(advances in econometrics)badi h. baltagi-nonstationary panels, panel cointegration, and dynamic...

TRANSCRIPT

LIST OF CONTRIBUTORS

Badi H. Baltagi Texas A&M University, Department ofEconomics, College Station, TX 77843-4228,USA. E-mail: [email protected]

M. Douglas Berg Department of Economics and InternationalBusiness, Sam Houston State University,Huntsville, TX 77341, USA

Richard Blundell Institute for Fiscal Studies and UniversityCollege London, UK.E-mail: [email protected]

Stephen Bond Institute for Fiscal Studies and NuffieldCollege, Oxford, UK.E-mail: [email protected]

Jörg Breitung Humboldt University Berlin, Institute ofStatistics and Econometrics, SpandauerStrasse 1, D-10178 Berlin, Germany.Fax: + 49.30.2093.5712;E-mail: [email protected]

Min-Hsien Chiang National Cheng-Kung University, Institute ofInternational Business, Tainan, Taiwan.Fax: 886-6-2766459;E-mail: [email protected]

Alain Hecq University Maastricht, Department ofQuantitative Economics, P.O. Box 616, 6200MD Maastricht, The Netherlands.Fax: + 31-43-388 48 74

Nazrul Islam Department of Economics, Emory University,Atlanta, GA 30322-2240, USA.Fax: 404-727-4639;E-mail: [email protected]

vii

Chihwa Kao Syracuse University, Center for PolicyResearch, Syracuse, NY 13244-1020, USA.Fax: 315-443-1081;E-mail: [email protected]

Heikki Kauppi University of Helsinki, Department ofEconomics, P.O. Box 54 (Unioninkatu 37),FIN-00014 University of Helsinki, Finland.Fax: + 358-9-1917980;E-mail: [email protected]

Qi Li Department of Economics, Texas A&MUniversity, College Station, TX 77843 andDepartment of Economics, University ofGuelph, Guelph, Ontario, N1G 2W1 Canada.E-mail: [email protected]

Chris Murray Department of Economics, University ofHouston, Houston, TX 77204-5882, USA.Fax: (713) 743-3798;E-mail: [email protected]

Franz C. Palm University Maastricht, Department ofQuantitative Economics, P.O. Box 616, 6200MD Maastricht, The Netherlands.Fax: + 31-43-388 48 74

David H. Papell Department of Economics, University ofHouston, Houston, TX 77204-5882, USA.Fax: (713) 743-3798;E-mail: [email protected]

Peter Pedroni Indiana University, Department ofEconomics, Bloomington, IN 47405, USA.E-mail: [email protected]

Aman Ullah Department of Economics, University ofCalifornia, Riverside, CA 92521, USA

viii

Jean-Pierre Urbain University Maastricht, Department ofQuantitative Economics, P.O. Box 616, 6200MD Maastricht, The Netherlands.Fax: + 31-43-388 48 74;E-mail: [email protected]

Frank Windmeijer Institute for Fiscal Studies, 7 RidgmountStreet, London WC1E 7AE, UK.Fax: + 44.(0)20.7323.4780;E-mail: [email protected]

Showen Wu Department of Finance and ManagerialEconomics, State University of New York atBuffalo, Buffalo, NY 14260, USA

Yong Yin Department of Economics, State Universityof New York at Buffalo, Buffalo, NY 14260,USA. Fax: 716-645-2127;E-mail: [email protected]

ix

INTRODUCTION

Badi H. Baltagi, Thomas B. Fomby and R. Carter Hill

Twenty two years ago, the first special issue on panel data econometrics waspublished by the Annales de l’INSEE. This consisted of two volumescontaining a list of ‘who’s who’ in economics and econometrics of panel datathat was edited by Mazodier (1978). Since then, several books on panel datahave been written including the econometric society monograph by Hsiao(1986), a two volume collection of classic papers on the subject by Maddala(1993), a Handbook, which in its second edition contained 33 chapters editedby Matyas & Sevestre (1996) and a textbook by Baltagi (1995a). Severalspecial issues of journals with a panel data theme have also appeared since1978, those include Raj & Baltagi (1992), Matyas (1992), Carraro, et al.(1993), Baltagi (1995b), Sevestre (1999) and Banerjee (1999). There have beennine international conferences on panel data since the first conference atINSEE, the last one was held at the University of Geneva in June, 2000. Paneldata econometrics continues to have an important impact on today’s empiricaleconomics studies. A Journal of Economic Literature search returned 2780citations using the words ‘panel data’ between 1980 and 2000. This volume isdedicated to two recent intensive areas of research in the econometrics of paneldata: nonstationary panels and dynamic panels, see the survey chapter byBaltagi & Kao in this volume. The volume includes eleven refereed chapters onthis subject written by twenty authors. The editors are grateful to the authorsand referees for their cooperation.

The chapter by Baltagi & Kao surveys the nonstationary panels, cointegra-tion in panels and dynamic panels literature. In particular, panel unit root testsare considered first and several important chapters are reviewed including asummary of the finite sample properties of these unit roots tests obtained from

Nonstationary Panels, Panel Cointegration and Dynamic Panels, Volume 15, pages 1–5.Copyright © 2000 by Elsevier Science Inc.All rights of reproduction in any form reserved.ISBN: 0-7623-0688-2

1

extensive simulations. Also, spurious regressions in panel data are consideredfollowed by panel cointegration tests with a summary of the finite sampleproperties of these cointegration tests using Monte Carlo experiments. Next,estimation and inference in panel cointegration models is considered and thechapter concludes with a review of recent developments in dynamic panel datamodels that have occurred over the last five years.

The chapter by Blundell, Bond & Windmeijer reviews recent developmentsin the estimation of dynamic panel data models using generalized method ofmoments (GMM). In particular, this chapter focuses on the system GMMestimator derived by Blundell & Bond (1998) which relies on relatively mildrestrictions on the initial condition process. This system GMM estimatorencompasses the GMM estimator based on the non-linear moment conditionsavailable in the dynamic error components model. Monte Carlo experimentsand asymptotic variance calculations show that this extended GMM estimatorcan offer considerable efficiency gains in situations where the first differencedGMM estimator performs poorly.

The chapter by Pedroni develops methods for estimating and testinghypotheses for cointegrating vectors in dynamic panels. In particular, thischapter proposes methods based on fully modified OLS principles whichaccount for considerable heterogeneity across individual members of the panel.The asymptotic properties of various estimators are compared based on poolingalong the within and between dimensions of the panel. Monte Carlosimulations show that the group mean estimator is well behaved even inrelatively small samples under a variety of scenarios.

The chapter by Hecq, Palm & Urbain extends the concept of serialcorrelation common features analysis to nonstationary panel data models. Thisanalysis is motivated both by the need to study and test for common structuresand comovements in panel data with autocorrelation present and by an increasein efficiency due to pooling. The authors propose sequential testing proceduresand test their performance using a small scale Monte Carlo. Concentratingupon the fixed effects model, they define homogeneous panel common featuremodels and give a series of steps to implement these tests. These tests are usedto investigate the liquidity constraints model for 22 OECD and G7 countries.The presence of a panel common feature vector is rejected at the 5% nominallevel.

The chapter by Breitung studies the local power of panel unit root teststatistics against a sequence of local power alternatives. In particular, thischapter finds that the Levin & Lin (1993) (LL) and Im, Pesaran & Shin (1997)(IPS) tests suffer from severe loss of power if individual specific trends are

2 BADI H. BALTAGI, THOMAS B. FOMBY & R. CARTER HILL

included. Breitung suggests a test statistic that does not employ a biasadjustment whose power is substantially higher than that of LL or the IPS testsusing Monte Carlo experiments. This chapter also finds that the power of theLL and IPS tests is sensitive to the specification of the deterministic terms.

