actuarial function holder - zurich · actuarial function holder report – esi scheme 1 . proposed...

TRANSCRIPT

Actuarial Function Holder Report – ESI Scheme

1

Proposed Scheme to Transfer the Long-Term Insurance Business of the Maltese Branch of Eagle Star Insurance Company Limited (‘ESI’) to the Maltese Branch of Zurich Assurance

Ltd (‘ZAL’)

Report of ESI’s and ZAL’s

Actuarial Function Holder

on the proposed transfer of business pursuant to Part VII of the Financial Services and Markets Act (2000) (“FSMA”).

David Ford, FIA Actuarial Function Holder 20 May 2015

Actuarial Function Holder Report – ESI Scheme

2

Contents 1 Introduction ..................................................................................................................... 4

1.1 Background .......................................................................................................................... 4

1.2 Disclosures .......................................................................................................................... 4

1.3 Compliance with Technical Actuarial Standards ............................................................ 4

1.4 Definitions and abbreviations ............................................................................................ 5

1.5 Structure of report ............................................................................................................... 5

2 Overview of ZAL .............................................................................................................. 6

2.1 Background .......................................................................................................................... 6

2.2 Business ............................................................................................................................... 6

2.3 Pillar 1 position of ZAL ....................................................................................................... 7

2.4 Risk profile of the business ............................................................................................... 8

2.5 Capital management policy ................................................................................................ 8

3 Overview of ESI ............................................................................................................... 9

3.1 Background .......................................................................................................................... 9

3.2 Business ............................................................................................................................... 9

3.3 Pillar 1 position of ESI ...................................................................................................... 10

3.4 Risk profile of the business ............................................................................................. 11

3.5 Capital management policy .............................................................................................. 11

3.6 Ownership of ESI long-term fund surplus assets ......................................................... 11

3.7 Surplus assets in the shareholder’s fund ...................................................................... 12

4 Summary of the proposed ESI Scheme ..................................................................... 13

4.1 Background ........................................................................................................................ 13

4.2 Scheme summary .............................................................................................................. 13

5 Financial position before and after transfer.............................................................. 15

5.1 Introduction ........................................................................................................................ 15

5.2 Solvency I Pillar 1 .............................................................................................................. 15

5.3 Solvency I Pillar 2 .............................................................................................................. 17

5.4 Solvency II .......................................................................................................................... 17

Actuarial Function Holder Report – ESI Scheme

3

6 The effect of the Scheme on policyholders .............................................................. 18

6.1 Risk profile of the combined businesses ....................................................................... 18

6.2 Security of policyholder benefits .................................................................................... 18

6.3 Benefit expectations – with-profits policyholders ........................................................ 18

6.4 Benefit expectations – non-profit policyholders ........................................................... 19

6.5 Governance of the with-profits fund ............................................................................... 19

6.6 Service standards .............................................................................................................. 19

6.7 Taxation .............................................................................................................................. 19

6.8 Policyholder communications ......................................................................................... 19

6.9 Report of the With-Profits Actuary .................................................................................. 20

7 Conclusion ..................................................................................................................... 21

Appendix A: Terms and definitions .................................................................................. 22

Terms used in this report ............................................................................................................ 22

Company abbreviations referred to in this report .................................................................... 23

Actuarial Function Holder Report – ESI Scheme

4

1 Introduction

1.1 Background

1.1.1 The purpose of this report is to describe the impact on the policyholders of Zurich Assurance Ltd (‘ZAL’) and of Eagle Star Insurance Company Limited (‘ESI’) of a Part VII Scheme under the Financial Services and Markets Act 2000 (the ‘ESI Scheme’ or ‘Scheme’), the objective of which is to transfer the long-term insurance business of the Maltese branch of ESI to the Maltese branch of ZAL.

1.1.2 In particular, this report states how it will affect the security of the policyholder’s benefits and their reasonable benefit expectations, and how, in my view, the Scheme is consistent with the requirements to treat customers fairly.

1.1.3 I am writing this report in my capacity as the Actuarial Function Holder for both ZAL and ESI. It should be read in conjunction with the Scheme, the With-Profits Actuary’s Report on the Scheme, and the Independent Expert’s Report on the Scheme.

1.2 Disclosures

1.2.1 I am a Fellow of the Institute & Faculty of Actuaries, having qualified in 1990, and hold a certificate issued by the Institute & Faculty of Actuaries to act as Actuarial Function Holder (AFH). I have been the AFH for ZAL and ESI since June 2008. I have over 25 years of experience working in the UK life assurance industry.

1.2.2 I am an employee of Zurich Employment Services Ltd, which is a wholly owned subsidiary of Zurich Financial Services (UKISA) Limited. Zurich Insurance Group Ltd (ZIG) is the ultimate parent of both companies, and of both ESI and ZAL.

1.2.3 I do not hold any individual insurance policies with either ZAL or ESI, other than as a member of the Zurich Financial Services UK Pension Scheme defined contribution pension arrangement. I have a direct interest in shares of ZIG, and am entitled to participate in both the Group’s Long Term and Short Term Incentive Plans.

1.2.4 I confirm that my financial and personal interests in ZIG have not influenced me in reaching any of the conclusions detailed in this report.

