a history of philanthropic...

TRANSCRIPT

A HISTORY OF PHILANTHROPIC FOUNDATIONS: THE ISLAMIC WORLD FROM THE SEVENTH CENTURY TO THE PRESENT

BY

MURAT Ç�ZAKÇA ECONOMICS DEPARTMENT

BOGAZICI UNIVERSITY ISTANBUL

EIGHTH DRAFT

2

TABLE OF CONTENTS

Acknowledgements Chapter One: Economic Dimension and Origins

I. Introduction II. Economic Dimension III. The Origins IV. Impact on Others

Chapter Two: Functioning of the System and Judicial Problems I. The Founders

1. The Ten Conditions II. Beneficiaries and the Family Waqf Controversy III. The Trustees (mutawallis) IV. The Original Capital of the Endowment (Corpus) Chapter Three: Cash Waqfs in the Islamic World

I. Legal Issues 1. Introduction 2. The Hanafi Position on the Waqf of Movables (Cash Waqfs) 3. The Shafi’i Position 4. The Maliki Position 5. The Hanbali Position 6. The Shi’ite Position

II. Cash Waqfs in History and Present 1. Introduction 2. Cash Waqfs in the Ottoman Economy 3. Decline of the Ottoman Cash Waqfs 4. Cash Waqfs in Syria 5. Cash Waqfs in Egypt 6. Cash Waqfs in Central Asia 7. Cash Waqfs in India 8. Cash Waqfs in Malaysia and Singapore

Chapter Four: Centralization of the Waqf System I. Introduction II. Centralization in the Ottoman Empire and Turkey

1. The Turkish Republic 2. Survival and Restoration of Waqfs in Turkey

III. Egypt 1. Egyptian Waqfs Under the Mamluks 2. Egyptian Waqfs Under the Ottomans 3. Crises in the Late Ottoman Era and the Republic

IV. The Sudan V. Morocco

VI. Iran VII. India

1. Introduction 2. Legal Issues 3. The Central Waqf Act, 1954 4. Taxation of Waqfs in India 5. The Waqf Act, 1995

3

VIII. Waqfs in Pakistan and Bangladesh IX. Waqfs in Malaysia and Singapore

1. Introduction 2. Legal Issues 3. Waqf Administration in Malaysia

X. Waqfs in Philippines XI. Conclusion Bibliography Glossary General Index

4

ACKNOWLEDGEMENTS

This book has been written during a sabbatical leave. I am grateful to my colleagues at Bo�aziçi University, Istanbul, for granting me this precious opportunity.

I spent the first part of my sabbatical leave at the International Institute of Islamic Thought and Civilization (ISTAC) in Kuala Lumpur, Malaysia. This was the second time Professor Dr. Syed Muhammad Naquib al-Attas, the Founder-Director of ISTAC, had invited me to his institute and so my foremost thanks go to him. Actually, it is becoming habitual for me to thank Professor al-Attas, for it was in the same institute, even in the same room, that I had completed the first draft of my previous book A Comparative Evolution of Business Partnerships a few years ago. By a marvellous coincidence, the published version of it was handed to me by the postman the day I arrived at ISTAC for my second sabbatical. I thought this was a good sign and started my work on the present book with renewed vigour.

I fully utilised everything ISTAC had to offer: I greatly benefited from the superb library and would like to thank particularly Haji Ali Haji Ahmad, the Chief Librarian, for his friendly support. I was constantly encouraged and supported by my colleagues at ISTAC. Special thanks are due to Professors Alparslan Açıkgenç, Wan Mohd Nor Wan Daud (ISTAC’s Acting Deputy Director), Teoman Duralı, Mehmet �p�irli, Bilal Ku�pınar and Sabri Orman for their constant encouragement and constructive criticism. Professor Ahmad Kazemi Moussavi played a special role in obtaining information for me on the current laws pertaining to waqfs in the Islamic Republic of Iran. I would like to thank, in the same context, H.E. Ali Reza Dardmand, Cultural Attaché, Embassy of the Islamic Republic of Iran in Kuala Lumpur, and the authorities in the Endowments and Charity Affairs Organisation in Teheran, Iran. In Kuala Lumpur I found support from sources outside ISTAC as well. Royal Professor Ungku Abdul Aziz shared with me his precious time and knowledge. Dr. Zeti Akhtar Aziz, Assistant Governor of the Central Bank of Malaysia, allowed me to interview bank officials. Professor Ahmad Ibrahim of the International Islamic University, Malaysia introduced me to his important work on the present situation of waqf law in Malaysia. Professor Syed Khalid Rashid of the same university and an authority on the history of the Indian waqf system, generously gave me his time and read the part on Indian waqfs. I also benefited greatly from the research papers by my students participating in the Poverty Alleviation seminar. Some of the papers written by these young scholars were so original and important that I have not hesitated to refer to them in this book.

Professor Faruk Bilici of Institut National des Langues et Civilisations Orientales provided support all the way from Paris and, my sister, Professor Dr. Çi�dem Ka�ıtçıba�ı of Koç University, Istanbul, sent me important material concerning the well-known Vehbi Koç Foundation. After having returned to Turkey, I have had the opportunity to interview Rahmi Koç, Aydın Bolak, Turhan Esener and Erdal Yıldırım about the Vehbi Koç Foundation as well as the drafting of the 1967 Law. I am grateful to all of them. Special thanks are also due to Sharifah Shifa al-Attas, General Editor of ISTAC, and Aida Melly Tan Mutalib, Editorial Assistant, as well as Sylvia Jones who read the entire manuscript and made innumerable corrections. While I am grateful to all of these colleagues, it goes without saying that I, alone, bear all the responsibility for any shortcomings and mistakes. Finally, I would like to thank my wife, Kitty Çizakça for reading the entire manuscript and sharing my life, together with my daughter Defne, in Kuala Lumpur.

5

TO THE FOUNDER-DIRECTOR, FACULTY AND STUDENTS OF ISTAC

6

NOTES ON TRANSLITERATION AND PRONUNCIATION

All foreign words, excluding foreign names, are italicised except the word waqf and its plural awqaf. These words appear so frequently throughout the text that it has been decided not to italicise them. Although I have generally preferred for the plural, waqfs rather than the Arabic plural awqaf, I have occasionally used the latter in order to avoid repetition. Most transliterations follow modern Turkish spelling, even for words, which originated in Arabic or Persian. If such words, however, have become part of English in their Arabic versions, then their Arabic transliteration has been preferred. Thus, waqf (and not vakıf) has been used. Turkish words, which have become anglicised, have been kept in the latter form. Thus pasha (and not Pasha) has been used. For those who are unfamiliar with the pronunciation of modern Turkish spelling, the following rudimentary rules (according to Geffery Lewis’ grammar) may be of some help: c is pronounced j as in jam; ç is pronounced ch as in church; g is pronounced as in the word goat; � lengthens the vowel preceding it; y sounds like the u in radium; ö and ü as in German könig and führer respectively; and � is pronounced as in sh in shall.

LIST OF TABLES

Table 1: Waqf Properties in Turkey Table 2: The Public Awqaf in Sudan Table 3: Sudanese Awqaf in Eight States Table 4: Number of Waqfs in India Table 5: Increase in Real Total Revenue for the Awqaf Department Punjab

7

CHAPTER ONE: ECONOMIC DIMENSION AND ORIGINS

8

CHAPTER ONE: ECONOMIC DIMENSION AND ORIGINS I. Introduction

Philanthropic foundations are known in the Islamic world as waqf or habs. Whereas the latter term is used primarily in North Africa, the former is known, with slight variations, in the rest of the Islamic world. The word waqf and its plural form awqaf are derived from the Arabic root verb waqafa, which means to cause a thing to stop and stand still. A second meaning is simply philanthropic foundations.

However defined, this institution, whereby a privately owned property, corpus, is endowed for a charitable purpose in perpetuity and the revenue generated is spent for this purpose, stands out as one of the greatest achievements of Islamic civilization. All over the vast Islamic world, from the Atlantic to the Pacific, magnificent works of architecture as well as a wealth of services vitally important to the society have been financed and maintained for centuries through this system. It has even been argued that many waqfs had survived for considerably longer than half a millennium and some even for more than a millennium (Crecelius, 1995: 260).

Despite these overwhelming achievements, the history of waqfs is a turbulent one. For centuries the fate of these institutions was closely linked to the fates of the states under which they functioned. Consequently, they experienced dramatic ups and downs: the period of establishment and growth was often followed by one of decline and neglect until with a new state emerging, renewal and prosperity once again prevailed.

Nowhere in this long history of fluctuations, however, did the waqfs experience the universal and deliberate destruction that was inflicted upon them during the nineteenth and twentieth centuries, a fact which pinpoints, of course, to western imperialism as the culprit. Yet, the greatest destruction took place not in a region colonised by the great powers, but in Turkey, one of the rare countries in the Islamic world, which was not colonised. This paradox, among other things, will be addressed later.

