a young eu member’s ageing: budgetary and macroeconomic consequences of slovenia’s demographic...

TRANSCRIPT

ORI GIN AL PA PER

A young EU member’s ageing: budgetaryand macroeconomic consequences of Slovenia’sdemographic prospects

Klaus Weyerstrass • Reinhard Neck

Published online: 8 May 2013

� Springer Science+Business Media New York 2013

Abstract In this paper, we simulate a macroeconometric model of Slovenia over

the period 2012–2060, using the projected demographic development as input, and

determine time paths for budgetary and macroeconomic variables under alternative

assumptions about Slovenian policy instruments so as to limit budgetary pressures

stemming from population ageing. The main macroeconomic indicators (growth,

employment, price stability, sustainable public finances) are shown to depend on the

assumed long-run policy options followed. It is demonstrated that the ageing of the

Slovenian population projected in the demographic forecast leads to severe bud-

getary problems unless increases of the retirement age, rising social security con-

tributions or reductions of state financed pensions are implemented. A reduction of

the pension replacement rate turns out to be the most effective measure to cope with

the budgetary implications of population ageing. However, none of the analysed

policy measures is sufficient to stabilise the debt ratio.

Keywords Macroeconomics � Fiscal policy � Ageing � Slovenia � Pension

economics � Public debt

JEL Classification E17 � E37 � H63

1 Introduction

Recently, concerns have been raised about the consequences of demographic

developments for the fiscal stance and the economic outlook for many industrialised

K. Weyerstrass

Institute for Advanced Studies, Vienna, Austria

R. Neck (&)

Alpen-Adria-Universitat Klagenfurt, Klagenfurt, Austria

e-mail: [email protected]

123

Empirica (2013) 40:427–456

DOI 10.1007/s10663-013-9217-z

countries, especially in Europe (see, among others, Auerbach and Lee 2001; Kasek

et al. 2008; Banca d’Italia 2009). The financial and economic crisis of 2007–2009,

the ‘‘Great Recession’’, which resulted in negative growth and increasing

unemployment in nearly all industrial countries irrespective of their initial situation,

aggravated the budgetary problems in addition to already high and rising

government debt before the crisis (e.g., Balassone et al. 2011). Some countries

were hit particularly hard, which was partly due to government failures, i.e. to

special reactions of their economic policy makers. This is also true for Slovenia,

whose economic situation deteriorated very strongly during the last few years.

Slovenia was the only country of former Yugoslavia to enter the European Union

(EU) together with most former socialist countries from Central and Eastern Europe

in 2004, and it managed to introduce the euro as legal tender already in 2007. The

economic development of Slovenia was successful in terms of the main

macroeconomic indicators before the ‘‘Great Recession’’. Between 2005 and

2008, real GDP grew by 5 % per year on average, the registered unemployment rate

declined from 11 to 7 %, and the debt-to-GDP ratio decreased from 26.7 to 22 %.

However, the impact of the recession was especially deep in Slovenia, with a

decline in GDP of almost 8 % in one single year (2009) and an increase in

unemployment to the level of the year before Slovenia joined the Euro Area (2006).

Also in 2010 and 2011 the Slovenian economy did not recover well (real GDP grew

by just 1.2 % in 2010 and by 0.6 % in 2011), in contrast to most EU member states,

and at present the macroeconomic prospects for the following years are not very

favourable according to most national and international forecasts. For 2012, in their

Autumn outlooks, the European Commission, the International Monetary Fund

(IMF) and the OECD estimate a decline of real GDP by 2.2–2.4 % (European

Commission 2012b; IMF 2012; OECD 2012). For 2013 a further decrease in the

quite wide range of 0.4–2.1 % is forecasted, followed by a growth of about 1 % in

2014.

Part of the problem results from the enormous fiscal deficits and the resulting

increase of public debt during the last few years. As Figs. 1 and 2 show, after 2007

public finances in Slovenia deteriorated sharply. After having achieved a balanced

budget in 2007, in 2008 a deficit of about 2 % in relation to GDP occurred. In the

following years, this deficit widened considerably, reaching about 6 % in relation to

GDP in the period 2009–2011.

As a consequence of this budgetary development, the debt-to-GDP ratio

increased to 47 % in 2011, more than twice the figure of 2008. Part of this debt

increase was caused by financial assistance the government had to give to the

banking system as some banks faced severe capital losses due to the bursting of a

housing bubble which had contributed to the high economic growth prior to 2009.

According to the 2012 update of the Slovenian Stability Programme, the deficit-to-

GDP ratio shall be gradually reduced below 3 % in 2013 and to close to balance by

2015, i.e. the end of the current Stability Programme period. According to this

projection, the debt ratio should peak at 53 % in 2013. By 2015 it should have

declined slightly to 51 %. However, in light of the adverse economic development

in 2012, the European Commission expects a budget deficit of around 4 % in

428 Empirica (2013) 40:427–456

123

relation to GDP also in 2013 and 2014, and a further increase of the debt ratio to

62 % in 2014. The OECD is only slightly more optimistic.

The amount of government debt piled up points toward long-run problems as

causes in addition to the short-run effects of the ‘‘Great Recession’’. One of these

problems, which was at the centre of recent political debates in Slovenia and

contributed markedly to the demise of the last government, was the pension

problem, which is prominent on the agenda of the new administration but far from

being close to a solution. In this paper we analyse potential effects of the

demographic development projected for Slovenia on this country’s government

budget and on the labour market, with special emphasis on the pension problem. A

long-run projection of the age composition of the Slovenian population is used as

the basis of several scenarios simulated with the macroeconometric model

SLOPOL.

The structure of the paper is as follows. In the next section, demographic

projections and some features of the current Slovenian pension system are

presented. The SLOPOL model used for the simulations is sketched in Sect. 3. In

Fig. 1 Budget balance in relation to GDP. Source Eurostat; from 2012 onwards Slovenian Ministry ofFinance, Stability Programme, 2012 update; authors’ illustration

Fig. 2 Public debt in relation to GDP. Source Eurostat; from 2012 onwards Slovenian Ministry ofFinance, Stability Programme, 2012 update; authors’ illustration

Empirica (2013) 40:427–456 429

123

Sect. 4, the design of the simulation experiments is outlined. The results of the

simulations are presented in Sect. 5. Section 6 concludes with a summary of the

results.

2 Demographic projections and some features of the Slovenian pension system

In the coming decades, the demographic development will put considerable pressure

on public finances in Slovenia, as in most European countries. For this paper, the

population projection EUROPOP2010 by Eurostat has been used.1 The EURO-

POP2010 population projections are based on assumptions of fertility, mortality and

migration. The population projections assume convergence, meaning that socio-

economic and cultural differences between the EU countries will decrease over

time. Therefore, the realisations of the demographic components on which the

projections are based will be the same in all countries in the convergence year

(2150). This implies that in the year 2150 no net migration will take place in the

countries considered and that the fertility rate as well as life expectancy at birth will

be equalised by that year. The population of Slovenia will continue to grow quite

quickly until about 2025 (to approximately 2,155,000). Afterwards total population

is projected to decline slowly. As can be clearly seen from Fig. 3, the projected

demographic development in Slovenia will lead to a marked increase in the share of

people aged 65 and more. This will bring about a sharp rise of the dependency ratio,

i.e. the relation between people in the working age and those in retirement. The

share of people aged 65 years and more is projected to almost double from 16.5 %

in 2011 to 31.5 % in 2060. Due to a low fertility rate (which is assumed to rise

marginally from 1.55 in 2011 to 1.65 in 2060), the increase in the ratio between

people in the retirement age (65 and older) and those in working age (15 to

Fig. 3 Demographic projections for Slovenia. Source Eurostat (EUROPOP2010); authors’ illustration

1 Details on the EUROPOP2010 projections in general can be found on the EU website:

http://epp.eurostat.ec.europa.eu/statistics_explained/index.php/Population_projections. Details for

Slovenia are available from the website of the Slovenian Statistical office:

http://www.stat.si/eng/novica_prikazi.aspx?id=3989.