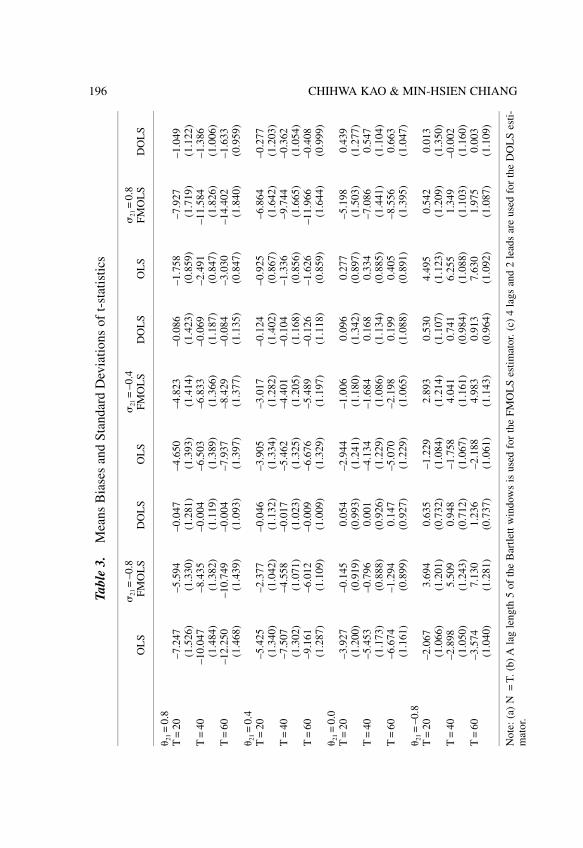

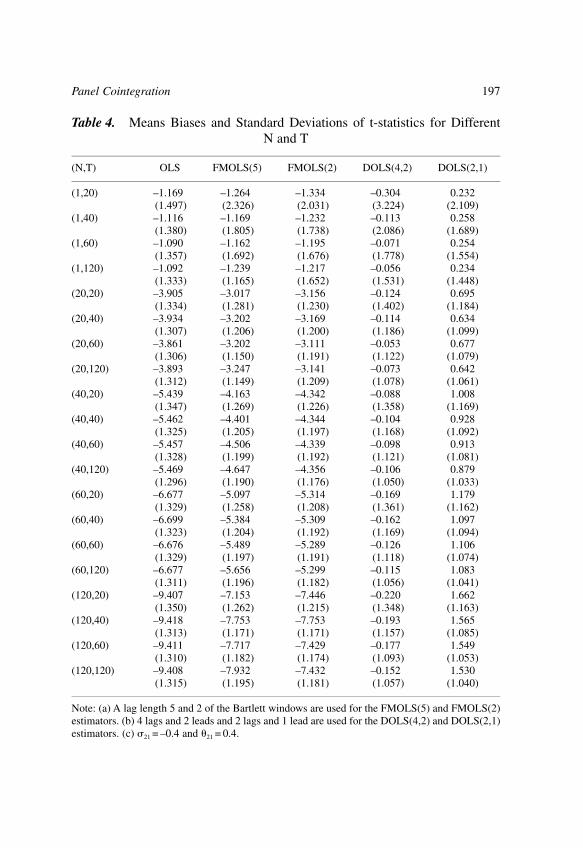

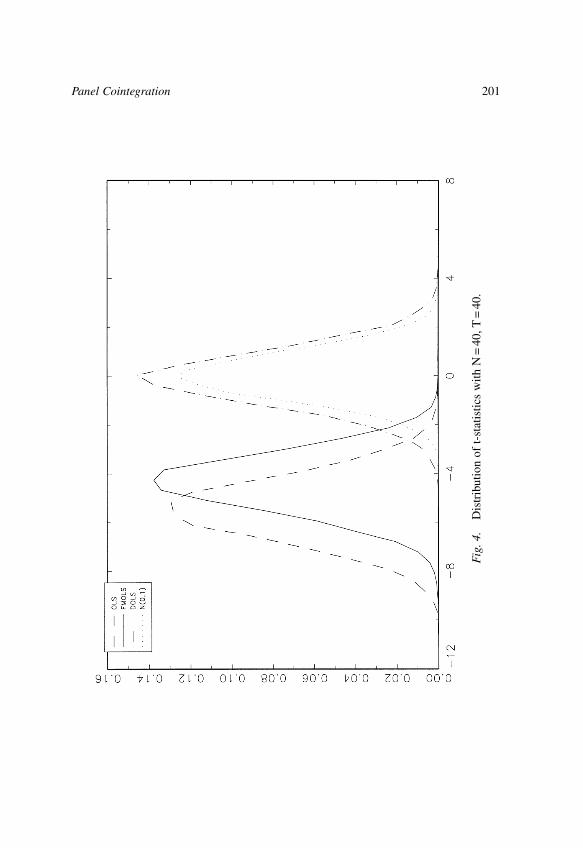

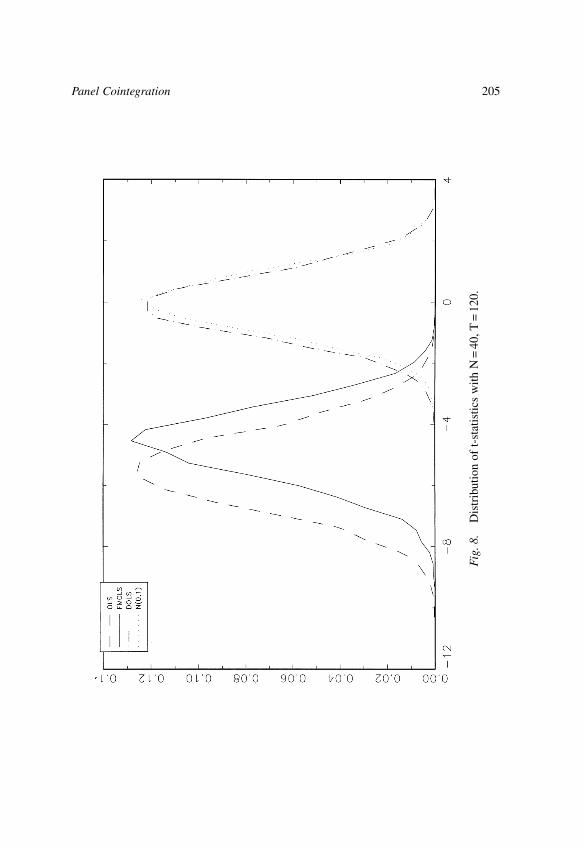

The chapter by Kao & Chiang studies the limiting distributions of ordinaryleast squares (OLS), fully modified OLS (FMOLS) and dynamic OLS (DOLS)estimators in a panel cointegrated regression model. This chapter shows thatthe OLS, FMOLS and DOLS estimators are all asymptotically normallydistributed. However, the asymptotic distribution of the OLS estimator has anon-zero mean. Extensive Monte Carlo experiments are performed which showthat the OLS estimator has a non-negligible bias in finite samples, the FMOLSestimator does not improve on the OLS estimator in general, and the DOLSestimator outperforms both OLS and FMOLS.

The chapter by Murray & Papell proposes a panel unit roots test in thepresence of structural change. In particular, this chapter proposes a unit roottest for non-trending data in the presence of a one-time change in the mean fora heterogeneous panel. The date of the break is endogenously determined. Theresultant test allows for both serial and contemporaneous correlation, both ofwhich are often found to be important in the panel unit roots context. Murray& Papell conduct two power experiments for panels of non-trending, stationaryseries with a one-time change in means and find that conventional panel unitroot tests generally have very low power. Then they conduct the sameexperiment using methods that test for unit roots in the presence of structuralchange and find that the power of the test is much improved.

The chapter by Kauppi develops a new limit theory for panel data that maybe cross sectionally heterogeneous in a fairly general way. This limit theorybuilds upon the concepts of joint convergence in probability and in distributionfor double indexed processes by Phillips & Moon (1999a). This limit theory isapplied to a panel regression model with regressors that are generated by anautoregressive process with a root local to unity. The main results are thefollowing: (i) the usual pooled panel OLS estimator is invalid for inference, (ii)a bias corrected pooled OLS proves to be �NT consistent with an asymptoticnormal distribution centered on the true parameter value irrespective ofwhether the regressors have near or exact unit roots. This positive result holdsonly in the special case where the model does not exhibit any deterministiceffects, such as individual intercepts. (iii) The fully modified panel estimator ofPhillips & Moon (1999a) is also subject to severe bias effects if the regressorsare nearly rather than exactly cointegrated. These theoretical results areconfirmed using Monte Carlo results.

3Introduction

The chapter by Yin & Wu proposes stationarity tests for a heterogeneouspanel data model. The authors consider the case of serially correlated errors inthe level and trend stationary models. The proposed panel tests utilize theKwaitkowski, Phillips, Schmidt & Shin (1992) test and the Leybourne &McCabe (1994) test from the time series literature. Two different ways ofpooling information from the independent tests are used. In particular, thegroup mean and the Fisher type tests are used to develop the panel stationaritytests. Monte Carlo experiments are performed that reveal good small sampleperformance in terms of size and power.

The chapter by Berg, Li & Ullah considers the problem of estimating asemiparametric partially linear dynamic panel data model with disturbancesthat follow a one-way error component structure. Two new semiparametricinstrumental variable (IV) estimators are proposed for the coefficient of theparametric component. These are shown to be more efficient than the onessuggested by Li & Stengos (1996) and Li & Ullah (1998) because they makefull use of the error component structure. This is confirmed using Monte Carloexperiments.

The chapter by Islam conducts a Monte Carlo study to investigate the smallsample properties of dynamic panel data estimators. Although there areextensive Monte Carlo studies on this subject, this study customizes the designto the estimation of the growth convergence equation using the Summers-Heston data. Islam concludes that the OLS estimation of thegrowth-convergence equation is likely to give misleading results. At the sametime, indiscriminate use of panel estimators is risky and one should makejudicious choice of panel estimators.

REFERENCES

Only references that are not cited later in the volume are given here.

Baltagi, B. H. (1995b). Editor’s Introduction: Panel Data. Journal of Econometrics, 68, 1–4.Banerjee, A. (1999). Panel Data Unit Roots and Cointegration: An Overview. Oxford Bulletin of

Economics and Statistics, 61, 607–629.Carraro, C., Peracchi, F., & Weber, G. (Eds.) (1993). The Econometrics of Panels and Pseudo

Panels. Journal of Econometrics, 59, 1–211.Hsiao, C. (1986). Analysis of Panel Data. Cambridge: Cambridge University Press.Maddala, G. S. (Ed.) (1993). The Econometrics of Panel Data. Vols. 1 and 2. Cheltenham: Edward

Elgar.Matyas, L. (Ed.) (1996). Modelling Panel Data. Structural Change and Economic Dynamics, 3,

291–384.

4 BADI H. BALTAGI, THOMAS B. FOMBY & R. CARTER HILL

Matyas, L., & Sevestre, P. (Eds.) (1996). The Econometrics of Panel Data: Handbook of Theoryand Applications. Dordrecht: Kluwer Academic Publishers.

Mazodier P. (Ed.) (1978). The Econometrics of Panel Data. Annales de I’INSEE, 30/31.Raj, B., & Baltagi, B. (1992). Editors’ Introduction and Overview: Panel Data Analysis. Empirical

Economics, 17, 1–8.Sevestre, P. (1999). 1977–1997: Changes and Continuities in Panel Data. Annales D’Economie et

de Statistique, 55–56, 15–25.

5Introduction

NONSTATIONARY PANELS,COINTEGRATION IN PANELS ANDDYNAMIC PANELS: A SURVEY

Badi H. Baltagi and Chihwa Kao

ABSTRACT

This chapter provides an overview of topics in nonstationary panels: panelunit root tests, panel cointegration tests, and estimation of panelcointegration models. In addition it surveys recent developments indynamic panel data models.

