990-t exempt organization business income tax … no. 1545-0687 form 990-t exempt organization...

TRANSCRIPT

OMB No. 1545-0687Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e))Form 990-T

For calendar year 2012 or other tax year beginning , 2012, andDepartment of the Treasury

Open to Public Inspection for501(c)(3) Organizations Onlyending , 20 . See separate instructions.Internal Revenue Service

D Employer identification number(Employees' trust, see instructions.)

Name of organization ( Check box if name changed and see instructions.)Check box ifA address changed

B Exempt under sectionPrint

orType

Number, street, and room or suite no. If a P.O. box, see instructions.501( )( ) E Unrelated business activity codes

(see instructions.)408(e) 220(e)

408A 530(a)City or town, state, and ZIP code529(a)

C Book value of all assetsat end of year F Group exemption number (see instructions)

G Check organization type 501(c) corporation 501(c) trust 401(a) trust Other trust

H Describe the organization's primary unrelated business activity.

I During the tax year, was the corporation a subsidiary in an affiliated group or a parent-subsidiary controlled group? Yes No If "Yes," enter the name and identifying number of the parent corporation.

J The books are in care of Telephone number(A) Income (B) Expenses (C) NetUnrelated Trade or Business IncomePart I

1

234

5678

9

10111213

ab

abc

Gross receipts or salesLess returns and allowances

Cost of goods sold (Schedule A, line 7)Gross profit. Subtract line 2 from line 1cCapital gain net income (attach Schedule D)Net gain (loss) (Form 4797, Part II, line 17) (attach Form 4797)

Capital loss deduction for trustsIncome (loss) from partnerships and S corporations (attach statement)

Rent income (Schedule C)Unrelated debt-financed income (Schedule E)

c Balance 1c23

4a4b4c567

8

910111213

Interest, annuities, royalties, and rents from controlledorganizations (Schedule F) Investment income of a section 501(c)(7), (9), or (17)organization (Schedule G) Exploited exempt activity income (Schedule I)Advertising income (Schedule J)Other income (see instructions; attach statement)Total. Combine lines 3 through 12

Deductions Not Taken Elsewhere (see instructions for limitations on deductions) (except for contributions,Part II deductions must be directly connected with the unrelated business income)

141516171819202122232425262728293031323334

Compensation of officers, directors, and trustees (Schedule K)Salaries and wagesRepairs and maintenanceBad debtsInterest (attach statement)Taxes and licensesCharitable contributions (see instructions for limitation rules)Depreciation (attach Form 4562)Less depreciation claimed on Schedule A and elsewhere on returnDepletionContributions to deferred compensation plansEmployee benefit programsExcess exempt expenses (Schedule I)Excess readership costs (Schedule J)Other deductions (attach statement)Total deductions. Add lines 14 through 28Unrelated business taxable income before net operating loss deduction. Subtract line 29 from line 13Net operating loss deduction (limited to the amount on line 30)Unrelated business taxable income before specific deduction. Subtract line 31 from line 30Specific deduction (generally $1,000, but see line 33 instructions for exceptions)Unrelated business taxable income. Subtract line 33 from line 32. If line 33 is greater than line 32,enter the smaller of zero or line 32

14151617181920

22b2324252627282930313233

34

2122a

JSA For Paperwork Reduction Act Notice, see instructions. Form 990-T (2012)2E1610 1.000

07/011306/30

PACIFIC UNIVERSITYX C 3 93-0386892

2043 COLLEGE WAY

FOREST GROVE, OR 97116 541800 900000

XADVERTISING/PARTNERSHIP/CONFERENCES

X

ALLIE LOSLI 503-352-2819

2,919. ATCH 1 2,919.

3,488. 3,488.394,458. ATCH 2 394,458.400,865. 400,865.

339,990.

19,666.19,666.

35,157.

ATTACHMENT 3 82,511.477,324.-76,459.

-76,459.1,000.

-76,459.

NY2934 1783 V 12-7.12 67971

Public

icblt)

wherehere (see (seetly connectely connect

s, and trusteesnd trustee

Inspe

ction

pns

nontioctiespnsn99

1010111

2,919.2,919.

Copy

Copy

CpyopCoCC

xp

224,673,746

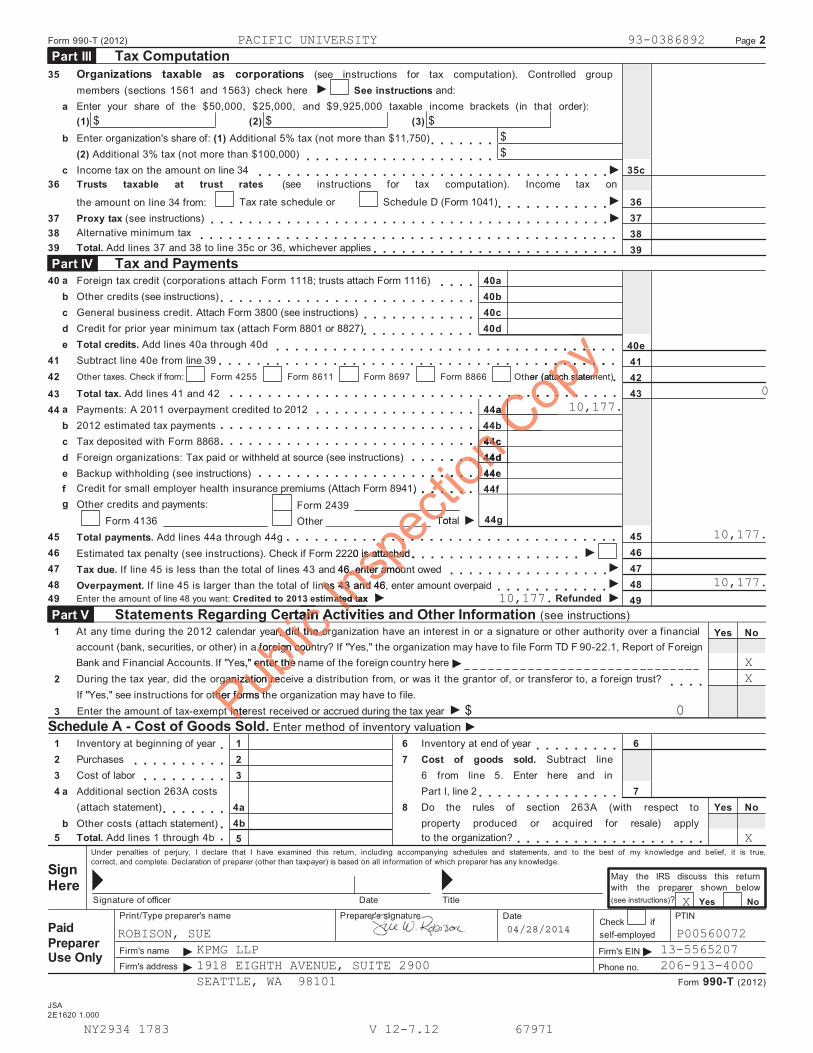

Form 990-T (2012) Page 2Tax ComputationPart III

35 Organizations taxable as corporations (see instructions for tax computation). Controlled group

members (sections 1561 and 1563) check here See instructions and:a Enter your share of the $50,000, $25,000, and $9,925,000 taxable income brackets (in that order):

