ada number of pages : 5 total marks: 100 number of...

TRANSCRIPT

ADA

Number of Pages : 5 Total Marks: 100

Number of Questions: 6 Time Allowed: 3 Hrs

Answer all questions Working notes should form part of the answer.

Wherever necessary, suitable assumptions may be made by the candidates.

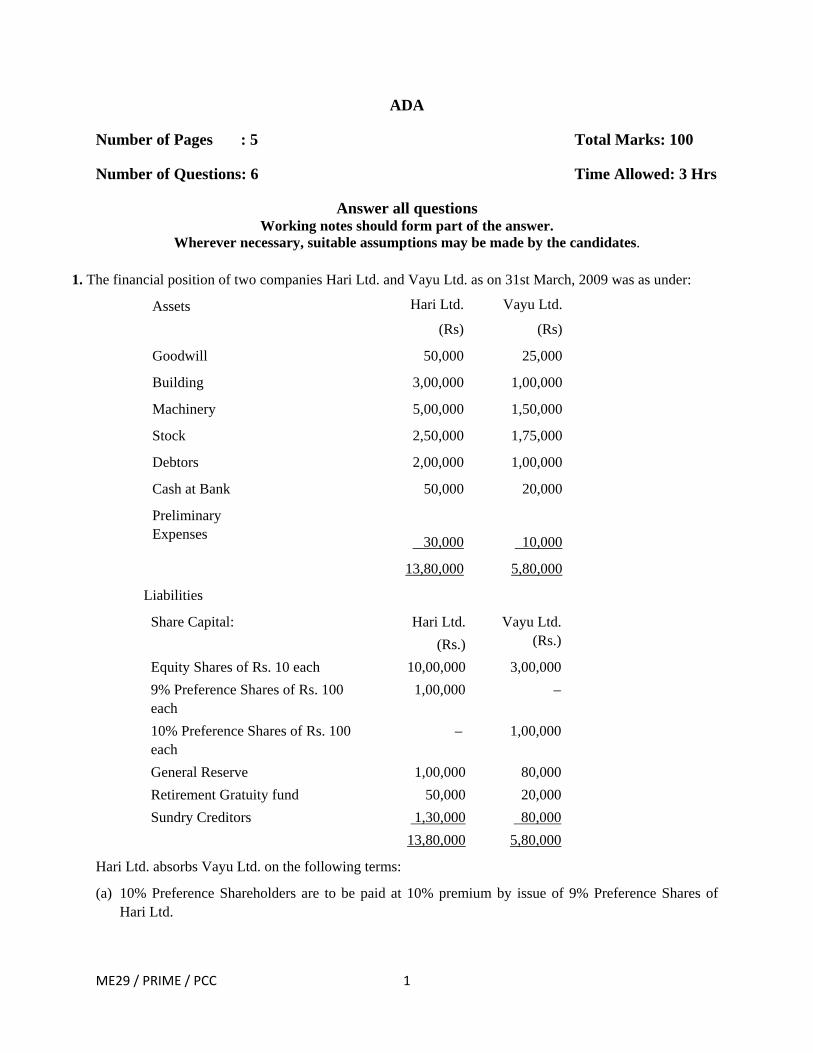

1. The financial position of two companies Hari Ltd. and Vayu Ltd. as on 31st March, 2009 was as under:

Assets Hari Ltd.

(Rs)

Vayu Ltd.

(Rs)

Goodwill 50,000 25,000

Building 3,00,000 1,00,000

Machinery 5,00,000 1,50,000

Stock 2,50,000 1,75,000

Debtors 2,00,000 1,00,000

Cash at Bank 50,000 20,000

Preliminary Expenses

30,000

10,000

13,80,000 5,80,000

Liabilities

Share Capital: Hari Ltd.

(Rs.)

Vayu Ltd. (Rs.)

Equity Shares of Rs. 10 each 10,00,000 3,00,000

9% Preference Shares of Rs. 100 each

1,00,000 –

10% Preference Shares of Rs. 100 each

– 1,00,000

General Reserve 1,00,000 80,000

Retirement Gratuity fund 50,000 20,000

Sundry Creditors 1,30,000 80,000

13,80,000 5,80,000

Hari Ltd. absorbs Vayu Ltd. on the following terms:

(a) 10% Preference Shareholders are to be paid at 10% premium by issue of 9% Preference Shares of Hari Ltd.

ME29 / PRIME / PCC 1

(b) Goodwill of Vayu Ltd. is valued at Rs. 50,000, Buildings are valued at Rs. 1,50,000 and the Machinery at Rs. 1,60,000.

(c) Stock to be taken over at 10% less value and Reserve for Bad and Doubtful Debts to be created @ 7.5%.

(d) Equity Shareholders of Vayu Ltd. will be issued Equity Shares @ 5% premium.

Prepare necessary Ledger Accounts to close the books of Vayu Ltd. and show the acquisition entries in the books of Hari Ltd. Also draft the Balance Sheet after absorption as at 31st March, 2009.

(20 Marks)

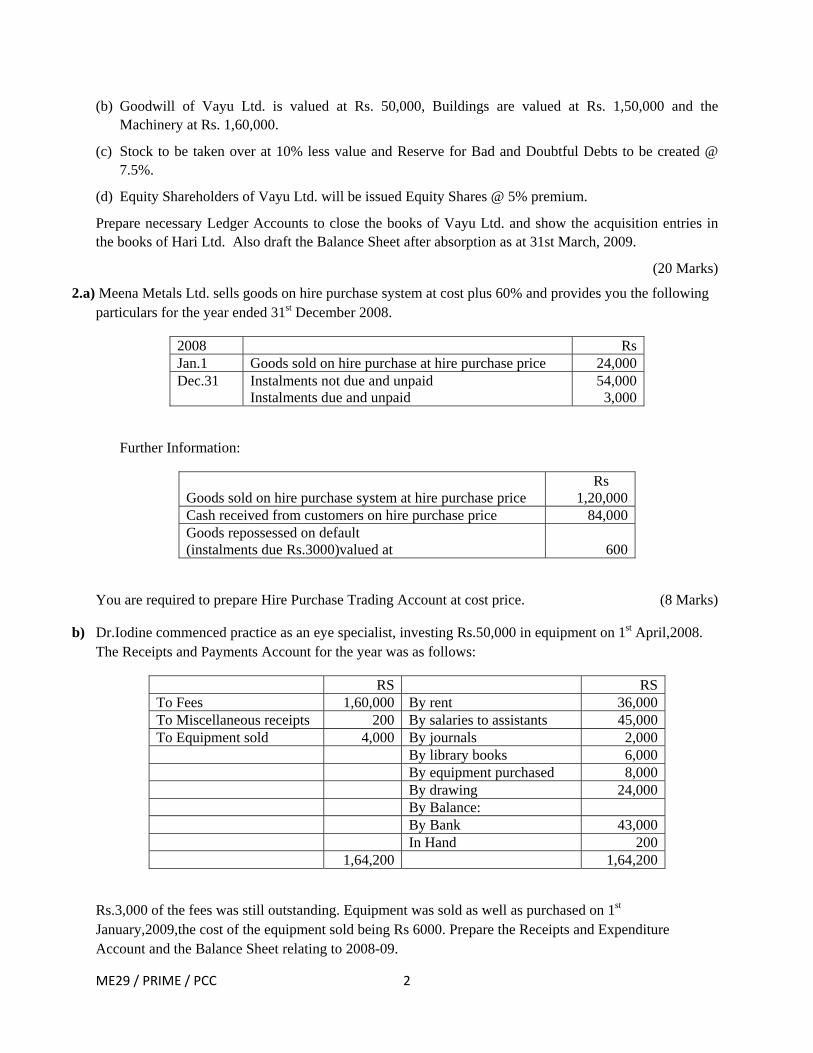

2.a) Meena Metals Ltd. sells goods on hire purchase system at cost plus 60% and provides you the following particulars for the year ended 31st December 2008.

2008 Rs Jan.1 Goods sold on hire purchase at hire purchase price 24,000 Dec.31 Instalments not due and unpaid

Instalments due and unpaid 54,000

3,000

Further Information:

Goods sold on hire purchase system at hire purchase price

Rs 1,20,000

Cash received from customers on hire purchase price 84,000 Goods repossessed on default (instalments due Rs.3000)valued at

600

You are required to prepare Hire Purchase Trading Account at cost price. (8 Marks)

b) Dr.Iodine commenced practice as an eye specialist, investing Rs.50,000 in equipment on 1st April,2008. The Receipts and Payments Account for the year was as follows:

RS RSTo Fees 1,60,000 By rent 36,000To Miscellaneous receipts 200 By salaries to assistants 45,000To Equipment sold 4,000 By journals 2,000 By library books 6,000 By equipment purchased 8,000 By drawing 24,000 By Balance: By Bank 43,000 In Hand 200 1,64,200 1,64,200

Rs.3,000 of the fees was still outstanding. Equipment was sold as well as purchased on 1st January,2009,the cost of the equipment sold being Rs 6000. Prepare the Receipts and Expenditure Account and the Balance Sheet relating to 2008-09.

ME29 / PRIME / PCC 2

(8 Marks)

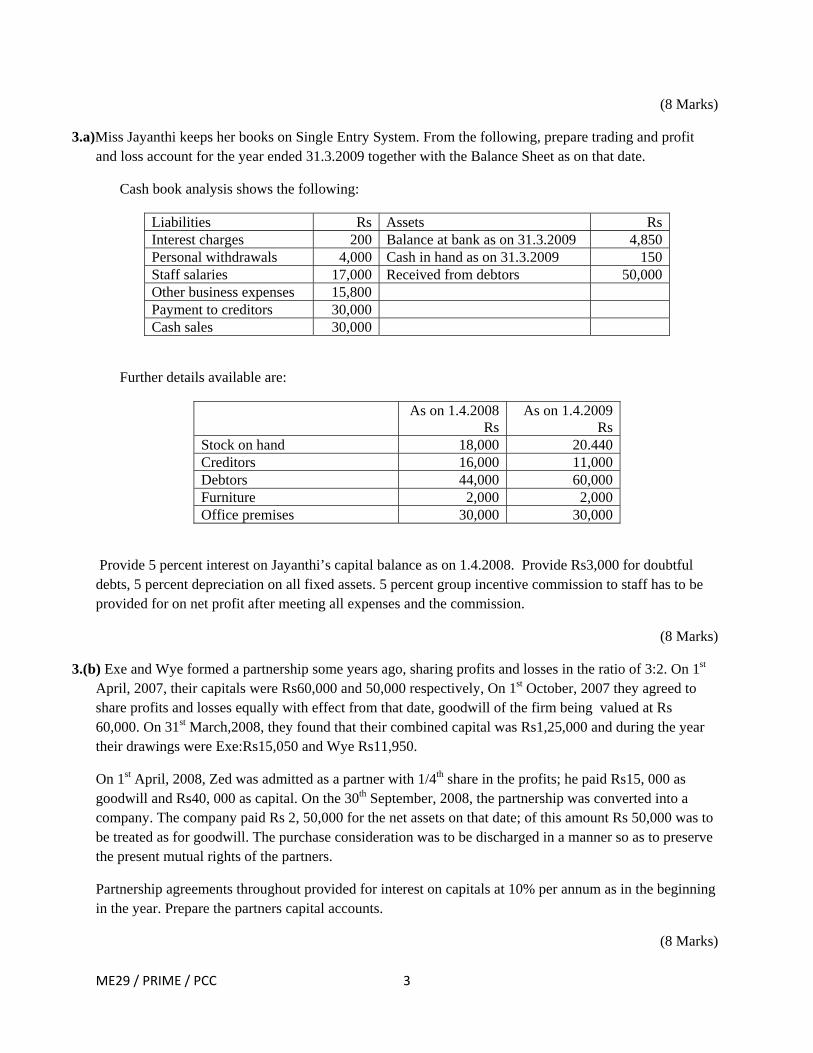

3.a)Miss Jayanthi keeps her books on Single Entry System. From the following, prepare trading and profit and loss account for the year ended 31.3.2009 together with the Balance Sheet as on that date.

Cash book analysis shows the following:

Liabilities Rs Assets RsInterest charges 200 Balance at bank as on 31.3.2009 4,850Personal withdrawals 4,000 Cash in hand as on 31.3.2009 150Staff salaries 17,000 Received from debtors 50,000Other business expenses 15,800 Payment to creditors 30,000 Cash sales 30,000

Further details available are:

As on 1.4.2008 Rs

As on 1.4.2009 Rs

Stock on hand 18,000 20.440 Creditors 16,000 11,000 Debtors 44,000 60,000 Furniture 2,000 2,000 Office premises 30,000 30,000

Provide 5 percent interest on Jayanthi’s capital balance as on 1.4.2008. Provide Rs3,000 for doubtful debts, 5 percent depreciation on all fixed assets. 5 percent group incentive commission to staff has to be provided for on net profit after meeting all expenses and the commission.