II. Economic Dimension

Although this book will deal primarily with the economic history of the waqf system, it is appropriate to point out briefly the relevance of the waqf system for modern Islamic societies. Indeed, economists looking at the waqf system would be perplexed by the fact that a myriad of essential services such as health, education, municipal, etc., have historically been provided at no cost whatsoever to the government. Therefore, ceteris paribus, the waqf system can contribute significantly towards that ultimate goal of so many modern economists: massive reduction in government expenditure, which leads to a smaller budget deficit, which in turn lowers the need for government borrowing thus curbing the “crowding-out effect” and leads to a reduction in the rate of interest, consequently reining in a basic impediment to private investment and growth.

The waqf could fulfil these above-mentioned functions by voluntary donations made by the well to do. Thus, privately accumulated capital is voluntarily endowed to finance all sorts of social services to the society. At this point another extremely important function of the waqf becomes apparent: not only does it help reduce government expenditure and consequently the rate of interest and pave the way for growth, it also achieves another modern economic goal; a better distribution of income in the economy. For, this improvement in the distribution of income would be achieved essentially through voluntary donations. In this process taxation is definitively assigned a secondary role.

There are further implications: a lower tax burden means an enhancement in the consumers’ and producers’ surpluses and a diminution in the “dead-weight cost of the tax”. Consequently, lower taxes would have a positive impact on aggregate production while at the

9

same time reducing costs. Prices to the consumers would come down and pave the way for non-inflationary growth (Wanniski, 1975: 49-50; The Economist, September 20th, 1997: 20).

Moreover, the waqf definitely solves the problem of the under supply of public goods, so often observed in conventional economies. This point needs to be elaborated. In this context we must first of all note that the services offered by the waqfs constitute public goods, the consumption of which is non-rivalrous and the provision thereof non-excludable.

As is well known, the standard economic theory envisages that since, as rational individuals, consumers of public goods tend to free ride, they fail to contribute to the costs of creating these goods. Consequently, where rational behaviour prevails, public goods would be under produced in conventional economies (Bates, 1995: 30).

As far as the Islamic world is concerned, there is much evidence to the contrary, i.e., to the ubiquitousness of the public goods supplied by the waqfs. Therefore, it seems more appropriate to talk about an excess supply of public goods rather than their scarcity. In an Islamic economy this excess supply, not scarcity, may emerge as the basic problem. It should be emphasised at this point that this observation is not confined to past history but is valid for all times. Indeed, there is no justification for the assumption that modern Muslims would be less interested in charity then their forefathers. Given the right conditions, modern Muslims have demonstrated that they are just as keen as their forefathers to establish waqfs.1

All the social and economic contributions of the waqf system mentioned above, are based upon the crucial assumption that the waqfs are managed by prudent and efficient trustees. History, unfortunately, provides evidence that this was not often the case. Archives, indeed, are full of documents indicating the corruption of waqf officials. In short, there is a serious agency problem associated with the waqf system. This constitutes one of the greatest challenges to modern Islamic economists interested in revitalising this system.

The waqf system contributed significantly to another major economic problem: employment. The ratio of persons employed by the waqf system to those employed directly by the state fluctuated in Turkey as follows: at the turn of the century 8.23%, in 1931 12.68%, and in the 1990s 0.76%. Consequently, the waqf system appears to have ceased being a major source of employment in the Turkish Republic. Although these figures do not include the 30,000 various self-employed retailers and small-scale producers using the waqf premises and the tens of thousands of individuals employed by the new waqfs established according to the secular Turkish Civil Law (Bilici, 1992 and 1993), it is clear that the overall contribution of the waqf system to employment has fallen significantly. This is in sharp contrast with the West where the non-profit sector, which includes trusts and foundations, Western equivalents of waqfs, accounted for an average of 13% of the net new jobs added between 1980 and 1990 in France, Germany and the United States. In the United States the non-profit sector accounts for 6.9% of total employment (Salamon and Anheier, 1996: xviii).

The decline in the contribution of the waqf system to employment reflects the overall decline of the system in Turkey prior to the 1967 Act. This decline was a direct outcome of a deliberate state policy. To understand this dramatic phenomenon we must first of all analyse the forces, which prompted the state to attack the waqf system.

It might be appropriate to start with a few questions:

a. Why does the state feel the need to centralise and even to destroy the waqf system? This question assumes great importance if the waqfs are to avoid the wrath of the state in the future. b. Since even the state had to obey some rules, what were the legal premises behind the state’s interference? c. Was the process of centralization and the pursuant destruction linear or cyclical?

1 The latest evidence from Turkey concerning the dynamic expansion in the number of newly established waqfs confirms this. For details see below.

10

These questions move us from the realm of economics into that of history and for that, we need to go to the very origins. III. The Origins

It is well known that philanthropic endowments have a history considerably older than Islam and it is also very likely that Islam may have been influenced by earlier civilisations. Ancient Mesopotamia, Greece, Rome as well as the pre-Islamic Arabs certainly knew of such endowments (Laum, 1914; Rockwell, 1909; Rostowzew; Othman, 1982; Duncan-Jones, 1982). The extent to which Islamic waqfs were influenced by these ancient institutions and the extent to which they were the product of the genius of Islam, is a question that is still not resolved. Roman, Byzantine, but also Mesopotamian, Sasanid, Jewish and Buddhist influences have been accepted as plausible (Köprülü, 1942: 10-11; Coing, 1981: 272-274). Latest research is more decisive and points to the Sasanid law as the most likely source (Arjomand, 1998: 110-111). Thus, we have a fairly clear situation: Muslims were urged strongly to endow their assets in the service of mankind and they knew how to do it from the earlier civilisations, which had dominated the region in which they had found themselves (Crecelius, 1995: 249). At this point the reader may be impressed by the ability of Islam to borrow from other civilisations. This ability may well have originated with a tradition attributed to Prophet Muhammad:

“Abu Hurairah reported Allah’s messenger as saying: A word of wisdom is the lost property of a believer, he can take it wherever he finds it, because he is more entitled to it.” (al-Tirmidhi, 1992: 2687)

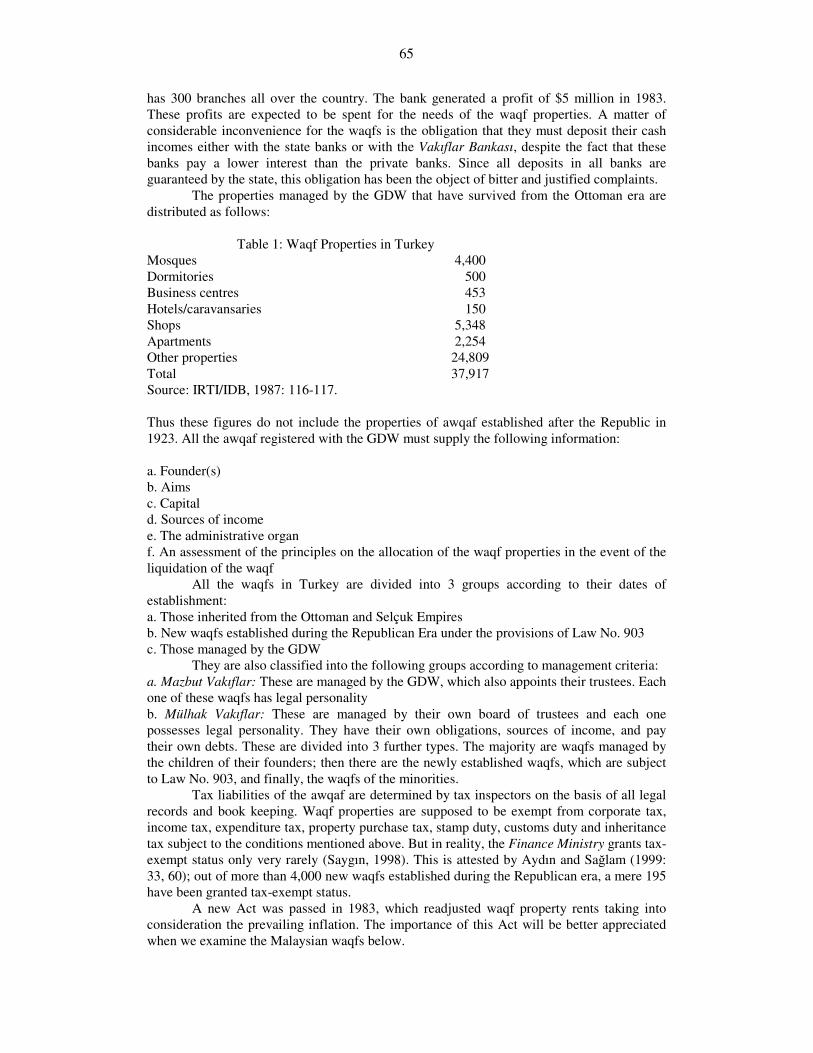

Although waqf is not specifically mentioned therein, the concept of wealth re-distribution is strongly emphasised in the Qur’an (2:215, 264, 270, 280). Moreover, there is definitive evidence that many great personalities of Islam had endowed their properties for charitable purposes. A hadith narrated again by Abu Hurairah most probably accounts for the origin of this institution in the world of Islam:

“Abu Hurairah reported Allah’s messenger as saying: When a man dies, all his acts come to an end, but three: recurring charity, or knowledge (by which people benefit), or a pious offspring, who prays for him” (Muslim, 1992: bab3, hadith 14).