430 Empirica (2013) 40:427–456

123

64 years) is even more dramatic. This ratio is projected to rise from slightly below

24 % in 2011 to almost 58 % in 2060.

For the 2012 update of the Slovenian Stability Programme, the consequences of

the projected demographic development for public finances have been assessed in

Slovenian Ministry of Finance (2012). The most important results are summarised

in Table 1. As can be seen, age related public expenditures are projected to increase

by more than 9 % points from about one quarter to more than one-third of GDP.

This is mainly caused by the increase in pensions. As a consequence of this

projected development of expenditures, the budget balance will deteriorate

dramatically. The high budget deficit will push up public debt. As a result, interest

payments will rise sharply, contributing to a further increase in the budget deficit.

According to these projections by the Slovenian government, in 2060 the primary

budget deficit will amount to 13.4 % in relation to nominal GDP. Due to the high

public debt, which is projected to reach nearly 550 % in relation to GDP, interest

expenditures will account for almost one quarter of GDP. Hence, by 2060 the

overall budget deficit-to-GDP ratio would reach as much as 36.5 %.

The sharp deterioration of public finances is brought about by two factors. First,

the rising number of the elderly increases pension payments. At the same time, the

size of the working-age population decreases, hence funds flowing into the pension

system which are financed by employees’ and employers’ contributions and hence

linked to the number of employed people decline unless contribution rates are

raised. Higher contributions, on the other hand, reduce the purchasing power of

employees and raise production costs for companies. At the same time, the

production potential is limited by a declining labour force. This can be compensated

only to a limited extent by raising capital intensity and technical progress.

The projections shown in Table 1 demonstrate clearly that Slovenian public

finances are far from being sustainable in the long run if no corrective measures are

implemented. Hence adaptations of the pension system to the ageing of the

population are of utmost importance. At present, the statutory retirement age is

63 years for men and 61 for women. The minimum insurance period required for

Table 1 Projections of public finance related to population ageing

Percent of GDP 2010 2030 2060

Age related expenditures 24.6 27.7 35.1

Pensions 11.2 13.3 18.3

Health care 6.1 6.8 7.2

Long-term care 1.4 1.9 3.0

Education 4.7 4.8 5.2

Others 1.2 0.9 1.4

Interest expenditures 1.4 5.2 23.0

Primary budget balance -3.9 -4.9 -13.4

Overall budget balance -5.2 -10.1 -36.5

Government debt 37.1 125.6 548.6

Source Slovenian Ministry of Finance, Stability Programme, 2012 update

Empirica (2013) 40:427–456 431

123

retirement at these ages is 20 years. Early retirement is possible at the age of 58 with

40 years of insurance for men and 38 years of insurance for women. In the past,

annual pension increases were related to the rise in nominal wages. Since the latest

pension reform introduced in 1999, in February of each year pensions are increased

by the growth rate of nominal wages in the previous year minus 0.6 % points.

Currently, negative accrual rates for early retirement are rather small and do not

exceed 3.6 % per year. Similarly, additional accrual rates for postponing retirement

are also rather low. They are digressive and do not exceed 3.6 % per year

(Stanovnik et al. 2012). The 1999 pension reform has resulted in a stabilisation of

the effective retirement age as well as pension expenditures in relation to GDP. In

2010, the effective retirement age was 61 years and 10 months for men and

58 years and 5 months for women. The average old-age pension amounted to about

65 % of the average net wage, and pension expenditures made up 11 % of GDP.

As the projections in Table 1 above show clearly, although the 1999 pension

reform has temporarily stabilised the budgetary pressures from pension liabilities,

further reforms are necessary. According to the 2012 Ageing Report of the

European Union (European Commission 2012a), until 2060 among the 27 EU

member states only in Luxembourg age-related expenditures will increase more

than in Slovenia.

After a reform proposal had been rejected in a referendum by a vast majority of

72 %, the previous Slovenian government failed. The new government slightly

modified the pension reform which passed the Slovenian parliament in December

2012. As the Constitutional Court had decided that the new pension reform would

not be subject to a referendum, it could come into effect on 1 January 2013. The

amended legislation stipulates stricter retirement conditions. Via transitional

periods, the reform raises the retirement age to 65 years for both genders. Early

retirement will be possible at 60 years of age on the basis of 40 years of service.

Furthermore, the period for calculating the pension basis is increased from the

current 18–24 years. In addition, a more stimulating policy of bonuses for later

retirement and a more restrictive policy of reductions (maluses) for early retirement

are established.2 This reform will help to mitigate some of the adverse age-related

impacts on public finances as pointed out, e.g. in the EU Ageing Report. However,

the pronounced increase in life-expectancy is likely to put additional pressure on

public finances in Slovenia also in the future, as in most European countries. As

long as the increase in the retirement age is not indexed to the increase in life

expectancy, the pension system is inherently lagging behind the demographic

development. Furthermore, the declining labour force puts a drag on the long-term

growth potential if labour market participation of the elderly is not raised

substantially. Lower long-run growth aggravates the budgetary pressures due to

negative impacts on the tax base, in particular regarding corporate and personal

income taxes.

2 Slovenian Ministry of Labour, Family and Social Affairs, Press Releases, 4. 12. 2012, Slovenia passes

pension reform.

432 Empirica (2013) 40:427–456

123

3 The SLOPOL model

The simulations for the present paper have been conducted with the macroecono-

metric model SLOPOL (SLOvenian POLicy model, version 9). In its current

version, SLOPOL has 72 equations of which 27 are behavioural. The econometric

estimations are based on quarterly data for the period 1995 q1 to 2011 q4. The

equations and variable definitions are provided in the appendix. A more detailed

description of an earlier version can be found in Weyerstrass et al. (2011). SLOPOL

contains behavioural equations for the labour, goods, financial, and labour markets.

The demand side of the economy is modelled in more detail and affects the

development of the macroeconomic variables more strongly than the supply side. In

particular, real GDP and its expenditure components (exports, imports, private and

public consumption, gross fixed capital formation), prices, wages, interest rates,

employment, and labour supply are determined endogenously. In addition, the

public sector and the population structure are modelled in detail. As unit root tests

identify almost all variables as integrated of order one, with only a few exceptions

the equations are specified as error correction models with the growth rate of the

respective variable over the same quarter of the previous year as the endogenous

variable.

Private consumption depends on real disposable income and on the real long-

term interest rate. This specification combines the traditional Keynesian view with

more modern consumption theories such as the permanent income hypothesis. It is

safe to assume that most households try to smooth consumption over time; hence

their consumption expenditures depend on wealth rather than on current disposable

income. These wealth effects are captured by the real interest rate. Disposable

income includes both wage income and yields from financial wealth. Income from

wealth is determined by multiplying the stock of financial wealth by the average

interest rate. Financial wealth is extrapolated with the growth rate of the nominal

capital stock. A certain share of households is credit constrained, and for them

current income is relevant. Gross fixed capital formation is influenced by final

demand (the accelerator hypothesis), by the user cost of capital, and by capacity

utilisation. The user cost of capital is approximated by the real interest rate and the

depreciation rate on the capital stock. Including the ratio between actual and

potential GDP (i.e. the macroeconomic capacity utilisation rate) is based on the idea

that higher net investment becomes necessary when the utilisation of the existing

capital stock increases. Real exports depend on world trade and on the international

price competitiveness of Slovenian goods and services on the world market.

