affordable loan & program matrix december 20

TRANSCRIPT

1 | P a g e Minnesota Homeownership Center

December 2020

Affordable Loan & Program Matrix – December 2020This tool is designed for housing counselors and industry professionals. If you are purchasing your first home and would like

to learn more about mortgage loans that might be right for you, contact a Homeownership Advisor in your area for

unbiased, professional information. To find a local Homeownership Advisor visit www.hocmn.org or call the Minnesota

Homeownership Center at (651) 659-9336.

PURPOSE: Produced by the Minnesota Homeownership Center, this tool is intended to inform homeownership advisors and

industry professionals of affordable loans and programs available to their customers. It is not designed for consumers. Loans and

programs included in the Matrix generally have flexible underwriting guidelines, allow higher LTV limits, lower buyer investment

and require homebuyer education and/or counseling.

This Matrix is updated by the Center biannually. Please note loan criteria may change prior to the next scheduled update.

Questions regarding programs should be directed to the lender or program contact. If you have specific questions about the Matrix

or would like to add your program, please contact the Center by email: [email protected]

Table of Contents 1

Associated Bank – CARE (Community Affordable Real Estate) Product ....................................................................................................................... 2

Bremer – Gateway Community Mortgage Program ....................................................................................................................................................... 4 BMO Harris Bank – Neighborhood Home Loan Product (NHLP) ................................................................................................................................... 3

Community Land Trusts ................................................................................................................................................................................................. 5 Dakota County CDA’s First Time Homebuyer Program ................................................................................................................................................. 8 FHA – 203B, 203(k) Streamlined ................................................................................................................................................................................... 9

Minnesota Housing - Start Up ....................................................................................................................................................................................... 11 Minnesota Housing – Step Up ...................................................................................................................................................................................... 12

Sunrise Banks Open Door Program (with ITIN option) ................................................................................................................................................. 14 Section 184 Indian Home Loan Guarantee Program .................................................................................................................................................... 13

TCHFH Lending, Inc. – Twin Cities Habitat for Humanity Loan Fund ........................................................................................................................... 15 US Bank – American Dream ........................................................................................................................................................................................ 16 USDA Rural Development 502 Direct ............................................ ............................................................................................................................... 17

USDA Rural Development 502 Guaranteed Loans ...................................................................................................................................................... 18Wells Fargo Bank – yourFirst Mortgage ......................................................................................................................................................... 19

Loan programs are compiled by the Center based on the most recent available information. Information is subject to change.

Midwest One – First Home Now.................................................................................................................................................................................... 10

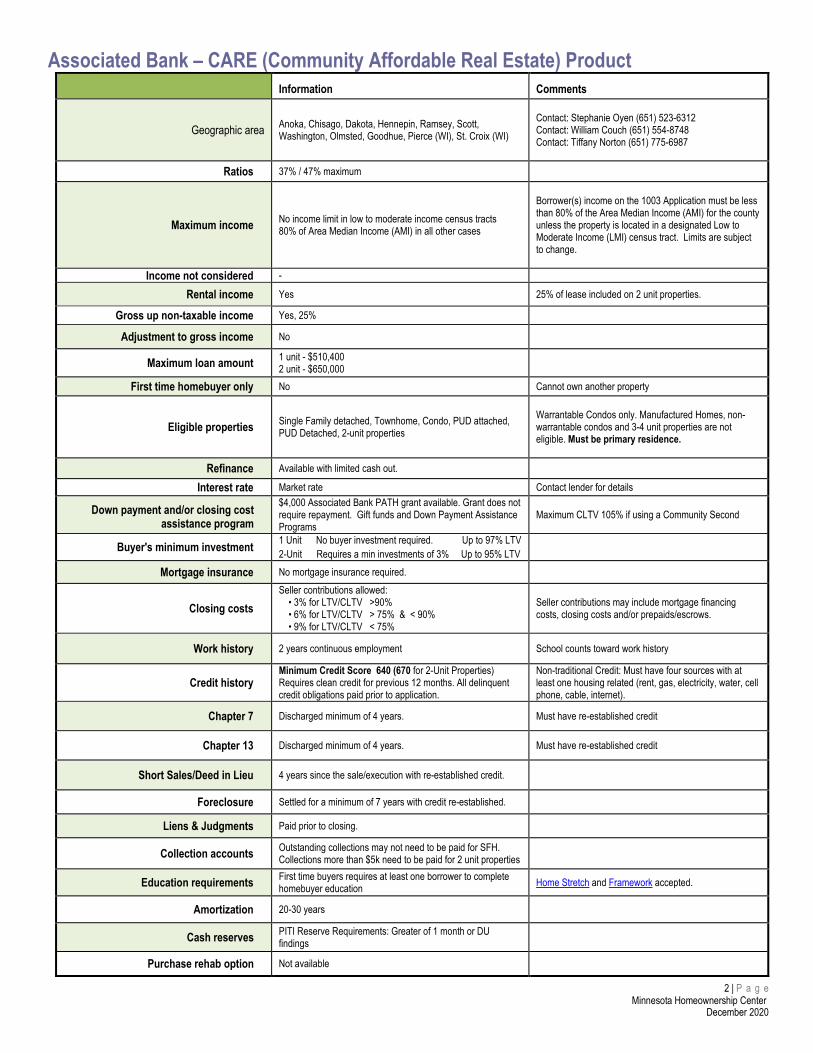

Associated Bank – CARE (Community Affordable Real Estate) Product Information Comments

Geographic area Anoka, Chisago, Dakota, Hennepin, Ramsey, Scott, Washington, Olmsted, Goodhue, Pierce (WI), St. Croix (WI)

Contact: Stephanie Oyen (651) 523-6312 Contact: William Couch (651) 554-8748 Contact: Tiffany Norton (651) 775-6987

Ratios 37% / 47% maximum

Maximum income No income limit in low to moderate income census tracts 80% of Area Median Income (AMI) in all other cases

Borrower(s) income on the 1003 Application must be less than 80% of the Area Median Income (AMI) for the county unless the property is located in a designated Low to Moderate Income (LMI) census tract. Limits are subject to change.

Income not considered -

Rental income Yes 25% of lease included on 2 unit properties.

Gross up non-taxable income Yes, 25%

Adjustment to gross income No

Maximum loan amount 1 unit - $510,400 2 unit - $650,000

First time homebuyer only No Cannot own another property

Eligible properties Single Family detached, Townhome, Condo, PUD attached, PUD Detached, 2-unit properties

Warrantable Condos only. Manufactured Homes, non-warrantable condos and 3-4 unit properties are not eligible. Must be primary residence.

Refinance Available with limited cash out.

Interest rate Market rate Contact lender for details

Down payment and/or closing cost assistance program

$4,000 Associated Bank PATH grant available. Grant does not require repayment. Gift funds and Down Payment Assistance Programs

Maximum CLTV 105% if using a Community Second

Buyer's minimum investment 1 Unit No buyer investment required. Up to 97% LTV 2-Unit Requires a min investments of 3% Up to 95% LTV

Mortgage insurance No mortgage insurance required.

Closing costs Seller contributions allowed:

• 3% for LTV/CLTV >90% • 6% for LTV/CLTV > 75% & < 90% • 9% for LTV/CLTV < 75%

Seller contributions may include mortgage financing costs, closing costs and/or prepaids/escrows.

Work history 2 years continuous employment School counts toward work history

Credit history Minimum Credit Score 640 (670 for 2-Unit Properties) Requires clean credit for previous 12 months. All delinquent credit obligations paid prior to application.

Non-traditional Credit: Must have four sources with at least one housing related (rent, gas, electricity, water, cell phone, cable, internet).

Chapter 7 Discharged minimum of 4 years. Must have re-established credit

Chapter 13 Discharged minimum of 4 years. Must have re-established credit

Short Sales/Deed in Lieu 4 years since the sale/execution with re-established credit.

Foreclosure Settled for a minimum of 7 years with credit re-established.

Liens & Judgments Paid prior to closing.

Collection accounts Outstanding collections may not need to be paid for SFH. Collections more than $5k need to be paid for 2 unit properties

Education requirements First time buyers requires at least one borrower to complete homebuyer education Home Stretch and Framework accepted.

Amortization 20-30 years

Cash reserves PITI Reserve Requirements: Greater of 1 month or DU findings

Purchase rehab option Not available

2 | P a g e Minnesota Homeownership Center

December 2020

BMO Harris Bank – Neighborhood Home Loan Product (NHLP) Information Comments

Geographic area Properties located in designated counties in Minnesota The property must be located in a Low or Moderate Income Census Tract or borrower income must be below Low Income Limit

Ratios 40% for FICO < 680; 43% for FICO 680 +

Maximum income None

Income not considered Must follow Freddie Mac’s guidelines

Rental income No Borrowers with NHLP mortgages may not have any ownership interest in any other residential properties as of the Note Date.

Gross up non-taxable income -

Adjustment to gross income -

Maximum loan amount Conforming

First time homebuyer only No Homebuyer education required for purchase transactions.

Eligible properties Single Family, Condominium, Townhouse, PUD and Manufactured Homes

1‐2 Units only, Primary Residence (owner-occupied) Only Non‐occupant co‐borrowers are not eligible.

Refinance Yes - Rate/Term Refinance only Interest rate Note Rate /Fixed for Life of Loan for the 30 year FRM 5/1 ARM also available

Down payment and/or closing cost assistance program Approved affordable seconds and/or Grants available

Buyer's minimum investment Must be borrower own funds. Minimum Borrower Contribution: Greater of $1,000 or 1% of loan amount (3% if FICO <660)

Note: On refinance transactions, Equity can be used to meet the minimum borrower contribution. Down payment Requirements: Purchase (1 unit): 3%, Purchase (2 unit): 5% Refinance (1‐2 unit): 5%

Mortgage insurance No

Closing costs Seller contributions allowed, cannot exceed 3% of the lesser of sales price or appraised value on LTVs > 90% and 6% on LTVs < 90%. Seller contributions may include mortgage financing costs, closing costs and/or prepaids/escrows.

Work history 2 years verifiable income Must follow Freddie Mac’s guidelines

Credit history Purchase: 660 Refinance: 680 FICO

Regardless of the credit score, borrowers need three valid trade lines but those do not have to be on the credit report. The trade lines need to meet Freddie Mac’s guideline for non‐traditional or alternative credit (see Freddie Mac. All Regs, Chapter 37.4 (b) for further details).

