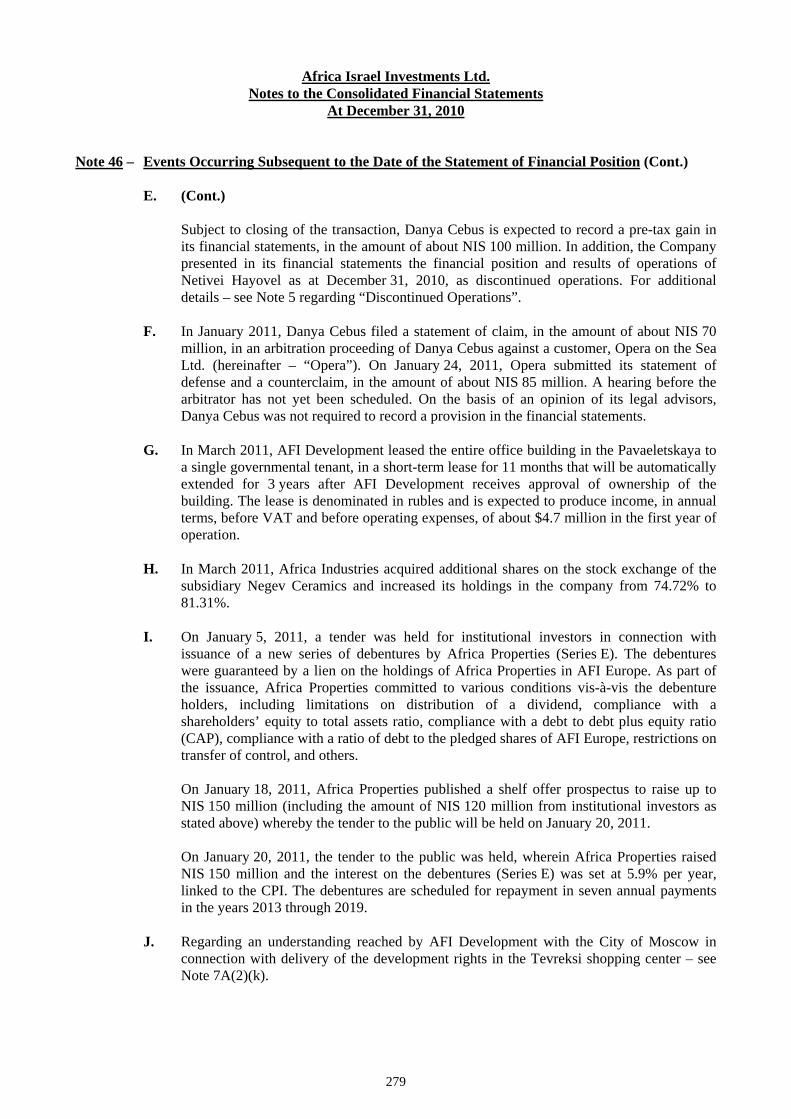

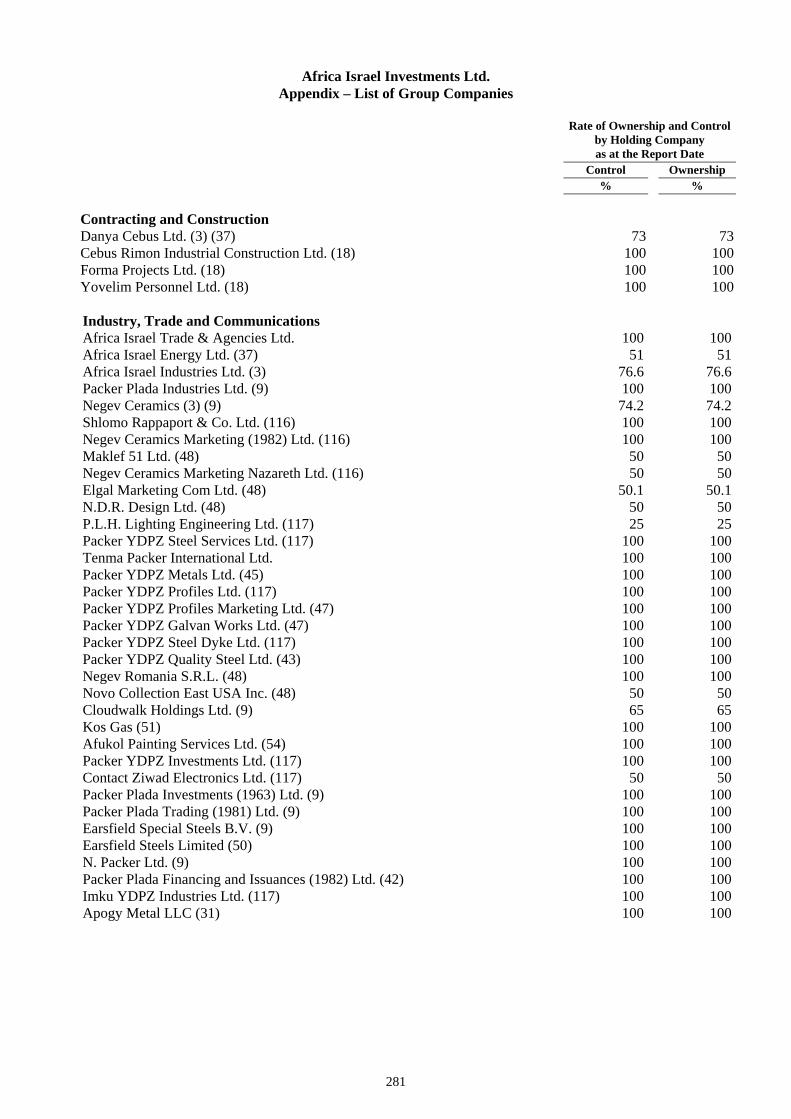

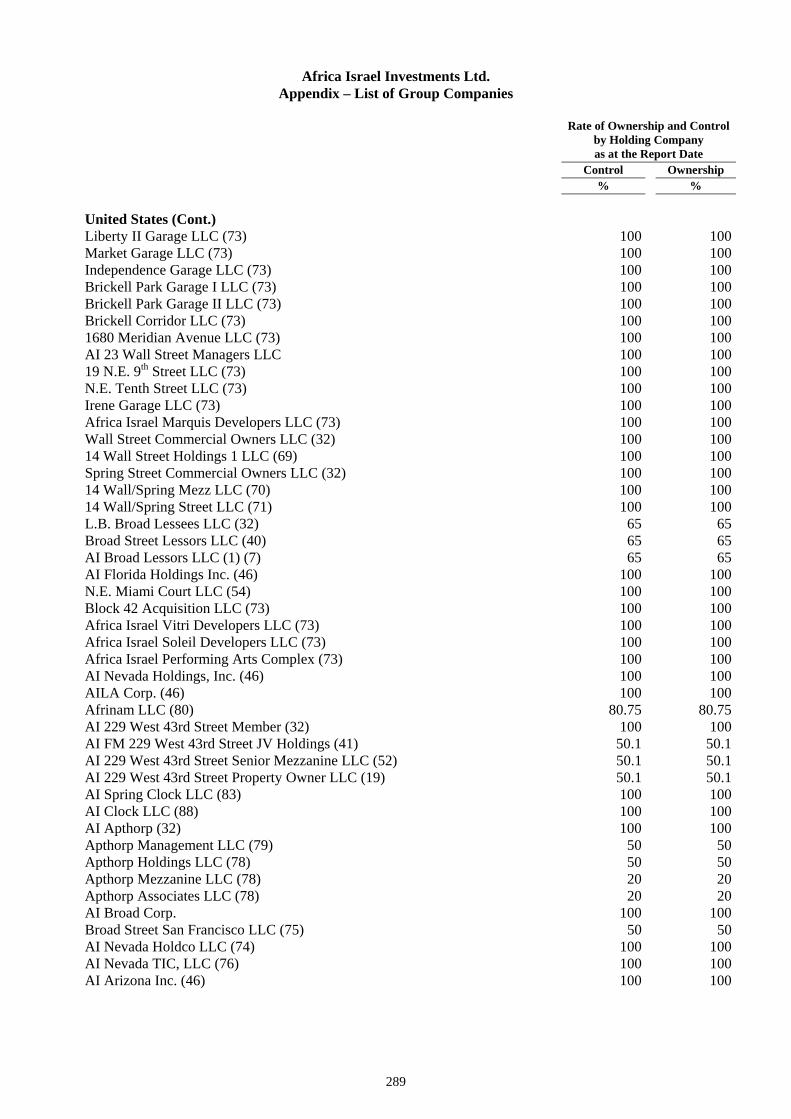

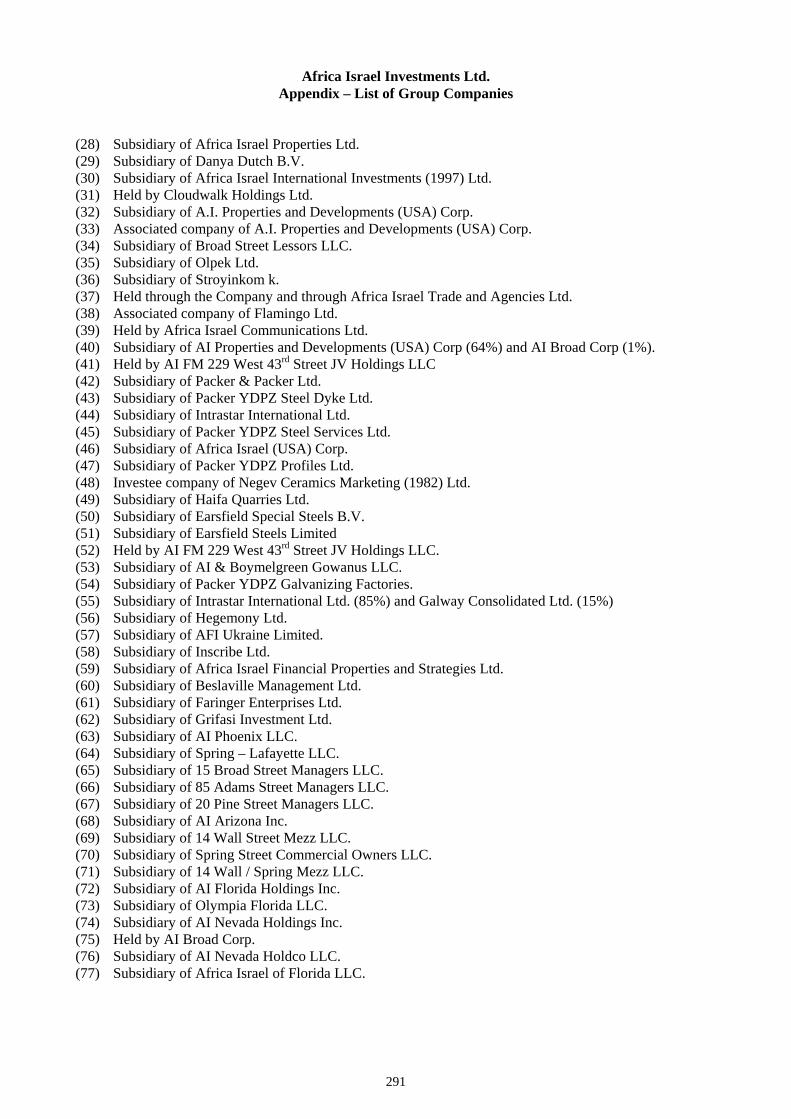

africa israel investments ltd

TRANSCRIPT

Africa Israel Investments Ltd.

Consolidated Financial Statements

At December 31, 2010

Africa Israel Investments Ltd. Consolidated Financial Statements

At December 31, 2010

Contents

Page Auditors’ Reports 2 – 3 Consolidated Statements of Financial Position 4 – 5 Consolidated Statements of Income 6 Consolidated Statements of Comprehensive Income 7 Consolidated Statements of Changes in Shareholders’ Equity 8 – 9 Consolidated Statements of Cash Flows 10 – 11 Notes to the Financial Statements 12 Appendix – List of Group Companies 280

2

Report of the Auditors to the Shareholders of Africa Israel Investments Ltd. regarding Audit of Internal Control Components over Financial Reporting In accordance with Section 9B(c) of the Securities Regulations (Periodic and Immediate Reports), 1970 We have audited internal control components over financial reporting of Africa Israel Investments Ltd. and its subsidiaries (hereinafter – “the Company”) as at December 31, 2010. These internal control components were determined as explained in the following paragraph. The Company’s Board of Directors and Management are responsible for maintenance of effective internal control over financial reporting and for their evaluation of the effectiveness of internal control components over financial reporting attached to the Periodic Report for the above-mentioned date. Our responsibility is to express an opinion on internal control components over the Company’s financial reporting based on our audit. Internal control components over financial reporting audited by us were determined in accordance with Audit Standard 104 of the Institute of Certified Public Accountants in Israel “Audit of Internal Control over Financial Reporting” (hereinafter – “Audit Standard 104”). These components are: (1) controls at the level of the organization, including controls over the preparation and closing process of financial reporting and general controls of information systems; (2) controls over investments in investee companies; (3) controls over investment property; (4) controls over inventory of buildings held for sale (all of these will be referred to hereinafter as – “the Audited Control Components”). We conducted our audit in accordance with Audit Standard 104. Pursuant to this Standard we are required to plan and perform the audit with the goal of identifying the Audited Control Components and to obtain a reasonable level of certainty whether these control components were effectively maintained in all material respects. Our audit included gaining an understanding of the internal control over financial reporting, identification of the Audited Control Components, evaluation of the risk that a significant weakness exists in the Audited Control Components, and examination and evaluation of the effectiveness of the planning and operation of those control components based on the assessed risk. Our audit, with respect to those control components, also included performance of other procedures such as those we considered necessary under the circumstances. Our audit referred solely to the Audited Control Components, as opposed to internal control over the overall significant processes in connection with the financial reporting and, therefore, our opinion relates solely to the Audited Control Components. In addition, our audit did not refer to reciprocal impacts between the Audited Control Components and those not audited and, therefore, our opinion does not take into account these possible impacts. We believe our audit provides a reasonable basis for our opinion in the context described above. Due to built-in limitations, internal control over financial reporting, in general, and components thereof, in particular, may not prevent or discover a material misrepresentation. In addition, making of conclusions with respect to the future on the basis of evaluation of any present effectiveness whatsoever is exposed to risk that the controls will become inappropriate due to changes in circumstances or the extent of compliance with the policies or the procedures will change for the worse. In our opinion, the Company effectively maintained, in all material respects, the Audited Control Components as at December 31, 2010. We have also audited, in accordance with generally accepted auditing standards in Israel, the Company’s consolidated financial statements as at December 31, 2010 and 2009 and for each of the three years the last one of which ended on December 31, 2010 and our report, dated March 30, 2011, included an unqualified opinion on those financial statements, based on our audit and the reports of the other auditors.

Somekh Chaikin Breitman Almogar Zohar & Co. Certified Public Accountants (Isr.) Certified Public Accountants (Isr.)

March 30, 2011

3

Auditors’ Report to the Shareholders of Africa Israel Investments Ltd.