Although the classical sources have, traditionally, taken into consideration each one of these good deeds, sawabs, separately, we prefer to combine them. For it will be argued here that such a combination constitutes the very essence of the Islamic waqfs. Thus, Muslims needed an institution that would enable them to perform all three of these good deeds. The waqf fitted the criteria. It indeed, assures ongoing, recurring charity for many years, even centuries, after the death of the founder; it can finance scholars whose lasting works will benefit mankind for a long period and the sawabs, good deeds, that accrue to them would be shared by the waqf ’s founder who had provided for their sustenance in the first place. Finally the management of the waqf can be entrusted to the offspring of the founder so that while, on the one hand, careful and loyal management is assured, on the other, the offspring would pray for the deceased since, thanks to his waqf, he or she is not destitute.

Although Muslims may have been encouraged to borrow ideas from other civilisations without any hesitation, as the aforementioned hadith suggests, the actual process of borrowing was not simple. For, whatever institution was borrowed, it had to be moulded and re-shaped to conform to the basic teachings of Islam. There were substantial differences in the opinions of the early great jurists concerning the structure and judicial framework of the waqf. While Imam Shafi’i had objections to certain aspects of the institution, among the

11

Hanafis, Imam Abu Yusuf differed from his mentors. Without going into details, it can be argued, in general, that Imams Shafi`i and Abu Yusuf wanted to expand the waqfs and therefore facilitated their foundation, but others preferred to restrict this institution. The basic problem pertained to the Islamic law of inheritance: since a founder could entrust the management of his waqf to any one of his offspring and thus initiate a de facto primogeniture, this could violate the basic principles of Islamic law, which promulgates a distribution of property among all the inheritors. Consequently, most of the jurists found it very difficult to sanction the waqfs.

But for reasons that will be explained below, the Muslim society needed this institution. So the great jurists ended up tolerating it. The turning point came when Abu Yusuf observed how important these institutions had become during his pilgrimage and introduced new legislature, which facilitated the establishment of foundations. The institution of waqf thus emerged after the death of the Prophet and its legal structure was firmly established during the second half of the second century (Köprülü, 1942: 4).

At this point we need to explain how a system, which did not originate in Islam, not specifically mentioned in the Qur’an and objected to initially by many of the eminent jurists, was embraced so enthusiastically and developed to such a phenomenal dimension. There can be two explanations, historical and economic. Let us first consider the former: the great Islamic conquests had enriched the Muslim world beyond any imagination achieving the economic preconditions for the emergence of this institution. We have to remember, moreover, the emphasis attached in the prophetic traditions on the importance of doing good and charitable deeds. Since wealth in Islam is considered an important source of trial, the natural tendency among the Muslim rich to do good deeds as a preparation for the hereafter can be easily understood. Thus, it is for these historical reasons that although not mentioned in the Qur’an specifically, and objected to initially, the waqf has been embraced so enthusiastically.

But this is not all; economic theory also has its own explanation of why the waqf system was needed. Indeed, according to the theory there were compelling reasons for the waqf system to emerge. We have seen above that under the conditions of rational behaviour, public goods would tend to be under produced. This dilemma pertaining to the creation of public goods promotes a demand for the creation of non-market institutions.

This “demand for the creation of non-market institutions” may also explain why the waqf became so popular and widespread in most of the Muslim world. The theory explains, furthermore, the universality of the waqfs or waqf-like non-market institutions. After all, as briefly mentioned above, endowments are known not only in the Muslim world but also in the West and other great civilisations (Salamon and Anheier, 1997; Geremek 1994; Coing, 1981, Crecelius, 1995). In the remainder of this chapter, evidence for this argument pertaining to three cases: England, Spain and South Africa, will be provided IV. Impact on Others

Having lost all contact with Rome, Medieval Europe had to become acquainted with philanthropic endowments through the Islamic waqf system. This is attested to by Monica Gaudiosi, who has initiated an inquiry regarding the origins of English trusts (Gaudiosi, 1988). Gaudiosi first puts to test the conventional wisdom prevailing among the European scholarship that the origin of the English trust rests with the Roman or Germanic laws. She challenges this view by arguing that the trusts developed from a medieval English device for holding land known as the use.

Furthermore, considering the Roman fideicommissum first, she reminds us that the linkage between this institution and the English trusts had already been dismissed by the nineteenth century on the grounds that not only were the similarities between the two institutions merely superficial, but also, whereas the Roman device was purely testamentary, the early English use seldom arose by will.

12

Next she challenges the notion that the origin of the English trusts can be traced back to Lex Salica, the legal code of the Salian Franks, a German tribe. In this rejection, Cattan also supports her. This is then followed by a vigorous argument about why Islamic waqfs constitute the origin of the English trusts. The basic points of this argument are as follows:

a. Whereas, the separation of ownership from usufruct was not a new legal concept, the settlement of the usufruct of the endowed property on successive generations in perpetuity for a charitable purpose was an institution, which was created by the classical Muslim jurists of the first three centuries of Islam. There is no evidence that such a complex system of appropriating the usufruct to varying and successive beneficiaries existed prior to Islam (Cattan, 1955: 205). b. The emergence of the trust coincides with a period of increased contact between Europe

and the Muslim world. Indeed, the Franciscan Friars who are believed to have introduced the use in England were active in the Middle East. Saint Francis, himself, spent the years 1219 and 1220 in Islamic territory.

c. Jerusalem was a particularly significant point of contact between England and the Muslim world because of the presence there of the Orders of the Templars or the Hospitalers. Since it is well known that these orders had been influential in the development of the Inns of Court in fourteenth century England, the transmission of legal institutions from the Islamic world to England has already been demonstrated. Recent research has, moreover, shown that the transmission of legal institutions did not remain limited to the Inns of Court, and that the bulk of the partnership law was also borrowed from the Muslims (Çizakça, 1996). Consequently, all the conditions necessary for the transfer of waqfs, i.e., contact, detailed knowledge about the way the institution to be borrowed functions, etc., already existed.

d. More importantly, similarity between Islamic waqfs and English trusts, is striking. Under both systems, property is reserved and the usufruct is appropriated for the benefits of specific individuals or for a general charitable purpose. The corpus becomes inalienable; estates for life in favour of successive beneficiaries can be created at the will of a founder without regard to the law of inheritance or the rights of the heirs and continuity is secured by successive appointments of trustees.

e. It has been argued that a major difference between the two systems exists: whereas in the English case, the trustee is considered to be the owner of the trust, in the Islamic waqf the trustee (mutawalli) is not considered to be the owner. In reality, the trustee is no more the owner of a trust than the mutawalli could be the owner of a waqf. The main function of both is to administer the property for the benefit not of themselves but for the beneficiaries as specified by the trust or waqf.

f. Another alleged difference pertains to the duration: the waqf must be perpetual, while a trust, except a charitable one, cannot be perpetual. It must be remembered, however, that in England the trusts could originally be made in perpetuity until the rule against perpetuities came into force.

g. It has been argued, however, that there is one very important difference: purpose of the waqf or trust. A trust may be made for any lawful objective, a waqf, by contrast, must be charitable. Charitability is a conditio sine qua non for all waqfs including the family endowments (Cattan, 1955: 212). But this difference much emphasised by Cattan, has been watered down in reality. Ottoman documents indicate there were many waqfs endowed for a wide range of purposes some of which can hardly be considered as strictly charitable.

While all of the above provide substantial and convincing evidence for the argument that Islamic waqfs constituted the origins of the English trusts, some subtle ritualistic differences between the two systems are also acknowledged. These ritualistic differences have already been very adequately explained in Jones (1980) and Hodgson (1968).

13

While it is important to appreciate the ritualistic differences between the Christian and Muslim endowments, the reader should not go to the other extreme and dismiss the arguments made by Gaudiosi and Cattan. The evidence presented by these two authors that the Islamic waqf system has constituted the origins of the English trusts, is substantial and convincing. It is appropriate to include here an analysis of the 1264 Statutes of Merton College, Oxford, provided by Gaudiosi, which is further evidence. Walter de Merton, the founder of the Merton College, Oxford, was a thirteenth century English clergyman and government servant who three times held the powerful position of the Chancellor of England. It is well known that de Merton was closely associated with the New Temple which was the English headquarters of the Knights Templars who had significant contact with the Middle East and particularly with Jerusalem. During de Merton’s final term in office, he wielded unusual power, being described as “practically the regent of the Kingdom”, while Edward I was on crusade in the Holy Land. Surely, his position of authority would have involved him in relations between the Middle East and England particularly during the Crusades. De Merton’s college went through a number of stages before it attained its status as “a watershed in the history of colleges” (Makdisi, 1984). Concerned with the provision of a university education for his nephews, de Merton in 1262 obtained a license to vest certain properties for the support of university students. Two years later, the final form of the 1264 Statutes of Merton College was registered. In the opening sentences of the statutes, de Merton set forth a charitable purpose for his trust and properties for the support of that objective. As is well known, this procedure is a conditio sine qua non for any classical Islamic waqf. The first condition of the trust was that any member of the founder’s family must be supported by the trust in return for appropriate service. Again, this is another provision sanctioned by Islamic law. Given that the focus of de Merton’s foundation was the establishment of a college, it would correspond to the charitable waqf, waqf khayri. The designation of certain family members as beneficiaries, moreover, would certainly conform to the traditions of the Prophet of Islam. Gaudiosi provides a host of further evidence from sumptuary regulations to the provisions allowing the beneficiaries to appoint an overseer to examine the accounts of the trustee and observes that “the structure of Merton College fulfils a number of conditions necessary for the establishment of an Islamic waqf and does not violate any of the stipulations of the Islamic waqf law”. Her conclusion is striking: “Were the Merton documents written in Arabic rather than Latin, the statutes could surely be accepted as a waqf instrument”.

