about color themes choose the appropriate design theme for your presentation. the first two options...

TRANSCRIPT

The Philanthropy Conference:EY GibraltarHow is the asset management industry catering for investors wanting sustainable returns from ethical investments?

Gillian Lofts

17 November 2013

The Philanthropy Conference: EY Gibraltar

Introduction

Page 2

We will cover :

► The current trends of the asset management industry and their impact on the sustainable and ethical investment world

► The significant growth of ethical investing and who is saying what about it

► The root causes of this sector’s emergence and exponential growth rates

► How it is being manifested day-to-day and what the future holds

Investor demand for sustainable

and ethical products has grown

significantly in the last two

decades. This presentation

analyses the change in demand

of the investor and the response

by the industry

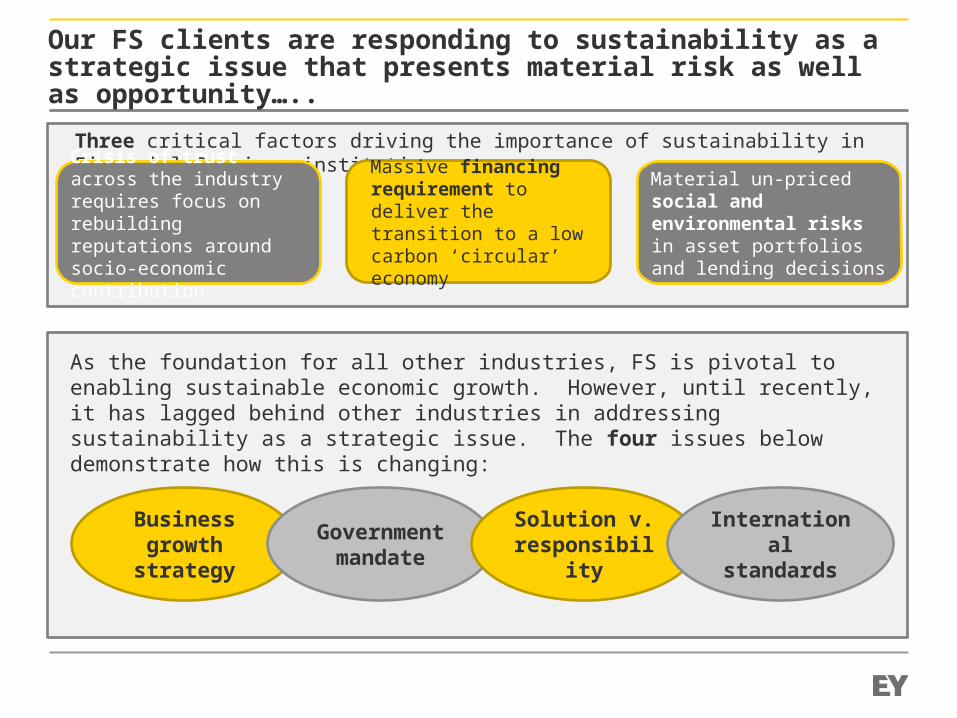

Our FS clients are responding to sustainability as a strategic issue that presents material risk as well as opportunity…..

As the foundation for all other industries, FS is pivotal to enabling sustainable economic growth. However, until recently, it has lagged behind other industries in addressing sustainability as a strategic issue. The four issues below demonstrate how this is changing:

Three critical factors driving the importance of sustainability in Financial Services institutions:

Massive financing requirement to deliver the transition to a low carbon ‘circular’ economy

Crisis of trust across the industry requires focus on rebuilding reputations around socio-economic contribution

Material un-priced social and environmental risks in asset portfolios and lending decisions

