a strategic review of the petroleum refinery industry sector · petroleum refinery industry sector....

TRANSCRIPT

R&D Publication 21i

A Strategic Review of the Petroleum Refinery Industry Sector

R&D Publication 21

Research Contractor:

Foster Wheeler Energy Ltd

R&D Publication 21ii

Publishing OrganisationEnvironment AgencyRio HouseWaterside DriveAztec WestAlmondsburyBRISTOLBS32 4UD.

Tel: 01454 624400 Fax: 01454 624409

ISBN: 1 85705 213 7

© Environment Agency 1999

All rights reserved. No part of this document may be reproduced, stored in a retrieval system, or transmitted, in anyform or by any means, electronic, mechanical, photocopying, recording or otherwise without the prior permission ofthe Environment Agency.

The views expressed in this document are not necessarily those of the Environment agency. Its officers, servants oragents accept not liability whatsoever for any loss or damage arising from the interpretation or use of theinformation, or reliance upon the views contained herein.

Dissemination StatusInternal: Released to RegionsExternal: Released to Public Domain

Statement of UseThis report reviews the environmental performance of the UK petroleum refinery industry sector in the context ofworld-wide best practice. Five practical options for reducing emissions are examined. The report will be used bothexternally and internally, by policy and operational staff, in the development of policies for the regulation of thepetroleum refinery industry sector.

Research ContractorThis document was produced under Environment Agency R&D Project P4-035 by:

Foster Wheeler LtdFoster Wheeler HouseStation RoadReadingBerkshireRG1 1LX

Environment Agency Project ManagerThe Environment Agency’s Project Manager for R&D Project P4-035 was:Mr Colin Foan, Environment Agency, National Centre for Risk Analysis and Options Appraisal.

Fur ther copies of this r epor t are available from:Environment Agency R&D Dissemination Centre, c/oWRc, Frankland Road, Swindon, Wilts SN5 8YF

tel: 01793-865138 fax: 01793-514562 e-mail: [email protected]

R&D Publication 21iii

CONTENTSPage

Executive Summary 1

1. Introduction 5

2. Key Factors Affecting UK Refiner ies up to 2005 72.1 Crude Supply and Quality 72.2 Product Quality Changes 132.3 The Future for Fuel Oil 152.4 UK Refinery Capacity and Economics 172.5 Discussions with Operators 202.6 Legislation for Releases to Air 222.7 Legislation for Releases to Water and Land 24

3. UK Refiner ies 263.1 Types of UK Refinery 263.2 Sources of Polluting Emissions on Refineries 283.3 Discussions with Local Inspectors 313.4 Inventory of UK Refinery Sector Releases 33

4. Wor ld-Wide Refinery Best Practice 404.1 Introduction 404.2 USA 404.3 Scandinavia 434.4 Japan 434.5 The Netherlands 444.6 Summary and Comparison with UK Practice 44

5. Pollution Reduction Issues, Techniques and Costs 465.1 Introduction 465.2 Sulphur and Sulphur Dioxide Abatement 465.3 Sulphur Recovery Units (SRU) and Sulphur Balance 495.4 Abatement of Oxides of Nitrogen (NOx) 505.5 Particulate Abatement 535.6 CCGT/CHP Facilities 535.7 VOC Abatement 535.8 Effluent Water Treatment 535.9 Summary of Costs of Abatement Plant 55

6. Pollution Reduction Strategies 586.1 General Considerations 586.2 Options for Reduction of Releases to Air 596.3 Results of Evaluation of Options 626.4 Implications for the Refinery Sector 656.5 Comparison with Legislation 666.6 Timetable for Implementation of the Options/Strategies 66

7. Longer -Ter m Strategies and Influences 687.1 Introduction 687.2 Sulphur Removal 687.3 Oxides of Nitrogen 697.4 Particulates 697.5 Volatile Organic Compounds (VOCs) 707.6 Carbon Dioxide Releases 707.7 The Emergence of Fuel-Cell Technology and Effect on Refineries 717.8 Summary 72

8. Conclusions 74

R&D Publication 21iv

Appendices

A1 Description of UK Refineries 77A2 Brief Layman’s Guide to Oil Refineries 80A3 Glossary of Terms and List of References 83

This Review has been prepared by Foster Wheeler Energy Limited under the terms of its contract with theEnvironment Agency. Whilst the report and recommendations have been prepared in accordance with normalprofessional standards, information contained herein is largely dependent upon data in the public domain providedfrom the Environment Agency Public Register and other third parties. Foster Wheeler has not made any independentverification of such data. Accordingly, Foster Wheeler makes no representation or warranty, express or implied,with respect to the completeness or accuracy of any information contained in this Report. This Review is intendedfor the sole use of the Environment Agency and Foster Wheeler shall have no responsibility whatsoever to any thirdparty for the whole or any part of this Report or the information contained herein.

R&D Publication 211

FOREWORD

The Environment Agency has the strategic aim andduty to protect and enhance the environment. Tosupport this work it also has a duty to undertakeresearch and make the results available to others.

Processes with a significant potential to causepollution are regulated by the Agency underprovisions in The Environmental Protection Act1990. Included within these processes are many inthe petroleum refinery industry sector. Operators ofthese techically complex processes are required touse the best available technique not entailingexcessive cost to prevent or minimise releases ofpolluting substances in order to achieve the bestpracticable environmental option.

The Agency, therefore, commissioned thisindependent report from Foster Wheeler EnergyLimited to help it form an objective view of thecurrent environmental performance of the UKrefinery sector. The study has sought to identifysignificant issues that could affect the industry’senvironmental performance. Emissions, processoptions and abatement practices from a number ofcountries were investigated and worldwide bestpractice considered in the context of applicability tothe UK situation.

Recent changes in the European transport fuelspecifications and the UN sulphur protocol areevidently going to present the sector with somesignificant and conflicting economic and technicalchallenges. The results of this review will assist us tomake appropriate regulatory decisions to ensure thatthe UK refinery sector uses the best availabletechniques not entailing excessive cost to protect theenvironment. It will also serve as an importantcontribution to the efficient regulation of thepetroleum refinery industry sector.

Dr R J PentreathChief Scientist and Director of EnvironmentalStrategy

EXECUTIVE SUMMARY

European, including the UK, refiners have beenstruggling with over capacity and poor or negativemargins for many years. This situation has beenespecially difficult since 1994. Overall, utilisationlevels have risen recently but highly-efficient marketshave resulted in any surplus product reducingprevailing prices and preventing improvedprofitability.

One result of low profitability is that refiners have,where possible, minimised capital expenditure andreduced operating costs. However, there has been,and will be, some expenditure to meet newenvironmental specifications on product quality andrequirements for control of releases to theenvironment. The availability of plenty of light, low-sulphur North Sea crude has helped to minimise thisexpenditure. UK refineries have as a result nowbecome dependent to a greater or lesser extent onlight, low-sulphur feedstock to meet current productspecifications and emission-release limits.

The continuing availability of this quality of crude istherefore a key factor in determining the futureprofile of UK refineries. An assessment of crude oilavailability from the North Sea has been carried outand it is concluded that supplies will continue to beadequate at least until 2005, and probably beyond. Itis to be expected that UK refiners will continue todepend mainly on North Sea crude during this period.

Given this premise, one of the most important factorsfor refiners during the period that this Review coversis the further tightening of product quality standards,particularly those for transport fuels. The EuropeanCommission and Parliament have recently agreednew standards, which are to become effective from2000 and 2005. The 2005 standards include a sharpreduction in levels of benzene, aromatics and sulphurin gasoline and sulphur in diesel. It has beenestimated that the increased refinery processing,mainly in the form of extra hydrotreatment, needed tomeet the fuel specifications for 2005 would mean theUK refinery sector increasing its CO2 emissions bybetween 2% and 4%. The supply of hydrogenrequired for this extra hydrotreatment will be an issuerefiners will need to address.

The investment needed to meet these new standardswill mark a watershed for European refiners. Mostrefineries will require modification as they will beunable to produce compliant product, even whenprocessing the best quality crudes such as those fromthe North Sea. Depending on the overall profitabilitylevels of the industry in the next few years, we couldsee a significant investment programme or a series ofclosures and mergers. If margins rise to the levelwhich offers a reasonable rate of return then, besidesinvestment to meet EU product quality legislation,further upgrades to the bottom of the barrel would be

R&D Publication 212

expected to occur. This would entail substantialexpenditure. However, if margins remain depressed,some further mergers or closures might be expected,since, for some operators, it is likely to beuneconomic to carry out a heavy programme ofinvestment under these circumstances.

In addition to these tighter EU product specificationsthere are a number of pieces of existing orprospective legislation that will require reductions inreleases to air. These include:

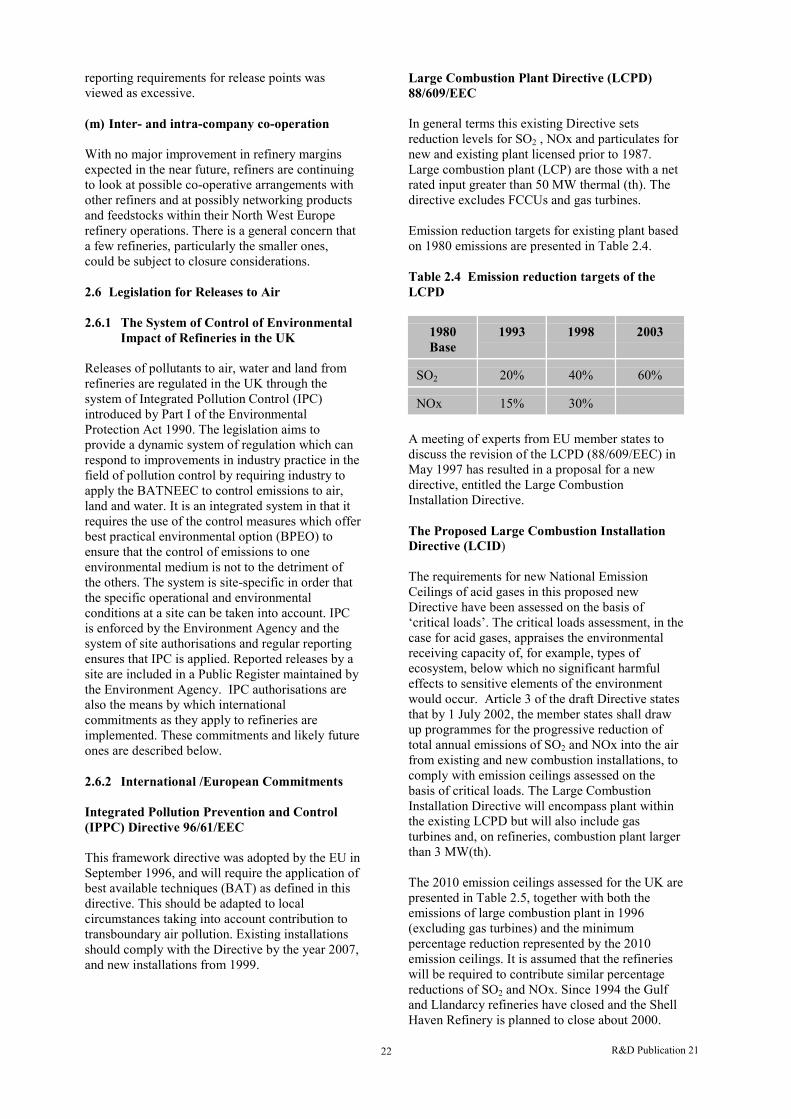

• the existing Large Combustion Plant Directive(LCPD) 88/609/EEC covering SO2 and NOx;

• the proposed new Large Combustion InstallationDirective (LCID);

• the United Nations Economic Commission forEurope (UNECE) Second Sulphur Protocol(1994);

• the proposed EU Communication on Acidification(COA) strategy for Europe covering SO2, NOxand ammonia. (This Communication is now likelyto be in the form of a proposed National EmissionCeilings Directive;

• the proposed EU Directive on ‘The reduction ofthe sulphur content of certain liquid fuels’(regarding fuel oil).

