a primer on microfinance - upati.gov.inupati.gov.in/mediagallery/microfoinance primer - to...

TRANSCRIPT

A Primer on MicrofinanceA Primer on Microfinance

U. B. DesaiU. B. Desai

SPANN Lab.SPANN Lab.

Dept. of EEDept. of EE

IITIIT--BombayBombay

www.ee.iitb.ac.in/~ubdesaiwww.ee.iitb.ac.in/~ubdesai

Oct 2008 2IT 625: ICT4SED

Some Basic QuestionSome Basic Question

�� Why do we need finance?Why do we need finance?

�� Why the special need for finance for the Why the special need for finance for the

underserved communities?underserved communities?

�� Why do poor still go to unorganized financial Why do poor still go to unorganized financial

institutions (money lenders, institutions (money lenders, shaukarsshaukars, ...)?, ...)?

Oct 2008 3IT 625: ICT4SED

�� Why is the spread of microfinance so Why is the spread of microfinance so

slow?slow?

�� Why are commercial banks hesitant to Why are commercial banks hesitant to

enter microfinance?enter microfinance?

Oct 2008 4IT 625: ICT4SED

Some Basic QuestionSome Basic Question

�� Why do we need finance?Why do we need finance?� credit is an instrument for investment and growth.

�� Why the special need for finance for the underserved communitiesWhy the special need for finance for the underserved communities??�� Same as aboveSame as above

�� Shift in Perspective: From poverty alleviation to wealth generatShift in Perspective: From poverty alleviation to wealth generation ion ------microfinance will enable wealth generationmicrofinance will enable wealth generation

�� Why do poor still go to unorganized financial institutions (moneWhy do poor still go to unorganized financial institutions (money y lenders, lenders, shaukarsshaukars, ...)?, ...)?�� We will look at this during the talkWe will look at this during the talk

�� Why is the spread of microfinance so slow?Why is the spread of microfinance so slow?�� Commercial financial institutions are not ready to enter this arCommercial financial institutions are not ready to enter this arenaena

�� Why are commercial banks hesitant to enter microfinance?Why are commercial banks hesitant to enter microfinance?�� We will explore this in the talkWe will explore this in the talk

Oct 2008 5IT 625: ICT4SED

General BeliefGeneral Belief

�� Poor are too difficult to reach.Poor are too difficult to reach.

�� Small loans to poor is not a financially Small loans to poor is not a financially

viable propositionviable proposition

�� Financial institutions will loose money Financial institutions will loose money

when they give when they give microcreditmicrocredit to the poorto the poor

�� MicrocreditMicrocredit or or microloansmicroloans will only increase will only increase

the debt burden for the poorthe debt burden for the poor

Do you agree? What is your opinion?Do you agree? What is your opinion?

Oct 2008 6IT 625: ICT4SED

Microfinance (Microfinance (mFImFI))

�� A clever scheme for A clever scheme for smallsmall--savings and smallsavings and small--loan for the underserved loan for the underserved community community

�� A financial service for the A financial service for the poorpoor

�� A financial approach A financial approach empowering the poorempowering the poor

�� Microfinance brings in Microfinance brings in incremental changesincremental changes�� It does not bring in It does not bring in dramatic changes like the dramatic changes like the ones that occur when a ones that occur when a company goes in for an company goes in for an IPOIPO

�� Microfinance may also be Microfinance may also be considered a tool to give considered a tool to give poor people the poor people the opportunity to participate opportunity to participate fully in economic lifefully in economic life

�� Will improve the village Will improve the village economy economy �� Facilitate increase in cash Facilitate increase in cash flowflow

�� Bring more villages into the Bring more villages into the market; monetize more market; monetize more villages villages

�� Help generate trade thru Help generate trade thru micromicro--enterprisesenterprises

Oct 2008 7IT 625: ICT4SED

Microfinance: Interplay Among ..Microfinance: Interplay Among ..

�� Institutions:Institutions:�� Access points for the poor to get financial services Access points for the poor to get financial services

(e.g. SEWA, (e.g. SEWA, GrameenGrameen Bank, etc.)Bank, etc.)

�� These could be bank branches (could be virtual These could be bank branches (could be virtual

branches), socially oriented financial institutions, or a branches), socially oriented financial institutions, or a

partnership between the two partnership between the two

�� Funding Sources:Funding Sources: Domestic savings (~70%), Domestic savings (~70%),

““private socially responsible citizensprivate socially responsible citizens”” (~30%) (~30%)

�� Infrastructure:Infrastructure: Here ICT can play a major role Here ICT can play a major role

Oct 2008 8IT 625: ICT4SED

Unorganized Unorganized mFImFI Institutions (Institutions (mFImFI))

�� Exorbitant interest rates Exorbitant interest rates

�� On the low end 3% per month On the low end 3% per month (36% per annum) (36% per annum)

�� can be much morecan be much more

�� Often collateral, like cattle, Often collateral, like cattle, jewelry, etc not returnedjewelry, etc not returned

�� Often the poor get into a debt Often the poor get into a debt cycle for life!cycle for life!

� UmFI does not give loans for sustainability (for e.g. starting a micro-enterprise!)

�� Still the poor approach Still the poor approach UmFIUmFI -------- Why?Why?

�� Always available (always on!)Always available (always on!)

