ac239 managerial accounting seminar 6 jim eads, cpa, mst, msf budgeting 1

TRANSCRIPT

AC239AC239Managerial AccountingManagerial Accounting

Seminar 6Seminar 6

Jim Eads, CPA, MST, MSFJim Eads, CPA, MST, MSF

BudgetingBudgeting

11

BudgetBudget

A A budgetbudget charts a course for a charts a course for a business by outlining the plans of the business by outlining the plans of the business in financial terms. business in financial terms.

Budgeting objectives:Budgeting objectives: Planning: Establishing specific goalsPlanning: Establishing specific goals Directing: Executing plans to achieve the Directing: Executing plans to achieve the

goalsgoals Controlling: Periodically comparing actual Controlling: Periodically comparing actual

results to the goalsresults to the goals22

PlanningPlanning

Budgeting supports the Budgeting supports the planning planning processprocess by requiring all organizational by requiring all organizational units to establish their goals for the units to establish their goals for the upcoming period. upcoming period.

These goals motivate individuals and These goals motivate individuals and groups to groups to perform at high levelsperform at high levels. . Planning also motivates employees to Planning also motivates employees to attain goals andattain goals and improve overall improve overall decision makingdecision making..

33

DirectingDirecting

The budget can be used to The budget can be used to directdirect and and coordinatecoordinate operations in operations in order to achieve the stated goals.order to achieve the stated goals.

44

DirectingDirecting

Responsibility centers are the Responsibility centers are the budgetary units of an budgetary units of an organization. organization.

Each responsibility center is led by Each responsibility center is led by a manager who has the authority a manager who has the authority over and responsibility for the over and responsibility for the unit’s performance.unit’s performance.

55

ControllingControlling

As time passes, the actual As time passes, the actual performance of an operation can be performance of an operation can be compared against the planned goals. compared against the planned goals.

This provides prompt This provides prompt feedback feedback to to employees about their performance. employees about their performance. If necessary, employees can use If necessary, employees can use such feedback to adjust their such feedback to adjust their activities in the future.activities in the future.

66

Human BehaviorHuman Behavior

Human behavior problems can arise if:Human behavior problems can arise if:– the budget goal is too tight and very the budget goal is too tight and very

hard for the employee to achieve.hard for the employee to achieve.– the budget goal is too loose and very the budget goal is too loose and very

easy for the employee to achieve. easy for the employee to achieve. Called budgetary slackCalled budgetary slack

– the budget goals of a business conflict the budget goals of a business conflict with the objectives of the employees.with the objectives of the employees.

77

Types of BudgetingTypes of Budgeting

Fiscal-year budgeting Fiscal-year budgeting is is budgeting for an accounting year.budgeting for an accounting year.

Continuous budgeting Continuous budgeting always always budgets a rolling 12 months budgets a rolling 12 months future.future.

Zero-based budgeting Zero-based budgeting starts starts with a clean slate each year as if with a clean slate each year as if the business was just starting.the business was just starting.

88

Types of BudgetingTypes of Budgeting

Traditional budgetingTraditional budgeting uses prior uses prior period results and modifies for period results and modifies for expected changesexpected changes..

– Static budgetStatic budget– Flexible budgetFlexible budget

99

Static BudgetStatic Budget

A A static budgetstatic budget shows the expected shows the expected results of a responsibility center for results of a responsibility center for only only one activity levelone activity level. The budget . The budget does not change even if the activity does not change even if the activity changes.changes.

A static budget is used by many service A static budget is used by many service companies and for some companies and for some administrative functions of administrative functions of manufacturing companies.manufacturing companies.

1010

Static BudgetStatic Budget

Strength:Strength: A static budget is A static budget is simple—all expenses are simple—all expenses are budgeted as fixed costs.budgeted as fixed costs.

Weakness:Weakness: A static budget does A static budget does not adjust for changes in not adjust for changes in revenues and expenses that revenues and expenses that occur as volumes change.occur as volumes change.

1111

Flexible BudgetFlexible Budget

Flexible budgetsFlexible budgets show the show the expected results of a expected results of a responsibility center for several responsibility center for several activity levelsactivity levels

A flexible budget is especially A flexible budget is especially useful in estimating and useful in estimating and controlling factory costs and controlling factory costs and operating expenses.operating expenses.

1212

Flexible BudgetFlexible Budget

Strength:Strength: Flexible budgeting Flexible budgeting provides information needed to provides information needed to analyze the impact of volume analyze the impact of volume changes on actual operating results.changes on actual operating results.

