a look at the recession us-india tis dispute 2.3

TRANSCRIPT

A Look at the Causes and Consequences of the Recession in

Global IT:

The Sources of Immigration Restriction in U.S.-India Trade in

Services, 2007-2010

Non-Tariff Barriers to Trade in Services (NTB-

TIS) Issues in U.S. Business Immigration

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

1 | P a g e

Non-Tariff Barriers to Trade in Services (NTB-TIS) Issues in U.S. Business Immigration

This Draft October, 2010

Updated January 2013

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

2 | P a g e

Contents Executive Summary (Part 1): ................................................................................................................... 8

PART I: Indian H-1B Consulting Firms or U.S.-based Multinational Corporations – Which is the Primary Source of IT Sector Unemployment in the U.S.? ................................................................... 13

1. The Two U.S. Economies and the Dual International Trade Systems ............................................. 13

1. How U.S.-Based Multinationals Control the Overall Pace and Location of Global Hiring in the IT Sector ...................................................................................................................................................... 15

2. U.S.-India Terms of Trade: Small and Relatively Stable .................................................................. 29

Table 1. Top Ten Countries with which the U.S. has a Trade Deficit .......................................... 29

For the month of June 2010............................................................................................................ 29

Table 2: US EXPORTS OF GOODS AND SERVICES TO INDIA (Q1 2009-Q1 2010) ....... 31

Table 3: US IMPORTS OF GOODS AND SERVICES FROM INDIA (Q1 2009-Q1 2010) . 32

Table 4: US EXPORTS OF SERVICES TO INDIA (HISTORICAL) ............................................. 34

Table 5: US IMPORTS OF SERVICES FROM INDIA (HISTORICAL) ....................................... 34

3. Growth Trends in the U.S.-India Services Trade ......................................................................... 35

4. Increasing U.S. Deficits in Global Trade in Goods ........................................................................... 39

Key EU Trade and Investment Data and Trends ........................................................................ 41

5. Tier One – The Multinationals at the Top of the Global Food Chain .............................................. 42

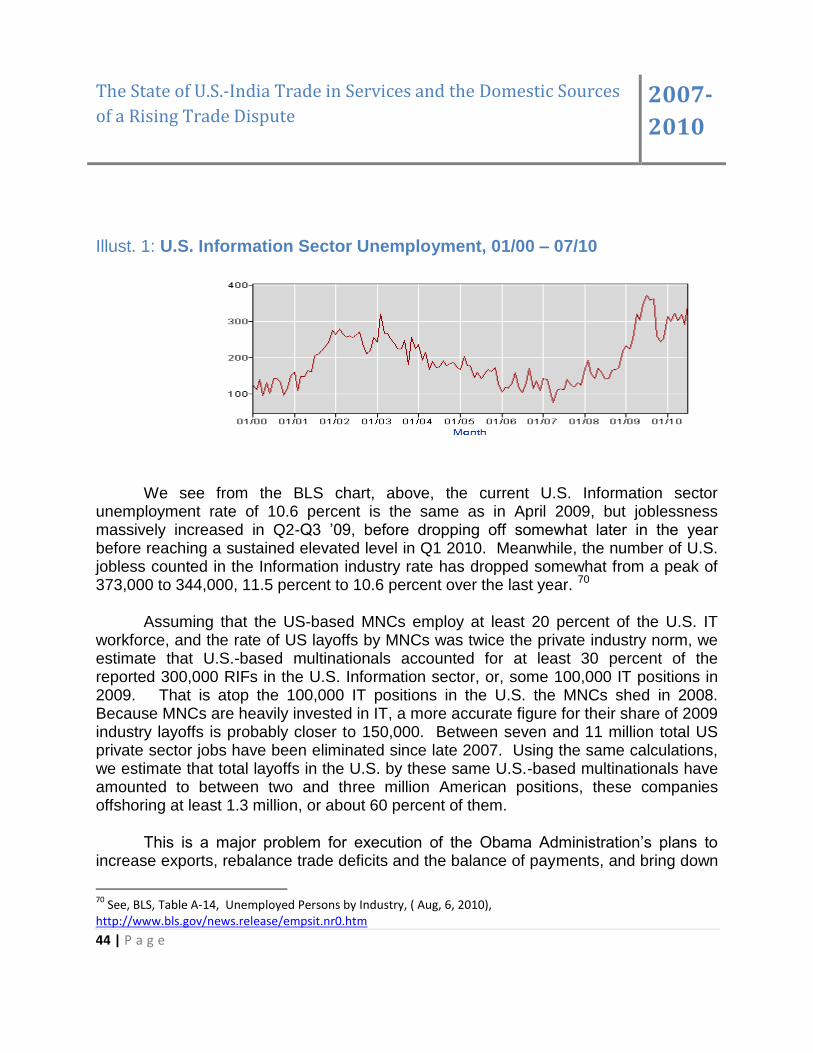

Illust. 1: U.S. Information Sector Unemployment, 01/00 – 07/10 .................................................. 44

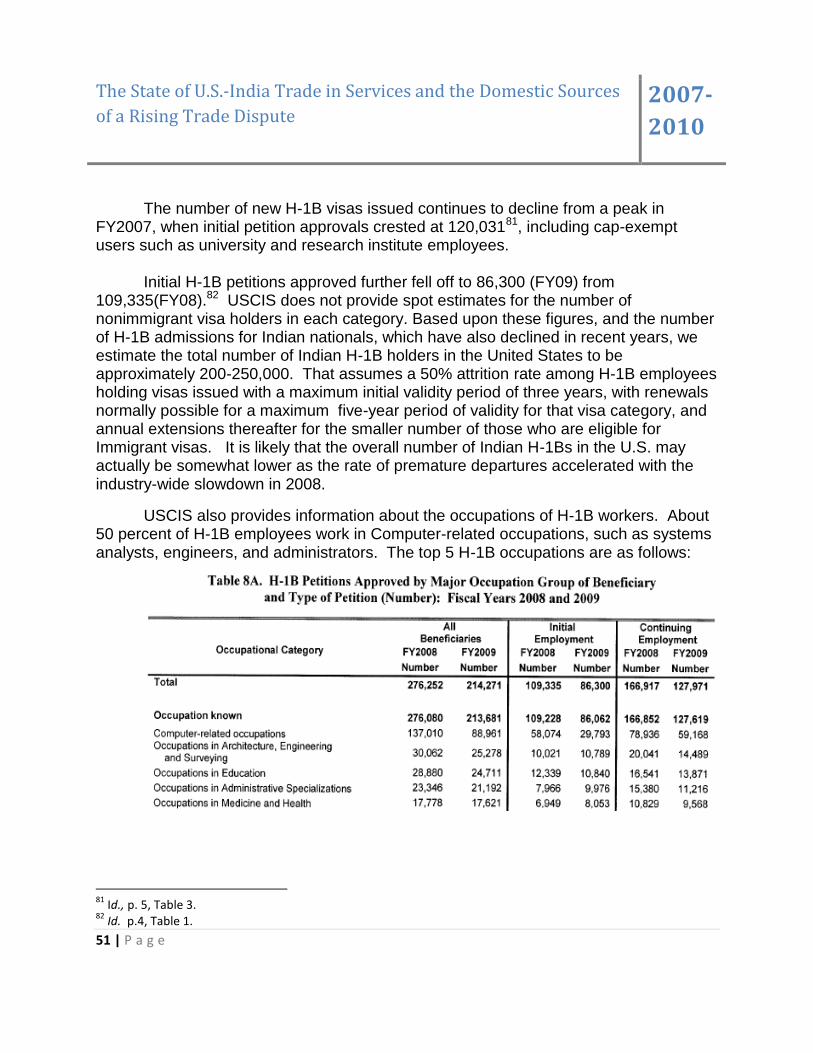

6. Portrait of the Disappearing Indian H-1B Worker, and the Negligible Impact of Foreign Workers on the U.S. Labor Market ........................................................................................................................ 49

Direct and Indirect Benefits to the U.S. from Value-Added by Indian H-1B Workers ....................... 53

7. FY 2009 H-1B Report Shows Continuing Trends ................................................................................. 54

8. H-1B Highlights (FY 2009) .................................................................................................................... 56

9. Characteristics of H-1 Workers (FY 2000-2009) .................................................................................. 57

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

3 | P a g e

11. The Perils of Growing U.S. Trade Protectionism ......................................................................... 62

12. The Role of the MNCs in U.S. and Indian IT Industry Unemployment ........................................ 64

13. IBM: A Case Study in Planned Globalization by a U.S.-based Multinational, and the Botched U.S. Regulatory Response ....................................................................................................................... 68

Illustration 2. IBM Global Staffing and Wages Projection (2005-10) ........................................... 70

14. Other Long-term Effects of U.S. Regulatory Excess .................................................................... 72

15. A Misdirected U.S. Policy Response Foreshadows a Bigger Conflict with Global Corporate Governance, with Serious Economic Consequences for All to Come ..................................................... 74

16. PART 1 Conclusion ...................................................................................................................... 77

APPENDIX I: ................................................................................................................................................ 78

Table 1. Private sector gross job gains and losses, seasonally adjusted ................................... 78

Has U.S. Immigration Law Become an Impermissible Non-Tariff Barrier to Trade Under the WTO General Agreement on Trade in Services (GATS)? .............................................................................. 80