�� You get it when you really You get it when you really need it need it

�� Quick disbursementQuick disbursement

�� Negligible transaction timeNegligible transaction time

�� Poor go for microPoor go for micro--loans just loans just before they really need itbefore they really need it

�� Loans without collateralLoans without collateral

�� Dependence of lowDependence of low--income income households on informal households on informal sources for loans is nearly 78 sources for loans is nearly 78 per cent.per cent.

The poor not only has low income but irregular cycle of paymentsand withdrawals. The informal financial institutions (money lenders) satisfy this need to the tee

Oct 2008 9IT 625: ICT4SED

UmFIUmFI: Case of : Case of SolapurSolapur DistrictDistrict

�� Collateral based lendingCollateral based lending�� Gold is typically the collateralGold is typically the collateral

�� Borrowers: small time office Borrowers: small time office clerks, peons, clerks, peons, …… people who people who have permanent jobshave permanent jobs

�� Collateral amount is 1.5 times Collateral amount is 1.5 times the loan valuethe loan value

�� Loans taken for illness, family Loans taken for illness, family function, etc. function, etc.

�� Interest is 3% per monthInterest is 3% per month

�� Default rate 80% Default rate 80% ---- most of most of the time gold is confiscated the time gold is confiscated

�� About 100 lenders each About 100 lenders each lending about a Rs.10 lending about a Rs.10 lakhslakhs; ; totaling totaling Rs.10 Rs.10 crscrs..

�� Lending without collateralLending without collateral�� Interest rates are around 3% Interest rates are around 3% per monthper month

�� Repayment is on a daily basisRepayment is on a daily basis

�� Hawker, vegetable vendors will Hawker, vegetable vendors will go for such loansgo for such loans

�� Often, most of the income Often, most of the income goes in loan paymentgoes in loan payment

�� About 200 to 300 lenders in About 200 to 300 lenders in this categorythis category

�� Each loaning about 5 to 10 Each loaning about 5 to 10 lakhslakhs

�� Totaling about Totaling about 20 20 crscrs

Oct 2008 10IT 625: ICT4SED

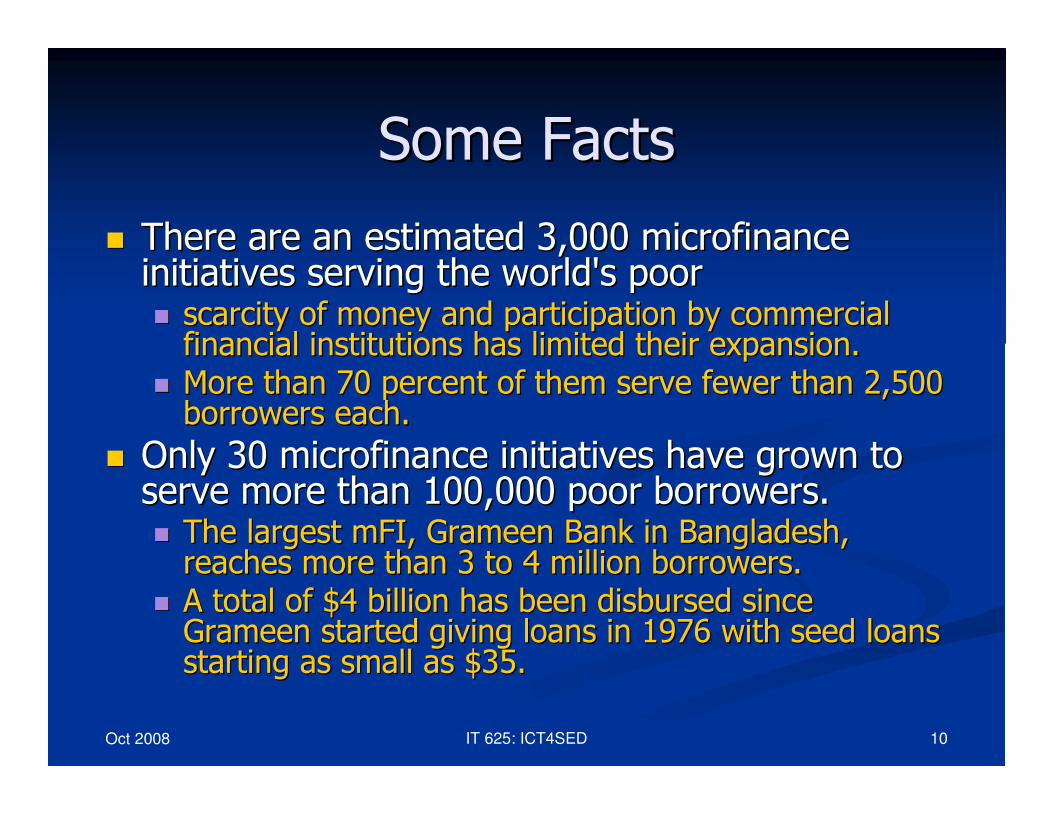

Some FactsSome Facts

�� There are an estimated 3,000 microfinance There are an estimated 3,000 microfinance initiatives serving the world's poor initiatives serving the world's poor �� scarcity of money and participation by commercial scarcity of money and participation by commercial financial institutions has limited their expansion. financial institutions has limited their expansion.

�� More than 70 percent of them serve fewer than 2,500 More than 70 percent of them serve fewer than 2,500 borrowers each.borrowers each.

�� Only 30 microfinance initiatives have grown to Only 30 microfinance initiatives have grown to serve more than 100,000 poor borrowers. serve more than 100,000 poor borrowers. �� The largest The largest mFImFI, , GrameenGrameen Bank in Bangladesh, Bank in Bangladesh, reaches more than 3 to 4 million borrowers. reaches more than 3 to 4 million borrowers.

