a survey of 351 - american bar association · introduction • section 351 permits persons to...

TRANSCRIPT

A Survey of §351

American Bar Association

Section of Taxation

Boca Raton, Florida

January 21, 2011

Brandon Hayes Meghan Walsh Don Leatherman

Ernst & Young LLP WilmerHale University of Tennessee

Washington, DC Boston, MA Knoxville, TN

Introduction

• Section 351 permits persons to incorporate a business without immediate tax.

• It is a “non-recognition” provision, deferring, not eliminating, realized gain or loss.

• Its earliest predecessor was enacted in 1921 s an exception to recognition under the predecessor to §1001(c).

2

Outline of discussion

• Base cases

– Tax consequences

– Qualification

• Liability assumptions

• Additional rules

– Nonqualified preferred stock

– Bankruptcy transfers

– Investment companies

– Anti-abuse rules

3

Base cases

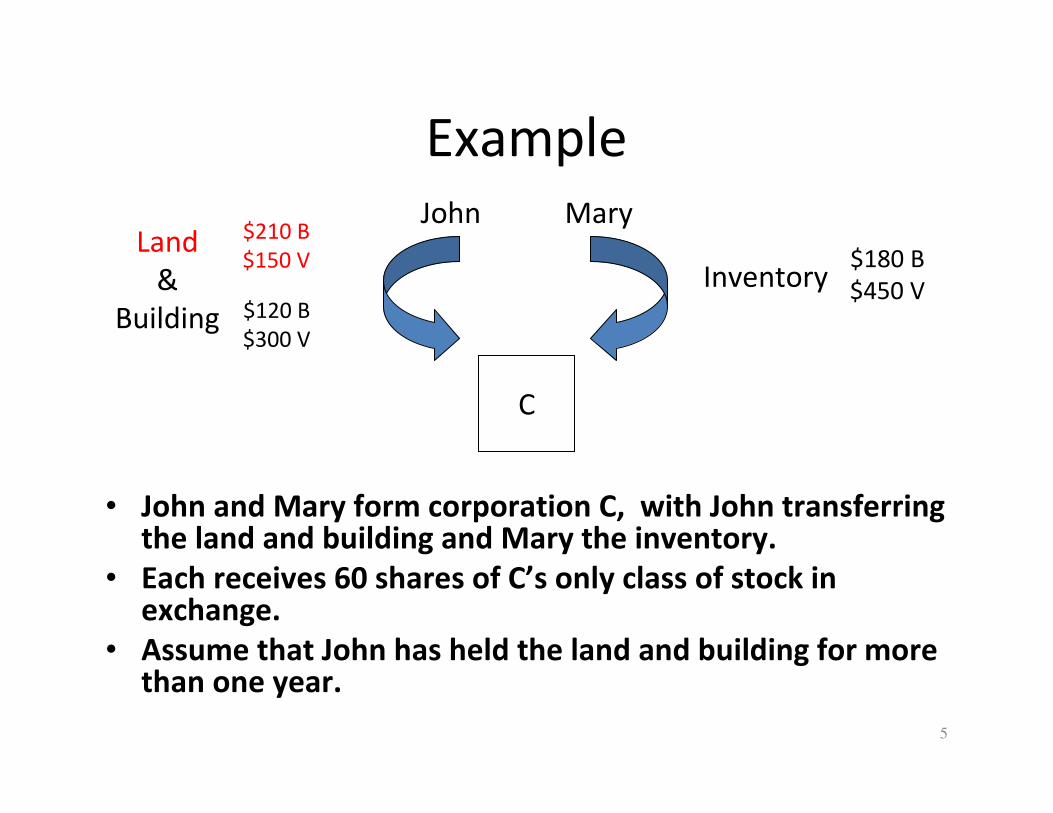

Example

• John and Mary form corporation C, with John transferring the land and building and Mary the inventory.

• Each receives 60 shares of C’s only class of stock in exchange.

• Assume that John has held the land and building for more than one year.

John

C

Land

&

Building

Mary

Inventory$180 B

$450 V

$210 B

$150 V

$120 B

$300 V

5

Shareholder consequences

If §351 applies to a person’s transfer of property to a corporation in exchange for the corporation’s stock –

– The person recognizes no loss and recognizes realized gain equal to the smaller of –

• Realized gain; or

• The value of any boot received.

§351(a) and (b).

– The person generally takes a basis in the stock received equal to the adjusted basis of the property transferred, plus any recognized gain, minus the value of any boot received. §358(a)(1); but see §362(e)(2).

6

Shareholder consequences (cont’d)

– The person takes a basis in any boot received equal

to its value. §358(a)(2).

