accenture payment services immediate payments: … · it’s a stark choice—and it’s down to...

TRANSCRIPT

Accenture Payment Services

Immediate payments: seizing the customer opportunityWhy real-time transfer and availability of funds is key to the success of the Everyday Bank

Executive summary 3

Payments in the era of the Everyday Bank 4

Market context: payments must catch up with today’s realities 7

The case for action: benefits for all users 8

Immediate payments in action: the UK’s Faster Payments Service 12

Digital payments innovation: paving the way for future services 14

A call to action for banks— and a change of mindset 16

2 | EVERYDAY BANK RESEARCH SERIES

As banks across the world strive to become “Everyday Banks” with a central role in their customers’ digital lives, it’s increasingly clear that offering immediate payments capabilities to customers will be critical for seizing this opportunity. What’s also clear is that it’s not only payment confirmation that must be instantaneous. For immediate payments to truly engage customers and drive ongoing payments innovation, monetary value must also be available immediately for customers to digitally spend as they wish.

The need for instant access to value is consistently underlined by customer research studies—and by the rising number of immediate payments infrastructures being set up and operated around the world. From the UK to Singapore, from Australia to the USA, immediate payments are either already available or being planned. The momentum is unstoppable—and growing.

Countries’ increased adoption of immediate payments infrastructure reflects the significant benefits immediate payments can deliver to end-users. Governments gain advantages ranging from reduced cash and check handling to easier management of economic risks. Businesses can pay employees and suppliers faster, have funds available quickly, and gain access to rich payments data. Consumers stand to benefit most, with convenient 24x7 availability, a compelling end-to-end payments experience, and ideally, immediate access to value.

The reality of these benefits is proven by consumers’ rapid take-up of existing immediate payments services such as the UK’s Faster Payments Service, but the advantages realized to date are just the start. Immediate payments systems being developed are ever more sophisticated, with potential for future innovation built in: for example, Australia’s New Payments Platform, based on a multi-layered infrastructure designed to improve payments experience to end-users, promote competition and drive innovation in payments services.

Also emerging are ever more intuitive and sophisticated services and applications that leverage the underlying immediate payments capabilities to meet a growing range of customer needs in real time. From instantaneous person-to-person transfers to parking payments, from geo-ticketing to crowd-sharing, new applications are appearing constantly. In part due to these newcomers, Accenture and VocaLink believe banks need to choose their digital service models carefully.

Either they can stand back and allow themselves to be relegated to the status of transaction utilities, with customer value, relevance and relationships migrating elsewhere. Or they can embrace the full potential of immediate payments, and innovate individually and collaboratively to seize their rightful position in the payments ecosystem and their customers’ lifestyles. In our view, those banks that choose the second option will emerge as the industry’s winners of tomorrow.

Executive summary

EVERYDAY BANK RESEARCH SERIES | 3

Due to the impact of digital technology on consumers’ behaviors and expectations worldwide, today’s banks are at a crossroads.

They can become central to their customers’ everyday purchasing activities, in the same way that social media and online retailers have become central to consumers’ purchasing decisions—tapping detailed customer data to offer relevant discounts and offers, pre-sale advice, post-sale support, and cross-sale opportunities. Or today’s banks can stay on the periphery of their customers’ lives, acting merely as transactional utilities handling financing and fund transfers.

It’s a stark choice—and it’s down to the banks themselves to make it. Newcomers are beginning to threaten banks’ revenues, by offering intuitive mobile payment applications and websites. In Accenture’s view, a third of bank’s revenues are in jeopardy by continuing on their current trajectory of offering limited digital services to customers—the apparently “safe” route.1 In contrast, Accenture analysis suggests that those that choose to position themselves as the “Everyday Bank”—harnessing their extensive customer data to reinvent themselves as value aggregators, advice providers and access facilitators—can expect an overall difference of 50 percentage points in operating income over those who do not.2

The digital revolution in payments… Payments play a key role in banks’ transformations into Everyday Banks—particularly recently, due to the adoption of immediate payments infrastructure by increasing numbers of countries. The convergence of immediate payments with steadily growing usage of smartphones and other digital channels presents an opportunity for bank accounts to become focal points for customer interactions and engagement—outlined in Accenture’s vision for Everyday Payments.3

Capitalizing on this opportunity will mean that the Everyday Bank can increasingly help to fulfill customers’ non-financial as well as financial needs, forging deep and more durable two-way relationships in the process. Against this background, we have created this point of view on immediate payments.

…demands that customers have immediate access to funds For this point of view, Accenture defines “real-time payments systems” or “immediate payments” as an interbank account-to account payment that is posted and confirmed to the originating bank within one minute, so the payee can use this value instantly and the payer has confirmation of the status of the transaction.

For banks and payment providers to reposition themselves as trusted and indispensable digital partners for consumers, we believe a new immediate payments industry capability will be needed: one that supports and enables

real-time account-to-account transfers and payments between connected Everyday Banks, Everyday Payment Providers, and relevant partners in the interconnected payments ecosystem.

Some banks have argued that “immediate payments” services could viably be offered by providing immediate messaging to confirm the payment, with settlement then being completed later—the next day, for example—at which point the funds would become available. However, Accenture believes banks will be making a big mistake if they press ahead with “immediate payments” offerings based on this type of definition. While a guarantee that funds will be delivered in the future may work for merchants accepting credit card payments, this model will simply not be enough to give customers—both businesses and consumers—the seamless payments experience they are now demanding. This will also miss out on a whole world of new digital business models enabled by real-time availability of funds. We explain our thinking on this issue in more detail in the accompanying information panel.