(8 Marks)

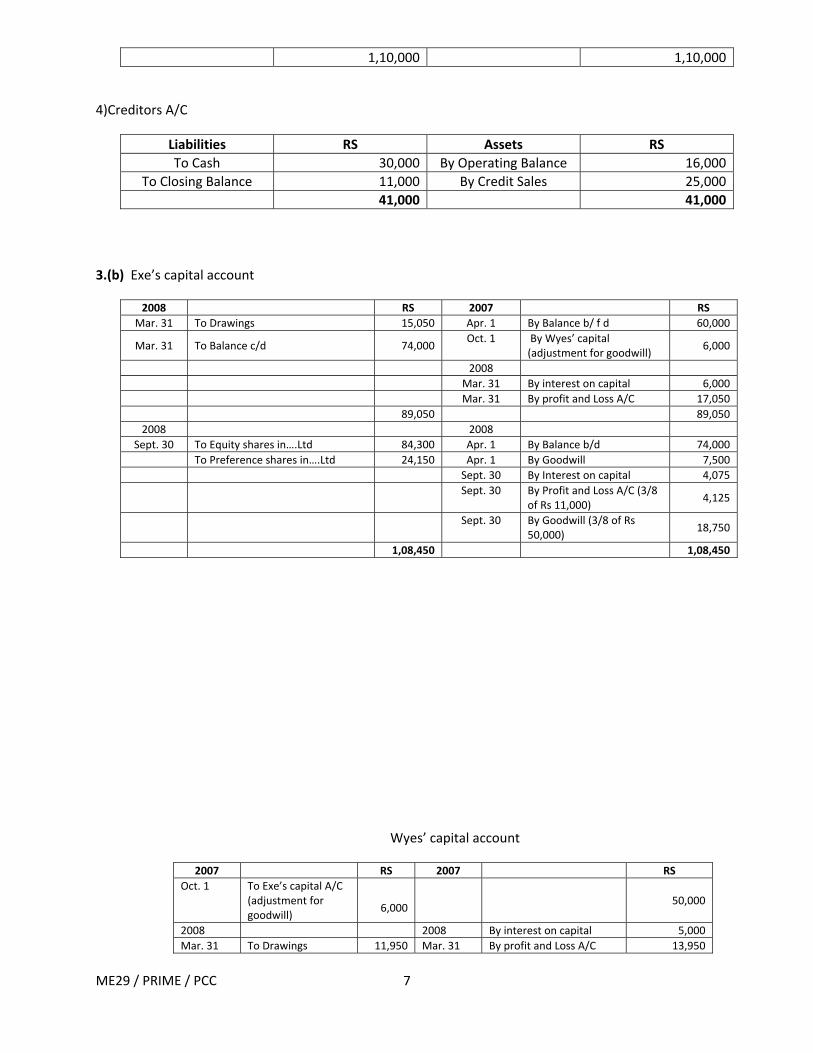

3.(b) Exe and Wye formed a partnership some years ago, sharing profits and losses in the ratio of 3:2. On 1st April, 2007, their capitals were Rs60,000 and 50,000 respectively, On 1st October, 2007 they agreed to share profits and losses equally with effect from that date, goodwill of the firm being valued at Rs 60,000. On 31st March,2008, they found that their combined capital was Rs1,25,000 and during the year their drawings were Exe:Rs15,050 and Wye Rs11,950.

On 1st April, 2008, Zed was admitted as a partner with 1/4th share in the profits; he paid Rs15, 000 as goodwill and Rs40, 000 as capital. On the 30th September, 2008, the partnership was converted into a company. The company paid Rs 2, 50,000 for the net assets on that date; of this amount Rs 50,000 was to be treated as for goodwill. The purchase consideration was to be discharged in a manner so as to preserve the present mutual rights of the partners.

Partnership agreements throughout provided for interest on capitals at 10% per annum as in the beginning in the year. Prepare the partners capital accounts.

(8 Marks)

ME29 / PRIME / PCC 3

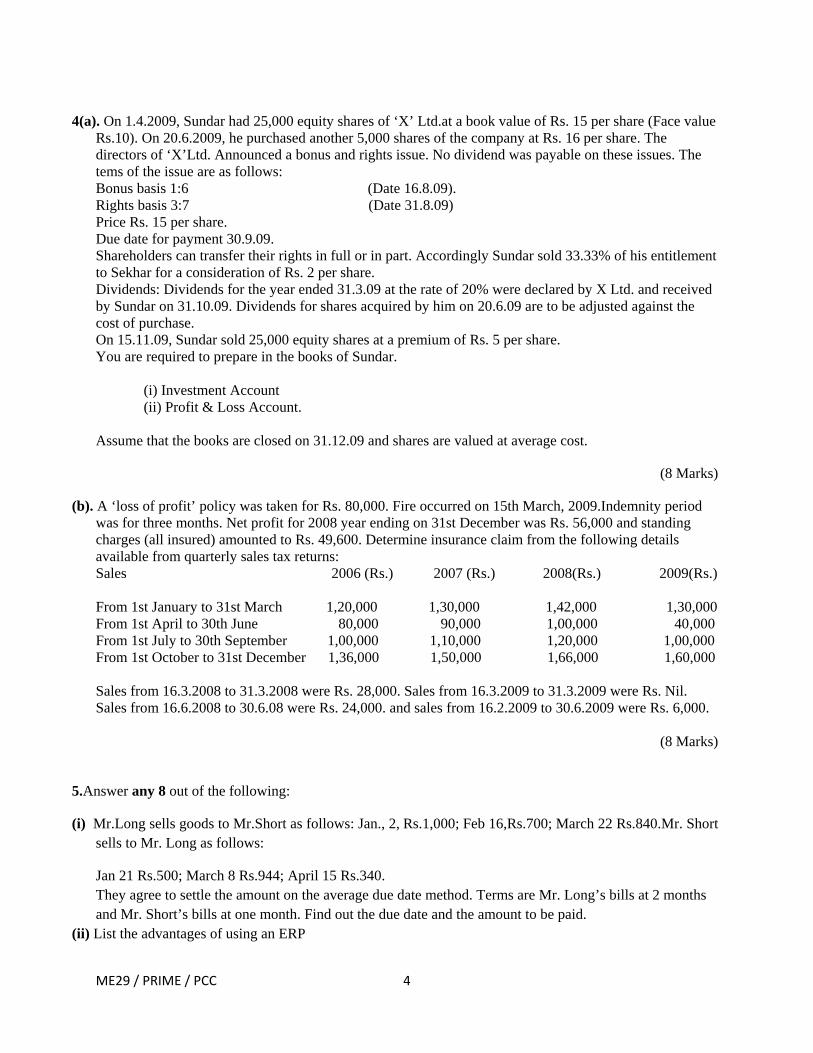

4(a). On 1.4.2009, Sundar had 25,000 equity shares of ‘X’ Ltd.at a book value of Rs. 15 per share (Face value

Rs.10). On 20.6.2009, he purchased another 5,000 shares of the company at Rs. 16 per share. The directors of ‘X’Ltd. Announced a bonus and rights issue. No dividend was payable on these issues. The tems of the issue are as follows: Bonus basis 1:6 (Date 16.8.09). Rights basis 3:7 (Date 31.8.09) Price Rs. 15 per share. Due date for payment 30.9.09. Shareholders can transfer their rights in full or in part. Accordingly Sundar sold 33.33% of his entitlement to Sekhar for a consideration of Rs. 2 per share. Dividends: Dividends for the year ended 31.3.09 at the rate of 20% were declared by X Ltd. and received by Sundar on 31.10.09. Dividends for shares acquired by him on 20.6.09 are to be adjusted against the cost of purchase. On 15.11.09, Sundar sold 25,000 equity shares at a premium of Rs. 5 per share. You are required to prepare in the books of Sundar.

(i) Investment Account (ii) Profit & Loss Account.

Assume that the books are closed on 31.12.09 and shares are valued at average cost.

(8 Marks)

(b). A ‘loss of profit’ policy was taken for Rs. 80,000. Fire occurred on 15th March, 2009.Indemnity period was for three months. Net profit for 2008 year ending on 31st December was Rs. 56,000 and standing charges (all insured) amounted to Rs. 49,600. Determine insurance claim from the following details available from quarterly sales tax returns: Sales 2006 (Rs.) 2007 (Rs.) 2008(Rs.) 2009(Rs.) From 1st January to 31st March 1,20,000 1,30,000 1,42,000 1,30,000 From 1st April to 30th June 80,000 90,000 1,00,000 40,000 From 1st July to 30th September 1,00,000 1,10,000 1,20,000 1,00,000 From 1st October to 31st December 1,36,000 1,50,000 1,66,000 1,60,000 Sales from 16.3.2008 to 31.3.2008 were Rs. 28,000. Sales from 16.3.2009 to 31.3.2009 were Rs. Nil. Sales from 16.6.2008 to 30.6.08 were Rs. 24,000. and sales from 16.2.2009 to 30.6.2009 were Rs. 6,000.

(8 Marks)

5.Answer any 8 out of the following:

(i) Mr.Long sells goods to Mr.Short as follows: Jan., 2, Rs.1,000; Feb 16,Rs.700; March 22 Rs.840.Mr. Short sells to Mr. Long as follows:

Jan 21 Rs.500; March 8 Rs.944; April 15 Rs.340. They agree to settle the amount on the average due date method. Terms are Mr. Long’s bills at 2 months and Mr. Short’s bills at one month. Find out the due date and the amount to be paid.

(ii) List the advantages of using an ERP

ME29 / PRIME / PCC 4

ME29 / PRIME / PCC 5

(iii) Ashok and Bhushan started business on 1st July, 2008, without any partnership deed. They introduced capital of Rs.40,000 and Rs.70,000 respectively. On 1st October, 2008, Bhushan advanced Rs.30,000 as loan to the firm. The profit & loss account for the year ending 31st March, 2009, discloses a profit of Rs.24,900, but the partners cannot be agree upon the question of interest and profit sharing ratio. You are requested to distribute the profit between them as per the partnership Act, 1932.

(iv) Arun and Barun are partners in the ratio of 3:2. They admit Chaman for 1/4th share. In future the ratio between Arun and Barun would be 1:1. Calculate new profit sharing ratio and sacrificing ratio.

(v) The company deals in three products, A, B and C, which are neither similar nor interchangeable. At the time of closing of its account for the year 2008-09. The Historical Cost and Net Realizable Value of the items of closing stock are determined as follows:

Items Historical Cost (Rs. in lakhs) Net Realisable Value (Rs. in lakhs) A 40 28 B 32 32 C 16 24

What will be the value of Closing Stock? .

(vi) Name four areas in which different accounting policies may be adopted.

(vii) How are self constructed fixed assets valued?

(viii) Ram Ltd. Purchased a land for Rs.50 lakhs.On purchase of the assets government granted it a grant for

Rs.10 lakhs.Grant was considered as refundable in the end of the 2nd year to the extent of Rs.7,00,000.Pass journal entry for the refund of the grant.

(ix) What is the accounting treatment for interest on own debentures.

(x) Advantages of self balancing ledgers.

(8 x 2=16 Marks)

6. Answer any four questions: (i) Write a short note on “Pre incorporation profits” (ii) Valuation of investments for the purpose of balance sheet. (iii) Non performing assets and its valuation. (iv) List B contributories (v) Heera Ltd. has two divisions. It provides depreciation for both divisions on straight line basis as per rates

prescribed by Schedule XIV to the Companies Act. While finalizing the accounts for the year ended 31-3-2007, it however wants to change the method to Written Down Value method for one of its divisions since in the opinion of the management the assets of the said division suffer faster wear andtear. Please advise the company on the above and also whether the change should be prospective or retrospective.

(4 x 4=16 Marks)

PRIME ACADEMY 29TH SESSION MODEL EXAM

PCC – ADVANCE ACCOUNTING SUGGESTED ANSWERS

1.

In the Books of Vayu Ltd. Realisation Account

Rs. Rs.

To Sundry Assets (5,80,000 – 10,000) 5,70,000 By Gratuity Fund 20,000

To Preference Shareholders

(Premium on Redemption)

10,000

By

By

Sundry Creditors

Hari Ltd.

80,000

To Equity Shareholders (Purchase Consideration) 5,30,000

(Profit on Realisation) 50,000

6,30,000 6,30,000

Equity Shareholders Account

Rs. Rs.

