a new era of networking - beatrice companies, inc. · pdf filea new era of networking ......

TRANSCRIPT

Corporate Profile

Who we are

A New Era of Networking

www.nortelnetworks.com

annual.report.98

65097.11/03-99www.nortelnetworks.com

A New Era of Networking

www.nortelnetworks.com

annual.report.98

Nortel Networks is a global supplier of

communications networks and services for

data and telephony, bringing together a

broad range of complementary networking

technologies, skills, distributor channels,

and integrated networking capabilities.

Nortel Networks works with carrier and

enterprise customers worldwide to design,

build, and deliver Unified Network

solutions. Unified Networks create greater

value for customers worldwide through

integrated network solutions spanning

data and telephony. Unified Networks

blend routing, optical, wireline, wireless,

switching, and Internet Protocol tech-

nologies in a seamless manner to deliver

service predictability and security.

Customers include public and private

enterprises and institutions; Internet service

providers; local and long-distance, cellular,

and PCS communications companies; cable

television carriers; and public utilities.

Nortel Networks’ common shares are

listed on the New York, Toronto, Montréal,

Vancouver, and London stock exchanges.

Nortel Networks had 1998 revenues

of $17.6 billion and has approximately

75,000 employees in over 150 countries

and territories.

Annual.report.98

The Web is changing everything

1 Letter to Shareholders

5 Year in Review

9 Financial Section

10 Financial Review

30 Consolidated Financial Statements

36 Notes to Consolidated Financial Statements

68 Directors and Officers

Corporate Information

The Web is changing everything, including

our annual report.

Last year, we defined our webtone

vision of making the World Wide Web the

foundation for a dramatically different

kind of service to society. We set out to use

our experience and networking expertise

to build the Web into a reliable, secure,

commercial-grade system that could support

a wide array of business transactions.

We’re leading the way by using the Web

to maintain closer relationships with

customers, employees, suppliers, analysts,

and – starting with this year’s annual

report – our investors.

In the new era of Web-based communi-

cations, the traditional annual report is a

relic from the past. Therefore, as part of

evolving into a more Web-centric company,

we are providing a less elaborate report in

printed form and a Web-based interactive

version in the Investor Relations section

of our website.

The benefits include shareholder-ready

access to information about the com-

pany, as well as savings in design, paper,

production, and distribution costs.

The document in hand provides you with

detailed information about the company’s

financial performance in 1998, in line

with meeting our requirements to deliver

an annual report to shareholders.

For comprehensive information about our

business and integrated network solutions,

visit www.nortelnetworks.com.

All dollar amounts in this annual report are in U.S. dollars

unless otherwise stated.

Annual.report.98

Letter to Shareholders

2 NORTEL NETWORKS 1998 ANNUAL REPORT

The global communications industry hasexperienced more than two decades of rev-olutionary ferment. As we approach the endof the twentieth century, the pace of changehas never been more rapid nor the changesmore profound.

The marketplace is being dramaticallyreshaped by deregulation, technology, andmobility, compounded by the explosivegrowth of the Internet, as both a communi-cations medium and a business phenomenon.Powerful drivers of change are transformingnetwork economics, creating new customerrelationships, and generating massive invest-ment in network infrastructure, services,

and applications. These are the characteris-tics of a new era of networking that willdefine the global economy and society ofthe next century.

The new era of networking excites theimagination in many ways. Sometimes it’sthe little things that capture our attention,such as getting a better deal on a new carafter comparison shopping on the Web, oreffortlessly reaching the office through awireless laptop connection.

But the new era of networking is aboutbig things, too. It offers a panoramic vision of a networked society that allows our ideasand aspirations to soar around the globe and into cyberspace.

At the Heart of the Revolution

Telecommunications is the “killer app” driv-ing the Internet revolution. This is goodnews for a company like Nortel Networksthat understands both telecommunicationsand the Internet. It puts your company atthe heart of the revolution the comingtogether of public and private networks withthe Internet. High-performance optical

technology is powering the Internet revolu-tion that’s changing the way the world com-municates. Seventy-five percent of Internettraffic in North America is carried on NortelNetworks high-performance optical networks.

After just a few short years, the Internetis becoming part of everyday life. It elimi-nates the constraints of time and distanceand gives us global access to information,not only in online libraries, but in businessesand in people’s minds.

Together, the Internet and the WorldWide Web are having a major impact on thevolume and kinds of traffic carried on theworld’s networks. They’re helping to change

the way we think about networks and thevery nature of what networks do.

Until recently, “the network” referred tothe worldwide telecommunications infra-structure of local and long-distance networkswhose primary service was voice telephony.Not any more. Today, “the network” is anexpanding web of interconnected voice anddata networks, private and public networks,and wireline and wireless networks.

The traditional telecom and data net-working industries have changed fundamen-tally. The market is volatile and customersare uncertain about the demands end-users will put on their networks and howthose networks will evolve. The boundariesbetween enterprise and carrier networks andbetween wireless and wireline are blurring.

New and traditional customers are movinginto a world of networks designed for data.Increasingly, these data networks use theInternet Protocol (IP), the language of theInternet and the standard for the networksof the future. But the thousands of circuit-switched networks built for voice commu-nication worldwide during the past century

will be with us for many years to come. Customers today require networks capa-

ble of handling both voice and data traffic,unifying circuit and packet systems.Leading-edge networks blend switching,routing, IP networking, fiber optics, wireless,and other technologies. These are the funda-mental building blocks for networks capableof carrying huge volumes of Internet trafficefficiently, quickly, and most important ascommerce moves onto the Web reliably.

Nortel Networks brings to the market a unique ability to integrate and combinedisparate technologies in reliable, secureUnified Networks that span data and tele-phony. With our competence and strength inall major networking technologies, we canreach into our portfolio of technologies andservices and put together solutions that meetdiverse needs. We are one of the few com-panies capable of guiding customers to thefuture, no matter how their networks evolve.

Our mission is to deliver greater value tocustomers worldwide through integratednetwork solutions. We’re bringing togetherand unifying many diverse networks andbuilding a more reliable Internet to enablenew ways for people to share ideas, do business, and improve the quality of life forthemselves and their communities.

Our Financial Performance

Our strong position was gained during ayear of dramatic change in the industry andthe global economy, as well as in NortelNetworks, which experienced more funda-mental change in 1998 than at any othertime in its history. But your companyentered 1999 in better shape than ever, lay-ing new foundations for growth by workingwith customers and partners to create a newera of networking.

By any measure, 1998 was a year of ac-complishment for your company. Thanks tothe support of our customers and investors,and the commitment of 75,000 employeesaround the world, Nortel Networks set newrecords for financial performance:

Annual.report.98

Letter to Shareholders

Nortel Networks is at the heart of the Internet

revolution and the opportunities it offers for creating a

new era of networking.

A New Era of Networking

• Revenues rose 14 percent to an all-timehigh of $17.6 billion.

• Net earnings applicable to commonshares of $1.07 billion (before acquisition-related costs, one-time gains, and charges),or $1.86 per share, were up 32 percent and21 percent, respectively, over 1997.

• Record order input of $18.5 billion fromongoing operations represented an increaseof 16 percent over 1997.

Nortel Networks is a well-balanced com-pany, supported by a broad customer baseand the broadest portfolio of technologiesand network solutions in the industry.Revenues from carrier customers grew 14 percent globally, with a dramatic increasein sales of our broadband network offerings.Enterprise revenues were up 26 percentover 1997, reflecting the comprehensive datanetworking portfolio we can offer sinceacquiring Bay Networks.

Nortel Networks is well-balanced geo-graphically, and revenues from NorthAmerica, Europe, Asia Pacific, and CALA(Caribbean and Latin America) all showedstrong growth during the year. As the Yearin Review following this letter highlights,we had major wins in markets around theworld and in all market segments.

Expenses relating to sales, marketing,and general administration were $3.09 bil-lion, or 17.6 percent of revenues, reflectingour investments to support global market-ing programs and streamline our businessprocesses. We continue to focus on mak-ing every dollar of expense go further inresearch and development (R&D) andother activities. R&D expenses increased to$2.45 billion, or 14 percent of revenues,from $2.15 billion, or 13.9 percent of rev-enues, in 1997, a level consistent withplanned and ongoing investments across allbusiness units.

Our strong financial performance in1998 demonstrated the effectiveness of ourstrategy of increasing value for our share-holders by building on our core strengthsand by working hard to increase the satis-

faction and loyalty of our customers.Customer satisfaction and loyalty ratingsboth increased two percentage points over1997. With our solid fourth quarter andrecord order input for the year, we began1999 with strong momentum and confi-dence in the future.

