absolute and relative var of a mutual fund

TRANSCRIPT

Asset Management Group Assignment Style Analysis

Contents Indexes Selection ................................................................................................... 3

Sector Style Analysis .............................................................................................. 5

Strategic ........................................................................................................ 5

Rolling ........................................................................................................... 5

Tactical .......................................................................................................... 6

Geographic Style Analysis ...................................................................................... 7

Strategic ........................................................................................................ 7

Rolling ........................................................................................................... 8

Tactical .......................................................................................................... 9

Confidence Interval ..................................................................................... 11

Efficient Frontier ......................................................................................... 11

Appendix I: Correlation Matrix of Indexes ............................................................ 13

Group Assignment – Style Analysis The analysis carried out is grounded on the application of Sharpe's Style Analysis to the mutual fund BGF GLOBAL EQUITY FUND CLASS A2 EUR and will allow us to assess its composition relying on publicly available quotations of the fund itself obtained from the website www.blackrock.co.uk.

Indexes Selection

Since BGF GLOBAL EQUITY FUND CLASS A2 EUR is a global fund, we reckon that a proper Style Analysis should be based on both geographic areas and industry sectors rather than on specific styles. For what concerns the indexes to be used to perform the Style Analysis by Industry Sectors we have decided to include ten of them, choosing each one according to the characteristics of mutual exclusivity, exhaustivity and low level of correlation that each asset class should have. Initially, we intended to select indexes according to their average mutual correlation1, but such a method provided us with inconsistent results because many of them were not mutually exclusive. For instance, basing on this reasoning we had to include on our analysis both Pharmaceutical, Biotech, Pharma/Biotech and Healthcare together as indexes. However, Healthcare Sector already includes both Pharma and Biotech and Pharma/Biotech which of course already embeds both Biotech and Pharma. This is the list of the sectors that have been included in the analysis:

Industrials

Materials

Consumer Discretionary

Energy

IT

Consumer Staples

Health Care

Financials

Telecommunication

Utilities According to the MSCI methodology selection criteria2, these sectors are the most comprehensive ones, in the sense that each company is contained in one and only one of the above said sectors

1 See Appendix I.

2 MSCI Global Investable Market Indexes Methodology. MSCI Index Research, pp. 98-106 (Appendix V: Global Industry

Classification Standard), November 2014.

Referring to the indexes to be used to carry out the Style Analysis by geographic areas, we have decided to include seven of them with the aim of selecting all possible geographic areas. Thus, we opted to take into account:

MSCI Emerging Markets Asia

MSCI Pacific

MSCI Europe

MSCI North America

MSCI Emerging Markets America Latina

MSCI Emerging Markets EMEA

In this way, we covered both North America and Latin America, as well as all European countries

(not only nations whose currency is Euro, but also States like Switzerland and UK which are not

comprised in indexes like MSCI EMU). Exposure to Europe, Middle East and Africa was guaranteed

by MSCI Emerging Markets EMEA. We covered the Asian world by using just two indexes: MSCI

Pacific which contains developed countries such as Australia, Hong Kong and Japan and MSCI

Emerging Market Asia which is made up of the emerging countries Korea, Taiwan, China, India. To

sum up, we had a complete coverage of the countries of the 5 continents by considering just 6

indexes. Furthermore, we decided to consider also the amount of money that the fund keeps in

cash by using a monetary market fund. In particular, we selected JPM Global 3M as a proxy for

cash.

The analysis does not change that much by including cash or not. Tactical and Strategic Style

Analysis yield the same results, thus showing that no cash is held by the fund. Rolling Style Analysis

reveals to us that a constant proportion equal to 1.6% is kept in cash. The fact that the figure is

constant over time may seem odd, but there is no reason to exclude the fact that Blackrock

manager’s systematically keep a portion of the fund invested in cash to satisfy redemption needs.

Blackrock itself discloses that roughly 4% of assets are put in cash.