To Preliminary Expenses 10,000 By Share Capital 3,00,000

To Equity Shares of Hari Ltd. 4,20,000 By General Reserve 80,000

By Realisation Account

(Profit on Realisation)

50,000

4,30,000 4,30,000

Preference Shareholders Account

Rs. Rs.

To 9% Preference Shares of Hari Ltd. 1,10,000 By Preference Share Capital 1,00,000

By Realisation Account

(Premium on Redemption of Preference Shares)

10,000

1,10,000 1,10,000

Hari Ltd. Account

Rs. Rs.

To Realisation Account 5,30,000 By 9% Preference Shares 1,10,000

By Equity Shares 4,20,000

5,30,000 5,30,000

ME29 / PRIME / PCC 1

In the Books of Hari Ltd. Journal Entries

Dr. Cr.

Rs. Rs.

Goodwill Account Dr. 50,000

Building Account Dr. 1,50,000

Machinery Account Dr. 1,60,000

Stock Account Dr. 1,57,500

Debtors Account Dr. 1,00,000

Bank Account Dr. 20,000

To Gratuity Fund Account 20,000

To Sundry Creditors Account 80,000

To Provision for Doubtful Debts Account 7,500

To Liquidators of Vayu Ltd. Account 5,30,000

(Being Assets and Liabilities takenover as per

agreed valuation).

Liquidators of Vayu Ltd. A/c Dr. 5,30,000

To 9% Preference Share Capital A/c 1,10,000

To Equity Share Capital A/c 4,00,000

To Securities Premium A/c 20,000

(Being Purchase Consideration satisfied as above).

ME29 / PRIME / PCC 2

Balance Sheet of Hari Ltd. (after absorption) as at 31st March, 2009

Liabilities Rs. Assets Rs. Rs.

Share Capital :

2,100 9% Preference Shares of Rs.100 each

2,10,000

Fixed Assets:

Goodwill

1,00,000

1,40,000 Equity Shares of Rs. 10 each fully paid

14,00,000

Building

Machinery

4,50,000

6,60,000

(1,100 Preference Shares and 40,000 Equity Shares

were issued in consideration other than for cash)

Current Assets:

Reserve and Surplus:

Stock

Debtors

3,00,000

4,07,500

Securities Premium 20,000 Less: Provision for bad debts 7,500 2,92,500

General Reserve 1,00,000 Cash and Bank 70,000

Current Liabilities:

Gratuity Fund

70,000

Miscellaneous Expenses to the

extent not written off

Sundry Creditors 2,10,000 Preliminary expenses 30,000

Total 20,10,000 20,10,000

2(a)

Hire Purchase Trading A/C

For the year ending 31st December 2008

Particulars RS Particulars RS

To Goods sold on Hire Purchase A/c (at cost price) (24,000*100/160)

15,000 By Cash A/C

84,000

To Goods sold during the year (at cost) (1,20,000*100/160)

75,000 By Instalments due

3,000

To Net profit transferred to General P & L A/C

31,350 By Goods Returned

600

By Instalments not due unpaid (at cost) (54,000*100/160)

33,750

1,21,350 1,21,350

ME29 / PRIME / PCC 3

2.b)Receipts and expenditure account of Dr. Iodine for the year ended March 31, 2009

RS RS RS

To salaries to Assistants: Paid 45,000 Add 2,000 Outstanding salaries 47,000

By Fees: Received

Add Outstanding Fees

1,60,000

3,000

1,63,000

Journal 2,000 By Miscellaneous Receipts 200

To Depreciation on: Equipment Library Books

10,100300

To Reserve for outstanding fees 3,000

To loss on sale of equipment 1,100

To surplus i.e. excess of income over expenditure

63,700

TOTAL 1,63,000 TOTAL 1,63,000

Balance Sheets of Dr. Iodine as on March 31, 2009

Liabilities Rs. Rs. Assets Rs. Rs.

Expenses Outstanding 2,000 Cash in hand 200

Capital: Introduced 50,000 Cash at Bank 43,000

Add surplus for the year 63,700 Equipment: Cost 50,000

1,13,700 Add Additions 8,000

Less drawings 24,000 89,700 58,000

Less cost of equipments sold 6,000

52,000

Less depreciation 9,200 42,800

Library: Cost 6,000

Less Depreciation 300 5,700

Outstanding fees 3,000

Less Reserve 3,000

Total 91,700 Total 91,700

Notes:‐

ME29 / PRIME / PCC 4

1)Depreciation on Equipment has been calculated as follows:

Rs.

On Rs 44,000 for one year 8,800

On Rs 6,000 for 9 months 900

On Rs 8,000 for 3 months 400

10,100

2)Loss on sale of equipment:

Rs.

Cost 6,000

Less Depreciation 900

5,100

Less sales proceeds 4,000

Loss 1,100

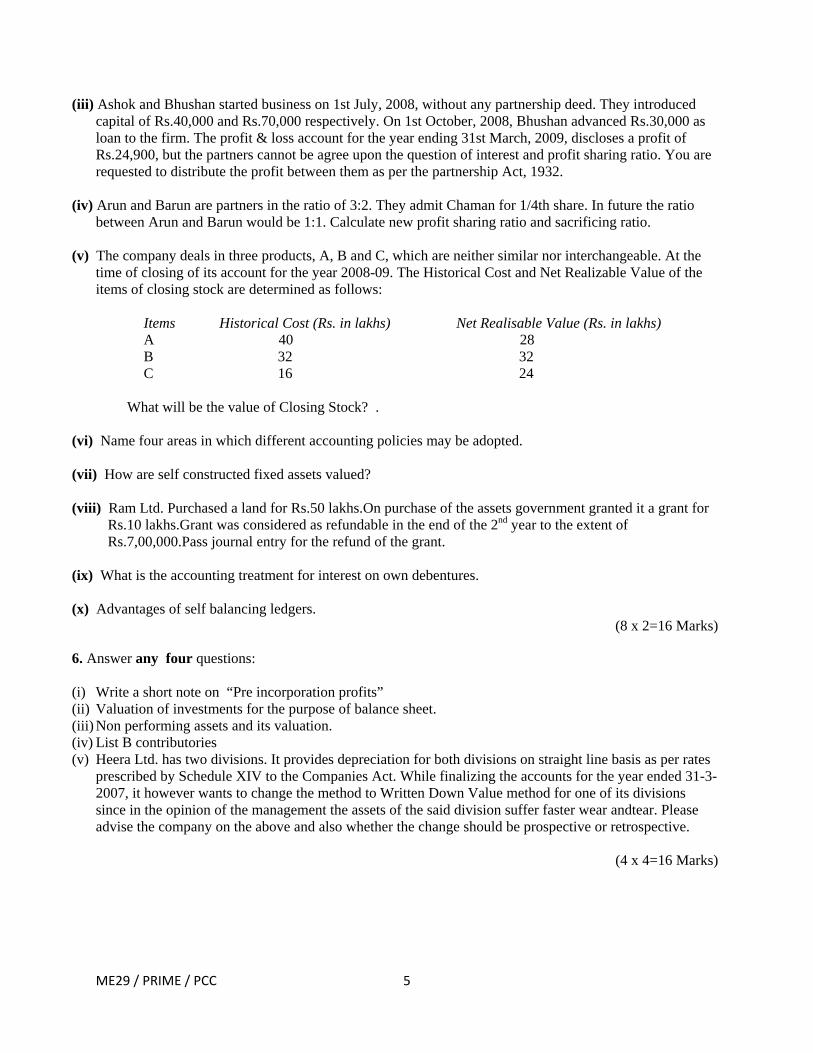

3.a)Trading and Profit and Loss Account of Miss.Jayanthi For the year ended March year ended march 31 2009.

Liabilities RS RS Assets RS RS

To opening stock 18,000 By sales Cash

Credit (3) 30,00066,000 96,000

To credit Purchases (4)

25,000 By closing stock 20,440

To Gross Profit 73,440 1,16,440

1,16,440 By Gross profit b/d 73,440

To Interest 200

To Salaries 17,000

To Other business expenses 15,800

To Provision for doubtful debts 3,000

To Interest on capital 3,500

To Depreciation On furniture On premises 100

1,500 1,600

To Group commission (5) 1,540

To Net Profit 30,800

73,440 73,440

BALANCE SHEETS OF MISS JAYANTHI AS ON MARCH 31,2009

Liabilities RS RS Assets RS RS

ME29 / PRIME / PCC 5

Capital (2) 70,000 Premises 30,000

Add: N/P Interest

30,800 3,500

Less: Depreciation Furniture

1,5002,000

28,500

1,04,300 Less: Depreciation 100 1,900

Less: Drawings 4,000 1,00,300 Stock on hand Debtors 60,000

20,440

Sundry creditors 11,000

Less: Provision for doubtful debts 3,000 57,000

Group commission 1,540 Cash at Bank 4,850

Cash in hand 150

73,440 73,440

WORKING NOTES:‐

1)CASH BOOK

Date Receipts RS Date Payments RS

1998 1997

Mar. 30 To Debtors 50,000 April 1 By Balance b/d 8,000

To sales 30,000 1998

Mar. 31 By Interest 200

By Drawings 4,000

By Salaries 17,000

By Expenses 15,800

By Creditors 30,000

By Balance c/d Cash Bank

1504,850

80,000 80,000

2)BALANCE SHEETS AS ON April 1, 2008

Liabilities RS Assets RS

Capital 70,000 Stock in hand 18,000

Bank overdraft (1) 8,000 Debtors 44,000

Creditors 16,000 Furniture 2,000

Office premises 30,000

94,000 94,000

3)Debtors A/C

Liabilities RS Assets RS

To Operating Balance 44,000 By Cash 50,000

To Credit Sales 66,000 By Closing Balance 60,000

ME29 / PRIME / PCC 6

1,10,000 1,10,000

4)Creditors A/C

Liabilities RS Assets RS

To Cash 30,000 By Operating Balance 16,000

To Closing Balance 11,000 By Credit Sales 25,000

41,000 41,000

3.(b) Exe’s capital account

2008 RS 2007 RS

Mar. 31 To Drawings 15,050 Apr. 1 By Balance b/ f d 60,000

Mar. 31 To Balance c/d 74,000 Oct. 1 By Wyes’ capital

(adjustment for goodwill) 6,000

2008

Mar. 31 By interest on capital 6,000

Mar. 31 By profit and Loss A/C 17,050

89,050 89,050

2008 2008

Sept. 30 To Equity shares in….Ltd 84,300 Apr. 1 By Balance b/d 74,000

To Preference shares in….Ltd 24,150 Apr. 1 By Goodwill 7,500

Sept. 30 By Interest on capital 4,075

Sept. 30 By Profit and Loss A/C (3/8

of Rs 11,000) 4,125

Sept. 30 By Goodwill (3/8 of Rs

50,000) 18,750

1,08,450 1,08,450

Wyes’ capital account

2007 RS 2007 RS

Oct. 1 To Exe’s capital A/C (adjustment for goodwill)

6,000

50,000

2008 2008 By interest on capital 5,000

Mar. 31 To Drawings 11,950 Mar. 31 By profit and Loss A/C 13,950

ME29 / PRIME / PCC 7

Mar. 31 To Balance c/d 51,000 Mar. 31

68,950 68,950

2008 2008

Sept. 30 To Equity shares in….Ltd

84,300 Apr. 1 By Balance b/d

51,000

Apr. 1 By Goodwill 7,500

Sept. 30 By Interest on capital 2925

Sept. 30 By Profit and Loss A/C (3/8 of Rs 11,000)

4,125

Sept. 30 By Goodwill (3/8 of Rs 50,000)

18,750

84,300 84,300

Zed’s capital account

2008 Rs. 2008 Rs.

Sept. 30 To Equity shares in….Ltd 56,200 Apr. 1 By Bank 40,000

To 10% Preference shares in….Ltd

1,050 Sept. 30 By Interest on capital

2,000

Sept. 30 By Profit and Loss A/C (1/4of Rs 11,000)

2,750

Sept. 30 By Goodwill (1/4 of Rs 50,000) 12,500

57,250 57,250

WORKING:

1)

Profit during the year ended 31st March, 2008: RS

Total capital on 31st March, 2008 1,25,000

Add : Drawings during the year(Rs 60,000 + Rs 50,000) 27,000

1,52,000

Less: Capital on 1st April, 2007 (Rs 60,000 + Rs 50,000) 1,10,000

Profit before interest during the year ended 31st March 2008 42,000

Profit for half year (Rs 42,000‐2) 21,000

Less : interest on total capital for six months 5,500

Profit for six months after interest on capital 15,500

Share of profits‐

Exe RS

Wye Rs

Up to 1st October, 2008 in the ratio of 3:2

9,300 6,200

After1st October, 2008 equally 7,750 7,750

ME29 / PRIME / PCC 8

17,050 13,950

2)Adjustment for goodwill :‐

Rs.