�� A total of $4 billion has been disbursed since A total of $4 billion has been disbursed since GrameenGrameen started giving loans in 1976 with seed loans started giving loans in 1976 with seed loans starting as small as $35.starting as small as $35.

Oct 2008 11IT 625: ICT4SED

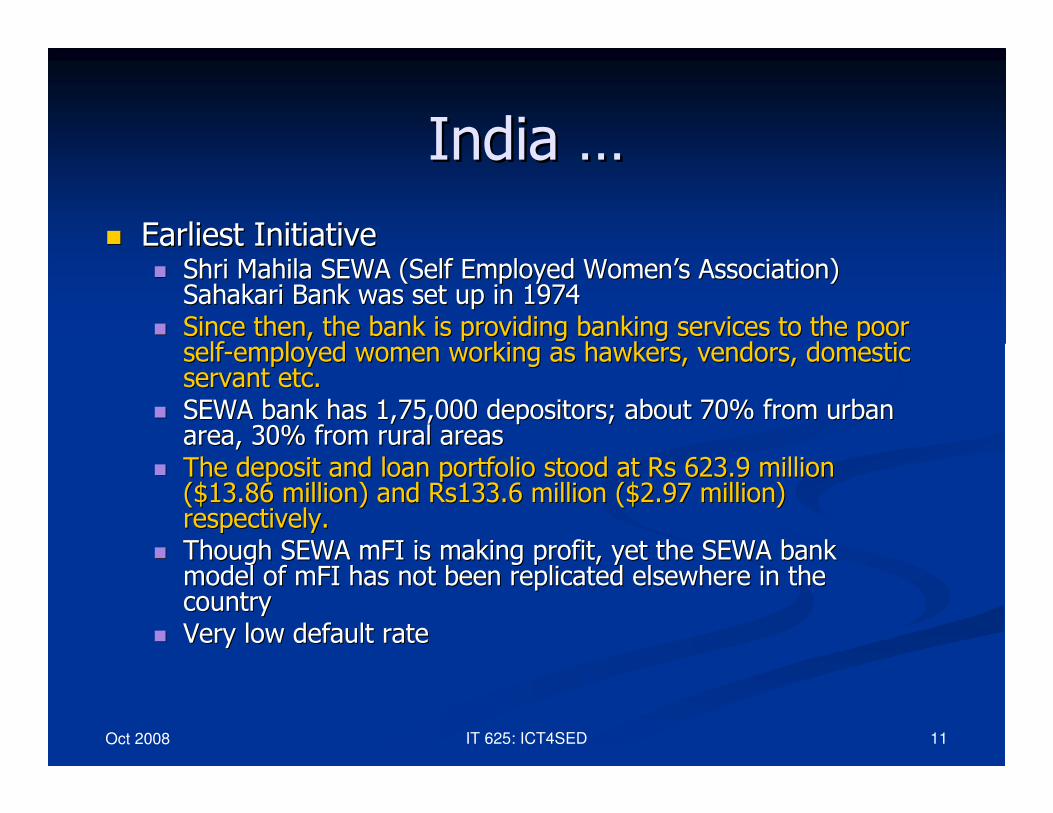

India India ……

�� Earliest InitiativeEarliest Initiative�� ShriShri MahilaMahila SEWA (Self Employed WomenSEWA (Self Employed Women’’s Association) s Association) SahakariSahakari Bank was set up in 1974Bank was set up in 1974

�� Since then, the bank is providing banking services to the poor Since then, the bank is providing banking services to the poor selfself--employed women working as hawkers, vendors, domestic employed women working as hawkers, vendors, domestic servant etc. servant etc.

�� SEWA bank has 1,75,000 depositors; about 70% from urban SEWA bank has 1,75,000 depositors; about 70% from urban area, 30% from rural areasarea, 30% from rural areas

�� The deposit and loan portfolio stood at The deposit and loan portfolio stood at RsRs 623.9 million 623.9 million ($13.86 million) and Rs133.6 million ($2.97 million) ($13.86 million) and Rs133.6 million ($2.97 million) respectively. respectively.

�� Though SEWA Though SEWA mFImFI is making profit, yet the SEWA bank is making profit, yet the SEWA bank model of model of mFImFI has not been replicated elsewhere in the has not been replicated elsewhere in the countrycountry

�� Very low default rateVery low default rate

Oct 2008 12IT 625: ICT4SED

India India ……

�� Today, there are about 60,000 Today, there are about 60,000 retail credit outlets of the retail credit outlets of the formal banking sector in the formal banking sector in the rural areas comprisingrural areas comprising�� 12,000 branches of district 12,000 branches of district level cooperative bankslevel cooperative banks

�� over 14,000 branches of the over 14,000 branches of the Regional Rural Banks (Regional Rural Banks (RRBsRRBs) )

�� over 30,000 rural and semiover 30,000 rural and semi--urban branches of commercial urban branches of commercial banksbanks

�� besides almost 90,000 besides almost 90,000 cooperatives credit societies at cooperatives credit societies at the village levelthe village level

�� On an average, there is at On an average, there is at least one retail credit outlet for least one retail credit outlet for about 5,000 rural peopleabout 5,000 rural people

�� While there is no published While there is no published data on private data on private mFIsmFIs operating operating in India, in India, �� the number of the number of mFIsmFIs is is estimated to be around 800.estimated to be around 800.