We have audited the accompanying consolidated statements of financial position of Africa Israel Investments Ltd. (hereinafter – “the Company”) as at December 31, 2010 and 2009, and the consolidated statements of income, the consolidated statements of comprehensive income, the consolidated statements changes in shareholders’ equity, and the consolidated statements cash flows for each of the three years the last one of which ended on December 31, 2010. These financial statements are the responsibility of the Company’s Board of Directors and of its Management. Our responsibility is to express an opinion on these financial statements based on our audits. We did not audit the financial statements of certain consolidated subsidiaries and joint ventures, whose assets constitute about 12% and about 13% of the total consolidated assets as at December 31, 2010 and 2009 respectively, and whose revenues constitute about 20%, about 19% and about 42% of the total consolidated revenues for the three years the last one of which ended on December 31, 2010, respectively. In addition, we did not audit the financial statements of investee companies and jointly controlled entities, the investment in which totaled NIS 354,419 thousand and NIS 406,424 thousand, as at December 31, 2010 and 2009, respectively, and the Company’s share in their income (losses) was NIS 113,630 thousand, NIS (167,716) thousand and NIS (533,336) thousand for the three years the last one of which ended on December 31, 2010, respectively. The financial statements of those companies were audited by other auditors, whose reports thereon were furnished to us, and our opinion, insofar as it relates to amounts included in respect of those companies, is based on reports of the other auditors. We conducted our audits in accordance with generally accepted auditing standards in Israel, including standards prescribed by the Auditors’ Regulations (Manner of Auditor’s Performance), 1973. Such standards require that we plan and perform the audits in order to obtain reasonable assurance that the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by the Company’s Board of Directors and by its Management, as well as evaluating the overall financial-statement presentation. We believe that our audits and the reports of the other auditors provide a reasonable basis for our opinion. In our opinion, based on our audits and on the reports of other auditors, the financial statements referred to above present fairly, in all material respects, the financial position of the Company and its subsidiaries as at December 31, 2010 and 2009, and the results of their operations, the changes in the shareholders’ equity and their cash flows, for each of the three years the last one of which ended on December 31, 2010, in accordance with International Financial Reporting Standards (IFRS) and the provisions of the Securities Regulations (Annual Financial Statements), 2010. We also audited, in accordance with Auditing Standard 104 of the Institute of Certified Public Accountants in Israel “Audit of Internal Control Components over Financial Reporting” the internal control components over the Company’s financial reporting as at December 31, 2010, and our report dated March 30, 2011 included an unqualified opinion with respect to the effective maintenance of those internal control components.

Somekh Chaikin Breitman Almogar Zohar & Co. Certified Public Accountants (Isr.) Certified Public Accountants (Isr.)

March 30, 2011

4

Africa Israel Investments Ltd. Consolidated Statements of Financial Position

In Thousands of New Israeli Shekels At December 31 Note 2010 2009

Current Assets

Cash and cash equivalents 8 2,155,726 1,560,504 Short-term investments 9 191,524 353,971 Marketable securities 10 424,706 567,148 Trade receivables 11 937,090 865,776 Other receivables and debit balances, including financial derivatives 11 1,064,851 931,075 Income taxes receivable 32,443 79,617 Inventory of buildings held for sale 12 3,007,503 *3,438,636 Other inventories 13 553,467 364,195 Assets held for sale 14 1,784,298 883,969 10,151,608 9,044,891 -------------- --------------

Non-Current Assets

Investments in investee companies accounted for using the equity method of accounting 15 1,516,346 1,174,053 Loans to investee companies 15 883,034 1,288,968 Property, plant and equipment 16 591,661 **1,582,910 Investment property 17 5,192,277 5,387,076 Investment property under construction 18 6,051,801 5,265,491 Long-term loans, investments and other debit balances 19 164,368 1,887,436 Inventory of real estate 20 1,639,952 *1,986,328 Intangible assets 21 113,714 114,247 Excess of assets over liabilities in respect of employee benefits 22 1,626 2,332 Deferred tax assets 36 96,429 100,452 16,251,208 18,789,293 -------------- -------------- 26,402,816 27,834,184 * Reclassified – see Note 2G. ** Retroactive application of new accounting standard – see Note 2(H)2.

____________________________ ________________________ _________________________ Lev Leviev

Chairman of the Board of Directors Izzi Cohen

CEO Ron Fainaro

CFO Approval date of the financial statements: March 30, 2011

The accompanying notes to the consolidated financial statements are an integral part thereof.