Total value of goodwill 60,000

Share of profit gained by Wye 1/2‐2/5 or 1/10 Goodwill to be surrendered by Wye Rs60,000*1/10 Goodwill brought in by Zed will be shared equally

6,000

3)Profit up to 30th September, 2008:

Rs.

Net Assets less goodwill 2,00,000

Total capital as on 1st April, 2008 1,80,000

Profit before interest on capital 20,000

Interest on capital @ 10% p . a 9,000

Profit after allowing interest on capital 11,000

4)

Exe RS

Wye RS

Zed RS

Capitals as on 30th September, 2008 1,08,460 84,300 57,250

Ratio 3 3 3

Capital divided by ratio 36,150 28,100 28,265

Capitals of partners in profit sharing ratio, taking Wyes’ capital as base (Equity shares to be issued for these amounts as their future profits will be shared in the ratio of 3:3:2)

84,300 84,300 56,200

For the balance, 10% preference shares 24,150 NIL 1,050

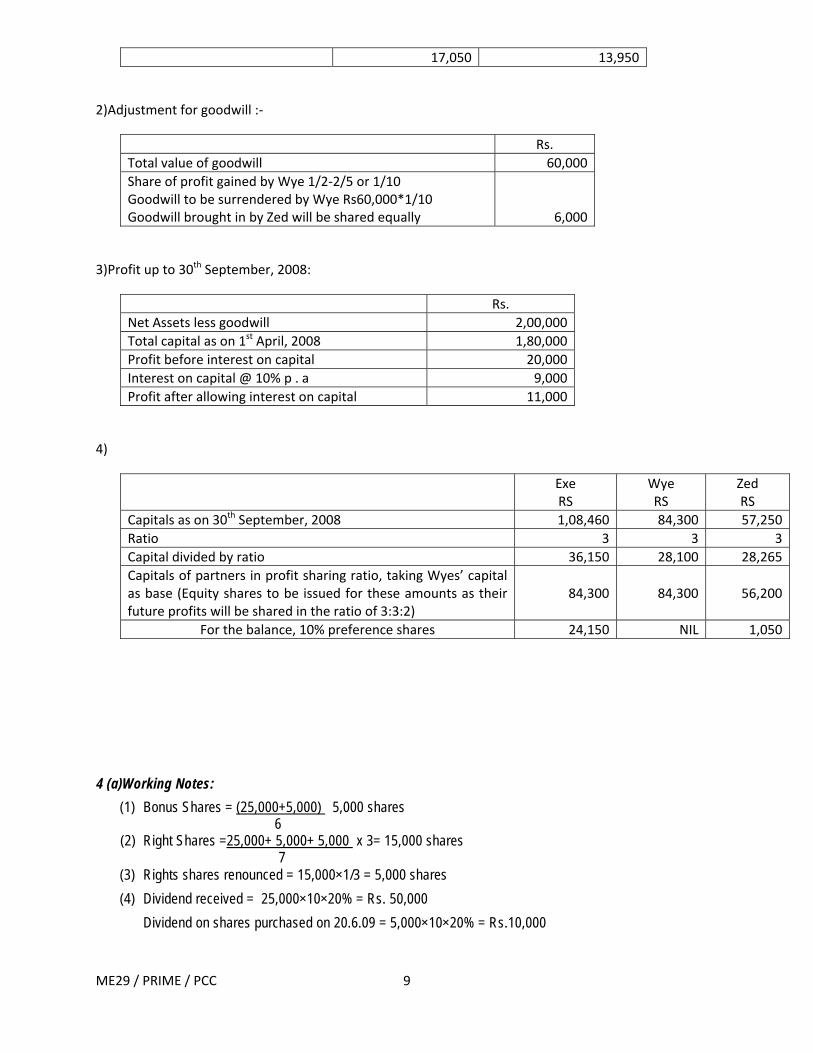

4 (a)Working Notes:

(1) Bonus Shares = (25,000+5,000) 5,000 shares 6 (2) Right Shares =25,000+ 5,000+ 5,000 x 3= 15,000 shares 7 (3) Rights shares renounced = 15,000×1/3 = 5,000 shares

(4) Dividend received = 25,000×10×20% = Rs. 50,000

Dividend on shares purchased on 20.6.09 = 5,000×10×20% = Rs.10,000

ME29 / PRIME / PCC 9

is adjusted to Investment A/c

(5) Cost of shares on 31.12.09 (3,75,000+80,000+1,50,000-10,000-10,000) x 20,000 = 2,60,000 45,000

EQUITY SHARES ACCOUNT

Date No Amount Date No Amount

01.04.09 To Balance 25000 375000 30.09.09 By Bank (sale of nights)

10,000

20.06.09 To Branch 5000 80,000

By Bank (Dividend and share acquired in 20.6.09)

10,000

16.08.09 To Bonus 5000By Bank (Sale of share)

25000 3750000

30.09.09 To Bank (Its share)

10,000 1,50,000By Balance c /d

20,000 2,60,000

15.11.09 To Profit Transferred

50,000

450000 6,55,000

P&L Account

PARTICULARS Rs. PARTICULARS Rs.

To Balance c /d 1,00,000 By profit Transferred 50,000

By Dividend 50,000

ME29 / PRIME / PCC 10

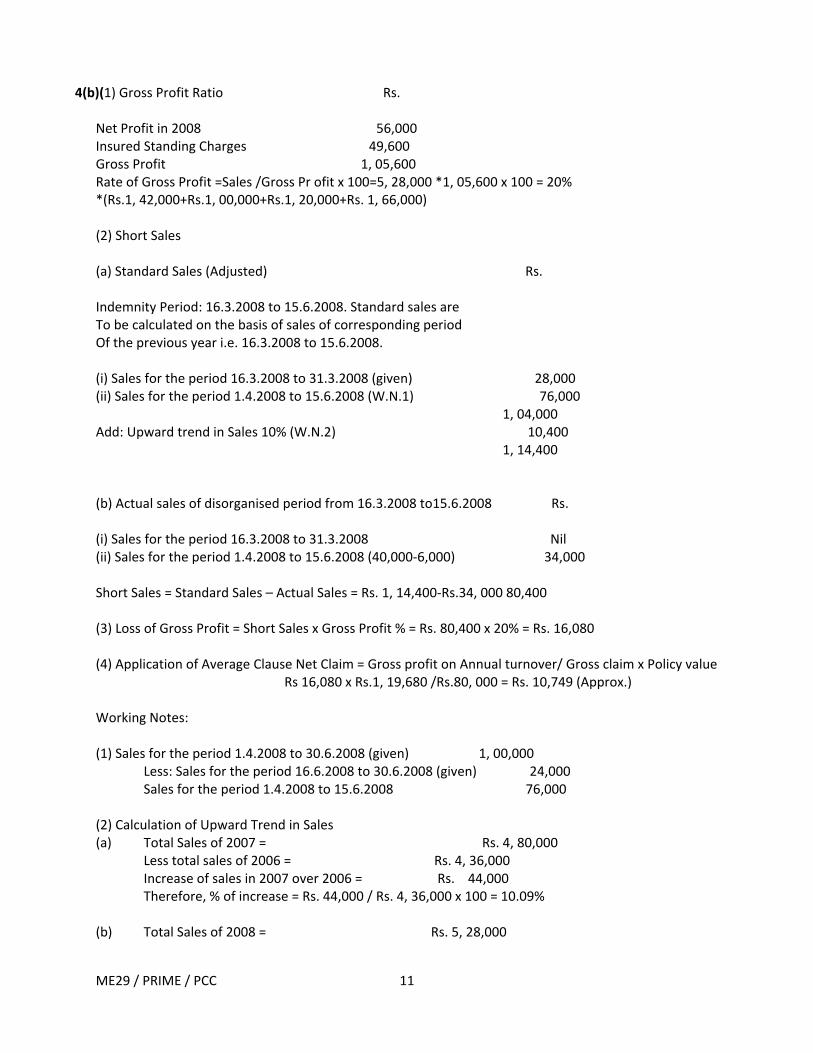

4(b)(1) Gross Profit Ratio Rs.

Net Profit in 2008 56,000 Insured Standing Charges 49,600 Gross Profit 1, 05,600 Rate of Gross Profit =Sales /Gross Pr ofit x 100=5, 28,000 *1, 05,600 x 100 = 20% *(Rs.1, 42,000+Rs.1, 00,000+Rs.1, 20,000+Rs. 1, 66,000) (2) Short Sales (a) Standard Sales (Adjusted) Rs. Indemnity Period: 16.3.2008 to 15.6.2008. Standard sales are To be calculated on the basis of sales of corresponding period Of the previous year i.e. 16.3.2008 to 15.6.2008. (i) Sales for the period 16.3.2008 to 31.3.2008 (given) 28,000 (ii) Sales for the period 1.4.2008 to 15.6.2008 (W.N.1) 76,000 1, 04,000 Add: Upward trend in Sales 10% (W.N.2) 10,400 1, 14,400 (b) Actual sales of disorganised period from 16.3.2008 to15.6.2008 Rs. (i) Sales for the period 16.3.2008 to 31.3.2008 Nil (ii) Sales for the period 1.4.2008 to 15.6.2008 (40,000‐6,000) 34,000 Short Sales = Standard Sales – Actual Sales = Rs. 1, 14,400‐Rs.34, 000 80,400 (3) Loss of Gross Profit = Short Sales x Gross Profit % = Rs. 80,400 x 20% = Rs. 16,080 (4) Application of Average Clause Net Claim = Gross profit on Annual turnover/ Gross claim x Policy value Rs 16,080 x Rs.1, 19,680 /Rs.80, 000 = Rs. 10,749 (Approx.) Working Notes: (1) Sales for the period 1.4.2008 to 30.6.2008 (given) 1, 00,000

Less: Sales for the period 16.6.2008 to 30.6.2008 (given) 24,000 Sales for the period 1.4.2008 to 15.6.2008 76,000

(2) Calculation of Upward Trend in Sales (a) Total Sales of 2007 = Rs. 4, 80,000 Less total sales of 2006 = Rs. 4, 36,000 Increase of sales in 2007 over 2006 = Rs. 44,000 Therefore, % of increase = Rs. 44,000 / Rs. 4, 36,000 x 100 = 10.09% (b) Total Sales of 2008 = Rs. 5, 28,000

ME29 / PRIME / PCC 11

Less total sales of 2007 = Rs. 4, 80,000 Increase of sales in 2008 over 2007 = Rs. 48,000 Therefore, % of increase = Rs. 48,000 / Rs. 4, 80,000 x 100 = 10% Average percentage of increase = 10.09% +10%/2 = 10% (Approx.) (3) Annual Sales Rs. Sales from 16.3.2008 to 31.3.2008 28,000 Sales from 1.4.2008 to 30.6.2008 1, 00,000 Sales from 1.7.2008 to 30.9.2008 1, 20,000 Sales from 1.10.2008 to 31.12.2008 1, 66,000 Sales from 1.1.2009 to 5.3.2009 (Rs. 30,000 – Nil between 16.3.2009 to 31.3.2009) 1, 30,000 Sales for 12 months just before fire took place 5, 44,000 Add: 10% increase (upward trend) 54,400 Adjusted sales of 12 months just before fire 5, 98,400 Gross Profit on Annual Sales = Rs. 5, 98,400 x 20% 1, 19,680

