adapting to a challenging oil price environment in aberdeen

TRANSCRIPT

Adapting to a Challenging Oil Price Environment

in Aberdeen

Professor Alex Kemp

University of Aberdeen

0

100

200

300

400

500

600

700

800

1965 1970 1975 1980 1985 1990 1995 2000 2005

Millio

n B

arr

els

Oil E

qu

ivale

nt

Average Discovery Size on UKCS, 1965 - 2009

Average Discovery Size on UKCS, 1965 - 2005,

with Major Post-1974 Discoveries

0

100

200

300

400

500

600

700

800

900

1965 1970 1975 1980 1985 1990 1995 2000 2005

Millio

n B

arr

els

Oil E

qu

ivale

nt

Average Discovery Size

Major Post-1974 Discoveries

Source: DECC

0

10

20

30

40

50

60

70

80

90

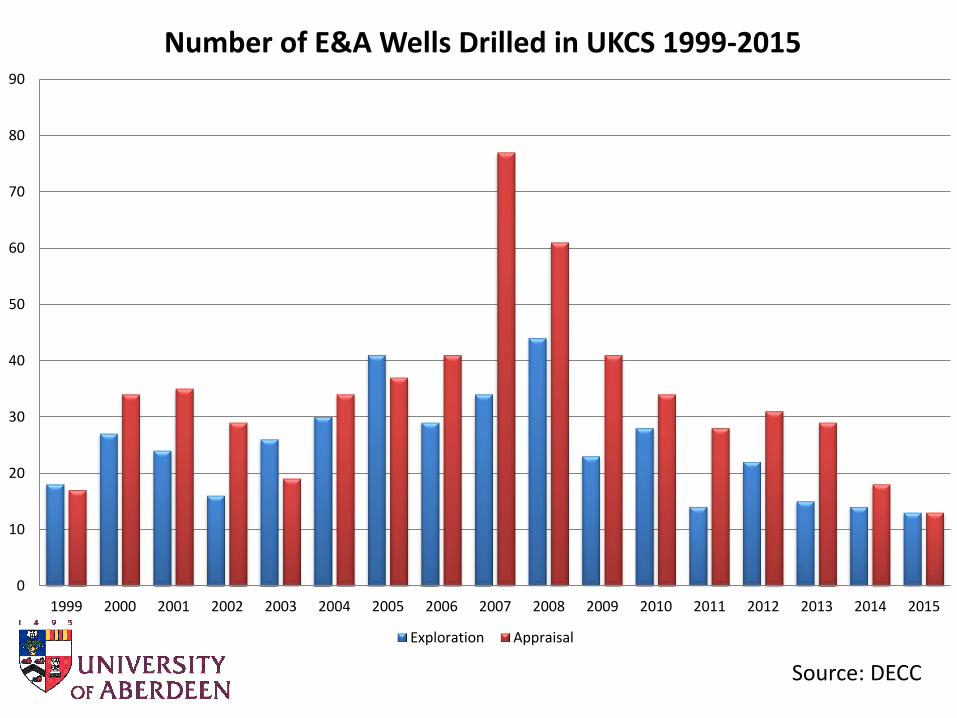

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Number of E&A Wells Drilled in UKCS 1999-2015

Exploration Appraisal

Source: DECC

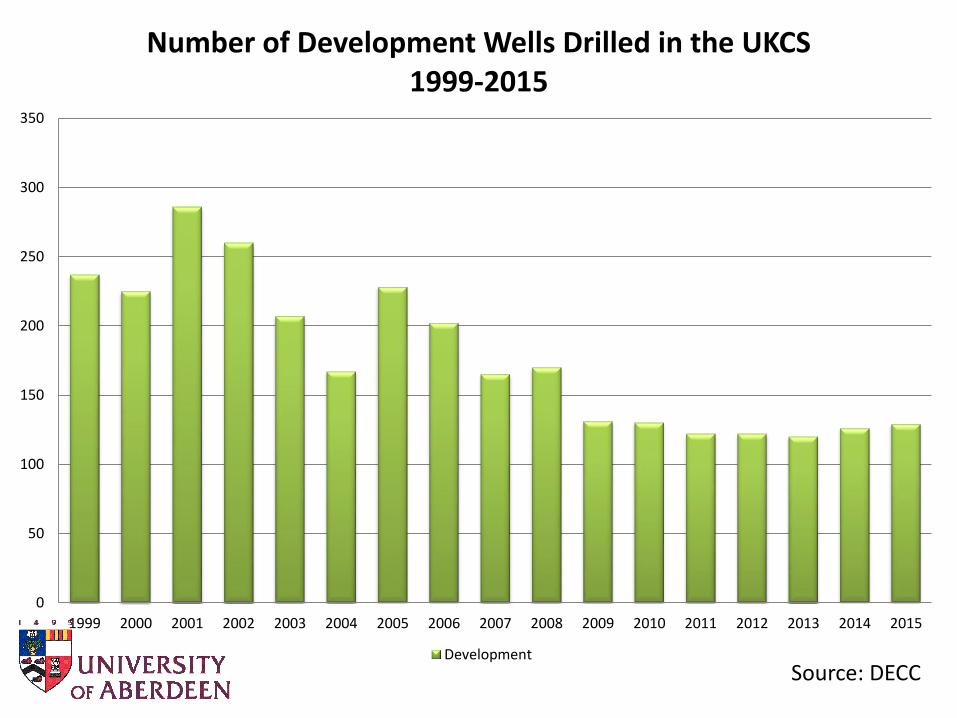

0

50

100

150

200

250

300

350

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Number of Development Wells Drilled in the UKCS1999-2015

Development

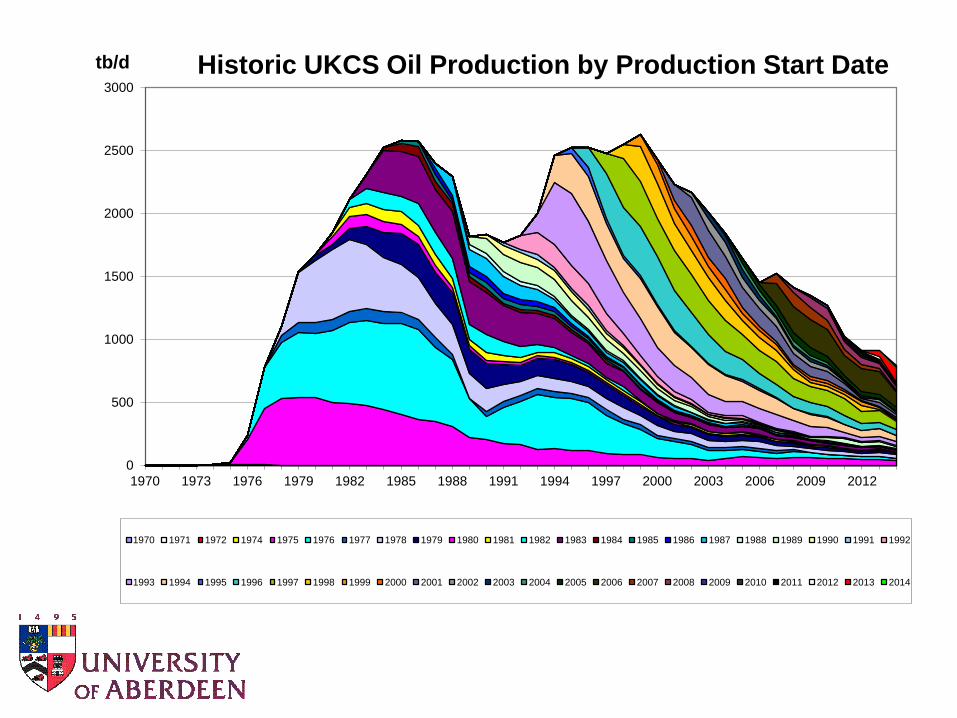

0

500

1000

1500

2000

2500

3000

1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012

tb/d Historic UKCS Oil Production by Production Start Date

1970 1971 1972 1974 1975 1976 1977 1978 1979 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

2000

4000

6000

8000

10000

12000

1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012

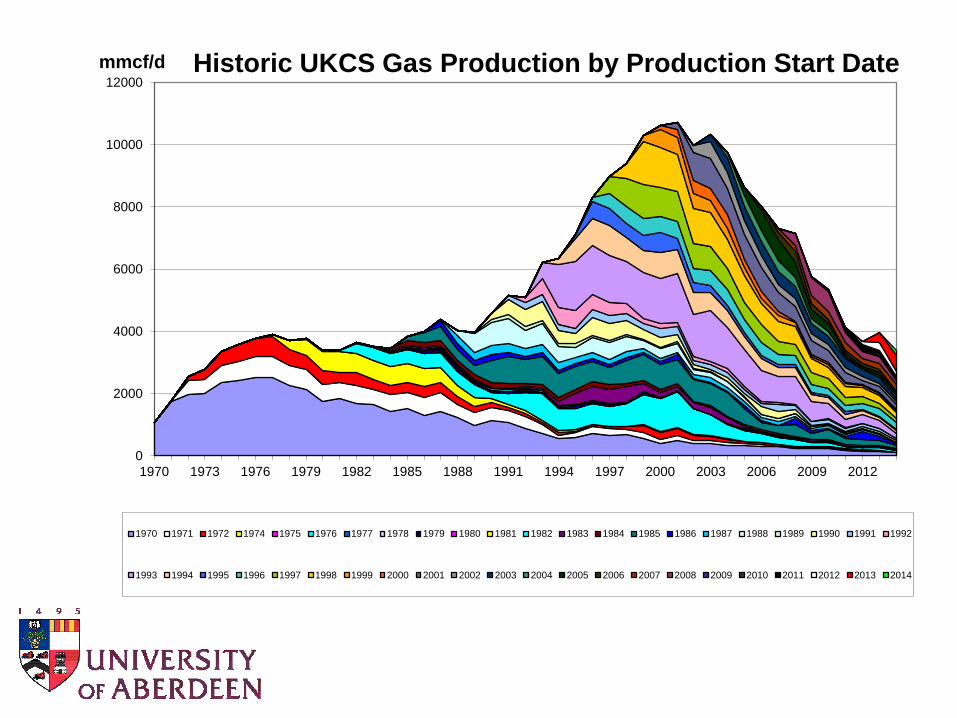

mmcf/d Historic UKCS Gas Production by Production Start Date

1970 1971 1972 1974 1975 1976 1977 1978 1979 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0