5

Africa Israel Investments Ltd. Consolidated Statements of Financial Position

In Thousands of New Israeli Shekels At December 31 Note 2010 2009 Current Liabilities

Debentures 23 1,277,346 7,576,961 Short-term credit from banks and others 23 2,270,373 3,984,439 Contractors and suppliers 24 805,608 760,025 Other payables and credit balances, including financial derivatives 25 888,624 1,212,956 Income taxes payable 90,613 49,629 Advances from customers 26 814,160 742,907 Provisions 27 377,819 415,757 Liabilities held for sale 14 1,620,226 26,681 8,144,769 14,769,355 -------------- --------------

Long-Term Liabilities

Debentures 23 3,984,767 1,701,023 Liabilities to banks 23 4,965,081 5,469,018 Other liabilities 23 595,623 777,431 Excess of losses on investments in investee companies accounted for using the equity method of accounting 15 155,723 253,458 Options issued 7D(1) 10,698 34,986 Employee benefits 22 14,749 19,259 Provisions 27 – 3,139 Liabilities for deferred taxes 36 490,500 486,113 10,217,141 8,744,427 -------------- --------------

Equity 37

Share capital and premium 374,841 368,604 Premium on shares 3,552,657 1,812,964 Capital reserves (2,350,584) (1,295,145) Retained earnings 1,955,851 249,293 Total equity allocated to the owners of the Company 3,532,765 1,135,716 Rights not conferring control 4,508,141 *3,184,686 Total equity 8,040,906 4,320,402 -------------- -------------- 26,402,816 27,834,184 * Retroactive application of new accounting standard – see Note 2(H)1.

The accompanying notes to the consolidated financial statements are an integral part thereof.

6

Africa Israel Investments Ltd. Consolidated Statements of Income

In Thousands of New Israeli Shekels (unless stated otherwise)

For the Year Ended December 31 Note 2010 *2009 *2008

Revenues Construction and real estate transactions 28 2,706,043 2,491,739 2,783,908 Rental and operation of properties 440,152 487,926 564,452 Industry 1,876,727 1,383,938 1,915,557 Other activities 28,246 11,860 20,550 Share in income of investee companies accounted for using the equity method of accounting, net 15 365,167 – – Increase in fair value of investment property, net 17 221,242 – 166,660 Other income 29 286,786 264,064 194,653 5,924,363 4,639,527 5,645,780 ------------- ------------- -------------Cost and expenses Construction and real estate transactions 30 2,363,278 2,201,499 2,630,412 Update of provision for decline in value of inventory of land and buildings 28 (60,195) 577,125 1,365,968 Maintenance, supervision and management of real estate and properties 31 107,743 186,674 191,460 Decline in value of investment property, net 17 – 245,951 – Decline in value of investment property under construction, net 18 20,290 156,494 2,060,671 Industry 32 1,724,479 1,300,536 1,815,630 Other activities 39,440 2,412 3,232 Share in losses of investee companies accounted for using the equity method of accounting, net 15 – 249,002 519,679 Administrative and general expenses 34 296,731 272,783 361,634 Amortization of intangible and other expenses 33 255,139 316,137 379,929 4,746,905 5,508,613 9,328,615 ------------- ------------- -------------

Operating income (loss) 1,177,458 (869,086) (3,682,835) ------------- ------------- -------------

Financing expenses 35 (1,130,883) (1,404,568) (1,532,785) Financing income (see Note 1C) 35 1,729,598 1,891,138 461,965 Financing income (expenses), net 598,715 486,570 (1,070,820) ------------- ------------- -------------

Operating income (loss) before taxes on income 1,776,173 (382,516) (4,753,655)

Taxes on income 36 (155,825) (327,434) (174,952)

Income (loss) from continuing activities 1,620,348 (709,950) (4,928,607)

Income (loss) from discontinued activities (after taxes) 5 213,327 (53,428) (18,618)

Income (loss) for the year 1,833,675 (763,378) (4,947,225)

Allocated to: The owners of the Company 1,702,056 (673,023) (4,860,956) Rights not conferring control 131,619 (90,355) (86,269) Income (loss) for the year 1,833,675 (763,378) (4,947,225)

Income (loss) per share attributed to the owners of the Company

Basic income (loss) per share (in NIS) 38 17.96 **(12.14) **(91.67)

Diluted income (loss) per share (in NIS) 38 17.94 **(12.14) **(91.67)

* Restated due to discontinuance of activities – see Note 5. ** Restated due to issuance of rights – see Note 1C. *** Regarding income (loss) per share from discontinued activities – see Note 5.

The accompanying notes to the consolidated financial statements are an integral part thereof.

7

Africa Israel Investments Ltd. Consolidated Statements of Comprehensive Income

In Thousands of New Israeli Shekels For the Year Ended December 31 2010 2009 2008 Income (loss) for the year 1,833,675 (763,378) (4,947,225) Other components of comprehensive income (loss) Foreign currency translation differences in respect of foreign activities (834,266) 145,713 (1,037,627) Change in fair value of cash flow hedges, net of tax 39,389 (4,312) (52,983) Change in fair value of financial assets available for sale, net of tax 3,694 (33,217) – Loss from decline in value of financial assets available for sale transferred to the statement of income, net of tax – 33,217 – Loss of control in subsidiary, net of tax – (14,893) – Realization of comprehensive income of investee company accounted for using the equity method of accounting, net of tax (594) 15,857 – Total comprehensive income (loss) for the year 1,041,898 (621,013) (6,037,835) Total comprehensive income (loss) allocated to: The owners of the Company 1,290,425 (555,809) (5,651,480) Rights not conferring control (248,527) (65,204) (386,355) Total comprehensive income (loss) for the year 1,041,898 (621,013) (6,037,835)

The accompanying notes to the consolidated financial statements are an integral part thereof.

8

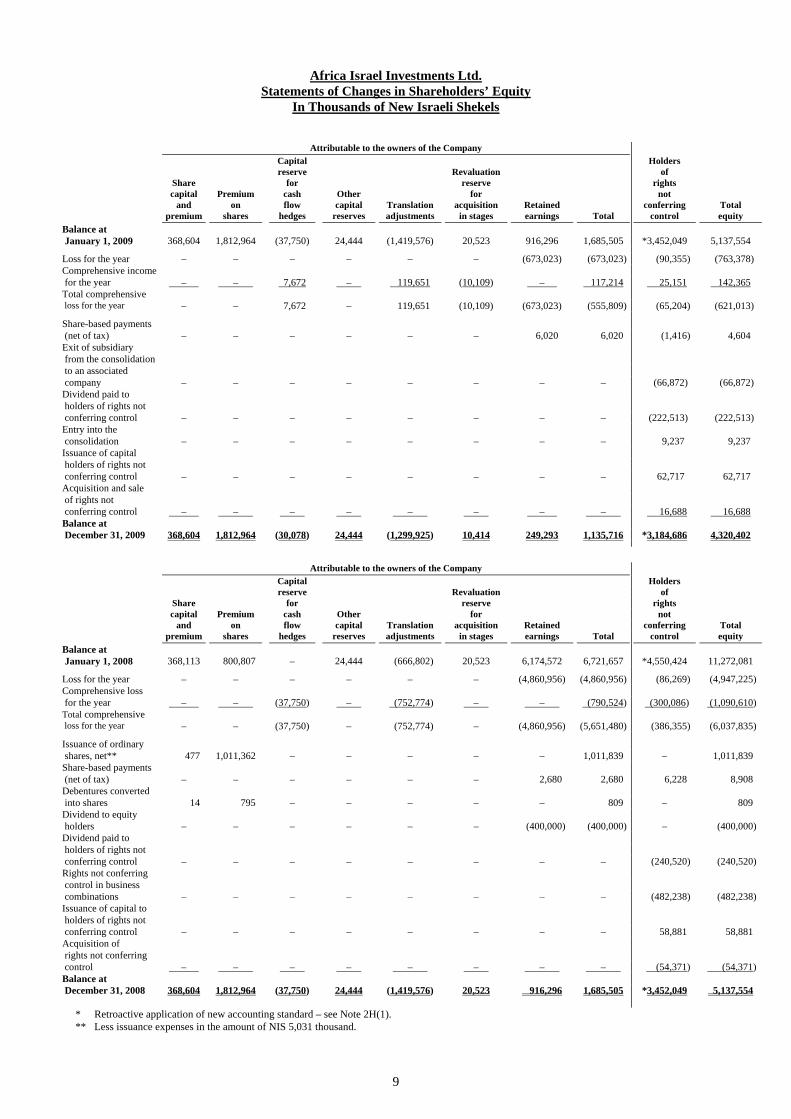

Africa Israel Investments Ltd. Statements of Changes in Shareholders’ Equity

In Thousands of New Israeli Shekels

Attributable to the owners of the Company

Reserve for transactions Capital with Holders reserve Revaluation holders of of Share from reserve rights rights capital Premium cash Other for not not and on flow capital Translation acquisition conferring Retained conferring Total premium shares hedges reserves adjustments in stages control earnings Total control equity

Balance at January 1, 2010 368,604 1,812,964 (30,078) 24,444 (1,299,925) 10,414 – 249,293 1,135,716 *3,184,686 4,320,402

Net income for the year – – – – – – – 1,702,056 1,702,056 131,619 1,833,675 Other comprehensive loss for the year – – 24,914 3,694 (440,239) – – – (411,631) (380,146) (791,777) Total comprehensive income (loss) for the year – – 24,914 3,694 (440,239) – – 1,702,056 1,290,425 (248,527) 1,041,898

Issuance of ordinary shares, net** 6,237 1,739,693 – – – – – – 1,745,930 – 1,745,930 Share-based payments (net of tax) – – – – – – – 4,502 4,502 948 5,450 Dividend to holders of rights not conferring control – – – – – – – – – (15,430) (15,430) Issuance of capital to holders of rights not conferring control – – – – – – – – – 120,538 120,538 Acquisition and sale of rights not conferring control – – 3,265 – 139,205 (1,819) (784,459) – (643,808) 1,465,926 822,118 Balance at December 31, 2010 374,841 3,552,657 (1,899) 28,138 (1,600,959) 8,595 (784,459) 1,955,851 3,532,765 4,508,141 8,040,906

* Retroactive application of new accounting standard – see Note 2H(1). ** See Note 1C.