– The holding period for stock received includes the

holding period of transferred property if the

property was a capital or §1231 asset. §1223(1).

– The holding period for boot received begins on the

exchange date.

7

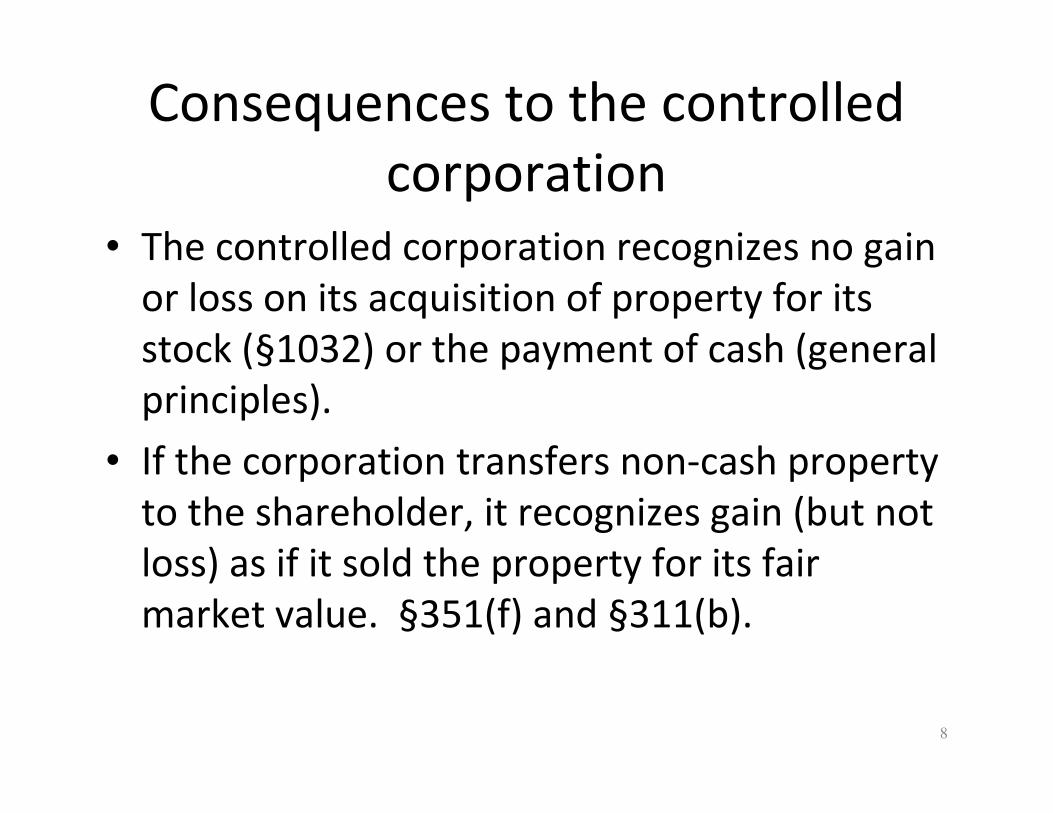

Consequences to the controlled

corporation

• The controlled corporation recognizes no gain

or loss on its acquisition of property for its

stock (§1032) or the payment of cash (general

principles).

• If the corporation transfers non-cash property

to the shareholder, it recognizes gain (but not

loss) as if it sold the property for its fair

market value. §351(f) and §311(b).

8

Consequences to the controlled

corporation (cont’d)

• Its basis in property acquired in the exchange generally equals the (i) shareholder’s adjusted basis plus (ii) any gain recognized by the shareholder on the exchange. §362(a)(1); but see §362(e).

• Its holding period for any property acquired includes the transferring shareholder’s holding period. §1223(2).

9

Example 1 – solely stock

• John and Mary form corporation C, with John transferring the land and building and Mary the inventory.

• Each receives 60 shares of C’s only class of stock in exchange.

• Assume that John has held the land and building for more than one year and that §351 applies to the exchanges.

John

C

Land

&

Building

Mary

Inventory$180 B

$450 V

$210 B

$150 V

$120 B

$300 V

10

Example 2 – boot to Mary

• The facts are the same as in the previous example, except that Mary receives 40 shares of C stock plus $150.

• How do the results change if C transfers Microsoft stock to Mary with –– A $120 basis and $150 value?

– A $170 basis and $150 value?