$ $ $(1) (2) (3)$b Enter organization's share of: (1) Additional 5% tax (not more than $11,750) $(2) Additional 3% tax (not more than $100,000)

c Income tax on the amount on line 34 35c 36 Trusts taxable at trust rates (see instructions for tax computation). Income tax on

Tax rate schedule or Schedule D (Form 1041) 36the amount on line 34 from: 3737 Proxy tax (see instructions)

Alternative minimum tax38 3839

39 Total. Add lines 37 and 38 to line 35c or 36, whichever applies

Tax and PaymentsPart IV a40 Foreign tax credit (corporations attach Form 1118; trusts attach Form 1116) 40a b Other credits (see instructions) 40b c General business credit. Attach Form 3800 (see instructions) 40c d Credit for prior year minimum tax (attach Form 8801 or 8827) 40d e Total credits. Add lines 40a through 40d 40e

41 Subtract line 40e from line 39 41Other taxes. Check if from: Form 4255 Form 8611 Form 8697 Form 8866 Other (attach statement)42 42Total tax. Add lines 41 and 42 4343

a Payments: A 2011 overpayment credited to 2012 44a44 b 2012 estimated tax payments 44b c Tax deposited with Form 8868 44c d Foreign organizations: Tax paid or withheld at source (see instructions) 44d e Backup withholding (see instructions) 44e

Credit for small employer health insurance premiums (Attach Form 8941)f 44f g Other credits and payments: Form 2439

Other 44gTotalForm 41364545 Total payments. Add lines 44a through 44g

4646 Estimated tax penalty (see instructions). Check if Form 2220 is attached 4747 Tax due. If line 45 is less than the total of lines 43 and 46, enter amount owed 4848 Overpayment. If line 45 is larger than the total of lines 43 and 46, enter amount overpaid

Enter the amount of line 48 you want: Credited to 2013 estimated tax Refunded49 49Statements Regarding Certain Activities and Other Information (see instructions)Part V

1 At any time during the 2012 calendar year, did the organization have an interest in or a signature or other authority over a financialaccount (bank, securities, or other) in a foreign country? If "Yes," the organization may have to file Form TD F 90-22.1, Report of Foreign

Yes No

Bank and Financial Accounts. If "Yes," enter the name of the foreign country here2 During the tax year, did the organization receive a distribution from, or was it the grantor of, or transferor to, a foreign trust?

If "Yes," see instructions for other forms the organization may have to file.

Enter the amount of tax-exempt interest received or accrued during the tax year $3

Schedule A - Cost of Goods Sold. Enter method of inventory valuation1 Inventory at beginning of year 1 6 Inventory at end of year 6 2 Purchases 2 7 Cost of goods sold. Subtract line 3 Cost of labor 3 6 from line 5. Enter here and in 4 a Additional section 263A costs Part I, line 2 7

(attach statement) 4a 8 Do the rules of section 263A (with respect to Yes No 4b property produced or acquired for resale) applyb Other costs (attach statement) 5 Total. Add lines 1 through 4b to the organization?5

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true,correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

Sign May the IRS discuss this returnwith the preparer shown belowHere(see instructions)?Signature of officer Date Title Yes No

Print/Type preparer's name Preparer's signature Date PTINCheck ifPaid self-employed

PreparerFirm's name

Firm's address

Firm's EINUse OnlyPhone no.

Form 990-T (2012)

JSA2E1620 1.000

PACIFIC UNIVERSITY 93-0386892

010,177.

10,177.

10,177.10,177.

X X

X

X

ROBISON, SUE P00560072KPMG LLP 13-55652071918 EIGHTH AVENUE, SUITE 2900 206-913-4000SEATTLE, WA 98101

NY2934 1783 V 12-7.12 67971

PPPublic

iccc3 e

ertain Aertain Aear, did the orr, did the or

a foreign coun foreign counes," enter the nenter the

ganization recganization recther forms thther forms th

t intert int

InIInspe

ction

onnono

eec

444c44c 44d44 44e

) 4 TotaT

20 is attachedis attached

d 46, enter amou6, enter amounes 43 and 46, nes 43 and

mated taxmated ta

iviti

Copy

CCC

ther (attach stateme(attach stateme

4a 1

0

04/28/2014er'rrerrerererer s ss ss ss ss ss ss sss ss ss signiiiiiiii atureeeeeeee

Form 990-T (2012) Page 3Schedule C - Rent Income (From Real Property and Personal Property Leased With Real Property)

(see instructions)

1. Description of property

(1)(2)(3)(4)

2. Rent received or accrued

(a) From personal property (if the percentage of rentfor personal property is more than 10% but not

more than 50%)

(b) From real and personal property (if thepercentage of rent for personal property exceeds50% or if the rent is based on profit or income)

3(a) Deductions directly connected with the incomein columns 2(a) and 2(b) (attach statement)

(1)(2)(3)(4)Total Total

(b) Total deductions.Enter here and on page 1,Part I, line 6, column (B)

(c) Total income. Add totals of columns 2(a) and 2(b). Enter here and on page 1, Part I, line 6, column (A) Schedule E - Unrelated Debt-Financed Income (see instructions)

3. Deductions directly connected with or allocable todebt-financed property2. Gross income from or

allocable to debt-financedproperty

1. Description of debt-financed property(a) Straight line depreciation

(attach statement)(b) Other deductions(attach statement)

(1)(2)(3)(4)

4. Amount of averageacquisition debt on or

allocable to debt-financedproperty (attach statement)

5. Average adjusted basisof or allocable to

debt-financed property(attach statement)

6. Column4 divided

by column 5

8. Allocable deductions(column 6 x total of columns

3(a) and 3(b))

7. Gross income reportable(column 2 x column 6)

(1)(2)(3)(4)

%%%%

Enter here and on page 1,Part I, line 7, column (A).

Enter here and on page 1,Part I, line 7, column (B).

Totals Total dividends-received deductions included in column 8

Schedule F - Interest, Annuities, Royalties, and Rents From Controlled Organizations (see instructions)Exempt Controlled Organizations

1. Name of controlledorganization

2. Employer identification number

5. Part of column 4 that is included in the controlling

organization's gross income

6. Deductions directlyconnected with income

in column 5

3. Net unrelated income(loss) (see instructions)

4. Total of specifiedpayments made

(1)(2)(3)(4)Nonexempt Controlled Organizations

10. Part of column 9 that isincluded in the controlling

organization's gross income

11. Deductions directlyconnected with income in

column 10

8. Net unrelated income(loss) (see instructions)

9. Total of specifiedpayments made

7. Taxable Income

(1)(2)(3)(4)

Add columns 5 and 10. Enter here and on page 1, Part I, line 8, column (A).

Add columns 6 and 11. Enter here and on page 1, Part I, line 8, column (B).

Totals Form 990-T (2012)JSA

2E1630 1.000

PACIFIC UNIVERSITY 93-0386892

NY2934 1783 V 12-7.12 67971

Puububblic

c uded in columed in colu

ies, Royaltiies, Royalti

2.2

InInInspe

ction

In

onontioctipespnsInI

Columnmn4 divideddivided

by column 5by column

CCCopypyoppy

Cootal dede

er here andhere aPart I, line 6, colu I, line 6,

3. Deductions direeductions ddd

) Straight line depStraight li(attach state(attach s

Form 990-T (2012) Page 4Investment Income of a Section 501(c)(7), (9), or (17) Organization (see instructions)Schedule G -

3. Deductionsdirectly connected(attach statement)

5. Total deductionsand set-asides (col. 3

plus col. 4)4. Set-asides

(attach statement)1. Description of income 2. Amount of income

(1)(2)(3)(4)

Enter here and on page 1,Part I, line 9, column (A).