1.3 Compliance with Technical Actuarial Standards

1.3.1 The Financial Reporting Council has issued standards known as Technical Actuarial Standards (TAS). Four standards applicable to this Report were in effect at the date of its preparation:

• Technical Actuarial Standard R: Reporting Actuarial Information (TAS R) version 2, effective 1 April 2010

• Technical Actuarial Standard D: Data (TAS D) version 1, effective 1 July 2010

• Technical Actuarial Standard M: Modelling (TAS M) version 1, effective 1 April 2011

Actuarial Function Holder Report – ESI Scheme

5

• The Insurance Technical Actuarial Standard (The Insurance TAS) version 1, effective 1 October 2011

This report has been prepared in accordance with these standards.

1.4 Definitions and abbreviations

1.4.1 A list of the definitions and abbreviations that I have used in this document is included in Appendix A.

1.5 Structure of report

1.5.1 This report is structured as follows:

• Section 2 provides an overview of ZAL;

• Section 3 provides an overview of ESI;

• Section 4 outlines the proposed Scheme;

• Section 5 considers the estimated financial position of the companies before and after the Transfer;

• Section 6 sets out the effect of the Scheme on ZAL and ESI policyholders;

• Section 7 sets out my conclusions;

• Appendix A lists the abbreviations used in this report.

Actuarial Function Holder Report – ESI Scheme

6

2 Overview of ZAL

2.1 Background

2.1.1 ZAL is a UK registered, wholly-owned indirect subsidiary of Zurich Insurance Group Ltd, a company incorporated in Switzerland which is the ultimate holding company of the Zurich group of companies. ZAL is regulated in the UK.

2.1.2 Eagle Star Life Assurance Company Limited (ESLAC) was formed in 1990 and the UK long-term business of ESI was transferred into ESLAC in 1991. In 2005, other long-term insurance business (that of Allied Dunbar Assurance plc being the largest of these) was transferred into ESLAC. In 2005, the name of ESLAC was also changed to Zurich Assurance Ltd (ie ZAL).

2.1.3 The Maltese branch of ZAL sold life business for four years until 31 December 1994; all policies were sold to Maltese residents.

2.2 Business

2.2.1 Below is a summary of the in-force business of ZAL at 31 December 2014 as shown in the Prudential Regulation Authority (“PRA”) Annual Return (Forms 50 through 54):

Actuarial Function Holder Report – ESI Scheme

7

2.2.2 ZAL writes a full range of life assurance business, but unit-linked business predominates.

2.3 Pillar 1 position of ZAL

2.3.1 The Pillar 1 position of ZAL at 31 December 2014 was as follows:

Table 2.1: ZAL Mathematical Reserves as at 31 December 2014

Number of Policies

Gross of Reinsurance

Reinsurance Ceded - External

Reinsurance Ceded -

Intra-GroupNet of

Reinsurance£000 £000 £000 £000

Non-Linked Business

UK Life Business (With-Profits) 16,176 265,783 - - 265,783UK Life Business (Non-Profit) 470,844 398,373 (63,180) 118,038 343,516UK Pensions Business (With-Profits) 13,285 847,522 - - 847,522UK Pensions Business (Non-Profit) 1,156,446 2,230,598 346,365 1,187,299 696,934Overseas Business (With-Profits) 1,835 31,815 - - 31,815Overseas Business (Non-Profit) 42,650 387,539 20 - 387,519

1,701,236 4,161,629 283,205 1,305,336 2,573,088

Accumulating With-Profits Business

UK Life Business (With-Profits) 5,731 134,751 - - 134,751UK Pensions Business (With-Profits) 37,515 390,012 - - 390,012Overseas Business (With-Profits) 14,747 177,878 - - 177,878

57,993 702,641 - - 702,641

Property-Linked Business *

UK Life Business (Unit-Linked) 457,937 11,624,486 - 171 11,624,316UK Life Business (Non-Linked) 196,410 3,033 2,806 190,571UK Pensions Business (Unit-Linked) 828,061 27,957,263 9,022,193 - 18,935,070UK Pensions Business (Non-Linked) 147,724 (19,652) - 167,376Overseas Business Unit-Linked) 10,802 337,382 - 15,063 322,318Overseas Business (Non-Linked) 4,456 - 119 4,337

1,296,800 40,267,721 9,005,574 18,159 31,243,988

Index-Linked Business *

UK Life Business (Unit-Linked) 208 15,830 - - 15,830UK Life Business (Non-Linked) - - - - UK Pensions Business (Unit-Linked) 701 93,429 3,595 81,169 8,666UK Pensions Business (Non-Linked) - - - - Overseas Business Unit-Linked) 34 2,473 - - 2,473Overseas Business (Non-Linked) - - - -

943 111,732 3,595 81,169 26,969

Total mathematical reserves 3,056,972 45,243,723 9,292,374 1,404,664 34,546,685 * Non-linked liability attaches to a linked policy so no policy count is shown under non-linked

Actuarial Function Holder Report – ESI Scheme

8

2.4 Risk profile of the business

2.4.1 The risk profile of ZAL is characterised by the fact it writes a broad range of life insurance business and is exposed to the usual risks, including:

• Market risk from the impact of market movements on the assets it holds backing policyholder liabilities;

• Insurance risks, particularly in respect of mortality, longevity, lapses and expenses; • Operational risk, including in respect of strategic initiatives to develop ZAL’s business; • Credit risk, particularly in respect of holdings in investment grade corporate bonds and

counterparty risk as a result of external reassurance.

