af5 exam preparation - personal finance society · af5 exam preparation page 2 of 36 ... knowledge...

TRANSCRIPT

Page 1 of 36 © Technical Connection 2013

www.4chartered.co.uk

Advanced Financial Planning

AF5 Financial Planning

Exam Preparation Guide

AF5 Exam Preparation

Page 2 of 36 © Technical Connection 2013

www.4chartered.co.uk

Contents

Introduction 3

To Access Your Free Techlink Professional Trial 4

October 2013 AF5 Case Study Analysis – PFS Rate 5

4th October 2013 AF5 Case Study Revision Day – PFS Rate 6

Section 1 7

A: Overview of the Exam 7

B: Study Materials 8

C: Analysing the Case Study 9

Section 2 11

D: Question Types 11

E: Fact-finding: Immediate and Long-term Financial Objectives 12

F: Risk Based Tasks 13

G: Recommendations 14

H: Review Questions 15

I: Non Standard Questions 16

Section 3 18

J: CII Written Exams 18

K: In the Examination 21

Appendices 22

Appendix 1: Case Study Summary Grid 22

Appendix 2: Summary of Objectives Tested 23

Appendix 3: Risk Based Tasks 28

Appendix 4: Risks and their Explanations 29

Appendix 5: Summary of Objectives Tested 30

Appendix 6: Review 34

Appendix 7: Example Technical note 35

AF5 Exam Preparation

Page 3 of 36 © Technical Connection 2013

www.4chartered.co.uk

Introduction

The purpose of this guide is to help you prepare for the October 2013 AF5 examination. It is divided into three sections:

Section 1 will give you an overview of the examination as a whole and then look at what you can expect from the case study you will be able to download from the CII website receive on or around 20 September 2013 (and which should have arrived by post on 23 September 2013). In particular it will focus on what you should do when the case study arrives.

Section 2 will look at the types of questions typically asked in an AF5 examination and includes some study aids for the most commonly asked questions.

Section 3 looks at the importance of good exam technique and shows you some examples of questions that would gain good marks and those that wouldn’t.

All AF5 candidates have free access to Techlink Professional to help you prepare for the exam this is an invaluable source of technical information and is an accredited CII CPD tool.

Finally, we will be producing our AF5 October 2013 case study analysis at least one week before your October exam. This is designed to help you to build up your technical knowledge based upon the October 2013 case study.

We trust that this guide helps you to prepare for your exam.

Good luck.

AF5 Exam Preparation

Page 4 of 36 © Technical Connection 2013

www.4chartered.co.uk

To Access Your Free Techlink Professional Trial

You can never have enough help that is why we are offering you a free trial of Techlink Professional Knowledge Management system during your revision period and as a PFS member you will receive a special subscription rate after the trial has ended.

This is an invaluable tool as you prepare for your Advanced financial planning exam.

Techlink Professional is all you need to

Keep up to date professionally and technically Research the answers you need to your technical questions Secure business generation ideas Carry out, automatically track , record and test CPD that is accredited by the

C.I.I.

Through our:

And, exclusively for subscribers to Techlink Professional, there is the increasingly popular (but optional and separately charged) “ASK” service, through which you can secure answers to your case and issue specific questions and challenges.

To access your free trial during you revision period

1. Call Clare Thomas or Derek Lovell on 020 7405 1600 or

2. Go to www.techlink.co.uk and click the Free Trial link at the right of the screen and then request which free trial you wish to have from the options shown.

AF5 Exam Preparation

Page 5 of 36 © Technical Connection 2013

www.4chartered.co.uk

October 2013 AF5 Case Study Analysis – Special PFS Member Rate

At least one week before your AF5 exam we will be publishing our AF5 case study analysis which is designed to help you to focus your revision and the key points. PFS members can purchase the analysis at a special rate of £60 plus VAT via www.4chartered.co.uk.

It includes an analysis of:

- Immediate and long-term financial needs

- Potential review questions

- Potential assumption questions

- Potential technical and miscellaneous questions

This is an invaluable tool as you prepare for your Advanced Financial Planning exam.

PFS members can purchase the analysis at a special rate of £60 plus VAT via www.4chartered.co.uk.

AF5 Exam Preparation

Page 6 of 36 © Technical Connection 2013

www.4chartered.co.uk

4th October 2013 AF5 Case Study Revision Day – Special PFS Member Rate

In Association with Technical Connection Ltd and sponsored by Brewin Dolphin Ltd we are pleased to offer an AF5 October 2013 Case Study analysis workshop. Looking specifically at the case study your exam will be based upon.

This session will be invaluable for those taking the AF5 exam on the 10th October 2013.

The day will combine both technical knowledge and exam technique with specific focus on the October 2013 case study.

By the end of the day you will have:

• covered the key case study areas • received a delegate pack which includes a mock exam • practised your skills and tested your knowledge

Previous course feedback

"I passed and no doubt thanks, in no small part, to your course. I found your course incredibly constructive and you guys pretty much perfectly anticipated the exam questions. So, a huge thank you - money well spent!!" Mark Malone, AWD

"Passed and delighted. Without the day I think I might have fallen short. The session made a real difference and I've told numerous other colleagues about how good it was." Tim Hutchence, Towry

PFS members can purchase the analysis at a special rate of £149 plus VAT via https://af504102013.eventbrite.co.uk/

Section 1 – Overview of the Exam

Page 7 of 36 © Technical Connection 2013

www.4chartered.co.uk

Section 1

A Overview of the exam

AF5 is the exam you must pass if you wish to achieve the CII’s ‘Chartered Financial Planner’ designation. It is a three hour, 160 mark exam designed to test delegates ability to offer holistic financial advice. As with all CII written papers, the nominal pass mark is around 55% which in this case means you will need to achieve at least 88 of the 160 marks to pass the exam, however, as the CII moderate their pass marks, it is wiser to aim for around 60% (i.e. 96 marks) to be sure of achieving a passing grade.

The exam questions (in AF5 they are called ‘tasks’) are all based on one case study which you can download from the CII website and which they also send to you as a hardcopy in the post. Recently, the case study has been posted on a Friday morning, giving you nearly three weeks to prepare for the exam itself. This case study is presented in the form of a fact find and attempts, as much as is possible within an examination format, to mirror the complexities and variety of financial planning needs advisors can encounter in their day to day lives. The April 2013 fact find ran to ten pages and you should not underestimate the time required to read and thoroughly absorb the information contained within it.

As you would imagine, the case study can cover any areas of financial planning and in the past has covered all the general financial planning areas of tax planning, pension build up, pensions in payment, investments, business planning and trusts. As with RO6, an area which has been tested in every exam so far is that of protection and this, along with some other key areas, will be looked at in greater detail in Section 2 of this guide.

In addition to the general planning areas, the exam will usually present you with a more unusual planning area. For example, in the April 2011 exam the case study included a child who had suffered brain damage at birth and was, as a result, severely disabled. This is an area that many advisors sitting the exam had little or no knowledge in and therefore required some research before the examination and then an ability to apply the knowledge gained to the tasks in the exam itself.

The case study you receive through the post and/ or download cannot be taken into the exam. A new copy will be issued in the exam room and whilst this will be identical in all aspects to the case study you have already seen, you will also receive a summary of the clients short and long term financial aims. These will then form the basis of the questions that are asked, however, they should have been apparent from the information provided in the case study and should only come as a surprise to a poorly prepared candidate.

The CII will send you a hard copy of the case study however it is also available to download from the CII website.

Section 1 – Study Materials

Page 8 of 36 © Technical Connection 2013

www.4chartered.co.uk

B Study Materials

As with all the AF level exams AF5 does not have a study text, however, unlike the other AF exams, it does not have a case study book either. This is because the exam is testing the knowledge candidates have gained from sitting (and passing) the technical RO, JO and AF exams. Therefore, the only materials available to candidates to prepare for this exam are the past examination papers published by the CII, material supplied by third parties (such as this guide) and any study days attended prior to the exam sitting.

As with any examination, the past papers provide the best possible means for you to understand the type of questions asked and also the answers the examiners are looking for. You should ensure you spend time studying these and you will maximise the benefit if you attempt at least one (and preferably more) past paper as a ‘mock exam’ and write your answers down before checking them against the model answers in the examination guide. This is time consuming and can seem a little daunting – it is also intensely frustrating if your answers don’t seem to match those shown in the study guides - but it is only by understanding where you are going wrong that you can adapt your answers to the style and content required to gain the marks needed to pass the exam. This is something you cannot learn by simply reading through the examination guides.

There are many other sources of help available. Once you have reviewed the case study and have established the technical areas likely to be tested you can determine the additional material needed to support your existing knowledge levels. This could be provided, for example, through your employer’s technical team, making use of the course books of RO2, RO3, RO4 and RO5 and JO2, JO3 and JO5, material provided by product providers either in hard copy form or via their websites and the Revenue websites for tax, trusts, pensions etc.

In using all of these sources you should bear in mind what you have learned from your study of the past papers in terms of the depth of knowledge typically tested in an AF5 examination and how it must be applied to the circumstances outlined in the case study. Having an extensive knowledge of a subject is never a bad thing however if you cannot communicate this in a manner that will allow the examiner to give you the marks available you could still fail. We will look at exam technique in greater detail in Section 3.

