a bond notes/cf ch7.pdf · 2014-10-24 · bond pricing theorems 1.bond prices and market interest...

TRANSCRIPT

1

1

Chapter 7Interest Rates and Bond Valuation

Chapter Organization7.1. Bonds and Bond Valuation7.2. More on Bond Features7.3. Bond Ratings7.4. Some Different Types of Bonds7.5. Bond Markets7.6. Inflation and Interest Rates7.7. Determinants of Bond Rates

2

7.1. Bonds and Bond Valuation

A bond is normally an interest-only loan, meaning that the borrower will pay the interest every period, but none of the principal will be repaid until the end of the loan.

3

7.1. Bonds and Bond Valuation0 1 2 3 4 5 29 30

120 120 120 120 120 ......... 120 120

1.000

The 120 regular interest payments are called the bond’s coupons.

The principal amount that will be repaid at the end of the loan is called the bond’s face value or par value.

The number of years until the face value is paid is called the bond’s time to maturity

4

7.1. Bonds and Bond Valuation

The interest rate required in the market on a bond is called the bond’s yield to maturity (YTM). This rate is called the bond’s yieldfor short.

The interest changes in the marketplace. The cash flow from a bond stays the same. As a result, the value of the bond will fluctuate.

2

5

7.1. Bonds and Bond Valuation

Suppose the X Co. were to issue a bond with 10 years to maturity. The X bond has an annual coupon of 80. Similar bonds have a yield to maturity of 8 %.

0 1 2 3 4 5 6 7 8 9 10

80 80 80 80 80 80 80 80 80 80

1.000

6

7.1. Bonds and Bond Valuation

Present value = 1.000 / 1,0810 = = 1.000 / 2,1589 = 463,19

Annuity present value = = 80 x (1- 1/1,0810) / 0,08 =

= 80 x (1- 1 / 2,1589) / 0,08 = = 80 x 6,7101 = 536,81

Total bond value = 463,19 + 536,81 = 1.000

7

7.1. Bonds and Bond Valuation

Suppose that a year has gone by. The X bond now has nine years to maturity. If the interest rate in the market has risen to 10%, what will the bond be worth?

0 1 2 3 4 5 6 7 8 9 10

80 80 80 80 80 80 80 80 80

1.000

8

7.1. Bonds and Bond Valuation

Present value = 1.000 / 1,109 = = 1000 / 2,3579 = 424,10

Annuity present value = = 80 x (1- 1/1,109) / 0,10 =

= 80 x (1- 1 / 2,3579) / 0,10 = = 80 x 5,7590 = 460,72

Total bond value = 424,10 + 460,72 = 884,82A discount bond 1.000 – 884,82 = 115,18

3

9

7.1. Bonds and Bond Valuation

The bond is discounted by 115 is to note that the 80 coupon is 20 below the coupon on a newly issued par value bond.

Annuity PV = 20 x (1-1 / 1,109) / 0,10 == 20 x 5,7590 = 115,18

10

7.1. Bonds and Bond Valuation

Suppose that interest rates had dropped by 2% instead of rising by 2 %. The X bond now has a coupon rate of 8% when the market rate is only 6%.

0 1 2 3 4 5 6 7 8 9 10

80 80 80 80 80 80 80 80 80

1.000

11

7.1. Bonds and Bond ValuationPresent value = 1.000 / 1,069 = = 1.000 / 1,6895 = 591,89

Annuity present value = = 80 x (1- 1/1,069) / 0,06 =

= 80 x (1- 1 / 1,6895) / 0,06 = = 80 x 6,8017 = 544,14

Total bond value = 591,89 + 544,14 = 1.136,03A premium bond 1.136,03 – 1.000,00 = 136,03

12

7.1. Bonds and Bond Valuation

The bond value is therefore about 136 in excess of par value.

