actuarial funding - ibexi solutions ::: reflecting on the future

TRANSCRIPT

Ibexi Solutions Page 1

Actuarial Funding

Tushar Falodia & Surajit Basu

Table of Contents

Executive Summary ..............................................................................................3 About the Authors.................................................................................................3 Introduction...........................................................................................................4 Insurance Concepts ...............................................................................................5

Traditional products ........................................................................................................5 Unit-linked products........................................................................................................5

Spreading out the charge across years ..................................................................7 Actuarial Funding .................................................................................................9 Multiple types of units ........................................................................................10 Early surrender: risk and restrictions ..................................................................11 Claims: reserves and risk ....................................................................................12 Capital adequacy impact: reserves and risk........................................................13 Issues ...................................................................................................................17 Conclusion ..........................................................................................................17

Ibexi Solutions Page 2

Special thanks .....................................................................................................18

Surajit Basu is an IBEXI consultant with over 15 years of experience. His focus is enterprise-wide implementations, management reporting and data warehousing for insurance.

Tushar Falodia is a consultant with IBEXI Solutions. He specializes in analysis in insurance. He has previously been a research analyst with a hedge fund. He holds an MBA in finance from Sydenham Institute Of Management Studies.

Executive Summary The journey of actuarial funding from its nativity in mutual funds to maturity in insurance has been evolutionary and experimental, with occasional challenges from regulators. The evolution of the insurance products from traditional to unit-linked has led to this concept. There are high initial costs incurred by the life insurance company; these are due to sales and marketing expenses, medical checks, underwriting and other administrative overheads. How will this be paid without charging all these to the customer immediately? Arising out of this need by insurers to manage the high initial charges with a seemingly more levelled charging structure, insurers use a concept of actuarial funding. This seems to solve the problem of the high initial charges, sustained regular charges, and higher early policy values. This model has its own challenges and complexities. Multiple types of units, with the same underlying investment pattern, early surrender, claims, capital adequacy and operational issues are some of these challenges. Balancing the benefits while managing the mis-selling potentials is not an easy task. Regulators are often left with the decision to allow or ban these products – with predictable results.

About the Authors

Ibexi Solutions Page 3

A similar story has occurred in an emerging market: India. Copying from the UK, some insurers started selling products based on actuarial funding. IRDA had asked companies to phase out these products from the market by 1st Jan ’08 on similar grounds as the UK. IRDA said “one reason why the regulator chose to ban the products rather than insist on better disclosure norms was concerns over rampant mis-selling. With over two million agents now selling insurance, the regulator has decided to standardize terms to make it easier for policyholder to understand costs and risk. Actuarial-funded policies increase the complexity.”

Introduction

The history of actuarial funding is unknown: there is no exact date or an inventor of the concept. It is a result of the experiments done by the mutual fund industry to find a way to recover the high initial expenses in the early years of the instrument, and yet keep intact the perception that they are investing a large percentage of the customer’s investments. This concept became popular in UK in the insurance industry also for their unit-linked products, as the concepts of the unit-linked products are similar to the mutual fund instruments. These products had a complicated structure, which made it very difficult for policyholders to work out exactly how much they were being charged. Because of this major drawback they were banned in the UK. More transparent charging structures became the norm for the industry. However, because of their long-term nature, many policies of this type are still in force in the UK.

The concern of the regulators is justifiable: policyholders believe these products have allocations of 95% or more, but technically it’s not true.

Ibexi Solutions Page 4

Again, as in UK, the policies sold will continue for the next several decades.

Insurance Concepts

The concept of actuarial funding is not widely known. The evolution of the insurance products from traditional to unit-linked has led to this concept.

Traditional products In traditional policies, the sum assured and bonuses (already declared) are guaranteed even if the investment conditions turn adverse. This means that the insurer covers both mortality and investment related risks. If investment conditions are favourable, the policyholder typically gets at least 90 per cent of the resulting profits after tax or depending on the profit sharing arrangement of the company. The high initial expenses are absorbed during the life of the policy. The company pays low dividends in the initial years on participating policies. Also, there is no surrender value for the first few years; even after that, the surrender value is low for the next few years.