The AF5 Examination Guides are available on the CII website. The two most recent should be available as part of your entry to the exam but otherwise can be purchased from the AF5 ‘courseware’ section. Previous papers (going back as far as 2007) can be found on the Knowledge Services section of the website and are free to download.

Section 1 – Analysing the Case Study

Page 9 of 36 © Technical Connection 2013

www.4chartered.co.uk

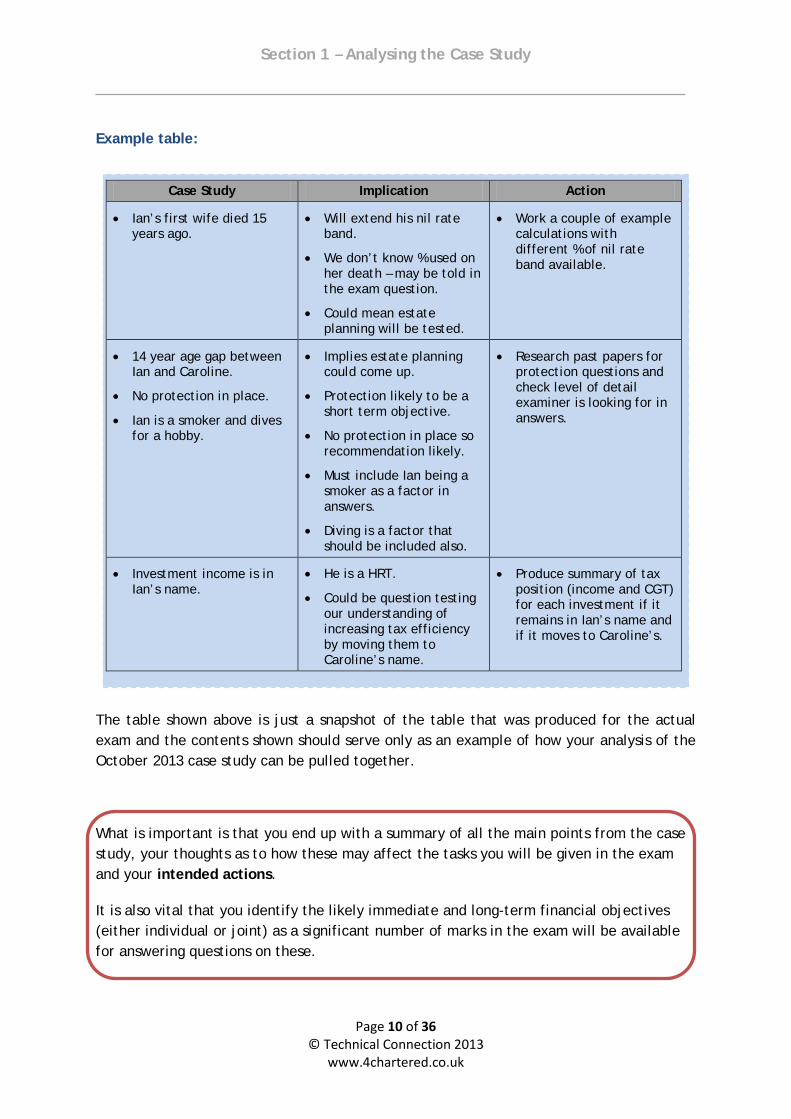

C Analysing the Case Study

As you know the case study is presented in the form of a fact find. This is a lengthy document and is designed to closely resemble the type of fact find commonly used by advisers. The fact find for the April 2013 exam ran to ten pages and contained fifteen sections of information for the candidates to consider. You should read and re-read this document multiple times in the weeks leading up to the exam.

What follows is a suggested process for the initial phase of developing your knowledge and understanding of the information contained within the fact find. You should try to set aside a couple of hours for this.

Organising your notes can be done in a variety of ways but one way that works is to capture the information in a table. You should use the facts you noted down in Step 2 and start to expand these and possibly group them together where you believe the facts are interlinked. An example using the October 2010 exam case study is shown on the next page and a blank grid for you to use is included as Appendix 1.

STEP ONE

You need a good overall understanding of the circumstances of the case study so you should start by reading the whole fact find from start to finish without stopping - not even to take notes!

STEP TWO

Read it again and note down the bits that stand out to you, e.g. they are married with children but don't have Wills. Don't worry about drawing conclusions or linking pieces of information together at this stage.

STEP THREE

You will be starting to identify the short and long term need areas and be developing some ideas for the tasks you may be set in the exam. So now you need to organise your notes!

Section 1 – Analysing the Case Study

Page 10 of 36 © Technical Connection 2013

www.4chartered.co.uk

Case Study Implication Action

• Ian’s first wife died 15 years ago.

• Will extend his nil rate band.

• We don’t know % used on her death – may be told in the exam question.

• Could mean estate planning will be tested.

• Work a couple of example calculations with different % of nil rate band available.

• 14 year age gap between Ian and Caroline.

• No protection in place.

• Ian is a smoker and dives for a hobby.

• Implies estate planning could come up.

• Protection likely to be a short term objective.

• No protection in place so recommendation likely.

• Must include Ian being a smoker as a factor in answers.

• Diving is a factor that should be included also.

• Research past papers for protection questions and check level of detail examiner is looking for in answers.

• Investment income is in Ian’s name.

• He is a HRT.

• Could be question testing our understanding of increasing tax efficiency by moving them to Caroline’s name.

• Produce summary of tax position (income and CGT) for each investment if it remains in Ian’s name and if it moves to Caroline’s.

Example table:

The table shown above is just a snapshot of the table that was produced for the actual exam and the contents shown should serve only as an example of how your analysis of the October 2013 case study can be pulled together.

What is important is that you end up with a summary of all the main points from the case study, your thoughts as to how these may affect the tasks you will be given in the exam and your intended actions.

It is also vital that you identify the likely immediate and long-term financial objectives (either individual or joint) as a significant number of marks in the exam will be available for answering questions on these.

Section 2 – Question Types

Page 11 of 36 © Technical Connection 2013

www.4chartered.co.uk

Section 2

D Question Types

We will now look at the different types of questions (tasks) set in an AF5 exam. Some tasks appear on every paper using almost identical wording each time (e.g. fact-finding, recommendations and risk) whereas others are tested frequently but do not occur in the same form at each sitting (e.g. the ‘review’ task).

Of course many of the questions will change from exam to exam to suit the different circumstances outlined in the case study and to a certain extent the whim of the examiner. Where a major change in legislation has occurred, such as the changes in the pension’s rules at the start of the 2011/12 tax year, the examiner may prefer to avoid asking questions on this area (particularly if the change in rules happens just prior to the exam sitting) or they may choose to target it (where the rules have been in place for a while).

Throughout this section you will be encouraged to make use of past papers to help you understand what must be included in your answers in order for the examiner to be able to award you the marks available. The importance of spending time looking at the past papers cannot be over emphasized as this is the only way you can develop the exam technique required. We will look at exam technique in greater detail in Section 3.

Section 2 – Fact-finding: Immediate and Long Term Financial Objectives

Page 12 of 36 © Technical Connection 2013

www.4chartered.co.uk

E Fact-finding: Immediate and Long-term Financial Objectives

This task, which has been examined as Task 1 in every AF5 exam so far, with the exception of the October 2012 exam where it was examined as Task 2 (a question on fees was set as Task 1). The Task on the immediate and long-term financial objectives is divided into parts (a) and (b). In part (a) you will be asked to identify the additional information you would need in order to advise the clients on meeting their immediate objectives and part (b) will ask you to identify the additional information you would need to advise them about their longer-term objectives.

You will be given a note of the clients immediate and longer-term objectives in the examination (it is the only additional piece of information you will be given) and you should base your answers on this information. None of these objectives should come as a surprise to you if you have spent sufficient time analysing the case study prior to the exam and have spent time determining the likely objectives.

Some objectives, such as protection, are tested in every exam sitting; others such as increasing disposable income and planning for retirement have been tested frequently. As a result you will have a selection of model answers available which cover the likely objectives for the October 2013 case study. Using these and applying the information from the case study will put you in the best possible position to gain good marks on this task.