Competitiveness is approximated by the real effective exchange rate vis-a-vis

Slovenia’s 41 most important trading partners. The real exchange rate takes the

nominal exchange rates and the ratio of consumer prices into account. Real imports

are influenced by domestic demand in Slovenia and also by the real effective

exchange rate. Employment depends on real GDP and on the real gross wage. In

order to prevent employment to exceed the working age population in long-term

forecasts, the employment function explains the employment rate, i.e. the number of

employees in relation to the total working age population, rather than the

employment level. Labour supply by private households is determined by

Empirica (2013) 40:427–456 433

123

multiplying the labour force participation rate by the working age population. In a

behavioural equation, the participation rate is positively related to the real net wage.

The positive coefficient implies that the positive substitution effect of an increasing

net wage dominates the negative income effect.

Wages are determined in an extended Phillips curve equation. Hence, gross

wages depend on consumer prices, labour productivity and the labour market

situation. The labour market tightness is captured via the difference between the

actual and the structural unemployment rate. The consumer price index (CPI) is

determined by exogenous and endogenous factors. For a small open economy like

Slovenia, international raw material prices are important determinants for the

domestic price development. This is taken into account by including the import

deflator in the consumer price equation, together with the wage rate as the dominant

internal price determinant. The deflators for private and for public consumption are

related to the CPI. Taking the high import content of exports into account, the

export deflator is explained by the import deflator in addition to unit labour costs as

the most important domestic cost factor. The import deflator is influenced by the oil

price in euro, where the oil price approximates international raw material prices in

general.

The equation for the short-term interest rate takes into account that Slovenia was

outside the Euro Area during the first years of the period for which data for the

estimation of the equations have been used, while the country joined the Euro Area

in 2007. Hence, the short-term interest rate in Slovenia might deviate slightly from

the Euro Area average, but it converges towards the Euro Area interest rate over

time. The long-term interest rate in Slovenia is determined by the short-term interest

rate in Slovenia and by the Euro Area average long-term interest rate. The latter

again accounts for convergence between Slovenia and the Euro Area average over

time. As the financial crisis has clearly shown, the long-term interest rate also

contains a risk premium which is positively related to the public debt level. As

financial market participants doubt the long-term sustainability of public finances,

they demand a higher risk premium. This is captured by including the debt-to-GDP

ratio in the equation for the long-term interest rate. The implicit interest rate on

public debt is explained by the long-term market interest rate. The real effective

exchange rate vis-a-vis Slovenia’s 41 most important trading partners is explained

by the nominal exchange rate between the euro and the US dollar (taking Slovenia’s

Euro Area membership since 2007 into account), the exchange rate between the

Slovenian tolar and the euro (accounting for Slovenia’s own currency before joining

the Euro Area), and CPI inflation in Slovenia. While the nominal exchange rates vis-

a-vis the other Euro Area member states do not exist, deviating price developments

are relevant and important also within the monetary union.

On the supply side, potential GDP is determined via a Cobb-Douglas production

function with labour, capital and autonomous technical progress as input factors.

Since potential GDP is a long-term concept, it is not the actual but the trend

realisations of the production factors that are used for its estimation. For the factor

labour, this implies the estimation of the structural, i.e. the non-accelerating

inflation rate of unemployment (NAIRU). The latter is estimated by applying the

434 Empirica (2013) 40:427–456

123

Hodrick-Prescott filter to the actual unemployment rate. The NAIRU is then

endogenised via a moving average equation.

The model comprises a number of potential fiscal policy instruments, namely

transfers paid to households, public consumption, public investment, as well as tax

rates. Regarding transfers, in the context of the present investigation transfers other

than pensions are considered separately. Pensions are calculated as the average

pension replacement rate multiplied by the average gross wage rate. In the

simulations, the pension replacement rate is considered as a policy instrument. A

further instrument is the average social security contribution rate as percentage of

the average gross wage. With regard to fiscal implications of the demographic

development, the retirement age is the third important policy instrument considered

in the SLOPOL model. As Slovenia is a member of the Euro Area, its monetary

policy is conducted by the Eurosystem and the European Central Bank (ECB) in

particular.

4 Simulation design

The SLOPOL model gives forecasts of the most important macroeconomic

variables for Slovenia under alternative settings of the policy instruments. For the

present paper, those instruments relevant in the context of the pension system are

varied in the different scenarios. These policy instruments are (a) the average

pension replacement rate, i.e. the average pension as a percentage of the average

gross wage; (b) the social security contribution rate, also specified relative to the

average gross wage; (c) the average (i.e. not the statutory) pension age. The time

paths of the remaining policy instruments (public consumption and investment, tax

rates, transfers other than pensions, monetary policy) are identical across the

scenarios. The following simulations are run:

i. Baseline: First, a baseline run with the assumption of no policy change is run

over the time horizon 2012 to 2060. In this baseline, the policy instruments are

projected from their actual 2011 values, as are all other exogenous variables.

ii. Pension age: In this scenario, the average pension age is raised from the actual

level of about 60 years in 2011 to 63 years from 2015 and to 65 years from

2018 onwards. The scenario is further divided into two sub-scenarios: in

scenario (ii. a), it is assumed that 75 % of all people that were retired in the

baseline scenario and are now not eligible to retire are employed. In contrast,

for scenario (ii. b) it is assumed that the Slovenian labour market is able to

absorb only 25 % of the additional labour force. Hence, the majority of the

older people that have to remain in the labour force for another three to five

years are now assumed to be unemployed. Although in Slovenia older

employees are protected from being dismissed by law, it is reasonable to

assume that not all older people are able to find an adequate job. Even though

the demographic development in Slovenia will probably cause skills shortages

in certain sectors, as in most European countries, it is reasonable to assume that

Empirica (2013) 40:427–456 435

123

there remains a skill mismatch between labour demand and supply, in particular

with regard to older people.

iii. Reduced gross pension replacement rate: Here the average pension replace-

ment rate, i.e. the average pension in percent of the gross wage, is reduced by 5

% points from 2012 onwards. In 2011, the average pension replacement rate

amounted to about 45 %.

iv. Increased social security contribution rate: In this scenario, from 2012

onwards the average social security contribution rate (including both

employers’ and employees’ contributions) is increased by 1 % point to about

22 % of the average gross wage.

5 Simulation results

The results of the simulations are visualised in Figs. 4, 5, 6, 7, 8, 9, 10. Each figure

depicts the respective variable in the baseline scenario (denoted by Baseline) and in

the reform scenarios: the increase in the retirement age with 75 % of the additional

labour force being employed (age_1), the increase in the retirement age with 25 %

of the additional labour force being employed (age_2), the scenario with a reduced

pension replacement rate (rep_rate), and the scenario with a higher social security

contribution rate (contr_rate).