Alongside the growing demand from customers for instantly accessible monetary value, it’s also important to take into account the additional benefits and opportunities that spring from increasing the velocity of money. On the business front, it means companies can get paid more quickly and manage their cash flows efficiently by holding onto funds for longer before paying salaries or suppliers. And in society generally, it opens the way to faster and more effective emergency payments—enabling, for example, instantaneous financial transfers to the victims of a natural disaster.

Payments in the era of the Everyday Bank

4 | EVERYDAY BANK RESEARCH SERIES

Immediate messaging and next day settlement15%

Immediate messaging and batched settlement a few times per day36%

Immediate messaging and settlement49%

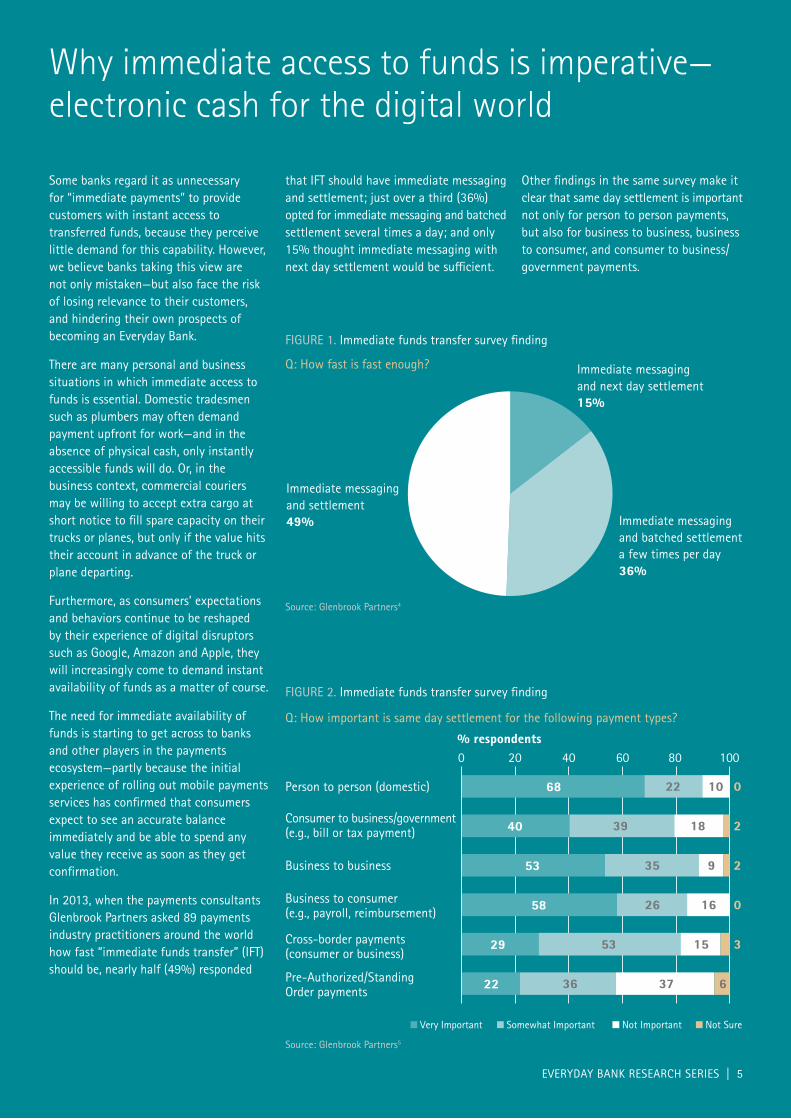

Some banks regard it as unnecessary for “immediate payments” to provide customers with instant access to transferred funds, because they perceive little demand for this capability. However, we believe banks taking this view are not only mistaken—but also face the risk of losing relevance to their customers, and hindering their own prospects of becoming an Everyday Bank.

There are many personal and business situations in which immediate access to funds is essential. Domestic tradesmen such as plumbers may often demand payment upfront for work—and in the absence of physical cash, only instantly accessible funds will do. Or, in the business context, commercial couriers may be willing to accept extra cargo at short notice to fill spare capacity on their trucks or planes, but only if the value hits their account in advance of the truck or plane departing.

Furthermore, as consumers’ expectations and behaviors continue to be reshaped by their experience of digital disruptors such as Google, Amazon and Apple, they will increasingly come to demand instant availability of funds as a matter of course.

The need for immediate availability of funds is starting to get across to banks and other players in the payments ecosystem—partly because the initial experience of rolling out mobile payments services has confirmed that consumers expect to see an accurate balance immediately and be able to spend any value they receive as soon as they get confirmation.

In 2013, when the payments consultants Glenbrook Partners asked 89 payments industry practitioners around the world how fast “immediate funds transfer” (IFT) should be, nearly half (49%) responded

that IFT should have immediate messaging and settlement; just over a third (36%) opted for immediate messaging and batched settlement several times a day; and only 15% thought immediate messaging with next day settlement would be sufficient.

Other findings in the same survey make it clear that same day settlement is important not only for person to person payments, but also for business to business, business to consumer, and consumer to business/government payments.

