a uu ii n a a ncc

TRANSCRIPT

AANNNNUUAALL FFIINNAANNCCIIAALL SSTTAATTEEMMEENNTTSS 22002200 ((0011..0011..22002200 -- 3311..1122..22002200))

iinn ccoommpplliiaannccee wwiitthh IIFFRRSS

PANCRETA BANK | ANNUAL FINANCIAL STATEMENTS FOR THE PERIOD FROM 01.01.2020 TO 31.12.2020 | - 2- |

Table of Contents

Α. Representations of the Board of Directors .................................................................................................... 5 Β. Independent Auditors Report .......................................................................................................................... 6 C. Annual Management Report ........................................................................................................................... 9 D. Annual Financial Statements for the period 1.1.2020 – 31.12.2020 ............................................................. 22 Ε. Notes to Financial Statements 2020............................................................................................................. 26 1. General information about the Bank ........................................................................................................ 26 2. Bases for the preparation of the annual Financial Statements ............................................................... 26 2.1. General Information .......................................................................................................................... 26 2.2. Going concern assumption ............................................................................................................... 26 2.3. New Accounting Standards and Interpretations .............................................................................. 28 2.5. Cash and cash equivalents ............................................................................................................... 31 2.6. Financial instruments ......................................................................................................................... 31 2.7. Associates .......................................................................................................................................... 35 2.8. Investment property ........................................................................................................................... 35 2.9. Intangible assets ................................................................................................................................ 35 2.10. Property, plant and equipment ......................................................................................................... 36 2.12. Income tax and deferred tax ............................................................................................................ 37 2.13. Foreclosed assets .............................................................................................................................. 37 2.14. Other financial liabilities ................................................................................................................... 37 2.16. Employee benefits ............................................................................................................................. 38 2.17. Equity ................................................................................................................................................. 38 2.19. Leases ................................................................................................................................................ 38 2.20. Revenue recognition .......................................................................................................................... 39 2.21. Earnings per share ............................................................................................................................ 40 2.23. Reporting segments ........................................................................................................................... 40 3.2. Recoverability of deferred taxes ....................................................................................................... 41 4. Risk Factors ................................................................................................................................................ 42 4.1. Risk management framework............................................................................................................ 42 4.3. Rusks related to Greek economy ...................................................................................................... 42 4.4. Financial risks .................................................................................................................................... 43 4.4.1. Credit risk ........................................................................................................................................... 43 4.4.2. Interest rate risk ................................................................................................................................. 55 4.4.3. Liquidity risk ....................................................................................................................................... 56 4.5. Operational risk ................................................................................................................................. 58 4.6. Capital adequacy .............................................................................................................................. 58 4.7. Regulatory risk ................................................................................................................................... 59 4.8. Market risk ......................................................................................................................................... 60 4.9. Foreign currency risk ......................................................................................................................... 60 4.10. Other risks .......................................................................................................................................... 60 5. Net interest income ................................................................................................................................... 61 6. Net commission income ............................................................................................................................. 61 7. Results of financial operations, dividends and other income ................................................................... 62 8. Payroll expenses ........................................................................................................................................ 63 9. General administrative expenses .............................................................................................................. 63 10. Other operating expenses................................................................................................................. 64 11. Provisions for impairment of receivables .......................................................................................... 64 12. Other results ...................................................................................................................................... 64 13. Deferred tax and other tax charges ................................................................................................. 65 15. Cash and balance with the Central Bank ......................................................................................... 65 16. Receivables from credit institutions .................................................................................................. 65 17. Financial assets ................................................................................................................................. 66 19. Tangible assets .................................................................................................................................. 70 20. Investment property ........................................................................................................................... 70 21. Intangible assets ................................................................................................................................ 71

PANCRETA BANK | ANNUAL FINANCIAL STATEMENTS FOR THE PERIOD FROM 01.01.2020 TO 31.12.2020 | - 3- |

22. Deferred tax assets ............................................................................................................................ 71 23. Other assets ....................................................................................................................................... 73 24. Foreclosed assets .............................................................................................................................. 73 25. Liabilities to central banks ................................................................................................................ 73 26. Liabilities to other credit institutions ................................................................................................. 74 27. Liabilities to customers ...................................................................................................................... 74 28. Debt securities and other borrowed funds ....................................................................................... 74 29. Employee benefits obligations .......................................................................................................... 75 30. Other liabilities .................................................................................................................................. 76 31. Share capital ..................................................................................................................................... 76 32. Share premium .................................................................................................................................. 77 33. Other reserves, retained earnings .................................................................................................... 77 34. Analysis of changes in financing activities ....................................................................................... 78 35. Leases ................................................................................................................................................ 78 40. Other information .............................................................................................................................. 80 (Potential differences in the amounts are due to rounding)

PANCRETA BANK | ANNUAL FINANCIAL STATEMENTS FOR THE PERIOD FROM 01.01.2020 TO 31.12.2020 | - 4- |

Title Pancretan Cooperative Bank LTD

Legal Framework

The Bank was constituted following the transition of the "PANCRETAN COOPERATIVE BANK Co." to a Société anonyme, in compliance with (i) the decision as of 28.06.2020 of the General Meeting of its members, registered in G.E.MI. on 24.07.2020 under K.A.K. 2181040 (ii) the act of transformation under number 17092 / 03-07-2020 of the notary of Heraklion Styliani Kalogeraki-Archontaki, registered in G.E.MI. on 24.07.2020 under K.A.K. 2181075 and (iii) number 4909 / 24.07.2020 (ΑΔΑ 61Μ4469ΗΛΞ - Θ4Θ) Decision of the Head of the G.E.MI. Service of the Chamber of Heraklion. The framework of foundation, operation and activity of the Bank is defined by the provisions of: a) Law 4548/2018 as applicable, b) Law 4261/5.5.2014, c) the Bank's Charter.

Year of foundation 1993

Operating License of Cooperative Credit Institution Bank of Greece Governor's Act 2306/19.5.1994

Number of Branches 42 branches, 9 sub-branches, 62 ΑΤΜ

Hellenic Business Registry Number 077156527000

T.I.N. - Tax Authority 096121548 , Tax Authority of Heraklion

Address 5 Ikarou Avenue, P.C. 71306, Heraklion, Crete

Phone 2810 338800

Website www.pancretabank.gr

E-mail Address [email protected]

Composition of Board of Directors

Executive Members

Chief Executive Officer Antonios Vartholomeos

Deputy Chief Executive Officer Georgios Kourletakis

Non-Executive Members

Chairman Dimitrios Dimopoulos

Α’ Vice President Iosif Sifakis

B’ Vice President Georgios Sallas

C’ Vice President Antonios Vasilakis

Independent Non-Executive Member Iordanis Hatzikonstantinou

Other Non-Executive Members Konstantinos Papadakis

Stylianos Vorgias

The current Annual Financial Report comprises as follows: (Α) Representations of the Board of Directors, (Β) Independent Auditor’s Report, (C) Board of Directors’ Annual Report, (D) Annual Financial Statements for Financial Year 2020 (1.1 – 31.12.2020), and (Ε) Notes to Financial Statements for Financial Year 2020 (1.1 – 31.12.2020).

PANCRETA BANK | ANNUAL FINANCIAL STATEMENTS FOR THE PERIOD FROM 01.01.2020 TO 31.12.2020 | - 5- |

Α. Representations of the Board of Directors The below statements are made by the following Members of the Board of Directors of Pancreta Bank SA:

1. Dimitrios G. Dimopoulos, Chairman of the Board of Directors, 2. Antonios M. Vartholomeos, Chief Executive Officer 3. Georgios P. Kourletakis, Deputy Chief Executive Officer

We certify, that as far as we know: a) The Annual Financial Statements for the financial year ended as of December 31, 2020, were prepared according to the effective I.F.R.S., present truly and fairly the Assets and Liabilities, the Equity and the Financial Results of Pancreta Bank , and b) The Board of Directors Annual Report provides a true view of the Banks performance and results including a description of the main risks and uncertainties it is exposed to.

Heraklion, 30 June 2021

The Chairman of the Board of Directors

The Chief Executive Officer The Deputy Chief Executive Officer

Dimitrios G. Dimopoulos Antonios M. Vartholomeos Georgios P. Kourletakis

PANCRETA BANK | ANNUAL FINANCIAL STATEMENTS FOR THE PERIOD FROM 01.01.2020 TO 31.12.2020 | - 6- |

Β. Independent Auditors Report Independent Auditors Report To the Shareholders of “PANCRETA BANK SA” Report on the financial statements Opinion We have audited the accompanying financial statements of “PANCRETA BANK SA”(the Bank), which comprise the statement of financial position as at December 31st, 2020, the statements of comprehensive income, changes in equity and cash flows for the year then ended and a summary of significant accounting policies and other explanatory information. In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position of the Bank as at 31 December, 2020, its financial performance and cash flows for the year then ended, in accordance with International Financial Reporting Standards (I.F.R.S.), as adopted by the European Union. Material uncertainty related to going concern We draw your attention to Notes 2.2 and 4.6 to the financial statements, in particular to the following issues: a) the Bank's capital surplus as at 31.12.2020 is limited (Total Capital Ratio), b) its operating profitability does not provide sufficient margin to absorb expected credit losses that may increase due to the overall slowdown in economy arising from COVID-19 as well as the actions taken by the Management in order to facilitate frontloaded decrease in NPEs, and) c) the intended increase in the share capital of the Bank that may be necessary for maintaining its capital adequate which is a future event not controlled exclusively by the Bank. The above events indicate the existence of substantial uncertainty that may cast significant doubt on the Bank's ability to continue as a going concern. Our opinion is not qualified in respect of this matter. Key audit matters Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of the financial statements of the current period. These matters, as well as the related risks of significant misstatement, were addressed in the context of our audit of the financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters. Impairment of loans and receivables from clients at amortized cost Description Addressing As at 31 December, 2020, loans and other receivables from the Bank’s clients stood at € 1,23 billion, compared to € 1,145 billion as at 31 December, 2019, after accumulated provisions for impairment losses of € 342 million as at 31 December, 2020, compared to € 340 million as at 31 December, 2019. The Bank calculates the provision for impairment of loans in accordance with IFRS 9 on an individual or collective basis. IFRS 9 refers to the expected credit losses (ECL). Measurement of expected credit losses requires the use of complex models, as well as a significant number of estimates and assumptions regarding the future economic conditions and potential behavior of borrowers. Given the significance of the factors, mentioned below, we considered that impairment of loans from customers constitutes a key audit matter and a significant audit risk: Significance of the size of the loans in the financial

statements. Complexity of the loan impairment calculation. Subjectivity of the management's estimates and

assumptions required for that purpose. Effect of COVID-19 pandemic on making estimates, on

the Greek economy and tourism to which the Bank has a high exposure.

