a study on growth of limited liability partnerships … govindan 361-388.pdfgovindan: a study on...

TRANSCRIPT

Prajnan, Vol. XLVII, No. 4, 2018-19 © 2018-19, NIBM, Pune

Received: 29/08/2018

Accepted: 31/10/2018

A Study on Growth of Limited LiabilityPartnerships (LLPs) in India – An Innovative

Vehicle for Entrepreneurial Development

P Govindan

This present study aims to assess the trend of registration of LimitedLiability Partnerships (LLPs) in India after implementation of companiesAct 2013 and Goods and Services Tax Act 2017. This study usesdescriptive and inferential statistical tools for analysis andinterpretation of data. This study results indicate that economic activity-wise maximum numbers of registered and active LLPs were in servicesectors 76 per cent, followed by industry 22 per cent and agriculturesectors 2 per cent. This study finally concluded and suggests thatState, Central and Union Territories (UTs) governments, must takenecessary steps for increasing new startups in LLPs in India. Theseinclude financial assistance at concessional rates, tax holidays,subsidies for existing as well as new domestic and foreignentrepreneurs. It creates better environment for investors by enhancingease of doing business indicator in India and protecting theirinvestments.

Keywords: Goods and Service Tax (GST), Taxation, Company Performance

JEL Classification: G18, G30, H20

Section IIntroduction

In today's modern commercial world everyone wants to decrease his liabilitiesand likes to live in a flexible but profitable environment. Based on the sameline the new concept of Limited Liability Partnership and its association withthe corporate form has evolved. The origins of the concept of limited liabilitycan be traced back to medieval times (Lipton, 2018). Limited partnershipscan be traced to early French law. It's starting with the development of theconcept of general partnership, moving on to the idea of limited partnership

P Govindan ([email protected]), Assistant Professor in Commerce, Department of Commerce,K S Rangasamy College of Arts and Science (Autonomous), Tiruchengode 637 215, Namakkal, TamilNadu, India,

362 Prajnan

which finally led to the concept of limited liability partnership. The origin ofthe concept of limited liability partnerships can be traced to the growth oflimited liability business forms in United States (Meena & Nainawa, 2010).The first LLP legislation in the US was passed in Texas in 1991 and limitedliability Signaled comfort with business entity combining statutory limitedliability protection.

The introduction of general limited liability did not, however, completelyeliminate the liabilities of the shareholder (Ireland, 2010). Corporate limitedliability refers to a widespread legal principle that limits the accountabilityof shareholders-owners for the debts of their companies to the currentvalue of their shareholding (Blankenburg, et. al. 2010). The sudden emergenceof new limited liability vehicles notably limited liability companies and limitedliability partnerships (LLPs) suggest a revolution in the law of limited liabilitystriking resemblance to modem forms of business association, most notablythe limited liability partnership (William, 1997). The widespread adoption oflimited liability company statutes has been a much-heralded development incorporate law (Maizes, 2012). The concept of limited liability fueled thepopularity of joint-stock companies need to incorporate necessary changes incorporate laws new regulatory environment for incorporation with limitedliability. It is an alternative form of organization and facilitates their evaluationof the investing opportunity realized at different times and indifferent countriesas the preferred business form for small firms.

The invention of the limited liability company in the mid-nineteenth centuryled to the formation of vast amounts of capital, the generation of countlessjobs, and the creation of incredible worldwide wealth over the years (Tricker,2011). Limited liability therefore may be an efficient and the new law alsotransits significant role in a country's economy and make a special contributionto national development. LLP is one of widespread forms of corporation andwas introduced into circulation in the 19 century and significant changes inthe provisions related to governance, e-management, compliance andenforcement of disclosure norms. Governments worldwide recognize theeconomic, political benefits of improved business regulation, reforms to easedoing business, importance of effective corporate governance and reformsnecessary for development and growth of economy.

The limited liability form most common among domestic firms is chosenpromote domestic investment depending on how business friendly entryregulations are in the host economy. Service sectors in providing employmentopportunities for the growing workforce and comparatively new form ofbusiness organization in India. For startups, partnership is one of the mostcommon forms of organization to commence business. Until 2008, anypartnership formed in India implied unlimited liability for the partners. LimitedLiability Partnerships (LLPs), making it possible for every member of anordinary partnership to limit their liability.

Govindan: A Study on Growth of Limited Liability Partnerships (LLPs) in India 363

Limited Liability Partnership in India and Advantages – An OverviewLimited Liability Partnership (LLP) is a legal form which is governed by theLimited Liability Partnership Act, 2008. LLP is a new business vehicle in bodycorporate form, and therefore, a separate legal entity which limits the liabilityof the partners to their agreed contribution. Any two or more individuals orbodies corporate may incorporate an LLP for carrying on a lawful businesswith a view to profit. LLP structure is not restricted to any specific trade,business, profession or service. LLP is a legal entity separate from its partnersand has perpetual succession. The LLP structure allows the enterprises theflexibility of organizing internal structure as a partnership.

The provisions of the newly enacted Limited Liability Partnership Act, 2008have been notified for implementation with effect from 31-03-2009. The LimitedLiability Partnership Rules, 2009 have been notified on 01st April 2009. Theprovisions relating to conversion of partnership firms, private company andunlisted public company into LLP came into effect from 31st May 2009. InIndia about 95 per cent of the industrial units are small and medium enterprises(SMEs). As per the survey conducted by the Ministry of Micro, Small andMedium enterprises (MSME), over 90 per cent of these SMEs are registered asProprietorships, about 2 per cent to 3 per cent as Partnerships and less than2 per cent as Companies. The corporate form does not appear to be widelyprevalent amongst SMEs. On an assessment of the data collected by the Ministryof MSME, it was found that the high compliance cost under the CompaniesAct, 1956 deterred the SMEs from adopting the corporate form.

In this background, a need was felt for a new corporate form that would providean alternative to the traditional partnership with unlimited personal liabilityon the one hand, and the statute-based governance structure of the limitedliability company on the other, in order to enable professional expertise andentrepreneurial initiative to combine, organize and operate in a flexible,innovative and efficient manner. Internationally, Limited Liability Partnerships(LLPs) are the preferred vehicle of business particularly for the service industryor for activities involving professionals, especially in countries like the UnitedKingdom, United States of America, Australia, Singapore, etc.

The Government has therefore permitted the Limited Liability Partnership formof business organization in India with a view to creating a facilitatingenvironment for entrepreneurs, service providers and professionals to meetthe challenges of global competition. Parliament enacted the Limited LiabilityPartnership Act, 2008, which was notified on 09.01.2009, and came to effecton 31.03.2009. The enabling rules were notified on 01.04.2009 and the firstLLP was registered on 02.04.2009. LLP is an alternative corporate businessvehicle that enables professional expertise and entrepreneurial initiative tocombine and operate in a flexible, innovative and efficient manner, providingbenefits of limited liability while allowing its members the flexibility fororganizing their internal structure as a partnership based on an agreement. It

364 Prajnan

is a form of business entity, which allows individual partners to be protectedfrom the joint and several liabilities of partners in a partnership firm.

