a deep dive into the salt implications of federal tax reform · 2017 new england state and local...

TRANSCRIPT

2017 NEW ENGLAND STATE AND LOCAL TAX FORUM

2017 New England SALT Forum

A Deep Dive into the SALT Implications of Federal Tax Reform

1

David PopeBaker & McKenzie LLP

[email protected](212) 626-4289

Andrew ApplebyEversheds Sutherland (US) LLP

[email protected](212) 389-5042

Karl FriedenCouncil On State Taxation

[email protected](202) 484-5215

2017 NEW ENGLAND STATE AND LOCAL TAX FORUM

Agenda

1. State Tax Implications of Federal Tax Reform2. Business Tax Reform3. International Tax Reform4. Personal Income Tax Reform5. Final Observations

2

State Tax Implications of Federal Tax Reform

2017 NEW ENGLAND STATE AND LOCAL TAX FORUM

State Dependence/Independence with Federal Income Tax Law

– Due to state conformity with federal tax laws, changes at the federal level flow to state level.

– As a result, federal legislation may increase or decrease state tax revenues.

– States may diverge from federal tax law via state “decoupling” modifications.

– Taxpayers must separately track, monitor, and implement state modifications to federal provisions.

4

2017 NEW ENGLAND STATE AND LOCAL TAX FORUM

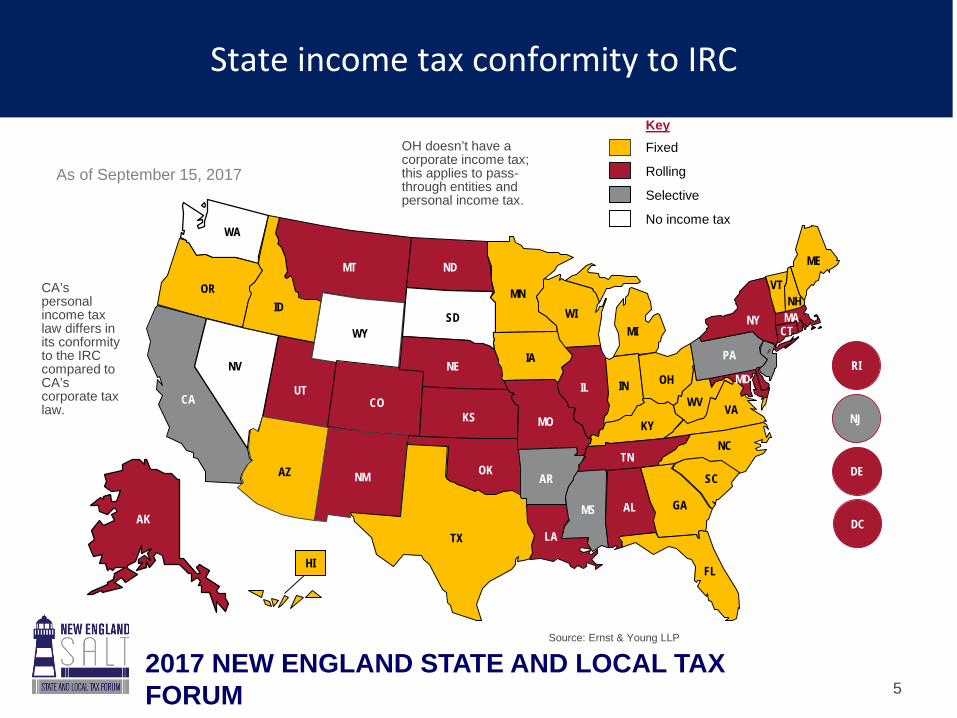

State income tax conformity to IRC

AK

HI

ME

VTNH

MANYCT

PA

WV

NC

SC

GA

FL

IL OHIN

MIWI

KY

TN

ALMS

AR

LATX

OK

MOKS

IA

MN

ND

SD

NE

NMAZ

COUT

WY

MT

ORID

NV

CAVA

MD

KeyFixed

Rolling

Selective

No income tax

As of September 15, 2017

CA’s personal income tax law differs in its conformity to the IRC compared to CA’s corporate tax law.

TX’s conformity date is January 1, 2007.

RI

NJ

DE

DC

OH doesn’t have a corporate income tax; this applies to pass-through entities and personal income tax.