Note 2.6 to the Bank’s financial statements refers to the key accounting policies and note 4.4.1 discloses credit risk.

Following the Risk-Based Approach, we evaluated the methodology and policies applied by the management in relation to impairment of loans and receivables from clients. Our audit procedures included, inter alia, the following: We assessed completeness of IFRS 9 application, giving special emphasis on methodology, policies and significant assumptions applied by the management in order to determine the expected credit losses. In particular: We assessed the business model and the appropriate

classification of financial assets at amortized cost based on assessment of contractual cash flows solely relating to capital and interest payments (SPPI test)

We assessed consistency of the methodology followed while staging

We assessed the reasonableness of the assumptions used by the management under applying the expected credit loss model and the amendments required due to Covid-19 pandemic.

We reviewed the procedures applied in calculating the expected credit loss and examined the reasonableness of the amount in relation to the exposure classification and key assumptions of the model (PD, LGD, Cure rate), definition of default and macroeconomic assumptions.

We confirmed, on a sample basis, the reasonableness of the key assumptions used to measure impairment of individually assessed exposures, existence and valuation of collaterals as well as other specific characteristics of the loan.

We assessed the design and implementation of internal controls related to calculating expected credit losses (ECL) based on the applied methodology.

Furthermore, we received the loan tape of the Bank in electronic form and examined: sound technical functioning of the formulas applied for

calculating expected credit loss and other quantitative parameters and data.

PANCRETA BANK | ANNUAL FINANCIAL STATEMENTS FOR THE PERIOD FROM 01.01.2020 TO 31.12.2020 | - 7- |

the numerical agreement and accuracy with the Bank's Trial Balance and the respective accounts of the financial statements.

We evaluated the extent to which the disclosures in the financial statements adequately reflect the volume of the credit risk.

Recoverability of deferred tax assets Description Addressing As at December 31, 2020, deferred tax assets of the Bank amounted to € 67.9 million, compared to € 69.67 million as at 31 December, 2019, of which, an amount of € 45 million is not necessarily based on future profitability but pertains to deferred tax assets within the meaning of Article 27A of Law 4172/2013, according to which the Bank can convert deferred tax assets (DTA) to deferred tax credit (DTC). The measurement of recoverability of deferred tax assets is considered a key audit matter as it is highly subjective in terms of assumptions and expectations regarding the existence of future taxable profits and the assessment of the special tax framework (articles 27 & 27A of Law 4172/2013).

Following the Risk-Based Approach we evaluated the method used by the management in order to determine the recoverable amount of deferred tax assets and we examined the banks business plan as well as the assumptions used regarding the existence of future taxable profits. Our audit procedures included, inter alia, the following: We evaluated the design and implementation of internal controls related to the preparation and the review of budgets and expectations, including internal controls related to significant estimates, data, calculation and applied methodologies. We evaluated the management's estimate regarding the recent changes in the tax legislation affecting the balance of the deferred tax assets, in particular, the provisions of articles 27 and 27A of Law 4172/2013. We evaluated the reasonableness of the most significant assumptions and expectations of the management regarding future taxable profits in the light of confirming these expectations historically, based on current results and tax legislation. We evaluated the extent to which the disclosures relating to the recoverability of deferred tax assets in the financial statements are adequate.

Financial reporting ΙΤ systems Description Addressing Information systems operation and governance is a matter of high significance, since it ensures their sound operation, reliability and availability, while at the same time providing a protection framework for security, integrity, validity and accuracy of the data managed by the Bank. Consequently, the Banks’ financial reporting significantly depends significantly on its information systems as well as the automated procedures and controls of these systems. Given the complexity of these systems as well as the nature and the volume of transactions, conducted on a daily basis, the risk of error and inefficient communication between information systems is considered increased. In particular, the risk is identified in case there are incomplete or non-existent procedures and controls at entity level (General IT controls) regarding the following procedures:

Security administration Program maintenance controls Program execution controls

Should the Bank's controls not function effectively and/or are not replaced or adequately mitigated, the diffuse effect of such controls may affect our ability to ensure the completeness and accuracy of the financial reporting, recorded in the financial statements.

Our audit procedures include the following: We obtained understand of the IT environment

assisted by an IT specialist in order to identify the relevant risks.

We discussed the issues with the IT administrators and carried out walkthroughs in order to evaluate the design and implementation of the relevant general controls (General IT controls /design and implementation testing).

We confirmed the effectiveness of the general IT controls (testing of operating effectiveness).

PANCRETA BANK | ANNUAL FINANCIAL STATEMENTS FOR THE PERIOD FROM 01.01.2020 TO 31.12.2020 | - 8- |

Other information The management is responsible for the other information. The other information included in the Annual Financial Report, comprise of the Board of Director’s Report, reference to which is made in the “Report on Other Legal and Regulatory Requirements” section of our Report and the Statements of the Members of the Board of Directors, but not of the financial statements and the auditor’s report thereon. Our opinion on the financial statements does not cover the other information and we will not express with this opinion any form of assurance conclusion thereon. In connection with our audit of the Bank’s financial statements, our responsibility is to read the other information identified above and, in doing so, consider whether the other information is materially inconsistent with the financial statements or our knowledge obtained in the audit, or otherwise, appears to be materially misstated. If, based on the audit work performed, we conclude that there is a material misstatement therein, we are required to communicate that matter. No such issue has arisen. Responsibilities of management and of those charged with governance for the financial statements The management is responsible for the preparation and fair presentation of the financial statements in accordance with I.F.R.S., as adopted by the European Union, as well as for those internal controls the management determines as necessary, in order the preparation of financial statements that are free from material misstatement, whether due to fraud or error, to be possible. During preparing the financial statements, the management is responsible for assessing the Bank’s ability to continue as a going concern, disclosing, when applicable, matters related to going concern and the use of going concern basis of accounting, unless the management’s intention is to proceed with liquidating the Bank or discontinuing its operations, or has no other realistic option but to proceed with those actions. The Banks’s Audit Committee (article 44, Law 4449/2017) is responsible for overseeing the Bank’s financial reporting process. Auditor’s responsibilities for the audit of the financial statements Our objectives are to obtain reasonable assurance about whether the financial statements, as an aggregate, are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report, which includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that the audit conducted in accordance with ISAs, incorporated into the Greek Legislation, will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to affect the economic decisions of users, taken on the basis of these financial statements. As duty of the audit, in accordance with ISAs, as incorporated into the Greek Legislation, we exercise professional judgment and maintain professional skepticism throughout the audit. We also: Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, by designing and performing audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than that resulting from error, as fraud may include collusion, forgery, intentional omissions, misrepresentations, or the override of internal controls. Obtain an understanding of the internal controls relevant to the audit, in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Bank’s internal controls. Evaluate the appropriateness of accounting principles and policies used and the reasonableness of the accounting estimates and the related disclosures made by the management. Conclude on the appropriateness of management’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Bank’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in the auditor’s report to the related disclosures in the financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on audit evidence obtained up to the date of the auditor’s report. However, future events or conditions may cause the Bank to cease to continue as a going concern. Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether the financial statements represent the underlying transactions and events in a manner that achieves fair presentation. We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit, as well as significant audit findings, including any significant deficiencies in internal controls that we identify during our audit. We also provide those charged with governance with a statement that we have complied with the relevant ethical requirements regarding independence, and we communicate with them all relationships and other matters that may reasonably be thought to bear on our independence, and where applicable, related safeguards. From the matters communicated with those charged with governance, we determine those matters that were of most significance in the audit of the financial statements of the current period and are therefore the key audit matters. Report on Other Legal and Regulatory Requirements 1. Board of Directors’Report

Taking into consideration the fact that under the provisions of paragraph 5, article 2 of Law 4336/2015 (part B), the management has the responsibility for the preparation of the Board of Directors’ Report included into this Annual Financial Report, the following is to be noted:

1. In our opinion, the Board of Directors’ Report has been prepared in compliance with the effective legal requirements of Articles 150-151, Law 4548/2018 and its content corresponds to the accompanying financial statements for the year ended as at 31/12/2020.

2. Based on the knowledge we acquired during our audit, regarding PANCRETAN COOPERATIVE BANK Ltd” and its environment, we have not identified any material misstatements in the Board of Directors’ Report.

2. Additional Report to the Audit Committee Our opinion on the accompanying financial statements is consistent with our Additional Report to the Bank’s Audit Committee,

PANCRETA BANK | ANNUAL FINANCIAL STATEMENTS FOR THE PERIOD FROM 01.01.2020 TO 31.12.2020 | - 9- |

prepared in compliance with article 11, regulation (EU) No 537/2014. 3. Provision of Non-Audit Services

We have not provided the Bank with the prohibited non-audit services referred to in article 5 of regulation (EU) No 537/2014. Non-prohibited non-audit services provided by us to the Bank during the year ended as at December 31, 2020, are disclosed in note 41 to its accompanying financial statements. 4. Auditor’s Appointment

We were first appointed as the Bank’s Chartered Accountants following as of 14.5.1995 decision of the annual regular general meeting of the partners. We were appointed again as the Bank’s Chartered Accountants following as of 11.5.1997 decision of the annual regular general meeting of the partners. Since then, our appointment has been constantly renewed for a total period of 24 years in compliance with the decisions of the annual regular general meetings of the partners.

