a cushman & wakefield research & insight .../media/reports/uk/uk shopping...a cushman &...

TRANSCRIPT

SEPTEMBER 2017

UK SHOPPING CENTRES: DEAD OR ALIVE?

A CUSHMAN & WAKEFIELD RESEARCH & INSIGHT PUBLICATION

Cover image courtesy of LandSec

CONTENTS

PAGE

OVERVIEW 02

RECENT TRENDS 05

FUTURE TRENDS 10

OUTLOOK 12

`

OVERVIEW

For some years now, there has been a seemingly endless stream of negative headlines surrounding the UK retail sector, in particular the shopping centre market. It is generally accepted that UK retailers now need fewer stores and vacancy rates are very high in some areas, particularly in secondary locations in smaller towns – as high as 30-40% in some cases. But, should we believe all the headlines forecasting doom and gloom in the UK shopping centre sector, and is bricks and mortar retailing really in terminal decline?

WHAT NEXT FOR UK SHOPPING

CENTRES?

RETAILER ADMINISTRATIONS

RISE

FOOTFALL TRACKING DOWN

BUSINESS RATES TO INCREASE

BRICKS AND MORTAR RETAILING UNDER PRESSURE

BREXIT IMPACTING ON RETAIL SALES

UK SHOP VACANCY RATES RISING

ONLINE RETAIL SPEND GROWING RAPIDLY TO 16%

OF TOTAL SALES IN 2017

POLITICAL UNCERTAINTY HAVING

A NEGATIVE IMPACT ON CONSUMER CONFIDENCE

2

`

Our view is that this is not the case. While it is undeniable that some parts of the retail sector are struggling, our latest research on the UK shopping centre market shows that much of the sector – notably more dominant schemes - continues to perform well. In fact, as graph 1 shows, rental growth for the larger out-of-town shopping centres has easily exceeded that for the other retail sub-sectors over the last five years. New developments and extensions to existing schemes are delivering significantly improved customer experiences – which many agree cannot be replicated online – with plenty of new and exciting retail formats entering the market.

Much of the ‘damage’ being done to physical retail results from the growth in internet sales, which now account for around 16% of total retail sales. However, on a positive note, the rate of growth in online shopping is slowing.

Clearly, there are significant variations between sectors, with online sales of electronics, music and entertainment products already accounting for nearly 50% of total sales, while food and health & beauty products are still way behind at just 5-6% of overall retail sales. That said, for the retailer, it is arguably irrelevant where the sale takes place, provided they have a balanced digital/physical platform. However, for the landlord it does matter and a new way of benchmarking and evaluating rental levels will be required.

The human desire to go out, socialise, exchange ideas and touch objects is unlikely to change for the foreseeable future. So, we believe that the majority of consumers will still want to go shopping or at least out for an experience which includes shopping. However, the reality is that we will need less physical space and the remaining space will have to work much harder to attract customers.

In fact, we tend to underestimate the importance of the shop. It is estimated that ‘Click & Collect’ in store and online sales which have been previously browsed in-store add another 5% to store sales. Research done by Verdict (now part of GlobalData) suggests that there is also a ‘halo effect’ which is hard to quantify, whereby some online purchases not browsed in store are driven by the improved brand awareness, good customer service and the trust that comes from having a physical store portfolio instils in increasingly educated shoppers.

Stores are still very important as they still touch nearly 90% of all retail sales

Source: MSCI

GRAPH 1 - RENTAL PERFORMANCE (OVER 1 & 5 YEARS)

5 year figure = average p.a. compoundFigures as at May 2017

2

1 .5

1

0.5

00

-0.5

-1

-1 .5

STANDARD SHOPS IN-TOWN SHOPPING CENTRES

OUT-OF-TOWN SHOPPING CENTRES

RETAIL WAREHOUSES

1.1%

1.6%

0.8%

-0.8%

0.4%

1.4%

0.4%

-1.2%

1 YEAR 5 YEARS

%

3

UK SHOPPING CENTRES : DEAD OR ALIVE?

‘Click & Collect’ accounts for around

of online spend but for some retailers it’s much higher.