A More Powerful Company

Our customers are seeing a more powerfulcompany building even greater strength bybringing together new technologies, skills,

channels to the market, and integrated networking capabilities designed to meettheir needs.

This demonstrates the major progress inbuilding Nortel Networks into an IP data-networking powerhouse ready to capitalizeon new market opportunities and satisfychanging customer demands. During 1998,we brought together the portfolio of tech-nologies, products, and solutions to establishNortel Networks as a new class of company,and equipped our people to build next-generation wireless and wireline networks.

To help expand the portfolio andstrengthen our position, we invested in a hostof companies developing innovative tech-nologies in high-growth market segmentsand sold minority investments in othersthat no longer served our strategic needs.With internally generated innovations, ourlarge portfolio of patents is growing at a rateof three patent filings per day.

We made selective acquisitions to bringnew technology, skills, and capabilities into the company. With the purchase of Broadband Networks Inc., we could offerinnovative technology for high-quality wire-less voice, video, data, and Internet services.The purchase of Aptis Communications, Inc.

brought us expertise in next-generationremote-access data networking and virtualprivate networks. With Cambrian SystemsCorporation, we added metropolitan areasto our world-leading position in optical networking.

The acquisition of Bay Networks, com-pleted smoothly and in record time,brought us leading-edge customers andenterprise sales channel partners, a strongportfolio, and 7,000 talented people skilledin routing and IP technologies. By the end

of the year, we were recognized by NetworkWorld magazine as one of the five most powerful companies in the global network-ing industry.

We made organizational changes to con-centrate our efforts on new opportunities inboth the carrier and enterprise segments.We merged Bay Networks with our enter-prise data networks unit and consolidatedour packet technologies, products, andskills within a new and formidable businesscapable of offering carriers an impressivearray of Unified Network solutions.

We continued retooling the Corporationfor greater speed and responsiveness. Wecompleted the reengineering of the R&Dorganization to bring customers and design-ers closer together, initiated the consoli-dation of manufacturing, and eliminatedbusiness practices no longer appropriate forour future.

During the coming year, we’ll continueleveraging our unique breadth of people,skills, and technologies to generate new revenues, gain market share, and delivergreater value to our customers and share-holders. We’ll continue building the portfo-lio, streamlining our procedures, and movingmore of our business processes to the Web.

NORTEL NETWORKS 1998 ANNUAL REPORT 3

Nortel Networks brings to the market a unique ability to

integrate and combine disparate technologies in reliable,

secure Unified Networks that span data and telephony.

The Network is our Business

As this annual report demonstrates, we’reincreasingly using the Web to communicatewith our employees, partners, suppliers, andinvestors, as well as build closer relation-ships with our customers. We’re leading theway in leveraging networking technologyfor critical business applications. Our inter-nal network is much more than a collectionof technologies linking people at corpo-rate sites worldwide. At Nortel Networks, as at other companies today, the network isour business.

That’s why we’re building a Web reliableenough to handle our business 24 hours a day. We operate one of the largest corpo-rate networks in the world, managing voice, data, and video traffic between employees,management teams, R&D labs, manufac-turing operations, and many customers,suppliers, and partners. The network is aliving lab that gives us tremendous insightsinto the architecture, the components, and the expertise required to build next-generation networks with the capacity, reli-ability, and quality of service that can makebusinesses more competitive and meetfuture growth needs.

Nortel Networks is already a leader inimplementing “network commerce,” a termencompassing all forms of e-commerce/telephony commerce, including electronicdata interchange (EDI), electronic fundstransfer, and various forms of telephonycommerce, such as 1-800 services, call cen-ters, and interactive voice response systems.

Our ServiceWeb customer service andsupport tool lets customers receive productinformation, download software patches,and resolve issues via the Internet. With1,700 users and 130 user sessions a day atthe end of 1998, volume is expected toreach 10,000 users and 1,000 sessions a dayby 2000.

Our network has already had a majorimpact on the way we do business, movingus closer to customers and making us more

effective, efficient, and flexible in respond-ing to market needs. Doing more businesselectronically will have a positive impact onrevenues, profitability, and value for ourcustomers and shareholders.

Capitalizing on Change

Your company has always succeeded by taking a leadership position, embracing discontinuities and capitalizing on changeto fuel new growth and improve competi-tiveness. Nortel Networks rose to the chal-lenges of leadership with digital, wireless,and fiber-optic systems. Now we are leadingthe way by providing enterprises and serviceproviders with high-value, Unified Networksolutions spanning data and telephony,wireless and wireline, and circuit-switchedand packet technologies.

As we take up the challenge of creating anew era of networking, we’re continuingour efforts to help our customers succeed ina highly competitive world. We’re providingintegrated network solutions to a diverseand growing base of customers in morethan 150 countries and territories, buildingsome of the fastest, most reliable, and cost-effective networks in the world today.

We’re laying the foundation for newgrowth, guided by the vision of makingNortel Networks the most valued companyin the industry. We will be valued by ouremployees by continuing to provide a greatplace to work, with multiple career pathsand challenging opportunities. We will bevalued by the communities where our peoplelive and work by continuing our tradition of community support, with an emphasison expanding educational opportunities inevery region where we operate.

Nortel Networks will be valued by cus-tomers by providing the network solutions,applications, services, and skills that helpthem make the transition to the new era ofnetworking. And that will help us continuegenerating the strong returns that buildlong-term value for our shareholders.

As we come to the end of the century,we’re pursuing several of the biggest growthopportunities in the history of our industryand our company. We’re determined to seizethese opportunities. In the process, we’llplay a role in reshaping economic life andhow the world shares ideas, overcoming oldbarriers and boundaries that have limitedthe possibilities for interaction, coopera-tion, and growth. In these efforts, thanks tothe support of our customers, employees,and shareholders, we’re strongly positionedfor success.

We also wish to thank Paul Oreffice forthe contributions he made during his yearsof distinguished service as a director of the Corporation. Mr. Oreffice retired as a director on April 23, 1998. At the sametime, we welcome to the board of directorsSir Antony Pilkington, retired chairman,Pilkington plc; Richard J. Currie, presidentof George Weston Limited; and David L.House, who joined the board as president of Northern Telecom Limited in August,following the acquisition of Bay Networks,where he was chairman, president, and chiefexecutive officer.

Donald J. SchuenkeChairman of the Board

John A. RothVice-Chairman and Chief Executive Officer

February 25, 1999

4 NORTEL NETWORKS 1998 ANNUAL REPORT

Donald J. Schuenke

John A. Roth

Annual.report.98

Year in Review

6 NORTEL NETWORKS 1998 ANNUAL REPORT

Acquisitions

■■ Bay Networks, Inc., a California-based leader in the world-wide data networking market. Northern Telecom acquired BayNetworks, which more than doubled the number of registered andbeneficial shareholders of Nortel Networks stock, and announcedthe new corporate brand name of the merged business NortelNetworks. This new brand communicates and reinforces our lead-ership in providing high-value, unified network solutions to adiverse and growing base of telephony and data customers world-wide. Nortel Networks’ $6.9 billion acquisition of Bay Networksexpanded significantly its base of high-speed packet and IP-optimized network solutions. As a result of the acquisition, Nortel Networks became the largest company in Canada and BCE Inc. reduced its ownership to approximately 41 percent. ■■ AptisCommunications, Inc., a Massachusetts-based, data network-ing start-up company, with leadership in the remote-access area.■■ Broadband Networks Inc., a Manitoba-based start-up com-pany and a leader in the design and manufacture of fixed broad-band wireless communications networks. ■■ Cambrian SystemsCorporation, an Ontario-based developer of an innovative tech-nology to speed the flow of network traffic between metropolitanareas and optical Internet backbone networks. ■■ Minorityinterests in companies such as Avici Systems, Inc. and interWAVECommunications International Ltd.