Unit-linked products The value of a unit-linked policy is the product of the number of units under the policy and market value of the unit (known as net asset value or NAV). It can show an impressive gain when the market is bullish but can touch the bottom when bearish. The risk is borne entirely by the policyholder. Though investment related risks are not covered, these policies are attractive because of the chance they provide to secure high returns. The returns are visible immediately in terms of the increase in NAV. High expenses in first year are charged directly to customer early, and the reduced amount is used to buy units. So

returns are on the lower invested amount. Also, sometimes, there is no surrender value for the first few years. Let us consider a typical unit-linked plan. The allocation charge is 26.5 per cent of the premium in the first year and 2.5 per cent in subsequent years. If the annual premium is Rs. 50,000, a sum of Rs. 13,250 will be deducted from the first premium and the balance (known as allocation rate) of Rs. 36,750 will be allocated in the form of units.

Ibexi Solutions Page 5

Money allocated to the unit fund is used to purchase units in an investment fund (e.g. unit trust). The units have a selling price at which they may be

purchased from the fund managers and a re-purchase price at which they may be sold to the fund managers. The face value of each unit will be Rs. 10 while the real value — the NAV —

can be higher or lower, depending on market conditions. If the NAV is Rs.12.50 on the day the premium is received, 2940 units will be allotted. If it is Rs.7.50, then 4900 units will be allotted. From the second year onwards, the allocation rate is 97.5 per cent. When the market value of the assets increases, the value of the funds, and hence the NAV of the invested units will increase. The position will be the reverse when the market value decreases. In addition to the front-end charges, the managers will impose an annual management charge usually expressed as a (small) percentage of the value of the units on the day the charge is levied. These charges will accrue to the non-unit fund. Typically, there would be a deduction each month - say, of Rs. 60 per month in the first year and Rs. 20 per month in subsequent years towards administrative expenses. Apart from this, typically 1.5 per cent of the value of the fund pertaining to the policy will be deducted per year towards fund management expenses. Monthly charges towards risk cover will depend on the age of the life assured and the nature of risk covered.

Ibexi Solutions Page 6

There are high initial costs incurred by the life insurance company; these are due to sales and marketing expenses, medical checks, underwriting and other administrative overheads. How will this be paid? One model is to have a very high initial charge on the policy, matching the high initial costs. There is thus a very low allocation rate in the first year. Unfortunately, this leads to the customer unhappiness on seeing high deductions in the first year. It is especially difficult to compete with mutual funds that have a lower cost structure in the first year.

Spreading out the charge across years The real long-term profit for the company flows from the deductions towards fund management expenses, which is a percentage of the value of the fund also from Policy admin charge and mortality charge. Each has a profit component in their estimates. For the management charge as the fund size increases year after year, the amount deducted will also increase and be substantial after few years. To make its product attractive, a company may waive the deduction towards marketing expenses in the first year, allowing the allocation rate to go up to 100 per cent or even higher. Now the question arises. How then can it meet the high initial expenses in the first year? The answer is simple: the company can have lower than actual initial year charges by having higher than actual annual charges for future years. Example: A company offering 100 per cent allocation in the first year compensates itself by charging higher administrative and fund management expenses. For example, a fund management charge of, say, 2.5 per cent will be made instead of the usual 1-1.5 per cent. As actual expenses will be below 1 per cent, it will make money in the longer term which will offset the initial losses. For the customer, the initial cost is absorbed by the company, while a sustained growth is visible. This is marginally lower than the earlier approach, but the consistent lowering rather than a sudden drop makes it easier to sell this policy structure. Assuming NAV of 7.5 growing at 8% annually, with mortality cost of 5,000 growing at 4% annually, administration charges of 60/month for the first year, and 20/ month for subsequent years, two scenarios were simulated for an annual deposit of 50,000. Scenario 1: With 26.5% initial charge, 2.5% in subsequent years; 1.5% fund admin charge Scenario 2: With 0% initial charge, 2.5% in subsequent years; 2.5% fund admin charge

Ibexi Solutions Page 7

The fund growth illustrates that the scenario 2 starts with a higher fund value, but falls slowly over time. For the customer, the end-results of two scenarios may be similar at some point; scenario 1 is better in the long-term, and scenario 2 in the short-run.

Charge per year

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

1 2 3 4 5 6 7 8 9 10

Time in years

Ch

arg

e a

mo

un

t

Charges - 1Charges - 2Total charge - 1Total charge - 2

Ibexi Solutions Page 8

Fund growth

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

1 2 3 4 5 6 7 8 9 10

Time in years

Am

ount

Scenario 1 - Fund value

Scenario 2 - Fund value

The policy structure will lead to a combination of level and gradually increasing amounts of money flowing into the non-unit fund. Over 10 years, the marginal difference in the fund admin charge becomes significant, and hence the scenario 2 will be more profitable than scenario 1.