�� Not more than 10 Not more than 10 mFIsmFIs are are reported to have an outreach reported to have an outreach of 100,000 microfinance of 100,000 microfinance clients. clients.

�� An overwhelming majority of An overwhelming majority of mFIsmFIs are operating on a are operating on a smaller scale with clients smaller scale with clients ranging between 500 to 1500 ranging between 500 to 1500 per per mFImFI. .

Oct 2008 13IT 625: ICT4SED

Target Populace for Target Populace for muFmuF

�� Rural Poor WomenRural Poor Women

�� Asset value less than Asset value less than RsRs. 20,000/. 20,000/--

�� Per capita income is less than Per capita income is less than RsRs. 350/. 350/--

per month per month

�� Live in poor housing conditionsLive in poor housing conditions

(from SHARE Microfinance Ltd.)(from SHARE Microfinance Ltd.)

Oct 2008 14IT 625: ICT4SED

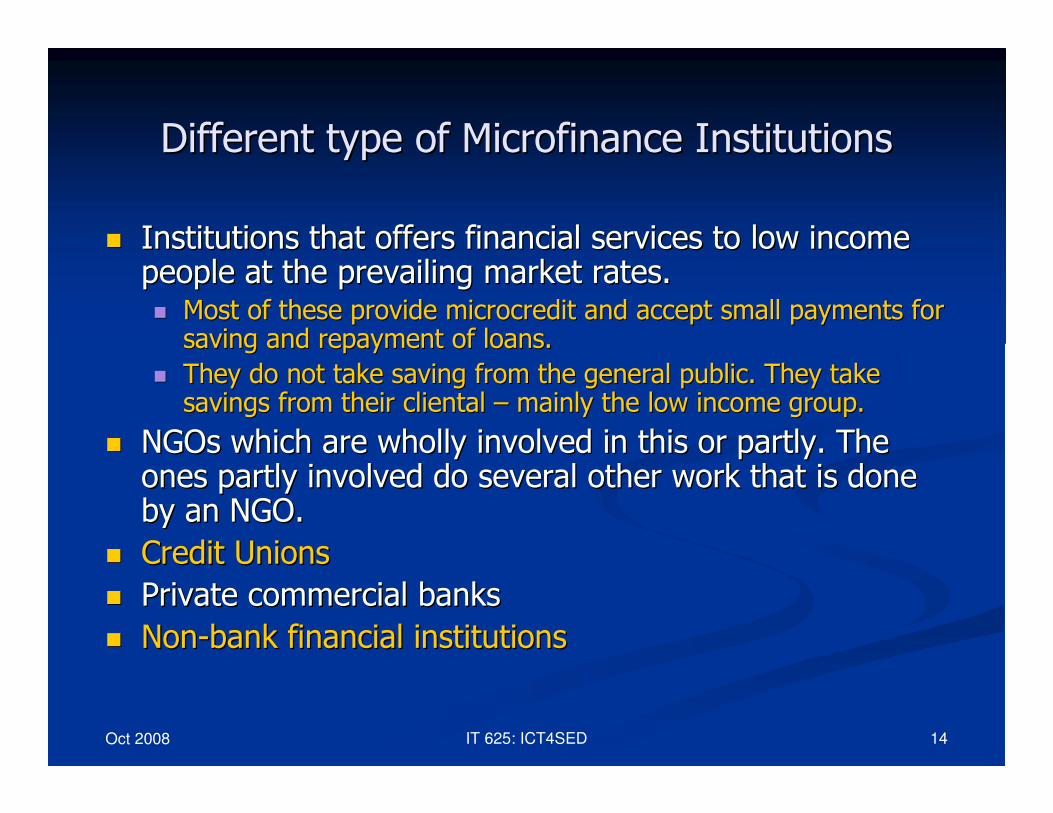

Different type of Microfinance InstitutionsDifferent type of Microfinance Institutions

�� Institutions that offers financial services to low income Institutions that offers financial services to low income people at the prevailing market rates. people at the prevailing market rates. �� Most of these provide Most of these provide microcreditmicrocredit and accept small payments for and accept small payments for saving and repayment of loans. saving and repayment of loans.

�� They do not take saving from the general public. They take They do not take saving from the general public. They take savings from their cliental savings from their cliental –– mainly the low income group.mainly the low income group.

�� NGOs which are wholly involved in this or partly. The NGOs which are wholly involved in this or partly. The ones partly involved do several other work that is done ones partly involved do several other work that is done by an NGO.by an NGO.

�� Credit UnionsCredit Unions

�� Private commercial banksPrivate commercial banks

�� NonNon--bank financial institutionsbank financial institutions

Oct 2008 15IT 625: ICT4SED

�� Often one classifies financial institutions like Often one classifies financial institutions like

�� National Bank for Agriculture and Rural Development National Bank for Agriculture and Rural Development

(NABARD)(NABARD)

�� Small Industries Development Bank of India (SIDBI)Small Industries Development Bank of India (SIDBI)

�� RashtriyaRashtriya MahilaMahila KoshKosh (RMK) (RMK)

as as mFIsmFIs;;

�� But, I feel ,they do not fit the bill, because they But, I feel ,they do not fit the bill, because they

do not cater to the kind of income talked about do not cater to the kind of income talked about

earlier earlier

Oct 2008 16IT 625: ICT4SED

Appropriateness of mFAppropriateness of mF

�� mF works best for those who have identified an mF works best for those who have identified an opportunity and the credit can be used to exploit opportunity and the credit can be used to exploit this opportunity to develop a sustainable source this opportunity to develop a sustainable source of income.of income.

