advanced manufacturing: ohio iron and steel industry

TRANSCRIPT

Research Office A State Affiliate of the U.S. Census Bureau

Advanced Manufacturing: Ohio Iron and Steel Industry

December, 2017

Inside front cover

ADVANCED MANUFACTURING: The Ohio Iron and Steel Industry

December 2017

B1001 Don Larrick, Principal Analyst Office of Research, Ohio Development Services Agency

P.O. Box 1001, Columbus, Oh. 43216-1001 Production Support: Steve Kelley, Editor; Robert Schmidley, GIS Specialist

TABLE OF CONTENTS Page Executive Summary 1 Description of Ohio’s Iron and Steel Industry - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - 3 Notable Iron and Steel Industry Manufacturers 5 Globalization and Foreign Investment in Ohio - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - 8 Recent Expansion and Attraction Announcements 11 Iron and Steel Industry Concentration in Ohio - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - 13 The Composition of Ohio’s Iron and Steel Industry: Employment 15 Industry Pay- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - 17 The Distribution of Industry Establishments in Ohio 19 The Distribution of Industry Employment in Ohio - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - 21 Trends 23 Raw Steel Production - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - 25 Production as Measured by Value-Added 29 Capital Expenditures- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - 31 Establishments 33 Employment- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - 35

i

Exports from Ohio 37 Notes on U.S. Imports and Exports - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - 39 Overview and Outlooks 41 An Overview of the Industry - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - 42 The Near- and Long-Term Outlooks 47 Appendices- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - 50

Detailed Tables 51

Table A1: Notable Iron and Steel Manufacturing Companies in Ohio, 2017 52 Table A2: Expansion and Attraction Announcements in Ohio’s Iron and Steel Industry, 2013-2016 54 Table A3: Iron and Steel Industry Concentration in Ohio 55 Table A4: Establishments and Employment in the Iron and Steel Industry, Ohio and U.S., 2015 56 Table A5: Employment and Pay in the Iron and Steel Industry, Ohio and U.S., 2015 57 Table A6: Establishments and Employment in Ohio’s Iron and Steel Industry, by County, 2015 58 Table A7: Raw Steel Production in Ohio and the U.S., 1971-2016 59 Table A8: Trends in Value-Added for Ohio and the U.S., 2005-2015 60 Table A9: Trends in Capital Expenditures for Ohio and the U.S., 2005-2015 61 Table A10: Detailed Iron and Steel Industry Establishment Trends in Ohio and the U.S., 2005-2015 62 Table A11: Detailed Iron and Steel Industry Employment Trends in Ohio and the U.S., 2005-2015 63 Table A12: Trends in Exports from Ohio 64 Table A13: U.S. Imports and Exports of Steel Mill Products and Derived Statistics, 1995-2016 65 Table A14: Projections for Iron and Steel Industry Employment, Ohio and the U.S., 2014-2024 66

Industry Definition and Examples of Products 67

Glossary - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - 69 A Primer on Iron and Steel Production Processes 72

ii

Notes- - - - - - - - - - - - - - - - - - - - -- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - 73 Sources and References Cited 78

iii

EXECUTIVE SUMMARY • Ohio ranked second in the nation in raw steel production every year of the last decade, annually pouring anywhere

from 6.6 to 16.1 million tons, or 10.1 to 14.9 percent of total U.S. output. • Ohio ranked third in the encompassing iron, steel and ferroalloy products group (NAICS 3311, which includes products

made at the mills), second in manufacturing products made from purchased steel (3312), and third in the combination of the two groups – as judged by dollar value-add in the latest Annual Survey of Manufactures by the Census Bureau.

• 11 companies on Fortune magazine’s U.S.-1,000 or Global- 500 lists have iron and steel industry establishments in

Ohio; two of them – AK Steel and Worthington Industries – maintain their world headquarters here, and ArcelorMittal [sic], the world’s largest steel company, has a regional headquarters here.

• ArcelorMittal can pour at least 3.8 million tons of raw steel per year in Ohio. It is followed by AK Steel with a minimum

of 3.5 million, Republic Steel at nearly 2.4 million, North Star BlueScope [sic] at close to 2.2 million and TimkenSteel [sic] at over 1.5 million. Total capacity in Ohio is at least 14.7 million tons per year.

• 180 industry establishments employed 25,821 people in Ohio according to the latest County Business Patterns data.

53 counties had at least one iron and steel industry establishment, with the majority in 10 counties: Columbiana, Cuya-hoga, Franklin, Mahoning, Montgomery, Richland, Stark, Summit, Trumbull and Washington; three-fifths of the jobs were found in an overlapping list of seven counties: Butler, Cuyahoga, Defiance, Franklin, Lorain, Richland and Stark.

• AK is the largest industry employer in Ohio at about 3,300, followed by ArcelorMittal with well over 2,500 and Timken-

Steel with an estimated 1,900-plus; General Motors is the largest foundry operation with at least 1,100. • 17 companies announced 20 major iron and steel industry investments in Ohio from 2013 through 2016. Planned ex-

penditures were nearly $252 million, with close to 280 new jobs anticipated when the projects are completed.

• International investment is very important, with 15 companies from 12 foreign nations employing close to 5,500 in Ohio making iron, steel, ferroalloy and foundry products; two of them are on Fortune’s Global-500 list. ArcelorMittal, Indus-trias CH SAB de CV (which owns Republic Steel) and Vallourec SA are the largest employers.

• People working in Ohio’s iron and steel industry averaged $65,700 in annual pay – about $2,600 more than the corre-

sponding national average – according to the latest County Business Patterns data from the Census Bureau.

1

This page intentionally blank

2

DESCRIPTION OF OHIO’S IRON AND STEEL INDUSTRY

3

!

!

!

!! !

!

!

!

!

!

!

!

!!