The Liability of partners incurred in the normal course of business does notextend to the personal assets of the partners. It is capable of entering intocontracts and holding property in its own name. An LLP would be able tofulfill the compliance norms with much greater ease, coupled with limitationof liability. The corporate structure of LLP and the statutory disclosurerequirements would enable higher access to credit in the market. Only LLPswith turnover exceeding 40 lakh and contribution exceeding Rs. 25 lakh haveto get their accounts audited, providing for much greater flexibility. Theintroduction of LLP form of business is expected to promote entrepreneurship,particularly in relation to the knowledge based industries, such as theinformation technology and biotechnology sectors, and other service providersand professionals.

In order to enhance and extend the operational convenience to stakeholders,and grouping of all registry related functions on a single platform, LimitedLiability Partnership (LLP) e-governance was integrated with MCA21 from11.06.2012. With this integration, the filing and approval of 'LLP forms' isbeing done through the MCA 21 website, and stakeholders are presently availingall existing facilities of MCA 21 for LLP forms filing, including online payment,or use of internet banking from designated banks, in addition to credit cardpayment. In addition, the regulation of LLPs has been decentralized amongstthe 20 Registrars of Companies across the country, enabling direct promotionof the new form of corporate entity in their region (Various Annual Reports,Ministry of Corporate Affairs, Government of India). Natural persons and bodycorporate, Indian or foreign, can be partners in an LLP. At least two of themhave to be "Designated Partners", of which at least one should be a resident inIndia. A body corporate can also be a designated partner, and in such a case,an individual authorized by the body corporate will function as the designatedpartner. The LLP can continue its existence irrespective of changes in partners.

GST – The Game Changer in Indian Corporate SectorsGST was firstly introduced in France in 1954, with introduction of GST Francebecame the first country ever to introduce GST (Kour et. al. 2016). TheGoods and Services Tax (GST) is one of the biggest economic and taxationreforms undertaken in India. In India goods and service tax was a historicalmovement for implementation a significant indirect tax reforms. It means thatmixed up various numbers of indirect taxes which levied by both central andstate government to made up a single tax. After the enactment of various GSTlaws, GST was launched with effect from 1st July 2017 by Shri Narendra Modi,Hon'ble Prime Minister of India in the presence of Shri Pranab Mukherjee, thethen President of India in a mid-night function at the Central Hall of Parliamentof India. The objective being, to bring about uniformity in taxation by merging

Govindan: A Study on Growth of Limited Liability Partnerships (LLPs) in India 365

all these taxes, which in turn will assist in reducing the hassles of compliancesassociated and help in improving tax governance in India (Deo, 2017).

The advantage of GST is that it will replace Indirect Taxes which are levied byCentral and State Government. The GST structure will present a transparentsystem which will be helpful to reduce the burden of cascading effectand it will also improve the tax compliances and tax collection. GST willprove the uniformity of taxes in all over the country. The GST based taxationsystem brings more transparency in taxation system reduces tax theft andcorruption in country. GST is one indirect tax for the whole nation, which willmake India one unified common market. It is a single tax on the supply ofgoods and services, right from the manufacturer to the consumer.

This tax reform will lead to creation of a single national market, common taxbase and common tax laws for the Centre and States. This tax reform will besupported by extensive use of Information Technology, which will lead to greatertransparency in tax burden, accountability of the tax administrations of theCentre and the States and also improve compliance levels at reduced cost ofcompliance for taxpayers. Studies indicate that introduction of GST wouldinstantly spur economic growth and can potentially lead to additional GDPgrowth in the range of 1 per cent to 2 per cent.

Advantages to Trade and IndustrySimpler tax regime with fewer exemptions;

Increased ease of doing business;

Reduction in multiplicity of taxes that are at present governing our indirecttax system leading to simplification and uniformity;

Elimination of double taxation on certain sectors like works contract, software,hospitality sector;

Will mitigate cascading of taxes as Input Tax Credit will be available acrossgoods and services at every stage of supply;

Reduction in compliance costs – No multiple record keeping for a variety oftaxes – so lesser investment of resources and manpower in maintainingrecords;

More efficient neutralization of taxes especially for exports thereby makingour products more competitive in the international market and give boost toIndian Exports;

Simplified and automated procedures for various processes such asregistration, returns, refunds, tax payments, etc;

Average tax burden on supply of goods or services is expected to come downwhich would lead to more consumption, which in turn means more productionthereby helping in the growth of the industries manufacturing in India.

366 Prajnan

Table 1Comparison of LLP with Partnership Firm,

Public Company and Private Company

S.No. Points of Limited Liability Partnership Public PrivateComparison Partnership Company Company

1 Act Applicable LLP Act,2008 Partnership Companies CompaniesAct,1932 Act, 2013 Act, 2013

2 Registration Registration with Registration Registration RegistrationROC required Optional with ROC with ROC

required required

3 Numbers of Minimum-(2) Minimum-(2) Minimum-(2) Minimum-(2)partners/ Maximum- Maximum-(20) Maximum- Maximum-Members Unlimited Unlimited (200)

4 Agreement LLP Agreements Partnership Memorandum MemorandumDocuments Deed and articles of and articles

association of association

5 Liability Limited Unlimited Limited Limited

6 Legal entity Yes, Can sue or No separate Yes, Can sue or Yes, Can suebe sued in the legal entity be sued in the or be sued inname of LLP name of Public the name of

company Privatecompany

7 Minimum No No Rs.5,00,000 Rs.1,00,000Capital Requirement Requirement

8 Terms used LLP &Co. limited Private limitedat end name

9 Succession Perpetual Ceases to exist Perpetual PerpetualSuccession on change or Succession Succession

death of partner

10 Board of No No Minimum-(3) Minimum-(2)Directors Requirement Requirement Maximum-(15)

11 Number of As per LLP As per (4) Meetings are (4) MeetingsBoard Meetings Agreements Partnership Mandatory in are Mandatory

Deed every year in every year

12 Shareholders Not Not As per As perMeeting Applicable Applicable companies Act companies Act

13 Maintenance of Not Not Applicable, As Applicable, AsStatutory Applicable Applicable per companies per companiesRegisters Act 2013 Act 2013

14 Conversion Can be converted Can be Can be Can beinto a company converted into converted into converted into

a company or a Company or company ora LLP a LLP a LLP

15 Directorship/ Foreign National Foreign National Foreign National ForeignPartnership can be partner cannot be partner can be Director National can be

in LLP in firm (expect in the company Director in thesome cases) company

16 Dissolution By agreement or By agreement, By court order By court orderby order of mutual consent, once the affairs once the affairsNational Company insolvency of the company of the companyLaw Tribunal have wound up have wound up

Govindan: A Study on Growth of Limited Liability Partnerships (LLPs) in India 367

ObjectiveThe global business regulatory environment has changed dramatically. Policyreforms catalyze private investment. Promoting a well-functioning private sectoris a major undertaking for any government. It requires long-term policies ofremoving administrative barriers and strengthening laws that promoteentrepreneurship (Georgieva, 2018). The composition and quality of taxationcan have a significant impact on productivity and economic growth. India maderesolving insolvency easier by adopting a new insolvency and bankruptcy codethat introduced organization procedure for corporate debtors and facilitatedcontinuation of the debtor's business during insolvency proceedings. Indiareduced the number of procedures and time required to obtain a buildingpermit by implementing an online system and made paying taxes easier byrequiring that payments be made electronically and in a historic tax reform,the goods and services tax was rolled out on 1st July, 2017, subsuming almostall major indirect taxes enable the new entrants to establish business operationsin India. In this above surroundings this research study examines the Growthof Limited Liability Partnerships in India, Obligation of Contribution and alsolook into sectors-wise Active Limited Liability Partnerships (LLPs) in India ason 30th June, 2017.