I. INTRODUCTION

Two important areas in the econometrics of panel data that have received muchattention recently are dynamic panel data1 and nonstationary panel time seriesmodels.2 This special issue focuses on these two topics. With the growing useof cross-country data over time to study purchasing power parity, growthconvergence and international R&D spillovers, the focus of panel dataeconometrics has shifted towards studying the asymptotics of macro panelswith large N (number of countries) and large T (length of the time series) ratherthan the usual asymptotics of micro panels with large N and small T. In fact, thelimiting distributions of double indexed integrated processes had to bedeveloped, see Phillips & Moon (1999a). The fact that T is allowed to increaseto infinity in macro panel data, generated two strands of ideas. The first rejectedthe homogeneity of the regression parameters implicit in the use of a pooled

Nonstationary Panels, Panel Cointegration and Dynamic Panels, Volume 15, pages 7–51.Copyright © 2000 by Elsevier Science Inc.All rights of reproduction in any form reserved.ISBN: 0-7623-0688-2

7

regression model in favor of heterogeneous regressions, i.e. one for eachcountry, see Pesaran & Smith (1995), Im, Pesaran & Shin (1997), Lee, Pesaran& Smith (1997), Pesaran, Shin & Smith (1999) and Pesaran & Zhao (1999) tomention a few. This literature critically relies on T being large to estimate eachcountry’s regression separately. Another strand of literature applied time seriesprocedures to panels, worrying about non-stationarity, spurious regressions andcointegration. Adding the cross-section dimension to the time-series dimensionoffers an advantage in the testing for nonstationarity and cointegration. Thehope of the econometrics of nonstationary panel data is to combine the best ofboth worlds: the method of dealing with nonstationary data from the time seriesand the increased data and power from the cross-section. The addition of thecross-section dimension, under certain assumptions, can act as repeated drawsfrom the same distribution. Thus as the time and cross-section dimensionincrease panel test statistics and estimators can be derived which converge indistribution to normally distributed random variables.

However, the use of such panel data methods are not without their critics, seeMaddala, Wu & Liu (2000) who argue that panel data unit root tests do notrescue purchasing power parity (PPP). In fact, the results on PPP with panelsare mixed depending on the group of countries studied, the period of study andthe type of unit root test used. More damaging is the argument by Maddala etal. that for PPP, panel data tests are the wrong answer to the low power of unitroot tests in single time series. After all, the null hypothesis of a single unit rootis different from the null hypothesis of a panel unit root for the PPP hypothesis.Using the same line of criticism, Maddala (1999) argued that panel unit roottests did not help settle the question of growth convergence among countries.However, it was useful in spurring much needed research into dynamic paneldata models. Also, Quah (1996) who argued that the basic issues of whetherpoor countries catch up with the rich can never be answered by the use oftraditional panels. Instead, Quah suggested formulating and estimating modelsof income dynamics.

One can find numerous applications of time series methods applied to panelsin recent years. Examples from the purchasing power parity literature includeBernard & Jones (1996), Jorion & Sweeney (1996), MacDonald (1996), Oh(1996), Wu (1996), Coakley & Fuertes (1997), Culver & Papell (1997), Papell(1997), O’Connell (1998), Choi (1999a), Andersson & Lyhagen (1999), andCanzoneri, Cumby & Diba (1999) to mention a few. On health careexpenditures, see McCoskey & Selden (1998), and Gerdtham & Löthgren(1998). On growth and convergence, see Islam (1995), Evans & Karas (1996),Sala-i-Martin (1996), Lee, Pesaran & Smith (1997), and McCoskey & Kao

8 BADI H. BALTAGI & CHIHWA KAO

(1999a). On international R&D spillovers, see Funk (1998) and Kao, Chiang &Chen (1999). On exchange rate models, see Groen & Kleibergen (1999), andGroen (1999). On savings and investment models, see Coakely, Kulasi & Smith(1996) and Moon & Phillips (1998).

The first part of this chapter surveys some of the developments innonstationary panel models that have occurred since the middle of 1990s. Twoother recent surveys on this subject include Phillips & Moon (1999b) on multi-indexed processes and Banerjee (1999) on panel unit roots and cointegrationtests. We will pay attention to the following three topics: (1) panel unit roottests, (2) panel cointegration tests, and (3) estimation and inference in the panelcointegration models. The discussion of each topic will be illustrated byexamples taken from the aforementioned list of references. Section 2 reviewspanel unit root tests, while Section 3 discusses the panel spurious models.Section 4 considers the panel cointegration tests, while Section 5 discussespanel cointegration models. Section 6 reviews some recent developments indynamic panels and Section 7 gives our conclusion.

A word on notation. We write the integral �10 W(s)ds, as � W when there is no

ambiguity over limits. We define �1/2 to be any matrix such that

� = (�1/2)(�1/2), use ⇒ to denote weak convergence, →p to denote convergencein probability, I(0) and I(1) to signify a time series that is integrated of orderzero and one, respectively, and WZ(r) = W(r) � [� WZ�][� ZZ�]Z(r) to denote anL2 projection residual of W(r) on Z(r).

II. PANEL UNIT ROOTS TESTS

Testing for unit roots in time series studies is now common practice amongapplied researchers and has become an integral part of econometric courses.However, testing for unit roots in panels is recent, see Levin & Lin (1992), Im,Pesaran & Shin (1997), Harris & Tzavalis (1999), Maddala & Wu (1999), Choi(1999a), and Hadri (1999). Exceptions are Bharagava et al. (1982), Boumahdi& Thomas (1991), Breitung & Meyer (1994), and Quah (1994). Bharagava etal. proposed a test for random walk residuals in a dynamic model with fixedeffects. They suggested a modified Durbin-Watson (DW) statistic based onfixed effects residuals and two other test statistics based on differenced OLSresiduals. In typical micro panels with N→�, they recommended theirmodified DW statistic. Boumahdi & Thomas (1991) proposed a generalizationof the Dickey-Fuller (DF) test for unit roots in panel data to assess theefficiency of the French capital market using 140 French stock prices over the

9Nonstationary Panels, Cointegration in Panels and Dynamic Panels: A Survey

period January 1973 to February 1986. Breitung & Meyer (1994) appliedvarious modified DF test statistics to test for unit roots in a panel of contractedwages negotiated at the firm and industry level for Western Germany over theperiod 1972–1987. Quah (1994) suggested a test for unit root in a panel datamodel without fixed effects where both N and T go to infinity at the same ratesuch that N/T is constant. Levin & Lin (1992) generalized this model to allowfor fixed effects, individual deterministic trends and heterogeneous seriallycorrelated errors. They assumed that both N and T tend to infinity. However, Tincreases at a faster rate than N with N/T→0. Even though this literature grewfrom time series and panel data, the way in which N, the number of cross-section units, and T, the length of the time series, tend to infinity is crucial fordetermining asymptotic properties of estimators and tests proposed fornonstationary panels, see Phillips & Moon (1999a). Several approaches arepossible including: (i) sequential limits where one index, say N, is fixed and Tis allowed to increase to infinity, giving an intermediate limit. Then by lettingN tend to infinity subsequently, a sequential limit theory is obtained. Phillips &Moon (1999b) argued that these sequential limits are easy to derive and arehelpful in extracting quick asymptotics. However, Phillips and Moon provideda simple example that illustrates how sequential limits can sometimes givemisleading asymptotic results. (ii) A second approach, used by Quah (1994)and Levin & Lin (1992) is to allow the two indexes, N and T to pass to infinityalong a specific diagonal path in the two dimensional array. This path can bedetermined by a monotonically increasing functional relation of the typeT = T(N) which applies as the index N→�. Phillips & Moon (1999b) showedthat the limit theory obtained by this approach is dependent on the specificfunctional relation T = T(N) and the assumed expansion path may not providean appropriate approximation for a given (T, N) situation. (iii) A third approachis a joint limit theory allowing both N and T to pass to infinity simultaneouslywithout placing specific diagonal path restrictions on the divergence. Somecontrol over the relative rate of expansion may have to be exercised in order toget definitive results. Phillips & Moon argued that, in general, joint limit theoryis more robust than either sequential limit or diagonal path limit. However, itis usually more difficult to derive and requires stronger conditions such as theexistence of higher moments that will allow for uniformity in the convergencearguments. The muti-index asymptotic theory in Phillips & Moon (1999a, b) isapplied to joint limits in which T, N→� and (T/N)→�, i.e. to situations wherethe time series sample is large relative to the cross-section sample. However,the general approach given there is also applicable to situations in which (T/N)→0 although different limit results will generally obtain in that case.

10 BADI H. BALTAGI & CHIHWA KAO

A. Levin & Lin (1992) Tests

Consider the model

yit = �iyit�1 + z�it�i + uit, i = 1, . . . , N; t = 1, . . . , T, (1)

where zit is the deterministic component and uit is a stationary process. zit couldbe zero, one, the fixed effects, �i, or fixed effect as well as a time trend, t. TheLevin & Lin (LL) tests assume that uit are iid(0, 2

u) and �i = � for all i. LL areinterested in testing the null hypothesis

H0 : � = 1 (2)

against the alternative hypothesis

Ha : � < 1.

Let � be the OLS estimator of � in (1) and define

zt = (z1t, . . . , zNt)�,

h(t, s) = z�t��T

t=1

ztz�t��1

zs,

uit = uit ��T

s=1

h(t, s)uis,

and

yit = yit ��T

s=1

h(t, s)yis. (3)

Then we have

�NT(� � 1) =

1

�N�N

i=1

1

T�T

t=1

yi, t�1uit

1N�

N

i=1

1T2 �T

t=1

y2i, t�1

and the corresponding t-statistic, under the null hypothesis is given by

t� =

(� � 1)� �N

i=1�T

t=1

y2i, t�1

se

,

11Nonstationary Panels, Cointegration in Panels and Dynamic Panels: A Survey

where

s2e =

1NT�

N

i=1�T

t=1

u2it.

Assume that there exists a scaling matrix DT and piecewise continuousfunction Z(r) such that

D�1T z[Tr] →Z(r)

uniformly for r�[0, 1]. For a fixed N, we have

1

�N�N

i=1

1T�

T

t=1

yi, t�1uit ⇒1

�N�N

i=1�WiZ dWiZ

and

1N�

N

i=1

1T2 �T

t=1

y2i, t�1 ⇒ 1

N�N

i=1

�W 2iZ,

as T→�. Next we assume that � WiZ dWiZ and � W2iZ, are independent across i

and have finite second moments. Then it follows that

1N�

N

i=1

�W 2iZ →p E�W 2

iZ1

�N�N

i=1

��WiZ dWiZ � E�WiZ dWiZ�⇒ N�0, Var��WiZ dWiZ��as N→� by a law of large numbers and the Lindeberg-Levy central limittheorem. The following moments are taken from Levin & Lin (1992):

zit E[� WiZ dWiZ] Var[� WiZ dWiZ] E[� W2iZ] Var[� WiZ

2 ]

0 012

12

13

1 013

12

? (4)

�i �12

112

16

145

(�i, t) �12

160

115

116300

12 BADI H. BALTAGI & CHIHWA KAO

Using (4), Levin & Lin (1992) obtain the following limiting distributions of�NT(� � 1) and t�:

zit � t�

0 �NT(� � 1) ⇒ N(0, 2) t� ⇒ N(0, 1)

1 �NT(� � 1) ⇒ N(0, 2) t� ⇒ N(0, 1)

�i �NT(� � 1) + 3�N ⇒�0,515 � �1.25t� + �1.875N ⇒ N(0, 1) (5)

(�i, t)��N(T(� � 1) + 7.5) ⇒ N�0,2895112 � �448

277(t� + �3.75N) ⇒ N(0, 1)

Sequential limit theory, i.e. T→� followed by N→�, is used to derive thelimiting distributions in (5). In case uit is stationary, the asymptotic distributionsof � and t� need to be modified due to the presence of serial correlation.

