accounting for payroll

TRANSCRIPT

1 10/13/2011 ACTBAS1 Lectures, Prof. L. Landicho, DLSU, 2nd Term AY 2011-2012

Payroll and related fringe benefits often make up a large percentage of current liabilities Employee compensation is often the most significant expense that a firm incurs Government regulations relating to the payment and reporting of payroll taxes apply only to employees

2 10/13/2011 ACTBAS1 Lectures, Prof. L. Landicho, DLSU, 2nd Term AY 2011-2012

Payroll pertains to both salaries and wages Managerial, administrative, and sales personnel are generally paid salaries. Salaries are often expressed in terms of a specified amount per month or year Sale assistants, factory employees and manual labourers are normally paid wages based on a rate per hour Payments made to professional individuals who are independent contractors are called professional fees

3 10/13/2011 ACTBAS1 Lectures, Prof. L. Landicho, DLSU, 2nd Term AY 2011-2012

Objectives of internal accounting control concerning payroll: To safeguard company assets from unauthorised payments of payrolls To ensure the accuracy and reliability of the accounting records pertaining to payrolls

Payroll activities involve four functions: hiring employees timekeeping preparing the payroll paying the payroll

4 10/13/2011 ACTBAS1 Lectures, Prof. L. Landicho, DLSU, 2nd Term AY 2011-2012

Hiring Employees The human resources (personnel) department is responsible for posting job openings, screening and interviewing applicants, and hiring employees The human resources department is also responsible for authorizing changes in employment status:

Changes in pay rates Termination of employment

5 10/13/2011 ACTBAS1 Lectures, Prof. L. Landicho, DLSU, 2nd Term AY 2011-2012

Timekeeping Hourly employees are usually required to

In large companies procedures are often monitored to ensure an employee punches only 1 card

Approves the hours shown by signing the time card at the end of the pay period Authorises overtime hours for an employee

6 10/13/2011 ACTBAS1 Lectures, Prof. L. Landicho, DLSU, 2nd Term AY 2011-2012

Preparing the payroll The payroll is prepared in the payroll department on the basis of two inputs:

Human resources department authorisations Approved time cards

7 10/13/2011 ACTBAS1 Lectures, Prof. L. Landicho, DLSU, 2nd Term AY 2011-2012

Paying the payroll Payroll is paid by the finance department Many employees have their pay credited electronically into their bank accounts Employers use a payroll software package which processes the pay and provides control Some firms prefer to pay by cheque which also minimises risk of loss from theft

8 10/13/2011 ACTBAS1 Lectures, Prof. L. Landicho, DLSU, 2nd Term AY 2011-2012

Determining the payroll involves calculating 3 amounts

Gross earnings Payroll deductions Net pay

Gross Earnings This is the total compensation earned by an employee It consists of wages or salaries, plus any bonuses and commissions