Significance of the studyThe opening of the Indian economy, the entrepreneurship, knowledge and riskcapital had combined to provide a further impetus to India's economic growth.LLP is one of widespread forms of corporation, flexible legal structures, offerlimited liability and rapidly emerging as an alternative to companies andpartnership firms which have traditionally been used as forms of businessentities. The LLP is a kind of a hybrid entity which combines the advantages ofa partnership firm and a limited company. It provides the benefits of limitedliability, greater tax efficiency and allows its members the flexibility of organizingtheir internal structure as a partnership based on a mutually arrived atagreement. India continues to be one of the fastest growing large economies inthe world witnessing an upward moving trend in LLP registrations and thenew small and medium start ups prefer LLP as it is tax efficient and burden ofcompliance is lesser as compared to company and low compliance regime of apartnership. In order to attract new investments, develop infrastructure andpromote export industries, India offers various incentives such as tax holidays,investment allowances, tax credits, rebates. In this environment this researchpaper mainly will focus on Growth of Limited Liability Partnerships in India,Obligation of Contribution and also explore sector-wise such as agricultureand allied activities, industry, manufacturing, construction, business services,electricity, gas and water, mining & quarrying, transport, storage andcommunication, community, personal & social services, real estate and rentingactive limited Liability Partnerships (LLPs) as on 30th June, 2018.

368 Prajnan

Section IILiterature Review

Fletcher , Hughes and Williams (2013) examined the distribution and sectoralbreakdown of LLPs in the UK, explained the growth in number of LLPsregistered, identified the factors underlying decisions to adopt or not adoptthe LLP form assessed whether the LLP form has encouraged greater economicactivity/likelihood of starting a business, Categorized different forms and typesof LLPs within the SME sector and evaluated the tax benefits and tax incentivesassociated with setting up an LLPs.

Sharma and Garg (2014) Attempted issues relating to concepts, various taxationand implementation of Limited Liability Partnerships. The paper concludedthat inner future, more Limited Liability Partnerships will come into existencegiven its advantages over the partnership and company form of organizationin India.

Singh (2007) suggested that suitable changes in the provisions of income taxrelated with the taxations issues; because taxation is one the major motivationalfactor other then limited liability for the partners of LLPs.

Bharat (2013) concluded that LLP vehicle will be advantageous and will promisea glowing and blushing future for the Indian business environment. Varottil(2014) explained political, legislative process, critical aspects of the IndianLLP Act, and examined some of the challenges and uncertainties that mayderail the success of the LLP form. This study concluded that evolution andrationale for the LLP Act is extremely relevant and timely, especially given thelimited literature about this business form in India. Gandhi and Thakurconcluded that SMEs which are looking for such a business structure whichhas a limited liability along with less cumbersome setting up and taxationprocedures, LLP is the best option to go for and also suggested that these needto be addressed by the law makers for smooth running of such structure.Khan, and Azam, Nagma (2012), explained that GST would be beneficialfor the consumers as it reduces the final burden of taxation.

This research paper examined many international and national and researcharticles, studies, journals, working papers, books, policy documents, localand international news papers and seminars edited publications relating toLLPs. This study investigates and brings out the growth of LLPs. It also examinesobligation of contribution and of economic activity-wise of LLPs in India as on30th June, 2018.In these environments the current research differs from theearly researches in various ways and presents the existing literature.

Govindan: A Study on Growth of Limited Liability Partnerships (LLPs) in India 369

Section IIIResearch Methodology

Data Collection and Statistical Tools

The research study is explorative in nature and will be based on in-depthanalysis of data and statistics, collected from the secondary sources. It includesinformation collected from Ministry of Corporate Affairs, Ministry of Tradeand Commerce, WTO Reports, World Bank Reports, Reserve Bank of India,Ministry of Finance, NITI Aayog, various professional institutes Reports,Journal/Article published, reference books related to corporate law, bar acts,publications by the states and central government in India websites andinternational organizations relating to commerce and trade. In this study useddescriptive statistical tools such as percentage analysis, tables, and charts areused for analysis and interpretation of data. This present's research studyperiod covers LLPs in India as on 30th June, 2018.

Objectives of the studyThe following are the objectives of the present study:

To analyse the total numbers of registered Limited Liability Partnerships (LLPs)in India as on 30th June, 2018.

To assess the economic activity-wise number and authorized capital wise activeLimited Liability Partnerships (LLPs) in India as on 30th June, 2018.

To examine obligation of contribution wise active Limited LiabilityPartnerships(LLPs) as on 30th June, 2018

To investigate on impact LLPs registrations before and after implementationof Companies Act 2013 and Goods and Services Tax Act 2017 as on 30thJune, 2018.

Analysis and Description of DataTable 1a and Chart 1 indicates that the financial year wise LLPs registrationand total obligation (Rs. in crore) from 01.04.2009 to 30.06.2018. Since thentotal of 1, 26,733 LLPs had been registered with Total Obligation of Contribution(Rs. in crore) 38,447.21 in the country, as on 30.06.2018.They comprise freshentities registered as LLPs, and companies and partnership firms that havebeen converted into LLPs.

370 Prajnan

Table 1aTotal Number of LLPs Registered and Total Obligation of

Contribution as on 30.06.2018

Financial Year Total Number of Per cent growth Total Obligation Per cent growth(April to March) LLP Registered over previous year of Contribution over previous

(Rs. in. Crore) year

2009-10 1,055 – 596.55 –

2010-11 3,261 209 2758.37 462.39

2011-12 4,319 32 3049.73 110.56

2012-13 5,167 20 1854.50 -60.81

2013-14 7,982 54 2029.56 109.44

2014-15 14,682 84 2650.05 130.57

2015-16 22,505 49 8872.33 334.80

2016-17 29,407 34 8,420.63 94.91

2017-18 32,934 22 5,545.15 65.85

2018-19 *(Upto 5,421 – 2,670.34 –30.06.2018)

TOTAL 1,26,733 38,447.21

Source: Ministry of Corporate Affairs, Monthly Information Bulletin on Corporate Sector

During the financial year from 2009-10 totally 1,055 LLPs registered, followedby next financial year 2010-11 totally 3,261 LLPs have been registered,compared to the previous year's figure of more than two times were increasedfor the corresponding period. During the all financial years, year 2011-12 (32percent), 2012-13 (20 per cent), 2013-14 (54 per cent), 2014-15 (84 per cent),2015-16 (49 per cent), 2016-17 (34 per cent) and 2017-18 (22 per cent) areshowed percentage of growth over previous year are in positive growing trend.Chart 1 depicts the number of LLPs registered during the 2009-10 to30.06.2018. Total obligation (Rs. in crore) from 01.04.2009 to 30.06.2018shows as increasing trend except in the 2012-13 indicates at negative growth.