There is, of course, always the chance of an objective coming up that has not been tested previously, however, if you have spent enough time looking at this task and how it has been examined in previous papers you should still be a position to gain good marks

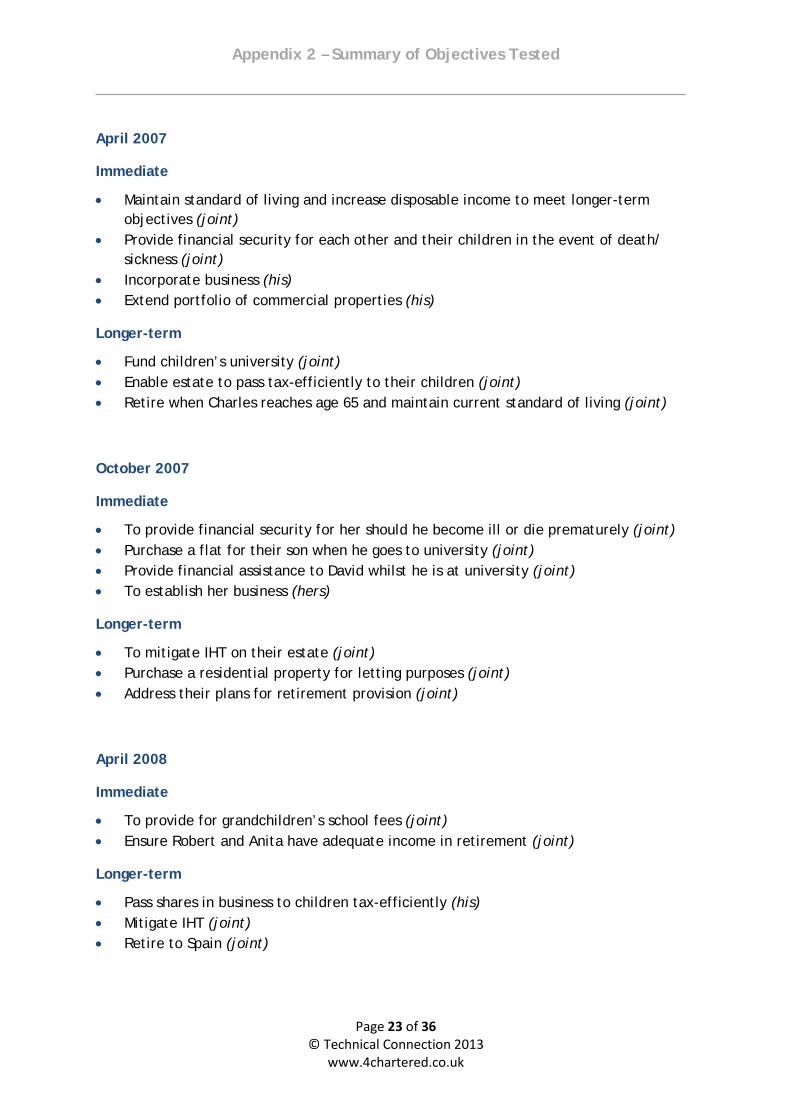

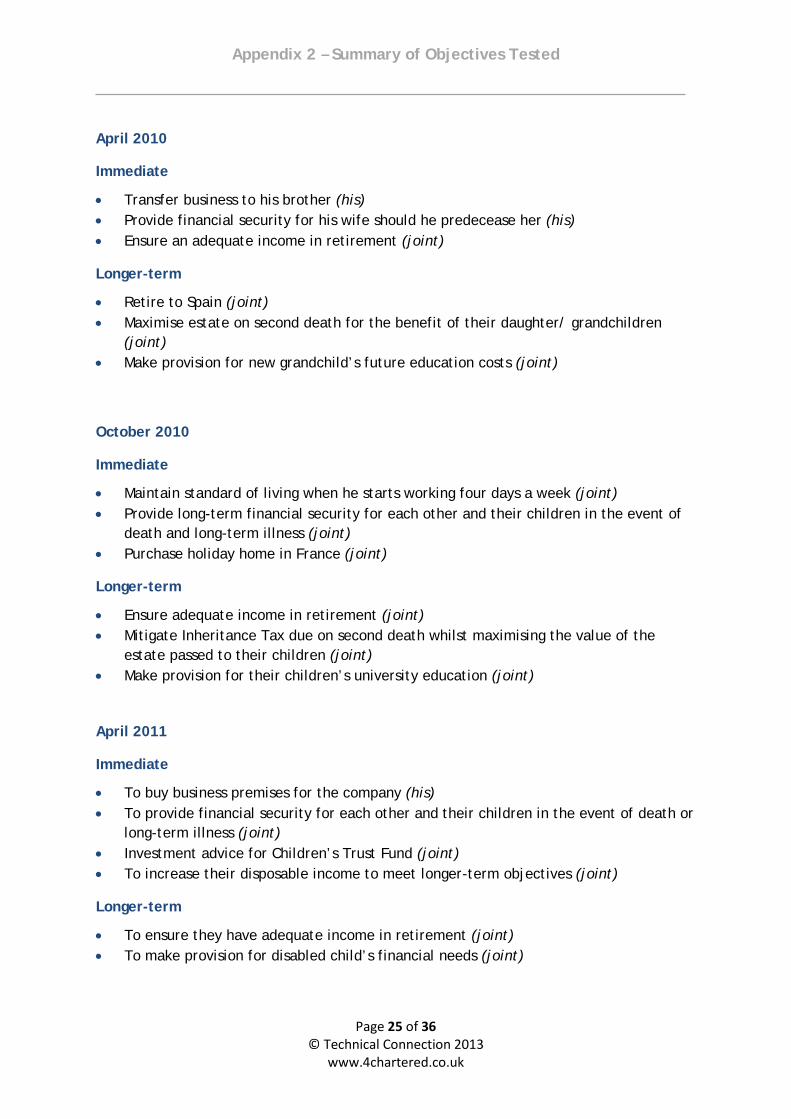

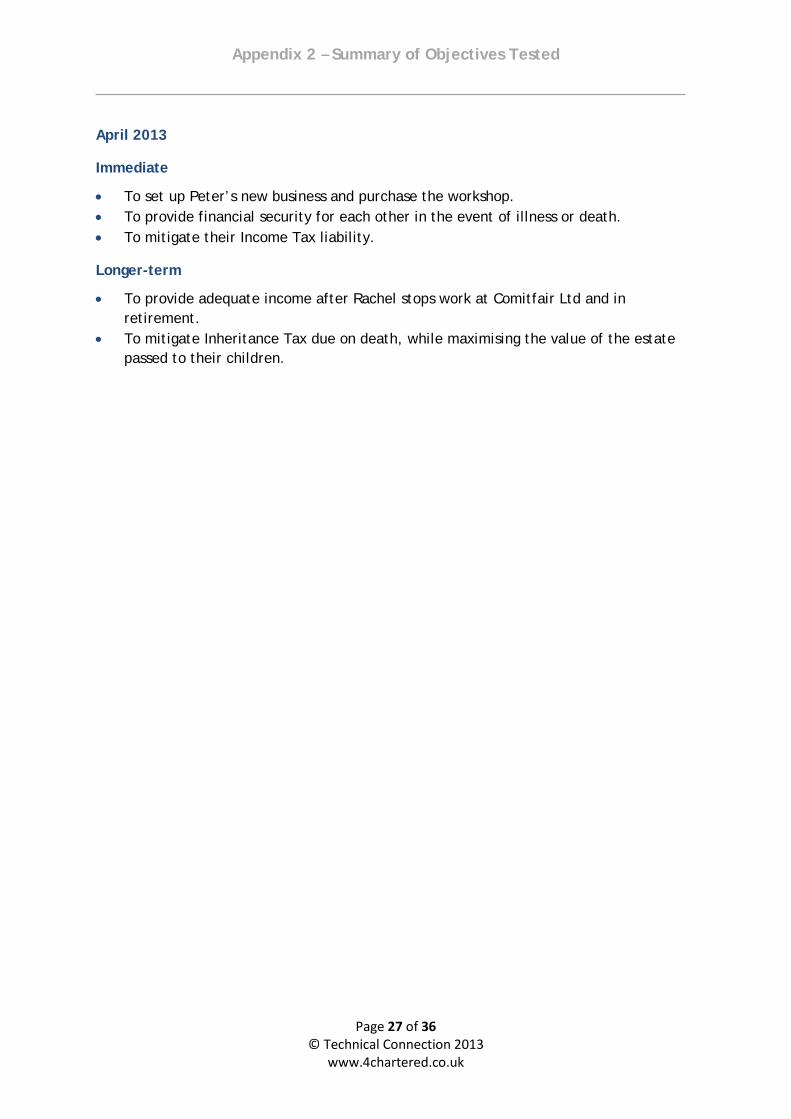

To help you find the appropriate model answers to use in your preparation, a summary of all the immediate and long-term objectives tested previously as part of Task 1 are shown in Appendix 2.

The number of marks available for Task 1 varies from exam to exam but averages around 12 marks for part (a) and 12 for part (b). Assuming you are aiming for 96 marks in total (see Section 1A) this question alone is 25% of the marks you are looking for.

Section 2 – Risk Based Tasks

Page 13 of 36 © Technical Connection 2013

www.4chartered.co.uk

F Risk Based Tasks

A task on ‘risk’ has been included in every AF5 exam so far. Typically it will form part or all of Task 2 or Task 3 however, unlike the fact-finding task, the format of this question has evolved over the life of the exam.

For example, in the early years the task was usually to identify and describe the types of risk the client may be exposed to whereas in the more recent exams the task has asked candidates to detail the risk faced by the client(s) in one particular aspect of their finances. In October 2011 candidates were asked to identify the risks associated with the client’s ISAs and their proposed ownership of a flat and in April 2011 it was about the risk faced by the client in respect of his shareholding in a private limited company. Most recently in April 2013 candidates were asked to comment on the key risks associated with the client’s holding of private listed shares.

The marks available for this task tend to vary somewhat. In April 2007 the task was worth 23 marks, in October 2009 21 marks were available and most recently in October 2012 18 marks were up for grabs. At the other end of the scale in April 2011 and most recently in April 2013 only 6 marks were available.

These are relatively straightforward marks to get if you spend some time looking through the risk questions on the previous papers and make sure you take into account the circumstances outlined in the case study.

