accounting and auditing update presented by joanna g. brumsey, cpa

TRANSCRIPT

Accounting and Auditing Update

Presented by Joanna G. Brumsey, CPA

Objective

• To enable participants to apply selected newly issued and effective technical accounting and auditing pronouncements

• To educate participants regarding upcoming changes

Outline

• Section I: Hot topics for our profession

• Section II: Recent accounting and auditing standards

• Section III: Proposed updates

• Section IV: Miscellaneous

Hot Topics for our ProfessionSection I

Hot Topics for our Profession

• COSO Framework• Private Company Financial Reporting• Third party verification letters

New & Improved COSO Framework

• Retained

• Definition of internal control• Five components of internal control• Criteria to assess effectiveness• Apply with judgment

• Improvements

• Codify criteria based on 17 principles that have universal application

• More advice and implementation guidance regarding internal and nonfinancial reporting

• Updated for today’s business and risk environment

Significant Changes

• 17 Principles, and related attributes, are explicitly linked with the components

• Reflects increased relevance of technology• Enhanced governance concepts• Expanded reporting objectives (external, internal,

financial and non-financial)• Enhanced consideration of anti-fraud

expectations• Expanded business models and organizational

structures• Additional guidance for business conducted on a

multi-locational or global basis• Special considerations for smaller entities (seg. Of

duties, management override, etc.)

Effective Date

• Transition as soon as possible; original framework superseded as of December 15, 2014

• Guidance on Internal Control Over External Financial Reporting (ICEFR)• Developed to assist users in applying

the Framework to external financial reporting objectives

• Issued May 2013

PRIVATE COMPANY FINANCIAL REPORTING

Blue Ribbon Panel

• Established in December, 2009, by the AICPA, FAF and NASBA

• Mission is to address how U.S. accounting standards can best meet the needs of users of private company financial statements

FAF Establishes Private Company Council

• Established May 2012• Private Company Council (PCC) will identify,

propose, deliberate, and formally vote on specific exceptions or modifications to U.S. GAAP for private companies

• Approve decisions subject to FASB due process

Private Company Council

FASB issued 3 PCC exposure drafts:• Business Combination – would permit private

companies to recognize separately from goodwill only certain intangibles

• Intangibles – would allow amortization of goodwill; test for impairment only upon triggering event; test impairment at entity-wide level

• Derivatives and hedging – would allow simpler approach for interest rate swaps

FRF for SMEs

• Released by AICPA

• Financial Reporting Framework (FRF) for small and medium sized entities released June 2013

• The framework has not been approved or disapproved by any technical body; no authoritative status

• Optional implementation, thus no “effective date”

• AICPA website has toolkits and FAQs

FRF for SMEs

Highlights:

• Not based on GAAP; “Other Comprehensive Bases of Accounting (OCBOA)”

• Defined set of criteria to determine measurement, recognition, presentation and disclosure of material items

• No standard definition of an SME; characteristics generally defined for guidance

• No industry specific guidance

• Non-CPAs may prepare

FRF for SMEs

Who can use?:

• Smaller – to – medium sized companies

• Owner-managed

• For profit entities

• Internal or external users have direct access to the owner-manager

• GAAP financial statements not required

• No plans to become a public company

FRF for SMEs

Key provisions:

• Based on a foundation of reliable and comprehensive accounting principles

• Historical cost is primary measurement

• Uses familiar and traditional accounting methods

• Reduced disclosures from GAAP

• Financial reporting is less complicated and leaner

• Fewer adjustments to reconcile income tax return income with book income

• Retains a traditional approach to lease accounting

FRF for SMEs

Key provisions, continued:

• Guidance on matters typically encountered by SMEs

• Asset and liability matters

• Accounting changes

• Business combinations

• Nonmonetary transactions

• Leases

• Subsequent events

• Contingencies

• Related party transactions

FRF for SMEs

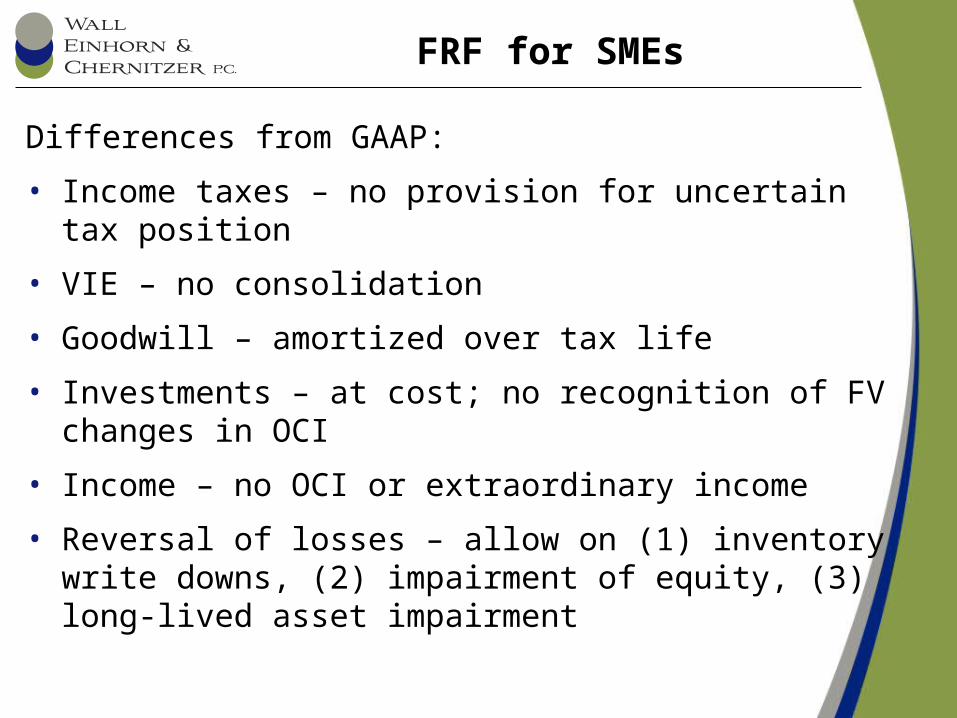

Differences from GAAP:

• Income taxes – no provision for uncertain tax position

• VIE – no consolidation

• Goodwill – amortized over tax life

• Investments – at cost; no recognition of FV changes in OCI

• Income – no OCI or extraordinary income

• Reversal of losses – allow on (1) inventory write downs, (2) impairment of equity, (3) long-lived asset impairment

PCC vs. FRF for SMEs

• PCC focuses on modifications to US GAAP for private companies in need of statements prepared in accordance with GAAP

• FRF for SMEs is a relevant framework for SMEs where US GAAP statements are not required