9 10/13/2011 ACTBAS1 Lectures, Prof. L. Landicho, DLSU, 2nd Term AY 2011-2012

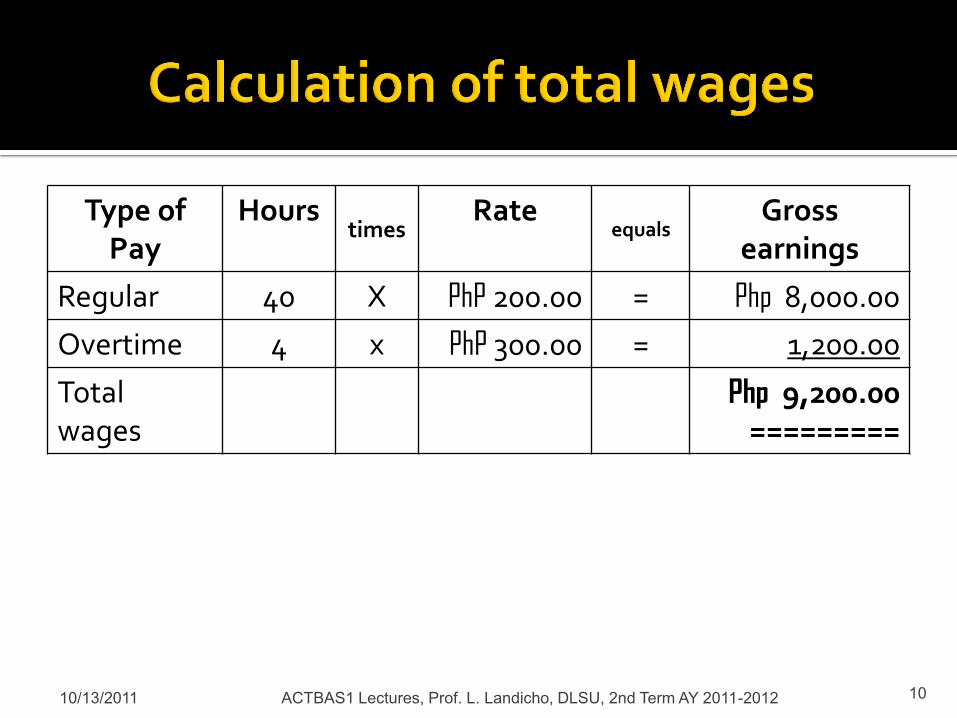

Type of Pay

Hours times Rate

equals Gross

earnings

Regular 40 X PhP 200.00 = Php 8,000.00

Overtime 4 x PhP 300.00 = 1,200.00

Total wages

Php 9,200.00 =========

10 10/13/2011 ACTBAS1 Lectures, Prof. L. Landicho, DLSU, 2nd Term AY 2011-2012

Payroll Deductions The difference between gross pay and amount actually received is attributable to payroll deductions Mandatory deductions are required by law are income taxes & government fund contributions The employer is merely a collection agent and subsequently transfers the amounts deducted to the government and designated recipients

11 10/13/2011 ACTBAS1 Lectures, Prof. L. Landicho, DLSU, 2nd Term AY 2011-2012

Income Taxes Under Philippine laws on withholding of income tax, employers are required to withhold income tax from employees each pay period The amount to be withheld depends on

Any special allowances Length of pay period

12 10/13/2011 ACTBAS1 Lectures, Prof. L. Landicho, DLSU, 2nd Term AY 2011-2012

Other Deductions Employees may voluntarily authorise withholdings for charitable donations and other purposes [i.e. union dues]

Other Requirements The employer is to pay SSS, HDMF & PHIC contributions on behalf of employees This is partly an expense of the business, and

13 10/13/2011 ACTBAS1 Lectures, Prof. L. Landicho, DLSU, 2nd Term AY 2011-2012

Net Pay This is determined by subtracting payroll deductions from gross earnings

Example

14

Gross earnings 20,000.00 Payroll deductions Income taxes 4,333.33 SSS, HDMF & PHIC 850.00 Union fees 500.00 5,683.33 Net pay PhP 14,316.67

10/13/2011 ACTBAS1 Lectures, Prof. L. Landicho, DLSU, 2nd Term AY 2011-2012

Maintaining payroll department records An employee earnings record is a cumulative record of gross earnings, deductions and net pay during the year A separate earnings record is kept for each employee Firms may also prepare a payroll register to accumulate gross earnings, deductions and net pay by employee for each pay period

15 10/13/2011 ACTBAS1 Lectures, Prof. L. Landicho, DLSU, 2nd Term AY 2011-2012

Recognising payroll expenses and liabilities Example

16

May 21 Office Salaries Expense 82,300 Wages Expense 122,700 Income Taxes Payable 38,000 SSS, HDMF & PHIC Payable 12,500 Union Fees Payable 20,000 Salaries and Wages Payable 134,500

(To record payroll for the week ending 21 May)

10/13/2011 ACTBAS1 Lectures, Prof. L. Landicho, DLSU, 2nd Term AY 2011-2012

Recognising employer SSS, HDMF & PHIC contributions

Example

17

May 21 SSS, HDMF & PHIC Expense 20,000 SSS, HDMF & PHIC Payable 20,000

(To record SSS, HDMF & PHIC employer share for pay period ending 21 May)

10/13/2011 ACTBAS1 Lectures, Prof. L. Landicho, DLSU, 2nd Term AY 2011-2012

Recognising annual leave provisions Regular employees are entitled to mandatory 5 days incentive leave pay Therefore, for each pay period, the employer is required to record the amount of the liability owing to employees

18

May 21 Annual Leave Expense 7,200 Provision for Annual Leave 7,200

(To record the annual leave payable )

10/13/2011 ACTBAS1 Lectures, Prof. L. Landicho, DLSU, 2nd Term AY 2011-2012

Recording payment of the payroll Payment by cheque is made either from the

account, and is accompanied by a payslip document

Journal entry to record payroll payment:

19

May 21 Salaries and Wages Payable 134,500 Cash 134,500 (To record payment of payroll)

10/13/2011 ACTBAS1 Lectures, Prof. L. Landicho, DLSU, 2nd Term AY 2011-2012

20 10/13/2011 ACTBAS1 Lectures, Prof. L. Landicho, DLSU, 2nd Term AY 2011-2012

Preparation of payroll tax returns is the responsibility of the payroll department Payment of the taxes is made by the finance department Much of the information in the returns is obtained from employee earnings records Under taxation law, firms must keep payroll records for at least 5 years

21 10/13/2011 ACTBAS1 Lectures, Prof. L. Landicho, DLSU, 2nd Term AY 2011-2012

22

Identify two internal control procedures that apply to each payroll function. What are the primary sources of gross earnings?

What payroll deductions are (a) mandatory and (b) voluntary? What account titles are used in recording a payroll, assuming only mandatory payroll deductions are involved?

10/13/2011 ACTBAS1 Lectures, Prof. L. Landicho, DLSU, 2nd Term AY 2011-2012