Achievements

■■ Internet Backbones: 75 percent of backbone Internet trafficin North America is carried on optical equipment supplied by Nortel Networks, which also supplies six out of seven pan-EuropeanInternet backbones. ■■ Qwest, United States: Augmenting its1997 purchase of Nortel Networks advanced fiber-optic transmissionequipment for its 16,000-mile coast-to-coast telecommunicationsnetwork, Qwest Communications International, Inc., a multimediacommunications company, has chosen Nortel Networks backboneswitching hubs Nortel Networks DMS-250 SuperNode tandemswitching systems and ServiceBuilder Intelligent Network (IN)service creation platform to address its expanding networkneeds. ■■ Level 3 Communications, Inc., United States: Tocomplete Level 3 Communications’ global end-to-end network bythe year 2001, using IP-based technology, Nortel Networks andCorning Incorporated worked together on delivering the best fiber solution, using Siecor’s cable design and Corning’s fiber.■■ Colombia: In April 1998, Nortel Networks announced that more than 80 percent of Colombia’s 1.2 million cellular sub-scribers were being served by Nortel Networks wireless solutions.■■ Cellcom Israel: Nortel Networks helped Cellcom Israel buildthe world’s first all-digital TDMA wireless network to reach onemillion subscribers. ■■ Bouygues Telecom, France: Superiorquality of service is available to subscribers in the Paris, Bordeaux,Aquitaine Poitou, and Southwestern regions, as Bouygues Telecomcontinues to use Nortel Networks’ radio equipment and installa-tion services to expand its GSM 1800 digital wireless network.■■ JazzTel, Spain: Jazz Telecom S.A., Spain’s first competitivelocal exchange carrier, is building a new national network withSpain’s SAINCO and Nortel Networks. The new network will offerbusiness customers a broader range of advanced, high-quality, cost-

effective services, including access to the Internet. ■■ IomegaCorporation, United States: To save time and increase produc-tivity, the manufacturer of the award-winning Zip and Jaz drivesand disks has implemented Nortel Networks Symposium CallCenter Server, a leading-edge software solution utilizing MicrosoftWindows NT. Hewlett-Packard and Bell Canada are amongother customers who have installed the system. ■■ Reuters,London: The world’s leading financial and news informationorganization wanted to build a network with new architecture andnetwork infrastructure capable of scaling well beyond anythingpredictable today. Reuters chose a next generation high-performanceWAN backbone based on a Nortel Networks Passport infrastruc-ture. Nortel Networks’ architecture will carry all Reuters’ legacyproducts on one network, together with its IP and frame relaytraffic, as well as saving money by using asynchronous transfermode (ATM) backbones. Nortel Networks dominates the infor-mation provider market, which includes Reuters, Telerate,Bloombergs, and Bridge Information Systems. ■■ Primus,Australia: Primus Telecommunications, one of Australia’s leadingcarriers, selected Nortel Networks to provide a turnkey solution forits new Internet service, internetPrimus, which will cover all thecapital cities in Australia and an additional twenty-seven majorregional centers. ■■ Cable & Wireless Communications,London: Corporate and business customers will have increasedspeed, capacity, and reliability in voice and data services throughCable & Wireless Communications’ $650 million network upgradeand expansion, which will be created through a three-year workingrelationship with Nortel Networks and will produce substantialoperating efficiencies for Cable & Wireless Communications.■■ Federa, The Netherlands: A new GSM 1800 radio networkis now available in The Netherlands, as Nortel Networks suppliedseveral hundred cell sites for the network to Federa, the new Dutchtelecom operator owned by France Télécom Mobiles International,ABN Amro Bank, and Rabobank. ■■ Hebei PTA, The People’sRepublic of China: By mid-year 1999, a major expansion of theprovince’s GSM digital cellular network will create the capacity for651,000 new subscribers. The Hebei Post and TelecommunicationsAdministration’s Phase Five expansion project represents the largestcontract for a single project that Nortel Networks has ever signedin China. ■■ State Postal Bureau, The People’s Republicof China: China’s State Postal Bureau is constructing computernetworks to connect central offices and branches in ministries,provinces, and post areas. Nortel Networks will supply all of the routing equipment, which includes 237 different router products, for the integrated service network router backbone.■■ SUNDAY, Hong Kong SAR: Hong Kong’s new generationGSM operator awarded Nortel Networks a series of projects tostrengthen and expand its mobile phone network, which will enableSUNDAY to become one of the most comprehensive networks in Hong Kong. ■■ Telstra, Australia: Australia’s principal tele-communications company and largest mobile telecommunicationscompany has selected Nortel Networks to build a national turn-key cdmaOne (IS-95 CDMA) mobile telephone network withservice beginning in the third quarter of 1999. ■■ Net2000Communications, United States: To support Net2000’s goal tobe the leading super-regional integrated communications provider,Nortel Networks will provide the foundation for this emergingcompetitive local exchange carrier’s state-of-the-art voice and data

Annual.report.98

Year in Review

NORTEL NETWORKS 1998 ANNUAL REPORT 7

network serving the eastern United States. ■■ Liz ClaiborneInc., United States: One of the largest manufacturers of women’sapparel and accessories in the United States will help maximize itscompetitive position with a Nortel Networks high-speed network that features a multi-service ATM and Ethernet-switched backbone.■■ City of Philadelphia, United States: Philadelphia deployedNortel Networks Accelar 1200 routing switches in two new five-story city administration buildings to provide high-speed, Layer 3IP-forwarding for citywide applications. ■■ BT, its Europeanpartners Albacom (Italy), BT Belgium, Cegetel (France),Sunrise (Switzerland), Telfort (The Netherlands), and ViagInterkom (Germany) and Nortel Networks are building a newpan-European network to meet the explosive growth in theInternet and demand for bandwidth-hungry, high-speed data ser-vices. ■■ Formus Communications, United States: This global competitive carrier will provide data and Internet services to busi-nesses in selected markets around the world with Nortel NetworksUnified Network solutions for high-speed, broadband wirelessservices. The deal is expected to be worth as much as $500 millionand will include Nortel Networks Reunion broadband wirelessaccess equipment, Passport ATM switching, and system integra-tion services. ■■ MetroNet Communications Corp., Canada:Business customers of Canada’s first and largest facilities-basednational competitive provider of local telecommunications ser-vices will have access to one of the most advanced networks inCanada, through access, high-capacity and local transport opticalequipment, and switching systems from Nortel Networks. ■■AT&T, United States: To support its thrust into local telephony, AT&T has selected the Cornerstone cable telephony communi-cations system from ANTEC and Arris Interactive, a NortelNetworks/ANTEC joint venture, to serve up to two million homes.The initial order for Cornerstone product represents the first stepin an agreement that could result in sales of up to $900 million.More cable operators have deployed Cornerstone than any othercable telephony product worldwide, including Cox, TCI,Cablevision Lightpath, Time Warner, Titus Communications(Japan), VTR Telefonica (Chile), Jupiter Telecommunications(Japan), and Priority Telecom (Austria). ■■ Telgua, Guatemala:Several key regions in Guatemala will benefit from more readilyavailable voice, data, and enhanced calling services. GuatemalaCity was the first to have Nortel Networks’ infrastructure installedfor a 150,000-subscriber expansion of the Telecomunicaciones deGuatemala network. This agreement with Telgua for a CDMA-based network makes Nortel Networks the only supplier to have allmajor wireless technologies (AMPS, GSM, TDMA, and CDMA)in implementation in Latin America. ■■ Cybercare Inc.,United States: Cybercare selected Nortel Networks to provide acomplete home health/remote health system known as CybercareElectronic House Call system, which incorporates technologydeveloped by Medical College of Georgia and Georgia Institute ofTechnology. Health care providers will be able to see and talk withpatients in their homes and assess key health indicators such as heart rate, blood pressure, blood-oxygen and blood-sugar levels, thanks to this system which enhances the accessibility and delivery of medical care at a lower overall cost. ■■ IXCCommunications, Inc., United States: This provider of inte-grated network solutions is using Nortel Networks optical net-working equipment for a coast-to-coast network linking San