The present value of 20 per year for nine years at 6% is:

Annuity PV = 20 x (1-1 / 1,069) / 0,06 == 20 x 6,8017 = 136,03

4

13

7.1. Bonds and Bond Valuation

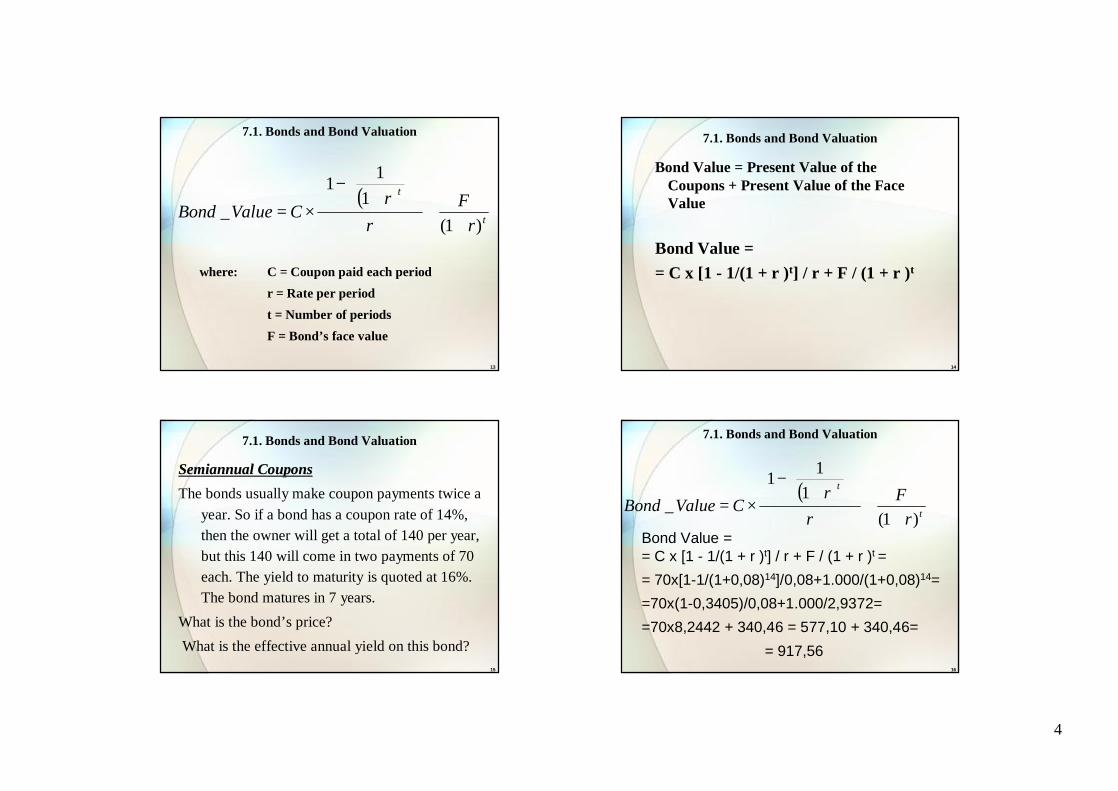

where: C = Coupon paid each periodr = Rate per periodt = Number of periodsF = Bond’s face value

( )t

t

rF

rr

CValueBond)1(

111

_+

+

+

−

×=

14

7.1. Bonds and Bond Valuation

Bond Value = Present Value of the Coupons + Present Value of the Face Value

Bond Value = = C x [1 - 1/(1 + r )t] / r + F / (1 + r )t

15

7.1. Bonds and Bond Valuation

Semiannual CouponsSemiannual CouponsThe bonds usually make coupon payments twice a

year. So if a bond has a coupon rate of 14%, then the owner will get a total of 140 per year, but this 140 will come in two payments of 70 each. The yield to maturity is quoted at 16%. The bond matures in 7 years.

What is the bond’s price? What is the effective annual yield on this bond?

16

7.1. Bonds and Bond Valuation

( )t

t

rF

rr

CValueBond)1(

111

_+

+

+−

×=

Bond Value = = C x [1 - 1/(1 + r )t] / r + F / (1 + r )t == 70x[1-1/(1+0,08)14]/0,08+1.000/(1+0,08)14==70x(1-0,3405)/0,08+1.000/2,9372==70x8,2442 + 340,46 = 577,10 + 340,46=

= 917,56

5

17

7.1. Bonds and Bond Valuation

To calculate the effective yield on this bond, note that 8% every six months is equivalent to:

EAR = [ 1+ (APR/m )]m – 1EAR = [ 1+ (0.08/2 )]2 – 1 = 16,64%

18

7.1. Bonds and Bond Valuation

Interest rate riskInterest rate riskThe risk that arises for bond owners from

fluctuating interest rates is called interest rate risk.

