abn amro investor day...it matters and efficiency everywhere else drive the sustainable agenda to...

TRANSCRIPT

ABN AMRO Investor Day

ABN AMRO Investor Day

London, 16 November 2018

2

For the purposes of this disclaimer ABN AMRO

Group N.V. and its consolidated subsidiaries are

referred to as "ABN AMRO“. This document (the

“Presentation”) has been prepared by ABN

AMRO. For purposes of this notice, the

Presentation shall include any document that

follows and relates to any oral briefings by ABN

AMRO and any question-and-answer session

that follows such briefings. The Presentation is

informative in nature and is solely intended to

provide financial and general information about

ABN AMRO. This Presentation has been

prepared with care and must be read in

connection with the relevant Financial

Documents (latest Quarterly Report and Annual

Financial Statements, "Financial Documents").

In case of any difference between the Financial

Documents and this Presentation the Financial

Documents are leading. The Presentation does

not constitute an offer of securities or a

solicitation to make such an offer, and may not

be used for such purposes, in any jurisdiction

(including the member states of the European

Union and the United States) nor does it

constitute investment advice or an investment

recommendation in respect of any financial

instrument. Any securities referred to in the

Presentation have not been and will not be

registered under the US Securities Act of 1933.

The information in the Presentation is, unless

expressly stated otherwise, not intended for

residents of the United States or any "U.S.

person" (as defined in Regulation S of the US

Securities Act 1933). No reliance may be placed

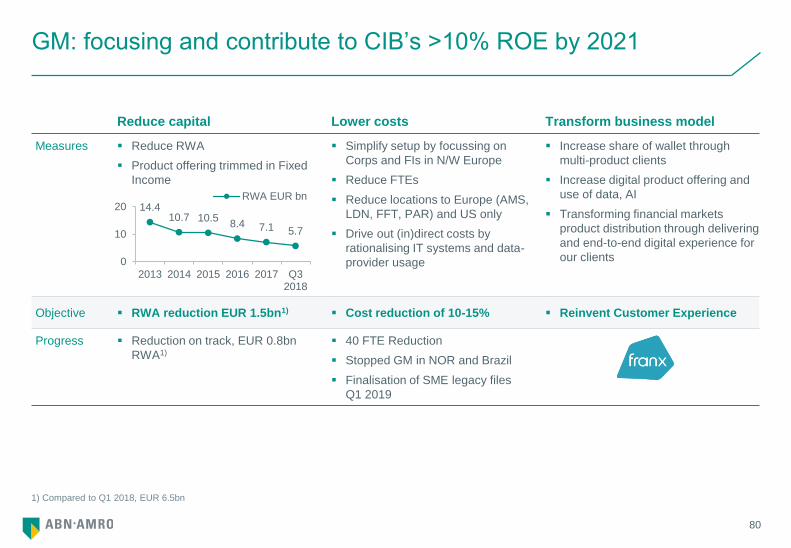

on the information contained in the Presentation.

No representation or warranty, express or

implied, is given by or on behalf of ABN AMRO,

or any of its directors or employees as to the

accuracy or completeness of the information

contained in the Presentation. ABN AMRO

accepts no liability for any loss arising, directly

or indirectly, from the use of such information.

Nothing contained herein shall form the basis of

any commitment whatsoever. ABN AMRO has

included in this Presentation, and from time to

time may make certain statements in its public

statements that may constitute “forward-looking

statements”. This includes, without limitation,

such statements that include the words ‘expect’,

‘estimate’, ‘project’, ‘anticipate’, ‘should’, ‘intend’,

‘plan’, ‘probability’, ‘risk’, ‘Value-at-Risk (“VaR”)’,

‘target’, ‘goal’, ‘objective’, ‘will’, ‘endeavour’,

‘outlook’, 'optimistic', 'prospects' and similar

expressions or variations on such expressions.

In particular, the Presentation may include

forward-looking statements relating but not

limited to ABN AMRO’s potential exposures to

various types of operational, credit and market

risk. Such statements are subject to

uncertainties. Forward-looking statements are

not historical facts and represent only ABN

AMRO's current views and assumptions on

future events, many of which, by their nature,

are inherently uncertain and beyond our control.

Factors that could cause actual results to differ

materially from those anticipated by forward-

looking statements include, but are not limited

to, (macro)-economic, demographic and political

conditions and risks, actions taken and policies

applied by governments and their agencies,

financial regulators and private organisations

(including credit rating agencies), market

conditions and turbulence in financial and other

markets, and the success of ABN AMRO in

managing the risks involved in the foregoing.

Any forward-looking statements made by ABN

AMRO are current views as at the date they are

made. Subject to statutory obligations, ABN

AMRO does not intend to publicly update or

revise forward-looking statements to reflect

events or circumstances after the date the

statements were made, and ABN AMRO

assumes no obligation to do so.

Disclaimer

3

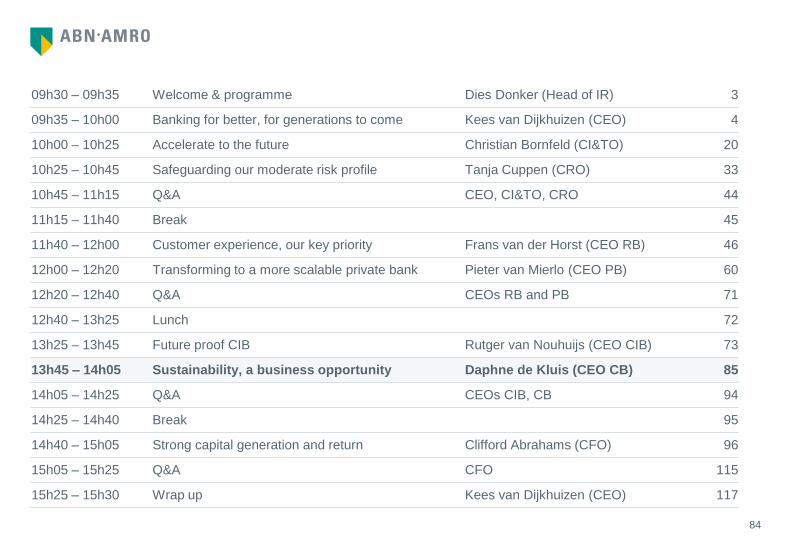

09h30 – 09h35 Welcome & programme Dies Donker (Head of IR) 3

09h35 – 10h00 Banking for better, for generations to come Kees van Dijkhuizen (CEO) 4

10h00 – 10h25 Accelerate to the future Christian Bornfeld (CI&TO) 20

10h25 – 10h45 Safeguarding our moderate risk profile Tanja Cuppen (CRO) 33

10h45 – 11h15 Q&A CEO, CI&TO, CRO 44

11h15 – 11h40 Break - 45

11h40 – 12h00 Customer experience, our key priority Frans van der Horst (CEO RB) 46

12h00 – 12h20 Transforming to a more scalable private bank Pieter van Mierlo (CEO PB) 60

12h20 – 12h40 Q&A CEOs RB and PB 71

12h40 – 13h25 Lunch - 72

13h25 – 13h45 Future proof CIB Rutger van Nouhuijs (CEO CIB) 73

13h45 – 14h05 Sustainability, a business opportunity Daphne de Kluis (CEO CB) 85

14h05 – 14h25 Q&A CEOs CIB, CB 94

14h25 – 14h40 Break - 95

14h40 – 15h05 Strong capital generation and return Clifford Abrahams (CFO) 96

15h05 – 15h25 Q&A CFO 115

15h25 – 15h30 Wrap up Kees van Dijkhuizen (CEO) 117

Do not remove these hyper links to the respective chapters (required for the pdf on IR website)

Link to slide 3, paste over

AA logo on all title pages

ABN AMRO Investor Day

Banking for better,

for generations to come

CEO | Kees van Dijkhuizen

16 November 2018

5

Decisive management team achieving good results

Disciplined delivery since IPO

Strategic steps taken to further improve the bank

Accelerating the sustainability shift of our clients in

a profitable way

Photo to be updated

Moderate risk profile as evidenced by our good

2018 EU-wide stress results, confirming resilience

in adverse economic scenarios

Delivering attractive results with high capital return

6

50%

75%

100%

125%

150%

€9.0

€14.0

€19.0

€24.0

€29.0

Nov 2015 Nov 2016 Nov 2017 Nov 2018

ABN AMRO

STOXX Banks 600 Europe

Strong results and steady capital generation since IPO in 2015

1) Excluding the gain on PB Asia sale, the ROE was 13.4% and C/I was 61.2%

2) Cost/Income in the 4th quarter will be higher due to. regulatory levies , among other things

3) Dividend accrual YTD of 60%; final decision in FY results.