Business growth

strategy

Government mandate

Solution v. responsibility

International standards

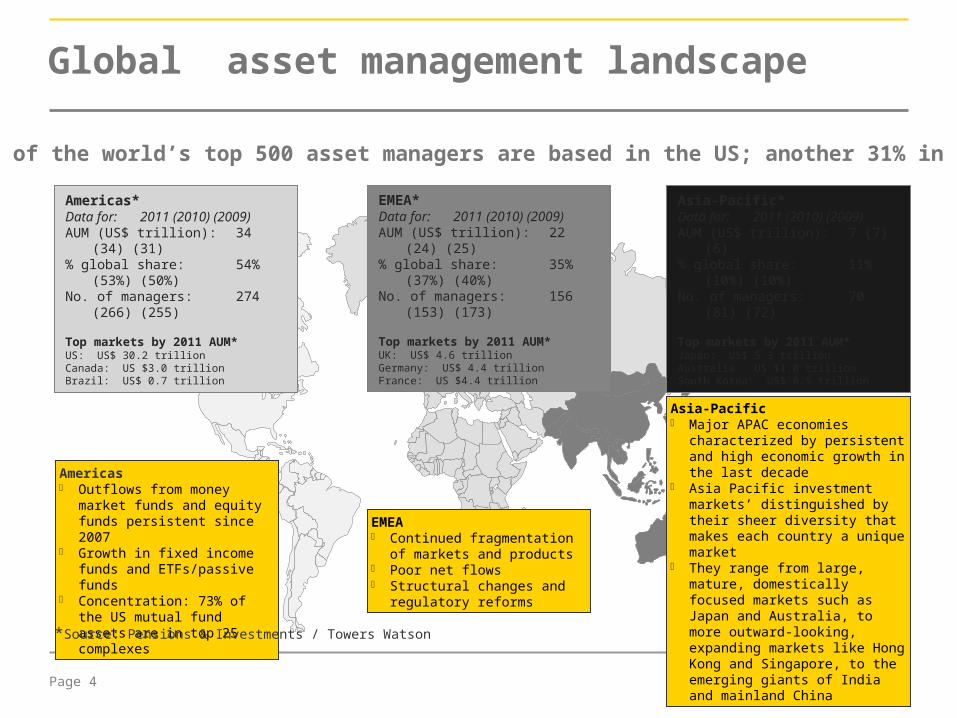

Global asset management landscape

Page 4

Americas*Data for: 2011 (2010)

(2009)AUM (US$ trillion): 34 (34) (31)% global share: 54% (53%)

(50%) No. of managers: 274 (266) (255)

Top markets by 2011 AUM*US: US$ 30.2 trillionCanada: US $3.0 trillionBrazil: US$ 0.7 trillion

EMEA*Data for: 2011 (2010)

(2009)AUM (US$ trillion): 22 (24) (25)% global share: 35% (37%)

(40%)No. of managers: 156 (153) (173)

Top markets by 2011 AUM*UK: US$ 4.6 trillionGermany: US$ 4.4 trillionFrance: US $4.4 trillion

Asia-Pacific*Data for: 2011 (2010)

(2009)AUM (US$ trillion): 7 (7) (6)% global share: 11% (10%)

(10%)No. of managers: 70 (81) (72)

Top markets by 2011 AUM*Japan: US$ 5.3 trillionAustralia: US $1.0 trillionSouth Korea: US$ 0.5 trillion

Americas Outflows from money market

funds and equity funds persistent since 2007

Growth in fixed income funds and ETFs/passive funds

Concentration: 73% of the US mutual fund assets are in top 25 complexes

EMEA Continued fragmentation of

markets and products Poor net flows Structural changes and

regulatory reforms

Asia-Pacific Major APAC economies

characterized by persistent and high economic growth in the last decade

Asia Pacific investment markets’ distinguished by their sheer diversity that makes each country a unique market

They range from large, mature, domestically focused markets such as Japan and Australia, to more outward-looking, expanding markets like Hong Kong and Singapore, to the emerging giants of India and mainland China

55% of the world’s top 500 asset managers are based in the US; another 31% in Europe