1. All other things being equal, the longer the time to maturity, the greater the interest rate risk.

2. All other things being equal, the lower the coupon rate, the greater the interest rate risk.

19

7.1. Bonds and Bond Valuation

To illustrate the first of these two points, we compute and plot prices under different interest rate scenarios for 10% coupon bonds with maturities of 1 year and 30 years

502,11916,6720%671,70956,5215%

1.000,001.000,0010%1.768,621.047,625%

30 Years1 YearInterest rates Time to Maturity

20

7.1. Bonds and Bond Valuation

6

21

7.1. Bonds and Bond Valuation

( )t

t

rF

rr

CValueBond)1(

111

_+

+

+

−

×=

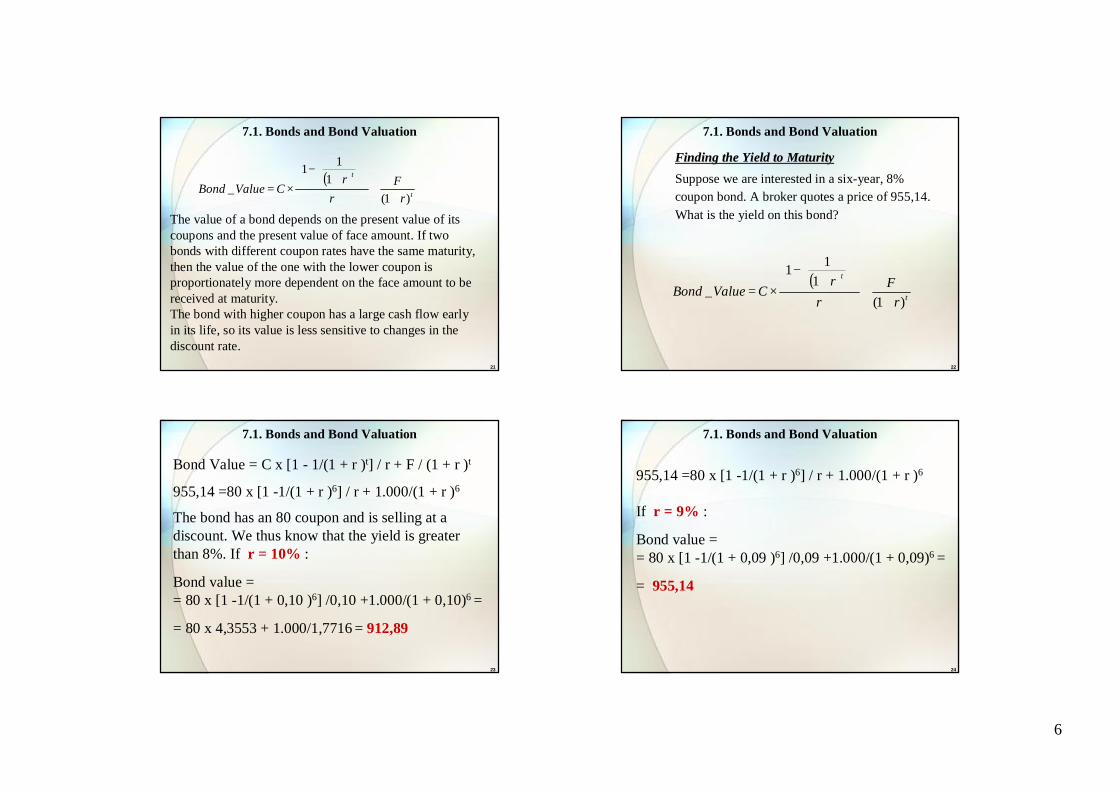

The value of a bond depends on the present value of its coupons and the present value of face amount. If two bonds with different coupon rates have the same maturity, then the value of the one with the lower coupon is proportionately more dependent on the face amount to be received at maturity. The bond with higher coupon has a large cash flow early in its life, so its value is less sensitive to changes in the discount rate.

22

7.1. Bonds and Bond Valuation

Finding the Yield to MaturityFinding the Yield to MaturitySuppose we are interested in a six-year, 8% coupon bond. A broker quotes a price of 955,14. What is the yield on this bond?