Executive Summary ......................................................................................................................... 81

BACKGROUND .................................................................................................................................... 83

UNDUE RESTRICTIONS UPON L-1 INTRACOMPANY TRANSFERS UNDER GATS MODE 3 .............................................................................................................................................................. 91

SOME USCIS DE FACTO RULES AND PRACTICES VIOLATE SPECIFIC GATS COMMITMENTS .................................................................................................................................. 98

Unlawful Restrictions on Mode 3 Commercial Presence (L-1 Intracompany Transferees) .. 98

Restrictions on Mode 4 Service Providers (H-1B Specialty Workers) - Less Clearly Discriminatory ................................................................................................................................. 103

Specialty occupation aliens and their employers must be in compliance with all labour

condition application requirements that are attested to by the established employer. ........ 105

B-1 Short-Term Visitors for Business .............................................................................................. 110

CONCLUSION: ....................................................................................................................................... 112

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

4 | P a g e

*** .............................................................................................................................................................. 113

APPENDIX I: Neufeld Memo Documentary Requirements ............................................................ 113

FAQs - FREQUENTLY ASKED QUESTIONS ABOUT ISSUES OF EMPLOYER “CONTROL” OVER H-1B WORKERS ................................................................................................................... 115

Q. What are the attestations and/or documents that now need to be filed with H-1B petitions to demonstrate control? ..................................................................................................................... 115

A. The memo signals that new filings of H-1B petitions will have to attest to, and where

applicable, be accompanied by the following types of documents: ............................................ 115

Q. What is the basis for the above list of required attestations and requirements? ............... 120

*** .............................................................................................................................................................. 122

APPENDIX II: Significant Articles in the GATS Agreement ............................................................ 122

APPENDIX III: SCHEDULE OF SPECIFIC U.S. COMMITMENTS AND RESERVATIONS TO THE WTO GATS TREATY ................................................................................................................... 144

APPENDIX IV: Significant Trade Disputes and Related Events Involving National Legislation325

HISTORICAL HIGHLIGHTS AND HISTORY OF WTO-MEDIATED TRADE DISPUTES INVOLVING US LEGISLATION, OR FOREIGN LEGISLATION ................................................ 325

OTHER SIGNIFICANT GATS/GATT DISPUTES ......................................................................... 327

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

5 | P a g e

OVERVIEW

Part 1 of this report explores the causes and effects of the recent recession and lingering effects that severely impacted the U.S. IT industry and workforce during the period 2007-2010. We discuss several related trade and economic-related issues, beginning with the affects of Indian IT consulting and outsourcing firms on the domestic U.S. economy, the role of U.S.-based Multinational Corporations (MNCs), and their historical dominance of employment in the domestic technology and business services sectors, and approaches to removal of lingering regulatory Non-Tariff Barriers to Trade in Services (NTB-TIS) that continue to strain trade relations between the U.S. and India.

This study applies a balance of trade approach to study the impact of competition from the Indian tech sector and “H-1B workers” on the US economy and U.S. immigration policy. We find that the numbers of H-1B petitions approved for Indian nonimmigrant IT specialty workers declined dramatically between FY2007 and FY2008, and that they had little or no net impact on the rise in U.S. unemployment during that period. Looked at in terms of sheer numbers, approximately 200,000 Indian H-1B workers would have minimal impact under any circumstances on employment levels in the four million worker U.S. IT industry. The number of Indian workers in computer-related occupations during the crisis amounted to less than four percent. We show that H-1B workers actually have a positive effect on the bottom-line for U.S. firms, their third-party clients, and the overall U.S. economy, which translates into reduced unemployment and a faster recovery than would have otherwise occurred in this sector. We additionally find that H-1B workers allow third-party U.S. client firms to access some of the enhanced value-added market long enjoyed by large MNCs, a competitive advantage in tradable goods and services which the data shows the overall employment gains in high value-added industries amount to a fifty percent increase in overall employment compared to the low value-added sector.

Specifically, when we apply a value-added measure of the effect of H-1B on the balance of trade in services between the U.S. and India, we see that H-1B workers actually have no real net impact on that balance in the IT sector. We find that since the beginning of the last decade about half of the Indian H-1B temporary workers working in

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

6 | P a g e

computer occupations are actually employed by consulting firms with corporate headquarters in India with the remainder working for U.S. firms. The value-added of Indian H-1B workers is thus split about 50-50 between the two countries. Therefore, we conclude, the presence of Indian H-1Bs working in the US has had no appreciable effect on the US-India balance of trade in services. However, since many U.S. third-party client firms benefit from this labor and expertise, the overall effect in economic terms has been GDP gains, enhancement of firm profitability and global industrial competitiveness that accrues to U.S. industry from continued operation of the H-1B visa program. The bottom-line lesson is that even at a time of rising U.S. unemployment and economic crisis, H-1B is beneficial in terms of GDP, profitability of firms, and maintaining US employment.

We look at a variety of U.S. Government (USG), Government of India (GOI), and OECD data sets, and find that the effects of Indian nonimmigrant workers in domestic industry have had a political impact that is disproportionate and contradictory to their net positive domestic employment and economic effects. We discuss the implications that has had for U.S. trade and immigration policy, which is to reinforce de facto restrictionist immigration measures aimed at India, in particular, complicating bilateral trade relations and impeding liberalization in Trade in Services (TIS) and the ability of U.S. firms to access and conduct global trade and operate profitably in the U.S. market, more generally. Furthermore, we locate the primary source of the actual recent displacement and downsizing of US workers in the IT sector. We find large U.S.-based Multinational Corporations (MNCs) have historically played the dominant role in determining employment levels in the U.S. and global IT sector and are a major influence in the overall steep decline in employment in the U.S. economy during the period 2007-2010. U.S. Commerce Dept. Bureau of Economic Analysis (BEA) data shows the MNCs employ about one-in-five U.S. workers, overall, and about 30 percent of employment in the IT industry, and were the source of lay-offs of U.S. workers at a rate three times that of the national average during the recession that officially began in December 2007 and ended in June 2009, according to the NBER. BEA report shows that between 2007-2008, MNCs sharply reduced payrolls in the US. Domestic layoffs were greatest by U.S.-held multinationals in the non-financial sector,1 with cuts in US R&D of over 2% while simultaneously employment and investment in foreign affiliate R&D increased by 1.1%, most of that increase in

1 See, Barefoot, K. and Mataloni, R.J., “U.S. Multinational Companies Operations Abroad and in the United States”

2008”, (BEA, August 2010), 205-230, 206, http://www.bea.gov/scb/pdf/2010/08%20August/0810_mncs.pdf

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

7 | P a g e

investment in foreign affiliates occurring in India and the BRIC countries. The benefit to India of picking up business due to losses in US employment is also found to be minimal, and the recession has instead had a major negative impact upon the revenues of Indian IT firms during that period. Finally, Part 1 concludes with a discussion of how the U.S. can leverage its continuing advantages in terms of Trade in Services globally by more rational trade-focused regulation of its immigration programs, and how U.S. and Indian policymakers can deal more effectively with the economic and employment effects of MNCs in both markets. Part 2, that follows, explores more closely the recourse that the Government of India (GOI) and India-based IT consulting industry stakeholders have under WTO trade rules to challenge U.S. immigration and labor restrictions on Indian firms and service workers. In this section, we look at the specific bases under WTO rules and precedent decision that would support a complaint by India of preferential and national treatment made before the WTO Dispute Settlement Body (DSB) showing that U.S. immigration law has become an impermissible barrier to trade in violation of the General Agreement on Trade in Services (GATS). We demonstrate how a strong case can be made that the USG has violated its treaty commitments under GATS Modes 3 and 4 by imposing improper regulatory and other Non-Tariff Barriers (NTB) to the entry and commercial presence of Indian companies and Indian national specialty workers in the U.S. Specifically, we identify grounds for a complaint in administrative measures taken in recent years by the USG to restrict visa issuances in the L-1 and H-1B categories. These have had disproportionate economic impact upon India-based consulting firms, and that this along with discriminatory application of fee surcharges, are properly the subject of a consultation process recently started at the WTO by India. Beyond the familiar controversy over H-1B are restrictive measures and de facto discriminatory rules that the U.S. has imposed to withhold L-1 visas needed by multinational companies to do business in the United States. This is an area of concern shared by all multinationals, U.S.-based and Indian companies, alike, and an area of potential common purpose in a dual-track approach to pursuing equitable solutions before the WTO and in the U.S. courts, along with whatever relief may be possible through a deadlocked U.S. political process.

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

8 | P a g e

Part 2 continues with an analysis of the cross-cutting interests held by MNCs and India-based firms and MNCs with U.S. affiliates. This analysis of stakeholders suggests a common strategy toward addressing and countering restrictive administrative measures. In addition, we conclude that U.S. Trade and Immigration policy-makers seem to lack an awareness of the impact that each have on the other, and as a result U.S. agencies and policies sometimes appear to work at cross-purposes. Both areas of policy need to be considered together and a common analytical framework developed that considers economic effects as well as political and institutional interests at stake. This monograph identifies these Non-Tariff Barriers to Trade in Services (NTB-TIS) in U.S. Immigration regulation and identifies some features of a unified conceptual framework based in a more realistic economic analysis of the benefits and costs of foreign workers. We look at US Immigration law and policy with a view toward better conformity with the WTO DSB rulings and the WTO processes and trade rules, and examine US court cases that are relevant and valuable to WTO trade decisions. Finally, the debate over reform of U.S. business Immigration has long been conceptually paralyzed and politically deadlocked within domestic interest group politics. The paper shows how trade law and economics provides a set of practical policy tools, a quantifiable issues-framework, and organized solutions to trade issues that can be applied to immigration to unlock that deadlock. As a cross-disciplinary policy tool, the NTB-TIS framework identifies the linkages and common steps to be taken in efforts to reform both trade and business immigration as part of a comprehensive program of elimination of NTB barriers and harmonization of U.S. Trade in Services with GATS requirements.