We also considered alternative combinations of index. We thought about splitting up MSCI North

America into MSCI USA and MSCI Canada, which are the only two constituents of the first

mentioned index. Plus, we had intention to cover Europe by using two variables: MSCI Europe ex

UK and MSCI UK. At first sight, such a combination appeared to us more sensible because it allows

to clearly identify the weights of the countries in which the fund allocates a big share (54% in USA

and 7% in UK), while isolating the contribution of other countries of lower importance together.

When we ran the analysis, we saw that it produced unreasonable results3 . This is probably due to

the fact that the system is not able to distinguish UK from rest of Europe, thus returning an

abnormally low result for UK.

Furthermore, as there are some variables with zero-weight, we considered the possibility just to

use 4 indexes: Europe, North America, Pacific and Emerging Markets. In this case, the R-squared

appeared to be quite low (70%), so we dropped this model.

3 Namely, only 1% invested in UK when the actual percentage is instead 7%.

Sector Style Analysis

Strategic The Strategic Style Analysis is implemented by using 60 months of data. As it is possible to see in the graph below, almost half of the total allocation appears to have been assigned to Consumer Discretionary. Furthermore, Materials, Industrials and Energy hold a significant portion of the portfolio: the allocation relative to these ones is respectively 22,5%, 7,1% and 4,1%. However, no shares have been allocated to IT, Telecommunications and Utilities. The R-squared achieved by this approach is quite satisfying, as it is 80,31%.

Rolling It is helpful to examine the behavior of a manager's average exposure to asset classes by implementing a Time Series Analysis, by the use of a fixed number of periods for each one through time. To do so, we performed a Rolling Style Analysis, which iterates through the multivariate regression model in a series of continuous time windows, each of them with a fixed number of observations. In our analysis, we used a rolling window of 36 weeks, which is updated for 24 periods. As it is plainly evident, there is a significant allocation to Consumer Discretionary. However, in recent months we witness a pattern reversion, as the fund managers suddenly decided to disinvest from the index. The same thing happened to MSCI World Materials and MSCI World Industrials. Correspondingly, managers tended to increase the weights given to new indexes such as MSCI World Energy and MSCI World Utilities. It appears that there has been a lot of activism of asset managers. This could be partly explained by the fact that managers in charge of the fund changed frequently. The R-squared of the Rolling Style Analysis rarely falls below 80%. This is a good result, since it means that the model explains most of the variability of the independent variable.

7,1%

22,5%

4,1%

54,2%

2,9% 5,9%

3,4% 0,0% 0,0% 0,0%

Energy Materials Industrials Cons.Discr.

Cons.Staples

HealthCare

Financials IT TLC Utilities

0,0%

10,0%

20,0%

30,0%

40,0%

50,0%

60,0%

Strategic Style Analysis

Tactical If the main goal is to monitor the more recent situation, the Tactical Style Analysis perfectly matches such objective. This method is implemented by using the last 52 weeks of data. It is possible to notice that on the one hand, the fund managers fully disinvested from Financials, Chemicals and Infrastructure while on the other hand, they greatly rose the share invested in new sectors such as Industrials, Materials and Energy. Their weights respectively increased to 25,4%, 23,9% and 10%. The graph below also confirms what has been demonstrated in the previous Rolling Window Analysis, that is the downward trend of the weight given to Consumer Discretionary, which

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Rolling Style Analysis

MSCI World Utilities

MSCI World Telecomunications

MSCI World IT

MSCI World Financials

MSCI World Health Care

MSCI World Cons. Staples

MSCI World Cons. Discr.

MSCI World Industrials

MSCI World Materials

MSCI World Energy

0,00%

20,00%

40,00%

60,00%

80,00%

100,00%

31-Oct-2012 31-Mar-2013 31-Aug-2013 31-Jan-2014 30-Jun-2014

Style R2

dropped to 16,5%. The Tactical Style Analysis shows an acceptable value of the R-squared, 78,92%.

Geographic Style Analysis

Strategic

The Strategic Style Analysis is carried out by using 60 months. The R-squared obtained with such a

method is equal to 79.74%. We deem that such a value is rather acceptable since it is close to 80%.