The accompanying notes to the consolidated financial statements are an integral part thereof.

9

Africa Israel Investments Ltd. Statements of Changes in Shareholders’ Equity

In Thousands of New Israeli Shekels

Attributable to the owners of the Company

Capital Holders reserve Revaluation of Share for reserve rights capital Premium cash Other for not and on flow capital Translation acquisition Retained conferring Total premium shares hedges reserves adjustments in stages earnings Total control equity

Balance at January 1, 2009 368,604 1,812,964 (37,750) 24,444 (1,419,576) 20,523 916,296 1,685,505 *3,452,049 5,137,554

Loss for the year – – – – – – (673,023) (673,023) (90,355) (763,378) Comprehensive income for the year – – 7,672 – 119,651 (10,109) – 117,214 25,151 142,365 Total comprehensive loss for the year – – 7,672 – 119,651 (10,109) (673,023) (555,809) (65,204) (621,013)

Share-based payments (net of tax) – – – – – – 6,020 6,020 (1,416) 4,604 Exit of subsidiary from the consolidation to an associated company – – – – – – – – (66,872) (66,872) Dividend paid to holders of rights not conferring control – – – – – – – – (222,513) (222,513) Entry into the consolidation – – – – – – – – 9,237 9,237 Issuance of capital holders of rights not conferring control – – – – – – – – 62,717 62,717 Acquisition and sale of rights not conferring control – – – – – – – – 16,688 16,688 Balance at December 31, 2009 368,604 1,812,964 (30,078) 24,444 (1,299,925) 10,414 249,293 1,135,716 *3,184,686 4,320,402

Attributable to the owners of the Company

Capital Holders reserve Revaluation of Share for reserve rights capital Premium cash Other for not and on flow capital Translation acquisition Retained conferring Total premium shares hedges reserves adjustments in stages earnings Total control equity

Balance at January 1, 2008 368,113 800,807 – 24,444 (666,802) 20,523 6,174,572 6,721,657 *4,550,424 11,272,081

Loss for the year – – – – – – (4,860,956) (4,860,956) (86,269) (4,947,225) Comprehensive loss for the year – – (37,750) – (752,774) – – (790,524) (300,086) (1,090,610) Total comprehensive loss for the year – – (37,750) – (752,774) – (4,860,956) (5,651,480) (386,355) (6,037,835)

Issuance of ordinary shares, net** 477 1,011,362 – – – – – 1,011,839 – 1,011,839 Share-based payments (net of tax) – – – – – – 2,680 2,680 6,228 8,908 Debentures converted into shares 14 795 – – – – – 809 – 809 Dividend to equity holders – – – – – – (400,000) (400,000) – (400,000) Dividend paid to holders of rights not conferring control – – – – – – – – (240,520) (240,520) Rights not conferring control in business combinations – – – – – – – – (482,238) (482,238) Issuance of capital to holders of rights not conferring control – – – – – – – – 58,881 58,881 Acquisition of rights not conferring control – – – – – – – – (54,371) (54,371) Balance at December 31, 2008 368,604 1,812,964 (37,750) 24,444 (1,419,576) 20,523 916,296 1,685,505 *3,452,049 5,137,554

* Retroactive application of new accounting standard – see Note 2H(1). ** Less issuance expenses in the amount of NIS 5,031 thousand.

10

The accompanying notes to the consolidated financial statements are an integral part thereof.

11

Africa Israel Investments Ltd. Consolidated Statements of Cash Flows

In Thousands of New Israeli Shekels

For the Year Ended December 31 2010 2009 2008 Cash flows from operating activities Net income (loss) for the year 1,833,675 (763,378) (4,947,225) Adjustments: Share in losses (income) of investee companies accounted for using the equity method of accounting, net (352,615) 252,758 533,074 Gain from decline in rate of holdings (483,950) (49,769) (34,303) Depreciation and amortization and decline in value of property, plant and equipment 258,655 157,987 120,960 Update of provision for decline in value of inventory of land and buildings (60,195) 577,125 1,365,968 Decline in value of investments, net 10,781 97,248 44,672 Loss from decline in value of intangible assets – 32,959 155,662 Change in fair value of investment property under construction, net 20,290 156,494 2,060,671 Capital losses (gains) on sale of property, plant and equipment and investment property, net 8,714 53,632 (118,122) Share-based payments 5,450 4,604 8,908 Marketable securities, net 20,386 75,961 36,562 Change in fair value of investment property, net (221,242) 245,951 (165,585) Taxes on income 158,776 310,665 171,538 Change in time value in respect of put options to holders of rights not conferring control (586) 1,391 5,260 Financing (income) expenses, net (562,736) (559,793) 1,229,710 Change in real estate category 53,572 103,542 (95,470) Change in long-term debt 33,772 308,635 (336,070) Change in inventory of buildings held for sale 472,719 (30,984) (630,035) Change in other inventories (200,537) 61,828 32,298 Change in trade receivables and other receivables and debits (88,659) 354,017 161,573 Change in contractors, trade payables and other payables and credits 136,536 (507,552) 141,916 Change in advance deposits from customers 79,902 50,122 (183,563) Change in provisions and employee benefits 21,319 13,637 22,599 Income taxes paid, net (29,208) (6,053) (238,252) Net cash provided by (used in) operating activities 1,114,819 941,027 (657,254) ------------- ------------- -------------

The accompanying notes to the consolidated financial statements are an integral part thereof.

12

Africa Israel Investments Ltd. Consolidated Statements of Cash Flows

In Thousands of New Israeli Shekels

For the Year Ended December 31 2010 2009 2008

Cash flows from investing activities Initial consolidation of subsidiary – (75,666) (181,097) Investment in associated and other companies (10,831) (76,613) (284,936) Repayment (provision) of loans to associated companies, net 327,584 (8,017) (209,229) Investment in intangible assets (4,785) (11,527) (9,767) Proceeds from sale of shares of investee companies 379,937 373,951 580,624 Investment in investment property and investment property under construction (638,446) (1,516,903) (2,803,281) Investment in property, plant and equipment (108,151) (85,504) (310,029) Proceeds from sale of property, plant and equipment 3,886 14,527 162,463 Proceeds from sale of investment property 32,869 763,537 587,250 Investment in long-term deposits and loans (62,265) (113,522) (4,678) Repayment of long-term deposits and loans 213,048 81,586 212,772 Acquisition of marketable securities (424,921) (581,712) (2,242,642) Sale of marketable securities 441,251 433,152 3,234,230 Dividends received 14,227 26,863 38,313 Interest received 120,525 154,149 89,722 Short-term investments, net 133,590 30,324 (110,268)

Net cash provided by (used in) investing activities 417,518 (591,375) (1,250,553) ------------- ------------- -------------

Cash flows from financing activities Interest paid (880,078) (960,753) (1,132,869) Dividend paid to holders of rights not conferring control (15,430) (222,513) (240,520) Dividend paid to the equity holders – – (400,000) Acquisition of rights not conferring control (22,805) *(5,516) *(121,599) Issuance of capital to the owners of the Company 380,559 – 1,016,870 Issuance expenses – – (5,031) Proceeds from issuance of rights in subsidiaries 3,278 – – Issuance of capital to holders of rights not conferring control 118,884 64,621 58,881 Receipt of long-term loans and liabilities 1,132,763 3,642,624 4,566,102 Repayment of long-term loans and liabilities (1,511,412) (2,321,485) (1,939,481) Short-term credit, net (94,787) (1,416,157) (1,818,976)

Net cash used in financing activities (889,028) (1,219,179) (16,623) ------------- ------------- -------------

Increase (decrease) in cash and cash equivalents 643,309 (869,527) (1,924,430)

Cash and equivalents at the beginning of the year 1,560,504 2,263,510 4,502,529

Cash from discontinued operations (24,457) – –

Effect of exchange rate fluctuations on balances of cash and cash equivalents (23,630) 166,521 (314,589)

Cash and cash equivalents at the end of the year 2,155,726 1,560,504 2,263,510 * Retroactive application of new accounting standard – see Note 2H(1).

The accompanying notes to the consolidated financial statements are an integral part thereof.

13

Africa Israel Investments Ltd. Notes to the Consolidated Financial Statements

At December 31, 2010

All amounts are presented In Thousands of New Israeli Shekels unless indicated otherwise Note 1 – General

A. The Reporting Entity Africa Israel Investments Ltd. (hereinafter – “the Company”) is an Israeli-resident

company that was incorporated in Israel and its registered address is Derech Hahoresh 4, Yehud. The Group’s consolidated financial statements as at December 31, 2010, include the financial statements of the Company and those of its subsidiaries (hereinafter – “the Group”) as well as the Group’s rights in associated companies and jointly controlled entities. The Company’s controlling shareholder is Mr. Lev Leviev, who holds the Company directly as well as through companies he wholly owns and controls.

The Group is engaged in holdings and investments in a variety of sectors in and outside of

Israel. The Company’s securities are registered for trading on the Tel-Aviv Stock Exchange.

B. Impacts of the Global Financial Crisis on the Group’s Activities Since September 2008 and thereafter, the global financial crisis has taken a dramatic turn

for the worse and the extent of its impact has increased on both the world economy and the Israeli economy. As a result of the said crisis, which has triggered the collapse of significant players in the world credit market, there has been a decline in the amount of credit extended by banks and non-bank lenders (in and outside of Israel), and a process of a general economic slowdown has taken hold in a large number of countries throughout the world, including countries in which the Group companies operate.