***

Executive Summary (Part 1):

At the second anniversary of the Wall Street meltdown of September 2008, the United

States continued to experience its most prolonged period of high unemployment since

the Great Depression. In Q3 2010, joblessness in many sectors of the U.S.

economy, including IT, was still typically double what it was in 2007.

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

9 | P a g e

In a country that has long had what many view as the least adequate social safety net

among the developed western nations, there is undeniable widespread suffering for the

unemployed, as millions of jobless Americans face foreclosures and decline into

poverty. A record 40.8 million Americans are on food stamps and 45% of the

unemployed having been seeking employment for 27 weeks or more, another record

high. The increasingly bleak prospects have made many desperate, fearful, and angry;

it is not surprising that elected officials in both U.S. political parties are seeking a

convenient scapegoat to deflect a growing public discontent with unemployment

and trade policy.

As is the pattern in western countries -- the targets of convenience are immigrants and

foreign-owned companies. In America, public wrath has overwhelmingly focused

on one country, India, and one alleged cause of displacement of U.S. workers:

Indian H-1B temporary workers in the global IT industry, a valuable and growing

market sector where India is challenging historical U.S. dominance.

The policy chosen by the U.S., to restrict foreign temporary workers, actually

exacerbates and accelerates two much larger economic problems: the country’s

enormous deficits in trade and balance of payments, and the planned exit

strategy of Multi-National Corporations (MNCs) to offshore supply-chains,

increase R&D outside the U.S., and otherwise relocate global headquarters

overseas. U.S.-India trade in services and immigration is also a captive of larger trade

and political issues, such as pressures and incentives to India that date from the Bush

Administration pushing India to reinvest some of its growing dollar-denominated foreign

exchange surpluses into the purchase of big-ticket U.S. goods, particularly nuclear

plants and military arms, as well as efforts to open its growing consumer market to large

U.S.-based retailers, particularly Walmart. There is also major pressure applied by U.S.

agricultural interests and other exporters to get India to relax its protection of domestic

farmers and open its markets for goods and services, which remain among the most

restricted by a myriad of complex regulatory barriers of any major U.S. trade partner.

How these larger issues play out in the years to come will to a large degree determine

whether the U.S. again opens its doors to Indian consulting firms and large numbers of

Indian service providers, as it did in the middle of the past decade under the Bush

Administration.

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

10 | P a g e

At present, however, the balance of payments in services, while enormously important

to India, has little overall impact upon the U.S. economy. India accounts for only a tiny

percentage of the overall U.S. trade deficit, and the U.S. actually maintains a huge

global surplus in Trade in Services, including a sizable surplus in computer

services. The US continues to enjoy a large Trade in Services surplus with most of its

primary global trading partners, along with a global surplus in computer services of

$12.6 billion. The total U.S. private services deficit with India, the most effective

global competitor to the U.S. in the IT-BPO sector, is small and declining, only

$159 million in Q1 2010, according to the latest Commerce Dept. data. That

amount is insignificant compared to the quarterly Trade in Goods deficit with

China, which stands at nearly $60 billion.

If the anger of the American people at trade deficits were proportional to their actual

size, we would be more than twice as enraged at Ireland, which currently enjoys an

overall surplus of $11 billion in its trade with the U.S.; Ireland’s Information sector

also receives a disproportionately large share of U.S. Foreign Direct Investment

(FDI), about $5 billion last year in an information sector that employs only 73,000

people, compared to a U.S. FDI of a mere $191 million in an Indian IT services

industry that employs more than two million.

Trade in Services, including computer services, is a long-term winner for America. The

balance of imports to exports of goods, particularly the quarter-trillion dollar annual

deficit in trade in manufactured goods with China and the $43 billion industrial

deficit with Germany, have the heaviest negative impact upon the U.S. economy

and joblessness, which U.S. policy-makers must address, but have thus far failed

to do so with a coherent, sustained industrial strategy. This paralysis is due to

conflicts of interest and the influence wielded in Washington by MNCs and global

banks that are heavily invested in China and other offshore manufacturing

centers.

Since the start of the recession in Q2 2008, MNCs have laid-off U.S. workers at a

rate two to three times greater than other companies. This also has a deleterious

effect on the U.S. balance of trade. In the technology sector, in particular, strategic

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

11 | P a g e

decisions made by U.S.-based multinational corporations have an overwhelming impact

upon U.S. jobs, and the pattern in recent years has been for every plant closed and job

lost here – and there were about 200,000 net U.S. jobs shed in the Information sector in

20092 -- has been expansion of employment abroad by these same companies, but,

notably, not a full one-for-one substitution of jobs. Overall since the recession started in

late 2007, U.S.-based MNCs, which employ one-in-five U.S. workers, have shed more

than two million jobs here, most of them in manufacturing, and more than 150,000 in the

Information sector, while creating some 1.3 million positions offshore. The net result

has been major downsizing of U.S. employment by these same companies with some

offsetting jobs expansion abroad. The result is a significant cut in global payroll costs

and attendant rise in bottom-line corporate profitability. This would appear to indicate

that these same corporations have taken the opportunity of the general economic

decline to carry out global restructuring and downsizing with the intent of enhancing

profitability and retained earnings, largely at the expense of reduced U.S. workforces.

Nonetheless, the trade data shows India did not appear to benefit directly and immediately in jobs or in revenue gains from the massive U.S. layoffs that followed the Wall Street meltdown. As layoffs accelerated to record levels in U.S. industry during 2008-2009, the balance of Trade in Services with India remained almost even. That contradicts the common misconception that during this crisis, American layoffs have resulted in mass substitution by Indian labor in the U.S. and in India.

The number of Indian nationals working in the U.S. IT industry has steeply declined for several years, about a 50 percent drop in new H-1B approvals since 2007. At the same time, contrary to some claims, growth in revenues for the Indian service sector did not swell during the great waves of global layoffs that occurred in early 2009, but actually declined. While the major MNCs consolidated and restructured to shore up their profitability at the bottom of the recession, employment at Indian firms along with U.S. employment were cut.

The trade in services deficit with India, never very large, has practically disappeared in the first half of 2010, a time that one would expect to see rapid expansion of employment in India if there were an actual practice of immediate

2 See, Bureau of Labor Statistics, Table 3: Private sector gross job gains and losses by industry, seasonally adjusted,

http://www.bls.gov/news.release/cewbd.t03.htm,

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

12 | P a g e

offshoring and job transfers. One will have to look at this data in the future to see the longer-term effects and for evidence of an overall transfer of jobs to India.

Even though the trade and jobs data does not support it, the misperception persists that

the Indian consulting industry took unfair advantage of layoffs in the American economy

to gain market share, a myth that generates resentment and is invoked to justify

legislative and regulatory restrictions on its firms and nonimmigrant workers in the U.S.

2009 new hires by Indian IT firms, about 100,000, were fewer than the number of

U.S. positions hired back during the upsurge in domestic IT re-employment of

mid-2009. Overall, Indian IT picked up less than 3500 net positions in its trade

with the US, about one-tenth of one percent of the U.S. Information sector

workforce.

Instead of predatory or opportunistic behavior by Indian firms, the data instead shows

the largest contributor to historically high levels of prolonged IT joblessness is offshore

outsourcing by large U.S.-based Multinational Corporations. In both cases, a major

factor contributing to corporate decisions to move jobs offshore is the declining

revenues and rising costs in the U.S. market due to regulatory restrictions and

increasing compliance risks and costs attendant to a much harsher USCIS and

USDOL enforcement regime. If jobs attached to global supply chains cannot be kept

here, because immigration rules restrict the movement of essential personnel across

borders, then these corporate functions will be – and are – being moved increasingly

offshore by companies established in the U.S, that maintain a U.S. identity for tax and

other reasons. As far as U.S. workers are concerned, offshoring is essentially a

phenomenon of U.S. companies, not one created by foreign competitors.

Globalized supply chains and corporate operations are a fact of life. If companies

cannot continue to provide goods and services in a competitive, cost-effective way in

the U.S., they will and increasingly do relocate offshore. Increasingly, we are seeing

that even high-order Research & Development (R&D), executive, and professional

support functions are now offshored, and this will continue until policies change

and the US is again perceived as a favorable business environment for global

enterprise. The H-1B program allows U.S. firms to compete with large

multinationals on a more even basis, which is also a good thing for U.S. workers.

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

13 | P a g e

PART I: Indian H-1B Consulting Firms or U.S.-based Multinational

Corporations – Which is the Primary Source of IT Sector Unemployment

in the U.S.?

1.1 The Two U.S. Economies and the Dual International Trade

Systems

During 2009, there were some encouraging signs of an U.S. economic

turnaround. However, full recovery has proven elusive, uncertain and highly uneven.