*Source: Pensions & Investments / Towers Watson

EMEIA FSO – Asset Management Update

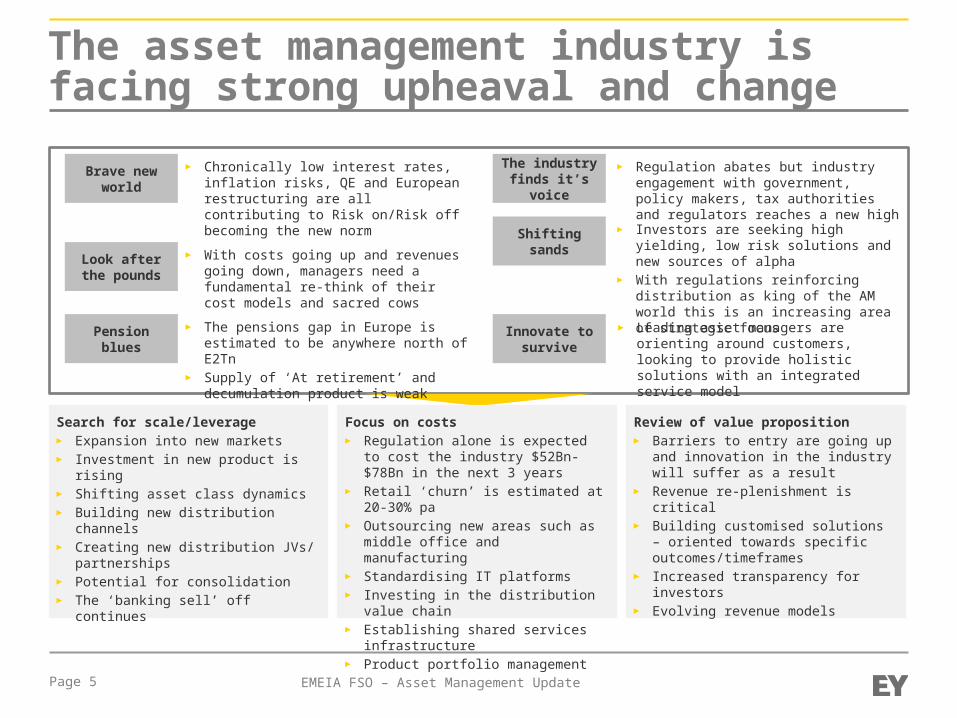

The asset management industry is facing strong upheaval and change

Page 5

Brave new world

► Chronically low interest rates, inflation risks, QE and European restructuring are all contributing to Risk on/Risk off becoming the new norm

The industry finds it’s voice

► Regulation abates but industry engagement with government, policy makers, tax authorities and regulators reaches a new high

Look after the pounds

► With costs going up and revenues going down, managers need a fundamental re-think of their cost models and sacred cows

Search for scale/leverage► Expansion into new markets ► Investment in new product is rising► Shifting asset class dynamics► Building new distribution channels► Creating new distribution JVs/

partnerships ► Potential for consolidation► The ‘banking sell’ off continues

Focus on costs► Regulation alone is expected to cost the

industry $52Bn-$78Bn in the next 3 years► Retail ‘churn’ is estimated at 20-30% pa► Outsourcing new areas such as middle

office and manufacturing► Standardising IT platforms► Investing in the distribution value chain► Establishing shared services

infrastructure► Product portfolio management

Review of value proposition► Barriers to entry are going up and

innovation in the industry will suffer as a result

► Revenue re-plenishment is critical► Building customised solutions – oriented

towards specific outcomes/timeframes► Increased transparency for investors► Evolving revenue models

Shifting sands► Investors are seeking high yielding, low risk

solutions and new sources of alpha► With regulations reinforcing distribution as

king of the AM world this is an increasing area of strategic focus

Pension blues► The pensions gap in Europe is estimated to

be anywhere north of E2Tn► Supply of ‘At retirement’ and decumulation

product is weak

Innovate to survive

► Leading asset managers are orienting around customers, looking to provide holistic solutions with an integrated service model

The Philanthropy Conference: EY Gibraltar

Overview

How has the asset management industry responded to consumer demand for sustainable and ethical investment products?

Page 6

What? Why? How?

