a few more bubbles fin254f: spring 2010 lecture notes 2.3-2.4 readings: shiller 1-2, kindleberger...

Post on 20-Dec-2015

219 views

TRANSCRIPT

A Few More Bubbles

Fin254f: Spring 2010

Lecture notes 2.3-2.4

Readings: Shiller 1-2, Kindleberger and Aliber, 8,

"What Moves Stock Prices"

Outline

The U.S. stock market summary The U.S. real estate market Three recent events

Japan 1980's East Asia 1990's U.S: dot.com 90-2000's

Real U.S. Stock Prices

Shiller's P/D plots

and U.S. Price/Earnings Ratio1881-2009

Unusual Periods for U.S.

Twentieth century peak, June 1901, P/E = 25.2 Real earnings double over previous 5 years Real return 10 years after this = 4.4% per year, 20

years = -0.2% (includes dividends) Sept 1929: P/E = 32.6,

Real index does not return to this price level until mid 1950’s

Real price drop into early 1930’s = -80.6% Real return = -1.4% over 10 years, 0.4% over next

20 years (includes dividends)

Unusual Periods for U.S.

January 1966: P/E = 24.1, Kennedy/Johnson peak Earnings up over previous 5 years 36% Real stock prices do not return to this level

until 1992 Real return over next 10 years = -1.8%,

1.9% over the next 20 years

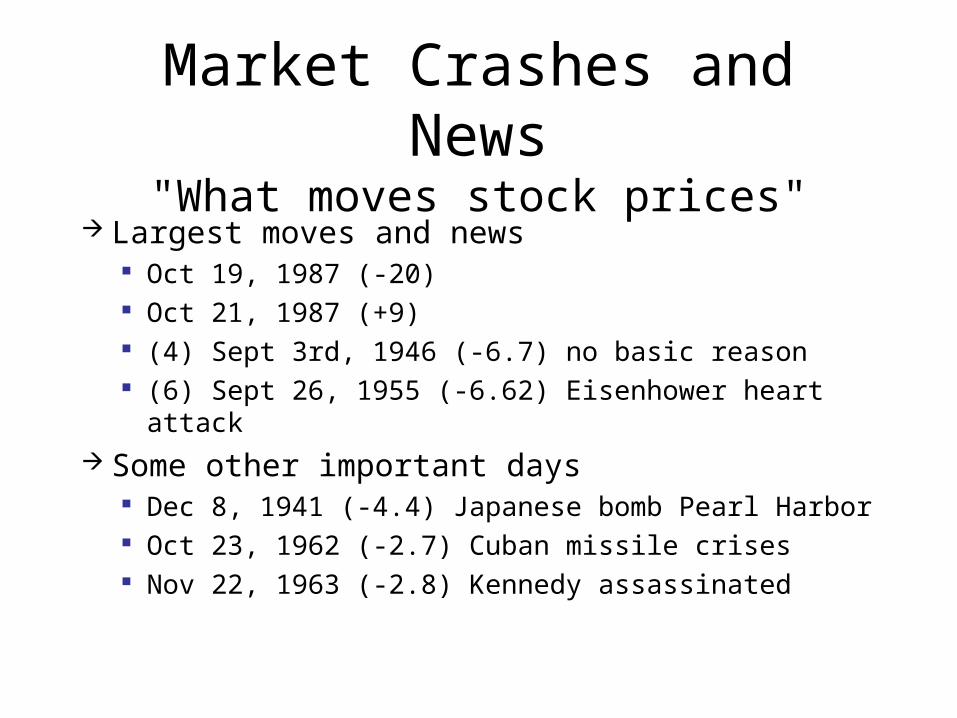

Market Crashes and News"What moves stock prices"

Largest moves and news Oct 19, 1987 (-20) Oct 21, 1987 (+9) (4) Sept 3rd, 1946 (-6.7) no basic reason (6) Sept 26, 1955 (-6.62) Eisenhower heart attack

Some other important days Dec 8, 1941 (-4.4) Japanese bomb Pearl Harbor Oct 23, 1962 (-2.7) Cuban missile crises Nov 22, 1963 (-2.8) Kennedy assassinated

U.S. Interest Rates

U.S. Interest Rates

U.S. Interest Rates

Few obvious movements with stock prices

International Comovements

Figure 1.2

Outline

The U.S. stock market summary The U.S. real estate market Three recent events

Japan 1980's East Asia 1990's U.S: dot.com 90-2000's

U.S. House Prices (long)

U.S. Real Estate Prices

Shiller figure 2.1Predictability (R2 = 0.5)Run ups are small than stocksPast not informative (nonstationary??)