Why immediate access to funds is imperative—electronic cash for the digital world

FIGURE 1. Immediate funds transfer survey finding

Q: How fast is fast enough?

Q: How important is same day settlement for the following payment types?

Source: Glenbrook Partners4

Source: Glenbrook Partners5

FIGURE 2. Immediate funds transfer survey finding

68

40

53

58

29

22

22

39

35

26

53

36

10

18

9

16

15

37

0

2

2

0

3

6

0 20 40 60 80 100

Person to person (domestic)

% respondents

Consumer to business/government(e.g., bill or tax payment)

Business to business

Business to consumer (e.g., payroll, reimbursement)

Cross-border payments (consumer or business)

Pre-Authorized/Standing Order payments

Very Important Somewhat Important Not Important Not Sure

EVERYDAY BANK RESEARCH SERIES | 5

Meet John and JennyJohn and Jenny are a young couple who originally featured in Accenture’s Everyday Payments point of view.6 In that paper, they had recently graduated and were engaged to be married. In this paper they’re now married and have a young family.

To mark their son Hugo’s second birthday, John and Jenny are holding a birthday party for Hugo’s friends and their parents. Ahead of the event, Jenny books a children’s entertainer, who stresses that he wants payment up-front before performing. John was supposed to pick up some cash the night before, but had a last-minute crisis at work and forgot to visit an ATM on the way home to get the money.

When the entertainer arrives at the house and finds John and Jenny do not have the cash to give him, he is on the point of walking out. But fortunately Jenny’s bank offers a mobile payments service that provides immediate availability of funds. Jenny transfers the money to the entertainer’s mobile phone, he opens his box of magic tricks—and the party goes with a swing.

PAYMENT

RECEIVEDPAYMENTSENT

HAPPY BIRTHDAY!HUGO

6 | EVERYDAY BANK RESEARCH SERIES

As commerce around the world continues to evolve into a 24x7 real-time ecosystem, there is growing pressure for payments infrastructure to keep pace with today’s realities. But the process of transacting payments has so far failed to stay abreast of advances and innovations in business and technology—or with the changes in consumers’ digital behaviors and expectations. Accenture believes the fundamental requirement is the ability to move money from one account to another immediately, with certainty, convenience and at low cost to all stakeholders. The reality is that most existing payment infrastructures currently lack this capability, and most are not compatible with online and mobile channels.

While the growing demand for immediate payments has triggered a global move towards real-time payments systems, only a handful of countries currently have a real-time or near-real time payments infrastructure in place. According to VocaLink, at least 13 real-time systems have been built or have gone into development over the past decade, including six which have been developed in the past three years alone.7

Examples include the UK’s Faster Payments Service—the largest real-time payment system in the world, and FAST (Fast and Secure Transfers), recently gone live in Singapore. Elsewhere, Australia is seeking to implement a New Payments Platform (NPP), and in late 2013, the United States Federal Reserve Banks released a “Payment System Improvement—Public Consultation Paper” and has spent 2014 conducting research on ways to improve the United States’ payment system.8

Shared factors drive payments change across the globe As the characteristics and benefits of immediate payment infrastructures become clearer, there is increasing interest and demand at all levels for immediate payments. Among those countries currently holding industry consultations or even taking the step to implementation—including Finland, the USA, Australia, and a couple of markets in the Middle East—this interest has been reflected by statements of the clear rationale for moving to immediate payments.

While the precise drivers for implementation vary between countries, there are a number of shared factors driving change across different markets, as highlighted some years ago by the World Bank in Outcomes of the Global Payments Systems Survey 2010.10 The report identifies six key factors as having played a significant role in triggering the reform of payment systems worldwide—with

the first three being the most important reasons for implementation of immediate payments infrastructure, in previous years:

• The need to improve the overall efficiency of the payments system.

• Responding to technological innovations.

• The need to reduce systemic risk.

• Demand from the markets for better payment and settlement systems.

• Demand from end-users for better payment and settlement services.

• Demand from government institutions for better payment services.

With implementations advancing and new immediate payments infrastructures and services rolling out, we believe the focus is now shifting to the last three of these drivers—which can be generally summed up as the growing demand from end-users of payments services for better solutions more suited to their needs. As the new world of immediate payments takes shape, it is—quite rightly—the customers who will have the final say.

Market context: payments must catch up with today’s realities

Source: VocaLink9

FIGURE 3. Immediate payments deployments around the world

Brasil

Chile

Mexico

Nigeria

South Africa

India

Poland

SwedenUnited Kingdom

TurkeySwitzerland

Japan

Taiwan

EVERYDAY BANK RESEARCH SERIES | 7

Across the world, the potential advantages for all end-users of all types—consumers, businesses and governments/central banks—are highlighted by industry consultation documents related to national immediate payments proposals.

One example includes the recent initiatives by the Federal Reserve Banks in the United States (see sidebar below).

To summarize this and other industry consultation documents related to national immediate payments proposals,

we found that immediate payments promise the following benefits for the various end-users:

Governments/ central banksGovernments/central banks gain support for government agendas to replace cash and checks, and an opportunity to increase the velocity of money—bringing positive implications for the entire economy. A real-time infrastructure also makes it easier to manage risk across the economy compared to batch infrastructure. The true benefit is naturally dependent on the type of settlement arrangement.

BusinessesBusinesses gains the advantages of immediate payments functionalities for payments to individuals—such as wages or for settling customer claims—and for payments to suppliers when they need to receive the value before releasing the goods or performing the service. Immediate payments also provide businesses with a viable alternative to checks.