Despite some income gains since the financial sector meltdown, 2010 total American

household net worth remains, at $54.6 trillion, 20 percent less than its 2007 peak3,

leaving disparities in wealth in the United States at the worst levels since the 1930s.

Increasingly, joblessness and declining incomes are claiming highly-educated

professionals and managers, and jobs creation in upper incomes has slowed

disproportionately, with concurrent net job loss in professional and technical services.4

This crisis placed strains upon the U.S. political system, leading to destabilization and

increasingly extreme policy responses, including discriminatory trade measures and

restrictions on business immigration.

3 See,

http://online.wsj.com/article/SB10001424052748704312104575298652567988246.html?mod=WSJ_business_whatsNews 4 See, National Employment Law Project, “A First Look at Private Industry Job Growth & Wages in 2010”,

http://www.nelp.org/page/-/Justice/2010/WhereTheJobsAreAugust2010.pdf?nocdn=1

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

14 | P a g e

Restrictive measures on business and highly-skilled immigration – particularly,

curtailment of the H-1B program -- until recently the marginalized agenda of some

organized labor groups and fringe activists, are now heard from top Congressional

leaders. On August 11, 2010, NY Senator Charles Schumer delivered a speech in

support of a drastic surcharge in filing fees imposed upon L-1 and H-1B visas. In that

speech, he stated that the purpose was to undercut the competitive advantage enjoyed

by India based “chop shops”, as he termed them, over US MNCs in the same industry.5

The measure passed by unanimous consent, and fees were raised by thousands of

dollars. Whether he realized it or not, that message delivered the clearest possible

evidence that the US was deliberately imposing discriminatory measures that

disadvantage Indian firms in direct violation of the WTO General Agreement on Trade in

Services (GATS). In Part 2, below, we discuss how this and similar restrictive U.S.

immigration measures violate GATS and may lead to WTO sanctions and countervailing

measures.

The widening calls for further restrictions on immigration and the employment of

non-immigrant workers is symptomatic of political stresses that have little to do with

displacement of U.S. workers, but are actually caused by the business operations of

U.S.-based multinational corporations (MNCs), which for decades have been offshoring

an increasing percentage of their operations and high-value added functions, as well as

growing alarm at a staggering half-trillion dollar annual deficit in trade in goods with

major trade partners.

Meanwhile, despite a dramatic drop in demand for imports after the Q3 2008 financial markets blowout, the U.S. continues to suffer worsening international trade deficits6. For the year ending June 2010, imports of goods are almost a 2:1 ratio to exports. This is due to a long-term and growing visible trade deficit in the export of manufactured goods, as corporations have been slow to staff up plants and factories and rehire in the U.S. market.

5 See, Statement of Sen. Charles Schumer, Chairman, Senate Immigration Subcommittee, August 11, 2010, Senator

Charles E. Schumer's speech on border Security bill and ...; related, Ariana Unjung Cha, “Indian Gov’t Calls H-1B Fee Hike ‘Discriminatory’”, Washington Post, (Aug. 11, 2010), http://voices.washingtonpost.com/political-economy/2010/08/indian_government_calls_h1b_vi.html 6 See, http://www.census.gov/indicator/www/ustrade.html

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

15 | P a g e

After a drop-off following the 2008 crash, imports and the combined trade deficit have started to trend upward again. In June, 2010 the combined trade deficit rose to $50 billion, the highest level since the Wall Street meltdown. This was offset to a significant degree, however, by the continuing overall surplus the U.S. has long maintained in Trade in Services.

1.2 How U.S.-Based Multinationals Control the Overall Pace and

Location of Global Hiring in the IT Sector

Long-term Competitive Advantages of MNCs in Tradable Goods Has Not

Translated into Gains in U.S. Employment

It is not surprising that large multinational corporations continue to enjoy

international trade advantages over their smaller rivals and national-based

competitors. That has been the case as long as there have been MNCs, which has

been for more than a century in industries such as mining, petrochemicals,

automobile manufacturing, and other capital, technology and labor-intensive

industries. A study by Nobel Laureate Michael Spence and Sandile Hlatshwayo tracks

trends in employment, value added, and value added per employee in the American

economy from 1990 to 2008 and shows that these trends are closely connected with

complementary trends in the size and structure of firms. Scrutinizing historical time

series data from the Bureau of Labor Statistics (BLS) and the Bureau of Economic

Analysis (BEA), U.S. industries are separated into internationally tradable and

nontradable components. Following the trade and employment data, they find:7

Value added grew across the [U.S.] economy, but almost all of the incremental

employment increase of 27.3 million jobs was on the nontradable side. On the

nontradable side, government and health care are the largest employers and provided

the largest increments (an additional 10.4 million jobs) over the past two decades.

7 Spence, M. and Hlatshwayo, S., “The Evolving Sructure of the American Economy and the Employment

Challenge”, The Brookings Institution, Working Paper, (March 2011), http://www.cfr.org/industrial-policy/evolving-structure-american-economy-employment-challenge/p24366

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

16 | P a g e

This points to structural causes of growing U.S. unemployment in a global economy

increasingly dominated by extremely large multinational firms operating in many

jurisdictions. These large MNCs are able to arbitrage labor costs more effectively than

their competitors, and thus reap the benefits of innovations and process improvements

by being the first to offshore new production processes and an increasing percentage of

firm operations to lower-wage affiliates abroad. This process of offshoring tradable

goods and services production, along with central corporate functions such as R&D,

leaves older economies, such as the U.S. holding onto non-tradable sectors and lower

value-added jobs, which result in a significantly slower growing, less profitable, and less

employment-intensive economy, with particular negative and mounting downward push

upon middle-class jobs and earnings. The result, according to the authors:

The trends in value added per employee are consistent with the adverse movements in the distribution of U.S. income over the past twenty years, particularly the subdued income growth in the middle of the income range. The tradable side of the economy is shifting up the value-added chain with lower and middle components of these chains moving abroad, especially to the rapidly growing emerging markets. The latter themselves are moving rapidly up the value-added chains, and higher- paying jobs may therefore leave the United States, following the migration pattern of lower-paying ones. The evolution of the U.S. economy supports the notion of there being a long-term structural challenge with respect to the quantity and quality of employment opportunities in the United States. A related set of challenges concerns the income distribution; almost all incremental employment has occurred in the nontradable sector, which has experienced much slower growth in value added per employee. Because that number is highly correlated with income, it goes a long way to explain the stagnation of wages across large segments of the workforce.

The Declining Value-Added Per Person (VAP)

Trade economists have looked at value-added and employment data and arrived at

estimates for Value Added per Person (VAP) for various occupations, as well as entire

industries, and the national economies in both tradable and nontradable sectors.

In 1990, value added per person employed (VAP) in the tradable and nontradable sectors was rather similar, the tradable sector at almost $80,000, roughly $10,000 above the nontradable figure (see figure 15). But the value added per person

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

17 | P a g e

employed on both sides diverged slowly during the 1990s and then rapidly after 2000. VAP in the tradable sector grew at an average of 2.3 percent per annum, and the nontradable sector at 0.7 percent. By 2008, VAP in the tradable sector was just over 50 percent above that for the nontradable sector.

For a long time, recognition of the importance of immigration to trade was

delayed by conceptual peculiarities of traditional neoliberal economic theory, which held

that migration, trade, and FDI were substitutes for each other. It was long held that an

increase in one would likely preclude a decision by firms to invest in another, a sort of

zero-sum game, which escaped serious challenge until recently. More recent literature

has started to focus on the costs to business and trade of regulatory impediments to

immigration and the free movement of cross-border service providers. Aubry, et al.,

summarize the change in view as follows:8

Standard neoclassical trade theory models trade, migration and FDI as substitutes in the sense that factor movements reduce the scope for trade and vice versa. This neglects the potential for migration to favor trade and FDI through a reduction in bilateral transaction costs, as emphasized by recent literature on migration and diaspora networks.

Those investigators identify a number of studies that identify the categories of

factors for which data exists measuring factors that increase costs of trade measured

for 203 countries. They then applied regressional analysis to develop a theoretical

framework for establishing correlations between these factors, from which this table in

particular emerges:

Table A.2: 2001-2006 Average Trade, No Migration

8 See, Aubry, A., Kugler, M. and Rappaport, H., “Migration, FDI, and the Margins of Trade”, Project of the

"Migration, International Capital Flows and Economic Development" program based at the Harvard Center for International Development and funded by the MacArthur Foundation’s Initiative on Global Migration and Human Mobility. http://econ.biu.ac.il/files/economics/seminars/amandine_aubry.pdf

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

18 | P a g e

(1)

Ind(trade)

Probit

(2)

ln(trade)

ols

(3)

ln(trade)

benchmark

(4)

ln(trade)

nls

(5)

ln(trade)

Polynomial

(6)

ln(trade)

bin 50

(7)

ln(trade)

bin 100

(8)

ln(trade)

firm heterogeneity

(9)

ln(trade) firm

selection

ln(distance) -0.0521∗∗∗ -1.663∗∗∗ -1.663∗∗∗ -1.052∗∗∗ -1.176∗∗∗ -1.154∗∗∗ -1.144∗∗∗ -0.955∗∗∗ -1.732∗∗∗

(0.0028) (0.031) (0.031) (0.063) (0.045) (0.050) (0.050) (0.049) (0.031)