In view of everything said above, we reach the conclusion that the origin of the English trusts can almost certainly be traced back to the Islamic waqf system. It is also telling that in the mid-thirteenth century two other colleges of Oxford were also founded as charitable trusts (Arjomand, 1998: 115).

If, however, far away England had, indeed, been affected to such a degree by the waqfs, it is reasonable to argue that the Christian Mediterranean, much nearer to the Islamic world, would certainly have been affected as well. This is confirmed by Gilbert who has shown that Collége des Dix-Huit established in Paris by one John of London in 1180 was strongly influenced by the waqf madrasas he had seen in Jerusalem (Arjomand, 1988: 114-115). Other evidence is provided by Santiago De Los Espanoles, a foundation established by the Crown of Castile in Rome for the welfare of the Spanish pilgrims, appears to have had an identical organisational structure to an Islamic waqf. There appears to have been only one

14

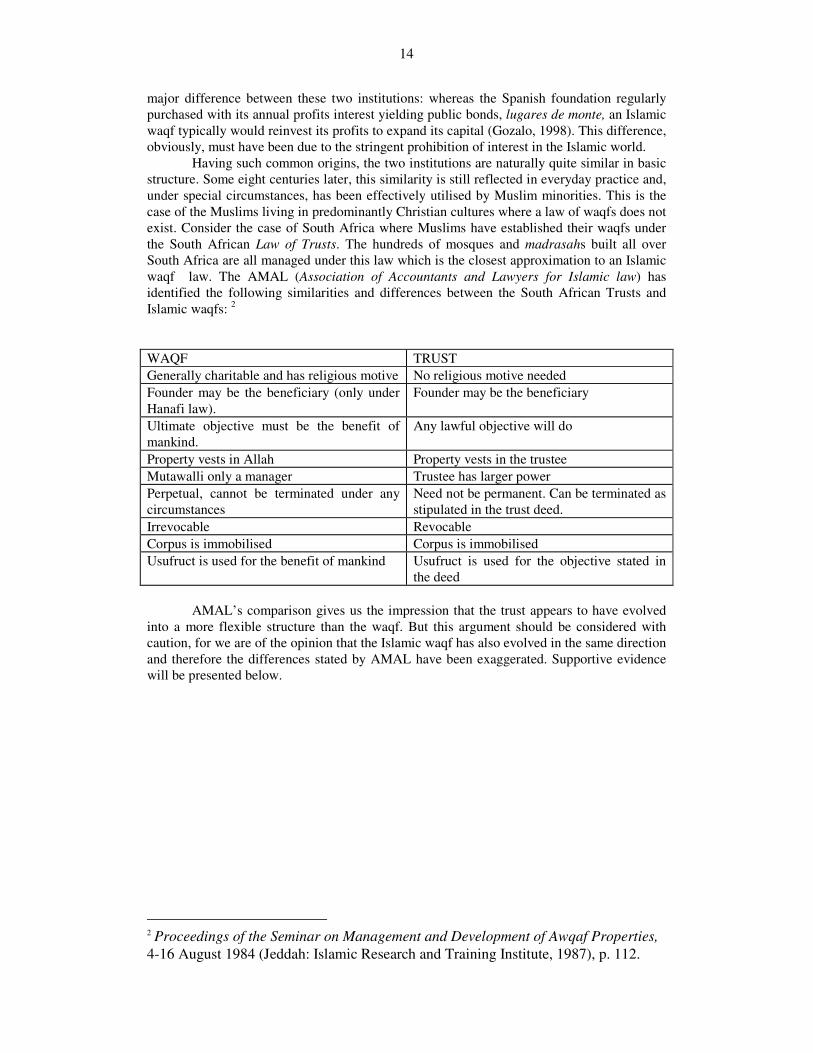

major difference between these two institutions: whereas the Spanish foundation regularly purchased with its annual profits interest yielding public bonds, lugares de monte, an Islamic waqf typically would reinvest its profits to expand its capital (Gozalo, 1998). This difference, obviously, must have been due to the stringent prohibition of interest in the Islamic world.

Having such common origins, the two institutions are naturally quite similar in basic structure. Some eight centuries later, this similarity is still reflected in everyday practice and, under special circumstances, has been effectively utilised by Muslim minorities. This is the case of the Muslims living in predominantly Christian cultures where a law of waqfs does not exist. Consider the case of South Africa where Muslims have established their waqfs under the South African Law of Trusts. The hundreds of mosques and madrasahs built all over South Africa are all managed under this law which is the closest approximation to an Islamic waqf law. The AMAL (Association of Accountants and Lawyers for Islamic law) has identified the following similarities and differences between the South African Trusts and Islamic waqfs: 2 WAQF TRUST Generally charitable and has religious motive No religious motive needed Founder may be the beneficiary (only under Hanafi law).

Founder may be the beneficiary

Ultimate objective must be the benefit of mankind.

Any lawful objective will do

Property vests in Allah Property vests in the trustee Mutawalli only a manager Trustee has larger power Perpetual, cannot be terminated under any circumstances

Need not be permanent. Can be terminated as stipulated in the trust deed.

Irrevocable Revocable Corpus is immobilised Corpus is immobilised Usufruct is used for the benefit of mankind Usufruct is used for the objective stated in

the deed AMAL’s comparison gives us the impression that the trust appears to have evolved into a more flexible structure than the waqf. But this argument should be considered with caution, for we are of the opinion that the Islamic waqf has also evolved in the same direction and therefore the differences stated by AMAL have been exaggerated. Supportive evidence will be presented below.

2 Proceedings of the Seminar on Management and Development of Awqaf Properties, 4-16 August 1984 (Jeddah: Islamic Research and Training Institute, 1987), p. 112.

15

CHAPTER TWO: FUNCTIONING OF THE SYSTEM AND JUDICIAL PROBLEMS CHAPTER TWO: FUNCTIONING OF THE SYSTEM AND JUDICIAL PROBLEMS

In a nutshell, a waqf functions as follows: a founder who has accumulated private wealth decides to endow his personal property for a specific, often, pious, purpose. The amount of the original capital, corpus, the purpose for which it is endowed and all the other conditions of management are clearly registered in a deed of endowment, submitted to the authorities. In this way the privately accumulated wealth of a pious Muslim becomes God’s property. The founder strictly stipulates how the annual revenue of the waqf should be spent. This revenue (usufruct) may be allocated completely for a pious purpose (waqf khayri), or to a group of beneficiaries. The offspring of the founder may also be the primary recipients of this annual revenue. Such waqfs are known as the family waqfs or waqf ahli. The

17

management of the waqf is entrusted to a trustee, mutawalli, whose functions may be fulfilled by the founder himself during his lifetime. Thus, there are four major components of any waqf: the founder, the beneficiaries, the trustees and the endowed capital corpus itself. We will now consider each one of these components in detail. I. The Founders It is appropriate to start this section with an analysis of the founders. Research based upon more than 300 waqfs of fifteenth and sixteenth century Edirne, a frontier town in the Ottoman Balkans, has revealed that the vast majority of the Ottoman waqfs were founded by private individuals rather than the sultans whose waqfs constituted a mere 1 to 2% of the total (Gerber, 1983: 29). The overall number of founders, with the exception of the sultanic and those founded by women, was 233. Of these founders 43% (100) were ordinary citizens and 57% (133) were members of the elite. In order to compare the sizes, privately endowed waqfs were categorised into three groups according to the endowment capital: small, medium, and large waqfs. There were 216 waqfs, which could be classified according to size (including the sultanic and women’s waqfs). Of these 30% belonged to the smallest category; 70% were middle sized; and only 1% was large.

As for the connection between the founders and the size, ordinary citizens generally founded small waqfs - 62% of their endowments were small and 48% medium. In contrast, members of the elite generally established medium sized waqfs (5% small, 93% medium and 2% large). Women established only 20% of the waqfs in Edirne.

In Istanbul and Aleppo, by contrast, the equivalent percentage was at least 40%. Gerber has attempted to account for this discrepancy with the argument that Edirne was a frontier town and consequently it must have had a relatively smaller and passive female population.