The case for action: benefits for all users

In September 2013 the Federal Reserve Banks (FRB) published online a “Payment System Improvement—Public Consultation Paper”, stating that:

[…] opportunity exists to improve speed and efficiency of payments and to maintain payment system safety in the face of escalating threats. […] ongoing innovation is necessary to ensure safe, efficient, and accessible payments that support economic activity and help maintain the global competitiveness of the United States.11

Receiving over 200 responses, the FRB has since completed several research activities to identify potential strategies to improve the United States’ payment system and advance its strategic direction. Those research activities included:

• Faster Payments Assessment—a high-level study of alternatives for speeding up US payments, including the exploration of a near-real-time retail payment system.

• Business Case Assessment—a review of whether or not ISO 20022 adoption is necessary for the US payment system to remain interoperable and competitive with other markets around the world.

• Payments Security Landscape Study—an assessment of the Federal Reserve’s payment security goals, the payment landscape in the US today and the identification of weaknesses and opportunities that exist in the US payment system.

In September 2014, the FRB announced that it plans to use research conclusions and stakeholder feedback to prepare and share in the coming months a roadmap for payment system improvements.12

US government research and industry consultation for a Payment System Improvement Roadmap

8 | EVERYDAY BANK RESEARCH SERIES

EVERYDAY BANK RESEARCH SERIES | 9

Businesses that operate as the receivers in payments transactions also gain a number of benefits from immediate payments, such as faster availability of funds, an easier reconciliation process, and fewer customer dropouts during the payments process. They also have the ability to make an outgoing payment on receipt of an incoming payment—a digital and more efficient version of the cashflow management practice commonly used by small businesses, of paying outgoing checks against incoming checks. Moreover, immediate payments mean all businesses benefit from the availability of more comprehensive, accurate and timely data from payments (assuming they use a richer data format such as ISO20022). The possibilities and the associated benefits of richer data being utilized throughout an eco-system are endless.

ConsumersConsumers gain perhaps the widest range of benefits of all the users of immediate payments. These include the convenience of 24-hour availability, immediate confirmation of payments, and irrevocability of payment. As we highlighted earlier, they should also gain immediate use of the funds.

In our view, truly “immediate” payment capabilities—complete with real-time payment finality and balance update—are essential to a compelling end-to-end payments experience for consumers. The immediacy of the solution fits into the digital lifestyle—and this alignment will increase as digital behaviors and expectations continue to spread across consumer populations worldwide.

24x7 availability is essential because—quite simply—consumers use their smartphones 24x7, and expect the same functionality and services at any time of the day or night. Just as it would be absurd for a retailer to try and operate a 9-to-5 app or ecommerce site, so it would be impractical to offer a 9-to-5 real-time payment service. This view is supported by the fact that some smaller banks in the UK do not have 24x7 capabilities, and are at a significant disadvantage in their ability to offer faster payments compared to those banks that do.

John receives a text from his younger sister. It is 10pm and she is trying to get home after seeing a movie in town. Her bank account is overdrawn and she can’t get on a bus with her contactless bank card. John immediately sends her $15 using his mobile phone to credit her bank account. She receives a text confirming the funds are in her account, and she catches the next bus safely home.

Jenny goes out with a digital wristband that is digitally connected to her bank account, and a small clutch bag for her make-up, but no wallet. She sets a spending limit of $50 on her wristband through her mobile banking app. During the evening she pays in restaurants, bars and clubs using only her wristband. The band has a digital display and she always knows how much money she has left to spend. She and John have a great evening, dancing the night away without worrying about handling cash or overspending.

BUS

ACCOUNTBALANCE

$15

TOTAL$5.00

tap-payPay $5

balance $45

10 | EVERYDAY BANK RESEARCH SERIES

A recent research study by VocaLink into usage and perceptions of mobile payments among consumers and SMEs, Immediate mobile payments: The voice of the customer,13 further reinforces the case for immediate payments:

“… research reveals that the proposition offers real value: consumers and sole traders are prepared to pay for this service. Most of those who are excited by the service envisage using it occasionally when convenience and immediacy are most important. However, some view the service as ‘electronic cash’ and envisage using it extensively. It also seems likely that occasional users will find the service useful and convenient and will increase usage as any doubt about security is assuaged. As mobile phone usage continues to proliferate, immediate mobile payments have the potential to become ubiquitous, initially among the younger generation. Awareness is likely to be disseminated virally: through word of mouth and social networking sites as well as bank recommendation.”

The study adds that the only major reservation felt about immediate mobile payments relates to security. “People want the convenience of immediate mobile payments but they also want to be reassured that the service is secure,” it comments. “Consumers are used to PINs and passwords and assume such security provides adequate fraud prevention. However, security measures must not become so cumbersome or prohibitive to the extent that they impair the user experience.”

VocaLink study of immediate mobile payments reinforces the business case

EVERYDAY BANK RESEARCH SERIES | 11

John is helping his father buy a new car and accompanies him to a car showroom to test drive a few models. His father is set on buying one of them, but rather than let him go away to think about it, the dealer offers him $1,000 off to buy it immediately, and in part exchange for his existing car. The dealer won’t accept a credit card or debit card for such a high value purchase, but John’s father uses his mobile banking app to transfer the funds from his savings account to his bank account, and then a real-time payment from his bank account to the car dealer. The car dealer receives a confirmation he has received payment, and John’s father drives out of the show room, the proud owner of the new car.