UK refineries range from a relatively simplehydroskimming refinery to cracking and bottom ofthe barrel upgrading refineries. Upgrading refineriesare more complex and have proportionately largermass emissions as cracking and bottom of the barrelupgrading are more energy demanding thanhydroskimming.

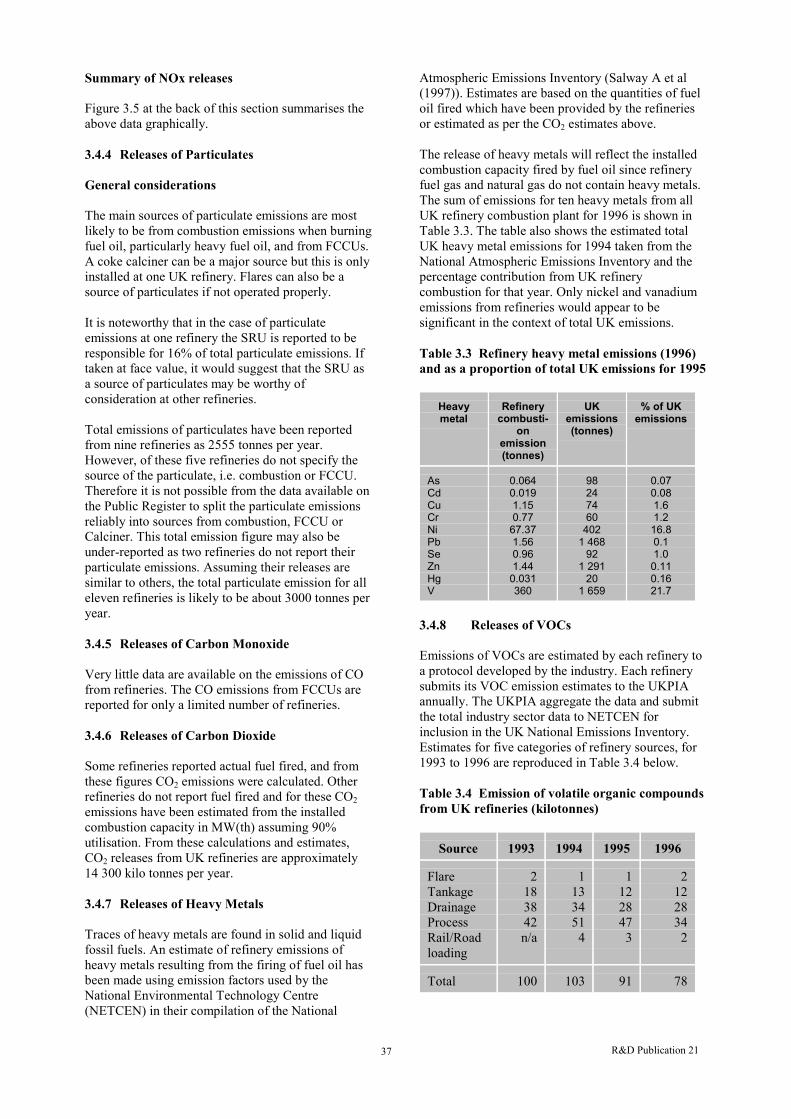

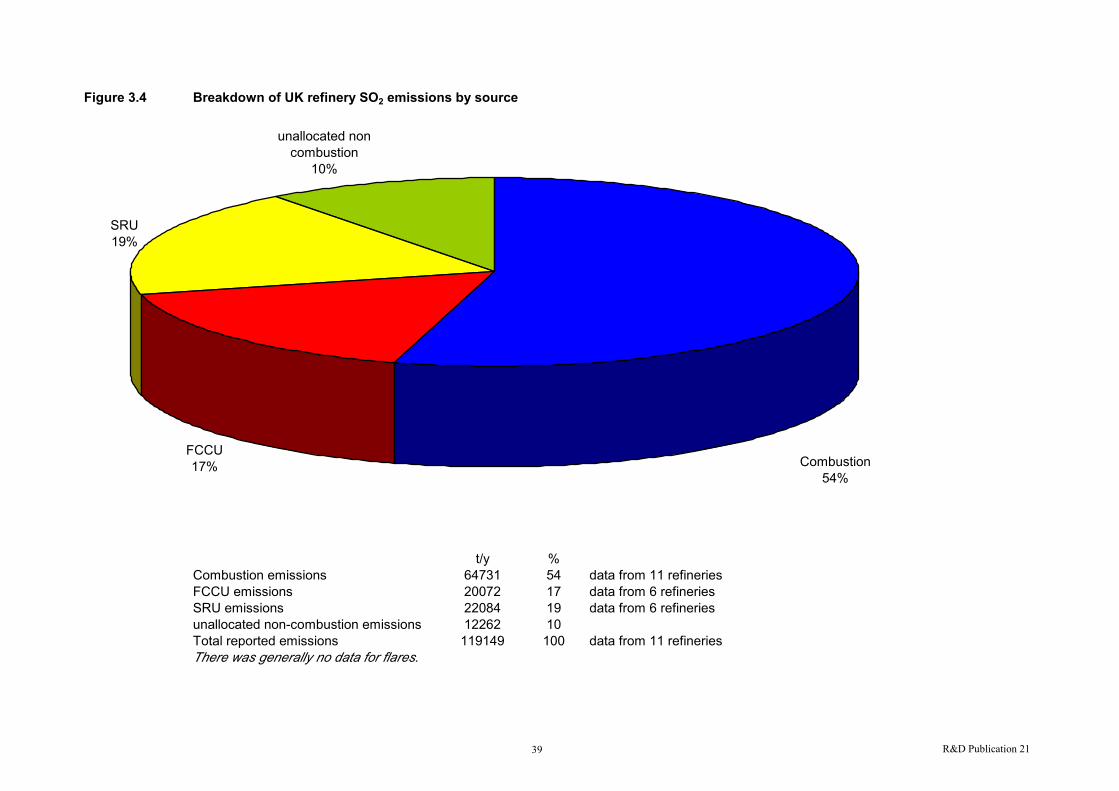

As requested by the Environment Agency a refineryrelease inventory has been developed as part of thisReview using information from the Public Register.This shows that in 1996 reported UK refineryemissions of SO2 were about 120 000 tonnes, whichrepresents about 5% of national emissions. In respectof NOx, reported refinery emissions were about30 000 tonnes in 1996 forming approximately 1.3%of national emissions. Reported particulate releasesconstitute about 0.8% of national emissions based on2600 tonnes from refineries in 1996. Total sector CO2releases were estimated to be 2.6% of the nationalemissions. The inventory also shows that on arefinery-sector basis approximately 54% of SO2releases are from combustion processes, 17% fromFCCUs (fluid catalytic cracker units), 19% fromSRUs (sulphur recovery units) and about 10% fromvarious other sources. Similarly for NOx on a sectorbasis, 81% of releases come from combustion, 15%from FCCUs and 14% from other sources includingcalciners. Not all emissions are reported (notablyparticulates) and insufficient data were available forflare emissions to be considered in the abovenumbers.

A number of comments have been made in thisReview concerning the data on the Public Register.For example, the Environment Agency may wish toconsider requesting, as a standard requirement, aVOC (volatile organic compound) release inventoryand a sulphur balance for each refinery, informationthat only a few refiners presently supply. It was notpossible to complete an extensive inventory ofreleases to water owing to lack of consistent data onthe Public Register.

Data from the Public Register also show that forsome combustion plant and FCCUs actual 1996reported release levels, especially SO2, weresignificantly below the release limits set by theEnvironment Agency. While there may be goodreasons for this, it could also mean that potentiallysignificant increases in current refinery releases to aircould occur within existing limits. However, anyrevision to limit levels, with this in mind, would needto take account of a refinery’s complexity,particularly the processing scheme and product slate.

Meetings were held with the local EnvironmentAgency inspector responsible for each refinery aswell as with all refinery operators. Notes of thesemeetings have been sent separately to theEnvironment Agency and although they are notincluded in the Review, the information gained,which was not confidential, has been used whereappropriate. Similarly, notes of meetings withoperators have been made and sent to themindividually and they are not included in thisdocument. However, a summary of the main pointsmade by most operators is included in Chapter 2. Themain points they emphasised included the fact thatthey are concerned to have clear target/limits inrespect of environmental releases and that theseshould be based on ‘sound science’. They also saidthey had no major investment plans in the near future,i.e. the next 12 months.

Comparison of UK abatement practice with world-wide refinery best practice in such countries as theUSA, Scandinavia, Japan, and the Netherlands showsthat the UK lags behind in the levels of abatementapplied. Scandinavian refineries represent the world’sbest practice. The SO2 release levels, for example,from the Mongstad refinery (Norway), which has acrude capacity of about 38 million barrels/year, areabout 2000 tonnes/year compared to UK refinerieswhich have SO2 releases ranging between5000-20 000 tonnes per year with crude capacities of28 to 98 million barrels/year. However, it should benoted that many of these countries with which theUK is compared, including Scandinavia, haveparticular, in-country, reasons for requiring very lowrelease levels.