THIRD PARTY VERIFICATION LETTERS

Third Party Verification Letters

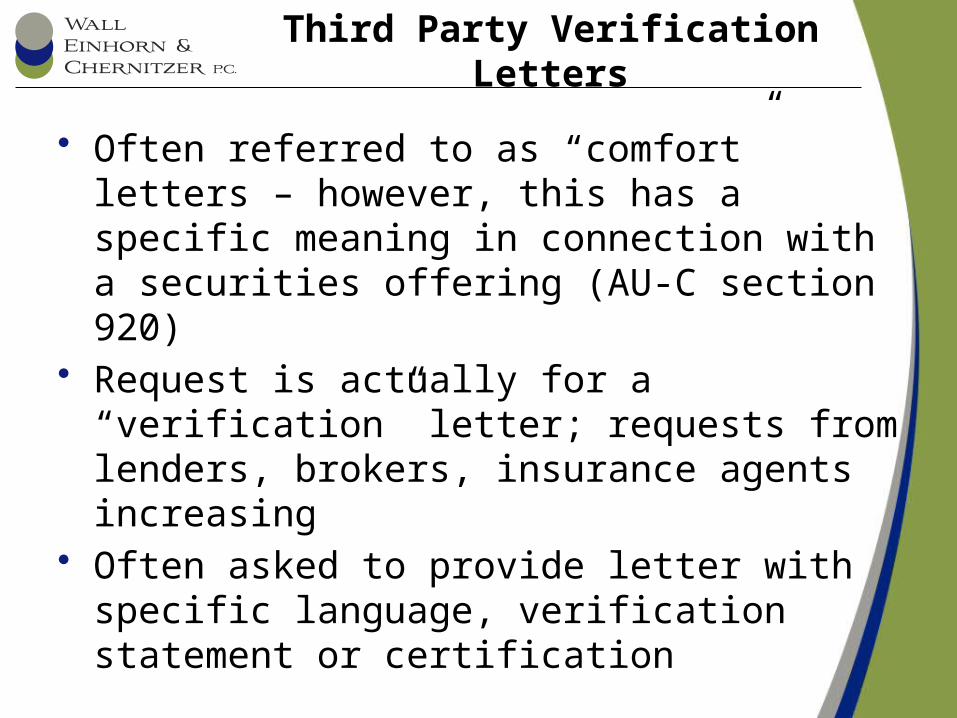

• Often referred to as “comfort” letters – however, this has a specific meaning in connection with a securities offering (AU-C section 920)

• Request is actually for a “verification” letter; requests from lenders, brokers, insurance agents increasing

• Often asked to provide letter with specific language, verification statement or certification

Third Party Verification Letters

• CPAs may supply verification letters on matters except solvency – – Is not insolvent at the time the debt is

incurred or would not be rendered insolvent as a result;

– Does not have unreasonably small capital;– Has the ability to pay debts as they mature

• Declining to offer assurance on solvency is not a RISK decision, it’s an ethical violation

• Also remember client confidentiality when supplying information

Third Party Verification Letters

• Reasons to give lenders and others – – “lender comfort letters” – AICPA technical practice

aid (non-authoritative guidance) TIS Section 9110• Refers you to AT Section 101• Suggests other services that may be performed, such as

audits/reviews/compilations, AUP, reports on prospective information, reports on pro forma personal financial information

• Offer copy of tax return (with client’s consent)

– Interpretation No. 2 of AT Section 101 – “responding to requests for reports on matters relating to solvency”

• Most banks have no such requirement; Freddie Mac and Fannie Mae have already rescinded such requests yet the practice remains

Recent Accounting and Auditing

StandardsSection II

FASB Accounting Standards

Recent FASB Accounting Standards

• ASU 2011-10 Property, Plant and Equipment• ASU 2011-11 Offsetting Assets and Liabilities• ASU 2012-01 Health Care Entities• ASU 2012-04 Technical Corrections and Improvements• ASU 2012-05 State of Cash Flows NFP• ASU 2012-06 Business Combinations• ASU 2012-07 Entertainment – Films• ASU 2013-01 Balance Sheet – Clarifying 2011-11• ASU 2013-02 Comprehensive Income• ASU 2013-03 Financial Instruments• ASU 2013-04 Liabilities• ASU 2013-05 Foreign Currency Matters• ASU 2013-06 NFP: Services Rec’d from Personnel of affiliate• ASU 2013-07 Liquidation Basis of Accounting• ASU 2013-08 Financial Services – Investment Companies• ASU 2013-09 FV Measurement• ASU 2013-10 Derivatives and Hedging• ASU 2013-11 Income Taxes

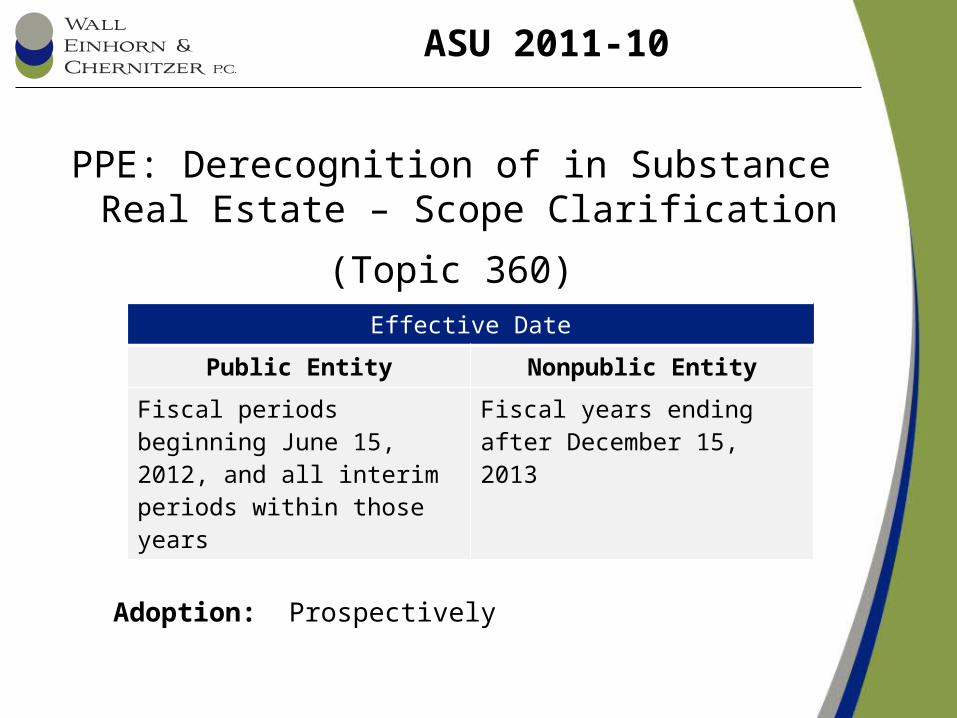

ASU 2011-10

PPE: Derecognition of in Substance Real Estate – Scope Clarification

(Topic 360)Effective Date

Public Entity Nonpublic Entity

Fiscal periods beginning June 15, 2012, and all interim periods within those years