( )t

t

rF

rr

CValueBond)1(

111

_+

+

+

−

×=

23

7.1. Bonds and Bond Valuation

Bond Value = C x [1 - 1/(1 + r )t] / r + F / (1 + r )t

955,14 =80 x [1 -1/(1 + r )6] / r + 1.000/(1 + r )6

The bond has an 80 coupon and is selling at a discount. We thus know that the yield is greater than 8%. If r = 10% :

Bond value = = 80 x [1 -1/(1 + 0,10 )6] /0,10 +1.000/(1 + 0,10)6 =

= 80 x 4,3553 + 1.000/1,7716 = 912,89

24

7.1. Bonds and Bond Valuation

955,14 =80 x [1 -1/(1 + r )6] / r + 1.000/(1 + r )6

If r = 9% :

Bond value = = 80 x [1 -1/(1 + 0,09 )6] /0,09 +1.000/(1 + 0,09)6 =

= 955,14

7

25

7.1. Bonds and Bond Valuation

Bond Pricing Theorems1.Bond prices and market interest rates move in

opposite directions.2.When a bond’s coupon rate is (greater than /

equal to / less than) the market’s required return, the bond’s market value will be (greater than / equal to / less than) its par value.

26

7.1. Bonds and Bond Valuation

3.Given two bonds identical but for maturity, the price of the longer-term bond will change more (in percentage terms) than that of the shorter-term bond, for a given change in market interest rates.

4.Given two bonds identical but for coupon, the price of the lower-coupon bond will change more (in percentage terms) than that of the higher-coupon bond, for a given change in market interest rates.

27

7.1. Bonds and Bond Valuation

Bond YieldsBond YieldsYou’re looking at two bonds identical in every

way except for their coupons and their price. Both have 12 years maturity. The first bond has a 10% coupon rate and sells for 935,08. The second has a 12% coupon rate. What do you think it would sell for?

28

7.1. Bonds and Bond Valuation

……..935,08Bond value

12 years12 yearst

12%10%CR%

1.0001.000F

Bond12%Bond10%

8

29

7.1. Bonds and Bond Valuation

=..……………..=r……..935,08Bond value

12 years12 yearst

12%10%CR%

1.0001.000F

Bond12%Bond10%

30

7.1. Bonds and Bond Valuation

935,08 =100x[1-1/(1+r )12]/r+1.000/(1+r)12

If r =11%100x[1-1/(1+0,11)12]/0,11+1.000/(1+0,11)12== 100x6,4924 + 285,84 = 935,08Bond Value12% = =120x[1-1/(1+0,11)12]/0,11+1.000/(1+0,11)12== 120x6,4924 + 1.000/3,4985 = = 779,08 + 285,84 = 1.064,92

31

7.2. More on Bond Features

Securities issued by corporations may be classified as equity securities and debt securities

The main differences between debt and equity are the following:

1. Debt is not an ownership interest in the firm. Creditors do not have voting power.

32

7.2. More on Bond Features

2. The corporation’s payment of interest on debt is considered a cost of doing business and fully tax deductible. Dividends paid to stockholders are not tax deductible.

3. Unpaid debt is a liability of the firm. If it is not paid, it can result in liquidation or reorganization, two of possible consequences of bankruptcy. This possibility does not arise when equity is issued.

9

33

7.2. More on Bond Features

Sometimes it is not clear if a security is debt or equity. For example, suppose a corporation issues a perpetual bond with interest payable solely from corporate income if and only if earned.

34

7.2. More on Bond Features

The distinction between debt and equity is very important for tax purposes. So corporations try to create a debt security that is really equity is to obtain the tax benefits of debt and the bankruptcy benefits of equity.

35

7.2. More on Bond FeaturesThere are a number of features that distinguish these

securities from one another.Debt securities can be short-term or long-term.Debt securities are typically called notes,

debentures, or bonds.The two major forms of long-term debt are public

issue and privately placed.There are many other dimensions to long-term debt,

including such things as security, call features, sinking funds, ratings, and protective covenants

36

7.2. More on Bond Features

Term Explanation

Amount of issue $200 million The company issued $200 million worth of bonds.

Date of issue 8/4/94 The bonds were sold on 8/4/94.Maturity 8/1/24 The principal will be paid 30 years after

the issue date.Face Value $1,000 The denomination of the bonds is $1,000.Annual coupon 8.375 Each bondholder will receive $83.75 per

bond per year (8.375% of the face value).Offer price 100 The offer price will be 100% of the $1,000

face value per bond.

Features of a May Department Stores Bond

10

37

7.2. More on Bond FeaturesFeatures of a May Department Stores Bond

Term Explanation

Coupon payment dates 2/1, 8/1 Coupons of $83.75/2 = $41.875 will be paid on these dates.