2.4.2 ZAL is not directly exposed to pension scheme risk as two management services companies (Zurich Employment Services Limited for Life business staff and Zurich UK General Employee Services Limited for General business staff) are the participating employers in the scheme and ZAL is not responsible for making any payments to reduce any deficit for past service. Any risk arising from changes in future service contribution levels is part of expense risk.

2.5 Capital management policy

2.5.1 ZAL's operates target solvency levels on both a Pillar 1 and a Pillar 2 basis. Its solvency at 31 December 2014 was significantly above these levels, but it paid an interim dividend of £230m during March 2015 which reduced the extent of the excess capital.

2.5.2 ZAL has not yet determined its Solvency II capital buffer.

Table 2.2: Solvency Position of ZAL

31 Dec 2014£000

Long-term fundRegulatory value of assets 35,680,607Mathematical reserves (Non-Profit) (32,698,925)Mathematical reserves (With-Profits) after distribution of reversionary bonus (1,853,081)Other liabilities (679,754)Excess of assets over liabilities (A) 448,847

Shareholders' fundRegulatory value of assets 637,302Other liabilities (10,727)Shareholder net assets (B) 626,575

Capital resources (C = A + B) 1,075,422

Capital resources requirement (CRR) (D) 651,796

Excess of capital resources over CRR (E = C - D) 423,626Ratio of excess capital resources to CRR (F = E / D) 65%

Actuarial Function Holder Report – ESI Scheme

9

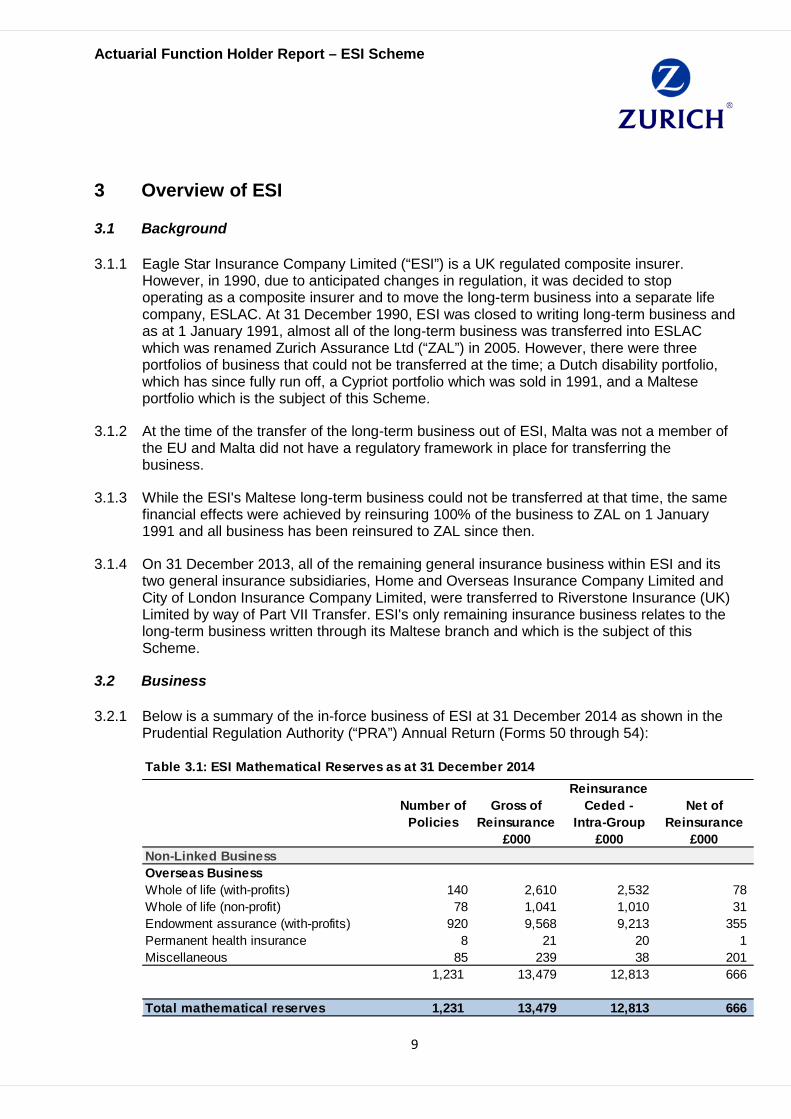

3 Overview of ESI

3.1 Background

3.1.1 Eagle Star Insurance Company Limited (“ESI”) is a UK regulated composite insurer. However, in 1990, due to anticipated changes in regulation, it was decided to stop operating as a composite insurer and to move the long-term business into a separate life company, ESLAC. At 31 December 1990, ESI was closed to writing long-term business and as at 1 January 1991, almost all of the long-term business was transferred into ESLAC which was renamed Zurich Assurance Ltd (“ZAL”) in 2005. However, there were three portfolios of business that could not be transferred at the time; a Dutch disability portfolio, which has since fully run off, a Cypriot portfolio which was sold in 1991, and a Maltese portfolio which is the subject of this Scheme.

3.1.2 At the time of the transfer of the long-term business out of ESI, Malta was not a member of the EU and Malta did not have a regulatory framework in place for transferring the business.

3.1.3 While the ESI's Maltese long-term business could not be transferred at that time, the same financial effects were achieved by reinsuring 100% of the business to ZAL on 1 January 1991 and all business has been reinsured to ZAL since then.

