acquiring labor - csef · –employees are increasingly valuable part of firm ... joint...

TRANSCRIPT

Acquiring Labor

Paige Ouimet – University of North Carolina

Rebecca Zarutskie – Federal Reserve Board

• Any opinions and conclusions expressed herein are those of the author(s) and do not necessarily represent the views of the U.S. Census Bureau. All results have been reviewed to ensure that no confidential information is disclosed.

• These results and conclusions in the paper do not necessarily reflect the views of the Federal Reserve Board or other members of the Federal Reserve System.

Key Question

• Are some M&As motivated as a means to acquire labor?

• No:

– Employees can leave post-acquisition

– Why not just make job offers to desirable employees?

• Yes:

– Employees are increasingly valuable part of firm

– The value of a given employee may be lower if leaves existing firm (e.g. more productive in a specific team)

Research Design

• Examine employment, turnover and wage changes at target firms around an M&A

– Show summary statistics

– Show large cross-sectional variation

• Explain the cross-sectional variation

– Does the acquiring labor hypothesis explain the cross-sectional variation?

M&A Data

• M&A sample is from SDC

• Private targets, public or private acquirers

• Announced between 1985 and 2001

• Deal is completed and for majority control

• Require non-missing data for key variables

• 2,003 unique M&As

Table 1: M&A Summary Stats Variable Mean N

Target characteristics

Target assets 2,171.4 2003

Target market capitalization 1,074.3 2003

Target PP&E 326.1 2003

Target OBID/assets (percent) 2.5 2003

Target firm-level employment 4,218.2 2003

Target average number of employees per establishment 125.7 2003

Target average establishment age (years) 9.0 2003

Acquirer characteristics

Acquirer assets 16,532.9 715

Acquirer mkt cap 17,355.6 715

Private acquirer (percent) 21.2 2003

Deal characteristics

Diversifying acquisition (percent) 58.0 2003

Acquirer announcement CAR (percent) -1.3 715

Target announcement CAR (percent) 23.6% 715

Joint announcement CAR (percent) 1.8% 715

Census Data

• The Longitudinal Business Database (LBD) – Establishment-level data, covers all establishments

in US with at least 1 employee

– Provides information on industry, geography, total employment and total payroll

– LBDNUM allows establishment to be tracked over time, even in the event of a change in ownership

– FIRMID provides information on ultimate owner. But, not always quickly updated around M&A events

Firm A Establishment 1

Firm A Establishment 2

Firm A Establishment 3

Pre-merger Firm B buys Firm A (date from SDC)

Post-Merger

Firm A Establishment 1

Firm A Establishment 2

Firm A Establishment 3

Firm B Establishment 1

Firm B Establishment 2

Firm B Establishment 3

Establishments are cleanly tracked over time • Can observe and track target establishments, even after they are acquired Ultimate owner is updated following an M&A, but often with a significant time lag • Use SDC to identify timing of M&A events • But there is still one problem…

Firm A Establishment 1

Firm A Establishment 2

Firm A Establishment 3

Pre-merger Firm B buys Firm A (date from SDC)

Post-Merger

Firm A Establishment 1

Firm A Establishment 2

Firm A Establishment 3

Firm B Establishment 1

Firm B Establishment 2

Firm B Establishment 4

Firm B Establishment 4

Suppose firm gets a better lease across the street. Closes all operations at establishment 4 and moves all equipment and employees to new establishment 4.

Establishment Tracking

• Can observe all establishments owned by target prior to M&A deal and track these establishment following a change in control.

• Cannot observe new target establishments created after the change in control – This leads to negative employment change bias. – New target establishments are in the data – but are

identified as acquirer establishments. – Could measure if looked at total target and acquirer

employment. However, this is noisy as acquirer is typically 5-10x larger.