Therefore …

The Philanthropy Conference: EY Gibraltar

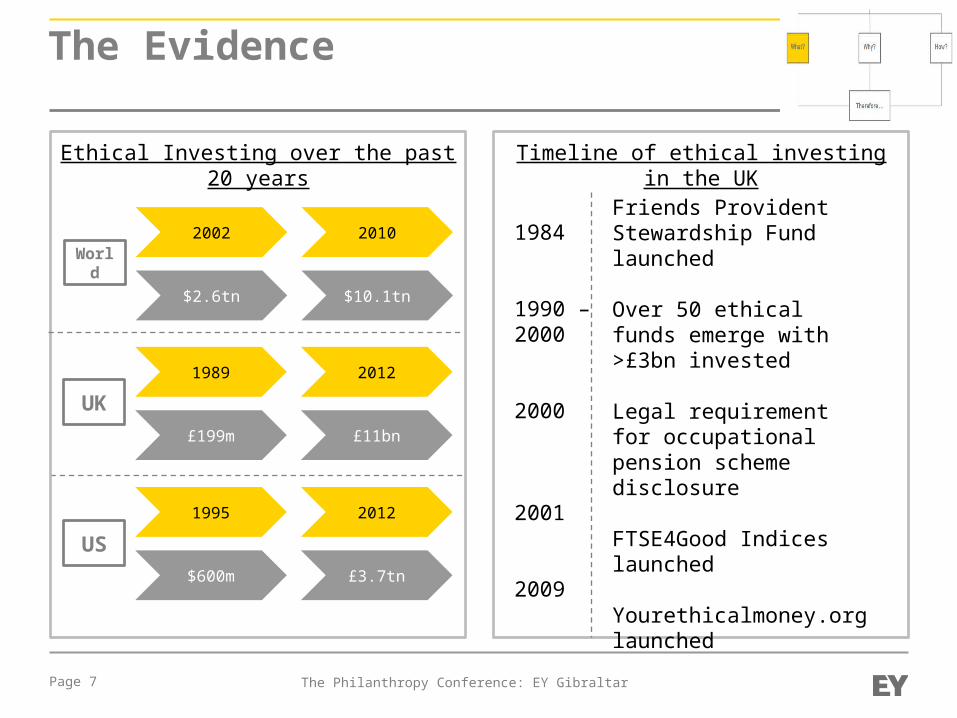

The Evidence

Page 7

UK

US

1989

£199m

1995

$600m

2012

£11bn

2012

£3.7tn

Ethical Investing over the past 20 years Timeline of ethical investing in the UK

1984

1990 – 2000

2000

2001

2009

Friends Provident Stewardship Fund launched

Over 50 ethical funds emerge with >£3bn invested

Legal requirement for occupational pension scheme disclosure

FTSE4Good Indices launched

Yourethicalmoney.org launched

World

2010

$10.1tn

2002

$2.6tn

The Philanthropy Conference: EY Gibraltar