Chapter 7 Must follow Freddie Mac’s guidelines

Chapter 13 Must follow Freddie Mac’s guidelines

Liens -

Foreclosure -

Judgments -

Collection accounts -

Education requirements Homebuyer education is required for all purchase transactions. The Purchase Counseling Advisory Letter must be signed at closing as it is required for all purchase transactions. Home Stretch and Framework are accepted.

Amortization 30 Years Insurance and tax escrows are required.

Cash reserves None required

Purchase rehab option No- limited repair loan. Repairs limited to those which do not affect the livability of the home. Max amount of repairs cannot exceed 15% ($10,000 for Conv., $5,000 for FHA) of “As Completed” value.

Escrow requirements: 110% for Conventional or 150% for FHA ($500 minimum). Percentage based on estimated cost of repairs.

3 | P a g e Minnesota Homeownership Center

December 2020

Bremer – Gateway Community Mortgage Program Information Comments

Geographic area Bremer Bank lending areas of MN, ND and WI Home must be located in a low or moderate census tract

Ratios 43%

Maximum income No income limit

Income not considered • Self-employed with duration less than 1 year • Part-time received for less than 1 year• Income if returned to workforce for less than 6 months

Maximum Loan to Value 97% Combined Loan to Value to 105% with acceptable down payment assistance programs approved by Bremer Bank

Gross up non-taxable income Available contact lender for details Must follow current portfolio guidelines

Adjustment to gross income - -

Maximum loan amount $307,900 No minimum

First time homebuyer only No

Eligible properties

• Single Family• Condominiums and townhomes (conforming to FNMA req.) • Planned Unit Developments• Community Land Trusts• Acreage limited to 10 acre parcels

Refinance No Only permitted to improve Bremer Bank’s position for a loan held in our in-house portfolio

Interest rate Slightly higher than Market Rate, Fixed

Down payment and/or closing cost assistance program

Allowable from acceptable sources Contact lender for details

Buyer's minimum investment 1% or $1000 Whichever is less

Mortgage insurance Not applicable

Additional closing costs No

Work history Two years continuous stable income College is acceptable as part of the two year history and documented

Credit history • No foreclosure within the last 7 years• Minimum 640 credit score • All collections, judgements and liens must be paid in full

Non-traditional credit: must have 3 sources – rent receipts, utility payments, telephone or cable bills, or other sources of credit or services for which the borrower has/had a regular financial obligation

Chapter 7 Follow FNMA Guidelines

Chapter 13 Follow FNMA Guidelines

Liens Paid in full

Foreclosure None within the last 7 years Explanations required

Judgments Paid in full with 3rd party verification required of reason for default (default must be beyond borrower’s control).

Collection accounts Paid in full

Education requirements Yes. Sole borrower must attend. For co-borrowers, at least one borrower must attend.

www.hocmn.org to find a Home Stretch workshop or register for the online course Framework

Amortization 30 years fixed, fully amortizing

Cash reserves One month reserves of PITI Must be accessible

Purchase rehab option Not available

4 | P a g e Minnesota Homeownership Center

December 2020

5 | P a g e Minnesota Homeownership Center

December 2020

Information Comments

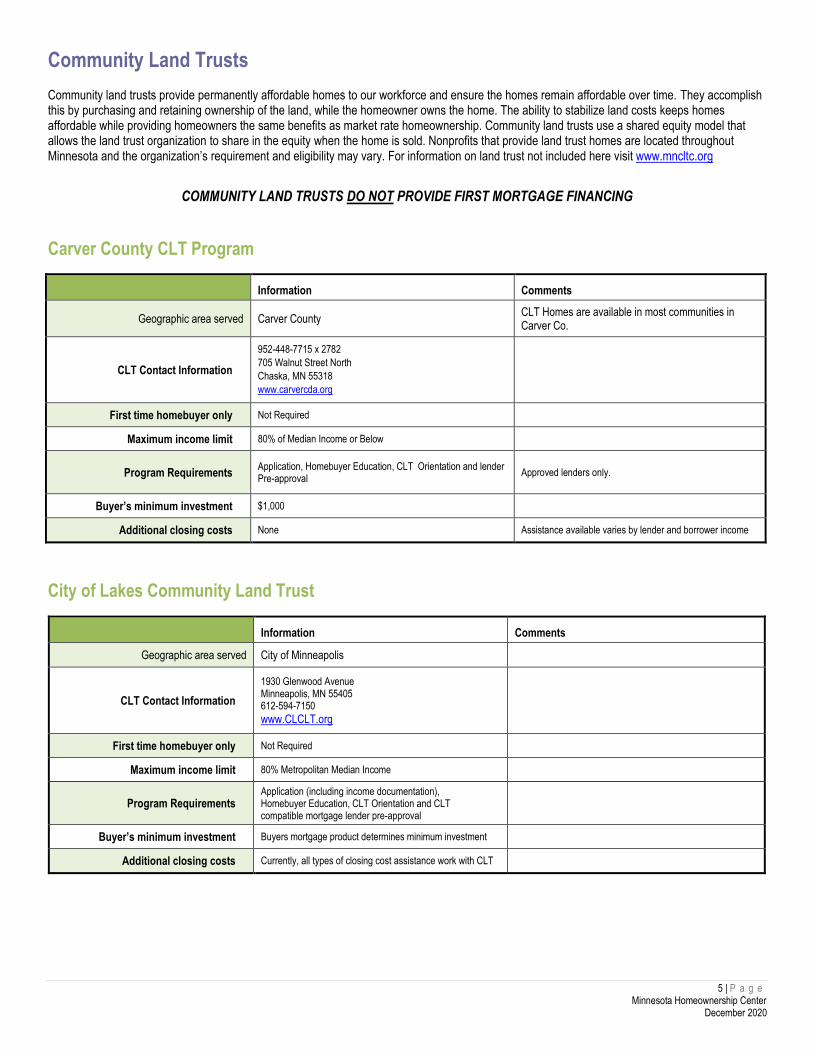

Geographic area served Carver County CLT Homes are available in most communities in Carver Co.

CLT Contact Information

952-448-7715 x 2782

705 Walnut Street North

Chaska, MN 55318

www.carvercda.org

First time homebuyer only Not Required

Maximum income limit 80% of Median Income or Below

Program Requirements Application, Homebuyer Education, CLT Orientation and lender Pre-approval

Approved lenders only.

Buyer’s minimum investment $1,000

Additional closing costs None Assistance available varies by lender and borrower income

Information Comments

Geographic area served City of Minneapolis

CLT Contact Information

1930 Glenwood Avenue Minneapolis, MN 55405 612-594-7150

www.CLCLT.org

First time homebuyer only Not Required

Maximum income limit 80% Metropolitan Median Income

Program Requirements Application (including income documentation), Homebuyer Education, CLT Orientation and CLT compatible mortgage lender pre-approval

Buyer’s minimum investment Buyers mortgage product determines minimum investment

Additional closing costs Currently, all types of closing cost assistance work with CLT

Community Land Trusts

Community land trusts provide permanently affordable homes to our workforce and ensure the homes remain affordable over time. They accomplish this by purchasing and retaining ownership of the land, while the homeowner owns the home. The ability to stabilize land costs keeps homes affordable while providing homeowners the same benefits as market rate homeownership. Community land trusts use a shared equity model that allows the land trust organization to share in the equity when the home is sold. Nonprofits that provide land trust homes are located throughout Minnesota and the organization’s requirement and eligibility may vary. For information on land trust not included here visit www.mncltc.org

COMMUNITY LAND TRUSTS DO NOT PROVIDE FIRST MORTGAGE FINANCING

Carver County CLT Program

City of Lakes Community Land Trust

6 | P a g e Minnesota Homeownership Center

December 2020

Information Comments

Geographic area served Rochester & 30-mile surrounding area

CLT Contact Information:

507-287-7117

12 Elton Hills Drive NW

Rochester, MN 55901

First time homebuyer only Not Required

Maximum income limit 80% of State Median Income

Program Requirements Meet income limit; Qualify for Mortgage; Home Buyer Education

Buyer’s minimum investment 1% of purchase price

Additional closing costs None Gap loan available if needed

Information Comments

Geographic area served Duluth and surrounding communities.

CLT Contact Information 12 East 4th Street

Duluth, MN 55805

www.1roofhousing.org | 218-727-5372

First time homebuyer only Not required

Maximum income limit 80% Area Median Income Some units available up to 115% AMI

Program Requirements Application, Homebuyer education, CLT Orientation and lender Preapproval

Buyer’s minimum investment $1000

Additional closing costs Recording fees for ground lease and related documents.

Information Comments

Geographic area served Suburbs of Hennepin County

Bloomington, Brooklyn Park, Crystal, Deephaven, Eden Prairie, Edina, Golden Valley, Maple Grove, Minnetonka, New Hope, Plymouth Richfield, St. Louis Park and Wayzata

CLT Contact Information 5101 Thimsen Avenue, Suite 202

Minnetonka, MN 55345

www.homeswithinreach.org | 952-401-7071

First time homebuyer only Not Required

Maximum income limit 80% of Hennepin County Housing Consortium Income Limits (HUD)

Program Requirements Application, Homebuyer Education, CLT Orientation and lender Pre-approval