Ross

Stark

Pike

Wood

Darke

Knox

Licking

SciotoAdamsGallia

Wayne

Perry

Clark

Huron

Allen

Butler

Lorain

Seneca

Logan

Brown

Athens

Union

Trumbull

Meigs

Ashtabula

Hardin

Henry

Franklin

PrebleNoble

Mercer

Portage

Fulton

Miami

Erie

Belmont

Hancock

Vinton

Fairfield

Putnam

Highland

Lucas

Carroll

Shelby

Richland

Monroe

Clinton

Greene

Muskingum

Fayette

Marion

Medina

Warren

Holmes

Pickaway

Guernsey

Morgan

Madison

Washington

Coshocton

Geauga

Jackson

Hocking

Summit

Ashland

Morrow

Lake

Clermont

Tuscarawas

Delaware

Williams

Harrison

Paulding

Defiance

Lawrence

Auglaize

Van Wert

Cuyahoga

Wyandot

Hamilton

Columbiana

Jefferson

Crawford

Sandusky

Mahoning

Champaign

Ottawa

Montgomery

McWaneAK Steel

Coshocton

CharterSteel

AK SteelMiddletown

ArcelorMittalCleveland

GM DefianceFoundary

North StarBluescope

RepublicSteel

VallourecStar

ArcelorMittalShelby

RepublicSteel

TimkenSteel:Harrison

GambrinusFaircrest

NucorMarion

!"c$

!"c$

!"̀$

!"f$!"g$

!"̀$

!"e$

!"e$

!"a$

!"a$

!"g$!"f$

!"g$

!"f$

Ohio Steel IndustryNotable Establishments*

Key

! Notable Establishment*

Interstate Highway

Ohio County

*Major melt facility or establishmentbelieved to employ 400 or more

Sources:Hoover's Inc., Office of Research,news reports, company web sites,

and U.S. Census Bureau

Prepared by:Office of Research

Ohio Development Services Agency

November 2017

R102717A

4

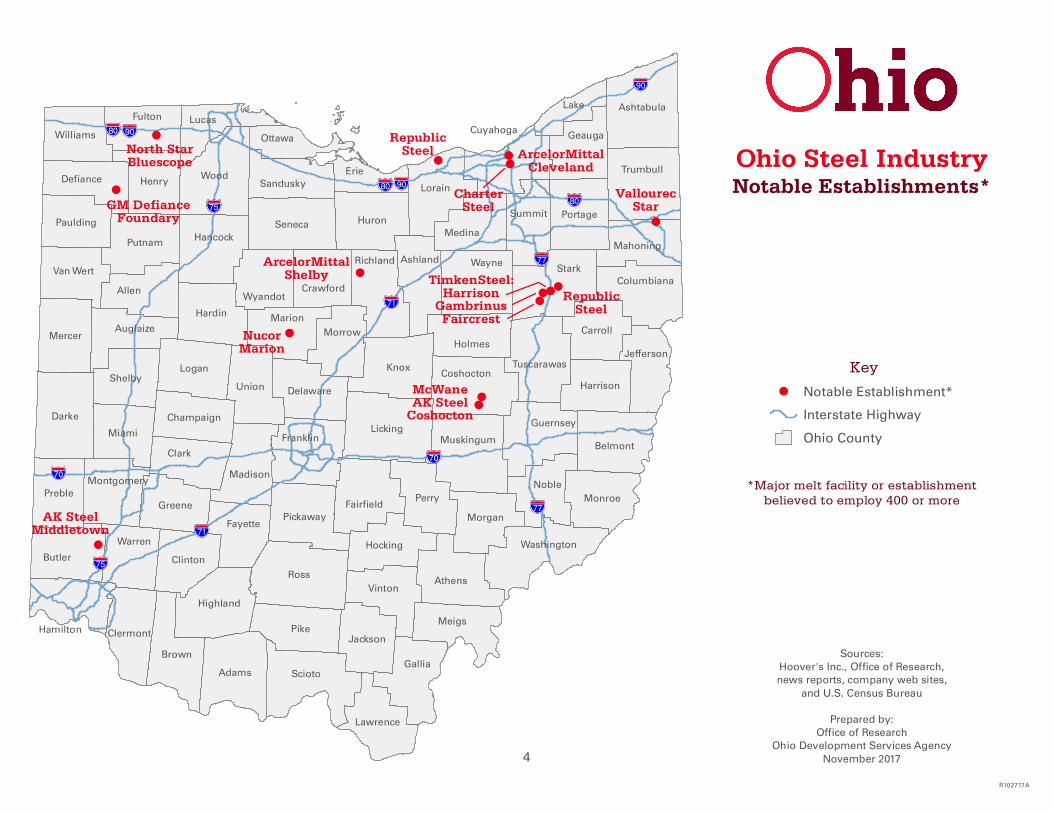

NOTABLE IRON AND STEEL INDUSTRY MANUFACTURERS

Eleven companies on Fortune’s U.S.-1,000 or Global-500 lists have iron and steel industry establishments in Ohio. Two of them maintain their world headquarters in Ohio: AK Steel and Worthington Industries. AK Steel is the largest industry employer in Ohio at about 3,300 people, followed by ArcelorMittal [sic] with well over 2,500, and TimkenSteel [sic] with an estimated 1,900-plus. (These figures included headquarters employment; TimkenSteel split from Timken-the-fabricated-metal-products-company in 2013.) General Motors operates the largest foundry with more than 1,100.1 Four more com-panies – regardless of their Fortune status – employ between 400 and 900 here. The map above shows establishments employing at least 400 or the location of major furnaces. TimkenSteel’s Faircrest, Gambrinus and Harrison form an integrated complex. The list below includes companies employing 400 or more people in Ohio and (generally) having at least 25 people at a site as well as Fortune company sites regardless of size. Establish-ments are grouped by NAICS code and note the city where the site is located. See Appendix Table A1 for the complete list organized by company. Industry Group: Notable Co.^/Subsidiary or Division NAICS City Jobs at Site1

3311: Iron and Steel Mills and Steel Mill Products AK Steel Holding Corp.*/AK Steel Corp.2 3311 Middletown 2,100 AK Steel Holding Corp.*/AK Steel Corp.2 3311 Mansfield 333 ArcelorMittal SA*/ArcelorMittal Cleveland LLC (east and west sites combined)3 3311 Cleveland 1,927 BlueScope Steel Ltd./North Star BlueScope4 3311 Delta 380 Charter Manufacturing Co., Inc./Charter Steel Division5 3311 Cleveland 330 Industrias CH, SAB de CV/Republic Steel Canton Bloom Casting6 3311 Canton 400 Nucor Corp.*/Nucor Steel Marion, Inc.3 3311 Marion 265 TimkenSteel Corp. (Faircrest, Gambrinus & Harrison)9 3311 Canton 1,650

3312: Steel Products from Purchased Steel ArcelorMittal SA*/ArcelorMittal Tubular Products3 33121 Shelby 496 ArcelorMittal SA*/ArcelorMittal Tubular Products3 33121 Marion 100 United States Steel Corp.*10 33121 Lorain 167 Vallourec SA/Vallourec Star, LP11 33121 Youngstown 550 AK Steel Holding Corp.*/AK Steel Corp.2 331221 Coshocton 420 AK Steel Holding Corp.*/AK Steel Corp.2 331221 Zanesville 143 Allegheny Technologies, Inc.*/Allegheny Ludlum, LLC 331221 Louisville 26 Industrias CH, SAB de CV/Republic Steel Cold-finished Plant6 331221 Massillon 200 Industrias CH, SAB de CV/Republic Steel Hot-rolled Bar Plant6, 7 331221 Lorain 10

5

Industry Group: Notable Co.^/Subsidiary or Division NAICS City Jobs at Site1

Mitsui & Co., Ltd.*/Steel Technologies LLC6 331221 Ottawa 100 Mitsui & Co., Ltd.*/Steel Technologies LLC6 331221 Willoughby 30 Nucor Corp.*/Nucor Bright Bar Orrville LLC 331221 Orrville 19 TimkenSteel Corp. (St. Clair) 331221 Eaton 97 Worthington Industries, Inc.*/Worthington Steel Co. 331221 Cleveland 175 Carpenter Technology Corp.*/Latrobe Specialty Metals Co., LLC 331222 Wauseon 76 Industrias CH, SAB de CV/Republic Steel Wire Processing Division6 331222 Solon 15 Leggett & Platt, Inc.*/Solon Specialty Wire Co. 331222 Solon 25

33151: Iron and Steel Foundries General Motors Co.*/Defiance Casting3 331511 Defiance 1,128 McWane, Inc. (fka Clow Water Systems)8 331511 Coshocton 425 Osco Industries, Inc.3 331511 Portsmouth 200 Osco Industries, Inc.3 331511 Jackson 140 Osco Industries, Inc.3 331511 New Boston 70 Westinghouse Air Brake Technologies Corp.*/Wabtec/Sancast12 331511 Coshocton 40 Worthington Industries, Inc.*/Worthington Steel Co. 331513 Monroe 165 Worthington Industries, Inc.*/Worthington Steelpac Systems 331513 Columbus 250

5511: Corporate, Subsidiary and Regional Management AK Steel Holding Corp.*/AK Steel Corp. (HQ) 551112/4 West Chester 300 ArcelorMittal SA*/ArcelorMittal USA LLC (regional HQ)3 551114 Richfield 30 Industrias CH, SAB de CV/Republic Steel Hot-rolled Plant (regional HQ)6 551114 Canton 100 TimkenSteel Corp. (HQ)9 551114 Canton 187 Worthington Industries, Inc.* (HQ) 551114 Worthington 250