Security None The bonds are debentures.

Sinking fund Annual The firm will make annual payments beginning 8/1/05 toward the sinking fund.

Call provision Not callable The bonds have a deferred call feature.before 8/1/04

Call price 104.188 initially, After 8/1/04, the company can buy backdeclining to 100 the bonds for $1,041.88 per bond, with

this price declining to $1,000 on 8/1/14.

Rating Moody’s A2 This is one of Moody’s higher ratings. The bonds have a low probability of default.

38

7.2. More on Bond Features

The indenture is the written agreement between the corporation and the lender detailing the terms of the debt issue.

A trustee (a bank) is appointed by the corporation to represent the bondholders.

The trust company must1) Make sure the terms of the indenture are

obeyed,2) Manage the sinking fund,3) Represent the bondholders in default

39

7.2. More on Bond Features

The bond indenture is a three-party contract between the bond issuer, the bondholders, and the trustee. The trustee is hired by the issuer to protect the bondholders’ interests.

The indenture includes:1. The basic terms of the bond issue;2. The total amount of bonds issued;3. A description of the security;4. The repayment arrangements;5. The call provisions;6. Details of the protective covenants.

40

7.2. More on Bond Features

Terms of a BondA registered form is the form of the bond issue in

which the registrar of the company records ownership of each bond; payment is made directly to the owner of record.

A bearer form is the form of bond issue in which the bond is issued without record of the owner’s name; payment is made to whoever holds the bond.

11

41

7.2. More on Bond Features

SecurityDebt securities are classified according to the

collateral and mortgages used to protect the bondholders.

Collateral is a general term that frequently means securities that are pledged as security for debt payment.

The term collateral is commonly used to refer to any asset pledged on a debt.

42

7.2. More on Bond Features

Mortgage securities are secured by a mortgage on the real estate property of the borrower.

A debenture is an unsecured bond, for which no specific pledge of property is made and usually with a maturity of 10 years or more.

A note is an unsecured debt, usually with a maturity under 10 years.

43

7.2. More on Bond Features

SeniorityA seniority indicates preferences in position

over other lenders, and debts are sometimes labeled as senior or junior to indicate seniority. Some debt is subordinated. This means that the subordinated lenders will be paid off only after the specified creditors have been compensated.

44

7.2. More on Bond FeaturesRepaymentBonds can be repaid at maturity or they may be

repaid in part or in entirety before maturity. Early repayment is often handled through a sinking fund.

A sinking fund is an account managed by the bond trustee for early bond redemption. The company makes annual payments to the trustee, who then uses the funds to retire a portion of debt.

12

45

7.2. More on Bond Features

There are many different kinds of sinking fund arrangements, for example:

1.Some sinking funds start about 10 years after the initial issuance.

2.Some sinking funds establish equal payments over the life of the bond.

3.Some high-quality bond issues establish payments to the sinking fund that are not sufficient to redeem the entire issue and there is the possibility of a large “balloon payment” at maturity. 46

7.2. More on Bond Features

The Call ProvisionThe call provision is an agreement giving the

corporation the option to repurchase the bond at a specified price prior to maturity.

The call premium is the amount by which the call price exceeds the par value of the bond.

47

7.2. More on Bond Features

A deferred call provision is a call provision prohibiting the company from redeeming the bond prior to a certain date.

A call protected bond is a bond that, during a certain period, cannot be redeemed by the issuer.

48

7.2. More on Bond Features

Protective CovenantsA protective covenant is a part of the indenture

limiting certain actions that might be taken during the term of the loan, usually to protect the lender’s interest.

13

49

7.2. More on Bond Features

Protective covenants can be classified into negative covenants and positive covenants.

Some typical negative covenants examples are:1. The firm must limit the amount of dividends

it pays according to some formula.2. The firm cannot pledge any assets to other

lenders.

50

7.2. More on Bond Features

3.The firm cannot merge with another firm.4.The firm cannot sell or lease any major assets

without the lender’s approval.5.The firm cannot issue additional long-term

debt.

51

7.2. More on Bond Features

Some typical positive covenants examples are:1.The company must maintain its working capital

at or above some specified minimum level.2.The company must periodically furnish audited

financial statements to the lender.3.The firm must maintain any collateral or

security in good condition.