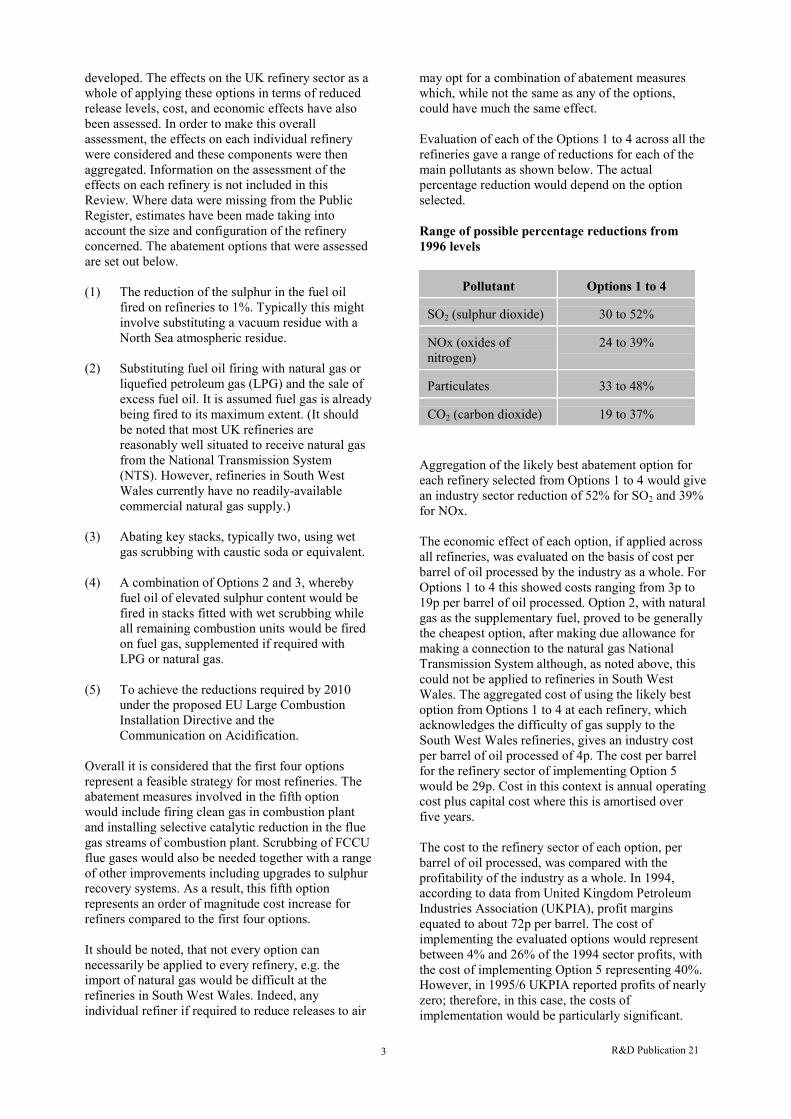

Based on analysis of the refinery release inventoryprepared for this Review, a number of options (orstrategies) for reduction of releases have been

R&D Publication 213

developed. The effects on the UK refinery sector as awhole of applying these options in terms of reducedrelease levels, cost, and economic effects have alsobeen assessed. In order to make this overallassessment, the effects on each individual refinerywere considered and these components were thenaggregated. Information on the assessment of theeffects on each refinery is not included in thisReview. Where data were missing from the PublicRegister, estimates have been made taking intoaccount the size and configuration of the refineryconcerned. The abatement options that were assessedare set out below.

(1) The reduction of the sulphur in the fuel oilfired on refineries to 1%. Typically this mightinvolve substituting a vacuum residue with aNorth Sea atmospheric residue.

(2) Substituting fuel oil firing with natural gas orliquefied petroleum gas (LPG) and the sale ofexcess fuel oil. It is assumed fuel gas is alreadybeing fired to its maximum extent. (It shouldbe noted that most UK refineries arereasonably well situated to receive natural gasfrom the National Transmission System(NTS). However, refineries in South WestWales currently have no readily-availablecommercial natural gas supply.)

(3) Abating key stacks, typically two, using wetgas scrubbing with caustic soda or equivalent.

(4) A combination of Options 2 and 3, wherebyfuel oil of elevated sulphur content would befired in stacks fitted with wet scrubbing whileall remaining combustion units would be firedon fuel gas, supplemented if required withLPG or natural gas.

(5) To achieve the reductions required by 2010under the proposed EU Large CombustionInstallation Directive and theCommunication on Acidification.

Overall it is considered that the first four optionsrepresent a feasible strategy for most refineries. Theabatement measures involved in the fifth optionwould include firing clean gas in combustion plantand installing selective catalytic reduction in the fluegas streams of combustion plant. Scrubbing of FCCUflue gases would also be needed together with a rangeof other improvements including upgrades to sulphurrecovery systems. As a result, this fifth optionrepresents an order of magnitude cost increase forrefiners compared to the first four options.

It should be noted, that not every option cannecessarily be applied to every refinery, e.g. theimport of natural gas would be difficult at therefineries in South West Wales. Indeed, anyindividual refiner if required to reduce releases to air

may opt for a combination of abatement measureswhich, while not the same as any of the options,could have much the same effect.

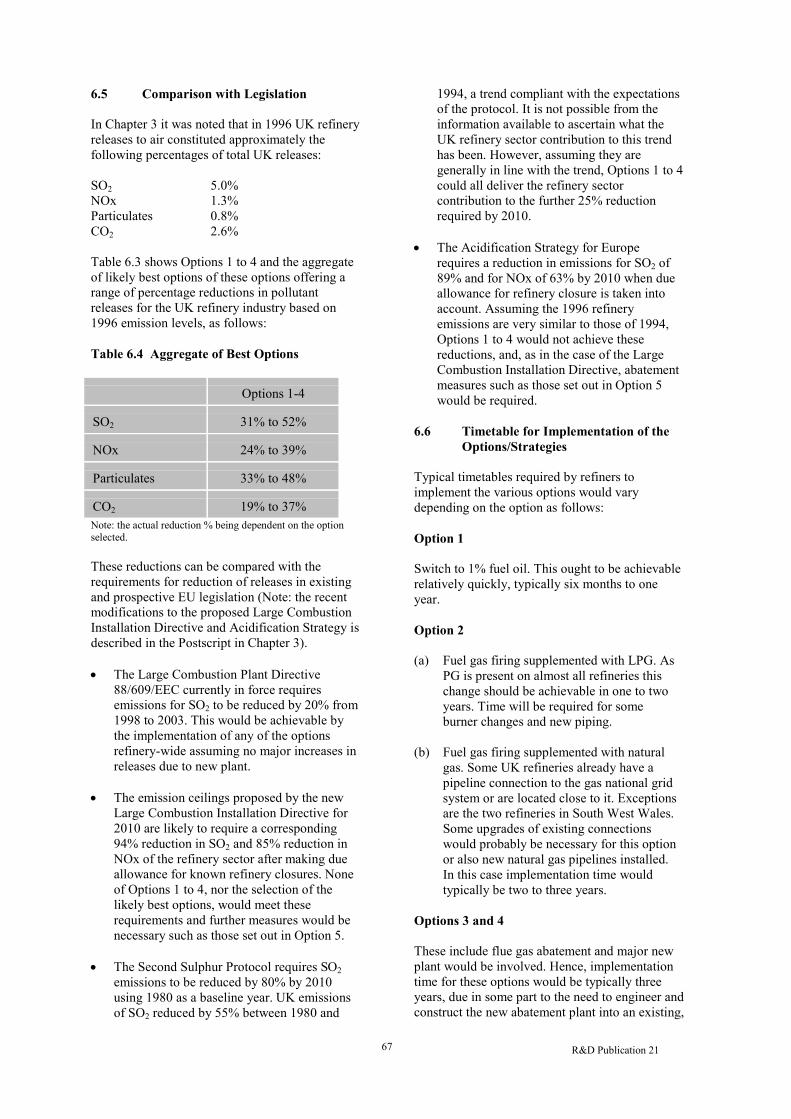

Evaluation of each of the Options 1 to 4 across all therefineries gave a range of reductions for each of themain pollutants as shown below. The actualpercentage reduction would depend on the optionselected.

Range of possible percentage reductions from1996 levels

Pollutant Options 1 to 4

SO2 (sulphur dioxide) 30 to 52%

NOx (oxides ofnitrogen)

24 to 39%

Particulates 33 to 48%

CO2 (carbon dioxide) 19 to 37%

Aggregation of the likely best abatement option foreach refinery selected from Options 1 to 4 would givean industry sector reduction of 52% for SO2 and 39%for NOx.

The economic effect of each option, if applied acrossall refineries, was evaluated on the basis of cost perbarrel of oil processed by the industry as a whole. ForOptions 1 to 4 this showed costs ranging from 3p to19p per barrel of oil processed. Option 2, with naturalgas as the supplementary fuel, proved to be generallythe cheapest option, after making due allowance formaking a connection to the natural gas NationalTransmission System although, as noted above, thiscould not be applied to refineries in South WestWales. The aggregated cost of using the likely bestoption from Options 1 to 4 at each refinery, whichacknowledges the difficulty of gas supply to theSouth West Wales refineries, gives an industry costper barrel of oil processed of 4p. The cost per barrelfor the refinery sector of implementing Option 5would be 29p. Cost in this context is annual operatingcost plus capital cost where this is amortised overfive years.

The cost to the refinery sector of each option, perbarrel of oil processed, was compared with theprofitability of the industry as a whole. In 1994,according to data from United Kingdom PetroleumIndustries Association (UKPIA), profit marginsequated to about 72p per barrel. The cost ofimplementing the evaluated options would representbetween 4% and 26% of the 1994 sector profits, withthe cost of implementing Option 5 representing 40%.However, in 1995/6 UKPIA reported profits of nearlyzero; therefore, in this case, the costs ofimplementation would be particularly significant.

R&D Publication 214

It should be recognised that this economic analysishas been restricted to assessment of the refineryindustry sector only. It has not considered the broadereconomic base of the operating companies whichown the refineries, which usually include oilproduction facilities and downstream chemicalsmanufacture.

The reductions offered by the options were comparedwith the requirements of current and potentiallegislation. This showed that, if implemented acrossall refineries, Options 1 to 4 would provide therequired levels of abatement to meet the existingLCPD 88/609/EEC and the UNECE Second SulphurProtocol (1994). This is based on the assumption thatthe UK refinery industry has met the reductions thatare required by the LCPD and the Protocol up to thepresent time. None of Options 1 to 4 would providethe level of abatement needed to meet therequirements of the proposed new LCID and the EUCOA acidification strategy. Only Option 5 would dothis.

If installed to meet the 2005 fuel specifications,FCCU hydrotreatment would provide about a 90%reduction in SO2 releases from the FCCUregenerators. However, due to its high capital cost itis not seen as a measure that can reasonably beapplied for the sole reason of abatement.