The financial crisis has affected the Israeli economy and capital markets, in general, and

the Group companies, in particular, including by causing an increase in the interest rates paid on bank loans, stricter terms for receipt and/or renewal of financing, an adverse effect on the Company’s ability to sell its properties, a decline in the fair value of investment and real estate properties, a slowdown in the rate of sales of residential units and construction of residential projects by the Group companies and a decrease in the demand for rental properties. In addition, in certain cases the crisis has given rise to an increase in the discount rates, which in turn affects the results of the Company’s operations.

The financial crisis has caused a number of the Group companies not to comply with

financial covenants with respect to part of the liabilities (as stated in Note 23) and the need to make a significant change in the terms of the loans by means of, among other things, active requests by the Group to financers and lenders, in order to conform the loans and financing terms of the Group’s projects in and outside of Israel to the present financial situation.

In light of the credit bottleneck caused by the said crisis, and taking into account the

significant credit available to the Group at the outbreak of the crisis, on August 30, 2009, the Company’s Board of Directors authorized Company Management to start talks with the holders of the Company’s debentures in order to formulate a plan for reorganization of the Company’s liabilities to the holders of all its different debenture series and on May 16, 2010, the debt arrangement process was completed. For details regarding the debt arrangement and its impact on the Company’s financial statements – see Section C., below.

14

Africa Israel Investments Ltd. Notes to the Consolidated Financial Statements

At December 31, 2010 Note 1 – General (Cont.)

B. Impacts of the Global Financial Crisis on the Group’s Activities (Cont.) At the present time, the markets are still in a crisis condition, however, the indicators have

strengthened that it may be concluded that in mid 2009 the worldwide recession bottomed out (this can be learned mainly from the rise in the prices of securities on the world stock markets, relaxation of the global credit bottleneck, and from appearance of signs of renewal of capital fundraisings by means of issuance of debentures and shares). Nevertheless, it is noted that the demand and worldwide activities are still at a low level.

It is not possible know whether the full impacts of the crisis, as stated, have been

exhausted, and there is a fear of a worsening of the recession in more and more of the world’s economies.

The above-mentioned developments impact and may continue to impact in the future, both

directly and indirectly, the Group’s business activities, including the value of its assets, its liquidity, its ability to sell off its properties, as well as its ability to raise capital and comply with its financial covenants.

C. Debt Arrangement On February 9, 2010, the Company published an Immediate Report regarding convening

of a meeting of the holders of the Company’s debentures, for approval of the arrangement with the holders of the Company’s debentures, as well as an Immediate Report regarding convening of a meeting of the Company’s shareholders for approval of the above-mentioned arrangement, pursuant to Section 350 of the Companies Law.

(1) Set forth below are the highlights of the arrangement with the holders of the

Company’s debentures:

(a) Under the proposed arrangement, the Company’s controlling shareholder (including through a company in his control and/or a trustee on behalf of either) and/or any representative thereof shall invest in the Company the amount of NIS 750 million on the dates and under the terms set forth hereinafter:

– No later than the execution date of the arrangement, an issuance of rights to

the Company’s shareholders will be completed, designed to raise capital in the amount of no less than about NIS 400 million (hereinafter – “Initial Rights Offer”). The controlling shareholder (as defined in the arrangement) undertook to respond to the Initial Rights Offer and invest in the Initial Rights Offer pro rata to his share in the Company’s current share capital (about 74.8254%), that is, a total of NIS 300 million and partial linkage differences (defined hereinafter) (hereinafter – “the Initial Investment”). See also Section 2A below.

– After the Execution Date, the controlling shareholder committed as part of

the commitment certificate, to invest NIS 450 million including partial linkage differences (as defined below) (hereinafter – “the Additional Investments”), on the dates and under the terms as follows:

15

Africa Israel Investments Ltd. Notes to the Consolidated Financial Statements

At December 31, 2010 Note 1 – General (Cont.)

C. Debt Arrangement (Cont.)

(1) Set forth below are the highlights of the arrangement with the holders of the Company’s debentures: (Cont.)

(a) (Cont.)

– (Cont.)

(i) An additional amount of NIS 100 million no later than one year from the Execution Date;

(ii) An additional amount of NIS 100 million no later than two years from the Execution Date;

(iii) An additional amount of NIS 100 million no later than three years from the Execution Date;

(iv) An additional amount of NIS 150 million no later than four years from the Execution Date.

The Additional Investments (or a part thereof, as set forth below) are to be

executed in the form of private placements: however the controlling shareholder may decide, prior to the Execution Date of each investment increment, that execution of any of the investment increments set forth in Sections (i)-(iv) above (the above amounts represent the share of the controlling shareholder only) (or any part thereof) will be executed in the form of an issuance of rights, in place of a private placement, provided that (a) the share of the controlling shareholder in the rights issuance is no less than NIS 25 million (with this amount being linked to the partial linkage differences); (b) the Company’s Board of Directors approves the rights issue in place of the private placement, and; (c) the rights issuance shall not postpone the investment of the relevant amounts by the controlling shareholder in full and in a timely manner.

Investments of monies under this Section shall be executed according to a

share price of NIS 36.12681 (hereinafter – “the Base Share Price”). The Base Share Price shall be subject to adjustments in respect of distributions of bonus shares and dividends, provided that the reduction of the Base Share Price resulting from the said dividend distribution does not exceed 5% of the Base Share Price in any year, cumulatively, beginning on the date of the repayment of the debentures (Series Y) and onward. To the extent that investments of the monies are executed in the form of an issue of rights, the said investments will be executed according to a share price that does not exceed 90% of the average closing price of a Company share on the TASE in the three trading days preceding the date of the resolution by the Company’s Board of Directors regarding execution of the rights issuance.

– The amounts of the Initial Investment and the Additional Investments, shall

be linked to one-half of the rate of increase in the CPI compared to the index for September 2009 published on October 15, 2009 (hereinabove and hereinafter – “the Partial Linkage Differences”).

16

Africa Israel Investments Ltd. Notes to the Consolidated Financial Statements

At December 31, 2010 Note 1 – General (Cont.)

C. Debt Arrangement (Cont.)

(1) Set forth below are the highlights of the arrangement with the holders of the Company’s debentures: (Cont.)

(a) (Cont.)

– No later than the Execution Date, the Company shall issue to the trustee of the debenture holders (Series Z) shares, the number of which shall be equal to the Additional Investments including the Partial Linkage Differences up to the issuance date; divided by the Base Share Price (hereinafter – “the Agreed Relief Shares”). So long as the Agreed Relief Shares are held by the Share Trustee they will constitute dormant shares, which do not grant any party, including the controlling shareholder, the new debenture holders, or the Share Trustee, any rights in the Company, its capital or voting rights (including the right to receive dividends) and/or any other right (including the right to participate in an issue of rights) (see also Section (2)(b), below). Immediately prior to execution of any investment increment of any Additional Investment, the Company will issue to the Share Trustee additional shares, the quantity of which shall be equal to the difference between the balance of the Additional Investments linked to the Partial Linkage Differentials (up to the issuance date), divided by the Base Share Price, adjusted for the distribution of dividends and bonus shares; and the quantity of Agreed Relief Shares held by the Share Trustee in trust.

– Immediately after execution of each Additional Investment, the Share Trustee

shall transfer to the controlling shareholder ordinary shares of the Company, from the Agreed Relief Shares, in a quantity equal to the amounts of the Additional Investments, including the Partial Linkage Differentials; divided by the Base Share Price subject to adjustments in respect of distributions of dividends and bonus shares. It is clarified that the controlling shareholder may execute each Additional Investment in several parts or at once, at his discretion. In the event that the Controlling Shareholder breaches his obligation to invest the first or second increment of the Additional Investments in entirety and/or in a timely manner, the Share Trustee shall transfer a relative share of the Agreed Relief Shares to the new debenture holders (as defined below) who shall hold shares on the entitlement date (as published by the Share Trustee). In the event that the Controlling Shareholder breaches his obligation to invest the third or fourth increment of the Additional Investments in entirety and/or in a timely manner, the Share Trustee shall transfer the relative share of the Agreed Relief Shares to the Bondholders (Series Z) who shall hold shares on the entitlement date.

17

Africa Israel Investments Ltd. Notes to the Consolidated Financial Statements

At December 31, 2010 Note 1 – General (Cont.)

C. Debt Arrangement (Cont.)

(1) Set forth below are the highlights of the arrangement with the holders of the Company’s debentures: (Cont.)

(b) No later than the Execution Date, the Company shall repay, as a partial

repayment, to all holders of the debentures holding debentures on the determining date, the amount of NIS 559 million (hereinafter – “the Cash Payment”) under the following terms and in the following manner (this amount includes NIS 3.6 million paid to holders of the debentures (Series I) in January 2010 for accumulated interest in respect of the debentures (Series I) up to January 5, 2010):

(c) On the Execution Date, the Company shall issue to all the debenture holders who

hold debentures on the determining date in respect of the balance of their holdings in the debentures after the Cash Payment and execution of the partial repayment as set forth in Section (b) above), two new series of debentures whose terms are as follows (see also Section 2(c), below):

i. NIS 1,016 million par value of registered debentures (Series Y) of the

Company of par value NIS 1 each, payable in a single installment at the end of twenty-four months (24) from the Execution Date. The Debentures (Series Y) shall be linked to the CPI (principal and interest), and the base index is the index known on the Determining Date, and shall bear fixed annual interest from the Execution Date at the rate of 4.5%, payable together with the Debentures (Series Y) principal on the final redemption date of the Debentures (Series Y), as stated above. The Debentures (Series Y) shall be secured by collateral as set forth below. On the Execution Date, the Debentures shall be replaced by Debentures (Series Y) in the matter set forth in the arrangement.

ii. NIS 3,626 par value of registered debentures (Series Z), with a par value of

NIS 1 each, repayable in thirteen (13) consecutive annual installments beginning after the elapse of three years from the Execution Date (that is, one payment of principal in each of the years from 2013 to 2025). The Debentures (Series Z) shall be linked to the CPI known on the Determining Date, and shall bear effective annual interest at an average rate of 7% per annum, to be increased gradually from 6% per year to 10.75% per year, all as set forth in the arrangement. The interest in respect of the Debentures (Series Z) is payable in consecutive semi-annual installments beginning six months after the Execution Date, in each of the years from 2010 to 2025. The Company shall take steps to have the Debentures (Series Z) rated by a rating company certified by the Supervisor of the Capital Market, no later than one year from the Determining Date. Furthermore, the Company shall take steps to maintain the rating of the Debentures (Series Z) by said rating company during the entire term of the Debentures (Series Z). On the Execution Date, the Debentures (Series Z) will be substituted replaced in the manner set forth in the arrangement. The debentures (Series Y) and the debentures (Series Z), will be referred to hereinafter and hereinabove, together, a “the New Debentures”).