John

C

Land

&

Building

Mary

Inventory$180 B

$450 V

$210 B

$150 V

$120 B

$300 V

11

Multiple asset transfers --

Additional issues

If a shareholder transfers multiple assets to a corporation in a §351 exchange, how does the shareholder (i) allocate any boot received among the transferred assets and (ii) determine the holding period or periods of stock received?– See Rev. Rul. 68-55, 1968-1 C.B. 140 (requiring boot to be

allocated proportionately by value among the transferred assets).

– See Rev. Rul. 85-164, 1985-2 C.B. 117 (where relevant, requiring split bases and holding periods for each share received).

12

Example 3 – boot to John

The facts are the same as in Example 1, except

that John receives 40 C shares and $150 cash.

John

C

Land

&

Building

Mary

Inventory$180 B

$450 V

$210 B

$150 V

$120 B

$300 V

13

Section 362(e)(2)

Special basis rules apply to a §351 transfer if the controlled corporation would take an aggregate “loss”basis under §362(a) in property transferred to it by a taxable, domestic shareholder. See §362(e)(2). Cf. §362(e)(1).

• As a general rule, the corporation's aggregate basis in the property cannot exceed the property's value (i.e., the aggregate basis is reduced to the property's value). §362(e)(2)(A).– The total basis reduction is allocated among the transferred built-

in loss property in proportion their built-in losses. Id. at (e)(2)(B).

– Property has a built-in loss to the extent its adjusted basis exceeds its value.

14

Election

• In lieu of the corporation reducing its basis, the

transferring shareholder can take a fair market

value basis in the corporation's stock received

in the exchange. §362(e)(2)(C)(i).

• Both the transferring shareholder and

corporation must elect to have this rule apply.

Id. at (e)(2)(C)(ii).

15

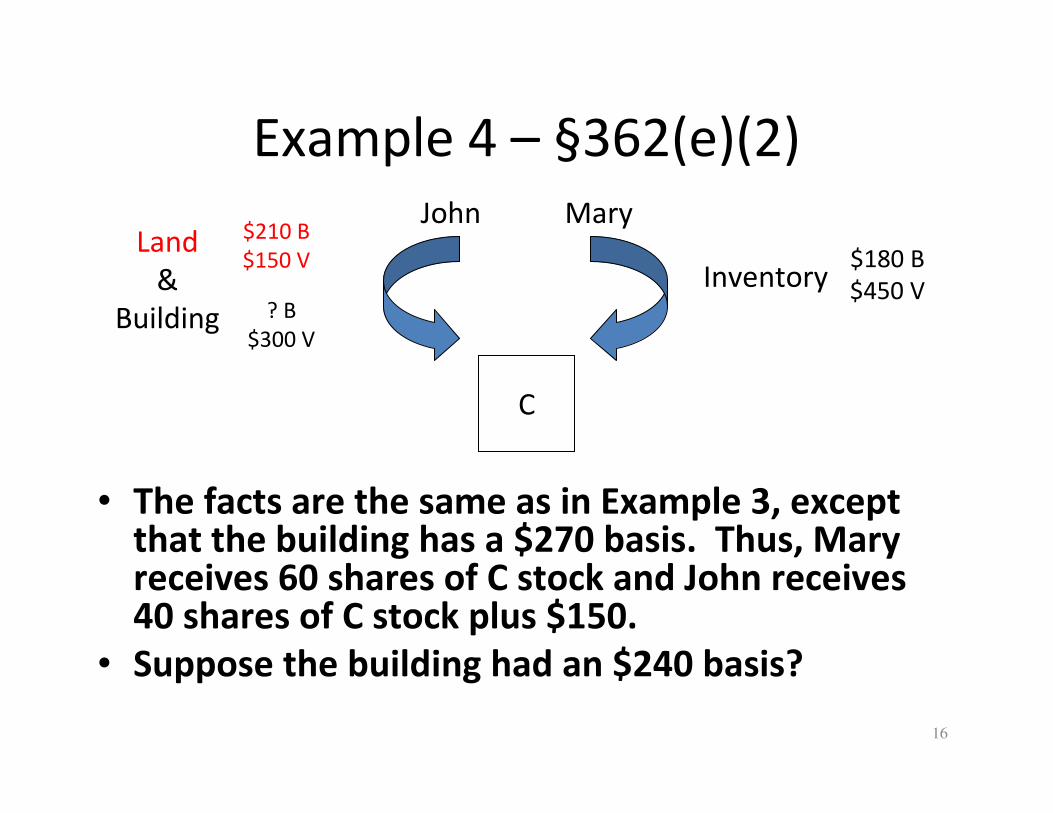

Example 4 – §362(e)(2)

• The facts are the same as in Example 3, except that the building has a $270 basis. Thus, Mary receives 60 shares of C stock and John receives 40 shares of C stock plus $150.