Fiscal years ending after December 15, 2013

Adoption: Prospectively

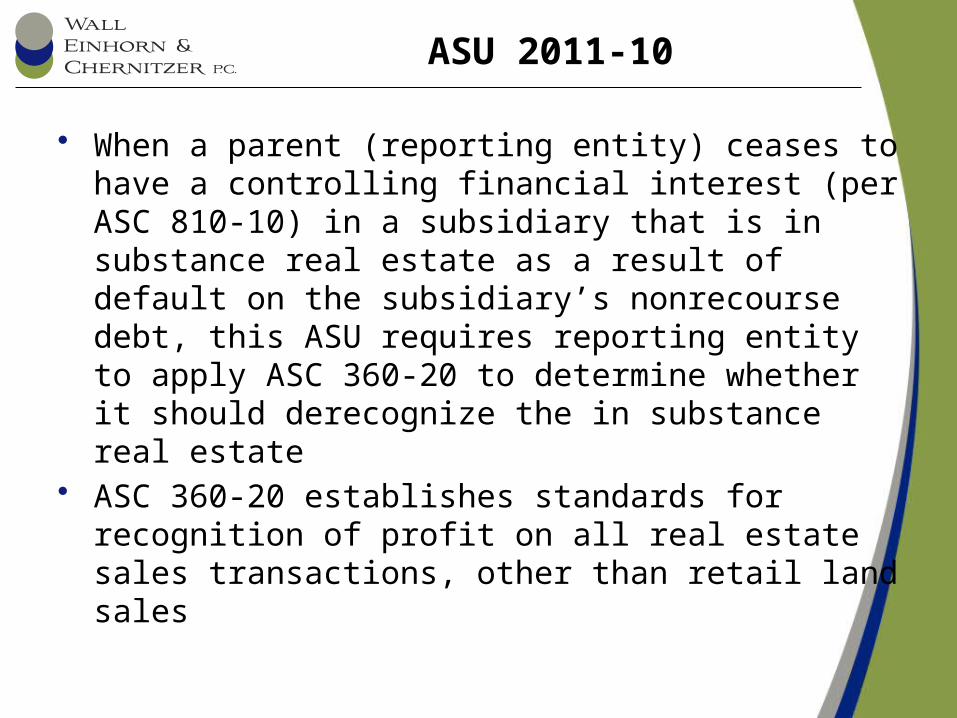

ASU 2011-10

• When a parent (reporting entity) ceases to have a controlling financial interest (per ASC 810-10) in a subsidiary that is in substance real estate as a result of default on the subsidiary’s nonrecourse debt, this ASU requires reporting entity to apply ASC 360-20 to determine whether it should derecognize the in substance real estate

• ASC 360-20 establishes standards for recognition of profit on all real estate sales transactions, other than retail land sales

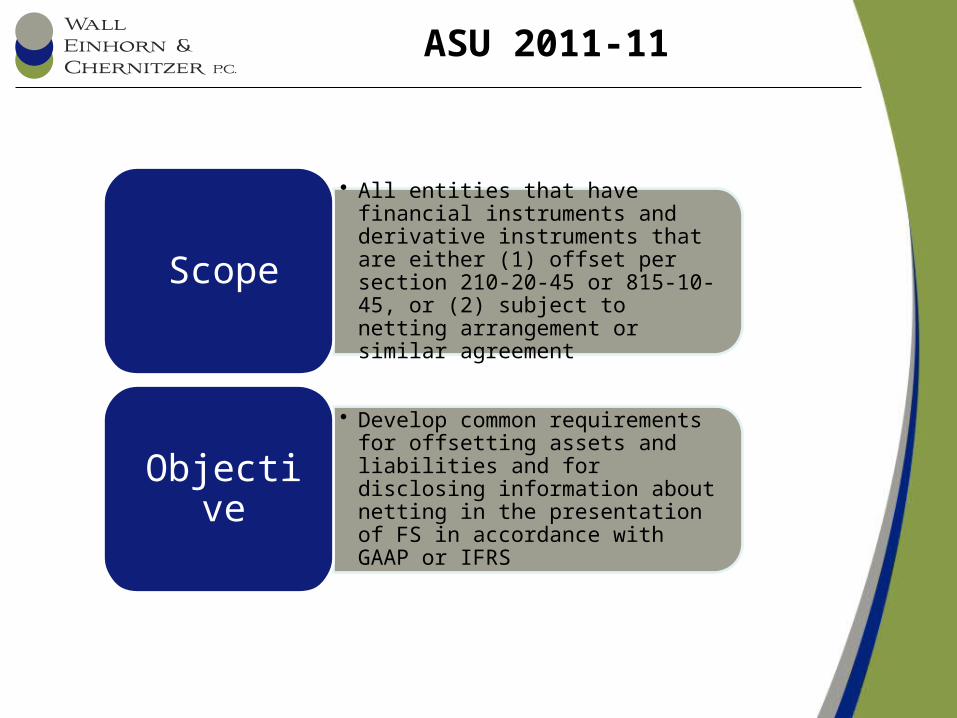

ASU 2011-11

Disclosures about Offsetting Assets and Liabilities

(Topic 210)

Effective Date

Public Entity Nonpublic Entity

Annual periods beginning January 1, 2013, and interim periods within those years

Same

Adoption: Retrospective for all prior periods presented

• All entities that have financial instruments and derivative instruments that are either (1) offset per section 210-20-45 or 815-10-45, or (2) subject to netting arrangement or similar agreement

Scope

• Develop common requirements for offsetting assets and liabilities and for disclosing information about netting in the presentation of FS in accordance with GAAP or IFRS

Objective

ASU 2011-11

Why this ASU?

• FASB and IASB agreed to disagree on when to offset

• ASU seeks to obtain convergence and comparability through disclosure

• Disclosures– Required irrespective of whether instruments are

offset or not

– Require net and gross information

– Assets and liabilities separately

– Description of the rights of set off

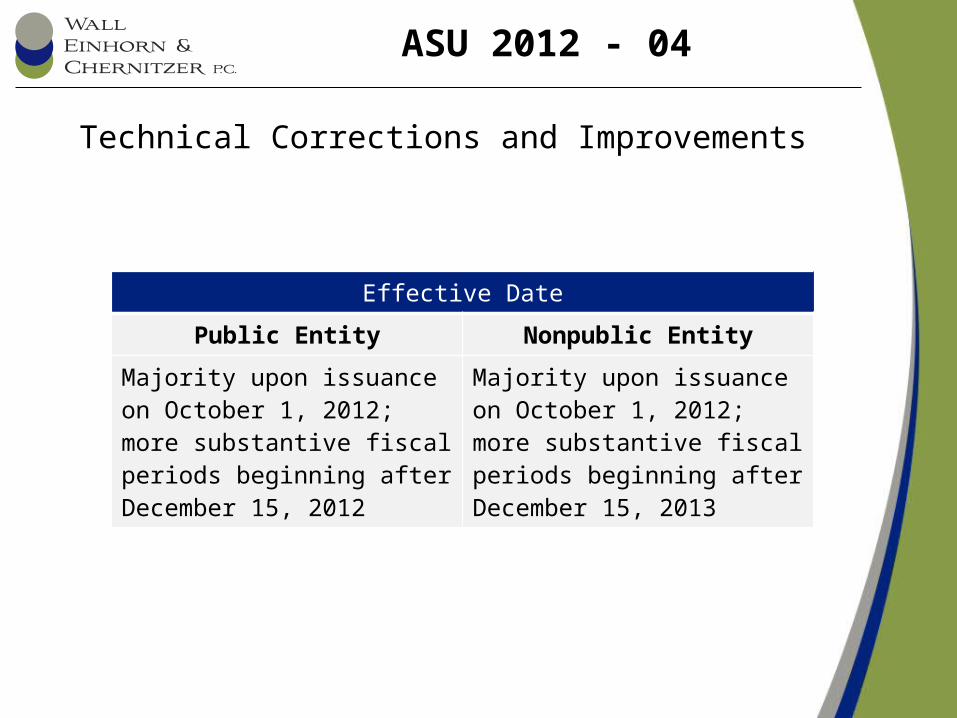

ASU 2012 - 04

Technical Corrections and Improvements

Effective Date

Public Entity Nonpublic Entity

Majority upon issuance on October 1, 2012; more substantive fiscal periods beginning after December 15, 2012

Majority upon issuance on October 1, 2012; more substantive fiscal periods beginning after December 15, 2013