Thus Gerber has reached a very clear conclusion: ordinary citizens tended to establish small and medium sized waqfs, while the elite founded larger ones. The vast majority were established by ordinary citizens. Unfortunately, similar statistics do not exist for other Islamic countries but it is reasonable to assume that the situation should be similar elsewhere.

1. The Ten Conditions At this point it is appropriate to identify the powers, which the founders reserve for

themselves during the establishment of their waqfs. Put differently, when endowing their properties and transferring the ownership from their own possession to that of God, the founders had to follow a strict procedure but they were permitted to retain certain powers. These powers are to be found in almost all the endowment deeds and have been called the ten conditions by the late Hanafi jurists. They are traditionally expressed as five twin conditions, which negate each other: a. Expand-Reduce (teksîr-taklîl): The founder can expand the share of a beneficiary from the

usufruct of the endowment, or can reduce it. Normally, the founder would be allowed to make such changes only once, unless he has stipulated in the endowment deed that he wishes to enjoy the right to expand or reduce for as long as he lives.

b. Enter-Exit (idhal-ihrac): The founder is empowered to make a person beneficiary even if he would not be considered one under normal circumstances (idhal). Conversely, the founder also has the power to deprive a beneficiary of his normal privilege. The Hanafis consider the idhal-ihrac as the absolute prerogative of the founder, while the Shafi’is and the Hanbalis are of the opinion that this is not an absolute but a limited one.

c. Pay-Freeze (I’tâ-Hirman): The founder may assign priority to the regular and uninterrupted payment of one beneficiary (i’tâ) and conversely, postpone the payment to others (hirman). This flexibility, which is granted not only to the founder but also to the

18

trustee, allows a waqf to manage its budget according to a list of priorities determined by its founder. The condition assumes particular importance for those waqfs, which have a multitude of beneficiaries.

d. Changing Conditions-Purpose (ta�yir-tebdil): The founder enjoys the right to change the conditions stipulated in the waqf deed (ta�yir). He or she also retains the power to change the original purpose of the waqf, like converting a charitable waqf into a family waqf or vice versa.3

e. Sell- Exchange (ibdal-�stibdal): The founder may permit himself to sell the corpus of the

waqf for cash (ibdal), or exchange it for another property (istibdal). In historical documents, istibdal, is more often used and usually pertains to both sale and exchange of the corpus.

This is an important power that the founder can bestow upon himself. The

importance of istibdal lies in the fact that it embodies certain dynamism. By allowing the founder to sell the waqf property the system is made responsive to market conditions. Thus, if a waqf land which happens to be originally at the outskirts of a town ends up being in the middle of it due to urban expansion and its value skyrockets as a result, the founder is enabled to exchange the waqf land for another one, and in the process, can either expand the waqf land, again, at the outskirts by purchasing much more land or enrich his waqf with cash.

Furthermore, istibdal assumes great importance particularly for those waqfs whose corpus is constituted of movables. Such waqfs achieve perpetuity, a conditio sine qua non, often by applying istibdal. Indeed, if we consider a cash waqf i.e., where the original endowment was in cash, and assume further that the government is planning to change the currency of the country or debase it, istibdal under such conditions, becomes a vitally important instrument to assure the perpetuity of the waqf.

It goes without saying that while certain dynamism is indeed embodied in istibdal, this rule also embodies great potential for misuse. So much so that this instrument essential for the survival of the institution of waqfs has been used by its opponents to destroy it (Akgündüz, 1988: 291). The details of this phenomenon will be presented below. Meanwhile, we may note that wherever applied, this instrument has fuelled passions. This is understandable, for istibdal allows the sale of a waqf property, which is supposed to belong to God and be perpetual. Behrens-Abouseif has even argued that the Ottoman occupation of Egypt was prompted by an illegal istibdal procedure, which attempted to sell the Al-Azhar complex (1994: 146-147). This brings us to the question of under what conditions istibdal would be legal. The answer is complicated by the fact that the four major schools of Sunni Islam do not agree on this problem. The Malikis, for instance, strictly prohibit istibdal in real estate waqfs with very few exceptions. But the Malikis are considerably less strict concerning the istibdal of the waqf of movables. The only condition they attach to such istibdal is that the movable corpus of the waqf should have been reduced to such a state that it has become impossible to fulfil the original purpose of the waqf because it is not generating sufficient returns.

3 A real case from Ottoman Egypt may illustrate the point: Iskender Pasha who governed Egypt from 1556 to 1559 had a foundation which was a religious complex. Whatever remained of the waqf revenues after the obligations of the endowment were fulfilled reverted to the founder during his lifetime. After his death, 2/3 of the surplus revenues were to be added to the foundation, and 1/3 would go to the founder’s heirs or, if he had none, to the foundation.This stipulation was later changed to give the heirs 2/3 instead of 1/3, thereby decreasing the charitable portion of the waqf (Behrens-Abouseif, 1994: 195).

19

The Shafi’is are also against istibdal, which in their opinion can be used as an instrument to destroy waqf properties. They even prohibit the sale of a totally destroyed mosque on the grounds that it may be restored some day. Thus, the Shafi’i position is even more stringent than that of the Malikis. In view of this, Behrens-Abouseif’s above-mentioned argument that the attempted sale of the Al-Azhar had prompted the Ottoman Sultan to occupy Egypt, which in his opinion had become totally corrupt, can be understood better. For, Shafi’i law was the prevailing law in pre-Ottoman Egypt and selling any waqf property, let alone the famous Al-Azhar, should have been strictly prohibited. The irony of all this was that the Ottoman Sultan belonged to the Hanafi School, which had the most liberal perspective on istibdal. The Hanafi position on istibdal has been summarised as follows: if the founder of the waqf has not made any stipulation in the deed about the sale or exchange of the waqf’s property, then an istibdal transaction would not be permitted. But if the waqf’s property is in such a poor state that it does not generate any revenue or the revenue that it generates is not sufficient to cover its expenses and therefore an istibdal of waqf property is deemed to be beneficial for the waqf, then under such circumstances, even if the founder has not stipulated istibdal in the deed of endowment, such a transaction may be permitted subject to the approval of the judge as well as the permission of the Sultan. This latter condition prohibiting istibdal unless permitted by a sultanic decree, irade-i seniye, was promulgated in the year 951 A.H. by the Ottoman �eyhülislam Ebussuud Efendi (Ömer Hilmi, 1307A.H.: 198).

Yet, even the Hanafi position was controversial. According to this school there can be three alternatives pertaining to istibdal:

a. When the founder has permitted himself, according to the ten conditions mentioned

above, to resort to istibdal. Under this condition three conflicting opinions have been voiced:

i. Imam Muhammad (al-Shaybani) has rejected this condition and argued that while the waqf would be valid, the condition itself would be void. Put differently, according to Imam Muhammad, the founder cannot vest himself with such an authority.

ii. A group of Hanafi jurists have argued that if a founder reserves for himself the right to apply istibdal, both the waqf and the condition would be void.

iii. Led by Abu Yusuf, the majority of the Hanafi School considers such a waqf as well as the tenth condition of ibdal-istibdal as valid.

b. When the waqf properties are ruined to the extent that they have become totally useless, i.e., generating no revenue or not enough to cover its expenses. Under such conditions, even if the original founder had not vested himself with the authority to resort to istibdal, and providing that the local judge decides that an istibdal would be beneficial to the waqf, the great majority of the Hanafi jurists, including Imam Muhammad, have approved of istibdal.

c. When the founder has not vested himself with the right to resort to istibdal and when the waqf properties are still usable, but it is argued that if the waqf property were subjected to istibdal, it would generate greater revenue for the waqf.

i. A group of jurists, led by Hilâl, have argued that this may lead to corruption and should therefore be prohibited.

ii. Led by Abu Yusuf, another group is of the opinion that, providing the judge’s permission is obtained, istibdal would be valid.

d. Finally, when the founder has ruled that istibdal is void. Under this situation two conflicting opinions have been propounded:

i. In such a situation neither the judge nor any other person can resort to istibdal.

20

ii. Led by Abu Yusuf, another group of jurists have argued that if the judge considers it beneficial to the waqf, he can override the original conditions stipulated by the founder.

Thus, in short, istibdal is a highly controversial issue in Islamic law and has been likened to a sharp knife capable of cutting both for good and for evil (Akgündüz, 1988: 296). The latter, however, has been challenged by recent research. In a fascinating article Miriam Hoexter has argued that the alleged direct linkage between istibdal and corruption should not be taken for granted. On the contrary, she has furnished solid evidence from the Algerian waqf registers that istibdal transactions were not only economically fair but also constituted a very profitable business for the Algerian Harameyn waqfs (Hoexter, 1997).