In the longer term gasification is seen as a possiblesolution for the disposal of high sulphur residue oils.It would produce ‘syngas’, which could be used as aclean gaseous fuel for combustion as well asproviding hydrogen for hydrotreatment and carbonmonoxide feedstock for organic chemical synthesis.However, current economic factors are very muchagainst the process being selected by refiners in theshort term except perhaps on a co-operative basis.These factors include the relatively high capital andoperating cost of the process, the reasonable marketfor fuel oil still prevailing, the relatively low cost ofnatural gas as a fuel for combustion, the good supplyof light sweet North Sea crude oil, and the small pricedifferentials currently existing between the sweetcrudes and the heavier sourer crudes. If any of thesefactors were to change significantly, and the emissionlevels proposed under the LCID and COA were tobecome firm requirements, refiners might considergasification more seriously.

The combustion of ‘clean’ gaseous fuels offers manyadvantages over heavy fuel oil including lower SO2,NOx, particulates, heavy metals and CO2 releases.However, the amounts of refinery fuel gas availablefor combustion in refineries may decrease due to itshydrogen component being required for the extrahydrotreatment needed to meet the 2005 fuelspecifications. Some refiners may invest in newreforming plant to provide the extra hydrogenrequired; however, others may wish to burn more fueloil. Even if low sulphur fuel oil is fired this could still

lead to increases in levels of NOx , particulates andheavy metals unless additional abatement is provided.

The optimum route for the reduction of CO2emissions in the longer term seems likely to be thecombustion of gaseous fuels with highhydrogen/carbon ratios such as refinery fuel gas,natural gas, LPG or hydrogen itself possiblyproduced from reforming or gasification processes..

There are reports that significant advances have beenmade recently in hydrogen/oxygen fuel celltechnology for the powering of vehicle transport. Iffuel-cell-powered vehicles should prove technicallyand commercially viable in the next five to ten years,the major effect on refineries would be the need tosupply the new fuel to the required specification,while maintaining existing fuel types.

Postscript

Since completing this Review a recent change hasbeen made by the EU to the proposed LargeCombustion Installation Directive. Originally thisspecified emission limits for SO2 and NOx releasesfrom existing and new large combustion installationsincluding gas turbines. The proposal has recentlybeen modified so as not to apply to existing plant.However, demanding National Emission Ceilings,designed to be met by the year 2010, are proposed bythe EU as a result of the Communication onAcidification. The softening of the LCIDrequirements therefore will only have a relativelyminor effect on the evaluations made in respect ofOption 5 in this Review.

Key words

refinerypetroleumemissionsabatementoil

R&D Publication 215

1. INTRODUCTION

This Strategic Review of the Petroleum RefineryIndustry Sector has been carried out by FosterWheeler Energy Limited on behalf of theEnvironment Agency. Specifically, Foster Wheelerwas requested to:

• Review the UK petroleum refining industry andcompare the UK refinery practice with bestpractice around the world.

• Prepare a national inventory of releases (includingboth authorised and fugitive releases) made by thesector to air, water and land and indicate whichpollutants have the greatest environmental impact.

• Prepare a range of strategies to reduce the releasesfrom the refinery industry sector. These shouldconcentrate on the pollutants with the mostsignificant environmental impact.

• Estimate the overall costs of each of the mostsignificant pollution release reduction strategiesand undertake detailed economic analysis of theimplications.

• Predict the probable effect upon the releaseinventory of implementing the most significantpollution release reduction options.

• Examine strategies to reduce pollution releasesfrom the petroleum refinery sector in the longerterm (25 years).

Chapter 2 of this Review discusses the importantfactors currently affecting UK refineries such ascrude oil supply, environmental legislation, productdemands and refinery economics.

Chapter 3 includes reviews of the current levels ofabatement applied to UK refineries and an inventoryof their releases to air.

Chapter 4 compares UK abatement practice withworld-wide best practice. Countries such as the USA,Japan, the Netherlands and Scandinavia areconsidered.

Chapter 5 discusses pollution reduction issues forrefineries, techniques for pollution reduction andtheir costs.

Chapter 6 sets out five options (or strategies) forpossible pollution reduction and assesses theireffectiveness and cost with current and proposedenvironmental legislation for the refinery sector as awhole:

Chapter 7 discusses pollution reduction technologyand associated issues in the longer term.

A number of important points should be notedregarding the Review. These are as follows-

(a) The UK refineries considered in this Revieware BP Grangemouth, Phillips Petroleum NorthTees, Lindsey at Killingholme, Conoco also atKillingholme, Shell Stanlow, BP Coryton,Shell at Shell Haven, Esso Fawley, MobilLlandarcy, Texaco Pembroke and Elf atMilford Haven. Gulf also at Milford Haven hasalready been closed and has therefore not beenconsidered in detail. Shell Haven is planned toclose in 2000 but has been included as part ofthis Review. It should be noted that while thisReview has included BP Grangemouth, thisrefinery is authorised by Scottish EnvironmentProtection Agency (SEPA) and not by theEnvironment Agency which is responsible forrefineries within England and Wales only. Theinclusion of BP Grangemouth is designed tocomplete the overall picture of the UK refineryindustry.

(b) It has been prepared using only information inthe public domain. In particular it is based ondata for releases to the environment taken fromthe Public Registers held by EnvironmentAgency offices in Britain. These release dataare for the year 1996 representing the latestand most complete set of information availableat the time this Review was prepared.

(c) The Review, as far as possible, takes accountof prevailing (1997 to 1998) refinery practice,economics, crude oil supply, market trends,environmental legislation including likelyfuture legislation, product demand, possiblepollution abatement techniques and the viewsof the refinery operators. It should be notedthat, like all industries, any of these factors canbe subject to relatively rapid change.

(d) Oil refineries are extremely complexoperations, probably the most technically andoperationally complex of all industry sectors,with a large number of integrated, high costprocessing units producing a wide range ofmainly combustible products in very largevolumes. Each refinery will therefore havemany constraints which will influence itspreferred methods of dealing withenvironmental factors and pollution abatement.This Review addresses these subjects as far aspossible when choosing the five possiblepollution abatement options, although incovering the whole refinery sector it isnecessarily generic in its approach. It is to beexpected that refiners could offer alternativesolutions and strategies to those contained in

R&D Publication 216

this Review which could achieve similarabatement results. The complexity of thisReview is, to a large extent, due to thecomplexity of the industry sector.

(e) Due to the very site-specific nature of local airand water quality, no assessment has beenmade of the current effects individualrefineries may be having on the local air andwater quality in their areas, nor on theimprovements the possible abatement optionsmight have on local air and water quality. Todo this would require a detailed assessment ofeach refinery's releases using dispersionmodelling techniques.

(f) Discussions have been held with each of theUK refinery operators together with the UKPetroleum Industries Association (UKPIA).Their views are set out in Chapter 2 of thisdocument.

(g) Little major new investment is envisaged in theUK refinery sector in the immediate future (thenext one to two years). This Review thereforemainly addresses existing refinery plant and itsoperation.

(h) While the information given in this Review isessentially based on data for individualrefineries taken from the Environment AgencyPublic Register and elsewhere within thepublic domain, the data have been analysed soas to present further information and commentfor the whole of the UK refinery sector.

(i) The Environment Agency terms of referencefor this Review ask that the options andstrategies prepared should concentrate on thepollutants with the most significantenvironmental impact. A number of UKGovernment and European environmentalreports and legislation give guidance on thismatter, such as the proposed EU acidificationstrategy, the second UNECE SO2 protocol andthe proposed Directive on Large CombustionInstallations. Guidance from these documentshas therefore been followed rather thandeveloping this subject afresh in this Review.

(j) This Review has assumed that the reader has abasic understanding of oil refinery operationsand processes. Readers less familiar with thisindustry sector may find the descriptions andexplanations helpful that are given inAppendix 2 of this Review, and in the HMSOChief Inspectors Guidance Note for ProcessesSubject to Integrated Pollution Control entitled‘S21.10 - Petroleum Processes: Oil Refiningand Associated Processes’.

R&D Publication 217

2. KEY FACTORS AFFECTING UKREFINERIES UP TO 2005

There are a number of important economic factors aswell as significant current and future environmentallegislative measures which will directly andindirectly affect refineries and their releases to theenvironment. These include:

• future crude quality and supply;• future markets for fuel oil;• refinery capacity and economics;• product quality changes;• current and future environmental legislation.

These factors are discussed in further detail below.

2.1 Crude Supply and Quality

Almost all the UK refineries are currently processingNorth Sea crude oil to a greater or lesser extent.Compared with other crude oils produced around theworld North Sea crude is both light (contains a higherproportion of lower boiling point fractions) and sweet(low in sulphur). The effect of North Sea crudeprocessing on UK refineries is threefold. First, due tothe relatively low sulphur content of the crude, SO2emission limits are generally met comfortably bymost refineries. Second, the crude produces more ofthe profitable light transportation fuels (gasoline anddiesel) in the first stage of crude processing and theserequire less hydrotreatment to remove sulphur. Third,the quality of the resulting residue is such that it isrelatively low in sulphur and permits greaterconversion to these lighter transportation fuels and acorrespondingly lower proportion of fuel oil. By wayof simple illustration, a given refinery configurationprocessing a North Sea crude could have a 20% fueloil yield, whereas the same refinery processing heavyArabian crude would have a 50% to 70% fuel oilyield. In reality each refinery has its own specificconfiguration and crude diet, and a few UK refineriesare processing heavier crudes in combination withNorth Sea crude. UK refiners are dependent uponNorth Sea crude to meet current and future marketdemands and sulphur emission limits.

It is therefore important to assess whether light/sweetcrudes will continue to be available to UK refineries.

To this end an assessment has been undertaken ofboth the future production of North Sea crude and thelikelihood that UK refineries can rely on supply ofthis crude in a competitive world market place.

2.1.1 UK Production

The North Sea is a significant supplier(approximately 20%) of non-OPEC (Organisation ofPetroleum Exporting Countries) crude oil. Althoughin general the qualities of North Sea crude are beingmaintained, more recently the Chevron Alba Fieldsand Statoil’s Heidrun Field have produced acidiccrude oil and special arrangements have had to bemade to refine this. High acidity crudes are forecastto rise in production from 0.5 million barrels per dayto 1.1 million barrels per day by the year 2000.