ASU 2012-04

• Not expected to have significant impact on current practice

• Clarifies or corrects unintended application of guidance

• Some terminology changes – – Market value/current value to “fair

value”– Mark to market to “subsequently

measure at fair value”

ASU 2012 - 05

Statement of Cash Flows: NFP Entities – Classification of Sales Proceeds of Donated

Financial Assets(Topic 230)

Effective Date

Public Entity Nonpublic Entity

Fiscal years beginning after June 15, 2013, and interim periods within those years; early adoption from beg. of fiscal year permitted

Adoption: Prospectively; Retrospective application to prior periods presented is permitted

ASU 2012-05

• NFP entities that accept donated securitiesScope

• Standardize classification of cash receipts arising from the sales of donated securities in the statement of CF

Objective

ASU 2012-05

• Operating CF – IF upon receipt of donated assets, they are directed for sale without any limitations and are converted nearly immediately into cash (to avoid significant investment risks and rewards)

• Financing CF – IF the donor has restricted the use of securities to a long-term purpose

• Investing CF – All other cash receipts resulting from the sale of debt and equity securities not meeting other conditions above

ASU 2013 - 01

Balance Sheet – Clarifying the Scope of Disclosures about Offsetting Assets and Liabilities

(Topic 210)

Effective Date

Public Entity Nonpublic Entity

Fiscal years beginning January 1, 2013, and interim periods within those years

Same

Adoption: Retrospective for all prior periods presented

• Entities that hold derivativesScope

• Clarify scope of the disclosures required by the offsetting requirements of Topic 210

Objective

ASU 2013 - 01

ASU 2013-01

• Derivatives accounted for under topic 815– Bifurcated embedded derivatives– Repurchase agreements– Reverse repurchase agreements– Securities borrowing– Securities lending

• Financial assets and liabilities offset in accordance with – – Section 210– Section 815– Master netting arrangement

ASU 2013 - 02

Comprehensive Income – Reporting of Amounts Reclassified Out of Accumulated Other Comprehensive Income

(Topic 220)

Effective Date

Public Entity Nonpublic Entity

Fiscal years beginning after December 15, 2012

Fiscal years beginning after December 15, 2013

Adoption: Prospectively

• All entities that report items of comprehensive income

Scope

• Improve the reporting of reclassifications out of accumulated comprehensive income

Objective

ASU 2013 - 02

ASU 2013-02

Disclosure Requirements• Information about amounts

reclassified out of AOCI by component

• Components = DBP, CF Hedge, FX, AFS

• Net of tax by component• Presented on face or footnote by line

item of net income• Cross reference to other disclosures

Sample Disclosures

Notes to FSReclassifications Out of AOCI

Unrealized gains/losses on

Available for Sale Securities

$2,300(285)

(15)2,000(500)

$1,500

Realized G/L on saleImpairment exp.Insignificant itemTotal before tax

Tax expenseNet of tax

Sample Disclosures

Notes to FSReclassifications Out of AOCI

Gains/losses on Cash Flow Hedges:

Interest rate contracts

Credit derivativesFX contracts

$1,000(500)2,5003,000(250)

$2,750

Interest incomeOther income (exp)

Sales/revenueTotal before tax

Tax expenseNet of tax

ASU 2013-03

Financial Instruments – Clarifying Scope and Applicability of Particular Disclosure to Non-Public Entity

(Topic 825)

Effective Date

Public Entity Nonpublic Entity

N/A Upon Issuance

Adoption: Prospectively

• Non-public entities that have total assets of $100m or more or that have one or more derivative instruments

Scope

• Clarify scope and applicability of ASU 2011-04, Fair Value Measurement

Objective

ASU 2013-03

ASU 2013-03

Clarifies disclosure exception for nonpublic entities – – All nonpublic entities that meet the criteria

would NOT BE required to provide the level of the FV hierarchy within which FV measurements are categorized in the entirety (level 1, 2, 3) for such measurements that are only disclosed (i.e., they are not measured at FV in the balance sheet)

ASU 2013-04

Obligations resulting from Joint and Several Liability Arrangements for Which the Total Amount of Obligation is Fixed at the Reporting

Date

(Topic 405)

Effective Date

Public Entity Nonpublic Entity

Fiscal years beginning after December 15, 2013

Fiscal years beginning after December 15, 2014

Adoption: Retrospective for all prior periods presented

ASU 2013-04

• Joint and several liability arrangements for which the total amount of the obligation is fixed at the reporting date– Debt arrangements– Other contractual obligations– Settled litigation and judicial rulings

ASU 2013-04

Why this standard?

Variance in practice• Record entire amount under the joint and several

liability arrangement• Record less than the amount to the total

obligation:– Allocated amount– Proceeds received– Portion of amount agreed to pay to co-obligors

ASU 2013-04 measurement

Amount agreed to pay

on basis of arrangement

with co-obligors

Any additional amount

expected to be paid on behalf of co-obligors

Total fixed obligation at the reporting

date

ASU 2013-04

Disclosure requirements• Nature of arrangement• Total outstanding amount• Carrying amount• Nature of recourse provisions• Corresponding entries

ASU 2013-06

NFP Entities – Services Related from Personnel of an Affiliate

(Topic 958)

Effective Date

Public Entity Nonpublic Entity

Fiscal years beginning after June 15, 2014

Adoption: Prospectively

• All NFP entities that receive personnel services from an affiliate for which the affiliate does not seek compensation from the recipient NFP

Scope

• Standardize accounting for personnel services received from affiliates

Objective

ASU 2013-06

ASU 2013-06

NFP entity

Direct or Common control

Control Intermediat

e

Control

ASU 2013-06

• Statement of activities– Measurement at cost of services

recorded by affiliate (payroll + fringe)– Included in change in net assets in

equity transfer for business-type entity– Health care entities use guidance ASC

954– All others as expenses

ASU 2013-07

The Liquidation Basis of Accounting

Effective Date

Public Entity Nonpublic Entity

Annual reporting periods beginning after December 15, 2013, and interim periods therein.

Same

Adoption: Prospectively; early adoption permitted

ASU 2013-07

Required when liquidation is imminent– Plan is approved and likelihood is

remote that the plan will be blocked by other parties

– Plan is imposed by other forces (e.g., involuntary bankruptcy) and likelihood is remote that entity will return from liquidation

– Liquidation plan differs from liquidation plan in governing documents

ASU 2013-07

Measurement– Assets and liabilities – amount of cash or

other consideration expected to receive or pay

– Expected aggregate liquidation and disposal costs associated with settlement of those assets/liabilities

– Expected future costs/income during course of liquidation (e.g., payroll and interest income)

ASU 2013-07

Presentation and Disclosure– Description of liquidation plan, including

manner of disposal and duration of liquidation

– Methods and significant assumptions used to measure assets/liabilities and any changes in method

– Type and amount of costs and income accrued

Auditing Update

Peer Review Under AU-C (Clarity)

• Peer review team captains now must consider the results of regulatory and/or governmental oversights– Selection of engagements to review– Risk assessment (nature, cause, pattern,

pervasiveness of oversight results)– Evaluate the firm’s response to the results– Examine the remediation efforts by the firm

• If similar issues are raised in both the regulatory and/or governmental oversight and in the peer review, the review should consider whether there is a systemic problem with the design of the system of QC or compliance with it

Peer Review Under AU-C (clarity)

• Review teams will document – – Firm’s knowledge of the clarified audit standards– Review the quality control document for modifications

related to the clarified audit standards• Major focus for peer review

– Changes to auditor’s reports– Updated engagement letter wording– Inspecting correspondence with relevant licensing and

regulatory authorities to identify instances of non-compliance with laws and regulations

– Changes to internal control communications– Changes to requirements regarding RP when reporting

on FS prepared in accordance with special purpose framework

– Compliance with the requirements for group auditsNoncompliance = modified peer review report

Latest issues with Audit Productivity

Determining testing scope• How to link to

PM and what % range to use?