Chart 1Total number of LLPs Registered as on 31.03.2018

Govindan: A Study on Growth of Limited Liability Partnerships (LLPs) in India 371

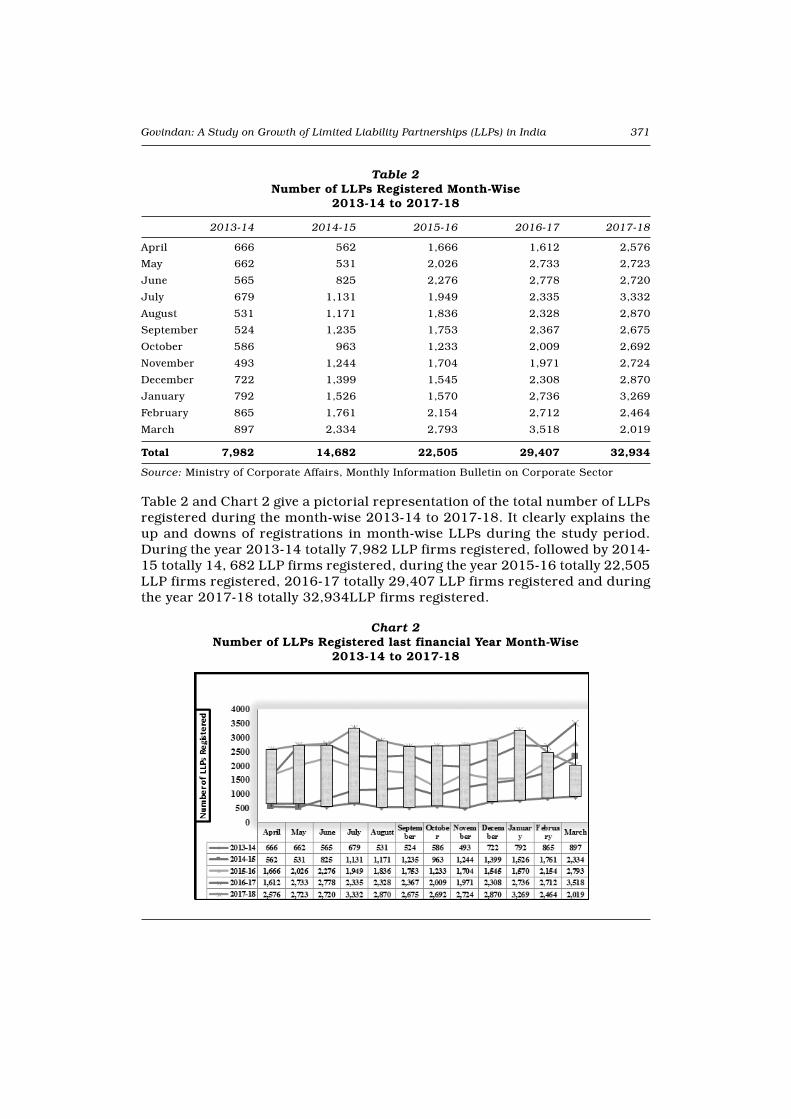

Table 2Number of LLPs Registered Month-Wise

2013-14 to 2017-18

2013-14 2014-15 2015-16 2016-17 2017-18

April 666 562 1,666 1,612 2,576

May 662 531 2,026 2,733 2,723

June 565 825 2,276 2,778 2,720

July 679 1,131 1,949 2,335 3,332

August 531 1,171 1,836 2,328 2,870

September 524 1,235 1,753 2,367 2,675

October 586 963 1,233 2,009 2,692

November 493 1,244 1,704 1,971 2,724

December 722 1,399 1,545 2,308 2,870

January 792 1,526 1,570 2,736 3,269

February 865 1,761 2,154 2,712 2,464

March 897 2,334 2,793 3,518 2,019

Total 7,982 14,682 22,505 29,407 32,934

Source: Ministry of Corporate Affairs, Monthly Information Bulletin on Corporate Sector

Table 2 and Chart 2 give a pictorial representation of the total number of LLPsregistered during the month-wise 2013-14 to 2017-18. It clearly explains theup and downs of registrations in month-wise LLPs during the study period.During the year 2013-14 totally 7,982 LLP firms registered, followed by 2014-15 totally 14, 682 LLP firms registered, during the year 2015-16 totally 22,505LLP firms registered, 2016-17 totally 29,407 LLP firms registered and duringthe year 2017-18 totally 32,934LLP firms registered.

Chart 2Number of LLPs Registered last financial Year Month-Wise

2013-14 to 2017-18

372 Prajnan

Table 3Sector-Wise Active Number of LLPs

(As on 30th June, 2018)

Sl. Sectors Number Per cent Obligation of Per centNo. Contribution (in Rs Lakh)

I Agriculture 2,147 2 87,727.27 1

II Industry 24,887 22 1,646,657.60 28

III Services 87,659 76 4,137,591.79 71

IV Others 1 0 10 0

Total 114,694 100 5,871,986.66 100

Source: Monthly Information Bulletin on Corporate Sector, June 2018

Table 3 and Chart 3 show that sector wise classification of active LLPs as on30th June 2018. It indicates service sector account for 87,659 LLPs, followedby Industry and Agriculture sectors accounting for 24,887 and 2,147respectively. Chart 3 also show that 76 per cent active number of LLPs in theservice sectors followed by industry sector 22 per cent and agriculture andallied sectors 2 per cent. Sector wise obligation of contribution (in Rs lakh) ofactive LLPs as on 30thJune 2018 reveals that service sector have an accountfor obligation of contribution (in Rs. lakh) 4,137,591.79, followed by industryand agriculture sectors accounting for obligation of contribution (in Rslakh)1,646,657.60and obligation of contribution (in Rs lakh) 87,727.27. Itexplains that obligation of contribution (in Rs. lakh) 71 per cent in the servicesectors, followed by industry sector 28 per cent and agriculture and alliedsectors 1 per cent.

Chart 3Sector-Wise Active LLPs

Govindan: A Study on Growth of Limited Liability Partnerships (LLPs) in India 373

Table 4Economic Activity-wise Active LLPs

(As on 30th June, 2018)

Sl. Economic Activity Number Per cent Obligation of Per centNo. Contribution (in Rs Lakh)

1 Business Services 47,285 41 1,391,056.01 24

2 Trading 14,320 12 972,344.60 17

3 Manufacturing 13,496 11 897,223.08 15

4 Real Estate 11,571 10 837,341.11 14

5 Construction 10,052 9 587,977.38 10

6 Community 10,067 9 523,433.62 9

7 Agriculture 2,147 2 312,400.41 5

8 Transport 2,456 2 195,507.83 3

9 Finance 1,733 2 87,727.27 1

10 Mining & Quarrying 689 1 30,493.06 1

11 Electricity & Gas 650 1 33,085.87 1

12 Insurance 227 0 3,386.43 0

13 Others 1 0 10 0

Total 1,14,694 100 5,871,986.66 100

Source: Monthly Information Bulletin on Corporate Sector, June 2018

The above Table 4 shows that economic-activity wise classification of activeLLPs as on 30th June 2018 further exhibits that large number of LLPs are inbusiness services sector 47,285 followed by trading sector14,320,manufacturing sector 13,496, real estate and renting sector 11,571,construction sector 10,052,community, personal and social servicessector10,067, transport, storage and communications sector 2,456 agricultureand allied activities sector 2,147,finance sector 1,733, mining and quarryingsector 689, electricity, gas and water companies sector 650, insurance sector227 and others sectors.

