a shale gas strategic alliance

TRANSCRIPT

Excellence in Oil & Gas

A Shale Gas Strategic Alliance Drillsearch-QGC Cooper Basin Shale Gas JV

Excellence in Oil & Gas

MARCH 2012

Excellence in Oil & Gas

2 Investment Proposition

Active EXPLORATION program

Growing OIL production

First WET GAS production

Huge UNCONVENTIONAL gas resource potential

FULLY FUNDED work program

Delivering GROWTH in reserves, production and cashflow

TRANSITIONING to significant oil and gas producer

Excellence in Oil & Gas

3 Changing Environment for the Cooper Basin

Market factors fostering a Cooper Basin renaissance. . .

LNG demand has transformed markets

Oil-linked pricing improves commerciality

CSG ramp up complexity is real

Simplified supply chain response

LNG project expansions require large scale resources

Cooper Basin shale, mixed lithology, tight & basin centred gas

resources well positioned to satisfy these demands

Excellence in Oil & Gas

4

60.%

80.%

100.%

120.%

140.%

160.%

180.%

200.%

220.%

240.%

260.%

01 Feb

11

03 Mar

11

04 Apr

11

05 May

11

06 Jun

11

06 Jul

11

05 Aug

11

06 Sep

11

06 Oct

11

07 Nov

11

07 Dec

11

09 Jan

12

08 Feb

12

09 Mar

12

%

DLS.ASX XEJ.ASX

Drillsearch Snapshot

Cooper Basin focus

Significant acreage position

Operator with high JV interests

Oil producer with significant new discoveries

New wet gas production

High leverage to liquids

Huge unconventional gas potential

Key Data

Share Price (20 March 2012) $1.44

Shares on Issue 337M

Market Cap $485M

Cash (31 December 2011) $33.7M

Debt Nil

2P Total Reserves 11.3 mmboe

2P + 2C Reserves and Resources 17.5 mmboe

Relative Performance DLS / ASX Energy 200

DLS

XEJ

Excellence in Oil & Gas

5 Three Growth Platforms

OIL

WET GAS

Short, medium and long-term growth opportunities

Oil

Wet Gas

Unconventional

Short, medium and long-term growth opportunities

Excellence in Oil & Gas

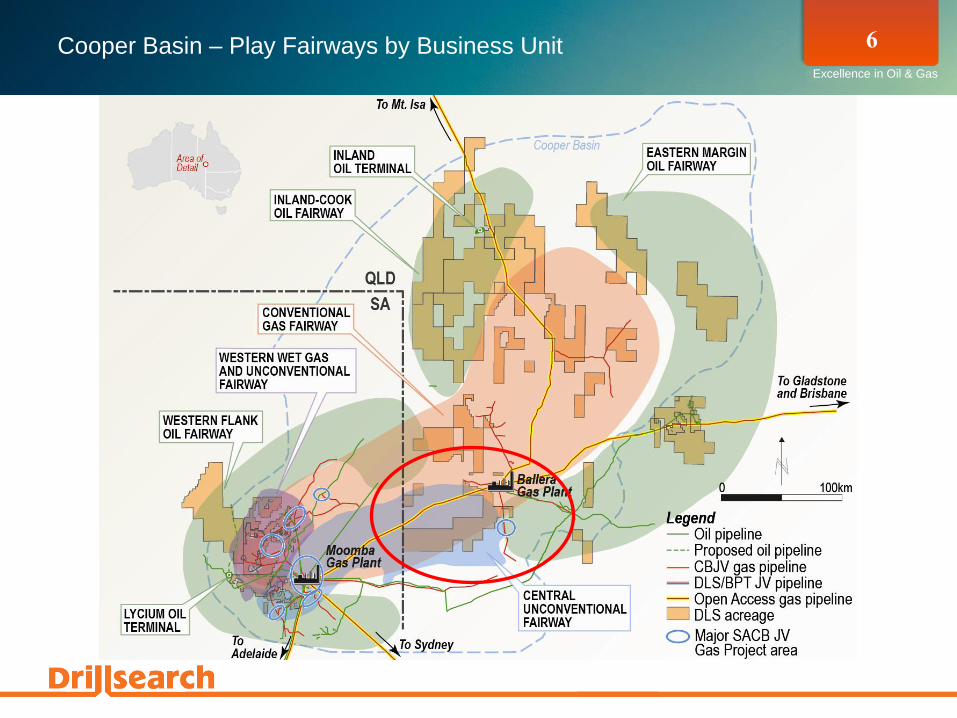

6 Cooper Basin – Play Fairways by Business Unit

OIL

WET GAS

UNCONVENTIONAL

Short, medium and long-term growth opportunities

Excellence in Oil & Gas

7 Comparative Cooper Basin Acreage Holdings

Source: GPinfo Petroleum Permits of Australia 2011, Company websites and Annual Reports