Heraklion, 09 July 2021

The Chartered Accountant

Emmanouil Nik. Diamantoulakis S.O.E.L. Reg. Num. 13 101

C. Annual Management Report

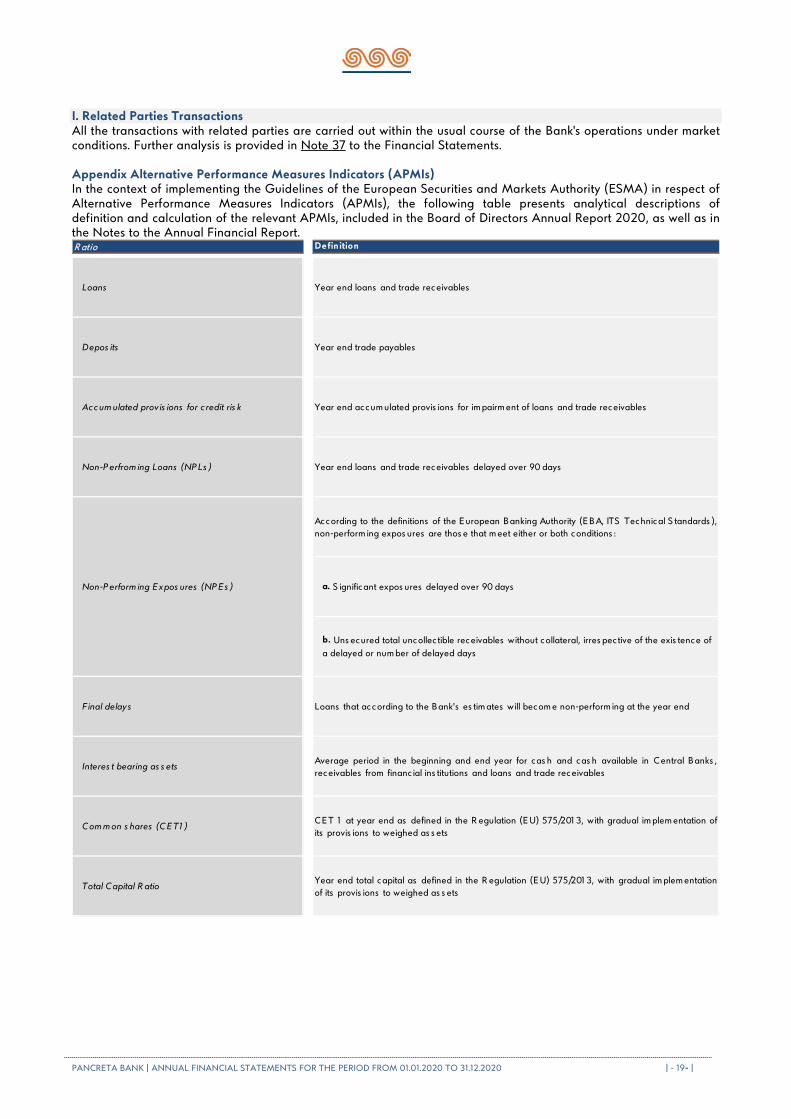

The current Annual Report of the Board of Directors (hereinafter referred to as «the Report») pertains to the annual financial year 2020 (1.1.2020 – 31.12.2020). The current Report has been prepared and is in compliance with the relevant provisions of Article 150 – 152 of the Law 4548/18. The current Report fairly presents all the relative and legally mandatory financial information in order to provide the users of financial statements with meaningful and comprehensive information regarding the Pancretan Cooperative Bank Ltd (hereinafter referred to as the «Bank» or «Pancreta») operations within the aforementioned period. The Report, as well as the Financial Statements of the Bank and all the legally required data and statements are included in the Annual Financial Report for the financial year 2020. SECTION Α. Greek Economy SECTION B. Hellenic Bank System SECTION C. Pancreta Bank (Significant Events & Issues) SECTION D. Financial Sizes and Performance in 2020 SECTION Ε. Risk Management SECTION F. Prospects for the Future SECTION G. Non-financial information SECTION H. Publication of information under Article 6, Law 4374/2016 SECTION I. Related Parties Transactions Appendix Alternative Performance Measures Indicators (APMIs)

PANCRETA BANK | ANNUAL FINANCIAL STATEMENTS FOR THE PERIOD FROM 01.01.2020 TO 31.12.2020 | - 10- |

Α. Greek Economy

Since the end of the first quarter of 2020, the coronavirus pandemic has reversed the course of the mild recovery, in which the Greek economy had entered since 2017, setting as an immediate priority of economic policy the protection of public health and the containment of the economic losses in income and employment in order to avoid the risk of turning a temporary recession into a long-term economic crisis. Economic activity recorded significant decrease due to the COVID-19 pandemic and the restrictions imposed to address it. GDP decreased by 8.2% versus foxed prices of 2015, as both domestic and external demand shrank. Tourism activity has decreased due to the global spread of the virus and the restrictive measures taken by most governments. At the same time, suspension of operations or under-operation of companies due to restrictive measures, especially in the second and fourth quarters of the year, had an adverse impact mainly on the segment of services. The development of financial ratios and the economic climate during 2020 reflects the course of the pandemic. Business expectations have deteriorated compared to the high levels of 2019, while the consumer confidence index has lost much of the improvement in recent years. The Purchasing Managers' Index (PMI) recorded large fluctuations during the year, while the industrial production volume index decreased by 2.1%. Retail sales decreased by 4.0% in terms of volume, while passenger car sales also decreased (for the first time since 2012) (-26.6%). Multiple fiscal measures have been taken and remain effective to support businesses and employees, which, in combination with the policy actions of the European institutions - which include fiscal, monetary and structural interventions - have significantly reduced the impact. The fiscal support measures of 11.2% of GDP implemented in 2020 and the recession led to a sharp shift in the general government fiscal output from a surplus to a deficit and combined with the sharp decline in nominal output, to a significant increase in the debt-to-GDP ratio. Specifically, based on the revised provisions of the Bank of Greece, it is estimated that in 2020 the general government deficit according to the definition of enhanced supervision - will amount to 7.0% of GDP, compared to a surplus of 3.6% of GDP in 2019. Government debt is estimated to have increased to 205% of GDP in 2020, from 180.5% of GDP in 2019, mainly due to the reduction in nominal GDP. The contribution of the difference between the indirect lending rate and the rate of change of the nominal GDP (snowball effect) to the increase of the debt to GDP ratio is estimated at about 22 percentage points, reflecting the contraction of the nominal GDP. Despite the fact that in highly indebted economies such as Greece, the dynamics of public debt is an issue, affecting the growth dynamics and fiscal sustainability in the long run, inclusion of Greek government bonds, although still lagging behind the investment tier, in the emergency program of the ECB Pandemic Emergency Purchase Program (PEPP) and their acceptance as collateral in the refinancing operations of Greek banks by the Eurosystem, as well as the positive developments in the international financial markets, contributed to uninterrupted access of the Greek Government to the markets and further reduction of Greek government bond yields. The recovery of private consumption and aggregate demand is projected to gain ground later in the year, specifically from the second quarter, and lead to a positive and strong growth rate of the Greek economy. According to the provisions of the Bank of Greece, the real GDP growth rate in 2021 will be 4.2%. This provision, however, includes great uncertainty due to the risks directly related to the development of epidemiological data and the possibility of immediate removal of many restrictive and restrictive measures, but also to its particular structural characteristics of economy that largely determine the extent of the economic impact. It is estimated that, upon lifting the restrictions on citizens' mobility and gradual reopening of the economy, the resulting increase in savings will help pay off debts currently suspended and will partially finance future increases in private spending, contributing thus in the recovery of economic activity. As noted in the annual report of the Governor of the Bank of Greece, the rate, at which the Greek economy will recover, depends on three key factors: First, accelerating vaccination campaign not only nationally but also globally as the success of vaccinations will strengthen citizens' confidence in resolving the health crisis and enable them to return to normal way of life by lifting travel and other restrictions, thus contributing to the recovery of external demand, especially services such as tourism and travel. At the same time, reducing uncertainty and lifting restrictive measures will allow a gradual increase in domestic consumption and domestic investment. Secondly, the maintenance until the end of the pandemic and the consolidation of the recovery, the targeted fiscal interventions and the emergency measures taken by the banking system in categories of employees but also in productive sectors that have been hit hardest but remain financially sound. Third, the rate of activation of the Greek National Recovery and Resilience Plan (NNRP) for the absorption of capital resources to which Greece is entitled by the European instrument NGEU. Utilizing European resources from the second half of 2021 to 2026 will significantly boost growth momentum and facilitate the restoration of fiscal balance without the need to return to the austerity policies of the past that have trapped the economy in a vicious cycle of recession and stagnation. In fact, for countries like Greece, with a high ratio of public debt to GDP, the combination

PANCRETA BANK | ANNUAL FINANCIAL STATEMENTS FOR THE PERIOD FROM 01.01.2020 TO 31.12.2020 | - 11- |

of the highest possible nominal GDP growth rate and the lowest nominal lending rates possible is crucial for the de-escalation of the debt dynamics. Therefore, regarding the process of gradual return of the Greek economy to the normal way of life, it is necessary to define a hierarchy of the medium-term priorities of the economic policy around three central axes: a) restoring the fiscal balance in order to ensure the country's debt, b) strengthening the development (c) accelerating implementation of the national reform program, including the liquidations and write offs of low-quality assets held by the credit institutions. Β. Hellenic Bank System General: As recorded in the annual report of the Governor of the Bank of Greece, the main factors that shaped the financial and supervisory sizes of banks in 2020 were recording a significant amount of non-recurring income, evaluation of increased provisions for credit risk, its maintenance capital adequacy at a satisfactory level and further reduction of the stock of non-performing loans (NPLs).

Results: Regarding the results of the Banks, in the period January-September 2020, the bank sector recorded a significant increase in their operating income which, however, arose mainly from non-recurring income from financial transactions, mainly related to the Greek government bond portfolio held by the banks. There was a decrease in net interest income, mainly due to reduction in loan balance and further decline of the interest margin, which highly offset the positive effect on income of the liquidity borrowing costs decrease. Operating expenses declined, mainly due to further downsizing staff and the consequent decrease in related expenses. As a result of the above, net income increased. However, taking into account the increased provisions made in order to cover credit risk, bank sector recorded losses.