Setting a significant difference threshold for analytical procedures• When am I

done?

Structuring tests of redundant controls• What sample

size to use?

Defining Acceptable Difference

Analytic – example 1

Deposits at 12-31-10Deposits at 12-31-11Deposits at 12-31-12= Expectation (Avg.)- Actual= Difference% Difference

FactsTM $75,000; RMM – HighPrimary Test of Area

$80,000 25,000120,000 75,000 85,000$10,000 12%

1. Suitability2. Reliability of Data3. Precision of

Expectation4. Acceptable

Difference5. Are we done?

Defining Acceptable Difference

Analytic – example 2

Units Shipped* Average $= Expectation- Actual= Difference% Difference

FactsTM $75,000; RMM – ModPrimary Test of Area

890,000 $11.50

10,235,000

10,375,000

$140,000

1.4%

1. Suitability2. Reliability of Data3. Precision of

Expectation4. Acceptable

Difference5. Are we done?

Defining Acceptable Difference

Analytic – example 3

Debt* Average rate= Expectation- Actual= Difference% Difference

FactsTM $75,000; RMM – LowPrimary Test of Area

$1,000,000

7.4% 74,000 83,500 $9,500

11.4%

1. Suitability2. Reliability of Data3. Precision of

Expectation4. Acceptable

Difference5. Are we done?

Defining Acceptable Difference

Analytic – example 4

# of employees* Average salary= Expectation- Actual= Difference% Difference

FactsTM $75,000; RMM – HighCombined with balance sheet

test of detail (accrued payroll)

41 $32,800 1,344,800 1,280,000 $64,800

5.1%

1. Suitability2. Reliability of Data3. Precision of

Expectation4. Acceptable

Difference5. Are we done?

Redundant Controls

• Several controls address same risk• Auditor may –

– Test just one if effective by itself– Test both controls if both needed to be

effective– Test one control at low risk of overreliance

(large sample size) and one at high risk of overreliance (small sample size)

– Test both at higher risk of overreliance (two smaller samples instead of one large)

Electronic Evidence

• What do the standards require?

• What is legally required?

• What maximizes effectiveness and efficiency?

Electronic Evidence

Professional standards• Does not restrict form of evidence

– Electronic is permissible– No requirement for manual signatures– Confirmation may be scanned

• E-mail correspondence (including confirmation replies) is OK

AU-C 230.A5 audit documentation may be on electronic or other media

SQCS No.8 (QC 10.A58) apply procedures to ensure a faithful copy, both in form and content, when transferring or copying paper documentation or other media

Electronic Evidence

Legal considerations• Hard copies of signed documents may be

required in some states (if auditor considered a party to the contract)– Rep letters, engagement letters, etc.– Consult attorney

Electronic Evidence

Effectiveness and Efficiency• Lock down, archive and retention policies• Perm file or not• On-site versus remote auditing• Determining what to retain in audit files (obtain versus

retain)– Bank rec, bank statement agreed to bank rec– Returned bank confirmation– Detail of prepaid expenses less than TM in their entirety– Client calculation of the allowance for bad debts used only to agree to TB;

auditor test-work was to develop independent expectation of the required allowance through separate procedures

– Client provided analysis of inventory reserve with tabs for current year and prior 10 years

– Template for analyzing inventory overhead allocation in a year when FG and WIP balances are below TM

– Detail of fixed asset roll-forward when additions and disposals are minimal– Large AP detail used in search for unrecorded but nothing else

Proposed Updates

Section III

Proposed Updates

– Revenue Recognition– Lease Accounting

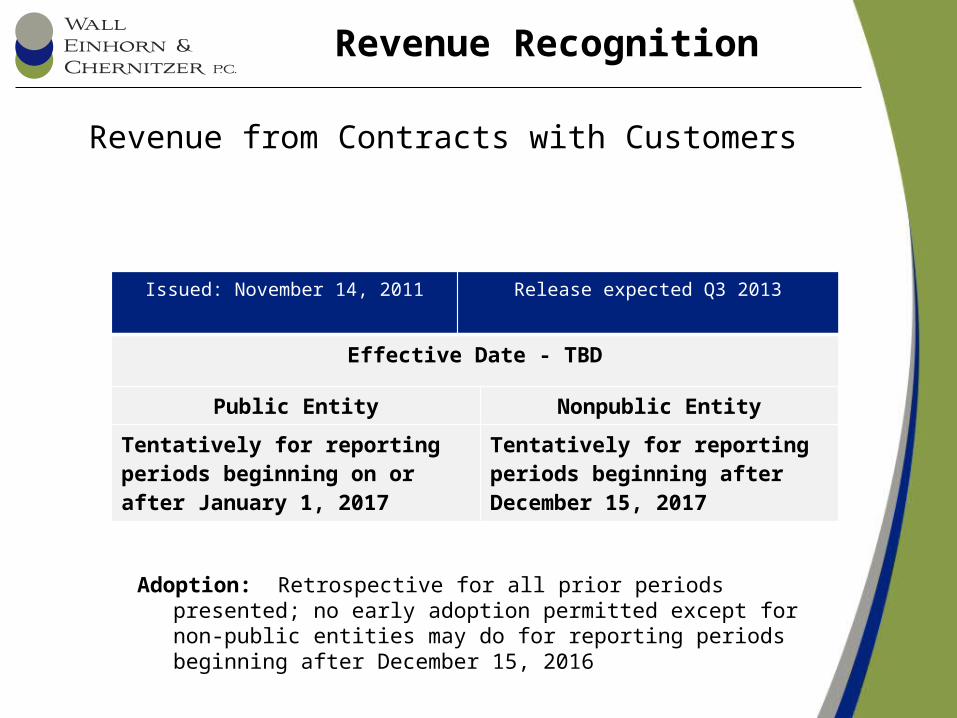

Revenue Recognition

Revenue from Contracts with Customers

Issued: November 14, 2011 Release expected Q3 2013

Effective Date - TBD

Public Entity Nonpublic Entity

Tentatively for reporting periods beginning on or after January 1, 2017

Tentatively for reporting periods beginning after December 15, 2017

Adoption: Retrospective for all prior periods presented; no early adoption permitted except for non-public entities may do for reporting periods beginning after December 15, 2016

Current Revenue Recognition Criteria

Earned & realizable

• Arrangement exists• Delivery occurred or services rendered

• Price is fixed or determinable• Collectability is reasonable assured

Current rules define the above criteria differently for specific industries (e.g., construction vs. manufacturing)and transactions

(e.g., tangible vs. software vs. bundled goods)

Fundamentally changes rules from “industry” based to “contract” based

#1

• Identify contract(s)