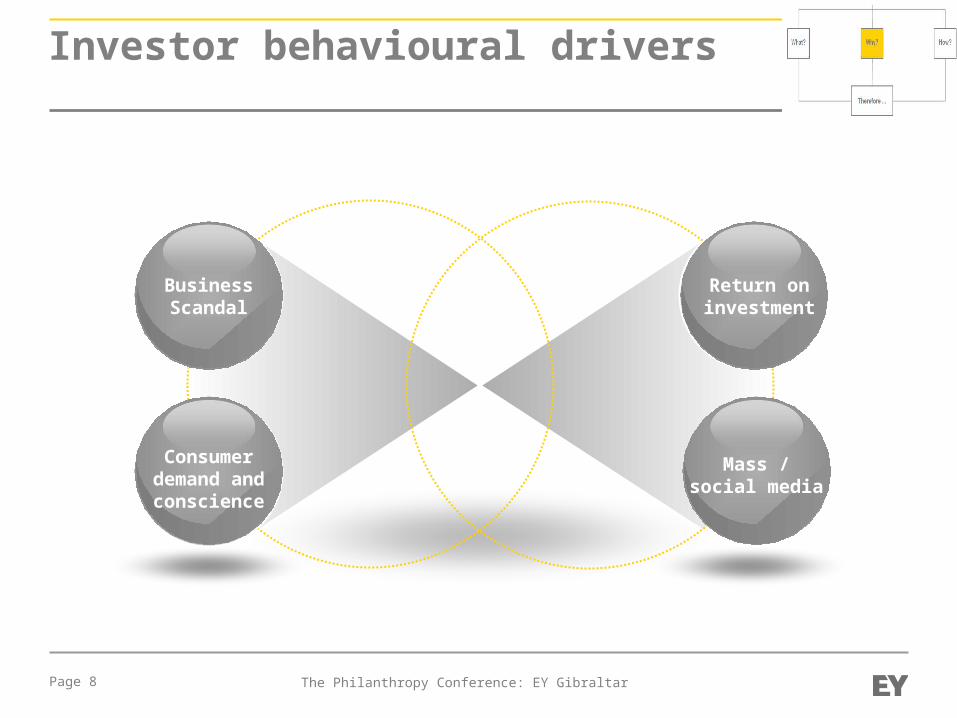

Investor behavioural drivers

Page 8

Building a better working

world

Consumer demand and conscience

Business Scandal

Return on investment

Mass / social media

The Philanthropy Conference: EY Gibraltar

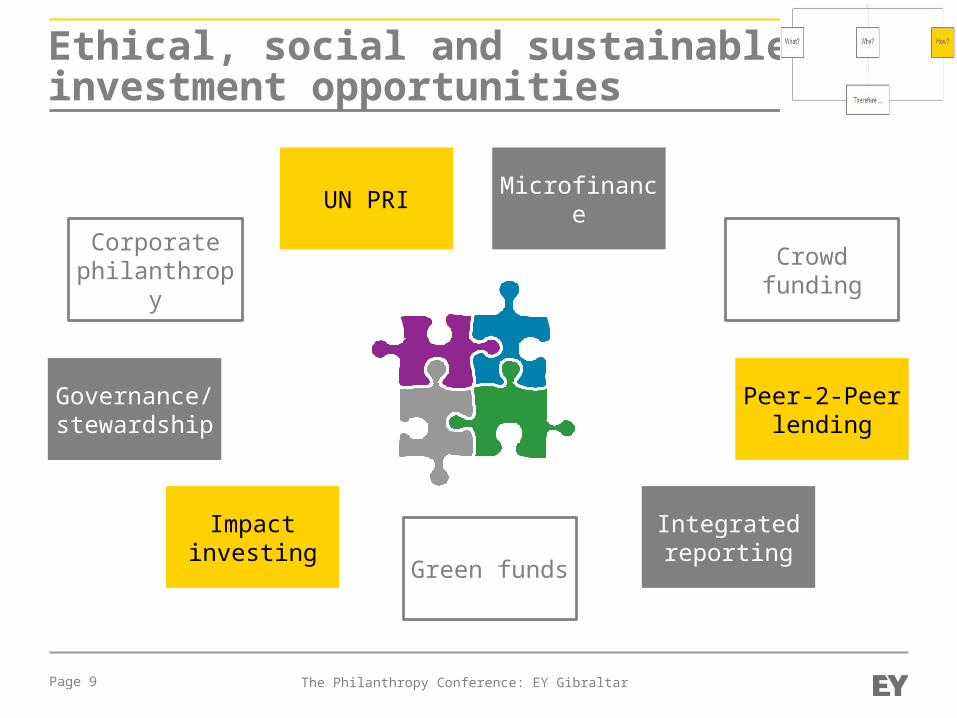

Ethical, social and sustainable investment opportunities

Page 9

Crowd funding

Microfinance

Governance/stewardship

Peer-2-Peer lending

Green funds

Integrated reporting

Impact investing

UN PRI

Corporate philanthropy

The Philanthropy Conference: EY Gibraltar

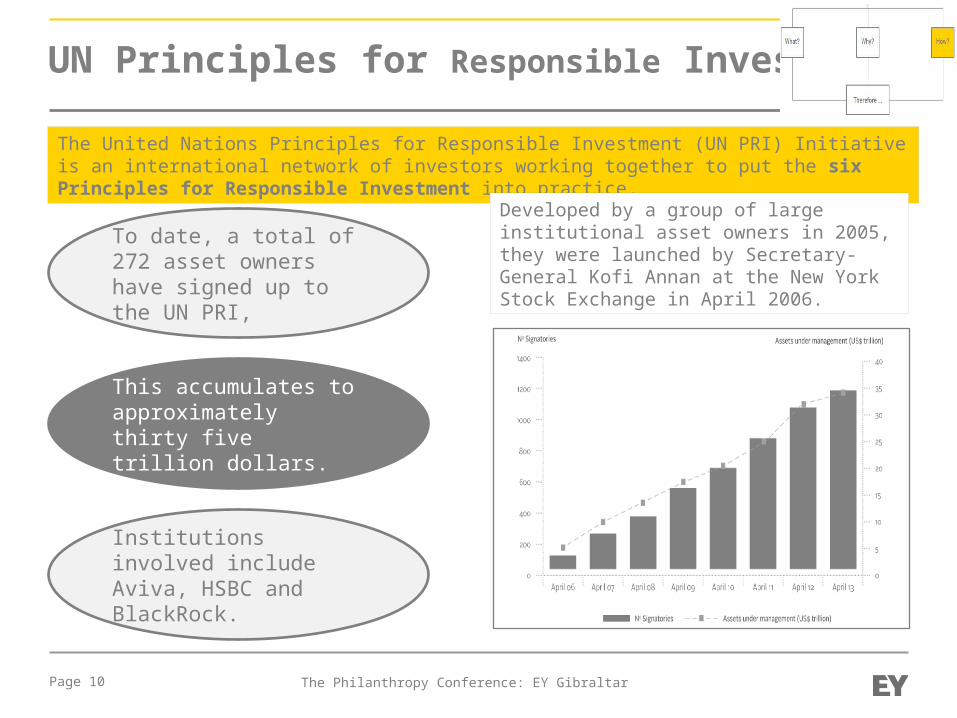

UN Principles for Responsible Investing

Page 10

The United Nations Principles for Responsible Investment (UN PRI) Initiative is an international network of investors working together to put the six Principles for Responsible Investment into practice.

To date, a total of 272 asset owners have signed up to the UN PRI,

This accumulates to approximately thirty five trillion dollars.

Institutions involved include Aviva, HSBC and BlackRock.

Developed by a group of large institutional asset owners in 2005, they were launched by Secretary-General Kofi Annan at the New York Stock Exchange in April 2006.