Financing: Credit expansion accelerated in 2020 compared to 2019, with annual growth rate of bank financing to private sector reaching 1.2% on average in 2020, compared to a negative rate of -0.4% in 2019. This upward trend in 2020 reflects an increase in financing towards non-financial corporations as opposed to household bank financing which continued to decline in 2020 at essentially the same average annual rate compared to 2019. During the pandemic crisis, the annual rate of credit expansion from banks to non-financial corporations (NFCs) accelerated after March 2020, reaching high levels in the second half of the year. In particular, this rate stood at 5.6% on average in 2020 (2019: 2.2%) and rose to 10.0% in December 2020, the highest level observed since June 2009. Credit expansion to NFCs during the pandemic was facilitated by the improved ability of banks to raise funds from the Eurosystem on improved terms. A significant role was also played by the increase in the inflow of bank deposits, which increased the total funds of the banks that are available for re-financing. Without overlooking the practical support of the Banking Institutions to the real economy in the midst of an economic crisis, it should be noted that in the upward trend of credit expansion to NFCs, the programs of strengthening the bank financing to companies (in sectors of the economy which have been affected by the pandemic effects), managed by the Hellenic Development Bank: the guarantee program of the COVID-19 Business Guarantee Fund and the co-financing and interest rate subsidy program of the Entrepreneurship Fund (TEPIX II). These programs encouraged the supply of loans by banks, as they reduced the credit risk of their respective portfolio. They also encouraged demand from businesses by offering them an attractive option of financing emergency capital in very favourable terms, which under regular conditions would not be available. The cumulative flow of loans disbursed in 2020 to NFCs (and self-employed) through two programs of the Hellenic Development Bank amounted to 6.4 billion euro (January-February 2021: 0.6 billion euro). In addition to the provision of new loans by banks, the measure of suspension of arrears payments by debtors, in agreement with the banks, was effective. Postponement of loan repayments by borrowers to banks temporarily increases the amount of net loan flow and their annual change rates, respectively. Deposits: In 2020, private sector deposits recorded a cumulative increase of 20.6 billion euro or 14%, which was more than double regarding the corresponding flow in 2019 (8.9 billion euro). Compared to the previous years, the non-financial corporations sector played a significant role in this increase. Domestic NFC deposits increased by 9.1 billion euro in 2020 (representing 45% of private sector flow, compared to 21% in 2019). This is justified by the effort of companies to facilitate liquidity reserves given the pandemic as well as the accumulation of liquidity resulting from direct state aid and increased bank loans credited to corporate accounts. The aforementioned increase in deposits was also helped by the measures of suspension of payments of loans and tax obligations, as well as in general by the avoidance of capital expenditures mainly during the pandemic period. Household deposits, which make up for the bulk (approximately 80%) of domestic private sector deposits, rose by € 10.0 billion in 2020, from € 6.6 billion in 2019, at an average annual growth rate and slightly accelerated during the last quarter of the year. The increase in household deposits continued in January 2021 (by 0.7 billion euro). Despite the ongoing decline in mortgage and consumer loan balances, disposable income and household deposits were assisted by fiscal pandemic income support measures as well as deferral of consumer and other spending or liabilities, while employment prospects helped to strengthen the savings behavior of households for welfare purposes against future needs.

PANCRETA BANK | ANNUAL FINANCIAL STATEMENTS FOR THE PERIOD FROM 01.01.2020 TO 31.12.2020 | - 12- |

However, the year 2020 recorded a decline in central government deposits in the banking system, mainly as a result of extensive fiscal measures to support businesses and households due to the pandemic. In particular, in 2020, central government deposits in commercial banks decreased by 4.2 billion euro or 40% compared to the end of 2019, while central government deposits in the Bank of Greece also declined between the end of 2019 and the end of 2020 by 2.3 billion euro. Deposits in the commercial banks of the Social Security Institutions (OKA) and the Local Government Organizations (OTA), which together with the central government constitute the general government sector, decreased by 1.3 billion euro or 24%. In other sectors, deposits of insurance companies and other financial institutions increased by 44%, contributing positively to the deposit base of banks by 1.4 billion euro (2019: 0.4 billion euro, 2018: 0.3 billion euro), and non-residents' deposits also increased by € 0.7 billion (or 10%) (2019: € 0.2 billion, 2018: € 0.6 billion). Bank interest rates: Deposit rates offered to non-financial corporations and households further decrease in 2020 compared to the previous year and averaged slightly above 0.20%, attributed to the improvement of credit institutions' liquidity conditions due to favourable decisions taken by the ECB on the terms of cash withdrawals from the Eurosystem and on the other hand due to the strengthening of retail deposits, it facilitated a further decrease in interest rates. More specifically, the weighted average interest rate on time deposits by households in 2020 stood at 0.26% (average 2019: 0.51%, average 2010-2018: 2.41% and January 2021: 0, 19%) and the corresponding for corporate time deposits stood at 0.22% (average 2019: 0.69%, average 2010-2018: 2.24% and January 2021: 0.11%). The overnight deposit rate fell slightly to 0.05% for households and 0.09% for NFCs, ie a decrease of 4 and 7 basis points (bp) respectively (average 2010-2018: households : 0.29%, NFC: 0.30%). In real terms, the interest rate on time deposits for both NFCs and households received positive values, as deflationary pressures prevailed from the second quarter. More specifically, the average weighted interest rate on time deposits by households stood at 1.52% in 2020 (average 2019: -0.01%) and the corresponding rate on corporate time deposits stood at 1.48% ( average 2019: 0.17%). The downward trend followed by the cost of bank financing to NFCs since the end of 2011 was halted around the first quarter of 2020, mainly due to developments in interest rates on smaller business loans. However, due to the prevailing trend, the average borrowing rate stood at a lower level in 2020 compared to 2019. More specifically, the weighted average interest rate on pre-determined loans stood at 3.06% on average in 2020, 72 basis points lower compared to the average interest rate of 2019 (average 2011-2018: 5.18% and January 2021: 2.89%). Respectively, the weighted average interest rate on loans of indefinite term amounted to 4.54% on average in 2020, basis point lower compared to the average interest rate of 2019 (average 2011-2018: 6.53% and January 2021: 4.36%). NPLs management: Regarding the quality of the domestic loan portfolio, at the end of December 2020 NPLs amounted to 47.4 billion euro, decreased by approximately 21 billion euro compared to the end of December 2019 as well as by approximately 60 billion compared to March 2016, when the highest level of NPLs was recorded. The decline in the stock of NPLs during 2020 is mainly due to sales of loans amounting to 19.3 billion euro on an individual basis (due to the utilization of the state guarantee program in securitization of loans to credit institutions, known as "Hercules") and in write-offs of 2.6 billion euro and less in receipts through active management (i.e. through restructuring/loan arrangements, collection of arrears, liquidation of collateral, etc.). Also, the reduction of NPLs was helped by the measures of inclusion of customers in a regime of suspension of instalment payment. In terms of key quality indicators of NPLs, the NPL ratio to total loans remained high (30.2%) at the end of 2020, almost ten times the corresponding size for banks supervised by the Single Supervisory Mechanism. Also, the cure rates of regular loan servicing and default rate were low during the period. Realization of securitizations through utilization of the "Hercules" program was a significant development during 2020. Moreover, some banks have launched operational transformation processes through hive down in the context of reducing the existing NPL stock. However, even after the completion of the "Hercules" program in 2021, it is estimated that the ratio of NPLs to total loans will fall to about 25% and the average capital adequacy ratio to lower than current levels with a simultaneous deterioration of the percentage of the deferred tax asset on the banks' capital. It is to be noted that the aforementioned estimates do not include the new NPLs that are expected to be added to the existing volume due to the effects of the health crisis. The Bank of Greece has estimated that this inflow of new NPLs will be approximately 8-10 billion euro, while approximately 1/3 of the loans that are in arrears are classified as loans with a significant increase in risk (Stage 2 under IFRS 9). Liquidity: The ECB package, including the acceptance of Greek bonds in refinancing operations and supervisory measures, significantly increased the liquidity of the Greek banking system. In particular, since the first quarter of 2020 Greece has benefited significantly from the ECB decisions regarding the granting of a waiver for securities issued by the Greek State from the Eurosystem eligibility criteria: a) regarding their inclusion in the extraordinary ECB (Pandemic Emergency Purchase Program - PEPP) due to pandemic and b) their acceptance of collateral in the refinancing operations of Greek banks by the Eurosystem.

Capital adequacy: Regarding capital adequacy, both the Common Equity Tier 1 (CET1) and the Capital Adequacy Ratio on a consolidated basis slightly decreased during the year-end period, but remained at a satisfactory level of 2020 (15.0% and 16.6% respectively). Incorporating the full effect of International Financial Reporting Standard 9

PANCRETA BANK | ANNUAL FINANCIAL STATEMENTS FOR THE PERIOD FROM 01.01.2020 TO 31.12.2020 | - 13- |

(IFRS 9), the CET1 ratio stood at 12.5% and the Capital Adequacy Ratio at 14.3%. In this context, it is emphasized that more than half of the banks' capital corresponds to a deferred tax receivable against the Greek State.

Hedging coronavirus (COVID-19) impact: From the beginning of March 2020 and over the next few months, the ECB Board of Directors has repeatedly instituted monetary policy measures to enable all sectors of the economy, ie households and businesses, banks and governments, to take advantage of supportive financing conditions that help absorbing the vibrations. In particular, the ECB Board of Directors decided on the following:

1. Additional acquisitions of securities under the APP program. 2. Conducting additional LTRO at a more favorable interest rate than before. 3. Significant cost reduction and increase in permitted volume of funding to be raised through targeted longer-

term refinancing operations (TLTRO-III). Also, expansion of the possibilities of early repayment of this financing.