2013 2015 2017 2018 YTD IPO target

ROE 5.5% 12.0% 14.5%1) 13.1% 10-13% in coming years

C/I ratio 63.6% 61.8% 60.1%1) 55.3%2) 56-60% 2017

CET1 ratio 13.9% 15.5% 17.7% 18.6% 11.5-13.5% fully loaded

Dividend

pay-out ratio 30% 40% 50% 60%3) 50%

2017

Development key financial targets ABN AMRO share price since IPO

20/11/

2015

2016 2017 2018

7

Strategic steps taken to further improve profile and profitability

Sharpened C/I ratio to 56-58% by 2020

Nominal cost level 2020 lower than 2015

Focus on sustainability

Real Estate portfolio to average energy label ‘A’ in 2030, sustainable investments as the

norm and becoming a partner of choice to support clients in a circular business model

Continued IT Transformation and digitalisation

Strong digital offering. 65% of retail sales digital

Peer-to-peer app Tikkie with close to 5 million users

CIB Update

Reduction of RWAs from 39 bn to 34 bn to improve ROE above10% by 2021

Strategic focus Private Bank

Scalable franchise with strong local brands in core countries in NW Europe

New and decisive management team in place

8

Banking

for better,

for generations

to come

Purpose-led organisation to benefit all stakeholders

Clients

Effortless customer experience

Proactive and relevant advice

Safe, stable banking services

Employees

Purpose-led and values-driven culture

Improving the employee journey

Investors

Attractive returns

High capital return

A responsible investment proposition

Society

Integrate societal impact in decisions

Accelerate the sustainability shift

Megatrends

Climate change

Sharing economy

Ageing population

Continuously changing expectations

New technology

Increasing regulation

Safety and security

Unbundling of value chains

Digital ecosystems and partnerships

Disintermediation

Open Banking

Societal and banking trends Stakeholder expectations

9

Three pillars to help us live our purpose throughout the bank

Clear business opportunity

Engage with clients to support the

transition to sustainable business

model

Maintain strong DJSI score

Lead by example

Sustainability

Treasuring the customer relationship

Customer-focused and data-driven

Effortless and recognizable customer

experience

Partner to deliver better services and

extend to adjacent industries

Customer experience

Purpose-led and values-driven culture

Product and process rationalisation

and optimisation

Continued I&T improvements guided

by business needs

Improving the employee journey

Future-proof bank

Build on three pillars to the benefit of all our stakeholders: clients, employees, investors and society

10

250135

Continued focus on strong digital proposition of Retail Banking

1) Based on 13.5% CET1

37%65% ‘D’‘A’

Focus on Dutch, mass affluent clients

5 million clients, primary bank for 20% of Dutch population

Strong digital focus: >1 billion annual client contacts

Short-term revenue pressure due to continued low interest

rates

Efficiency drives stable and strong ROE of 33%1) YTD

Key features

Building on proven track record for delivery and address short

term revenue pressure

Delivering differentiating customer experiences by enhancing

our core offering and a continued focus on the shift to digital

Maintaining our forefront position in innovation to increase

customer loyalty and monetise our strong customer interface

Committed to

branches

(2016-2018)

Share of digital sales

(2016-2018)

Average energy level by 2030 in the

EUR 150bn residential real estate portfolio

11

Scalable Private Bank in NW Europe with growth potential

1) Based on 13.5% CET1

81% NL 56% DE 42% FR 52 80%

Focus on onshore North West Europe

Managing EUR 195bn of client assets

Focus on Private Wealth Management, Entrepreneurs &

Enterprise and LifeCycle segments

Clear market leader in NL, number 3 and 5 positions in

Germany and France

ROE of 23%1) YTD

Key features

Continued focus on North West Europe, pursuing organic and

inorganic growth

Further harmonise and digitise, achieving a C/I ratio <70% by

2021

Offer our clients sustainable investments as a standard

Committed to

One platform in NL and one shared platform

in all other locations (2017-2021)

Clients using online solutions

(August 2018)

Of new clients opt for

sustainable investments in NL

12

Growth through sustainable revenues in Commercial Banking

1) Based on 13.5% CET1

2) For enterprises with a yearly turnover below EUR 2.5 million

365,000 small-mid sized Dutch clients

Primary bank for 25% of Dutch enterprises

Strong economy supports good ROE of 15%1) YTD

Sector knowledge as a clear differentiator

Key features

Service the Dutch SME market guided by client intimacy where

it matters and efficiency everywhere else

Drive the sustainable agenda to accelerate the sustainability

shift, which contributes to society and our financial

performance

Grow our top line profitably and manage cost effectively

Committed to

Product reduction

in 2020

Of all contacts are initiated

digitally by 20222)

Circular assets and 100 circular

deals by 2020

EUR 1bn 85% 50%

13

RWA reduction in CIB to increase profitability to at least 10%

1) Based on 13.5% CET1

EUR 8bn Advisor on 12 deals Green bonds

in 2018 YTD

>60% of global clients are multi-product

by 2020

10% ROE by

2021

3,000 large corporate and financials clients in North West

Europe and specific global sectors

Leading domestic franchise, established positions in selected

global sectors

Sector knowledge leveraged to neighbouring countries

Strategic update to deliver ROE of at least 10%

(YTD 9.4%1))

Key features

Sustainable relationships with multi-product clients in

profitable sectors

Reducing RWA, lowering cost, and strict discipline in capital

allocation

Delivering >10% ROE targets in 2021 under Basel III and

transform as preparation for Basel IV

Committed to

14

Flattish loan book in 2019-2020, opportunities in medium term

Loan book expectation flattish for 2019-2020 due to interest

rate environment and disciplined margin behaviour, however at

high ROE and CET1 levels

After 2020 moderate growth of 1-3% of the loan book is

expected

Stable fees in short term; thereafter modest pickup from

growth initiatives, reflecting new services & business models,

and from partnerships

Strengthen return on capital through originate-to-distribute

opportunities

Disciplined delivery

Bolt-on

Not transformational

Within ROE hurdle in reasonable timeframe

Manageable by local management

Maintain capital position

Seize bolt-on opportunities for inorganic growth

15

Delivering on cost savings whilst investing in growth and digital

Cumulative cost savings of EUR 640m delivered at the end

of Q3 2018

Internal and external FTEs to decline by 14% by 2020

(vs. YE2015); actual FTEs down by 12.4% vs. YE2015

Further cost savings expected from digitalisation & process

optimisation, TOPS2020 & retail digitalisation and support

& control activities

Well on track to meet 56-58% in 2020

C/I target sharpened to <55%1) for 2022

Increase IT cost efficiency

Further product and process rationalisation and improvement

across business lines and support functions

Disciplined delivery Cost measures to ensure continued C/I improvements

59%

70% 65%

62% 56-58%

<55%

2010 2013 2015 Last 4Q 2020 2022

1) Based on assumptions of ABN AMRO group economics, incl on GDP, interest rates and the mortgage market

16

Strong capital position, well positioned for a dividend pay-out >50%

With Basel III CET1 ratio of 18.6%, well positioned for Basel IV

Our Basel III CET1 improved from 17.7% to 18.6% YTD 2018, while Basel IV CET 1 remained more

or less stable at c.13%, before mitigations, as Basel IV inflation increased from 35% to 43%

Mitigating actions lower Basel IV inflation from 43% to 35%. We expect to maintain our capital target

range in 2019 at 17.5%-18.5% (subject to SREP)

EU-wide stress test confirms resilience in adverse economic scenarios

Leverage ratio a constraint in 2018, less so in later years

− Possible legal merger Bank and Group: c.0.2%

− SA-CCR (Clearing) expected by 2021 at the latest: c.0.5%

YTD 2018 60% of profit accrued for dividend, final decision with FY result, subject to SREP

Strong ROE and moderate RWA growth create further room for a dividend pay-out clearly above 50%

in later years

17

1) Excluding the gain on PB Asia sale, the ROE was 13.4% and C/I was 61.2%

2) Cost/Income in the 4th quarter will be higher due to regulatory levies, among other things

3) Based on assumptions of ABN AMRO group economics, incl on GDP, interest rates and the mortgage market

4) Additional distributions will be considered when capital is within or above the target range, and are subject to other circumstances,

including regulatory and commercial considerations. Capital target range to be reviewed annually

5) Dividend accrual YTD of 60%; final decision in with FY results

6) Sustainable profit attributable to shareholders excludes exceptional items that significantly distort profitability; examples from the past

would have been the PB Asia divestment (2017) and the provision for SME derivatives (2016)

Financial targets

2017 2018 YTD Targets

ROE 14.5%1) 13.1% 10-13%

C/I ratio 60.1%1) 55.3%2) 56-58% by 2020

<55%3) by 2022

CET1 ratio 17.7% 18.6%

17.5-18.5%4)

2019

Dividend

pay-out ratio 50% 60%5) Additional distributions above

50% of sustainable profit4,6)

18

Responsible investment choice with high returns

Domestic champion in Retail, Private, Commercial and Corporate Banking in digitally-savvy and strong

Dutch market

Making a positive impact in a profitable way by accelerating the sustainability shift of our clients

Treasuring the customer relationship increasingly working with partners

Demonstrated delivery on cost savings, with Innovation & Technology as a critical enabler for efficiency

Moderate risk profile based on discipline, strong capitalisation and a clean balance sheet

Delivering attractive returns with high capital return

Decisive and agile management team

19

09h30 – 09h35 Welcome & programme Dies Donker (Head of IR) 3

09h35 – 10h00 Banking for better, for generations to come Kees van Dijkhuizen (CEO) 4

10h00 – 10h25 Accelerate to the future Christian Bornfeld (CI&TO) 20

10h25 – 10h45 Safeguarding our moderate risk profile Tanja Cuppen (CRO) 33

10h45 – 11h15 Q&A CEO, CI&TO, CRO 44

11h15 – 11h40 Break 45

11h40 – 12h00 Customer experience, our key priority Frans van der Horst (CEO RB) 46

12h00 – 12h20 Transforming to a more scalable private bank Pieter van Mierlo (CEO PB) 60