Buyer’s minimum investment $1,000

Additional closing costs None

First Homes

Homes Within Reach

One Roof Community Housing

7 | P a g e Minnesota Homeownership Center

December 2020

Information Comments

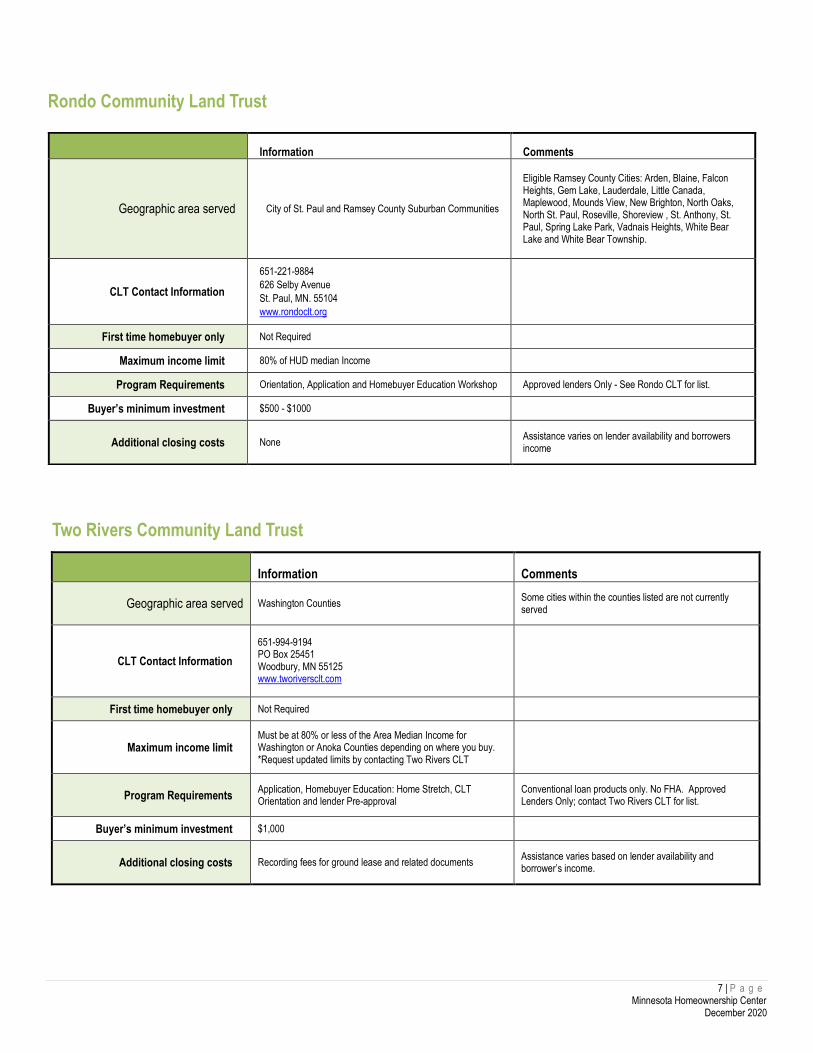

Geographic area served Washington Counties Some cities within the counties listed are not currently served

CLT Contact Information

651-994-9194 PO Box 25451 Woodbury, MN 55125 www.tworiversclt.com

First time homebuyer only Not Required

Maximum income limit Must be at 80% or less of the Area Median Income for Washington or Anoka Counties depending on where you buy. *Request updated limits by contacting Two Rivers CLT

Program Requirements Application, Homebuyer Education: Home Stretch, CLT Orientation and lender Pre-approval

Conventional loan products only. No FHA. Approved Lenders Only; contact Two Rivers CLT for list.

Buyer’s minimum investment $1,000

Additional closing costs Recording fees for ground lease and related documents Assistance varies based on lender availability and borrower’s income.

Rondo Community Land Trust

Two Rivers Community Land Trust

Information Comments

Geographic area served City of St. Paul and Ramsey County Suburban Communities

Eligible Ramsey County Cities: Arden, Blaine, Falcon Heights, Gem Lake, Lauderdale, Little Canada, Maplewood, Mounds View, New Brighton, North Oaks, North St. Paul, Roseville, Shoreview , St. Anthony, St. Paul, Spring Lake Park, Vadnais Heights, White Bear Lake and White Bear Township.

CLT Contact Information

651-221-9884

626 Selby Avenue

St. Paul, MN. 55104

www.rondoclt.org

First time homebuyer only Not Required

Maximum income limit 80% of HUD median Income

Program Requirements Orientation, Application and Homebuyer Education Workshop Approved lenders Only - See Rondo CLT for list.

Buyer’s minimum investment $500 - $1000

Additional closing costs None Assistance varies on lender availability and borrowers income

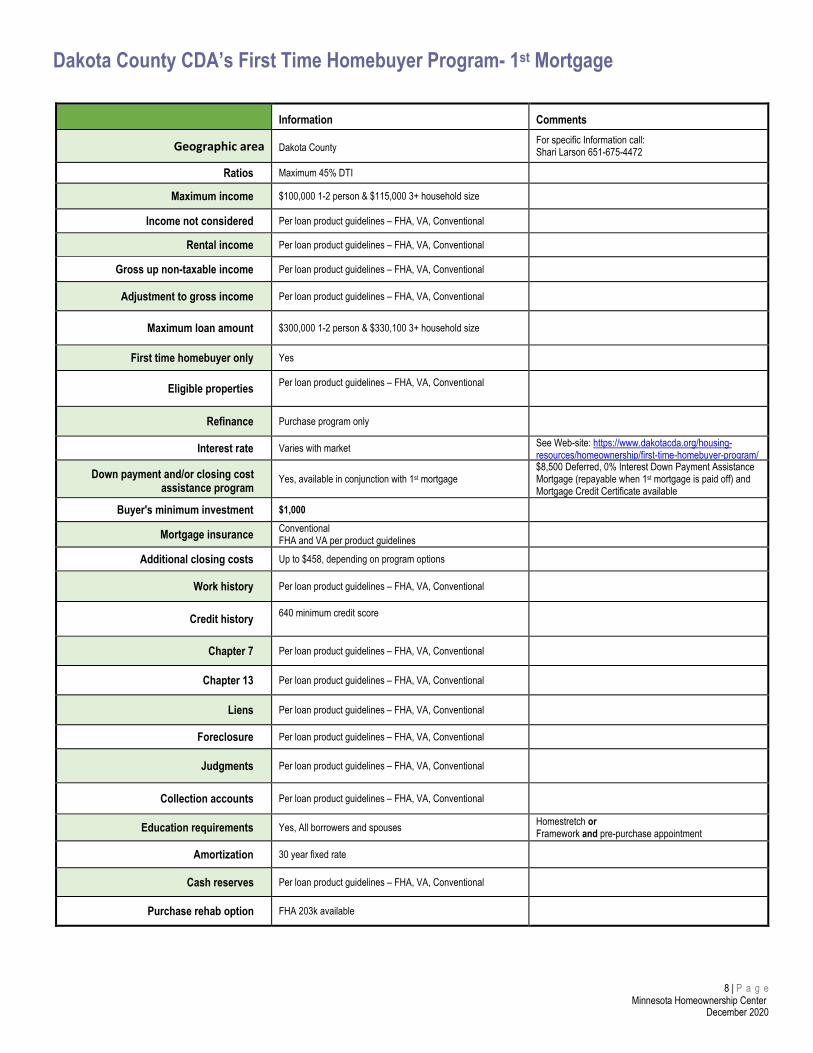

Dakota County CDA’s First Time Homebuyer Program- 1st Mortgage

Information Comments

Geographic area Dakota County For specific Information call: Shari Larson 651-675-4472

Ratios Maximum 45% DTI

Maximum income $100,000 1-2 person & $115,000 3+ household size

Income not considered Per loan product guidelines – FHA, VA, Conventional

Rental income Per loan product guidelines – FHA, VA, Conventional

Gross up non-taxable income Per loan product guidelines – FHA, VA, Conventional

Adjustment to gross income Per loan product guidelines – FHA, VA, Conventional

Maximum loan amount $300,000 1-2 person & $330,100 3+ household size

First time homebuyer only Yes

Eligible properties Per loan product guidelines – FHA, VA, Conventional

Refinance Purchase program only

Interest rate Varies with market See Web-site: https://www.dakotacda.org/housing-resources/homeownership/first-time-homebuyer-program/ Down payment and/or closing cost

assistance program Yes, available in conjunction with 1st mortgage

$8,500 Deferred, 0% Interest Down Payment Assistance Mortgage (repayable when 1st mortgage is paid off) and Mortgage Credit Certificate available

Buyer's minimum investment $1,000

Mortgage insurance Conventional FHA and VA per product guidelines

Additional closing costs Up to $458, depending on program options

Work history Per loan product guidelines – FHA, VA, Conventional

Credit history 640 minimum credit score

Chapter 7 Per loan product guidelines – FHA, VA, Conventional

Chapter 13 Per loan product guidelines – FHA, VA, Conventional

Liens Per loan product guidelines – FHA, VA, Conventional

Foreclosure Per loan product guidelines – FHA, VA, Conventional

Judgments Per loan product guidelines – FHA, VA, Conventional

Collection accounts Per loan product guidelines – FHA, VA, Conventional

Education requirements Yes, All borrowers and spouses Homestretch or Framework and pre-purchase appointment

Amortization 30 year fixed rate

Cash reserves Per loan product guidelines – FHA, VA, Conventional

Purchase rehab option FHA 203k available

8 | P a g e Minnesota Homeownership Center

December 2020

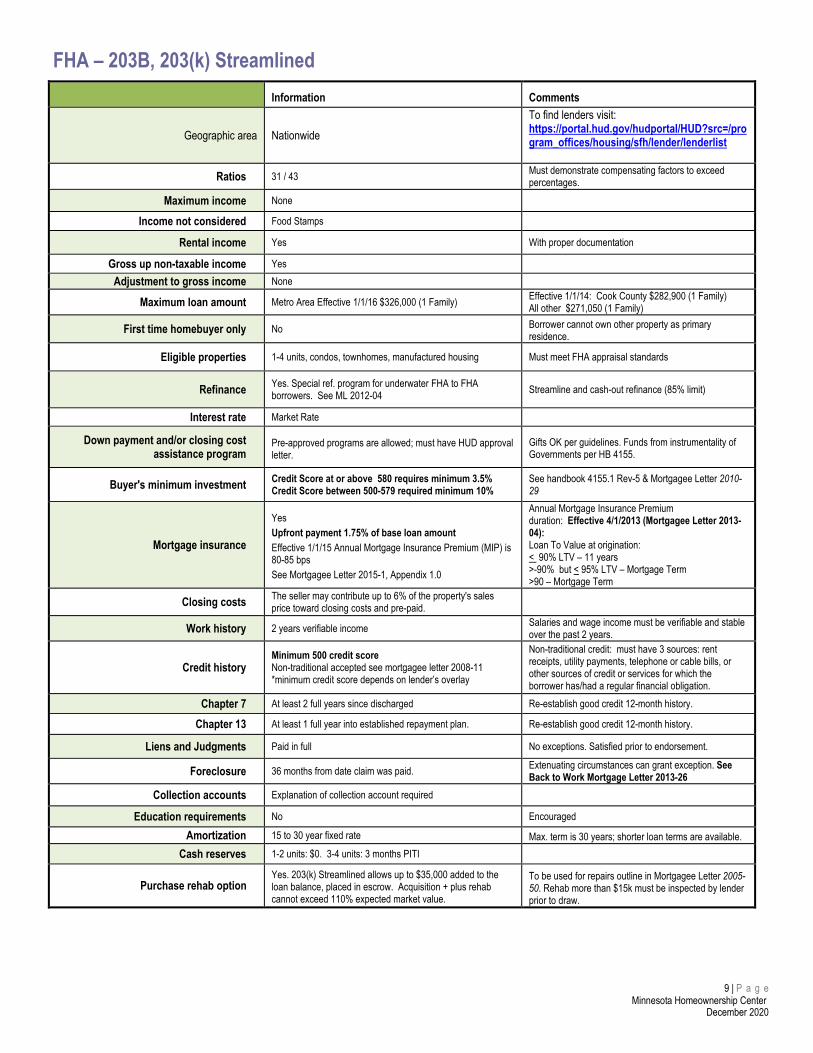

FHA – 203B, 203(k) Streamlined Information Comments

Geographic area Nationwide To find lenders visit: https://portal.hud.gov/hudportal/HUD?src=/program_offices/housing/sfh/lender/lenderlist

Ratios 31 / 43 Must demonstrate compensating factors to exceed percentages.