Employment Change Measurement

• Employment changei= 𝑒𝑚𝑝𝑙𝑜𝑦𝑚𝑒𝑛𝑡(𝑡=3)−𝑒𝑚𝑝𝑙𝑜𝑦𝑚𝑒𝑛𝑡(𝑡=−1)

1

2∗[𝑒𝑚𝑝𝑙𝑜𝑦𝑚𝑒𝑛𝑡(𝑡=3)+𝑒𝑚𝑝𝑙𝑜𝑦𝑚𝑒𝑛𝑡(𝑡=−1)]

• Post period = 3 years after M&A • Pre period = 1 year prior to MA& • Excess employment change = employment

changei – employment change at matched establishment – Matched by industry, year and employment size

• Excess employment change address bias mentioned on previous slide and controls for industry-year patterns

Table 2. Employment Changes around M&A Events

Deal-

weighted

average

Median-

weighted

average

Employee-

weighted

average

N

Raw employment

change -0.810 -0.677 -0.430 2003

Excess employment

change -0.120 -0.052 0.128 2003

Excess wage changes

for all observed

employees

0.012 0.002 0.032 1523

Excess wage change

limited to surviving

establishments 0.024 0.016 0.045 1523

Table 4. Employment and Wage Changes at Target Firms of Completed

and Cancelled Deals. Completed

Deals

Cancelled

Deals

Difference T-test of

differences

Raw employment change -0.810 -0.561 -0.249 -3.22 ***

Excess employment

change -0.120 0.073 -0.193 -2.29 **

Excess wage changes for

all observed employees 0.012 -0.028 0.040 0.86

Excess wage change

limited to surviving

establishments 0.024 -0.064 0.088 2.21 **

Testing Acquiring Labor Hypothesis

• We observe large variation in ex-post employment changes.

• Acquiring labor hypothesis predicts that target firms with most “desirable” labor will be associated with most positive ex-post outcomes.

• What makes a firm’s employees more “desirable”?

• We start with target firms with the most employees, ie the most labor to acquire.

• This is an indirect proxy. Will later show 2 types of robustness tests.

Table 5. Target Ex Ante Employment and

Post-merger Excess Employment Changes. 1 2 3

Target ex ante employment 0.091***

(0.013)

0.117***

(0.021)

0.092***

(0.018)

Diversifying acquisition 0.187***

(0.046)

0.180***

(0.046)

0.187***

(0.046)

Target assets -0.033

(0.049)

Target assets squared -0.001

(0.004)

Target market capitalization 0.015

(0.027)

Target market capitalization squared -0.002

(0.002)

Year and industry FE yes yes yes

N 2003 2003 2003

R-squared 0.097 0.100 0.097

Regressions also include controls for target profitability, target industry unionization and whether or not the acquirer is private.

Table 5. Target Ex Ante Employment and

Post-merger Excess Employment Changes. 1 2 3

Target ex ante employment 0.091***

(0.013)

0.117***

(0.021)

0.092***

(0.018)

Diversifying acquisition 0.187***

(0.046)

0.180***

(0.046)

0.187***

(0.046)

Target assets -0.033

(0.049)

Target assets squared -0.001

(0.004)

Target market capitalization 0.015

(0.027)

Target market capitalization squared -0.002

(0.002)

Year and industry FE yes yes yes

N 2003 2003 2003

R-squared 0.097 0.100 0.097

Regressions also include controls for target profitability, target industry unionization and whether or not the acquirer is private.

Table 5. Target Ex Ante Employment and

Post-merger Excess Employment Changes. 1 2 3

Target ex ante employment 0.091***

(0.013)

0.117***

(0.021)

0.092***

(0.018)

Diversifying acquisition 0.187***

(0.046)

0.180***

(0.046)

0.187***

(0.046)

Target assets -0.033

(0.049)

Target assets squared -0.001

(0.004)

Target market capitalization 0.015

(0.027)

Target market capitalization squared -0.002

(0.002)

Year and industry FE yes yes yes

N 2003 2003 2003

R-squared 0.097 0.100 0.097

Regressions also include controls for target profitability, target industry unionization and whether or not the acquirer is private.