Notes: ^ - "notable" means a company either (a) a Fortune U.S.-1,000 or Global-500 company, (b) employing at least 400 people in Ohio, or (c) having a major melt facility in Ohio; * - a Fortune company; 1 - jobs figures are from Hoover's (2017) unless otherwise noted; they are the best available estimates, but their accuracy cannot be guaranteed; 2 - jobs figures at least partially based on U.S. Census Bureau (2017b); 3 - jobs figures from company website(s); 4 - jobs figure from Binsted (2016); 5 - jobs figure from Plain-Dealer (2017), with 25 expected to be added in 2018; 6 - jobs figures from Office of Research (2016a); 7 - the plant is changing to pig iron production with new jobs expected (Payerchin, 2017); 8 - jobs figure from Hannahs (2017); 9 - HQ jobs figure derived from McKinnon (2015); Faircrest-Gambrinus-Harrison figure is company-reported union-only; 10 - jobs figure derived from Nix (2016); 11 - jobs figure from Tribune-Chronicle (2017); 12 - jobs figure from Williams (2017). Sources: Binsted (2016), Fortune (2017), Hannahs (2017), Hoover's (2017), McKinnon (2015), Nix (2016), Office of Research (2016a), Payerchin (2017), Plain-Dealer (2107), Tribune-Chronicle (2017), U.S. Census Bureau (2017b), Williams (2017) and company websites. Prepared by: Office of Research, Ohio Development Services Agency. Telephone 614-466-2116 (DL, 10/17).

6

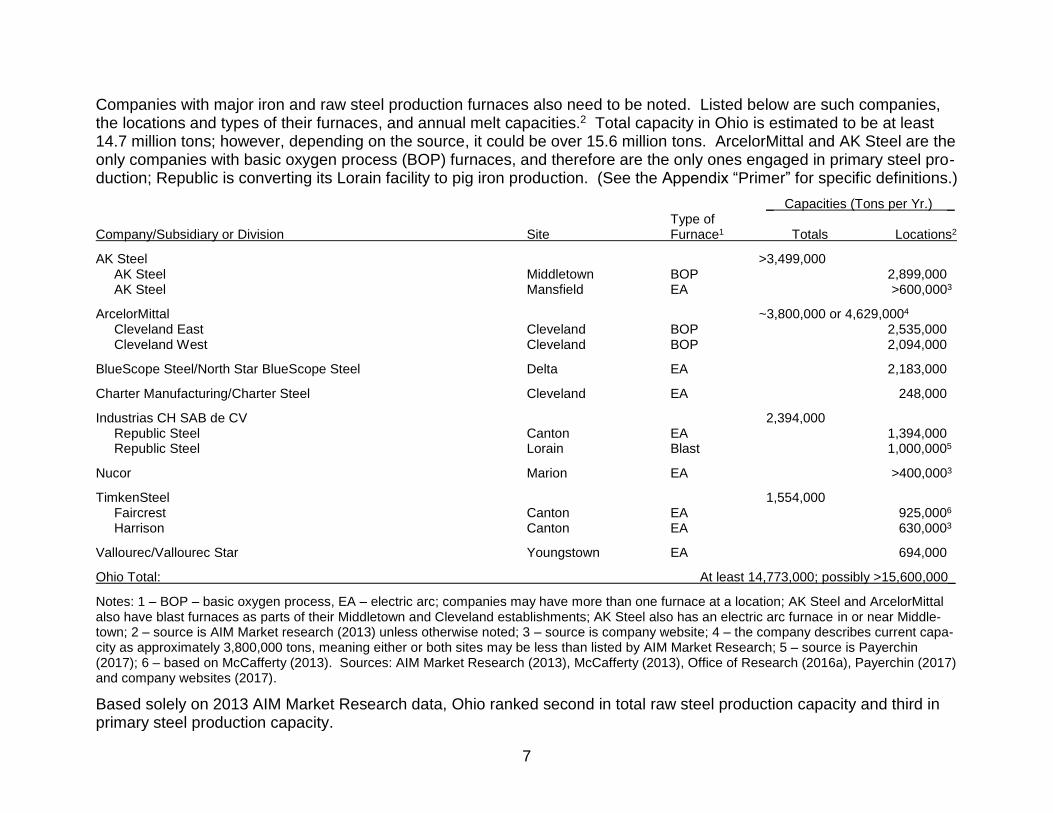

Companies with major iron and raw steel production furnaces also need to be noted. Listed below are such companies, the locations and types of their furnaces, and annual melt capacities.2 Total capacity in Ohio is estimated to be at least 14.7 million tons; however, depending on the source, it could be over 15.6 million tons. ArcelorMittal and AK Steel are the only companies with basic oxygen process (BOP) furnaces, and therefore are the only ones engaged in primary steel pro-duction; Republic is converting its Lorain facility to pig iron production. (See the Appendix “Primer” for specific definitions.)

_ Capacities (Tons per Yr.) _ Type of Company/Subsidiary or Division Site Furnace1 Totals Locations2

AK Steel >3,499,000 AK Steel Middletown BOP 2,899,000 AK Steel Mansfield EA >600,0003

ArcelorMittal ~3,800,000 or 4,629,0004 Cleveland East Cleveland BOP 2,535,000 Cleveland West Cleveland BOP 2,094,000

BlueScope Steel/North Star BlueScope Steel Delta EA 2,183,000

Charter Manufacturing/Charter Steel Cleveland EA 248,000

Industrias CH SAB de CV 2,394,000 Republic Steel Canton EA 1,394,000 Republic Steel Lorain Blast 1,000,0005

Nucor Marion EA >400,0003

TimkenSteel 1,554,000 Faircrest Canton EA 925,0006 Harrison Canton EA 630,0003

Vallourec/Vallourec Star Youngstown EA 694,000

Ohio Total: At least 14,773,000; possibly >15,600,000_

Notes: 1 – BOP – basic oxygen process, EA – electric arc; companies may have more than one furnace at a location; AK Steel and ArcelorMittal also have blast furnaces as parts of their Middletown and Cleveland establishments; AK Steel also has an electric arc furnace in or near Middle-town; 2 – source is AIM Market research (2013) unless otherwise noted; 3 – source is company website; 4 – the company describes current capa-city as approximately 3,800,000 tons, meaning either or both sites may be less than listed by AIM Market Research; 5 – source is Payerchin (2017); 6 – based on McCafferty (2013). Sources: AIM Market Research (2013), McCafferty (2013), Office of Research (2016a), Payerchin (2017) and company websites (2017).

Based solely on 2013 AIM Market Research data, Ohio ranked second in total raw steel production capacity and third in primary steel production capacity.

7

GLOBALIZATION AND FOREIGN INVESTMENT IN OHIO

Foreign investment in Ohio is part of the globalization about which industry analysts write, and has become increasingly important for companies (Hadid, 2017; Leach, 2017; Yucel, 2017a, 2017b). Fifteen foreign-based companies have 21 subsidiary manufacturing establishments in Ohio’s iron and steel industry; two of the companies are on Fortune’s Global-500 list. All companies with at least five employees are listed below, along with the countries where the home office is located, their Ohio subsidiaries, NAICS code(s) and the estimated number of employees here. ArcelorMittal is the largest employer with 2,523 people, followed by Industrias CH, SAB de CV with 725. Eramet is the only company specializing in ferroalloys (specifically manganese). Altogether, the 15 companies employ close to 5,500 in their mills, plants and foun-dries in Ohio. (Some companies also have separate facilities for coke production, fabricated metals activities, research and development, and/or distribution centers; such employment is not included here.)

