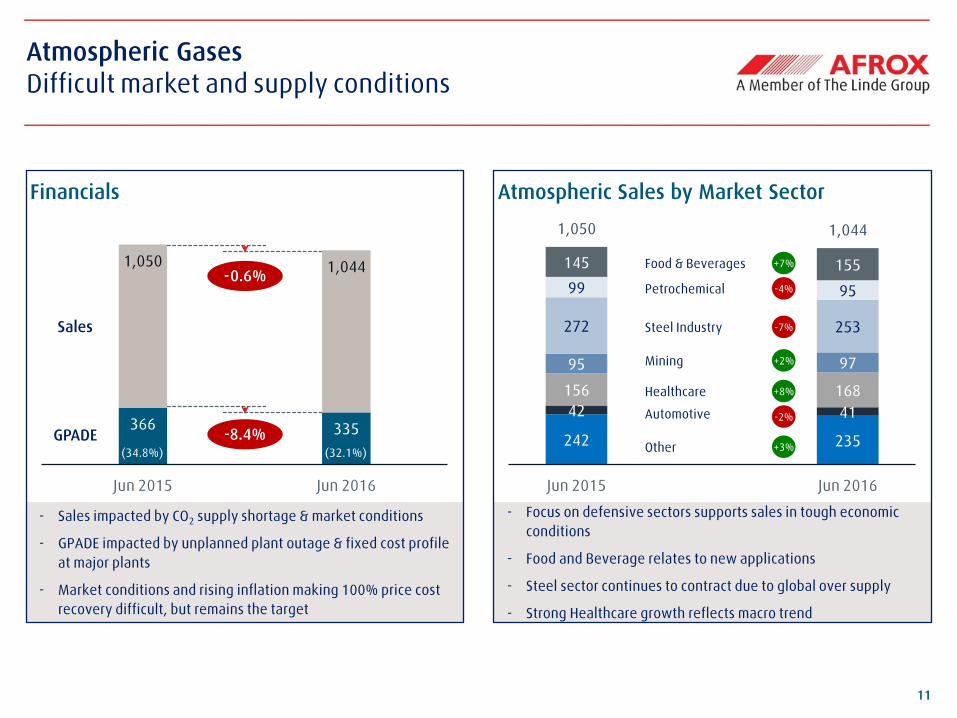

- Focus on defensive sectors supports sales in tough economic

conditions

- Food and Beverage relates to new applications

- Steel sector continues to contract due to global over supply

- Strong Healthcare growth reflects macro trend

Atmospheric Sales by Market Sector

242 235

42 41

156 168

95 97

272 253

99 95

145 155

1,050 1,044

Jun 2015 Column1 Jun 2016

366 335

1,050 1,044

Jun 2015 Jun 2016

- Sales impacted by CO2 supply shortage & market conditions

- GPADE impacted by unplanned plant outage & fixed cost profile

at major plants

- Market conditions and rising inflation making 100% price cost

recovery difficult, but remains the target

Atmospheric Gases

Difficult market and supply conditions

Financials

Sales

GPADE -8.4% (34.8%) (32.1%)

-0.6%

Automotive

Other

Healthcare

Mining

Steel Industry

Petrochemical

Food & Beverages +7%

-4%

-7%

+2%

-2%

+3%

+8%

12

163 185

862 852

Jun 2015 Jun 2016

23 25 25

39 37 36

62 62 60

Jun 2014 Jun 2015 Jun 2016

- Q1 saw supply shortages impact volume and increase supply

chain costs

- Q2 new supply contract and better PCR, and well position for H2

2016

- GPADE growth reflects supply chain cost savings and good price

cost recovery

Financials

Sales

GPADE

+13.6%

(18.8%) (21.7%)

-1.2%

LPG

Higher margin due to improved supply chain

* Excluding change in market LPG prices

Volume (KT) development 2014-2016

-3.0%*

Cylinder

Bulk

+0.5% -2.8%*

6

8

10

12

14

16

18 Margin per ton development Jan-13 to Jun-16

13

148

114

400

336

Jun 2015 Jun 2016

Hard Goods

Impacted by slowdown in mining industry

Financials Performance

- Volumes continue to be impacted by lower

demand in manufacturing and from strong

downturn in mining

- Shedding low margin business and rationalising

SKUs

- Pricing under pressure as some markets contract

while costs impacted by ZAR declines

- Outsourcing gas equipment manufacturing has

supported margins in this lower volume

environment

Sales

GPADE

-15.9%

-23.2%

(37.1%) (33.9%)