#2

• Identify performance obligations

#3

• Determine transaction price

#4

• Allocate price

#5

• Recognize revenue when performance obligations satisfied

Current Revenue Recognition Criteria

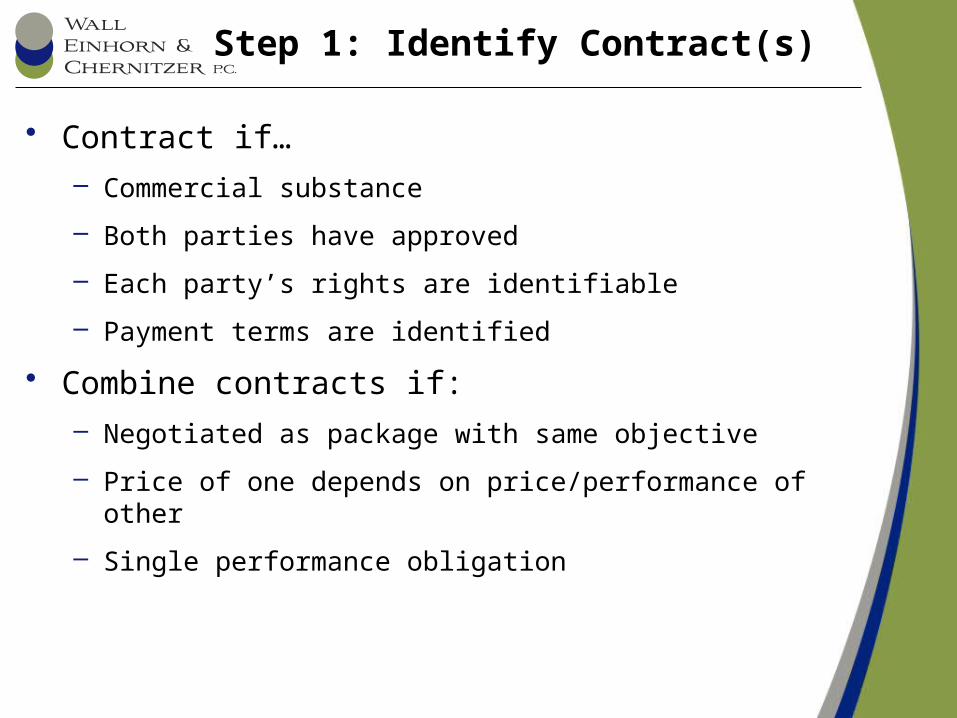

Step 1: Identify Contract(s)

• Contract if…– Commercial substance

– Both parties have approved

– Each party’s rights are identifiable

– Payment terms are identified

• Combine contracts if:– Negotiated as package with same objective

– Price of one depends on price/performance of other

– Single performance obligation

Step 2: Identify Performance Obligations

• Bundles goods/services – highly interrelated with significant integration and requires significant modification or customization

• Goods/services transfer at same time

Single

• Goods/services transfer at different times, and

• Goods/service has a distinct functionSeparate

Distinct function: (1) regularly sold separately, or (2) can be used separately on its own or together with other readily available resources

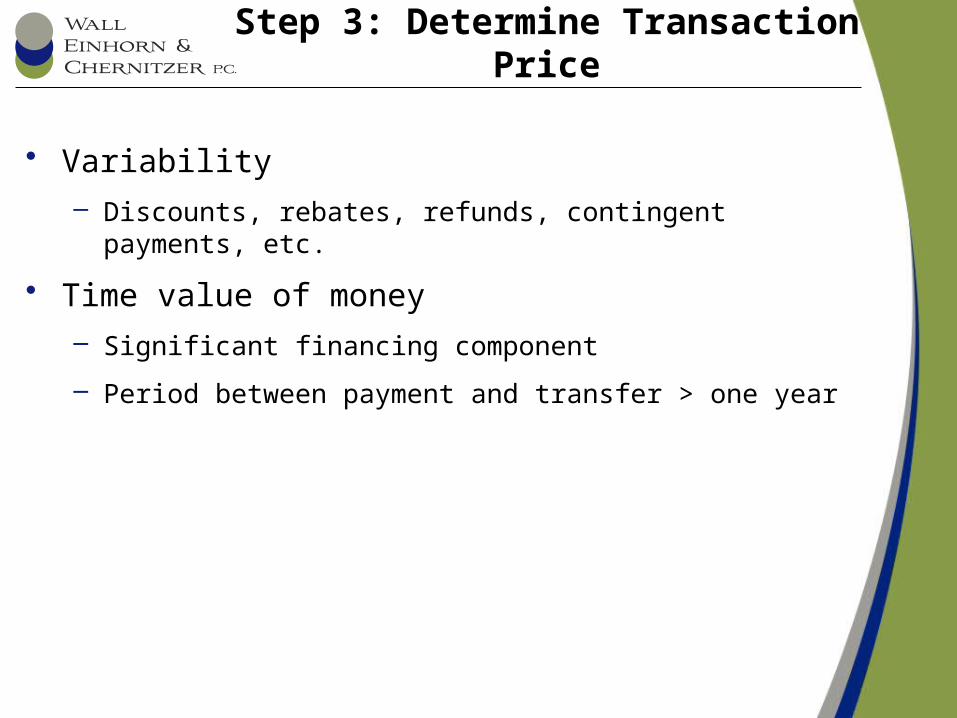

Step 3: Determine Transaction Price

• Variability– Discounts, rebates, refunds, contingent payments, etc.

• Time value of money

Variability

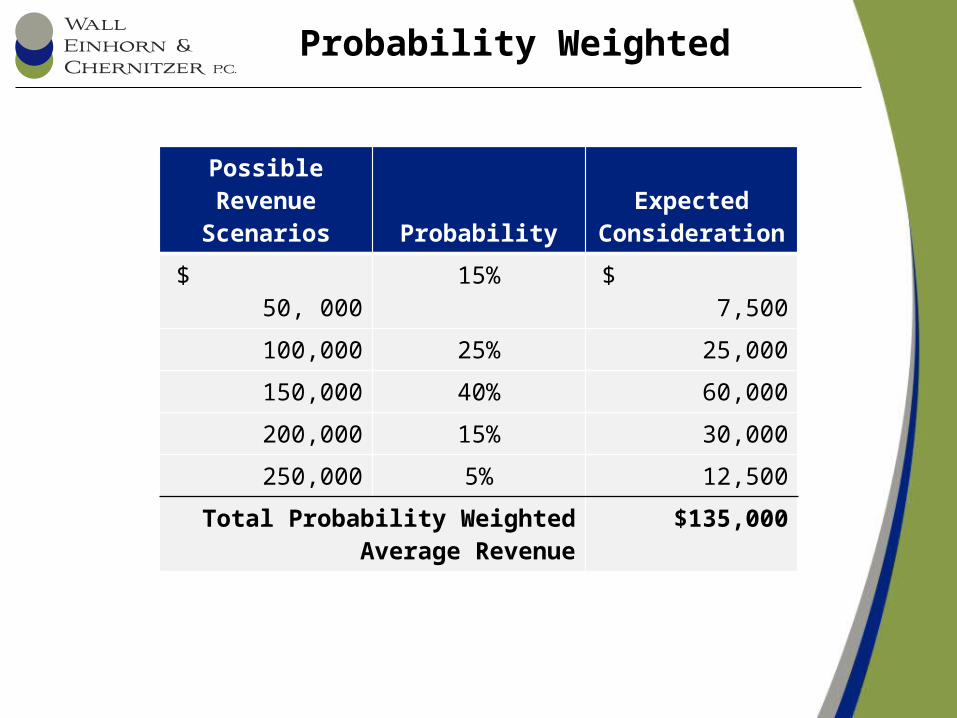

• Expected value (probability weighted) or most likely amount (which ever is most predictive)

• Reasonably assured to be entitled– Has experience (or can access others experience)

and

– Experience is predictive

Probability Weighted

Possible Revenue Scenarios Probability

Expected Consideration

$ 50, 000

15% $ 7,500

100,000 25% 25,000

150,000 40% 60,000

200,000 15% 30,000

250,000 5% 12,500

Total Probability Weighted Average Revenue

$135,000

When Is Experience Not Predictive?