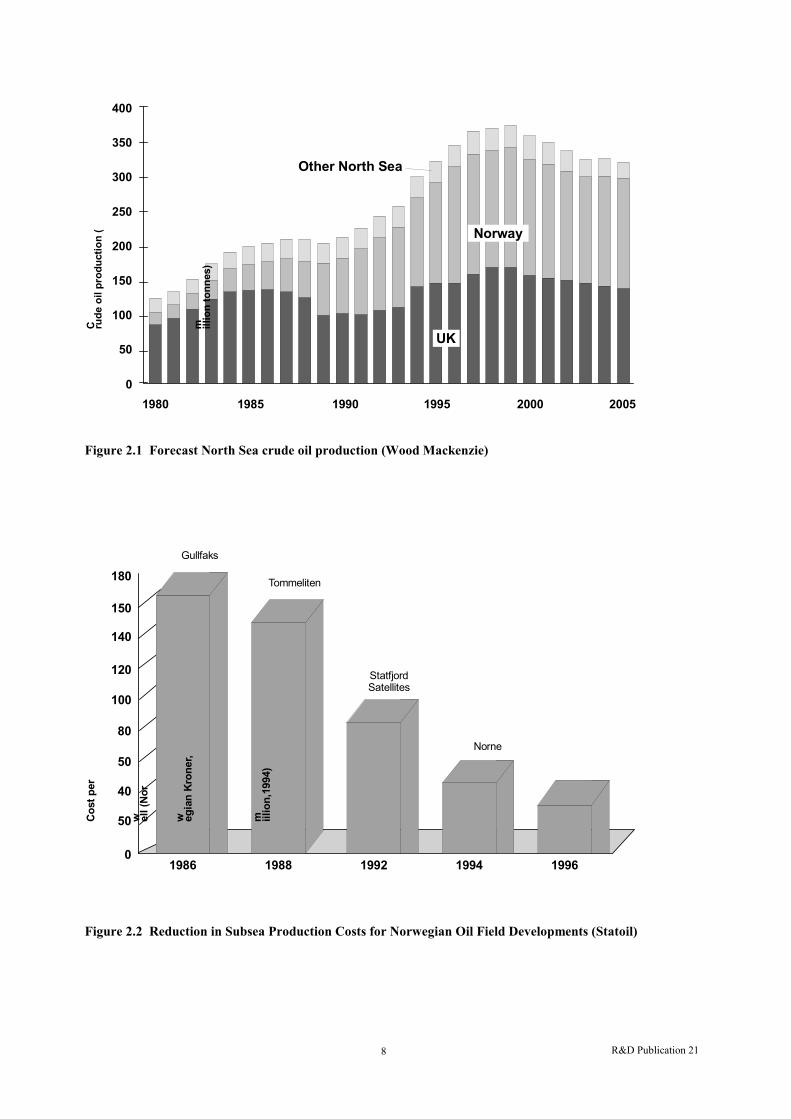

Looking to the future, Figure 2.1 shows a currentforecast of total North Sea crude production up to2005. It shows that Norwegian output is due toremain at or near current levels and that UK crude oiloutput, after a peak in 1998, is forecast to declinesteadily but still remain at a high level in historicalterms.

The rate of decline in the volume of UK suppliespost-2000 will be inevitably a matter of debate.Pessimists will argue that there are too few new smallfields to compensate for the decline in output fromolder large fields.

Sir David Simon, until quite recently chairman of BP,said in June 1997: “Finding and development costs inthe UK Continental Shelf have fallen by $8 per barrelsince 1990. That has been enough - in combinationwith a creative and responsive tax regime - to sustainboth exploration and development activity.Production looks set to increase for at least anothertwo years and the UK should still be producing asmuch as 2 million barrels of oil per day even in 15years’ time”.

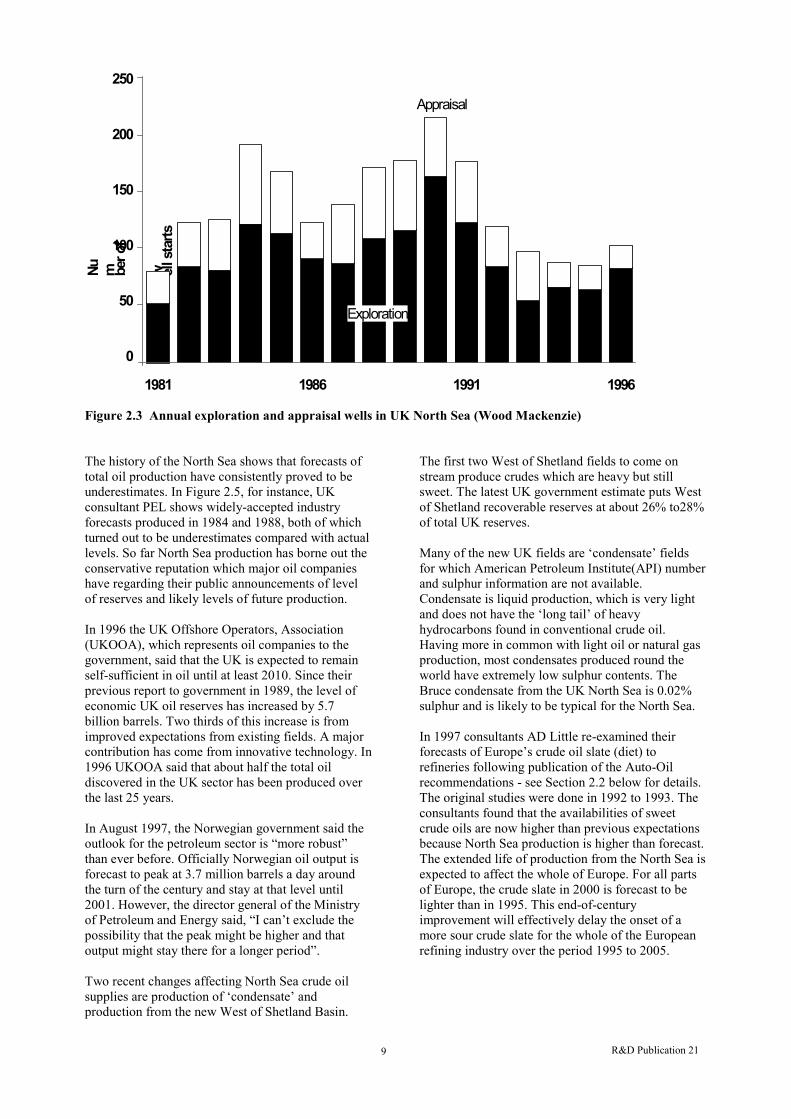

Costs of North Sea production have fallen due to bothtechnical improvements (e.g. 3-D seismic, horizontaldrilling, sea-bed production facilities, increasedrecovery rates, floating production vessels etc.) andcommercial improvements (‘out sourcing’, alliancecontracts etc.). For instance, Figure 2.2 illustrates thedramatic cost reduction in subsea facilities achievedin the last ten years.

Figures 2.3 and 2.4 show the level of explorationactivity and success respectively.

R&D Publication 218

400

0

350

300

250

200

150

100

50

1980 19901985 1995 2000 2005

Norway

UK

Other North Sea

C rude

oil

prod

uctio

n (

m illio

n to

nnes

)

Figure 2.1 Forecast Nor th Sea crude oil production (Wood Mackenzie)

1986 1988 1992 1994 19960

50

100

120

140

180

150

40

50

80

Year

Cos

t per

w ell (

Nor

w egia

n K

rone

r,

m iilio

n,19

94)

Gullfaks

Tommeliten

StatfjordSatellites

Norne

Figure 2.2 Reduction in Subsea Production Costs for Norwegian Oil Field Developments (Statoil)

R&D Publication 219

1981

Nu m ber o

f

w ell s

tarts

Appraisal

1986 1991 1996

250

200

150

100

50

0

Exploration

Figure 2.3 Annual exploration and appraisal wells in UK Nor th Sea (Wood Mackenzie)

The history of the North Sea shows that forecasts oftotal oil production have consistently proved to beunderestimates. In Figure 2.5, for instance, UKconsultant PEL shows widely-accepted industryforecasts produced in 1984 and 1988, both of whichturned out to be underestimates compared with actuallevels. So far North Sea production has borne out theconservative reputation which major oil companieshave regarding their public announcements of levelof reserves and likely levels of future production.

In 1996 the UK Offshore Operators, Association(UKOOA), which represents oil companies to thegovernment, said that the UK is expected to remainself-sufficient in oil until at least 2010. Since theirprevious report to government in 1989, the level ofeconomic UK oil reserves has increased by 5.7billion barrels. Two thirds of this increase is fromimproved expectations from existing fields. A majorcontribution has come from innovative technology. In1996 UKOOA said that about half the total oildiscovered in the UK sector has been produced overthe last 25 years.

In August 1997, the Norwegian government said theoutlook for the petroleum sector is “more robust”than ever before. Officially Norwegian oil output isforecast to peak at 3.7 million barrels a day aroundthe turn of the century and stay at that level until2001. However, the director general of the Ministryof Petroleum and Energy said, “I can’t exclude thepossibility that the peak might be higher and thatoutput might stay there for a longer period”.

Two recent changes affecting North Sea crude oilsupplies are production of ‘condensate’ andproduction from the new West of Shetland Basin.

The first two West of Shetland fields to come onstream produce crudes which are heavy but stillsweet. The latest UK government estimate puts Westof Shetland recoverable reserves at about 26% to28%of total UK reserves.

Many of the new UK fields are ‘condensate’ fieldsfor which American Petroleum Institute(API) numberand sulphur information are not available.Condensate is liquid production, which is very lightand does not have the ‘long tail’ of heavyhydrocarbons found in conventional crude oil.Having more in common with light oil or natural gasproduction, most condensates produced round theworld have extremely low sulphur contents. TheBruce condensate from the UK North Sea is 0.02%sulphur and is likely to be typical for the North Sea.

In 1997 consultants AD Little re-examined theirforecasts of Europe’s crude oil slate (diet) torefineries following publication of the Auto-Oilrecommendations - see Section 2.2 below for details.The original studies were done in 1992 to 1993. Theconsultants found that the availabilities of sweetcrude oils are now higher than previous expectationsbecause North Sea production is higher than forecast.The extended life of production from the North Sea isexpected to affect the whole of Europe. For all partsof Europe, the crude slate in 2000 is forecast to belighter than in 1995. This end-of-centuryimprovement will effectively delay the onset of amore sour crude slate for the whole of the Europeanrefining industry over the period 1995 to 2005.

R&D Publication 2110

Figure 2.5 Past industry forecasts of Nor th Sea oil production (PEL)

Figure 2.4 UK exploration success ratio (Wood Mackenzie)

R&D Publication 2111

It can therefore be concluded that there is more thansufficient light/sweet crude remaining in the NorthSea to meet UK refinery demand up to and beyond2005.

2.1.2 Effect of Global Oil Supplies on EuropeanCrude Availability to 2005

Although supplies of North Sea crude are sufficientfor the foreseeable future, the question ariseswhether UK refiners are likely to continue actually touse this local North Sea crude. For instance, by 2005,North Sea producers may prefer to export most oftheir light/sweet oil to other regions of the world or,conversely, will UK refiners choose to import largevolumes of lower-quality, higher-sulphur crude fromnon-North Sea sources especially if there is asignificant price differential between these and NorthSea crude.