PAY NOW

PAYMENTRECEIVED SALE

New TT

CONTINUE

TRANSFERfrom: 010to: 101

12 | EVERYDAY BANK RESEARCH SERIES

In those countries that have implemented immediate payment schemes, the ability to effect payments instantly on a 24x7 basis has changed payments usage patterns forever.

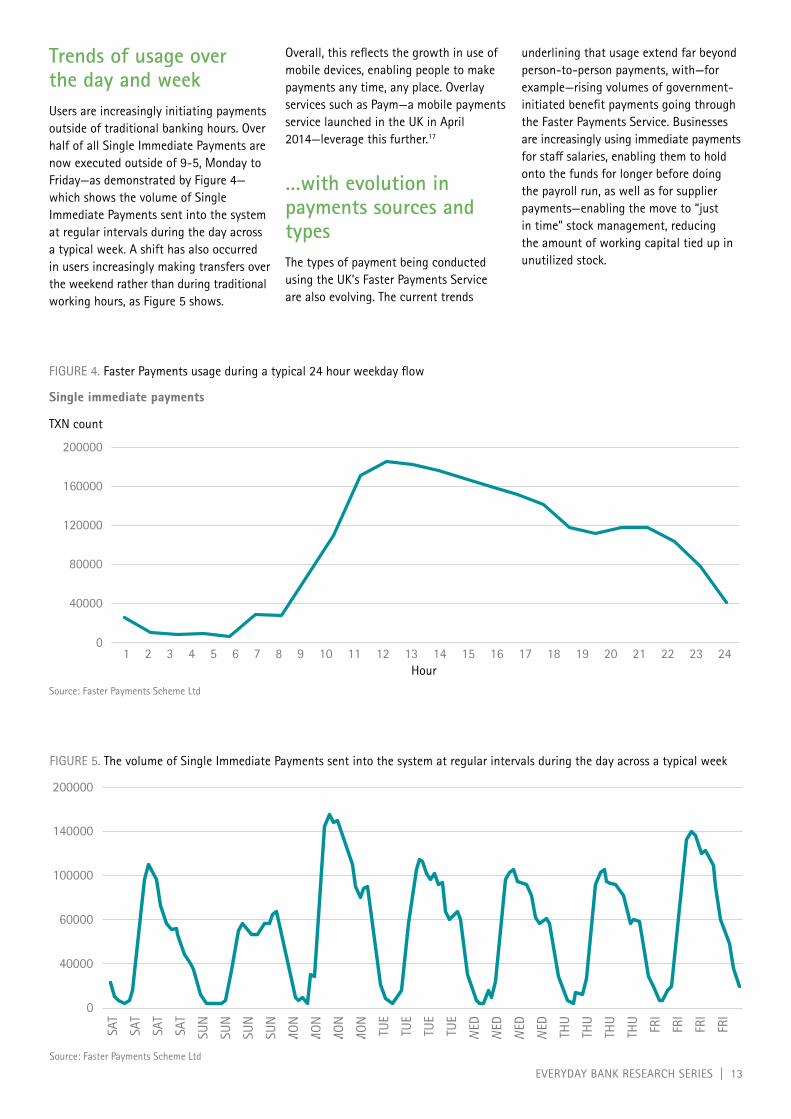

The UK has one of the world’s most mature immediate payments environments, launching its Faster Payments Service (FPS) in May 2008. By August 2014, over 3.8 billion payments worth more than £2.5 trillion have been processed through FPS. The headlong growth in usage saw the number of Faster Payments transactions reach around one billion in 2013 alone.14

Ongoing growth in volumes and value…The UK Payments Council’s statistics for the first two quarters of 2014 underline the success and ongoing growth of the Faster Payments Service.15 The total number of immediate payments in the UK grew 19% from the Q1 2013 to Q1 2014 (221 to 261 million) and 13% from Q2 2013 to Q2 2014 (239 to 270 million). The combined value of Faster Payments increased by 23% year-on-year to £212 billion in the first quarter of 2014.

Four different kinds of payment can be initiated via the Faster Payments Service. The statistics show that the strongest annual volume growth between Q1 2013 and Q1 2014 was for Single Immediate Payments at 31%, followed by Forward Dated Payments at 9%.16 Standing Order volumes were the slowest-growing segment, up by 7%. These varying relative growth rates are driven by one-off payments online, payments of credit card bills and inter-account transfers.

Immediate payments in action: the UK’s Faster Payments Service

Source: Faster Payments Scheme Ltd

FIGURE 5. The volume of Single Immediate Payments sent into the system at regular intervals during the day across a typical week

0

40000

60000

100000

140000

200000

SAT

SAT

SAT

SAT

SUN

SUN

SUN

SUN

MON

MON

MON

MON TU

E

TUE

TUE

TUE

WED

WED

WED

WED THU

THU

THU

THU

FRI

FRI

FRI

FRI

EVERYDAY BANK RESEARCH SERIES | 13

Trends of usage over the day and weekUsers are increasingly initiating payments outside of traditional banking hours. Over half of all Single Immediate Payments are now executed outside of 9-5, Monday to Friday—as demonstrated by Figure 4—which shows the volume of Single Immediate Payments sent into the system at regular intervals during the day across a typical week. A shift has also occurred in users increasingly making transfers over the weekend rather than during traditional working hours, as Figure 5 shows.