II. Beneficiaries and the Family Waqf Controversy It is well known that the waqf system provided regular salaries to many beneficiaries. Recently, these beneficiaries who were paid from the annual revenues of the awqaf have been categorised into various groups: administration, education, food for the public, family of the founders, maintenance, religion, municipal services, tax relief, etc. (Çizakça, 1995: 339). Since a detailed analysis of these groups has already been made, we will not repeat it here. It should suffice to note that a long-term analysis of the relative amount each group obtained from the waqf system in any given city would reveal important insight into the prevailing value system of that city and its evolution (Çizakça, 1994). At this point it is important to remember that waqfs allocated their annual revenues to a myriad of beneficiaries, a founder could also appoint himself or his inheritors as the primary beneficiary. This type is known as the ehli vakıf, or the family waqf. The revenue of such waqfs are reserved for the benefit of the founder or the offspring. Initially public benefit is of secondary importance; it assumes primary importance only after the nesil expires, i.e., when there are no more descendants of the founder and so the entire revenue of the waqf accrues to public purposes. Through such waqfs it was also possible to avoid Islamic inheritance rules and to bequeath to a specific member of the family. In short, though not sanctioned by Islamic law, primogeniture could be applied in the Islamic world by resorting to family waqfs. This possibility had, naturally, far reaching consequences throughout the world of Islam, to which reference will be made later. The origins of this specific type of waqf are obscure and controversial. French orientalists, for instance, have argued that the family waqfs originated in the reaction of the Arabs to the Islamic law of inheritance, which aimed at improving the position of women in the society. But when women were made eligible to inherit, this offended the local traditions and the Arabs tried to find an indirect way to circumvent the new law and still apply a sort of primogeniture or at least to bequeath only to the male offspring. These orientalists thus argued that whereas the origins of waqf were undoubtedly Islamic, in the later centuries they evolved primarily to circumvent the law of inheritance.

This line of reasoning ignores the Prophetic traditions fully sanctioning pious offerings for provisioning the self, the children and the needy relatives (Qureshi, 1990: 82). Thus, the whole argument that the family waqfs were a relatively late development is false. It is well known, moreover, that when Omar, the Second Caliph, endowed his land in Khaibar, he allocated its usufruct, among other things, to his offspring following the Prophet’s advice, and that Imam Shafi’i, himself, had also endowed his house in Fustat to his offspring. Moreover, it is also well known that the great Hanafite jurists were involved in a bitter controversy over the legality of family waqfs, which casts further doubt on the orientalist argument that this institution was a later Arab invention. The controversy was between Imam Abu Yusuf on the one hand and Imam Hanafi and Muhammad (Shaybani) on the other, in short, a conflict among the giants of Islamic (Hanafite) jurisprudence.

21

It is therefore all the more remarkable that Abu Yusuf’s complicated and controversial position came to be accepted not only by the Hanafite regions of Islam but even by some other regions where Hanafite law was not dominant (such as Algiers). The permission granted by Abu Yusuf to the family waqfs was well accepted by the Islamic world in general and assumed a definitive character particularly in the Hanafite regions. But the controversy did not wane and resurfaced time and again. The seventeenth century Ottoman controversy triggered by the great statesman Koçi Bey was based on the following observation: the conversion of state lands into personal property and then into waqf. Thus the lands, which were originally assigned for the military fief (tımar), were being increasingly re-allocated for religious/non-military usage through the waqf system. This problem was not apparently so serious in Mughal India, for the Mughals, according to Kozlowski, were cash rich: all the Mughal land tax came to the treasury as cash. So the emperors made cash grants to those they wished to patronise rather than alienating state lands to them (Crecelius, 1995: 259). But it assumed serious proportions in the Ottoman Empire and led to bitter complaints. Finally, 200 years later in French North Africa and British India, the controversy resurfaced again, this time, by the colonialists and orientalists who challenged the legitimacy of family waqfs for their own ends.

Most orientalists have argued that family waqfs were also resorted to in order to protect the family property from arbitrary confiscations of the rulers. This was apparently another reason why this institution had become so popular. Köprülü accepts this explanation as plausible but argues that this motive cannot explain all the waqfs. Consider, for instance, the palace eunuchs who had no offspring but who established substantial foundations (Köprülü, 1942: 5-6). The strongest refutation to the confiscation argument has been provided, however, by Gerber who demonstrated that the women of Edirne, who had nothing to fear from confiscations, established 65% of the waqfs they endowed as family waqfs, while 80% of the waqfs endowed by those who had the most to fear, the elite, were charitable. Thus Gerber concludes:

“In fifteenth and sixteenth centuries Edirne, the waqf was used only in a minor capacity or even rarely in order to safeguard the property of the founders for transmission purposes” (1983: 35). In any case, family waqfs, in general, did not constitute the majority of the waqfs in

the Ottoman Empire: Barkan has shown that the ratio of family/charitable waqf ratio was not particularly high during the sixteenth century while a recent analysis has revealed that during the eighteenth century merely 14.20% of the total awqaf revenue and during the nineteenth, 16.87%, was reserved for the family members of the founders. In Aleppo the ratio was somewhat larger: of the total of 687 waqfs established in this city between 1718 and 1800, 50.7% were charitable, 39.3% were family and 10% were mixed (Öztürk, 1995: 249; Masters, 1988: 173).

Another motive in establishing family waqfs, it has been argued, was to protect the property of an indebted person. In the Ottoman lands this practice was prohibited by a fatwa of Ebussuud during the sixteenth century while in India it led to a huge controversy beginning in 1894 with the Abdul Fata (and others) v. Russomoy (and others) case in the Privy Council and culminating in Muhammad Ali Jinnah’s victory and the passing of the Mussalman Waqf Validating Act of 1913.

Meanwhile the popularity in Egypt of the family waqfs has been demonstrated by the fact that these awqaf yielded more revenue in 1928-29 than all the other types. This situation was one of the reasons, which eventually led to the total prohibition of these waqfs in Egypt later.

III. The Trustees (mutawallis)

22

Islamic law considers trustees strictly as managers to whom the waqf is entrusted. While these individuals were the ones who actually preserved the magnificent Islamic heritage through the centuries and enabled many waqfs to survive for centuries, it was also they who ended up being accused ruthlessly and held responsible for the demise of the system. It can be argued that all the major changes in the administration of the waqf system throughout history were undertaken in order to put these trustees under stricter control and end their opportunities for misuse and embezzlement. Sometimes accusations against them were justified, after all the trustees were only humans, but sometimes they were simply used as scapegoats and served the more sinister schemes of the state. The details of how the trustees fared as individuals crucial for the survival of the waqf system and as culprits, will be presented below.

IV. The Original Capital of the Endowment (corpus) The conditio sine qua non of any waqf is that it should be established with privately owned capital. Behind this simple statement, however, there are bitter debates and controversies. Consider, for instance, land as the corpus. Was land a privately owned commodity under Islamic law, and had the corpus to be restricted to land and other real estate? There are two huge controversies contained within this simple question. The one pertaining to the private ownership of land, led to an enormously complex relationship: the state vis- a- vis the waqfs. The other one pertaining to the type of the corpus, i.e., movables versus immovables, led to the cash waqf controversy. The latter will be dealt with first.

CHAPTER THREE: CASH WAQFS IN THE ISLAMIC WORLD CHAPTER THREE: CASH WAQFS IN THE ISLAMIC WORLD

I. Legal Issues 1. Introduction

The cash waqf was a special type of endowment which differed from the ordinary

real estate waqf in that its original capital, asl al-mal or, corpus, consisted purely or partially,

24

of cash. The earliest origins of the cash waqfs in the Islamic world,4 may be traced back to the eighth century, when Imam Zufer was asked how such waqfs should function. The fact that the question was asked at all, may be taken as an indication of the existence of such waqfs at that time. Be that as it may, these endowments had been approved by the Ottoman courts as early as the fifteenth century and by the end of the sixteenth they had become the dominant form of waqf all over Anatolia and the Balkans (Çizakça, 1995; Sucesk, 1966).

It has been argued that cash waqfs were legalised only in the Turkish speaking parts of the Ottoman Empire, i.e., Anatolia and the Balkans and that the more pious Arabs never allowed these waqfs in the Arab provinces (Mandaville, 1979). While this view may have had some legitimacy in history, it is no longer acceptable, for later research has revealed that cash waqfs exist in Syria, Egypt, Sudan and Aden.5 In Egypt, waqf of movables has been permitted by the law number 48, dated 1946. Moreover, the diffusion of cash waqfs is far more extensive than once presumed: they have been observed in the Ural-Volga region; in India and Pakistan they are considered to be legal since 1913; in Iraq, as we will see below, there is a fatwa issued by the celebrated Mujtahid of Karbala, permitting them; in the Islamic Republic of Iran the famous waqf Astan-e Qods-e Razawi has recently purchased shares in various industrial complexes thus establishing cash waqfs, again in Iran, they have been permitted by the May 17, 1986 Cabinet Decree, Article no. 44; and finally they have been observed in the Malay world and in Singapore.6

The legality of the cash waqfs in the vast lands from the Balkans to the Malay world thus implies a general acceptance by all the major schools of Islamic jurisprudence. But this general acceptance has not been without a fierce controversy that lasted at least from the sixteenth century until the twentieth.