12h20 – 12h40 Q&A CEOs RB and PB 71

12h40 – 13h25 Lunch 72

13h25 – 13h45 Future proof CIB Rutger van Nouhuijs (CEO CIB) 73

13h45 – 14h05 Sustainability, a business opportunity Daphne de Kluis (CEO CB) 85

14h05 – 14h25 Q&A CEOs CIB, CB 94

14h25 – 14h40 Break 95

14h40 – 15h05 Strong capital generation and return Clifford Abrahams (CFO) 96

15h05 – 15h25 Q&A CFO 115

15h25 – 15h30 Wrap up Kees van Dijkhuizen (CEO) 117

ABN AMRO Investor Day

Accelerate to the future

Innovation & Technology | Christian Bornfeld

16 November 2018

21

We are committed to

Modernising our IT landscape without large-scale re-platforming; competitive

digital offering and solid roadmap in place

Reducing the IT spend while increasing competitiveness; further simplification

of IT landscape and adjustments to delivery model as key levers for efficiency

Evolving client offerings by reinventing client journeys and further leveraging

partnerships

22

Two strategic pillars strongly tied to innovation and technology

Sustain a high level of employee engagement

Develop, attract and retain key skills in areas like

sustainability, innovation, digitalisation and analytics

Continue consolidation, rationalisation and digitalisation

of products, processes and platforms

Strengthen data management capabilities as enabler for

regulatory agenda and client offerings

Increase cost and capital efficiency as well as agility and

learning in order to reduce time-to-market

Evolve our partnership, vendor and utility landscape to

reflect the future industry dynamics

Extend our lead in digital advisory and sales

Enhance the customer experience − anytime, anywhere

on any device

Leverage advanced analytics and AI to increase

relevance and proactivity in customer experience

Innovate and enable new business models that extend

beyond traditional banking

Address opportunities and threats associated with Open

Banking

Retain the trust of clients through continued focus on

cyber security and privacy

Reinvent the customer experience Build a future-proof bank

23

Solid base for reaching our ambitions

Large-scale decommissioning and

re-platforming achieved

Agile way of working adopted for all

change activities

No large-scale core system

replacement needed; step-wise

rejuvenation plan established

55% reduction in paper documents

sent to customers over 6 years

Strong digital offering in the retail

market with award winning apps, e.g.

Tikkie and Grip

Digitalisation roadmap in place for

Commercial and Private Banking

Key building blocks in place: Group

Innovation, Digital Impact Fund,

developer portal and partnerships

Strong innovation culture and

knowledge on key technologies like:

AI, Block chain and Cloud

Multiple learnings from our own

challenger banks

82 76

70 60

52

37

Modernised IT platform Digital focus Innovation enablers

# m. paper documents sent to customers

2013 2014 2015 2016 2017 2018 2014 2015 2016 2017 2018T 2019E

100%

(~730)

100%

(~2000)

Migration of applications to Cloud in scope

Decommissioning applications in scope

24

Historic distribution of IT spend

Multiple levers to improve focus and IT cost efficiency

Demand: Consolidate and focus

Adopt shared platforms across business lines, geographies

and subsidiaries

Further rationalise IT application landscape based on focussed

client value propositions

Reduce IT investment in non-strategic areas

Productivity: Automation and shift to cloud

From Agile to DevOps with integrated teams and a higher

degree of automation

Continue the shift to a hybrid cloud delivery model for IT

applications

Optimise our off-shore delivery model

Supply: Standardise and right-source

Standardised technology platforms and tools

Evolve partnerships to reflect cloud computing

Consolidate and optimise vendor landscape

Run Costs 55%

Change Costs 45%

Key levers to increase focus and IT cost efficiency

Share of IT spend for change activities historically higher

than peers

Maintained flat IT run spend since 2015 despite strong

increase of transaction volumes

IT change spend is not capitalised which gives us more

flexibility to adjust our IT spend as amortisation is limited

Full-year IT costs avg. 2015-2017

EUR

1.5 bn

25

Reducing IT spend while remaining fit for the future

IT is a critical enabler in decreasing

the overall cost/income ratio

IT spend as share of income will

decrease over the coming years

Decrease is enabled by delivering

required capacity for less spend,

combined with increased focus

Clear prioritisation in delivery of

regulatory and strategic priorities

1) European IT Benchmarking in Banking (EITBB) 2017. C/I Ratio: operating expenses as a percentage of operating income.

IT C/I Ratio: operating IT expenses as a percentage of operating income

IT C/I1)

Ratio (%)

Top

Quartile

(52,6%)

20 5 10 15

C/I Ratio1) (%)

2018 (Indicative)

Northern and Central Europe European Union

Type I

More technology &

automation?

Type II

How to leverage IT

spending?

Type III

Do we overspend?

Type IV

Is this sustainable?

Study Avg.

(13.2%)

30

90

60

50

Right-sizing the IT spend Top Quartile

(10.9%)

Study Avg.

(61.1%)

‘Sweet spot’

2017

Continuously manage the balance of

efficient and sufficient IT investments

26

60

200

400

Achieving our ambitions by moving to the sweet spot

1) IT C/I Ratio: IT expenses as a percentage of operating income

2) Including SaaS applications

2017 Sweet Spot

1,900 2,000 2,200

100%

3%

Private 97%

30%

70%

Public2)

Leading indicators

Reduction in number of applications since 2014 (accumulated)

Demand:

Consolidation

Productivity:

Automation

Supply: Cloud

delivery model

Focused effort over several years provides good starting point

Ambition to hit ‘sweet spot’ by gradually reducing IT spend as

share of operating income

Next steps in IT rejuvenation will be conducted step-wise

through multiple levers

IT C/I Ratio ‘sweet spot’ of 12-13%

IT C/I Ratio1) in %

12-13%

~16%

2019 2018 2022

2018 2019 2020

2017 2018 2022

Number of teams with DevOps capabilities

Cloud delivery models split (%)

27

Two parallel approaches to reinvent the customer experience

Create new offerings and experiences

Sharpen value proposition for key client

segments, allowing us to reduce complexity

Reduce client hassle by removing the need for

paper and physical signatures

Decrease processing time and increase

conversion rates on key processes

Further improve client access through digital

channels, e.g. video meetings and chatbots

Establish a proactive dialogue based on

predictive data models

Common capabilities (examples)

Extend our strong position step-by-step

‘Zoom out’ to identify key customer experience

points and new business opportunities

Establish new partnerships both within and

outside the financial sector

Address the threats and opportunities related to

Open Banking by providing APIs

Develop challenger propositions to experiment

with brand-neutral offerings

Engage with regulators to ensure alignment and

level playing field in new types of offerings

Key focus areas (examples)

Reinvented

Customer Experience

Online

On-boarding Users & clients Digital identity

Voice of client

& analytics Video & chat Track & trace

Energy

transition

Urbanisation &

future of work

Ownership,

access, usage

Privacy & trust AI Block chain

Step-

by-Step Reinvent

28

Realising my entrepreneurial dream1)

Extending into new client journeys

Two-pronged approach

1) Step-by-step approach to extend our position in the areas

in which we currently excel

2) Extending into new offerings and experiences

Current initiatives

Selected set of customer journeys is being mapped with a

broad sample of clients within focus segments

Multiple partnerships being explored to unlock business

potential in line with strategic identity

13 Touchpoint with AAB Client opportunity AAB Customer action

Awareness Ideation Starting a business Growth Consolidate / Exit

‘Zoom Out’ Identify customer decision points

‘Zoom Out’ Identify customer decision points

‘I need to employ more staff’

‘I need advice from an accountant and a lawyer’

‘I need to register with the corporate registry’

‘I need to extend my client base’

1

2 3 4

5 16

17 18

20

21

22 23

24

25

26

27

28 29

30

31

7

8a 9

10

11

12

14

13 19

6 15

‘I need to find a suitable office location’

‘I need a transaction account and liquidity management’

‘I need to invest in my inventory’

‘I need to do research and build my business plan’

‘I need to decrease my environmental footprint’

ABN AMRO What we excel in right now

‘I need help with a payment that won’t go through’

8b

Data driven

1) Simplified example

29

Leveraging on partners

Distribution

Digital and Personal Banking

Production

API based financial services

KYC Mortgage

processing …

IT

infrastructure

Cash

Handling ATMs

Big

tech

/

Fin

tech

Pe

ers

Pa

rtn

ers

Cha

llen

ge

rs

APIs

AI & security

Fin

tech

s

Pe

ers

Ch

alle

ng

ers

Pa

rtne

rs

Effect of Open Banking

Digital channels

and agents

Data, Analytics,

Privacy &

automation

Clie

nts

Communities

Platforms

(open, curated

or composed)

Aggregation

Utilities

30

Complemented by Digital Impact Fund investments

Learning by experimenting with challenger banks and impact fund

A new proposition can be built and brought to market in less

than a year

Agile practices combined with DevOps capabilities, cloud

technologies and Fintech solutions is highly efficient

Both proposition and timing need to be right

Client acquisition is expensive and association with a trusted

brand like ABN AMRO is key

Scale-up of operational processes as well as risk and

compliance functions is expensive in a stand-alone setup

Key learnings ABN AMRO challenger banks

New stand-alone propositions complement or replace part of

the ABN AMRO offering

Scale-up by redeploying solution under the main ABN AMRO

brand

Continuously evolve the challenger set-up to ensure return on

investment

Extracting value from challenger banks

fast and efficient

SME lending peer-to-peer

payment requests

future asset

management

special purchase

loans

FX and

multi-currency

payments

fully digital

financial services trade &

commodity

finance

31

We are committed to

Modernising our IT landscape without large-scale re-platforming; competitive

digital offering and solid roadmap in place

Reducing the IT spend while increasing competitiveness; further simplification of IT

landscape and adjustments to delivery model as key levers for efficiency

Evolving client offerings by reinventing client journeys and further leveraging

partnerships

32

09h30 – 09h35 Welcome & programme Dies Donker (Head of IR) 3

09h35 – 10h00 Banking for better, for generations to come Kees van Dijkhuizen (CEO) 4

10h00 – 10h25 Accelerate to the future Christian Bornfeld (CI&TO) 20

10h25 – 10h45 Safeguarding our moderate risk profile Tanja Cuppen (CRO) 33

10h45 – 11h15 Q&A CEO, CI&TO, CRO 44

11h15 – 11h40 Break 45

11h40 – 12h00 Customer experience, our key priority Frans van der Horst (CEO RB) 46