�� Microfinance is not appropriate for Microfinance is not appropriate for �� Extremely poor, Extremely poor, destitutesdestitutes

�� There has to be some viable way of microThere has to be some viable way of micro--loan loan repaymentrepayment

�� People who are extremely poor may get into debt People who are extremely poor may get into debt trap with microfinancetrap with microfinance

�� Numbers vary, but some feel that one has to have Numbers vary, but some feel that one has to have 98% loan repayments rate for an MFI to succeed.98% loan repayments rate for an MFI to succeed.

Oct 2008 17IT 625: ICT4SED

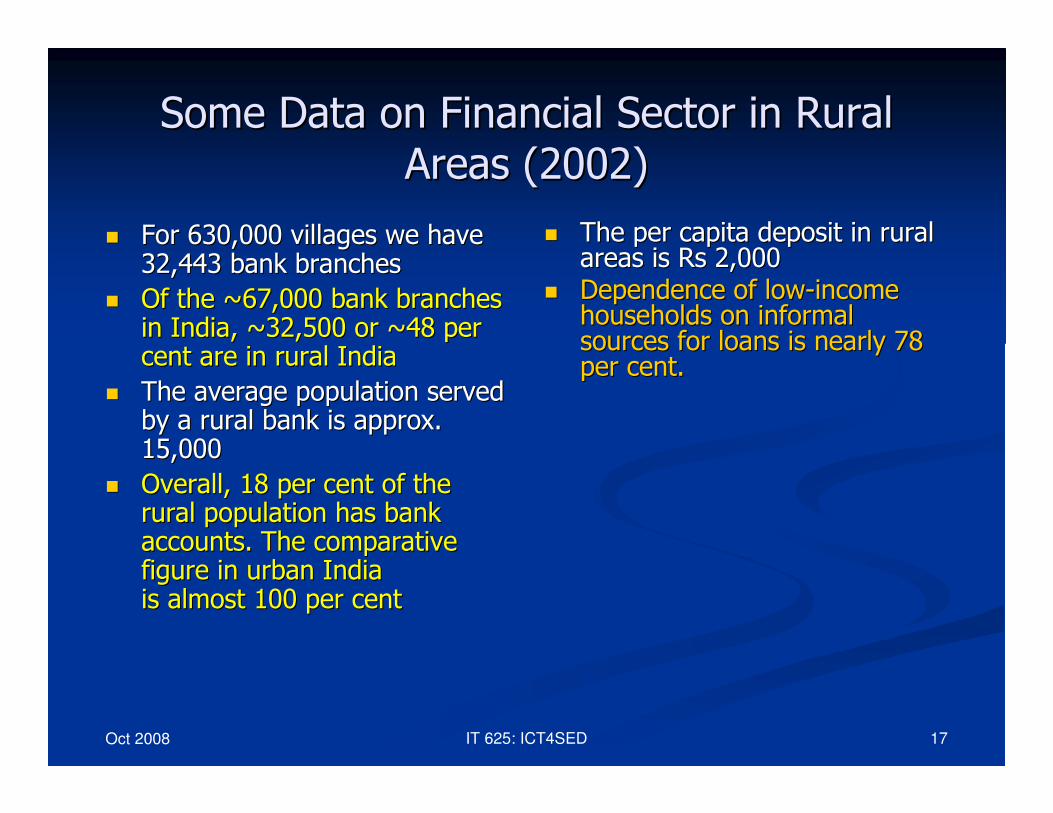

Some Data on Financial Sector in Rural Some Data on Financial Sector in Rural

Areas (2002)Areas (2002)

�� For 630,000 villages we have For 630,000 villages we have 32,443 bank branches32,443 bank branches

�� Of the ~67,000 bank branches Of the ~67,000 bank branches in India, ~32,500 or ~48 per in India, ~32,500 or ~48 per cent are in rural Indiacent are in rural India

�� The average population served The average population served by a rural bank is approx. by a rural bank is approx. 15,00015,000

�� Overall, 18 per cent of the Overall, 18 per cent of the rural population has bank rural population has bank accounts. The comparative accounts. The comparative figure in urban Indiafigure in urban Indiais almost 100 per centis almost 100 per cent

�� The per capita deposit in rural The per capita deposit in rural areas is areas is RsRs 2,0002,000

�� Dependence of lowDependence of low--income income households on informal households on informal sources for loans is nearly 78 sources for loans is nearly 78 per cent.per cent.

Oct 2008 18IT 625: ICT4SED

Share of Different Sectors in GDP(GDP at factor cost, 1993-94 Prices)Rs. In crores

-- RBI, Handbook of Statistics on the Indian Economy

56%1320733739842 288266 292625 2002-03

55%1265429 691016272359 302054 2001-02

54%1198685 649011 263797 285877 2000-01

46%692871319374 150383223114 1990-91

43%401128171148 70687159293 1980-81

38%296278113438 46151 137320 1970-71

Services%TotalServices

IndustryAgri.