18

Africa Israel Investments Ltd. Notes to the Consolidated Financial Statements

At December 31, 2010 Note 1 – General (Cont.)

C. Debt Arrangement (Cont.)

(1) Set forth below are the highlights of the arrangement with the holders of the Company’s debentures: (Cont.)

(c) (Cont.)

iii. It is noted that the arrangement defines provisions regarding the matter of early redemption of the New Debentures, whether the Company elects to make an early repayment as stated, or whether the Company is obligated to make the said early repayment, as well as provisions concerning damages to the holders of the New Debentures (in certain cases) in respect of a voluntary early repayment of the Debentures (Series Z), all as set forth in the arrangement. As at the date of the report, there is no violation requiring early repayment of the debentures.

(d) On the Execution Date, the Company is to issue to the debenture holders who

hold debentures on the Determining Date, in respect of the balance of their holdings in the debentures (after the Cash Payment and the partial redemption as set forth in Section (b) above, and issuance of the New Debentures as set forth in Section (c) above), ordinary shares of NIS 0.1 par value each of the Company, in a quantity equal to the debt converted into Company shares (that is, a total of NIS 1.4 billion) divided by the Base Share Price. Company shares so issued to the debenture holders shall be listed for trading from the date of issue, (see also Section 2(e) below).

(e) On the Execution Date, the Company will transfer to the debenture holders who

hold debentures on the Determining Date, in respect of the balance of their holdings in the debentures, 92,720,923 global depository receipts (GDRs) representing 17.7% of the shares of AFI Development PLC, and shares of Africa Israel Properties (hereinafter in this Section – “AFI Development” and “Africa Properties,” respectively, and jointly – “the Shares of the Subsidiaries”), such that the value (defined below) of the Shares of the Subsidiaries amounts to the amount of the debt converted into the Shares of the Subsidiaries.

“The debt converted into the Shares of the Subsidiaries” – a total amount of

NIS 1.2 billion. Shares of the Subsidiaries transferred to the debenture holders shall be listed for

trading from the date of their transfer. “Value” – for purposes of this Section, shall be determined on the basis of the

average of the market value and the book value known on the Determining Date of each of the Subsidiaries.

Based on the conditions, on the execution date of the arrangement, the Company

transferred to the New Debenture holders 92,720,923 global deposit receipts (GDRs) and 3,372,948 shares of Africa Properties – see Section 2(d) below.

19

Africa Israel Investments Ltd. Notes to the Consolidated Financial Statements

At December 31, 2010 Note 1 – General (Cont.)

C. Debt Arrangement (Cont.)

(1) Set forth below are the highlights of the arrangement with the holders of the Company’s debentures: (Cont.)

(f) The Company has tax arrangements granted by the Tax Authorities and VAT

Authorities regarding the arrangement that govern the various tax aspects – all as detailed in the arrangement.

(g) To secure the Company’s obligations under the New Debentures, the Company

shall pledge on the Execution Date, in favor of the trustees of the New Debenture Holders, pro rata to the par value amount of the New Debentures part of the Company’s share holdings and accompanying rights in Africa Properties, the Company’s rights in the shareholders’ loans granted to Africa Properties and management fees from Africa Properties as well as part of the rights in AFI Development.

The Company may exchange the Pledged Assets or any part thereof for the Shares

of the Subsidiaries and/or other negotiable securities held by the Company, subject to several conditions defined in the arrangement.

No later than the date of the final, full, and precise repayment of the New

Debentures, the Company undertakes, in respect of each of its own (solo) assets, existing now or hereafter on the Determining Date of the Arrangement (jointly hereinafter – “the Company’s Assets”), to refrain from pledging, mortgaging, assigning through a lien, or granting it as other collateral of any other kind or as other guarantee for any debt of the Company or of others, in favor of any third party, without approval of the New Debenture Holders, as the case may be, to be adopted by regular majority. It is clarified that the restrictions imposed on the Company under the negative pledge, shall also apply to transfer of any of the Company’s Assets with no consideration.

This undertaking shall not apply to any of the following actions or transactions:

i. A specific charge on any asset, the purchase and/or development of which were financed by any third party, provided that the charge secures only the amount of financing provided by the third party for the purchase and/or development of said asset (as the case may be)(lien in rem);

ii. Granting a specific charge on any of the Company’s Assets in favor of a

buyer or the entity that finances purchase of the Asset by the buyer, provided that the charge secures only the transfer of rights in the Asset in the Buyer’s favor and/or satisfaction of the Company’s obligations under its agreement with the Buyer, and prior to creation of the charge, the Buyer transfers to the Company (or to its trustee, including a joint trustee with the Buyer) the entire consideration (or a material part thereof) in respect of the purchase of the asset;

20

Africa Israel Investments Ltd. Notes to the Consolidated Financial Statements

At December 31, 2010 Note 1 – General (Cont.)

C. Debt Arrangement (Cont.)

(1) Set forth below are the highlights of the arrangement with the holders of the Company’s debentures: (Cont.)

(g) (Cont.)

iii. A charge and/or other security interest of any kind on the Company’s Assets, against receipt of financing to be used to discharge liabilities to the New Debenture Holders and the banks, provided that the ratio between the amount discharged to the New Debenture Holders and the amount discharged to banks is not smaller than the ratio between the debt balance in respect of the New Debentures and the debt balance to the banks on the date of the discharge of the liabilities; and the charge and/or security interest shall secure only the amount of financing provided by the third part to discharge the liabilities to the financial creditors, as stated above.

iv. A charge in favor of banks against the assets and/or projects set forth in the

arrangement.

(h) The Company undertakes that, until the final and absolute repayment of the New Debentures, the ratio between the net financial debt and the CAP, as defined in Appendix R to the Proposed Arrangement, shall not exceed 70% (subject to the allowance of a minor deviation of no more than 10% in the stated ratio in the first two years subsequent to the Execution Date, and 5% thereafter) (hereinafter – “the Financial Covenants”). Subject to the restrictions defined, any breach by the Company of its obligation to comply with the Financial Covenants shall constitute grounds for a demand for immediate repayment based on the New Debentures, in addition to the grounds for action set forth in the deeds of trust concerning the New Debentures. As at the date of the report, the Company is in compliance with the covenants determined.

(i) The Company may make a distribution, as defined in the Companies Law,

exclusively subject to the following cumulative conditions: the Company is in compliance with the Financial Covenants on the date of the decision to make a distribution; the distribution does not constitute or cause any non-compliance with the Financial Covenants; the Company transferred to the trustees a confirmation signed by the Company regarding this matter and a copy of the transcript of the decision of the Company’s Board of Directors with respect to the distribution, wherein the Board of Directors confirms that, in its opinion and after having reviewed the Company’s situation, it concluded that no reasonable risk exists that the distribution will prevent the Company from being able to repay the New Debentures based on their terms.

21

Africa Israel Investments Ltd. Notes to the Consolidated Financial Statements

At December 31, 2010 Note 1 – General (Cont.)

C. Debt Arrangement (Cont.)

(1) Set forth below are the highlights of the arrangement with the holders of the Company’s debentures: (Cont.)

(i) (Cont.) Notwithstanding that stated above, to the extent that the debentures (Series Y)

have not yet been repaid, the Company may not make a distribution, as this term is defined in the Companies Law, without approval of the New Debenture Holders, adopted by a regular majority at a meeting of the New Debenture Holders prior to the distribution declaration date. The Company will take steps to convene said meeting prior to the distribution declaration date. The restriction on making a “distribution” under this Section shall not apply after the earlier of repayment of debentures (Series Y) or the Controlling Shareholder performs his obligation to make additional investments in the amount of NIS 200 million, as stated in Section (a) above. In the event that the Controlling Shareholder breaches his obligation to make one or more of the payments which he undertook to pay over the four years subsequent to the Execution Date (that amount to a total of NIS 450 million), as stated in Section (a) above (hereinafter – “the Controlling Shareholder’s Investment Obligation”), all the funds that the Controlling Shareholder is entitled to receive in respect of any distribution by the Company shall be applied to payments on account of the Controlling Shareholder’s Investment Obligation, the payment date of which has not yet occurred. The Company will set off from the amounts of said distribution, [amounts] in respect of the Controlling Shareholder’s Investment Obligation, and any said set-off is deemed performance of the Controlling Shareholder’s Investment Obligations whose payment date has not yet occurred, and which shall grant the Controlling Shareholder the right to receive Agreed Relief Shares. The arrangement under this Section shall remain in force until the earlier of full satisfaction of the Controlling Shareholder’s Investment Obligations or the elapse of four (4) years from the Determining Date.