Common border -0.0182 0.725∗∗∗ 0.725∗∗∗ 0.859∗∗∗ 0.847∗∗∗ 0.859∗∗∗ 0.844∗∗∗ 0.884∗∗∗ 0.662∗∗∗

(0.0221) (0.132) (0.132) (0.139) (0.129) (0.128) (0.128) (0.131) (0.134)

Currency union 0.0221∗∗ 0.842∗∗∗ 0.842∗∗∗ 0.491∗∗ 0.516∗∗∗ 0.500∗∗ 0.502∗∗ 0.433∗∗ 0.935∗∗∗

(0.0059) (0.202) (0.202) (0.193) (0.195) (0.196) (0.196) (0.195) (0.205)

Free trade agreement 0.0275∗∗∗ 0.897∗∗∗ 0.897∗∗∗ 0.551∗∗∗ 0.695∗∗∗ 0.675∗∗∗ 0.667∗∗∗ 0.495∗∗∗ 0.881∗∗∗

(0.0034) (0.085) (0.085) (0.097) (0.081) (0.082) (0.082) (0.083) (0.086)

Country is landlocked -0.0139∗ -0.647∗∗∗ -0.647∗∗∗ -0.478∗∗∗ -0.475∗∗∗ -0.477∗∗∗ -0.486∗∗∗ -0.454∗∗∗ -0.673∗∗∗

(0.0077) (0.128) (0.128) (0.124) (0.126) (0.127) (0.127) (0.127) (0.128)

Same legal sytem 0.0075∗∗∗ 0.359∗∗∗ 0.359∗∗∗ 0.262∗∗∗ 0.301∗∗∗ 0.296∗∗∗ 0.298∗∗∗ 0.246∗∗∗ 0.359∗∗∗

(0.0024) (0.046) (0.046) (0.046) (0.046) (0.046) (0.046) (0.046) (0.046)

Same official language 0.0237∗∗∗ 0.819∗∗∗ 0.819∗∗∗ 0.431∗∗∗ 0.478∗∗∗ 0.469∗∗∗ 0.463∗∗∗ 0.372∗∗∗ 0.869∗∗∗

(0.025) (0.065) (0.065) (0.074) (0.069) (0.070) (0.070) (0.069) (0.066)

Colonial tie -0.2913∗∗ 0.541∗∗∗ 0.541∗∗∗ 1.744∗∗∗ 1.451∗∗∗ 1.494∗∗∗ 1.515∗∗∗ 1.932∗∗∗ 0.479∗∗∗

(0.199) (0.175) (0.175) (0.245) (0.168) (0.174) (0.173) (0.176) (0.182)

Time (days) to start a business -0.0955∗∗∗ 0.036 δ

(0.0253) (1.058)

1.126∗∗∗

z

(0.100)

3.250∗∗∗

1.330∗∗∗

(0.527) (0.070)

z2 -0.493∗∗∗

(0.159)

z3 0.028∗

(0.016)

η 0.543∗∗∗

(0.125)

1.810∗∗∗

(0.263)

0.749∗∗∗

(0.118)

Observations 19547 15800 15800 15800 15800 15800 15800 15800 15800

R2 68.7 68.7 69.3 69.5 69.6 69.7 69.3 68.8

Standard errors in parentheses.They are clustered by country pair.

∗ p<0.1, ∗∗ p<0.05, ∗∗∗ p<0.01

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

19 | P a g e

These insights and changing view about the importance of immigration to high

value-added positions and global trade to the overall vitality of firms and the economy

has several implications that suggest the H-1B program actually has significant

advantages in terms of overall job creation, regardless of transient changes in

employment levels. This suggests a set of conclusions and policy approaches as

follows:

First, since employment of H-1B workers convey high value-added along

with the advantages of globalized supply chains and networks to their U.S.

clients, these workers and firms represent a degree of net positive to the

U.S. economy and indirect jobs creation.

H-1B and outsourcing convey competitive benefits and value-added for

U.S. firms that are roughly proportionate, if not equal to, the overall

advantage enjoyed by MNCs, which also enjoy advantages of lower

foreign wages and established and closely-held marketing networks and

customer bases in many overseas jurisdictions which are difficult for

smaller and U.S. firms to quickly replicate. We will therefore arbitrarily

assign a downward corrective factor of .20 to our thumbnail estimate

based upon the competitive advantage cited for MNCs.

U.S. immigration policy should operate so as to increase the overall value-

added of U.S. firms, and policymakers should better understand trade

factors and should take value-added and the distinction between tradable

and non-tradable into consideration.

The implication of a trade-based approach is that immigration policy and

programs should permit a freer flow of global talent into positions for firms

that can demonstrate a potential benefit from high value-added in terms of

their competitiveness and potential improvement in carrying capacity for

employment creation, both direct and indirect, from trade.

To some degree, actual H-1B usage by industry closely tracks the rise of

high-value added occupations, and this shows that U.S. companies are

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

20 | P a g e

reacting in a rational manner to increasing need for skills in some

occupations, as shown in the following tables. The following occupations

are shown to be among those found to be most tradable and fastest

growing in the U.S.:

o Computer systems design

o Management, scientific and technical consulting

o Accounting

o Business support services

o Mining

o Other professional services

o R&D

o Adverstising

o Aerospace

Tradable Industry Jobs Gains, 1990–20089

9 Source: Ibid. 18

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

21 | P a g e

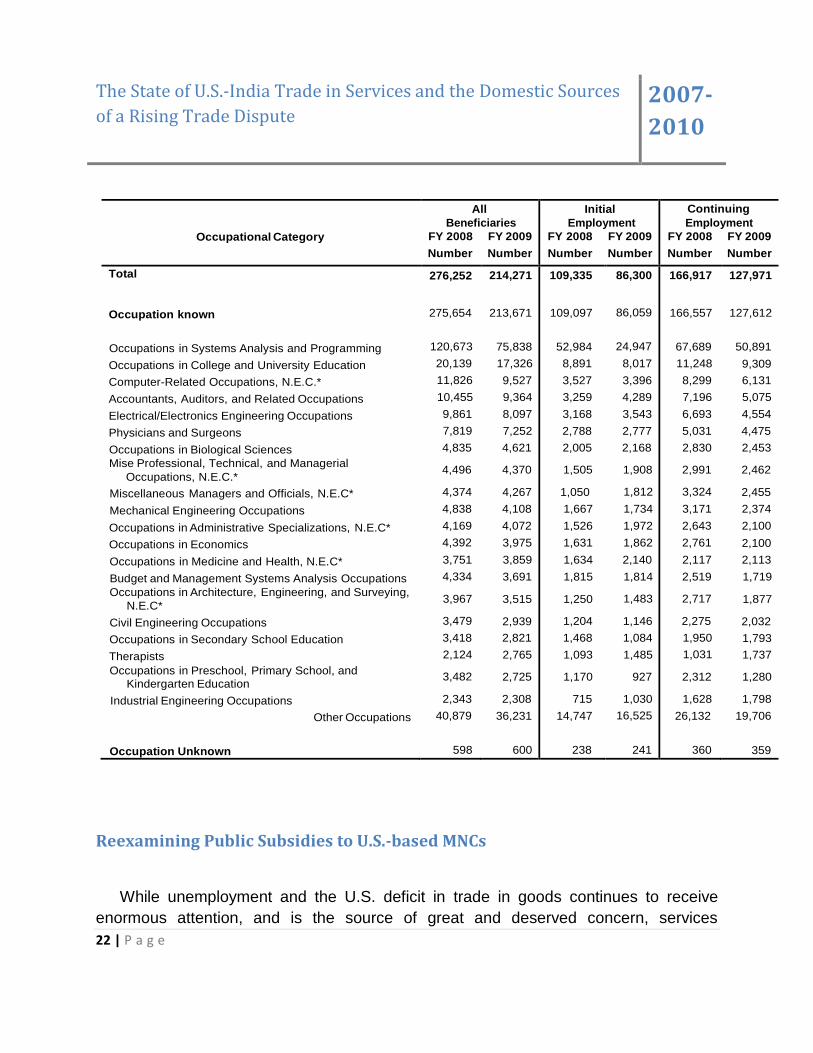

H-1B Approvals by Occupation, FY 2008-0910

Table 9A. H-lB Petitions Approved by Detailed Occupation of Beneficiary and Type of Petition (Number): Fiscal Years 2008 and 2009

10

Source: USCIS Characteristics of H-1B Specialty Workers, (FY 2009), Table 9A, http://www.uscis.gov/USCIS/Resources/Reports%20and%20Studies/H-1B/h1b-fy-09-characteristics.pdf