Current UK crude oil tr ade pattern

Currently the UK is both an importer and exporter ofcrude oil. About 570 million bbl per annum of crudeoil is currently refined in the UK, of which about 250million bbl per annum is imported. These imports areoverwhelmingly light/sweet crude from theNorwegian North Sea. Exports from the UK arecurrently about 500 million bbl per annum (twice thelevel of imports), mainly destined for coastal ports inNorthWest Europe and deep-water exports to theUSA.

The trend over the last five years has been for UKexports to grow strongly while imports haveremained fairly steady. Exports started to increasefrom about 375 million bbl per annum in 1993 whena surge of UK North Sea capacity came on stream.During this period exports to the USA increased from20% to 27% of the rising total while exports to NorthWest Europe fell in relative terms from 50% to 44%.Over the same period Norway’s share of exports tothe UK increased from 50% to over 67% whileimports from the Middle East fell from 12% to just6%.

The observed trading pattern of UK refineries usinglargely North Sea crudes is understandable on thebasis of logistical costs. The UK is the closestrefining centre to most North Sea oil production andmost North Sea oil export pipelines land in the UK,offering the lowest delivery costs to the refinery gate.For offshore fields using direct tanker loading, thetankers are usually designed for regional rather thaninternational trading. It is because of this that the UKwill continue to compete strongly for North Sea crudeeven in the scenario that there is increasedcompetition in Europe for this crude due to EU fuelspecifications, (i.e. European refineries currentlyprocessing sour crudes may wish to switch andprocess sweet crudes so that specifications can bemore easily attained).

Summarising, the UK crude supply industry is fairly‘self-contained’: most oil refined in the UK issourced locally from the North Sea. Imports fromNorway are increasing but dependence on MiddleEast oil is both low and falling. A base load of oilexports goes to local European countries while, inrecent years, the USA has taken most of the UK’sincreased production. The UK’s strong exports to theUSA are aided by American-owned multinational oilcompanies which own or produce over a third of UKproduction.

Therefore, if current trends are any guide to thefuture, any significant increase in imports by the UKare likely to come from Norway and any majorincreases in exports are likely to go to the USA.

Current global crude oil tr ade pattern

Turning to global crude oil trade, Figure 2.6 shows a‘helicopter-view’ of the world’s biggest importersand exporters in 1996. Looking at the information ona regional basis, the figure shows that Asia importsthe largest amount of crude oil and is heavilydependent upon the Middle East. Western Europeimports a significant volume but from severalsources, such as the Middle East, Africa and theFormer Soviet Union. The USA imports a totalvolume similar to Western Europe but from a morediversified range of sources, i.e. Latin America, theMiddle East, Africa, Mexico, Canada and the NorthSea.

The trend in these data over the last five years showsthat the overall world pattern has remained basicallysimilar but imports by Asia from the Middle Easthave increased by 40% as Asian economies havedeveloped. In contrast Western Europe has reducedimports from the Middle East while increasingimports from the Former Soviet Union. Similarly, theUSA has slightly reduced imports from the MiddleEast but increased imports from other sources, i.e.Latin America, Mexico, Africa and the North Sea.

Current global crude oil quality

Quality of crude oil is a key factor which drivesinternational oil trading because the price ofindividual crudes depends upon their quality. Thecommonly-quoted headline ‘world oil price’ is in factthe price of one particular crude - Dubai - a medium-sulphur crude from the Middle East. As such, Dubaicrude usually has a medium price within a range ofcurrent crude prices. For instance, Dubai is usuallyabout $2 per barrel more expensive than a high-sulphur/heavy crude but about $2 cheaper than good-quality light/sweet crudes, such as Brent from theNorth Sea. These crude-oil price differentials, or‘spreads’, reflect the value of the crude to an averagerefiner: a barrel of low-price heavy/sour crude willrequire significant refining whereas a barrel of high-price sweet/light crude is ‘easy’ to refine.

R&D Publication 2112

Figure 2.6 Major oil tr ade flows in 1996 (BPStatistical Review of Wor ld Energy 1997)

Crude oil price differentials are a complex subject.For instance, besides light/sweet crudes andheavy/sour crudes there are also other combinations,e.g. light/sour crudes and heavy/sweet crudes. Theconsequence is that if differentials are high, then UKrefiners may be ‘outbid’ to acquire North Sea crude.At the same time other UK refiners, with sufficientspare refinery upgrading capacity, may choose toimport cheaper high-sulphur crudes and add value byprocessing.

Regarding trends in global crude oil quality, WoodMackenzie has suggested that the average worldcrude quality became marginally lighter and sweeterduring the 1990s. This was the result of increases inproduction of non-OPEC light/sweet crudes,including the North Sea, and a policy shift by SaudiArabia and Iran to maximise their lighter crudeoutput in order to increase revenues after the MiddleEast Gulf war in 1991.

USA consultants Purvin and Gertz suggest that thisshift to lighter crude production combined with overinvestment in upgrading capacity during the early1990s has resulted in very narrow heavy/light andsweet/sour crude price differentials. More thananything else these two factors have led to poorrefinery profitability in the early 1990s on a world-wide basis including the UK.

Future global scenar ios to 2005

Two alternative scenarios might be considered for thefuture development of global crude trade and itsimplications for the UK up to 2005. These twoscenarios might be termed, ‘The ConventionalWisdom’ and ‘More Independent USA’.

The conventional wisdom scenar io

This is based upon light/sweet crude oil becomingmore scarce. Two-thirds of world oil reserves arelocated in the Middle East, where the oil ispredominately heavy and sour, while only about one-third of global production currently comes from thearea. Therefore over time, as reserves run down

elsewhere, an increasing proportion of globalproduction must become heavier.

Within this scenario, oil production in non-OPECcountries declines, while OPEC remains a disciplinedorganisation and firmly ‘in the driving seat’. TheUSA, with declining domestic production, willincrease imports mainly from the Middle East. Worldoil prices will tend to rise, Middle East governmentfinances will improve, the need to ‘over-produce’light crudes will decline, shut-in heavy oil fields willre-open and crude price differentials will widen.

Under these circumstances, those UK refiners withsuitable upgrading capacity may choose to importcheaper heavy/sour crudes while minimising use ofexpensive North Sea crudes.

Recent evidence supporting this scenario includes:

• global oil demand is increasing quite rapidly (1.5million barrels per day);

• Middle East reserves increased by about one-third in the late 1980s;

• several ‘new’ production areas will produce sourcrude, i.e. deepwater US Gulf of Mexico, andVenezuela.

The more independent USA

The second scenario is based upon an extension ofrecent trends which appear to show that oil reservesare widely dispersed around the globe. In particular,within this scenario, the USA has the opportunity toreduce its dependence upon Middle East oil bydeveloping reserves throughout North and SouthAmerica and the Atlantic basin.

In this scenario, there is no potential global shortageof crude supplies. Current and future USA demand(see Table 2.1) is, and is likely to be, met byincreased oil production from many sourcesthroughout the Western Hemisphere - fromdeepwater US Gulf of Mexico, Canada, Mexico,Venezuela, Colombia, West Africa, North Africa andthe North Sea. Middle East producers increasinglyredirect their crude exports towards expanding Asiaand reduce exports to the Atlantic basin. With thepotential ‘loss’ of American markets and Venezuelanmembership, OPEC is weaker, crude prices tend tofall. Shortage of revenue encourages Middle Eastproducers to maximise production of higher-pricelight crudes and to restrict supply of low-priceheavy/sour crude. Crude price differentials remaincomparatively narrow.

In these circumstances, UK/European refiners willhave both less access to Middle East heavy/sourcrudes and limited financial incentive to refine it. TheUK is likely to increase exports to an import-hungryUSA and possibly compensate by increasing importsfrom Norway.

R&D Publication 2113

Recent evidence supporting this scenario is listedbelow.

• Some ‘new’ production in the Atlantic basin is ofsweet crude, i.e. Colombia, North Africa,deepwater West Africa, North Sea.

• Potential supply of crude to the USA is greaterthan potential USA import demand.

• Export of sweet West African crudes hasswitched from the Western Hemisphere to Asiaas western area sources replace this supply.

• Iraq traditionally exported crude to Asia andwould be expected to resume in future.

• Ecuador and Gabon have already left OPEC.

• Multinational oil companies have regained entryinto several OPEC countries.

• Asia often pays a higher price for Middle Eastcrude than the West.

• Venezuela is ignoring OPEC quotas.

• American refiners are investing in upgrading(cokers) to process local heavy/sour crude.

• Canada and Venezuela are investing insynfuel/extra-heavy crude upgrading projects.

• Canadian crude exports to the USA are growing,particularly from new East Coast fields.

• NAFTA trade agreement eases energy tradebetween the USA, Canada and Mexico.

• USA plans to ‘extend’ NAFTA to Latin Americaby creating FTAA by 2005.

• Technology is dramatically reducing oilproduction costs for non-OPEC countries.

• There is growing world-wide production of sweetcondensates.

Table 2.1 Potential changes in crude supplies toUSA from 1995 to 2000

Change intotal refinerythroughputbarrels/day

Change inUSA oil

productionbarrels/day

Increase inimpor ts tothe USA

barrels/day

650 000 200 000 450 000

Source PEL January 1997

Of the two scenarios the second is thought to moreclosely reflect what is likely to occur. It is foreseenthat the number of ‘new’ non-OPEC oil-producingcountries will keep growing which ultimately adds tosupply flexibility and weakens oil prices. The nextmajor newcomers are likely to be Azerbaijan andKazakhstan which are expected to be exporting toEurope by 2005.

Furthermore, even if the first scenario does turn outto be closer to the truth, then the Middle East oilexporters will still be most dependent upon Asiancustomers. Therefore if in the future Asian/Chinesegrowth slows down, as it recently has, the MiddleEast suppliers will be directly affected and oilprices/differentials will tend to fall even in thisscenario.

In conclusion it is foreseen that while fluctuationswill occur, crude oil prices and price differentials willcontinue to be low. As a consequence this willprovide little financial benefit to UK refineries. TheUK oil industry is likely to remain fairly ‘self-contained’ and UK refineries will continue to runlocal North Sea crudes to 2005 and beyond.

2.2 Product Quality Changes

Almost all fuel products of petroleum refining havebeen or will be affected by legislation aimed atreducing environmental impacts of fuels at their pointof use. It is at the refineries where a response to theserequirements will be met. The following sectionoutlines current and possible future legislative effectson product quality.

2.2.1 Road Transpor tation Fuel Quality

The continued pressure for clean fuels is manifest inthe recent EU legislation amending Directive93/12/EEC relating to the sulphur content of certainliquid fuels. The amendment details gasoline anddiesel specifications for the year 2000 and 2005, asshown in Tables 2.2 and 2.3. EU refiners willtherefore be required to meet tighter specificationsfor the year 2000. By the year 2005 they will berequired to meet what many observers regard as thetoughest transportation fuel specifications in theworld. This inevitably will also require EU refineryprocessing operations to be among the most complexand sophisticated in the world.