Harris & Tzavalis (1999) also derived unit root tests for (1) withzit = {0}, {�i}, or {(�i, t)�} when the time dimension of the panel, T, is fixed.This is the typical case for micro panel studies. The main results are:

zit �

0 �N(� � 1) ⇒ N�0,2

T(T � 1)��i �N�� � 1 +

3T + 1�⇒ N�0,

3(17T2 � 20T + 17)5(T � 1)(T + 1)3 �

(�i, t)� �N�� � 1 +15

2(T + 2)�⇒ N�0,15(193T2 � 728T + 1147)

112(T + 2)3(T � 2) �Harris & Tzavalis (1999) also showed that the assumption that T tends toinfinity at a faster rate than N as in LL rather than T fixed as in the case in micropanels, yields tests which are substantially undersized and have low powerespecially when T is small.

Recently, Frankel & Rose (1996), Oh (1996), and Lothian (1996) tested thePPP hypothesis using panel data. All of these articles use LL tests and some ofthem report evidence supporting the PPP hypothesis. O’Connell (1998),

13Nonstationary Panels, Cointegration in Panels and Dynamic Panels: A Survey

however, showed that the LL tests suffered from significant size distortion inthe presence of correlation among contemporaneous cross-sectional errorterms. O’Connell highlighted the importance of controlling for cross-sectionaldependence when testing for a unit root in panels of real exchange rates. Heshowed that, controlling for cross-sectional dependence, no evidence againstthe null of a random walk can be found in panels of up to 64 real exchangerates.

Virtually all the existing nonstationary panel literature assume cross-sectional independence. It is true that the assumption of independence across iis rather strong, but it is needed in order to satisfy the requirement of theLindeberg-Levy central limit theorem. Moreover, as pointed out by Quah(1994), modeling cross-sectional dependence is involved because individualobservations in a cross-section have no natural ordering. Driscoll & Kraay(1998) presented a simple extension of common nonparametric covariancematrix estimation techniques which yields standard errors that are robust tovery general forms of spatial and temporal dependence as the time dimensionbecomes large. In a recent paper, Conley (1999) presented a spatial model ofdependence among agents using a metric of economic distance that providescross-sectional data with a structure similar to time-series data. Conleyproposed a generalized method of moments (GMM) using such dependent dataand a class of nonparametric covariance matrix estimators that allow for ageneral form of dependence characterized by economic distance.

B. Im, Pesaran & Shin (1997) Tests

The LL test is restrictive in the sense that it requires � to be homogeneousacross i. As Maddala (1999) pointed out, the null may be fine for testingconvergence in growth among countries, but the alternative restricts everycountry to converge at the same rate. Im, Pesaran & Shin (1997) (IPS) allow fora heterogeneous coefficient of yit�1 and proposed an alternative testingprocedure based on averaging individual unit root test statistics. IPS suggestedan average of the augmented DF (ADF) tests when uit is serially correlated withdifferent serial correlation properties across cross-sectional units, i.e. uit =�pi

j=1 ijuit� j + �it. Substituting this uit in (1) we get:

yit = �iyit�1 +�pi

j=1

ij �yit� j + z�it�i + �it. (6)

The null hypothesis is

H0 : �i = 1

14 BADI H. BALTAGI & CHIHWA KAO

for all i and the alternative hypothesis is

Ha : �i < 1

for at least one i. The IPS t-bar statistic is defined as the average of theindividual ADF statistics as

t =1N�

N

i=1

t�i, (7)

where t�iis the individual t-statistic of testing H0 : �i = 1 in (6). It is known that

for a fixed N

t�i⇒� 1

0

WiZ dWiZ

� 1

0

W2iZ1/2

= tiT (8)

as T→�. IPS assume that tiT are iid and have finite mean and variance. Then

�N�1N�

N

i=1

tiT � E[tiT | �i = 1]��Var[tiT | �i = 1]

⇒ N(0, 1) (9)

as N→� by the Lindeberg-Levy central limit theorem. Hence

tIPS =�N(t � E[tiT | �i = ])

�Var[tiT | �i = 1]⇒ N(0, 1) (10)

as T→� followed by N→� sequentially. The values of E[tiT | �i = 1] andVar[tiT | �i = 1] have been computed by IPS via simulations for different valuesof T and p�is.

In this volume, Breitung (2000) studies the local power of LL and IPS testsstatistics against a sequence of local alternatives. Breitung finds that the LL andIPS tests suffer from a dramatic loss of power if individual specific trends areincluded. This is due to the bias correction that also removes the mean underthe sequence of local alternatives. The simulation results indicate that thepower of LL and IPS tests is very sensitive to the specification of thedeterministic terms.

McCoskey & Selden (1998) applied the IPS test for testing unit root for percapita national health care expenditures (HE) and gross domestic product(GDP) for a panel of OECD countries. McCoskey & Selden rejected the null

15Nonstationary Panels, Cointegration in Panels and Dynamic Panels: A Survey

hypothesis that these two series contain unit roots. Gerdtham & Löthgren(1998) claimed that the stationarity found by McCoskey & Selden are driven bythe omission of time trends in their ADF regression in (6). Using the IPS testwith a time trend, Gerdtham & Löthgren found that both HE and GDP arenonstationary. They concluded that HE and GDP are cointegrated around lineartrends following the results of McCoskey & Kao (1999b).

C. Combining P-Values Tests

Let GiTibe a unit root test statistic for the i-th group in (1) and assume that as

Ti →�, GiTi⇒ Gi. Let pi be the p-value of a unit root test for cross-section i, i.e.

pi = F(GiTi), where F(·) is the distribution function of the random variable Gi.

Maddala & Wu (1999) and Choi (1999a) proposed a Fisher type test

P = � 2�N

i=1

ln pi (11)

which combines the p-values from unit root tests for each cross-section i to testfor unit root in panel data. P is distributed as 2 with 2N degrees of freedom asTi →� for all N. Maddala et al. (1999) argued that the IPS and Fisher tests relaxthe restrictive assumption of the LL test that �i is the same under the alternative.Both the IPS and Fisher tests combine information based on individual unitroot tests. However, the Fisher test has the advantage over the IPS test in thatit does not require a balanced panel. Also, the Fisher test can use different laglengths in the individual ADF regressions and can be applied to any other unitroot tests. The disadvantage is that the p-values have to be derived by MonteCarlo simulations. Choi (1999a) echoes similar advantages of the Fisher test:(1) the cross-sectional dimension, N, can be either finite or infinite, (2) eachgroup can have different types of nonstochastic and stochastic components, (3)the time series dimension, T, can be different for each i, and (4) the alternativehypothesis would allow some groups to have unit roots while others may not.

When N is large, Choi (1999a) proposed a Z test,

Z =

1

�N�N

i=1

( � 2 ln pi � 2)

2(12)

since E[ � 2 ln pi] = 2 and Var[ � 2 ln pi] = 4. Assume that the pi’s are iid anduse the Lindeberg-Levy central limit theorem to get

Z ⇒ N(0, 1)

16 BADI H. BALTAGI & CHIHWA KAO

as Ti →� followed by N→�.3

Choi (1999a) applied the Z test in (12) and the IPS test in (7) to panel dataof real exchange rates and provided evidence in favor of the PPP hypothesis.Choi claimed that this is due to the improved finite sample power of the Fishertest. Maddala & Wu (1999) and Maddala et al. (1999) find that the Fisher testis superior to the IPS test, but they argue that these panel unit root tests still donot rescue the PPP hypothesis. When allowance is made for the deficiency inthe panel data unit root tests and panel estimation methods, support for PPPturns out to be weak.

D. Residual Based LM Test

Hadri (1999) proposed a residual based Lagrange Multiplier (LM) test for thenull that the time series for each i are stationary around a deterministic trendagainst the alternative of a unit root in panel data. Consider the followingmodel

yit = z�it� + rit + �it (13)

where zit is the deterministic component, rit is a random walk

rit = rit�1 + uit

uit ~ iid(0, 2u) and �it is a stationary process. (13) can be written as

yit = z�it� + eit (14)

where

eit =�t

j=1

uij + �it.

Let eit be the residuals from the regression in (14) and 2e be the estimate of the

error variance. Also, let Sit be the partial sum process of the residuals,

Sit =�t

j=1

eij.

Then the LM statistic is

LM =

1N�

N

i=1

1T2 �T

t=1

S2it

2e

.

17Nonstationary Panels, Cointegration in Panels and Dynamic Panels: A Survey

It can be shown that

LM→p E� W 2iZ

as T→� followed by N→� provided E[� W2iZ] < �. Also,

�N(LM � E[� W2iZ])

�Var[� W2iZ]

⇒ N(0, 1)

as T→� followed by N→�.

E. Finite Sample Properties of Unit Root Tests

Extensive simulations have been conducted to explore the finite sampleperformance of panel unit root tests, e.g. Karlsson & Löthgren (1999), Im et.al. (1997), Maddala & Wu (1999), and Choi (1999a). Choi (1999a) studied thesmall sample properties of IPS t-bar test in (7) and Fisher’s test in (11). Choi’smajor findings are the following:

(1) The empirical size of the IPS and the Fisher test are reasonably close totheir nominal size 0.05 when N is small. But the Fisher test shows mild sizedistortions at N = 100, which is expected from the asymptotic theory.Overall, the IPS t-bar test has the most stable size.