12h00 – 12h20 Transforming to a more scalable private bank Pieter van Mierlo (CEO PB) 60

12h20 – 12h40 Q&A CEOs RB and PB 71

12h40 – 13h25 Lunch 72

13h25 – 13h45 Future proof CIB Rutger van Nouhuijs (CEO CIB) 73

13h45 – 14h05 Sustainability, a business opportunity Daphne de Kluis (CEO CB) 85

14h05 – 14h25 Q&A CEOs CIB, CB 94

14h25 – 14h40 Break 95

14h40 – 15h05 Strong capital generation and return Clifford Abrahams (CFO) 96

15h05 – 15h25 Q&A CFO 115

15h25 – 15h30 Wrap up Kees van Dijkhuizen (CEO) 117

ABN AMRO Investor Day

Safeguarding our moderate

risk profile

CRO | Tanja Cuppen

16 November 2018

34

Refreshed strategy fully aligned to moderate risk profile

Building long-term relationships with clients in strong economies

Taking risks leading to sound asset quality and strong balance sheet

Being well prepared to anticipate and absorb impact of changes in the

economy, regulations and technology

We are committed to our moderate risk profile by …

35

Serving clients in strong economies

1) Based on 2018 Q3 RWA balances

2) Through-the-cycle (‘TTC’) cost of risk expressed as impairments over average gross loans (client lending)

Business profile Retail Banking Private Banking Commercial Banking C&I Banking

Client type Mass

affluent

Individuals, PWM, E&E

Institutions & Charities

Small-mid

sized companies

Large corporates

and Financials

Footprint Dutch NW-Europe Dutch NW Europe and

specific global sectors

Risk profile

Client lending 156bn 13bn 42bn 44bn

Portfolio granularity c.5m clients c.100k clients c.365k clients c.3k clients

RWA allocation 1) 26% 9% 24% 36%

Avg. cost of risk

since 2015 (IPO) c.1bps c.5bps c.23bps

TTC cost of risk 1) 5-7bps on domestic

mortgages 40-60bps

36

Sound asset quality reflected in decline of impairments

Cost of risk well below TTC level … … mainly driven by corporate loans

Average of 4Q cost of risk (bps) Average of 4Q impairments by product (EUR m)

Sound credit quality loan portfolio reflected in clear and significant cost-of-risk improvement to well below through-the-cycle levels

Elevated impairments in corporate loan niches (mainly CIB), resulted in implementation of mitigating measures

Impairments in 2018 reflect mainly IFRS9 stage 3 charges on existing non-performing files

Overall sound asset quality, portfolio behaving well,

defaulted portfolio expected to decline further

-25

0

25

50

75

2014 2015 2016 2017 2018

25-30bps TTC Cost of Risk

4Q Rolling average

-25

50

125

200

2017 2018

Mortgages Consumer loans

Corporate loans Total impairments

right hand chart

37

Impairments sector/file specific, not indicative for rest of loan book

1) Natural Resources includes Energy, Offshore Services and Basic Materials, Trade & Commodity Finance (TCF) includes EUR 1.1bn Diamond & Jewellery (D&J), Global

Transportation & Logistics (GTL) includes Shipping.

2) Impairments year-to-date 2018, expressed as percentage of total reported year-to-date impairments of EUR 447m.

Sectors 1) Natural Resources TCF (incl. D&J) GTL (incl. Shipping) Healthcare

Client lending EUR 8.5bn EUR 11.1bn EUR 10.4bn EUR 4.9bn (EAD)

Challenged

markets

Offshore services

Upstream energy

Diamond & Jewellery

TCF

Offshore Service Vessels

Crude oil tankers

Short sea

Domestic hospitals &

cure

Impairments 2) EUR 150m, 34% of YTD

impairments

EUR 69m, 15% of YTD

impairments

EUR 47m, 11% of YTD

impairments

EUR 39m, 9% of YTD

impairments

Market

dynamics

Signs of recovery

Higher oil prices should

lead to new contracts

Diamond production

shifts to India

Antwerp & Dubai focus

more on trading

Recovery seen in dry

bulk and containers

Regulatory changes

Overcapacity

Government cost focus

impacts client revenues

De-risking Offshore services

Several exposures sold

Diamond & Jewellery

Dubai & Moscow closure

Offshore Service Vessels

Several exposures sold

Close monitoring

Selective origination

Risk outlook Material additional impairments currently not expected, though challenges are expected to remain

We are currently

working on an

updated deep dive

hospitals healthcare.

Our portfolio includes

35 hospitals with a

total OOE of EUR

2.602 billion.

- 30 general and top-

clinical hospitals

(OOE EUR 2.153

billion)

- 2 academic hospitals

(OOE EUR 0.383

billion)

- 3 specialised

hospitals (OOE EUR

0.066 billion)

Part of Corporate & Institutional Banking Part of Commercial Banking

38

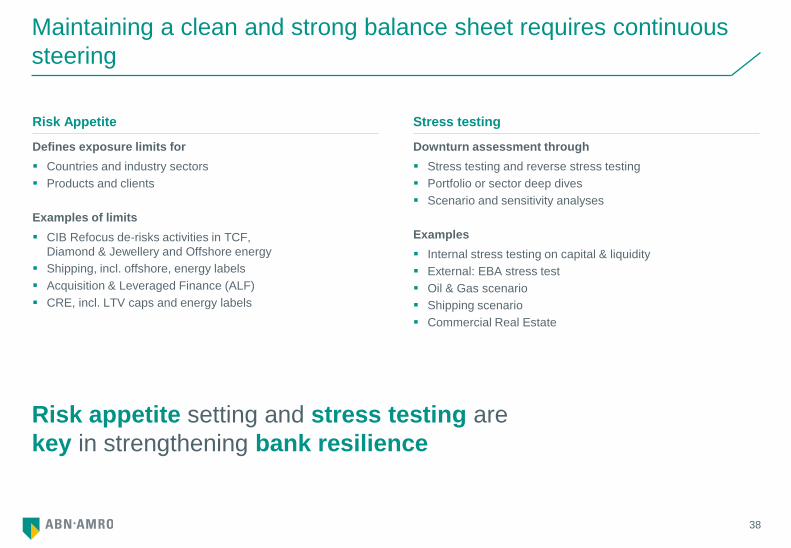

Maintaining a clean and strong balance sheet requires continuous

steering

Risk appetite setting and stress testing are

key in strengthening bank resilience

Defines exposure limits for

Countries and industry sectors

Products and clients

Examples of limits

CIB Refocus de-risks activities in TCF,

Diamond & Jewellery and Offshore energy

Shipping, incl. offshore, energy labels

Acquisition & Leveraged Finance (ALF)

CRE, incl. LTV caps and energy labels

Risk Appetite

Downturn assessment through

Stress testing and reverse stress testing

Portfolio or sector deep dives

Scenario and sensitivity analyses

Examples

Internal stress testing on capital & liquidity

External: EBA stress test

Oil & Gas scenario

Shipping scenario

Commercial Real Estate

Stress testing

CRE

Voor wat betreft kantoren is dat

als volgt: ABN AMRO Real Estate

financiert alleen nog kantoren met

een Label C of beter. Dit is van

toepassing op nieuwe

financieringen en

herfinancieringen.

Uitzonderingen:

1. Er is een plan voor

verduurzaming naar Label C of

beter

2. Kantoor wordt herontwikkeld

naar andere bestemming zoals

wonen

3. Het is een monument

4. Kantoor < 100 m2

Voor de andere assetclasses

geldt dat we het gesprek aangaan

met onze klanten over

verduurzamen. We financieren

nog "alles".

Daarnaast werken we met een

team aan het automatisch

beoordelen van de duurzaamheid

van een object. Als onderdeel van

de digitale bank voor Real

Estate.

39

-2.67% -2.36% -1.50%

-0.30%

-3.85% -3.56% -4.05%

-7.42% -6.94%

-7.69%

ABN AMRO Benelux Peers EBA sample

Low Average High

Moderate risk profile demonstrated by resilience to stress

1) Source: www.eba.europa.eu

Resilience under EBA stress test More resilient than peers

Loss of fully loaded CET1 under adverse scenario vs YE2017 starting

point under IFRS9

With -2.67% fully loaded CET1 deduction under the adverse stress

scenario ABN AMRO scored versus the EBA sample

Stress test confirms ABN AMRO’s resilient capital position: performed well vs. EBA sample

Adverse stress test scenario resulted in CET1 impact of -2.67% vs. -5.91% in the stress test of 2016

Stress test does not contain a pass or fail. Under adverse stress the CET1 remained well above the 2018 SREP of 10.425%

Impact of stress under Basel IV expected to be less significant given binding output floor

17.65%

14.85%

-0.13% -2.67%

YE2017 IFRS9 Adversescenario

YE2020

ABN AMRO CET1 Scenario impact IFRS9

40

Healthy outlook on credit quality, short-term outlook of below TTC

cost of risk

Growing share amortising and savings

loans, full interest-only declining

NHG remains popular

Strong focus on duty of care, full

recourse on collateral

Avg. LtMV: 66%, vs. 82% at YE2012

LtMV>100%: 3.3% of mortgages, vs.