3.1.4 On 31 December 2013, all of the remaining general insurance business within ESI and its two general insurance subsidiaries, Home and Overseas Insurance Company Limited and City of London Insurance Company Limited, were transferred to Riverstone Insurance (UK) Limited by way of Part VII Transfer. ESI's only remaining insurance business relates to the long-term business written through its Maltese branch and which is the subject of this Scheme.

3.2 Business

3.2.1 Below is a summary of the in-force business of ESI at 31 December 2014 as shown in the Prudential Regulation Authority (“PRA”) Annual Return (Forms 50 through 54):

Table 3.1: ESI Mathematical Reserves as at 31 December 2014

Number of Policies

Gross of Reinsurance

Reinsurance Ceded -

Intra-GroupNet of

Reinsurance£000 £000 £000

Non-Linked BusinessOverseas BusinessWhole of life (with-profits) 140 2,610 2,532 78Whole of life (non-profit) 78 1,041 1,010 31Endowment assurance (with-profits) 920 9,568 9,213 355Permanent health insurance 8 21 20 1Miscellaneous 85 239 38 201

1,231 13,479 12,813 666

Total mathematical reserves 1,231 13,479 12,813 666

Actuarial Function Holder Report – ESI Scheme

10

3.2.2 As at 31 December 2014 there were 1060 with-profits polices (90:10 endowment assurance and whole of life polices) and 171 non-profit policies (mostly whole of life and level term). There was no unit-linked or index-linked business.

3.2.3 The gross technical provisions at year end 2014 were £13.5m and the net technical provisions were £0.7m, comprising £0.4m for counterparty credit risk (set at 3.0% of the technical provisions ceded), £0.2m in case of future policyholder complaints and £0.1m expense allowance for the cost of preparing the statutory returns.

3.2.4 Given the small number of Maltese policies, the impact of expenses on policyholder returns became an issue in the 1990s and the decision was taken by management, in the interests of the policyholders’ reasonable expectations, to set the bonus rates on the Maltese business to be equivalent to similar policies in the UK. This was discussed at the time with the Maltese Financial Services Authority (MFSA) and is communicated to policyholders via the annual bonus communications.

3.3 Pillar 1 position of ESI

3.3.1 The Pillar 1 position of ESI at 31 December 2014 was as follows:

3.3.2 As ESI is no longer authorised for general insurance business, the Capital Resources Requirement (CRR) is that for a life assurance company.

Table 3.2: Solvency Position of ESI

31 Dec 2014£000

Long-term fundRegulatory value of assets 1,365Mathematical reserves (non-profit) (233)Mathematical reserves (with-profit) after distribution of reversionary bonus (433)Other liabilities (699)Excess of assets over liabilities (A) -

Shareholders' fundRegulatory value of assets 35,743Other liabilities (7,860)Shareholder net assets (B) 27,883

Capital resources (C = A + B) 27,883

Capital resources requirement (CRR) (D) 2,902

Excess of capital resources over CRR (E = C - D) 24,981Ratio of excess capital resources to CRR (F = E / D) 861%

Actuarial Function Holder Report – ESI Scheme

11

3.4 Risk profile of the business

3.4.1 The risk profile of ESI is characterised by the fact that the whole of its life business is reinsured to ZAL.

3.4.2 The investments held by ESI are not held to back insurance liabilities and largely short-term money market investments; market risk is therefore limited.

3.4.3 ESI is not exposed to life insurance risks as a result of the reinsurance arrangements, but has a counterparty risk exposure relating to that reinsurance.

3.4.4 In addition, it has counterparty risk exposure to ZIC as a result of an inter-company loan of £135m to that entity which is not admissible for Pillar 1 solvency purposes. However, given the financial strength of ZIC (AA- rated), the risk of any potential loss arising from the loan is considered to be significantly lower than the ICA or Solvency II thresholds of 1:200.

3.4.5 In respect of operational risk, ESI outsources the administration of its Maltese life business to Eagle Star (Malta) Limited (ESM), a wholly owned subsidiary of ZAL. Given the control framework in place at ESM and ESI management’s regular liaison with ESM, I do not consider that material operational risk exposure arises within ESI.

3.4.6 ESI is also not directly exposed to pension scheme risk as the management services companies are the participating employers in the scheme and ESI is not responsible for making any payments to reduce any deficit for past service. Any risk arising from changes in future service contribution levels is part of expense risk.

3.5 Capital management policy

3.5.1 Given the very significant restructuring that ESI has been undergoing, the proposed transfer of the remaining life business to ZAL, and its eventual de-authorisation, ESI currently has capital significantly in excess of that which it would retain if it were continuing as a stand-alone life insurer in run-off. I have been informed that the company will pay a dividend to reduce the extent of that excess capital but that is not currently expected to take place until after the scheme effective date.

3.6 Ownership of ESI long-term fund surplus assets

3.6.1 At 31 December 2014 ESI’s long-term fund had no surplus assets but the scheme will result in the release of reserves in respect of credit risk and the expense reserve to cover the cost of producing regulatory returns. It is therefore appropriate to consider the source of those surplus assets, which dates back to the 1990 Scheme:

• Para 2(i) of the 1990 Scheme states that the assets retained in the ESI long-term fund are those attributable to the Dutch disability policies. This is supported by the reports of both the ESI Actuary (para 1) and the Independent Actuary (paras 3.1 and 3.2).