500

1000

1500

2000

2500

3000

3500

4000

4500

1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012

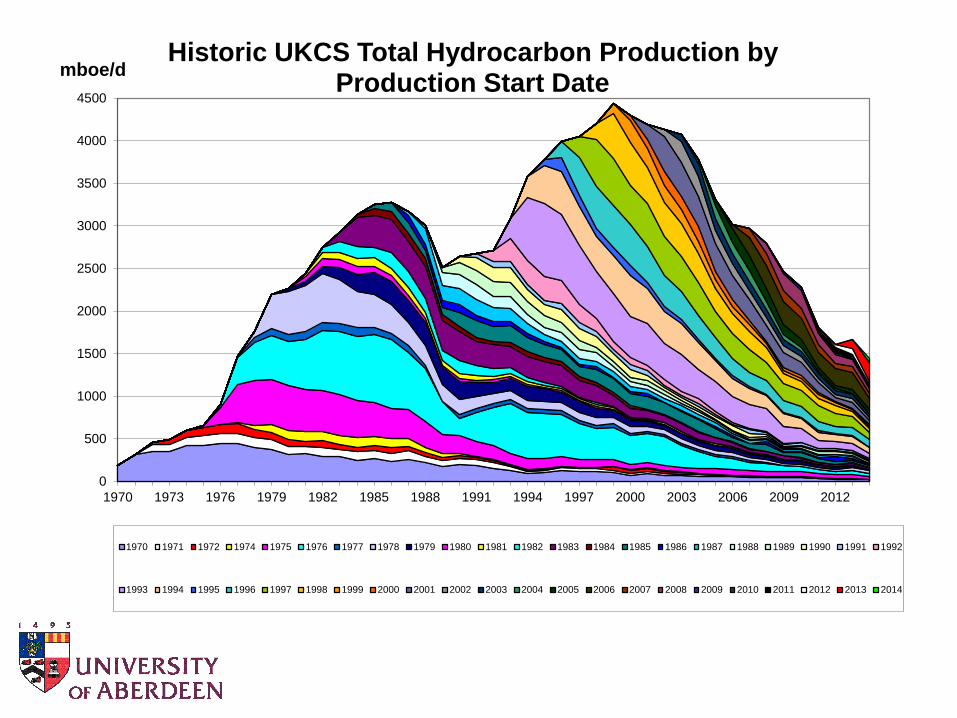

mboe/dHistoric UKCS Total Hydrocarbon Production by

Production Start Date

1970 1971 1972 1974 1975 1976 1977 1978 1979 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Source: DECC

Source: DECC

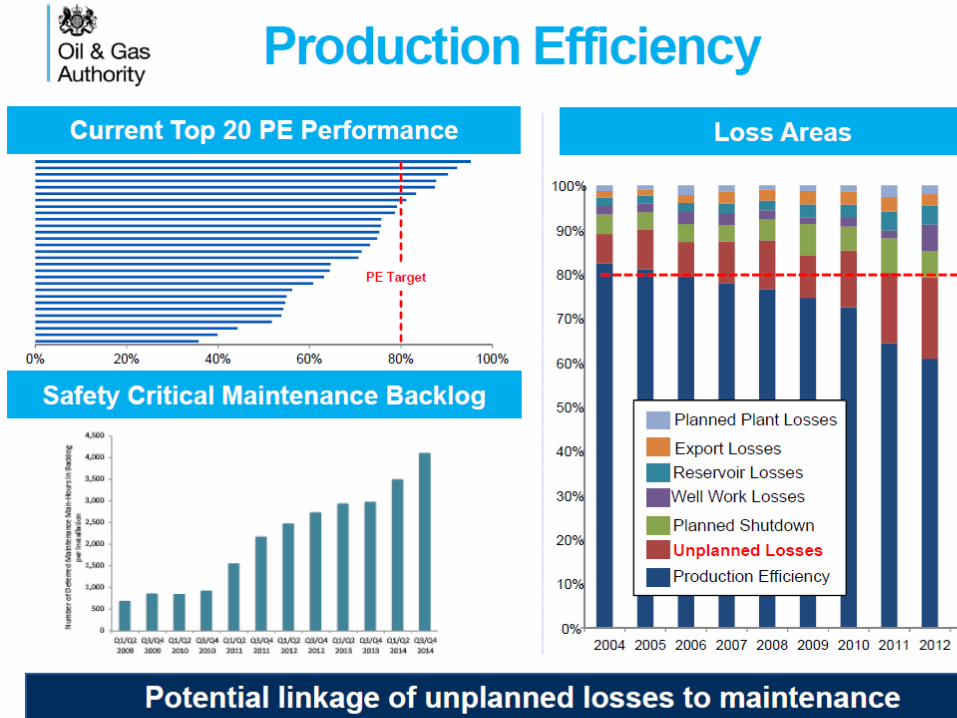

Production Efficiency

- Stability but little gain PE at UKCS level up v. slightly

on 2013

[“green shoots?”]

Production steady.

Some prior production

returned.