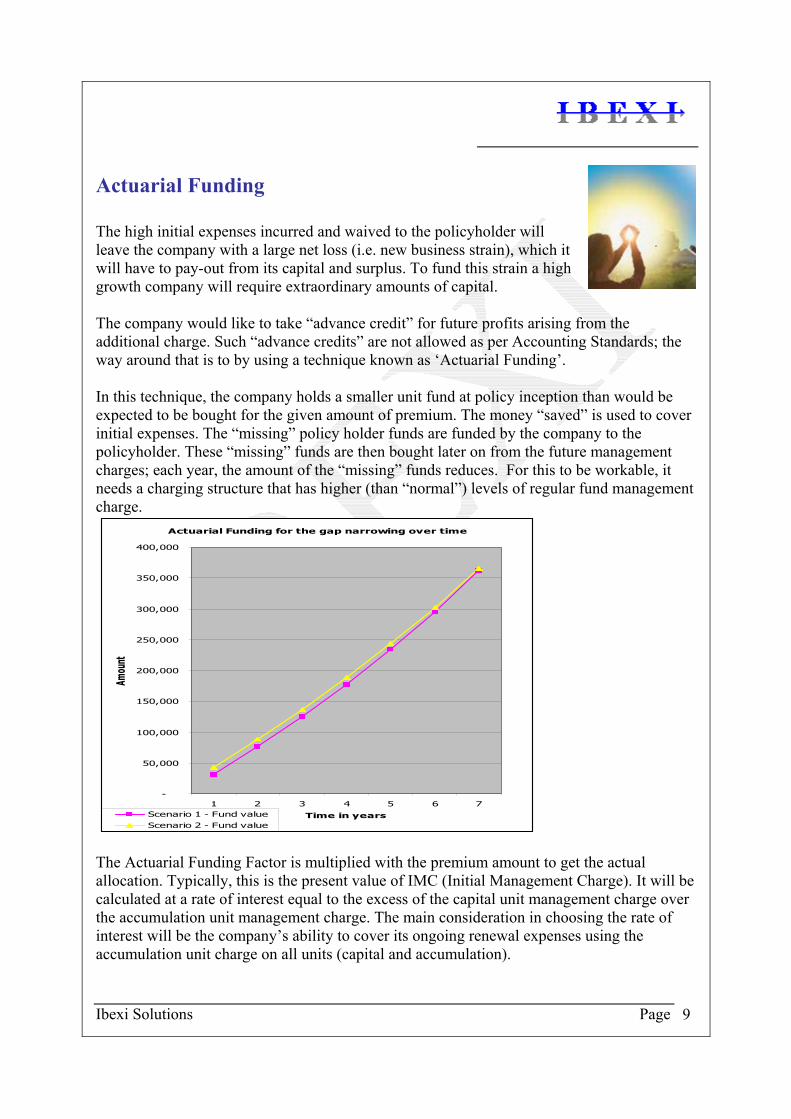

Actuarial Funding for the gap narrowing over time

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

1 2 3 4 5 6 7

Time in years

Amou

nt

Scenario 1 - Fund valueScenario 2 - Fund value

Actuarial Funding The high initial expenses incurred and waived to the policyholder will leave the company with a large net loss (i.e. new business strain), which it will have to pay-out from its capital and surplus. To fund this strain a high growth company will require extraordinary amounts of capital. The company would like to take “advance credit” for future profits arising from the additional charge. Such “advance credits” are not allowed as per Accounting Standards; the way around that is to by using a technique known as ‘Actuarial Funding’. In this technique, the company holds a smaller unit fund at policy inception than would be expected to be bought for the given amount of premium. The money “saved” is used to cover initial expenses. The “missing” policy holder funds are funded by the company to the policyholder. These “missing” funds are then bought later on from the future management charges; each year, the amount of the “missing” funds reduces. For this to be workable, it needs a charging structure that has higher (than “normal”) levels of regular fund management charge.