Overall, this reflects the growth in use of mobile devices, enabling people to make payments any time, any place. Overlay services such as Paym—a mobile payments service launched in the UK in April 2014—leverage this further.17

…with evolution in payments sources and typesThe types of payment being conducted using the UK’s Faster Payments Service are also evolving. The current trends

underlining that usage extend far beyond person-to-person payments, with—for example—rising volumes of government-initiated benefit payments going through the Faster Payments Service. Businesses are increasingly using immediate payments for staff salaries, enabling them to hold onto the funds for longer before doing the payroll run, as well as for supplier payments—enabling the move to “just in time” stock management, reducing the amount of working capital tied up in unutilized stock.

FIGURE 4. Faster Payments usage during a typical 24 hour weekday flow

Source: Faster Payments Scheme Ltd

Single immediate payments

40000

80000

120000

160000

200000

01 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

Hour

TXN count

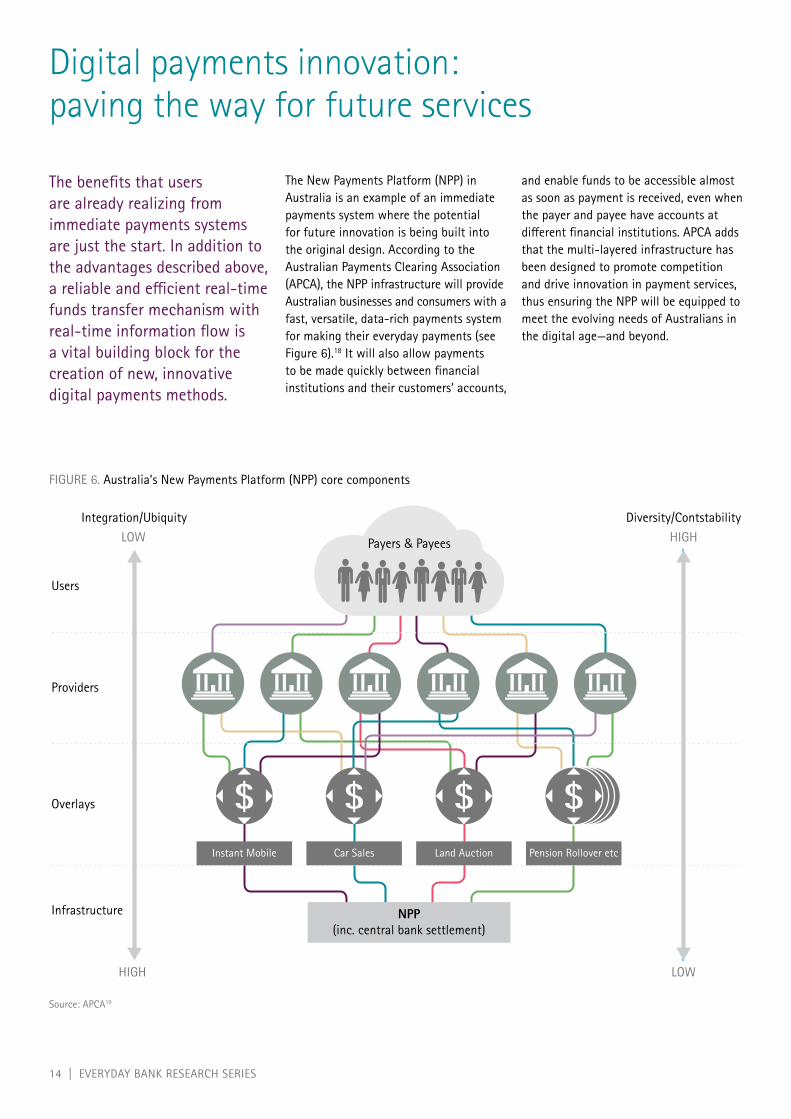

The benefits that users are already realizing from immediate payments systems are just the start. In addition to the advantages described above, a reliable and efficient real-time funds transfer mechanism with real-time information flow is a vital building block for the creation of new, innovative digital payments methods.

The New Payments Platform (NPP) in Australia is an example of an immediate payments system where the potential for future innovation is being built into the original design. According to the Australian Payments Clearing Association (APCA), the NPP infrastructure will provide Australian businesses and consumers with a fast, versatile, data-rich payments system for making their everyday payments (see Figure 6).18 It will also allow payments to be made quickly between financial institutions and their customers’ accounts,

and enable funds to be accessible almost as soon as payment is received, even when the payer and payee have accounts at different financial institutions. APCA adds that the multi-layered infrastructure has been designed to promote competition and drive innovation in payment services, thus ensuring the NPP will be equipped to meet the evolving needs of Australians in the digital age—and beyond.

Digital payments innovation: paving the way for future services

Source: APCA19

FIGURE 6. Australia’s New Payments Platform (NPP) core components

$$$$$ $ $

Payers & Payees

Instant Mobile Car Sales Land Auction

NPP(inc. central bank settlement)

Pension Rollover etc

HIGH

LOWIntegration/Ubiquity

Users

Providers

Overlays

Infrastructure

LOW

Diversity/ContstabilityHIGH

14 | EVERYDAY BANK RESEARCH SERIES

John and Jenny are at a shopping mall looking to buy a new television for their lounge.