Parent NAICS Total Ultimate Foreign Parent Country Ohio Subsidiary (no. of sites) Code(s) Jobs^

ArcelorMittal SA *1 Luxembourg ArcelorMittal (4, including a RHQ) 331: 1, 21, 51 2,523 BlueScope Steel Ltd.2 Australia North Star BlueScope Steel LLC (1) 3311 380 Caparo International. Corp. United Kingdom Bull Moose Tube Co. (1) 33121 40 Egon Evertz KG Germany Evertz Technology Services USA, Inc. (1) 33151 30 Eramet SA France Eramet Marietta, Inc. (1) 3311 200 GKN plc United Kingdom GKN Sinter Metals, Inc. (1) 331221 160 Industrias CH, SAB de CV Mexico Republic Steel (5, including a RHQ) 331: 1, 2 725 Miba AG Austria Miba Sinter USA LLC (1) 3311 115 Mitsui & Co., Ltd.* Japan Steel Technologies LLC (2) 331221 130 NV Bekaert SA Belgium Bekaert Corp. (1) 331222 200 OAO TMK Russia TMK Ipsco (1) 33121 105 Shinagawa Refractories Co., Ltd. Japan Shinagawa Advanced Materials Americas, Inc. (1) 33151 28 Tata Sons Ltd./Tata Steel Ltd. India Thomas Steel Strip Corp. (1) 331221 285 Vallourec SA3 France Vallourec Star (1) 33121 550 Van Merksteijn International Netherlands Van Merksteijn USA, LLC (1) 331222 15

Notes: ^ - “Jobs” figures are thought to be the best available at the time of publication, but their accuracy cannot be guaranteed; * - a Fortune U.S.-1,000 or Global-500 company; RHQ – regional headquarters 1 – employment figures from company website; 2 – jobs figure from Binsted (2016); 3 – jobs figure from Business Tribune (2017). Sources: Business-Tribune (2017), company websites (2017), Fortune (2017), Lexis-Nexis (2017), Office of Research, ODSA (2016a).

The foreign parent companies are headquartered in 12 nations. France, Japan and the United Kingdom are home to two each. Australia, Austria, Belgium, Germany, India, Luxembourg, Mexico, the Netherlands and Russia are home to one each. ArcelorMittal and Industrias are the only companies with establishments in more than one specific industry.

8

A second way to understand the role of foreign investors in Ohio’s industry is to note their iron and raw steel production capacity. Four companies – ArcelorMittal, BlueScope Steel, Industrias and Vallourec – own six of the 12 major melt sites in Ohio. Their combined annual melt capacity is estimated at 9.0 to 9.9 million tons, which is most of Ohio’s total capacity. Furthermore, ArcelorMittal owns two of the three basic oxygen process (BOP) sites – in turn, most of Ohio’s primary steel production capacity. The significant role of foreign investment in Ohio’s iron and steel industry in this regard is not atypi-cal; foreign-based steel companies owned an estimated 43.4 percent of all major melt capacity in America and an esti-mated 50.0 percent of U.S. primary steel production capacity in 2013 (drawn from AIM Market Research, 2013). Foreign ownership or investment in the U.S. iron and steel industry is only one aspect of globalization. The converse as-pect has been the establishment of foreign operations by American companies. U.S.-based companies have set-up or acquired over-seas operation for various reasons: less regulation, lower labor costs, and/or a desire to expand world mar-ket share along with more rapid growth prospects in emerging economies. This is particularly true of iron and steel pro-ducers (Hadid, 2017), but much less so of foundry companies and producers using purchased steel (Leach, 2017; Yucel, 2017a, 2017b). Setting up operations outside of home countries – whether it is foreign companies here or U.S.-based companies elsewhere – circumvents trade barriers.

9

$144.3

$84.0

$8.5

$15.2

83

126

38

31

0

30

60

90

120

150

$0.0

$30.0

$60.0

$90.0

$120.0

$150.0

2013 2014 2015 2016

New

Jo

bs

An

tic

ipa

ted

An

no

un

ce

d In

ve

stm

en

ts(i

n m

illi

on

s)

Major Projects in Ohio's Iron & Steel Industry, 2013-2016

Announced Investments New Jobs Anticipated

Source: Office of Research, ODSA

10

RECENT EXPANSION AND ATTRACTION ANNOUNCEMENTS

Seventeen companies announced 20 major investments in Ohio’s iron and steel industry from 2013 through 2016. Plan-ned expenditures were nearly $252.0 million, with close to 280 new jobs anticipated when the projects are completed. The chart above shows that the largest aggregate amount of intended investments occurred in 2013, while the greatest number of new jobs was anticipated beginning in 2014. $131.0 million were intended for iron and steel mills and ferroalloy production (NAICS 3311), followed by $108.8 million for manufacturing steel products from purchased steel (3312), and almost $12.2 million for foundry work (33151). Those figures are 52.0, 43.2 and 4.8 percent of the total. 124 of the new jobs – 44.6 percent – were anticipated in the iron and steel mills and ferroalloys group, 86 – 30.9 percent – for the products from purchased steel group, and 68 – 24.5 percent – in the foundries sub-group. ArcelorMittal led all investors with two announcements totaling $84.1 million. It was followed by Vallourec Star with the single largest announcement – $65.0 million in 2013 – and TimkenSteel with $42.0 million. GKN Sinter Metals and Liber-ty Castings each anticipated adding at least 50 jobs when their projects were completed, closely followed by Arcelor-Mittal with 45 new jobs at its Tubular Products division. The counts and summary figures are drawn from a list of major investments compiled by the Office of Research (2014b-2017b). Companies on the list met at least one of the following criteria: at least $1 million committed for land, building(s) or equipment; at least 20,000 square feet of new space added to a facility; or a minimum of 20 or 50 new jobs (depending on the year). Many major investments are phased-in over two or three years, with employee counts following upon pro-ject completion. Dollar figures are not comparable with the Census Bureau’s capital expenditures data.

11

See Table A2

3.4%

11.2% 11.2% 11.1%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Total GDP Combined VA (3311-2) Iron/Steel/Alloys VA (3311) Steel Products VA (3312)

Oh

io a

s a

Pe

rce

nta

ge

of

the

U.S

. T

ota

lsThe Concentration of the Iron & Steel Industry in Ohio, 2015

12

Sources: U.S. Bureaus of the Census and Economic Analysis

Gross Domestic Product Value-Added

IRON AND STEEL INDUSTRY CONCENTRATION IN OHIO

The chart above illustrates the concentration of iron and steel industry groups in Ohio. During 2015, 11.2 percent of the value-added by U.S. iron, steel and ferroalloy producers (NAICS 3311) came from plants in Ohio, while 11.1 percent of steel-products-from-purchased-steel (3312) value-added originated in Ohio. The two groups combined were 11.2 percent of national output (U.S. Bureau of the Census, 2017a).3 More industry-specific data from the 2012 Census of Manufac-tures in Appendix Table A3 show 9.9 percent of ferrous metal foundry (33151) value-added came from Ohio. When com-bined with iron, steel, ferroalloy and steel-products-purchased-steel output that year, 11.0 percent of total iron and steel industry value-added came from Ohio. By comparison, 3.4 percent of the value of all goods and services provided in America in 2015 originated in Ohio according to the latest gross domestic product (GDP) figures from the U.S. Bureau of Economic Analysis (2017).4 The greater portions of the former compared with the last indicate the concentration of the industry here. The following table shows that the summary concentration of the iron and steel industry is broadly based on all specific industries and not reflective of an extraordinary concentration in just one. Percent of Apparent Value-added Rank in Industry Code and Description in the U.S. the U.S.*

3311: Iron & Steel Mills & Ferroalloys 12.7% 3rd 33121: Iron & Steel Pipes & Tubes from Purchased Steel 16.4% 1st 331221: Rolled Steel Shapes from Purchased Steel 10.2% 1st 331222: Steel Wire Drawing from Purchased Steel 8.1% 2nd 331511: Iron Foundries 7.9% 5th 331512: Steel Investment Foundries 13.7% 2nd 331513: Steel Foundries (except Investment) 10.7% 2nd

Note: * - Not every state with at least one industry establishment can be ranked based on value-added due to confiden-tiality restraints. Source: U.S. Bureau of the Census (2015c). Three factors help explain the industry’s historical and continuing concentration in Ohio: the raw materials – principally iron ore and coal – are in the region; bulk transportation, whether by water or rail, of both raw materials and products is convenient; and secondary manufacturers using purchased iron and steel (3312 and 33151) prefer to locate near their suppliers (3311), keeping transportation costs low (drawn from Yucel, 2015).