Enter here and on page 1,Part I, line 9, column (B).

Totals Schedule I - Exploited Exempt Activity Income, Other Than Advertising Income (see instructions)

4. Net income(loss) from

unrelated trade orbusiness (column2 minus column

3). If a gain,compute cols. 5

through 7.

3. Expensesdirectly

connected withproduction of

unrelatedbusiness income

7. Excess exemptexpenses

(column 6 minuscolumn 5, but not

more thancolumn 4).

2. Grossunrelated

business incomefrom trade or

business

5. Gross incomefrom activity thatis not unrelatedbusiness income

6. Expensesattributable to

column 51. Description of exploited activity

(1)(2)(3)(4)

Enter here and onpage 1, Part I,

line 10, col. (A).

Enter here and onpage 1, Part I,

line 10, col. (B).

Enter here andon page 1,

Part II, line 26.

Totals Schedule J - Advertising Income (see instructions)

Income From Periodicals Reported on a Consolidated BasisPart I

4. Advertisinggain or (loss) (col.2 minus col. 3). Ifa gain, compute

cols. 5 through 7.

7. Excess readershipcosts (column 6

minus column 5, butnot more than

column 4).

2. Grossadvertising

income3. Direct

advertising costs5. Circulation

income6. Readership

costs1. Name of periodical

(1)(2)(3)(4)

Totals (carry to Part II, line (5)) Income From Periodicals Reported on a Separate Basis (For each periodical listed in Part II, fill in columns 2Part II through 7 on a line-by-line basis.)

7. Excess readershipcosts (column 6

minus column 5, butnot more than

column 4).

4. Advertisinggain or (loss) (col.2 minus col. 3). Ifa gain, compute

cols. 5 through 7.

2. Grossadvertising

income3. Direct

advertising costs5. Circulation

income6. Readership

costs1. Name of periodical

(1)(2)(3)(4)Totals from Part I

Enter here and onpage 1, Part I,

line 11, col. (A).

Enter here and onpage 1, Part I

line 11, col. (B).

Enter here andon page 1,

Part II, line 27.

Totals, Part II (lines 1-5) Schedule K - Compensation of Officers, Directors, and Trustees (see instructions)

3. Percent oftime devoted to

business4. Compensation attributable to

unrelated business1. Name 2. Title

(1) %(2) %(3) %(4) %

Total. Enter here and on page 1, Part II, line 14 Form 990-T (2012)JSA

2E1640 1.000

PACIFIC UNIVERSITY 93-0386892

ATCH 4 3,488. 3,488.

3,488.

NY2934 1783 V 12-7.12 67971

Public

iciblbleported onported on

e basis.)basis.)

2. 2 GrossGrossadvertisinadvertisin

incom

Inspe

ctpeepspnsp

ction

nn

In

s

vertisingvertisingor (loss) (col.or (loss) (col.

minus col. 3). Ifnus col. 3)a gain, computegain, comp

cols. 5 throughcols. 5 thr

Copy

Copyypy

CCpy

0.