After browsing through the various TVs on display, they choose the 42” flat screen television they want, and John clicks the “Pay with Zapp” mark next to the product. A unique and secure Zapp code is generated on the screen.

John then logs into the mobile banking app on his smartphone and selects Zapp, using the unique capability of checking that he has the necessary funds in his account to pay for the purchase. He enters the secure code, views his order summary on-screen, and confirms the payment.

The bank authorizes the transaction, the store’s website is updated automatically, and John receives confirmation that his payment has been successful.

Jenny orders some groceries from her favorite online supermarket and elects to pay on delivery. The groceries duly arrive that evening at the hour she requested. Jenny inspects the goods and accepts them, with the exception of some fruit that does not look fresh. The delivery driver adjusts the goods received note and invoice, Jenny pays for all the goods except the fruit with an immediate payment using her mobile phone, and after receiving confirmation the driver leaves for his next appointment.

Subtotal: $60(3 items disc.) -$10TOTAL: $50

NEWTOTAL

$50PAY NOW

onlinegroceries

PAYMENTAPPROVED

WELCOMETO ZAPP

secure code

PAY WITH ZA

PP

EVERYDAY BANK RESEARCH SERIES | 15

The UK is clearly further down the road than Australia in immediate payments—and it is significant that the UK’s Faster Payment Service has already paved the way for further innovation. A mobile payments service, Paym, was launched in April 2014 by the UK Payments Council, enabling consumers to send immediate payments between bank accounts using mobile phone numbers.20 At launch, the ability to send and receive Paym payments became available to more than 30 million people across the UK, and the service is targeted to reach more than nine out of ten current accounts, covering in excess of 40 million customers.

A further UK innovation, scheduled for launch in 2015, is a person-to-business payments service, Zapp.21 Owned by VocaLink, Zapp will allow consumers to make immediate payments from their bank accounts via their mobile phones when shopping online or in-store, or when paying small traders such as plumbers and larger businesses such as utilities.

Other potential services overlaying the core Faster Payments infrastructure may include parking payments and real-time taxi payments. Across all these advances, immediate availability of funds will be a key selling-point for users—as will the availability of richer data from immediate payments transactions conducted via mobile.

The pace of innovation is being sustained and accelerated through new approaches based on concepts such as collaboration and gamification. For example, in July 2014, Zapp held the first-ever Zapp Hackathon in London, challenging some of the UK’s leading third-party innovators—including retail and financial technology start-ups—to envision, develop and test a platform, app or concept that would benefit from being “powered by Zapp”.22 The winner of the Hackathon, using the Zapp platform, was Sage Pay—who developed an app that uses geo-location technology to enable a gig-goer to pay for a concert automatically when they arrive.23 This geo-ticketing solution is a great example of how mobile payments can help to blur the lines between online, mobile, and the in-store—or at-event—shopping experience.

As we’ve described, immediate availability of value is key for immediate payments infrastructure to deliver full potential benefits to users. In our view, banks need to take this imperative on board—and change their mindset to view the immediate payments opportunity from the perspective of an Everyday Bank and/or Everyday Payments Provider.

Accenture’s Everyday Payments point of view sets out a vision for how banks can avoid being relegated to the status of mere providers of “dumb” transactions—and instead occupy a position as a true partners at the heart of their consumers’ lifestyles.24 Embracing immediate payments in their truest sense will be key to achieving this positioning.

Understanding how a real-time system can benefit the key stakeholders and what the commercial benefits will be are crucial to the business case. Immediate payments will be the backbone to successful innovation for banks and the adoption of this capability is a natural step in their evolution as they look to stand their ground against new and non-traditional entrants.

The opportunity is there, and we believe banks must seize it, or face losing relevance—and ultimately revenues.

A call to action for banks— and a change of mindset

John and Jenny are on holiday in Venice. They plan to take a private boat tour and open the Hez!Presto! app on John’s mobile. Hez!Presto! is an “immediate crowd-sharing” app—one of the latest new business models to hit the digital scene, enabling users to pool payments instantaneously to share an experience unique to them, such as pop-up street performances or meals, shared taxi rides, or car sharing. In this case, John selects a private boat tour for 12 people for 600 euros, and the app broadcasts an invite for others to join. Within five minutes, ten nearby tourists have signed up, so the app automatically collects 50 euros from each and summons the tour. The boat arrives, Hez!Presto! credits the combined payments in real time to the boat owner’s bank account, and five minutes later John and Jenny are heading up the Grand Canal with their new-found companions.

HEZ! PRESTO!

EVENTCONFIRMED!

CONFIRMED

HEZ! PRESTO!HEZ! PRESTO!

create an event

Venice

16 | EVERYDAY BANK RESEARCH SERIES

EVERYDAY BANK RESEARCH SERIES | 17

1 The estimate of one-third of banking revenues at risk is based on an analysis of Western European banking revenue pools under the scenario of continued digital disruption and limited response from traditional banks. See also: http://bankingblog.accenture.com/retail-banking-revenues-at-risk-how-real-is-the-threat-of-digital-disruption-to-retail-banks/.

2 Accenture analysis for the “Everyday Bank”: See page 3 of http://www.accenture.com/microsite/everydaybank/Documents/media/EverydayBank-POV.pdf.

3 http://www.accenture.com/SiteCollectionDocuments/PDF/Accenture-Everyday-Payments.pdf.