The recent EU legislation offers some derogation inrespect of time for the implementation of the newspecifications, subject to EU approval. However, forthis Review it is assumed that the EU specificationsin respect of the UK will apply, and that by the year2005 refiners will be producing fuels to meet theultra-low sulphur levels.

R&D Publication 2114

The implications of these 2000 and 2005Specifications on UK refineries are now discussedbelow.

Table 2.2 EU Requirements for gasoline

Item Currentlimits

93/12/EEC

Max.Limits for

2000

Max.Limits for

2005

Sulphurppm

500 150 50

Olefins% by vol

None 18 *

Aromatics% by vol

None 42 35

Benzene% by vol

5 1 1

* Specification not yet set for 2005. This will be set followingreport by Auto Oil II programme.

Note: Certain other limits also apply but are not included above.

Table 2.3 EU Requirements for diesel

Item Currentlimits

93/12/EEC(from

1.10.96)

Max.Limits for

2000

Max.Limits for

2005

Sulphurppm

500 380 50

CetaneNumber

49 51 (min.) *

PolycyclicAromatics% weight

None 11 *

DensityKg/m3

860 845 *

* Specification not yet set for 2005. This will be set followingreport by Auto Oil II programme.

Note: Certain other limits also apply but are not included above.

Meeting 2000 specifications (gasoline and diesel)

While the year 2000 will be important for refiners interms of EU fuel specifications, it is believed that themajority of refiners have already put in placeinvestment plans to produce fuels to meet them.Those refiners who have not already prepared for thereduction of sulphur and benzene in gasoline willnow be investing in benzene and sulphur reductiontechnology, although by continuing to process low-sulphur North Sea crude, most refiners will be able tomeet the low-sulphur levels with only modestinvestment costs.

In terms of overall emissions from the refinery, thesechanges will only give rise to a marginal increase.

Meeting 2005 specifications (gasoline and diesel)

There is no doubt that refiners will be required toinvest significantly to meet the gasoline and dieselspecifications for 2005.

Gasoline

The majority of UK refining installations operate afluid catalytic cracker unit (FCCU) for upgradingheavy fractions to lighter products. The naphtha fromthe FCCU is the primary contributor of sulphur to therefinery gasoline pool. Reducing contribution ofsulphur is the critical issue for meeting reducedgasoline sulphur specifications.

The sulphur is not evenly distributed throughout theboiling range of FCCU naphtha. Typically about halfthe sulphur found in the FCCU naphtha isconcentrated in the final 10% of the boiling range.This gives the refiner some flexibility to minimisetreatment by focusing on the heavier fraction ofnaphtha. The sulphur specification for 2005 is lowand even when processing North Sea crude, a typicalrefiner will need to hydrotreat the majority of FCCUnaphtha in order to meet the required level.Hydrotreatment of the FCCU naphtha reduces theolefin content which reduces octane. The impact ofoctane reduction on the gasoline pool needs to beconsidered on a refinery-specific basis.

Alternatively the refiner could hydrotreat the feed tothe FCCU, in which case any further hydrotreatmentmay be restricted to the heavier fraction of FCCUnaphtha or potentially avoided altogether. Thedecision to install a catalytic feed hydrotreater (CFH)of this complexity and cost will usually be made onmarket investment criteria since there are benefits interms of increased conversion to higher qualityproducts. It is not expected that a CFH will beadopted by many refiners as a method for achieving2005 specifications.

The refiner may also utilise alternative approachessuch as use of FCCU catalyst additives, blending ofhigher sulphur components, and extractive caustictreatment, but these are only partial solutions at best.Hydrotreatment is therefore expected to be the keyapproach adopted by most refiners, with associatedfacilities to manage the consequent octane loss fromthe gasoline pool perhaps being needed. Reduction inaromatics content of gasoline, also a requirement ofthe 2005 specification, will remove a valuable octaneenhancer from the pool, further restricting therefiner’s ability to manage the octane loss.

Diesel

For diesel, sulphur reduction to 2005specificationsrequires investment to hydrotreat the entire roaddiesel pool. The severity required will be determinedpartly by cetane and polycyclic aromatic hydrocarbon

R&D Publication 2115

specifications. Hydrogen will be required forhydrotreatment and its sourcing will need to beaddressed as noted above.

2.2.2 Bunker Fuel

Bunker fuel is used in ships’ boilers for propulsion. Itnormally originates from the residue of atmosphericand vacuum distillation in the refinery and sulphurtends to concentrate in this product. This is one of thefew markets for residues which has thus far beenunaffected by environmental legislation.

The Marpol Convention (Annex 6) is currently underdiscussion and is being developed under the auspicesof the International Maritime Organisation (IMO).This aims to control emissions of air pollutants fromshipping. It proposes a global cap of 4.5% on thesulphur content of bunker oil, with a lower limit of1.5% in especially sensitive areas. A conference tookplace in September 1997 which resulted in the BalticSea areas accepting the 1.5% limit; however, thecountries bordering parts of the North Sea did notagree to the proposals. This Air Pollution Annex willform part of the Marpol Convention which, onceratified, should come into force within three to fiveyears. The IMO will revisit the proposals if they failto be ratified by 2002.

Indications are that countries , such as thosebordering the Baltic and North Sea, may introducedomestic legislation before the Annex becomesinternationally ratified.

2.2.3 Gas Oil

The sulphur content of all gas oils (except aviationkerosene) was limited to 0.2% by weight (2000 ppm)from 1st October 1994 by implementation of ECDirective 93/12/EEC.

2.2.4 Kerosene (Jet Fuel)

The European Commission is to propose a new limitvalue for aircraft kerosene. Details of the proposednew limit are still awaited but speculative limitssuggest a sulphur limit of 100 ppm.

2.2.5 Fuel Oil

Draft EC Directive 97/0105 (SYN.) includes aproposal amending Directive 93/12/EEC whichwould limit the sulphur content of heavy fuel oil to1% from 1999. The limit would not apply to fuel oilcombusted in the refining industry, or in largecombustion plant which is new or which alreadycomplies with the emission limits for such plant inEC Directive 88/609/EEC. The derogation forrefineries and large combustion plant from thisDirective is allowed on the basis that it is more costeffective to use flue gas abatement technologies toremove SO2. (This may not be so for refineries.)

The EU acidification strategy, part of a proposed ECstrategy to combat acidification of sensitiveecosystems, suggests that 9.03 million tonnes of fueloil were utilised in the UK in 1995. Of this 3.44million tonnes were utilised by major powerproducers (likely to come under Directive88/609/EEC) and 2.32 million tonnes were used byrefineries which in that year would leave 3.26 milliontonnes consumed in other uses. If this proportion isreflected in future years then 36% of fuel oil used inthe UK would have to be below 1% sulphur. Thisneed to supply the low sulphur fuel oil would meanthat higher sulphur fuel oil could probably bepreferentially fired in the derogated refinery andpower sectors.

2.3 The Future for Fuel Oil

2.3.1 The Cur rent Fuel Oil Market and Trends

This section reviews the future markets for fuel oil.Fuel oil is a large volume product produced byrefineries. It normally contains relatively highamounts of sulphur compared with other refineryproducts and its future large scale use is at presentparticularly uncertain. The product is of importancein the context of refinery emissions, as decliningsales demand for fuel oil is likely to increase pressurefor its use as a fuel on the refinery. An increase in theproportion of fuel oil to refinery gas combustedwould see a corresponding increase in emissions ofSO2, CO2, NOx, particulates and heavy metals.

In practice, internal refinery fuel oil consumption isset by the difference between total fuel demand andinternal fuel gas supply. The fuel balance within eachrefinery is specific to its configuration. Other factorssuch as energy efficiency, electrical power importand the recovery of useful components from the fuelgas, which can contain about 50% hydrogen, willdetermine the final balance and hence fuel oildemand. This balance is subject to change whensignificant additional processing units are installed,especially those demanding fuel gas and/or hydrogensuch as additional hydrotreatment.

Total European consumption of fuel oil has beenfalling consistently for many years as a result ofstructural change in the industrial sector and thecompetitive impact of other fuels, notably naturalgas. European consumption fell from 162 milliontonnes in 1982 to 107 million in 1996. By the latteryear ships' bunkers accounted for about 25% of totalconsumption, the one sector of the market which hasnot been shrinking. The UK is a small market,consuming 9 million tonnes in 1995 and only 6.85million tonnes in 1996.

Within Europe the decline has been most marked inthe industrial sector with 1982 consumption of 50million tonnes falling to less than 20 million by 1995.Power generation from fuel oil has also fallen sharply

R&D Publication 2116

although most of this decline occurred in the 1980s.The power market is now dominated by ENEL ofItaly which consumes 34% of Europe's inland fuel oiland ENEL's requirements will have a major impacton the direction of fuel oil markets in Europe over thenext ten years. ENEL currently specifies a maximumof 1% sulphur for 60% of its purchases but is likelyto apply the restriction to a higher percentage of itspurchases in the future.

Traditionally much of the fuel oil consumed inEurope has had a higher sulphur content than this,although the sulphur percentage has been graduallydeclining in the face of tighter environmentallegislation controlling acid gas emissions, such as theLarge Combustion Plant Directive. The exception isbunker fuel but this may become subject to tighterregulations within EU coastal waters. (See Section2.2.2.)

With regard to the quality of fuel oil used generallyin the UK and its imports and exports, there is verylittle detailed information publicly available, but whatthere is would suggest the following:

(1) High sulphur fuel oil is produced to only alimited extent by UK refineries. This tends tobe, for example, where heavier crudes whichtend to have a high sulphur content arerequired for production of bitumen and lubeoils. An indication of this may be seen inTable 3.1 where fuel oils with sulphur contentsgreater than 2% suggest some processing ofnon-North Sea crudes.

(2) High sulphur crudes are not processed by UKrefineries to a significant extent due to theseveral advantages North Sea crude offers,especially its low sulphur content.

(3) Fuel oil exports from the UK are likely to bepreferentially low sulphur to markets whichdemand this, for example, Italy. Fuel oilexports from the UK were 1 979 000 tonnes in1996(i) (Dti, 1996) although there is noindication of the sulphur content.

(4) Fuel oil imports to UK industrial sectors otherthan the refinery sector are likely to be highersulphur fuel oil, this normally being cheaper.While releases of SO2 to air are controlled, theuse of high sulphur fuel oil is not restricted inthe UK, except indirectly where the processrequires it or where release limits of SO2 inany site authorisation can only be met bycombusting low sulphur fuel oil. The UK fueloil imports were 5 343 000 tonnes in 1996(Dti, 1996) although again there are no specificdata on the sulphur content of those imports.However, returns to the Environment Agencyfrom the electricity supply industry indicate

that where fuel oil is used it is often over 2.5%sulphur.