(2) In terms of the size-adjusted power, the Fisher test seems to be superior tothe IPS t-bar test.

(3) When a linear time trend is included in the model, the power of all testsdecrease considerably.

III. SPURIOUS REGRESSION IN PANEL DATA

Entorf (1997) studied spurious fixed effects regressions when the true modelinvolves independent random walks with and without drifts. Entorf found thatfor T→� and N finite, the nonsense regression phenomenon holds for spuriousfixed effects models and inference based on t-values can be highly misleading.Kao (1999) and Phillips & Moon (1999a) derived the asymptotic distributionsof the least squares dummy variable estimator and various conventionalstatistics from the spurious regression in panel data.

Consider a spurious regression model for all i using panel data:

yit = x�it� + z�it� + eit, (15)

where

18 BADI H. BALTAGI & CHIHWA KAO

xit = xit�1 + �it,

and eit is I(1). The OLS estimator of � is

� =�N

i=1�T

t=1

xit xit��1�N

i=1�T

t=1

xityit, (16)

where yit is defined in (3) and

xit = xit ��T

s=1

h(t, s)xis.

It is known that if a time-series regression for a given i is performed in model(15), the OLS estimator of � is spurious. It is easy to see that

1N�

N

i=1

1T2 �T

t=1

xit xit →p E�WiZW�iZ��

and

1N�

N

i=1

1T2 �T

t=1

xityit →p EWiZW�iZ�u�

as by a sequential limit theory, where

zit E[� WiZWiZ�]

012

112

�i

12

Ik

(�i, t)1

15Ik

Then we have

�→p��1

� ��u. (17)

(17) shows that the OLS estimator of �, �, is consistent for its true value,��1

� �u�. This is due to the fact that the noise, eit, is as strong as the signal, xit,

19Nonstationary Panels, Cointegration in Panels and Dynamic Panels: A Survey

since both eit and xit are I(1). In the panel regression (15) with a large numberof cross-sections, the strong noise of eit is attenuated by pooling the data anda consistent estimate of � can be extracted. The asymptotics of the OLSestimator are very different from those of the spurious regression in pure timeseries. This has an important consequence for residual-based cointegration testsin panel data, because the null distribution of residual-based cointegration testsdepends on the asymptotics of the OLS estimator. This point is explainedfurther in the next section.

IV. PANEL COINTEGRATION TESTS

A. Kao Tests

Kao (1999) presented two types of cointegration tests in panel data, the DF andADF types tests. The DF type tests from Kao can be calculated from theestimated residuals in (15) as:

eit = �eit�1 + vit, (18)

where

eit = yit � x�it�.

In order to test the null hypothesis of no cointegration, the null can be writtenas H0 : � = 1. The OLS estimate of � and the t-statistic are given as:

� =�N

i=1�T

t=2

eiteit�1

�N

i=1�T

t=2

e2it

and

t� =

(� � 1)��N

i=1�T

t=2

e2it�1

se

,

where s2e =

1NT�

N

i=1�T

t=2

(eit � �eit�1)2. Kao proposed the following four DF type

tests by assuming zit = {�i}:

DF� =�NT(� � 1) + 3�N

�10.2,

20 BADI H. BALTAGI & CHIHWA KAO

DFt = �1.25t� + �1.875N,

DF*� =�NT(� � 1) +

3�N2�

20�

�3 +364

�

540�

,

and

DF*t =t� +

�6N�

20�

� 20�

22�

+32

�

1020�

,

where 2� = �u � �u��

�1� and 2

0� = �u � �u����1. While DF� and DFt are based

on the strong exogeneity of the regressors and errors, DF*� and DF*t are for thecointegration with endogenous relationship between regressors and errors. Forthe ADF test, we can run the following regression:

eit = �eit�1 +�j=1

p

�j�eit� j + �itp. (19)

With the null hypothesis of no cointegration, the ADF test statistics can beconstructed as:

ADF =tADF +

�6N�

20�

� 0�2

2�2 +

3�2

100�2

where tADF is the t-statistic of � in (19). The asymptotic distributions of DF�,DFt, DF*�, DF*t, and ADF converge to a standard normal distribution N(0, 1) bythe sequential limit theory.

B. Residual Based LM Test

McCoskey & Kao (1998) derived a residual-based test for the null ofcointegration rather than the null of no cointegration in panels. This test is anextension of the LM test and the locally best invariant (LBI) test for an MA unitroot in the time series literature, see Harris & Inder (1994) and Shin (1994).Under the null, the asymptotics no longer depend on the asymptotic properties

21Nonstationary Panels, Cointegration in Panels and Dynamic Panels: A Survey

of the estimating spurious regression, rather the asymptotics of the estimationof a cointegrated relationship are needed. For models which allow thecointegrating vector to change across the cross-sectional observations, theasymptotics depend merely on the time series results as each cross-section isestimated independently. For models with common slopes, the estimation isdone jointly and therefore the asymptotic theory is based on the joint estimationof a cointegrated relationship in panel data.

For the residual based test of the null of cointegration, it is necessary to usean efficient estimation technique of cointegrated variables. In the time seriesliterature a variety of methods have been shown to be efficient asymptotically.These include the fully modified (FM) estimator of Phillips & Hansen (1990)and the dynamic least squares (DOLS) estimator as proposed by Saikkonen(1991) and Stock & Watson (1993). For panel data, Kao & Chiang (2000)showed that both the FM and DOLS methods can produce estimators which areasymptotically normally distributed with zero means.

The model presented allows for varying slopes and intercepts:

yit = �i + x�it�i + eit, (20)

xit = xit�1 + �it (21)

eit = �it + uit, (22)

and

�it = �it�1 + �uit,

where uit are i.i.d(0, u2). The null of hypothesis of cointegration is equivalent

to � = 0.The test statistic proposed by McCoskey & Kao (1998) is defined as

follows:

LM =

1N�

i=1

N1T2 �

t=1

T

Sit2

e2 , (23)

where Sit, is partial sum process of the residuals,

Sit =�j=1

t

eij

and e2 is defined in McCoskey and Kao. The asymptotic result for the test is:

�N(LM � ��) ⇒ N(0, �2). (24)

22 BADI H. BALTAGI & CHIHWA KAO

The moments, �� and �2, can be found through Monte Carlo simulation. The

limiting distribution of LM is then free of nuisance parameters and robust toheteroskedasticity.

Urban economists have long sought to explain the relationship betweenurbanization levels and output. McCoskey & Kao (1999a) revisited thisquestion and test the long run stability of a production function includingurbanization using nonstationary panel data techniques. McCoskey and Kaoapplied the IPS test and LM in (23) and showed that a long run relationshipbetween urbanization, output per worker and capital per worker cannot berejected for the sample of thirty developing countries or the sample of twenty-two developed countries over the period 1965–1989. They do find, however,that the sign and magnitude of the impact of urbanization varies considerablyacross the countries. These results offer new insights and potential for dynamicurban models rather than the simple cross-section approach.

C. Pedroni Tests

Pedroni (1997a) also proposed several tests for the null hypothesis of nocointegration in a panel data model that allows for considerable heterogeneity.His tests can be classified into two categories. The first set is similar to the testsdiscussed above, and involve averaging test statistics for cointegration in thetime series across cross-sections. The second set group the statistics such thatinstead of averaging across statistics, the averaging is done in pieces so that thelimiting distributions are based on limits of piecewise numerator anddenominator terms.

The first set of statistics as discussed includes a form of the average of thePhillips & Ouliaris (1990) statistic:

Z� =�i=1

N �t=1

T

(eit�1�eit � �i)

��t=1

T

eit�12 �

, (25)

where eit is estimated from (15), and �i =12

(i2 � si

2), for which i2 and si

2 are

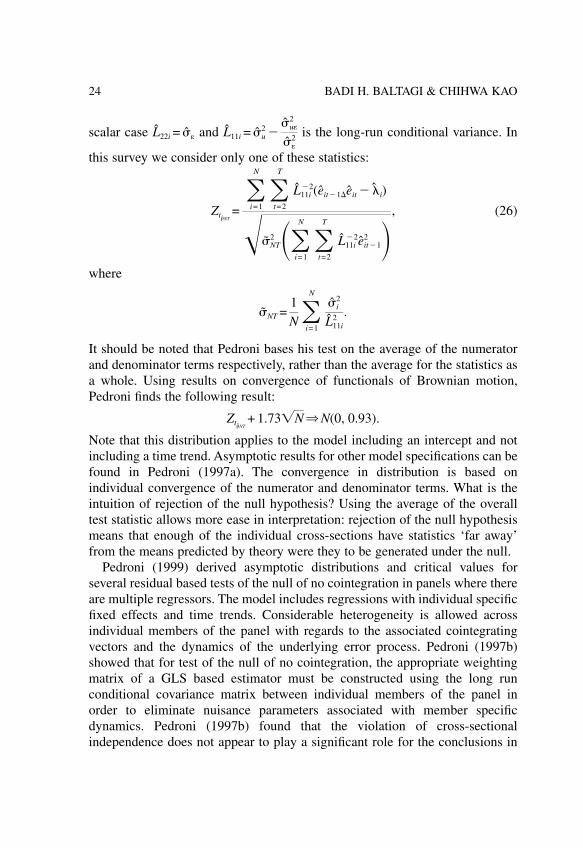

individual long-run and contemporaneous variances respectively of the residualeit. For his second set of statistics, Pedroni defines four panel test statistics. Let�i be a consistent estimate of �i, the long-run variance-covariance matrix.Define Li to be the lower triangular Cholesky composition of �i such that in the

23Nonstationary Panels, Cointegration in Panels and Dynamic Panels: A Survey

scalar case L22i = � and L11i = u2 �

u�2

�2 is the long-run conditional variance. In

this survey we consider only one of these statistics:

Zt�NT=�i=1

N �t=2

T

L11i�2(eit�1�eit � �i)

�NT2 ��

i=1

N �t=2

T

L11i�2eit�1

2 �, (26)

where

NT =1N�

i=1

Ni

2

L11i2 .

It should be noted that Pedroni bases his test on the average of the numeratorand denominator terms respectively, rather than the average for the statistics asa whole. Using results on convergence of functionals of Brownian motion,Pedroni finds the following result:

Zt�NT+ 1.73�N ⇒ N(0, 0.93).