21.1% at YE2012

Positive outlook on credit quality in

mortgage book

Mostly NW Europe, more than half in

the Netherlands

Benefit from Dutch economy and

positive consumer sentiment

Large diversified corporates expected

to remain less sensitive to shocks

Limited direct Brexit & trade war

exposure, indirect effects possible

Granular and stable loan book

Predominantly Dutch

Limited exposure to credit cards

Small average loan size

Strong duty of care rules

Low level of impairments

Good risk/return profile

18%

33%

25%

24%

37%

32%

18%

13%

Amortising& savings

Partialinterest only

Full interestonly

Life & other

Q4 2012 (avg LtMV 82%)

Q2 2018 (avg LtMV xx%)

3.6 3.1

1.0

4.8

Personalloans

Advances Creditcards

Otherconsumer

loans

200

400

600

2015 2016 2017 2018

Q3

Domestic mortgage loans (150bn) Corporate loans (92bn) Consumer loans (13bn)

18%

33%

25%

24%

39%

32%

17%

12%

Amortising& savings

Partialinterest only

Full interestonly

Life & other

Q4 2012 (avg LtMV 82%)

Q3 2018 (avg LtMV 66%)

Consumer loan book well diversified, 3.9%

impaired, 50.9% coverage ratio (Q3 2018)

Strong shift in mortgage portfolio towards

amortisation

Historic low Dutch bankruptcy rate

(monthly businesses & institutions, CBS)

41

Well prepared to absorb impact of industry-wide regulatory changes

1) ECB & EBA: Banks with gross NPL ratios of >5% should establish an NPE strategy, effective June 2019. ABN AMRO's gross NPL ratio is well below the 5% threshold

2) ECB: Banks should book maximum level of P&L provisions. If accounting standards do not fulfil prudential provisioning backstop, banks should adjust their CET1 capital

3) EBA aims to harmonise the definition of default, guidelines aim to increase comparability of risk estimates and own funds requirements across banks, effective Jan 2021

Basel IV implementation in EU

Leverage ratio & MREL

Model reviews & TRIM

IFRS9 replaced IAS39 accounting

standard

Overhaul of impairment methodology

NPE guidelines 1)

NPE reviews & backstops 2)

Definition of Default 3)

Capital Prudential regulation Impairments

Prospects

Implementation risks: transition to new

models and lack of guidance

Material RWA impact, reflecting 72.5%

output floor

Aim to be fully loaded compliant early

in the phase-in period

Prospects

Recognise impairments earlier, in

stage 2

Expected more P&L volatility from

stage 2

No change in incurred loss

Prospects

Governance, operating model, NPE

targets and implementation in risk

framework and recovery planning will

need to be developed

Prepare impact assessment

Lowers available capital

42

Strong focus on non-financial risk in changing world

Cyber attacks grow in number, severity

and risk: DDoS, phishing, hacking

New risks arise from digital

developments: open banking, PSDII,

APIs, electronic contracting, etc.

Key focus area of regulators, society

and management

Financial crime often internationally

organised and becoming more

sophisticated

KYC upgrades in implementation

Providing financial services in new

ways

Energy transition and financing of

clean, circular or new business models

Social Impact Finance (AASIF)

Cyber risk Innovation Conduct & AML

Activities

Cyber risk oversight in place and

further strengthened

Continuous investments in security

measures, penetration testing

Close cooperation with suppliers,

peers, authorities and law enforcement

agencies is key

Activities

Continuous investments in capabilities,

(new) systems and people

Develop public-private partnerships for

intelligence and solutions

Ongoing programmes to enhance

client files

Open dialogue with authorities

Activities

Training to enhance risk identification

of new technologies

Assessments on climate risk and

stranded assets

Define risk appetite for innovative

activities

43

We are committed to safeguarding our moderate risk profile

We are

Building long-term relationships with clients in strong economies

Taking risks leading to sound asset quality and strong balance sheet

Being well prepared to anticipate and absorb the impact of changes in the

economy, regulations and technology

Questions

CEO | CI&TO | CRO

45

09h30 – 09h35 Welcome & programme Dies Donker (Head of IR) 3

09h35 – 10h00 Banking for better, for generations to come Kees van Dijkhuizen (CEO) 4

10h00 – 10h25 Accelerate to the future Christian Bornfeld (CI&TO) 20

10h25 – 10h45 Safeguarding our moderate risk profile Tanja Cuppen (CRO) 33

10h45 – 11h15 Q&A CEO, CI&TO, CRO 44

11h15 – 11h40 Break 45

11h40 – 12h00 Customer experience, our key priority Frans van der Horst (CEO RB) 46

12h00 – 12h20 Transforming to a more scalable private bank Pieter van Mierlo (CEO PB) 60

12h20 – 12h40 Q&A CEOs RB and PB 71

12h40 – 13h25 Lunch 72

13h25 – 13h45 Future proof CIB Rutger van Nouhuijs (CEO CIB) 73

13h45 – 14h05 Sustainability, a business opportunity Daphne de Kluis (CEO CB) 85

14h05 – 14h25 Q&A CEOs CIB, CB 94

14h25 – 14h40 Break 95

14h40 – 15h05 Strong capital generation and return Clifford Abrahams (CFO) 96

15h05 – 15h25 Q&A CFO 115

15h25 – 15h30 Wrap up Kees van Dijkhuizen (CEO) 117

ABN AMRO Investor Day

Customer experience, our key

priority

Retail Banking | Frans van der Horst

16 November 2018

47

We are committed to

Building on proven track record for delivery and addressing short-term

revenue pressure

Delivering differentiating customer experiences by enhancing our core offering

and a continued focus on the shift to digital

Maintaining our forefront position in innovation to increase customer loyalty

and monetise our strong customer interface

Continuing to focus on the customer experience

48

Leading retail bank in the Netherlands

Primary bank for ~20% of Dutch population

Strong presence in urban areas

Strong and highly digital customer interface

> 1 billion annual customer contacts

> 7 million apps downloaded

Omni-channel distribution model

Strong remote advisory capabilities

Top-class digital offering

Solid revenue contributor

Strong position in core products

Tailored approach to address changing client behaviour

Client-driven and digital-focused business model

Stable base

of 5 million

customers

49

Short-term revenue pressure due to continued low interest rates

NII

Fees

Other

Current developments Revenue model Retail Banking

Relative high dependency on net interest income

Three products drive majority of revenue base

Revenues per product, in descending order

1) Mortgages

2) Savings

3) Lending

4) Payments

5) Investments

6) Insurances

EUR 2.7bn

Q3 2018

Fierce price competition pressures market share ABN AMRO

Main deposit rate at 3bps, little or no room to lower further

FTP deposits Main savings rate

deposit margins depend on rate developments

Base

Neg.

Pos.

Past Today Future

0

5

10

15

20

25

Jan-18 Jul-17 Mar-18 Sep-17 May-18 Jul-18 Nov-17 Sep-18

19.6%

7.4%

3.8%

5.3%

15.2%

16.8%

Source: Land registry

50

Focus on customer experience to address revenue pressure

Continued focus on digital first to

improve customer experience and

drive efficiency

− digitising all relevant core processes

and customer journeys and

assisting our clients’ shift to digital

− leveraging next generation tooling

like video banking to get closer to

our clients and increase flexibility

Expanding our involvement in broader

ecosystems and client journeys

outside our own

Aligning core offering with changed

client behaviour and expectations to

strengthen revenue base

− off-balance models in mortgages

− optimising funnel management in

consumer lending

− enhancing insurance and

investment offerings to drive fees

Leveraging relevant customer

touchpoints to strengthen engagement

and develop new sources of income

− driving customer relevancy and

loyalty

− expanding presence in our clients’

context post PSD2

− exploring different roles and

revenue models

Client-oriented offering Digital first Valuable customer interface

51

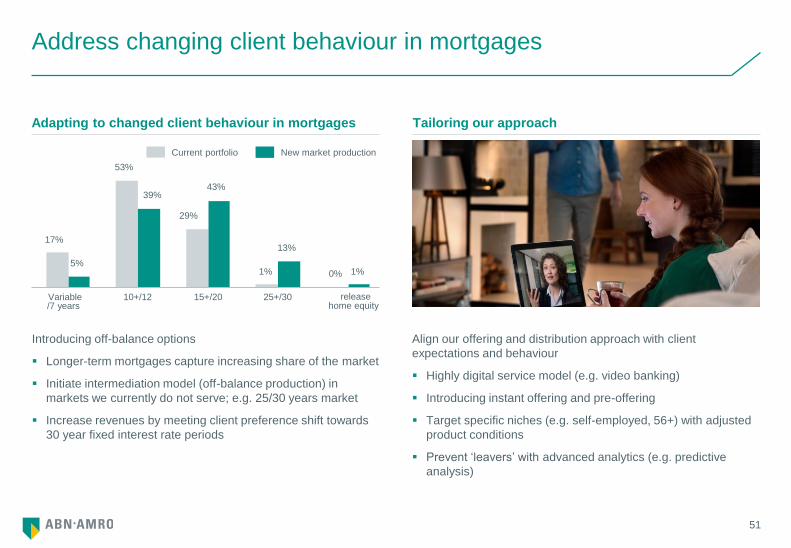

Tailoring our approach Adapting to changed client behaviour in mortgages

Address changing client behaviour in mortgages

Introducing off-balance options

Longer-term mortgages capture increasing share of the market

Initiate intermediation model (off-balance production) in

markets we currently do not serve; e.g. 25/30 years market

Increase revenues by meeting client preference shift towards

30 year fixed interest rate periods

25+/30 15+/20 10+/12 Variable /7 years

1% 0%

29%

53%

13%

39%

1% 5%

43%

17%

release home equity

Current portfolio New market production

Align our offering and distribution approach with client

expectations and behaviour

Highly digital service model (e.g. video banking)

Introducing instant offering and pre-offering

Target specific niches (e.g. self-employed, 56+) with adjusted

product conditions

Prevent ‘leavers’ with advanced analytics (e.g. predictive

analysis)