(j) As part of the arrangement, restrictions were placed on sale of Company shares by

the controlling shareholder. (k) The Company may not extend any of the New Debentures series without approval

of separate meetings of the New Debenture Holders, by resolution adopted by a regular majority. In addition, so long as the debentures (Series Z) have not yet been repaid in full, the Company may not issue additional series of debentures whose terms are identical, similar, or preferred compared to the terms of the New Debentures, according to criteria set forth in the Proposed Arrangement, and subject to specific restrictions defined. Further, the Company may, at any time, purchase new debentures at any price it deems fit, without detracting from the obligation to repay the outstanding the New Debentures, provided that purchase of the new debentures by the Company in transactions over the counter shall not be performed from a Related Holder (as defined below). The new debentures so purchased and/or held by the Company shall be voided upon their purchase and stricken from trading, and the Company may not re-issue them.

22

Africa Israel Investments Ltd. Notes to the Consolidated Financial Statements

At December 31, 2010 Note 1 – General (Cont.)

C. Debt Arrangement (Cont.)

(1) Set forth below are the highlights of the arrangement with the holders of the Company’s debentures: (Cont.)

(k) (Cont.) Any Company (direct or indirect) subsidiary and/or company controlled by the

Company and/or the Company’s Controlling Shareholder and/or company controlled by the Company’s Controlling Shareholder (hereinabove and hereinafter – “a Related Holder”) may, from time to time, purchase and/or sell new debentures on the open market, at a price as they deem fit and to sell them accordingly. As long as the new debentures are held by a Related Holder, they shall not grant to the Related Holder any voting right in meetings of the holders of the new debentures and shall not be taken into account in calculating the legal quorum required to initiate the meeting, and the Company may not purchase these debentures in transactions over the counter.

(l) During five (5) years from the Execution Date, the trustee of holders of the

debentures (Series Z) may decide to appoint an independent director to the Company’s Board of Directors. The Independent Director shall be appointed as a member of the Board of Directors in addition to the two outside directors of the Company, which the Company is required to appoint by law. Such a director was appointed in the period of the report.

(m) On the Execution Date and as an integral part of the Proposed Arrangement, the

debenture holders shall waive all demands, claims, and/or suits against the Company, the Controlling Shareholder, its directors and officers, advisors, employees, and all parties acting in its behalf, whether these are or are not known to them, concerning the purchase and/or holding of the debentures.

(2) Execution of the debt arrangement On March 14, 2010, the meeting of the Company’s debenture holders and the meeting

of the Company’s shareholders approved the arrangement, and on March 21, 2010, the District Court of Tel-Aviv approved the arrangement.

On February 26, 2010, the Company published a prospectus from an issuance by

means of rights the purpose of which was to raise about NIS 400 million, and it increased its authorized capital to about 150,000,000 ordinary shares.

On April 19, 2010, the Company published an amendment to the prospectus for

issuance of rights dated February 26, 2010 (hereinafter – “the Amendment to the Prospectus”) for issuance of rights to the Company’s shareholders in the amount of about NIS 400 million. Pursuant to the terms of the arrangement, the Company’s controlling shareholder committed, including through companies he controls, to exercise all the rights issued to him as part of the said rights’ offering, in amount of about NIS 300 million.

23

Africa Israel Investments Ltd. Notes to the Consolidated Financial Statements

At December 31, 2010 Note 1 – General (Cont.)

C. Debt Arrangement (Cont.)

(2) Execution of the debt arrangement (Cont.) As agreed between the Company and the Joint Representatives of the Debenture

Holders, the execution date of the arrangement was set as May 16, 2010, and as a result the Company executed the following actions:

(a) The Company offered its shareholders 11,097,857 ordinary registered shares of

NIS 0.1 par value each of the Company by means of rights. Up to the final day for exercise of the rights, which fell on May 10, 2010, notifications were received for acquisition of 10,534,388 ordinary registered shares of NIS 0.1 par value each of the Company.

In consideration for the rights exercised, the Company received the gross amount

of about NIS 380 million. The controlling shareholder exercised all the rights to which he was entitled based

on the shelf offer prospectus, in accordance with the rate of his holdings in the Company’s issued shares (74.8%) and acquired 8,304,018.

As a result of the rights’ issuance, the Company restated the basic and diluted loss

per share data for the year ended December 31, 2009 and for the year ended December 31, 2008.

Set for below is the impact of the restatement:

Impact As presented As of the in these previously retroactive financial reported application statements In NIS

For the year ended December 31, 2009 (audited) (12.16) 0.02 (12.14)

For the year ended December 31, 2009 (audited) (91.85) 0.18 (91.67)

(b) The Company issued to a trustee 12,456,126 ordinary shares of the Company,

which constitute the agreed relief shares in accordance with the arrangement. (c) The Company issued marketable debentures (Series Y), in the aggregate stated

principal amount of about NIS 1,016 million, with an annual effective interest rate of about 10%, and marketable debentures (Series Z) in the aggregate stated principal amount of about NIS 3,626 million with an annual effective interest rate of about 14%.

24

Africa Israel Investments Ltd. Notes to the Consolidated Financial Statements

At December 31, 2010 Note 1 – General (Cont.)

C. Debt Arrangement (Cont.)

(2) Execution of the debt arrangement (Cont.)

(d) The Company transferred to the debt holders the total amount of 3,372,948 ordinary shares of NIS 1 par value each of Africa Properties, such that the Company’s rate of holdings in Africa Properties declined from about 68% to about 56%, and a total of 92,720,923 Global Deposit Certificates registered for trading on the London Stock Exchange and representing ordinary shares of AFI Development of $0.001 par value each, such that the Company’s rate of holdings in AFI Development declined from 71.7% to about 54%.

(e) The Company issued to the debenture holders 39,383,506 ordinary shares of

NIS 0.1 par each of the Company and also made a cash payment of about NIS 450 million as partial redemption to all the debenture holders (plus redemption of the debentures in cash of about NIS 109 million, which was paid in January 2010).

In May 2010, trading in the debentures was suspended. As a result, Midrug gave

notice of discontinuing rating of the Company’s debentures in light of suspension of their trading. On May 16, 2010 trading commenced in the components of the arrangement package listed for trading on the Stock Exchange.

In addition, as part of the debt arrangement with the debenture holders, an agreement

was signed with the banks whereby the repayment dates of the Company’s loans, in the amount of about NIS 400 million, will be extended, and therefore they were reclassified in the financial statements from short-term liabilities to long-term liabilities.

(3) The accounting treatment of the debt arrangement is detailed below:

(a) The Company’s shares issued as well as the shares of the subsidiaries given were recorded based on their fair value on the date of their issuance/transfer.

(b) The debentures issued as part of the arrangement have significantly different

economic terms and characteristics than the old debentures, and with respect to each of the old debenture series there is a change in the present value of more than 10% pursuant to the calculation included in the Standard (IAS 39). Therefore, an elimination was made of the old debentures and the new debentures were recorded based on their fair values on the date of their issuance.

(c) The difference between the fair value of the shares of the subsidiaries

AFI Development and Africa Properties given, and the increase in the rights that do not confer control, was recorded in a reserve for transactions with holders of rights not conferring control.

(d) The liability of the controlling shareholder to make an additional capital

investment in the Company in the future was broken down into two components:

25

Africa Israel Investments Ltd. Notes to the Consolidated Financial Statements

At December 31, 2010 Note 1 – General (Cont.)

C. Debt Arrangement (Cont.)

(3) The accounting treatment of the debt arrangement is detailed below: (Cont.)

(d) (Cont.)

– A fixed component – an additional investment of NIS 450 million constituting an additional capital component in the exchange package. On the issuance date of the dormant shares, their fair value was recorded as a premium on shares.

– A variable component – the liability of the controlling shareholder to invest

monies in an amount equal to the linkage differences accrued on the fixed component pursuant to the linkage mechanism provided in the arrangement. Since the quantity of shares to be issued by the Company in respect of the variable component is not known in advance, and since the amount of money the Company will receive in respect of these shares in the future is not fixed, the variable component constitutes a derivative instrument that was recognized as a liability in the amount of its fair value and will be updated every period through the statement of income.

The total gain recorded as a result of the debt arrangement in the period of the

report amounts to about NIS 1.45 billion and it is calculated as the difference between the fair value of the components of the consideration and the carrying value of the old debentures in the books. This gain is presented in the “financing income” category in the statement of income.

(4) Regarding a request to file a class action claim on behalf of a purchaser of debentures

(Series I) of the Company – see Note 43C.

D. Definitions In these financial statements:

1. International Financial Reporting Standards (hereinafter – “IFRS”) – standards and interpretations adopted by the International Accounting Standards Board (IASB) that include International Financial Reporting Standards (IFRS) and International Accounting Standards (IAS), including interpretations to these standards by the International Financial Reporting Interpretations Committee (IFRIC) or interpretations by the Standing Interpretations Committee (SIC), respectively.

2. The Company – Africa Israel Investments Ltd. 3. The Group – the Company and its subsidiaries. 4. Subsidiaries – companies the financial statements of which are fully consolidated,

directly or indirectly, with the Company’s financial statements.

26

Africa Israel Investments Ltd. Notes to the Consolidated Financial Statements

At December 31, 2010 Note 1 – General (Cont.)

D. Definitions (Cont.)

5. Investee companies – subsidiaries and companies, including a partnership or joint venture, where the Company’s investment therein is included, directly or indirectly, in the financial statements based on the equity method of accounting.

6. Related party – within the meaning thereof in International Accounting Standard 24 regarding “Related Parties”.

7. Interested parties – within the meaning thereof in Paragraph (1) of the definition of an “interested party” in a company in Section 1 of the Securities Law, 1968.

8. CPI/Index – the Consumer Price Index published by the Central Bureau of Statistics.

Note 2 – Basis of Preparation of the Financial Statements

A. Declaration of compliance with International Financial Reporting Standards (IFRS) The consolidated financial statements were prepared by the Group in accordance with

International Financial Reporting Standards (IFRS). The Group adopted IFRS for the first time in 2008, where the transition date to IFRS is January 1, 2007 (hereinafter – “the Transition Date”).