2. The Hanafi Position on the Waqf of Movables (Cash Waqfs)

Probably the most detailed account of this controversy has been studied by

Suhrawardy, an Indian jurist-scholar who travelled to the Ottoman lands at the height of another controversy, that of the family waqfs, prevailing in India. His major Article on the legality of cash waqfs (Suhrawardy, 1911) was published just two years before the family waqf controversy ended in the victory of Muslims against the British establishment. Thus the first two decades of the present century was one of fierce legal debate about the waqfs

4 For perpetual cash foundations in Roman empire see; Duncan-Jones (1982: 133-138). 5 For Syrian cash waqfs (sixteenth-seventeenth centuries) see; Bruce Masters, The Origins of Western Economic Dominance in the Middle East (New York: New York University Press, 1988), p. 162; for Egyptian (modern), see the two fatwas given by the muftis of Egypt and of Alexandria in 1908 presented below; see also G. Baer, Studies in the Social History of Modern Egypt (Chicago: UCP, 1969), p. 80, as well as A History of Land Ownership in Modern Egypt (London: Oxford University Press, 1962), p. 153 and Syed Ameer, Muhammadan Law (New Delhi: 1985), fourth edition, p. 249. For the Sudan (also modern) see; Sumaiya Sid Ahmed Abdel Hadi, The Waqf Institution in Sudan (Kuala Lumpur: ISTAC, Unpublished Research Paper, 1997), pp. 10, 20; for the indirect evidence for Aden see; J. N. D. Anderson, Islamic law in Africa (London: Frank Cass, 1978, second edition), p. 37, footnote no.5.m. For Malaysia and Singapore see; Moshe Yegar, Islam and Islamic Institutions in British Malaya (Jerusalem/ al-Quds: The Magnes Press, 1979), pp. 207, 209. 6 Majlis Ugama Islam Singapura, Annual Report 1995, pp. 54-55. In Singapore cash waqfs’ status is ambigious and transitionary. For details see below the section: “Cash Waqfs in Malaysia and Singapore”.

25

(family as well as cash) in India and we should view Suhrawardy’s work from this perspective.

The reason Suhrawardy travelled all the way to Istanbul is explained by himself in the “acknowledgements” as follows:

“I take this opportunity of expressing my sincere thanks to Muhammad Ali �evki Bey, and to Zaimzade Hasan Fehmi Bey, grandson and First Secretary to Field Marshall Ghazi Ahmet Muhtar Pasha, late Ottoman High Commissioner in Egypt, for obtaining access for me to several important libraries in the Ottoman Empire and also for procuring for me the fatwas of the Grand Mufti of Egypt and of the Mufti of Alexandria …. In a subsequent issue of this journal I hope to give a translation of the well-known treatise on the subject of this paper by the celebrated Sheikh al-Islam, Mufti, Ebussuud, a manuscript copy of which I have just discovered in Constantinople.” Thus, the purpose of his visit to the Ottoman lands was to study the cash waqf

controversy in the Ottoman Empire itself and to find out about the legality of this institution. The manuscript of Ebussuud that he refers to was obviously the one written during the sixteenth century at the height of the Ottoman cash waqf controversy (Mandaville, 1979). It is noteworthy that he did not limit himself to the famous treatise but went so far as to obtain fatwas from Egypt.

Actually, at the beginning of the twentieth century looking at the Ottoman Caliphate and Egypt for solutions to the prevailing legal problems in India appears to have become the established norm for Indian Muslims. For the family waqf controversy also the same method was used. The implications of this situation should not escape us here. The Ottoman Caliphate was the symbol of legitimacy in the Islamic world and any legal issue that was solved in the Caliphate would be considered as solved in India as well. This was particularly so as both regions followed the Hanafi law.7

Since the sixteenth century Ottoman legal debate concerning the validity of cash waqfs has been well documented and summarised by Mandaville, we will concentrate here on the controversy as it was reviewed by Suhrawardy at the beginning of this century. Suhrawardy starts his work by a short statement, which reveals his overall purpose:

“A careful perusal of this paper … will, I venture to hope, leave no doubt in the minds of the readers about the validity of the waqf of movables, including money, shares in companies, securities, stocks etc.” This is followed by a useful account of the methodology of Islamic jurisprudence

with particular emphasis on the hierarchy of jurists and the reliability of sources. He then acknowledges that divergence of opinion exists among the jurists and suggests that, according to Prophetic tradition, this is a blessing.

Concerning the legality of cash waqfs, which he considers a special form of the waqf of movables,8 the first source Suhrawardy consults is the Is’af of Burhan al-Din Ibrahim

7 Even in far away Malaysia, where the Shafi’i law prevails, the Ottoman codification of Islamic Law, or the Mecelle, is presently used by the Islamic reformists who needed categories of punishment more tolerant than the strict hudud (Horowitz, 1994: 243). 8 The question whether the cash waqfs were simply a special form of the waqf of movables was fiercely debated during the sixteenth century. Both Imams Muhammad (al-Shaybani) and Abu Yusuf permitted the waqf of movables, but they were silent about cash waqfs. It was Abussuud, the Ottoman �eyhülislam, who considered cash

26

written in 1499. Burhan al-din refers to Imam Muhammad (al-Shaybani) and argues that he had permitted the endowment of movables subject to custom. Burhan el-din dismisses the problem of the perpetuity of the endowment’s corpus based upon both custom and Prophetic tradition, the latter referring to the well known cases of waqfs founded during the early days of Islam with movables such as arms and horses.

Next, Suhrawardy has consulted Fatawa Kadi Khan where the great Hanafi jurist al-Sarakhsi is quoted. Al-Sarakhsi repeats Muhammad’s approval of the endowment of movables.

Durr al Muntaqa where the true flexibility of Imam Muhammad’s permission is referred to for the first time has provided a far more detailed analysis. This is the fact that the permission to endow movables had been granted subject to custom as well as in the absence of custom, i.e., that the permission was absolute. It was Abu Yusuf, who had permitted the endowment of movables strictly subject to custom.

The next source consulted by Suhrawardy, Majma al-Anhur, repeats the approval of Imam Muhammad and Abu Yusuf, but then takes a step further arguing that since a custom regarding the endowment of cash had already surfaced at the time of Zufer, who was a companion of the great Imam Abu Hanife, then these waqfs came within the purview of the dictum of both Imam Muhammad as well as Abu Yusuf and therefore they must be allowed without any doubt whatsoever. Thus,

“fatwa of some to the effect that the view declaring the validity of the waqf of

dirhams is weak, because of its having been reported from Zufer, is incorrect”9 Next we come to the controversy concerning the nature of custom, ta’amul. The

debate here is between the purists who argue that only custom prevailing at the time of the Prophet and his companions should be considered, and the “liberals” arguing that custom of all times must be considered as a source of jurisprudence. Majma al-Anhur rejects the purist argument. Actually the rejection can be traced right back to the Prophet himself, who had said as reported by Ahmad:

“Whatever is good in the sight of the Muslims is good in the sight of God !”

indicating that he trusted the judgement of Muslims as embodied in the established custom, at all times. It is for this reason that custom is stronger than analogy, qiyas, as well as juristic preference, istihsan and again, it is for this reason that Imam Abu Yusuf must have ruled the waqf of movables valid subject to the existence of custom.

waqfs simply as a special form of the waqf of movables for the first time (Mandaville, 1979: 300-301). 9 ‘The Mufti should give fatwa according to the dictum of the Imam absolutely, then according to the dictum of the second, then of the third, then according to that of Zufar and Hasan b. Ziyad. It is laid down in the chapter on the Bahr al-Raiq that when there are two “correct views” regarding any particular question, it is lawful to give judgement according to either of them’, Suhrawardy, “The Waqf of Movables”, op.cit., p. 326. Thus we are informed about the hierarchy among the great Imams of the Hanafi school. Here, “Imam” refers to Abu Hanifah, himself, “the second” refers to Abu Yusuf and “the third” to Muhammad al-Shaybani. But in Umdat al-Riayah, A Commentary on the Sharh al-Wiqayah, (Lucknow), p. 16, Abu Yusuf and Muhammad are given equal weight. This may well be because Muhammad al-Shaybani was probably the very last student of Imam Hanifah attending his very last tutorials which he held in prison.

27

The legal implications of a situation whereby custom appeared after Imam Muhammad’s time and in a different country have been referred to in the Tahtawi. Reporting that al-Nahr limits the validity of a waqf to the countries where it has been recognised, Tahtawi rejects this argument based upon Ebussuud. He then provides the examples of various movable waqfs which did not exist at the time of Imam Muhammad and for which custom emerged afterwards. The most important example of such waqfs is the waqf of ships.

“In our time practice has arisen with regard to the ships of the Red Sea. For some of them are made waqf of for transporting grains destined for Mecca and Medina10 ”.