Weakness:Weakness: Flexible budgeting Flexible budgeting requires greater research into costs. requires greater research into costs. There must be a differentiation There must be a differentiation between fixed and variable costs.between fixed and variable costs.

1313

Types of BudgetsTypes of Budgets

Income statement budgetsIncome statement budgets– Cost of goods sold budget:Cost of goods sold budget:

Production budgetProduction budget Direct materials purchases budgetDirect materials purchases budget Direct labor cost budgetDirect labor cost budget Factory overhead cost budgetFactory overhead cost budget

– Selling and administrative expense budgetSelling and administrative expense budget

Balance sheet budgetsBalance sheet budgets– Cash budgetCash budget– Capital expenditures budgetCapital expenditures budget

1414

Types of BudgetsTypes of Budgets

1515

Sales BudgetSales Budget

The The sales budgetsales budget normally normally indicates for each productindicates for each product::

– the quantity of estimated sales and the quantity of estimated sales and – the expected unit selling price.the expected unit selling price.

1616

Sales BudgetSales Budget

1717

Production BudgetProduction Budget

The production budget sets forth the The production budget sets forth the number of units to be manufactured number of units to be manufactured to meet budgeted sales and inventory to meet budgeted sales and inventory needs for eachneeds for each..

Estimated unit salesEstimated unit sales

++Desired unit ending inventoryDesired unit ending inventory- Unit beginning inventoryUnit beginning inventory

Units to be producedUnits to be produced1818

Direct Materials Purchases BudgetDirect Materials Purchases Budget

The direct materials production budget The direct materials production budget sets forth the quantity of materials sets forth the quantity of materials needed to manufacture the units needed to manufacture the units specified by the production budget.specified by the production budget.

Materials needed for productionMaterials needed for production

++Desired ending materials inventoryDesired ending materials inventory- Beginning materials inventoryBeginning materials inventory

Materials to be purchasedMaterials to be purchased

1919

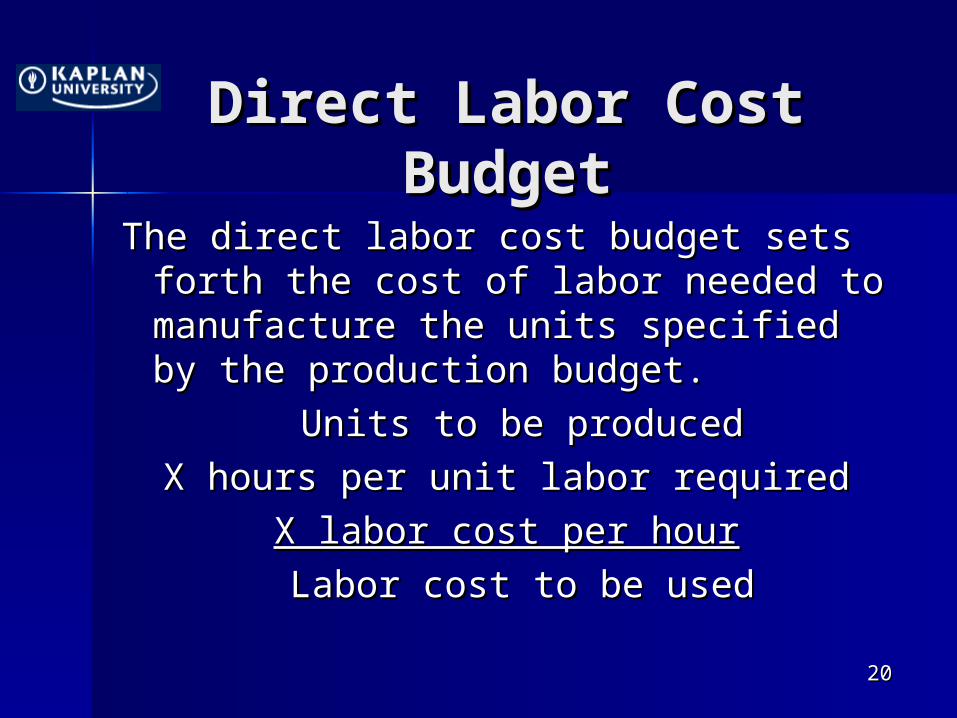

Direct Labor Cost Direct Labor Cost BudgetBudget

The direct labor cost budget sets The direct labor cost budget sets forth the cost of labor needed to forth the cost of labor needed to manufacture the units specified by manufacture the units specified by the production budget.the production budget.