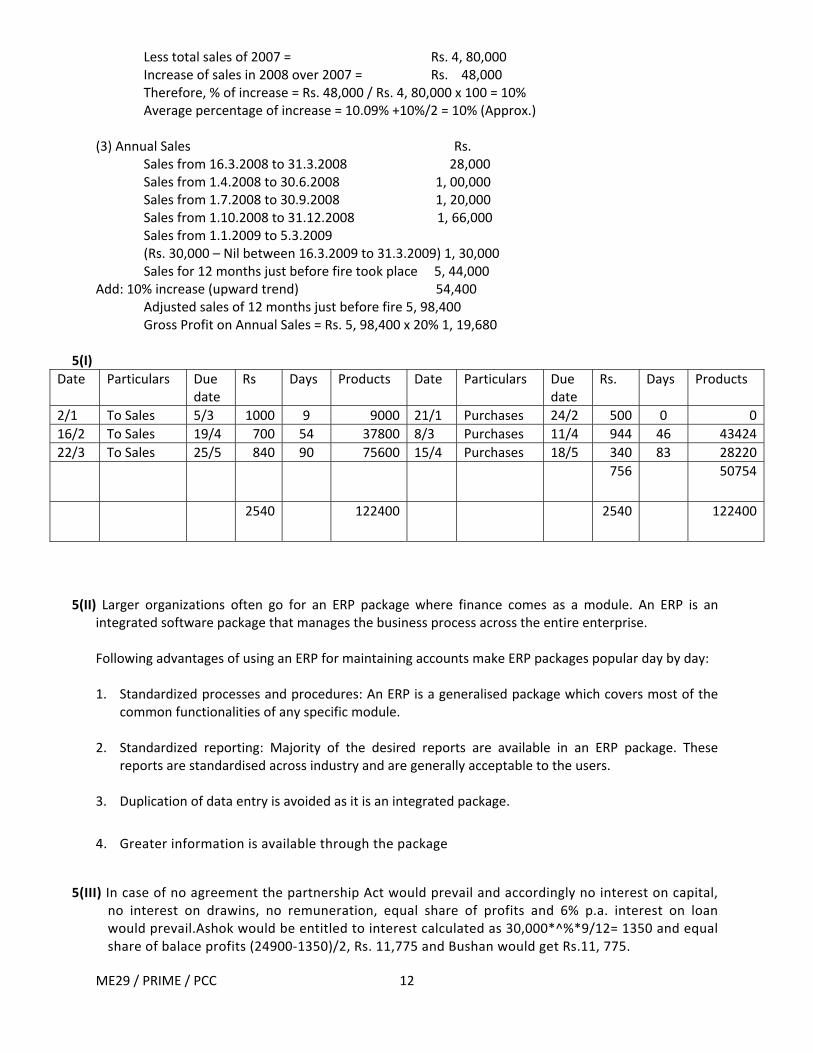

5(I)

Date ticdate

Da r D

. s cts Par ulars Due

Rs ys P oducts ate Particulars Duedate

Rs Day Produ

2/1 Sal /3 00 9 9 2 0 0 0To es 5 1 0 000 1/1 Purchases 24/2 50

16/2 Sal 9/4 3 8 4 424 To es 1 700 54 7800 /3 Purchases 11/4 94 46 43

22/3 Sal 5/5 7 1 0 220 To es 2 840 90 5600 5/4 Purchases 18/5 34 83 28

6 75475 50

254 1 0 4000 22400 254 122

5(II) Larger organizations often go for an ERP package where finance comes as a module. An ERP is an integrated software package that manages the business process across the entire enterprise. Following advantages of using an ERP for maintaining accounts make ERP packages popular day by day: 1. Standardized processes and procedures: An ERP is a generalised package which covers most of the

common functionalities of any specific module. 2. Standardized reporting: Majority of the desired reports are available in an ERP package. These

reports are standardised across industry and are generally acceptable to the users. 3. Duplication of data entry is avoided as it is an integrated package.

4. Greater information is available through the package

5(III) In case of no agreement the partnership Act would prevail and accordingly no interest on capital, no interest on drawins, no remuneration, equal share of profits and 6% p.a. interest on loan would prevail.Ashok would be entitled to interest calculated as 30,000*^%*9/12= 1350 and equal share of balace profits (24900‐1350)/2, Rs. 11,775 and Bushan would get Rs.11, 775.

ME29 / PRIME / PCC 12

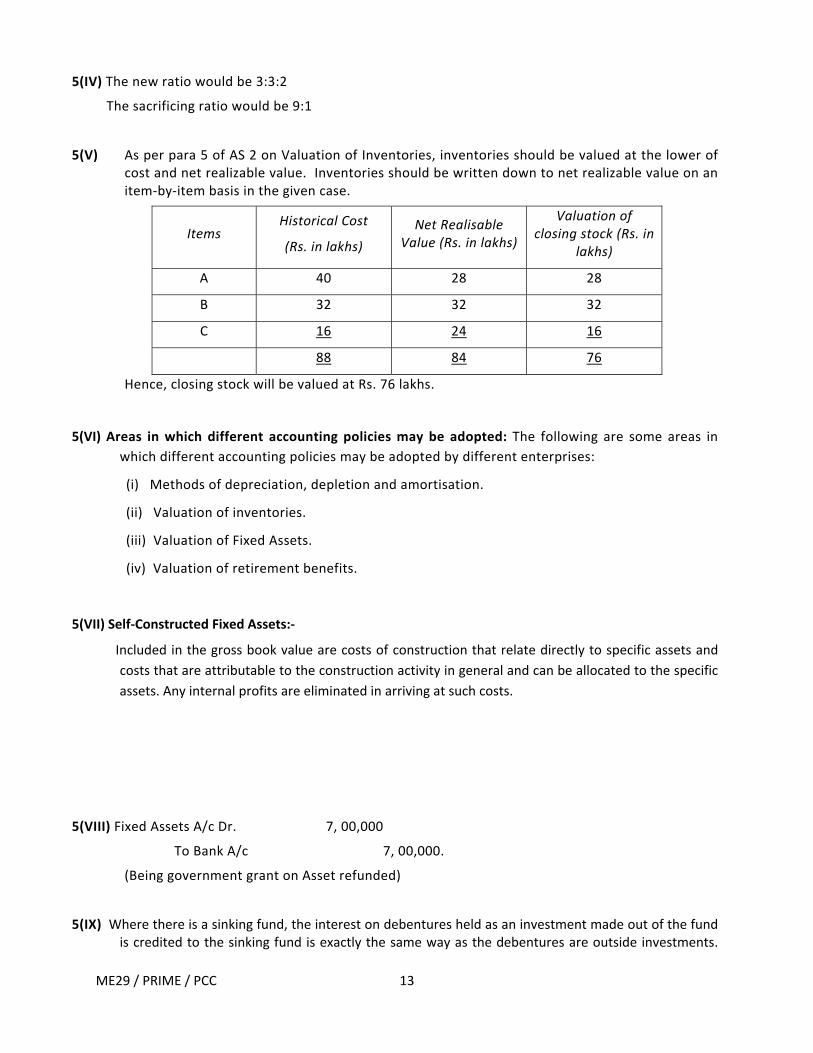

5(IV) The new ratio would be 3:3:2

The sacrificing ratio would be 9:1

5(V) As per para 5 of AS 2 on Valuation of Inventories, inventories should be valued at the lower of cost and net realizable value. Inventories should be written down to net realizable value on an item‐by‐item basis in the given case.

Items Historical Cost

(Rs. in lakhs)

Net Realisable Value (Rs. in lakhs)

Valuation of closing stock (Rs. in

lakhs)

A 40 28 28

B 32 32 32

C 16 24 16

88 84 76

Hence, closing stock will be valued at Rs. 76 lakhs.

5(VI) Areas in which different accounting policies may be adopted: The following are some areas in

which different accounting policies may be adopted by different enterprises:

(i) Methods of depreciation, depletion and amortisation.

(ii) Valuation of inventories.

(iii) Valuation of Fixed Assets.

(iv) Valuation of retirement benefits.

5(VII) Self‐Constructed Fixed Assets:‐

Included in the gross book value are costs of construction that relate directly to specific assets and

costs that are attributable to the construction activity in general and can be allocated to the specific

assets. Any internal profits are eliminated in arriving at such costs.

5(VIII) Fixed Assets A/c Dr. 7, 00,000

To Bank A/c 7, 00,000.

(Being government grant on Asset refunded)

5(IX) Where there is a sinking fund, the interest on debentures held as an investment made out of the fund is credited to the sinking fund is exactly the same way as the debentures are outside investments.

ME29 / PRIME / PCC 13

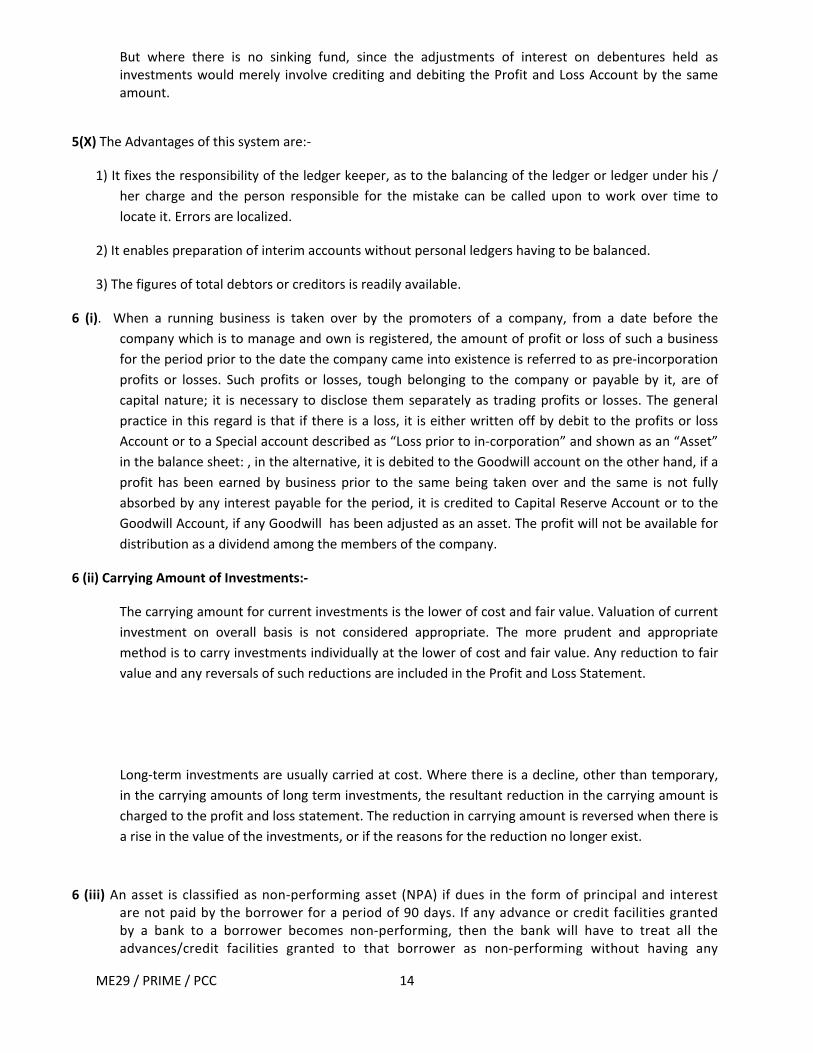

But where there is no sinking fund, since the adjustments of interest on debentures held as investments would merely involve crediting and debiting the Profit and Loss Account by the same amount.

5(X) The Advantages of this system are:‐

1) It fixes the responsibility of the ledger keeper, as to the balancing of the ledger or ledger under his /

her charge and the person responsible for the mistake can be called upon to work over time to

locate it. Errors are localized.

2) It enables preparation of interim accounts without personal ledgers having to be balanced.

3) The figures of total debtors or creditors is readily available.

6 (i). When a running business is taken over by the promoters of a company, from a date before the

company which is to manage and own is registered, the amount of profit or loss of such a business

for the period prior to the date the company came into existence is referred to as pre‐incorporation

profits or losses. Such profits or losses, tough belonging to the company or payable by it, are of

capital nature; it is necessary to disclose them separately as trading profits or losses. The general

practice in this regard is that if there is a loss, it is either written off by debit to the profits or loss

Account or to a Special account described as “Loss prior to in‐corporation” and shown as an “Asset”

in the balance sheet: , in the alternative, it is debited to the Goodwill account on the other hand, if a

profit has been earned by business prior to the same being taken over and the same is not fully

absorbed by any interest payable for the period, it is credited to Capital Reserve Account or to the

Goodwill Account, if any Goodwill has been adjusted as an asset. The profit will not be available for

distribution as a dividend among the members of the company.

6 (ii) Carrying Amount of Investments:‐

The carrying amount for current investments is the lower of cost and fair value. Valuation of current

investment on overall basis is not considered appropriate. The more prudent and appropriate

method is to carry investments individually at the lower of cost and fair value. Any reduction to fair

value and any reversals of such reductions are included in the Profit and Loss Statement.

Long‐term investments are usually carried at cost. Where there is a decline, other than temporary,

in the carrying amounts of long term investments, the resultant reduction in the carrying amount is

charged to the profit and loss statement. The reduction in carrying amount is reversed when there is

a rise in the value of the investments, or if the reasons for the reduction no longer exist.

6 (iii) An asset is classified as non‐performing asset (NPA) if dues in the form of principal and interest are not paid by the borrower for a period of 90 days. If any advance or credit facilities granted by a bank to a borrower becomes non‐performing, then the bank will have to treat all the advances/credit facilities granted to that borrower as non‐performing without having any

ME29 / PRIME / PCC 14

regard to the fact that there may still exist certain advances/credit facilities having performing status.