• Amount is highly susceptible to factors outside the entity’s influence

• Uncertainty is not expected to be resolved for a long period of time

• Experience is limited

• Large number and broad range of possibilities

Step 3: Determine Transaction Price

• Variability– Discounts, rebates, refunds, contingent payments, etc.

• Time value of money– Significant financing component

– Period between payment and transfer > one year

Step 4: Allocating the Contract Price

An entity enters into a contract to deliver and install a manufacturing system for $100,000. The stand-alone market value for the installation is $20,000 and the separate selling price for the equipment is $90,000.

– The price would be allocated as follows:

Stand-Alone Price

Allocated Selling Price

Calculation

Equipment $90,000 $81,800 81.8% x $100,000 (90,000/110,000 = 81.8%)

Installation

$20,000 $18,200 18.2% x $100,000 (20,000/110,000 = 18.2%

Total $110,000 $100,000

Step 5: Revenue Recognition

• Performance obligation is satisfied when customer obtains control.

• “…the ability to direct the use of and obtain substantially all of the remaining benefits from the asset. Control includes the ability to prevent other entities from directing the use of and obtaining the benefits from an asset.”

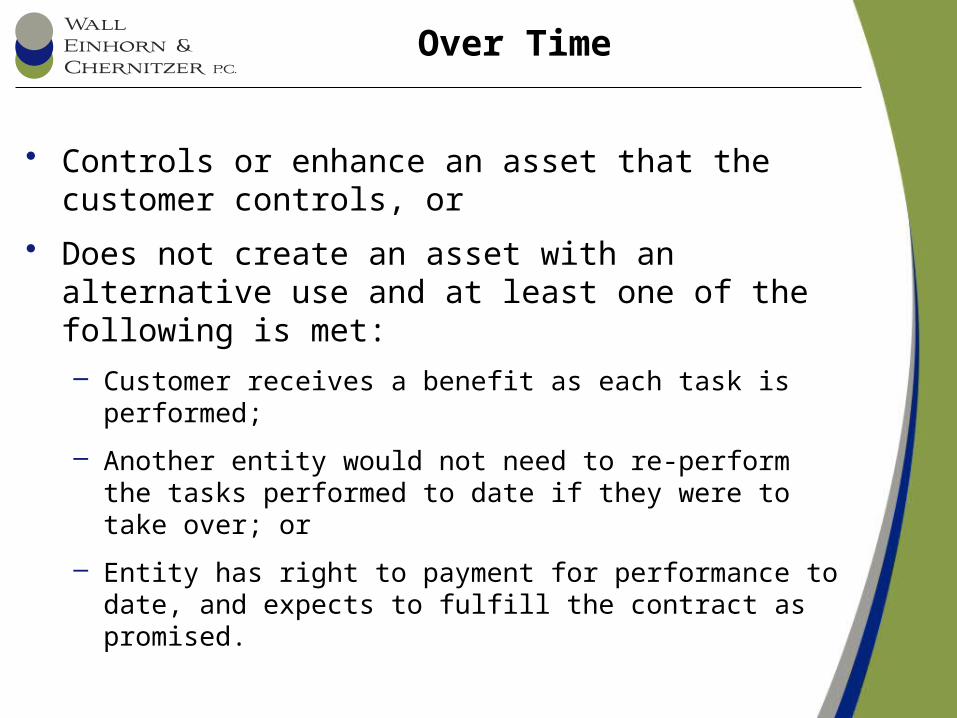

Over Time

• Controls or enhance an asset that the customer controls, or

• Does not create an asset with an alternative use and at least one of the following is met:– Customer receives a benefit as each task is performed;

– Another entity would not need to re-perform the tasks performed to date if they were to take over; or

– Entity has right to payment for performance to date, and expects to fulfill the contract as promised.

Point in Time

• Indicators that control has transferred– Right to payment

– Customer has legal title

– Physical possession is transferred

– Customer has risk and rewards

– Customer has accepted

Other Issues

• Contract modifications

• Onerous performance obligations

• Contract costs

• Collectability – contra-revenue

• Transfer of a nonfinancial asset

• Disclosures

• Tax implications

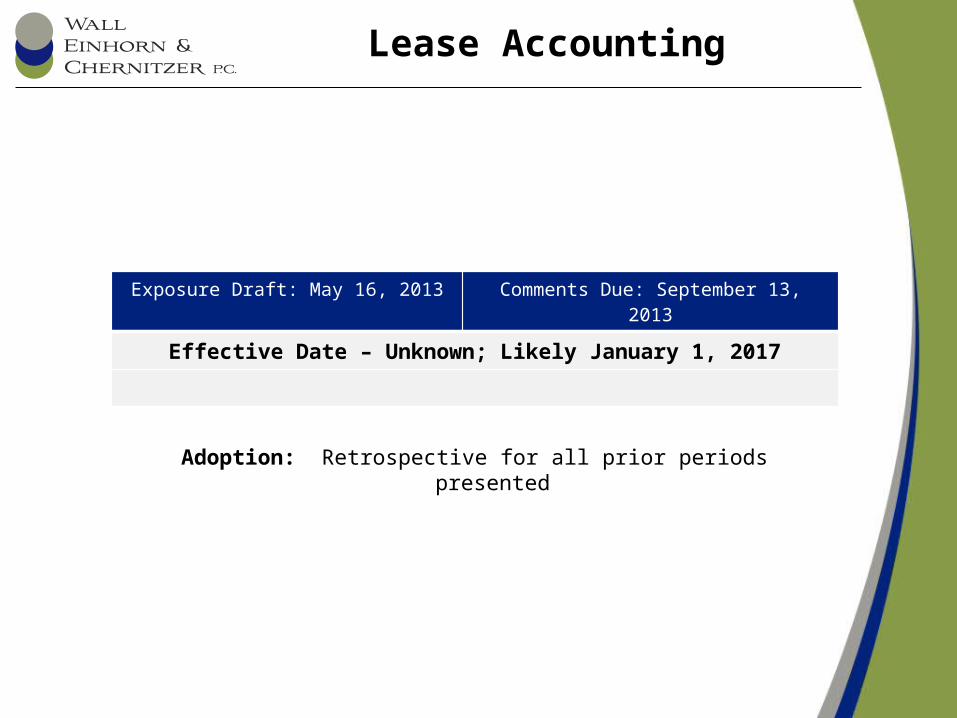

Lease Accounting

Exposure Draft: May 16, 2013 Comments Due: September 13, 2013

Effective Date – Unknown; Likely January 1, 2017

Adoption: Retrospective for all prior periods presented

Lease Proposal

• Main Emphasis – to get all obligations on the balance sheet

• Lease placed in one of 2 categories – impacts revenue and expense recognition (timing and character) and what ends up on the balance sheet for both lessor and lessee