Fig. 4 Budget balance in relation to GDP. Source Authors’ illustration

436 Empirica (2013) 40:427–456

123

Fig. 5 Public debt in relation to GDP. Source Authors’ illustration

Fig. 6 Pensions in relation to GDP. Source Authors’ illustration

Empirica (2013) 40:427–456 437

123

Fig. 7 Real GDP growth rate. Source Authors’ illustration

Fig. 8 Employment (persons). Source: Authors’ illustration

438 Empirica (2013) 40:427–456

123

Fig. 9 Unemployment (persons). Source Authors’ illustration

Fig. 10 Unemployment rate. Source Authors’ illustration

Empirica (2013) 40:427–456 439

123

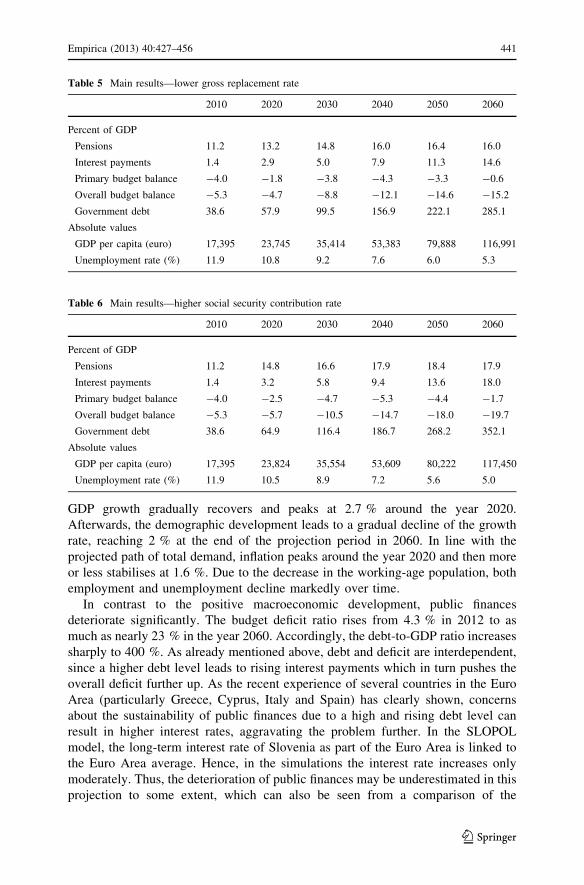

Tables 2, 3, 4, 5, 6 summarise the main results for the last year of the previous

and the following decades until 2060.

In terms of the macroeconomic performance, the baseline projection shows a

relatively favourable development. After the recession years 2011 and 2012, real

Table 2 Main results—baseline scenario

2010 2020 2030 2040 2050 2060

Percent of GDP

Pensions 11.2 14.8 16.5 17.9 18.3 17.9

Interest payments 1.4 3.5 6.5 10.6 15.3 20.4

Primary budget balance -4.0 -3.3 -5.4 -6.0 -5.1 -2.3

Overall budget balance -5.3 -6.8 -11.9 -16.5 -20.4 -22.7

Government debt 38.6 71.2 131.0 210.3 302.2 399.5

Absolute values

GDP per capita (euro) 17,395 23,809 35,554 53,610 80,216 117,430

Unemployment rate (%) 11.9 10.8 9.2 7.5 5.9 5.2

Table 3 Main results—higher pension age, 75 % find employment

2010 2020 2030 2040 2050 2060

Percent of GDP

Pensions 11.2 13.4 15.2 16.4 17.0 16.8

Interest payments 1.4 3.1 5.1 8.0 11.5 15.0

Primary budget balance -4.0 -1.7 -3.7 -4.2 -3.5 -1.1

Overall budget balance -5.3 -4.8 -8.9 -12.2 -15.0 -16.1

Government debt 38.6 62.7 102.7 160.0 226.3 293.8

Absolute values

GDP per capita (euro) 17,395 23,564 35,302 53,139 79,571 116,682

Unemployment rate (%) 11.9 12.9 11.3 10.1 8.4 7.3

Table 4 Main results—higher pension age, 25 % find employment

2010 2020 2030 2040 2050 2060

Percent of GDP

Pensions 11.2 13.1 14.8 16.0 16.6 16.5

Interest payments 1.4 3.6 6.4 10.3 14.8 19.6

Primary budget balance -4.0 -3.3 -5.1 -5.7 -4.8 -2.1

Overall budget balance -5.3 -6.9 -11.5 -16.0 -19.6 -21.7

Government debt 38.6 72.9 129.1 205.2 292.5 383.3

Absolute values

GDP per capita (euro) 17,395 23,156 34,825 52,329 78,456 115,397

Unemployment rate (%) 11.9 17.5 16.0 15.4 13.3 11.4

440 Empirica (2013) 40:427–456

123

GDP growth gradually recovers and peaks at 2.7 % around the year 2020.

Afterwards, the demographic development leads to a gradual decline of the growth

rate, reaching 2 % at the end of the projection period in 2060. In line with the

projected path of total demand, inflation peaks around the year 2020 and then more

or less stabilises at 1.6 %. Due to the decrease in the working-age population, both

employment and unemployment decline markedly over time.

In contrast to the positive macroeconomic development, public finances

deteriorate significantly. The budget deficit ratio rises from 4.3 % in 2012 to as

much as nearly 23 % in the year 2060. Accordingly, the debt-to-GDP ratio increases

sharply to 400 %. As already mentioned above, debt and deficit are interdependent,

since a higher debt level leads to rising interest payments which in turn pushes the

overall deficit further up. As the recent experience of several countries in the Euro

Area (particularly Greece, Cyprus, Italy and Spain) has clearly shown, concerns

about the sustainability of public finances due to a high and rising debt level can

result in higher interest rates, aggravating the problem further. In the SLOPOL

model, the long-term interest rate of Slovenia as part of the Euro Area is linked to

the Euro Area average. Hence, in the simulations the interest rate increases only

moderately. Thus, the deterioration of public finances may be underestimated in this

projection to some extent, which can also be seen from a comparison of the

Table 5 Main results—lower gross replacement rate

2010 2020 2030 2040 2050 2060

Percent of GDP

Pensions 11.2 13.2 14.8 16.0 16.4 16.0

Interest payments 1.4 2.9 5.0 7.9 11.3 14.6

Primary budget balance -4.0 -1.8 -3.8 -4.3 -3.3 -0.6

Overall budget balance -5.3 -4.7 -8.8 -12.1 -14.6 -15.2

Government debt 38.6 57.9 99.5 156.9 222.1 285.1

Absolute values

GDP per capita (euro) 17,395 23,745 35,414 53,383 79,888 116,991

Unemployment rate (%) 11.9 10.8 9.2 7.6 6.0 5.3

Table 6 Main results—higher social security contribution rate

2010 2020 2030 2040 2050 2060

Percent of GDP

Pensions 11.2 14.8 16.6 17.9 18.4 17.9

Interest payments 1.4 3.2 5.8 9.4 13.6 18.0

Primary budget balance -4.0 -2.5 -4.7 -5.3 -4.4 -1.7

Overall budget balance -5.3 -5.7 -10.5 -14.7 -18.0 -19.7

Government debt 38.6 64.9 116.4 186.7 268.2 352.1

Absolute values

GDP per capita (euro) 17,395 23,824 35,554 53,609 80,222 117,450

Unemployment rate (%) 11.9 10.5 8.9 7.2 5.6 5.0

Empirica (2013) 40:427–456 441

123

projected debt ratio of 550 % in the Slovenian Stability Programme (cf. Table 1)

and our projection of 400 % in 2060.

Among the pension reform options considered in the simulations, the reduced

pension replacement rate and the increase in the average retirement age are the most

effective measures to combat the deterioration of public finances, provided (in the

latter case) that most additional older people in the labour force find employment. In

the former scenario (rep_rate), the budget deficit rises to 15 % of GDP in 2060, in

the latter one (age_1), to 16 % in 2060. As a result, the debt ratio ‘‘only’’ increases

to 285 and 294 %, respectively, which means a reduction of more than one quarter

as compared to the baseline scenario.

On the other hand, if the retirement rate is increased but most of the additional

persons in the labour force become unemployed (age_2), the development of public

finances is less favourable. On average, the deficit ratio is then about 3 % points higher

as compared to scenario age_1. In the final year of the simulation period it amounts to

22 %. This is only less than 1 % point lower than in the baseline. The debt ratio

increases to 383 %, which is also closer to the baseline than to scenario age_1.

Regarding the labour market, both scenarios deviate markedly from the baseline

and from each other. In scenario age_1, over the period 2015 (the first year with a

higher retirement age in the simulations) to 2060, employment is on average about

35,000 persons higher than in the baseline. In scenario age_2, employment on average

deviates by 16,000 persons. In terms of unemployment, the differences are even more

pronounced. By 2060, the number of unemployed persons declines from 110,000 in

the year 2011 to less than 40,000 both in the baseline scenario and in the scenario with

the reduced replacement rate. In scenarios age_1 and age_2, due to the assumption that

not all people staying in the labour force find a job, unemployment decreases to 55,000

and 80,000, respectively. Hence, over the entire period of the implementation of the

higher retirement age (i.e. from 2015 onwards), unemployment is higher in both

reform scenarios age_1 and age_2. The budgetary improvement in these scenarios is

caused by the fact that the average unemployment benefit is significantly lower than

the average pension. In this respect, the reduction of the pension replacement rate is

more favourable, increasing unemployment only marginally over the values of the

baseline scenario.