• Suppose the building had an $240 basis?

John

C

Land

&

Building

Mary

Inventory$180 B

$450 V

$210 B

$150 V

? B

$300 V

16

Section 351 -- Qualification

• A person or persons (the "transferor group") must transfer property to a corporation (the "controlled corporation")

• Each member of the transferor group must receive controlled corporation stock in the exchange.

• The transferor group must control the corporation immediately after the exchange

17

Section 351(a) -- Questions

• What is a "person"? See §7701(a)(1).

• What is "property"?

• Can stock be deemed received?

• When are persons considered part of a

transferor group? See Reg. §1.351-1(a)(1).

• How is control measured? See §368(c).

• What does it mean to control a corporation

"immediately after the exchange?”

18

Person -- § 7701(a)

A person includes an individual, a trust,

estate, partnership, association, company,

or corporation. See also Reg. §1.351-1(a)

(containing a similar definition).

19

When is property transferred?

• A person transfers property to a corporation if the person transfers all of his or her interests in an asset to the corporation.– Cf. DuPont v. U.S., 471 F.2d 1211 (Ct.Cl. 1973) (patent

holder transferred property when it transferred a non-exclusive license for the remaining life of a patent).

• A transfer of services is not a transfer of property, even if the service provider creates an asset. – Compare James V. Comm’r, 53 T.C. 63 (1969)

(shareholder provided a service when he acquired FHA commitment for a corporation) with U.S. v. Stafford, 727 F.2d 1043 (11th Cir. 1984) (shareholder transferred property to a corporation when he transferred a non-binding letter addressed to him promising financing).

20

Example 5 – Stock requirement

Section 351 does not apply to a person’s exchange, unless the person receives (or is deemed to receive) stock in the exchange.

• Is John deemed to receive C stock in the exchange?

• Would the answer change if John owned all C common stock and Mary owned all C non-voting preferred stock?

John

C

Property 100% John owns all C stock. He transfers

property to C but receives no stock

in exchange.

21

"Meaningless gesture" doctrine

• Under the "meaningless gesture" doctrine,

stock is deemed issued to a shareholder

without an actual issuance.

• This doctrine applies if, with or without a

stock issuance, the rights of the

corporation's shareholders would be the

same.

22

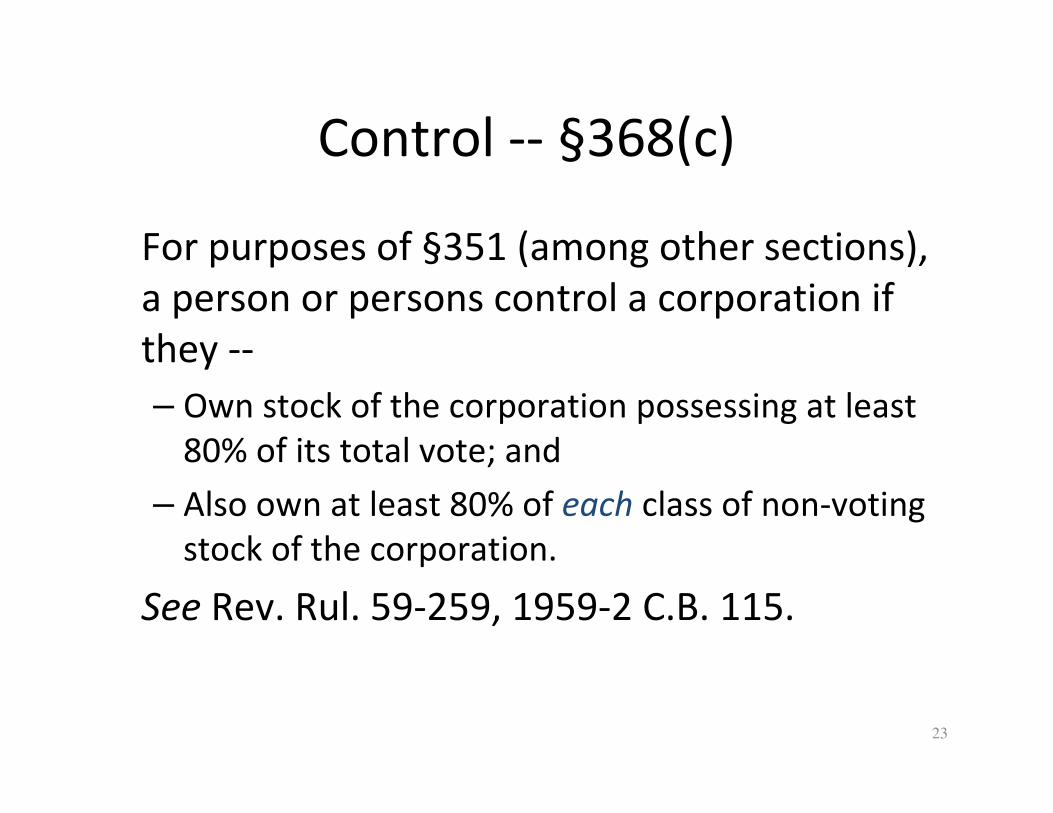

Control -- §368(c)