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

22 | P a g e

Occupational Category

All

Beneficiaries

FY 2008 FY 2009

Number Number

Initial

Employment

FY 2008 FY 2009

Number Number

Continuing

Employment

FY 2008 FY 2009

Number Number

Total

Occupation known

Occupations in Systems Analysis and Programming

Occupations in College and University Education

Computer-Related Occupations, N.E.C.*

Accountants, Auditors, and Related Occupations

Electrical/Electronics Engineering Occupations

Physicians and Surgeons

Occupations in Biological Sciences

Mise Professional, Technical, and Managerial

Occupations, N.E.C.*

Miscellaneous Managers and Officials, N.E.C*

Mechanical Engineering Occupations

Occupations in Administrative Specializations, N.E.C*

Occupations in Economics

Occupations in Medicine and Health, N.E.C*

Budget and Management Systems Analysis Occupations

Occupations in Architecture, Engineering, and Surveying,

N.E.C*

Civil Engineering Occupations

Occupations in Secondary School Education

Therapists

Occupations in Preschool, Primary School, and Kindergarten Education

Industrial Engineering Occupations

Other Occupations

Occupation Unknown

276,252

275,654

120,673

20,139

11,826

10,455

9,861

7,819

4,835

4,496

4,374

4,838

4,169

4,392

3,751

4,334

3,967

3,479

3,418

2,124

3,482

2,343

40,879

598

214,271

213,671

75,838

17,326

9,527

9,364

8,097

7,252

4,621

4,370

4,267

4,108

4,072

3,975

3,859

3,691

3,515

2,939

2,821

2,765

2,725

2,308

36,231

600

109,335

109,097

52,984

8,891

3,527

3,259

3,168

2,788

2,005

1,505

1,050

1,667

1,526

1,631

1,634

1,815

1,250

1,204

1,468

1,093

1,170

715

14,747

238

86,300

86,059

24,947

8,017

3,396

4,289

3,543

2,777

2,168

1,908

1,812

1,734

1,972

1,862

2,140

1,814

1,483

1,146

1,084

1,485

927

1,030

16,525

241

166,917

166,557

67,689

11,248

8,299

7,196

6,693

5,031

2,830

2,991

3,324

3,171

2,643

2,761

2,117

2,519

2,717

2,275

1,950

1,031

2,312

1,628

26,132

360

127,971

127,612

50,891

9,309

6,131

5,075

4,554

4,475

2,453

2,462

2,455

2,374

2,100

2,100

2,113

1,719

1,877

2,032

1,793

1,737

1,280

1,798

19,706

359

Reexamining Public Subsidies to U.S.-based MNCs

While unemployment and the U.S. deficit in trade in goods continues to receive

enormous attention, and is the source of great and deserved concern, services

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

23 | P a g e

represent nearly 78% of US economic output, and a similar proportion of private

employment. In terms of global trade, the services side of the U.S. economy continues

to be relatively robust, and the US still dominates bi-lateral Trade in Services with most

of its partners. To some extent, this is due to the vast public subsidies that are pumped

into the U.S. financial system much of which flow to MNCs.

However central and necessary they are to the U.S. economy, and they are the

source of development of many key innovations, MNCs have been a central source of

a multitude of problems, leading to the outflow of capital and high value added jobs

resulting in structural unemployment and disinvestment in low value added sectors in

the U.S. While problematic, large MNCs are among the most heavily subsidized entities

in the U.S., which gives them an even greater competitive advantage over smaller

competitors, preferential treatment that offends both free trade principles and basic

fairness.

Net capital outflows by large global firms now present serious long-term

competitiveness problems for the U.S. Foreign Direct Investment (FDI) by U.S.-based

MNCs has escalated steadily in recent years, climbing from $2.4 Trillion to $3.5 Trillion

during 2005-09.11 Globalized firms are flush with cash, both from global earnings and

from massive infusions of federal bailouts12 and stimulus money along with historically

cheap dollars pumped into the system by the U.S. Federal Reserve and other central

11

See, US Dept. of Commerce, Bureau of Economic Analysis (BEA), Operations of Multinational Companies,

http://www.bea.gov/international/di1usdbal.htm, Industry detail (includes all industries), Position on a historical-

cost basis, total financial flows without current-cost adjustment, and income without current-cost adjustment,

2005-2009| XLS

12 One of the biggest beneficiaries of TARP is AIG, which received $180 billion to cover its losses from distressed

assets and its huge portfolio of derivatives. However, as the AIG Congressional Oversight Panel report found (p

159), http://www.gpo.gov/fdsys/pkg/CPRT-111JPRT56698/html/CPRT-111JPRT56698.htm : “AIG, for example,

used part of its bailout funds to repay debts owed through financial trades to other banking institutions,including

$12.9 billion to Goldman Sachs, $11.9 billion to Societe Generale, $11.8 billion to Deutsche Bank, $8.5 billion to

Barclays, $6.8 billion to Merrill Lynch, and $5.2 billion to Bank of America. These payments led some to question

whether the AIG bailout was in fact an AIG creditor bailout. AIG then paid out $165 million in retention bonuses to

executives at AIG FP, the division that engaged in the MBS transactions that brought AIG to the brink of disaster.”

[citations omitted]

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

24 | P a g e

banks. While the U.S. Congress and Treasury have been generous in bailing-out global

financial and industrial firms, policymakers have been lax in attaching explicit conditions

on how and where these funds are spent. Evidence mounts that global banks and

MNCs, some of which received TARP assistance, continue to offshore profits and

refuse to repatriate them until Congress and the Administration grant tax concessions.

The result has been net disinvestment by global firms and an outward drain of capital,

revenues, and jobs.

The Congressional Research Service estimates U.S. multinational firms avoid

anywhere from $10 billion to $60 billion a year in taxes because of loopholes in the tax

code favoring offshore retention of profits. 83 of the 100 largest publicly traded U.S.

corporations have subsidiaries in locations listed as tax havens or financial privacy

jurisdictions. Because of incentives in the US tax code, MNCs have steadily increased

the amount of undistributed foreign earnings they “park” offshore, that doubling about

every five years since the1990s. 13 The total cumulative amount of undistributed

earnings held by offshore affiliates of US-based MNCs amounts to more than $1 trillion.

This has also led to serious revenue and deficit problems. GE and GM, two of

the largest and oldest U.S.-based multinationals reportedly paid no taxes in 2008, due

in large part to reported losses in domestic sales and because of their operations in

offshore tax havens. 14

An analysis of the flow of funds effects of large global firms receiving TARP funds reports, "in 2008, Goldman Sachs, with 29 subsidiaries located in offshore tax havens, reported profits of over $2 billion and paid federal taxes of $14 million, an effective tax rate of just one percent, and less than one third what they paid their CEO Lloyd Blankfein ($42.9 million)."

The offshoring of revenues exacerbates an ongoing imbalance in the flow of

international investment favoring FDI over reinvestment. The U.S. International Trade

13

See,Blouin, J., “Is U.S. Multinational Intra-Firm Dividend Policy Influenced by Reporting Requirements?”, NYU School of Law Conference, (December 11, 2011), http://www.law.nyu.edu/ecm_dlv4/groups/public/@nyu_law_website__academics__colloquia__tax_policy/documents/documents/ecm_pro_068362.pdf 14

See, Congressional research Service, “Large US Corporations and Federal Contractors with Subsidiaries in Jurisdictions listed as Tax Havens or Financial Privacy Jurisdictions“ (December 2008), http://www.gao.gov/new.items/d09157.pdf

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

25 | P a g e

Commission has shown that MNCs are the primary drivers of FDI, and that for decades

US Direct Investment Abroad (USDIA) has exceeded Foreign Direct Investment in the

United States (FDIUS) by about 25 percent. A USITC study concluded15:

[T]he position (stock) of USDIA has exceeded that of FDIUS in every year since 1982.

Preliminary data for 2005 show the total USDIA position at $2.1 trillion, compared with an

FDIUS position of $1.6 trillion. Both USDIA and FDIUS have grown steadily since 1982,

averaging annually 11 percent for USDIA and 12 percent for FDIUS. For the years 2000-

2005, average annual growth has been 9 percent for USDIA and 5 percent for FDIUS.

According to the U.S. census, U.S. capital investment in foreign countries has risen

dramatically from $1.3 trillion in 2000 to $3.2 trillion in 2008. The vast majority of this

FDI is targeted at manufacturing, invested directly or indirectly in expansion of offshore

factories, much of it flowing through intermediary companies in Europe to affiliates in

high-growth, low-wage countries. Only about a quarter goes to offshore investments in

services. From 2005-09, annual FDI by US firms in foreign manufacturing increased

steadily from $431 to $541 billion. By comparison, U.S. investments in the overall

global Information industry is smaller but faster growing, increasing from $103 to $150

billion, of which the subcategory of investment in Internet, Data Processing and Other

Information Services grew from $9 to $25 billion per year over that period.16 In a

different industrial category for Professional, Scientific and Technical Services, foreign

investment in computer systems design and related services by U.S.-based

multinationals went up during this period from $28 to $42 billion, but fell off again to $34

billion in 2009 following the onset of the global financial crisis.17 This drop-off in foreign

investment in this services sector is an important point as we explain, below.

Indian Information firms have not been the major destination for US FDI in recent

years that it is often imagined to be. Looking at a different BEA data subset that shows

the country of destination, we see that of the $248 billion in “U.S. Direct Investment

15

See, Laura Bloodgood, Inbound and Outbound U.S. Direct Investment With Leading Partner Countries, USITA, (2007) http://www.usitc.gov/publications/332/journals/inbound_outbound_investment.pdf 16See, (BEA), Operations of Multinational Companies, http://www.bea.gov/international/di1usdbal.htm, Industry

detail (includes all industries), Position on a historical-cost basis, total financial flows without current-cost

adjustment, and income without current-cost adjustment, 2005-2009| XLS

17 Ibid., Line 195.

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

26 | P a g e

Abroad: Financial Outflows Without Current-Cost Adjustment18, 2009”, $11.7 billion

went into Information worldwide, of which only $191 million were shown to be invested

in the Indian Information sector19. Strangely, by far the single largest U.S. FDI

destination during 2009 in the Information sector in this data set is the $5.9 billion

invested in Ireland20, which has a miniscule Information sector that employs a mere

73,000 workers21 compared to 3.9 million in the U.S. and 2.2 million in India.