4. New Pandemic Emergency Purchase Program (PEPP). 5. Enrichment of the variety of assets accepted by the Eurosystem as collateral. Reduction of haircuts applied to

the valuations of these elements. 6. Arrangements to limit the impact on collateral availability due to downgrades of issuers' securities or the

credit rating of individual debt securities caused by the pandemic. 7. Conducting a new series of non-targeted operations for longer-term refinancing at a favorable interest rate

in view of the emergency created by the pandemic (PELTRO). 8. Establishment of a euro liquidity facility to non-euro area central banks (EUREP). 9. Continuing regular MRO and LTRO refinancing operations, for as long as necessary, through fixed interest

rate auctions without quantitative limitation on the amount of liquidity to be granted. As far as future developments concerns, the ECB Board of Directors estimates that in the medium term appropriate funding conditions will promote economic recovery and offset the diminishing impact of the pandemic on price developments, so that accelerating inflation can approach the target for a rate just below 2%. In 2021, the ECB Board of Directors is expected to complete a thorough review of the Eurosystem monetary policy strategy to ensure that the single monetary policy remains appropriate for the purpose it serves both now and in the future. In addition, the ECB Board of Directors will decide within the current year whether to launch the exploratory phase of the preparatory work for the possible issuance of the digital euro. C. Pancreta Bank (Significant Events) Annual Regular General Meeting: On June 28, 2020, the operations of the Annual Regular General Meeting in Heraklion, Crete were completed, and transformation of the Bank into a Societe Anonyme was decided according to provisions of Law 4601/2019. Its transformation into a modern credit institution will enable expansion of its operations, into a wider range of banking operations, such as Investment Banking, Treasury and Financial Markets, Leasing, Banking and Factoring agencies and Transaction Banking. In addition, the recommendations of the Board of Directors were approved on the other issues of the agenda regarding the presentation and approval of the financial statements for the year 2019 as well as the budget for 2020.

Board of Directors: On December 22, 2020, the new Board of Directors of Pancreta Bank was established after the assumption of duties from the Chief Executive Officer and Executive Member of the Board, Mr. Antonios Vartholomeos, while the position of the Chairman (Non-executive member) was assigned to Mr. Dimitrios Dimopoulos. The term of the Board of Directors is set until the Regular General Meeting of Shareholders which will be convened no later than September 10, 2021 with the election of a new Board of Directors by the General Meeting of the Bank's shareholders.

Development of branches: The Bank's new branch was opened in Agia Paraskevi, Attica, at 449 Mesogeion Ave., on August 3, 2020. Pancreta Bank continued implementing its transformation plan into a pioneering, friendly and flexible banking institution, as at December 16, 2020, starting operating the new branch opposite the City Hall of Heraklion, at 25th of August Avenue 94. These new branches located in areas with intense commercial activity reflect the Bank's policy to develop its clientele in small and medium enterprises.

Supporting real economy in the midst of COVID-19: Pancreta Bank, continuing its efforts to strengthen the liquidity of companies affected by the adverse effects of COVID-19, participated in the Business Financing program "TEPIX II" of the Hellenic Development Bank. Moreover, being on full readiness, the network of Pancreta Bank received and served a number of applications under the first and second round of COVID-19 guarantee loans, guaranteed by the Hellenic Development Bank (HDB). The total amount of loans granted under the above program in 2020 exceeded 50 million euro. At the same time, in order to align individuals with legal entities, the Bank offered the possibility of suspending the instalments of mortgage and consumer loans in the context of the supervisory facilities granted to credit institutions operating in the European Union.

PANCRETA BANK | ANNUAL FINANCIAL STATEMENTS FOR THE PERIOD FROM 01.01.2020 TO 31.12.2020 | - 14- |

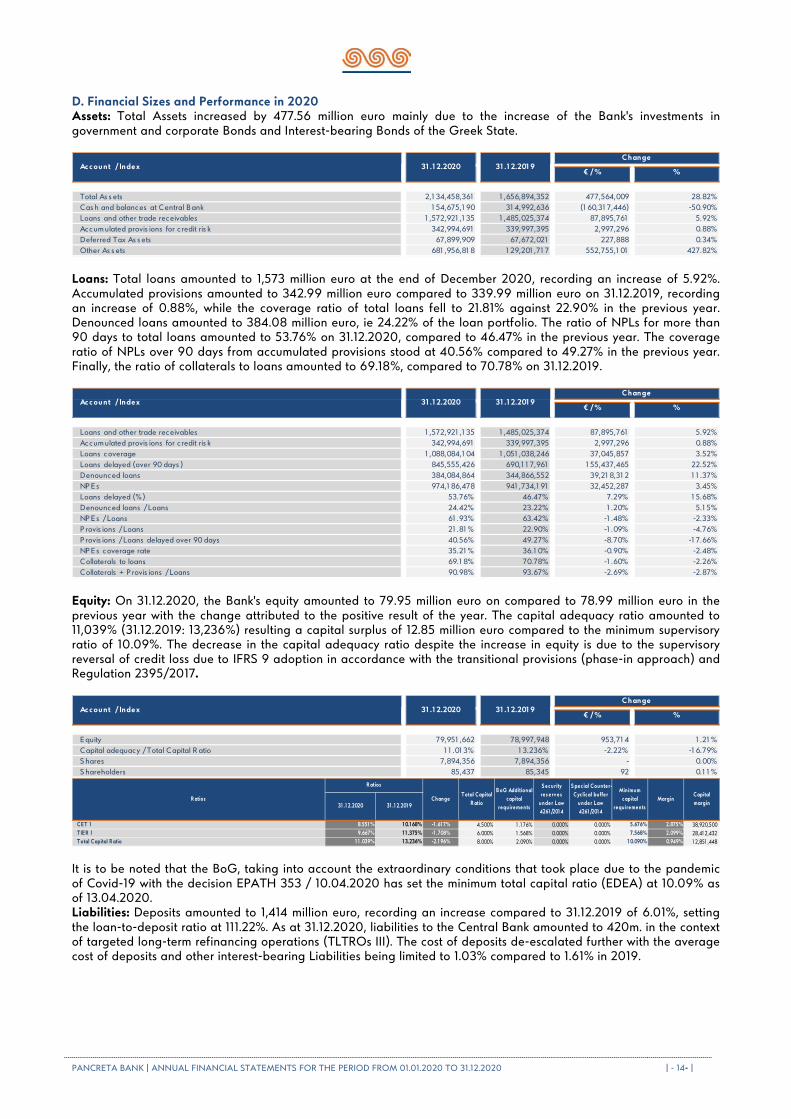

D. Financial Sizes and Performance in 2020 Assets: Total Assets increased by 477.56 million euro mainly due to the increase of the Bank's investments in government and corporate Bonds and Interest-bearing Bonds of the Greek State.

€ / % %

Total As s ets 2,1 34,458,361 1 ,656,894,352 477,564,009 28.82%Cas h and balances at Central Bank 1 54,675,1 90 31 4,992,636 (1 60,31 7,446) -50.90%Loans and other trade receivables 1 ,572,921 ,1 35 1 ,485,025,374 87,895,761 5.92%Accumulated provis ions for credit ris k 342,994,691 339,997,395 2,997,296 0.88%Deferred Tax As s ets 67,899,909 67,672,021 227,888 0.34%Other As s ets 681 ,956,81 8 1 29,201 ,71 7 552,755,1 01 427.82%

Change31 .1 2.2020 31 .1 2.201 9Account / Index

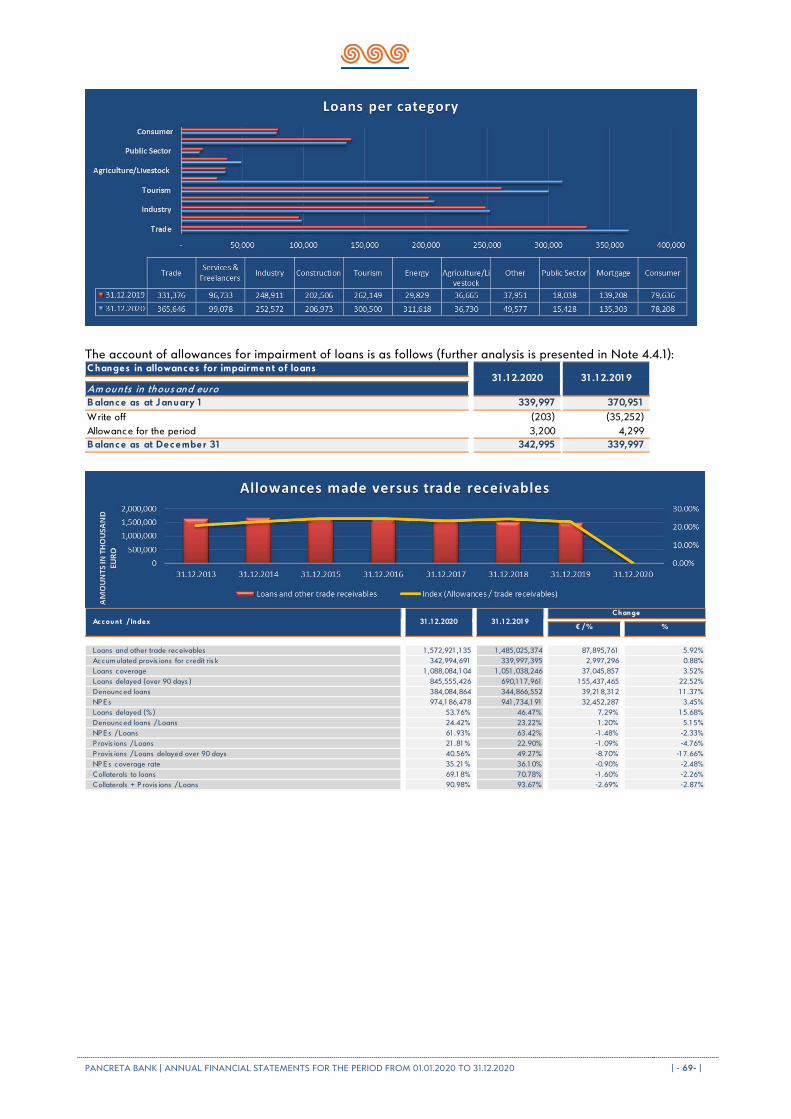

Loans: Total loans amounted to 1,573 million euro at the end of December 2020, recording an increase of 5.92%. Accumulated provisions amounted to 342.99 million euro compared to 339.99 million euro on 31.12.2019, recording an increase of 0.88%, while the coverage ratio of total loans fell to 21.81% against 22.90% in the previous year. Denounced loans amounted to 384.08 million euro, ie 24.22% of the loan portfolio. The ratio of NPLs for more than 90 days to total loans amounted to 53.76% on 31.12.2020, compared to 46.47% in the previous year. The coverage ratio of NPLs over 90 days from accumulated provisions stood at 40.56% compared to 49.27% in the previous year. Finally, the ratio of collaterals to loans amounted to 69.18%, compared to 70.78% on 31.12.2019.