Crude price crash

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Pro

du

ctio

n M

illio

n b

oe

/d

Pro

du

ctio

n E

ffic

ien

cy

Production Efficiency Production

11Source: OGA

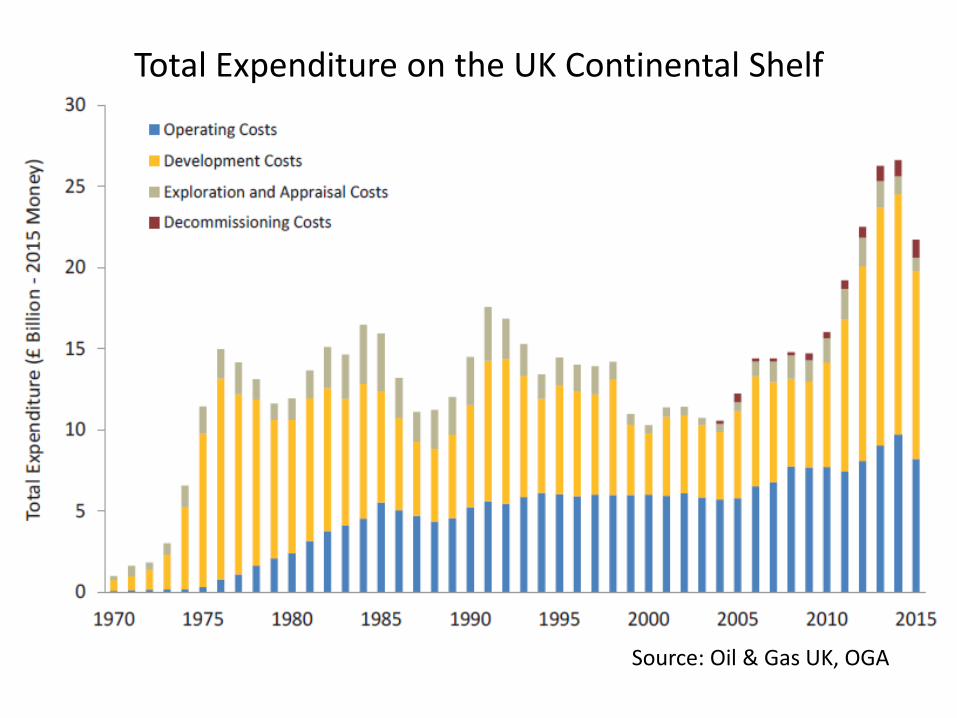

Total Expenditure on the UK Continental Shelf

Source: Oil & Gas UK, OGA

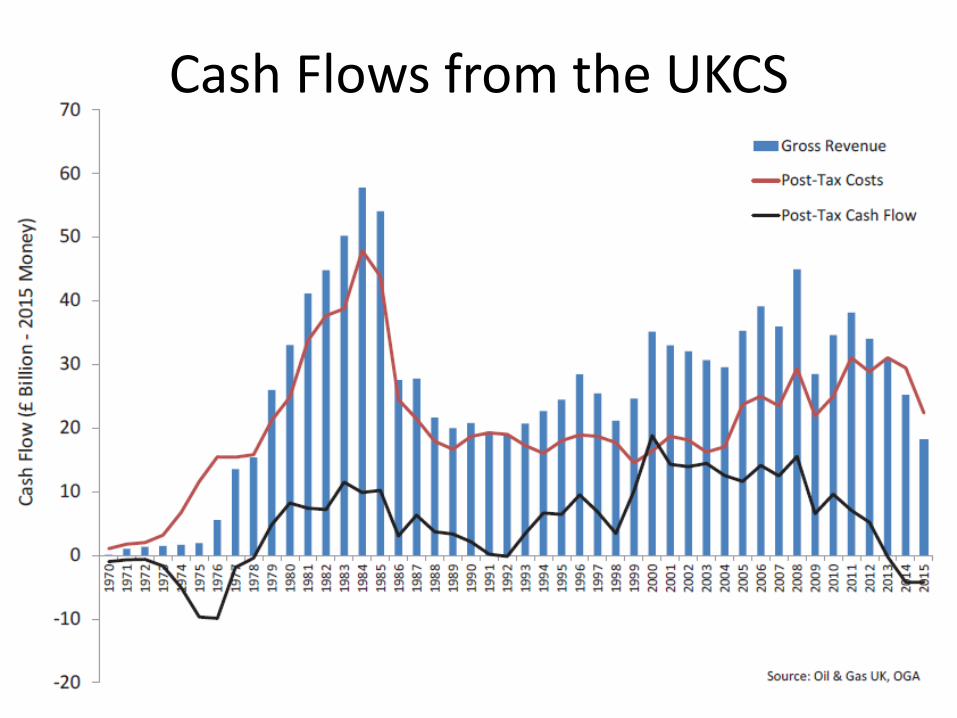

Cash Flows from the UKCS

Source: DECC

0

2

4

6

8

10

12

14

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Significant Discoveries

Significant Discoveries

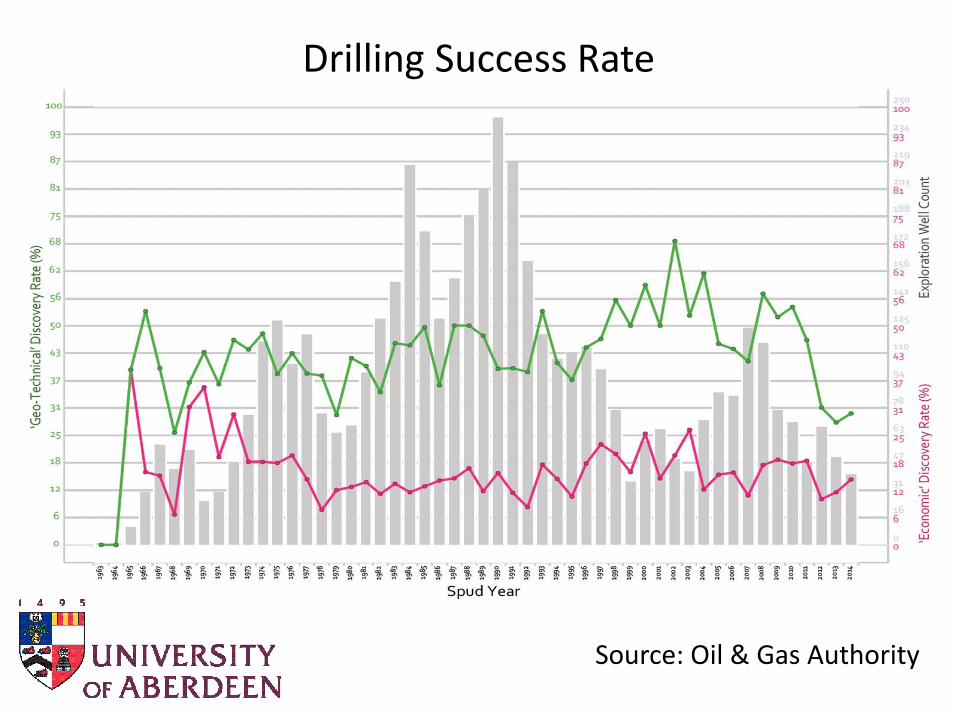

Drilling Success Rate

Source: Oil & Gas Authority

Budget 2015

• Basin-wide investment allowance to replace the existing offshore field allowances. Rate at 62.5% of investment expenditure from 1st

April 2015 onwards.

• Reduction in rate of SC to 20% from 1st

January 2015.

• Reduction in rate of PRT from 50% to 35% from 1st January 2016.

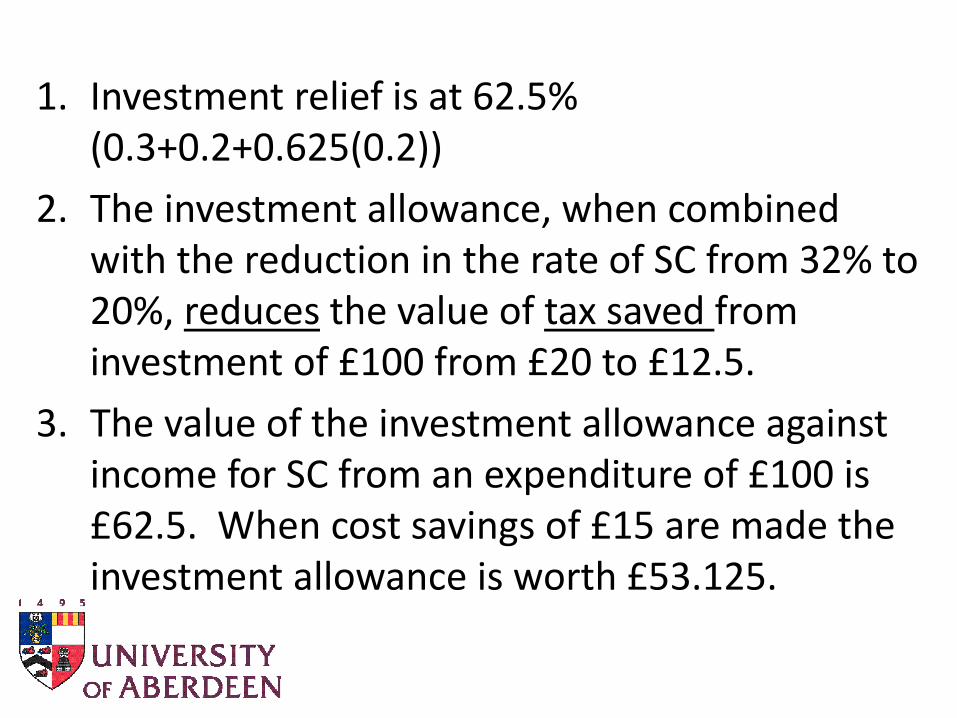

1. Investment relief is at 62.5% (0.3+0.2+0.625(0.2))

2. The investment allowance, when combined with the reduction in the rate of SC from 32% to 20%, reduces the value of tax saved from investment of £100 from £20 to £12.5.

3. The value of the investment allowance against income for SC from an expenditure of £100 is £62.5. When cost savings of £15 are made the investment allowance is worth £53.125.

$70, 45 pence Hurdle NPV/I > 0.32014 Tax System

Before Cost Reductions

0

5000

10000

15000

20000

25000

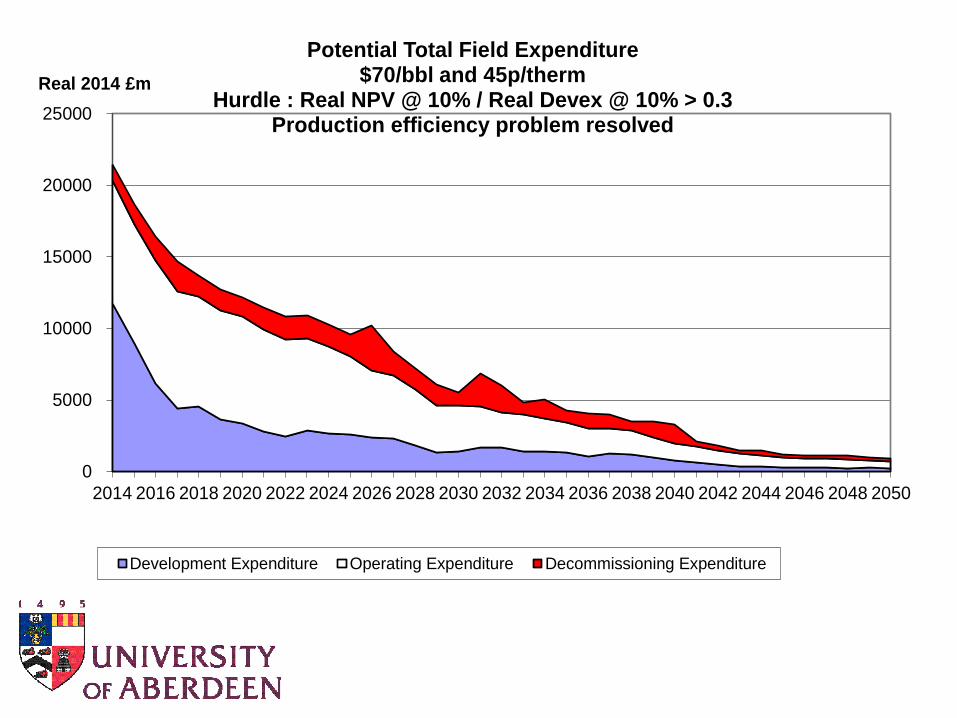

2014 2016 2018 2020 2022 2024 2026 2028 2030 2032 2034 2036 2038 2040 2042 2044 2046 2048 2050

Real 2014 £m

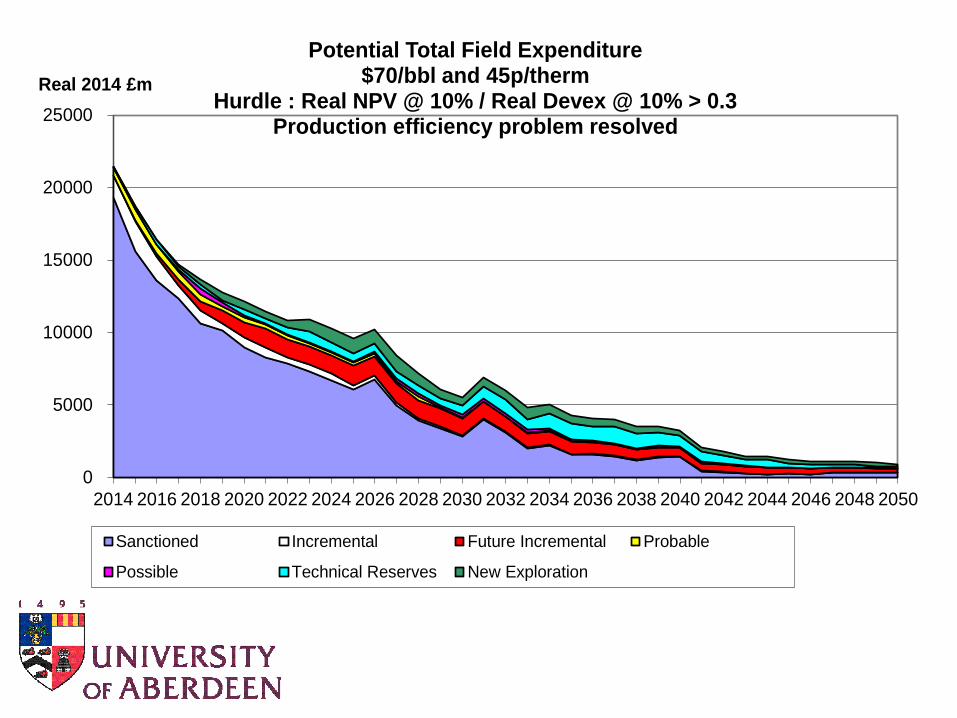

Potential Total Field Expenditure$70/bbl and 45p/therm

Hurdle : Real NPV @ 10% / Real Devex @ 10% > 0.3Production efficiency problem resolved

Sanctioned Incremental Future Incremental Probable

Possible Technical Reserves New Exploration

0

5000

10000

15000

20000

25000

2014 2016 2018 2020 2022 2024 2026 2028 2030 2032 2034 2036 2038 2040 2042 2044 2046 2048 2050