52

5

6

7

8

2017 2018 2019 2020 2021

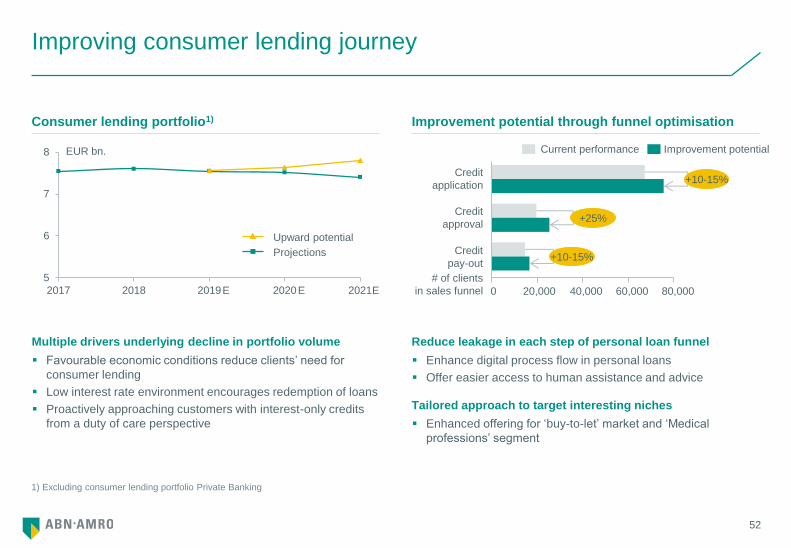

Improvement potential through funnel optimisation Consumer lending portfolio1)

Improving consumer lending journey

Multiple drivers underlying decline in portfolio volume

Favourable economic conditions reduce clients’ need for

consumer lending

Low interest rate environment encourages redemption of loans

Proactively approaching customers with interest-only credits

from a duty of care perspective

Reduce leakage in each step of personal loan funnel

Enhance digital process flow in personal loans

Offer easier access to human assistance and advice

Tailored approach to target interesting niches

Enhanced offering for ‘buy-to-let’ market and ‘Medical

professions’ segment

60,000 40,000 80,000 20,000 0

Credit

pay-out

Credit

approval

Credit

application

Current performance Improvement potential

# of clients

in sales funnel

+10-15%

+25%

+10-15%

EUR bn.

1) Excluding consumer lending portfolio Private Banking

E E E

Upward potential

Projections

53

0

1,000

2,000

3,000

2015 2016 2017 2018E 2019E 2020E 2021E

x k.

Enhancing complete insurance assortment to realise seamless

journeys in line with client expectations

− Improving digital request funnels car insurance and liability

insurance

− Integrating home-related insurances in mortgage sales

processes

− Expanding distribution strategy for term life insurances with

intermediary channel

Initial focus on car insurances, with already promising results

Growing fee income through investments and insurances

Insurances: increasing level of penetration Investments: targeting 30,000 new customers in 2019

Activate existing customer base by pro-actively providing

insights on relevant themes through launching ‘theme

investing’ app

Attract new investing customers through

− Enhanced offering and more competitive pricing of

‘execution only’ proposition

− Launch new investment app − leveraging Prospery

architecture − targeting younger customers and prospects

to start investing at a low threshold

Number of investing households expected to continue to grow

to over 2 million investing households by 2021

Current level of penetration emphasises growth potential

11% Level of

penetration

Premium inflow car insurances (in m.)

4 8 6 10 2 0

(YTD) 2018

2017 ~80%

Source: Kantar – TNS Retail Investor

54

412 366

303 260

221 202

135

Continued focus on digital first to improve customer experience and

drive efficiency

Share of digital continues to rise High level of customer satisfaction Consolidation of branch network

% of digital in sales and services % of 9+ experience digital channels # of branches

469

2018 2011 2019

E

65% 70%

FY

2016

FY

2015

YTD

2018

FY

2017

50%

37% 31%

FY

2014

34%

0

10

20

30

40

50

2011 YTD2018

Mobile banking Internet banking

Success of digital strategy emphasised by several use cases

Frontrunner in Video banking (‘Beeldbankieren’)

− Reduces necessity for a geographical footprint

− Clients value remote contact even higher than face-to-face contact

Continued focus on digitising our core, resulting in most advanced mobile banking app in the Netherlands

Redesign branches to assist-to-digital

Leveraging next generation tooling (e.g. chatbot, speech analytics) for better and more efficient client interactions

-70%

135

55

Increase loyalty and relevance

Resulting in strong growth of our mobile footprint

Multiple apps in place rather than one app with too many

functionalities as part of our constellation strategy

> 7 million apps downloaded

63% of Tikkie users are non ABN AMRO clients

Grip substantial growth potential after multi-bank aggregation

6

4

0

2

10

8

Dec-17 Jun-16 Dec-16 Jun-17 Jun-18

Grip Mobile Banking Wallet Tikkie

Contactless payment

with watch or ring

Overview and insight into

income and expenditure

Peer-to-peer

payments

Unique lending oppor-

tunities with Tweadle

56

Generating insight, creating pro-active customer interactions

Combining data from different apps to truly understand our

clients

Aggregation (multi-banking) to further increase value and

functionalities

Search for strategic partnerships with corporates

Smart connecting of data and insights across apps

Explore different revenue models (e.g. kick-back revenue

models)

06:30 12.30 08:25 08:45 12.45 17.30

Check personalized daily financial insight

Pick-up coffee on way to work

Check updates in ‘theme investment app’

Having lunch with colleagues, send payment request to settle bill

Notification – salary has been received

Time for groceries, skip the line, checkout with Tikkie

Alert: exceeded weekly budget for groceries

Check spend analysis, adjust weekly budgets and saving targets

22.45 17.30

Multiple possible models to monetise value Combination of above apps offers unique position

57

Well positioned to explore platform-oriented revenue models

API Developer platform to explore opportunities & connect with

developers, Beyond Banking Days to identify concepts

Expand our role and become involved in broader ecosystems

and customer journeys

Combining service with partners to deliver a broad value

proposition

Multiple capabilities and solutions in place that can be

leveraged through APIs

− Tikkie has potential as a B2B2C payments solution,

multiple third-party solutions being developed and validated

− Tweadle has future potential as lending API to distribute

capabilities to strategic suppliers

− Grip has potential in digitalising our advisory capabilities

Tikkie’s success proves platform potential Well positioned to explore different roles and models

Introduced as an innovative person-2-person payment solution

Tikkie has attracted a strong user base

Expanding product suite with business solution to attach

businesses to Tikkie and generate transaction based fees

With a growing base of users and businesses, Tikkie is well

positioned to explore platform-based revenue models (e.g.

monetise interactions between merchants and consumers)

Strong growth in number of fee-generating Tikkies

x k.

0

20

40

60

aug oct dec feb apr jun aug oct

Close to 5m users and still growing by 250k users a month

x m.

0 jan apr jul oct jan apr jul oct

2

4

6

58

We are committed to

Building on proven track record for delivery and addressing short-term revenue

pressure

Delivering differentiating customer experiences by enhancing our core offering

and a continued focus on the shift to digital

Maintaining our forefront position in innovation to increase customer loyalty and

monetise our strong customer interface

Continuing to focus on the customer experience

59

09h30 – 09h35 Welcome & programme Dies Donker (Head of IR) 3

09h35 – 10h00 Banking for better, for generations to come Kees van Dijkhuizen (CEO) 4

10h00 – 10h25 Accelerate to the future Christian Bornfeld (CI&TO) 20

10h25 – 10h45 Safeguarding our moderate risk profile Tanja Cuppen (CRO) 33

10h45 – 11h15 Q&A CEO, CI&TO, CRO 44

11h15 – 11h40 Break 45

11h40 – 12h00 Customer experience, our key priority Frans van der Horst (CEO RB) 46

12h00 – 12h20 Transforming to a more scalable private bank Pieter van Mierlo (CEO PB) 60

12h20 – 12h40 Q&A CEOs RB and PB 71

12h40 – 13h25 Lunch 72

13h25 – 13h45 Future proof CIB Rutger van Nouhuijs (CEO CIB) 73

13h45 – 14h05 Sustainability, a business opportunity Daphne de Kluis (CEO CB) 85

14h05 – 14h25 Q&A CEOs CIB, CB 94

14h25 – 14h40 Break 95

14h40 – 15h05 Strong capital generation and return Clifford Abrahams (CFO) 96

15h05 – 15h25 Q&A CFO 115

15h25 – 15h30 Wrap up Kees van Dijkhuizen (CEO) 117

ABN AMRO Investor Day

Transforming to a more

scalable private bank

Private Banking | Pieter van Mierlo

16 November 2018

61

We are committed to

Continue to focus on North West Europe, pursuing organic and inorganic growth

Further harmonise and digitise, achieving a C/I ratio <70% by 2021

Offer our clients sustainable investments as a standard

Transforming to a more scalable private bank

62

Market leader in the Netherlands with strong positions abroad

Netherlands #1 Germany #3 France #5 Belgium #8 Guernsey

Resilient income, low capital consumption

Strong contributor to group: 23% ROE (YTD)

Source of funding: EUR 66.7bn client deposits (YTD)

Unique combination of competitive advantages

Sustainability as a standard

Personal and digital service delivery

Open architecture product offering

Focus on onshore NW Europe

Acquisitions in Belgium (2018) and Germany (2011 & 2014)

Market consolidation offers additional growth opportunities

A leading cross-border private bank in NW Europe

Servicing

EUR 195bn

client assets

(Q3 2018)

63

Transforming to become a more scalable Private Bank

Regulatory pressure persists, including

MiFID II, KYC

Resulting processes and transparency

requirements put pressure on margins

Changing client expectations of digital

requires significant investments

1) Client assets, YTD 2018

2) Including announced acquisition in Belgium (2018)