Note that this distribution applies to the model including an intercept and notincluding a time trend. Asymptotic results for other model specifications can befound in Pedroni (1997a). The convergence in distribution is based onindividual convergence of the numerator and denominator terms. What is theintuition of rejection of the null hypothesis? Using the average of the overalltest statistic allows more ease in interpretation: rejection of the null hypothesismeans that enough of the individual cross-sections have statistics ‘far away’from the means predicted by theory were they to be generated under the null.

Pedroni (1999) derived asymptotic distributions and critical values forseveral residual based tests of the null of no cointegration in panels where thereare multiple regressors. The model includes regressions with individual specificfixed effects and time trends. Considerable heterogeneity is allowed acrossindividual members of the panel with regards to the associated cointegratingvectors and the dynamics of the underlying error process. Pedroni (1997b)showed that for test of the null of no cointegration, the appropriate weightingmatrix of a GLS based estimator must be constructed using the long runconditional covariance matrix between individual members of the panel inorder to eliminate nuisance parameters associated with member specificdynamics. Pedroni (1997b) found that the violation of cross-sectionalindependence does not appear to play a significant role for the conclusions in

24 BADI H. BALTAGI & CHIHWA KAO

favor of weak long run PPP provided that one also includes common timedummies in the regression. Pedroni (2000) also demonstrated how it is possibleto construct a test that can be employed to test whether or not members of apanel with heterogeneous short run dynamics converge to a single commonsteady state.

D. Likelihood-Based Cointegration Test

Larsson, Lyhagen & Löthgren (1998) presented a likelihood-based (LR) paneltest of cointegrating rank in heterogeneous panel models based on the averageof the individual rank trace statistics developed by Johansen (1995). Theproposed LR-bar statistic is very similar to the IPS t-bar statistic in (7) through(10). In Monte Carlo simulation, Larsson et al. investigated the small sampleproperties of the standardized LR-bar statistic. They found that the proposedtest requires a large time series dimension. Even if the panel has a large cross-sectional dimension, the size of the test will be severely distorted.

Groen & Kleibergen (1999) proposed a likelihood-based framework forcointegrating analysis in panels of a fixed number of vector error correctionmodels. Maximum likelihood estimators of the cointegrating vectors areconstructed using iterated generalized method of moments (GMM) estimators.Using these estimators Groen and Kleibergen construct likelihood ratiostatistics, LR(�B|�A), to test for a common cointegration rank across theindividual vector error correction models, both with heterogeneous andhomogeneous cointegrating vectors. Interestingly, the limiting distribution ofLR(�B|�A) is invariant to the covariance matrix of the error terms whichimplies that LR(�B|�A) is robust with respect to the choices of covariancematrix. Let us define the LRs(r|k) as the summation of the N individual tracestatistics

LRs(r | k) =�i=1

N

LRi(r | k) (27)

where LRi(r | k) is the i-th Johansen’s likelihood ratio statistic, so that

LRi(r | k) ⇒ tr�� dBk�r, iB�k�r, i � dBk�r, iB�k�r, i� dBk�r, iB�k�r, i�as T→�. Now for a fixed N, it is clear that

25Nonstationary Panels, Cointegration in Panels and Dynamic Panels: A Survey

LRs(r | k) =�i=1

N

LRi(r | k)

⇒�i=1

N

tr�� dBk�r, iB�k�r, i � dBk�r, iB�k�r, i� dBk�r, iB�k�r, i�(28)

as T→� by a continuous mapping theorem. It follows that LRs(r | k) isasymptotically equivalent to LR(�B | �A) when N is fixed and T is large. Thismeans that nothing is lost by assuming that the covariance matrix has zero non-diagonal covariances as far as the asymptotics are concerned for the proposedtest statistics in this chapter. More importantly, the tests based on the cross-independence like (27) will perform just as well (asymptotically) as the testsbased on the cross-dependence such as LR(�B | �A). Groen and Kleibergenverified that the likelihood-based cointegration tests proposed by Larsson et al.in (27) are robust with respect to the cross-dependence in panel data. The(asymptotic) equivalence of LRs(r | k) and LR(�B | �A) found in Groen andKleibergen has profound implications to econometricians and applied econo-mists, e.g. there exists tests/estimators based on the cross-independencewhich are equivalent to tests/estimators based on the cross-dependence innonstationary panel time series. Define LR(r | k) to be the average of LRi(r | k):

LR(r | k) =1N

LRs(r | k) =1N�

i=1

N

LRi(r | k).

It can be shown that

LR(r | k) � E[LR(r | k)]

Var[LR(r | k)]⇒ N(0, 1)

as T→� followed by N→� by a continuous mapping theorem and a centrallimit theorem provided E[LR(r | k)] and Var[LR(r | k)] are bounded. Define

LR(�B | �A) =1N

LR(�B | �A). (29)

For a fixed N, it is easy to show that

26 BADI H. BALTAGI & CHIHWA KAO

LR(�B | �A) =1N

LR(�B | �A)

⇒ 1N�

i=1

N

tr�� dBk�r, iB�k�r, i� dBk�r, iB�k�r, i�� dBk�r, iB�k�r, i�

=1N�

i=1

N

Zki

where

Zki = tr�� dBk�r, iB�k�r, i� dBk�r, iB�k�r, i� dBk�r, iB�k�r, i�as T→�. Then

1N�

i=1

N

Zki � E1N�

i=1

N

ZkiVar1

N�i=1

N

Zki ⇒ N(0, 1)

as N→� since Bk�r, i and Bk�r, j are independent for i ≠ j. It implies that

LR(�B | �A) � E[LR(�B | �A)]

Var[LR(�B | �A)]⇒ N(0, 1)

as T→� followed by N→�. The above discussion indicates that LR(r | k) andLR(�B | �A) are also equivalent when T and N are large.

Groen & Kleibergen (1999) applied LR(�B | �A) to a data set of exchangerates and appropriate monetary fundamentals. They found strong evidence forthe validity of the monetary exchange rate model within a panel of vectorcorrection models for three major European countries, whereas the resultsbased on individual vector error correction models for each of these countriesseparately are less supportive.

E. Finite Sample Properties

McCoskey & Kao (1999b) conducted Monte Carlo experiments to compare thesize and power of different residual based tests for cointegration in

27Nonstationary Panels, Cointegration in Panels and Dynamic Panels: A Survey

heterogeneous panel data: varying slopes and varying intercepts. Two of thetests are constructed under the null hypothesis of no cointegration. These testsare based on the average ADF test and Pedroni’s pooled tests in (25) and (26).The third test is based on the null hypothesis of cointegration which is basedon the McCoskey & Kao LM test in (23). Wu & Yin (1999) performed a similarcomparison for panel tests in which they consider only tests for which the nullhypothesis is that of no cointegration. Wu & Yin compared ADF statistics withmaximum eigenvalue statistics in pooling information on means and p-valuesrespectively. They found that the average ADF performs better with respect topower and their maximum eigenvalue based p-value performs better withregards to size.

The test of the null hypothesis was originally proposed in response to the lowpower of the tests of the null of no cointegration, especially in the time seriescase. Further, in cases where economic theory predicted a long run steady staterelationship, it seemed that a test of the null of cointegration rather than the nullof no cointegration would be appropriate. The results from the Monte Carlostudy showed that the McCoskey & Kao LM test outperforms the other twotests.

Of the two reasons for the introduction of the test of the null hypothesis ofcointegration, low power and attractiveness of the null, the introduction of thecross-section dimension of the panel solves one: all of the tests show decentpower when used with panel data. For those applications where the null ofcointegration is more logical than the null of no cointegration, McCoskey &Kao (1999b), at a minimum, conclude that using the McCoskey & Kao LM testdoes not compromise the ability of the researcher in determining the underlyingnature of the data.

Recently, Hall et al. (1999) proposed a new approach based on principalcomponents analysis to test for the number of common stochastic trendsdriving the nonstationary series in a panel data set. The test is consistent evenif there is a mixture of I(0) and I(1) series in the sample. This makes itunnecessary to pretest the panel for unit root. It also has the advantage ofsolving the problem of dimensionality encountered in large panel data sets.

V. ESTIMATION AND INFERENCE IN PANELCOINTEGRATION MODELS

This section discusses the issues that arise in estimation and inference ofcointegrated panel regression models. The asymptotic properties of theestimators of the regression coefficients and the associated statistical tests aredifferent from those of the time series cointegration regression models. Some

28 BADI H. BALTAGI & CHIHWA KAO

of these differences have become apparent in recent works by Kao & Chiang(2000), Phillips & Moon (1999a) and Pedroni (1996). The panel cointegrationmodels are directed at studying questions that surround long run economicrelationships typically encountered in macroeconomic and financial data. Sucha long run relationship is often predicted by economic theory and it is then ofcentral interest to estimate the regression coefficients and test whether theysatisfy theoretical restrictions. Kao & Chen (1995) showed that the OLS inpanel cointegrated models is asymptotically normal but still asymptoticallybiased. Chen, McCoskey & Kao (1999) investigated the finite sampleproprieties of the OLS estimator, the t-statistic, the bias-corrected OLSestimator, and the bias-corrected t-statistic. They found that the bias-correctedOLS estimator does not improve over the OLS estimator in general. The resultsof Chen et al. suggested that alternatives, such as the fully modified (FM)estimator or dynamic OLS (DOLS) estimator may be more promising incointegrated panel regressions. Phillips & Moon (1999a) and Pedroni (1996)proposed a FM estimator, which can be seen as a generalization of Phillips &Hansen (1990). In this volume, Kao & Chiang (2000) propose an alternativeapproach based on a panel dynamic least squares (DOLS) estimator, whichbuilds upon the work of Saikkonen (1991) and Stock & Watson (1993).

Next, we provide a brief discussion of the OLS estimation methods in apanel cointegrated model. Consider the following panel regression:

yit = x�it� + z�it�i + uit, (30)

where {yit} are 1 � 1, � is a k � 1 vector of the slope parameters, zit is thedeterministic component, and {uit} are the stationary disturbance terms. Weassume that {xit} are k � 1 integrated processes of order one for all i, where

xit = xit�1 + �it.