Real 2014 £m

Potential Total Field Expenditure$70/bbl and 45p/therm

Hurdle : Real NPV @ 10% / Real Devex @ 10% > 0.3Production efficiency problem resolved

Development Expenditure Operating Expenditure Decommissioning Expenditure

Cumulative Expenditures (£bn.2014)

Development 81.4

Operating 135.0

Decommissioning 41.8

TOTAL 258.2

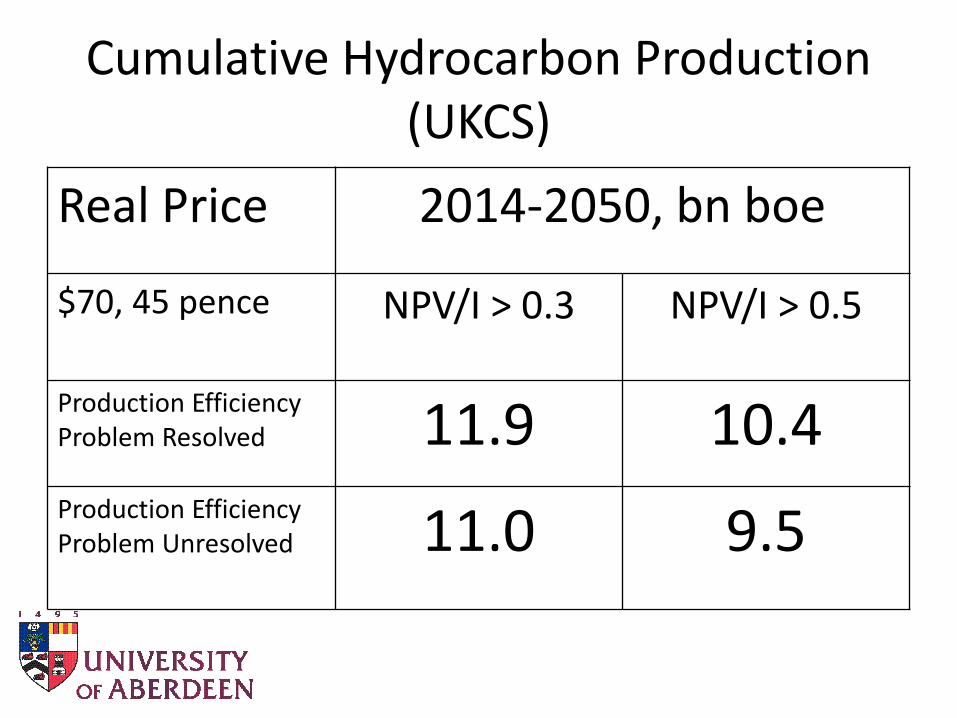

Cumulative Hydrocarbon Production (UKCS)

Real Price 2014-2050, bn boe

$70, 45 pence NPV/I > 0.3 NPV/I > 0.5

Production EfficiencyProblem Resolved 11.9 10.4Production EfficiencyProblem Unresolved 11.0 9.5

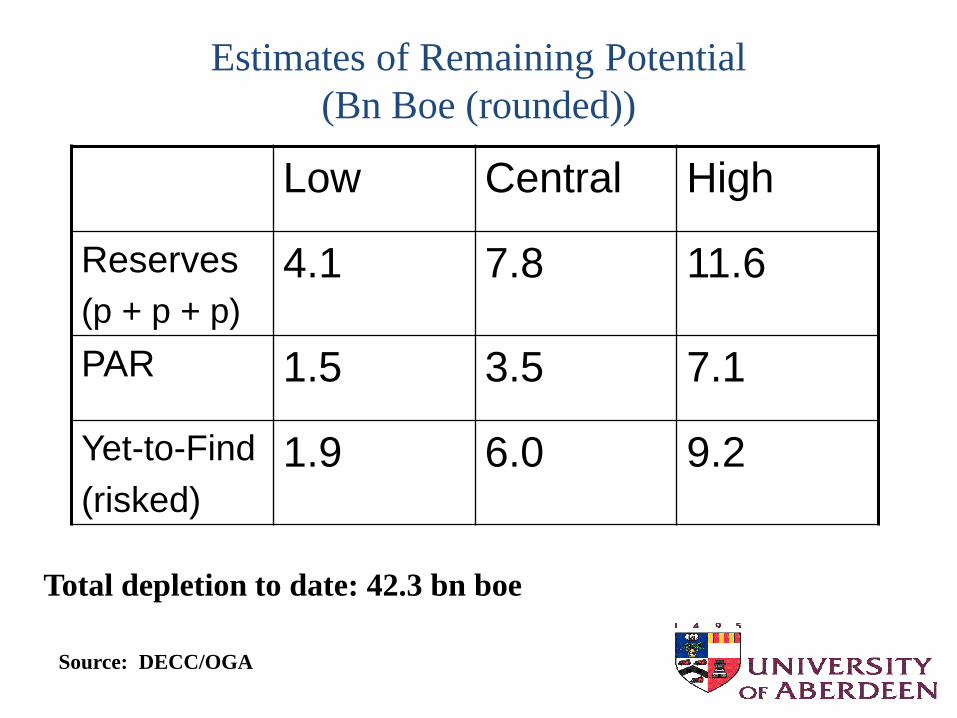

Estimates of Remaining Potential

(Bn Boe (rounded))

Total depletion to date: 42.3 bn boe

Source: DECC/OGA

Low Central High

Reserves

(p + p + p)

4.1 7.8 11.6

PAR 1.5 3.5 7.1

Yet-to-Find

(risked)