€ / % %

Loans and other trade receivables 1 ,572,921 ,1 35 1 ,485,025,374 87,895,761 5.92%Accumulated provis ions for credit ris k 342,994,691 339,997,395 2,997,296 0.88%Loans coverage 1 ,088,084,1 04 1 ,051 ,038,246 37,045,857 3.52%Loans delayed (over 90 days ) 845,555,426 690,1 1 7,961 1 55,437,465 22.52%Denounced loans 384,084,864 344,866,552 39,21 8,31 2 1 1 .37%NP Es 974,1 86,478 941 ,734,1 91 32,452,287 3.45%Loans delayed (%) 53.76% 46.47% 7.29% 1 5.68%Denounced loans / Loans 24.42% 23.22% 1 .20% 5.1 5%NP Es / Loans 61 .93% 63.42% -1 .48% -2.33%P rovis ions / Loans 21 .81 % 22.90% -1 .09% -4.76%P rovis ions / Loans delayed over 90 days 40.56% 49.27% -8.70% -1 7.66%NP Es coverage rate 35.21 % 36.1 0% -0.90% -2.48%Collaterals to loans 69.1 8% 70.78% -1 .60% -2.26%Collaterals + P rovis ions / Loans 90.98% 93.67% -2.69% -2.87%

Change31 .1 2.2020 31 .1 2.201 9Account / Index

Equity: On 31.12.2020, the Bank's equity amounted to 79.95 million euro on compared to 78.99 million euro in the previous year with the change attributed to the positive result of the year. The capital adequacy ratio amounted to 11,039% (31.12.2019: 13,236%) resulting a capital surplus of 12.85 million euro compared to the minimum supervisory ratio of 10.09%. The decrease in the capital adequacy ratio despite the increase in equity is due to the supervisory reversal of credit loss due to IFRS 9 adoption in accordance with the transitional provisions (phase-in approach) and Regulation 2395/2017.

€ / % %

Equity 79,951 ,662 78,997,948 953,71 4 1 .21 %Capital adequacy / Total Capital R atio 1 1 .01 3% 1 3.236% -2.22% -1 6.79%S hares 7,894,356 7,894,356 - 0.00%S hareholders 85,437 85,345 92 0.1 1 %

Change31 .1 2.2020 31 .1 2.201 9Account / Index

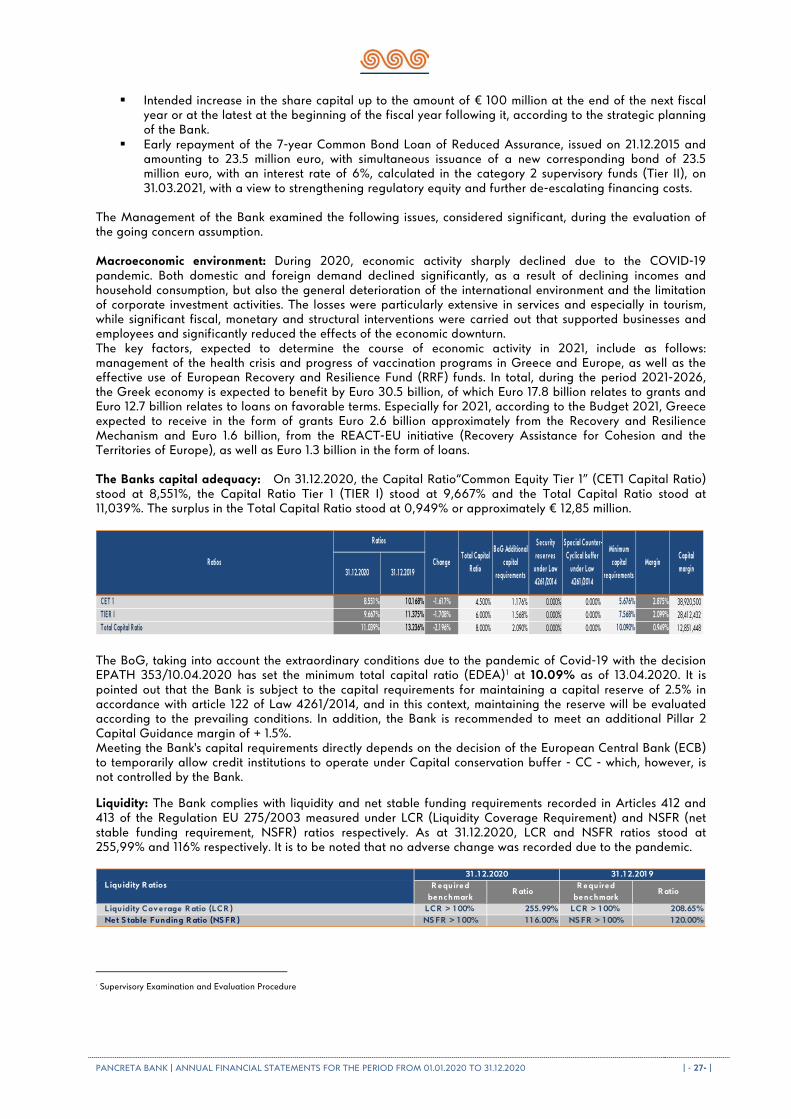

CET 1 8.551 % 1 0.1 68% -1 .61 7% 4.500% 1 .1 76% 0.000% 0.000% 5.676% 2.875% 38,920,500 TIER I 9.667% 1 1 .375% -1 .708% 6.000% 1 .568% 0.000% 0.000% 7.568% 2.099% 28,41 2,432 Total Capital R atio 1 1 .039% 1 3.236% -2.1 96% 8.000% 2.090% 0.000% 0.000% 1 0.090% 0.949% 1 2,851 ,448

Capital margin

R atios

ChangeTotal Capital

R atio

B oG Additional capital

requirements

S ecurity res erves

under Law 4261 /201 4

S pec ial Counter-Cyc lical buffer

under Law 4261 /201 4

Minimum capital

requirementsR atios Margin

31 .1 2.2020 31 .1 2.201 9

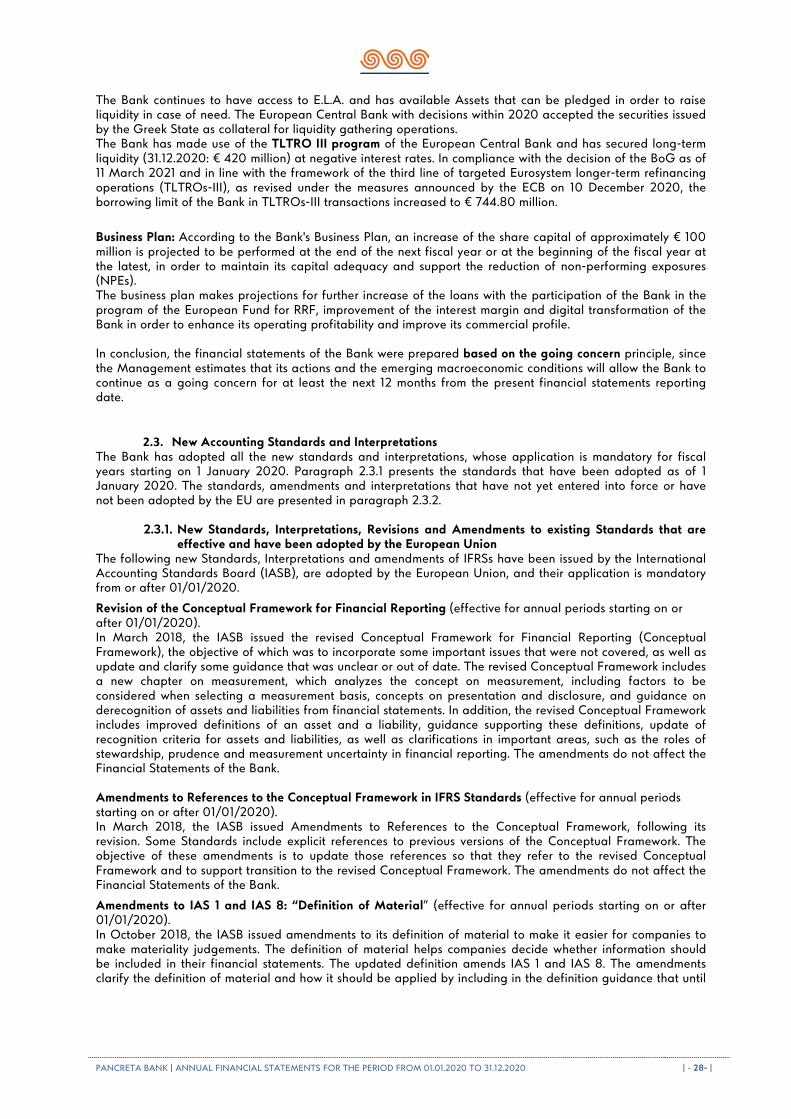

It is to be noted that the BoG, taking into account the extraordinary conditions that took place due to the pandemic of Covid-19 with the decision EPATH 353 / 10.04.2020 has set the minimum total capital ratio (EDEA) at 10.09% as of 13.04.2020. Liabilities: Deposits amounted to 1,414 million euro, recording an increase compared to 31.12.2019 of 6.01%, setting the loan-to-deposit ratio at 111.22%. As at 31.12.2020, liabilities to the Central Bank amounted to 420m. in the context of targeted long-term refinancing operations (TLTROs III). The cost of deposits de-escalated further with the average cost of deposits and other interest-bearing Liabilities being limited to 1.03% compared to 1.61% in 2019.