10%

Overall, ‘CLICK & COLLECT’ accounts for around 10% of online spend, but for some retailers it is much higher. At John Lewis, for example, ‘Click & Collect’ accounts for over 50% of online sales. Another important trend is that as much as a third of shoppers make an additional purchase instore when they use ‘Click & Collect’.

Retailers have been rationalising their store portfolios, notably in the UK and the US. However, another key trend is the polarisation between CONVENIENCE AND MORE EXPERIENTIAL RETAILING, which is creating significant leasing opportunities for many shopping centre landlords.

More retailers are looking for larger units in prime positions to serve as flagship stores and create a destination to showcase their brands. This has helped drive a strong rise in tenant demand in the major retail destinations.

At the same time, retailers are also looking to offer customers smaller formats or ‘Click & Collect’ facilities in convenient locations, with IKEA opening a number of smaller order and collect points in the UK for example. The key point is that major city centres and shopping centres need scale, flexibility and a variety of unit sizes in order to continue attracting retailers.

The net result of these trends has been a polarisation in rental levels across the shopping centre market, a trend we expect to continue: enhanced rents for the best schemes, as they become more important to retailers, while rents on mid-ranked schemes are likely to be lower. However, this will rely on creating a new and fair method of establishing rental levels.

The shopping centre is being transformed from a place where people just go to buy ‘stuff’ into a LIVE-WORK-PLAY ENVIRONMENT driven by food and beverage, experience and a sense of community. Shoppers also want variety, which is giving rise to more temporary stores with flexible leases.

The most successful schemes are those that bring together the physical and digital worlds through the use of technology. While shoppers want speed and convenience, especially for the more mundane shopping tasks, they also want a pleasurable retail experience. They want gathering spaces, showrooms, creative spaces, restaurants, classes and gyms, as well as shared experiences and memories.

The most successful schemes are those that bring together the physical and digital worlds through the use of technology.