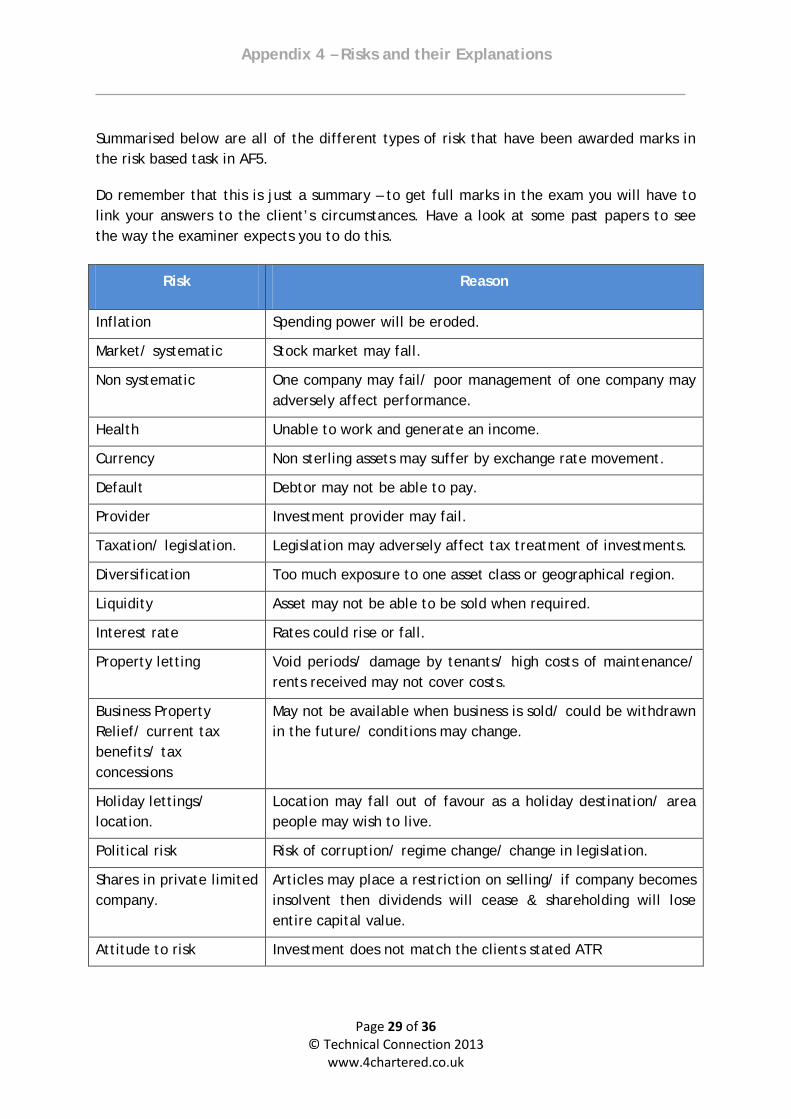

To help you find the appropriate model answers to use in your preparation, a summary of all the risk based tasks are shown in Appendix 3.

In addition a table setting out all the different types of risk that have been examined in AF5, with an explanation, is shown in Appendix 4.

Section 2 – Recommendations

Page 14 of 36 © Technical Connection 2013

www.4chartered.co.uk

G Recommendations

You will not be surprised to know that you will always be set the task of recommending a course of action based on the client’s objectives. Typically there will be one task asking you to recommend actions around one or more of the short-term objectives and then a second task asking you to do the same with regard to one or more of the client’s long term objectives. In addition, a recommendation could form part of another question where the examiner has asked you a more technical question regarding some aspect of the client’s finances.

As with the fact-finding task, this is a question you can prepare for ahead of the exam. Whilst you will not know precisely which of the objectives you will be asked about and how the question will be phrased, you will have identified the main need areas from your analysis of the case study. Using these you will be able to use the past exam papers to see how these areas have been tested in the past and therefore the sort of information the examiner is expecting to see in your answer.

The recommendation tasks are a vital part of the paper as typically they are worth between 43 – 68 marks.

A task asking you to make a recommendation regarding

protection has appeared on every paper with the exception of

October 2008 and April 2012 (in both cases the couple were already retired!) Other objectives that get

tested on most papers are retirement planning and estate

planning.

The way in which objectives are stated will vary from case study to case study but in Appendix 5 we have used the most common objectives and shown you which papers they appeared on, the task number and the marks that were available.

Section 2 – Review Question

Page 15 of 36 © Technical Connection 2013

www.4chartered.co.uk

H Review Question

The final task in AF5 has required candidates to identify a certain number of key events that may trigger a review or list a number of areas that should be addressed with the client at their next review. On occasions the question has asked them to do both. In some exam sittings either the ‘key events’ or the ‘areas’ question has been asked along with a more specific question – for example, in October 2011 the first part of the task asked for six key events that would trigger a review and the second part asked for four key pieces of information required when monitoring the client’s pension.

As with all AF5 questions the events/ areas included in your answer should be specific to the client and their circumstances.

The marks awarded for this question have been as low as 6 and as high as 12. This is another question you can be well prepared for prior to the actual exam as there are certain answers that tend to re-occur!

To help you out we have produced a list of the key events that trigger a review and the questions that should be addressed with a client at their next review. These are shown in Appendix 6.

Section 2 – Non Standard Questions

Page 16 of 36 © Technical Connection 2013

www.4chartered.co.uk

I Non Standard Questions

The remaining tasks in AF5 will be based on the circumstances of the case study and for that reason there is little we can do ahead of the case study being published to prepare for them.

The following are some examples of the variety of areas covered:

• Purchase of a flat in the mothers name for her son to use at university.

• Comment on the diversification of an investment portfolio.

• Explain CGT and IHT consequences of client’s actions.

• The impact a client’s death would have on the income and capital of the surviving spouse.

• Benefits of setting up a limited company.

• Use of a SSAS/ SIPP to purchase a business property.

• Comment on the present protection products and identify any weaknesses.

• Maintain current standard of living and continue to fund children’s education.

• Purchase a holiday home abroad.

• Methods and benefits of using a SIPP to purchase gold.

• List the principle duties of trustees.

• Suitable and tax-efficient investment portfolio within a trust fund.

Once the case study has been published and you have identified the client’s needs/ objectives you should spend some time reviewing the past papers for examples of similar questions (unless it is a totally new area) as these will be helpful in developing an understanding of the points the examiner is likely to be looking for in your answers.

As an example, for the October 2010 exam it was clear that the couple wished to provide for their children’s university costs. A review of the past papers showed that the following questions would be useful to study:

• April 2007: Task 1(b) & task 6(a)

• October 2007: Task 1(a) & task 4(c)

• April 2009: Task 1(b)

• October 2009: Task 1(a)

• April 2010: Task 1(b)

Section 2 – Non Standard Questions

Page 17 of 36 © Technical Connection 2013

www.4chartered.co.uk

You should undertake a similar exercise once you have completed your case study summary grid (Section 1C & Appendix 1).

AF5 can cover some unusual/ specialist areas and as a result there is likely to be some aspects of the case study that you may not come across in your day to day work. For example, drawdown pensions have been examined in the past but not every advisor deals with at retirement business.

As a result you may need to do some additional research in these areas and produce a ‘technical note’ to help you in your exam preparation. Even for areas that you are comfortable in there is no harm in producing a summary sheet of the technical information you feel is relevant to act as a revision aid.

An example of a ‘technical note’ produced for the October 2010 exam can be found in Appendix 7

Section 3 – CII Written Examinations

Page 18 of 36 © Technical Connection 2013

www.4chartered.co.uk

Section 3

J CII Written Examinations

This section is all about exam technique and we will start by considering how the CII award marks in a written exam.

The first thing to realise is that marks will be awarded on an objective basis – i.e. for factual information and reasoned arguments. For example, in the October 2011 exam candidates were asked to ‘comment on’ the client’s current protection arrangements and identify any weaknesses should either client suffer a long term illness.

The verb ‘comment’ inspires in many candidates a desire to ramble and wander off the topic. For example, someone may have written:

None of this is wrong but equally it isn’t very specific. Words like ‘probably’ should be avoided because they suggest you aren’t sure. Equally, telling the examiner that the arrangements ‘should be improved’ is fine but you won’t get the mark – what you need to do is provide evidence for this using the information from the case study. So a better way of saying the above would be:

Hopefully you can see the difference between the two answers. A point worth repeating is that you should always use the information in the case study when answering the questions (i.e. repeat back information to the examiner) – you will gain a lot of marks that way.

The next point to make is that the CII ‘positively’ mark. What this means is you can’t have marks taken away for a wrong answer and if you include a correct point in an otherwise poor answer you will get a mark for the correctly stated point. Therefore there is no point leaving any task unanswered, even if you don’t think you know the answer. In these cases it is better to make an educated guess and write something down as you at least stand a chance of getting a mark (or even two!) Who knows, it might be the difference between a pass and a narrow fail!

‘there would be an income shortfall if one or both fell ill as neither has long-term PHI cover on their earnings or any critical illness benefits.’

‘their arrangements are inadequate and should really be improved as currently there probably wouldn’t be enough income if one of them fell ill’.

Section 3 – CII Written Examinations

Page 19 of 36 © Technical Connection 2013

www.4chartered.co.uk

The CII use ‘method’ marking for calculations. This is a form of positive marking and works by giving you marks for the method you use in performing the calculation rather than for getting the correct answer.

If you go wrong in your calculation, rather than stop awarding you marks, the examiner will not award the mark for the step you got wrong but will continue to award marks for the remainder of the calculation provided the steps you perform are the correct ones (even if it is with the wrong figures). Provided you make no further mistakes you should end up with all but one or two of the marks available for the calculation even though your answer will be incorrect!