These financial statements were also prepared in accordance with the Securities

Regulations (Annual Financial Statements), 2010. The consolidated financial statements were approved for publication by the Company’s

Board of Directors on March 30, 2011. B. Functional currency and presentation currency The consolidated financial statements are presented in New Israeli Shekels (NIS), which is

the Company’s functional currency, and the amounts are rounded to the nearest thousand. The NIS is the currency that represents the main economic environment in which the Company operates.

C. Basis of measurement The statements were prepared on the basis of historical cost, with the exception of the

following assets and liabilities:

Financial instruments at fair value through the statement of income; Financial instruments classified as “available for sale”; Investment property and investment property under construction; Non-current assets held for sale and a group of assets held for sale; Inventory; Deferred tax assets and liabilities; Provisions: Assets and liabilities in respect of employee benefits; Investments in associated companies and jointly-controlled, equity-basis entities.

27

Africa Israel Investments Ltd. Notes to the Consolidated Financial Statements

At December 31, 2010 Note 2 – Basis of Preparation of the Financial Statements (Cont.)

C. Basis of measurement (Cont.) For information regarding measurement of these assets and liabilities – see Note 3

“Significant Accounting Policies”. The value of non-monetary assets and equity items measured on the basis of historical cost

was adjusted for changes in the CPI up to December 31, 2003, since up to this date Israel’s economy was considered a hyper-inflationary economy.

D. Operating cycle The Group has various different operating cycles. The normal operating cycle in the

construction sector is usually longer than one year and is generally up to two and a half years. The normal operating cycle in the construction sector in the infrastructures sector is longer than one year and may continue up to five years. The normal operating cycle in the real estate development area is longer than one year and is generally up to three years. With respect to the rest of the Group’s activities, the operating cycle is one year. As a result, the current assets and the current liabilities include items the realization of which is intended and anticipated to take place over the Group’s regular operating cycle – based on the type of activities.

E. Format for analysis of the expenses recognized in the statement of income The format for analysis of the expenses recognized in the statement of income is according

to the classification method based on the activity nature of the expense. Additional information regarding the substance of the expense is including in the notes to the financial statements.

F. Use of estimates and judgment In preparation of the financial statements in accordance with IFRS, Company management

is required to use judgment when making estimates, assessments and assumptions that affect implementation of the policies and the amounts of assets, liabilities, income and expenses. It is clarified that the actual results are likely to be different from these estimates.

When formulating the accounting estimates used in preparation of the Company’s financial

statements, Company management is required to make assumptions regarding circumstances and events involving significant uncertainty. When using its judgment in making the estimates, Company management bases itself on past experience, various facts, external factors and reasonable assumptions regarding the appropriate circumstances for each estimate.

The estimates and the assumptions used for preparing the financial statements are reviewed

on an ongoing basis. Changes in accounting estimates are recognized in the period during which the estimate was revised and in every future period affected.

28

Africa Israel Investments Ltd. Notes to the Consolidated Financial Statements

At December 31, 2010 Note 2 – Basis of Preparation of the Financial Statements (Cont.)

F. Use of estimates and judgment (Cont.) Change in estimates During the year ended December 31, 2010, a subsidiary examined the useful lives of

property, plant and equipment items and as a result the anticipated useful lives of certain property, plant and equipment items in the steel segment were changed. The impact of these changes in the years 2010, 2011 and 2012, is anticipated to be a decrease in the depreciation expenses of about NIS 5,089 thousand, NIS 4,819 thousand and about NIS 4,422 thousand, respectively.

Information with respect to assumptions made by the Group regarding the future and other

main uncertainty factors in connection with estimates where there is significant risk that their results will involve a material adjustment of the book values of assets and liabilities during the upcoming fiscal year is included in the following notes:

– Note 36, “Taxes on Income” – in connection with use of tax losses and recording of

tax expenses. – Note 27, “Provisions”. – Note 43, “Contingent Liabilities”. – Notes 17 and 18, “Investment Property” and “Investment Property under

Construction” – in connection with the measurement thereof at fair value. – Note 16, “Property, Plant and Equipment” – in connection with examination if the

amount at which the investment in non-monetary assets is presented can be recovered out of the anticipated discounted cash flows from the asset.

– Note 28, regarding recording revenues and expenses from work under an execution

contract in construction contractor projects on the statement of income in accordance with International Standard 11, based on the percentage of completion of the contract, where the results thereof can by reliably estimated.

– Note 19, regarding measurement of a financial asset in a project under the PPP method

(in the Highway 431 project), which expresses the debt of the public sector, and which bears financing income estimated based on the specific yield appropriate to assets having similar financial characteristics.

– Notes 12 and 20 regarding inventory of buildings held for sale and inventory of lands,

with respect to determination of the need to write down to net realizable value of the balances of inventory of lands and the inventory of buildings held for sale.

G. Change in classification In the statement of financial position as at December 31, 2009, the Company reclassified

various asset and liability items in amounts that are not material.

29

Africa Israel Investments Ltd. Notes to the Consolidated Financial Statements

At December 31, 2010 Note 2 – Basis of Preparation of the Financial Statements (Cont.)

H. Changes in accounting policies

(1) Business combinations and transactions with holders of rights not conferring control

Commencing from January 1, 2010 the Group applies IFRS 3 Business Combinations

(2008) and the amendment to IAS 27 from 2008 Consolidated and Separate Financial Statements (2008) (hereinafter – “IFRS 3” and “IAS 27”, respectively). In addition, commencing from this date, the Group is making early application of the following amendments to IFRS 3, which were published as part of the Improvements Project for 2010: an amendment with respect to the matter of a transitional rule relating to contingent consideration in a business combination occurring prior to the commencement date of IFRS 3; an amendment with respect to the matter of measurement of rights not conferring control, and an amendment with respect to the matter of share-based payment transactions that are not replaced or that are voluntarily replaced.

For additional information regarding the Group’s accounting policies in connection

with business combinations and transactions with holders of rights not conferring control – see Note 3 “Significant Accounting Policies”.

The changes in the accounting polices detailed above are being applied prospectively,

except for the impact of the retroactive application in respect of presentation of options of subsidiaries, in the amounts of about NIS 17,757 thousand and about NIS 19,173 thousand as at December 31, 2009 and December 31, 2008, respectively, which are now presented in the category “holders of rights not conferring control” in the statement of financial position.

In addition, acquisition of rights not conferring control, in the amount of about

NIS 5,516 thousand, for the year ended December 31, 2009 and about NIS 121,599 thousand, for the year ended December 31, 2008, were reclassified in the statements of cash flows from investing activities to financing activities, pursuant to the transitional rules of IAS 7, Statement of Cash Flows, as a result of the initial application of IFRS 3 and IAS 27.

In respect of partial realization of the Group’s holdings in the subsidiaries Africa

Properties and AFI Development, during the year ended December 31, 2010, the Group recognized the amount of about NIS 784 million, which was recorded to equity instead of on the statement of income, as would have been the case if the new Standard had not been adopted.

(2) Leases Commencing from January 1, 2010, the Group applies the amendment to IAS 17,

“Leases – Classification of Leases of Land and Buildings” (hereinafter – “the Amendment”), which was published as part of the Improvements to IFRS project from 2009.

30

Africa Israel Investments Ltd. Notes to the Consolidated Financial Statements

At December 31, 2010 Note 2 – Basis of Preparation of the Financial Statements (Cont.)

H. Changes in accounting policies (Cont.)

(2) Leases (Cont.) In accordance with the Amendment, the requirement no longer exists to classify a

lease of land as an operating lease in every case that the ownership is not expected to pass to the lessee at the end of the lease period. In accordance with the amended standard, the requirement is to examine the land lease in accordance with the regular criteria for classifying a lease as a financing lease or as an operating lease.

In addition, it is provided that in a lease of land and buildings, the land component and

buildings component are to be examined separately for purposes of classification of the leased items, based on these criteria, where a significant consideration regarding classification of the land is the fact that land normally has an indefinite useful life.

The Amendment is being applied retroactively with respect to existing leases where

the required information is available on the commencement date of the lease. Where the required information is not available, land leases will be re-examined on the adoption date of the standard.

The Group has lands (that are not investment property measured at fair value) held as

part of a lease arrangement with the Israel Lands Administration, where the payment in respect thereof is made every period. As a result of application of the new standard, the Group recognizes an asset and a liability in respect of a financing lease based on the lower of the fair value of the land or the present value of the minimum lease payments on the date of the lease undertaking.

The Group has lands leased from the Israel Lands Administration where the related

lease fees were paid in advance on the date of the lease undertaking. Amounts paid in respect of the above-mentioned leases, totaling about NIS 74,332 thousand as at December 31, 2009, and that were presented in the statement of financial position in the “prepaid expenses in respect of long-term operating leases” category, are now presented as part of the “property, plant and equipment” category, in light of the fact that pursuant to the Amendment leases are classified as financing leases.

(3) Decline in value of assets Commencing from January 1, 2010, the Group applies the amendment to IAS 36

“Decline in Value of Assets – Allocation of Goodwill to Cash Generating Units” (hereinafter – “the Amendment”), which was published as part of the Improvements to IFRS project from 2009. In accordance with the Amendment, for purposes of impairment testing, the largest cash-generating unit to which goodwill is to be allocated should not exceed the operating segment level as defined in IFRS 8 before applying the aggregation criteria in Section 12 of IFRS 8. The Amendment is being applied prospectively. The Group elected to examine decline in value of the goodwill in accordance with the Amendment’s transitional rules on the fixed date for the annual examination.

31

Africa Israel Investments Ltd. Notes to the Consolidated Financial Statements

At December 31, 2010 Note 2 – Basis of Preparation of the Financial Statements (Cont.)

H. Changes in accounting policies (Cont.)

(4) Exchange of debt and equity instruments Commencing from January 1, 2010, the Group is making early application of