4

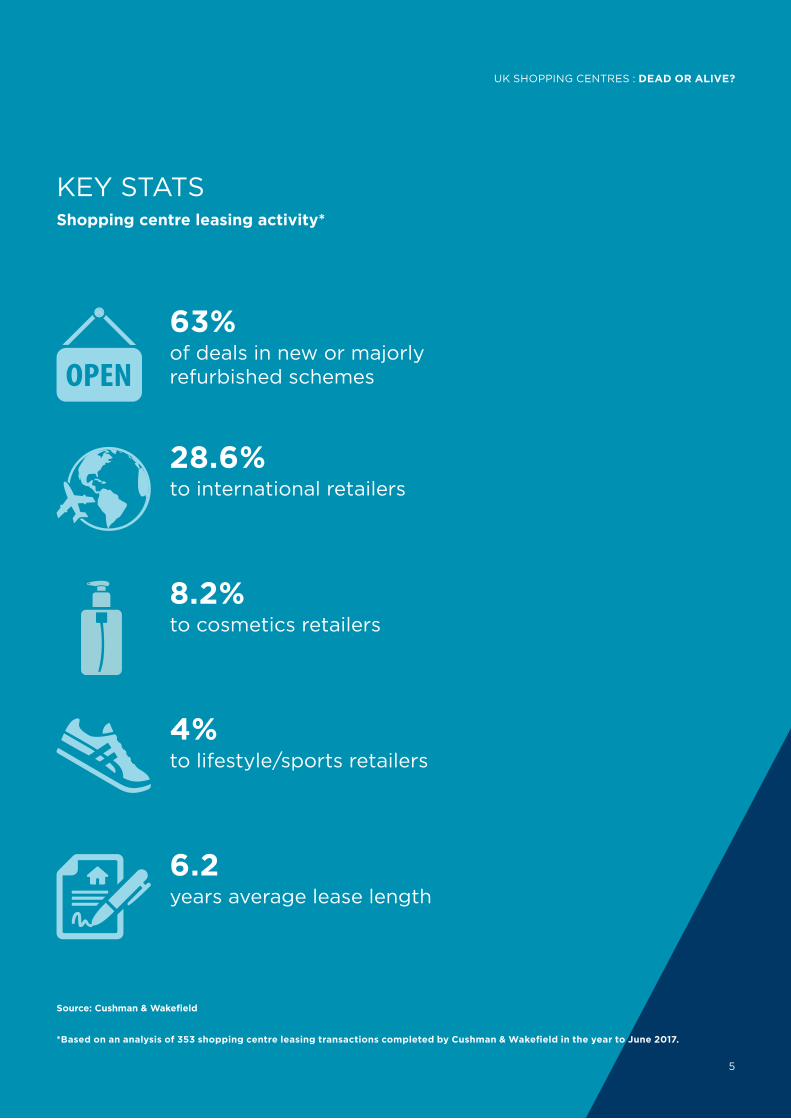

63%of deals in new or majorly refurbished schemes

28.6%to international retailers

8.2%to cosmetics retailers

4%to lifestyle/sports retailers

6.2years average lease length

KEY STATSShopping centre leasing activity*

Source: Cushman & Wakefield

*Based on an analysis of 353 shopping centre leasing transactions completed by Cushman & Wakefield in the year to June 2017.

5

UK SHOPPING CENTRES : DEAD OR ALIVE?

1. Right sizing/upsizing to create flagship storesThere has been a significant focus on right sizing/upsizing among existing tenants in order to create flagship stores and showcase their brands. Next, Zara, H&M, River Island and JD Sports have all been among the leading players but we are also seeing this with Apple, Schuh and Levi Strauss & Co., as well as a number jewellers and JD Sports is one of the tenants at the forefront of this trend and in Grosvenor’s Liverpool ONE scheme, JD Sports has increased its store size from 16,000 sq.ft to 30,000 sq.ft, while it has doubled the size of its Glasgow Fort (British Land) multi-brand store to 40,000 sq.ft.

2. Strong demand from international and multi-fascia retailersWhile the UK retail market has been international for many years, foreign operators remain very active. In the 12 months to June 2017, 28.6% of shopping centre leasing deals involved international retailers, including a number of operators with multiple trading brands. Both Inditex and H&M now trade from six different UK fascias, while L’Oréal (Urban Decay, NYX) and Estée Lauder (Bobbi Brown, Aveda, Smashbox, MAC, Jo Malone, Origins) and VF Corporation (Vans, Lee, Timberland and The North Face) have both been actively expanding.

3. Cosmetics, lifestyle brands and sports are among the most rapidly growing sectorsCosmetics, lifestyle brands and sports are among the most rapidly growing sectors. Indeed, some 8.2% of leasing transactions over the last 12 months were to cosmetics retailers, while 4% of deals involved lifestyle/sports brands, with particular growth in the leisurewear market.

At the new 800,000 sq.ft Westgate Oxford, a joint venture between Landsec and The Crown Estate opening in October 2017. Estée Lauder has taken units for five of its brands (MAC, Jo Malone, Bobbi Brown, Aveda and Smashbox), VF Corporation has taken units for two of its brands (Timberland and Vans). At Westfield Stratford meanwhile, MAC, NYX and Smashbox all took standalone stores in 2016, taking the total number of shops let to beauty brands in the scheme to 18.

The forthcoming 80,000 sq.ft Tunsgate Quarter development in Guildford, which is being developed by Queensberry (for Merseyside Pension Fund), will see the launch of a new lifestyle quarter, with tenants including OKA, Loaf, The White Company, Cath Kidston and Bobbi Brown. The scheme is scheduled to open in spring 2018 with five of the 26 units occupied by cafés and restaurants.

4. Occupiers are showing a strong bias toward new or majorly refurbished locationsIn the last 12 months, over 60% of the leasing transactions in our analysis were in new or majorly refurbished schemes. For example in Festival Place, Basingstoke, which is undergoing a major refurbishment, there have been 12 new transactions in the last year, including Next, Metro Bank and Smiggle.

It is evident that investment in the quality of shopping environment, the customer experience and brands leads to a corresponding rise in sales and leasing activity. Place-making is an absolutely critical factor in where retailers decide to put their brand and helps to creating vibrant, sustainable destinations, as well as drive rental growth.