• Furthermore, para 4.7 of the Independent Actuarial Report on the 1990 Scheme states that the Dutch policies are non-participating other than on a pooled basis.

Actuarial Function Holder Report – ESI Scheme

12

Review of recent regulatory returns shows that the last such policy expired during 2007.

3.6.2 I have investigated and, and having received legal advice, in light of 3.6.1 I concluded that, as the Dutch disability pool liability has been fully extinguished, any surplus arising in the long-term fund as a result of the scheme belongs entirely to shareholders.

3.7 Surplus assets in the shareholder’s fund

3.7.1 There are significant capital and reserves within the shareholder’s fund totalling some £163m, including an inadmissible asset in the form of an intra-group loan to Zurich Insurance Company Ltd (ZIC) of £135m. The reason for the magnitude of these assets relates to the fact the ESI was a major writer of general insurance before that business was transferred out under previous schemes, and the capital position of ESI has not yet been optimised. However, these assets are outside of the long-term fund and the 1990 scheme confirms that the long-term policyholders have no interest in them, other than to the extent that they provide additional capital support for the company.

Actuarial Function Holder Report – ESI Scheme

13

4 Summary of the proposed ESI Scheme

4.1 Background

4.1.1 When ESI transferred the bulk of its long-term business to ZAL on 1 January 1991 (at which date all other long-term business of ESI, other than the transferring Maltese policies, a Dutch disability portfolio (which has since fully run off) and a Cypriot portfolio (which was sold in 1991), was transferred to ZAL under the Companies Act 1982), Malta was not a member of the EU and the Maltese supervisor did not have a regulatory framework to govern the transfer of insurance businesses.

4.1.2 There is now such a regulatory framework in place in Malta (see Part VIII of the Insurance Business Act (1998)) and prior to the implementation of Solvency II, Zurich wishes to transfer the remaining long-term business in ESI to ZAL. This will simplify the implementation requirements of Solvency II and improve the capital efficiency of the Group without having a materially adverse impact on policyholders.

4.2 Scheme summary

4.2.1 Under the proposed ESI Scheme, all of the long-term business of ESI will be transferred to ZAL on the proposed Scheme Effective Date (SED). Except for any assets held in respect of residual policies, the assets covering ESI gross technical provisions will be transferred to the relevant ZAL long-term business fund when the reinsurance contract is cancelled on the SED. ESI will also make a payment of £187,000 to ZAL to cover the expected value of the additional Maltese Corporation Tax which ZAL will have to pay as a result of the scheme.

4.2.2 Under the terms of the 1990 Scheme, the assets retained within the ESI long-term fund are those attributable to Dutch disability business. All assets in which the Malta policyholders have an interest were transferred to ZAL as a result of that scheme. Consequently the estate pertaining to the Malta with-profits policies exists as part of the ZAL 90:10 with-profits fund and no part is contained within the ESI long-term fund.

4.2.3 Following the ESI Scheme the transferring contracts will be held within the ZAL long term fund to which they are currently reassured. If there are no residual contracts, ESI will have no remaining insurance business, and Zurich may seek to de-authorise the company.

4.2.4 No changes will be made to the terms and conditions of any policies as a result of the ESI Scheme.

4.2.5 The reinsurance arrangement currently in place with ZAL will terminate when all residual policies, if any, have transferred; there are no other reinsurance arrangements currently in force.

4.2.6 It is intended that the existing administration arrangements in respect of the ESI policies will continue unchanged as at the SED. The administration is carried out by Eagle Star (Malta) Limited, which is a wholly owned subsidiary of ZAL. Under the terms of the existing reinsurance agreement, Eagle Star (Malta) Limited was given the right to carry out the administration for ZAL and thus ESI. The rights and obligations of the third party administration agreements will in respect of the transferring policyholders be transferred

Actuarial Function Holder Report – ESI Scheme

14

with the business with effect from the SED. There are currently plans to rationalise the working hours of the Maltese office. However, this is a consequence of the decline in the number of in-force policies and is not as a result of the Scheme.

4.2.7 The legal and other costs incurred in preparing and implementing the ESI Scheme will be met by the shareholder funds of ESI.

Actuarial Function Holder Report – ESI Scheme

15

5 Financial position before and after transfer

5.1 Introduction

5.1.1 Under the current Solvency 1 regulations as applied in the UK, insurance companies are required to hold a minimum level of capital on two different bases.

5.1.2 Firstly, companies must hold assets in excess of the policyholder and other liabilities that are greater than the Capital Resource Requirement (CRR). This test is also known as Pillar 1 and an analysis of the capital position is published in the annual PRA returns.

5.1.3 In addition, insurance companies must also asses their capital on a risk-based economic basis under Individual Capital Assessment (the so-called ICA regime, or Pillar 2) and this assessment is shared privately with the PRA.

5.1.4 With effect from 1 January 2016, a new regulatory regime will be coming into effect called Solvency 2. This has many similarities with the ICA regime, but also has a number of important differences, including the requirement to hold a risk margin in excess of the best estimate liabilities and the determination of the relevant risk free interest rate, among others.