Maximum income None

Income not considered Food Stamps

Rental income Yes With proper documentation

Gross up non-taxable income Yes Adjustment to gross income None

Maximum loan amount Metro Area Effective 1/1/16 $326,000 (1 Family) Effective 1/1/14: Cook County $282,900 (1 Family) All other $271,050 (1 Family)

First time homebuyer only No Borrower cannot own other property as primary residence.

Eligible properties 1-4 units, condos, townhomes, manufactured housing Must meet FHA appraisal standards

Refinance Yes. Special ref. program for underwater FHA to FHA borrowers. See ML 2012-04 Streamline and cash-out refinance (85% limit)

Interest rate Market Rate

Down payment and/or closing cost assistance program

Pre-approved programs are allowed; must have HUD approval letter.

Gifts OK per guidelines. Funds from instrumentality of Governments per HB 4155.

Buyer's minimum investment Credit Score at or above 580 requires minimum 3.5% Credit Score between 500-579 required minimum 10%

See handbook 4155.1 Rev-5 & Mortgagee Letter 2010-29

Mortgage insurance

Yes Upfront payment 1.75% of base loan amount Effective 1/1/15 Annual Mortgage Insurance Premium (MIP) is 80-85 bps See Mortgagee Letter 2015-1, Appendix 1.0

Annual Mortgage Insurance Premium duration: Effective 4/1/2013 (Mortgagee Letter 2013-04): Loan To Value at origination: < 90% LTV – 11 years >-90% but < 95% LTV – Mortgage Term >90 – Mortgage Term

Closing costs The seller may contribute up to 6% of the property's sales price toward closing costs and pre-paid.

Work history 2 years verifiable income Salaries and wage income must be verifiable and stable over the past 2 years.

Credit history Minimum 500 credit score Non-traditional accepted see mortgagee letter 2008-11 *minimum credit score depends on lender’s overlay

Non-traditional credit: must have 3 sources: rent receipts, utility payments, telephone or cable bills, or other sources of credit or services for which the borrower has/had a regular financial obligation.

Chapter 7 At least 2 full years since discharged Re-establish good credit 12-month history.

Chapter 13 At least 1 full year into established repayment plan. Re-establish good credit 12-month history.

Liens and Judgments Paid in full No exceptions. Satisfied prior to endorsement.

Foreclosure 36 months from date claim was paid. Extenuating circumstances can grant exception. See Back to Work Mortgage Letter 2013-26

Collection accounts Explanation of collection account required

Education requirements No Encouraged

Amortization 15 to 30 year fixed rate Max. term is 30 years; shorter loan terms are available. Cash reserves 1-2 units: $0. 3-4 units: 3 months PITI

Purchase rehab option Yes. 203(k) Streamlined allows up to $35,000 added to the loan balance, placed in escrow. Acquisition + plus rehab cannot exceed 110% expected market value.

To be used for repairs outline in Mortgagee Letter 2005-50. Rehab more than $15k must be inspected by lender prior to draw.

9 | P a g e Minnesota Homeownership Center

December 2020

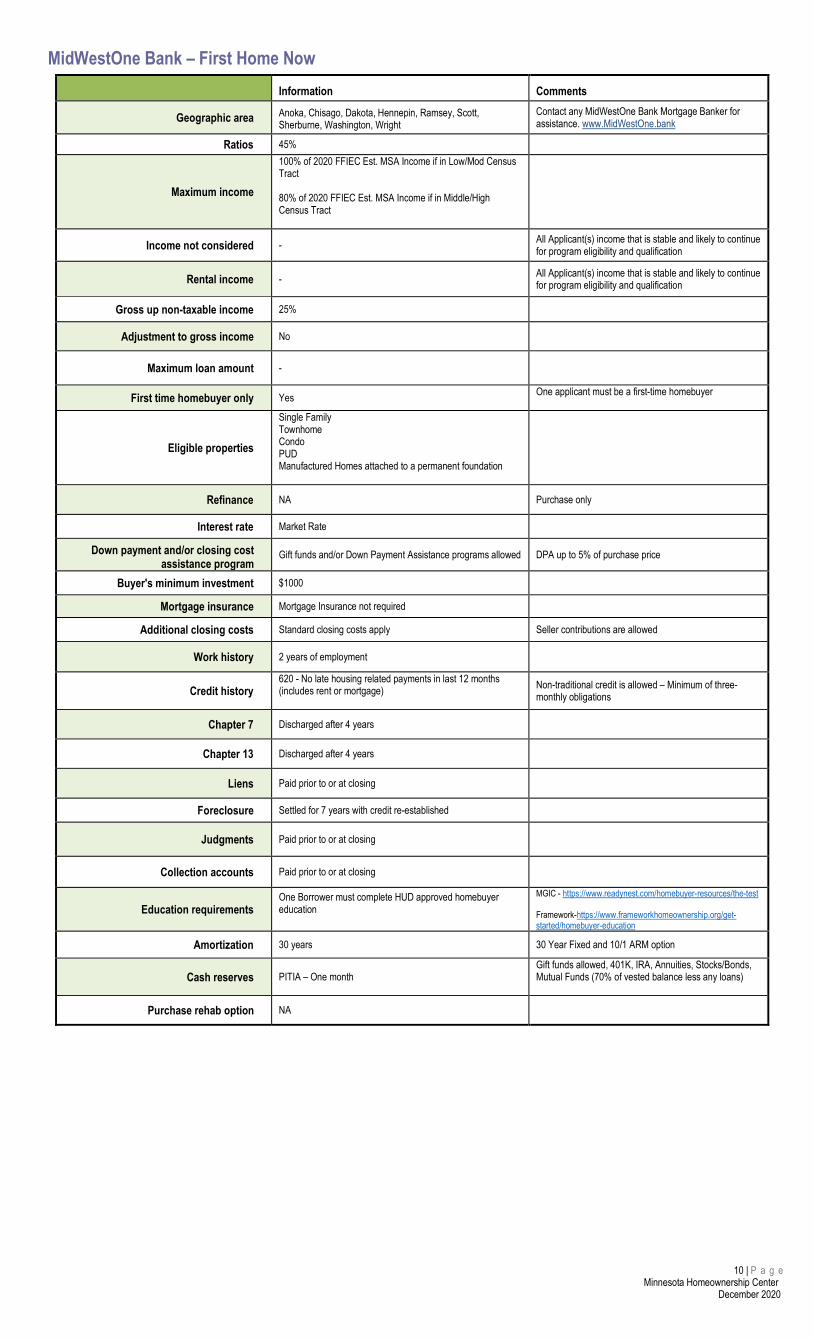

MidWestOne Bank – First Home Now Information Comments

Geographic area Anoka, Chisago, Dakota, Hennepin, Ramsey, Scott, Sherburne, Washington, Wright

Contact any MidWestOne Bank Mortgage Banker for assistance. www.MidWestOne.bank

Ratios 45%

Maximum income

100% of 2020 FFIEC Est. MSA Income if in Low/Mod Census Tract

80% of 2020 FFIEC Est. MSA Income if in Middle/High Census Tract

Income not considered - All Applicant(s) income that is stable and likely to continue for program eligibility and qualification

Rental income - All Applicant(s) income that is stable and likely to continue for program eligibility and qualification

Gross up non-taxable income 25%

Adjustment to gross income No

Maximum loan amount -

First time homebuyer only Yes One applicant must be a first-time homebuyer

Eligible properties

Single Family Townhome Condo PUD Manufactured Homes attached to a permanent foundation

Refinance NA Purchase only

Interest rate Market Rate

Down payment and/or closing cost assistance program

Gift funds and/or Down Payment Assistance programs allowed DPA up to 5% of purchase price

Buyer's minimum investment $1000

Mortgage insurance Mortgage Insurance not required

Additional closing costs Standard closing costs apply Seller contributions are allowed

Work history 2 years of employment

Credit history 620 - No late housing related payments in last 12 months (includes rent or mortgage) Non-traditional credit is allowed – Minimum of three-

monthly obligations

Chapter 7 Discharged after 4 years

Chapter 13 Discharged after 4 years

Liens Paid prior to or at closing

Foreclosure Settled for 7 years with credit re-established

Judgments Paid prior to or at closing

Collection accounts Paid prior to or at closing

Education requirements One Borrower must complete HUD approved homebuyer education

MGIC - https://www.readynest.com/homebuyer-resources/the-test

Framework-https://www.frameworkhomeownership.org/get-started/homebuyer-education

Amortization 30 years 30 Year Fixed and 10/1 ARM option

Cash reserves PITIA – One month Gift funds allowed, 401K, IRA, Annuities, Stocks/Bonds, Mutual Funds (70% of vested balance less any loans)