For purposes of §351 (among other sections),

a person or persons control a corporation if

they --

– Own stock of the corporation possessing at least

80% of its total vote; and

– Also own at least 80% of each class of non-voting

stock of the corporation.

See Rev. Rul. 59-259, 1959-2 C.B. 115.

23

When are persons members of a

transferor group?

• Persons generally are considered part of a transferor group if –– They exchange property for controlled

corporation stock under a plan that has previously defined their rights, and

– The plan is executed "with an expedition consistent with orderly procedure.“

Reg.§1.351-1(a)(1).• A person who makes an accommodation

transfer, however, is not treated as transferring property and thus cannot be part of a transferor group.

24

Accommodation transfers

A person makes an accommodation transfer if--

– In a purported §351 exchange, the person is issued controlled corporation stock for property that has a relatively small value compared with the stock he or she already owns (or will receive for services); and

– The person's primary purpose for the transfer is to qualify others under §351.

Reg. §1.351-1(a)(1)(ii).

25

Kamborian v. Comm’r, 56 T.C. 847

(1971)

• Solely in exchange for I/S stock, A-D transfer X stock to I/S and E transfers $5000 to I/S.

• Before the exchange, E owned about $595,000 of I/S stock.

• Immediately after the exchange, A-E own more than 80% of the I/S stock, but A-D own less than 80% of that stock.

• E’s primary purpose in making the transfer was to qualify A-D under §351. E made an accommodation transfer.

I/S

A B C D E Others

26

Rev. Proc. 77-37

Safe harbor

Under § 3.07 of Rev. Proc. 77-37, property

transferred in a purported § 351 transfer is

not treated as having a relatively small

value if it has a value equal to at least 10%

of the controlled corporation stock the

transferor already owns (or to be received

for services).

27

Immediately after the exchange;

Intermountain Lumber, 65 T.C. 1025 (1976)

• Before Step 1, S had a binding obligation to complete Step 2, and S

did not own the stock transferred in step 2 “immediately after the

exchange.”

• What if S did not have a binding obligation to complete Step 2?