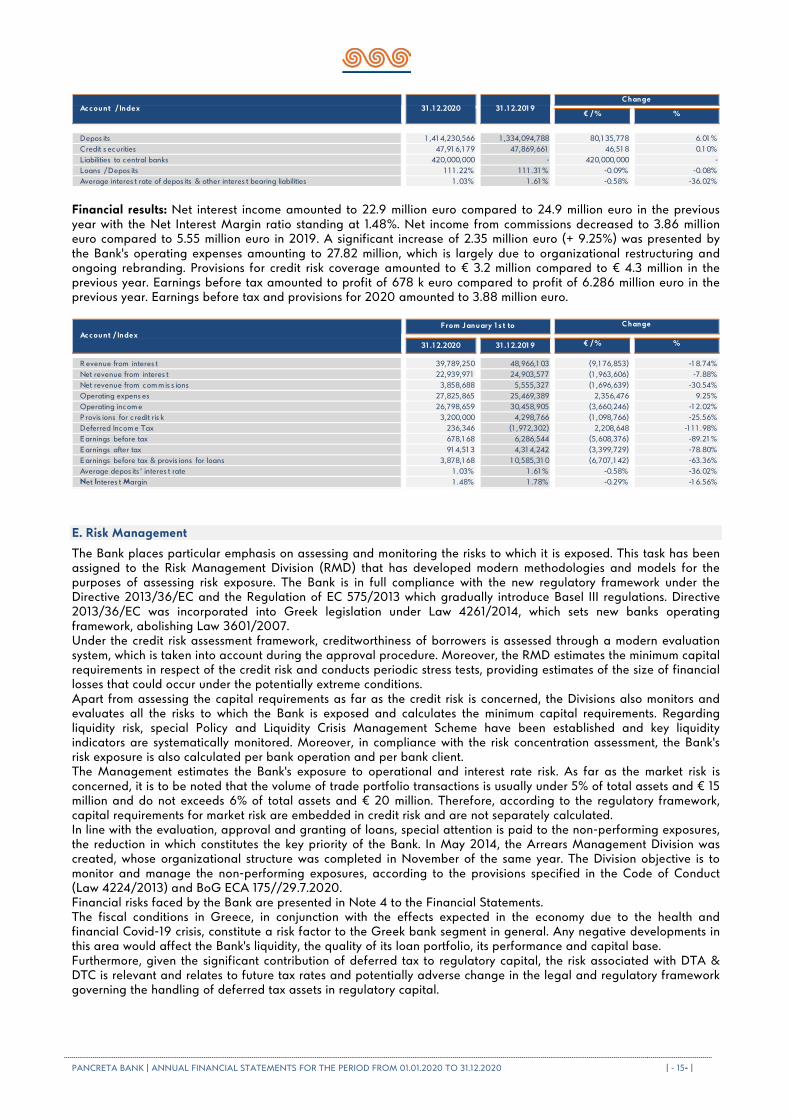

PANCRETA BANK | ANNUAL FINANCIAL STATEMENTS FOR THE PERIOD FROM 01.01.2020 TO 31.12.2020 | - 15- |

€ / % %

Depos its 1 ,41 4,230,566 1 ,334,094,788 80,1 35,778 6.01 %Credit s ecurities 47,91 6,1 79 47,869,661 46,51 8 0.1 0%Liabilities to central banks 420,000,000 - 420,000,000 -Loans / Depos its 1 1 1 .22% 1 1 1 .31 % -0.09% -0.08%Average interes t rate of depos its & other interes t bearing liabilities 1 .03% 1 .61 % -0.58% -36.02%

Change31 .1 2.2020 31 .1 2.201 9Account / Index

Financial results: Net interest income amounted to 22.9 million euro compared to 24.9 million euro in the previous year with the Net Interest Margin ratio standing at 1.48%. Net income from commissions decreased to 3.86 million euro compared to 5.55 million euro in 2019. A significant increase of 2.35 million euro (+ 9.25%) was presented by the Bank's operating expenses amounting to 27.82 million, which is largely due to organizational restructuring and ongoing rebranding. Provisions for credit risk coverage amounted to € 3.2 million compared to € 4.3 million in the previous year. Earnings before tax amounted to profit of 678 k euro compared to profit of 6.286 million euro in the previous year. Earnings before tax and provisions for 2020 amounted to 3.88 million euro.

31 .1 2.2020 31 .1 2.201 9 € / % %

R evenue from interes t 39,789,250 48,966,1 03 (9,1 76,853) -1 8.74%Net revenue from interes t 22,939,971 24,903,577 (1 ,963,606) -7.88%Net revenue from commis s ions 3,858,688 5,555,327 (1 ,696,639) -30.54%Operating expens es 27,825,865 25,469,389 2,356,476 9.25%Operating income 26,798,659 30,458,905 (3,660,246) -1 2.02%P rovis ions for credit ris k 3,200,000 4,298,766 (1 ,098,766) -25.56%Deferred Income Tax 236,346 (1 ,972,302) 2,208,648 -1 1 1 .98%Earnings before tax 678,1 68 6,286,544 (5,608,376) -89.21 %Earnings after tax 91 4,51 3 4,31 4,242 (3,399,729) -78.80%Earnings before tax & provis ions for loans 3,878,1 68 1 0,585,31 0 (6,707,1 42) -63.36%Average depos its ' interes t rate 1 .03% 1 .61 % -0.58% -36.02%Net Interes t Margin 1 .48% 1 .78% -0.29% -1 6.56%

Account / IndexChange From January 1 s t to

Ε. Risk Management

The Bank places particular emphasis on assessing and monitoring the risks to which it is exposed. This task has been assigned to the Risk Management Division (RMD) that has developed modern methodologies and models for the purposes of assessing risk exposure. The Bank is in full compliance with the new regulatory framework under the Directive 2013/36/EC and the Regulation of EC 575/2013 which gradually introduce Basel III regulations. Directive 2013/36/EC was incorporated into Greek legislation under Law 4261/2014, which sets new banks operating framework, abolishing Law 3601/2007. Under the credit risk assessment framework, creditworthiness of borrowers is assessed through a modern evaluation system, which is taken into account during the approval procedure. Moreover, the RMD estimates the minimum capital requirements in respect of the credit risk and conducts periodic stress tests, providing estimates of the size of financial losses that could occur under the potentially extreme conditions. Apart from assessing the capital requirements as far as the credit risk is concerned, the Divisions also monitors and evaluates all the risks to which the Bank is exposed and calculates the minimum capital requirements. Regarding liquidity risk, special Policy and Liquidity Crisis Management Scheme have been established and key liquidity indicators are systematically monitored. Moreover, in compliance with the risk concentration assessment, the Bank's risk exposure is also calculated per bank operation and per bank client. The Management estimates the Bank's exposure to operational and interest rate risk. As far as the market risk is concerned, it is to be noted that the volume of trade portfolio transactions is usually under 5% of total assets and € 15 million and do not exceeds 6% of total assets and € 20 million. Therefore, according to the regulatory framework, capital requirements for market risk are embedded in credit risk and are not separately calculated. In line with the evaluation, approval and granting of loans, special attention is paid to the non-performing exposures, the reduction in which constitutes the key priority of the Bank. In May 2014, the Arrears Management Division was created, whose organizational structure was completed in November of the same year. The Division objective is to monitor and manage the non-performing exposures, according to the provisions specified in the Code of Conduct (Law 4224/2013) and BoG ECA 175//29.7.2020. Financial risks faced by the Bank are presented in Note 4 to the Financial Statements. The fiscal conditions in Greece, in conjunction with the effects expected in the economy due to the health and financial Covid-19 crisis, constitute a risk factor to the Greek bank segment in general. Any negative developments in this area would affect the Bank's liquidity, the quality of its loan portfolio, its performance and capital base. Furthermore, given the significant contribution of deferred tax to regulatory capital, the risk associated with DTA & DTC is relevant and relates to future tax rates and potentially adverse change in the legal and regulatory framework governing the handling of deferred tax assets in regulatory capital.

PANCRETA BANK | ANNUAL FINANCIAL STATEMENTS FOR THE PERIOD FROM 01.01.2020 TO 31.12.2020 | - 16- |

F. Prospects for the Future

Gradual development of the new corporate identity of Pancreta Bank (rebranding) since 2018 has marked the beginning of a new era, with the Bank implementing significant modernization and development projects, investing in technological equipment, systems and applications, while reforming its structure in accordance with the principles of modern corporate governance. The aforementioned modernization includes the transformation of the Bank into a Societe Anonyme and the reorganization of the Corporate Governance system in the context of its harmonization with the provisions of Law 4706/2020 "Corporate governance of public limited companies, modern capital market, integration in the Greek legislation of Directive (EU) 2017/828 of the European Parliament and of the Council, measures to implement Regulation (EU) 2017/1131 and other provisions" effective from 01.07.2021. Finastra's Fusion Risk platform has been added to the Bank's information systems in order to more effectively manage credit risk and automate operations, allowing users to form a more accurate and faster view of the bank's balance sheet items, thus facilitating decision-making on reducing non-performing exposures and consolidating the loan portfolio. At the same time, ongoing upgrade of the cash management department (Treasury), the new electronic banking platform ebanking and mobile banking, as well as the new website highlight the dedication and constitute the Bank's philosophy regarding the configuration of advanced customer-centric systems that will adapt to modern needs of its customers as they are shaped by market demands. However, the growth dynamics presented by the Greek economy in the fiscal year 2019, on which the general business planning of the Pancreta Bank is based, was violently halted in the first quarter of 2020 by the coronavirus pandemic (COVID-19), creating significant pressures on the banking system and posing major obstacles to normalcy. More specifically, during 2020, economic activity recorded a large and sharp decline due to the COVID-19 pandemic. Domestic and external demand significantly declined as household incomes and consumption declined, the international environment deteriorated, and corporate investment activity were limited. The recovery of private consumption and aggregate demand is expected to be gradually restored in 2021 and specifically from the second quarter leading to a positive and strong growth rate of the Greek economy. According to the provisions of the Bank of Greece, the real GDP growth rate in 2021 is budgeted at 4.2%. However, this provision contains great uncertainty due to the risks directly related to the development of epidemiological data and the possibility of immediate lifting of many restrictive and prohibitive measures, but also to the particular structural features of the economy that largely determine the extent of economic impact. It is estimated that, with the lifting of restrictions on citizens' mobility and the gradual reopening of the economy, the increase in savings in 2020 will help the smooth repayment of currently suspended liabilities and will partially finance the future growth of private thus contributing to the recovery of economic activity. Given the above, the following key issues are to be addressed in 2021: Implementation of the Banks Business Plan, the main pillars of which are: a) reducing NPEs in the coming years

through securitizations and assignments to servicers. Already in the first quarter of 2021, the Bank signed a service agreement for part of the portfolio of NPEs with Quant Master Service, thus enacting its strategic planning for the optimization of its balance sheet. b) improvement of the net interest margin, c) strengthening of the Bank’s capital adequacy through capital increase d) increase of loans and exploitation of part of the loans of the Recovery and Sustainability Fund. Furthermore:

Supporting - financing wider economy in order to absorb the shocks from the effects of the coronavirus on the economy through the use of monetary and supervisory facilities of the ECB and the respective programs of the Hellenic Development Bank.