Of course this only works if you show the examiner every step of the calculation. A good principle to follow is to write down on the page every step you perform on a calculator as this ensures that all steps involved in the calculation are shown in your answer.

You have probably heard the phrase ‘always state the obvious’ – well the principle applies even in an advanced level exam. The reason it works is because the examiner doesn’t know who you are, what you know and your thought processes. They only know what you have written on the page. They can’t interpret or ‘guess’ what you mean – they have to take your words at face value. For that reason you don’t want to leave too many ‘gaps’ in the information you provide. Instead you should show the basis for each statement you make, i.e. when talking about the death benefits payable under a term assurance that is not in trust many candidates would simply write:

This is correct and is likely to gain a mark, however if you have been asked to explain or describe then there is probably another mark available for stating:

It seems ‘obvious’ and it is but it gets you a mark and shows the examiner that you can take a fact (the term assurance is not in trust) and explain or describe why this is a problem (because it will be paid into his estate on death). This is a simplified example but hopefully makes the point that stating the obvious gets you marks.

‘would be payable to the estate on his death’

‘his term assurance is not in trust and will therefore be paid into his estate on death’

Section 3 – CII Written Examinations

Page 20 of 36 © Technical Connection 2013

www.4chartered.co.uk

It also brings us neatly to the next point: that of the verb or verbs used in the wording of the task. Typical verbs used are describe, explain, identify, detail, justify, recommend, list and state. There is also an increasing use of the instruction ‘comment on’. The verbs used in a task instruction are carefully chosen and you should therefore pay close attention to them. In particular you should:

• Note when two verbs are used, for example, detail and justify; identify and describe. In these cases you must make sure you perform both parts of the task (i.e. detail the recommendation you would make and then justify why you have made it).

• Pay attention to the verb used and the number of marks awarded. If you are asked to ‘list’ the principle duties of a trustee and there are six marks available you should list at least 6 duties. Remember that positive marking applies – this means you can provide a list of 20 ‘duties’ and the whole list will be marked and if six are correct you will get six marks.

• Spend time looking at the verbs used in previous questions and the level of detail required in the answer to gain full marks.

Finally – this is not an English exam. You won’t lose marks for poor spelling, punctuation or grammar. You don’t even have to write in proper sentences as bullet point answers are acceptable (and encouraged). Reasons for writing your answers in bullet point form include:

• It is easier to keep track of how many points you have made and you will be trying to make one substantive point for each mark available.

• It is easier to review your answers.

• It takes up less time and therefore removes some of the time pressure.

Section 3 – In the Examination

Page 21 of 36 © Technical Connection 2013

www.4chartered.co.uk

K In the Examination

Finally, some points to remember on the day itself:

• Make sure you take your exam entry permit and ID with you. Check you know where the exam centre is and how to get there and leave yourself plenty of time.

• Take a few pens (black or blue – not red and don’t write in pencil), a highlighter pen and a calculator.

• You can’t take your copy of the case study in – they will give you a new one.

• Don’t start to write before they tell you that you can – you’ll be disqualified.

• You have 160 marks in 180 minutes so aim for 1 minute per 1 mark (so a question worth eight marks should take no longer than eight minutes). This will give you 20 minutes over.

• Take five minutes at the start to read through the objectives and the tasks. This leaves 15 minutes at the end to review your answers and add any extra points you would like to make.

• KEEP AN EYE ON THE TIME!

• You can answer the questions in any order you like and it is always best to start with one you are comfortable with.

• Bullet point your answers and don’t leave any question unanswered (even if you have to guess).

• If in doubt write it down. It is a positively marked exam and you can’t lose a mark unless you have contradicted yourself – i.e. you have said at the start of your answer an investment is paid gross and later in the same answer you state it is paid net of basic rate tax. This is a contradiction and you will not be awarded the mark.

• Try to write legibly. Examiners are pretty good at interpreting poor handwriting but you can help them out by dotting i’s, crossing t’s, making sure your g’s have a tail and your h’s don’t look like n’s!

• Above all: stay calm, make sure you are answering the question that was asked, state the obvious and repeat back information from the case study whenever relevant!

GOOD LUCK!!!

Appendix 1 – Case Study Summary Grid

Page 22 of 36 © Technical Connection 2013

www.4chartered.co.uk

Case Study Implication(s) Action(s)

Appendix 2 – Summary of Objectives Tested

Page 23 of 36 © Technical Connection 2013

www.4chartered.co.uk

April 2007

Immediate

• Maintain standard of living and increase disposable income to meet longer-term objectives (joint)

• Provide financial security for each other and their children in the event of death/ sickness (joint)

• Incorporate business (his) • Extend portfolio of commercial properties (his)

Longer-term

• Fund children’s university (joint) • Enable estate to pass tax-efficiently to their children (joint) • Retire when Charles reaches age 65 and maintain current standard of living (joint)

October 2007

Immediate

• To provide financial security for her should he become ill or die prematurely (joint) • Purchase a flat for their son when he goes to university (joint) • Provide financial assistance to David whilst he is at university (joint) • To establish her business (hers)

Longer-term

• To mitigate IHT on their estate (joint) • Purchase a residential property for letting purposes (joint) • Address their plans for retirement provision (joint)

April 2008

Immediate

• To provide for grandchildren’s school fees (joint) • Ensure Robert and Anita have adequate income in retirement (joint)

Longer-term

• Pass shares in business to children tax-efficiently (his) • Mitigate IHT (joint) • Retire to Spain (joint)

Appendix 2 – Summary of Objectives Tested

Page 24 of 36 © Technical Connection 2013

www.4chartered.co.uk

October 2008

Immediate

• Make a gift of £100,000 to their son to help with a property purchase (joint) • Generate additional income now that she has retired (joint) • Improve IT and CGT position (joint)

Longer-term

• Ensure she has sufficient income should he die (joint) • Mitigate potential IHT on their estate (joint)

April 2009

Immediate

• Increase disposable income to meet longer-term objectives (joint) • Provide financial security for each other and children in the event of death/ sickness

(joint) • Incorporate company (joint)

Longer-term

• Fund children’s private education (joint) • Enable the estate to pass tax-efficiently to children (joint) • Retire at 60 (joint)

October 2009

Immediate

• Set up her new business (hers) • Maintain current standard of living and fund children’s school fees and university costs

(joint) • Provide financial security for each other and children in the event of death/ sickness

(joint)

Longer-term

• Continue to secure her own source of income in retirement (hers) • Mitigate IHT on their estate (joint)

Appendix 2 – Summary of Objectives Tested

Page 25 of 36 © Technical Connection 2013

www.4chartered.co.uk

April 2010

Immediate

• Transfer business to his brother (his) • Provide financial security for his wife should he predecease her (his) • Ensure an adequate income in retirement (joint)

Longer-term

• Retire to Spain (joint) • Maximise estate on second death for the benefit of their daughter/ grandchildren

(joint) • Make provision for new grandchild’s future education costs (joint)

October 2010

Immediate

• Maintain standard of living when he starts working four days a week (joint) • Provide long-term financial security for each other and their children in the event of

death and long-term illness (joint) • Purchase holiday home in France (joint)

Longer-term

• Ensure adequate income in retirement (joint) • Mitigate Inheritance Tax due on second death whilst maximising the value of the

estate passed to their children (joint) • Make provision for their children’s university education (joint)

April 2011

Immediate

• To buy business premises for the company (his) • To provide financial security for each other and their children in the event of death or

long-term illness (joint) • Investment advice for Children’s Trust Fund (joint) • To increase their disposable income to meet longer-term objectives (joint)

Longer-term

• To ensure they have adequate income in retirement (joint) • To make provision for disabled child’s financial needs (joint)

Appendix 2 – Summary of Objectives Tested

Page 26 of 36 © Technical Connection 2013

www.4chartered.co.uk

October 2011

Immediate

• To provide financial security for each other and their children in the event of death or long-term illness (joint)

• To fund university costs for both children so they leave education without any debts (joint)

• To purchase a flat before the daughter starts her second year at university (joint) • To set up a translation business (her)

Longer-term

• To ensure they have adequate income in retirement (joint) • Mitigate IHT on second death while maximising the value of the estate passed to their

children (joint)

April 2012

Immediate

• To generate income in retirement when it is needed. (joint) • To organise their affairs in an income tax and capital gains tax efficient manner

(joint) • To make a gift of £50,000 to their son to help with wedding costs and property

purchase (joint)

Longer-term

• To ensure Margaret has sufficient income should Tony pre-decease her (joint) • Mitigate IHT on second death while maximising the value of the estate passed to their

children on second death (joint)

October 2012

Immediate

• To provide financial security for herself and her children in the event of illness or death.

• Investment review of existing J D Gilbert Will Trust • To purchase a holiday home in Spain

Longer-term

• To make provision for her children’s university education in a tax efficient manner • To provide adequate income in retirement • Mitigate IHT due on her death while maximising the value of the estate passed to her

children

Appendix 2 – Summary of Objectives Tested

Page 27 of 36 © Technical Connection 2013

www.4chartered.co.uk

April 2013

Immediate

• To set up Peter’s new business and purchase the workshop. • To provide financial security for each other in the event of illness or death. • To mitigate their Income Tax liability.

Longer-term

• To provide adequate income after Rachel stops work at Comitfair Ltd and in retirement.