13

See Table A3

3311: Iron & Steel Mills, 13,118, 51%

33121: Pipe & Tube Mfg., 3,564, 14%

331221: Rolled Steel Shapes, 932, 3%

331222: Steel Wire Drawing, 945, 4%

331511: Iron Foundries, 3,816, 15%

331512: Steel Investment Foundries, 1,741, 7%

331513: Other Steel Foundries, 1,710, 6%

Employment in Ohio's Iron and Steel Industryby Specific Industry, 2015

33151: Ferrous Foundries, 7,267, 28%

3312: Products from Purchased Steel,

5,441, 21%

Total: 25,821

14

Source: U.S. Census Bureau

THE COMPOSITION OF OHIO’S IRON AND STEEL INDUSTRY: EMPLOYMENT

180 establishments employed more than 25,800 people in Ohio’s iron and steel industry according to the latest compre-hensive data from the U.S. Bureau of the Census (2017b). 13,100-plus – 50.8 percent – worked in the iron-steel-ferro-alloys group (NAICS 3311). (Data gathered prior to implementing the 2012 NAICS show only a minute fraction of the group was in ferroalloy production.) The remaining industry employees were divided between the ferrous metal foundries subgroup (33151) with 7,200-plus – 28.1 percent of the industry – and the products-from-purchased-steel group (3312) with 5,400-plus and 21.1 percent. Iron foundries (331511) were the second largest employers after iron and steel mills with over 3,800 people (the plurality of which were people at GM’s Defiance foundry.) The remaining specific industries employed from 932 to 3,500-plus people – 3.6 to 13.8 percent of the industry total. Overall, 9.1 percent of the iron and steel industry establishments and 11.8 percent of the industry’s jobs in America are located in Ohio – concentrated when compared with Ohio’s portions of all private non-farm non-railroad establishments and employment – 3.3 and 3.8 percent, respectively. As with value-added in the preceding section, the concentration of industry employment was broadly based, not the result of extreme concentration in one specific industry. Portions in Ohio ranged from 6.3 to 14.2 percent of the corresponding U.S. totals (U.S. Bureau of the Census, 2017b).

15

See Table A4

$45,161

$65,700

$75,319

$59,017

$62,866

$51,710$50,012

$53,385 $53,347

$58,684

$47,156 $47,739

89.6%

104.2%

100.4%

108.5%111.8%

98.7%

85.9%

108.7%

105.0%

116.7%

90.9%93.5%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

As P

erc

en

tag

e o

f U

.S.

An

nu

al

Pay i

n O

hio

Annual Pay in Ohio's Iron and Steel Industryby Groups and Individual Industries, 2015

16

Source: U.S. Census Bureau

INDUSTRY PAY

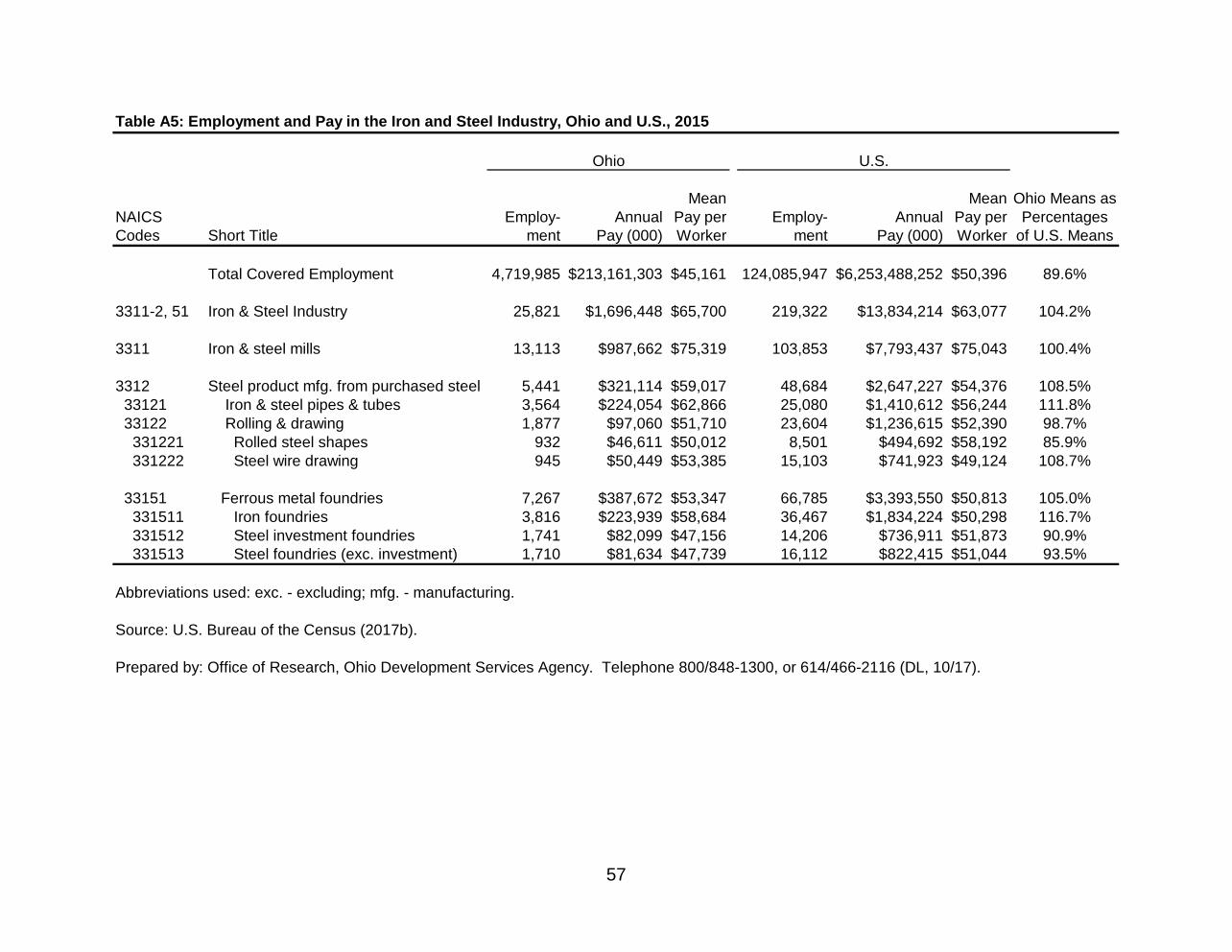

The chart above shows that annual pay for all non-farm, non-railroad private sector employees in Ohio averaged more than $45,100 in 2015. People employed in the state’s iron and steel industry averaged $65,700, but there is much varia-tion within. Pay was greatest in the iron-steel-ferroalloys group (NAICS 3311, $75,300-plus), followed by the products-from-purchased-steel group (3312, about $59,000) and ferrous metal foundries (33151, $53,300-plus). The chart also illustrates the variation within the latter two groups. The high pay in pipes and tubes (33121, $62,800-plus) is offset by the lower pay in rolled steel shapes (331221, about $50,000), while pay in wire drawing (331222, just under $53,400) fell in between. Similarly, the relatively high pay in iron foundries (331511, nearly $58,700) offsets the lower pay of work in steel foundries (331512 and 3, $47,100-plus and $47,700-plus). Nevertheless, pay in all specific industries was greater than the near-all-Ohio average of $45,100-plus. Mean iron and steel industry pay in Ohio was 104.2 percent of the corresponding U.S. average. Again, there is notable variation from one specific industry to the next:

• 331221: rolling steel shapes from purchased steel – 85.9 percent;

• 331512 and 3: steel foundries – 90.9 and 93.5 percent;

• 3311: iron and steel mill production – 100.4 percent;

• 331222: wire drawing from purchased steel – 108.7 percent;

• 33121: pipes and tubes from purchased steel – 111.8 percent;

• 33151: iron foundries – 116.7 percent.