10,0%

23,9% 25,4%

16,5%

10,4%

3,0%

0,0%

10,9%

0,0% 0,0% 0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

30,0%

Tactical Style Analysis

0,0%

28,3%

0,0%

5,8%

25,2%

40,7%

0,0% 0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

30,0%

35,0%

40,0%

45,0%

EM LatAm EM Asia Pacific EM EMEA Europe North Am Cash

Strategic Style Analysis

The allocation to Developed Countries is equal to 65.9%, although this figure has changed

significantly over time4. For what concerns Emerging Markets, the fund seems to invest largely in

Asian Developing Countries (28.3%), while only a marginal quantity of assets is allocated in EMEA

Emerging Countries (5,8%).

Rolling

The Rolling Style Analysis is performed by using a rolling window made up of 36 weeks which is

updated for 24 periods. This technique allows us to have an indication of how the managers

changed the allocation to each geographic area.

A pattern clearly emerges from the Rolling Style Analysis: the fund managers progressively

disinvested from Emerging Markets like EMEA and America Latina. They also took money out of

Asia-Pacific area. Symmetrically, they increased the share invested in North America and only very

recently they have allocated more money to Asian Emerging Countries.

The overall picture we got from this analysis is that the managers invested more in Developed

Economies and at the same time shrank the weight given to Developing Countries.

As a matter of fact, the share allotted to Europe and North America in September 2012 was equal

to 40%, even if such an allocation reached 70% two years later. Of course, this consideration is a

clear evidence of the level of activism of the fund. A point which may seem odd is the straight line

in the top part of the chart that shows us that the share invested in cash is literally always