Francisco, Los Angeles, Fort Worth, Texas, and New York and asoutheastern route connecting New York, Washington, D.C.,Atlanta, and Houston, Texas. Using 10 Gbps product and Multi-wavelength Optical Repeater (MOR) Systems, these networks willenable the transmission of up to 80 Gbps of multimedia, data, and voice traffic. ■■ Focal Communications Corporation,United States: This competitive local exchange carrier has selected DMS-500 local and long-distance switching systems and full-service AccessNode Express platforms to extend its exist-ing facilities-based telecommunications services into a nation-wide presence. ■■ Kaiser Permanente, United States: The largestnot-for-profit health maintenance organization (HMO) in theUnited States is implementing a nationwide high-performancedata network with more than 350 Nortel Networks Passport 6400enterprise network switches, which will enable it to enhance andincrease support to almost nine million health care customers and medical centers, data centers, and satellite offices. ■■ SBCCommunications Inc., United States: SBC Communications has selected Nortel Networks industry-leading network products DMS-100 digital switching equipment, hardware and softwareupgrades, and product conversion services for the company’sseven-state region, in a five-year contract expected to exceed $1.5 billion. ■■ Electric Lightwave, United States: ElectricLightwave, one of this nation’s leading integrated communicationsproviders, will deploy a high-capacity optical networking solutionin a 3,000-mile western SONET ring. As part of a five-year agreement, the network will carry traffic over a high-capacity net-work scalable up to 320 Gbps, using Nortel Networks’ 10 Gbps four-fiber ring architecture with Dense-Wavelength DivisionMultiplexing (D-WDM). ■■ Omnipoint Communications,United States: Omnipoint has selected Nortel Networks to buildGSM 1900 digital networks in Indianapolis, Detroit, and severalother basic trading areas (BTAs) under terms of a three-year supply agreement. ■■ Bell Atlantic, United States: BellAtlantic is modernizing its advanced telecommunications networkto better meet customer needs for new products and advancedservices, through DMS SuperNode processor upgrades, DMSEnhanced Networks, and Primary Rate ISDN hardware and software. ■■ United States Cellular, United States: Needingto rapidly address competitive challenges with new digital wirelessservice in Milwaukee and other markets in Wisconsin and Illinois,United States Cellular selected Nortel Networks to build newCDMA and TDMA digital wireless networks under a con-tract potentially worth more than $400 million over four years.■■ Société Européenne des Satellites, Luxembourg: SES has signed a contract with Nortel Networks for the provision of a turnkey interactive satellite system, which will consist of the Ground Network as well as Satellite Interactive Terminals to provide interactive broadband and bandwidth-on-demand multimedia services on upcoming ASTRA satellites. ■■ TurkTelekom, Turkey: Turk Telekom is using Nortel Networks’Proximity I fixed wireless access solution to provide domestic tele-phone service with wireline-equivalent digital voice, fax, high-speed data, Internet access, and other services for residential and small business customers. ■■ Copesa ComunicacionesPersonales S.A., Paraguay: Copesa selected Nortel Networks tosupply a complete GSM 1900 digital PCS network, includingswitching, radio base stations, and services for a nationwide

8 NORTEL NETWORKS 1998 ANNUAL REPORT

network expected to serve up to 100,000 subscribers. ■■ BellCanada: Bell Canada is using the 1-Meg Modem in Canada’slargest deployment of high-speed data access services. NortelNetworks’ revolutionary plug-and-play 1-Meg Modem was declared“the easiest, least expensive, and most practical” high-speedmodem to use in the industry by Computer Reseller News. Test engineers for Computer Reseller News noted the 1-MegModem solution “is the only one that can be rolled out to servicemore than 70 million subscribers today.” Just eight months afterlaunching the 1-Meg Modem, Nortel Networks had received morethan $1 billion in orders from public institutions, Internet ServiceProviders, and service providers throughout the United States.Major contracts include Transwire Communications Inc. of New York, MegsINet of Chicago, and AGIS Communicationsof Detroit. ■■ Global One: Global One, the worldwide jointventure of Deutsche Telekom, France Télécom, and Sprint, ispreparing to provide its customers with an advanced array of integrated telecommunications services spanning the globe. Athree-year supply and resale agreement covers the purchase of Nortel Networks Multimedia Carrier Switch (MMCS), DMS-Global Services Platform (DMS-GSP) switching systems,and NetWORKS network supervision systems, as well as the purchase and resale of Nortel Networks Passport and the resale of Nortel Networks Vector multimedia ATM switching systems.■■ GST Telecom, Inc., United States: GST and NortelNetworks are jointly building a “converged network,” integratingdata, voice, and video on a single network using a combination of packet, frame, and cell technologies. GST will deploy the nextgeneration Virtual Integrated Transport and Access (VITA) net-work using Nortel Networks Passport and Concorde ATM switches complementing its existing network of Nortel Networks voice, access, and optical network equipment. ■■ TelemigCelular S.A., Brazil: Telemig has selected Nortel Networks toexpand its statewide cellular network over the next three yearsthrough the manufacture, deployment, and integration of NortelNetworks DualMode Radios, DMS-MTX SuperNode digitalswitching systems, and other equipment and services. In additionto the Telemig project, Nortel Networks is deploying TDMA IS-136 digital wireless networks for operators in the city of Sao Paulo, in the capital city of Brasilia, and in the western and northeastern regions of Brazil. ■■ Walgreen Company,United States: The ten-millionth Norstar telephone system wassold to this national drugstore chain. Norstar IntegratedCommunications System is a leader in the global key system mar-ket. The Norstar system has received the Editor’s Choice Awardfrom CTI Magazine and Teleconnect. ■■ Université Laval,Canada: When a greater demand for bandwidth, resulting from anincreased number of users and increasingly demanding engineer-ing applications, made necessary an upgrade to the networkinginfrastructure of its new sciences and engineering faculty building,Université Laval selected Nortel Networks Accelar 1200 routingswitches and Gigabit Ethernet technology to deliver high-speedswitching and routing. ■■ Rite Aid, United States: Rite Aid,one of this nation’s largest drug store chains, wanted a highly scalable, resilient network to serve customers quickly and effi-ciently and is installing equipment such as Nortel NetworksAccelar routing switches for Gigabit Ethernet switching and Layer 3 connectivity into the company’s state-of-the-art distri-bution centers. ■■ Nielsen Media Research, United States:

Nortel Networks is supplying this leader in television ratings and audience estimates with reliable, high-performance Accelar1200 routing switches to improve the performance of its existingmission-critical network infrastructure and provide GigabitEthernet connectivity to link customers to the company’s analyti-cal databases and products. ■■ AirTouch Communications,United States: To lower costs, meet future demands of wirelesscustomers, and achieve a better balance among its mix of infra-structure suppliers, the world’s largest cellular phone service providersigned a letter of intent with Nortel Networks for the multi-yearpurchase of state-of-the-art network switches, base stations, and con-trollers. AirTouch will purchase analog and cdmaOne (IS-95 CDMA)digital network infrastructure in a contract which could reach $500 million. ■■ U S West, United States: U S West is enhancingits advanced payphone system by installing more than 5,000 NortelNetworks Millennium MultiPay MultiApplication payphones,capable of evolving with the dynamic needs of the public accessand electronic commerce marketplace. ■■ MCI WorldCom,United States: At the second annual InfoVision Exhibit onOctober 5, 1998, MCI WorldCom received a product recognitionaward for the deployment of the world’s first 80 Gbps route usingNortel Networks’ industry-leading S/DMS TransportNode OC-192(10 Gbps) system with Dense-Wavelength Division Multiplexing.In December of 1997, MCI WorldCom turned up live customertraffic on the 80 Gbps network span extending 170 miles from LosAngeles to Rialto, California. MCI WorldCom is also deploying aninterexchange carrier market beta trial of Nortel Networks DMS-Spectrum Peripheral Module. The DMS-SPM is a new peripheralservices platform for public network service providers deliveringhigh-speed, direct optical network connectivity. ■■ Sprint PCS,United States: In early 1999, Nortel Networks cdmaOne equip-ment will provide Sprint PCS service across the southern and midwestern United States as a result of an intensive, thirty-monthrollout involving more than 4,700 base stations and an infrastructureinvestment of $1.3 billion. ■■ Defense Advanced ResearchProjects Agency (DARPA), United States: In an effort to jumpstartthe development and deployment of the high-speed, high-band-width networks needed to maintain United States competitivenessin the global markets of the 21st century, DARPA has collectivelyawarded Nortel Networks; GST Telecommunications, Inc.; Sprintand Lawrence Livermore National Laboratory a $10 million, three-year contract to build the West Coast leg of its Next GenerationInternet (NGI) research network, an ultra high-speed, high-band-width network linking Seattle to San Diego with major nodes inthe Portland, San Francisco, and Los Angeles areas. ■■ AbileneNetwork, United States: Set to launch formally in February 1999,Abilene is a high-speed data network managed by the UniversityCorporation for Advanced Internet Development linking sixty uni-versities together for the development of new applications and otherexperiments. Its aim is to improve quality and performance whiledeveloping pioneering new uses for the global computer network.Nortel Networks has donated leading-edge optical networkingequipment to assist Qwest in the deployment of a 10,000-mile fiber-optic backbone linking all members of the Abilene consortium.Nortel Networks’ market-leading optical networking systems willinitially send data at the speed of 2.5 Gbps on the Abilene network,before rising to full capacity of 10 Gbps. The network being pro-vided to Abilene by Qwest, Nortel Networks, and Cisco SystemsInc. will represent an investment worth $500 million.

Annual.report.98

Financial Section

1994

1995

1996

1997

1998

0

.4

.8

1.2

1.6

2.0

2.4

1994

1995

1996

1997

1998

0

300

600

900

1,200

1,500

1,800

Supplementary

measure of net

earnings applicable

to common shares

($ millions)

Supplementary

measure of earnings

per common share

($)

1994

1995

1996

1997

1998

0

3,000

6,000

9,000

12,000

15,000

18,000

Revenues

($ millions)

Up

14%

➔

Up

32%

➔

Up

21%

➔

10 NORTEL NETWORKS 1998 ANNUAL REPORT

The following provides additional analysis as to Nortel Networks’ operations and current financial situation. Thiscommentary is supplementary to and should be read in conjunction with the Consolidated Financial Statementswhich begin on page 30. Unless the context indicates otherwise, Northern Telecom Limited (the Corporation) andits subsidiaries are collectively referred to as Nortel Networks.