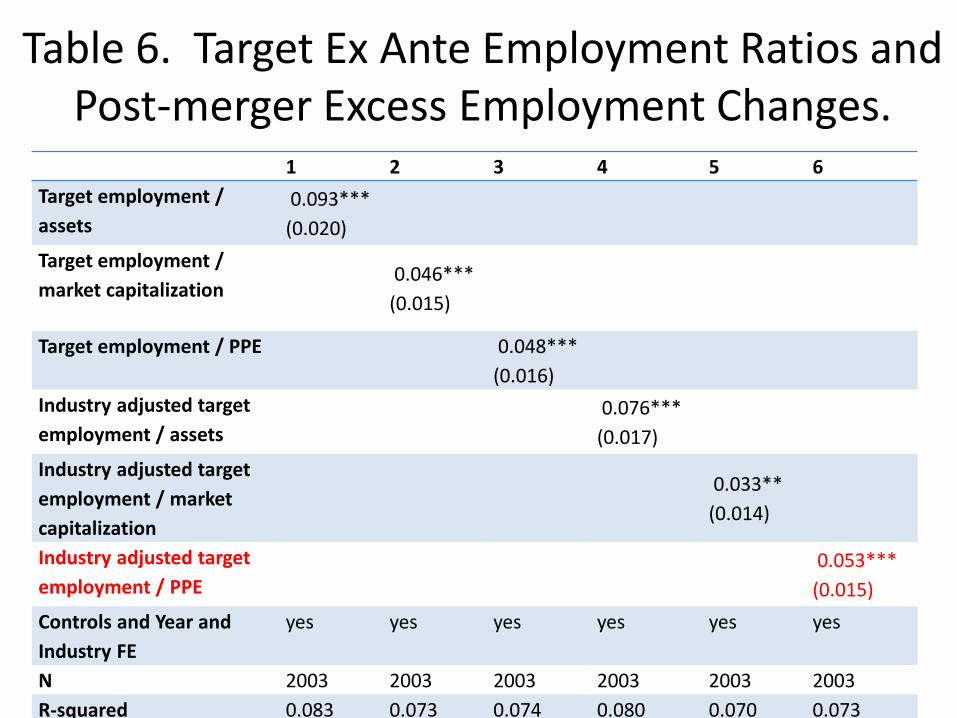

Table 6. Target Ex Ante Employment Ratios and Post-merger Excess Employment Changes.

1 2 3 4 5 6

Target employment /

assets

0.093***

(0.020)

Target employment /

market capitalization 0.046***

(0.015)

Target employment / PPE

0.048***

(0.016)

Industry adjusted target

employment / assets

0.076***

(0.017)

Industry adjusted target

employment / market

capitalization

0.033**

(0.014)

Industry adjusted target

employment / PPE

0.053***

(0.015)

Controls and Year and

Industry FE

yes yes yes yes yes yes

N 2003 2003 2003 2003 2003 2003

R-squared 0.083 0.073 0.074 0.080 0.070 0.073

Table 6. Target Ex Ante Employment Ratios and Post-merger Excess Employment Changes.

1 2 3 4 5 6

Target employment /

assets

0.093***

(0.020)

Target employment /

market capitalization 0.046***

(0.015)

Target employment / PPE

0.048***

(0.016)

Industry adjusted target

employment / assets

0.076***

(0.017)

Industry adjusted target

employment / market

capitalization

0.033**

(0.014)

Industry adjusted target

employment / PPE

0.053***

(0.015)

Controls and Year and

Industry FE

yes yes yes yes yes yes

N 2003 2003 2003 2003 2003 2003

R-squared 0.083 0.073 0.074 0.080 0.070 0.073

Table 6. Target Ex Ante Employment Ratios and Post-merger Excess Employment Changes.

1 2 3 4 5 6

Target employment /

assets

0.093***

(0.020)

Target employment /

market capitalization 0.046***

(0.015)

Target employment / PPE

0.048***

(0.016)

Industry adjusted target

employment / assets

0.076***

(0.017)

Industry adjusted target

employment / market

capitalization

0.033**

(0.014)

Industry adjusted target

employment / PPE

0.053***

(0.015)

Controls and Year and

Industry FE

yes yes yes yes yes yes

N 2003 2003 2003 2003 2003 2003

R-squared 0.083 0.073 0.074 0.080 0.070 0.073

Table 6. Target Ex Ante Employment Ratios and Post-merger Excess Employment Changes.