2.3.2 Future Markets

The outlook for fuel oil in Europe will be determinedby both supply and demand factors, with the shortterm position likely to be different from the situationpost-2000. In almost all cases inland demand isexpected to decline slightly between now and 2000but this will be matched by a similar drop inproduction as both minor and major refineryupgrades take effect. Post-2000 the situation isexpected to change more radically from both a supplyand demand perspective.

Demand

• In addition to the long-term gradual decline infuel oil consumption there is the prospect of amore rapid decline post-2000 as a result of newsupplies of gas becoming available in Europe atcompetitive prices following marketderegulation. There is no clear forecast available,but it is conceivable that the inland market forfuel oil could decline by 50% beyond 2005 whilebunker fuels remain static. If this happens,European consumption in 2005 would be around65 million tonnes.

• Trends in product quality are more importantthan the volume of demand. It seems highlylikely that industrial or power users will eitherhave to invest more widely in flue gasdesulphurisation or be restricted to buying fueloil with 1% or less of sulphur. It is unclear howfar legislation will tighten for ships’ bunker fuels,but any plan to tighten quality in bunker fuel willput further pressure on the high sulphur product.The scope for using fuel oil as a 'sink' for sulphurwill be greatly restricted.

• With declining markets at home, Europeanrefiners will be looking for other outlets for theirfuel oil. One potential market is Asia which isdeficient in fuel oil despite recent increases inrefinery capacity. Net imports to that region wereexpected to be around 4 million tonnes in 1997,rising to almost 20 million in 2000. Imports arethen forecast to decline to around 16 million in2005 although this assumes that a significantamount of new local production capacity is built.Not all of this market is available to Europeansuppliers since Asia is a well established marketfor Middle East refiners and supplies also comein from the West Coast of the USA. It does,however, provide an outlet for some of Europe'spotential surplus, although it should be noted thatmany Asian countries have introduced or areintroducing increasingly stringent environmentallegislation which may also require the firing oflow sulphur fuel oil.

R&D Publication 2117

Supply

• Over the next three to four years fuel oil outputfrom European refineries is likely to declineslightly, probably in line with falling demand.The situation may change more radically in theearly years of the next century as refiners cometo terms with much more stringent qualitystandards.

• European refiners may benefit from a reductionin fuel oil exports from the Former Soviet Union(FSU) which currently total about 20 milliontonnes per year into Western Europe. Over thenext ten years refinery closures and upgradingprojects will reduce the availability of fuel oilfrom that region. This may reduce the potentialsurplus in Europe but it will have no impact onthe trend to cleaner fuel oil.

2.3.3 Implications for UK Refiner ies

UK refineries have consistently produced anexportable surplus of fuel oil. In 1997 production was11.7 million tonnes, compared with consumption ofonly 3.9 million tonnes. Both domestic and Europeanmarkets are expected to continue a gradual declineover the next ten years which will put pressure onrefiners to either upgrade or find new export markets.The reduction of high sulphur fuel oil within Europeis expected to be more rapid for land-based markets,leaving a supply market for fuel oil to ships’ bunkersonly which would total about 25 million tonnes.Export markets outside Europe are moving the sameway, although at a slower pace, and 3.5% sulphurproduct will still be permitted in some countries for awhile. Countries such as Thailand have alreadyintroduced legislation to prohibit the burning of highsulphur fuel oil (HSFO) in the greater Bangkok areaand this trend will gradually extend to other countriesin the region.

Overall, therefore, UK refiners will have to manage agradual change in their fuel oil business as marketsdecline and quality standards improve. It will begradual, however, and no precipitative change isanticipated.

2.4 UK Refinery Capacity and Economics

The following section reviews recent trends andperformance in the capacity and economics of the UKrefinery sector.

This assessment has been restricted to the refineryindustry sector. It has not considered the broadereconomic base of the refining companies which oftenown integrated chemical complexes, usually locatedon the same site as their refinery; nor has itconsidered the interests and ownership the companiesoften have in oil production facilities in the North Seaand world-wide.

2.4.1 Current UK Refinery Capacity

Total UK refinery capacity reduced significantly inthe early 1980s in response to falling demand andpoor margins. Total distillation capacity fell fromabout 130 million tonnes in 1980 to a little over 90million tonnes by 1985, a level broadly maintainedsince then.

Utilisation rates were very low in the early 1980seven with capacity being closed. In 1983, forexample, the output of all products was only 70% ofinstalled distillation capacity. Sales to the UK marketwere even lower and surplus product had to beexported. Since then utilisation levels have risensteadily as Figure 2.7 illustrates.

In 1996 the utilisation level across the UK refinerysector was at least 92% with approximately 13% ofproduction being exported.

The Gulf Refinery at Milford Haven has now beenclosed which removes about 5 million tonnes ofcapacity from the UK total (approximately 5%reduction) and plans are being made to close theShell Refinery at Shell Haven and part of theLlandarcy Refinery.

2.4.2 Future Capacity

The increase in UK refinery utilisation levels whichhas occurred since 1980 has been due almost entirelyto capacity closures and a modest increase in exports.Domestic demand for all products has been almoststatic, having risen from 71 million tonnes in 1980 to75 million tonnes in 1996, an increase of only 5.6%after 16 years.

There is no reason to think that demand will growsignificantly between now and 2005. Demand fortransport fuels will be restrained by high taxationlevels and the possible impact of government policyon levels of car use as well as improvements in fuelefficiency. The UK consumption of fuel oil and gasoil for heating is likely to continue to fall in the faceof competition from gas. On this basis UK refinerswill continue to operate in a near-static domesticmarket and will look to export markets to take‘surplus’ product.

Over the past two years UK and other Europeanrefiners have been able to take advantage of buoyantUS demand for gasoline. Total gasoline exports in1996 were over 8 million tonnes.

Currently there is a gradual shift in transport fuelsfrom gasoline to diesel. If this slow shift continuesUK refiners will continue to look to the USA forgasoline exports. The long-term outlook for theseexports is unclear, being dependent, in part, onrefinery capacity increases in the USA and LatinAmerica.

R&D Publication 2118

Figure 2.7 UK refinery capacity utilisation

Given that UK and European demand will be fairlystatic, the key factor will be supply. There is likely tobe very little European demand for new refineries orlarge capacity increases between now and 2005although developments on the margin of WesternEurope, such as at Leuna, former East Germany, andMidor in Egypt, could have a major impact. Therewill continue to be capacity creep, due to theoccasional upgrade which will tend to increasecapacity on a modest scale.

With the above factors the importance of refineryclosures becomes apparent. There has been much talkof closure in recent years and some refineries havebeen shut down. Given the financial problems of theindustry more closures may be expected but timing isvery uncertain. It could well be the case that theprocess will accelerate post-2000 as refinerscontemplate heavy capital expenditure to meet 2005product specifications. The extent to which UKrefiners are affected by closure is impossible topredict. There is no doubt that overall marketconditions will put pressure on the refinery sector toreduce capacity but it may need a specific triggersuch as 2005 specifications to overcome the inertia inthe system caused by high site clean-up costs,employment protection agreements, etc.

2.4.3 UK Refinery Economics: Outlook to 2005

Refinery margins in Western Europe have been poorfor many years but the situation worsened from mid-1994 in the face of adverse global trends. Much

investment at refineries in the late-1980s/early-1990shad been based on the assumption that the averagebarrel of feedstock would become heavier and sourer.By 1994 this assumption had been undermined by anincrease in supply of light, low sulphur crude fromthe North Sea, Africa and, most unexpectedly, SaudiArabia. The result was that upgrading margins werebadly squeezed and overall profitability declinedeven further.

Figure 2.8, published by UKPIA, shows the steepdecline in operating profitability in the downstreamsector of the UK oil industry. It should be noted thatthe downstream sector includes both oil refining aswell as product distribution and retailing. By 1996there was an overall operating loss and while therewas some improvement in 1997 it was not dramatic.The situation is broadly similar throughout WesternEurope. In a recent presentation Rolf Stomberg of BPestimated that there is approximately 500 000 barrelsper day of surplus refinery capacity in the region. Theextent to which this surplus is eliminated is a keydeterminant of whether the industry can becomeconsistently profitable again.

Although demand for refinery products is fairly staticin overall terms, the market for particular products isexpected to change significantly over the next tenyears. The gradual reduction in fuel oil sales willincreasingly concentrate demand on transportationfuels and petrochemical feedstocks. Product qualitystandards for 2005 are well beyond the ability ofmost UK refineries to produce with their existing

0

20

40

60

80

100

120

Outp ut

Capac ity

R&D Publication 2119

91 92 93 94 95 96(200)

0

200

400

600

800

(2)

0

2

4

6

8£ M ill

ion

Per

cent

age

Return on Investment

Actual profit

Pro

fit

Figure 2.8 UK refinery sector profitability (Source UKPIA)

plant and equipment even when processing 100%North Sea crude. These factors will combine to putpressure on refiners by the early years of the newcentury and a point will be reached when decisionswill have to be made to upgrade or close downrefineries.

These comments assume that the European refiningindustry remains only marginally profitable as ithas been for several years. In the 1990s pooreconomic performance was due in part to very poorutilisation levels caused by an excess capacity.Since then much of this has been eliminated andEuropean refineries are now running at muchhigher levels - at least 92% on average in 1997.

Under these circumstances it might be assumed thatprofitability would have shown a markedimprovement. In reality, however, most refinersexperienced only a modest improvement in marginsduring 1997 to 1998, which was mainlyconcentrated in upgrading margins, due to highlycompetitive conditions at the point of sales.

Individual refiners have a tendency to process asmuch throughput as possible, since this improvesrevenue, but it is based on marginal costing. Aslong as the plant is amortised and requires littleadditional expenditure, this situation is sustainable.

The key issue for the future will be the recently-introduced legislation on fuels quality which willcompel most refiners to invest heavily. At thispoint margins must rise to a level which enables

new investment to be financed. If this is notforthcoming the rational market response would bea wave of refinery closures to create a much tightermarket, thereby improving margins. In the periodup to 2005 it is expected margins will improveslightly but remain low relative to other industries.

2.4.4 Likely Investment Patterns to 2005

In the present economic climate for refineries,operators/owners are expressing extreme reluctanceto invest in new plant, including abatement plant,for the following reasons:

• with intense forecourt competition any addedproduct value resulting from investment willalmost immediately be lost;

• investment for environmental purposesprovides no added product value and overallhas a marginally negative value on return oncapital employed (ROCE);

• some future environment specifications, e.g.the EU Acidification Strategy, are not firm.Refiners want clear targets in view of the highlevel of capital expenditure likely to beinvolved;

• the UK is now having to compete to someextent with countries who have alreadyinvested more heavily in environmental plant(i.e. sunk cost).

R&D Publication 2120