Units to be producedUnits to be produced

X hours per unit labor requiredX hours per unit labor required

X labor cost per hourX labor cost per hour

Labor cost to be usedLabor cost to be used2020

Factory Overhead Cost Factory Overhead Cost BudgetBudget

The factory overhead cost budget The factory overhead cost budget details the expected overhead details the expected overhead cost to produce the quantity of cost to produce the quantity of materials needed to manufacture materials needed to manufacture the units specified by the the units specified by the production budget.production budget.

2121

Factory Overhead Cost Factory Overhead Cost BudgetBudget

2222

Cost of Goods Sold Cost of Goods Sold BudgetBudget

Beginning Inventory Beginning Inventory

Materials, WIP & finished goodsMaterials, WIP & finished goods

++Materials to be purchasedMaterials to be purchased

++Labor needed for productionLabor needed for production

+ Factory overhead budget+ Factory overhead budget

-- Ending inventory (material, WIP & Ending inventory (material, WIP & FG)FG)

Cost of Goods SoldCost of Goods Sold2323

Selling and Selling and Administrative Expense Administrative Expense

BudgetBudget

2424

Budgeted Income Budgeted Income StatementStatement

2525

Cash BudgetCash Budget

The The cash budgetcash budget is one of the is one of the most important elements of the most important elements of the budgeted balance sheet. The budgeted balance sheet. The cash budget presents the cash budget presents the expected receipts (inflows) and expected receipts (inflows) and payments (outflows) of cash for a payments (outflows) of cash for a period of time.period of time.

2626

Estimated Cash Estimated Cash ReceiptsReceipts

Estimate:Estimate:

10% of sales are cash sales10% of sales are cash sales

60% are collected within the month60% are collected within the month

30% are collected in the next month30% are collected in the next month

2727

Collected in:

Month Sales January February March April

January 1,080,000

756,000 324,000

February 1,240,000

868,000 372,000

March 970,000 679,000 291,000

Total 1,192,000 1,051,000

Estimating Cash Estimating Cash PaymentsPayments

Estimate:Estimate:

50% are made in the current month50% are made in the current month

50% are paid within the month50% are paid within the month

Note: Exclude depreciationNote: Exclude depreciation

2828

Paid in:

Month Costs January February March April

January 900,000 450,000 450,000

February 1,250,000

625,000 625,000

March 1,400,000

700,000 700,000

Total 1,075,000 1,325,000

Cash BudgetCash Budget

2929

February March

Cash in 1,192,000 1,051,000

Cash out 1,075,000 1,325,000

Cash increase (decrease) 117,000 (274,000)

Cash at beginning of month 400,000 517,000

Cash at end of month 517,000 303,000

Minimum cash balance 320,000 320,000

Excess (deficiency) 197,000 (17,000)

Example Exercise 22-6Example Exercise 22-6(page 1016)(page 1016)

Landon Awards Co. collects 25% of its Landon Awards Co. collects 25% of its sales on account in the month of sales on account in the month of the sale and 75% in the month the sale and 75% in the month following the sale. If sales on following the sale. If sales on account are budgeted to be account are budgeted to be $100,000 for March and $126,000 $100,000 for March and $126,000 for April, what are the budgeted for April, what are the budgeted cash receipts from sales on account cash receipts from sales on account for April?for April?

3030

Example Exercise 22-6Example Exercise 22-6(page 986)(page 986)

Collections from March sales Collections from March sales

(75% x $100,000)(75% x $100,000) $ 75,000$ 75,000

Collections from April sales Collections from April sales

(25% x $126,000)(25% x $126,000) 31,500 31,500

TotalTotal $106,500$106,500

3131

CapitalCapitalExpenditures BudgetExpenditures Budget

The The capital expenditures capital expenditures budgetbudget summarizes plans for summarizes plans for acquiring fixed assets.acquiring fixed assets.

3232

Budgeted Balance Budgeted Balance SheetSheet

The The budgeted balance sheetbudgeted balance sheet estimates the financial condition estimates the financial condition at the end of a budget period.at the end of a budget period.

3333

Questions?Questions?

3434

One last thought….One last thought….

Make sure you read through Make sure you read through Chapter 23 Chapter 23 beforebefore next week’s next week’s seminar.seminar.

3535