Ibexi Solutions Page 9

The Actuarial Funding Factor is multiplied with the premium amount to get the actual allocation. Typically, this is the present value of IMC (Initial Management Charge). It will be calculated at a rate of interest equal to the excess of the capital unit management charge over the accumulation unit management charge. The main consideration in choosing the rate of interest will be the company’s ability to cover its ongoing renewal expenses using the accumulation unit charge on all units (capital and accumulation).

Multiple types of units

Insurers generally divide the premiums into two types of accounts within one investment fund. The first type of units are called capital or initial units, would attract a higher management charge than the second type which is called accumulation or ordinary units. Typically during the first few years of a unit-linked assurance, allocated premiums would be used to buy capital units. Subsequently, allocated premiums would be used to buy accumulation units. Another way is to utilize the full first year’s premium for buying capital units. The names “capital” and “accumulation” do not mean anything special – they were chosen historically for marketing reasons and became convention, at least in the UK. The underlying investments would be the same for the two types of units. The only difference between the two is the greater fund management charge on the capital units. The value of actuarially funded capital units will then be invested by the company to grow at a similar rate to its accumulation units, and the excess management charges regularly accruing will be used to purchase additional capital units.

Ibexi Solutions Page 10

Early surrender: risk and restrictions There is a difference between the fund value shown to the policy holder and the actual fund value, which is lower, at least in the initial years. If there is surrender in these initial years, the insurance company has to pay out the excess fund value shown to the policy holder. This is the risk of early surrender. This problem is countered by high surrender charges or surrender penalty. Surrender penalty is imposed to make the net present value indifferent to surrender; every surrender penalty would need to compensate the company for the loss of all the expected future profit that the policy would have earned had it remained in full force. It can also be said that the surrender penalty is the difference between the fund value shown to the customer and the actual fund value. The penalty or charge cannot, however, be explicitly calculated for the policy, as that would be the same as showing the difference between the fund value shown to the policy holder and the actual fund value. It would also be difficult to have predefined rules in the policy which allow the policy-holder to transparently calculate the surrender charges; this transparency is required at the time of selling. Insurers use different predefine models for these surrender charges. One way is to make this time-based: a high surrender charge for the first few years, assuming the units will grow sufficiently over this time. Another way is to lock in the first premium and its growth; thus, the initial premium would not be returned for early surrender. A third way –common in actuarial funding methods – is to lock in the capital units; initial premiums, and a reducing amount of the premiums of the next few years are invested in these capital units, which are not paid out for an early surrender. It is important to note that the pricing of these charges has to take into account the probability of early surrenders; otherwise, the insurer may charge a very high surrender charge to all policyholders, and minimise the market potential of the product.

Ibexi Solutions Page 11

Claims: reserves and risk

The other scenario of payout is claims, e.g. death. In this scenario also, the same question arises: by how much one can, or should, reduce unit fund (or unit reserve) in the actuarial funding process. Firstly the insurance company needs to be able to justify doing the process at all. As under the unit-linked contract, the full amount of the unit fund (i.e. its face value without any actuarial funding reduction) has to be available to the policyholder under a contractual claim. If the company holds a lower amount of reserve than this, won’t the company be in trouble? So how can a company hold lower reserves than the face value of the units? The answer is that the unit fund is accounted for separately from the non-unit fund. Usually the unit fund is fully funded in the sense that investments (units) are held which exactly match the value of the units purchased by the allocated premiums. However, the unit fund will only be required when certain contingent events occur or in endowments plans where the cash value will be returned on maturity. For example, when the policyholder dies, the unit fund, together with any additional payment from the non-unit fund to make the sum paid on death up to the guaranteed minimum payment, will be needed. Because the liabilities are contingent then it is reasonable to hold the actuarial present value of the unit fund rather than its fully funded value. It also creates an additional liability on the non-unit fund because on the death of the policyholder the amount required to make up the value of the unit fund to the guaranteed minimum sum assured will be larger. This expected additional death cost is a charge on the non-unit fund at end of each year.

Ibexi Solutions Page 12

Capital adequacy impact: reserves and risk As discussed earlier for a company selling actuarial products the capital needs for initial policy is huge as most of the initial expense occurred is funded from capital or surplus accounts. The question that arises is that, are the extra units really there? Or are they notionally bought by company, on proportional basis (using probability of surrender etc.). In profit testing terms, for capital units that are actuarially funded the usual cash flow of unit management charges from the unit fund to the non-unit fund will be adjusted to:

• A cash flow from the unit to the non-unit fund of the difference between fully funded and actuarially funded (unfunded) units on each unit purchase.