17

See Table A5

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! !

! ! !

! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! !

! ! !

! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! !

! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! ! !

! ! ! !

! ! ! !

! ! !

! ! !

! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! ! !

! ! ! !

! ! ! !

! ! !

! ! !

! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! !

! ! !

! ! !

! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! !

! ! !

! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! !

! ! !

! ! !

! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! !

! ! !

! ! !

! ! !

! !

! !

! !

! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! !

! ! !

! ! !

! ! !

! ! ! !

! ! ! !

! ! ! !

! ! !

! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

1

2

Stark14

Wood2

Darke1

Scioto2

Wayne3

Perry1

Clark1

Allen1

Butler5

Lorain4

Logan1 Union

2

Trumbull10

Hardin2

Henry1

Franklin6

Miami3

Fulton4

Erie1

Hancock3

Putnam1

Lucas5

Carroll1

Shelby1

Richland6

Clinton1

Greene1

Muskingum2

Marion3

Medina2

Warren1

Holmes1

Guernsey1

Madison1

Washington6

Coshocton3

Geauga1

Summit7

Jackson2

Tuscarawas3

Delaware2

Williams2

Paulding1

Defiance1

Auglaize2

Cuyahoga19

Wyandot1

Hamilton3

Columbiana7

Mahoning10

Lake5

Jefferson2

Montgomery9

Ross

Pike

Knox

Licking

AdamsGallia

HuronSeneca

Brown

Athens

Meigs

Ashtabula

NoblePreble

Mercer

Portage

Belmont

Vinton

Fairfield

Highland

Monroe

FayettePickaway Morgan

Hocking

Ashland

Morrow

Clermont

Harrison

Lawrence

Van WertCrawford

Sandusky

Champaign

Ottawa

Columbus

Akron

Toledo

Dayton

Cincinnati,OH-KY-IN

Cleveland-Elyria

Ohio Steel IndustryEstablishments by County

Statewide: 180

Steel IndustryEstablishments

in County

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

11 - 19

! ! ! !

! ! ! !

! ! !

! ! !

6 - 10

! ! !

! ! !

! !

! !

2 - 5

! !

! !

1

None

Source:2015 County Business Patterns

U.S. Census Bureau

Prepared by:Office of Research

Ohio Development Services AgencyNovember 2017

R102717A

18

Large Metro*

1 Canton-Massillon, OH2 Youngstown-Warren- Boardman, OH-PA

*Only those portions of the 8 MetropolitanStatistical Areas (Metros) that contain 2 or

more counties in Ohio are shown.

THE DISTRIBUTION OF INDUSTRY ESTABLISHMENTS IN OHIO

The map above illustrates the distribution of the 180 iron and steel industry establishments across Ohio according to the latest County Business Patterns data. Fifty-three counties had at least one industry establishment. However, just over one-half of the establishments were found in 10 counties: Cuyahoga had 19; Stark, 14; Mahoning and Trumbull, 10 each; Montgomery, nine; Columbiana and Summit, seven each; and Franklin, Richland and Washington, six each. The remain-ing 43 counties with establishments each had from one to five. One way to look at the map is to note the clustering of establishments in Northeastern metropolitan areas (MAs) long-noted for iron and steel operations. Canton-Massillon, Cleveland-Elyria, Mansfield and Youngstown-Warren, a total of 10 counties, have 72 establishments, or 40 percent of the industry total. This concentration is associated with the presence of nine major melt facilities in five counties in these MAs: Cuyahoga (ArcelorMittal’s two, and Charter), Lorain (Republic), Mahoning (Vallourec), Richland (AK Steel and Arcelor) and Stark (Republic and TimkenSteel). The five counties and these companies combine for roughly 64 percent of the state’s major melt capacity, including two of the three basic oxy-gen process sites. (The remaining major melt sites in the area use electric arc furnaces.) Yet 60 percent the industry establishments are outside of Northeastern Ohio regardless of metropolitan status. However, 14 counties in the Cincinnati, Columbus, Dayton and Toledo MAs combined for 45 establishments – 25 percent of Ohio’s total, including two major melt facilities in Butler and Fulton Counties (AK Steel and North Star BlueScope, respectively). Marion and Defiance Counties are the non-metropolitan exceptions with major establishments: Nucor and General Motors (the latter is Ohio’s largest foundry operator).

19

See Table A6

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! !

! ! !

! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! !

! !

! !

! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! !

! ! !

! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! !

! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! ! !

! ! ! !

! ! ! !

! ! !

! ! !

! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! !

! ! !

! ! !

! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! !

! ! !

! ! !

! ! !

! !

! !

! !

! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! ! ! ! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! !

! ! ! !

! ! ! !

! ! ! !

! ! ! !

! ! !

! ! !

! ! !

! ! !

! ! ! !

! ! ! !

! ! ! !

! ! !

! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

Stark4,993

Wood158

Darke7

Scioto209

Wayne695

Perry143

Clark66

Allen66

Butler2,046

Lorain1,476

Logan3

Union10

Trumbull966

Hardin143

Henry28

Franklin1,366

Miami314

Fulton190

Erie143

Hancock173

Putnam143

Lucas257

Carroll15

Shelby28

Richland1,158

Clinton15

Greene28

Muskingum285

Marion428

Medina95

Warren15

Holmes3

Guernsey143

Madison28

Washington518

Coshocton733

Geauga3

Summit260

Jackson145

Tuscarawas300

Delaware209

Williams43

Paulding28

Defiance1,183

Auglaize171

Cuyahoga3,233

Wyandot143

Hamilton377

Columbiana228

Mahoning775

Lake904

Jefferson31

Montgomery275

Ross

Pike

Knox

Licking

AdamsGallia

HuronSeneca

Brown

Athens

Meigs

Ashtabula

NoblePreble

Mercer

Portage

Belmont

Vinton

Fairfield

Highland

Monroe

FayettePickaway Morgan

Hocking

Ashland

Morrow

Clermont

Harrison

Lawrence

Van WertCrawford

Sandusky

Champaign

Ottawa

Columbus

Akron

Toledo

Dayton

Cincinnati,OH-KY-IN

Cleveland-Elyria

1

2

Ohio Steel IndustryEmployment by County*

Statewide: 25,821

Steel IndustryEmploymentin County*

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

! ! ! ! ! !

2,000 - 4,993

! ! ! !

! ! ! !

! ! !

! ! !

500 - 1,999

! !

! !

! !

! !

100 - 499

! !

!

1 - 99

None

Source:2015 County Business Patterns

U.S. Census Bureau

Prepared by:Office of Research

Ohio Development Services AgencyNovember 2017

R102717A

20

*County employment figures shown on thismap should be considered estimates.

Large Metro**

**Only those portions of the 8 MetropolitanStatistical Areas (Metros) that contain 2 or

more counties in Ohio are shown.