With regard to other macroeconomic indicators such as real GDP growth and

inflation, the differences between the baseline and the scenarios with a higher

pension age are small. The oscillations of GDP growth and inflation are slightly

higher, but over time the reform scenarios converge to the baseline. This applies

also to the other reform scenarios considered here, i.e. a higher social security

contribution rate (contr_rate) and a reduced pension replacement rate (rep_rate). In

these cases, real GDP growth is close to its baseline values. The small effects on

output even in case of additional employment are due to a decrease in labour

productivity associated with the increase in the labour force.

With respect to the fiscal indicators, the reduction of the pension replacement rate

(rep_rate) gives a more favourable development than the increase in the social

security contribution rate (contr_rate). Altogether, the reduction of the pension

replacement rate appears as the most favourable scenario for reducing the burden of

ageing in Slovenia, although it nevertheless leads to an unsustainable fiscal

442 Empirica (2013) 40:427–456

123

development. Therefore alternative policy options will have to be considered, such

as encouraging immigration of younger qualified workers, measures aiming at

increasing labour force participation, and creating incentives for the development of

innovative and productive industries.

6 Summary and conclusions

Slovenia was hit hard by the ‘‘Great Recession’’ of 2008 and 2009, followed by a

muted economic recovery and weak economic prospects for the years to come. The

working of the automatic stabilisers and discretionary fiscal policy measures led to a

drastic deterioration of public finances. In the coming decades, the projected

demographic development will put considerable additional pressure on the fiscal

position. According to recent projections by the Slovenian government, age related

public expenditures will soar from about 25 % of GDP in 2010 to 35 % in 2060.

This will push up public debt. At the same time, potential and actual economic

growth is limited by a shrinking working-age population.

In this paper, we used the macroeconometric model SLOPOL to simulate

macroeconomic and fiscal effects of different pension reform options. According to

the simulation results, lowering the pension replacement rate is most effective in

limiting the increase in the budget deficit and hence public debt without strong

negative effects on the labour market. Raising the average retirement rate can have

similar effects on the fiscal position of the country, but only if most of the additional

older workers find employment. When most of the additional persons in the labour

force are unemployed, public debt rises nearly as much as in the baseline, i.e. without

any policy measures. An increase in the social security contribution rate is less

effective in coping with the fiscal consequences of population ageing than a lower

pension replacement rate. In any case, none of the analysed measures is sufficient to

stabilise the debt ratio at values close to the reference level of 60 % set in the

Maastricht treaty. Hence, even more drastic reforms than the relatively moderate

options considered in this paper will be required to fully offset the pressure from

population ageing on public finances. Also with respect to the macroeconomic

performance, the scenario with a lower pension replacement rate gave the best

results. A next step of research will have to augment the SLOPOL model by a more

detailed model bloc of the supply side as well as a more elaborate financial markets

bloc and to check for the sensitivity of our results with respect to these additions.

Appendix: the SLOPOL model

Model equations

Behavioural equations

In the following, the equations of the SLOPOL model are presented together with

some statistics. R2 is the adjusted coefficient of determination, p(LM) is the

probability level of false rejection of the null hypothesis of no serial correlation up

Empirica (2013) 40:427–456 443

123

to lag 4; t-statistics are given in parentheses below coefficients. All equations have

been estimated with ordinary least squares (OLS). Variable definitions are provided

in ‘‘List of variables’’.