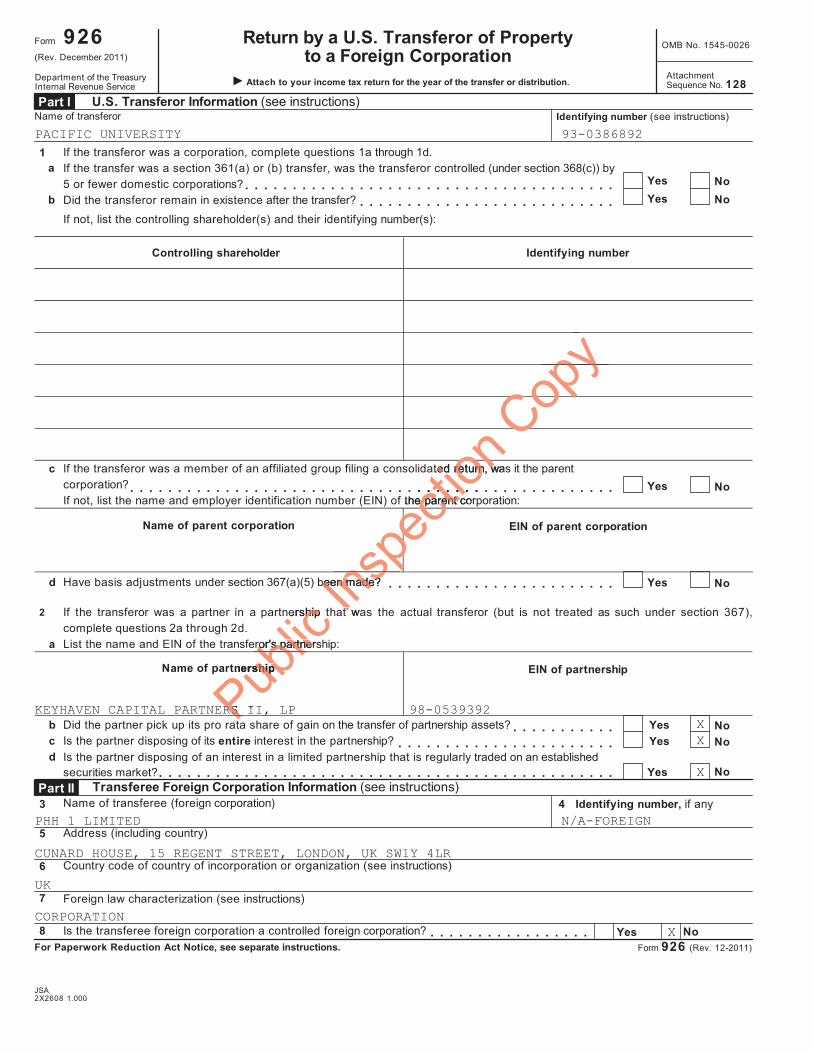

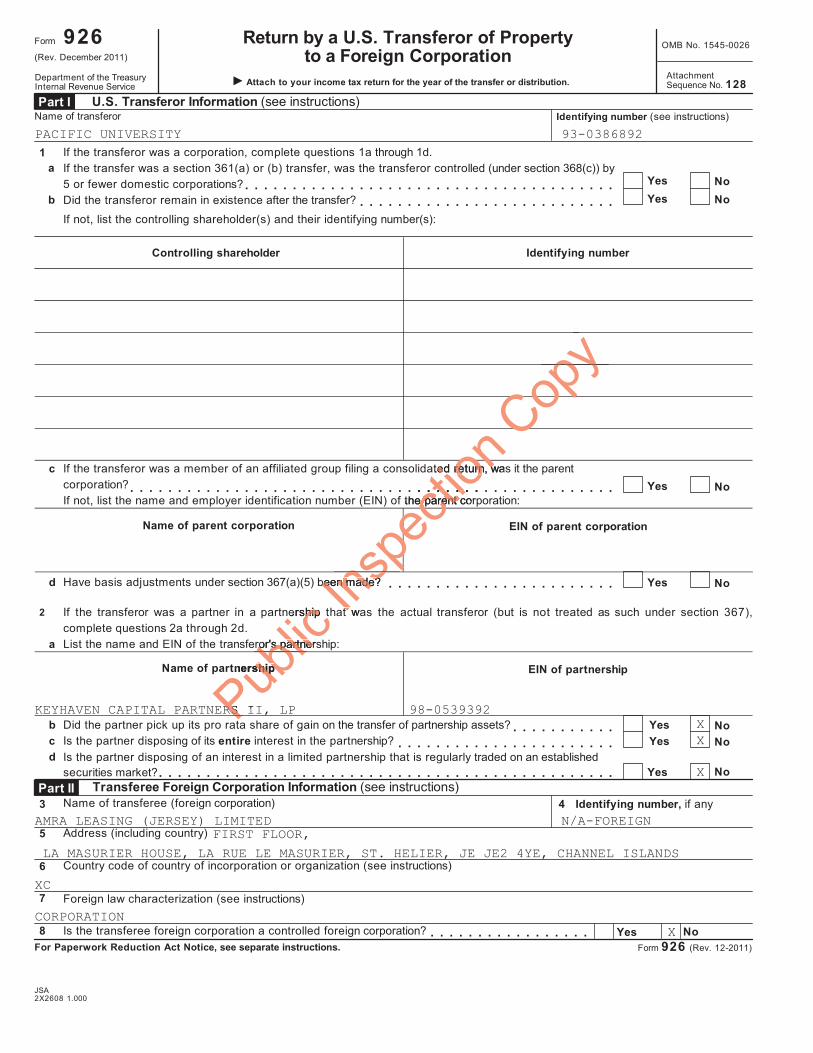

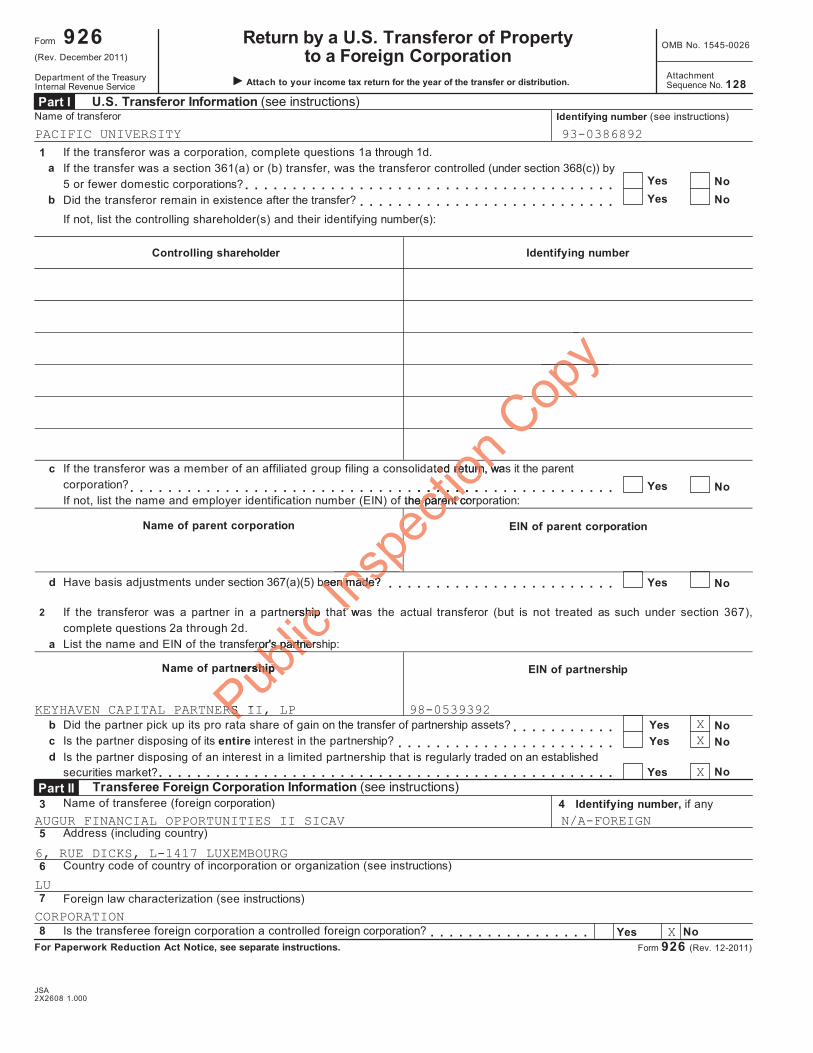

Return by a U.S. Transferor of Propertyto a Foreign Corporation

926Form OMB No. 1545-0026(Rev. December 2011)

AttachmentSequence No. 128Department of the Treasury

Internal Revenue Service Attach to your income tax return for the year of the transfer or distribution.

U.S. Transferor Information (see instructions) Part I Name of transferor Identifying number (see instructions)

If the transferor was a corporation, complete questions 1a through 1d.If the transfer was a section 361(a) or (b) transfer, was the transferor controlled (under section 368(c)) by5 or fewer domestic corporations?Did the transferor remain in existence after the transfer?

1a

bYes No Yes No

If not, list the controlling shareholder(s) and their identifying number(s):

Controlling shareholder Identifying number

c If the transferor was a member of an affiliated group filing a consolidated return, was it the parentcorporation?If not, list the name and employer identification number (EIN) of the parent corporation:

Yes No

Name of parent corporation EIN of parent corporation

d Have basis adjustments under section 367(a)(5) been made? Yes No If the transferor was a partner in a partnership that was the actual transferor (but is not treated as such under section 367),complete questions 2a through 2d.

2

a List the name and EIN of the transferor's partnership:

Name of partnership EIN of partnership

bcd

Did the partner pick up its pro rata share of gain on the transfer of partnership assets?Is the partner disposing of its entire interest in the partnership?

Yes No Yes No

Is the partner disposing of an interest in a limited partnership that is regularly traded on an establishedsecurities market? NoYes

Transferee Foreign Corporation Information (see instructions) Part II 3 4 Identifying number, if anyName of transferee (foreign corporation)

5 Address (including country)

6 Country code of country of incorporation or organization (see instructions)

7 Foreign law characterization (see instructions)

8 Is the transferee foreign corporation a controlled foreign corporation? NoYes For Paperwork Reduction Act Notice, see separate instructions. Form 926 (Rev. 12-2011)

JSA2X2608 1.000

PACIFIC UNIVERSITY 93-0386892

KEYHAVEN CAPITAL PARTNERS II, LP 98-0539392XX

X

BAYV INVESTMENTS LIMITED N/A-FOREIGN

KINGSWAY BUILDINGS, BRIDGEND INDUSTRIAL ESTATE, BRIDGEND, UK CF31 3RY

UK

CORPORATIONX

PPPublblblic ership tship t

ror's partnersror's partner

tnershipership

RS IRS

Inspe

ction

on

ecns

peated return, wased return, w

f the parent core parent

been made?been made?