1 Canton-Massillon, OH2 Youngstown-Warren- Boardman, OH-PA

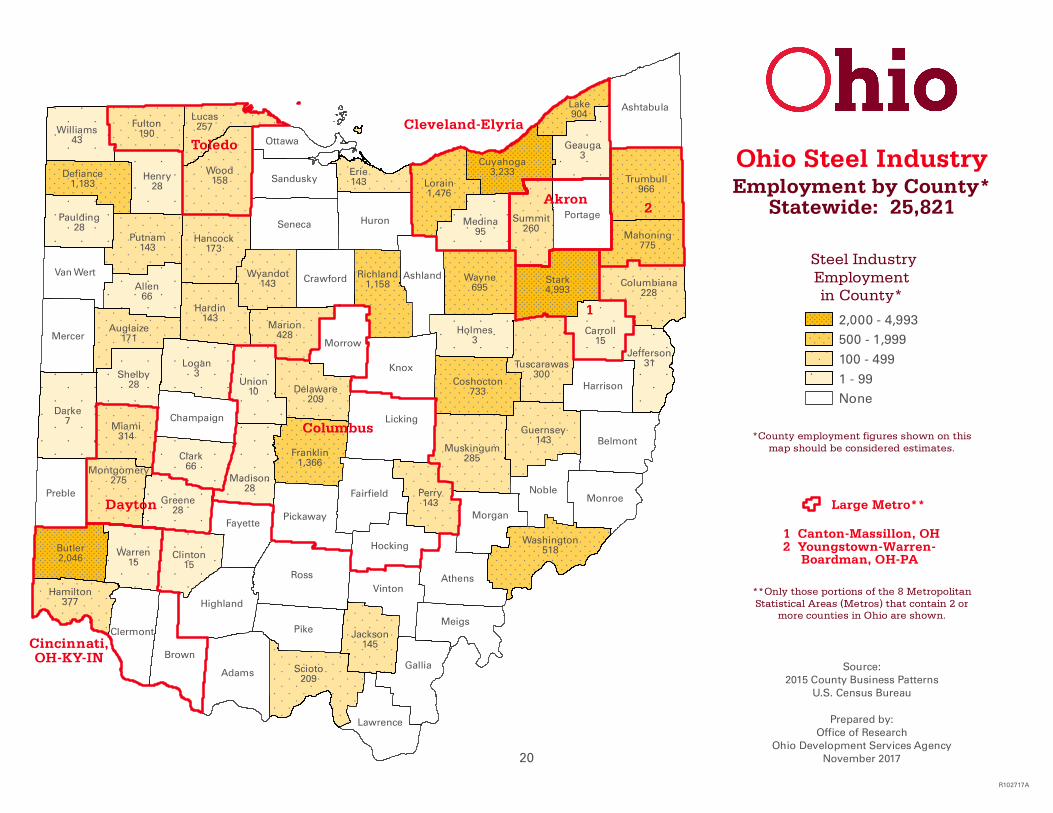

THE DISTRIBUTION OF INDUSTRY EMPLOYMENT IN OHIO

Employment is even more concentrated than the distribution of establishments; seven counties account for three-fifths of the industry jobs in Ohio. Stark topped the list with nearly 5,000, followed by Cuyahoga with 3,200-plus and Butler with at least 2,000. Defiance, Franklin, Richland and Lorain had between 1,100 and 1,500 each. Six counties had between 500 to 1,000 industry jobs: Coshocton, Lake, Mahoning, Trumbull, Washington and Wayne; 22 had 100 to 499, and 18 had 1 to 99 jobs.5 Counties with at least 500 employees often are associated with the facilities of notable industry companies: Butler is home to AK Steel; Coshocton has AK Steel and McWane; Cuyahoga has ArcelorMittal and Charter Steel; Defiance has a Gen-eral Motors foundry; Franklin is home to Worthington Industries; Lorain has Republic Steel and U.S. Steel; Mahoning has Vallourec Star; Richland has AK Steel and ArcelorMittal; Stark is home to Timken and has Republic Steel, including the latter’s regional headquarters; Trumbull has the Worthington Industries subsidiary Dietrich Industries. Lake and Wayne appear are exceptions in this regard. (The converse exception is Marion County, which has less than 500 employees, but has ArcelorMittal and Nucor establishments.)6

21

See Table A6

This page intentionally blank

22

TRENDS

23

14.5

16.3

17.7

16.5 16.8

14.2

15.516.1

16.7 16.416.8

15.8

16.817.5

18.3

15.7

14.6

13.1

15.816.4

15.9 16.1

14.8

6.6

9.3

11.6

13.7

11.5

12.6

11.3

9.7

17.8%18.2%

17.7%

16.9%17.0%

16.2%

16.7%16.5%16.6%

15.7%16.0%

14.6%

15.4%

16.3%16.3%

15.8%

14.5%

12.7%

14.4%

15.7%

14.6%14.9%

14.6%

10.1%10.4%

12.2%

14.0%

12.0%

13.0%13.0%

11.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

`86 `87 `88 `89 `90 `91 `92 `93 `94 `95 `96 `97 `98 `99 `00 `01 `02 `03 `04 `05 `06 `07 `08 `09 `10 `11 `12 `13 `14 `15 `16*

Perc

en

t o

f U

.S.

Millio

ns o

f N

et

To

ns

Estimated Raw Steel Production in Ohio, 1986-2016

Raw Steel Production Percent of U.S.