14

163 162

367 384

Jun 2015 Jun 2016

- Reported financials impacted by effects of Angola exit, LPG pass

through, currency translation effects and changes in stock

provisions

- Underlying Sales up 6.0% & GPADE down 2.8%

Rest of Africa

Performance impacted by portfolio change and LPG shortages

*Underlying financials excluding the impact of LPG pass through, currency translation, exit from Angola and stock provision changes

Financials Underlying performance

- Volumes holding up despite economic headwinds

- Margins declined due to very high inflation in

Zambia

- CO2 shortage in SA impacted margins into Zambia

and Malawi which are now resolved

- Currencies getting more volatile leading to high

imported inflation and frequent price increases

- Underlying Financials excluding the impact of LPG

pass through, currency translation, exit from

Angola and stock provision changes

Sales

GPADE

+4.6%

-0.8%

(44.4%) (42.1%)

+5.9%*

-2.8%*

15

555

458

Jun 2015¹ Jun 2016

Dec 2014 Jun 2015 Dec 2015 Jun 2016

- FTE reductions in line with turnaround plan

- Consolidation of head office implemented

- New procurement polices in place

- Outsourced fleet and implemented shared service centre

FTE development Other operating expenses

Other Operating Expenses & FTE development

Effects of turnaround materialised

-17.0%

(37.1%) (33.9%)

1 June 2015 excl. cost for restructure

-24%

16

Financial Performance H1: Key Indicators

Financial position remaining strong

Cash flow H1 2015 vs. H1 2016 June financial KPIs

- Free cash flow impacted by higher taxes, dividend payments and change in W/C

- Net debt ratio continues to improve relative to EBITDA

- Strong balance sheet with undrawn facilities

- ROCE improvement from higher profits

ZARm 2015 2016 ∆ in %

Operating cash flow 285 17 -94.0%

Investments (136) (112) 17.6%

Free cash flow 149 (95)

Cash at the end

of the period

646

757

16.3 14.4 12.9

16.6 18.6

2012 2013 2014 2015 2016

ROCE

0.8 0.7

0.6 0.63

0.3 Net debt/

EBITDA

17

Turnaround Update

18

Get healthy

- Introduce leaner organisation

- Rightsize operations*

- Better utilise assets*

- Outsource non-core operations

- More effective procurement

processes*

- Best commercial practice (BCP)