Using the same Commerce Dept. data set for Financial Outflows Without

Current-Cost Adjustment, 2009, the most recent trade data shows that FDI outflows

from the U.S. into the global IT sector are again on the rise. According to that

measure, U.S. worldwide FDI in global manufacturing was $47.7 billion, Europe ($30.6

billion), and the ASEAN countries ($5.4 billion), and China (about $6 billion)22 , which

gives us an idea of the relative scale of annual reported FDI outflows, but may not fully

track the flow of funds to various eventual destinations.

We may also compare that with the combined $16.4 billion (2009) of MNC

reinvested corporate earnings in Information23 and professional, scientific and technical

services worldwide.24 Worldwide investments by multinationals in FDI and their retained

global earnings in Information dwarf the U.S. trade deficit in technology-related services

18

The “current cost adjustment” method adds significantly to the stated value of the investment, as it reflects “book value” of the investment rather than the actual outward capital flow. See, http://www.gt-eins.de/Bilder/CER04/cer04.html 19

BEA, U.S. Direct Investment Abroad: Financial Outflows Without Current-Cost Adjustment, 2009 Lines B5, N5 and N79. 20

Ireland appears instead to have become a destination for MNC overseas profits “parking” as well as an intermediary. See, Frank Barry, “Making Sense of the Data on Ireland’s Inward FDI”, Jour, of Stat. & Socio Soc. Of Ireland, Vol. XXXIV, (17 Nov 2004), http://www.tara.tcd.ie/bitstream/2262/8778/4/JssisiVolXXXIV28_65.pdf 21

Central Statistics Office, Ireland, http://www.cso.ie/statistics/empandunempilo.htm

22 2009 Chinese outbound FDI to the US at an estimated $6.4 billion may have exceeded reported inbound FDI

flows. See, http://www.bilaterals.org/spip.php?article17652; however, US investment in Hong Kong matched that figure dollar for dollar. See, [ftn.8], Lines B77, 78. BEA shows 2009 US FDI in China and Hong Kong Information sectors were $38 and $172 million, respectively. 23

Note: The BEA table, 2009 U.S. Direct Investment Position Abroad on a Historical-Cost Basis: Industry Detail for Selected Countries - MNC Direct Investment Abroad category for “Information” includes a number of media and data subcategories, the annual value of which add up to $150 billion. Worldwide, software publishing accounts for $50 billion and Internet, Data Processing, and other Information Services for another $25 billion. 24

See, BEA, US Direct Investment Abroad, Annual Data, Reinvested Earnings without current cost adjustment, 2009.

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

27 | P a g e

with India, which in Q1 2010 stood at a mere $344 million, and the even smaller FDI

outflow from the US to the Indian information sector of $191 million in all of 2009,

according to BEA data.

Barefoot and Mataloni’s BEA study25 shows that during the period 2007-08,

MNCs reduced their US parent payrolls at a rate more than three times that of other US

employers. The MNCs simultaneously increased their nonfinancial acquisitions and

hirings abroad, particularly in R&D and technical services, while cutting U.S. staff in

these areas by a larger amount. The report finds:

Employment

In 2008, employment by nonbank U.S. MNCs decreased 1.1 percent to 31.2 million workers, reflecting partly offsetting changes for U.S. parents and foreign affiliates. The employment by U.S. parents decreased 2.1 percent to 21.1 million; the largest decreases were in “other industries,” in manufacturing, and in nonbank finance and insurance. The decrease in “other industries” was concentrated in “administration, support, and waste management” (mainly temporary employment services); the decrease in manufacturing was largest in transportation equipment, mainly motor vehicles; and the decrease in nonbank finance and insurance was concentrated in nonbank finance. The 2.1 percent decrease in parent employment, which mainly reflected decreases by companies that were parents in both 2007 and 2008, was greater than the 0.6 percent decrease in employment for all U.S. private nonbank industries. Employment by foreign affiliates increased 1.1 percent to 10.1 million. By area, the

largest increases in level were in Asia and Pacific (mainly China and India). By industry,

the largest increases were in “other industries” (mainly retail trade and “accommodation

and food services”) and “professional, scientific, and technical services.”

Meanwhile, these firms cut R&D expenditures in the US26 and UK27 by 2.2% and 14.1%,

respectively. This reflects the ongoing shift abroad of the most highly skilled technical

operations carried out by MNCs:28

In 2008, expenditures for R&D performed by nonbank U.S. parents decreased 2.2 percent to $199.1 billion. In contrast, R&D performed by all U.S. businesses increased 5.2 percent; as a result, the parent share of total private R&D performed in the United States decreased to 70.3 percent in 2008, from 75.6 percent in 2007.

25

Barefoot and Mataloni, Ibid. 220. 26

Ibid., 212. 27

Ibid., 220. 28

Ibid., 214.

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

28 | P a g e

The authors observe about US affiliate R&D hiring in the BRIC countries including

India:29

R&D expenditures in the BRIC countries continued to grow; the share of affiliate R&D

expenditures in these countries grew to 8.1 percent of total affiliate R&D in 2008 from

4.1 percent in 2004. The 2008 increase was partly due to strong growth in India and

Brazil, both of which experienced double-digit growth in affiliate R&D. Indian affiliates’

R&D expenditures increased 52.4 percent or $0.2 billion. By industry, a large portion of

the Indian R&D expenditures were in computers and electronic products manufacturing

and in professional, scientific, and technical services. The growth in R&D expenditures

by Indian affiliates appears to be driven by the expanded capabilities for R&D and

government support in India, which includes the development of an R&D infrastructure,

research funding, and increased education for human resource development.

The overall U.S. trade deficit last year would have been far worse, had not total

imports dropped by nearly $700 billion, about 25 percent, reflecting similar declines in

U.S. household net worth after the Wall Street crash. In terms of trade, however, this

was offset by a $270 billion decline in total U.S. exports in 2009. 30 In most sectors, the

drop in U.S. imports of goods exceeded the decline in U.S. exports.

The U.S. trade deficit receives a lot of attention, but the deficit in domestic

reinvestment and jobs creation by multinational corporations is rarely publicly

discussed. For decades, the balance of U.S. trade has been marked by mounting

deficits in goods as US-based companies have expanded industrial manufacturing and

assembly facilities abroad, exported goods back to the U.S. market, but not fully

repatriating the taxable earnings that might have resulted from those investments. All

the while, many of these same companies have been realizing a smaller, but consistent,

earnings surplus in global Trade in Services. For 2009, the U.S. trade deficit in goods

was $507 billion whilst the surplus in U.S. net services exports stood at $132 billion,

only a slight drop from the previous record year.

The staggering rise in the deficit in trade in goods accompanies the offshoring of

manufacturing jobs by U.S.-based multinational corporations is more widely understood.

29

Ibid.,220. 30

See, Id.

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

29 | P a g e

The net loss in U.S. employment accompanying the move to offshore manufacturing is

estimated to be more than two million U.S. positions resulting in a shift of about 1.3

million jobs abroad since 2007. Based upon Commerce Dept data and analysis, U.S.-

based multinationals employ one in five U.S. workers, 31 but carried out layoffs in 2008

at a rate more than twice all U.S. businesses.32 Our estimate of U.S. jobs elimination by

MNCs may be conservative, given that as many as 11 million U.S. positions have been

eliminated since the start of the current recession in late 2007.33

1.3 U.S.-India Terms of Trade in Services: Small and Relatively

Stable

Overall, U.S. trade with India is not a major factor in the global U.S. balance of accounts

problems. India is far down the list in terms of the total U.S. deficit of trade, at $5.164

billion for the year to date in 2010, it isn’t even close to making the top-ten list -- by

comparison, Ireland has a trade surplus that is more than twice as large:34

Table 1. Top Ten Countries with which the U.S. has a Trade Deficit

For the month of June 2010

Year To Date Deficit in Deficit in Millions Millions Country Name of U.S. $ of U.S. $ China -26,151.50 -119,451.79 Mexico -6,208.23 -33,120.90

31

See, See, BEA, Summary Estimates for Multinational Companies: Employment, Sales, and Capital Expenditures for 2008, April 16, 2010, http://www.bea.gov/newsreleases/international/mnc/2010/mnc2008.htm 32

See, Ibid. 33

See, http://www.investingcontrarian.com/index.php/financial-news-network/a-7-million-increase-in-us-population-results-in-a-labor-force-decline-why-the-us-has-really-lost-11-2-million-jobs-this-recession-2/. 34

See, http://www.census.gov/foreign-trade/statistics/country/index.html

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

30 | P a g e

Japan -5,246.87 -26,634.69 Federal Republic of Germany -3,056.90 -15,129.75 Canada -2,583.61 -16,880.93 Nigeria -2,343.98 -12,828.27 Ireland -2,298.23 -11,884.83 Russia -1,988.07 -9,280.41 Saudi Arabia -1,920.99 -9,516.04 Venezuela -1,695.84 -11,420.88

Instead, India distinguishes itself in its dynamic and growing Information Technology

(IT) and Business Process Outsourcing (BPO) industries, in which it now ranks second

in the world behind the United States.