Right to Control Model

Right of Use

Concept toRight to Control Concept

Lease under exposure draft as written would be a contract that conveys the right to control the

use of a specific identified asset for some form of consideration

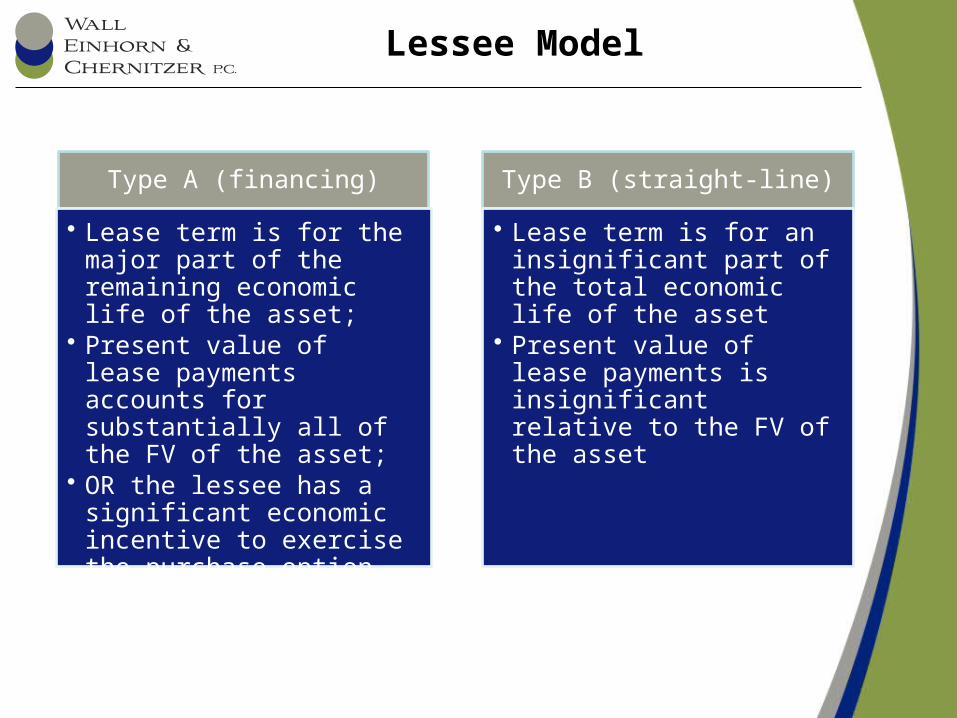

Lessee Model

Type A (financing)

• Lease term is for the major part of the remaining economic life of the asset;

• Present value of lease payments accounts for substantially all of the FV of the asset;

• OR the lessee has a significant economic incentive to exercise the purchase option

Type B (straight-line)

• Lease term is for an insignificant part of the total economic life of the asset

• Present value of lease payments is insignificant relative to the FV of the asset

Lessor Model

Type A (receivable & residual)

• Lease term is for the major part of the remaining economic life of the asset;

• Present value of lease payments accounts for substantially all of the FV of the asset;

• OR the lessee has a significant economic incentive to exercise the purchase option

Type B (operating lease)

• Lease term is for an insignificant part of the total economic life of the asset

• Present value of lease payments is insignificant relative to the FV of the asset

Type A Lessee vs. Lessor

Lessee

• Asset and liability on the balance sheet

• Asset/liability = PV of lease payments

• Liability relieved using effective interest method; asset amortized straight-line

Lessor

• Remove asset from books and recognize a profit potentially

• Lease receivable and residual asset on balance sheet

• Interest income

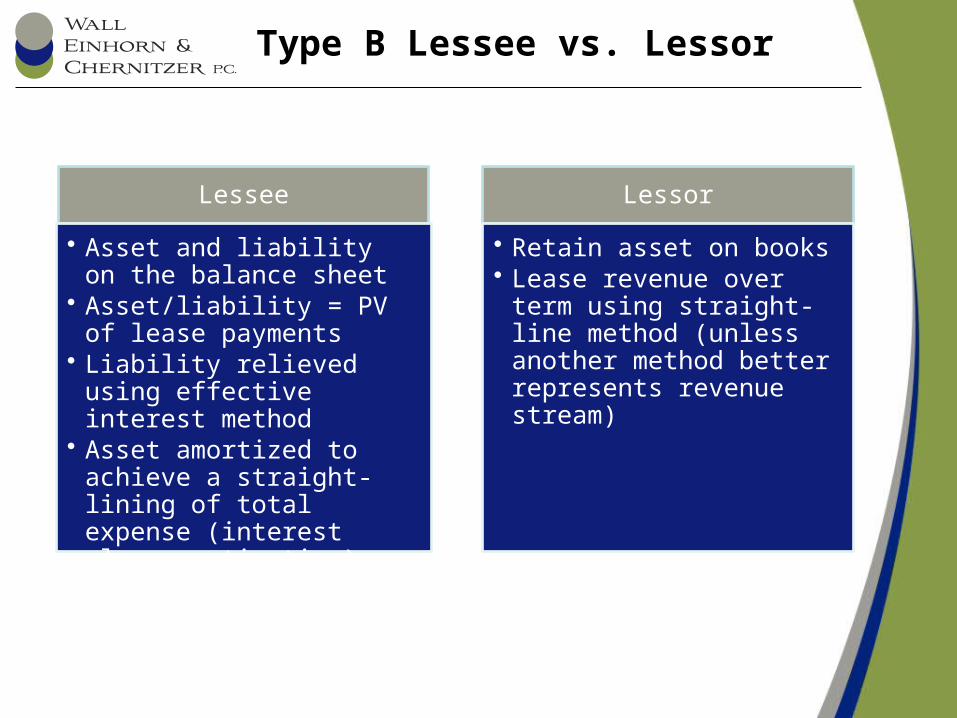

Type B Lessee vs. Lessor

Lessee

• Asset and liability on the balance sheet

• Asset/liability = PV of lease payments

• Liability relieved using effective interest method

• Asset amortized to achieve a straight-lining of total expense (interest plus amortization)

Lessor

• Retain asset on books• Lease revenue over term

using straight-line method (unless another method better represents revenue stream)

MiscellaneousSection IV

2012 Peer Review Report

• Disclosures relative to uncertain tax positions failed to include open tax years

• Failure to disclose FV of investments by level 1, 2 or 3• Failure to disclose 5 years debt maturities• Failure to properly identify operating vs. investment vs.

financing activities• Failure to properly disclose risks and uncertainties such as

nature of operations, use of estimates and concentrations• Failure to document communications with those charged

with governance• Incomplete or undocumented planning procedures related

to risk• Internal control communication

– Failure to note auditor’s responsibility– Failure to complete or inaccurate completion of work programs– Failure to identify matters during planning

2012 Peer Review Report

• Audit documentation not in accordance with standards• Analytical procedures – failure to document expectations

prior to performing final analytics, and then not comparing actual to expectations

2012 Peer Review Report

SSARS Issues• Compilation ITB financial statements – titles generally reflect GAAP• Compilation reports and review reports did not match minimum

requirements• Engagement letters for review engagements missing information –

– Engagements cannot be relied upon to disclose errors, fraud, illegal acts

– That accountant would inform the appropriate level of management if certain matters come to the accountant’s attention unless clearly inconsequential

• Review engagements – – failure to reference both periods covered in review report– failure to reference supplementary information in the review report– failure to document expectations prior to performing final analytics, and then not

comparing actual to expectations– Representation letter failed to cover all periods presented, and did not include

management’s responsibility re: responsibility to detect and prevent fraud