5. Resurgence of independent operators and the quest for community and authenticityConsumers are increasingly looking for their shops and restaurants to provide a sense of community and authenticity, which plays well to small independent retailers. In fact, data from the British Independent Retailers Association (BIRA) shows that more independent retail shops opened than closed in the first quarter of this year. This follows net increases in the number of independent retailers from 117 and 159 for 2015 and 2016 respectively.

Circus West Village, which opened in summer 2017, is London’s newest riverside village, located between the iconic Battersea Power Station and the 200-acre Battersea Park. Each retail partner has been specifically selected based on the quality and individuality of the experience they will bring to Circus West Village. Occupiers include Wright Brothers, Dodd’s Gin, Vagabond, General Store and Flour Power City Bakery.

RECENT TRENDS

6

Source: Cushman & Wakefield

SHOPPING CENTRE LEASING ACTIVITY IN THE YEAR TO JUNE 2017

New/majorly refurbished schemes

Domestic

Existing schemes

International retailers

New/MajorlyRefurbishedSchemes ExistingSchemes

New/MajorlyRefurbishedSchemes ExistingSchemes

37%

71.4%

63%

28.6%

New/majorly refurbished schemes

v Existing schemes

Domestic retailers v

International retailers

Circus West Village is London’s newest village

with specifically selected retail partners, based

on the quality and individuality of

experience they will bring.

7

UK SHOPPING CENTRES : DEAD OR ALIVE?

8

6. Continued flow of new entrants into the UK marketWhile foreign retailers who are already present here remain active (see above), the UK continues to attract new international retailers. New entrants in the last year or so have included House, Urban Revivo, Reserved, Smiggle, Lovisa, Inditex and H&M brands, Collette, Smashbox, Typo and Missguided. Victoria’s Secret has recently opened a new 10,000 sq.ft store at Churchill Square, Brighton which takes its UK store count to 20.

7. Flexible/shorter leases are now the norm – and can work for landlords and retailersThe trend towards more flexible and shorter leases has continued, with our analysis showing that the average lease length signed in shopping centres is 6.2 years but over 90% of tenants’ break clauses now contain a payback penalty. Landlords are increasingly embracing flexible leasing strategies, both to incubate new brands and to create opportunities to drive growth.

Notable examples include regular use of pop up stores in London locations such as Carnaby Street (Shaftesbury) and Spitalfields (Tribeca) to provide shoppers with a unique one-off experience. Landsec and The Crown Estate meanwhile have adopted an innovative leasing strategy at their Westgate Oxford scheme (opening Oct 2017), with occupiers taking short (5-8) year leases outside the Landlord & Tenant Act without institutional reviews but with annual rental increases either fixed or linked to RPI.

8. Shift in focus from the ‘traditional’ anchor storeThe ‘traditional’ anchor stores such as the large department store operators are consolidating both in terms of size and number of stores, while the international multi-brands are seeking more space. For example, Inditex now occupies 57,000 sq.ft of space at intu Trafford Centre across four of its brands and H&M has taken 112,000 sq.ft at Westfield Stratford for six of its brands. These are the new shopping centre anchors of the future.

9. Retailers are seeking to create both an experiential offer in-store and seamless omni-channelIt is now accepted that successful retailers need to adopt a strong omni-channel strategy. This entails complete operational integration and consistency between stores, online and social media - all of which need to provide the same products, level of service, messages and experience for the customer. In addition, retailers – and an increasing number of manufacturers – are also seeking to create an experiential store offer. Examples include electric car company Tesla which recently opened its 18th UK store in Cambridge’s Grand Arcade (USS), while Volkswagen opened a store at the Bull Ring Birmingham (Hammerson) in July 2017 and Westfield Stratford has seen exciting pop up concepts such as Kit Kat and Nestlé.

10. Greater diversity of brands and productsAs online shopping grows in popularity, established retailers have been adding new brands/product lines to their stores to try and lure more customers back into their shops. Sainsbury’s, which bought Home Retail Group last year, has introduced Argos and Habitat concessions into a number of its stores, as well as 17 Sushi Gourmet counters. They have just launched a Crussh food and juice bar in its Pimlico Store.