Private consumption

log CRt=CRt�4ð Þ ¼ 0:0601:973ð Þ

þ 0:4534:164ð Þ

�log CRt�1=CRt�5ð Þ

� 0:040�1:443ð Þ

� log CRt�4ð Þ � 0:506� 0:933 � log INCOMERt�4ð Þ½ �

� 0:004�2:195ð Þ

�GOV10R

�0:050�2:730ð Þ

�UM00 � SEAS 2ð Þ þ 0:0452:461ð Þ

�DUM07 � SEAS 3ð Þ

R2 ¼ 0:451 p LMð Þ ¼ 0:4434

Gross fixed capital formation

log PRINVRt=PRINVRt�4ð Þ ¼ 0:4804:542ð Þ

�log PRINVRt=PRINVRt�4ð Þ

þ 0:9022:718ð Þ

�log GDPRt=GDPRt�4ð Þ

� 0:004�0:841ð Þ

� UCCt�1 � UCCt�5ð Þ

� 0:200�2:127ð Þ

� log PRINVRt�4ð Þ þ 3:587½

�1:233 � log GDPRt�4ð Þ�þ 0:549

1:228ð Þ�log UTILt=UTILt�4ð Þ

þ 0:1452:282ð Þ

�DUM00 � SEAS 3ð Þ

� 0:1512:293ð Þ

�DUM00 � SEAS 3ð Þ

R2 ¼ 0:763 p LMð Þ ¼ 0:7665

Exports of goods and services

log EXRt=EXRt�4ð Þ ¼ 0:3486:068ð Þ

�log EXRt�1=EXRt�5ð Þ

þ 0:72510:416ð Þ

�log WTRADEt=WTRADEt�4ð Þ

� 0:223�2:435ð Þ

�log REERt�4=REERt�8ð Þ

� 0:083�3:259ð Þ

�DUM09 � SEAS 1ð Þ

� 0:236�2:865ð Þ

� log EXRt�4ð Þ � 0:381½

�1:089 � log WTRADEt�4ð Þ�

R2 ¼ 0:919 p LMð Þ ¼ 0:1731

444 Empirica (2013) 40:427–456

123

Imports of goods and services

log IMPRt=IMPRt�4ð Þ ¼ � 0:011�1:726ð Þ

þ 0:1942:451ð Þ

�log IMPRt�1=IMPRt�5ð Þ

þ 1:7038:934ð Þ

�log GDPRt=GDPRt�4ð Þ

þ 0:1381:015ð Þ

�log REERt�1=REERt�5ð Þ

� 0:592�5:377ð Þ

� log IMPRt�4ð Þ þ 7:594½

�1:802 � log GDPRt�4ð Þ�

R2 ¼ 0:818 p LMð Þ ¼ 0:1075

Employment

log EMPt=POP1564tð Þ ¼ 0:2114:249ð Þ

�log GDPRtð Þ � 0:251�3:958ð Þ

�log AGWRtð Þ

� 0:102�5:280ð Þ

�log EMPt�4=AGWRt�4ð Þ

R2 ¼ 0:702 p LMð Þ ¼ 0:0000

Labour supply

PARTRATEt � PARTRATEt�4ð Þ ¼ �0:0006�1:059ð Þ

þ 0:7859:230ð Þ

� PARTRATEt�1 � PARTRATEt�5ð Þ

þ 0:0332:639ð Þ

�log NETWAGERt�4=NETWAGERt�8ð Þ

R2 ¼ 0:608 p LMð Þ ¼ 0:8018

Wages

log AGWNt=AGWNt�4ð Þ ¼ 0:0082:408ð Þ

þ 0:6046:228ð Þ

�log AGWNt�1=AGWNt�5ð Þ

þ 0:3533:233ð Þ

�log CPIt�1=CPIt�5ð Þ

þ 0:0200:413ð Þ

�log PRODt=PRODt�4ð Þ

� 0:0023�1:461ð Þ

� URt � NAIRUtð Þ

� 0:074�7:520ð Þ

�DUM08 � SEAS 4ð Þ

þ 0:0373:232ð Þ

�DUM09 � SEAS 1ð Þ

R2 ¼ 0:910 p LMð Þ ¼ 0:1982

Empirica (2013) 40:427–456 445

123

Consumer price index HICP

log CPIt=CPIt�4ð Þ ¼ �0:125�1:566ð Þ

þ 0:5547:623ð Þ

�log CPIt�1=CPIt�5ð Þ

þ 0:0993:412ð Þ

�log IMPDEFt=IMPDEFt�4ð Þ

þ 0:2804:332ð Þ

�log AGWNt=AGWNt�4ð Þ

� 0:122�2:424ð Þ

�log CPIt�4ð Þ þ 0:0511:449ð Þ

�log AGWNt�4ð Þ

þ 0:0591:446ð Þ

�log IMPDEFt�4ð Þ

R2 ¼ 0:940 p LMð Þ ¼ 0:2742

GDP deflator

log GDPDEFt=GDPDEFt�4ð Þ ¼ 0:5116:987ð Þ

þ 0:6426:468ð Þ

�log CPIt=CPIt�4ð Þ

� 0:904�6:233ð Þ

�log GDPDEFt�4ð Þ

þ 0:7965:887ð Þ

�log CPIt�4ð Þ

� 0:016�3:748ð Þ

�SEAS 1ð Þ

R2 ¼ 0:836 p LMð Þ ¼ 0:0001

Private consumption deflator

log CDEFt=CDEFt�4ð Þ ¼ 0:1542:821ð Þ

þ 0:2612:814ð Þ

�log CDEFt=CDEFt�4ð Þ

þ 0:6896:747ð Þ

�log CPIt=CPIt�4ð Þ

� 0:343�3:345ð Þ

�log CDEFt�1ð Þ

þ 0:3103:286ð Þ

�log CPIt�4ð Þ

� 0:0064�2:263ð Þ

�SEAS 1ð Þ

R2 ¼ 0:917 p LMð Þ ¼ 0:1063

Public consumption deflator

log GDEFt=GDEFt�4ð Þ ¼ �0:153�2:638ð Þ

þ 0:6129:057ð Þ

�log GDEFt�1=GDEFt�5ð Þ

þ 0:5305:269ð Þ

�log CPIt=CPIt�4ð Þ � 0:254�3:837ð Þ

�log GDEFt�4ð Þ

þ 0:2853:942ð Þ

�log CPIt�4ð Þ

� 0:030�2:881ð Þ

�DUM07 � SEAS 4ð Þ

R2 ¼ 0:902 p LMð Þ ¼ 0:1543

446 Empirica (2013) 40:427–456

123

Export deflator

log EXPDEFt=EXPDEFt�4ð Þ ¼ 0:1143:032ð Þ

þ 0:3565:569ð Þ

�log EXPDEFt�1=EXPDEFt�5ð Þ

þ 0:0671:822ð Þ

�log ULCt=ULCt�4ð Þ

þ 0:44710:119ð Þ

�log IMPDEFt=IMPDEFt�4ð Þ

� 0:241�3:065ð Þ

�log EXPDEFt�4ð Þ

þ 0:2162:825ð Þ

�log IMPDEFt�4ð Þ

� 0:033�3:487ð Þ

�DUM97 � SEAS 1ð Þ

R2 ¼ 0:930 p LMð Þ ¼ 0:6973

Import deflator

log IMPDEFt=IMPDEFt�4ð Þ ¼ 0:4522:685ð Þ

þ 0:5457:473ð Þ

�log IMPDEFt�1=IMPDEFt�5ð Þ

þ 0:0676:940ð Þ

�log OILEURt=OILEURt�4ð Þ

� 0:122�2:509ð Þ

�log IMPDEFt�4ð Þ

þ 0:0311:945ð Þ

�log OILEURt�4ð Þ

R2 ¼ 0:829 p LMð Þ ¼ 0:5254

Short-term interest rate

SLOR3Mt � SLO3Mt�4ð Þ ¼ 0:9379:785ð Þ

� EUR3Mt � EUR3Mt�4ð Þ

� 0:691�6:003ð Þ

� SLO3Mt�4 � EUR3Mt�4ð Þ

R2 ¼ 0:631 p LMð Þ ¼ 0:0000

Long-term interest rate

GOV10Yt ¼ �4:455�5:467ð Þ

þ 0:56812:313ð Þ

GOV10Yt�4 þ 0:1382:330ð Þ

SLO3Mt

þ 1:4676:171ð Þ

EUR10Yt�4

þ 2:0041:498ð Þ

�d log DEBTGDPtð Þ½ �

R2 ¼ 0:925 p LMð Þ ¼ 0:0013

Implicit interest rate on public debt

IGOVDEBTt ¼ 0:4863:338ð Þ

þ 0:0392:642ð Þ

�GOV10Yt þ 1:4248:961ð Þ

�SEAS 1ð Þ þ 1:0726:888ð Þ

SEAS 2ð Þ

R2 ¼ 0:606 p LMð Þ ¼ 0:0999

Empirica (2013) 40:427–456 447

123

Real effective exchange rate

log REERt=REERt�4ð Þ ¼ � 0:021�4:271ð Þ

þ 0:5448:587ð Þ

�log REERt�1=REERt�5ð Þ

þ 0:3192:159ð Þ

�log SITEURt=SITEURt�4ð Þ

þ 0:0984:830ð Þ

�log EURUSDt=EURUSDt�4ð Þ

þ 0:5593:904ð Þ

�log CPIt=CPIt�4ð Þ þ 0:0405:102ð Þ

�DUM09

þ 0:0584:256ð Þ

�DUM09 � SEAS 4ð Þ � 0:039�3:012ð Þ

�DUM10 � SEAS 1ð Þ

R2 ¼ 0:837 p LMð Þ ¼ 0:0157

Social security contributions by companies

log SOCCOMPt=SOCCOMPt�4ð Þ ¼ �0:387�15:790ð Þ

þ 0:98732:953ð Þ

�log SOCEMPt=SOCEMPt�4ð Þ

� 0:605�46:386ð Þ

�log SOCCOMPt�4ð Þ

þ 0:63752:059ð Þ

�log SOCEMPt�4ð Þ � 0:048�11:094ð Þ

�DUM97

� 0:034�3:983ð Þ

�DUM00 � SEAS 4ð Þ

þ 0:0212:754ð Þ

�DUM03 � SEAS 2ð Þ

R2 ¼ 0:987 p LMð Þ ¼ 0:0000

Corporate income tax payments

INCTAXCORPt � INCTAXCORPt�4ð Þ ¼ �18:274�4:368ð Þ

þ 0:1153:633ð Þ

�log INCTAXCORPt�1=INCTAXCORPt�5ð Þ

þ 0:0648:007ð Þ

� GDPNt � GDPNt�4ð Þ

þ 224:48914:698ð Þ

�DUM06 � SEAS 2ð Þ

� 66:773�4:280ð Þ

�DUM07 � SEAS 2ð Þ

� 321:155�18:494ð Þ

�DUM09 � SEAS 2ð Þ

� 113:465�7:363ð Þ

�DUM10 � SEAS 2ð Þ

þ 238:40815:459ð Þ