WA

5

Source: Ernst & Young LLP

2017 NEW ENGLAND STATE AND LOCAL TAX FORUM

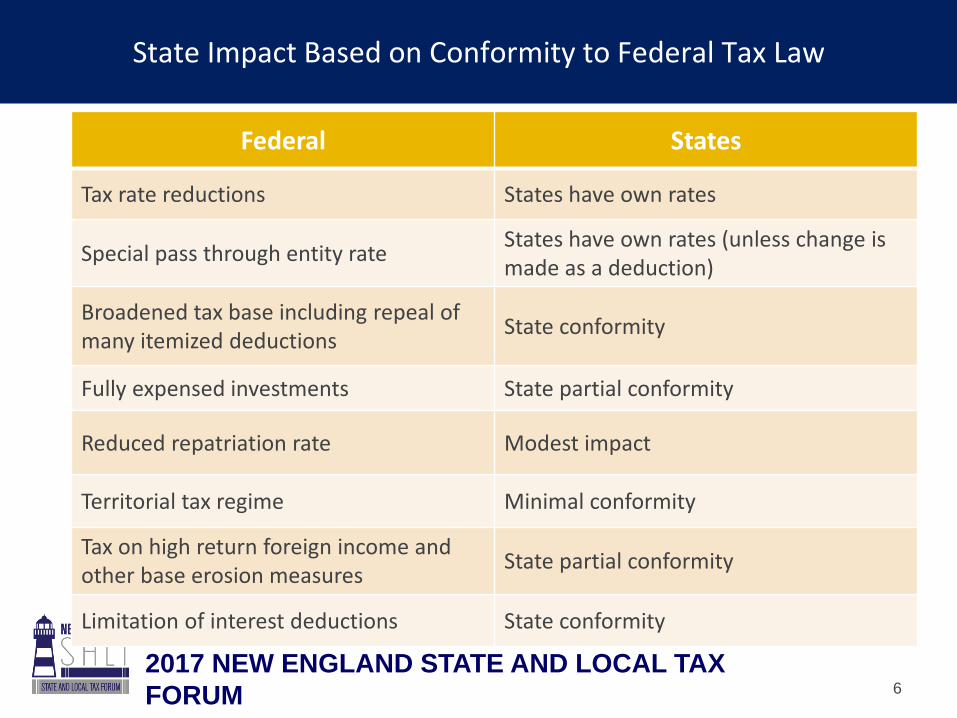

State Impact Based on Conformity to Federal Tax Law

Federal States

Tax rate reductions States have own rates

Special pass through entity rate States have own rates (unless change is made as a deduction)

Broadened tax base including repeal of many itemized deductions State conformity

Fully expensed investments State partial conformity

Reduced repatriation rate Modest impact

Territorial tax regime Minimal conformity

Tax on high return foreign income and other base erosion measures State partial conformity

Limitation of interest deductions State conformity

6

Business Tax Reform

2017 NEW ENGLAND STATE AND LOCAL TAX FORUM

Polling Question 1

What is the likelihood of ANY federal tax reform to be passed?