Tesco has been adding Arcadia brands such as Dorothy Perkins and Burton, while Debenhams has been adding brands including Sports Direct, Joe & The Juice, Patisserie Valerie and Franco Manca.

9

UK SHOPPING CENTRES : DEAD OR ALIVE?

1. Occupiers will trial new format stores and will continually seek alternative locationsOccupiers, like customers, no longer see a difference between in-town,

out-of-town, in-store or online. Generation Z –which various sources define as people born from the mid-1990s onwards - have no recollection of only bricks and mortar retailing. For them shopping is simply shopping. Occupiers, who are armed with more data on their customer than ever before, are becoming increasingly flexible and confident in trialling new formats and locations to meet ever-changing demands.

Traditionally associated with some of the biggest retail outlets in the world, IKEA opened its first small store concept in Westfield Stratford in August 2016. Measuring just 7,346 sq.ft on the ground floor, IKEA recognises that customers now want to shop and interact in different ways. In the last 18 months, Glasgow Fort – a major out-of-town shopping destination - has seen new openings by traditional ‘in-town’ occupiers, including Pandora, KIKO, Smiggle, Paperchase, Superdry, Pret a Manger and Yo! Sushi.

Moreover, an increasing number of pure play online retailers are turning to bricks & mortar, with Missguided opening its first flagship store in Westfield Stratford earlier this year. Will the likes of Amazon, Boden and Boohoo be following them? Amazon’s recent purchase of Whole Foods suggests it most certainly will.

2. New anchor stores are joining traditional anchorsWho will be the ‘anchor’ of the future? With traditional shopping centre anchors such as the department stores scaling back on store size and numbers, new

operators will have the opportunity to fill the gap. For the time being, the international multi-brand retailers look set to assume this role. With a growing focus on place making and an increasingly diverse tenant mix, it could be that schemes rely less on a single anchor store and more on destination concept anchors.

Anchors of the future will be defined as anything that can make lots of people travel to spend. They may not only be retail clusters but a combination of other things including transport hubs, cultural and civic attractions, music venues, family experiences, sport and health and fitness destinations, universities, food halls, flexible work spaces and even care homes.

Recent new developments confirm this trend, with schemes such as Coal Drops Yard at King’s Cross (Argent) bringing together a wide range of uses – offices (including co-working space), residential, shops, hotels, leisure and community facilities. Together with the adjacent international travel hub, music venues, galleries, the world famous art college Central Saint Martins and Google HQ shows that a major department store is no longer necessarily required to make a new development work.

Likewise, in Edinburgh St James (opening 2021), TH Real Estate have delivered a statement letting to the iconic lifestyle brand W Hotel. This will set the tone for the development to attract like-minded brands.

3. Experience retailing will continue to growAs our latest report on the Global Food & Beverage market shows, customers are spending more on ‘experience’ and less on fashion and other ‘stuff’. An analysis of credit

card data confirms that customer spending on clothing and footwear has been declining in the last 18 months. In contrast, expenditure on recreation, culture, hotels, bars & restaurants has been rising, not just in absolute terms but also as a proportion of the total. This trend is reflected in our own data, with 28% of leasing transactions in 2016/17 involving F&B occupiers.

FUTURE TRENDS

10

UK SHOPPING CENTRES : DEAD OR ALIVE?

4. A premium customer experience will be the minimum standardIf bricks and mortar retailing is ‘to beat’ the internet, owners of shopping destinations must ensure their customers encounter a

premium experience throughout their visit. From the car park via the mall to the restroom, owners have to deliver the best possible experience, including free unlimited Wi-Fi, charge points, valet parking, kids’ areas and rest areas.

The focus should be on creating an exceptional places that exceed customers’ expectations in every way. Tuition retailing is a growing trend which is enhancing the customer experience and offering something not available on-line. A good example is Lululemon, which is among a growing group of retailers constructing unique retail and customer service formats to create buzz and loyalty. Their highly trained ‘educators’ offer run clubs, yoga and nutrition classes with several in-store collaborations. These concepts are less about profit and more about testing out new ideas, evolving their brand and remaining relevant to customers.