Purchase rehab option NA

10 | P a g e Minnesota Homeownership Center

December 2020

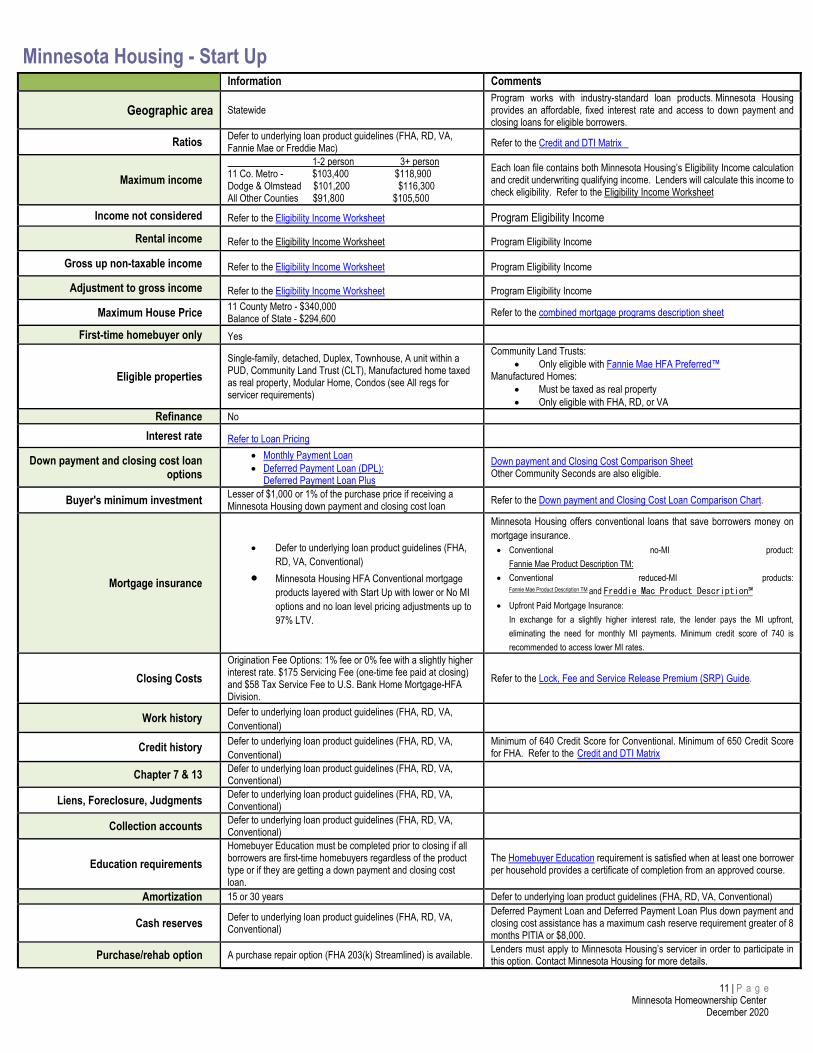

Minnesota Housing - Start Up Information Comments

Geographic area StatewideProgram works with industry-standard loan products. Minnesota Housing provides an affordable, fixed interest rate and access to down payment and closing loans for eligible borrowers.

Ratios Defer to underlying loan product guidelines (FHA, RD, VA, Fannie Mae or Freddie Mac) Refer to the Credit and DTI Matrix

Maximum income 1-2 person 3+ person

11 Co. Metro - $103,400 $118,900 Dodge & Olmstead $101,200 $116,300 All Other Counties $91,800 $105,500

Each loan file contains both Minnesota Housing’s Eligibility Income calculation and credit underwriting qualifying income. Lenders will calculate this income to check eligibility. Refer to the Eligibility Income Worksheet

Income not considered Refer to the Eligibility Income Worksheet Program Eligibility Income

Rental income Refer to the Eligibility Income Worksheet Program Eligibility Income

Gross up non-taxable income Refer to the Eligibility Income Worksheet Program Eligibility Income Adjustment to gross income Refer to the Eligibility Income Worksheet Program Eligibility Income

Maximum House Price 11 County Metro - $340,000 Balance of State - $294,600 Refer to the combined mortgage programs description sheet

First-time homebuyer only Yes

Eligible properties Single-family, detached, Duplex, Townhouse, A unit within a PUD, Community Land Trust (CLT), Manufactured home taxed as real property, Modular Home, Condos (see All regs for servicer requirements)

Community Land Trusts: • Only eligible with Fannie Mae HFA Preferred™

Manufactured Homes: • Must be taxed as real property• Only eligible with FHA, RD, or VA

Refinance No Interest rate Refer to Loan Pricing

Down payment and closing cost loan options

• Monthly Payment Loan• Deferred Payment Loan (DPL):

Deferred Payment Loan Plus

Down payment and Closing Cost Comparison Sheet Other Community Seconds are also eligible.

Buyer's minimum investment Lesser of $1,000 or 1% of the purchase price if receiving a Minnesota Housing down payment and closing cost loan Refer to the Down payment and Closing Cost Loan Comparison Chart.

Mortgage insurance

• Defer to underlying loan product guidelines (FHA, RD, VA, Conventional)

• Minnesota Housing HFA Conventional mortgage products layered with Start Up with lower or No MI options and no loan level pricing adjustments up to 97% LTV.

Minnesota Housing offers conventional loans that save borrowers money on mortgage insurance. • Conventional no-MI product:

Fannie Mae Product Description TM: • Conventional reduced-MI products:

Fannie Mae Product Description TM and Freddie Mac Product Description℠ • Upfront Paid Mortgage Insurance:

In exchange for a slightly higher interest rate, the lender pays the MI upfront,eliminating the need for monthly MI payments. Minimum credit score of 740 isrecommended to access lower MI rates.

Closing Costs Origination Fee Options: 1% fee or 0% fee with a slightly higher interest rate. $175 Servicing Fee (one-time fee paid at closing) and $58 Tax Service Fee to U.S. Bank Home Mortgage-HFA Division.

Refer to the Lock, Fee and Service Release Premium (SRP) Guide.

Work history Defer to underlying loan product guidelines (FHA, RD, VA, Conventional)

Credit history Defer to underlying loan product guidelines (FHA, RD, VA, Conventional)

Minimum of 640 Credit Score for Conventional. Minimum of 650 Credit Score for FHA. Refer to the Credit and DTI Matrix

Chapter 7 & 13 Defer to underlying loan product guidelines (FHA, RD, VA, Conventional)

Liens, Foreclosure, Judgments Defer to underlying loan product guidelines (FHA, RD, VA, Conventional)

Collection accounts Defer to underlying loan product guidelines (FHA, RD, VA, Conventional)

Education requirements Homebuyer Education must be completed prior to closing if all borrowers are first-time homebuyers regardless of the product type or if they are getting a down payment and closing cost loan.

The Homebuyer Education requirement is satisfied when at least one borrower per household provides a certificate of completion from an approved course.

Amortization 15 or 30 years Defer to underlying loan product guidelines (FHA, RD, VA, Conventional)

Cash reserves Defer to underlying loan product guidelines (FHA, RD, VA, Conventional)

Deferred Payment Loan and Deferred Payment Loan Plus down payment and closing cost assistance has a maximum cash reserve requirement greater of 8 months PITIA or $8,000.

Purchase/rehab option A purchase repair option (FHA 203(k) Streamlined) is available. Lenders must apply to Minnesota Housing’s servicer in order to participate in this option. Contact Minnesota Housing for more details.

11 | P a g e Minnesota Homeownership Center

December 2020

Minnesota Housing – Step Up Information Comments

Geographic area StatewideProgram works with industry-standard loan products. Minnesota Housing provides affordable, fixed interest rates and access to Monthly Payment Loan for eligible borrowers.

Ratios Defer to underlying loan product guidelines (FHA, RD, VA, Fannie Mae or Freddie Mac) See the Credit and DTI Matrix

Maximum income 11 Co. Metro - $154,600 Dodge & Olmstead $154,600 All Other Counties $137,200

Monthly Payment Income Limits align with the Step Up Program.

Income not considered Defer to underlying loan product guidelines (FHA, RD, VA, Conventional) Qualifying income guidelines Rental income Defer to underlying loan product guidelines (FHA, RD, VA, Conventional) Qualifying income guidelines

Gross up non-taxable income Defer to underlying loan product guidelines (FHA, RD, VA, Conventional) Qualifying income guidelines Adjustment to gross income Defer to underlying loan product guidelines (FHA, RD, VA, Conventional) Qualifying income guidelines

Maximum House Price One unit Two unit

11 County Metro - $382,950 $490,250Balance of State - $331,760 $424,800

Refer to the combined mortgages program descriptions sheet.

First-time homebuyer only No Step Up is available to repeat homebuyers or current

Eligible properties Single-family, detached, Duplex, Townhouse, A unit within a PUD, Community Land Trust (CLT), Manufactured home taxed as real property, Modular Home, Condos (see all regulations for servicer requirements)

Community Land Trusts: • Only eligible with Fannie Mae HFA Preferred™

Manufactured Homes: • Must be taxed as real property• Only eligible with FHA, RD, or VA

Refinance Yes Interest rate Visit: Minnesota Housing Interest Rates

Down payment and closing cost loan options Minnesota Housing Monthly Payment Loan Other Community Seconds also eligible.

Down payment and Closing Cost Loans Comparison Sheet

Buyer's minimum investment Lesser of $1,000 or 1% of the purchase price if receiving a Minnesota Housing Monthly Payment Loan.

Refer to the Down payment and Closing Cost Loans Comparison Sheet.

Mortgage insurance Defer to underlying loan product guidelines (FHA, RD, VA, Conventional)

Minnesota Housing offers conventional loans that save borrowers money on mortgage insurance. • Conventional no-MI product:

Fannie Mae HFA Preferred Risk SharingTM:• Conventional reduced-MI products:

Fannie Mae HFA PreferredTM and Freddie Mac HFA Advantage℠

• Upfront Paid Mortgage Insurance: In exchange for a slightly higher interest rate, the lender pays the MIupfront, eliminating the need for monthly MI payments. Minimum credit score of 720 is recommended to access lower MI rates.

Closing costs Origination Fee Options: 1% fee or 0% fee, with a slightly higher interest rate. $175 Servicing Fee (one-time fee paid at closing) and $58 Tax Service Fee to U.S. Bank Home Mortgage-HFA Division.

Refer to the Lock, Fee and Service Release Premium (SRP) Guide.

Work history Defer to underlying loan product guidelines (FHA, RD, VA, Conventional)

Credit history Defer to underlying loan product guidelines (FHA, RD, VA, Conventional)Minimum of 640 Credit Score for Conventional. Minimum of 650 Credit Score for FHA. Refer to the Credit and DTI Matrix

Chapter 7 & 13 Defer to underlying loan product guidelines (FHA, RD, VA, Conventional) Liens, Foreclosure, Judgments Defer to underlying loan product guidelines (FHA, RD, VA, Conventional)

Collection accounts Defer to underlying loan product guidelines (FHA, RD, VA, Conventional)

Education requirements Homebuyer Education must be completed prior to closing if all borrowers are first-time homebuyers regardless of the product type or if they are getting a down payment and closing cost loan.

The Homebuyer Education requirement is satisfied when at least one borrower per household provides a certificate of completion from an approved course.