• To mitigate Inheritance Tax due on death, while maximising the value of the estate passed to their children.

Appendix 3 – Risk Based Tasks

Page 28 of 36 © Technical Connection 2013

www.4chartered.co.uk

This table shows you where you can find all of the ‘risk based’ tasks asked on previous AF5 papers and shows you how many marks were available for them.

Exam Sitting Task Number Number of Marks

April 2007 2(a) & 2(b) 8 & 15

October 2007 3(a) & 3(b) 10 & 5

April 2008 3 7

October 2008 2(a) & 2(b) 10 & 12

April 2009 3(a) 7

October 2009 2(a) & 2(b) 9 & 12

April 2010 3(a) & 3(b) 5 & 5

October 2010 3(a) 10

April 2011 2(a) 6

October 2011 3(a) & 3(b) 8 & 10

April 2012 2 14

October 2012 3(a) & 3(b) 8 & 10

April 2013 3(a) 6

Appendix 4 – Risks and their Explanations

Page 29 of 36 © Technical Connection 2013

www.4chartered.co.uk

Summarised below are all of the different types of risk that have been awarded marks in the risk based task in AF5.

Do remember that this is just a summary – to get full marks in the exam you will have to link your answers to the client’s circumstances. Have a look at some past papers to see the way the examiner expects you to do this.

Risk Reason

Inflation Spending power will be eroded.

Market/ systematic Stock market may fall.

Non systematic One company may fail/ poor management of one company may adversely affect performance.

Health Unable to work and generate an income.

Currency Non sterling assets may suffer by exchange rate movement.

Default Debtor may not be able to pay.

Provider Investment provider may fail.

Taxation/ legislation. Legislation may adversely affect tax treatment of investments.

Diversification Too much exposure to one asset class or geographical region.

Liquidity Asset may not be able to be sold when required.

Interest rate Rates could rise or fall.

Property letting Void periods/ damage by tenants/ high costs of maintenance/ rents received may not cover costs.

Business Property Relief/ current tax benefits/ tax concessions

May not be available when business is sold/ could be withdrawn in the future/ conditions may change.

Holiday lettings/ location.

Location may fall out of favour as a holiday destination/ area people may wish to live.

Political risk Risk of corruption/ regime change/ change in legislation.

Shares in private limited company.

Articles may place a restriction on selling/ if company becomes insolvent then dividends will cease & shareholding will lose entire capital value.

Attitude to risk Investment does not match the clients stated ATR

Appendix 5 – Recommendations: Summary of Main Objectives Tested

Page 30 of 36 © Technical Connection 2013

www.4chartered.co.uk

Below are a summary of the ‘recommendation’ tasks.

Retirement Planning/ retirement income

Paper Task Number Marks Available

April 2007 5(e) 14

October 2007 4(f) 12

April 2008 4(a) 12

October 2008 5(b) & 6(a) 11 & 7

April 2009 7(c) 14

October 2009 7(a) 8

April 2010 6(b) 10

October 2010 7(c) 10

April 2011 7(b) 10

October 2011 7(a) 18

April 2012 5(a) & 6(a) 14 & 10

October 2012 7(b) 7

April 2013 7(c) 8

Provide financial security for each other (& children) in the event of death/ sickness