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

PGS COE BUL STX BPT DLS SXY STO

Non-Operated

Operated

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

PGS COE BUL STX BPT DLS SXY STO

KM

2

Cooper Basin Net AcreageCooper Basin Acreage

Excellence in Oil & Gas

8 Why focus on Cooper Basin Unconventional?

Underexplored & underexploited

Multiple conventional & unconventional plays

Production hub serving Eastern Australia

Established access to infrastructure

Minimal community impact

Seasonal cattle grazing not crops

ATP 940 Shale Gas Permit Area Oct 2011 Fiberspar installation PEL 106B Oct 2011

Excellence in Oil & Gas

9 Central Cooper Unconventional

Excellence in Oil & Gas

10 Drillsearch Unconventional Position – by play

Approx Top of Oil Window

Approx Top of Gas Window

Challum Gas Field

Moomba Gas Field

PEL 91 -106 -107-513 ATP 940P

REM Shale Gas Target

Patchawarra Formation

Basin-Centered, Tight Gas & Deep CSG

Excellence in Oil & Gas

11 Nappamerri Trough REM Shale Thickness

REM Shale remains thick across ATP 940P – providing a thick unconventional target zone

ATP 940P

Excellence in Oil & Gas

12 Nappamerri Trough – Near Top REM Shale Depth Map

REM Shale is shallower in ATP 940P – in a setting with more wet gas potential

ATP 940P

Excellence in Oil & Gas

13 REM – Indications of Wet Gas

Elevated Total Gas

(Red Shading) and

C4 Butane (Blue

Line) Wet Gas

reading in REM

Sequence

Two ATP 940P Near Offset Control Wells Displaying Elevated Gas Readings through the REM Sequence

Excellence in Oil & Gas

14 Our approach to Cooper Basin Unconventional

Drillsearch’s approach to unconventional based on 5 key principles:

Activity & investment targeted to “EAD Life Cycle”

Focus on activity to establish the 3 “P”s for the resource

The 3 “L”s – Look, Listen & Learn

Combine unconventional activities into conventional exploration and appraisal

“Measure twice, Cut once” - Use Best Available Technologies

Excellence in Oil & Gas

15 “Partnered to Perfection”

Commercialisation pathway

Improved access to technology & supply chain

Access to capital

Joint Venture alignment

Excellence in Oil & Gas

16 DLS-QGC Shale Gas Strategic Alliance - Exploration Program

Stage 1* Stage 2 Stage 3

$25m $33m $72m

Seismic

• 1,000km 2D seismic

reprocessing

• High resolution gravity

and aeromagnetic survey

• ~1,100km2 high resolution

3D seismic

Exploration drilling

• Two vertical exploration

wells

• Full coring program

• Fracture stimulation and

flow testing

Production pilot testing

• Four appraisal production

wells

- 2 vertical + 2 horizontal

• Fracture stimulation

• Production pilot

• Field development

decision (FDD)

FDD

2011 Jun 2013 Aug 2014 June 2016

* Stage 1 commences with the formal award of permit and registration of transfer to QGC

Excellence in Oil & Gas

17 Strategic Alliance Joint Venture Funding Mechanics

QGC reimburses DLS for up to $2.5m

of past costs – DLS Stage 1 spend

QGC funds 90% of first $100m of

agreed work program spend

DLS contributes 10% of each stage

subject to stage spending cap

Thereafter QGC and DLS will fund the

program on a 60/40 basis

QGC invests further $19.6m in DLS

through exercise of ~30 million options

Through QGC direct & indirect

investment DLS’ share of $130m multi-

year work program fully funded

$22.5m

$29.7m

$37.8m

$18.0m

$2.5m $3.3m $4.2m

$12.0m

Stage 1 Stage 2 Stage 3

carried

Stage 3

uncarried

Farm-in carry phase

DLS Cumulative Spend $2.5m $5.8m $10.0m $22.0m

Project Cumulative Spend $25.0m $58.0m $100.0m $130.0m

Excellence in Oil & Gas

18 Why QGC?

A global gas major

– QGC as part of the BG Group, brings relationships that facilitate commercialisation of

world class gas resources

Multiple gas commercialisation channels

– Currently developing the QCLNG development in Gladstone, QLD

– Major wholesale gas supplier to east coast gas markets, industrial and electricity

generation customers

Committed to Australia

– BG committed more than $15bn to Australia

Shale expertise

– Major positions in Marcellus and Haynesville shale and tight gas plays in North