�DUM11 � SEAS 2ð Þ

R2 ¼ 0:956 p LMð Þ ¼ 0:3119

448 Empirica (2013) 40:427–456

123

Value added tax (VAT) revenues

log VATt=VATt�4ð Þ ¼ �1:550�3:169ð Þ

þ 1:3424:823ð Þ

�log VATAXRATEt�1 � CNt�1ð Þ= VATAXRATEt�5 � CNt�5ð Þð Þ

� 0:606�8:142ð Þ

�log VATt�4ð Þ þ 0:4817:166ð Þ

�log VATAXRATEt�4 � CNt�4ð Þ

� 0:557�5:107ð Þ

�DUM01 � SEAS 1ð Þ � 0:676�5:772ð Þ

�DUM01 � SEAS 1ð Þ

R2 ¼ 0:648 p LMð Þ ¼ 0:0524

Remaining, un-specified government revenues

log REVRESTt=REVRESTt�1ð Þ ¼ 0:0231:021ð Þ

þ 1:2044:422ð Þ

�log GDPNt=GDPNt�1ð Þ

� 0:246�5:685ð Þ

�SEAS 1ð Þ þ 0:1976:380ð Þ

�SEAS 4ð Þ

� 0:435�4:434ð Þ

�DUM02 � SEAS 1ð Þ

R2 ¼ 0:838 p LMð Þ ¼ 0:0129

Public consumption according to fiscal statistics

log GNFINt=GNFINt�4ð Þ ¼ �0:043�3:346ð Þ

þ 0:3033:492ð Þ

�log GNFINt�1=GNFINt�5ð Þ

þ 0:9728:174ð Þ

�log GNt=GNt�4ð Þ

� 0:109�2:159ð Þ

�log GNFINt�4=GNt�4ð Þ

� 0:142�4:485ð Þ

�DUM04 � SEAS 4ð Þ

R2 ¼ 0:778 p LMð Þ ¼ 0:4029

Remaining, un-specified government expenditures

EXPRESTt=EXPRESTt�1ð Þ ¼ �04:043�1:178ð Þ

þ 0:2628:612ð Þ

� REVRESTt � REVRESTt�1ð Þ

� 0:194�3:379ð Þ

�log EXPRESTt�4=REVRESTt�4ð Þ

� 0:447�4:697ð Þ

�DUM00 � SEAS 1ð Þ þ 0:2064:018ð Þ

�DUM04

R2 ¼ 0:505 pðLMÞ ¼ 0:4876

Empirica (2013) 40:427–456 449

123

Trend total factor productivity

log TRENDTFPt=TRENDTFPt�4ð Þ ¼ 0:0000041:500ð Þ

þ 3:87266:026ð Þ

�log TRENDTFPt�1=TRENDTFPt�4ð Þ

� 5:680�32:759ð Þ

�log TRENDTFPt�2=TRENDTFPt�6ð Þ

þ 3:73921:537ð Þ

�log TRENDTFPt�3=TRENDTFPt�7ð Þ

� 0:932�15:821ð Þ

�log TRENDTFP�4=TRENDTFPt�8ð Þ

� 0:000038�3:224ð Þ

�DUM09 � SEAS 3ð Þ

� 0:000042�3:627ð Þ

�DUM09 � SEAS 3ð Þ

R2 ¼ 0:9999 p LMð Þ ¼ 0:0078

Financial wealth

log FINWEALTHt=FINWEALTHt�4ð Þ ¼ 0:0302:665ð Þ

þ 0:1307:874ð Þ

�DUM07� 0:032�1:877ð Þ

�DUM09

þ 0:3873:848ð Þ

�log CAPRt � GDPDEFt=100ð Þ=½

CAPR�4 � GDPDEF�4=100ð Þ�

R2 ¼ 0:573 p LMð Þ ¼ 0:0000

Non-accelerating rate of unemployment (NAIRU)

Eight quarter moving average (UR)

Change in inventories (INVENTR)

Eight quarter moving average INVENTRð Þ þ 0:07 � INVENTRt�4

Identities

log YPOTð Þ ¼ 0:65 � log TRENDEMPð Þ þ 1� 0:65ð Þ � log CAPRð Þþ log TRENDTFPð Þ

OILEUR ¼ OIL=EURUSD

GR ¼ GN=GDEF � 100

AGWR ¼ AGWN=CPI � 100

CAN ¼ EXR � EXPDEF=100� IMPR � IMPDEF=100

CAGDP ¼ CAN=GDPN � 100

GRGDPR ¼ GDPR=GDPRt�4 � 100� 100

GRYPOT ¼ ðYPOT=YPOTt�4 � 1Þ � 100

PROD ¼ GDPR=EMP � 100

ULC ¼ AGWN=PROD

DEMAND ¼ INVR þ CRþ GRþ EXR

450 Empirica (2013) 40:427–456

123

INCOME ¼ NETWAGEN � EMP=1000000þ RESTTRANSFERS þ PENSIONS

þ UNBENEFIT � INCTAXCORPþ FINWEALTH � EUR10Y=400

INCOMER ¼ INCOME=CPI � 100

INFL ¼ ðCPI=CPIt�4 � 1Þ � 100

GOV10YR ¼ GOV10Y � INFL

UCC ¼ GOV10YRþ DEPR

INCTAXPERS ¼ INCTAXRATE � AGWN � EMP=1000ð Þ=100

SOCEMP ¼ SOCEMPRATE � AGWN � EMP=1000ð Þ=100

WEDGE ¼ AGWN � INCTAXRATE=100þ SOCEMPRATE=100ð ÞNETWAGEN ¼ AGWN �WEDGE

NETWAGER ¼ NETWAGEN=CPI � 100

SOCTOTAL ¼ SOCCOMPþ SOCEMP

INCTAX ¼ INCTAXPERS þ INCTAXCORP

CAPR ¼ 1� DEPR=100ð Þ � CAPRt�1 þ INVR

GDPR ¼ CRþ GRþ INVRþ INVENTRþ EXR� IMPR

GDPN ¼ GDPR � GDPDEF=100

CN ¼ CR � CDEF=100

TRENDEMP ¼ LFORCE � 1� NAIRU=100ð ÞUTIL ¼ GDPR=YPOT � 100

INTEREST ¼ IGOVDEBT � DEBTt�1=100

BALANCEN ¼ VAT þ SOCTOTALþ INCTAX þ REVREST � GNFIN

� GINVN � PENSIONS

� UNBENEFIT � RESTTRANSFERS � INTEREST � EXPREST

BALANCEGDP ¼ BALANCEN=GDPN � 100

DEBT ¼ DEBT�1 � BALANCEN þ DEBTADJ

DEBTGDP ¼ DEBT=ðGDPN þ GDPNt�1 þ GDPNt�2 þ GDPNt�3Þ � 100

GINVR ¼ GINVN=GDPDEF � 100

INVR ¼ PRINVRþ GINVR

Empirica (2013) 40:427–456 451

123

PENSIONERS ¼ PENSIONERS1549þ PENSIONERS50

þ PENSIONERS51þ PENSIONERS52

þ PENSIONERS53þ PENSIONERS54

þ PENSIONERS55þ PENSIONERS56

þ PENSIONERS57þ PENSIONERS58

þ PENSIONERS59þ PENSIONERS60

þ PENSIONERS61þ PENSIONERS62

þ PENSIONERS63þ PENSIONERS64

þ PENSIONERS65þ PENSIONERS66

þ PENSIONERS67þ PENSIONERS68

þ PENSIONERS69þ PENSIONERS70PLUS

POP1564 ¼ POP1549þ POP50þ POP51þ POP52þ POP53

þ POP54þ POP55þ POP56þ POP57þ POP58

þ POP59þ POP60þ POP61þ POP62þ POP63þ POP64

AVPENSION ¼ REPRATE � AGWN

PENSIONS ¼ AVPENSION � PENSIONERS=1000000

AVUNBENEFIT ¼ UNBENEFITRATE � AGWN

UNBENEFIT ¼ AVUNBENEFIT � UN=1000000

LFORCE ¼ PARTRATE � POP1564

UN ¼ LFORCE � EMP

UR ¼ UN=LFORCE � 100

List of variables

Endogenous variables

AGWN Average gross wage per employee

AGWR Average real gross wage

AVPENSION Average pension

AVUNBENEFIT Average unemployment benefit

BALANCEN Budget balance

BALANCEGDP Budget balance in relation to GDP

CAN Current account balance

CAGDP Current account balance in percent of GDP

CAPR Capital stock, real

CDEF Private consumption deflator

CN Private consumption, nominal

CPI HICP for Slovenia

452 Empirica (2013) 40:427–456

123

CR Private consumption, real

DEBT Public debt

DEBTGDP Debt level in relation to GDP

DEMAND Final demand, real

EMP Employed persons

EXPDEF Export deflator

EXPREST Remaining, unspecified government expenditures

EXR Exports, real

FINWEALTH Financial wealth

GDEF Public consumption deflator

GDPDEF GDP deflator

GDPN GDP, nominal, Mio. euro

GDPR GDP, real, Mio euro, chained volumes

GINVR Real government investment

GNFIN Government consumption, financial statistics

GOV10Y Yield of 10 year government bonds

GOV10YR Real government bond yield

GR Government consumption, real

GRGDPR Real GDP growth rate

GRYPOT Growth rate of potential GDP

IGOVDEBT Implicit interest rate on government debt (quarterly rate)