Overall, the U.S. continues to enjoy a large global surplus in its terms of trade in

services. For 2008, U.S. global exports of business, professional, and technical

services, including computer services, amounted to $125 billion35, which dwarfed the

combined trade deficit with India, and indeed, exceeds the year-to-date deficit with

every other country.36

The 2009 U.S. deficit in trade in goods with India declined by nearly 40 percent

from its peak level the year before of $8.5 billion. After a lull following the financial crisis

of early 2009, U.S.-India trade rebounded sharply later in the year, and has skyrocketed

in early 2010, almost entirely due to a surge in U.S. imports of Indian-made goods from

$5.6 to $6.6 billion.

Meanwhile, the Q1 2010 U.S. deficit in trade in services with India – one of the

few countries where that U.S. account is in the red – which in 2008 stood at $1.6 billion

-- declined, and now stands at a quarterly figure of $159 million.37 [See, Tables 2-5,

below] [NOTE: This data includes income from imports of foreign affiliates of U.S.-

based MNCs. The BEA definition of exports excludes U.S. parents' payments to foreign

affiliates but includes U.S. affiliates' receipts from foreign parents. That definition of

35

See, BEA, Trade in Goods and Services, 1992-present, Table 1a (Excel) 36

See, http://www.census.gov/foreign-trade/balance/c5330.html#2008, (2008, last year for detailed sectoral breakdown) 37

See, BEA, http://www.bea.gov/international/bp_web/simple.cfm?anon=514770&table_id=10&area_id=37, data for US-India trade in goods and services, Table 12, reproduced at Appendix I.

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

31 | P a g e

imports also includes U.S. parents' payments to foreign affiliates but excludes U.S.

affiliates' receipts from foreign parents.]

The most detailed current BEA data for exports and imports of U.S.-India

services is for Q1 2010, which at Table 12, International Transactions Account Data,

shows the U.S. deficit in services with India was a mere $159 million. More specifically,

U.S. exports to India of “Other private services” (Table 2, line 4, below) were $2 billion,

while U.S. imports of same from India (Table 3, line 7, below) were $2.3 billion. This

indicates a current quarter private-sector Trade in Services deficit in Information and

business services (excluding air travel, transportation, royalties and license fees) of

$345 million.38 That figure includes all private-sector consulting and offshoring

services, including financial, business process, educational, legal, as well as Information

Technology, the deficit in which we estimate at slightly less than half of that total figure,

or about $150 million.

Table 2: US EXPORTS OF GOODS AND SERVICES TO INDIA (Q1 2009-Q1 2010)39

U.S. International Transactions, by Area - India 28

[Millions of dollars, not seasonally adjusted]

Li

ne (Credits +; debits -)

1

2009 2010

I II III IV I p

Current account

1 Exports of goods and services and

income receipts

6

6,862

7

7,736

8

8,472

6

6,684

7

7,913

2 Exports of goods and services 6,073 6,725 7,714 6,001 6,982

38

See, BEA, http://www.bea.gov/international/bp_web/simple.cfm?anon=514770&table_id=10&area_id=37 39

Ibid.

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

32 | P a g e

3 Goods, balance of payments basis2 3,323 4,169 5,010 4,007 4,012

4 Services3 2,750 2,556 2,704 1,995 2,970

5 Transfers under U.S. military

agency sales contracts4 1 4 3 3 5

6 Travel 516 888 741 432 523

7 Passenger fares 224 326 292 146 210

8 Other transportation 73 73 87 75 90

9 Royalties and license fees5 177 334 190 165 139

10 Other private services5 1,746 918 1,377 1,160 1,989

11 U.S. government miscellaneous

services 12 13 14 15 14

Table 3: US IMPORTS OF GOODS AND SERVICES FROM INDIA (Q1 2009-Q1 2010)

[Millions of dollars, not seasonally adjusted]

Lline (Credits +; debits -) 1

2009 2010

I II III IV I p

Current account

18 Imports of goods and services and income payments -8,723 -8,365 -9,012 -9,215 -10,163

19 Imports of goods and services -8,291 -7,969 -8,657 -8,805 -9,711

20 Goods, balance of payments basis2 -5,210 -4,969 -5,564 -5,559 -6,582

21 Services3 -3,081 -3,000 -3,093 -3,247 -3,129

22 Direct defense expenditures -4 -1 -5 -4 -4

The State of U.S.-India Trade in Services and the Domestic Sources

of a Rising Trade Dispute 2007-

2010

33 | P a g e

23 Travel -641 -489 -590 -682 -631

24 Passenger fares -72 -33 -39 -60 -72

25 Other transportation -29 -18 -39 -27 -45

26 Royalties and license fees5 -22 -32 -28 -36 -36

27 Other private services5 -2,306 -2,420 -2,385 -2,431 -2,334

28 U.S. government miscellaneous services -8 -7 -7 -7 -7

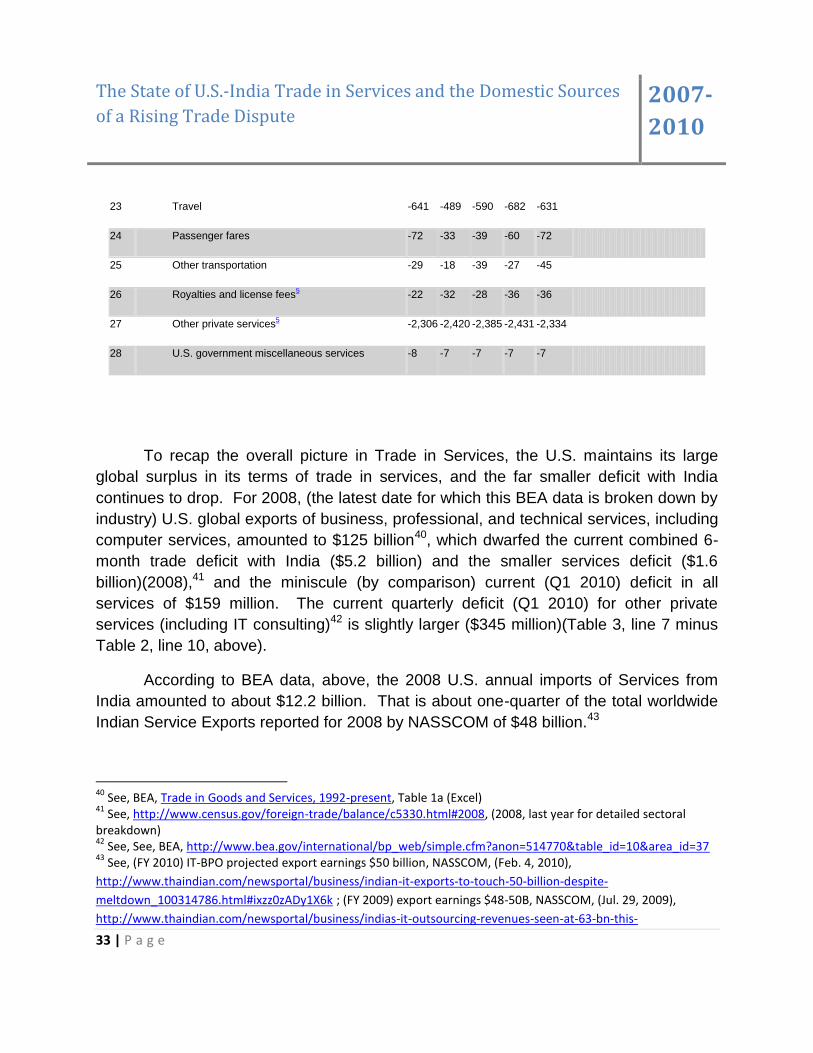

To recap the overall picture in Trade in Services, the U.S. maintains its large

global surplus in its terms of trade in services, and the far smaller deficit with India

continues to drop. For 2008, (the latest date for which this BEA data is broken down by

industry) U.S. global exports of business, professional, and technical services, including

computer services, amounted to $125 billion40, which dwarfed the current combined 6-

month trade deficit with India ($5.2 billion) and the smaller services deficit ($1.6

billion)(2008),41 and the miniscule (by comparison) current (Q1 2010) deficit in all

services of $159 million. The current quarterly deficit (Q1 2010) for other private

services (including IT consulting)42 is slightly larger ($345 million)(Table 3, line 7 minus

Table 2, line 10, above).

According to BEA data, above, the 2008 U.S. annual imports of Services from

India amounted to about $12.2 billion. That is about one-quarter of the total worldwide

Indian Service Exports reported for 2008 by NASSCOM of $48 billion.43

40

See, BEA, Trade in Goods and Services, 1992-present, Table 1a (Excel) 41

See, http://www.census.gov/foreign-trade/balance/c5330.html#2008, (2008, last year for detailed sectoral breakdown) 42

See, See, BEA, http://www.bea.gov/international/bp_web/simple.cfm?anon=514770&table_id=10&area_id=37 43

See, (FY 2010) IT-BPO projected export earnings $50 billion, NASSCOM, (Feb. 4, 2010),

http://www.thaindian.com/newsportal/business/indian-it-exports-to-touch-50-billion-despite-

meltdown_100314786.html#ixzz0zADy1X6k ; (FY 2009) export earnings $48-50B, NASSCOM, (Jul. 29, 2009),