1 2 3 4 5 6

Target employment /

assets

0.093***

(0.020)

Target employment /

market capitalization 0.046***

(0.015)

Target employment / PPE

0.048***

(0.016)

Industry adjusted target

employment / assets

0.076***

(0.017)

Industry adjusted target

employment / market

capitalization

0.033**

(0.014)

Industry adjusted target

employment / PPE

0.053***

(0.015)

Controls and Year and

Industry FE

yes yes yes yes yes yes

N 2003 2003 2003 2003 2003 2003

R-squared 0.083 0.073 0.074 0.080 0.070 0.073

Table 6. Target Ex Ante Employment Ratios and Post-merger Excess Employment Changes.

1 2 3 4 5 6

Target employment /

assets

0.093***

(0.020)

Target employment /

market capitalization 0.046***

(0.015)

Target employment / PPE

0.048***

(0.016)

Industry adjusted target

employment / assets

0.076***

(0.017)

Industry adjusted target

employment / market

capitalization

0.033**

(0.014)

Industry adjusted target

employment / PPE

0.053***

(0.015)

Controls and Year and

Industry FE

yes yes yes yes yes yes

N 2003 2003 2003 2003 2003 2003

R-squared 0.083 0.073 0.074 0.080 0.070 0.073

Table 6. Target Ex Ante Employment Ratios and Post-merger Excess Employment Changes.

1 2 3 4 5 6

Target employment /

assets

0.093***

(0.020)

Target employment /

market capitalization 0.046***

(0.015)

Target employment / PPE

0.048***

(0.016)

Industry adjusted target

employment / assets

0.076***

(0.017)

Industry adjusted target

employment / market

capitalization

0.033**

(0.014)

Industry adjusted target

employment / PPE

0.053***

(0.015)

Controls and Year and

Industry FE

yes yes yes yes yes yes

N 2003 2003 2003 2003 2003 2003

R-squared 0.083 0.073 0.074 0.080 0.070 0.073

Summary of Tables 5 & 6

• Target firms with higher ex-ante employment are associated with more positive ex-ante employment outcomes.

• Acquiring labor hypothesis predicts this correlation will be stronger when 1) employees are more skilled or 2) labor markets are tighter

Table 7. Target Ex Ante Employment and Post-merger Excess Employment Changes by Target

Industry Human Capital. 1 2 3 4

Target ex ante employment 0.035

(0.034)

-0.160

(0.109)

-0.147

(0.100)

0.087***

(0.013)

Industry college share -1.797*

(1.041)

Industry college share * Target ex ante employment 0.250*

(0.140)

Industry mean wages -0.524**

(0.260)

Industry mean wages * Target ex ante employment 0.072**

(0.031)

Industry median wages -0.483**

(0.230)

Industry median wages * Target ex ante employment 0.067**

(0.028)

Industry R&D / Sales -0.047

(0.036)

Industry R&D / Sales * Target ex ante employment 0.007

(0.005)

R-squared 0.095 0.095 0.095 0.093

Table 7. Target Ex Ante Employment and Post-merger Excess Employment Changes by Industry Employment.

1 2 3

Target ex ante employment 0.073***

(0.015)

0.069***

(0.019)

0.101***

(0.014)

Industry employment growth (2 yr) -3.181**

(1.388)

Industry employment growth (2 yr)* Target

ex ante employment

0.508***

(0.186)

Industry employment growth (2 yr) IF

NEGATIVE

-2.936

(1.986)

Industry employment growth (2 yr) IF

NEGATIVE * Target ex ante employment

0.505**

(0.256)

Industry employment growth (2 yr) IF

POSITIVE

-7.686***

(3.074)

Industry employment growth (2 yr) IF

POSITIVE * Target ex ante employment

1.217***

(0.443)

Year FE yes yes yes

N 2003 2003 2003

R-squared 0.100 0.099 0.100

Table 9 Target Ex Ante Employment and Post-merger Turnover Changes.