IMPDEF Import deflator

IMPR Imports, real

INCOME Disposable income of private households, nominal

INCOMER Disposable income of private households, real

INCTAX Total income tax revenues

INCTAXCORP Corporate taxes on income and profit

INCTAXPERS Individual taxes on income and profit

INFL Inflation rate

INTEREST Interest payments on outstanding public debt

INVENTR Change in inventories (? statistical discrepancy), real

INVR Gross fixed capital formation, real

LFORCE Labour force

NAIRU Non-accelerating inflation rate of unemployment

NETWAGEN Gross wage minus average income taxes and soc. secur.

contributions

NETWAGER Net wage, real

OILEUR Oil price in euro

PARTRATE Labour force participation rate

PENSIONERS Number of pensioners

PENSIONS Pensions paid by Pension Fund

POP1564 Population aged 15 to 64

PRINVR Real private investment

PROD Labour productivity

REER41 Real effective exchange rate, 41 partners, CPI based (Eurostat)

Empirica (2013) 40:427–456 453

123

REVREST Remaining government revenues

SLO3 M 3 months interest rate in Slovenia. Source: OECD, MEI

SOCCOMP Social security contributions by companies

SOCEMP Employees’ social security contributions

SOCTOTAL Social security contributions by employers and employees

TRENDEMP Trend of employment

TRENDTFP Trend of total factor productivity

UCC User cost of capital

ULC Unit labour cost

UN Unemployed persons

UR Unemployment rate

UNBENEFIT Total unemployment benefits

UTIL Capacity utilisation rate

VAT VAT and sales tax revenues

WEDGE Tax wedge on gross wages

YPOT Potential output

Exogenous variables

DEBTADJ Difference between change in public debt level and budget

balance

DEPR Capital stock depreciation rate

DUM97 Dummy variable, 1 in 1997, 0 otherwise

DUM98 Dummy variable, 1 in 1998, 0 otherwise

DUM99 Dummy variable, 1 in 1999 0 otherwise

DUM00 Dummy variable, 1 in 2000, 0 otherwise

DUM01 Dummy variable, 1 in 2001, 0 otherwise

DUM02 Dummy variable, 1 in 2002, 0 otherwise

DUM03 Dummy variable, 1 in 2003, 0 otherwise

DUM05 Dummy variable, 1 in 2005, 0 otherwise

DUM06 Dummy variable, 1 in 2006, 0 otherwise

DUM07 Dummy variable, 1 in 2007, 0 otherwise

DUM08 Dummy variable, 1 in 2008, 0 otherwise

DUM09 Dummy variable, 1 in 2009, 0 otherwise

DUM10 Dummy variable, 1 in 2010, 0 otherwise

DUM11 Dummy variable, 1 in 2011, 0 otherwise

SEAS(i) Seasonal Dummy: 1 in quarter i, 0 otherwise

EUR10Y 10 year government bond yield, Euro Area average

EUR3 M 3 months EURIBOR

EURUSD Exchange rate USD per EUR

GINVN Public investment, nominal

GN Government consumption, nominal

NCTAXRATE Average personal income tax rate

OIL Oil price, USD per barrel Brent

454 Empirica (2013) 40:427–456

123

PENSIONERS1549 Pensioners aged 15 to 49

PENSIONERS50 Pensioners aged 50

PENSIONERS51 Pensioners aged 51

PENSIONERS52 Pensioners aged 52

PENSIONERS53 Pensioners aged 53

PENSIONERS54 Pensioners aged 54

PENSIONERS55 Pensioners aged 55

PENSIONERS56 Pensioners aged 56

PENSIONERS57 Pensioners aged 57

PENSIONERS58 Pensioners aged 58

PENSIONERS59 Pensioners aged 59

PENSIONERS60 Pensioners aged 60

PENSIONERS61 Pensioners aged 61

PENSIONERS62 Pensioners aged 62

PENSIONERS63 Pensioners aged 63

PENSIONERS64 Pensioners aged 64

PENSIONERS65 Pensioners aged 65

PENSIONERS66 Pensioners aged 66

PENSIONERS67 Pensioners aged 67

PENSIONERS68 Pensioners aged 68

PENSIONERS69 Pensioners aged 69

PENSIONERS70PLUS Pensioners aged 70 plus

POP1549 Population aged 15 to 49

POP50 Population aged 50

POP51 Population aged 51

POP52 Population aged 52

POP53 Population aged 53

POP54 Population aged 54

POP55 Population aged 55

POP56 Population aged 56

POP57 Population aged 57

POP58 Population aged 58

POP59 Population aged 59

POP60 Population aged 60

POP61 Population aged 61

POP62 Population aged 62

POP63 Population aged 63

POP64 Population aged 64

REPRATE Pension replacement rate

RESTTRANSFERS Remaining public transfers to private households

SITEUR Exchange rate euro per 100 tolar

SOCEMPRATE Average social security contribution rate, employees

UNBENEFITRATE Unemployment benefit rate

VATAXRATE VAT rate

WTRADE World trade; Source: OECD

Empirica (2013) 40:427–456 455

123

References

Auerbach AJ, Lee RD (eds) (2001) Demographic change and fiscal policy. Cambridge University Press,

Cambridge, UK

Balassone F, Cunha J, Langenus G, Manzke B, Pavot J, Prammer D, Tommasino P (2011) Fiscal

sustainability and policy implications: a post-crisis analysis for the euro area. Int J Sustain Econ

3:210–234

Banca d’Italia (ed) (2009) Pension reform. Fiscal policy and economic performance. Banca d’Italia,

Rome

European Commission (2012a) The 2012 ageing report economic and budgetary projections for the 27

EU Member States (2010–2060). European Economy 2/2012, Brussels

European Commission (2012b), European Economic Forecast. Autumn 2012 European Economy 7/2012,

Brussels

IMF (2012) World economic outlook. October 2012. Coping with High Debt and Sluggish Growth.

Washington

Kasek L, Laursen L, Skrok E (2008) Sustainability of pension systems in the New EU Member States and

Croatia. World Bank Working paper no. 129. World Bank, Washington

OECD (2012), OECD Economic outlook No. 92. November 212, Paris

Slovenian Ministry of Finance (2012), Stability programme, Republic of Slovenia, 2012 update. Mimeo,

Ljubljana

Stanovnik T, Turk E, Rupel VP (2012) Annual National Report 2012. Pensions, Health Care and Long-

term Care. Slovenia. March 2012. Report on behalf of the European Commission, DG Employment,

Social Affairs and Inclusion

Weyerstrass K, Neck R, Blueschke D (2011) Optimal macroeconomic policies in a financial and

economic crisis: a case study for Slovenia. Empirica 38:435–459

456 Empirica (2013) 40:427–456

123