5.2 Solvency I Pillar 1

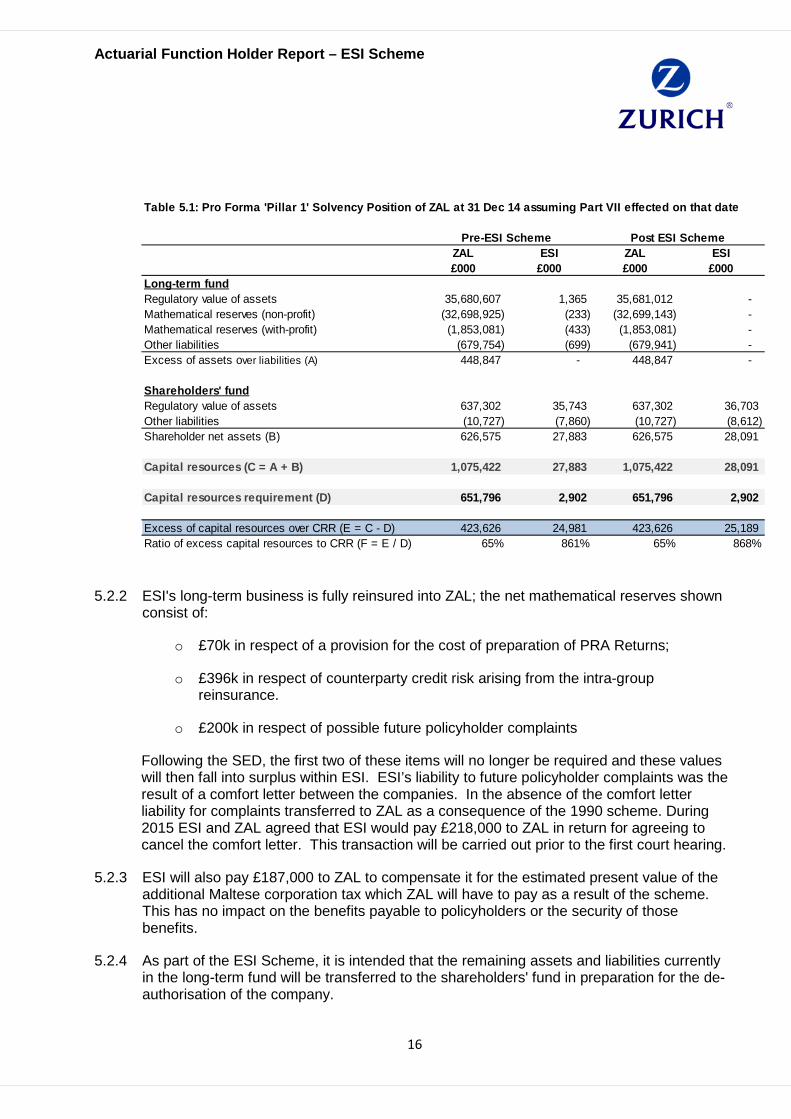

5.2.1 The pro forma Pillar 1 capital position as at 31 December 2014 assuming that the ESI Scheme had taken effect at that date is shown in the table below:

Actuarial Function Holder Report – ESI Scheme

16

5.2.2 ESI's long-term business is fully reinsured into ZAL; the net mathematical reserves shown consist of:

o £70k in respect of a provision for the cost of preparation of PRA Returns;

o £396k in respect of counterparty credit risk arising from the intra-group reinsurance.

o £200k in respect of possible future policyholder complaints

Following the SED, the first two of these items will no longer be required and these values will then fall into surplus within ESI. ESI’s liability to future policyholder complaints was the result of a comfort letter between the companies. In the absence of the comfort letter liability for complaints transferred to ZAL as a consequence of the 1990 scheme. During 2015 ESI and ZAL agreed that ESI would pay £218,000 to ZAL in return for agreeing to cancel the comfort letter. This transaction will be carried out prior to the first court hearing.

5.2.3 ESI will also pay £187,000 to ZAL to compensate it for the estimated present value of the additional Maltese corporation tax which ZAL will have to pay as a result of the scheme. This has no impact on the benefits payable to policyholders or the security of those benefits.

5.2.4 As part of the ESI Scheme, it is intended that the remaining assets and liabilities currently in the long-term fund will be transferred to the shareholders' fund in preparation for the de-authorisation of the company.

Table 5.1: Pro Forma 'Pillar 1' Solvency Position of ZAL at 31 Dec 14 assuming Part VII effected on that date

ZAL ESI ZAL ESI£000 £000 £000 £000

Long-term fundRegulatory value of assets 35,680,607 1,365 35,681,012 - Mathematical reserves (non-profit) (32,698,925) (233) (32,699,143) - Mathematical reserves (with-profit) (1,853,081) (433) (1,853,081) - Other liabilities (679,754) (699) (679,941) - Excess of assets over liabilities (A) 448,847 - 448,847 -

Shareholders' fundRegulatory value of assets 637,302 35,743 637,302 36,703Other liabilities (10,727) (7,860) (10,727) (8,612)Shareholder net assets (B) 626,575 27,883 626,575 28,091

Capital resources (C = A + B) 1,075,422 27,883 1,075,422 28,091

Capital resources requirement (D) 651,796 2,902 651,796 2,902

Excess of capital resources over CRR (E = C - D) 423,626 24,981 423,626 25,189Ratio of excess capital resources to CRR (F = E / D) 65% 861% 65% 868%

Pre-ESI Scheme Post ESI Scheme

Actuarial Function Holder Report – ESI Scheme

17

5.2.5 As part of this transfer, tax of 20.25% will be due on the mathematical reserves released, and this has been reflected as an increase in ‘other liabilities’ in the shareholder fund.