Under these specifications, (30) describes a system of cointegrated regressions,i.e. yit is cointegrated with xit. The OLS estimator of � is

�OLS =�i=1

N �t=1

T

xit x�it�1�i=1

N �t=1

T

xityit. (31)

It is easy to show that

1N�

i=1

N1T2 �

t=1

T

xit x�it →p limN→�

1N�

i=1

N

E[�2i], (32)

and

29Nonstationary Panels, Cointegration in Panels and Dynamic Panels: A Survey

1N�

i=1

N1T�

t=1

T

xituit ⇒ limN→�

1N�

i=1

N

E[�1i] (33)

using sequential limit theory, where

zit E[�1i] E[�2i]

0 012

1 0 0

�i �12

��ui + ��ui

16

��i

(�i, t) �12

��ui + ��ui

115

��i

and

�i =�ui

��ui

�u�i

��i

is the long-run covariance matrix of (uit, ��it)�, also �i =�ui

��ui

�u�i

��i is the one-

sided long-run covariance. For example, when zit = {�i}, we get

�NT(�OLS � �) � �N�NT ⇒ N�0, 6��1� � lim

N → �

1N�

N

i=1

�u.����i���1� �,

where �� = limN ⇒ �

1N�

N

i=1

��i and

�NT =1N�

N

i=1

1T2 �T

t=1

(xit � xi)(xit � xi)��1

�1N �

N

i=1

�1/2�i �� Wi dW�i���1/2

�i ��ui + ��ui.

Kao & Chiang (2000) in this volume studied the limiting distributions for theFM, and DOLS estimators in a cointegrated regression and showed they are

30 BADI H. BALTAGI & CHIHWA KAO

asymptotically normal. Phillips & Moon (1999a) and Pedroni (1996) alsoobtained similar results for the FM estimator. The reader is referred to the citedpapers for further details. Kao and Chiang also investigated the finite sampleproperties of the OLS, FM, and DOLS estimators. They found that: (i) the OLSestimator has a non-negligible bias in finite samples, (ii) the FM estimator doesnot improve over the OLS estimator in general, and (iii) the DOLS estimatormay be more promising than OLS or FM estimators in estimating thecointegrated panel regressions.

Choi (1999b) extended Kao & Chiang (2000) to study asymptotic propertiesof OLS, Within and GLS estimators for an error component model. The errorcomponent model involves both stationary and nonstationary regressors. Choi’ssimulation results indicated that the feasible GLS estimator is more efficientthan the Within estimator. Choi (1999c) studied instrumental variableestimation for an error component model with stationary and nearlynonstationary regressors.

Phillips & Moon (1999a) studied various regressions between two panelvectors that may or may not have cointegrating relations, and present afundamental framework for studying sequential and joint limit theories innonstationary panel data. In particular, Phillips and Moon studied regressionlimit theory of nonstationary panels when both N and T go to infinity. Theirlimit theory allows for both sequential limits, where T→� followed by N→�and joint limits, where T, N→� simultaneously. Phillips and Moon require thatN/T→0, so that these results apply for moderate N and large T macro paneldata and not large N and small T micro panel data. The panel modelsconsidered allow for four cases: (i) panel spurious regression, where there is notime series cointegration, (ii) heterogeneous panel cointegration, where eachindividual has its own specific cointegration relation, (iii) homogeneous panelcointegration where individuals have the same cointegration relation, and (iv)near-homogeneous panel cointegration, where individuals have slightlydifferent cointegration relations determined by the value of a localizingparameter. Phillips & Moon (1999a) investigated these four models anddeveloped panel asymptotics for regression coefficients and tests using bothsequential and joint limit arguments. In all cases considered the pooledestimator is consistent and has a normal limiting distribution. In fact, for thespurious panel regression, Phillips & Moon (1999a) showed that under quiteweak regularity conditions, the pooled least squares estimator of the slopecoefficient � is �N consistent for the long-run average relation parameter �and has a limiting normal distribution. Also, Moon & Phillips (1998a) showedthat a limiting cross-section regression with time averaged data is also �Nconsistent for � and has a limiting normal distribution. This is different from

31Nonstationary Panels, Cointegration in Panels and Dynamic Panels: A Survey

the pure time series spurious regression where the limit of the OLS estimatorof � is a nondegenerate random variate that is a functional of Brownianmotions and is therefore not consistent for �. The idea in Phillips & Moon(1999a) is that independent cross-section data in the panel adds informationand this leads to a stronger overall signal than the pure time series case. Pesaran& Smith (1995) studied limiting cross-section regressions with time averageddata and established consistency with restrictive assumptions on the heteroge-neous panel model. This differs from Phillips & Moon (1999a) in that theformer use an average of the cointegrating coefficients which is different fromthe long run average regression coefficient. This requires the existence ofcointegrating time series relations, whereas the long run average regressioncoefficient � is defined irrespective of the existence of individual cointegratingrelations and relies only on the long run average variance matrix of the panel.Phillips & Moon (1999a) also showed that for the homogeneous and nearhomogeneous cointegration cases, a consistent estimator of the long runregression coefficient can be constructed which they call a pooled FMestimator. They showed that this estimator has faster convergence rate than thesimple cross-section and time series estimators. See also Phillips & Moon(1999b) for a concise review. In fact, the latter paper also shows how to extendthe above ideas to models with individual effects in the data generating process.For the panel spurious regression with individual specific deterministic trends,estimates of the trend coefficients are obtained in the first step and thedetrended data is pooled and used in least squares regression to estimate � inthe second step. Two different detrending procedures are used based on OLSand GLS regressions. OLS detrending leads to an asymptotically more efficientestimator of the long run average coefficient � in pooled regression than GLSdetrending. Phillips & Moon (1999b) explain that ‘‘the residuals after timeseries GLS detrending have more cross section variation than they do after OLSdetrending and this produces great variation in the limit distribution of thepooled regression estimator of the long run average coefficient.”

Moon & Phillips (1999) investigate the asymptotic properties of theGaussian MLE of the localizing parameter in local to unity dynamic panelregression models with deterministic and stochastic trends. Moon and Phillipsfind that for the homogeneous trend model, the Gaussian MLE of the commonlocalizing parameter is �N consistent, while for the heterogeneous trendsmodel, it is inconsistent. The latter inconsistency is due to the presence of aninfinite number of incidental parameters (as N→�) for the individual trends.Unlike the fixed effects dynamic panel data model where this inconsistency dueto the incidental parameter problem disappears as T→�, the inconsistency of

32 BADI H. BALTAGI & CHIHWA KAO

the localizing parameter in the Moon and Phillips model persists even whenboth N and T go to infinity.

Pesaran, Shin & Smith (1999) derived the asymptotics of a pooled meangroup (PMG) estimator. The PMG estimation constrains the long runcoefficients to be identical, but allow the short run and adjustment coefficientsas the error variances to differ across the cross-sectional dimension.

Recently, Binder, Hsiao & Pesaran (2000) considered estimation andinference in panel vector autoregressions (PVARS) with fixed effects when T isfinite and N is large. A maximum likelihood estimator as well as unit root andcointegration tests are proposed based on a transformed likelihood function.This MLE is shown to be consistent and asymptotically normally distributedirrespective of the unit root and cointegrating properties of the PVAR model.The tests proposed are based on standard chi-square and normal distributedstatistics. Binder et al. also show that the conventional GMM estimators basedon standard orthogonality conditions break down if the underlying time seriescontain unit roots. Monte Carlo evidence is provided which favors MLE overGMM in small samples.

In this volume, Kauppi (2000) develops a new joint limit theory where thepanel data may be cross-sectionally heterogeneous in a general way. This limittheory builds upon the concepts of joint convergence in probability and indistribution for double indexed processes by Phillips & Moon (1999a) anddevelops new versions of the law of large numbers and the central limittheorem that apply in panels where the data may be cross-sectionallyheterogeneous in a fairly general way. Kauppi demonstrates how this joint limittheory can be applied to derive asymptotics for a panel regression where theregressors are generated by a local to unit root with heterogeneous localizingcoefficients across cross-sections. Kauppi discusses issues that arise in theestimation and inference of panel cointegrated regressions with near integratedregressors. Kauppi shows that a bias corrected pooled OLS for a commoncointegrating parameter has an asymptotic normal distribution centered on thetrue value irrespective of whether the regressor has near or exact unit root.However, if the regression model contains individual effects and/or determi-nistic trends, then Kauppi’s bias corrected pooled OLS still producesasymptotic bias. Kauppi also shows that the panel FM estimator is subject toasymptotic bias regardless of how individual effects and/or deterministic trendsare contained if the regressors are nearly rather than exacly integrated. Thisindicates that much care should be taken in interpreting empirical resultsachieved by the recent panel cointegration methods that assume exact unit rootswhen near unit roots are equally plausible.

33Nonstationary Panels, Cointegration in Panels and Dynamic Panels: A Survey

Kao et al. (1999) apply the asymptotic theory of panel cointegrationdeveloped by Kao & Chiang (2000) to the Coe & Helpman (1995) internationalR&D spillover regression. Using a sample of 21 OECD countries and Israel,they re-examine the effects of domestic and foreign R&D capital stocks on totalfactor productivity of these countries. They find that OLS with bias-correction,the fully modified (FM) and the dynamic OLS (DOLS) estimators producedifferent predictions about the impact of foreign R&D on total factorproductivity (TFP). However, all the estimators support the result that domesticR&D is related to TFP. Kao et al.’s empirical results indicate that the estimatedcoefficients in the Coe and Helpman’s regressions are subject to estimationbias. Given the superiority of the DOLS over FM as suggested by Kao &Chiang (2000), Kao et al. leaned towards rejecting the Coe and Helpmanhypothesis that international R&D spillovers are trade related.

Funk (1998) examined the relationship between trade patterns andinternational R&D spillovers among the OECD countries using the panelcointegration methods developed by Kao (1999), Kao & Chiang (2000), andPesaran, Shin & Smith (1999). Using randomly simulated bilateral tradepatterns, Funk found that the choice of weights used in constructing foreignR&D stocks is informative of the avenue of spillover transmission when panelcointegration methods are employed. A re-examination of the relationshipbetween import patterns and R&D spillovers found no evidence to link thepatterns of R&D spillovers to the patterns of imports. Funk found strongevidence indicating that exporters receive substantial R&D spillovers fromtheir customers.