t wat

Copypy

CopC

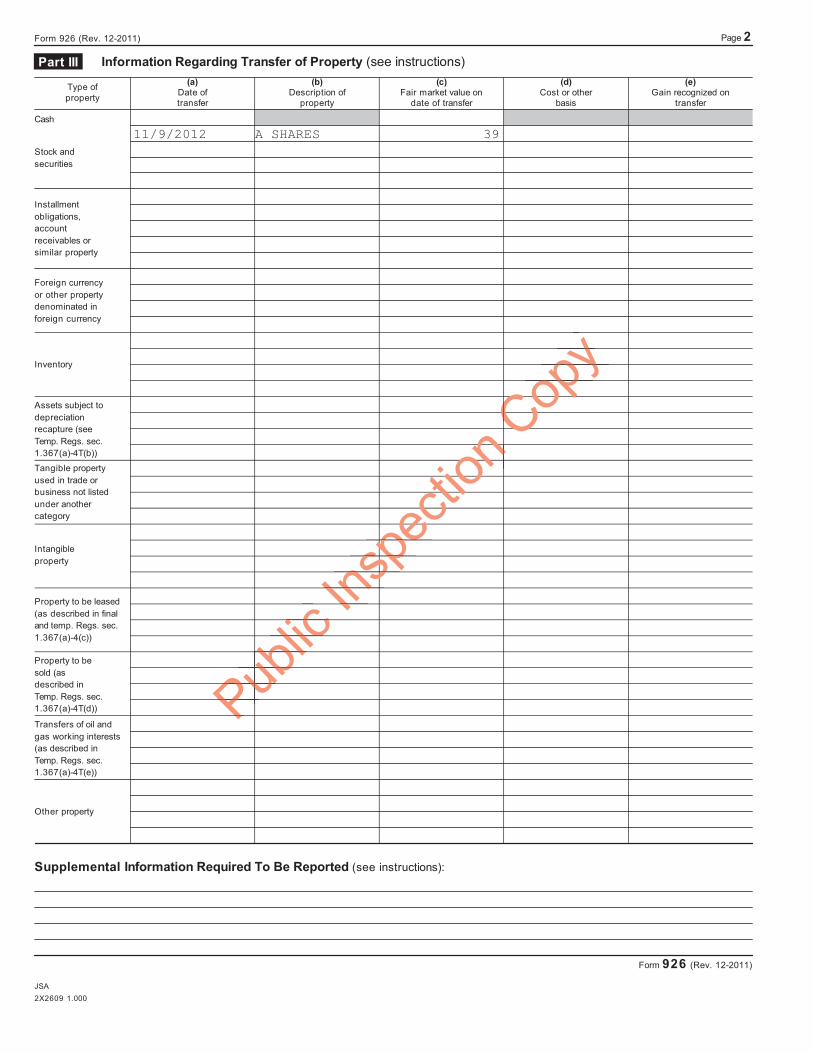

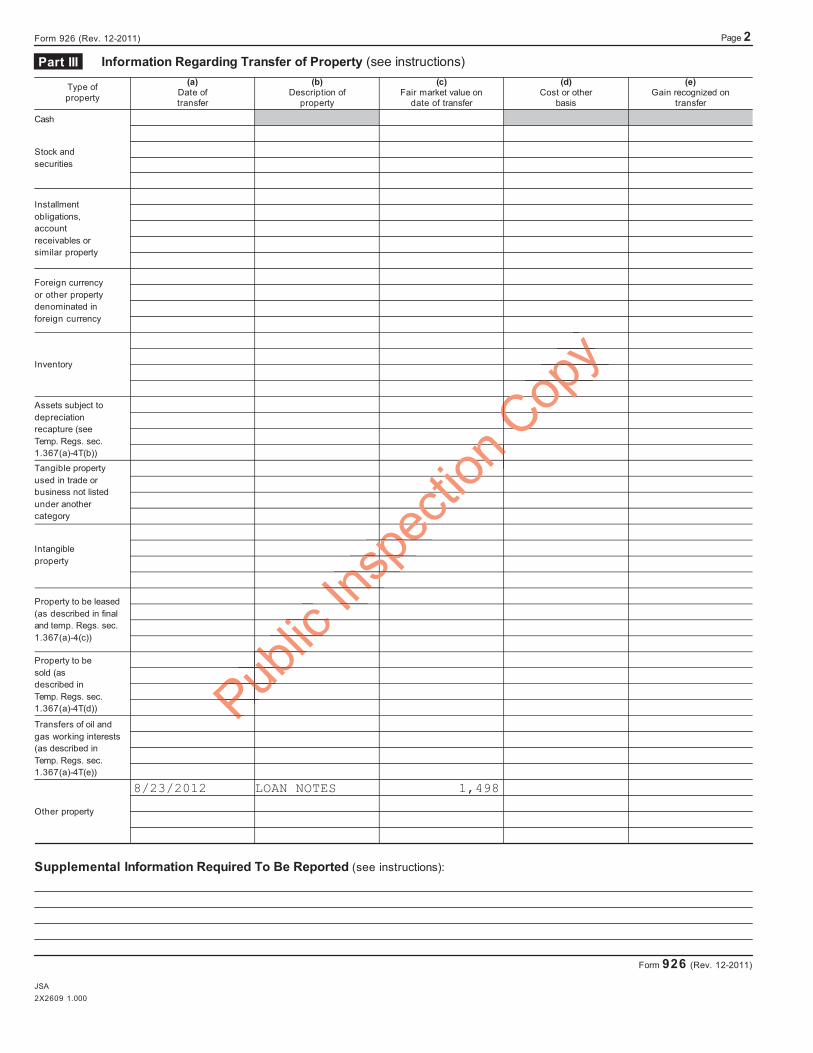

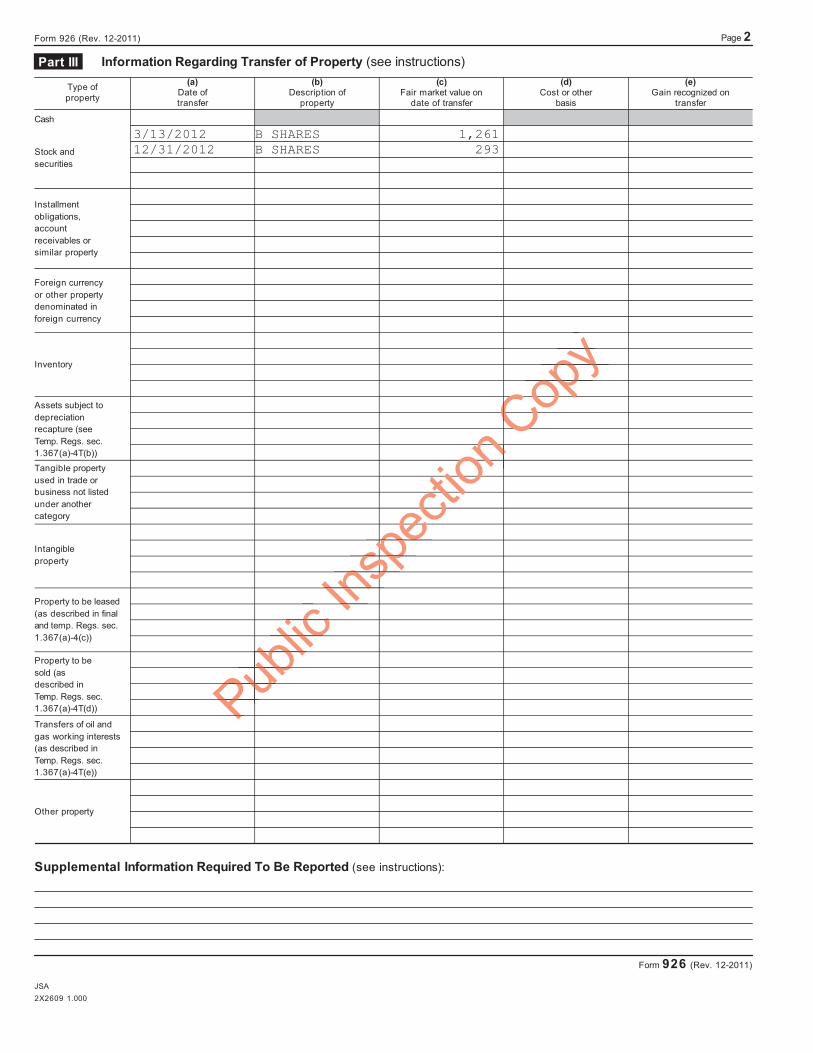

Page 2Form 926 (Rev. 12-2011)