1.9 6.0 9.2

Source: Wood Mackenzie

Source: Oil & Gas UK

Daily Rig Rates Based on Reported Contract Awards for Mobile Drilling Units

Source: Wood Mackenzie

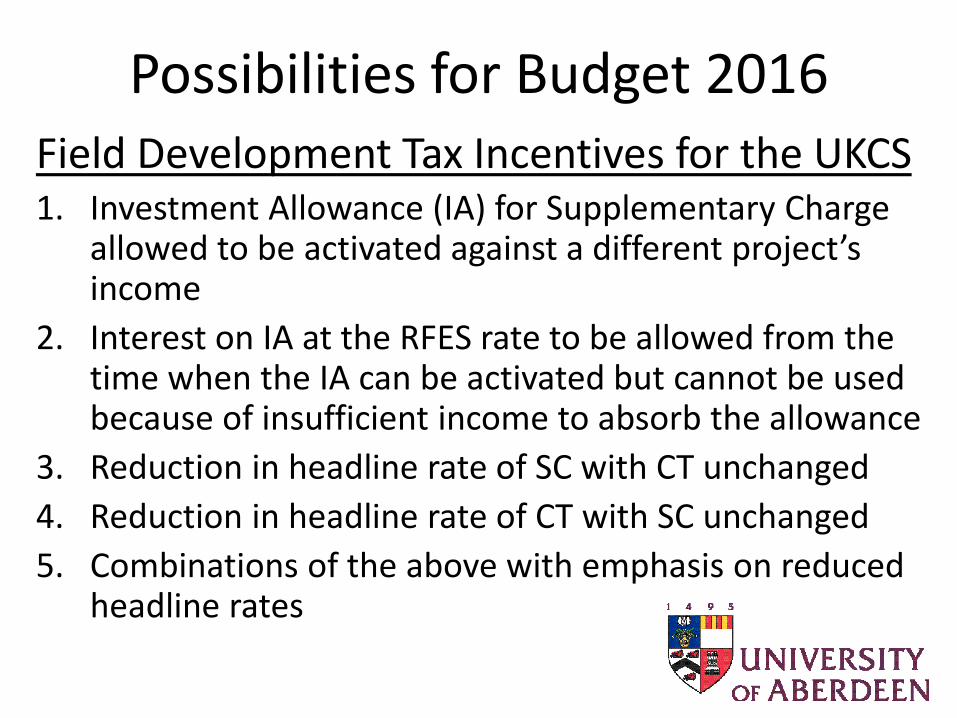

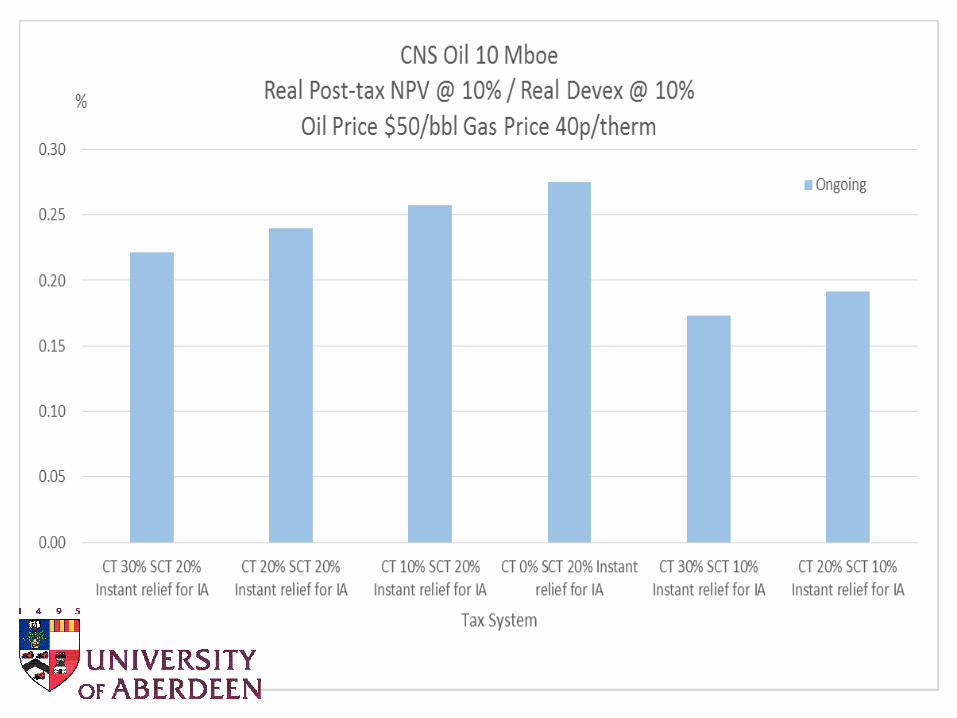

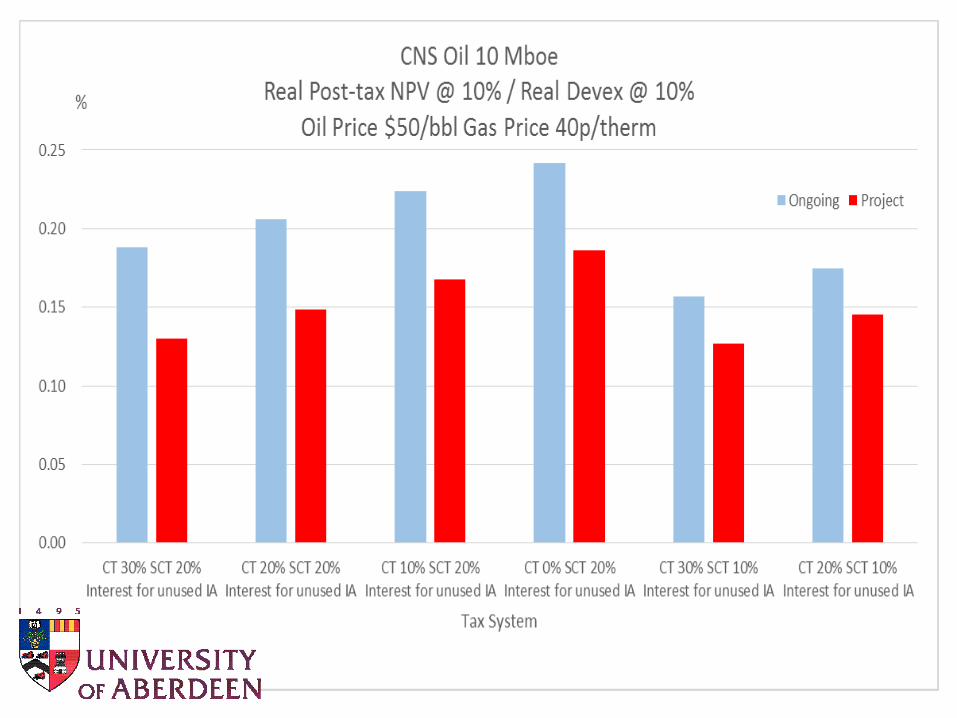

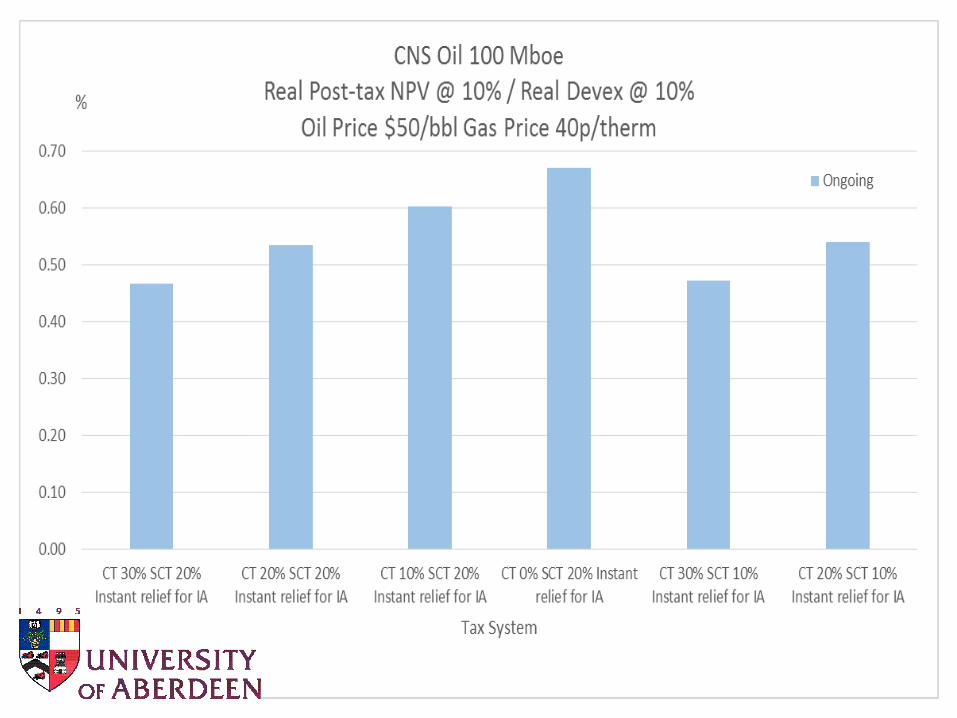

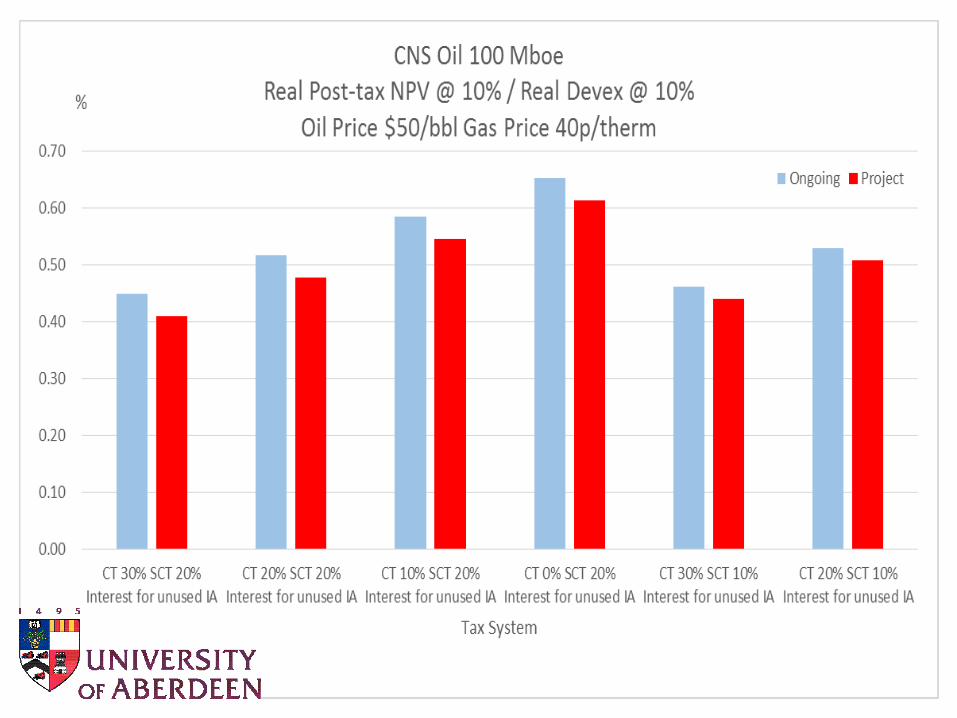

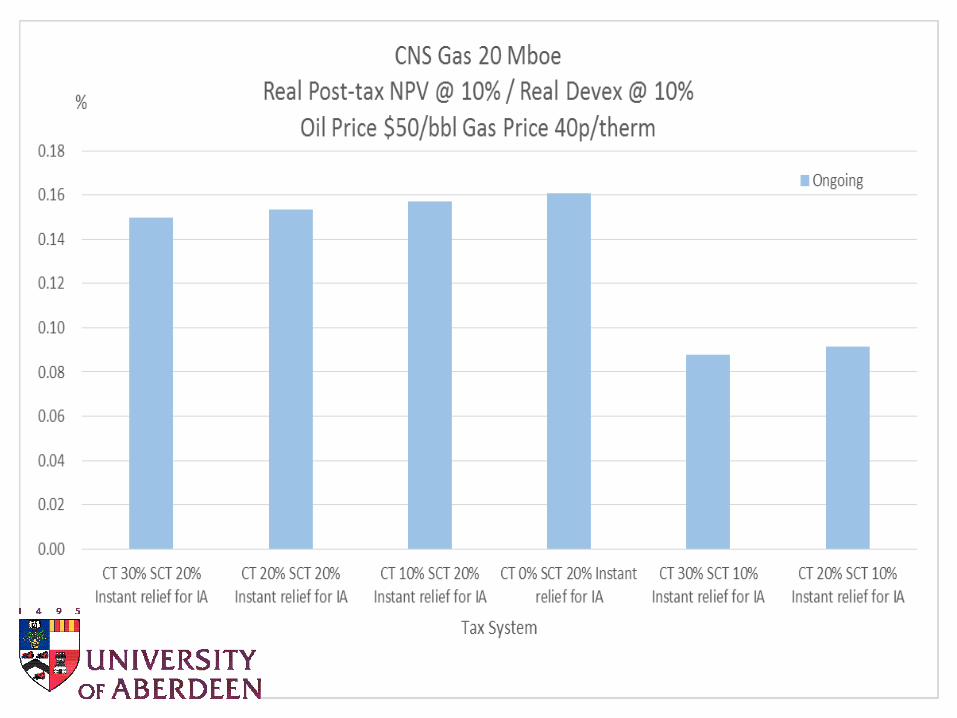

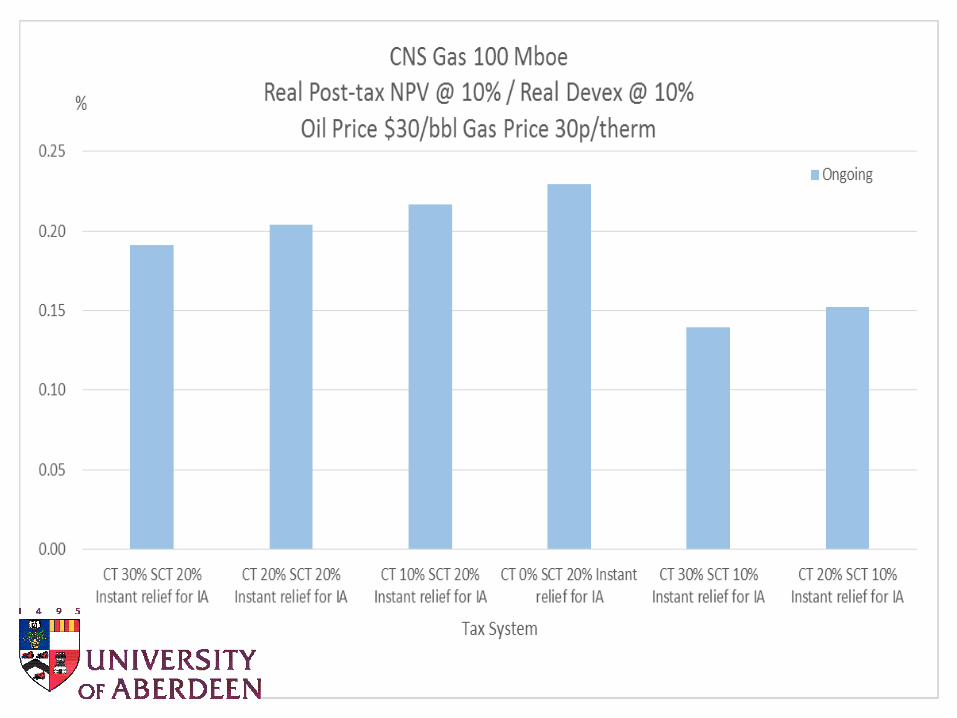

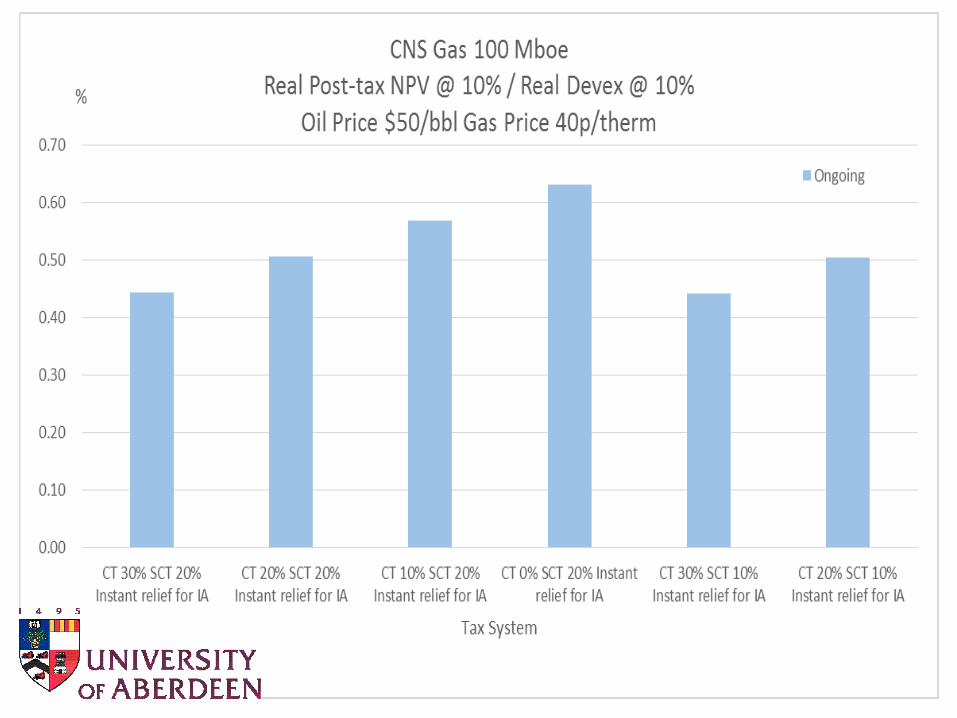

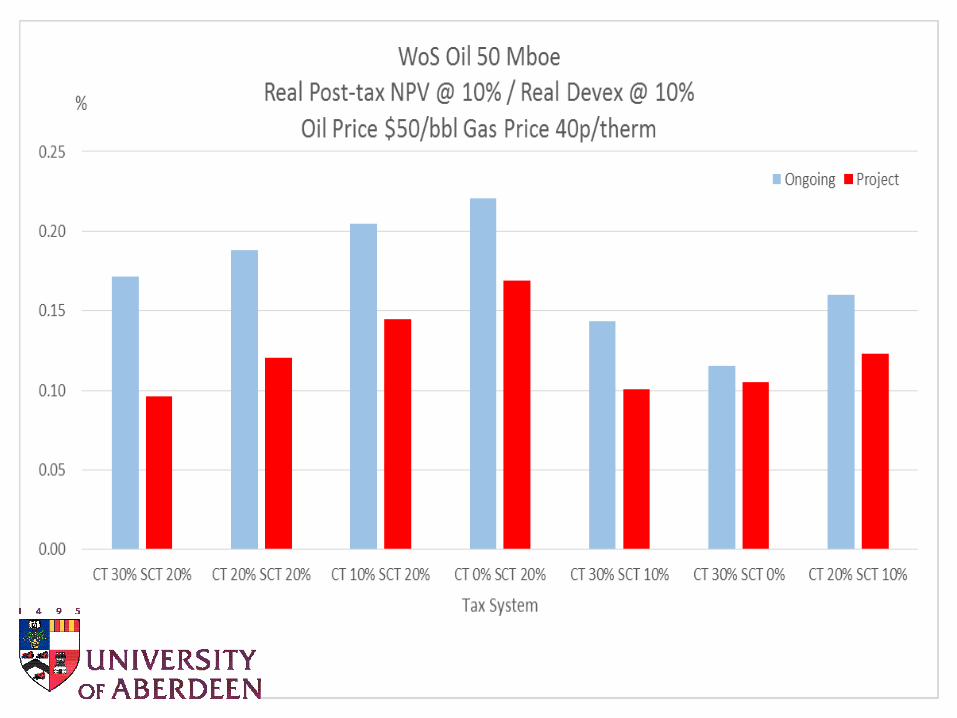

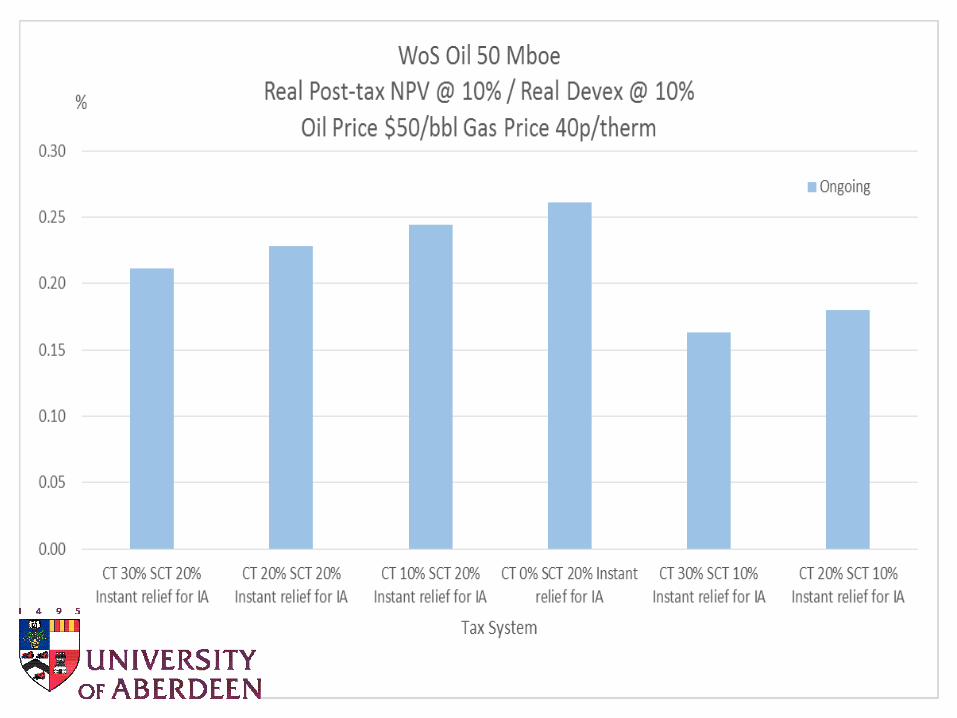

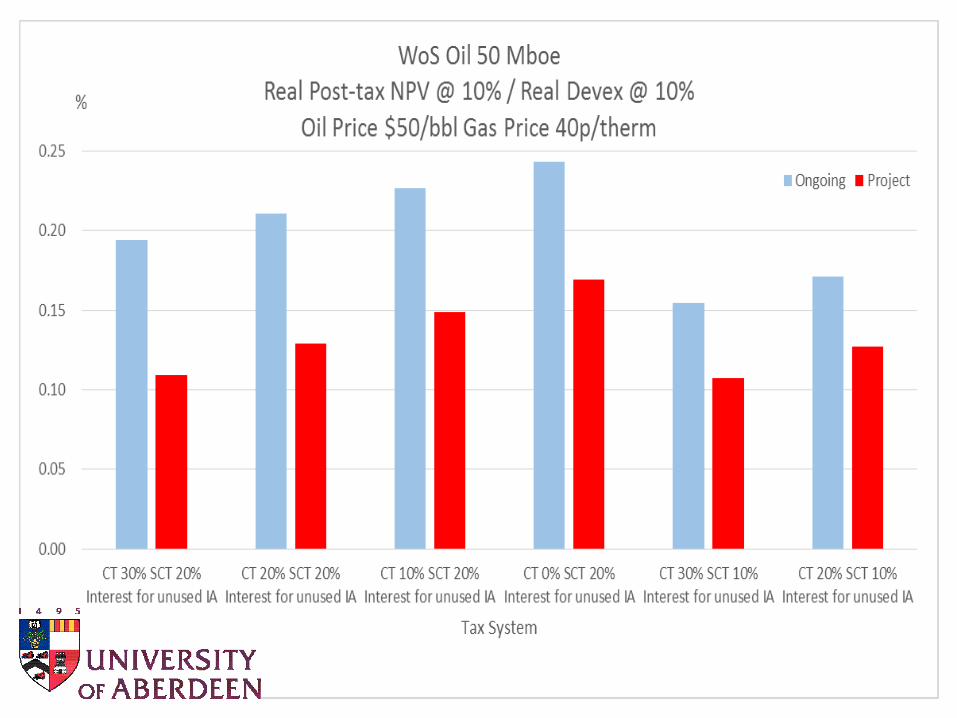

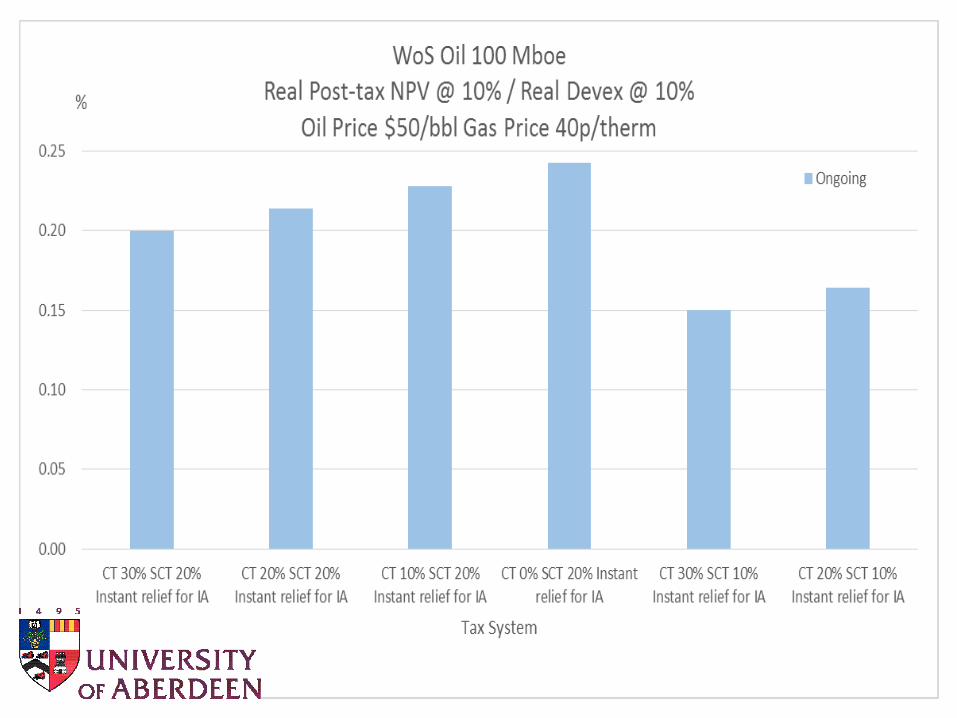

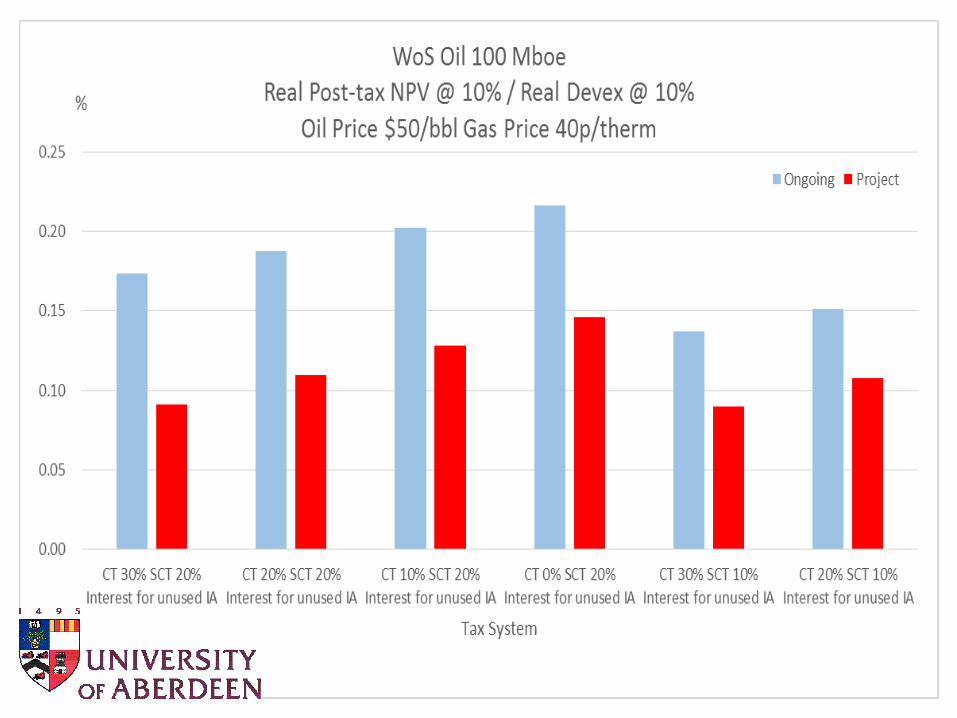

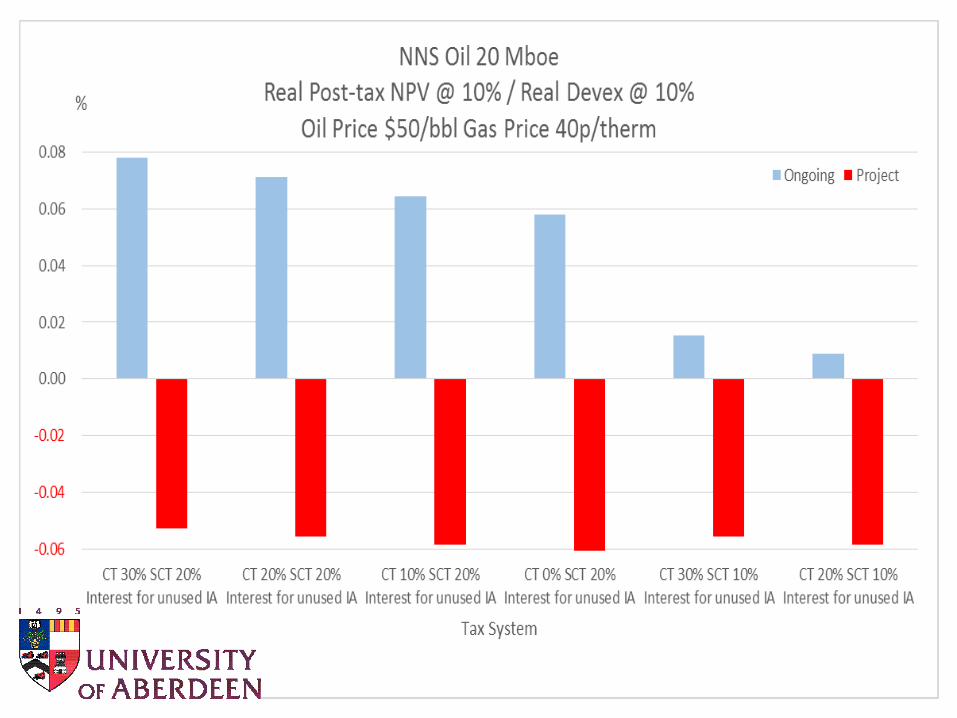

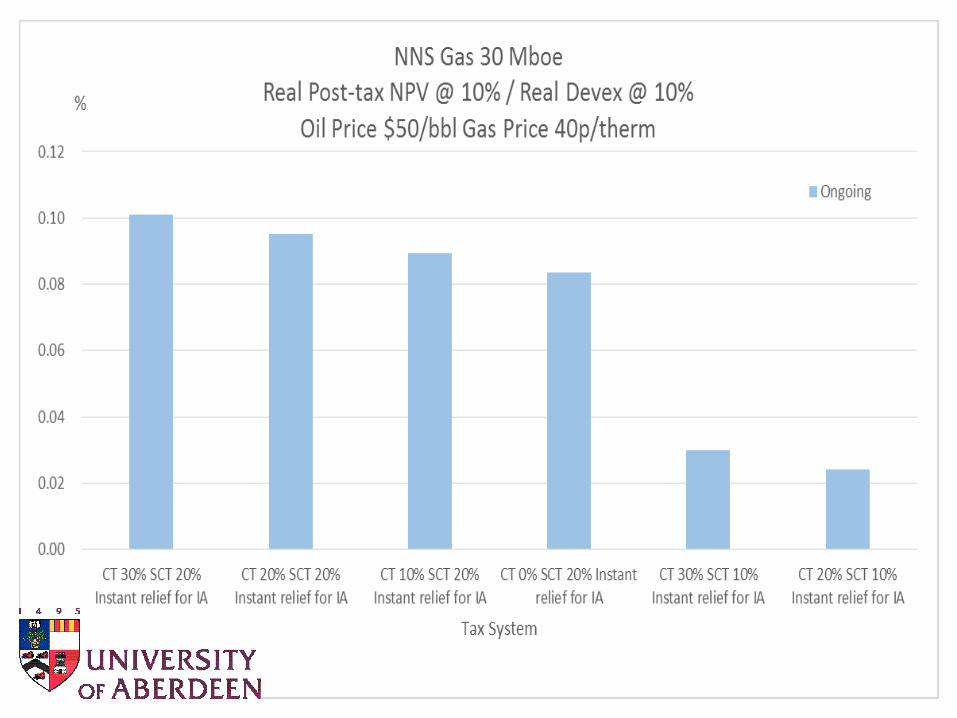