5. The Digital Experience will be critical to shopping centre successDestinations of the future will continue to be influenced by who/which developments can embrace and develop the digital revolution.

Retail destinations that can integrate new digital technology into their existing architecture will be the schemes that thrive in the future. Digital enhancing will bring a new dimension to the customer shopping experience, enabling landlords to deliver a distillation of the latest innovations in retailing and lifestyle malls.

6. Continuing shakeout of obsolete schemesHowever, it is undeniable

that some parts of the shopping centre sector are extremely challenged and the shakeout of weaker/obsolete schemes will continue. In some cases this will mean the complete demolition of existing schemes to make way for regeneration opportunities focused on mixed use, including residential, hotels and leisure. Prominent examples include the 1.7 million sq.ft Edinburgh St James development, as well as smaller schemes such as The Oaks in Acton, which will see the partial refurbishment, demolition and redevelopment of a shopping centre to leave a smaller retail component and more residential units. However, we do not see this as a negative trend, more as part of the ongoing evolution of retailing and the continuous renewal of our urban landscape.

11

Experience will be the future and shopping centres and landlords must adapt by creating spaces where customers can engage with brands without necessarily shopping. Human interaction and engagement are an essential part of providing the best possible experience for the consumer. All the points made in this paper reinforce the fact that good management is key to overcoming the challenges faced and will be all the more important in the future.

Physical stores will always be at the heart of this experience - what will change is how these stores operate and serve their customers, with a continuing trend towards personalised shopping. Tills may disappear and robots may take on more repetitive in-store tasks, but well-trained, knowledgeable and helpful staff are best-placed to offer expertise and personalised advice. Tuition retailing and ‘edutainment’, the concept of selling products through a combination of education and entertainment, will become the buzz words. However, for the foreseeable future, real people will remain at the heart of helping the customer to enjoy their shopping experience.

OUTLOOK

It is clear that, for all its innovation, online retailing has not been able to fully replicate the physical shopping experience. Many UK consumers continue to desire physical touch and peer to peer interaction. They want to fully engage with brands and to interact with products in the real world. Technology is simply a tool that assists this process – it does not replace that experience. The real world customer is still King.

12

Physical stores will always be at the heart of this experience - what will change is how these stores operate and serve their customers

13

UK SHOPPING CENTRES : DEAD OR ALIVE?

About Cushman & WakefieldCushman & Wakefield is a leading global real estate services firm that helps clients transform the way people work, shop, and live. Our 43,000 employees in more than 60 countries help investors and occupiers optimize the value of their real estate by combining our global perspective and deep local knowledge with an impressive platform of real estate solutions. Cushman & Wakefield is among the largest commercial real estate services firms with revenue of $5 billion across core services of agency leasing, asset services, capital markets, facility services (C&W Services), global occupier services, investment & asset management (DTZ Investors), project & development services, tenant representation, and valuation & advisory. To learn more, visit www.cushmanwakefield.com or follow @CushWake on Twitter.

This report has been produced by Cushman & Wakefield LLP (C&W) for use by those with an interest in commercial property solely for information purposes and should not be relied upon as a basis for entering into transactions without seeking specific, qualified professional advice. It is not intended to be a complete description of the markets or developments to which it refers. This report uses information obtained from public sources which C&W has rigorously checked and believes to be reliable, but C&W has not verified such information and cannot guarantee that it is accurate or complete. No warranty or representation, express or implied, is made as to the accuracy or completeness of any of the information contained in this report and C&W shall not be liable to any reader of this report or any third party in any way whatsoever. All expressions of opinion are subject to change. The prior written consent of C&W is required before this report or any information contained in it can be reproduced in whole or in part, and any such reproduction should be credited to C&W.

©2017 Cushman & Wakefield LLP. All rights reserved.For more information, please contact ourResearch Department: Cushman & Wakefield LLP125 Old Broad Street London EC2N 1ARcushmanwakefield.com

CWdt-2017-278_09/17

Darren YatesHead of EMEA Retail Research & Insight

[email protected] +44 20 3296 3911

Toby SykesHead of Shopping Centre Leasing

[email protected] +44 20 7152 5240