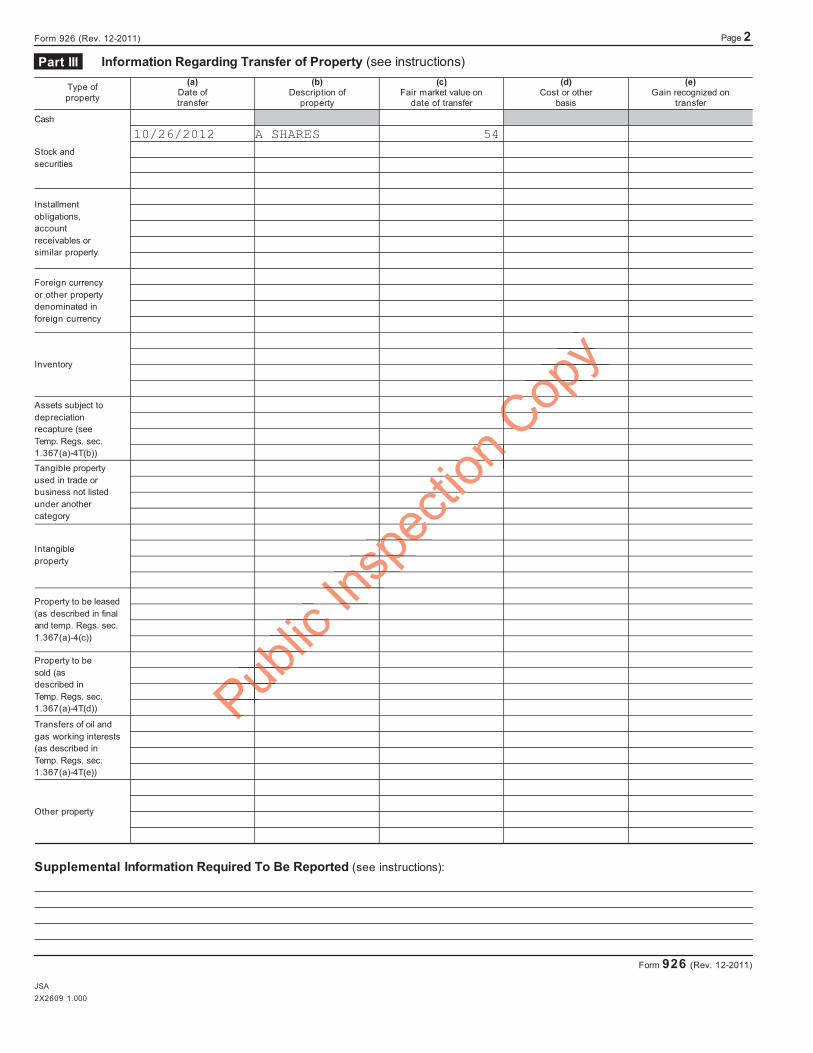

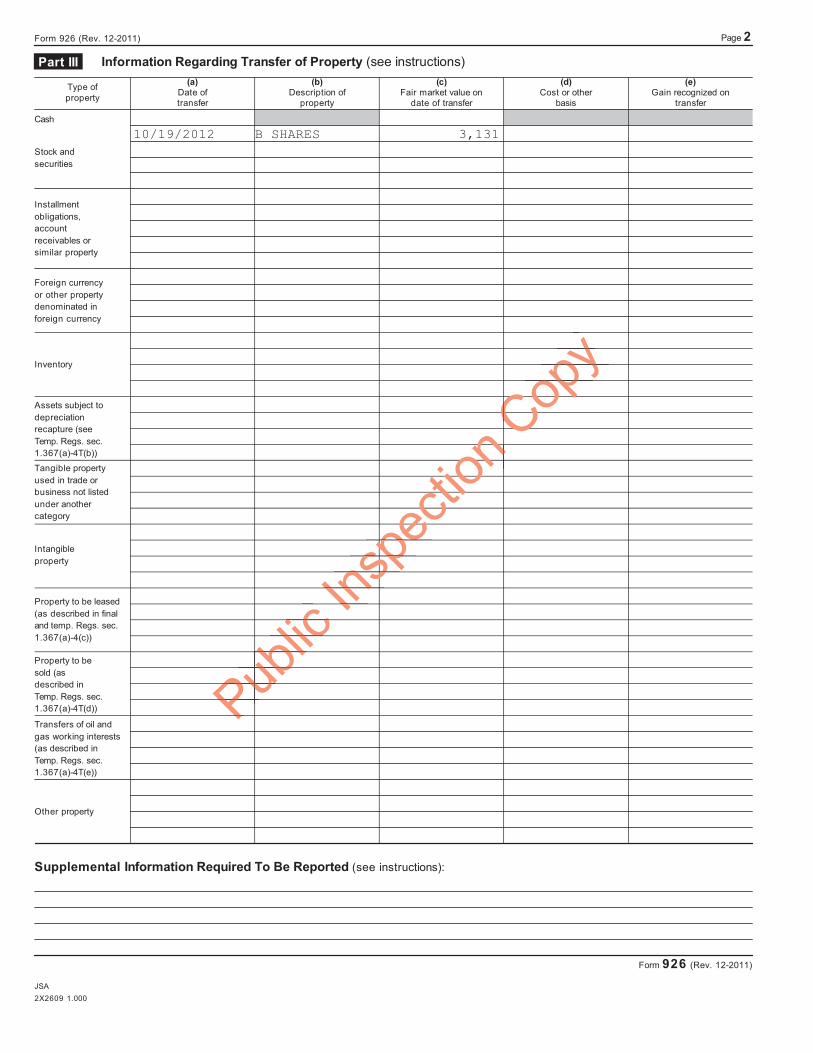

Information Regarding Transfer of Property (see instructions) Part III

Type ofproperty

(a)Date oftransfer

(b)Description of

property

(c)Fair market value on

date of transfer

(d)Cost or other

basis

(e)Gain recognized on

transfer

Cash

Stock andsecurities

Installmentobligations,accountreceivables orsimilar property

Foreign currencyor other propertydenominated inforeign currency

Inventory

Assets subject todepreciationrecapture (seeTemp. Regs. sec.1.367(a)-4T(b))

Tangible propertyused in trade orbusiness not listedunder anothercategory

Intangibleproperty

Property to be leased (as described in final and temp. Regs. sec.1.367(a)-4(c))

Property to besold (asdescribed inTemp. Regs. sec.1.367(a)-4T(d))

Transfers of oil andgas working interests(as described inTemp. Regs. sec.1.367(a)-4T(e))

Other property

Supplemental Information Required To Be Reported (see instructions):

Form 926 (Rev. 12-2011)