Step 1

S&W

Sawmill

business

S

All S&W

stock

Step 2

S W

50% of S&W stock

$91,000

obligation

28

Liability assumptions

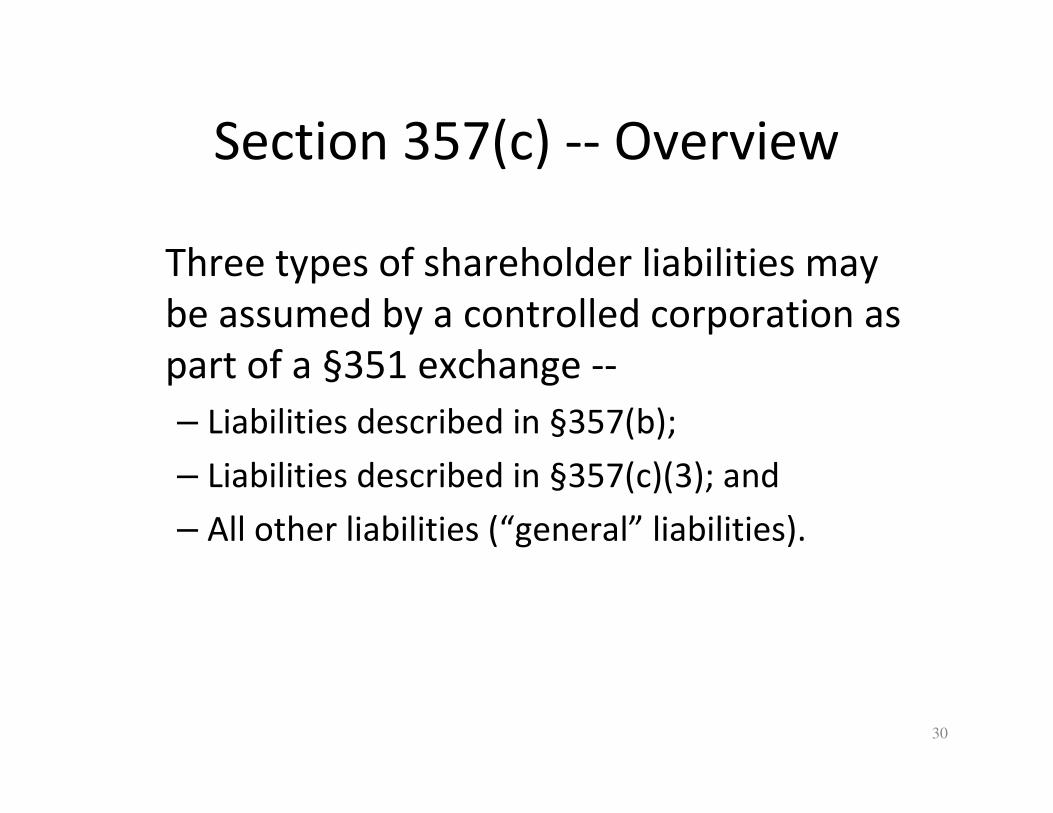

Section 357(c) -- Overview

Three types of shareholder liabilities may

be assumed by a controlled corporation as

part of a §351 exchange --

– Liabilities described in §357(b);

– Liabilities described in §357(c)(3); and

– All other liabilities (“general” liabilities).

30

When is a liability assumed?

– A corporation is treated as assuming a recourse liability

to the extent it agrees to and is expected to satisfy the

liability. §357(d)(1)(A).

– A corporation is treated as assuming the entire

amount of any non-recourse liability to which

transferred property is subject, reduced by the lesser

of --

• The portion of the liability secured by non-transferred

property that its owners have agreed, and are expected, to

satisfy, or

• The fair market value of the non-transferred property.

§357(d)(1)(B) and (2).

31

Section 357(b) and (c)(3) liabilities

• All assumed liabilities of a shareholder are §357(b) liabilities if one of those liabilities was assumed for a tax-avoidance purpose (or for a non-bona fide business purpose).– For purposes of §351 and §358, the assumption of these liabilities is

treated as money received in the exchange. They are disregardedfor purposes of §357(c)(1).

• A §357(c)(3) liability is one that, if paid by the shareholder, would have resulted in a deduction or added basis.– For purposes of §351, §357(c)(1), and §358, these liabilities are

disregarded.

– See Rev. Rul. 94-73, 1994-2 C.B. 36. See also Rev. Rul. 80-198, 1980-2 C.B. 113 (allowing the transferee corporation to deduct a “deductible” liability, unless the §351 exchange improperly separated income and related expenses).

32

General Liability -- Treatment

If the corporation assumes a shareholder’s general liabilities, the shareholder --

– Has gain to the extent that the aggregate amount of those liabilities exceeds the shareholder’s aggregate basis in the transferred property (§357(c)(1));

– Does not treat their assumption as the payment of boot for purposes of §351 (§357(a)); but

– Treats their assumption as money paid in the exchange for purposes of §358 (§358(d)(1)).

33

Example 6 – general liabilities

• What happens if the property has an aggregate basis of (i)

$120 or (ii) $70?

• What would happen in the latter case if John also contributed

his promise to pay C $30? Cf. Perrachi v. Comm’r, 143 F.3d

487 (9th Cir. 1998); Lessinger v. Comm’r, 872 F.2d 519 (2d Cir.

1989).

John

C

PropertyJohn transfers property worth

$200 to C for all C stock plus C’s

assumption of John’s $100 general

liability.

34

Additional rules

Nonqualified preferred stock

– Nonqualified preferred stock is treated as boot in applying §351,

although it is treated as stock in measuring control.

– With some exceptions, preferred stock is non-qualified preferred

stock if --

• The issuer (or a related person under §267(b) or §707(b)) is either--

– Required to redeem the stock, or

– Has the right to redeem the stock and the right is more likely than not

to be exercised;

• The holder can require either to redeem the stock;

• The dividend on the stock varies with interest rates, commodity

prices, or similar indices.

– For this purpose, preferred stock is stock that is limited and

preferred as to dividends and that does not participate in

earnings to any significant extent.

36

“Bankruptcy” rules

• For purposes of §351, stock issued for the

following consideration is not deemed issued

for property --

– Indebtedness of the transferee corporation not

evidenced by a security; and

– Interest on transferee debt accrued after the

transferor’s holding period for the debt began.

• The transferor recognizes gain or loss (in the

first case) or interest income (in the second).

37

Investment companies

• Section 351(e)(1): A transfer of property to an investment company will not qualify for tax-free treatment under §351.– The Code does not define an “investment company.”