Thus the wisdom of Imam Muhammad in considering custom from a flexible perspective is made crystal clear in Tahtawi. Muhammad held that the waqf of movables was valid not only subject to the existence of custom at his time but also subject to custom which may arise in another time and country. It is thanks to this flexibility that Islam gained two very important types of waqf: the waqf of grain ships which made pilgrimage possible and the cash waqfs. Suhrawardy finds the same point also emphasised in the Durr where it is stated that law is based on the recognised practice of the age in question. The Durr considers custom clearly as the basis of law in every clime and age. The Kifayah looks at the problem from a different perspective and after weighing the various methods of Islamic jurisprudence against each other reaches the conclusion that the negation of the waqf of movables based on analogy, qiyas, should be rejected. The analogy here pertains to the question of perpetuity, a primary condition of the validity of a waqf and leads to the argument that since movables cannot endure, they violate the perpetuity principle. Thus here we have two principles in conflict; analogy based on the problem of perpetuity rejecting the cash waqfs and Prophetic tradition permitting the endowment of movables in general, as well as custom permitting the specific form of movables. The Kifayah concludes that the force of analogy as based on perpetuity is abandoned by reason of custom as well as tradition. The latter pertains to a hadith to be found in al-Bukhari:

“For verily did Khalid ibn al-Walid, make waqf of armour he had in the way of Allah” (Sahih Buhari: 2547). while the former, i.e., the “antagonistic influence of custom” which has overruled analogy, pertains to the ruling of Imam Muhammad explained above. In short, the argument that the cash waqfs should be rejected because their corpus in the form of cash cannot be perpetual is rejected on the grounds of custom and tradition, both are more powerful than the analogy pertaining to perpetuity. Next we come to the fierce debate between al-Ramli (d.1004 A.H.) and Radd al-Mukhtar. Al-Ramli tried to use the custom argument against the cash waqfs by arguing that there were no cash waqfs at the time of Imam Muhammad and therefore no custom. But it should be noted here that al-Ramli was not aware of al-Sarakhsi’s report that Imam Muhammad had approved of the waqfs of movables even in the absence of custom.

Radd al-Mukhtar refutes and silences al-Ramli by arguing that cash has perpetuity, because one dirham is as good as the other (Mandaville, 1979: 299). Moreover, we have here 10 Endowing ships appears to have originated with the Mamluks and it has been argued that the Ottomans did not invent but took over this tradition. See, Doris Behrens-Abouseif, “Qaytbay’s Foundation in Medina…..”, Mamluk Studies Review, Volume II, 1998, p. 67. Hans Georg Majer rejects the idea of waqf ships altogether. He argues that the term “waqf ships” referred to those ships bought by the waqfs. Ships were not endowed as such and did not constitute the corpus of a waqf (Majer’s comment on my paper ‘Institutional Framework of Democratic Islam’ delivered at Munich University, July 1998).

28

the order of the Sultan himself in favour of the cash waqfs. This order is of crucial importance for Suhrawardy who argues that the Ottoman Sultan’s order is sufficient to legalise such a waqf not only in his country but throughout the Muslim world. This is because the order represents a given preference to one out of two views and this preference removes the conflict and gives generality and concurrence to the view so preferred. Secondly, the custom in Turkey cannot be called a practice in a particular country, but it is a general and universal practice “ta’amul alam” and it is good enough to embrace the whole of the Muslim world. Thirdly, if Turkey is a special country “balad khas”, within the meaning of the rule of jurisprudence as laid down in the Sharh Manafi’ al-Daqqaq, still there being no “nass” or tradition against the view of validity of any Islamic state, the view of the law in Turkey is binding over all the Muslim world. After providing us with these painstaking details of the debate on the validity of cash waqfs, Suhrawardy asked the help of Ottoman Field-Marshall Ghazi Muhtar Pasha, former governor of Egypt, for a fatwa from the Mufti of Egypt. Hasan Fehmi Bey, Secretary to Ghazi Muhtar Pasha asked the following to the Mufti (Suhrawardy, 1911: 371):

“What is your opinion concerning the following case? An Indian of the Hanafi sect makes a waqf of government securities, stocks and bonds known amongst Europeans as rente or of shares in trading companies, the practice of which has been recognised in our time in certain countries. Will such a waqf be valid and permissible in India if it is recognised in Turkey for instance … ?”

Answer (Written on 9 Muharrem 1326 A.H. (1908), fatwa no.167): “The subject of waqf must be property having legal value (mal al mutaqawwim)

provided it is land or movable property with regard to which there is custom. If the said securities be property having legal value and there has been a practice of endowing them in the country of the dedicator, their waqf would be valid according to Imam Muhammad, like the waqf of dirhams and dinars the waqf of which is now recognised ...This opinion has been adopted by the majority of jurists of various countries as stated in the Hidayah and this is the correct opinion as stated in the Is’af and it is the dictum of most doctors as stated in the Zahiriyyah. It is also laid down in Radd al-Mukhtar and it is expressly laid down in the commentary on the Durr that the fatwa is in accordance with this. As to the waqf of movables accessories to land, it is valid without any difference of opinion between Abu Yusuf and Muhammad …

Now, as to shares in trading companies, their waqf is of the nature of waqf of musha’. Now that you know that the waqf of movables is valid according to Muhammad you should have also regard for the conditions laid down by him, e.g., that they should be divided (not musha), when they are capable of division, and that they should be delivered to a mutawalli even though they do not satisfy the condition of perpetuity, ‘ta’bid’. Finally you should know that the language of the jurists here show some leaning towards taking special recognised practice, ‘urf khass, into consideration. This is one of the views of the school and it is a proper view, since the language of the dedicators is based on their special practice, ‘urf … Thus, the Mufti of Egypt has hesitated only on the question of whether the practice in Turkey can be taken as binding for all Muslims. But his final words; “you should know that … jurists here show some leaning towards taking special recognised practice, ‘urf khass, into consideration” makes clear that custom in a Muslim country would be respected by the others. To be on absolutely safe ground, Suhrawardy had Hasan Fehmi Bey ask the Mufti of Alexandria the same question as well. Answer (by Muhammad Bakhit al-Muti’i, the Hanafi jurist of the University Mosque of al-Azhar, Mufti of Alexandria):

29

“These shares etc. are all included under the term movables and the pertinent rule is as follows: “….the waqf of movables as accessories to land is valid without any difference of opinion between Abu Yusuf and Muhammad. If the waqf of such movables be made independently (not as accessories to land) then Abu Yusuf rejects it, but Muhammad accepts subject to ta’amul. This opinion has been adopted by the majority of jurists of various countries as stated in the Hidayah, the Is’af, and in the Zahiriyya. Moreover, it has been stated in the Mujtaba on the authority of the Siyar that according to Muhammad it is valid to make a waqf of movables unrestrictedly and according to Abu Yusuf only when there is ta’amul. Therefore, when a practice has arisen as to making waqf of these securities and shares, their waqf is valid, especially as they are of the nature of coins, dirhams and dinars. Now we find in the Manh: as a practice has arisen in our days in Turkey and other countries of making waqf of dirhams and dinars, they come under the dictum of Muhammad in accordance with which is the fatwa as regards movables in which there is ta’amul….

Since the ta’amul of the Muslims as regards to these things is based on the rule of recognised practice urf, whereby analogy is disregarded on account of the saying of the Prophet, “Whatever is good in the sight of Muslims is good in the sight of Allah” as reported by Ahmad. That is why it is laid down in the Mabsut, “What is established by usage, ‘urf, is like what is established by express text”. And God knows best. (Signed) Muhammad Bakhit al-Muti’i.

Two points attract our attention in this fatwa; first, Bakhit al-Muti’i seems to have been aware of Imam Muhammad’s permission regarding the waqf of movables whether there is established custom or not, hence his statement, “according to Muhammad it is valid to make a waqf of movables unrestrictedly” and second, based upon Mabsut by al-Sarakhsi, one of the most respected sources in Islamic jurisprudence, he gives custom an eminence approaching to that of the Qur’an and the sunnah. We are now in a position to summarise the Hanafi position on the validity of the waqfs of movables or their special form, the cash waqfs. The majority of the sources presented above are in agreement that as far as the validity of these waqfs is concerned there is no need to refer to Imam Zufer, who is considered to be a relatively weak source. The whole issue can be traced back to the “two companions” of Abu Hanife; Imam Abu Yusuf and Imam Muhammad al-Shaybani, both of whom are considered to be the greatest authorities of the Hanafi Law. It is important that both have approved the waqf of movables. The only point at which they differ is that whereas Abu Yusuf approves of them subject to custom, Muhammad’s approval is subject to custom prevailing at his own time and country and subject to custom that may emerge after his time and in any other land. This flexible interpretation of Imam Muhammad is conveyed to us by another eminent jurist, Shams al-A’immah al-Sarakhsi. Therefore, it is most reliable. It is for this reason that many sources quoted above consider Imam Muhammad’s approval as unrestricted. At this point the following rule applies: when of two conflicting opinions, one is more favourable to the waqf, the mufti should deliver fatwa in accordance with that opinion. Consequently, Imam Muhammad’s ruling applies and the Hanafi School declares the waqfs of movables, including cash waqfs and the waqf of ships, valid. Finally, it should be added that the endowed cash should be, preferably, invested through mudaraba, as Imam Zufer had suggested. 3. The Shafi’i Position:

30