Utilizing the expected credit loss estimation model in the context of NPEs management. Maintaining a balanced growth rate between deposits and loans. Maintaining satisfactory liquidity through deposits, but also partnerships with other financial institutions. Completing centralization of operations, while maintaining flexibility and ongoing upgrading of the quality of

services provided and customer service. The Banks Digital transformation

G. Non-financial information

Business model: PANCRETA BANK S.A. (referred and as Bank) was established in 1993 in accordance with the provisions of Law 1667/1986 and received a license to operate as Credit Institution in accordance with the 2306 / 19-5-1994 Act of the Governor of the BoG. The Bank was constituted following the transition of the "PANCRETAN COOPERATIVE BANK Co." to a Société anonyme, in compliance with (i) the decision as of 28.06.2020 of the General Meeting of its members, registered in G.E.MI. on 24.07.2020 under K.A.K. 2181040 (ii) the act of transformation under number 17092 / 03-07-2020 of the notary of Heraklion Styliani Kalogeraki-Archontaki, registered in G.E.MI. on 24.07.2020 under K.A.K. 2181075 and (iii) number 4909 / 24.07.2020 (ΑΔΑ 61Μ4469ΗΛΞ - Θ4Θ) Decision of the Head of the G.E.MI. Service of the Chamber of Heraklion. The framework of foundation, operation and activity of the Bank is defined by the provisions of: a) Law 4548/2018 as applicable, b) Law 4261/5.5.2014, c) the Bank's Charter.

PANCRETA BANK | ANNUAL FINANCIAL STATEMENTS FOR THE PERIOD FROM 01.01.2020 TO 31.12.2020 | - 17- |

Its objective is to generate corporate value aiming at the economic development of its shareholders and its clients. The bank has over 85,000 shareholders. It maintains an extensive customer service network, with 42 branches in Crete and 51 branches nationwide, and has a presence in Attica, Thessaloniki, Milos and Rhodes, while the network is complemented by 9 additional independent service points (ATMs). Pancreta Bank has a strong local character, as it holds a significant market share in Crete and especially in the prefecture of Heraklion but aims at the strategic development of branches nationwide. Furthermore, through its operations, the Bank supports the professionals in development of their businesses, as well as the startup businesses. Its participation in joint development efforts, with the aim of utilizing Community and National programs, participation in joint ventures aimed at strengthening local development and entrepreneurship and the generation of an organizational framework of free consulting, information, and support to its customers, differentiates Pancreta from the rest of the banking system and justify its role and existence as a successful business of the social economy.

Environment: The Bank applies environmentally responsible policies in its operational structures with the objective of reducing the PEF and especially the policies which aim at decreasing the energy and paper consumption and the enhancement of recycling programs of accumulators, electronic devices and paper. Moreover, the Bank has a firm commitment to expanding e-commerce and encourages its customers and staff in this direction. Community policy: The Bank supports various programs of communal objective, events and initiatives related to education, protection of the environment, culture, sports and the work of Non-Government-Organizations. The contribution of the Bank is focused mainly on development of cooperation, exchange of information, resources and skills, while at the same time it supports less privileged social groups, promotes culture and sports, protects the environment and promotes equal opportunities for education in a wide variety of sectors. In this context the Bank devoted to donations, sponsorships and grants the amount of € 167 k regarding various social organizations, and provides its conference room for free to culture & social and to non-profit organizations, Legal Entities of Public Law (as analyzed in the following chapter) and provides its conference room free of any charged for organizing culture & social events as well as non-profit organizations. Moreover, the Bank has developed an online portal for the purposes of providing information regarding economic and development incentives to OTAs, SMEs and Cooperatives as well as to primary sector producers and organizations. Labor issues: On 31.12.2020, the Bank employed 481 people, while the cost of payroll and other benefits for the year 2020, including insurance contributions, amounted to approximately 17.16 million Euro. The Bank responsibly applies the following policies regarding Human Resources:

Healthcare and safety Selection of staff, recruitment procedures, avoiding discriminations in the working place On-going training of employees

PANCRETA BANK | ANNUAL FINANCIAL STATEMENTS FOR THE PERIOD FROM 01.01.2020 TO 31.12.2020 | - 18- |

Recognizing the right of holding collective negotiation Providing fair payments, based on the agreements in line with those effective at the national labor market Development of evaluation & assessment systems

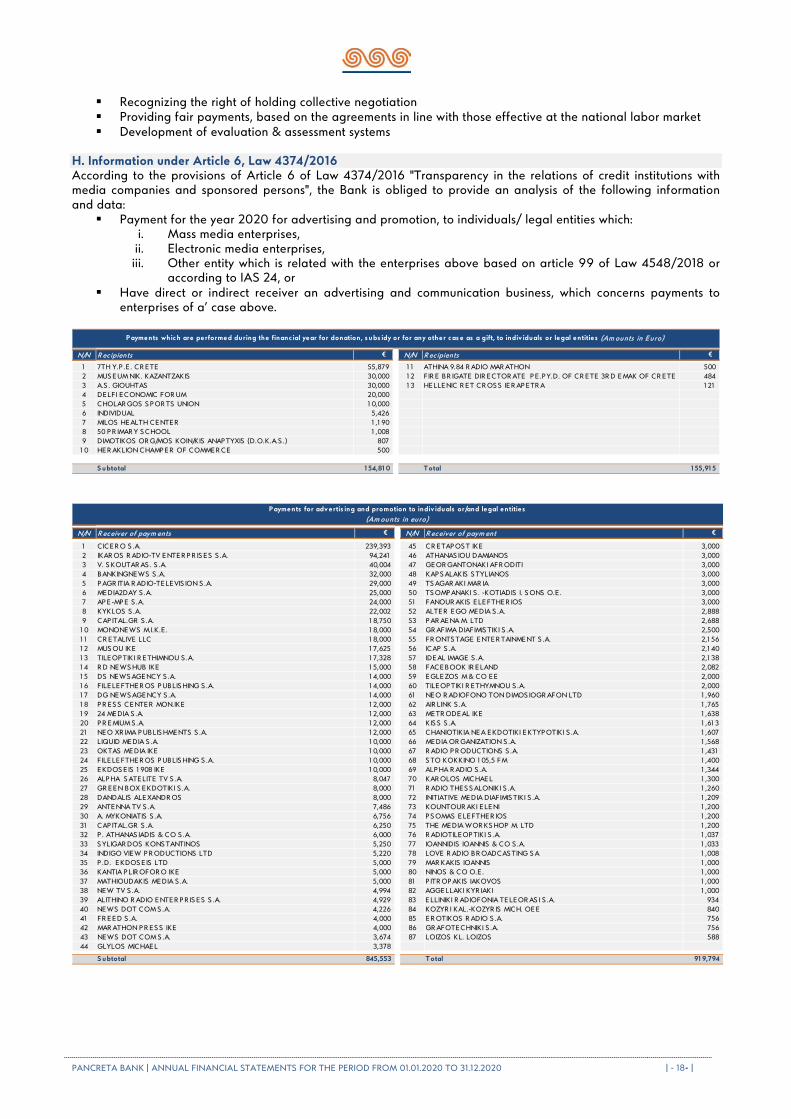

Η. Information under Article 6, Law 4374/2016 According to the provisions of Article 6 of Law 4374/2016 "Transparency in the relations of credit institutions with media companies and sponsored persons", the Bank is obliged to provide an analysis of the following information and data:

Payment for the year 2020 for advertising and promotion, to individuals/ legal entities which: i. Mass media enterprises, ii. Electronic media enterprises, iii. Other entity which is related with the enterprises above based on article 99 of Law 4548/2018 or

according to IAS 24, or Have direct or indirect receiver an advertising and communication business, which concerns payments to

enterprises of a’ case above.

N/N R ecipients € N/N R ecipients €

1 7TH Y.P .E . CR ETE 55,879 1 1 ATHINA 9.84 R ADIO MAR ATHON 500 2 MUS EUM NIK. KAZANTZAKIS 30,000 1 2 FIR E BR IGATE DIR ECTOR ATE P E .P Y.D. OF CR ETE 3R D EMAK OF CR ETE 484 3 A.S . GIOUHTAS 30,000 1 3 HELLENIC R ET CR OS S IER AP ETR A 1 21 4 DELFI ECONOMIC FOR UM 20,000 5 CHOLAR GOS S P OR TS UNION 1 0,000 6 INDIVIDUAL 5,426 7 MILOS HEALTH CENTER 1 ,1 90 8 50 P R IMAR Y S CHOOL 1 ,008 9 DIMOTIKOS OR G/MOS KOIN/KIS ANAP TYXIS (D.O.K.A.S .) 807

1 0 HER AKLION CHAMP ER OF COMMER CE 500

S ubtotal 1 54,81 0 Total 1 55,91 5

Payments which are performed during the financ ial year for donation, s ubs idy or for any other cas e as a gift, to indiv iduals or legal entities (Am ounts in Euro)

N/N R eceiver of paym ents € N/N R eceiver of paym ent €