Table 4 also gives the economic-activity wise classification obligation ofcontribution (in Rs lakh) of active LLPs as on 30th June 2018. It also explainsthat large amount of LLPs obligation of contribution (in Rs lakh) are in businessservices sector 1,391,056.01 followed by trading sector 972,344.60,manufacturing sector 897,223.08, real estate and renting sector 837,341.11,construction sector 587,977.38, community, personal and social services sector523,433.62, agriculture and allied activities sector 312,400.41,transport,storage and communications sector 195,507.83, finance sector 87,727.27,mining and quarrying sector 30,493.06, electricity, gas and water companiessector 33,085.87, insurance sector 3,386.43 and others sectors 10.

374 Prajnan

Table 5Obligation of Contribution wise Active LLPs

(As on 30th June, 2018)

Sl. Obligation of Contribution Number Active Obligation of ContributionNo. Range LLPs (in Rs Lakh)

Number per cent (in Rs Lakh) per cent

1 Up to 1 lakh 26,804 23.37 8,980.19 0.15

2 Above 1 lakh to 5 lakh 67,351 58.72 99,519.05 1.69

3 Above 5 lakh to 10 lakh 7,034 6.13 64,815.29 1.1

4 Above 10 lakh to 25 lakh 4,276 3.73 78,879.85 1.34

5 Above 25 lakh to 50 lakh 3,094 2.7 126,165.69 2.15

6 Above 50 lakh to 1 crore 2,486 2.17 210,766.87 3.59

7 Above 1 crore to 2 crore 1,256 1.1 194,447.01 3.31

8 Above 2 crore to 5 crore 1,226 1.07 426,601.23 7.27

9 Above 5 crore to 10 crore 512 0.45 391,735.26 6.67

10 Above 10 crore to 25 crore 390 0.34 625,277.55 10.65

11 Above 25 crore to 100 crore 213 0.19 1,071,227.11 18.24

12 Above 100 crore 52 0.05 2,573,571.56 43.83

Total 114,694 100 5,871,986.66 100

Source: Monthly Information Bulletin on Corporate Sector, June 2018

Table 5 elucidates that Obligation of Contribution wise Active LLPs as on 30thJune, 2018.These also detailed total numbers of 114,694 LLPs were active inthe country. About 58.72 per cent active LLPs (67,351 in number) haveobligation of contribution above 1 lakh to 5 lakh, followed by (26,804) up to 1lakh. It indicates that 82.09 per cent active LLPs (94,155 in numbers) haveobligation of contribution less than or equal to Rs. 5 lakh each. In case ofobligation of contribution above 5 lakh to 50 lakhs shows that 12.56 per centactive LLPs (14,404 in numbers); and only about 3.20 per cent (3,649 innumber) of LLPs have obligation of contribution above Rs.1 crore each.

Inferential Statistical Analysis

Correlation Analysis

Correlation is a bivariate analysis that measures the strength of associationbetween two variables and the direction of the relationship. In terms of thestrength of relationship, the value of the correlation coefficient varies between+1 and -1. A value of ± 1 indicates a perfect degree of association between thetwo variables. In this study used paired sample t-test for LLPs registrationsbefore and after implementation of Companies Act 2013 and LLPs registrationsbefore and after implementation of GST Act 2017.

Govindan: A Study on Growth of Limited Liability Partnerships (LLPs) in India 375

Hypothesis testing-1-Pearson Correlations Test-1

Table 6LLPs Registrations and

Total Obligation of Contribution(As on 30th June 2018)

Years Total Number of Total Obligation of ContributionLLPs Registrations (Rs. in. Crore)

2009-10 1,055 596.55

2010-11 3,261 2758.37

2011-12 4,319 3049.73

2012-13 5,167 1854.5

2013-14 7,982 2029.56

2014-15 14,682 2650.05

2015-16 22,505 8872.33

2016-17 29,407 8,420.63

2017-18 32,934 5,545.15

2018-19 *(Upto 30.06.2018) 5,421 2,670.34

Total 1,26,733 38,447.21

Source: Monthly Information Bulletin on Corporate Sector, March 2014 to June 2018

Hypothesis testing-1H0: ρ = 0 ("the population correlation coefficient is 0; there is no association")

H1: ρ > 0 ("the population correlation coefficient is greater than 0; a positivecorrelation could exist")

OR

H1: ρ < 0 ("the population correlation coefficient is less than 0; a negativecorrelation could exist")

Where ρ is the population correlation coefficient

376 Prajnan

Table 6.1Pearson Correlations Test

Total Number of Total Obligation ofLLPs Registrations Contribution

Total Number of Pearson Correlation 1 0.830**LLPs Registrations Sig. (2-tailed) 0.003

N 10 10

Total Obligation Pearson Correlation 0.830** 1of Contribution Sig. (2-tailed) 0.003

N 10 10

**. Correlation is significant at the 0.01 level (2-tailed).

Results of CorrelationsThe paired samples correlation Table shows that LLPs registrations and totalobligation of contribution (Rs. in. crore) are significantly highly positivelycorrelated (r = 0.830).

Hypothesis testing-2-Pearson Correlations Test-2

Table 7LLPs Registrations Economic Activity-wise Active and

Obligation of Contribution(As on 30th June, 2018)

Sl. Economic Activity Number of Active Obligation of ContributionNo. LLPs (Rs. in. Lakh)

1 Business Services 47,285 13,91,056.01

2 Trading 14,320 9,72,344.60

3 Manufacturing 13,496 8,97,223.08

4 Real Estate 11,571 8,37,341.11

5 Construction 10,052 5,87,977.38

6 Community 10,067 5,23,433.62

7 Agriculture 2,147 3,12,400.41

8 Transport 2,456 1,95,507.83

9 Finance 1,733 8,7,727.27

10 Mining & Quarrying 689 30,493.06

11 Electricity & Gas 650 33,085.87

12 Insurance 227 3,386.43

13 Others 1 10

Total 1,14,694 58,71,986.66

Source: Monthly Information Bulletin on Corporate Sector, June 2018.