– Unlike §721(b) (the parallel provision for partnerships), the provision does not deny a loss for a transfer to an investment company.

• Reg. §1.351-1(c)(1): §351(e) will apply if --– The transfer results, directly or indirectly, in diversification of the transferors’

interests, and

– The transferee is a (i) RIC, (ii) REIT, or (iii) corporation more than 80 percent the value of whose assets are specified assets that are held for investment (an “80% Corporation”).

• A transfer ordinarily results in diversification if two or more persons transfer non-identical assets to a corporation in the exchange (unless each person is transferring a diversified portfolio of securities).

38

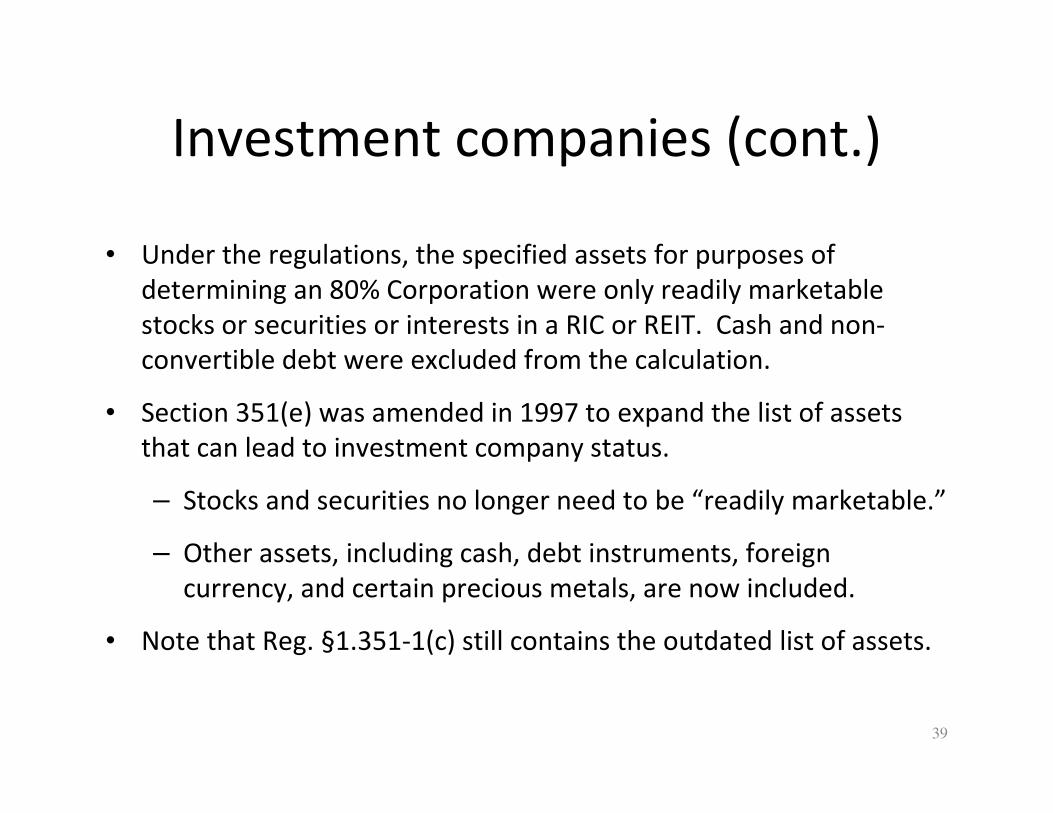

Investment companies (cont.)

• Under the regulations, the specified assets for purposes of

determining an 80% Corporation were only readily marketable

stocks or securities or interests in a RIC or REIT. Cash and non-

convertible debt were excluded from the calculation.

• Section 351(e) was amended in 1997 to expand the list of assets

that can lead to investment company status.

– Stocks and securities no longer need to be “readily marketable.”

– Other assets, including cash, debt instruments, foreign

currency, and certain precious metals, are now included.

• Note that Reg. §1.351-1(c) still contains the outdated list of assets.

39

Section 358(h)

• Under this provision, a shareholder's basis in stock received in a §351 exchange is reduced if --– The corporation assumes a shareholder's §357(c)(3) or

contingent liability, and

– Under §358(a)(1), the shareholder's basis in the corporation's stock exceeds its value.

• If §358(h) applies, the stock basis is reduced (but not below its value) by the amount of those assumed liabilities.– This reduction does not occur if the trade or business with

which the liability is associated is transferred to the corporation.

• It is unclear how §358(h) is coordinated with §362(e)(2).