Market profitability under pressure

Dutch activities (EUR 114bn client

assets) highly efficient, due to scale

Other locations working on reducing

C/I ratio, by harmonising and digitising

Well on track to reach a sustainable

C/I ratio <70% by 2021

Leverage on cross-border scale a

necessity

Scale to remain competitive

Building on our focused footprint,

creating significant cross-border scale

Divested non-core units, latest Asia &

Dubai (2017) and Luxembourg (2018)

Acquisitions in Belgium (2018) and

Germany (2011 & 2014)

Focus on onshore NW Europe

The Netherlands − EUR 114bn 1) Germany − EUR 38bn France − EUR 30bn Belgium − EUR 12bn 2) Channel Islands − EUR 8bn

64

1) Source: Worldbank

Announced acquisition Société Générale PB in Belgium

Further build on strong proposition in Belgium

Belgium market highly attractive (est. 4% client assets growth),

with highest share of millionaires in EU

Opportunity to increase scale, doubling client assets to EUR 12bn

Complementary footprint, similar products and segments,

resulting in considerable synergy potential

Closing expected in Q1 2019

Good add-on to existing portfolio In line with a clear PB M&A strategy

6bn 12bn Announced acquisition will double

client assets in Belgium

3.0%

2.0%

2.4%

2.9%

2.1%

BE NL DE FR EU

Selective bolt-on acquisitions in NW Europe, aiming to

leverage our proposition

Focus on onshore clients

Harmonised service propositions and platforms and

standardised processes to drive cross-country scale

Millionaires as percentage of population (2017) 1)

65

Sustainable investments is the new standard

1) On sustainable discretionary model portfolios

Partnership with University of Oxford

Funding chairs at Dutch universities

650 staff (23%) certified in the UN’s

PRI (Principles for Responsible

Investment)

Up to 50% less CO2 emission vs

benchmark 1)

Strict exclusions and positive

selections based on ESG criteria

Engagement with companies to

discuss UN Global Compact breaches

Leveraging open architecture model to

provide the best sustainable products

Increasing demand from next

generation

>30% of existing clients already own

sustainable investments (2017)

In NL 80% of new clients opt for

sustainable, other countries to follow

Shift also offered to existing clients

Expertise to support clients Clear investment strategy More demand for sustainable

Currently at EUR 13bn 8bn 16bn

Doubling sustainable client assets

(start 2017-2020)

66

Reinventing the customer experience

Segments redefined based on client’s wealth, source of wealth

and stage of life - implemented in NL, to be rolled out in other

locations

Development of dedicated value propositions per segment:

offering matches client needs

Cross-border focus segments first in line for investments

Client expectations of digital are changing, with remote

banking as a key factor to serve the next generation

Combine offline and online and realise seamless client

interaction at every touchpoint

Ambition to have almost 100% of our clients using our online

solutions

Segment propositions to optimise added value Taking customer experience into the digital age

Clients using online solutions

(August 2018)

81% NL 56% DE 42% FR

67

Building a future-proof private bank

1) Achieved a reduction from 3,122 to 2,828 FTEs from 2016 to 2018 YTD (excl. PB Asia and Luxembourg)

From different systems in each

location to a shared platform of

systems: core banking, CRM, portfolio

management

Belgium first-mover to new core

banking platform in Q1 2019

From inefficient and manual processes

to automated and simplified processes

All eligible processes digitised by 2020

One of the drivers for reduction in

FTEs

From very large product ranges in each

country to one product menu card

Each location with the same products,

based on cross-country client needs

Investments menu card defined, other

product groups to follow

Harmonise IT infrastructure Speed up digitisation One rationalised product offering

1 One cross-border

product menu card by 2020

5 2 One platform in NL together with Retail

Banking, one shared platform in all other

locations (2017-2021)

22% Expected total FTE reduction

2016-20211)

68

Further improve costs and efficiency with the transformation

1) Savings compared to the cost basis in 2016

2) Excluding publically disclosed incidentals

2017 2018E 2021E 2019E 2020E

BAU cost base Transformation investments

Transformation resulting in lower costs Well on track to reach a sustainable C/I ratio

On the back of the transformation, we expect to reach a

sustainable C/I ratio <70% by 2021

Taking into account continued investments in digital,

innovation and growth

Well on track with the transformation

Transformation investments total c. EUR 130m 2017–2021,

funded by realised savings

Large part investments used for harmonised IT platform

Cumulative cost savings to increase to c. EUR 100m as of

2021 1), mainly reflecting lower staff and IT costs

Cumulative cost savings EUR m 1) Operating expenses EUR m 2)

c.100

Cost/ income ratio 2)

80.2%

73.4%

2015 2016 2017 Last 4QLast 4Q 2015 2016 2017

1,050 950

69

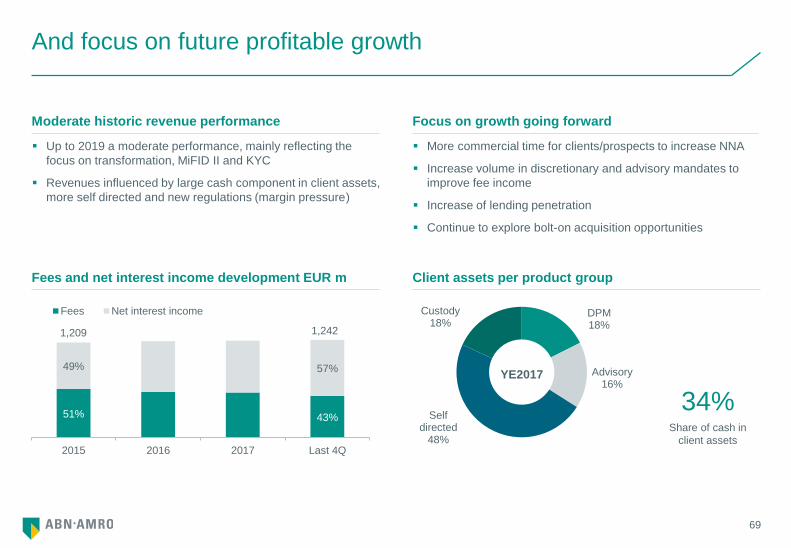

And focus on future profitable growth

Up to 2019 a moderate performance, mainly reflecting the

focus on transformation, MiFID II and KYC

Revenues influenced by large cash component in client assets,

more self directed and new regulations (margin pressure)

Moderate historic revenue performance

Client assets per product group

More commercial time for clients/prospects to increase NNA

Increase volume in discretionary and advisory mandates to

improve fee income

Increase of lending penetration

Continue to explore bolt-on acquisition opportunities

Focus on growth going forward

DPM 18%

Advisory 16%

Self directed

48%

Custody 18%

YE2017

34% Share of cash in

client assets

Fees and net interest income development EUR m

51% 43%

49% 57%

2015 2016 2017 Last 4Q

Fees Net interest income

1,209 1,242

70

We are committed to

Continue to focus on North West Europe, pursuing organic and inorganic growth

Further harmonise and digitise, achieving a C/I ratio <70% by 2021

Offer our clients sustainable investments as a standard

Transforming to a more scalable private bank

Questions

CEOs Retail & Private Banking

72

09h30 – 09h35 Welcome & programme Dies Donker (Head of IR) 3

09h35 – 10h00 Banking for better, for generations to come Kees van Dijkhuizen (CEO) 4

10h00 – 10h25 Accelerate to the future Christian Bornfeld (CI&TO) 20

10h25 – 10h45 Safeguarding our moderate risk profile Tanja Cuppen (CRO) 33

10h45 – 11h15 Q&A CEO, CI&TO, CRO 44

11h15 – 11h40 Break 45

11h40 – 12h00 Customer experience, our key priority Frans van der Horst (CEO RB) 46

12h00 – 12h20 Transforming to a more scalable private bank Pieter van Mierlo (CEO PB) 60

12h20 – 12h40 Q&A CEOs RB and PB 71

12h40 – 13h25 Lunch 72

13h25 – 13h45 Future proof CIB Rutger van Nouhuijs (CEO CIB) 73

13h45 – 14h05 Sustainability, a business opportunity Daphne de Kluis (CEO CB) 85

14h05 – 14h25 Q&A CEOs CIB, CB 94

14h25 – 14h40 Break 95

14h40 – 15h05 Strong capital generation and return Clifford Abrahams (CFO) 96

15h05 – 15h25 Q&A CFO 115

15h25 – 15h30 Wrap up Kees van Dijkhuizen (CEO) 117

ABN AMRO Investor Day

Future proof CIB

Corporate & Institutional Banking | Rutger van Nouhuijs

16 November 2018

74

Key takeaways

Sustainable relationships with multi-product clients in attractive sectors

Reducing RWA, lowering costs, and strict discipline in capital allocation

Delivering >10% ROE targets in 2021 under Basel III and transforming in

preparation for Basel IV

We are committed to:

75

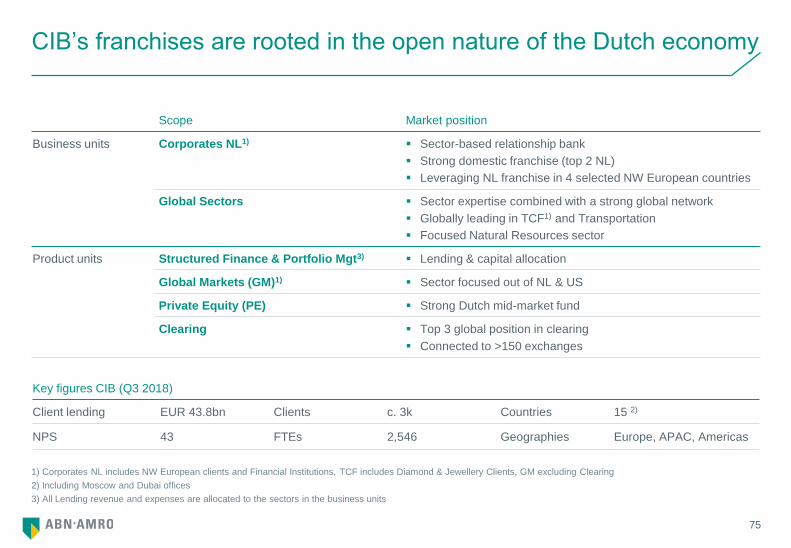

CIB’s franchises are rooted in the open nature of the Dutch economy

1) Corporates NL includes NW European clients and Financial Institutions, TCF includes Diamond & Jewellery Clients, GM excluding Clearing