5.3 Solvency I Pillar 2

5.3.1 The Pillar 2 solvency position as at 31 December 2014 has been estimated for both ZAL and ESI.

5.3.2 For both companies, the excess of capital resources over capital requirements increases when considered on a Pillar 2 basis. Since the Pillar 2 basis is less onerous than Pillar 1, it is appropriate to focus my considerations on the Pillar 1 position set out above. This position is expected to continue following the implementation of the Scheme.

5.4 Solvency II

5.4.1 Solvency II is the new EU regulatory framework for insurers that will replace the current capital adequacy regulations in January 2016. As the impact of the Solvency II regime has not yet been fully finalised, the impact of the transfer on capital requirements cannot be completely certain.

5.4.2 ZAL intends to adopt the standard formula approach to Solvency II. From the calculations performed as at 31 December 2014, the excess assets over the sum of the technical provisions and capital requirements under Solvency II and ICA are similar after removing pension scheme risk from the ICA to make it consistent with its treatment under Solvency II, despite there being significant differences in their compositions. On this basis I conclude that the position under Solvency II will be less onerous than under Solvency I Pillar 1.

5.4.3 Solvency II calculations have been performed on the ESI business as a standalone entity standard formula basis as at 31 December 2014. These show that the Solvency I and II capital requirements are the same due to the fact that in both cases the minimum capital requirement is applied. Given that ESI’s liabilities are already reinsured into ZAL, the total post-Scheme liabilities of ZAL will not change and the Scheme will not distort the relative strengths of ZAL’s Solvency I and Solvency II positions.

5.4.4 Based on the information available, I do not expect Solvency II to have an adverse impact on either ZAL’s or ESI’s solvency positions pre- or post-Scheme compared with their Solvency I positions and I conclude that it is reasonable to consider further the transfer solely on a Solvency I basis.

Actuarial Function Holder Report – ESI Scheme

18

6 The effect of the Scheme on policyholders

6.1 Risk profile of the combined businesses

6.1.1 ZAL policyholders are already exposed to the risks of ESI’s policyholders to a significant extent through the 100% reinsurance of all of ESI’s polices into ZAL. While, following the Scheme, ZAL policyholders will be more directly affected by the risks attaching to the policies transferring in from ESI, the difference is not considered to be material.

6.1.2 The risk of mis-selling complaints that previously resided in ESI was transferred to ZAL earlier in 2015 as a consequence of the cancellation of a letter of comfort between the two companies.

6.1.3 As a result of the transfer into ZAL, there will, however, be a change for ESI policyholders. The ESI policyholders will become exposed to the risks within ZAL’s business to which they are not currently exposed, other than as a consequence of the reassurance. On the other hand the current position is anomalous as the recent transfer of general insurance business has removed risks to which they were previously exposed.

6.1.4 I conclude, therefore, that there will be no material detriment as a result of the change in risk exposures as a result of transferring the policies into ZAL under the ESI Scheme.

6.2 Security of policyholder benefits

6.2.1 Both the non-profit and with-profits business of ESI is already fully reinsured into the ZAL funds and so the Scheme will not materially impact the security of ZAL policies which will continue to be protected by the significant excess of assets over liabilities in the long-term funds and the shareholders’ fund.

6.2.2 The financial information presented above shows that the ratio of the excess capital resources to the capital resources requirement will drop significantly for ESI policyholders following the implementation of the Scheme. However, the current security is supported by significant assets currently in the shareholder’s fund but which are expected to be repatriated to the parent company following the transfer out of ESI of the general insurance business in 2013.

6.2.3 I conclude therefore that there will be no materially adverse change to the security of ESI policies following the implementation of the proposed Scheme.

6.3 Benefit expectations – with-profits policyholders

6.3.1 No changes will occur as a result of the Scheme to investment strategy, expense allocation, policy charges or the methodology for setting or allocating bonuses for existing policyholders within the ZAL 90:10 with-profits fund. There will, therefore, be no changes to the benefit expectations of existing ZAL with-profits policies.

6.3.2 ESI’s with-profits policies, which comprise the bulk of the transferring policies, are already fully reinsured into the ZAL 90:10 with-profits fund and have been so since 1 January 1991. Moreover, bonus rates in Malta have been the same as those for equivalent UK policies

Actuarial Function Holder Report – ESI Scheme

19

since 9 March 1998 (as have ZAL Malta policies). There will, therefore, be no changes to the benefit expectations of existing ESI with-profits policies.

6.4 Benefit expectations – non-profit policyholders

6.4.1 The benefit expectations of ZAL non-profit policies will not impacted by the Scheme.

6.4.2 The majority of ESI non-profit policies have no features that grant management discretion in their interpretation or application. For others such as PHI, there is an element of discretion, but the terms for these policies and the process for exercising discretion is not changed by the Scheme.

6.5 Governance of the with-profits fund

6.5.1 Since the ESI with-profits policies are already fully reinsured into the ZAL 90:10 with-profits fund, there will be no changes required to the governance of the with-profits business which will continue as before.

6.6 Service standards

6.6.1 The services which are provided by the service company to ZAL will remain unchanged as a result of the Scheme.

6.6.2 Services to ESI are already provided by the same service company as for ZAL and the Scheme will not impact these arrangements.

6.7 Taxation

6.7.1 It is not expected that there will be any impact on the tax position of policyholders as a result of the Scheme. Confirmation of this is expected to be received from the Maltese tax authorities within the next few weeks.