Govindan: A Study on Growth of Limited Liability Partnerships (LLPs) in India 377

Hypothesis testing-2H0: ρ = 0 ("the population correlation coefficient is 0; there is no association")

H1: ρ > 0 ("the population correlation coefficient is greater than 0; a positivecorrelation could exist")

OR

H1: ρ < 0 ("the population correlation coefficient is less than 0; a negativecorrelation could exist")

Where ρ is the population correlation coefficient

Table 7.1Pearson Correlations Test

Total Number of Obligation ofActive LLPs Contribution (Rs. in Lakh

Number ofActive LLPs Pearson Correlation 1 0.888**

Sig. (2-tailed) 0.000N 13 13

Obligation of Pearson Correlation 0.888** 1Contribution Sig. (2-tailed) 0.000(Rs. in. Lakh) N 13 13

**. Correlation is significant at the 0.01 level (2-tailed).

Results of CorrelationsThe Paired Samples Correlation Table LLPs registrations economic activity-wise active and obligation of contribution (Rs. in. lakh) are significantly highlypositively correlated (r = 0.888).

Paired Sample T-TestThe paired sample t-test, sometimes called the dependent sample t-test, is astatistical procedure used to determine whether the mean difference betweentwo sets of observations is zero. In a paired sample t-test, each subject orentity is measured twice, resulting in pairs of observations. In this study usedcorrelation is a bivariate analysis that measures the strength of associationbetween LLPs registrations and total obligation of contribution, LLPsregistrations economic activity-wise active and obligation of contribution ason 30th June, 2018.

378 Prajnan

Hypothesis testing-3

Table 8LLPs Registrations Before and After

Implementation of Companies ACT 2013

LLPs Registrations Before Implementation LLPs Registrations After implementationof Companies ACT 2013 of Companies ACT 2013

Years LLPs Registrations Years LLPs Registrations

2010-11 3,261 2014-15 14,682

2011-12 4,319 2015-16 22,505

2012-13 5,167 2016-17 29,407

2013-14 7,982 2017-18 32,934

Source: Monthly Information Bulletin on Corporate Sector, March 2014 to June 2018

Hypothesis testing-3H0: μ1 = μ2: There is no difference in the LLPs Registrations afterimplementation of Companies Act 2013

H1: μ1 ≠ μ2: There is a difference in the LLPs Registrations after implementationof Companies Act 2013

Table 8.1Paired Samples Statistics LLPs Registrations Before and

After Implementation of Companies Act 2013

Mean N Std. Deviation Std. Error Mean

LLPs Registrations Before 5182.25 4 2022.81 1011.40310implementation ofCompanies Act 2013

Before & LLPs Registrations After 24882.00 4 8062.27 4031.13361After implementation of

Companies Act 2013

Table 8.2Paired Samples Correlations LLPs Registrations Before and

After Implementation of Companies Act 2013

N Correlation Sig.

Before & LLPs Registrations Before implementation

4 0.902 0.098After of Companies ACT 2013

LLPs Registrations After implementation ofCompanies ACT 2013

Govindan: A Study on Growth of Limited Liability Partnerships (LLPs) in India 379

Results of Paired Samples CorrelationsThe Paired Samples Correlation Table LLPs registrations before and afterimplementation of Companies Act 2013 are significantly highly positivelycorrelated (r = 0.902).

Table 8.3Paired Samples Test LLPs Registrations Before and

After Implementation of Companies Act 2013

Paired Differences

Mean Std. Std. 95per cent Confidence t df Sig.Deviation Error Interval of the Difference (2-tailed)

Mean Lower Upper

LLPs Before

-19699.75 6298.92 3149.46 -29722.74-9676.76 -6.255 3 0.008

implementationof Companies

BeforeAct 2013

and LLPs AfterAfter implementation

of CompaniesACT 2013

Results of Paired t testThe Table value of Paired t test with 5 per cent level of significance equals(t3 = -6.255, p < 0.008). This is less then (p< 0.05). Therefore, null hypothesisis rejected. There was a difference in the LLPs Registrations afterimplementation of Companies Act 2013. It concluded that there is growth inLLPs Registrations after implementation of Companies Act 2013.

380 Prajnan

Hypothesis Testing-4

Table 9LLPs Registrations Economic Activity-Wise Before and

After Implementation of Companies Act 2013

Sl. Economic LLPs Registrations Economic LLPs Registrations EconomicNo. Activity-Wise Activity-Wise Before Implementation Activity-Wise After Implementation

of Companies Act 2013 of Companies Act 201301.04.2009 To 31.03.2014 01.04.2104 To30.06.2018

1 Business Services 3,071 44,214

2 Trading 852 13,468

3 Manufacturing 812 12,684

4 Real Estate 1,028 10,543

5 Construction 988 9,064

6 Community 744 9,323

7 Agriculture 132 2,015

8 Transport 149 2,307

9 Finance 109 1,624

10 Mining & Quarrying 41 648

11 Electricity & Gas 55 595

12 Insurance 1 226

13 Others 0 1

Source: Monthly Information Bulletin on Corporate Sector, March 2014 to June 2018

Hypothesis Testing-4H0: μ1 = μ2: There is no difference in the LLPs registrations economicactivity-wise after Implementation of Companies Act 2013

H1: μ1 ≠ μ2: There is a difference in the LLPs registrations economicactivity-wise after Implementation of Companies Act 2013

Table 9.1Paired Samples Statistics

Mean N Std. Std. ErrorDeviation Mean

Before & LLPs registrations economic activity 614.0000 13 844.49285 234.22017After -wise before implementation of

Companies Act 2013

LLPs registrations economic activity 8208.6154 13 11952.21402 3314.94773-wise after implementation ofCompanies Act 2013

Govindan: A Study on Growth of Limited Liability Partnerships (LLPs) in India 381

Table 9.2Paired Samples Correlations

N Correlation Sig.

Before & LLPs registrations economic activity-wise 13 0.988 0.000After before implementation of Companies Act 2013

LLPs registrations economic activity-wiseafter implementation of Companies Act 2013

Results of Paired Samples Correlations: The Paired Samples CorrelationTable LLPs Registrations economic activity-wise before and afterimplementation of Companies Act 2013 are significantly highly positivelycorrelated (r = 0.988).

Table 9.3Paired Samples Test

Paired Differences

Mean Std. Std. 95 per cent Confidence t df Sig.Deviation Error Interval of the Difference (2-tailed)

Mean Lower Upper

Before LLPs registrations -7594.62 11119.06 3083.87 -14313.80 -875.43 -2.463 12 0.030and economic activity-After wise before

implementation ofCompanies Act 2013

LLPs registrationseconomic activity-wise afterimplementation ofCompanies Act 2013

Results of Paired t testThe Table value of Paired t test with 5 per cent level of significance equals(t12 = -2.463, p < 0.030). This is less then (p < 0.05). Therefore, null hypothesisis rejected. There was a difference in the LLPs registrations economicactivity-wise after implementation of Companies Act 2013. It concluded thatthere is growth in LLPs registrations economic activity-wise afterimplementation of Companies Act 2013.