Oct 2008 19IT 625: ICT4SED

Breakup of Indian GDPBreakup of Indian GDP

�� GDP for India: $1000 billionGDP for India: $1000 billion�� 1212thth largest in the wordlargest in the word

�� Approx. 4000 billion base Approx. 4000 billion base dpndpn PPPPPP

�� Rural GDP: ~$250 billion (25%)Rural GDP: ~$250 billion (25%)

56%

22%

22%

Compare this with IT industry, which is~ $ 20 billion

Oct 2008 20IT 625: ICT4SED

Credit to Deposit (CD) Ratio for banks in India

• Rural CD ratio needs to brought upto 60%• Low CD ~ a lot of cash is idling, or cash collected in rural areas is used

to give credit to urban areas

Oct 2008 21IT 625: ICT4SED

Different Financial Services under Different Financial Services under

MicrofinanceMicrofinance

�� Deposit services Deposit services

�� Credit linesCredit lines

�� Term loansTerm loans

�� Money transfers Money transfers

�� MicroMicro--Crop and life insuranceCrop and life insurance

�� Micro health insuranceMicro health insurance

Oct 2008 22IT 625: ICT4SED

Innovation in MicrofinanceInnovation in Microfinance

�� Development of finance products for the Development of finance products for the underserved underserved

�� Management of credit risk (minimization Management of credit risk (minimization losses in giving credit)losses in giving credit)

�� Scalability: how to reach a vast, diverse, Scalability: how to reach a vast, diverse, not easy to reach and geographically not easy to reach and geographically scattered populacescattered populace

�� Efficient delivery of Efficient delivery of microcreditmicrocredit�� exploit technologyexploit technology

Oct 2008 23IT 625: ICT4SED

Gautum Ivatury:Focus Notes, Jan 2006, CGAP(Consultative Group toAssists the Poor)www.cgap.org

Oct 2008 24IT 625: ICT4SED

MicrocreditMicrocredit

�� Delivery Delivery of of microcreditmicrocredit has to be done more and has to be done more and more efficiently more efficiently �� Here ICT can play a major roleHere ICT can play a major role

�� Determination of a borrower's Determination of a borrower's willingnesswillingness and and abilityability to repay a loan is critical if a to repay a loan is critical if a microlendermicrolenderis to minimize credit risk is to minimize credit risk �� WillingnessWillingness to repay a loan are complex and to repay a loan are complex and determined by economic, legal and moral incentivesdetermined by economic, legal and moral incentives�� Legal systems and Legal systems and community pressure (for rural areas)community pressure (for rural areas)contribute to a borrower's contribute to a borrower's willingnesswillingness to repay a loan to repay a loan

�� Ability Ability refers to a borrower having the financial refers to a borrower having the financial resources to make a scheduled loan payment. resources to make a scheduled loan payment.

Oct 2008 25IT 625: ICT4SED

�� Three operational areas on which a Three operational areas on which a

microlendermicrolender should focus to minimize should focus to minimize

credit risk:credit risk:

�� loan design loan design

�� underwriting underwriting

�� loan servicing loan servicing

Oct 2008 26IT 625: ICT4SED

MicroMicro--Loan DesignLoan Design

�� Balance between affordability needs of borrowers and Balance between affordability needs of borrowers and costs to microcosts to micro--lenders lenders �� Revolves on the design of Revolves on the design of interest rates (interest rates (must cover operating must cover operating costs, credit risk and funding costs)costs, credit risk and funding costs)

�� Interest are very critical to microfinance institutionInterest are very critical to microfinance institution�� mFImFI interest are not very low at presentinterest are not very low at present

�� 15% to 36% per annum (SEWA charges 15% to 18%)15% to 36% per annum (SEWA charges 15% to 18%)

�� Note: RBI interest ceiling is 21%Note: RBI interest ceiling is 21%

�� On the other hand, for rural poor, it has been observed On the other hand, for rural poor, it has been observed that the amount of monthly payment is much more that the amount of monthly payment is much more important than interestimportant than interest�� As long as they are comfortable with the scheduled payment As long as they are comfortable with the scheduled payment amount they do not worry too much about interest ratesamount they do not worry too much about interest rates

Oct 2008 27IT 625: ICT4SED

MicroMicro--loan Underwriting loan Underwriting

�� The process of determining a borrower's The process of determining a borrower's

credit worthinesscredit worthiness

�� abilityability and and willingnesswillingness to repay a loan to repay a loan

�� Most important from the Most important from the microlendermicrolender’’ss

point of viewpoint of view

Oct 2008 28IT 625: ICT4SED

MicroMicro--Loan ServicingLoan Servicing

�� Loan servicing is the act of collecting payments and maintainingLoan servicing is the act of collecting payments and maintaining the the balance of a loan balance of a loan �� In commercial banking, loan payments are made by bank draft or bIn commercial banking, loan payments are made by bank draft or by y directly debiting payroll or a bank account.directly debiting payroll or a bank account.

�� Things are not easy in the world of microfinance.Things are not easy in the world of microfinance.�� The typical borrower does not have access to a bank account and The typical borrower does not have access to a bank account and often often does not receive a formal salary. does not receive a formal salary.

�� This means that for many customers of This means that for many customers of microlendersmicrolenders making loan making loan payments can be difficult and put them in the position of makingpayments can be difficult and put them in the position of making the the choice to take time off from work (and possibly get fired) in orchoice to take time off from work (and possibly get fired) in order to der to deliver a loan payment or choose not to make a payment. deliver a loan payment or choose not to make a payment.

�� Successful lenders will set up payment kiosks in communities. ThSuccessful lenders will set up payment kiosks in communities. The e kiosks are typically open before the typical work day starts andkiosks are typically open before the typical work day starts and after it after it ends.ends.

�� Another effective method, albeit more labor intensive is doorAnother effective method, albeit more labor intensive is door--toto--door door collections. collections.