40

Example 7 -- §358(h)

• P and S file consolidated returns.

– P sells the S pure vanilla preferred stock for $1 million.

– S pays off the $99 million pension liability.

• What happens?

S

P

$100 million$1 million S vanilla preferred stock

+

Assumption of P’s $99 million pension liability

41

Section 362(e)(1)

• This provision applies if --

– The transferee corporation would take a net built-in loss in property transferred in a §351 exchange under §362(a),

– The transferor is not subject to tax on the property immediately before the transfer, but

– The transferee is subject to tax on the property immediately after the transfer.

• If the provision applies, the transferee takes fair market value bases in the property.

42

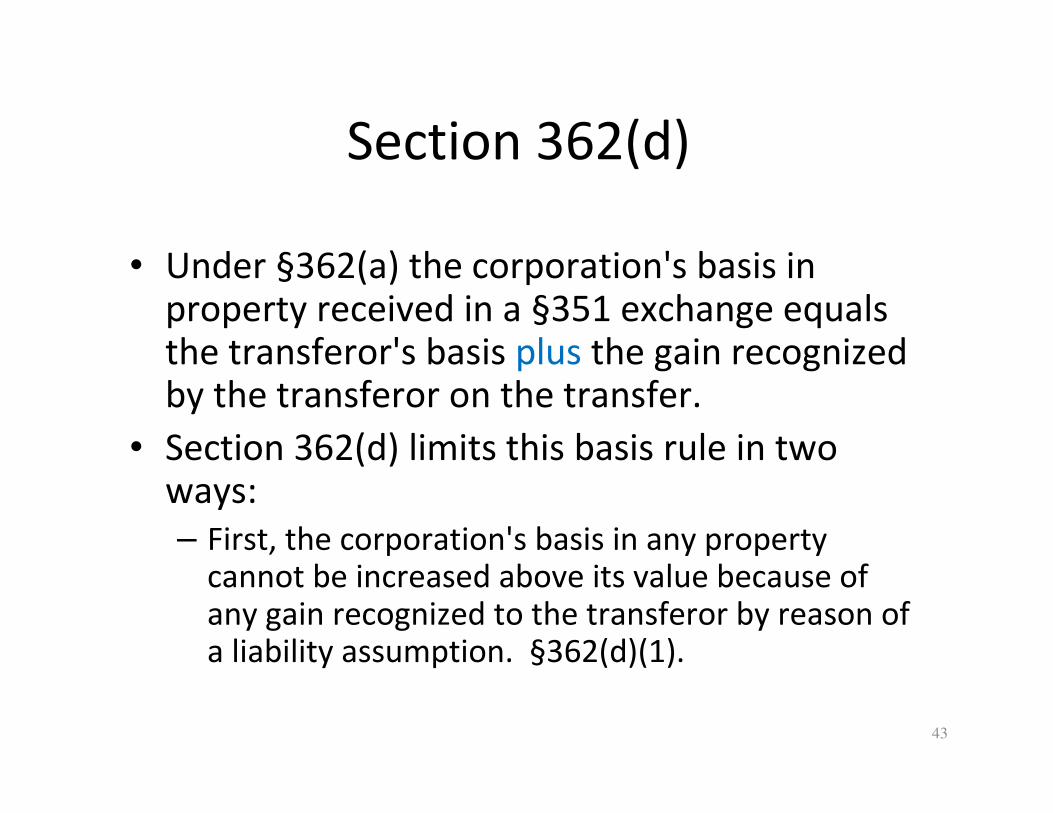

Section 362(d)

• Under §362(a) the corporation's basis in property received in a §351 exchange equals the transferor's basis plus the gain recognized by the transferor on the transfer.

• Section 362(d) limits this basis rule in two ways:

– First, the corporation's basis in any property cannot be increased above its value because of any gain recognized to the transferor by reason of a liability assumption. §362(d)(1).

43

Section 362(d)(2)

– Second, a special rule applies if --

• The transferor recognizes gain on the assumption of a non-recourse liability secured by non-transferred assets, and

• No person is subject to federal income tax on that gain.

– Then, the gain deemed recognized in applying §362(a) is computed as if the assumed liability equaled the transferee's ratable portion of the liability, based on the values of all assets subject to the liability.

44

Example 8 -- §362(d)(2)

• FP is a foreign corporation not subject to U.S. tax. S is

a domestic corporation.

• The liability is secured by $999,900 of other assets

retained by FP.

• S’s basis in the asset is $100.

S

FP

AssetS stock

+

Taking asset subject to $1 million liability

$100 B

$100 V

45