4 See next paragraph.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Rolling Style Analysis

JPM Global 3 mesi

MSCI Nord America

MSCI Europa

MSCI Emerging Market EMEA

MSCI Pacifico Free

MSCI Emerging Market Free Asia

MSCI Emerging Market Free AmericaLatina

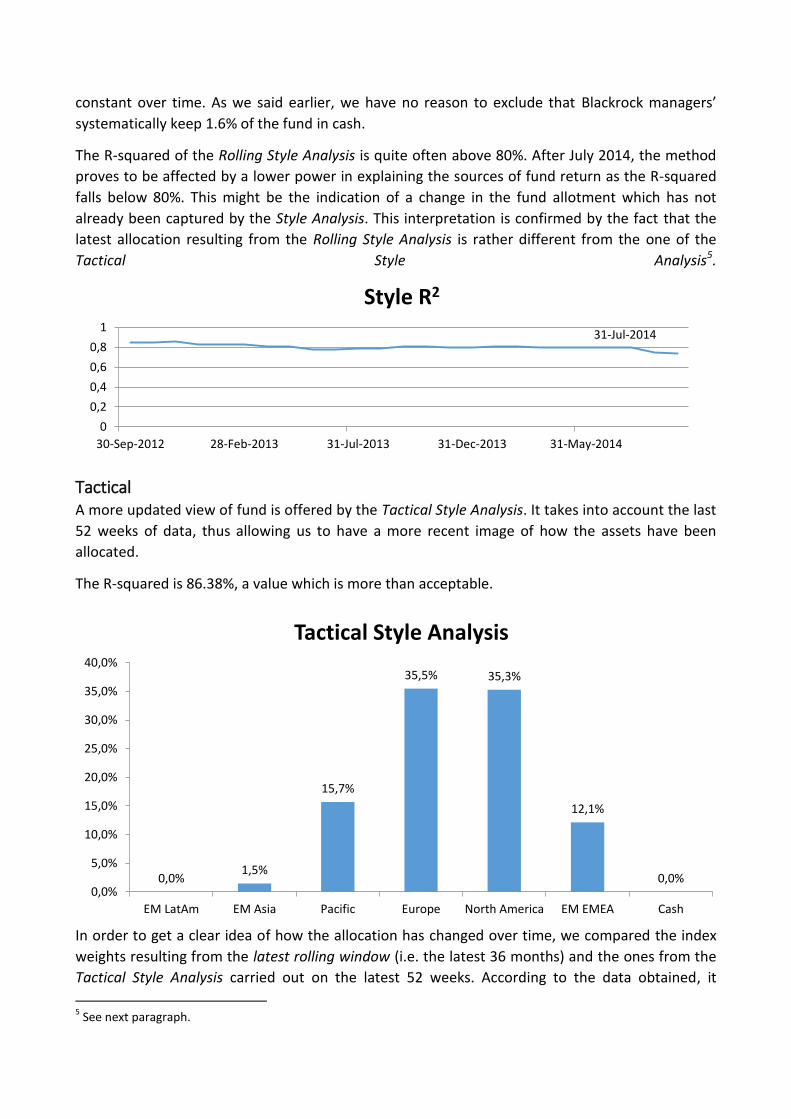

constant over time. As we said earlier, we have no reason to exclude that Blackrock managers’

systematically keep 1.6% of the fund in cash.

The R-squared of the Rolling Style Analysis is quite often above 80%. After July 2014, the method

proves to be affected by a lower power in explaining the sources of fund return as the R-squared

falls below 80%. This might be the indication of a change in the fund allotment which has not

already been captured by the Style Analysis. This interpretation is confirmed by the fact that the

latest allocation resulting from the Rolling Style Analysis is rather different from the one of the

Tactical Style Analysis5.

Tactical A more updated view of fund is offered by the Tactical Style Analysis. It takes into account the last

52 weeks of data, thus allowing us to have a more recent image of how the assets have been

allocated.

The R-squared is 86.38%, a value which is more than acceptable.

In order to get a clear idea of how the allocation has changed over time, we compared the index

weights resulting from the latest rolling window (i.e. the latest 36 months) and the ones from the

Tactical Style Analysis carried out on the latest 52 weeks. According to the data obtained, it

5 See next paragraph.

31-Jul-2014

0

0,2

0,4

0,6

0,8

1

30-Sep-2012 28-Feb-2013 31-Jul-2013 31-Dec-2013 31-May-2014

Style R2

0,0% 1,5%

15,7%

35,5% 35,3%

12,1%

0,0% 0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

30,0%

35,0%

40,0%

EM LatAm EM Asia Pacific Europe North America EM EMEA Cash

Tactical Style Analysis

appears that the asset managers overweighed Europe and underweighted North America.

Surprisingly, the weight assigned to Asian Emerging Countries dropped sharply from 25% to 1.5%.

At the same time, the fund exhibits a stake which goes from zero to a not negligible figure for

many indexes. This is the case for Pacific (from 0% to 15.7%) and for EM EMEA (from 0% to 12.1%).

The point is: did the allocation really swing so dramatically or is there any kind of estimation error?

In order to answer to this question, we compared the figures we got from our analysis with the

numbers officially published by Blackrock. We realized that the latest rolling style analysis gives us

results which are closer to the ones given by the management company, while the percentages

obtained through the Tactical Analysis seem to be more weird than before. For example, we have

55% of allocation to North America according to Blackrock and 51% according to the Rolling Style

Analysis, then we have 22% allocated to Europe versus 20% resulting from our analysis. The

Rolling Style Analysis appears to fail in distinguishing allocations of emerging countries, but it looks

like that the picture we had from the Rolling Style is more sensitive than the one we got from the

Tactical Analysis.