Oct 2008 29IT 625: ICT4SED

MicroMicro--Loan Servicing Loan Servicing ……

�� Provide positive incentives for payment.Provide positive incentives for payment.�� Borrowers respond well to positive incentives for good payment Borrowers respond well to positive incentives for good payment history.history.

�� MicrolendersMicrolenders and mortgage lenders have successfully used and mortgage lenders have successfully used incentives such as payment rebates, small appliances and food incentives such as payment rebates, small appliances and food to achieve very high levels of repayment. to achieve very high levels of repayment.

�� For example, one Mexican lender offered a free bag of corn meal For example, one Mexican lender offered a free bag of corn meal if a borrower made timely payments for six months. The result if a borrower made timely payments for six months. The result was a delinquency rate of less than 1%was a delinquency rate of less than 1%

�� Be proactive in dealing with delinquencies.Be proactive in dealing with delinquencies.�� Rather than wait until a loan goes into default, a Rather than wait until a loan goes into default, a microlendermicrolendershould investigate a loan within weeks of it first becoming should investigate a loan within weeks of it first becoming delinquent.delinquent.

�� Often, the cause of a delinquency is due to illness or Often, the cause of a delinquency is due to illness or unemployment. unemployment.

�� If caught early enough a lender can give the borrower If caught early enough a lender can give the borrower assistance as well as workout a equitable repayment plan. assistance as well as workout a equitable repayment plan.

Oct 2008 30IT 625: ICT4SED

ChallengesChallenges

�� Establishing the idea of Establishing the idea of access to financial services as access to financial services as human right; human right; just like health care, education etc. are just like health care, education etc. are basic rights (Mathew Bishop, Business Editor of The basic rights (Mathew Bishop, Business Editor of The Economist)Economist)

�� Managing credit risks in Managing credit risks in microlendingmicrolending operationsoperations�� Convincing, for profit organizations like established Convincing, for profit organizations like established banks, nonbanks, non--bank financial institutions, that microfinance bank financial institutions, that microfinance is a good business opportunity and they should commit is a good business opportunity and they should commit large capital to establish this business.large capital to establish this business.�� Also convincing them that charity (funds donated by established Also convincing them that charity (funds donated by established organization) is not a sustainable way for growthorganization) is not a sustainable way for growth

�� Developing a market driven interest rate schedule for Developing a market driven interest rate schedule for the poorthe poor

Oct 2008 31IT 625: ICT4SED

Challenges Challenges ……

�� Reaching people in sparsely populated, diverse, not easy to reacReaching people in sparsely populated, diverse, not easy to reach, h, and geographically scattered areasand geographically scattered areas�� Last mile problem of reaching the rural poor.Last mile problem of reaching the rural poor.

�� Most important challenge is to exploit technology to reduce Most important challenge is to exploit technology to reduce transaction costs so that financial institutions will indeed taktransaction costs so that financial institutions will indeed take up e up microfinance as one of their major service. microfinance as one of their major service.

�� Reaching the poorest of the poor Reaching the poorest of the poor –– the destitute:the destitute:�� Many ignore this segmentMany ignore this segment

�� Very difficult for a commercial institution to recover microVery difficult for a commercial institution to recover micro--credit given credit given to this segmentto this segment

�� Here Government will have to step n develop a scheme for microHere Government will have to step n develop a scheme for micro--grantsgrants

�� Make microfinance part of main stream financial marketMake microfinance part of main stream financial market

�� Data Collection Data Collection –– need to collect data that can indicate need to collect data that can indicate