52

7.3. Bond RatingsLow Quality, speculative,

Investment-Quality Bond Ratings and/or “Junk”

High Grade Medium Grade Low Grade Very Low Grade

Moody’s Aaa Aa A Baa Ba B Caa Ca C DDBRS (S&P) AAA AA A BBB BB B CCC CC C D

Moody’sDBRSAaa AAA Debt rated Aaa and AAA has the highest rating. Capacity to pay

interest and principal is extremely strong.Aa AA Debt rated Aa and AA has a very strong capacity to pay interest and

repay principal. Together with the highest rating, this group comprises the high-grade bond class.

A A Debt rated A has a strong capacity to pay interest and repay principal, although it is somewhat more susceptible to the adverse effectsof changes in circumstances and economic conditions than debt in high rated categories.

14

53

7.3. Bond RatingsBaa BBB Debt rated Baa and BBB is regarded as having an adequate capacity

to pay interest and repay principal. Whereas it normally exhibits adequate protection parameters, adverse economic conditions or

changing circumstances are more likely to lead to a weakened capacity to pay interest and repay principal for debt in this categorythan in higher rated categories. These bonds are medium-gradeobligations.

Ba, B BB, B Debt rated in these categories is regarded, on balance, as Ca, C CC, C predominantly speculative with respect to capacity to pay

interest and repay principal in accordance with the terms of theobligation. BB and Ba indicate the lowest degree of speculation, and CC and Ca the highest degree of speculation. Although such debt will likely have some quality and protective characteristics, these areout-weighed by large uncertainties or major risk exposures to adverse conditions. Some issues may be in default.

D D Debt rated D is in default, and payment of interest and/or repayment of principal is in arrears

54

7.4. Some Different Types of Bonds

A zero coupon bond is a bond that makes no coupon payments, thus initially priced at a deep discount.

Suppose the EIN Company issues a €1.000 – face value, five-year zero coupon bond. The initial price is set at €497. It is straightforward to verify that, at its price, the bond yields 15% to maturity (1000/1,155). The total interest paid over the life of the bond is 1.000 – 497 = 503

55

7.4. Some Different Types of Bonds

For tax purposes, the issuer of a zero coupon bond deducts interest every year even though no interest is actually paid.

Before 1982, corporations could calculate the interest deduction on a straight-line basis. For EIN, the annual interest deduction would have been 503/5=100,60 per year.

56

7.4. Some Different Types of Bonds

Under current tax law, the implicit interest is determined by amortizing the loan. We do this by first, calculating the bond’s value at the beginning of each year. For example, after one year, the bond will have four years until maturity, so it will be worth 1000/1,154=572; the value in two years will be 1000/1,153=658; an so on.

15

57

7.4. Some Different Types of Bonds

100,60987566583100,60866585722100,60755724971

503,00503Total

100,6013010008705100,601148707564

Straight-line Interest Expense

Implicit Interest Expense

Ending ValueBeginning Value

Year

58

7.4. Some Different Types of Bonds

With floating-rate bonds (floaters), the coupon payments are adjustable. The adjustments are tied to an interest rate index such as the Treasure bill interest rate or the 30-year Treasury bond rate.

The value of a floating-rate bond depends on exactly how the coupon payments are defined.

59

7.4. Some Different Types of Bonds

The majority of floaters have the following features:

1. The holder has a right to redeem his/her note at par on the coupon payment date after some specified amount of time. This is called a put provision.

2. The coupon rate has a floor and a ceiling. In this case, the coupon rate is said to be “capped,”and the upper and lower rates are sometimes called the collar

60

7.4. Some Different Types of Bonds

An inflation-linked bond have coupons that are adjusted according to the rate of inflation.

An income bonds are similar to conventional bonds, except that coupon payments are dependent on company income.

A convertible bond can be swapped for a fixed number of shares of stock anytime before maturity at the holder’s option.

16

61

7.4. Some Different Types of Bonds

A put bond allows the holder to force the issuer to buy the bond back at a stated price.

62

7.5. Bond Markets

Although most bond trading is OTC (over the counter), there is a corporate bond market associated with the New York Stock Exchange and other major exchanges. If you were to look in The Wall Street Journal, you would find price and volume information from this market.