1 2 3 4

Target ex ante

employment

-1.268***

(0.323)

Target employment /

assets

-1.711***

(0.455)

Target employment /

market capitalization

-1.179***

(0.328)

Target employment / PPE

-1.634***

(0.388)

Industry and year FE and

controls

Yes yes yes yes

N 309 309 309 309

R-squared 0.097 0.100 0.093 0.111

Table 10. Target Ex Ante Employment and Post-merger Wages Changes.

1 2 3 4

Target ex ante employment 0.032**

(0.017)

Target employment / assets

0.062***

(0.024)

Target employment / market capitalization

0.062***

(0.022)

Target employment / PPE

0.040*

(0.021)

Industry and year FE and controls yes yes yes yes

Year FE yes yes yes yes

N 774 774 774 774

R-squared 0.135 0.141 0.154 0.133

Alternative Proxies for Acquiring Labor M&A deals

• We assume language in a firm’s 10-K will reflect important firm attributes.

• For example: – “the need to retain employees is a significant business

risk” – “this new compensation plan is designed to retain

employees”

• We then create a proxy which is a simple count of the number of times “retain employees” is mentioned in a firm’s 10-K.

• Repeat for “hiring”, “skill”, “training” and “team”

Table 11. Target Ex Ante Employment Ratios and Acquirer Word Searches.

1 2 3 4 5 6

“retain employee” 0.35***

(0.07)

“retain employee” binary

0.37***

(0.08)

“skill*”

0.48***

(0.05)

“skill*” binary

0.61***

(0.07)

“team”

0.18***

(0.05)

“team” binary 0.27***

(0.08)

Year FE and controls Yes yes Yes Yes Yes Yes

N 1380 1380 1380 1380 1380 1380

R-squared 0.175 0.174 0.213 0.204 0.168 0.168

Table 12. Target Ex Ante Employment Ratios and Target Word Searches.

1 2 3 4 5 6

“retain employee” 0.40***

(0.07)

“retain employee” binary

0.43***

(0.08)

“skill*”

0.52***

(0.05)

“skill*” binary

0.67***

(0.07)

“team”

0.31***

(0.06)

“team” binary

0.43***

(0.08)

Year FE and controls Yes Yes Yes Yes Yes Yes

N 1189 1189 1189 1189 1189 1189

R-squared 0.182 0.181 0.227 0.215 0.181 0.179

Table A2. Correlations among Word Search Variables.

Retain employee Hiring Skill Training Team

Retain

employee 1.00 0.51 0.30 0.41 0.06

Hiring 0.51 1.00 0.26 0.36 0.07

Skill 0.30 0.26 1.00 0.36 0.12

Training 0.41 0.36 0.36 1.00 0.18

Team 0.06 0.07 0.12 0.18 1.00

Table A3. Correlations between Word Search Variables and Accounting Ratios.

Assets R&D/Sales

SG&A

/Sales

Profit

Margin MB

Mkt

cap

Retain

employee 0.047 0.005 0.007 -0.007 -0.001 0.015

Hiring 0.013 0.004 0.008 -0.007 -0.002 -0.011

Skill -0.011 0.000 -0.003 0.000 -0.001 -0.014

Training -0.012 -0.009 -0.005 0.007 -0.001 -0.009

Team 0.018 0.002 0.003 -0.004 0.000 0.025

Word Searches Summary

• Plan to test correlation between acquiring labor key word searches and ex post employment change once get data access again

• In the meantime, find strong correlation between acquiring labor key word searches and ex-ante target employment

• Find no strong correlation between key word searches and standard accounting variables

Conclusion

• Some firms appear to be pursing M&A activity with the specific objective of obtaining the target’s employees

• We find a positive relation between ex ante target employment and post-merger target employment change – Similar results with turnover and wages

– Pattern is stronger when workers are more skilled or labor markets are tighter.

• Consistent with acquirers selecting targets with large employment specifically for their employee base – External verification of proxy using 10-K language searches