Amortization 15 or 30 years Defer to underlying loan product guidelines (FHA, RD, VA, Conventional)

Cash reserves Defer to underlying loan product guidelines (FHA, RD, VA, Conventional)

Purchase rehab option A purchase repair option (FHA 203(k) Streamlined) is available.Lenders must apply to Minnesota Housing’s Master Servicer in order to participate in this option. Contact Minnesota Housing for more details.

12 | P a g e Minnesota Homeownership Center

December 2020

Section 184 Indian Home Loan Guarantee Program Information Comments

Geographic area Entire State, On or Off Tribal Land. For participating Tribes. Download a List of Participating Tribes.

Verification of enrollment is required at application. For a list of approved lenders in Minnesota, visit hud.gov

Ratios Maximum 41% debt-to- income Debt-to-income ratio exceeding 41% may be acceptable if significant compensating factors are presented.

Maximum income No maximum income

Income not considered All income considered

Rental income Must be demonstrated by tax return, shown as income. Gross up non-taxable income None

Adjustment to gross income None

Maximum loan amount Cannot excess the lessor of: 150% of the current median home price, or FHA limit Loan limits at: hud.gov

First time homebuyer only No

Eligible properties Single family homes (1-4 units) and must be primary residence. Existing Home, Construction for New Home, Purchase and Rehab; including Current Home.

Refinance Can be used to refinance current loan. Borrower must pay the same loan guarantee fee as is required of new acquisitions. This fee is non-refundable.

Interest rate Market Rate, Not based on Credit Score or History.

Down payment 2.25% loans > $50,000; 1.25% loans <$50,000 Allows gifts, down payment assistance.

Buyer's minimum investment None

Mortgage insurance No. Onetime upfront fee, 1% of loan. GF is 1.5% and there is now a small premium. Per month Added. Its .25% off the loan amount and divided into 12 months. Very minimal and will drop off at 78% LTV.

Upfront fee can be financed into the loan.

Closing costs Seller can contribute max 6%.

Work history 6 months stable employment accepted if able to document 2 years of employment prior to absence from workforce. Gaps greater than 30 days must be explained.

Credit history No late payments in the past 12 months on all accounts Nontraditional credit accepted

Chapter 7 Two years from the date of discharge. No bankruptcy in the past 24 months.

Chapter 13 One year of good payment history; judge allows mortgage. No bankruptcy in the past 24 months. Same standard for Debt Management Plans.

Liens Federal liens must be current, paid or satisfied. No liens in the past 24 months.

Foreclosure 3 years since completion of foreclosure.

Judgments Paid in Full Prior to Closing No judgments in the past 24 months.

Collection accounts Paid in Full Prior to Closing No accounts converted to collection in the past 12 months. All collections must have been paid in full 12 months prior to the date of application.

Education requirements Not required; strongly encouraged Home Stretch and Framework are accepted.

Amortization 30 years If leasing tribal land a 50-year lease is required.

Cash reserves Not required

Purchase rehab option Used to rehab current home.

13 | P a g e Minnesota Homeownership Center

December 2020

Sunrise Banks Open Door Program (with ITIN option) Information Comments

Geographic area Twin Cities 7 County Metro Area

Ratios 45% Debt to Income OK to pay off debt to qualify

Maximum income No

Income not considered Cash Deposits

Rental income Must have 12 months of verifiable of rental history Does not include future projected income

Gross up non-taxable income Yes

Adjustment to gross income

Maximum loan amount $510,100

First time homebuyer only No

Eligible properties 1-4 Residential Properties Borrower(s) must live or intend to live in as primary residence

Refinance Yes

Interest rate 7% 80-90% LTV, 6.50% for 70-80%, 6.25% 60-70%, 6.00% for 60% and lower LTV Rates are subject to change

Down payment and/or closing cost assistance program

FHLB Home Start Income and other eligibility requirements

Buyer's minimum investment $2500.00 – remaining funds can be from other verifiable sources Credit score to qualify 670 or higher

Mortgage insurance None Required

Additional closing costs 1% origination fee, $995 processing fee and traditional third party costs

Work history Two Years verifiable employment or self employed

Credit history Minimum 1 traditional trade line with 12 month minimum credit history with NO 30 day late payments

1 Trade line must be at least 12 months, no late housing payments. 1 non-housing late in last 24 mos.

Chapter 7 None in the last 7 years

Chapter 13 None in the last 7 years

Liens No

Foreclosure None in the last 7 years

Judgments Must be released prior to closing

Collection accounts None in the last 24 months. If older than that no need to be paid off prior to closing

Education requirements Framework or Homestretch

Amortization 30 years

Cash reserves None

Purchase rehab option No

14 | P a g e Minnesota Homeownership Center

December 2020

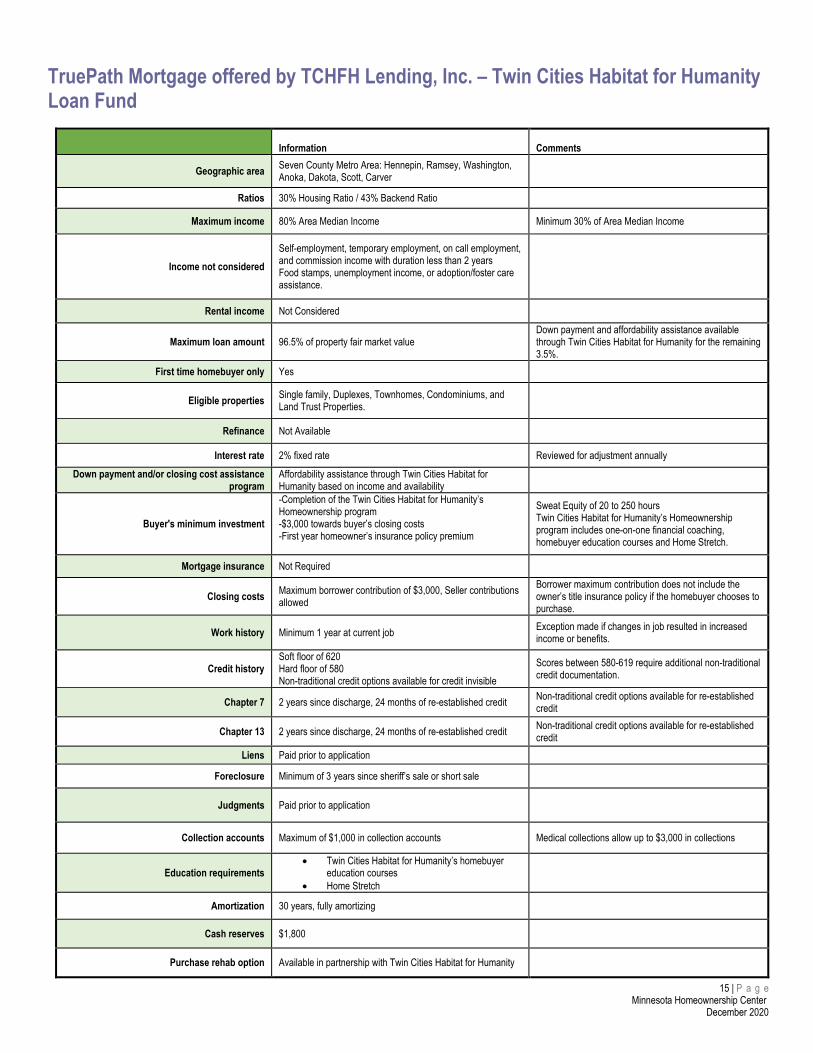

TruePath Mortgage offered by TCHFH Lending, Inc. – Twin Cities Habitat for Humanity Loan Fund

Information Comments

Geographic area Seven County Metro Area: Hennepin, Ramsey, Washington, Anoka, Dakota, Scott, Carver

Ratios 30% Housing Ratio / 43% Backend Ratio

Maximum income 80% Area Median Income Minimum 30% of Area Median Income

Income not considered Self-employment, temporary employment, on call employment, and commission income with duration less than 2 years Food stamps, unemployment income, or adoption/foster care assistance.

Rental income Not Considered

Maximum loan amount 96.5% of property fair market value Down payment and affordability assistance available through Twin Cities Habitat for Humanity for the remaining 3.5%.

First time homebuyer only Yes

Eligible properties Single family, Duplexes, Townhomes, Condominiums, and Land Trust Properties.

Refinance Not Available

Interest rate 2% fixed rate Reviewed for adjustment annually

Down payment and/or closing cost assistance program

Affordability assistance through Twin Cities Habitat for Humanity based on income and availability

Buyer's minimum investment

-Completion of the Twin Cities Habitat for Humanity’sHomeownership program -$3,000 towards buyer’s closing costs -First year homeowner’s insurance policy premium

Sweat Equity of 20 to 250 hours Twin Cities Habitat for Humanity’s Homeownership program includes one-on-one financial coaching, homebuyer education courses and Home Stretch.

Mortgage insurance Not Required

Closing costs Maximum borrower contribution of $3,000, Seller contributions allowed

Borrower maximum contribution does not include the owner’s title insurance policy if the homebuyer chooses to purchase.

Work history Minimum 1 year at current job Exception made if changes in job resulted in increased income or benefits.

Credit history Soft floor of 620 Hard floor of 580 Non-traditional credit options available for credit invisible

Scores between 580-619 require additional non-traditional credit documentation.