Statistics difficultFundamentals not well connected (fig.

2.1)

Other Data Features

Several major declines Small run up in the 1920’s Many regional bubbles

Geography is important Figs 2.2, 2.3 Not all cities move together, but more so now?

Large (and permanent) increase after WWII GI Bill of rights Home construction restricted during the war, then

expands

Why Do People Think Home Prices Always Rise?

Two possibilities Infrequent transactions Inflation

Example House bought in 1948 for $16,000, and sold for

$190,000 in 2004 Total real return = 48% Real return per year = 1% Also, property probably improved a lot over time

(different goods) - also in index too

Special Things about Real Estate

Long term comparative data Difficult Hard to find

Curious features about Care and owner/renter incentives

Special tax breaksLeverageCross country differences

Outline

The U.S. stock market summary The U.S. real estate market Three recent events

Japan 1980's East Asia 1990's U.S: dot.com 90-2000's

Bubbles in Asia (80’s-90’s)Kindleberger/Aliber (8)

Japan 1980’s Land values: Imperial palace = California Market value of Japanese land = 2 x U.S.

(land area = 5 percent of US) Stock market: Twice the market val of US

7/10 largest banks are Japanese (assets) Japanese firms acquiring “trophy” properties

Rockefeller center Pebble Beach Golf course

Japanese Growth History

Late 1800’s begins to industrialize Adopting foreign institutional models Early industry built around feudal families

Large multi-industry holding companies General MacArthur outlaws at end of WWII Firms replace this with “cross-holdings”

Holding of other firm’s shares 1950’s-1960’s, Japan starts to catch up

Growth rates near 10 percent per year

Japan in 1980’s

Global economic powerWorld leader in

Cars Electronics Photo optics

Industrial planning: “Japan Inc.”Financial structures: bank lending

Financial Regulation Restrictions on interest rates Negative real returns Leaves only real estate and stocks with positive

returns Mid 80’s begins to deregulate Begins to financially become more global Real estate and stock markets continue rising Bank assets increase, collateral increases, lending

increases Cross holdings magnify changes in asset values: Buy

shares of other firms rather than investing

Three Factors in the Japanese Real Estate Bubble

Long term positive returns (lots of scarce land?? Phoenix versus Tokyo)

Financial liberalization: Opens up more real estate lending

Monetary growth Bank of Japan intervenes to keep value of Yen low

relative to the dollar Money supply expands Banks increase reserves : can lend more

Stock Market Bubble Continues

Cross holdings drive firm and investor wealth

As value of Japanese market rises, international funds allocate larger amounts to Japan

Drives prices higher(Same in dot com bubble: Passive

funds part of problem.)

Peaks in 1989

Some real estate buyers in cash bind Rentals smaller than interest payments Think “Ponzi”! Distressed selling starts Land and stock prices begin falling

Downward spiral Property sales, price drops Bank capital falls Lending falls - > more price drops

Japan

Japan in the late 90’s and early 2000’s

Japan has some periods of deflation Near zero interest rates Bankruptcies rise Banks in trouble Depositors do not withdraw

Belief government will step in Too big to fail

Foreign lenders to Japanese banks believe government will not help them

Japanese lenders and firms move to foreign banks

Shift Away from Japan

Exports increase/Imports fallYen appreciates Investors shift to China, Malaysia,

Thailand where labor costs were lower

Early 1990's

East Asian "tigers"Beginning in the 1960's and 70'sKey aspects

Transformations Growth (often near 10%)

Stock markets in Thailand and Malaysia take off in the early 90's (300 - 500%)