The Philanthropy Conference: EY Gibraltar

Innovative financial industries

Page 11

Microfinance

Kiva

Crowd funding

UK Crowdfunding Association

The Philanthropy Conference: EY Gibraltar

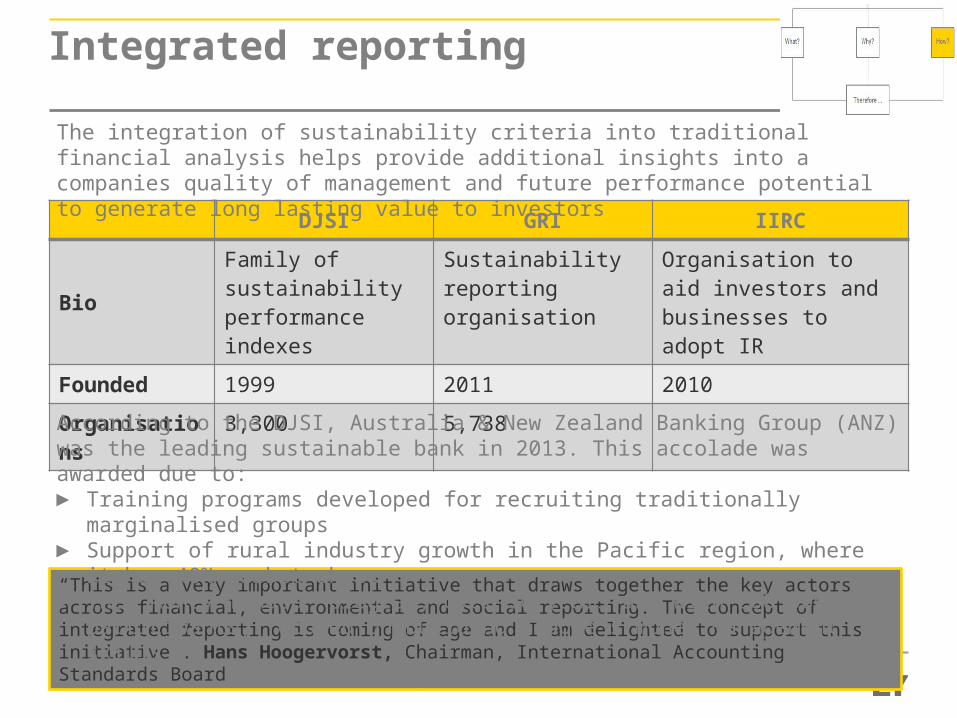

Integrated reporting

DJSI GRI IIRC

BioFamily of sustainability performance indexes

Sustainability reporting organisation

Organisation to aid investors and businesses to adopt IR

Founded 1999 2011 2010

Organisations 3,300 5,738

Page 12

“This is a very important initiative that draws together the key actors across financial, environmental and social reporting. The concept of integrated reporting is coming of age and I am delighted to support this initiative”. Hans Hoogervorst, Chairman, International Accounting Standards Board

The integration of sustainability criteria into traditional financial analysis helps provide additional insights into a companies quality of management and future performance potential to generate long lasting value to investors

According to the DJSI, Australia & New Zealand Banking Group (ANZ) was the leading sustainable bank in 2013. This accolade was awarded due to:► Training programs developed for recruiting traditionally marginalised groups► Support of rural industry growth in the Pacific region, where it has 40% market share► The ‘money minded’ program, over 10 years and with 200,000 participants, focused