Chapter 7 2 years since discharge, 24 months of re-established credit Non-traditional credit options available for re-established credit

Chapter 13 2 years since discharge, 24 months of re-established credit Non-traditional credit options available for re-established credit

Liens Paid prior to application

Foreclosure Minimum of 3 years since sheriff’s sale or short sale

Judgments Paid prior to application

Collection accounts Maximum of $1,000 in collection accounts Medical collections allow up to $3,000 in collections

Education requirements • Twin Cities Habitat for Humanity’s homebuyer

education courses • Home Stretch

Amortization 30 years, fully amortizing

Cash reserves $1,800

Purchase rehab option Available in partnership with Twin Cities Habitat for Humanity

15 | P a g e Minnesota Homeownership Center

December 2020

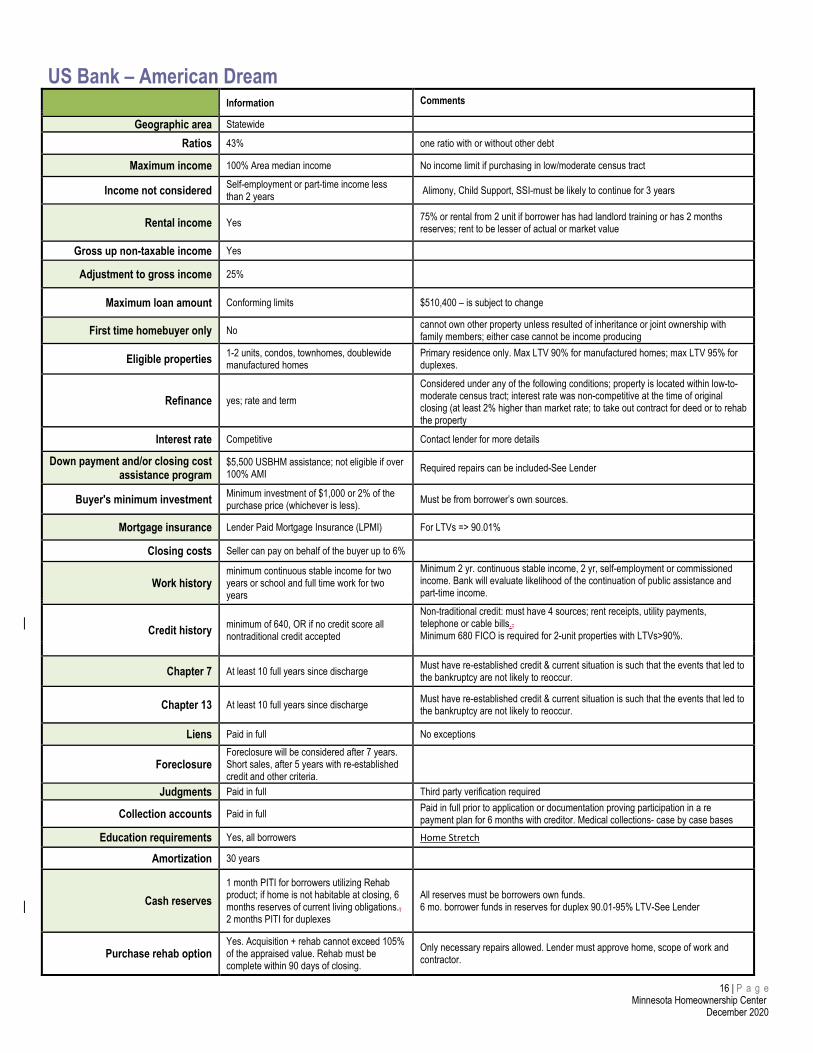

US Bank – American Dream Information Comments

Geographic area Statewide

Ratios 43% one ratio with or without other debt

Maximum income 100% Area median income No income limit if purchasing in low/moderate census tract

Income not considered Self-employment or part-time income less than 2 years Alimony, Child Support, SSI-must be likely to continue for 3 years

Rental income Yes 75% or rental from 2 unit if borrower has had landlord training or has 2 months reserves; rent to be lesser of actual or market value

Gross up non-taxable income Yes

Adjustment to gross income 25%

Maximum loan amount Conforming limits $510,400 – is subject to change

First time homebuyer only No cannot own other property unless resulted of inheritance or joint ownership with family members; either case cannot be income producing

Eligible properties 1-2 units, condos, townhomes, doublewide manufactured homes

Primary residence only. Max LTV 90% for manufactured homes; max LTV 95% for duplexes.

Refinance yes; rate and term Considered under any of the following conditions; property is located within low-to-moderate census tract; interest rate was non-competitive at the time of original closing (at least 2% higher than market rate; to take out contract for deed or to rehab the property

Interest rate Competitive Contact lender for more details

Down payment and/or closing cost assistance program

$5,500 USBHM assistance; not eligible if over 100% AMI Required repairs can be included-See Lender

Buyer's minimum investment Minimum investment of $1,000 or 2% of the purchase price (whichever is less). Must be from borrower’s own sources.

Mortgage insurance Lender Paid Mortgage Insurance (LPMI) For LTVs => 90.01%

Closing costs Seller can pay on behalf of the buyer up to 6%

Work history minimum continuous stable income for two years or school and full time work for two years

Minimum 2 yr. continuous stable income, 2 yr, self-employment or commissioned income. Bank will evaluate likelihood of the continuation of public assistance and part-time income.

Credit history minimum of 640, OR if no credit score all nontraditional credit accepted

Non-traditional credit: must have 4 sources; rent receipts, utility payments, telephone or cable bills., Minimum 680 FICO is required for 2-unit properties with LTVs>90%.

Chapter 7 At least 10 full years since discharge Must have re-established credit & current situation is such that the events that led to the bankruptcy are not likely to reoccur.

Chapter 13 At least 10 full years since discharge Must have re-established credit & current situation is such that the events that led to the bankruptcy are not likely to reoccur.

Liens Paid in full No exceptions

Foreclosure Foreclosure will be considered after 7 years. Short sales, after 5 years with re-established credit and other criteria.

Judgments Paid in full Third party verification required

Collection accounts Paid in full Paid in full prior to application or documentation proving participation in a re payment plan for 6 months with creditor. Medical collections- case by case bases

Education requirements Yes, all borrowers Home Stretch

Amortization 30 years

Cash reserves 1 month PITI for borrowers utilizing Rehab product; if home is not habitable at closing, 6 months reserves of current living obligations., 2 months PITI for duplexes

All reserves must be borrowers own funds. 6 mo. borrower funds in reserves for duplex 90.01-95% LTV-See Lender

Purchase rehab option Yes. Acquisition + rehab cannot exceed 105% of the appraised value. Rehab must be complete within 90 days of closing.

Only necessary repairs allowed. Lender must approve home, scope of work and contractor.

16 | P a g e Minnesota Homeownership Center

December 2020

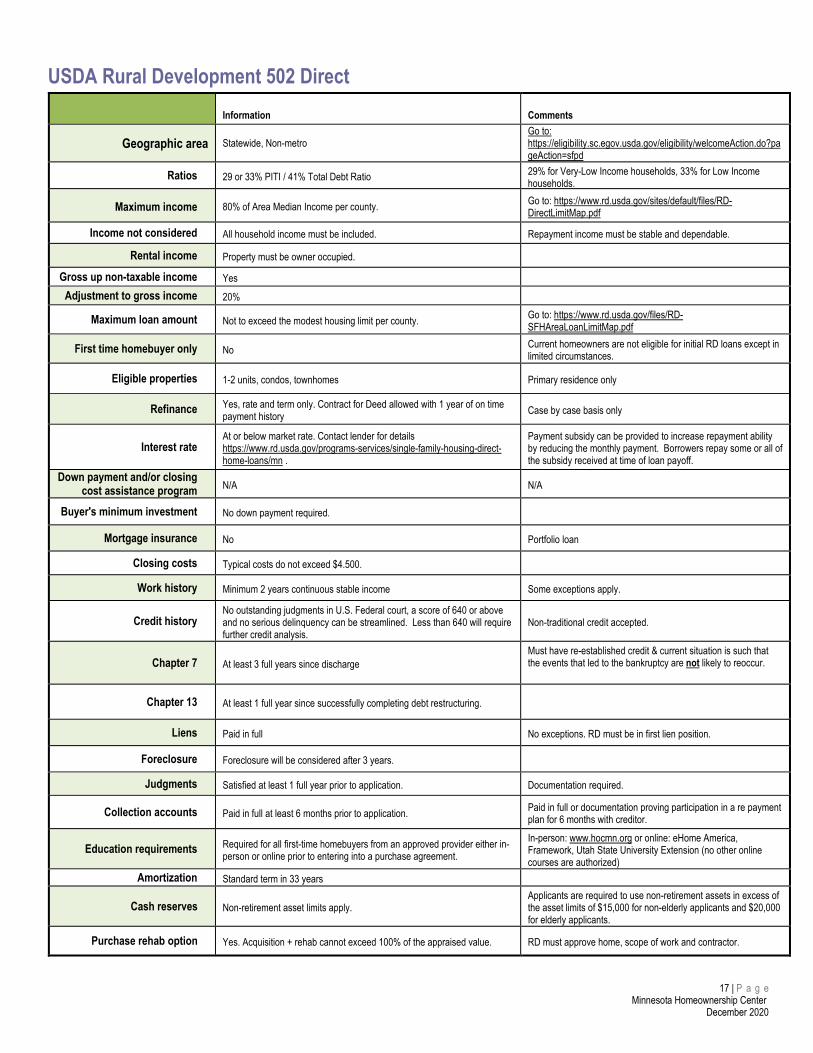

USDA Rural Development 502 Direct Information Comments

Geographic area Statewide, Non-metro Go to: https://eligibility.sc.egov.usda.gov/eligibility/welcomeAction.do?pageAction=sfpd

Ratios 29 or 33% PITI / 41% Total Debt Ratio 29% for Very-Low Income households, 33% for Low Income households.

Maximum income 80% of Area Median Income per county. Go to: https://www.rd.usda.gov/sites/default/files/RD-DirectLimitMap.pdf

Income not considered All household income must be included. Repayment income must be stable and dependable.

Rental income Property must be owner occupied.

Gross up non-taxable income Yes Adjustment to gross income 20%

Maximum loan amount Not to exceed the modest housing limit per county. Go to: https://www.rd.usda.gov/files/RD-SFHAreaLoanLimitMap.pdf

First time homebuyer only No Current homeowners are not eligible for initial RD loans except in limited circumstances.

Eligible properties 1-2 units, condos, townhomes Primary residence only

Refinance Yes, rate and term only. Contract for Deed allowed with 1 year of on time payment history Case by case basis only

Interest rate At or below market rate. Contact lender for details https://www.rd.usda.gov/programs-services/single-family-housing-direct-home-loans/mn .

Payment subsidy can be provided to increase repayment ability by reducing the monthly payment. Borrowers repay some or all of the subsidy received at time of loan payoff.

Down payment and/or closing cost assistance program N/A N/A

Buyer's minimum investment No down payment required.

Mortgage insurance No Portfolio loan

Closing costs Typical costs do not exceed $4.500.

Work history Minimum 2 years continuous stable income Some exceptions apply.

Credit history No outstanding judgments in U.S. Federal court, a score of 640 or above and no serious delinquency can be streamlined. Less than 640 will require further credit analysis.

Non-traditional credit accepted.

Chapter 7 At least 3 full years since discharge Must have re-established credit & current situation is such that the events that led to the bankruptcy are not likely to reoccur.

Chapter 13 At least 1 full year since successfully completing debt restructuring.