Sources: American Iron and Steel Institute; Hill, et.al.; U.S. Geological Survey

24

* - Preliminary

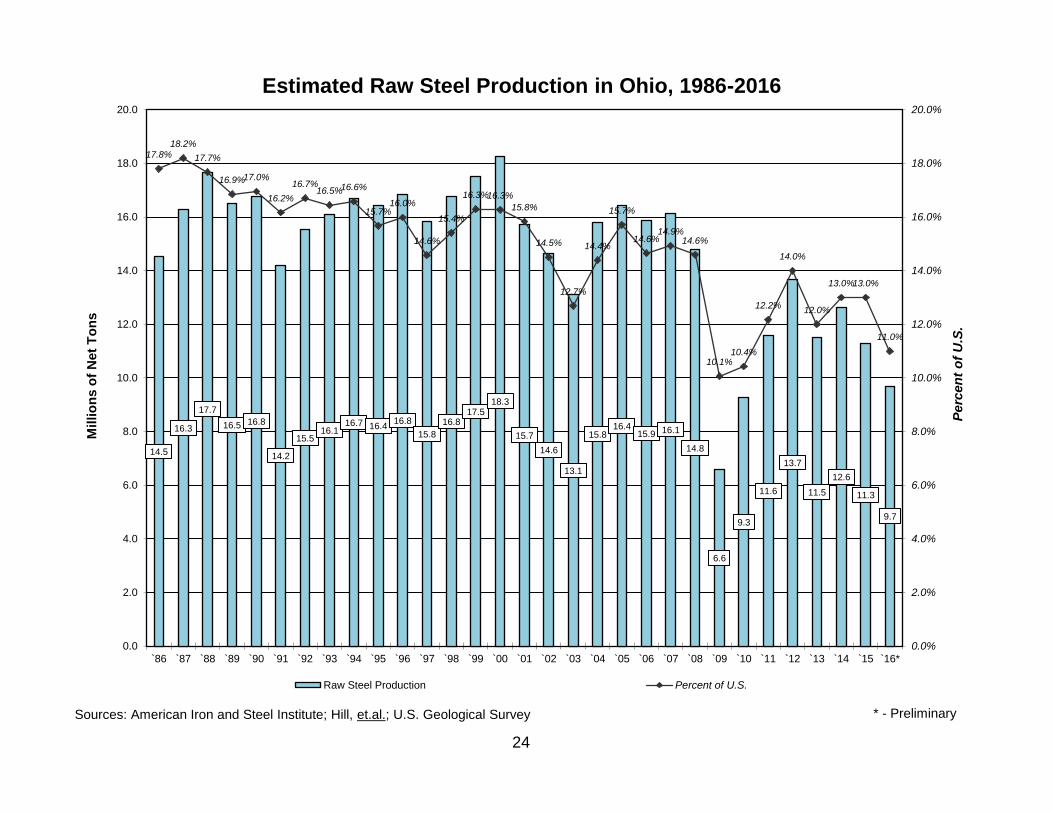

RAW STEEL PRODUCTION Raw steel production is the core of the iron and steel industry, the immediate or proximate starting point for all goods wholly or partially made of steel. The chart above illustrates the cyclical nature of the raw steel production in Ohio, with the relatively low output volumes during 1991, 2003 and 2009 closely corresponding with the depths of national reces-sions, and the relatively high output volumes during 1990, 2000 and 2007 matching the peaks (or ends) of national eco-nomic expansions. However, writers following the industry in Ohio believe the state’s recent drop in raw steel production – even as its and the U.S. economy have continued expanding – is at least partially due to the reduced demand for pipes used in extracting natural gas and oil from the Utica and Marcellus shale formations, and ultimately to lower prices for the latter (e.g., McCafferty, 2016).7 The highly cyclical character of raw steel production reflects the use of relatively large amounts of steel in products with high sale prices: transportation equipment, big appliances and machinery, some fabricated metal products, and non-residential construction projects. These steel-using industries tend to highly cyclical in response to changing consumer demand. When business is good and jobs are plentiful, consumers – individuals, families and organizations – feel con-fident in purchasing expensive goods. Conversely, consumers cut back or delay expenditures for the same goods during economic hard times, preferring to repair instead of replace (drawn from Levy, 2014, and Corridore, 2014; also see Hadid, 2017).8 The earlier part of economic recoveries and expansions generally are led by increasing demand for consumer durables: motor vehicles, appliances and other domestic equipment. By contrast, the demand for capital goods such as those used in non-residential construction, machinery and commercial equipment typically increases after the recovery is well under way and the demand for consumer durables plateaus (Larkin, 2013: O6). Overall, then, steel industry ship-ments continue throughout an economic expansion. The chart above also records how the percentage of U.S. raw steel production coming from Ohio seems to have trended lower during the last three decades, although year-to-year variations may be pronounced. Including data from Appendix Table A7, Ohio averaged 16.8 percent of U.S. raw steel production during the 1970s, 16.5 percent during the 1980s, 16.1 percent during the 1990s, but 14.5 percent during the 2000s, and 12.3 percent from 2010 through 2016. This may be due to the spread of minimills (which principally recycle steel) across the country as well as the latter’s increasing share of raw steel production. Despite the yearly variations and the slightly lower percentages, Ohio ranked second in raw steel pro-duction for every year shown above; 1981 was the last year it ranked third. Raw steel production methods have shifted over the years with technological advances. The chart on the following page illustrates (1) the demise of open hearth furnaces in favor of more efficient basic oxygen process furnaces (BOPFs) for primary steel production and (2) the growing role of electric arc furnaces (EAFs) for recycling in raw steel production.

25

4.1 3.05.1 4.5 3.5

1.6

58.7 58.9

58.0 59.6

59.160.0 62.0 60.6 60.7 59.6

57.4 56.2 54.9 53.8 53.0 52.649.6 49.0 47.9

45.042.9 41.8 42.6

38.2 38.7 39.7 40.9 39.437.4 37.0

33.0

37.2 38.1 36.9 35.9 37.3 38.4 38.0 39.4 39.3 40.442.6 43.8 45.1 46.2 47.0 47.4

50.4 51.0 52.155.0

57.1 58.2 57.4

61.8 61.3 60.3 59.1 60.662.6 63.0

67.0

55.2

59.8

61.3

64.8

67.4

75.8

79.3

85.7

89.591.1

93.294.7 95.5 95.6

96.4 97.2 97.2 97.3 97.1 96.8 96.7 96.7 96.4 97.0 97.4 98.0 98.6 98.8 98.5 99.0 99.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

`86 `87 `88 `89 `90 `91 `92 `93 `94 `95 `96 `97 `98 `99 `00 `01 `02 `03 `04 `05 `06 `07 `08 `09 `10 `11 `12 `13 `14 `15 `16*

Perc

en

t C

on

tin

uo

us

ly C

ast

Pe

rcen

tag

es

by F

urn

ac

e T

yp

eU.S. Raw Steel Production, 1986-2016

Percentages by Furnace Type and Cast

Open Hearth Basic Oxygen Process Electric Arc Continous

26

Sources: American Iron and Steel Institute; U.S. Geological Survey * - Preliminary

Iron and steel production was a vertically integrated process dominated by large companies for much of the 20th century. The companies owned the materials and equipment used at each step of the primary production process. These usually included the mines of iron ores, coal and fluxes, the coke ovens, the furnaces, the breakdown mills, and the service and distribution centers (i.e., wholesalers) for steel slitting and sales to end users (Larkin, 2013: O1). 91.6 percent of the raw steel produced in the U.S. during 1960 was made by this integrated primary production process (further described in the Appendices); only 8.4 percent came from mills focused exclusively on recycling scrap (cited by Larkin, 2013: O2 & O3). In contrast to primary producers, minimills make steel principally by recycling ferrous scrap in EAFs, although some can substitute directly reduced iron when scrap prices are high. Doing so means that they avoid the costs associated with blast- and BOPFs, coke ovens and equipment to handle raw materials. (Raw materials and the greater energy required for primary steel making are about two-thirds of the costs of primary producers.) Consequently, capital costs for minimills are much lower than for primary producers. Lower capital costs, a leaner management structure, and more flexible, less costly labor arrangements allowed minimills to undercut the prices primary producers would charge for the same products (Larkin, 2013: O1, O3; also Hadid, 2017). (Primary steelmakers also incorporate scrap. That reduces their costs some-what, but cannot compensate for their greater capital requirements and expenses.) Minimills initially were limited to lower-quality commodity products, but have increased their collective market share as quality improved. One key to their expansion was the development of thin slab and strip casters. These bypassed the need for reducing stands, permitting the direct production of thin slabs and strips from molten raw steel. (North Star Blue-Scope Steel is an Ohio minimill using such technology.) While primary producers also adopted them, they benefitted minimills more by the reduction of capital needed to compete in markets for higher quality goods such as pipes, plates, strips and sheets. Such items had been the domain of primary producers, but they were forced to abandon markets for specific products as minimills’ quality improved. Ultimately, then, it has been interrelated technological advances and reduced costs that enabled minimills to increase their share of domestic raw steel production at the expense of primary producers. Nevertheless, primary producers have remained the source for the highest-grade goods (Larkin, 1994, 1995, 2005, 2013).9

27

See Table A7

$4,588

$3,246

$4,014 $3,940

$520

$3,263

$3,722

$2,754$2,938

$3,309$3,057

$1,377

$1,697

$1,325$1,290

$674

$639

$680

$1,002$920

$917

$715

15.1%

12.6%

13.5% 13.6%

6.7%

11.9%12.2%

11.4%

10.7%

11.6%

11.2%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

To

tal a

s P

erc

en

t o

f U

.S.

To

tal

(Mil

lio

ns

)Value-Added in Ohio's Iron and Steel Products Groups, 2005-2015

(NAICS 3311-2, Standardized on 2009)

3311: Iron & Steel Mill Products 3312: Steel Products from Purchased Steel 3311-2: Percent of U.S. Total

28

Sources: U.S. Bureaus of the Census and Labor Statistics

$4,225

* - Preliminary

$3,773

$5,965

$4,943

$5,339$5,230

$1,194

$3,902

$4,403

$3,756$3,858

PRODUCTION AS MEASURED BY VALUE-ADDED