• A cash flow from the unit fund to the non-unit fund of the capital unit charge on the capital units, but followed at the same time by a cash flow from the non-unit fund to the unit fund to build up the (increasing number of) actuarially funded capital units required at the year-end.

To understand the concept better, let’s look at the example below comparing the normal unit-linked product and an Actuarial funded unit-linked product. Assumptions:

• Fund growth is constant at 10% • Expenses constant at 5%

Normal Unit-linked product

• Annual Premium paid by the policy holder is Rs 10,000 for 15yrs. • Low allocation percentage for initial 3 yrs and constant after 4th year. • Actual allocation after deducting 5% for expenses grows at 10 percent per annum. • Fund at the beginning of 2nd year onwards = (year’s premium * allocation

percentage) + fund value at the end of last year.

Ibexi Solutions Page 13

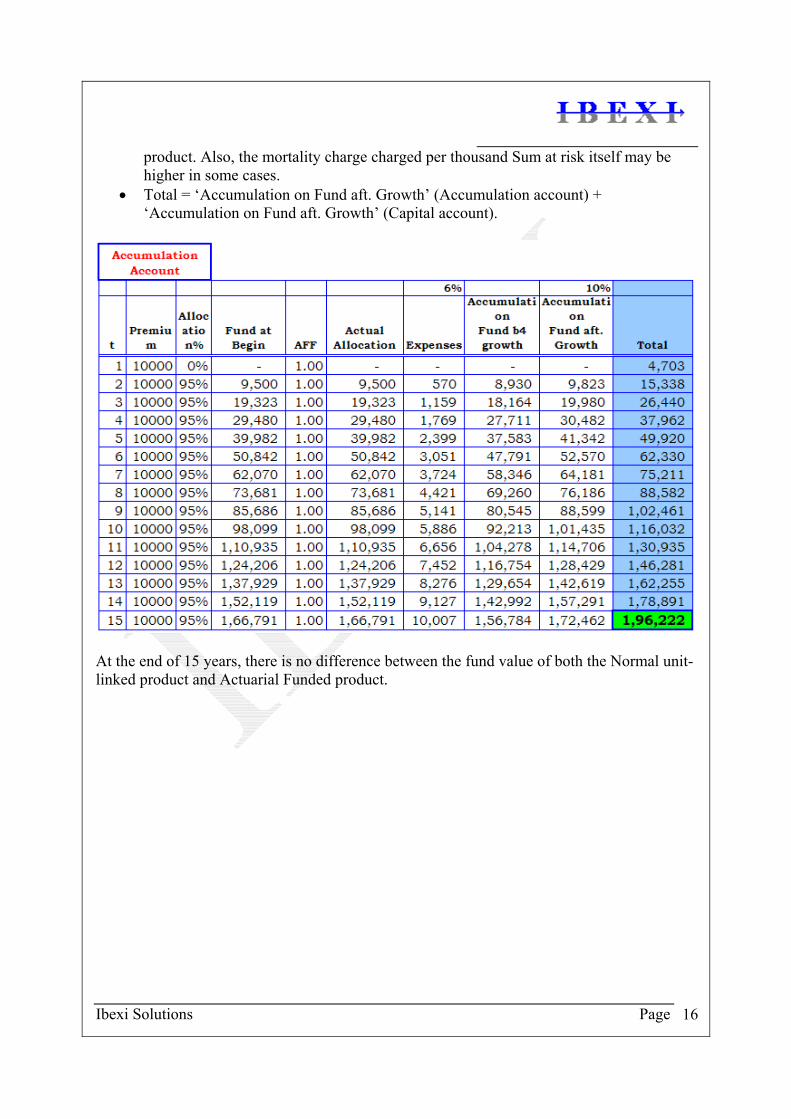

• At the end of the 15 years the fund value is Rs 1, 96,223.

Actuarial Funded Unit-linked product As discussed earlier the full first year premium goes towards Capital Account and 2nd year onwards it goes into Accumulation Account (it’s not a rule, it can be more than one year). In the table below both the accounts are explained. Capital A/c

• Only first year’s premium is accounted for in this account. • Fund statement shown to the policy owner is till ‘Unfunded capital Fund aft. Growth’

highlighted in yellow. Out of his total premium paid in the first year 95% is invested. • In the Capital Account maintained by the insurance company which show the actual

amount that will be paid to the policy holder at the time of surrender. The ‘Fund at the beginning’ amount is multiplied by the Actuarial Funding Factor to get the actual amount available (Funded Capital Fund) with the insurance company for purchasing unit. This amount grows at 10% for the year.