2) Including Moscow and Dubai offices

3) All Lending revenue and expenses are allocated to the sectors in the business units

Scope Market position

Business units

Corporates NL1) Sector-based relationship bank

Strong domestic franchise (top 2 NL)

Leveraging NL franchise in 4 selected NW European countries

Global Sectors Sector expertise combined with a strong global network

Globally leading in TCF1) and Transportation

Focused Natural Resources sector

Product units

Structured Finance & Portfolio Mgt3) Lending & capital allocation

Global Markets (GM)1) Sector focused out of NL & US

Private Equity (PE) Strong Dutch mid-market fund

Clearing Top 3 global position in clearing

Connected to >150 exchanges

Key figures CIB (Q3 2018)

Client lending EUR 43.8bn Clients c. 3k Countries 15 2)

NPS 43 FTEs 2,546 Geographies Europe, APAC, Americas

76

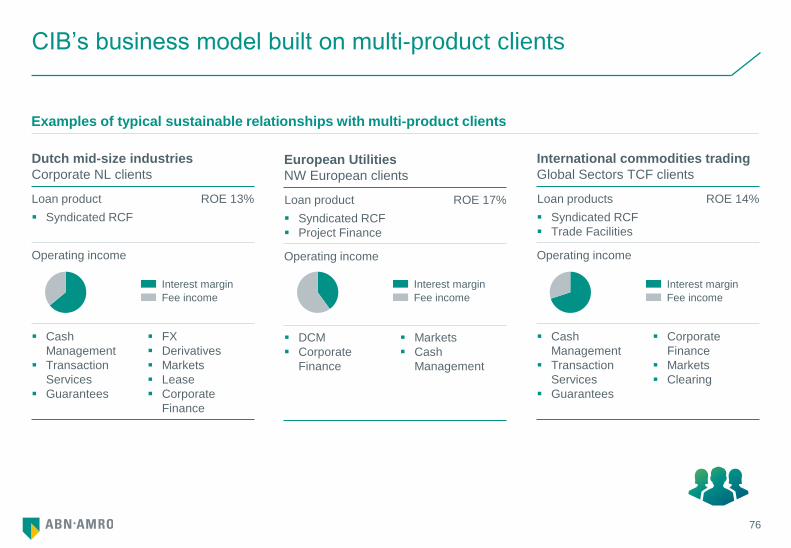

Dutch mid-size industries

Corporate NL clients

Loan product

Syndicated RCF

ROE 13%

Operating income

Cash

Management

Transaction

Services

Guarantees

FX

Derivatives

Markets

Lease

Corporate

Finance

CIB’s business model built on multi-product clients

Examples of typical sustainable relationships with multi-product clients

International commodities trading

Global Sectors TCF clients

Loan products

Syndicated RCF

Trade Facilities

ROE 14%

Operating income

Cash

Management

Transaction

Services

Guarantees

Corporate

Finance

Markets

Clearing

European Utilities

NW European clients

Loan product

Syndicated RCF

Project Finance

ROE 17%

Operating income

DCM

Corporate

Finance

Markets

Cash

Management

Interest margin

Fee income

Interest margin

Fee income

Interest margin

Fee income

Interest margin

Fee income

Interest margin

Fee income

Interest margin

Fee income

77

0%

2%

4%

6%

8%

10%

12%

0% 50% 100%

ROE 10%1)

1) ROE on basis of Basel III RWA and CET1 target of 13.5%. TTC = through-the-cycle

2) Including D&JC

Most businesses deliver returns through the cycle, some are lagging

Corporates NL sector serving mainly core clients

Mid-cap corporates where we have a broad relationship

Over 85% of clients are multi-product / service

ROE > 10%, helped by capital light fee income

Global sectors show mixed picture, one lagging sector TTC

Increasing level of multi-product clients, currently 50%

Asset-based lending, Basel IV vulnerable

TCF has high operational cost and a long tail of non-accretive

clients

Product units support the sectors

Global Markets is de-risking, client-driven, high cost base

Clearing is a generator of stable returns

Continued involvement in PE as cornerstone investor Size represents RWAs FY2017

Most CIB sectors deliver >10% ROE TTC impairments1) Above hurdle returns made on core clients

Operating Income adjusted for TTC impairments FY2017

Cost / Income (adj.)

Clearing

Income (adj) / RWA

ROE > 10% ROE < 10%

GTL

NR PE

TCF2) GM

Corporates NL

78

Improve capital & cost efficiency, to deliver >10% ROE by 2021

1) RWA EUR 5bn reduction (equals CET1 c. 0.9%) compared to Q1 2018, from around EUR 39bn to around EUR 34bn to be achieved by 2020, assuming static risk weighting,

i.e. excluding possible impact of TRIM or credit quality migrations.

2) EUR 27m restructuring costs were booked in Q3 2018

3) Under Basel III RWAs and a CET1 target of 13.5%

Reduce capital Lower costs Transform business model

Measures

Reduce non-core and cyclical

clients

Impacts TCF, offshore, shipping

Focus GM’s products and clients1)

Address low-return clients

FTE reduction & IT rationalisation

Right-size geographies & support

Capital efficient, focus on distribution

Focus on high share of wallet clients

Develop further sustainability

franchise

Objective

Net RWA reduction EUR 5bn1)

revenue impact c. EUR 100m

EUR 80m cost reduction

c.250 FTE reduction, restructuring

cost: c. EUR 50m 2)

CIB ROE >10% by 20213)

Progress

On track, reduced EUR 1.5bn1)

net RWA

Identified non-accretive clients and

developing client action plans

GM 40 FTEs reduction

Closed GM in NOR and Brazil

Closing Dubai & Moscow

Restructuring provision EUR 36m

Organisation restructuring

Energy transition plan

Excluded F&G labelled vessels

79

Reduce capital Lower costs Transform business model

Measures

Reduce non-accretive clients

Increase ownership based lending

D&JC: de-risking and exit

Dubai, US

Increase share of wallet in core

clients

Zero-loss mentality

Reduce FTEs in line with client

reductions

Simplify end-to-end processes

(‘lean’)

Centralise support activities

Closure of Dubai and Moscow

offices

Digitise paper based processes and

improve customer experience

Invest in block chain trade-finance

platforms

Objective

RWA reduction of EUR 3.5bn1)

Increase income / RWA

Direct cost reduction of

15-20%

Reinvent Customer Experience

Progress

Identified non-accretive clients

Capital reduction on track,

EUR 1.3bn RWA2)

Developing client action plans

Normalising level of provisions

Staff reduction of 20 FTEs

Centralised Dutch support activities

Implementing lean improvements

TCF: raising ROE to >10% by 2021

1) Including D&JC

2) Compared to Q1 2018

80

GM: focusing and contribute to CIB’s >10% ROE by 2021

1) Compared to Q1 2018, EUR 6.5bn

Reduce capital Lower costs Transform business model

Measures Reduce RWA

Product offering trimmed in Fixed

Income

Simplify setup by focussing on

Corps and FIs in N/W Europe

Reduce FTEs

Reduce locations to Europe (AMS,

LDN, FFT, PAR) and US only

Drive out (in)direct costs by

rationalising IT systems and data-

provider usage

Increase share of wallet through

multi-product clients

Increase digital product offering and

use of data, AI

Transforming financial markets

product distribution through delivering

and end-to-end digital experience for

our clients

Objective RWA reduction EUR 1.5bn1) Cost reduction of 10-15% Reinvent Customer Experience

Progress

Reduction on track, EUR 0.8bn

RWA1)

40 FTE Reduction

Stopped GM in NOR and Brazil

Finalisation of SME legacy files

Q1 2019

Check best

option 14.4

10.7 10.5 8.4 7.1 5.7

0

10

20

2013 2014 2015 2016 2017 Q32018

RWA EUR bn

81

Transforming CIB’s business model to increase capital efficiency

Improve cross-sell and lending efficiency

Stepping up in relationship tiering by

increasing underwrites to facilitate

cross-sell

Minimum of two cross-sell products

per client

Scale backs of product offerings

affected by Basel IV

Maximise capital efficiency

Central portfolio management steers

RWA under Basel III and Basel IV

Disciplined capital allocation for new

and existing transactions under BIII

and BIV

Progressive pricing during phase-in

of Basel IV

Increase fee income through distribution

More investor-centric origination

approach to increase asset turnover

Invest in origination and distribution

to support distribution efforts

Very substantially increase the current

3-5% risk distribution of the loan

portfolio

Focus on multi-product clients Strict capital discipline Increase capital velocity

82

1) Under Basel III RWAs and a CET1 target of 13.5%

2) RWA reduction of EUR 5bn vs. Q1 2018

Transformed business model to drive returns >10% under Basel IV

CIB to deliver >10% ROE by 20211) under BIII

Implement BIV mitigating actions

Transformed CIB business model is ready to drive capital

efficiency under Basel IV

− Steer capital allocation to least affected products and

sectors

− Higher capital velocity and increase fee income