Hypothesis testing-5H0: μ1 = μ2: There is no difference in the LLPs registrations afterimplementation of GST Act 2017

H1: μ1 ≠ μ2: There is a difference in the LLPs registrations after implementationof GST Act 2017

382 Prajnan

Table 10LLPs Registrations Before and After Implementation of GST Act 2017

Months LLPs Registrations Before LLPs Registrations AfterImplementation of GST Act 2017 Implementation of GST Act 2017

01-07.2016 to 30.06.2017 01-07.2017 to 30.06.2018

July 2335 3332

August 2328 2870

September 2367 2675

October 2009 2692

November 1971 2724

December 2308 2870

January 2736 3269

February 2712 2464

March 3518 2019

April 2576 1805

May 2723 2387

June 2720 1229

Source: Monthly Information Bulletin on Corporate Sector, March 2014 to June 2018

Hypothesis testing-5

Table 10.1Paired Samples Statistics

Mean N Std. Deviation Std. Error Mean

Before LLPs Registrations before GST 2525.25 12 411.81442 118.88058and After LLPs Registrations after GST 2528.00 12 603.74091 174.28499

Table 10.2Paired Samples Correlations

N Correlation Sig.

Before LLPs Registrations before GST &and After LLPs Registrations after GST 12 -0.435 0.157

Results of Paired Samples CorrelationsThe Paired Samples Correlation Table LLPs Registrations before and afterimplementation of Companies Act 2013 are significantly negatively correlated(r = -0.435).

Govindan: A Study on Growth of Limited Liability Partnerships (LLPs) in India 383

Table 10.3Paired Samples Test

Paired Differences

Mean Std. Std. 95per cent Confidence t df Sig.Deviation Error Interval of the Difference (2-tailed)

Mean Lower Upper

Before LLPs Registrationsand before GST -2.75 866.28 250.07 -553.16 547.66 -0.011 11 0.991After LLPs Registrations

after GST

Results of Paired t testThe Table value of Paired t test with 5 per cent level of significance equals(t11 = -0.011, p < 0.0.991). This is more then (p < 0.05). Therefore, nullhypothesis is accepted. There is no difference in the LLPs Registrations beforeand after implementation of GST Act 2017. It concluded that there is nodifference in the LLPs Registrations before and after implementation of GSTAct 2017.

Hypothesis Testing-6

Table 11LLPs Registrations Economic Activity Wise Before and

After Implementation of GSTAct 2017

Sl. Economic Activity-Wise LLPs Registrations Before GST LLPs Registrations After GSTNo. 01.04.2009 To 31.03.2014 01.04.2104 To 30.06.2018

1 Business Services 13022 8634

2 Trading 3621 2709

3 Manufacturing 3527 2752

4 Real Estate 2262 1881

5 Construction 2154 1321

6 Community 2711 1756

7 Agriculture 490 443

8 Transport 663 376

9 Finance 399 296

10 Mining & Quarrying 160 121

11 Electricity & Gas 178 65

12 Insurance 105 65

Source: Monthly Information Bulletin on Corporate Sector, March 2014 to June 2018

384 Prajnan

Hypothesis Testing-6H0: μ1 = μ2: There is no difference in the LLPs registrations economicactivity-wise after Implementation of GST Act 2017

H1: μ1 ≠ μ2: There is a difference in the LLPs registrations economicactivity-wise after Implementation of GST Act 2017

Table 11.1Paired Samples Statistics

Mean N Std. Std. ErrorDeviation Mean

BeforeLLPs Registrations Economic Activity-Wise 2441.0000 12 3588.30350 1035.85400

andBefore implementation of GST Act 2017

After LLPs Registrations Economic Activity -Wise 1701.5833 12 2403.19070 693.74140After implementation of GST Act 2017

Table 11.2Paired Samples Correlations

N Correlation Sig.

BeforeLLPs Registrations Economic Activity-Wise

12 0.997 0.000andBefore implementation of GST Act 2017

After LLPs Registrations Economic Activity -WiseAfter implementation of GST Act 2017

Results of Paired Samples CorrelationsThe Paired Samples Correlation Table LLPs registrations economicactivity-wise before and after implementation of GST Act 2017 are significantlyhighly positively correlated (r = 0.997).

Table 11.3Paired Samples Test

Paired Differences

Mean Std. Std. 95per cent Confidence t df Sig.Deviation Error Interval of the Difference (2-tailed)

Mean Lower Upper

LLPs Registrations 739.42 1205.60 348.03 -26.59 1505.42 2.125 11 0.057Economic Activity-Wise Beforeimplementation of

Before GST Act 2017

and LLPs RegistrationsAfter Economic Activity-

Wise Afterimplementation ofGST Act 2017

Govindan: A Study on Growth of Limited Liability Partnerships (LLPs) in India 385T

ab

le 1

2P

aire

d S

amp

les

Tes

t H

ypoth

esis

Res

ult

s

Pa

ired

Dif

fere

nce

s

Mea

nS

td.

Std

. E

rror

td

fS

ig.

(2-t

ail

ed)

Hy

pot

hes

isD

evia

tion

Mea

n

Low

erU

pp

er

Res

ult

ste

stin

gH

0: μ1

= μ

2

Pai

r 1

LL

Ps

Reg

istr

atio

ns

-19

69

9.7

56

29

8.9

23

14

9.4

6-2

97

22

.74

-96

76

.76

-6.2

55

30

.00

8A

ccep

ted

bef

ore

an

d a

fter

imp

lem

enta

tion

of

Com

pan

ies

Act

20

13

Pai

r 2

LL

Ps

regi

stra

tion

s-7

59

4.6

21

11

19

.06

30

83

.87

-14

31

3.8

0-8

75

.43

-2.4

63

12

0.0

30

Acc

epte

dec

on

om

ic a

ctiv

ity-

wis

e b

efor

e an

d a

fter

imp

lem

enta

tion

of

Com

pan

ies

Act

20

13

Pai

r 3

LL

Ps

Reg

istr

atio

ns

-2.7

58

66

.28

25

0.0

7-5

53

.16

54

7.6

6-0

.01

11

10

.99

1R

ejec

ted

bef

ore

an

d a

fter

imp

lem

enta

tion

of

GS

T A

ct 2

01

7

Pai

r 4

LL

Ps

Reg

istr

atio

ns

Eco

nom

ic A

ctiv

ity-

Wis

e b

efor

e an

daf

ter

imp

lem

enta

tion

of

GS

T A

ct 2

01

77

39

.42

12

05

.60

34

8.0

3-2

6.5

91

50

5.4

22

.12

51

10

.05

7R

ejec

ted

95

per

cen

t C

onfi

den

ceIn

terv

al o

f th

e D

iffe

ren

ce

386 Prajnan

Results of Paired t testThe Table value of Paired t test with 5 per cent level of significance equals(t11 = 2.125, p < 0.057). This is more then (p < 0.05). Therefore, null hypothesisis accepted. There is no difference in the LLPs registrations economicactivity-wise after implementation of GST Act 2017. It concluded that there isno growth LLPs registrations economic activity -wise after implementation ofGST Act 2017.