A. LikelyB. UnlikelyC. The most likely outcome is a lower rate onlyD. Unsure - by the time I’m done voting, another

revised bill will be published

8

2017 NEW ENGLAND STATE AND LOCAL TAX FORUM

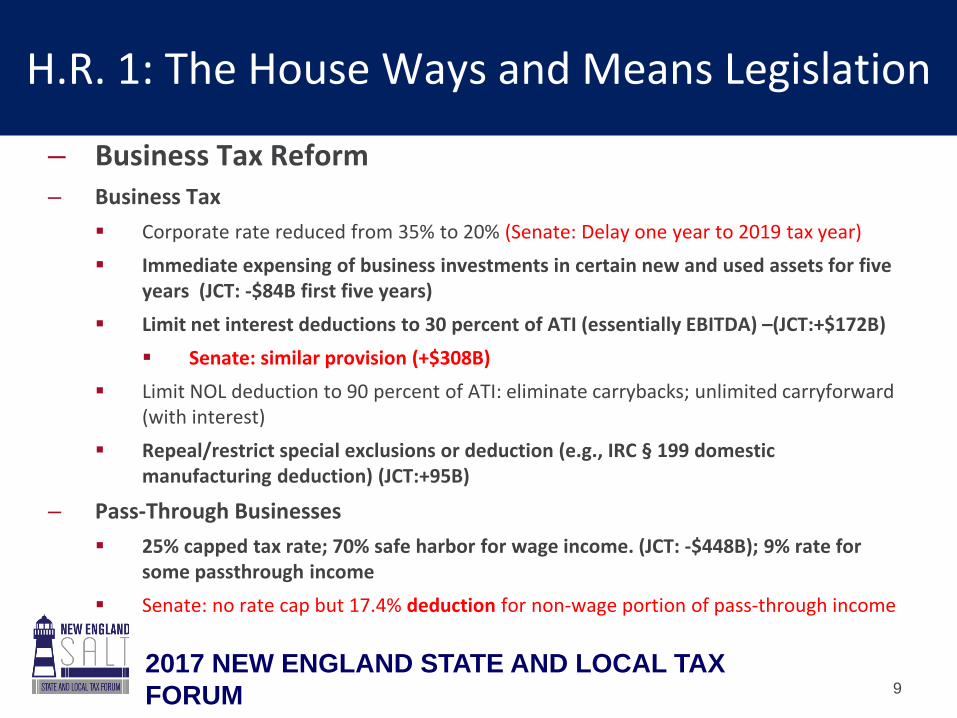

H.R. 1: The House Ways and Means Legislation

– Business Tax Reform– Business Tax

Corporate rate reduced from 35% to 20% (Senate: Delay one year to 2019 tax year) Immediate expensing of business investments in certain new and used assets for five

years (JCT: -$84B first five years) Limit net interest deductions to 30 percent of ATI (essentially EBITDA) –(JCT:+$172B)

Senate: similar provision (+$308B) Limit NOL deduction to 90 percent of ATI: eliminate carrybacks; unlimited carryforward

(with interest) Repeal/restrict special exclusions or deduction (e.g., IRC § 199 domestic

manufacturing deduction) (JCT:+95B)

– Pass-Through Businesses 25% capped tax rate; 70% safe harbor for wage income. (JCT: -$448B); 9% rate for

some passthrough income Senate: no rate cap but 17.4% deduction for non-wage portion of pass-through income

9

2017 NEW ENGLAND STATE AND LOCAL TAX FORUM

States decoupling from bonus depreciation

State conforms to bonus depreciation (Alaska)

No general corporate income tax

State does not conform to bonus depreciation (Hawaii)

Source: Thomson Reuters

10

International Tax Reform

2017 NEW ENGLAND STATE AND LOCAL TAX FORUM

Polling Question 2

Will international tax reform affect your business?

A. No, we’re located solely within the U.S.B. Yes - positivelyC. Yes - negativelyD. Unsure - by the time I’m done voting, another

revised bill will be published

12

2017 NEW ENGLAND STATE AND LOCAL TAX FORUM

H.R. 1: The House Ways and Means Legislation

– International Tax Reform Move from worldwide to territorial tax system

100% exemption for dividends from foreign subsidiaries (at least 10% owned)

Accumulated foreign earnings held overseas treated as repatriated under special Subpart F classification, with a bifurcated rate (14%/7%) for liquid and illiquid assets (JCT:+$293B) (Senate: 10%/5% rates)

Current year inclusion of income with “foreign high returns” (JCT:+$77B) Excise tax on outbound related party payments; ECI election (+154B) Require some R&D expenditures to be capitalized over 15 years for

research conducted outside the country (+$70B) Senate: Has its own base erosion measures ($123B) and a current-year

inclusion for global intangible low-taxed income ($115B).

13

2017 NEW ENGLAND STATE AND LOCAL TAX FORUM

State income tax: State law modifications for Subpart F income

KeyNo modification (potentially taxable)

Full modification (generally not taxable)

Special rules (taxability typically impacted by percentage ownership of subsidiary or state return filing methodology – see also notes)

No corporate income tax

Notes: – California: Controlled Foreign

Corporation (CFC) and its corporate owner that are included in same worldwide unitary combined return allowed a full modification (not taxable); CFC and its corporate owner that are included in the same water’s edge (WE) unitary combined return allowed a full modification (not taxable) if CFC is part of California WE group, but 25% inclusion if CFC and its corporate owner are unitary but are not part of the WE group

– Oregon: Dividends deemed received includes Subpart F income; 100% elimination if payor and recipient are members of the same unitary group filing an Oregon consolidated return; 80% if received from a 20%-or-more-owned foreign corporation; 70% if received from a less-than-20%-owned foreign corporation

– Utah: Federal dividends received deduction (DRD) added back; however, Utah allows a 50% DRD for dividends considered to be received or received from a subsidiary (which includes Subpart F income) that is: (1) a member of the unitary group, (2) organized or incorporated outside of the US, and (3) not included in a combined report

– Continued next page . . .