6.7.2 In respect of corporation tax, the Maltese branch pays tax on an income less expenses (I – E) basis using an apportionment ratio based on global premium income. For ZAL the proposed transfer would result in a higher Maltese tax liability. The Scheme provides for ESI to make a payment of £187,000 to ZAL in respect of the present value of the increase in future tax liabilities as a result of the Scheme.

6.8 Policyholder communications

6.8.1 A detailed communication plan has been produced the implementation of which will ensure policyholders are adequately informed of the nature and effect of the Scheme. The communications package includes direct mailing, press adverts and web content.

6.8.2 The regulations surrounding Part VII transfers require that, unless the Court otherwise orders, all policyholders in all affected companies should be written to in order to inform them of the proposed Scheme.

6.8.3 An application is to be made to the Court for a waiver to omit mailing the non-Maltese policyholders of ZAL on the grounds that the Scheme will not materially impact them – both

Actuarial Function Holder Report – ESI Scheme

20

the with-profits and non-profit business of ESI is already fully reinsured into ZAL’s long-term funds and the small amount of additional business is not of sufficient materiality to need to inform existing ZAL policyholders individually.

6.8.4 This has been discussed with the MFSA which has confirmed that it would have no objection to only the Maltese policyholders of both companies being written to in respect of the Scheme.

6.8.5 I am satisfied that the proposed communication plan described above is appropriate and consistent with the principles pertaining to the fair treatment of policyholders.

6.9 Report of the With-Profits Actuary

6.9.1 In forming my opinion on the effect of the Scheme on existing ESI and ZAL with-profits policyholders, I have taken into account, but not relied upon, the opinion of the WPA set out in a separate Report to the Boards of ZAL and ESI on the impact of the Scheme on the fair treatment of with-profits policyholders, the bonus expectations of with-profits policyholders and the effectiveness of the communications strategy, inter alia.

Actuarial Function Holder Report – ESI Scheme

21

7 Conclusion

7.1.1 It is my opinion that:

(i) The Scheme does not result in material changes to the benefit expectations of either the with-profits or non-profit policyholders. Policy terms, conditions and charges are unchanged. The circumstances under which policyholder benefits would be adversely affected are not materially changed as a result of the Scheme.

(ii) The security of benefits for both the non-profit and with-profits policyholders in both ZAL and ESI is not materially affected as a result of the Scheme.

(iii) Since the ESI with-profits business is already fully reinsured into the ZAL 90:10 with-profits fund, the Scheme does not result in any transfers into or out of any ZAL with-profits fund.

(iv) There are no changes to the principles or practices of financial management by which the ZAL 90:10 with-profits fund is managed, including the bonus setting methodology.

(v) The administration and management of policies and treatment of both the ZAL and ESI policyholders are unchanged as a result of the Scheme.

7.1.2 It is my opinion, therefore, that no class of ZAL or ESI policyholder will be adversely affected by the implementation of the proposed ESI Scheme. In particular, I believe that the ESI Scheme will maintain the security of benefits of all ZAL and ESI policyholders, have no materially adverse impact on their benefit expectations, and will not adversely impact on the ability for them to be treated fairly.

David Ford, FIA Actuarial Function Holder 20 May 2015

Actuarial Function Holder Report – ESI Scheme

22

Appendix A: Terms and definitions

Terms used in this report

Actuarial Function Holder, or AFH

The actuary appointed from time to time to perform the duties set out in Rule SUP 4.3.13 of the Combined PRA/FCA Handbook

FCA Financial Conduct Authority, the regulator of the financial services industry in the UK responsible for conduct of financial services firms including the fairness of financial services contracts

FSMA The Financial Services and Markets Act 2000

Independent Expert

The individual appointed to report on the terms of an insurance business transfer scheme and approved by the PRA and FCA pursuant to Section 109 of FSMA

Individual Capital Assessment (or ICA), or Pillar 2

An insurance company’s own assessment of the capital that it needs for regulatory purposes. This amount is reviewed and adjusted if necessary by the PRA

MFSA Malta Financial Services Authority, the regulator for financial services activities in Malta

Solvency 1 Calculation, or Pillar 1

Calculation of its solvency position that an insurance company regulated in the UK must carry out at regular intervals based on a calculation of its liabilities and its capital requirements on a regulatory basis, including the calculation of a With-Profits Insurance Capital Component for companies with large with-profits funds

PRA Prudential Regulation Authority, the regulator of the financial services industry in the UK responsible for the safety and soundness of firms and securing an appropriate degree of protection for policyholders

Scheme, or ESI Scheme

The insurance business transfer scheme that is the subject of this report

Scheme Effective Date, or SED

The date on which the ESI Scheme is implemented

Scheme Report The Independent Expert's report on the terms of the insurance business transfer scheme

Solvency II Revised capital adequacy regime for the European insurance industry covering both capital requirements and risk management standards. It will replace Solvency I from 1 January 2016

With-Profits Actuary, or WPA

An actuary appointed to perform the with-profits actuary function, a PRA controlled function

Actuarial Function Holder Report – ESI Scheme

23

Company abbreviations referred to in this report

ESI Eagle Star Insurance Company Limited

ESLAC Eagle Star Life Assurance Company Limited

ZAL Zurich Assurance Ltd

ZIC Zurich Insurance Company Ltd

ZIG Zurich Insurance Group Ltd