Overview

On August 31, 1998, the Corporation acquired Bay Networks, Inc. (Bay Networks), a Delaware corporation and aleading provider of data networking products and services (the Bay Networks Merger). The aggregate purchase pricewas approximately $6.9 billion, which was based on the closing market price of the Corporation’s common shares onthe closing day of the acquisition, the value of the assumed Bay Networks stock options, and merger-related costs. Forthe purpose of United States generally accepted accounting principles (GAAP), the aggregate purchase price wasapproximately $9.0 billion. The Bay Networks Merger added to Nortel Networks’ expertise and product portfolios indata and Internet Protocol (IP), increased Nortel Networks’ intellectual capital, provided new distribution channels tomarket, and broadened Nortel Networks’ customer base.

The rapid change of communications systems technology, based on current and future customer needs, is drivingthe convergence of data, telephony and video, and wireless and wireline technologies. The communications networks ofthe future are expected to combine packet and circuit technologies in a unified manner, allowing the smooth operationof applications using the best technology for each kind of traffic. These future networks are expected to create oppor-tunities for businesses to benefit from electronic commerce and the digital economy being created by the Internet,making it possible for the electronic business world to have high-performance networks using diverse IP and telephonytechnologies. Nortel Networks’ ability to develop products and services to meet these new market opportunities andcustomer needs is critical to its future success.

Acquisitions and dispositions

In pursuing its vision of Unified Networks (integrated networks blending routing, optical, wireless, wireline, switch-ing, and IP technologies in a seamless manner) and in strengthening its core business, Nortel Networks has completedthe following acquisitions and dispositions during the three years ended December 31:

December 22, 1998 Acquisition of all the remaining common and preferred shares of Nortel TechnologyLimited (formerly Bell-Northern Research Ltd.) from Bell Canada, increasing its owner-ship to 100 percent.

December 15, 1998 Acquisition of Cambrian Systems Corporation (Cambrian), a producer of metropolitan optical networking technology.

September 25, 1998 Sale of Advanced Power Systems business to Astec (BSR) plc (the Advanced Power Transaction).

August 31, 1998 Acquisition of Bay Networks, a leading provider of data networking products and services.

July 24, 1998 Sale of assembling and testing frames and cabinets facility in Creedmoor, North Carolina, to C-MAC Industries Inc. (the Creedmoor Facility Transaction).

June 25, 1998 Agreements by Matra Nortel Communications S.A.S. (MNC), formerly Matra Communi-cation S.A.S., to sell the Research and Development Centre of its GSM Terminals business to Finland Nokia Group (the GSM Terminals Transaction).

April 22, 1998 Acquisition of Aptis Communications, Inc. (Aptis), a remote-access data networkingstart-up company.

January 9, 1998 Acquisition of Broadband Networks Inc. (BNI), a designer and manufacturer of fixedbroadband wireless communications networks.

April 1, 1997 Sales of TTS Meridian Systems Inc. and Nortel Communications Systems Inc. distributionchannels to WilTel Communications, LLC (the WilTel Transaction).

June 21 1996 Acquisition of MICOM Communications Corp. (MICOM), a manufacturer and dis-tributor of integrated networking solutions.

February 2, 1996 Sale of structured wiring and copper wire and cable business to Cable Design Technologies(CDT) Canada Inc., since renamed NORDX/CDT, Inc.

Annual.report.98

Financial Review

NORTEL NETWORKS 1998 ANNUAL REPORT 11

Streamlining of business processes

On January 13, 1999, Nortel Networks announced the acceleration of its operations strategy designed to better meetthe rapidly changing needs and values of its customers worldwide. The strategy will simplify and streamline NortelNetworks’ businesses and operations processes, including the Corporation’s order-entry and fulfillment, delivery,service, and manufacturing systems over the next three years.

A key element of the Corporation’s strategy is the transition from vertical integration (making and assemblingmost of its products and systems) to virtual integration (acting as a systems house linking customers, design centers,internal production centers, contract manufacturers, and other resources). This transition better aligns Nortel Networksto focus on customers’ changing requirements for software technology and higher value-added integrated systemsand networks.

The operations strategy will involve plant divestitures, manufacturing rationalization, greater reliance on out-sourcing, and redeployment of employees. Approximately 10 percent of the Nortel Networks workforce will be affectedby the program. Divestitures, retraining, and attrition will minimize employee impact. As the program evolves overthe next eighteen to thirty-six months, the Corporation expects to realize savings in the range of $250 to $300 milliona year. The efficiencies generated by the program are not expected to significantly impact 1999 results from continuingoperations, but will position the Corporation for future growth. Over the coming years, the impact of the operationsstrategy is intended to contribute to Nortel Networks’ presence in the marketplace, growth in market share, higher revenue growth, and, ultimately, higher earnings growth.

The era of mega-telecom projects with long product-development cycles is coming to an end as the new economicsof networking take hold. The explosive growth of the Internet and data networking is shifting Nortel Networks’ pro-duct mix from hardware to software. In conjunction with these changes, speed-to-market is a critical factor in meetingcustomers’ demands for fast delivery, testing, and implementation of their unified telephony and data networks. Useof the World Wide Web, EDI (Electronic Document Interchange), and 800 numbers for order entry and fulfillmentwill provide faster and more responsive choices for Nortel Networks and its customers.

Results of operations

Consolidated represents Nortel Networks’ consolidated results.Carrier segment Nortel Networks’ operating segment delivering network solutions to carrier customers comprisedof products included in broadband networks, public carrier networks, and wireless networks.Enterprise segment Nortel Networks’ operating segment delivering network solutions to enterprise customerscomprised of products included in enterprise networks and Bay Networks.Corporate and Other segment (Other) Nortel Networks’ non-operating segment which includes revenues fromdivested businesses (restated annually to reflect in-year divestitures) and the components business, which provideshigh-performance semi-conductors, microwave modules, and other sub-assemblies and services. Other also includesexpenses for internal functions of the Corporation which are charged to the operating segments. Costs not chargedto the operating segments remain within the Corporate and Other segment.

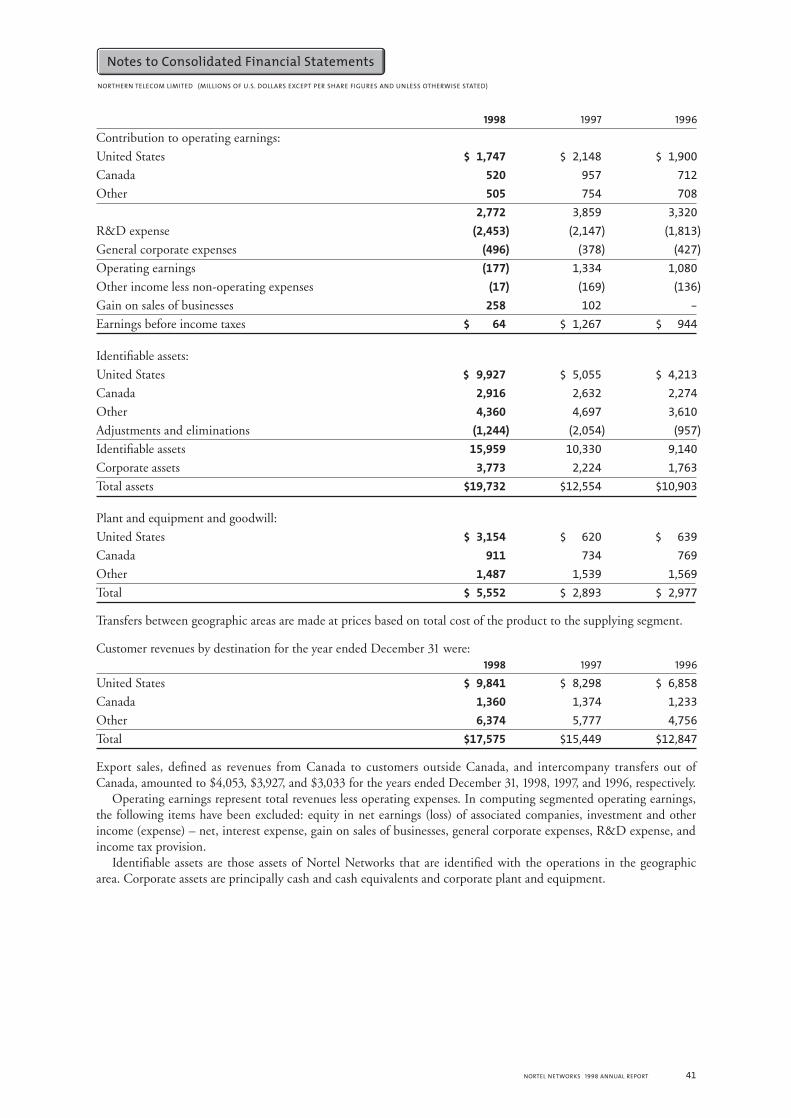

(millions of U.S. dollars, except per share figures) 1998 1997 § 1996 §

Consolidated revenues $17,575 $15,449 $12,847Carrier segment revenues 12,374 10,879 8,269Enterprise segment revenues 4,877 3,879 3,672