0

0,1

0,2

0,3

0,4

0,5

0,6

EM LatAm EM Asia Pacific Europe North America EM EMEA Cash

How the allocation has changed over time

First Rolling (36 Months) Latest Rolling (36 Months) Tactical (52 Weeks)

Confidence Interval

Weights 1_EM America Latina 2_EM Asia 3_Pacifico

4_EM EMEA 5_Europa

6_Nord America

1_EM America Latina 26,4% -6,1% 42,7% -6,5% 11,1%

2_EM Asia 42,3% 27,4% 25,6% 7,9% 17,6%

3_Pacifico -9,0% 25,0% 11,3% 12,3% 44,4%

4_EM EMEA 56,0% 20,9% 10,2% 35,4% -14,1%

5_Europa -9,7% 7,3% 12,6% 40,2% 41,0%

6_Nord America 20,3% 20,3% 56,0% -19,8% 50,8%

Sum of weights 100,0% 100,0% 100,0% 100,0% 100,0% 100,0%

R-squared 68% 65% 46% 71% 54% 47%

Confidence Interval 7,06% 8,93% 8,53% 8,07% 8,60% 9,57%

We adopted Lobosco and Di Bartolomeo’s procedure as a tool to test the goodness of our index

choice. The procedure outlined by the two authors envisages regressions of each index on the

others to discover, for each variable, the amount of information which is already contained in the

remaining indexes. This implies that the factors presenting a high level of R-squared have a

volatility well explained by the ones of the others. This means that such indexes do not add any

information to the dependent variable so they are supposed to be dropped.

Furthermore, Lobosco and Di Bartolomeo’s methodology allows to come up with confidence

intervals for the weights obtained in the Strategic Style Analysis. There is no need to say that the

lower the confidence interval, the better is the index choice.

Some regressions show a high R-squared (60/70%). This cannot be due to a geographic overlap, as

we have accurately avoided it during the preliminary selection of the factors. The most likely

reason is that there is a sort of Sector-Overlapping, namely that the indexes have exposure the

same industry sector.

On the contrary, the Confidence Interval is always low as it never exceeds 10%. This result confirms

the high accuracy of the chosen indexes .

Efficient Frontier Rather than using just 10 portfolios, which would have produced an unreadable chart, we took

into account 10 portfolios by equally spacing the returns from the minimum index to the maximum

index (as asked by the assignment), plus 5 portfolios with equally spacing returns from 0.19% to

0.13% in order to display better the inefficient part of the frontier. Of course, we plotted the fund

portfolio (the violet dot), the minimum variance portfolio (in green) and the benchmark portfolio

resulting from the Style Analysis (in brown). We also charted the indexes used for the

Geographical Style Analysis. Since the minimum variance portfolio is almost only invested in cash,

we decided to calculate also the minimum variance portfolio excluding cash (red dot). This last

portfolio lays on the inefficient area of the risk-return chart: this means that the use of cash allows

to enhance the risk-return profile with respect to only equity portfolios

.As it is possible to see the fund does not lie on the

efficient frontier, although it has been able to

generate higher returns with lower volatility with

respect to 4 indexes. The fund is dominated by the

benchmark obtained thanks to the Style Analysis and

by MSCI North America, which is the only portfolio to

be on the efficient frontier. On the other side, MSCI

Emerging Markets Latin America has been the worst

index, as it is aligned on the inefficient frontier.

Overall, it seems that the fund managers provided a

modest risk-adjusted return. This is also confirmed by

the t-test we performed against the MSCI World used

as benchmark. We hypothesized a difference in the

average returns equal to zero and the test failed to reject the null hypothesis. This is equivalent to

say that there is no sufficient statistical evidence to claim that the fund provided better returns

with respect to the benchmark.

0,13%

0,26%

0,39%

0,52%

0,64%

0,77%

0,90%

1,03%

1,15%

North America

MV 0,14%

0,15% 0,16% 0,17% 0,18%

Benchmark

Fund

EM LatAm

EM Asia

Pacific

EM EMEA

Europe

1,28%

Cash

MVadj

0,00%

0,20%

0,40%

0,60%

0,80%

1,00%

1,20%

1,40%

0,00% 1,00% 2,00% 3,00% 4,00% 5,00% 6,00%

Exp

ect

ed

Re

turn

Standard Deviation

Efficient Frontier

Test t:two samples with different variances

MSCI World BGF

Mean 0,0095 0,0079

Variance 0,0007 0,0012

# Obs 60 60

Difference 0 gdl 112 Stat t 0,3009

Appendix I: Correlation Matrix of Indexes