Paper Task Number Marks Available

April 2007 5(b) 10

October 2007 4(a) 12

April 2008 7 13

April 2009 6(b) 12

October 2009 6(c) 12

April 2010 6(a) 9

October 2010 5(b) 16

April 2011 6(a) & 6(b) 15 & 10

October 2011 6(a) 14

October 2012 6(a) 10

April 2013 7(a) 16

Appendix 5 – Recommendations: Summary of Main Objectives Tested

Page 31 of 36 © Technical Connection 2013

www.4chartered.co.uk

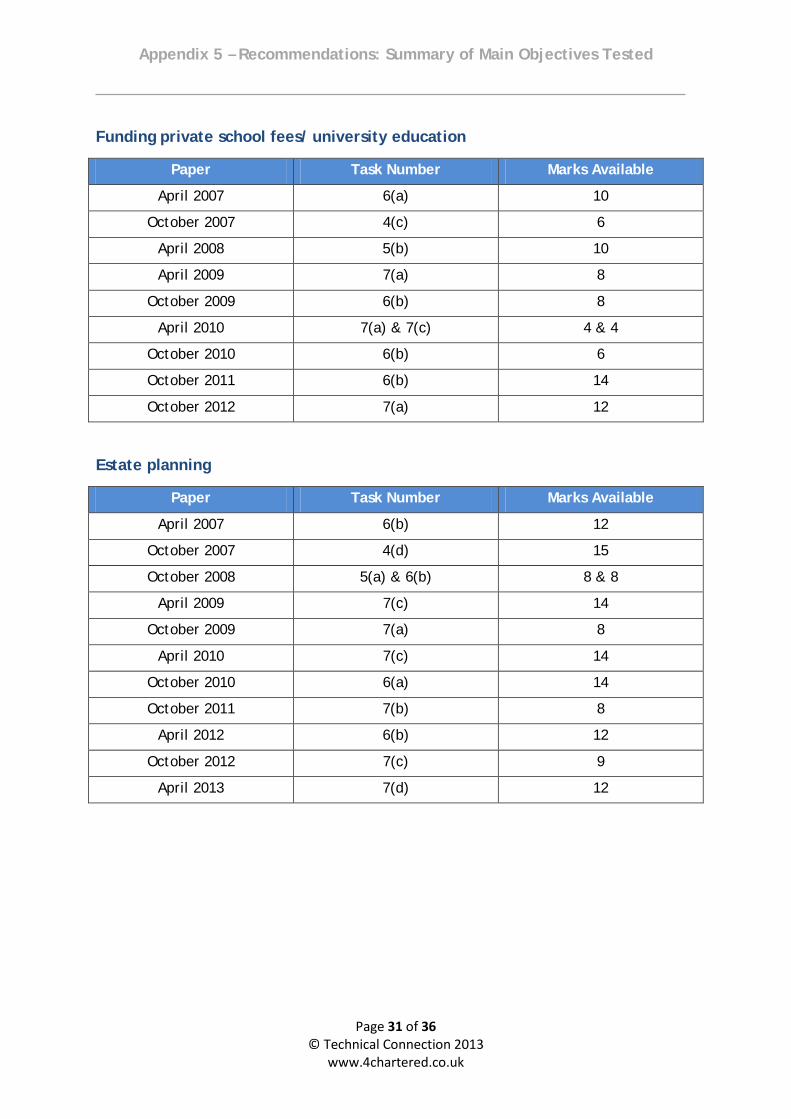

Funding private school fees/ university education

Paper Task Number Marks Available

April 2007 6(a) 10

October 2007 4(c) 6

April 2008 5(b) 10

April 2009 7(a) 8

October 2009 6(b) 8

April 2010 7(a) & 7(c) 4 & 4

October 2010 6(b) 6

October 2011 6(b) 14

October 2012 7(a) 12

Estate planning

Paper Task Number Marks Available

April 2007 6(b) 12

October 2007 4(d) 15

October 2008 5(a) & 6(b) 8 & 8

April 2009 7(c) 14

October 2009 7(a) 8

April 2010 7(c) 14

October 2010 6(a) 14

October 2011 7(b) 8

April 2012 6(b) 12

October 2012 7(c) 9

April 2013 7(d) 12

Appendix 5 – Recommendations: Summary of Main Objectives Tested

Page 32 of 36 © Technical Connection 2013

www.4chartered.co.uk

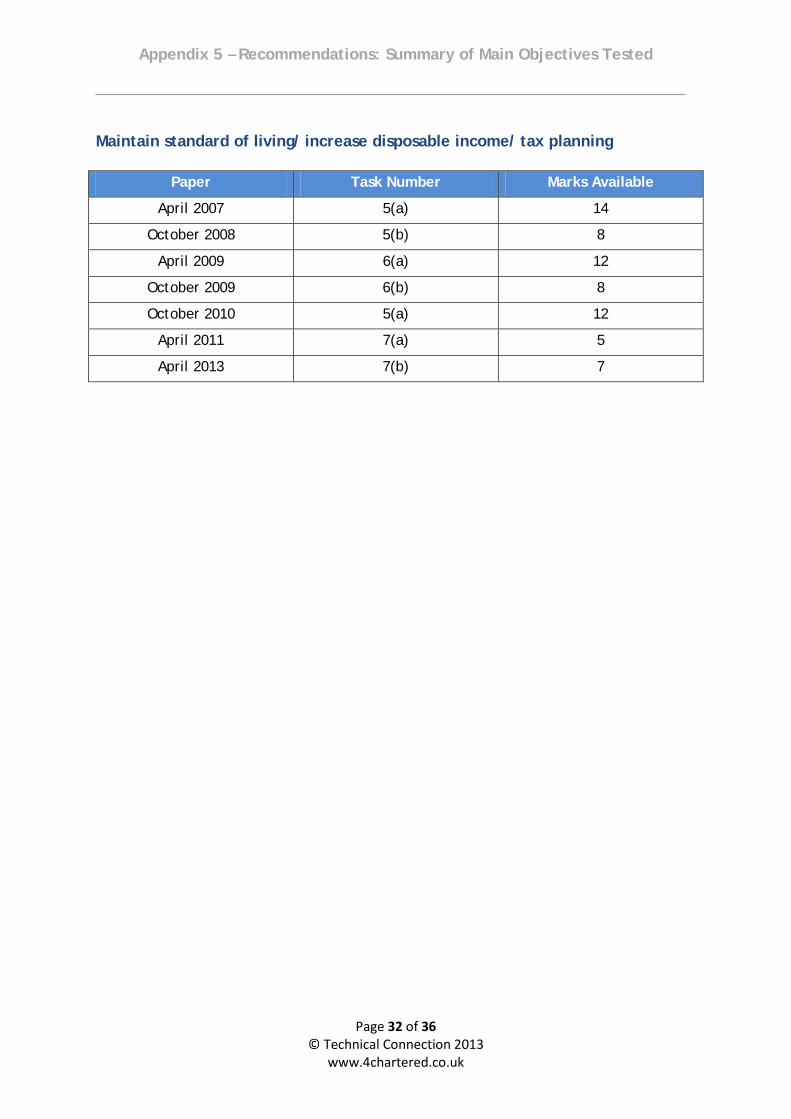

Maintain standard of living/ increase disposable income/ tax planning

Paper Task Number Marks Available

April 2007 5(a) 14

October 2008 5(b) 8

April 2009 6(a) 12

October 2009 6(b) 8

October 2010 5(a) 12

April 2011 7(a) 5

April 2013 7(b) 7

Appendix 6 – Review

Page 33 of 36 © Technical Connection 2013

www.4chartered.co.uk

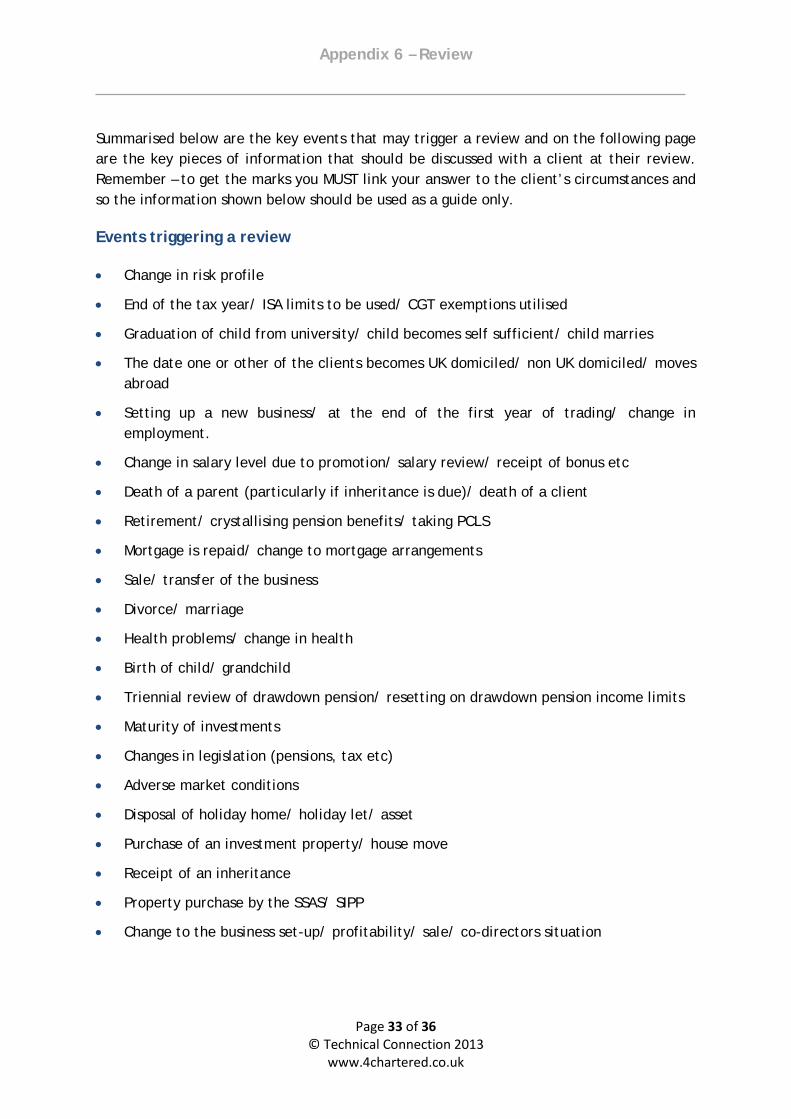

Summarised below are the key events that may trigger a review and on the following page are the key pieces of information that should be discussed with a client at their review. Remember – to get the marks you MUST link your answer to the client’s circumstances and so the information shown below should be used as a guide only.

Events triggering a review

• Change in risk profile

• End of the tax year/ ISA limits to be used/ CGT exemptions utilised

• Graduation of child from university/ child becomes self sufficient/ child marries

• The date one or other of the clients becomes UK domiciled/ non UK domiciled/ moves abroad

• Setting up a new business/ at the end of the first year of trading/ change in employment.

• Change in salary level due to promotion/ salary review/ receipt of bonus etc

• Death of a parent (particularly if inheritance is due)/ death of a client

• Retirement/ crystallising pension benefits/ taking PCLS

• Mortgage is repaid/ change to mortgage arrangements

• Sale/ transfer of the business

• Divorce/ marriage

• Health problems/ change in health

• Birth of child/ grandchild

• Triennial review of drawdown pension/ resetting on drawdown pension income limits

• Maturity of investments

• Changes in legislation (pensions, tax etc)

• Adverse market conditions

• Disposal of holiday home/ holiday let/ asset

• Purchase of an investment property/ house move

• Receipt of an inheritance

• Property purchase by the SSAS/ SIPP

• Change to the business set-up/ profitability/ sale/ co-directors situation

Appendix 6 – Review

Page 34 of 36 © Technical Connection 2013

www.4chartered.co.uk

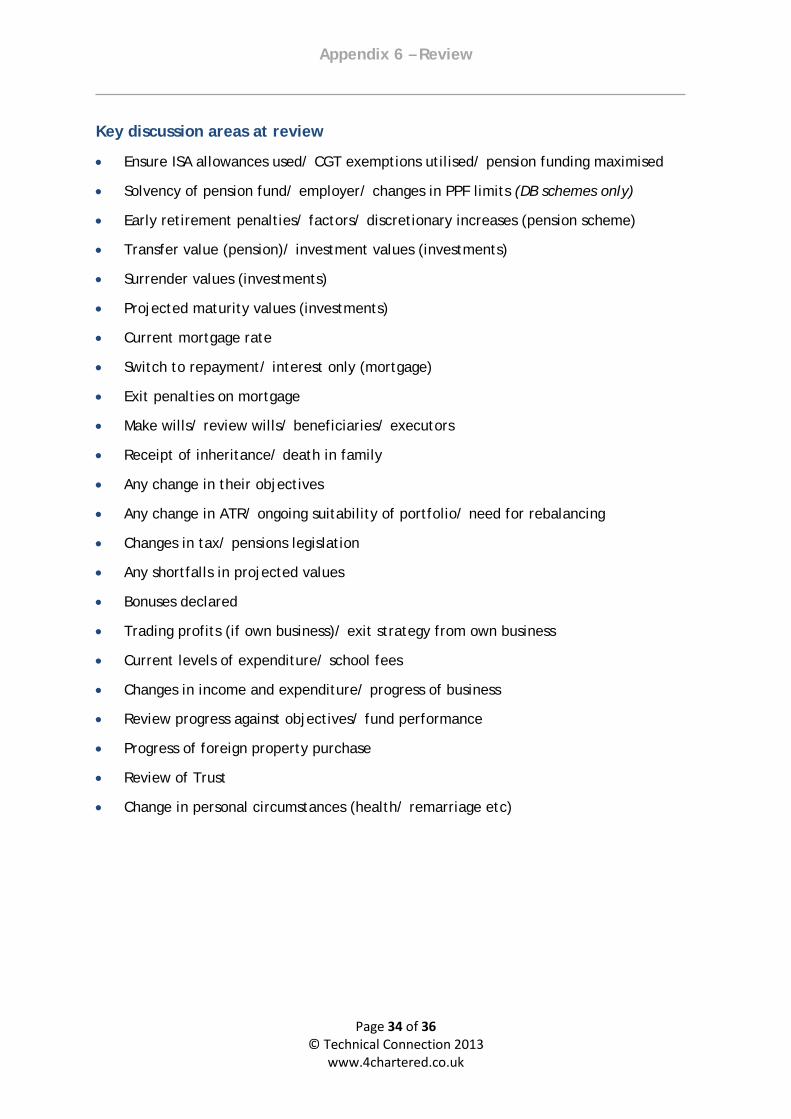

Key discussion areas at review

• Ensure ISA allowances used/ CGT exemptions utilised/ pension funding maximised

• Solvency of pension fund/ employer/ changes in PPF limits (DB schemes only)

• Early retirement penalties/ factors/ discretionary increases (pension scheme)

• Transfer value (pension)/ investment values (investments)

• Surrender values (investments)

• Projected maturity values (investments)

• Current mortgage rate

• Switch to repayment/ interest only (mortgage)