Net earnings (loss) applicable to common shares* $ (569) $ 812 $ 619Earnings (loss) per common share (.99) 1.56 1.20

Supplementary measure of net earnings† $ 1,065 $ 804 $ 619Supplementary measure of net earnings per common share† 1.86 1.54 1.20

Earnings before income taxes $ 64 $ 1,267 $ 944Earnings before income taxes, interest expense,

depreciation, and amortization (EBITDA)‡ 2,555 1,982 1,644

*Net earnings (loss) applicable to common shares for 1998 include the impact of amortization of Bay Networks intangible assets and purchased in-process research and development (R&D) from other acquisitions, and one-time gains and charges. Net earnings (loss) applicable to common sharesfor 1998, 1997, and 1996 were calculated after dividends on preferred shares of $32 million, $17 million, and $4 million, respectively.†As a measure to assess financial performance, management utilizes supplementary measures of net earnings and net earnings per common share whichexclude the impact of amortization of the Bay Networks intangible assets and purchased in-process R&D from other acquisitions, and one-time gainsand charges.‡EBITDA should not be considered as an alternative to net earnings (loss) from operations, net earnings (loss), or cash flows from operating activities(all as determined in accordance with GAAP). EBITDA is presented because it is a widely used financial indicator of a company’s ability to serviceindebtedness and other factors.§References to per share amounts have been restated to reflect the two-for-one stock split which was effective January 7, 1998.

Financial Review

12 NORTEL NETWORKS 1998 ANNUAL REPORT

Net earnings (loss) applicable to common shares

The net loss applicable to common shares for 1998 was primarily the result of the amortization of the Bay Networksintangible assets ($1,056 million), amortization of purchased in-process R&D from other acquisitions ($574 mil-lion), and pre-tax special charges of $447 million related primarily to the rationalization of certain Nortel Networks’operations, partially offset by one-time gains of $441 million, which included: $230 million from the AdvancedPower Transaction; $70 million from the sale of Lagardère SAS (Lagardère) shares; $89 million relating to EntrustTechnologies Inc. (Entrust Technologies); $30 million from the Creedmoor Facility Transaction; $24 million fromthe sale of Netspeed Inc. shares; $16 million loss from the GSM Terminals Transaction; and $14 million from the dis-position, in the second quarter of 1998, by MNC, of its 50 percent ownership in Matra Ericsson Telecommunications(MET Transaction). As a measure to assess financial performance, management utilizes supplementary measures ofnet earnings and net earnings per common share as discussed below.

Net earnings applicable to common shares in 1997, compared to 1996, reflected improved operating earnings,lower investment and other income (expense) net, and lower interest expense. Net earnings applicable to commonshares for 1997 included a pre-tax gain of $102 million related to the WilTel Transaction and pre-tax special chargesof $95 million related to the write-down of certain investments and the rationalization and/or relocation of certainmanufacturing facilities.

Supplementary measure of net earnings

The supplementary measure of net earnings, which excludes the amortization of the Bay Networks intangible assetsand purchased in-process R&D from other acquisitions, and one-time gains and charges, for the year ended Decem-ber 31, 1998, represents year-over-year growth in net earnings per common share of 21 percent for 1998 compared to1997, and of 28 percent for 1997 compared to 1996. The increase in the supplementary measure of net earnings for1998 primarily reflected a substantial increase in operating earnings, partially offset by a substantial increase in interestexpense. Net earnings were also impacted by substantial increases in investment and other income (expense) net.Excluding the impact of amortization of the Bay Networks intangible assets and in-process R&D from other acquisi-tions, and one-time gains and charges, Nortel Networks’ net earnings per common share would have been $1.86,$1.54, and $1.20 respectively, for 1998, 1997, and 1996.

Earnings before income taxes

The substantial decrease in 1998 earnings before income taxes is primarily the result of the significant acquisition-related costs that were incurred in 1998. These costs totalled $1.63 billion for the year. The 1998 acquisition-relatedcosts will continue to negatively impact Nortel Networks’ earnings before income taxes over the next years. On asegmented basis, earnings before income taxes from operations for Nortel Networks’ carrier segment was $1.58 bil-lion, an increase of $411 million over 1997 results, which were $354 million greater than 1996. The earnings beforeincome taxes from operations for Nortel Networks’ enterprise segment was $639 million for 1998, an increase of$184 million over 1997 results, which were $51 million lower than 1996. The earnings before income taxes fromoperations for Other was a loss of $515 million in 1998 compared to a loss of $360 million in 1997 and a loss of$373 million in 1996. The increase in the loss before income taxes in 1998 for Other is a result of higher interestexpense and goodwill amortization, and a loss on equity investments.

Revenues for the year ended December 31, 1998, compared to December 31, 1997

% of % of % change(millions of U.S. dollars) 1998 total 1997* total from 1997

Carrier segmentPublic carrier networks $ 4,118 23 $ 4,054 26 2Wireless networks 3,743 21 3,454 22 8Broadband networks 4,513 26 3,371 22 34

12,374 70 10,879 70 14Enterprise segment

Enterprise networks 4,877 28 3,879 25 26Other 324 2 691 5 (53)Total $17,575 100 $15,449 100 14

*Annual revenues by product line have been restated to reflect the repositioning of certain businesses, primarily divested businesses, within the man-agement structure. The primary effect of this reclassification was to move revenues from the enterprise segment to Other as a result of the WilTelTransaction and the MET Transaction.

Financial Review

NORTEL NETWORKS 1998 ANNUAL REPORT 13

The 14 percent increase in consolidated revenues in 1998 was attributable to an increase in sales volume of approxi-mately 19 percent, partially offset by price reductions (approximately 3 percent) and divestitures (approximately 2 percent.) Consolidated revenues in 1998 increased by 16 percent over the same period in 1997 after adjustment forthe impact of divested businesses (primarily the MET Transaction, the GSM Terminals Transaction, the WilTelTransaction, and the Advanced Power Transaction).

Carrier segment revenue growth of 14 percent in 1998 was largely driven by the growth in revenues of NortelNetworks’ optical networking solutions and also reflected growth in all carrier lines of business. This revenue growthwas attributable to a volume increase of approximately 17 percent, partially offset by price reductions of approxi-mately 3 percent. The 34 percent increase in broadband networks revenues in 1998 was driven by considerablegrowth across all regions. Wireless networks revenues increased 8 percent over 1997 levels as a result of considerablegrowth in sales in the Caribbean and Latin America region (CALA), significantly increased sales in the United States,and substantially increased sales in Asia Pacific. This increase was partially offset by a significant decline in European revenues and substantially lower Canadian sales. Public carrier networks revenues increased 2 percent in 1998 as aresult of higher sales in the United States and strong growth in Europe, offset by considerably lower sales in Asia Pacificand CALA, and significant decreases in Canada. North American revenues from traditional public carrier products areexpected to continue to be negatively affected by the shift in capital spending from public carrier products to highbandwidth broadband products.

Enterprise segment revenues in 1998 increased 26 percent over the same period in 1997. This increase was due togrowth across all major products and was primarily driven by the Bay Networks Merger. The increase in enterprisesegment revenues was attributable to a volume increase of approximately 27 percent, partially offset by price reductionsof approximately 1 percent. Enterprise networks revenue growth was a result of a considerable increase in revenuesfrom the United States (primarily as the result of the Bay Networks Merger) and strong revenue increases in all otherregions, except Canada, which had moderately lower revenues.

Other segment revenues in 1998 decreased 53 percent from the same period in 1997. The decrease was due pri-marily to the impact of lower revenues from divested businesses year-over-year.