• Actuarial Funding Factor: - Is constant after 10 years. It is nothing but the present value of IMC (Initial Management Charge) i.e. 5% per annum. It is charged on monthly basis to the account.

Ibexi Solutions Page 14

• The picture that is put forth to the policy holder shows the fund value as Rs 9,928 but actually he has only Rs 4,275 in his account. So what will happen if he surrenders the policy in the first year? How will insurance company make good the difference?

• The answer to this is Surrender Penalty. It is the difference of amount Rs 5,225 that will be reduced from his account value and he will be paid Rs 4,275 (Actual amount lying in his account). This is a penalty to the holder for surrendering the policy within 10 yrs.

Accumulation A/c:

• The entire premium amount from the 2nd year is accounted in accumulation account. • This is similar to the normal unit-linked account (Fig.1) except for the last column

highlighted in blue. • Why is there a 6 % expense when there is a constant growth rate & expenses

percentage? • This is because there is a mortality which depends on the fund value

Mortality charge = Mortality charge * Sum at Risk Where Sum at Risk = Sum Assured - Fund Value

Ibexi Solutions Page 15

For Actuarial Funded products the (actual) sum invested is less (after multiplying the allocated amount by Actuarial Funding Factor). Thus the Sum at Risk increases compared to normal Unit-linked products e.g. 95% of Premium is invested in normal Unit-linked product where as 95%of 0.45 = 42.5% is invested in Actuarial Funded products. Hence, fund value gets lesser. Hence the mortality charge is more for AFF

product. Also, the mortality charge charged per thousand Sum at risk itself may be higher in some cases.

• Total = ‘Accumulation on Fund aft. Growth’ (Accumulation account) + ‘Accumulation on Fund aft. Growth’ (Capital account).

Ibexi Solutions Page 16

At the end of 15 years, there is no difference between the fund value of both the Normal unit-linked product and Actuarial Funded product.

Issues There are many issues to be considered for these products. Some of these are:

• Difficult to maintain two accounts (Capital & Accumulation accounts).

• Difficult to understand the 2 accounts concept and present them correctly in various accounting treatments such as US GAAP.

• Difficult to handle cases of lapse. Once the policy is lapsed, should the insurer continue to deduct Initial management charge? If yes, why? On approach lies in maintaining two tables for the lapsed cases – one which deducts Initial management charge and the one which does not.

• A similar problem lies in reinstated cases: Because the funded value is calculated by multiplying Unfunded amounts by the Actuarial Funding Factor, and the unfunded value is not known for lapsed cases where the lapsed amount has not been processed for years.

• Increased Complexity as Lower initial charge is charged to the customer which is funded by long-term charges.

• Partial capital infusion in the early years of policy. To reduce the strain and low investment needs for company, as all units not bought upfront.

• Company gets huge profit if policy holder surrenders or policy lapses during the funding term. So it is a cash loss for the customer, with a non-transparent surrender charge process, as initial premiums and growth not returned to the policy holder. These lead to problems from the regulatory point of view.

Conclusion In the business of unit-linked products, simplicity is a complex requirement. Despite the best attempts by actuaries and insurers to create a simple-looking product which will grow uniformly over time, without a false start, the products and the processes have become increasingly complex. Some of these processes are invisible to the typical end-customer; this is done to create or maintain the illusion of simplicity. As the illusion of the product fades, confusion triumphs over clarity, mis-selling over modelling. Regulators tend to step in, and stop the product. Actuarial funding seems to emerge and then fade.

Ibexi Solutions Page 17

Ibexi Solutions Page 18

Special thanks

• D. Pashupati (Director, Ibexi Solution Pvt. Ltd.) • Bikash Choudhary (Sr. Manager – Actuarial, Bajaj Allianz Life Insurance Company

Ltd.) • Gautam Shah (Sr. Manager – Actuarial, Birla Sun Life Insurance Company Ltd.) • Mayukh Gayen (Manager-Actuarial, Bajaj Allianz Life Insurance Company Ltd.) • Neha Gupta (Manager-Actuarial, Birla Sun Life Insurance Company Ltd.)