63

7.4. Some Different Types of Bonds

NEW YORK BONDSCorporation BondsBONDS CUR YLD VOLUME CLOSE NET CHGAMR 9s16 12.6 190 71.50 -1.50AT&T 7s05 7.0 25 100.13 -.06AT&T 7 3/4s07 7.5 15 104 ...AT&T 6s09 5.9 29 102.25 -.88AT&T 6 1/2s13 6.2 20 104.63 .13AT&T 8.35s25 8.1 359 103.25 -.25AT&T 6 1/2s29 6.5 70 100 -1BJ Svc 7s06 6.8 3 102.31 .06

2005-03-25http://online.wsj.com/public/resources/documents/fbndsdec.txt

64

7.5. Bond Markets

“AT&T6s09”. This designation tells us that the bond was issued by AT&T, and that it will mature in 2009. The 6 is the bond’s coupon rate. Assuming the face value is 1000 the annual coupon on this bond is 0,06 X $1000 = $60. The small “s” stands for “space”.

17

65

7.5. Bond Markets

The column market “Close” gives us the last available price on the bond at close of business day before. This bond last sold for 102,25 percent of $1000 or $1022,50

“Net Chg,” indicates that yesterday’s closing price was -0,88%, or $8,80 lower than the previous day’s closing price.

66

7.5. Bond Markets

The bond’s current yield (“Cur Yld”) is equal to the annual coupon payment dividend divided by the bond’s closing price ($60/1022,50=5,87%, or 5,9% rounded off to one decimal place).

The number of bonds that were bought and sold is reported in the column “Vol”. Only 29 bonds changed hands during the day.

67

7.5. Bond Markets

+1/4??.?89.0Albanon 8s10+1/874.589.4Albanon ?s06+1/284.58?.?Albanon 8s98

Supply the missing information

Cur Yld = Coupon / Price = 8/84.5 = 9.5%

Coupon rate/74.5% = 9.4%

Coupon rate = 9.4% X 74.5% = 7.003%

8%/Price = 9%

Price = 8 / 9 = 88.9%68

7.6. Inflation and Interest Rates

Key issues:

• What is the difference between a realreturn and a nominal return?

• How can we convert from one to the other?

18

69

7.6. Inflation and Interest Rates

Example:Suppose we have $1000, and Diet Coke costs $2.00 per six pack. We can buy 500 six packs. Now suppose the rate of inflation is 5%, so that the price rises to $2.10 in one year. We invest $1000 and it grows to $1100 in one year. What’s our return in dollarsdollars? In six packssix packs?

70

7.6. Inflation and Interest Rates

A.DollarsDollars.Our return is

($1,100 - $1,000)/$1,000 = $100/$1,000 = 0,10.

The percentage increase in the amount of green stuff is 10%; our return is 10%.

71

7.6. Inflation and Interest Rates

B.B. Six packsSix packs. We can buy $1,100/$2.10 = 523.81 six

packs, so our return is(523.81 - 500)/500 = 23.81/500 =

4.76%The percentage increase in the amount of

brown stuff is 4.76%; our return is 4.76%.

72

7.6. Inflation and Interest Rates

Real versus nominal returns:Your nominal return is the percentage change in the amount of money you have.

Your real return is the percentage change in the amount of stuff you can actually buy.

19

73

7.6. Inflation and Interest Rates

The relationship between real and nominal returns is described by the Fisher Effect. Let:

R = the nominal returnr = the real returnh = the inflation rate

According to the Fisher Effect:1 + R = (1 + r) x (1 + h)

74

7.6. Inflation and Interest Rates

From the example, the real return is 4.76%; the nominal return is 10%,

and the inflation rate is 5%:(1 + R) = 1.10(1 + r) x (1 + h) = 1.0476 x 1.05 = 1.10

75

7.6. Inflation and Interest Rates

1 + R = (1 + r) x (1 + h)R = r + h + r x hR ≈ r + h

0.10 = 0.0476 + 0.05 + 0.0476 x 0.050.10 = 0.0476 + 0.05 + 0,002380.10 ≈ 0.0476 + 0.05

76

7.7. Determinants of Bond RatesU.S. Interest Rates: 1800-1997

20

77

7.7. Determinants of Bond Rates

The relationship between short- and long-term interest rates is known as the term structure of interest rates.

The term structure of interest rates tells us what nominal interest rates are on default-free, pure discount bonds of all maturities.

The term structure tells us the pure time value of money for different lengths of time.