Geographic revenues (1998 versus 1997)(Based on the location of the customer rather than the location of the selling organization)

% of % of % change(millions of U.S. dollars) 1998 total 1997 total from 1997

United States $ 9,841 56 $ 8,298 54 19Canada 1,360 8 1,374 9 (1)All other countries

Europe 3,718 21 3,476 22 7Other 2,656 15 2,301 15 15

6,374 36 5,777 37 10Total $17,575 100 $15,449 100 14

United States

The increase of 19 percent in revenues from the United States was primarily theresult of substantially increased revenues in enterprise networks, reflecting the BayNetworks Merger, and substantially increased revenues in broadband networks.Revenues increased in public carrier networks, significantly increased in wirelessnetworks, and declined substantially in Other (primarily the result of the WilTelTransaction). The increase in revenues from the United States over 1997 was theresult of substantially higher sales to interexchange carriers (IECs), independenttelephone operating companies (IOCs), and other United States customers anddistributors (the latter two increases were primarily as a result of the Bay NetworksMerger). Excluding the contribution of Bay Networks, revenues in the UnitedStates increased significantly.

Canada

Revenues in Canada decreased one percent compared to 1997 due to considerablylower sales in wireless networks and significantly lower sales in public carrier net-works, partially offset by substantially higher sales in broadband networks. Sales toBell Canada and other subsidiaries and related companies of BCE Inc. (the BCEgroup) declined from their 1997 level, and sales to other Canadian customersshowed a modest increase for the year.

Financial Review

1996

1997

1998

0

25

50

75

100

United States

Canada

Europe

Other

Revenues by

customer location

(percent)

14 NORTEL NETWORKS 1998 ANNUAL REPORT

Other countries

Revenues in Europe, Africa, and the Middle East (including the Commonwealth of Independent States) increased 7 percent from 1997 due to significantly increased revenues in enterprise networks and considerably increased revenues in broadband networks, partially offset by substantially lower revenues in Other (primarily the result of theMET Transaction and the GSM Terminals Transaction) and significantly lower revenues in wireless networks. Publiccarrier networks revenues increased from 1997.

Revenues in other markets, comprising CALA and Asia Pacific, increased 15 percent in 1998 when compared to1997. In CALA, sales in wireless networks increased substantially and both enterprise networks and broadband net-works sales rose significantly from 1997. Public carrier networks sales fell considerably compared to 1997. Revenues inAsia Pacific increased significantly in 1998 when compared to 1997, primarily driven by considerable increases inwireless networks revenues, partially offset by a sharp decrease in public carrier networks revenues. Sales in 1998 whencompared to 1997 were considerably higher in broadband networks and significantly higher in enterprise networks.

The recent devaluation of the Brazilian real is expected to slow economic growth in 1999 for the CALA region.Although demand for the Corporation’s products is expected to be impacted in the short term, the Corporation antic-ipates that the long-term growth prospects for the region remain strong.

The Asia Pacific region has been, and is expected to continue to be, affected for the foreseeable future by unstableeconomies caused in part by the volatility of certain currencies. Revenues from Asia Pacific (excluding China) were lessthan 3 percent and 4 percent, respectively, of the consolidated revenues for the years ended December 31, 1998, and1997. The current economic crisis in the affected Asia Pacific countries resulted in lower than anticipated demand forthe Corporation’s products in the second half of 1998 and it is expected that demand will continue to be impacted bythe crisis. In addition, the current economic crisis has spread to other countries, including countries in CALA, and this,together with global financial market uncertainty, may also impact demand generally for the Corporation’s products.

Revenues for the year ended December 31, 1997, compared to December 31, 1996

% of % of % change(millions of U.S. dollars) 1997* total 1996* total from 1996

Carrier segmentPublic carrier networks $ 4,054 26 $ 3,441 26 18Wireless networks 3,454 22 2,281 18 51Broadband networks 3,371 22 2,547 20 32

10,879 70 8,269 64 32Enterprise segment

Enterprise networks 3,879 25 3,672 29 6Other segment 691 5 906 7 (24)Total $15,449 100 $12,847 100 20

*Annual revenues by product line have been restated to reflect the repositioning of certain businesses, primarily divested businesses, within the man-agement structure. The primary effect of this reclassification was to move revenues from the enterprise segment to Other as a result of the WilTelTransaction and the MET Transaction.

The 20 percent increase in consolidated revenues in 1997 was attributable to an increase in sales volume of approxi-mately 24 percent, partially offset by divestitures (approximately 3 percent) and by price reductions (approximately 1 percent). Consolidated revenues in 1997 increased by 24 percent over the same period in 1996 when adjusted forthe impact of divested businesses.

Carrier segment revenue growth of 32 percent in 1997 was primarily due to higher revenues for wireless networks,broadband networks, and public carrier networks when compared to 1996. The revenue growth was attributable to avolume increase of approximately 33 percent partially offset by price reductions of approximately 1 percent. Publiccarrier networks revenues increased 18 percent in 1997 compared to 1996, primarily due to substantially increasedsales in the United States. Sales in 1997 when compared to 1996 were substantially lower in Asia Pacific, significantlyhigher in Europe, substantially higher in CALA, and higher in Canada. Wireless networks revenues increased by 51 percent in 1997 compared to 1996 due to substantially increased sales across all geographic regions. Broadbandnetworks revenues were up 32 percent in 1997 compared to 1996, primarily due to substantially increased sales inthe United States. When compared to 1996, broadband networks 1997 revenues were significantly higher in Europe,substantially higher in Canada, lower in CALA, and essentially flat in Asia Pacific.

Enterprise segment revenues increased in 1997 compared to 1996. Enterprise networks 1997 revenues increasedin the United States, increased substantially in CALA, increased in Asia Pacific, were essentially flat in Europe, andwere down slightly in Canada compared to 1996. The higher enterprise segment revenues in 1997 were attributableto an increase in sales volume.

Financial Review

NORTEL NETWORKS 1998 ANNUAL REPORT 15

Other revenues, comprising revenues from divested businesses and miscellaneous other revenues, decreased from 1996, primarily due to the WilTel Transaction.

Geographic revenues (1997 versus 1996)(Based on the location of the customer rather than the location of the selling organization)

% of % of % change(millions of U.S. dollars) 1997 total 1996 total from 1996

United States $ 8,298 54 $ 6,858 53 21Canada 1,374 9 1,233 10 11All other countries

Europe 3,476 22 3,029 24 15Other 2,301 15 1,727 13 33

5,777 37 4,756 37 21Total $15,449 100 $12,847 100 20

United States

The 21 percent increase in revenues in the United States in 1997 was due to higher revenues across all product linescompared to 1996. The increased revenues were due primarily to substantially higher sales to IECs, regional Bell oper-ating companies (RBOCs), other customers, and wireless operators, partially offset by lower sales to distributors.

Canada

Revenues in Canada in 1997 increased by 11 percent compared to 1996. The increased revenues were primarily dueto higher sales to wireless operators and increased sales to the BCE group.

Other countries

Revenues in Europe, Africa and the Middle East (including the Commonwealth of Independent States) in 1997,increased by 15 percent compared to 1996. The increase was due primarily to substantially increased sales in wirelessnetworks. Revenues in 1997 compared to 1996 were significantly higher in public carrier networks, broadband net-works, and other revenues, with enterprise networks sales essentially flat.

Revenues for 1997 in other markets, comprising Asia Pacific and CALA, increased by 33 percent compared with1996. Revenues in Asia Pacific increased significantly in 1997 compared to 1996, primarily due to substantiallyincreased sales in wireless networks. Sales in 1997 compared to 1996 were substantially lower in public carrier networks,higher in enterprise networks, substantially higher in other revenues, and essentially flat in broadband networks.Revenues in CALA increased substantially in 1997 compared to 1996, primarily due to substantially higher sales inwireless networks. Sales in 1997 when compared to 1996 were substantially higher in public carrier networks andenterprise networks, partially offset by lower sales in broadband networks and other revenues.

Gross profit

(billions of U.S. dollars) 1998 1997 1996Gross profit $7.53 $6.34 $5.13Gross margin 42.8% 41.0% 40.0%

The 1998 increase in gross profit over 1997 was primarily the result of increased sales volume in both the carrier andenterprise segments, partially offset by lower sales volume in Other, primarily due to the 1998 dispositions. Withinthe carrier segment, sales volume increased in broadband networks, wireless networks, and public carrier networks.Improvements due to product mix offset price reductions in both segments. When compared to 1996, the 1997increase in gross profit was primarily the result of increased sales in all segments, except Other, and improved marginsin both the enterprise and carrier segments. Gross profit in Other declined primarily due to the WilTel Transaction.

Improved gross margins in the enterprise and carrier segments contributed to the higher 1998 gross profit. Withinthe carrier segment, gross margins increased in public carrier networks, wireless networks, and broadband networks.Gross margins in 1998 were positively impacted by the Bay Networks Merger.