on building people’s money management skills

The Philanthropy Conference: EY Gibraltar

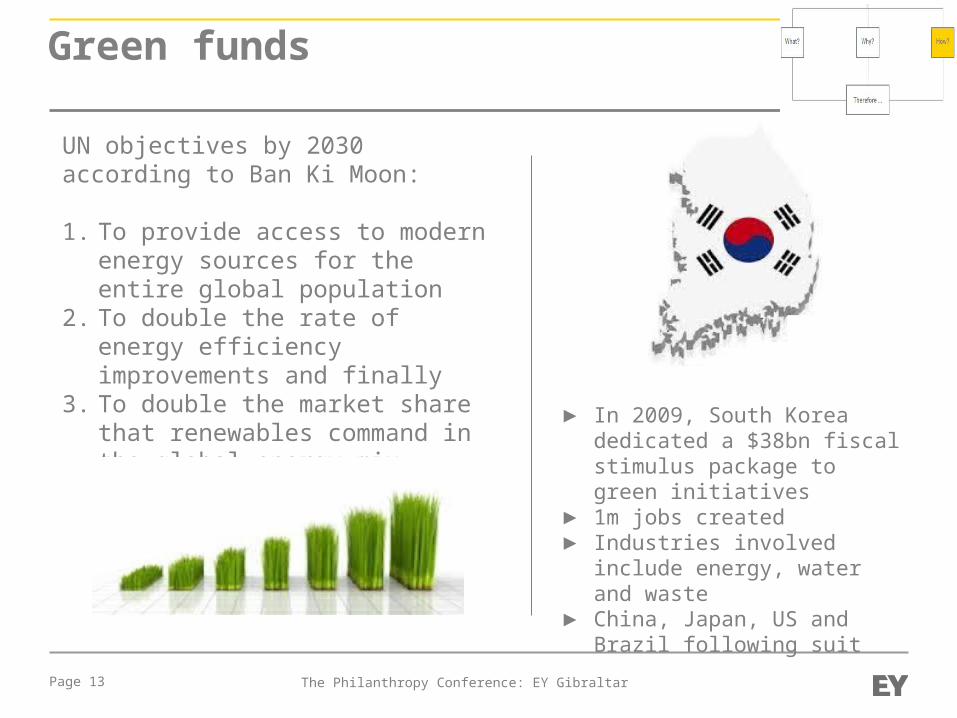

Green funds

Page 13

► In 2009, South Korea dedicated a $38bn fiscal stimulus package to green initiatives

► 1m jobs created► Industries involved include

energy, water and waste► China, Japan, US and Brazil

following suit

UN objectives by 2030 according to Ban Ki Moon:

1. To provide access to modern energy sources for the entire global population

2. To double the rate of energy efficiency improvements and finally

3. To double the market share that renewables command in the global energy mix.

The Philanthropy Conference: EY Gibraltar

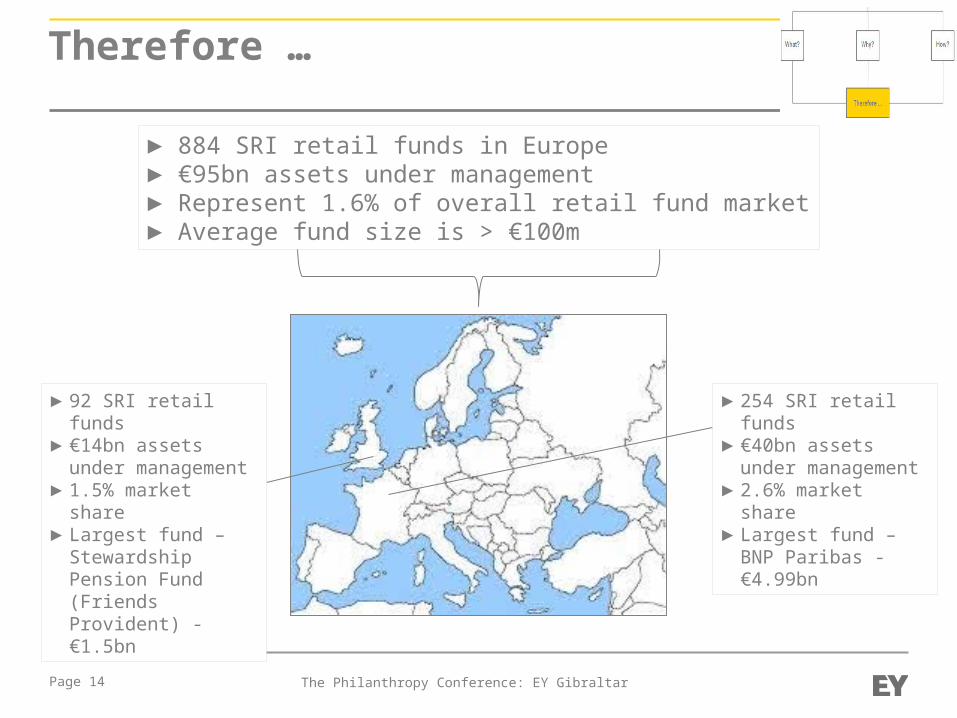

Therefore …

Page 14

►92 SRI retail funds►€14bn assets under

management►1.5% market share►Largest fund –

Stewardship Pension Fund (Friends Provident) - €1.5bn

►254 SRI retail funds►€40bn assets under

management►2.6% market share►Largest fund – BNP

Paribas - €4.99bn

► 884 SRI retail funds in Europe► €95bn assets under management► Represent 1.6% of overall retail fund market► Average fund size is > €100m

The Philanthropy Conference: EY Gibraltar

Therefore …

“We contribute to society because we are successful”(Giving something back)

Page 15

“We are successful because we

contribute to society”

(Creating shared value)

Thank you