VI. DYNAMIC PANEL DATA MODELS

This section surveys recent developments in dynamic panel data models. Thedynamic panel data regression is characterized by two sources of persistenceover time. Autocorrelation due to the presence of a lagged dependent variableamong the regressors and individual effects characterizing the heterogeneityamong the individuals

yit = �yi, t�1 + x�it� + �i + uit (34)

for i = 1, 2, . . . , N; and t = 1, 2, . . . , T. � is a scalar, xit is k � 1, �i denotes thei-th individuals effect and uit is the remainder disturbance. Basic introductionsto this topic are found in Hsiao (1986), Baltagi (1995) and Matyas & Sevestre(1996). Applications using this model are too many to enumerate. Theseinclude employment equations, see Arellano & Bond (1991), liquor demand,see Baltagi & Griffin (1995), growth convergence, see Islam (1995) and

34 BADI H. BALTAGI & CHIHWA KAO

Nerlove (1999), life cycle labor supply models, see Ziliak (1997), and demandfor gasoline, see Baltagi & Griffin (1997) to mention a few.

It is well known that for typical micro-panels where there are a large numberof firms or individuals (N) observed over a short period of time (T), the fixedeffects (FE) estimator is biased and inconsistent (since T is fixed and N→�),see Nickell (1981) and more recently Kiviet (1995, 1999). Monte Carlo resultshave shown that first order asymptotic properties do not necessarily yieldcorrect inference in finite samples. Therefore, Kiviet (1995) examined higherorder asymptotics which may approximate the actual finite sample propertiesmore closely and lead to better inference. In fact, Kiviet (1995) considered thesimple dynamic linear panel data model with serially uncorrelated disturbancesand strongly exogenous regressors and derived an approximation for the bias ofthe FE estimator. When a consistent estimator of this bias is subtracted from theoriginal FE estimator, a corrected FE estimator results. This corrected FEestimator performed well in simulations when compared with eight otherconsistent instrumental variable or GMM estimators.4

In macro-panels studying for example long run growth, the data covers alarge number of countries N over a moderate size T. In this case, T is not verysmall relative to N. Hence, some researchers may still favor the FE estimatorarguing that its bias may not be large. Judson & Owen (1999) performed someMonte Carlo experiments for N = 20 or 100 and T = 5, 10, 20 and 30 and foundthat the bias in the FE can be sizeable, even when T = 30. The bias of the FEestimator increases with � and decreases with T. But even for T = 30, this biascould be as much as 20% of the true value of the coefficient of interest. Judson& Owen (1999) recommend the corrected FE estimator proposed by Kiviet(1995) as the best choice, GMM being second best and for long panels, thecomputationally simpler Anderson & Hsiao (1982) estimator. This lastestimator first differences the data to get rid of the individual effects and thenuses lagged predetermined variables in levels as instruments.5 Arellano & Bond(1991) proposed GMM procedures that are more efficient than the Anderson &Hsiao (1982) estimator. Ahn & Schmidt (1995) derive additional nonlinearmoment restrictions not exploited by the Arellano & Bond (1991) GMMestimator.6 Ahn & Schmidt (1995, 1997) also give a complete count of the setof orthogonality conditions corresponding to a variety of assumptions imposedon the disturbances and the initial conditions of the dynamic panel data model.While many of the moment conditions are nonlinear in the parameters, Ahn &Schmidt (1997) propose a linearized GMM estimator that is asymptotically asefficient as the nonlinear GMM estimator. They also provide simple momenttests of the validity of these nonlinear restrictions. In addition, they investigatethe circumstances under which the optimal GMM estimator is equivalent to a

35Nonstationary Panels, Cointegration in Panels and Dynamic Panels: A Survey

linear instrumental variable estimator. They find that these circumstances arequite restrictive and go beyond uncorrelatedness and homoskedasticity of theerrors. Ahn & Schmidt (1995) provide some evidence on the efficiency gainsfrom the nonlinear moment conditions which provide support for their use inpractice. By employing all these conditions, the resulting GMM estimator isasymptotically efficient and has the same asymptotic variance as the MLEunder normality. In fact, Hahn (1997) showed that GMM based on anincreasing set of instruments as N→� would achieve the semiparametricefficiency bound.

Hahn (1997) considers the asymptotic efficient estimation of the dynamicpanel data model with sequential moment restrictions in an environment withi.i.d. observations. Hahn (1997) shows that the GMM estimator with anincreasing set of instruments as the sample size grows attains the semipara-metric efficiency bound of the model. Hahn (1997) explains how Fourier seriesor polynomials may be used as the set of instruments for efficient estimation.In a limited Monte Carlo comparison, Hahn finds that this estimator has similarfinite sample properties as the Keane & Runkle (1992) and/or Schmidt et al.(1992) estimators when the latter estimators are efficient. In cases where thelatter estimators are not efficient, the Hahn efficient estimator outperforms bothestimators in finite samples.

Recently, Wansbeek & Bekker (1996) considered a simple dynamic paneldata model with no exogenous regressors and disturbances uit and randomeffects �i that are independent and normally distributed. They derived anexpression for the optimal instrumental variable estimator, i.e. one withminimal asymptotic variance. A striking result is the difference in efficiencybetween the IV and ML estimators. They find that for regions of theautoregressive parameter � which are likely in practice, ML is superior. Thegap between IV (or GMM) and ML can be narrowed down by adding momentrestrictions of the type considered by Ahn & Schmidt (1995). Hence, Wansbeek& Bekker (1996) find support for adding these nonlinear moment restrictionsand warn against the loss in efficiency as compared with MLE by ignoringthem.

Blundell & Bond (1998) revisit the importance of exploiting the initialcondition in generating efficient estimators of the dynamic panel data modelwhen T is small. They consider a simple autoregressive panel data model withno exogenous regressors

yit = �yi, t�1 + �i + uit (35)

with E(�i) = 0; E(uit) = 0; and E(�iuit) = 0 for i = 1, 2, . . . , N; t = 1, 2, . . . , T.Blundell & Bond (1998) focus on the case where T = 3 and therefore there is

36 BADI H. BALTAGI & CHIHWA KAO

only one orthogonality condition given by E(yi1�ui3) = 0, so that � is just-identified. In this case, the first stage IV regression is obtained by running �yi2

on yi1. Note that this regression can be obtained from (2) evaluated at t = 2 bysubtracting yi1 from both sides of this equation, i.e.

�yi2 = (� � 1)yi, 1 + �i + ui2 (36)

Since we expect E(yi1�i) > 0, (� � 1) will be biased upwards with

plim(� � 1) = (� � 1)c

c + (�2 /u

2)(37)

where c = (1 � �)/(1 + �). The bias term effectively scales the estimatedcoefficient on the instrumental variable yi1 towards zero. They also find that theF-statistic of the first stage IV regression converges to 1

2 with noncentralityparameter

� =(u

2c)2

�2 + u

2c→0 as �→1 (37)

As �→0, the instrumental variable estimator performs poorly. Hence, Blundelland Bond attribute the bias and the poor precision of the first difference GMMestimator due to the problem of weak instruments described in Nelson & Startz(1990) and Staiger & Stock (1997) and characterize this weak IV by itsconcentration parameter �.

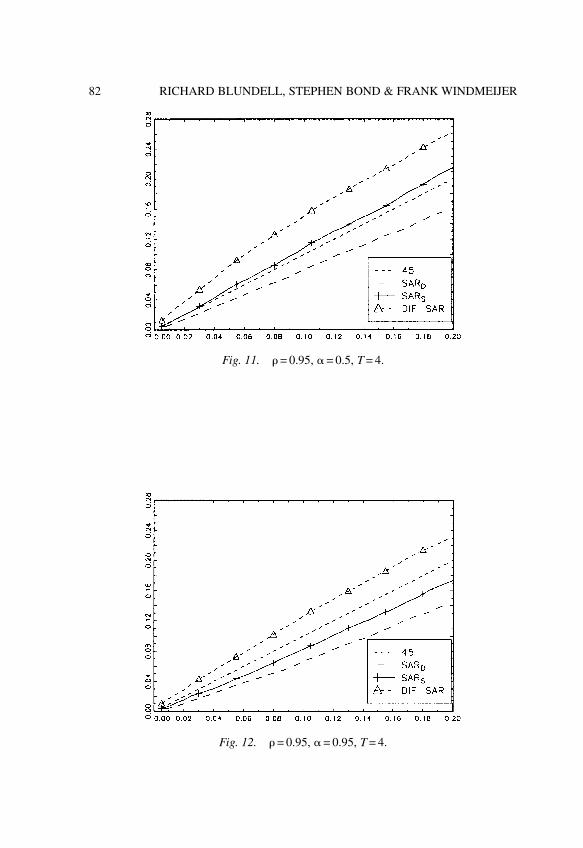

Next, Blundell & Bond (1998) show that an additional mild stationarityrestriction on the initial conditions process allows the use of an extendedsystem GMM estimator that uses lagged differences of yit as instruments forequations in levels, in addition to lagged levels of yit as instruments forequations in first differences, see Arellano & Bover (1995). The system GMMestimator is shown to have dramatic efficiency gains over the basic firstdifference GMM as �→1 and (�

2 /u2) increases. In fact, for T = 4 and (�

2 /u

2) = 1, the asymptotic variance ratio of the first difference GMM estimator tothis system GMM estimator is 1.75 for � = 0 and increases to 3.26 for � = 0.5and 55.4 for � = 0.9. This clearly demonstrates that the levels restrictionssuggested by Arellano & Bover (1995) remain informative in cases where firstdifferenced instruments become weak. Things improve for first differenceGMM as T increases. However, with short T and persistent series, the Blundelland Bond findings support the use of the extra moment conditions. Theseresults are reviewed and corroborated in Blundell, Bond & Windmeijer (2000)in this volume, using Monte Carlo experiments as well as an empiricalexample. In fact, simulations that include the weakly exogenous covariates findlarge finite sample bias and very low precision for the standard first differenced

37Nonstationary Panels, Cointegration in Panels and Dynamic Panels: A Survey