Income from the non‐performing assets can only be accounted for as and when it is actually received. In concept, any credit facility (assets) becomes non‐performing when it eases to generate income. The RBI has issued guidelines to commercial banks regarding the classification of advances between performing and non‐performing assets.

A term loan is treated as a non‐performing assets (NPA) if interest and/or instalments of principal remains over due for a period of more than 90 days. A cash credit/overdraft account is treated as NPA if it remains out of order for a period of more than 90 days. An account is treated an ‘out of order’ if any of the following conditions is satisfied:

(a) The outstanding balance remains continuously in excess of the sanctional

limit/drawing power.

(b)Though the outstanding balance is less than the sanctioned limit/drawing power—

(i) There are credits continuously for more than 90 days as on the date of balance sheet or

(ii) Credits during the aforesaid periods are not enough to cover the interest debited during the same period.

Bills purchased and discounted are treated as NPA if they remain overdue and unpaid for a period of more than 90 days. Necessary provision should be made for non‐performing assets after classifying them as sub‐standard, doubtful or loss asset as the case may be.

6(iv) The shareholders who transferred partly paid shares (otherwise than by operation of law or by death)

within one year, prior to the date of winding up may be called upon to pay an amount (not

exceeding the amount not called up when the shares were transferred) to pay off such creditors as

existed on the date of transfer of shares.

Their liability will crystallize only

(i) When the existing assets available with the liquidator are not sufficient to cover the liabilities;

(ii) When the existing shareholders fail to pay the amount due on the shares to the liquidator.

6(v) According to the Guidance Note on Accounting for Depreciation in Companies issued by ICAI, it is

permissible for a company to adopt more than one method of depreciation simultaneously that is to say that‐

1. Company may follow different methods for different types of assets; and 2. Company geographical locations can follow different methods.

Only condition is that same methods should be consistently adopted from year to year.

Change in the method of depreciation is a change in accounting policy.According to AS 6, such a change is permissible only when at least one of the following 3 conditions is satisfied:‐

ME29 / PRIME / PCC 15

ME29 / PRIME / PCC 16

(i) Such change is required by law.

(ii) Such change is required by the Accounting Standards

(iii) Such change will result in more appropriate presentation.

Here, from the facts given it appears that condition (iii) is satisfied i.e. change will lead to more appropriate presentation (since WDV method will better represent the pattern of faster wear & tear instead of SLM). According to AS 6, change should be retrospective. Any difference arising thereon should be changed/ credited to P&L account in the year of change.

1 ME29 / PRIME / PCC

AAG Number of Pages : 2 Total Marks: 100 Number of Questions: 8 Time Allowed: 3 Hrs

Answer all the questions

1 State with reasons (in short) whether the following statements are true or false:

(Answer any ten)

1) The term 'fund' and 'reserve' can be used interchangeably. 2) CARO '2004 is also applicable to the audit of branch of a company, except where the

Company is exempt from the applicability of the order. 3) All the joint auditors are jointly and severally responsible for the work, which is not

divided und carried on jointly by all the joint auditors. 4) Compliance procedures are tests designed to obtain audit evidence as to completeness,

accuracy and validity of the data produced by accounting system. 5) AAS-11 is related to Audit Materiality. 6) The auditor of a company is entitled to attend any General Meeting of the company as his

duty. 7) An Auditor may be removed from Office before the expiry of his term, by the company

in General Meeting. 8) Audit Working Papers to be kept at least for 3 (three) years. 9) AAS-6 has a purpose to Establish Standards to form procedures to be followed to have an

understanding of the Accounting and Internal Control system. 10) “Auditor is not an Insurer”. 11) The auditor examines debit notes to vouch sales return. 12) Inventory turnover ratio is calculated by the auditor to obtain evidence concerning

management’s assertion about valuation of inventory.

(10 X 2 = 20 Marks) 2 State briefly the duty of the auditor with regard to each of the following:

(i) A sum of Rs.10, 00,000 is received from Insurance Company in respect of a claim for loss of goods in transit costing Rs.8, 00,000. The amount is credited to purchases account.

(ii) A loss of Rs.2, 00,000 on account of embezzlement of cash was suffered by the Company and it was debited to salary account.

(iii) You are a Principal Auditor of Sri Company Limited which has three branches the

accounts of which are subject to audit by qualified branch auditors. One of the branch auditors qualified his report for non-provision of doubtful debts which he considered to be Material for the company as a whole. Subsequent to their reporting, but before you could Sign the audit report on the accounts of the company as a whole, the management informed you that the debt under the subject-matter of qualification in Branch Auditor’s Report had been fully recovered.

(iv) Traveling expenses of Rs. 2.25 lakhs shown in Profit and Loss Account of X Ltd., including a sum of Rs. 1.10 lakhs spent by a Director on his foreign travel for company’s Business accompanied by his mother for her medical treatment

(4 x 5 = 20 Marks)

2 ME29 / PRIME / PCC

3 (a) What are the various assertions an auditor is concerned with while obtaining audit evidence from substantive procedure?

(b) What does AAS-3 say about utility, ownership, custody and retention of working papers?

(6+4=10 Marks)

4 (a) What are the special steps involved in framing a system of Internal Check? (b) Explain propriety audit

(6+4=10 Marks)

5 (a) Discuss in brief the power of Company to purchase its own Securities.

(b) Under what circumstances the retiring Auditor can not be reappointed? (2 X 5 = 10 Marks)

6 (a) What steps would you take in to consideration in Auditing the receipts from patients of a Hospital?

(b) Distinguish between Internal evidence and External evidence.

(6+4 = 10 Marks)

7 How will you vouch and/or verify the following? Answer any two

a. Premium paid for insurance of a Motor car. b. Bank Balances c. Purchase return

(2 X 5=10 Marks)

8 Write Short Notes on the following: Any two

(a) Capital Expenditure (b) Audit Program (c) Procedures and technique

(2 x 5=10 Marks)

PRIME ACADEMY 29TH SESSION MODEL EXAM

PCC-AUDITING AND ASSURANCE- SUGGESTED ANSWERS

1 1) False: The term ‘fund’ in relation to any reserve should be used only where such reserve is

specifically represented by earmarked investments. 2) True : CARO’ 2004 is also applicable to the audit of branch of a company since subsection 3(a)

of the section 228 of the Companies Act clearly specifies that a branch auditor has the same duties as the company’s auditor.

3) True: As per AAS-12 on “responsibility of joint auditors” all the joint auditors are jointly and

severally responsible for the audit work which is not divided and carried on jointly by all the joint auditors.

4) False: Compliance procedures are tests designed to obtain reasonable assurance that those

internal controls on which audit reliance is to be placed are in effect. Here auditor is concerned with assertions that the control exists and is operating effectively.

5) False: AAS-11 is related to the Representation by Management. Audit of Materiality is discussed

in AAS-13. 6) False: It is partly true. The auditor of a company is entitled to attend any general meeting of the

company but it is not his duty to attend or take part in the discussion, further such a right extends only to meeting of the members and not to the meeting of directors.

7) False: As per Section 224(7), the auditor may be removed from the office before the expiry of his

term by the company in general meeting obtaining the prior approval of the Central Government. But such approval is not required for the removal of the first auditor appointed by the Director.

8) False: Audit working papers are to be kept at least 10 years. 9) True: AAS-6 enables the auditor to obtain an understanding of the accounting and internal

control system, so that he can plan the audit work in effective manner and develop an efficient audit approach.

10) True: While examining the evidences relating to business organization or the state of the affairs

of the company, the auditor’s duty is limited only to the verification of the evidence that is made available to him in ordinary course of audit or that which he would call upon to examine on a doubt having arisen that there is something wrong. Hence auditor is not an insurer.

11) False: The auditor should examine purchase return book with reference to copies of debit notes

issued to suppliers and outward return notes to vouch purchase return. 12) True: Calculation of inventory turnover ratio and their comparison with those of previous years’

ratio will provide evidence on correct valuation of slow-moving, defective and obsolete items included in inventories.

29ME/PRIME/PCC 1

2 (a) Claim received from insurance company (i) According to AS-5, “Net Profit or Loss for the Period, Prior Period Items and Changes in

Accounting Polices” requires that all items of income and expenses which are recognized in a period should be included in the determination of net profit or loss for the period.

The loss of goods in transit costing Rs.8,00,000 should be therefore, charged to profit and loss

account of present financial year and insurance claim of Rs.10,00,000 should be credited to profit and loss account under an appropriate head. It should not have been credited to purchases account. If done so, the purchases would be overstated. Insurance claim (excess) is profit from ordinary activities. AS-5 states that when items of income (and expense) within profit or loss from ordinary activities are of such size, nature or incidence that their disclosure is relevant to explain the performance of the entity for the period, the nature and amount of such items should be disclosed separately. Thus, a separate disclosure of insurance claim received is necessary as per the requirements of AS-5, and it should not be credited to purchases account.

(ii) Embezzlement of cash AS-5, Net Profit or Loss for the Period, Prior Period items and changes in

Accounting Policies “requires that (income and) expenses within (Profit of) loss from ordinary activities are of such size, nature or incidence that their disclosure is relevant to explain the performance of the enterprise for the period, the nature and amount of such items should be disclosed separately.”

Embezzlement of cash of Rs.2,00,000 is an ordinary business loss which as per the requirements

of AS-5 should be disclosed separately in the profit and loss account. It should not be merged with salary.

(iii) Qualification in branch auditor's report-subsequent events: The Branch auditor had

qualified on non-provision of a major debt. After his report but before the issue of report by Principal auditor an event happened which has thrown new light on the facts that existed as on the date of balance sheet date. This is a subsequent event within the meaning of AAS 19 i.e. event that had taken place between the date of balance sheet date and the date of signing the audit report. In relation to the cases where the component (i.e.branch) is audited by another auditor, the subsequent event would include events that had taken place between the date of audit report of the component and the date of signing the audit report of the entity as a whole by the principal auditor. On becoming aware of the subsequent events, the auditor should consider whether the accounts had been drawn so as to give effect to the facts of subsequent events. Accordingly, the auditor should omit qualification as the debt is no more doubtful in view of its recovery in full. However, the auditor may check that it has in fact been received by a substantial vouching of the subsequent events which had been considered by him to make himself fully satisfied about his report in the matter.

(iv) Personal Expenses Charged to Revenue Account: As per the provisions of Section 227(1A) of the Companies Act, 1956, the auditor shall enquire whether personal expenses have been charged to revenue account and make a report to the members in case he is not satisfied with the answer. In this case, the auditor should examine documentary evidence in support of the traveling expenses of Rs.1.10 lakhs incurred by the director and ascertain the personal component thereof. Then he should enquire as to whether such personal expenses incurred by the company are covered by contractual obligations or by any accepted business practices. In case, the answer is negative, the auditor should make a report thereon and qualify his audit report.

29ME/PRIME/PCC 2

3

(a) In obtaining audit evidence from substantive procedures, the auditor concerned with the following assertions:

(i) Existence - that an assets or liability exists at a given date. (ii) Rights and obligations - that an asset is a right of the entity and a liability is an obligation

at a given date. (iii) Occurrence - that a transaction or event took place which pertains to the entity. (iv) Completeness - that there are no unrecorded assets, liabilities or transaction. (v) Valuation - that an asset or liability is recorded at an appropriate carrying value. (vi) Measurement - that a transaction is recorded in the proper amount and revenue or

expenses are allocated to proper period. (vii) Presentation & disclosure - that an item is disclosed, classified and described in

accordance with recognized accounting policies, practices and statutory requirements.

(b) Utility of working papers: According to AAS-3 on ‘Documentation’ working papers helps in planning and performance of the audit, supervision and review of the audit work and provide evidence of the audit work performed to support the auditor’s opinion. Ownership of working papers: Working papers are the property of the auditor and he may, at his discretion, make portions of or extracts from his working papers to his client. Custody of working papers: The auditor should adopt reasonable procedures for safe custody and confidentiality of his working papers. Retention of working papers: Working papers should be retained, long enough, for a period of time sufficient to meet the needs of his practice and satisfy any legal or professional requirement of record retention.

4 (a) General Considerations in Framing a System of Internal Check: The term “internal check” is

defined as the “checks on day to day transactions which operate continuously as part of the routine system whereby the work of one person is proved independently or is complementary to the work of another, the object being the prevention or early detection of errors or fraud”. The following aspects should be considered in framing a system of internal check: (1) No single person should have an independent control over any important aspect of the

business. The work done by one person should automatically be checked by another person in routine course.

(2) The duties/work of members of the staff should be changed from time to time without any

previous notice so that the same officer or subordinate does not, without a break, perform the same function for a considerable length of time.