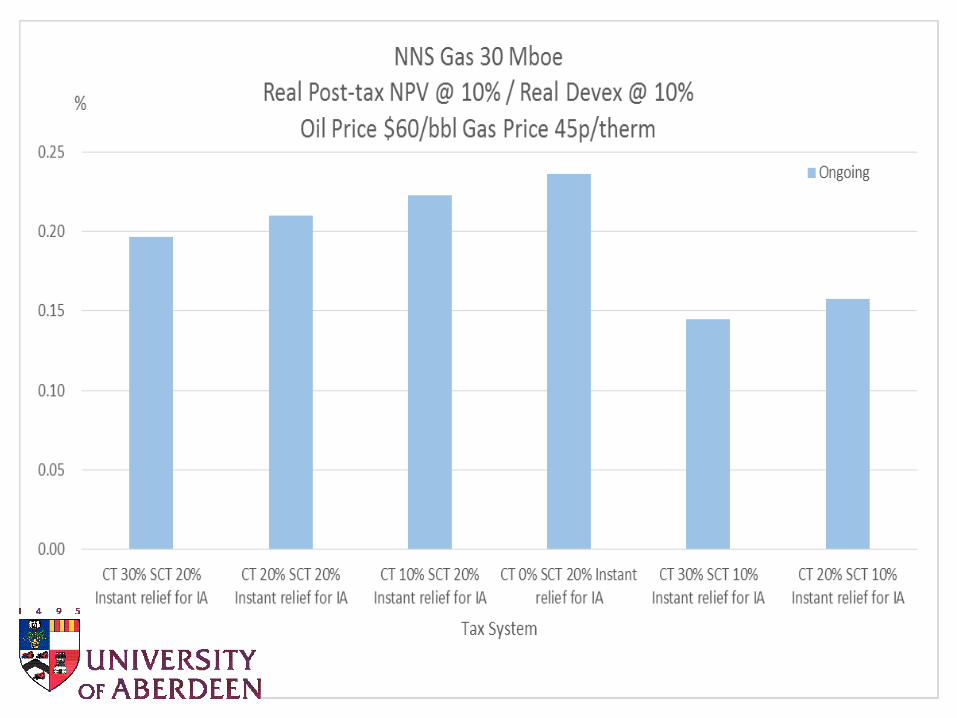

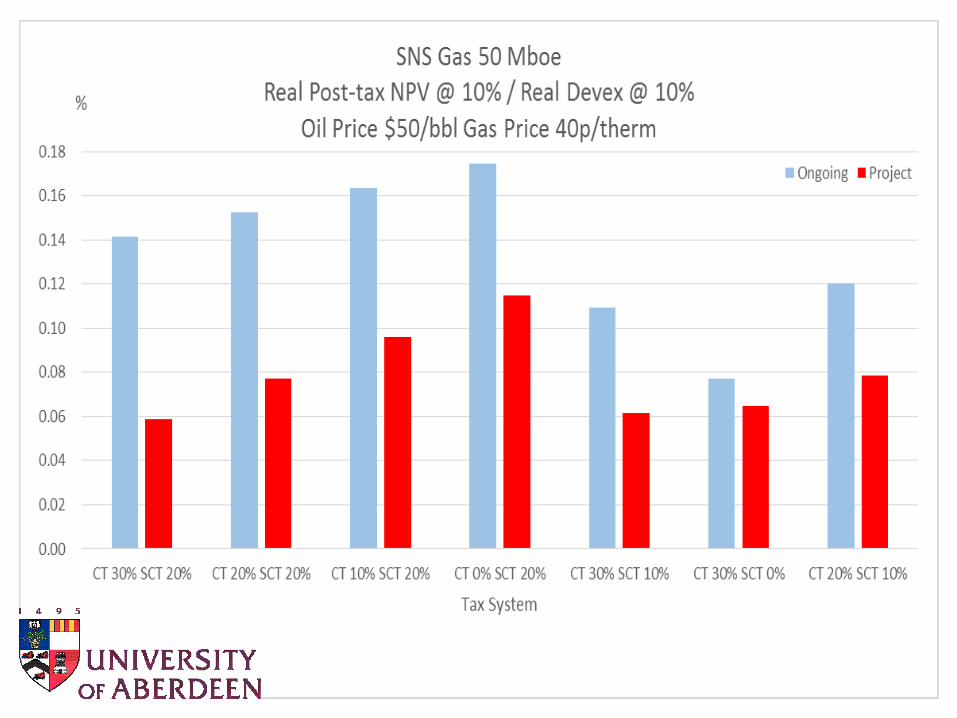

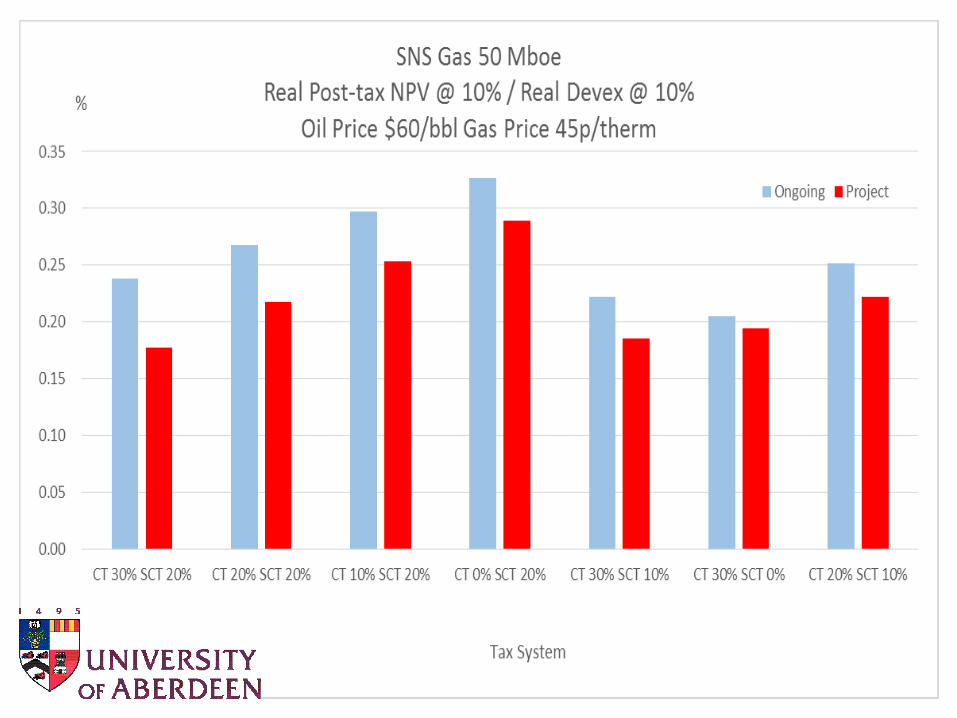

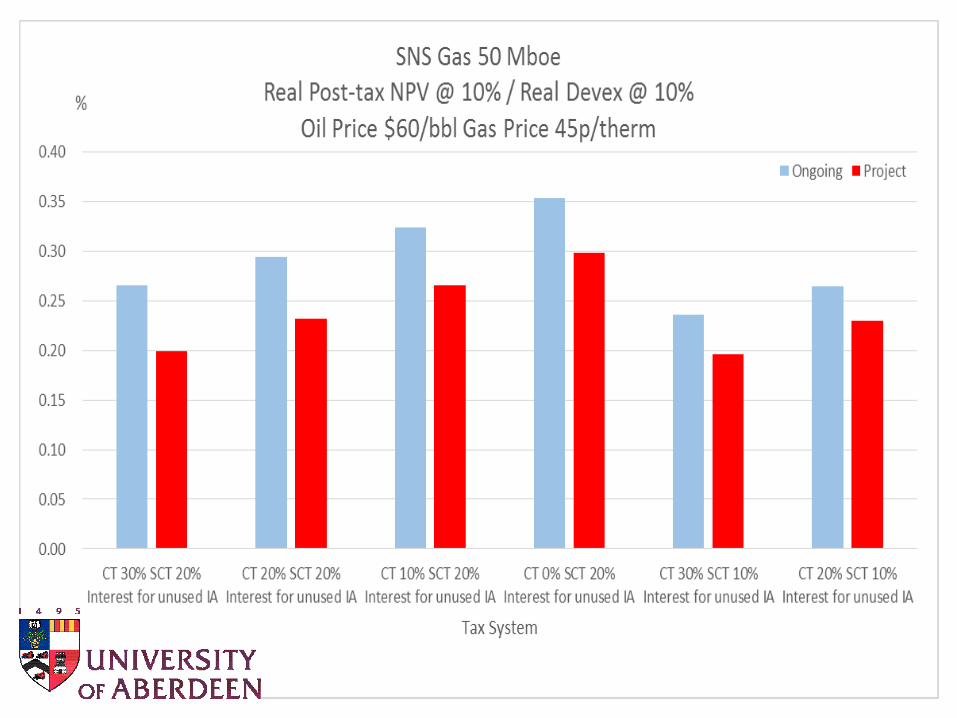

Possibilities for Budget 2016Field Development Tax Incentives for the UKCS1. Investment Allowance (IA) for Supplementary Charge

allowed to be activated against a different project’s income

2. Interest on IA at the RFES rate to be allowed from the time when the IA can be activated but cannot be used because of insufficient income to absorb the allowance

3. Reduction in headline rate of SC with CT unchanged

4. Reduction in headline rate of CT with SC unchanged

5. Combinations of the above with emphasis on reduced headline rates

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

10 Oil CNS 20 Oil CNS 30 Oil CNS 50 Oil CNS 100 OilCNS