78

7.7. Determinants of Bond Rates

When long-term rates are higher than short-terms rates, we say that the term structure is upward sloping.

When short-term rates are higher, we say it is downward sloping.

79

7.7. Determinants of Bond Rates

80

7.7. Determinants of Bond Rates

21

81

7.7. Determinants of Bond Rates

What factors affect observed bond yields?• The real rate of interest• Expected future inflation• Interest rate risk• Default risk premium• Taxability premium• Liquidity premium

82

7.7. Determinants of Bond Rates

The real rate of interest is the compensation investors demand for forgoing the use of their money.

83

7.7. Determinants of Bond Rates

Investors thinking about loaning money for various lengths of time recognize that future inflation erodes the value of the dollars that will be returned. As a result, investors demand compensation for this loss in the form of higher nominal rates.

This extra compensation is called the inflation premium.

84

7.7. Determinants of Bond Rates

The longer-term bonds have much greater risk of loss resulting from changes in interest rates than do shorter-term bonds.

The interest rate risk premium is the compensation investors demand for bearing interest rate risk.

22

85

7.7. Determinants of Bond Rates

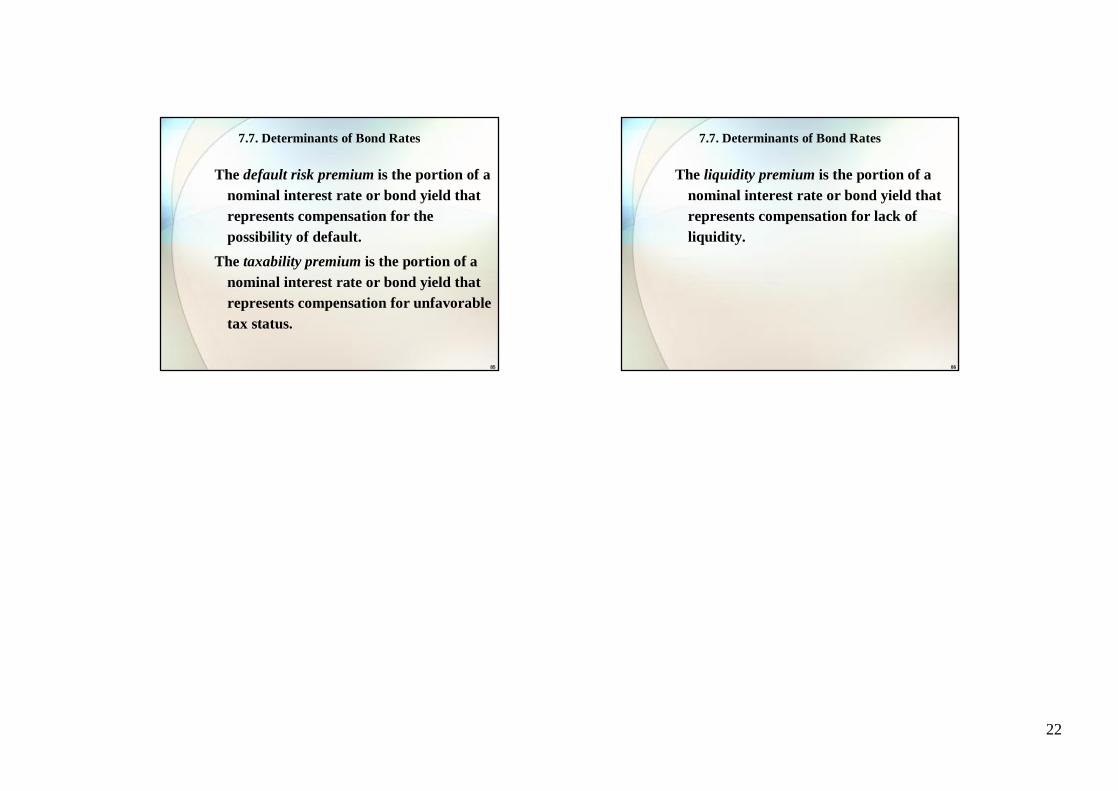

The default risk premium is the portion of a nominal interest rate or bond yield that represents compensation for the possibility of default.

The taxability premium is the portion of a nominal interest rate or bond yield that represents compensation for unfavorable tax status.

86

7.7. Determinants of Bond Rates

The liquidity premium is the portion of a nominal interest rate or bond yield that represents compensation for lack of liquidity.