(3) Every member of the staff should be encouraged to go on leave at least once in a year so

that frauds successfully concealed by such a person can be detected in his absence. (4) Persons having physical custody of assets must not be permitted to have access to the

books of account.

29ME/PRIME/PCC 3

(5) There should be an accounting control in respect of each important class of assets, in addition, these should be periodically inspected so as to establish their physical condition.

(6) The system of Budgetary Control should be introduced.

(7) For stock-taking, at the close of the year, trading activities should, if possible, be

suspended. The task of stock-taking, and evaluation should be done by staff belonging to other than stock section.

(b) Propriety Audit: Under ‘propriety audit’, the auditors try to bring out cases of improper, avoidable, or in fructuous expenditure even though the expenditure has been incurred in Conformity with the existing rules and regulations. However, some general principles have been laid down in the Audit Code, which have for long been recognized as standards of financial propriety. Audit against propriety seeks to ensure that expenditure conforms to these principles which have been stated as follows: (1) The expenditure should not be prima facie more than the occasion demands. Every public

officer is expected to exercise the same vigilance in respect of expenditure incurred from public moneys as a person of ordinary prudence would exercise in respect of expenditure of his own money.

(2) No authority should exercise its powers of sanctioning expenditure to pass an order which will

be directly or indirectly to its own advantage.

(3) Public moneys should not be utilized for the benefit of a particular person or section of the community unless:

(i) The amount of expenditure involved is insignificant; or

(ii) A claim for the amount could be enforced in a Court of law; or

(iii) The expenditure is in pursuance of a recognized policy or custom; and

(iv) The amount of allowances, such as traveling allowances, granted to meet expenditure of

particular type should be so regulated that the allowances are not, on the whole, sources

of profit to the recipients.

5 (a) Power of Company to Purchase its Own Securities:

The Companies (Amendment) Act, 1999 contains elaborate provisions enabling a company to buy-back its own securities. The work security includes both equity and preference shares. As per section 77A, a company may purchase its own shares or other specified securities (“buy-back”) out of-

(i) Its free reserves; or

(ii) The securities premium account; or

(iii) The proceeds of any earlier issue other than from issue of shares made specifically for buy-

back purposes.

No company shall purchase its own shares or other specified securities unless-

(a) The buy-back is authorized by its Articles;

(b) A special resolution has been passed in general meeting of the company authorizing the

buy-back;

29ME/PRIME/PCC 4

(c) The buy-back is or less than twenty-five per cent, of the total paid-up capital (equity shares

and preference shares) and free reserves of the company;

(d) The debt equity ratio is not more than 2:1 after such buy back.

(e) All the shares and other securities are fully paid up.

(f) Every buy back shall be completed within 12 months from the date of passing the Special

resolution.

(g) The company shall not make further issue of same kind of shares.

The company, after buy-back file with the Registration and SEBI, a return containing such particulars relating to buy-back within 30 days.

(b) In the following circumstances, the retiring auditor cannot be reappointed:

(1) A specific resolution has not been passed to reappoint the retiring auditor.

(2) The auditor proposed to be reappointed does not possess the qualification prescribed under

section 226.

(3) The proposed auditor suffers from the disqualifications under section 226(3) and 226

(4) He has given to the company notice in writing of his unwillingness to be reappointed.

(5) A resolution has been passed in AGM appointing somebody else or providing expressly that

the retiring auditor shall not be reappointed.

(6) A written certificate has not been obtained from the proposed auditor to the effect that the

appointment or reappointment, if made, will be in accordance within the limits specified under

section 224(1B).

6 (a)

1. Examine the internal check system as regards the receipts of bills from the patients.

2. Vouch the register of patients with copy of bills issued to them.

3. Verify bills for a selected period with the patient’s attendance record to see that the bills have

been correctly repaired.

4. See that bills have been issued to all the patients according to the rules of the Hospital.

5. Check cash collections as entered in the cash book with the receipts, counterfoils and other

evidence.

6. Compare the total income with the amount budgeted for the same and report to the

management for significant variations which have been taken place.

(b) Types of Audit Evidence:

There are two types of Audit evidence: Internal evidence and external evidence:

Evidence which originates within the organization being audited is internal evidence.

Example – sales invoice, copies of sales challan and forwarding note, goods received notes,

inspection report, copies of cash memo, debit and credit notes, etc. External evidence on the

other hand is the evidence that originates outside the client’s organization; for example, purchase

invoice, supplier’s challan and forward note, debit notes and credit notes coming from parties,

29ME/PRIME/PCC 5

quotations, confirmations, etc. In an audit situation, the bulk of evidence that an auditor gets is

internal in nature. However, substantial external evidence is also available to the auditor. Since in

the origination of internal evidence, the client and his staff have the control, the auditor should be

careful in putting reliance on such evidence. It is not suggested that they are to be suspected; but

an auditor has to be alive to the possibilities of manipulation and creation of false and misleading

evidence to suit the client or his staff. The external evidence is generally considered to be more

reliable as they come from third parties who are not normally interested in manipulation of the

accounting information of others. However, if the auditor has any reason to doubt the

independence of any third party who has provided any material evidence e.g., an invoice of an

associated concern, he should exercise greater vigilance in that matter. As an ordinary rule the

auditor should try to match internal and external evidence as far as practicable. Where external

evidence is not readily available to match, the auditor should see to what extent the various

internal evidence corroborate each other.

7 (a) Premium paid on Insurance of a Motor Car:

(i) Check insurance cover note issued by Insurance Company. Verify car no., period of Insurance etc. (ii) See that “No claim Bonus” is given, where entitled, by the Insurance Company. (iii) Ensure that proper adjustment is made for pre-paid insurance premium.

(b) Bank Balances

(I) Verify bank balance by reference to bank statements. (II) Examine the bank reconciliation statement prepared as on the last day of the year and see

whether

(a) Cheques issued by the entity but not presented for payment, and (b) Cheques deposited for collection by the entity but not credited in the bank account have been duly debited/credited in the subsequent period.

(III) Pay special attention to those items in the reconciliation statements which are outstanding for an unduly long period. The auditor should ascertain the reasons for such outstanding items from the management. He should also examine whether any such items require an adjustment! write-off.

(v) Examine relevant certificates in respect of fixed deposits or any type of deposits with banks duly supported by bank advices.

(v) Check the Balance Sheet as per Part I of Schedule VI which requires that the bank balance should be segregated as follows:

(i) With Scheduled Banks. And' (ii) With others. In the last mentioned case, the nature of interest, if any, of a director or his

relative with each of the bankers should be disclosed. The nature of deposit in each case should be stated, e.g., current, fixed, call, etc. in case of a non-scheduled bank, its name and the maximum balance that was held by it during the year should also be disclosed.

29ME/PRIME/PCC 6

(c) Purchase Return

(i) Examine debit note issued to the supplier which in turn may be confirmed by corresponding credit note issued by the supplier acknowledging the same. The relevant correspondence may also be examined.

(ii) Verify by reference to relevant corresponding record in good outward book or the stores

records. Further, the figures in these documentary evidence should be compared with the supplier’s original invoices for rates and other charges and calculation should also be checked.

(iii) Examine in depth to eliminate the possibility of fictitious purchase returns for covering

bogus purchases recorded earlier when such returns outwards are in substantial figure either at the beginning or end of the accounting year.

(iv) Cross-check with reference to original invoices any rebates in price or allowances if any

given by suppliers on strength of their Credit Notes.

8

(a) Capital Expenditure: A capital expenditure is that which is incurred for the under mentioned purposes: (a) Acquiring fixed assets, i.e., assets of a permanent or a semi-permanent nature, which

are held not for resale but for use with a view to earning profits. (b) Making additions to the existing fixed assets. (c) Increasing earning capacity of the business. (d) Reducing the cost of production. (e) Acquiring a benefit of enduring nature of a valuable right. The different forms that capital expenditure takes are: (i) land; (ii) building; (iii) plant and machinery; (iv) electric installations; (v) premium paid for the lease of a building; (vi) development expenditure on land; and (vii) goodwill; etc. Expenses which are essentially of a revenue nature, if incurred for creating an assets or adding to its value or achieving higher productivity, are also regarded as expenditure of a capital nature.

Examples :

(i) Material and wages-capital expenditure when expended on the construction of a building or erection of machinery.

(ii) Legal expenses- capital expenditure when incurred in connection with the purchase of land or building.

(iii) Freight- capital expenditure when incurred in respect of purchase of plant and machinery.

Whenever, therefore, a part of the expenditure, ostensibly of a revenue nature, is capitalized it is the duty of the auditor not only to examine the precise particulars of the expenditure but also the considerations on which it has been capitalized.

(b) Audit Programme : Audit Program is a written documents setting forth, in details, the various aspects of the proposed audit. Such Program is prepared before commencing the audit and it is updated with the progress of the audit.

Without a written and pre-determined Program, work is necessarily, to be carried out on the basis of some, ‘mental’ plan. In such a situation, there is always a danger of ignoring or overlooking certain books and records. Under a properly framed Program, the danger insignificantly less and the audit can proceed systematically.

It serves as a guide to be carried out in the succeeding year. A properly drawn up audit Program serve as evidence in the event of any charge of negligence being brought against auditor.

29ME/PRIME/PCC 7

29ME/PRIME/PCC 8

Audit Program normally provide for the following: (i) Audit procedure to be applied (ii) Extent of check (iii) Timing of check (iv) Allocation of work amongst the audit team members. (v) Special instructions based on past experience of the auditee.

Audit Program provides sufficient details to serves as a set of instruction to the team and also help to control the proper execution of work.

(C ) Procedures and technique The two terms, procedure and techniques, are often used interchangeably; in fact, however, a

distinction does exist. Procedure may comprise a number of techniques and represents the broad frame of the manner of handling the audit work; techniques stand for the methods employed for carrying out the procedure.

For example, procedure requires an examination of the documentary evidence. This job is

performed by the procedure known as vouching which would involve techniques of inspection and checking computation of documentary evidence. As per AAS-5 on Audit Evidence, basically audit procedures are broadly of two types viz. compliance procedures and tests of detail. Test of details are further comprised of substantive audit procedures and analytical review procedures. Vouching is a substantive audit procedure which involves audit techniques like casting, cross-casting, checking of posting, etc. On the other hand, verification of assets and liabilities is a substantive audit procedure which involves application of audit techniques like physical examination, confirmation from third parties, etc.

.

1 ME29 / PRIME / PCC

LSN

Number of Pages : 3 Total Marks: 100 Number of Questions: 20 Time Allowed: 3 Hrs

PART – I

Question no 1 and 2 are compulsory. Answer any 8 from the rest

1(a) How an offer is revoked?

5 Marks (b) Raman proposed to sell his house to Ramanathan, Ramanathan sent his acceptance

by post. Next day, Ramanathan sends a telegram withdrawing his acceptance. Examine the validity of the acceptance in the light of the following:

(i) The telegram of revocation of acceptance was received by Raman before the letter of acceptance.

(ii) The telegram of revocation of letter of acceptance both reached together 5 Marks

2. (i) State the following statements are correct or incorrect

(a) An agreement the meaning of which is neither certain nor capable of being made certain is

voidable. (b) “A” agrees to pay “B” 1,000 if two straight lines should enclose a space, this agreement is

valid because there is valid consideration. (c) When both parties to an agreement are under a mistake as to a matter fact essential, the

agreement is void. (d) “A” contract to indemnity “B” against consequences of any proceeding, which “C” may take

against “B” in respect of certain sum of 300 rupees, is contract of guarantee. (e) A person employed and acting under the control of the original agent in the business of

agency is co-agent. 5x1= 5 Marks

(ii) How a contract is assigned? 5 Marks

3. Pick up the correct answer from the following;

( i) A bearer instrument can be negotiated by :-

(a) Indorsement only (b) Delivery only (c) Both indorsement and delivery (d) None of the above

(ii) In which of the following case, the employee will be disqualified for bonus under section 9 of the

payment of Bonus Act, 1965:-

(a) fraud: or (b) riotous or violent behavior while on the premises of establishment: or

2 ME29 / PRIME / PCC

(c) Theft, misappropriation or sabotage of any property of the establishment: (d) All of the above.