Although competitive pricing pressures continue, particularly in wireless networks, Nortel Networks has beenable to offset such pressure through the sale of higher-margin products and manufacturing and other cost-reductionprograms. Gross margin is also affected by the level of software sales. Gross margin was negatively affected by theintroduction of new products, the continued expansion into new markets, and the increase in products manufacturedby other suppliers in network solutions offered by Nortel Networks.

Financial Review

16 NORTEL NETWORKS 1998 ANNUAL REPORT

Selling, general and administrative (SG&A) expense

(billions of U.S. dollars) 1998 1997 1996SG&A expense $3.09 $2.71 $2.20As a percentage of revenues 17.6% 17.6% 17.1%

In 1998, SG&A expense increased by 14 percent over 1997, which increased by 24 percent over 1996. The 1998increase in absolute dollars reflected the funding of North American and international market investments acrossboth operating segments, as well as increased investments supporting Nortel Networks’ global marketing programsand operations systems to simplify and streamline Nortel Networks’ business processes, ongoing investment in com-puter systems infrastructure related to the global supply chain management system, and the preparation for the Year 2000 (see “Impact of the Year 2000 issue”). The lower SG&A expenses in Other are the result of divestitures,primarily resulting from the WilTel Transaction. SG&A was also impacted by the provision for customer financingrisk. Prior to January 1, 1997, customer financing risks were reflected as a reduction in revenues.

Research and development (R&D) expense

(billions of U.S. dollars) 1998 1997 1996R&D expense* $2.45 $2.15 $1.81As a percentage of revenues 14.0% 13.9% 14.1%

*Net of global investment tax credits of $125 million, $123 million, and $118 million for 1998, 1997, and 1996 respectively.

The increased level of investment in absolute dollars in 1998 and 1997 reflects ongoing programs across the carrierand enterprise segments for new products, process development, advanced capabilities, and services for a broad arrayof applications. As a percentage of revenues, R&D expense has remained essentially flat since 1996.

Amortization of intangibles

Although Nortel Networks reported its first, second, and third quarter results of 1998 in accordance with establishedaccounting practice and valuations of purchased in-process R&D provided by independent valuators, these valuations have been reconsidered in light of guidance provided by the United States Securities and ExchangeCommission regarding valuation methodology. Based on this new valuation methodology, the value of the purchasedin-process R&D related to the Bay Networks Merger was reduced to $1.0 billion and goodwill was increased by $440 million. With respect to the Aptis acquisition, the value of the purchased in-process R&D was reduced to$203 million and goodwill was increased by $75 million. Similarly, the amount of purchased in-process R&D relatedto the BNI acquisition was reduced to $329 million and goodwill was increased by $64 million.

(millions of U.S. dollars) 1998 1997 1996In-process R&D $1,241 $ - $ -Acquired technology 228 - -Goodwill 240 48 45

The amortization of purchased in-process R&D for 1998 primarily reflects the charges relatedto the acquisitions of Bay Networks, BNI, Aptis, and Cambrian. The capitalized amount ofpurchased in-process R&D as at December 31, 1998, was $509 million.

The amortization of acquired technology for 1998 reflects the charge related to the BayNetworks Merger. The capitalized amount of acquired technology as at December 31, 1998,was $1.82 billion.

Goodwill for 1998 primarily reflects charges related to the Bay Networks Merger and toinvestments in STC plc, MNC, and MICOM. The capitalized amount of goodwill as atDecember 31, 1998, was $3.29 billion.

Special charges

Special charges, aggregating $447 million, were included in the results for the period endedDecember 31, 1998.

As part of the special charges, a provision of $377 million related to steps taken to stream-line management layers, gain operational efficiencies, and realign resources and investments wasrecorded. Included in the provision was $261 million representing the cost of severance andrelated benefits for approximately 4,100 employees worldwide, which includes $70 million for

Financial Review

1996

1997

1998

0

500

1,500

1,000

2,000

3,000

2,500

Research and

development

($ millions)

NORTEL NETWORKS 1998 ANNUAL REPORT 17

individuals in R&D activities. The majority of Nortel Networks’ business functions, job classes, and geographic areaswere impacted, with a majority of the reductions taking place in the United States and Canada. Also included in thisprovision was $93 million in non-cash expenses for plant and equipment and other write-downs, and $23 million infacilities and other costs, primarily related to wireless networks and enterprise networks. The anticipated benefits ofthese activities began to materialize in the Corporation’s consolidated results of operations during the fourth quarter of1998. All of these activities are expected to be substantially completed by September 30, 1999. As at December 31,1998, $119 million of severance, benefits, and other personnel-related costs, and $23 million in facilities and other costshad been paid. As well, $60 million in non-cash expenses for fixed asset and other write-downs had been recognized.

Included in the special charges for 1998 was a write-down in connection with MNC, primarily related to thereductions in the carrying value of certain assets. Nortel Networks’ proportionate share of this reduction was 50 per-cent of approximately $22 million, resulting in a write-down of approximately $11 million.

Also included in the special charges for 1998 was a provision of $59 million, which comprised a write-down of$32 million related to certain assets and investments held by the Corporation, severance payments of $16 million, andplant rearrangement and relocation costs of $11 million. The majority of the severance and plant rearrangement andrelocation costs related to a charge taken by Nortel plc to downsize a portion of its Fixed Wireless Access manufacturingoperations in Paignton, United Kingdom. The activities are expected to be substantially completed by June 30, 1999.

In 1997, the Corporation announced special charges aggregating $95 million, which comprised a write-down of$51 million related to certain investments held by the Corporation and a provision of $44 million for the rationaliza-tion and/or relocation of certain of the Corporation’s manufacturing facilities. These activities were substantiallycompleted by September 30, 1998.

Investment and other income – net and interest expense

(millions of U.S. dollars) 1998 1997 1996Equity in net earnings (loss) of associated companies $ (19) $ 14 $ (8)Investment and other income (expense) net 234 (14) 47

$215 $ - $ 39

Interest expense $232 $169 $175

The increase in investment and other income net in 1998 as compared to 1997, including equity in net earnings ofassociated companies, was primarily the result of the following items: a pre-tax gain of $70 million from the sale ofLagardère shares; a pre-tax gain of $77 million relating to Entrust Technologies’ initial public offering concurrent witha secondary offering of Entrust Technologies common shares by the Corporation; a pre-tax gain of $24 million onthe sale of Nortel Networks’ equity interest in Netspeed Inc.; and a pre-tax dilution gain of $12 million resulting fromEntrust Technologies’ acquisition of r3 Security Engineering AG (r3). Also contributing to the increase in investmentand other income net in 1998 was an increase of $29 million in interest income, primarily resulting from highercash balances following the Bay Networks Merger and higher levels of short-term investments due to increased cashflows from United States operations. In addition, minority interest has moved from an expense to an income, primari-ly due to the loss recorded by Entrust Technologies as a result of its acquisition of r3. These increases were partiallyoffset by the Corporation’s loss of $19 million from its equity in net earnings (loss) of associated companies, and byincreased foreign exchange losses (see below).

The decrease in investment and other income net in 1997 as compared to 1996 was primarily a result of sub-stantially higher net customer financing expenses, partially offset by significantly higher equity earnings. Investmentand other income net was also impacted by lower interest income earned in 1997 due to, among other things,reductions in short-term interest rates as compared to 1996. Significantly higher foreign exchange losses and higherminority interest compared to 1996 also impacted investment and other income net.

The higher interest expense in 1998 compared to 1997 is primarily due to the increased use of short-term debt,primarily in Colombia and Brazil, increased use of commercial paper, and an increase in short-term interest rates,which was partially offset by lower interest on long-term debt as the result of the settlement at maturity in the firstquarter of 1998 of a C$300 million debt which had been swapped to sterling. The decreased interest expense for1997, when compared to 1996, was primarily due to the reduced use of commercial paper as a result of higher cashbalances, partially offset by increased long-term debt in Colombia.

Nortel Networks continues to expand its business globally and, as such, an increasing proportion of its businesswill be denominated in currencies other than United States dollars. As a result, fluctuations in foreign currencies mayhave an impact on Nortel Networks’ business and financial results. Nortel Networks endeavours to minimize theimpact of such currency fluctuations through its ongoing commercial practices and by attempting to hedge its expo-sures to major currencies. In attempting to manage this foreign exchange risk, Nortel Networks identifies operationsand transactions that may have foreign exchange exposure, based upon, among other factors, the excess or deficiency of

Financial Review

18 NORTEL NETWORKS 1998 ANNUAL REPORT