4 http://paymentsviews.com/2013/05/01/immediate-funds-transfers-are-happening/

5 http://paymentsviews.com/2013/05/01/immediate-funds-transfers-are-happening/

6 http://www.accenture.com/microsites/everydaybank/Pages/everyday-bank-payments.aspx

7 The number of real-time systems in existence varies, owing to definition and categorisation. In this paper, real-time payment systems are defined as ‘an interbank account-to-account payment that is posted and confirmed to the originating bank within one minute, so the payee received and can use the value instantly and payer has confirmation of the status of the transaction’. These types of systems are also categorised as centralised, national payment systems.

8 http://www.bankingtech.com/wp-content/blogs.dir/94/files/2014/04/VocaLink_Supplement_low_res_Complete.pdf.

9 http://www.bankingtech.com/wp-content/blogs.dir/94/files/2014/04/VocaLink_Supplement_low_res_Complete.pdf.

10 “World Bank. 2011. Payment Systems Worldwide—A Snapshot: Outcomes of the Global Payment Systems Survey 2010.” World Bank, Washington, DC. © World Bank. https://openknowledge.worldbank.org/handle/10986/12813. License: CC BY 3.0 Unported.

11 http://fedpaymentsimprovement.org/wp-content/uploads/2013/09/Payment_System_Improvement-Public_Consultation_Paper.pdf (p1).

12 http://fedpaymentsimprovement.org/wp-content/uploads/final-phase-research-press-release.pdf.

13 http://www.vocalink.com/about-vocalink/industry-research.aspx.

14 http://www.fasterpayments.org.uk/press-release/faster-payments-sets-new-record-end-tax-year-rush.

15 UK Payments Council Quarterly Statistical report, 23 May 2014. http://www.paymentscouncil.org.uk/files/payments_council/free_industry_statistics/2014/payments_council_statistical_release_q1_2014.pdf.

16 For explanation of the different kinds of payment, please refer to http://www.fasterpayments.org.uk/about-us/benefits-faster-payments.

17 http://www.paym.co.uk.

18 http://www.apca.com.au/about-payments/future-of-payments/new-payments-platform.

19 http://www.apca.com.au/about-payments/future-of-payments/new-payments-platform.

20 http://www.paymentscouncil.org.uk/media_centre/press_releases/-/page/2878/.

21 http://www.zapp.co.uk.

22 http://www.zapp.co.uk/blog/2014/06/zapphack-london-2014-calling-retail-and-fintech-innovators-to-help-us-reviveretail/.

23 http://www.blog.sagepay.com/sage-pay-wins-zapphack-revive-retail-hackathon.

24 http://www.accenture.com/microsites/everydaybank/Pages/everyday-bank-payments.aspx.

Notes

18 | EVERYDAY BANK RESEARCH SERIES

EVERYDAY BANK RESEARCH SERIES | 19

ABOUT ACCENTUREAccenture is a global management consulting, technology services and outsourcing company, with more than 293,000 people serving clients in more than 120 countries. Combining unparalleled experience, comprehensive capabilities across all industries and business functions, and extensive research on the world’s most successful companies, Accenture collaborates with clients to help them become high-performance businesses and governments. The company generated net revenues of US$28.6 billion for the fiscal year ended Aug. 31, 2013. Its home page is www.accenture.com

ABOUT VOCALINKVocaLink is a global payments partner relied on by financial institutions, corporates and governments to provide high availability and resilient payment solutions. We operate world class leading payment clearing systems and ATM switching platforms which underpin the majority of UK electronic payments—we provide a national grid for payments. Our proven capability of implementing real time payment systems in the UK has led to the development of immediate payment solutions for other countries. Our platforms have made it easier to make payments confidently, securely and cost effectively. Last year we processed over 10 billion transactions with a value of £5 trillion.

We provide the platform for Bacs and the Current Account Switch Service; the real-time platform for the Faster Payments Service; and the LINK ATM Network, giving businesses and consumers simple, instant and reliable ways to access and move money. We are also at the forefront of mobile payments and Zapp, the UK’s leading mobile payment innovation, is empowering consumers to be able to make secure real-time consumer to merchant payments through existing mobile banking services.

VocaLink is Central Banking Payments and Clearing Technology Provider of the Year.

http://immediatepayments.vocalink.com/

ABOUT ACCENTURE PAYMENT SERVICESAccenture Payment Services, a business service within Accenture’s Financial Services operating group, helps banks improve business strategy, technology and operational efficiency in three key areas: core payments, card payments and digital payments. Accenture Payment Services and its more than 4,500 professionals dedicated to help banks simplify and integrate their payments systems and operations to reduce costs and improve productivity, meet new regulatory requirements, enable new mobile and digital offerings, and maintain payments as a revenue generator. More than 50 clients worldwide have engaged Accenture Payment Services to help them turn their payment operations into high-performing businesses. To learn more, visit www.accenture.com/paymentservices

The team would like to note that Pat Patel from VocaLink significantly contributed to this point of view.

To find out more about immediate payments, please contact:

Jeremy Light Accenture Payment Services [email protected]

Luigi Zanghellini Accenture Payment Services [email protected]

Paul Stoddart VocaLink Strategy and Business Development [email protected]

Kris Kubiena VocaLink Proposition Delivery [email protected]

Contact us

Copyright © 2014 Accenture All rights reserved.

Accenture, its logo, and High Performance Delivered are trademarks of Accenture. 14-4816/9-8270