pricing composition

Turnaround Plan

Balanced channels and business portfolio

1

Completed

Get strong

- New customer centric operating

model

- Increase effectiveness &

efficiency of traditional

channels

- Introduction of eCommerce &

EDI

- Portfolio management

- BCP price cost recovery

2

In progress

Get business

- Grow Rest of Africa

- Grow LPG

- Grow Healthcare

- Grow Special Gases

3

19

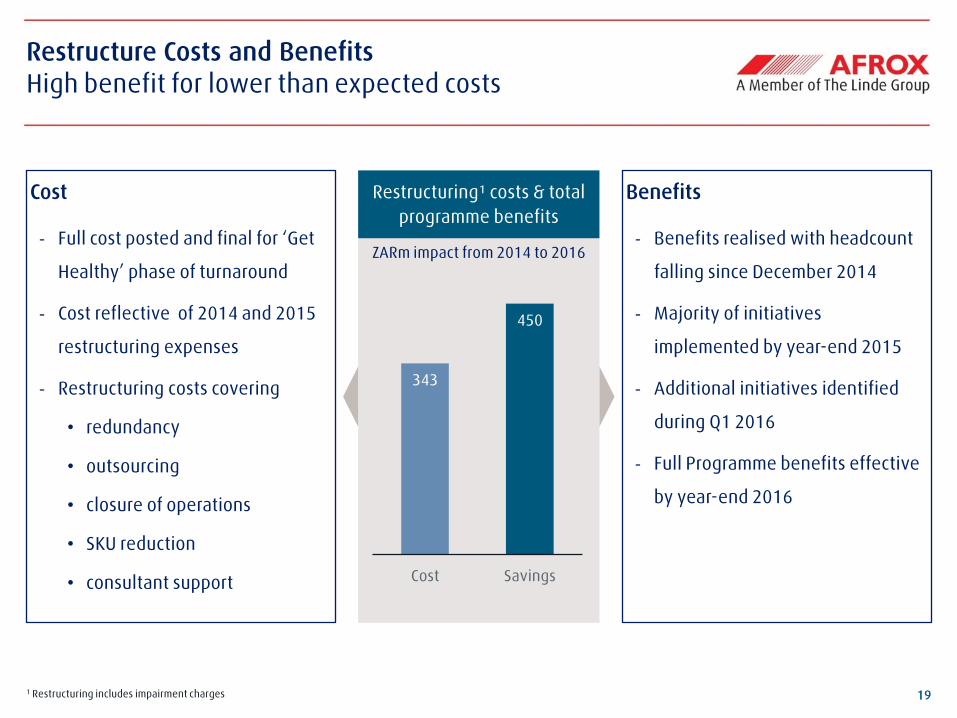

Restructure Costs and Benefits

High benefit for lower than expected costs

1 Restructuring includes impairment charges

Cost

- Full cost posted and final for ‘Get

Healthy’ phase of turnaround

- Cost reflective of 2014 and 2015

restructuring expenses

- Restructuring costs covering

• redundancy

• outsourcing

• closure of operations

• SKU reduction

• consultant support

Benefits

- Benefits realised with headcount

falling since December 2014

- Majority of initiatives

implemented by year-end 2015

- Additional initiatives identified

during Q1 2016

- Full Programme benefits effective

by year-end 2016

ZARm impact from 2014 to 2016

Restructuring¹ costs & total

programme benefits

343

450

Cost Savings

20

Key Project Update & Outlook

21

Key Project Update

1. Port Elizabeth ASU

- Successfully commissioned in April 2015, continues production since June 2015

- On-target performance to business case

2. New Durban Filling Plant, Riverhorse Valley

- New filling plant and equipment commissioned Q2 2016

- Project on-time and within budget

- External launch during H2 2016

3. Sale of Cornubia Land: 103 000m²

- Portion 79 was sold for R30m; 78 was sold for R24m

- Final portion, 77 sold in Q2 2016 for R66m

4. LPG Imports and Storage

- Bidvest Tanker Terminals (BTT) commissioned and operational since May 2016

- Improved security of LPG supply, ability to grow SA and Rest of Africa volumes

22

5. eCommerce Platform Update

- 11% of all delivered orders via eCommerce platforms

- 6 824 legal entities registered for eCommerce YTD

- 225 000 self-service transactions resulted in 18 000 man-hours saved

6.Helium Project

- Media release in Q2 2016

- Linde Engineering/Tetra 4 early engineering agreement in place

- Expected commercialisation 2018/19

Key Project Update Continued

23

- Ensure value of turnaround reflected in 2016 financials

- Implement ASU optimisation project

- Focus on price cost recovery (PCR)

- Improve asset utilisation

- Grow Special Gases, CO2, Healthcare, LPG, Rest of Africa

- Target ROCE of 20%+ in medium-term

Outlook

Thank You

25

Definition of Key Financial Figures

Appendix. III

GPADE

Gross Profit after Distribution Expenses

SG&A

Selling and marketing & general

administration costs

EBITDA

EBIT before non-recurring items adjusted

for amortisation of intangible assets and

depreciation of tangible assets

Return on Capital Employed (ROCE)

EBIT

before non-recurring items

Headline Earnings per Share (HEPS)

before non-recurring items

Profit for the period

before non-trading items

attributable to Afrox shareholders

Earnings per Share

(EPS)

Profit for the period

attributable to Afrox shareholders

Average Capital Employed

Equity (incl. non-controlling interests)

+ financial debt

+ liabilities from finance leases

- cash, cash equivalents & securities

- receivables from finance leases

Number of

weighted average

outstanding shares

Number of

weighted average

outstanding shares

26

AGM 26 May 2016

Interim Results Released 07 September 2016

Interim Investor and Analyst Presentation 08 September 2016

Contact

Phone: +27 11 490 0400

Email: [email protected]

Website: www.afrox.co.za

Investor Calendar 2016