Oct 2008 32IT 625: ICT4SED

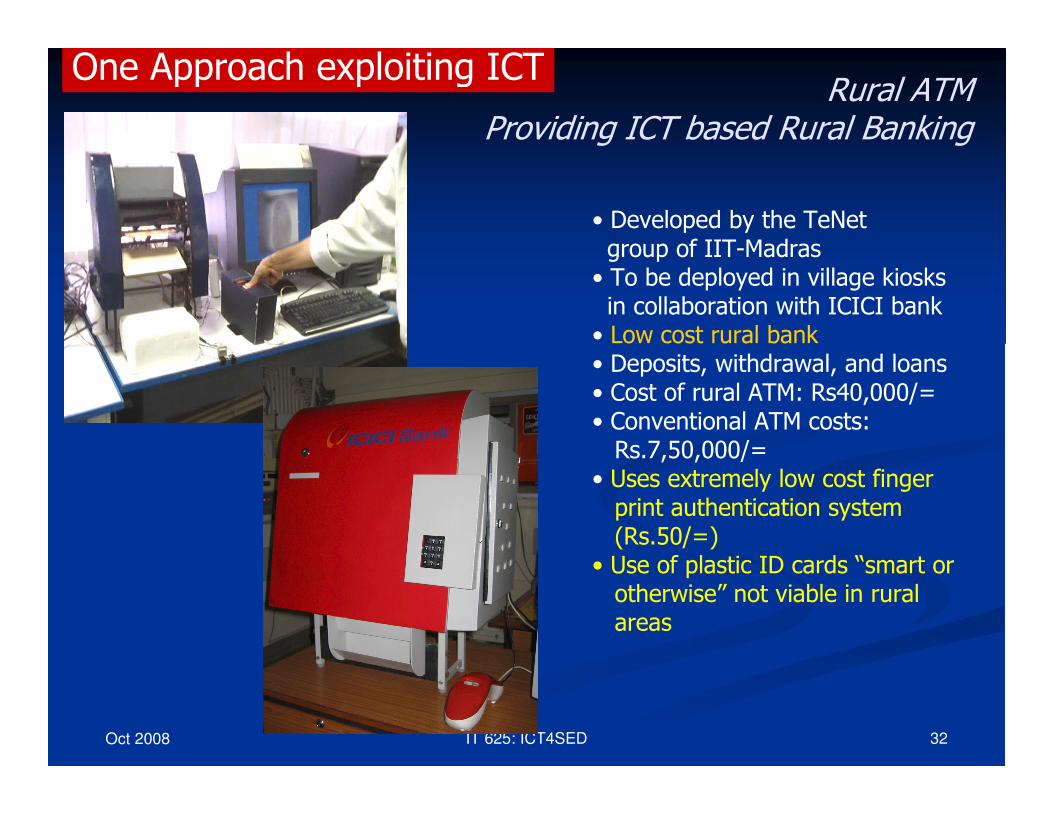

Rural ATM Providing ICT based Rural Banking

• Developed by the TeNetgroup of IIT-Madras• To be deployed in village kiosksin collaboration with ICICI bank• Low cost rural bank• Deposits, withdrawal, and loans• Cost of rural ATM: Rs40,000/=• Conventional ATM costs: Rs.7,50,000/=

• Uses extremely low cost finger print authentication system (Rs.50/=)

• Use of plastic ID cards “smart or otherwise” not viable in rural areas

One Approach exploiting ICT

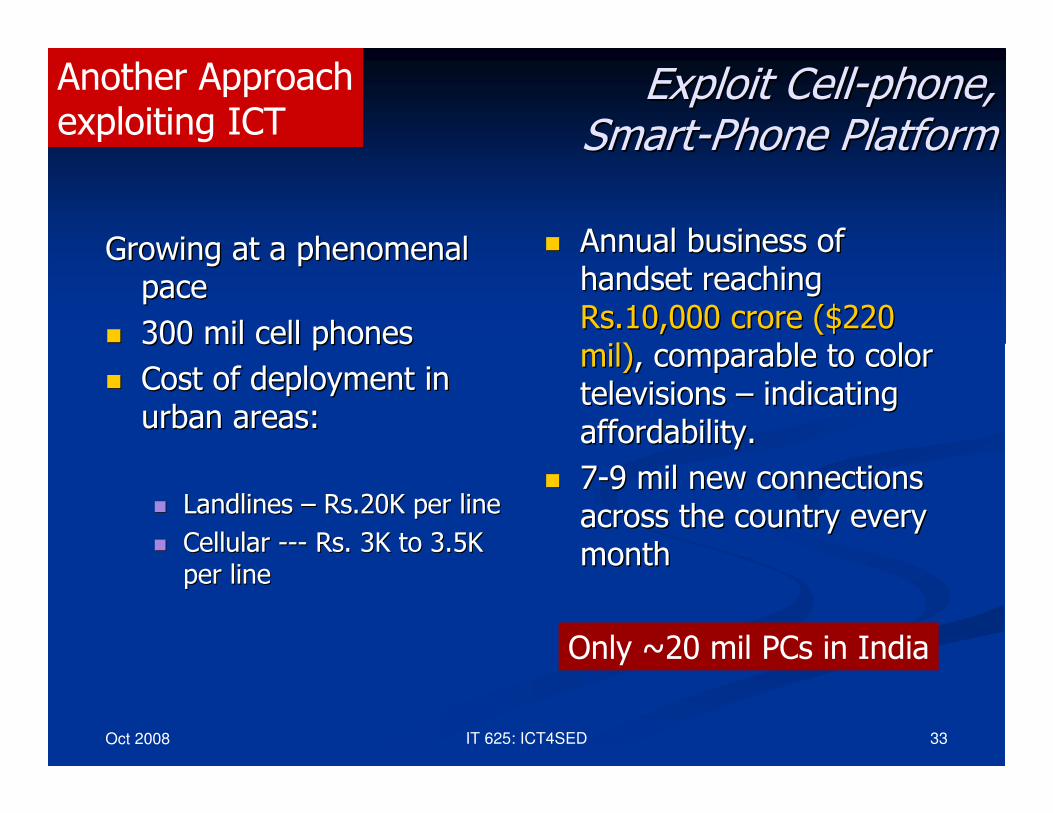

Oct 2008 33IT 625: ICT4SED

Exploit CellExploit Cell--phone, phone, SmartSmart--Phone PlatformPhone Platform

Growing at a phenomenal Growing at a phenomenal

pacepace

�� 300 mil cell phones300 mil cell phones

�� Cost of deployment in Cost of deployment in

urban areas: urban areas:

�� Landlines Landlines –– Rs.20K per lineRs.20K per line

�� Cellular Cellular ------ RsRs. 3K to 3.5K . 3K to 3.5K

per lineper line

�� Annual business of Annual business of

handset reaching handset reaching

Rs.10,000 Rs.10,000 crorecrore ($220 ($220

mil)mil), comparable to color , comparable to color

televisions televisions –– indicating indicating

affordability. affordability.

�� 77--9 mil new connections 9 mil new connections

across the country every across the country every

monthmonth

Only ~20 mil PCs in India

Another Approachexploiting ICT

Oct 2008 34IT 625: ICT4SED

Microfinance is a necessary input Microfinance is a necessary input

for rural wealth generationfor rural wealth generation

but by no means sufficientbut by no means sufficient

Oct 2008 35IT 625: ICT4SED