America

– Access to unconventional technology and service supply chain

Excellence in Oil & Gas

19

60.%

80.%

100.%

120.%

140.%

160.%

180.%

200.%

220.%

240.%

260.%

01 Feb

11

03 Mar

11

04 Apr

11

05 May

11

06 Jun

11

06 Jul

11

05 Aug

11

06 Sep

11

06 Oct

11

07 Nov

11

07 Dec

11

09 Jan

12

08 Feb

12

09 Mar

12

%

DLS.ASX XEJ.ASX

Cooper Basin re-rating – Recognition of the Shale Gas Potential

Relative Performance DLS / ASX Energy 200

$48m Capital Raising

DLS

XEJ

Western Flank Oil Exploration

Campaign Commences

QGC Cooper Basin

Shale Gas JV

EIA International

Shale Assessment Wet Gas Project Gas Sales

Agreement with SACBJV

QGC Exercises Options

Wet Gas Production

Commences

Reserves Upgrade

Excellence in Oil & Gas

20 Key implications

Validates the potential of Cooper Basin shale gas by a global leader in gas

commercialisation

Multiple gas commercialisation channels - domestic and export

Access to expertise and technology - world leading technical service

providers

Earlier recognition of the value of DLS unconventional assets

Funding in place to accelerate and complete “EAD” - exploration,

appraisal and delineation

Well positioned to capitalise on robust outlook for domestic and export

natural gas markets

Excellence in Oil & Gas

21 Investment Proposition

Active EXPLORATION program

Growing OIL production

First WET GAS production

Huge UNCONVENTIONAL gas resource potential

FULLY FUNDED work program

Delivering GROWTH in reserves, production and cashflow

TRANSITIONING to significant oil and gas producer

Excellence in Oil & Gas

22 Disclaimer and Important Notice

• This presentation does not constitute investment advice. Neither this presentation nor the information contained in it constitutes

an offer, invitation, solicitation or recommendation in relation to the purchase or sale of shares in any jurisdiction.

• Shareholders should not rely on this presentation. This presentation does not take into account any person's particular

investment objectives, financial resources or other relevant circumstances and the opinions and recommendations in this

presentation are not intended to represent recommendations of particular investments to particular persons. All securities

transactions involve risks, which include (among others) the risk of adverse or unanticipated market, financial or political

developments.

• The information set out in this presentation does not purport to be all inclusive or to contain all the information which its recipients

may require in order to make an informed assessment of Drillsearch. You should conduct your own investigations and perform

your own analysis in order to satisfy yourself as to the accuracy and completeness of the information, statements and opinions

contained in this presentation.

• To the fullest extent permitted by law, the Company does not make any representation or warranty, express or implied, as to the

accuracy or completeness of any information, statements, opinions, estimates, forecasts or other representations contained in

this presentation. No responsibility for any errors or omissions from this presentation arising out of negligence or otherwise is

accepted.

• This presentation may include forward looking statements. Forward looking statements are only predictions and are subject to

risks, uncertainties and assumptions which are outside the control of Drillsearch. These risks, uncertainties and assumptions

include commodity prices, currency fluctuations, economic and financial market conditions in various countries and regions,

environmental risks and legislative, fiscal or regulatory developments, political risks, project delay or advancement, approvals

and cost estimates. Actual values, results or events may be materially different to those expressed or implied in this presentation.

Given these uncertainties, readers are cautioned not to place reliance on forward looking statements.

• Any forward looking statements in this presentation speak only at the date of issue of this presentation. Subject to any continuing

obligations under applicable law and the ASX Listing Rules, Drillsearch does not undertake any obligation to update or revise any

information or any of the forward looking statements in this presentation or any changes in events, conditions or circumstances

on which any such forward looking statement is based.

• The Reserves and Resources assessment follows guidelines set forth by the Society of Petroleum Engineers - Petroleum

Resource Management System (SPE-PRMS). The Reserves estimates used in this presentation were compiled by Mr David

Evans, Chief Technical Officer of Drillsearch Energy Ltd, who is a qualified person as defined under ASX Listing Rule 5.11 and

has consented to the use of the Reserves figures in the form and context in which they appear in this presentation.