Foreign Capital

Foreign direct investment Setting up manufacturing Real estate booms Consumer lending takes off 1996: Consumer finance companies experience

losses, begin to fail Foreign creditors nervous Capital inflows suddenly stop Thai Baht can no longer be managed on a dollar

peg, currency collapses

Regional Contagion

Triggers crisis across regionOther currencies collapse

Indonesia loses 70 percent of valueStock prices down 30-60 percentLarge number of banks fail

"Miracle" Comments Disappear

Crony capitalismDestabilizing speculation

Ending in Asia, Starting in the U.S. (late 90's)

Current account deficits shift to surplus (Central bank reserves increase)

Exports to U.S. riseU.S. trade deficits riseU.S. dot com bubble gets really heated

Dot Com World

VC's, Entrepreneurs, IPO's First day "Price Pop" December 1996: Greenspan "Irrational

Exuberance" Dow = 6300, NASDAQ = 1300

End of 1999 Dow = 11700, NASDAQ = 5400

NASDAQ value = 80% NYSE value Initially "new economy" stocks Eventually all stocks

“Our proprietary portfolio of New Economy stocks was up

over 80.2% in 1998!”

“At this rate, $10,000 turns into $3.4 million in

10 years or less!”

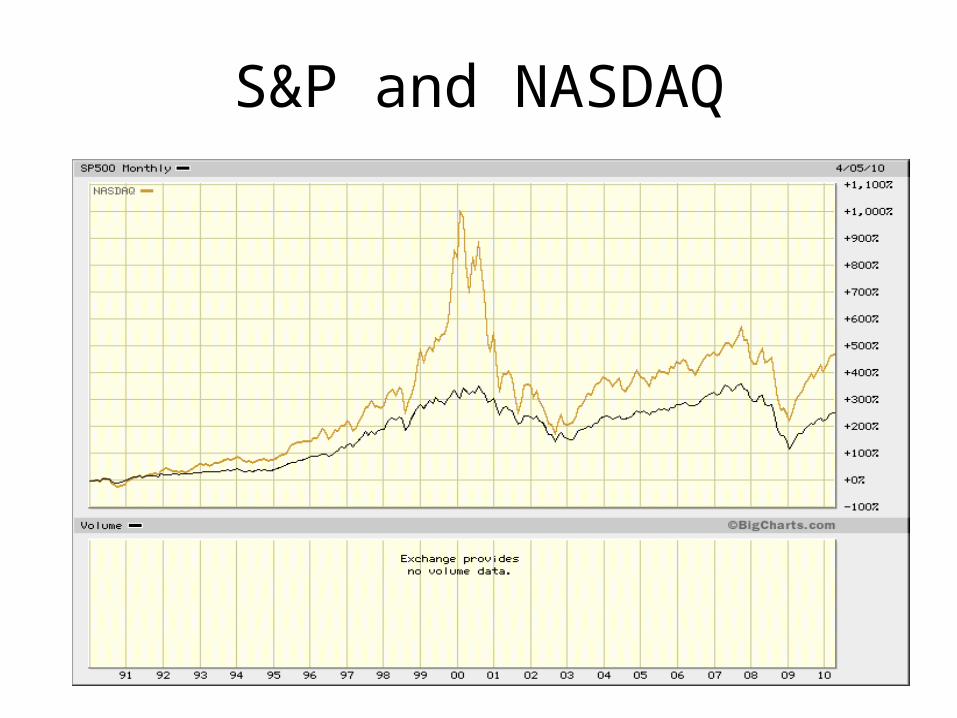

When Did the Bubble Start?

1995?1998?

S&P and NASDAQ

Bubble Persists

1999: Fed obsessed with Y2K Increases bank liquidityAfter 2000 Fed reduces liquidityStock market falls 40%, NASDAQ 80%

International Aspects of Dot.com

Capital inflows to U.S.Dollar appreciates Import prices fall in U.S.U.S. inflation lowU.S. savings rates fall

Summary: The Three Recent Bubbles

Japan: 1980'sEast Asia: 1990'sUS dot com: late 90's early 2000'sHow do they fit into the Minsky

taxonomy? Ponzi??