20 GasCNS

100 GasCNS

50 OilWoS

100 OilWoS

100 GasWoS

10 Oil NNS20 Oil NNS50 Oil NNS 100 OilNNS

30 GasNNS

10 GasSNS

20 GasSNS

50 GasSNS

%

Real Pre-tax NPV @ 10% / Real Devex @ 10%Oil Price $30/bbl Gas Price 30p/therm

Real Pre-tax @ 10%/ Real Devex @ 10%

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

10 Oil CNS20 Oil CNS30 Oil CNS50 Oil CNS 100 OilCNS

20 GasCNS

100 GasCNS

50 OilWoS

100 OilWoS

100 GasWoS

10 OilNNS

20 OilNNS

50 OilNNS

100 OilNNS

30 GasNNS

10 GasSNS

20 GasSNS

50 GasSNS

%

Real Pre-tax NPV @ 10% / Real Devex @ 10%Oil Price $50/bbl Gas Price 40p/therm

Real Pre-tax @ 10%/ Real Devex @ 10%

-0.5

0

0.5

1

1.5

2

2.5

10 Oil CNS20 Oil CNS30 Oil CNS50 Oil CNS 100 OilCNS

20 GasCNS

100 GasCNS

50 OilWoS

100 OilWoS

100 GasWoS

10 OilNNS

20 OilNNS

50 OilNNS

100 OilNNS

30 GasNNS

10 GasSNS

20 GasSNS

50 GasSNS

%

Real Pre-tax NPV @ 10% / Real Devex @ 10%Oil Price $60/bbl Gas Price 45p/therm

Real Pre-tax @ 10%/ Real Devex @ 10%

Conclusions1. Boom in period 2009-2014 concealed from the supply

chain emergence of problems in UKCS associated with maturity of the province. Serious cost inflation in that period added significantly to costs per boe. Collapse of oil price greatly exacerbated financial difficulties.

2. Remaining physical potential remains substantial.

3. At $30 or $35 price new field investments are generally uneconomic before tax.

4. At $50-$60 prices a combination of substantial cost reductions plus worthwhile tax reliefs can incentivise significant numbers of new field developments.