(iii) Which of the following is not included for the purpose of “salary” as per Employees

Provident fund & Misc Provisions act, 1952-

(a) The cash value of food concession (b) Any dearness allowance (c) Any presents made by the employer (d) All of the above

(iv) Completed year of service under the Payment of Gratuity Act means :-

(a) Service for one year (b) Continuous service (c) Continuous service for one year (d) Number of years of service

(v) A negotiable instrument payable to order can be can be transferred by:-

(a) Simple delivery (b) Endorsement (c) Both (a) and (b) (d) Registered post 5 Marks

4. A contracted with B to supply him (B) 500 tons of iron-steel @ Rs.5,000 per ton, to be delivered at a

specified time. Thereafter, A contracts with C for the purchase of 500 tons of iron-steel @ Rs.4,800 per ton, and at the same time told ‘C’ that he did so for the purpose of performing his contract entered into with B. C failed to perform his contract in due course. Consequently, A could not procure claim from C in the circumstances? Explain with reference to the provisions of the Indian Contract, 1872.

5 Marks

5. Explain protection against attachment of amount standing to the credit of member under Employees Provident Fund and Miscellaneous Provisions Act 1952

5 Marks

6. When presentment for payment is excused? 5 Marks

7. Ram Gupta is working as salesman in a company on salary basis the following payments were made to him by the company during the previous financial year.

(i) Overtime allowance (ii) Dearness allowance (iii) Commission on sales (iv) Employer’s contribution towards pension fund (v) Value of food

Examine as to which of the above payments from part of salary of Ram Gupta under payment of Bonus Act, 1965.

5 Marks

3 ME29 / PRIME / PCC

8. When does a Public Ltd Company become a Private Company? 5 Marks 9. The main objects of the company is to manufacture cement. Seeing the potential for new business the

board of directors decided to go in for manufacture of steel and steel related products. These are included in the other objects of the company. Can the company undertake the aforesaid new business?

5 Marks 10. What is the meaning of “Doctrine of indoor management “?

State whether the doctrine of indoor management applies in the following cases: (i) When the person dealing with the company had notice of the internal irregularity (ii) Where he is put upon an enquiry 5 Marks

11. What is the Golden Rule of prospectus? 5 Marks 12. State the purposes for which securities premium account can be utilized. 5 Marks

PART II

Question no 13 is compulsory. Answer any two of the rest.

13 (a) what do you mean by Business Ethics? Explain its features. 5 Marks

(b) Who is stakeholder? Whether competitor is a stakeholder? 5 Marks

14. State the main reasons for ethical dilemmas at work place. 5 Marks

15. Define “Corporate Social Responsibility.”

State the nature of corporate social responsibility 5 Marks

16. State the aspects of code of conduct at work place 5 Marks

PART III

Question no. 17 is compulsory. Answer any two from the rest.

17 (a) what are the advantages of grapevine? 5 Marks

(b) Explain the role of body language (kinesics) in communication. 5 Marks 18. “Silence is always good in communication.” Do you agree with this statement? 5 Marks 19. Draft an affidavit regarding personal drawing for submitting to Income tax officer

5 Marks

20. What are the characteristics of emotional intelligence? 5 Marks

29ME/PRIME/ PCC 1

PRIME ACADEMY 29TH SESSIONMODEL EXAM

PCC-LAW ETHICS AND COMMUNICATION SUGGESTED ANSWERS

PART - I 1. (a)

(i) Revocation by Notice: An offer can be revoked by giving a notice of revocation any time before the communication of acceptance is completed as against the proposer, but not afterwards.

For example: A offers to B to sell his house on 1st Jan by sending a letter. B receives the letter on 5th Jan and posts a letter of acceptance on 10th Jan. A at once changes his mind and decides not to sell his house to B, but he informs B about the revocation of offer on 11th Jan. In this case, A cannot revoke the offer, as B has already sent a letter of acceptance before the letter revocation

(ii) Revocation by Lapse of Time: If the offer is not accepted within the time prescribed by the offeror, it will automatically be revoked.

(iii) Revocation by the death or Proposer: If the fact of death or proposer comes to the

knowledge of the acceptor before acceptance, the offer is revoked. (iv) Revocation by the insanity of Proposer: If the fact of insanity of proposer comes

to the knowledge of the acceptor before acceptance, the offer is revoked. (v) Revocation by Counter Offer. (vi) Revocation by not accepting the offer in the mode prescribed. (vii) Revocation by failure of the acceptor to fulfill a condition precedent to

acceptance: As we know that all the conditions of an offer must be satisfied by the acceptor, therefore if the acceptor fails to fulfill a condition precedent to acceptance, it will be revoked. For Example: A applies for 100 shares of a company on the condition that he should be appointed Secretary of the company. The company allots him shares, but does not appoint him secretary. In this case, the offer lapses, as the company does not fulfill the condition precedent to acceptance, i.e, it does not appoint A as Secretary of the company.

(b) As per Sec. 4 of the Indian Contract Act, 1872, the communication of an acceptance is a complete as against the acceptor when it comes to the knowledge of the proposer. An acceptance may be revoked at any time before the communication of the acceptance is complete as against the acceptor, but not afterwards. Referring to the above provisions (i) Yes, the revocation of acceptance by Raman (the acceptor) is valid. (ii) If Raman opens the telegram first (and this would be normally so in case of a

rational person) and reads it, the acceptance stands revoked. If he opens the letter first and reads it, revocation of acceptance is not possible, as the contract has already been concluded.

29ME/PRIME/ PCC 2

2. (i) 1

(a) An agreement the meaning of which is neither certain nor capable of being made certain is voidable.

(b) “A” agrees to pay “B” 1,000 if two straight lines should enclose a space, this agreement is valid because there is valid consideration.

(c) When both parties to an agreement are under a mistake as to a matter fact essential, the agreement is not valid.

(d) “A” contract to indemnity “B” against consequences of any proceeding, which “C” may take against “B” in respect of certain sum of 300 rupees, is contract of guarantee.

(e) A person employed and acting under the control of the original agent in the business of agency is co-agent.

2(a) Incorrect. An agreement the meaning of which is neither certain nor capable of

being made certain is void.

(b) Incorrect. “A” agrees to pay “B” 1,000 if two straight lines should enclose a space; this agreement is void because there is impossibility of performance.

(c) Correct. When both parties to an agreement are under a mistake as to a matter

fact essential, the agreement is void. (d) Incorrect. The situation mentioned herein is contract of indemnity and not

contract of guarantee. (e) Incorrect. A person employed and acting under the control of the original agent

in the business of agency is Sub-agent.

2. (ii)

1. Assignment of a contract means transfer of right and liabilities arising out of a contract to a third party. Assignment is not possible where the contract is of personal nature. For example, if A has engaged B to sing songs in his theatre, B cannot assign the contract to C or anyone else. However, where the contract is not dependent upon the personal skill, it may be assigned subject to certain conditions. Contracts can be assigned in 2 ways: Assignment by Act of Parties:

(i) Novation: A contract which is not of personal nature may be assigned, if both the parties to the agreement agree.

For example: A owes B Rs.2 Lac. A and B, by an agreement with C, can agree that now C will pay Rs.2 Lac to B. By this agreement, liability of B to pay the debt is transferred from A to C.

Exceptions:

(a) A person cannot become creditor of another without his consent. Example: A Owes B Rs.1,000. B assigns his debt to C. C cannot recover the amount from A as C cannot become A’s creditor without A’s consent.

29ME/PRIME/ PCC 3

(b) A person is under no obligation to accept a stranger as is debtor.

Example: A owes Rs.1,000 to B. A cannot ask B to recover the amount from C without the consent of B and C.

(I) Performance of contract through Agent: Where the contract is not of a

personal nature, A party can perform the contract through the competent Agent, provided the contract does not expressly or impliedly require performance only by the promisor.

(II) Assignment of Actionable Claim: Actionable claims can be assigned by instrument in writing Examples of actionable claims are as under- 1) Right of action arising out of a Contract; 2) Money debts, i.e. a certain sum of money: 3) Book debts; 4) A share in a partnership firm.

2) Assignment by operation of Law:

(i) Death: Where the contract is not of personal nature 0 – Assignment to legal

representative with limited liability. Where the contract is of personal nature – Contract comes to an end. (ii) Insolvency: Under the insolvency law, rights and liabilities of an insolvent

pass on to the official receiver or assignee. 3.

(i) A bearer instrument can be negotiated by: -

(a) Endorsement only (b) Delivery only (c) Both indorsement and delivery (d) None of the above

(ii) In which of the following case, the employee will be disqualified for bonus under

section 9 of the payment of Bonus Act, 1965:-

(a) fraud: or (b) riotous or violent behavior while on the premises of establishment: or (c) Theft, misappropriation or sabotage of any property of the establishment: (d) All of the above.

(iii) Which of the following is not included in the Employees Provident fund & Misc. Provisions act, 1952-

(a) The cash value of food concession (b) Any dearness allowance (c) Any presents made by the employer (d) All of the above

29ME/PRIME/ PCC 4

(iv) Completed year of service under the Payment of Gratuity Act means:-

(a) Service for one year (b) Continuous service (c) Continuous service for one year (d) Number of years of service

(v) A negotiable instrument payable to order can be can be transferred by:-

(a) Simple delivery (b) Endorsement (c) Both (a) and (b) (d) Registered post

(e) 3(i) - (b) Delivery only 3(ii) - (d) All of the above.

3(iii) - All of the above 3 (iv) - Continuous service for one year 3 (v) - Both (a) and (b)

4. i). In the instant case ‘A’ had intimated to ‘C’ that he was procuring iron steel

from him for the purpose of performing his contract whit ‘B’ Thus, C had the knowledge of the special circumstance. Therefore, A is entitled to claim from ‘C’ Rs.1,00,000 (difference between the procuring price of iron steel and contracted selling price to ‘B’) being the amount of profit ‘A’ would have made by the performance of his contract with ‘B’.

ii). If A had told C of ‘B’s contract, then the amount of damages would have been

the difference between the contract price and the market price on the day of default.

5. (i) The amount standing to the credit of any member in the Fund or any exempted

employee in a provident fund shall not be ASSIGNED/CHARGED/LIABLE TO ATACHMENT under any decree or order of any Court in respect of any debt or liability incurred by the member or the exempted employee. The official assignee or Official receiver shall not have any claim on any such amount.

(ii) On the death of member, any amount standing to his credit shall vest in the

nominee and shall be free from any debt or other liability incurred by the deceased or the nominee before the death of the member and shall also not be liable to attachment under any decree or order of any Court.

29ME/PRIME/ PCC 5

6. Notes, bills, cheques must be presented for payment to the maker, acceptor or drawee

thereof respectively by or on the behalf of the holder [Sec.64(1)]. In default of such presentment, the person with primary liability will not discharge. The other parties to the instrument will be discharged. When the presentment for payment is excused (Sec. 76):

1. The maker, drawee, or acceptor intentionally prevents presentment of the Instrument.

2. The instrument is payable at the business place of the maker, acceptor or drawee of the note, bill or cheque, and such place on the due date during the usual business hours is closed.

3. The instrument is neither payable at a specified place, and neither the marker, acceptor or drawee, nor their authorised person is present, during the usual business hours.

4. The instrument is not payable at a specified place, and the payer cannot be found after reasonable search.

5. There is a promise to pay notwithstanding non-presentment. 6. Presentment for payment is waived either expressly or impliedly. 7. The drawer could not suffer damage for want of presentment. 8. The bill is dishonoured by non-acceptance. 9. The drawer is a fictitious person or the drawer and the drawee are the same

person. 10. Presentment becomes impossible. In these cases, the instrument is deemed to

be dishonoured on the due date of presentment for payment.

7. (i) Overtime allowance

(ii) Dearness allowance

(iii) Commission on sales

(iv) Employer’s contribution towards pension fund

(v) Value of food

Salary is defined in Section 2 (21 ) of the Payment of Bonus Act, 1965. Accordingly the following are applicable.

(i)Overtime allowance - Not a part of salary

(ii)Dearness allowance - Part of salary

(iii)Commission on sales - Not a part of salary

(iv)Employer’s contribution - Not a part of salary

towards pension fund

(v)Value of food - Part of salary, if it is given in lieu of the whole or

part of the salary or wages payable to him

29ME/PRIME/ PCC 6

8. A Public company may become a Private Company by adopting the following steps:-

1. Alteration of Articles: Passing of Special Resolution, authorising the conversion

and altering articles so as to contain the matters specified in Sec. 3(1)(iii), 2. Change the Name: Changing the name of the company by Special resolution as

required by Sec. 21. 3. Bring the number of members within the limits specified by 3(1)(iii), i.e. upto 50. 4. Approval of CG: Obtaining the Approval of the Central Government as required

by Sec.31; Proviso to Sec. 31 5. Filing the Documents With ROC:

- A Printed Copy of the Altered Articles within 1 month of the receipt of the approval of the Central Government.

- Special Resolutions

9. Yes, the company can undertake the business of manufacture of steel and steel related products which are included in other objects of the company.