• Exit penalties on mortgage

• Make wills/ review wills/ beneficiaries/ executors

• Receipt of inheritance/ death in family

• Any change in their objectives

• Any change in ATR/ ongoing suitability of portfolio/ need for rebalancing

• Changes in tax/ pensions legislation

• Any shortfalls in projected values

• Bonuses declared

• Trading profits (if own business)/ exit strategy from own business

• Current levels of expenditure/ school fees

• Changes in income and expenditure/ progress of business

• Review progress against objectives/ fund performance

• Progress of foreign property purchase

• Review of Trust

• Change in personal circumstances (health/ remarriage etc)

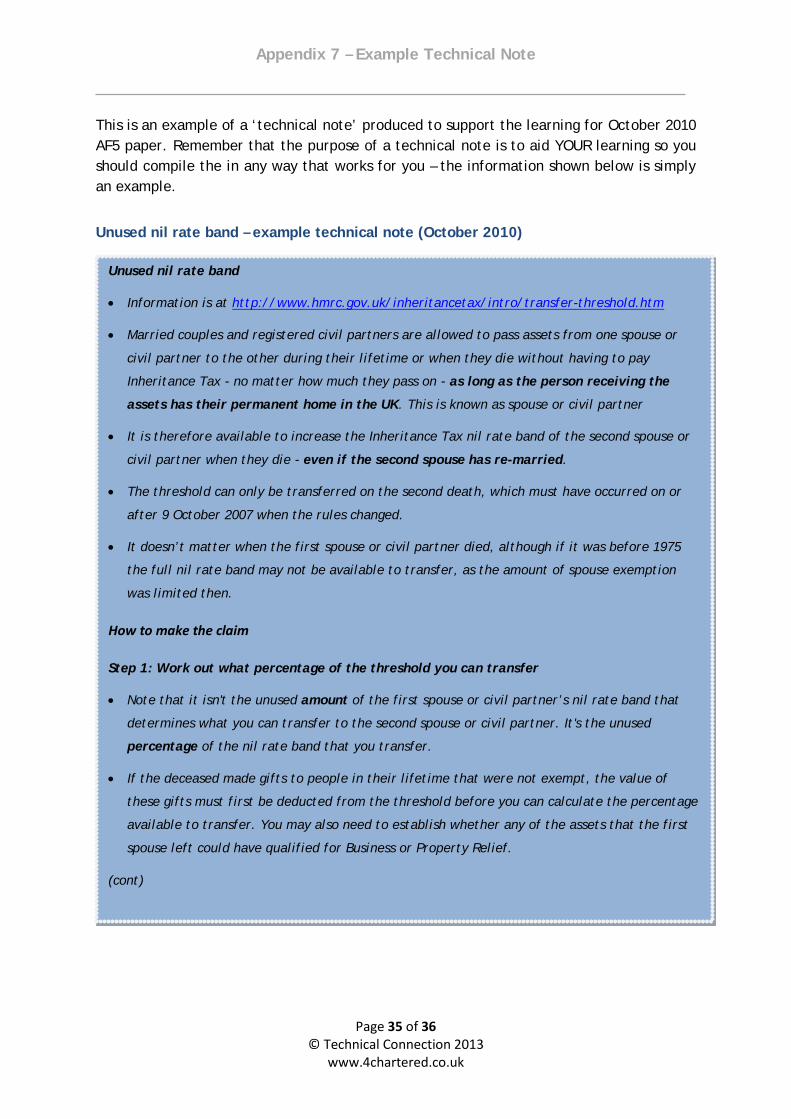

Appendix 7 – Example Technical Note

Page 35 of 36 © Technical Connection 2013

www.4chartered.co.uk

This is an example of a ‘technical note’ produced to support the learning for October 2010 AF5 paper. Remember that the purpose of a technical note is to aid YOUR learning so you should compile the in any way that works for you – the information shown below is simply an example.

Unused nil rate band – example technical note (October 2010)

Unused nil rate band

• Information is at http://www.hmrc.gov.uk/inheritancetax/intro/transfer-threshold.htm

• Married couples and registered civil partners are allowed to pass assets from one spouse or

civil partner to the other during their lifetime or when they die without having to pay

Inheritance Tax - no matter how much they pass on - as long as the person receiving the

assets has their permanent home in the UK. This is known as spouse or civil partner

• It is therefore available to increase the Inheritance Tax nil rate band of the second spouse or

civil partner when they die - even if the second spouse has re-married.

• The threshold can only be transferred on the second death, which must have occurred on or

after 9 October 2007 when the rules changed.

• It doesn’t matter when the first spouse or civil partner died, although if it was before 1975

the full nil rate band may not be available to transfer, as the amount of spouse exemption

was limited then.

How to make the claim

Step 1: Work out what percentage of the threshold you can transfer

• Note that it isn't the unused amount of the first spouse or civil partner’s nil rate band that

determines what you can transfer to the second spouse or civil partner. It's the unused

percentage of the nil rate band that you transfer.

• If the deceased made gifts to people in their lifetime that were not exempt, the value of

these gifts must first be deducted from the threshold before you can calculate the percentage

available to transfer. You may also need to establish whether any of the assets that the first

spouse left could have qualified for Business or Property Relief.

(cont)

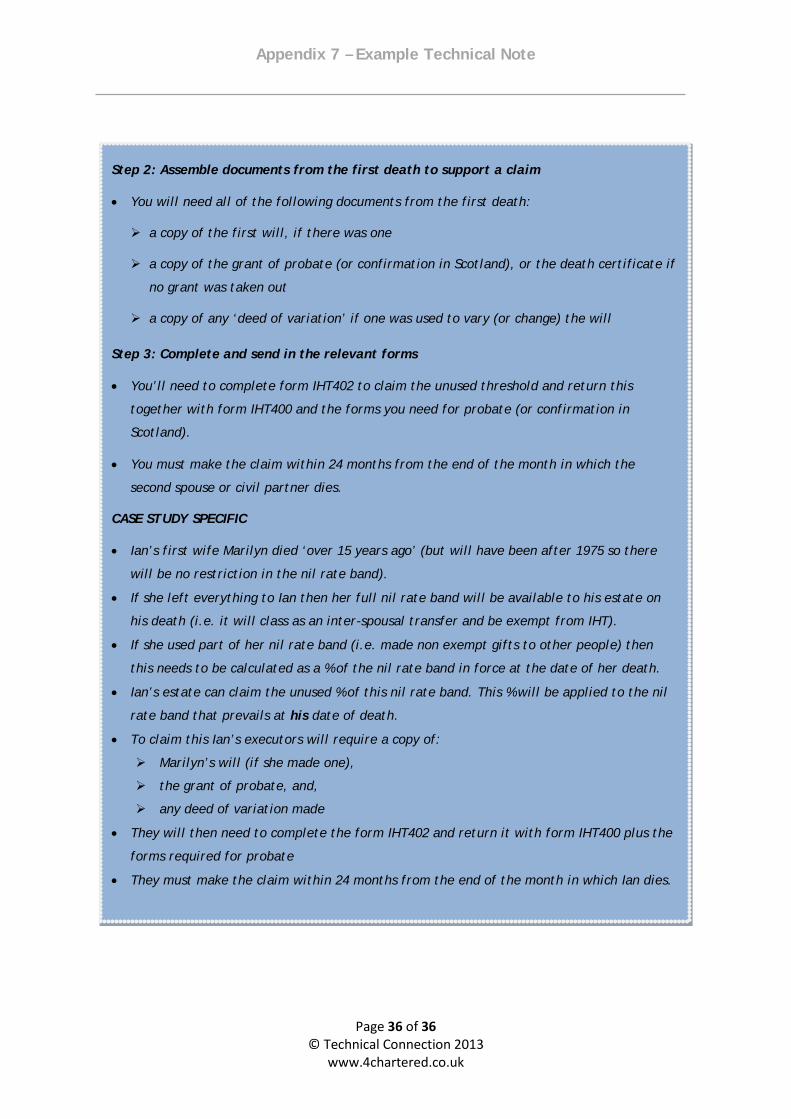

Appendix 7 – Example Technical Note

Page 36 of 36 © Technical Connection 2013

www.4chartered.co.uk

Step 2: Assemble documents from the first death to support a claim

• You will need all of the following documents from the first death:

a copy of the first will, if there was one

a copy of the grant of probate (or confirmation in Scotland), or the death certificate if

no grant was taken out

a copy of any ‘deed of variation’ if one was used to vary (or change) the will

Step 3: Complete and send in the relevant forms

• You’ll need to complete form IHT402 to claim the unused threshold and return this

together with form IHT400 and the forms you need for probate (or confirmation in

Scotland).

• You must make the claim within 24 months from the end of the month in which the

second spouse or civil partner dies.

CASE STUDY SPECIFIC

• Ian’s first wife Marilyn died ‘over 15 years ago’ (but will have been after 1975 so there

will be no restriction in the nil rate band).

• If she left everything to Ian then her full nil rate band will be available to his estate on

his death (i.e. it will class as an inter-spousal transfer and be exempt from IHT).

• If she used part of her nil rate band (i.e. made non exempt gifts to other people) then

this needs to be calculated as a % of the nil rate band in force at the date of her death.

• Ian’s estate can claim the unused % of this nil rate band. This % will be applied to the nil

rate band that prevails at his date of death.

• To claim this Ian’s executors will require a copy of:

Marilyn’s will (if she made one),

the grant of probate, and,

any deed of variation made

• They will then need to complete the form IHT402 and return it with form IHT400 plus the

forms required for probate

• They must make the claim within 24 months from the end of the month in which Ian dies.