As of October 11, 2017

AK

HI

ME

VTNH

NYCT

PA

WV

NC

SC

GA

FL

IL OHIN

MIWI

KY

TN

ALMS

AR

LATX

OK

MOKS

IA

MN

ND

SD

NE

NMAZ

COUT

WY

MT

WA

ORID

NV

CAVA

MA

MD RI

NJ

DE

DC

14

Source: Ernst & Young LLP

2017 NEW ENGLAND STATE AND LOCAL TAX FORUM

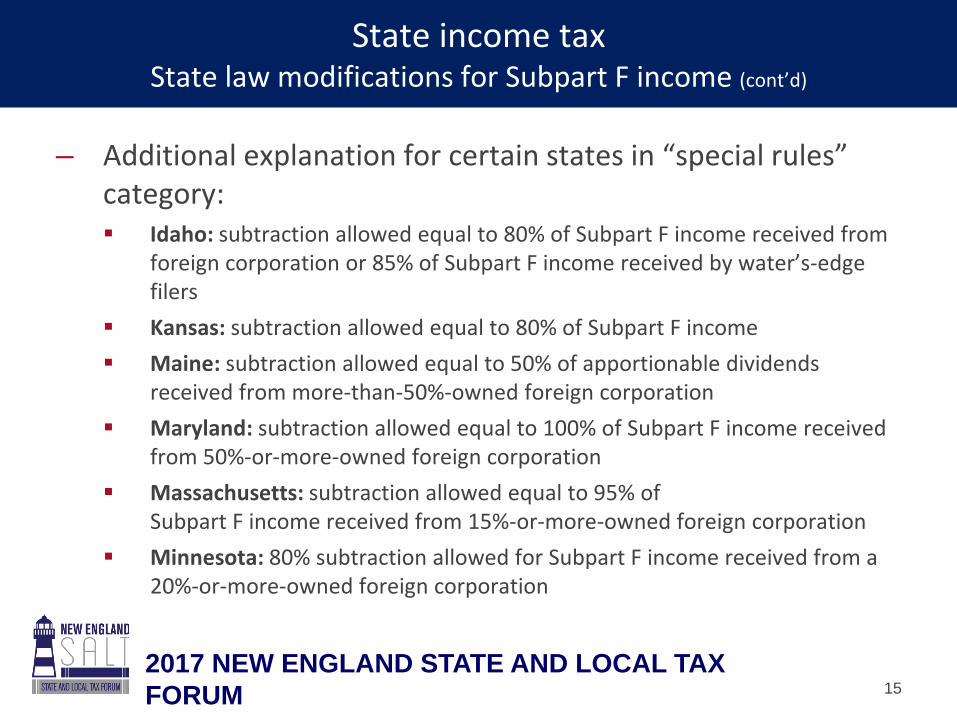

State income taxState law modifications for Subpart F income (cont’d)

– Additional explanation for certain states in “special rules” category: Idaho: subtraction allowed equal to 80% of Subpart F income received from

foreign corporation or 85% of Subpart F income received by water’s-edge filers

Kansas: subtraction allowed equal to 80% of Subpart F income Maine: subtraction allowed equal to 50% of apportionable dividends

received from more-than-50%-owned foreign corporation Maryland: subtraction allowed equal to 100% of Subpart F income received

from 50%-or-more-owned foreign corporation Massachusetts: subtraction allowed equal to 95% of

Subpart F income received from 15%-or-more-owned foreign corporation Minnesota: 80% subtraction allowed for Subpart F income received from a