Here, we have listed out major findings of the study: The Total number of LLPs1, 26,733 had been registered with Total Obligation of Contribution (Rs. incrore) 38,447.21 as on 30.06.2018 in India. Majority of 76 per cent activenumber of LLPs had been registered in the service sectors followed by industrysector 22 per cent and agriculture and allied sectors 2 per cent. Majority of 71per cent Obligation of Contribution in the service sectors followed by industrysector 28 per cent and agriculture and allied sectors 1 per cent. Large numberof LLPs are in business services sector 47,285 (41 per cent) followed by tradingsector14, 320 (12 per cent), manufacturing sector 13,496 (11 per cent) andreal estate and renting sector 11,571(10 per cent). It is amounted to 74 percent LLPs had been registered. large amount of LLPs Obligation of Contribution(in Rs lakh) are in business services sector (24 per cent) followed by tradingsector (17 per cent), manufacturing sector (15 per cent) and real estate andrenting sector (14 per cent). It is amounted to 70 per cent LLPs Obligation ofContribution.

Interestingly about 58.72 per cent active LLPs had been registered (67,351 innumber) have obligation of contribution above 1 lakh to 5 lakh, followed by(26,804) (23.37 per cent) up to 1 lakh. It indicates that 82.09 per cent activeLLPs obligation of contribution (94,155 in numbers) have obligation ofcontribution less than or equal to Rs. 5 lakh each.

Our paired samples correlation table reveals that LLPs registrations and totalobligation of contribution (Rs. in crore) are significantly highly positivelycorrelated (r = 0.830).

The paired t test result shows that there is growth in LLPs registrations afterimplementation of Companies Act 2013 (t = -6.25, p < 0.01).

Further, there is growth in LLPs registrations economic activity-wise afterimplementation of Companies Act 2013 as well. This is also confirmed byt-test (t = -2.463 and p < 0.03)

We have also found that there is no difference in the LLPs registrations beforeand after implementation of GST Act 2017 (t is insignificant).

Also there is no growth LLPs registrations economic activity-wise afterimplementation of GST Act 2017.

Govindan: A Study on Growth of Limited Liability Partnerships (LLPs) in India 387

Section IVConclusion

This study observes that during the study period growth of Limited LiabilityPartnership (LLPs) is phenomenal one. Since its implementation to as on30th June 2018, a total number of LLPs registered 1,26,733 out of them 1,14,694 LLPs were active in India. It indicates that positively growing one andalso it indicates that LLPs Act welcomed by investors. It concluded that thereis growth in LLPs registrations and economic activity -wise after implementationof Companies Act 2013. It concluded that there is no difference in the LLPsRegistrations before and after implementation of GST Act 2017. It is suggestedthat various tax reforms need in the GST to increase registration of LLPs.Comparison of LLPs with Partnership Firm, Public Company and PrivateCompany shows that LLPs is best innovative vehicle for small and mediumscale Entrepreneurs.

This study also suggests that in order to attract investors to new as well asexisting sectors both state, central governments and other agencies shouldtake new policy implementations and also revising existing policies. Afterimplementation historic tax reform in India, like Companies Act 2013, thegoods and services tax was rolled out on 1st July, 2017, subsuming almost allmajor indirect taxes facilitates enable the new domestic and foreign entrantsto establish business operations in India. After the economic liberalisation,with increase in domestic demand, a high return on investment, India hasemerged as a credible investment destination for domestic as well as foreigninvestors. In the challenging international business environments, India hasunderstood the role of strengthening infrastructure for starting new businessventure which will ultimately create more entrepreneurial opportunities inIndia.

References

1. Phillip, Lipton (2018), “The Introduction of Limited Liability into the English andAustralian Colonial Companies Acts: Inevitable Progression or Chaotic History?",Melbourne University Law Review, Vol. 41, No. 3.

2. Meena, Ravi and Renu Nainawa (2013), "LLP in India: As Advantageous BusinessModel", Global Journal of Management and Business Studies, Vol. 3, No. 10,pp 1051-1056.

3. Ireland, Paddy (2010), "Limited Liability, Shareholder Rights and the Problem ofCorporate Irresponsibility", Cambridge Journal of Economics, Vo. 34, No. 5,pp 837-856, doi:10.1093/cje/ben040

4. Blankenburg, Stephanie, Dan Plesch and Frank Wilkinson (2010), "Limited Liabilityand the Modern Corporation in Theory and in Practice", Cambridge Journal ofEconomics, Vol. 34, No. 5, pp. 821-836, doi:10.1093/cje/beq028.

388 Prajnan

5. Hillman, Robert W (1997), "Limited Liability in Historical Perspective", Washingtonand Lee Law Review, Vol 54, Issue 2, Article 10, pp 13-627.

6. Maizes, Rachel (2012) "Limited Liability Companies: A Critique", St. John's Law Review,Vol. 70, No. 3 pp. 575-608.

7. Tricker, B (2011), "Re-Inventing the Limited Liability Company", Corporate Governance:An International Review, Vol. 19, No. 4, pp 384-393. https://doi.org/10.1111/j.1467-8683.2011.00851.

8. Kour, Milandeep, Kajal Chaudhary, Surjan Singh and Baljinder Kaur (2016), "A Studyon Impact of GST after Its Implementation", International Journal of Innovative Studiesin Sociology and Humanities, Vol. 1, No. 2, pp 17-24.

9. Deo, Anand (2017) "Goods and Services Tax (GST) – Impact Analysis and Road Ahead",IBMRD's Journal of Management and Research, Vol. 6, No. 2, pp 17-28.

10. Georgieva, Kristalina (2018), "A World Bank Group Flagship Report", 15th Edition,Doing Business 2018, Reforming to Create Jobs, www.worldbank.org, ISBN (paper):978-1-4648-1146-3, ISBN (electronic): 978-1-4648-1147-0,DOI: 10.1596/978-1-4648-1146-3,ISSN: 1729-2638, pp 1-229.

11. Fletcher, Denise, Jane Frecknall-Hughes and Dr Stephen Williams (2013),"Understanding Limited Liability Partnerships in the Small and Medium-sized BusinessSector", ICAEW, www.icaew.com/academic, ISBN 978-0-85760-661-7, London EC2R6EA.Pp1-74.

12. Sharma, Radheyshyam and Bhamini Garg (2014) "Limited Liability Partnership inIndia: Study of Different Aspects for Optimum Growth", IRACST - International Journalof Commerce, Business and Management, Vol. 3, No. 5, pp 720-725.

13. Singh, Pradeep Kumar, (2007), "Limited Liability Partnership (LLPS) & Taxation Issues",http://www.indianmba.com/Faculty_Column/FC626/fc626.html.

14. Bharat, Arora (2013), "Law Relating To Limited Liability Partnership and Its Impacton Business Environment", Doctor of Philosophy Thesis, Panjab University, Chandigarh,pp 1-337.

15. Varottil, Umakanth (2014), "Paper on Limited Liability Partnership Law in India", https://indiacorplaw.in/2014/12/paper-on-limited-liability-partnership.html

16. Gandhi, Utsav and Ravi Thakur, "A Study on Limited Liability Partnership as anEmerging Business Form for Entrepreneurs", pp 301-317.

17. Khan, Mohd. Azam, Nagma Shadab (2012), "Goods and Services Tax (GST) in India:Prospect for States”, Budgetary Research Review (BRR), Vol. 4, No. 1, pp 38-64.