Liens Paid in full No exceptions. RD must be in first lien position.

Foreclosure Foreclosure will be considered after 3 years.

Judgments Satisfied at least 1 full year prior to application. Documentation required.

Collection accounts Paid in full at least 6 months prior to application. Paid in full or documentation proving participation in a re payment plan for 6 months with creditor.

Education requirements Required for all first-time homebuyers from an approved provider either in-person or online prior to entering into a purchase agreement.

In-person: www.hocmn.org or online: eHome America, Framework, Utah State University Extension (no other online courses are authorized)

Amortization Standard term in 33 years

Cash reserves Non-retirement asset limits apply. Applicants are required to use non-retirement assets in excess of the asset limits of $15,000 for non-elderly applicants and $20,000 for elderly applicants.

Purchase rehab option Yes. Acquisition + rehab cannot exceed 100% of the appraised value. RD must approve home, scope of work and contractor.

17 | P a g e Minnesota Homeownership Center

December 2020

USDA Rural Development 502 Guaranteed Loans Information Comments

Geographic area Statewide, Non-metro Go to: https://eligibility.sc.egov.usda.gov/eligibility/welcomeAction.do?pageAction=sfp

Ratios 29 / 41 Exceptions possible with underwriter approval and RD concurrence

Maximum income 115% of the median income for the area Go to: https://www.rd.usda.gov/files/RD-GRHLimitMap.pdf

Income not considered All income must be included for income limits

Rental income Property must be owner occupied

Gross up non-taxable income 15% to 25% Based on applicable tax rate. Check with investor

Adjustment to gross income $480 per dependent child plus child-care expenses. Elderly household deduction of $400, medical and disability expenses.

Maximum loan amount No maximum amount; loan is based on affordability ratios

First time homebuyer only No

Eligible properties Existing homes must meet HUD Handbooks 4000.1 https://www.hud.gov/program_offices/administration/hudclips/handbooks/hsgh

https://www.rd.usda.gov/sites/default/files/3555-1chapter12.pdf

Refinance Only on loans that are currently Guaranteed or Direct; upfront guarantee fee 2%, plus .5% annual fee

Interest rate May not exceed Fannie Mae 90-day + 6/10th and rounded up to the nearest 25%

Down payment and/or closing cost assistance program

100% of appraised value can be financed; zero down, closing costs can be financed if property value allows

Buyer's minimum investment No minimum Assets above the limits set by USDA must be used toward the home purchase, otherwise no down payment is required.

Mortgage insurance Annual fee of .5%

Closing costs 2% upfront guaranteed fee. Fee can be included in loan above the appraised value.

Work history Minimum 2 years continuous stable income

Credit history Nontraditional credit history accepted. 3 nontraditional credit sources required if no rental history; 2 required with current rent/housing history.

Chapter 7 At least 3 full years since discharge Mitigating circumstances are considered; waivers allowed

Chapter 13 At least 12 months since repayment plan was completed. Mitigating circumstances are considered; waivers allowed

Liens First lien required Soft seconds allowed for down payment/closing cost programs

Foreclosure 3 years from foreclosure sale

Judgments Paid in full or subordinated Mortgage requires first lien

Collection accounts Paid in full, unless FICO is 640+ and payment not required by lender No accounts turned to collection in last 12 months

Education requirements Homebuyer education not required, but recommended for first time buyers Discuss requirement with approved lender.

Amortization 30 years Cash reserves Not required

Purchase rehab option Not available

18 | P a g e Minnesota Homeownership Center

December 2020

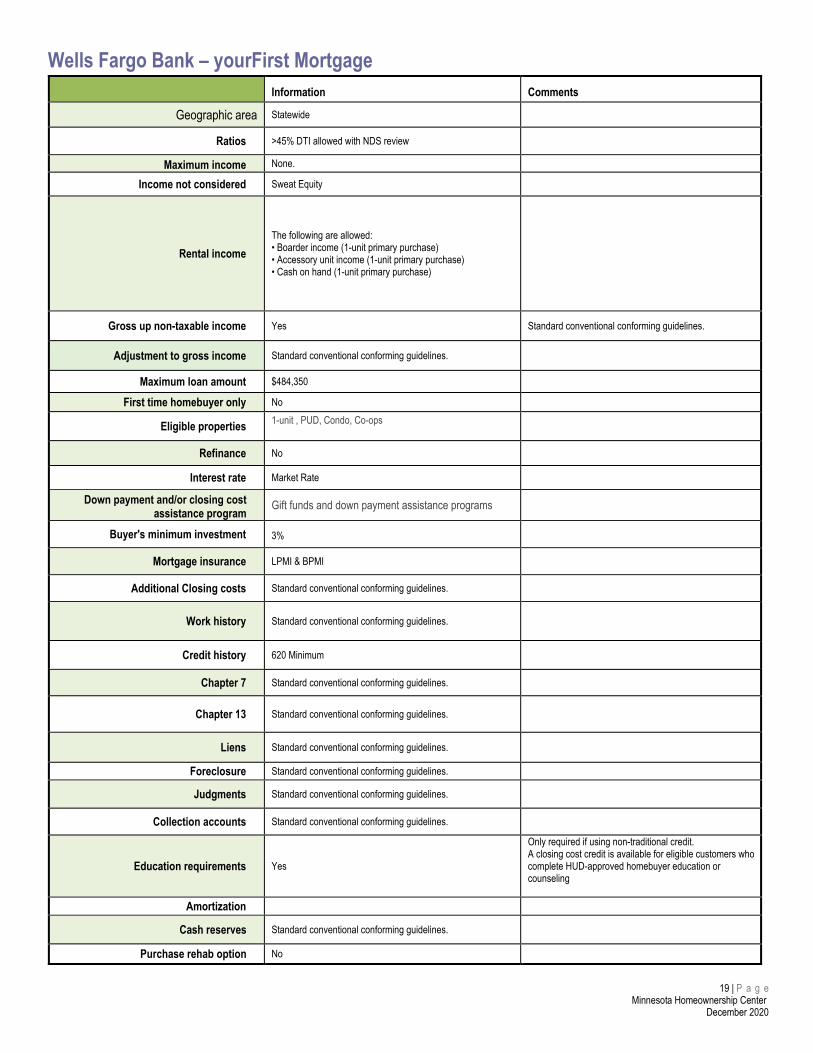

Wells Fargo Bank – yourFirst Mortgage Information Comments

Geographic area Statewide

Ratios >45% DTI allowed with NDS review

Maximum income None.

Income not considered Sweat Equity

Rental income The following are allowed: • Boarder income (1-unit primary purchase) • Accessory unit income (1-unit primary purchase) • Cash on hand (1-unit primary purchase)

Gross up non-taxable income Yes Standard conventional conforming guidelines.

Adjustment to gross income Standard conventional conforming guidelines.

Maximum loan amount $484,350

First time homebuyer only No

Eligible properties 1-unit , PUD, Condo, Co-ops

Refinance No

Interest rate Market Rate

Down payment and/or closing cost assistance program Gift funds and down payment assistance programs

Buyer's minimum investment 3%

Mortgage insurance LPMI & BPMI

Additional Closing costs Standard conventional conforming guidelines.

Work history Standard conventional conforming guidelines.

Credit history 620 Minimum

Chapter 7 Standard conventional conforming guidelines.

Chapter 13 Standard conventional conforming guidelines.

Liens Standard conventional conforming guidelines.

Foreclosure Standard conventional conforming guidelines.

Judgments Standard conventional conforming guidelines.

Collection accounts Standard conventional conforming guidelines.

Education requirements Yes

Only required if using non-traditional credit. A closing cost credit is available for eligible customers who complete HUD-approved homebuyer education or counseling

Amortization

Cash reserves Standard conventional conforming guidelines.

Purchase rehab option No

19 | P a g e Minnesota Homeownership Center

December 2020

Home - HOCMN

https://www.hocmn.org/[4/2/2021 2:14:50 PM]

Helping Minnesotans achievesustainable homeownership for more

than 25 years.

Click here to find a nonprofit homeownership advisor who can help you navigateyour situation for free →

Español Support Our Work Contact Us FORECLOSURE HELP

BUYING A HOME HOMEOWNERS PARTNER RESOURCES ABOUT US

WELCOME HOME BLOG

Want to learn how to

Home - HOCMN

https://www.hocmn.org/[4/2/2021 2:14:50 PM]

Get free help from nonprofit expertswhether you're just starting or ready

to close.

FIND A HOMEBUYER ADVISOR

Hear from lenders, real estate agents,and home inspectors about the home

buying process.

FIND HOMEBUYER WORKSHOPS

Connect with nonprofit experts that can help you keep your home.

FIND A FORCLOSURE ADVISOR

Tips for first time homebuyers and new homeowners.

SEE OUR LATEST POSTS

Need financial advice? buy a home?

Behind on mortgage?Looking for the latest

news and insights?

Home - HOCMN

https://www.hocmn.org/[4/2/2021 2:14:50 PM]

Featured Stories

The Paramount Importance of Equitable Access to Housing —Minnesota’s homeownership gap is one factor at the heart of theeconomic disparities keeping us stuck with an unfair and inequitablesystem.

BUYING A HOME

Center Releases Guide to Non-Interest-Bearing Financing in MinnesotaReport is a milestone in our continuing work to educate the real estate industry on emerging topics that have...

BUYING A HOME

Pandemic Crisis Media CoverageHere's a list of pandemic-related news articles that include comment from the Minnesota Homeownership Center.

BUYING A HOME

Homeownership in Minnesota: Quantifying the Need for Down Payment AssistanceMore than 100,000 renter households currently unable to afford to buy a home could do so with down payment...

MORE NEWS & INSIGHTS

The Minnesota Homeownership Center empowers smart homeownership choices through education, research andpartnerships grounded in the belief that sustainable homeownership has an essential role to play in fostering diverse,vibrant communities statewide.

Learn more about us >

Home - HOCMN

https://www.hocmn.org/[4/2/2021 2:14:50 PM]

Copyright © 2021 Minnesota Homeownership

Privacy Policy | Terms of Use

COMMON TOPICS

5 Myths, Mistakes and Misinformation about Homebuying

Home Stretch: An Insider’s Perspective

Home Repair Infographic – How Long Will It Last?

Spanish Loan Documents and Lender Resources

See All News & Insights >

CONNECT WITH US

Call today!We're here to help you.

In Minnesota: 651-659-9336 Toll Free: 866-462-6466