20%-or-more-owned foreign corporation

15

Personal Income Tax Reform

2017 NEW ENGLAND STATE AND LOCAL TAX FORUM

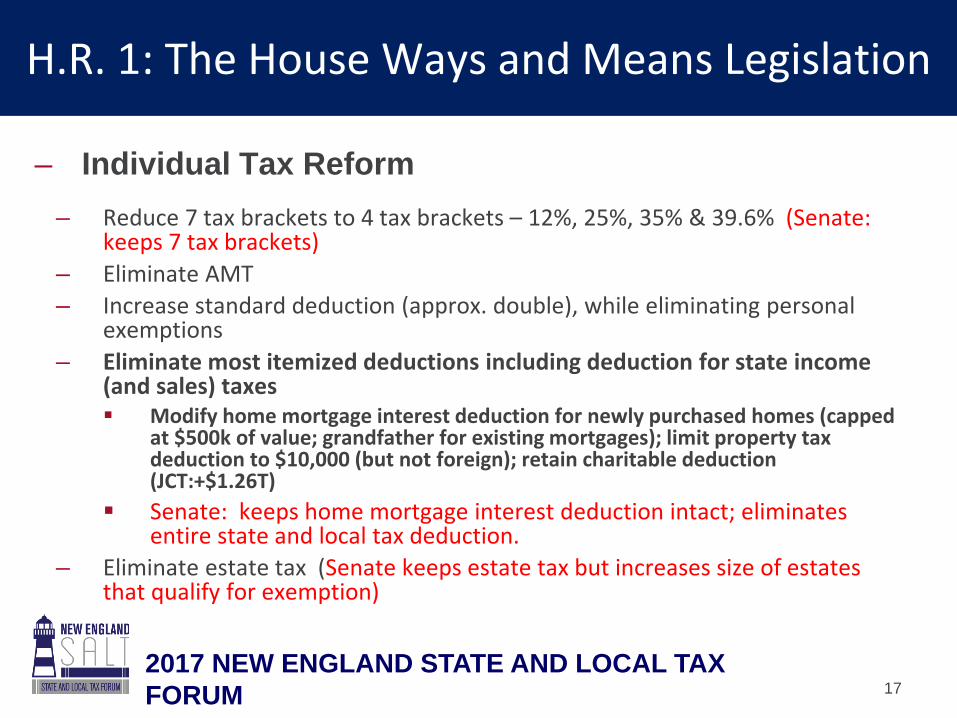

H.R. 1: The House Ways and Means Legislation

– Reduce 7 tax brackets to 4 tax brackets – 12%, 25%, 35% & 39.6% (Senate: keeps 7 tax brackets)

– Eliminate AMT– Increase standard deduction (approx. double), while eliminating personal

exemptions– Eliminate most itemized deductions including deduction for state income

(and sales) taxes Modify home mortgage interest deduction for newly purchased homes (capped

at $500k of value; grandfather for existing mortgages); limit property tax deduction to $10,000 (but not foreign); retain charitable deduction (JCT:+$1.26T)

Senate: keeps home mortgage interest deduction intact; eliminates entire state and local tax deduction.

– Eliminate estate tax (Senate keeps estate tax but increases size of estates that qualify for exemption)

– Individual Tax Reform

17

2017 NEW ENGLAND STATE AND LOCAL TAX FORUM

SALT Deduction by the numbers: TY2015 Deductions

Amount deducted

(in $000’s)

Number of returns

Estimated Tax Cost

(in $000’s)

Total state and local tax deduction

$ 553,015,621 44,191,436 $ 90,700,000

• Income tax $ 335,060,168 33,063,383

$ 56,230,000• Sales tax $ 17,641,159 9,627,447• Personal

property tax$ 9,312,994 18,858,908

• Other tax $ 2,395,266 2,744,266• Real estate tax $ 188,605,843 37,613,402 $ 34,470,000

► Elimination would significantly affect the federal income taxes that individuals pay.

Source: DEDUCTIONS: IRS, Statistics of Income Division, Publication 1304, September 2017Table 2.6. Returns with Itemized Deductions: Sources of Income, Adjustments, Itemized Deductions by Type, Exemptions, and Tax Items, by Age, Tax Year 2015 (Filing Year 2016) (available on the Internet at https://www.irs.gov/downloads/irs-soi?page=424&sort=asc&order=Date ; TAX EXPENDITURES U.S. Dept. of Treas. Office of Tax Analysis, Tax Expenditures (Sept. 28, 2016) (items 59 (Deductibility of State and local property tax on owner-occupied real estate) and 166 (Deduction of nonbusiness State and local taxes other than owner occupied real estate taxes)

18

Final Observations

2017 NEW ENGLAND STATE AND LOCAL TAX FORUM

What Happens Next?

– Generally effective for tax years beginning after 2017.– Will tax rate cuts and/or deductions be limited to 10 years to satisfy

requirements of the Senate Reconciliation process?– Will some of the pay-fors be changed? Fate of the state and local income and property tax deductions;

and the itemized deduction for home mortgage interest? Changes in the tax rate on repatriated income and “base erosion”

provisions taxing foreign income or outbound related-party payments on a current basis?

– Will federal tax reform survive the slim margin of error created by the narrow Republican majorities in the House and Senate?

– What long-term impact will federal tax reform have on state and local finances and taxes?

20

2017 NEW ENGLAND STATE AND LOCAL TAX FORUM

Source: National Conference of State Legislatures

21

The Political Road Map: 2016 Post-Election State Legislative Control

Thank You

David PopeBaker & McKenzie LLP

[email protected](212) 626-4289

Andrew ApplebyEversheds Sutherland (US) LLP

[email protected](212) 389-5042

Karl FriedenCouncil On State Taxation

[email protected](202) 484-5215