JSA2X2609 1.000

10/26/2012 A SHARES 54

Public

icblic

blubPuPPuP

Inspe

ction

nontioctiececpespnsInI

n

sp

CopyypyopCopCoCC

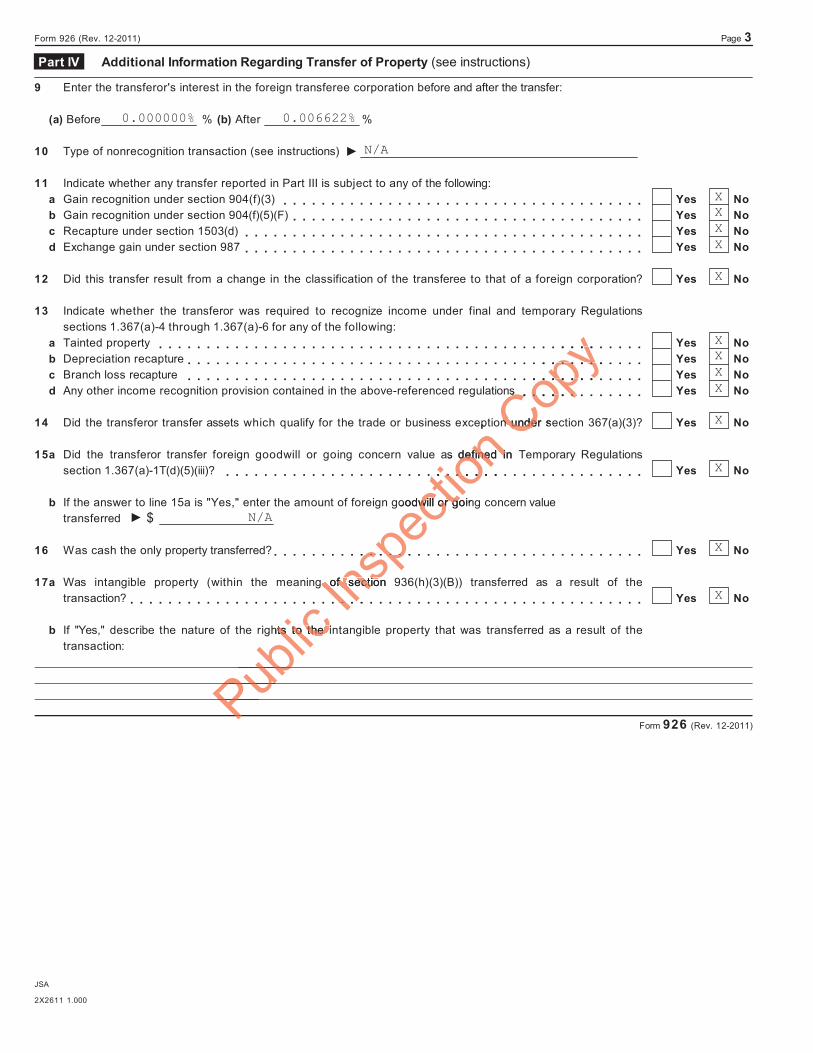

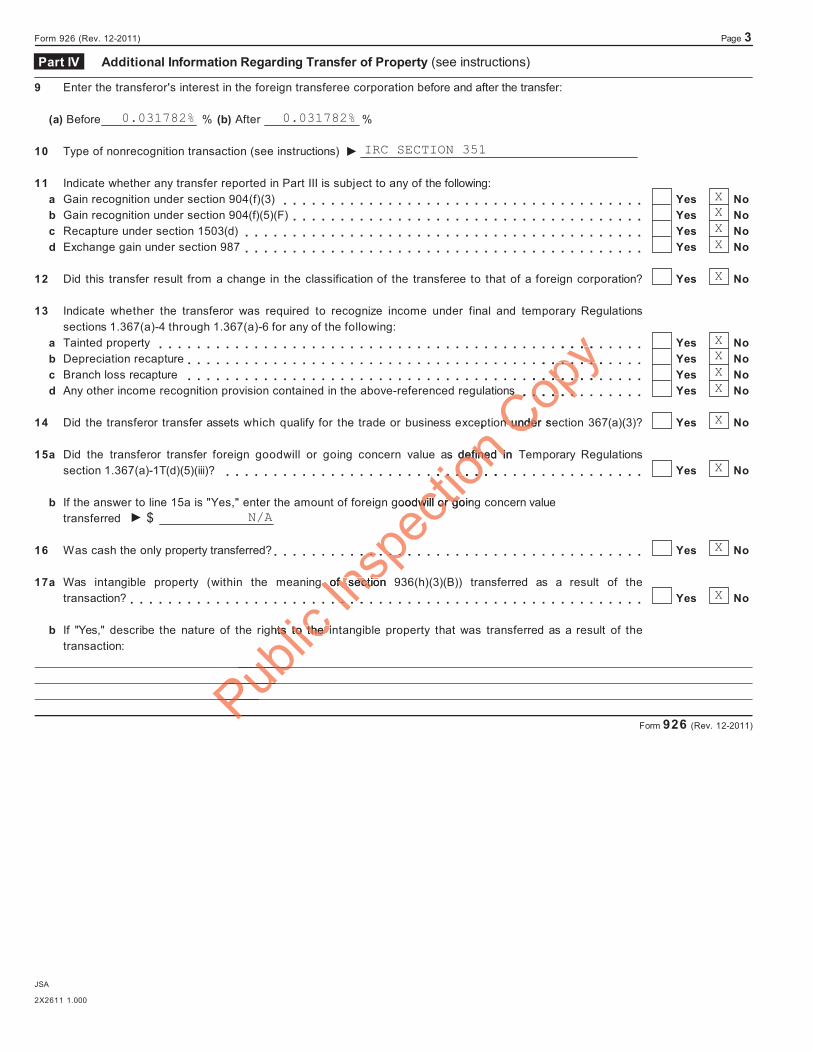

Form 926 (Rev. 12-2011) Page 3

Additional Information Regarding Transfer of Property (see instructions) Part IV

9

10

11

12

13

14

15

16

17

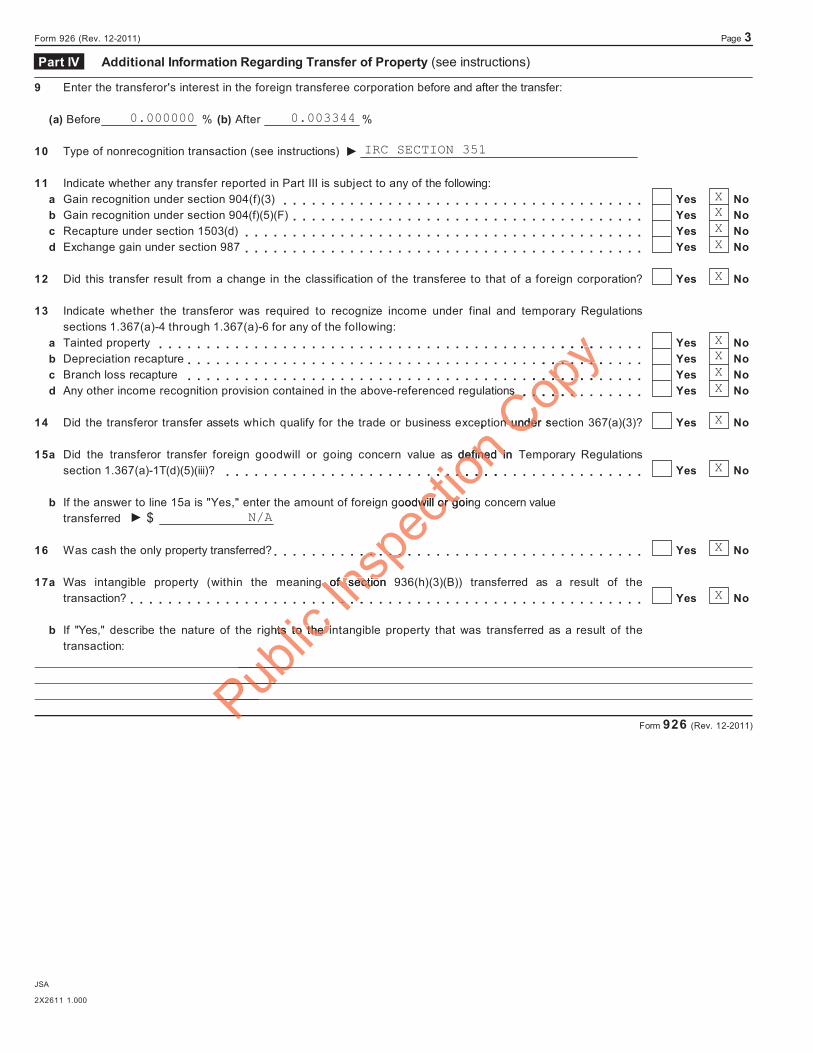

Enter the transferor's interest in the foreign transferee corporation before and after the transfer:

(a) Before % (b) After %

Type of nonrecognition transaction (see instructions)

Indicate whether any transfer reported in Part III is subject to any of the following:Gain recognition under section 904(f)(3)Gain recognition under section 904(f)(5)(F)Recapture under section 1503(d)Exchange gain under section 987

abcd

abcd

a

b

a

b

Yes No Yes No Yes No Yes No

Did this transfer result from a change in the classification of the transferee to that of a foreign corporation? Yes No

Indicate whether the transferor was required to recognize income under final and temporary Regulationssections 1.367(a)-4 through 1.367(a)-6 for any of the following:Tainted propertyDepreciation recaptureBranch loss recaptureAny other income recognition provision contained in the above-referenced regulations

Yes No Yes No Yes No Yes No

Did the transferor transfer assets which qualify for the trade or business exception under section 367(a)(3)? Yes No

Did the transferor transfer foreign goodwill or going concern value as defined in Temporary Regulationssection 1.367(a)-1T(d)(5)(iii)? Yes No If the answer to line 15a is "Yes," enter the amount of foreign goodwill or going concern valuetransferred

Was cash the only property transferred?

$

Yes No Was intangible property (within the meaning of section 936(h)(3)(B)) transferred as a result of thetransaction? Yes No If "Yes," describe the nature of the rights to the intangible property that was transferred as a result of thetransaction:

Form 926 (Rev. 12-2011)

JSA

2X2611 1.000

0.000000 0.003344

IRC SECTION 351

XXXX

X

XXXX

X

X

N/A

X

X

Public

PPPuubic

hts to the ints to the

Inspe

ction

ept

as defined in defined i

oodwill or goinwill or go

of section of sectio

Copy

nss

n under sen unde

Return by a U.S. Transferor of Propertyto a Foreign Corporation

926Form OMB No. 1545-0026(Rev. December 2011)

AttachmentSequence No. 128Department of the Treasury

Internal Revenue Service Attach to your income tax return for the year of the transfer or distribution.

U.S. Transferor Information (see instructions) Part I Name of transferor Identifying number (see instructions)

If the transferor was a corporation, complete questions 1a through 1d.If the transfer was a section 361(a) or (b) transfer, was the transferor controlled (under section 368(c)) by5 or fewer domestic corporations?Did the transferor remain in existence after the transfer?

1a

bYes No Yes No

If not, list the controlling shareholder(s) and their identifying number(s):

Controlling shareholder Identifying number

c If the transferor was a member of an affiliated group filing a consolidated return, was it the parentcorporation?If not, list the name and employer identification number (EIN) of the parent corporation:

Yes No

Name of parent corporation EIN of parent corporation

d Have basis adjustments under section 367(a)(5) been made? Yes No If the transferor was a partner in a partnership that was the actual transferor (but is not treated as such under section 367),complete questions 2a through 2d.

2

a List the name and EIN of the transferor's partnership:

Name of partnership EIN of partnership

bcd

Did the partner pick up its pro rata share of gain on the transfer of partnership assets?Is the partner disposing of its entire interest in the partnership?

Yes No Yes No

Is the partner disposing of an interest in a limited partnership that is regularly traded on an establishedsecurities market? NoYes

Transferee Foreign Corporation Information (see instructions) Part II 3 4 Identifying number, if anyName of transferee (foreign corporation)

5 Address (including country)

6 Country code of country of incorporation or organization (see instructions)

7 Foreign law characterization (see instructions)

8 Is the transferee foreign corporation a controlled foreign corporation? NoYes For Paperwork Reduction Act Notice, see separate instructions. Form 926 (Rev. 12-2011)

JSA2X2608 1.000

PACIFIC UNIVERSITY 93-0386892

KEYHAVEN CAPITAL PARTNERS II, LP 98-0539392XX

X

PHH 1 LIMITED N/A-FOREIGN

CUNARD HOUSE, 15 REGENT STREET, LONDON, UK SW1Y 4LR

UK

CORPORATIONX

PPPublblblic ership tship t

ror's partnersror's partner

tnershipership

RS IRS

Inspe

ction

on

ecns

peated return, wased return, w

f the parent core parent

been made?been made?

t wat

Copypy

CopC

Page 2Form 926 (Rev. 12-2011)

Information Regarding Transfer of Property (see instructions) Part III

Type ofproperty

(a)Date oftransfer

(b)Description of

property

(c)Fair market value on

date of transfer

(d)Cost or other

basis

(e)Gain recognized on

transfer

Cash

Stock andsecurities

Installmentobligations,accountreceivables orsimilar property

Foreign currencyor other propertydenominated inforeign currency

Inventory

Assets subject todepreciationrecapture (seeTemp. Regs. sec.1.367(a)-4T(b))

Tangible propertyused in trade orbusiness not listedunder anothercategory

Intangibleproperty

Property to be leased (as described in final and temp. Regs. sec.1.367(a)-4(c))

Property to besold (asdescribed inTemp. Regs. sec.1.367(a)-4T(d))

Transfers of oil andgas working interests(as described inTemp. Regs. sec.1.367(a)-4T(e))

Other property

Supplemental Information Required To Be Reported (see instructions):

Form 926 (Rev. 12-2011)

JSA2X2609 1.000

11/9/2012 A SHARES 39

Public

icblic

blubPuPPuP

Inspe

ction

nontioctiececpespnsInI

n

sp

CopyypyopCopCoCC

Form 926 (Rev. 12-2011) Page 3

Additional Information Regarding Transfer of Property (see instructions) Part IV

9

10

11

12

13

14

15

16

17

Enter the transferor's interest in the foreign transferee corporation before and after the transfer:

(a) Before % (b) After %

Type of nonrecognition transaction (see instructions)

Indicate whether any transfer reported in Part III is subject to any of the following:Gain recognition under section 904(f)(3)Gain recognition under section 904(f)(5)(F)Recapture under section 1503(d)Exchange gain under section 987

abcd

abcd

a

b

a

b

Yes No Yes No Yes No Yes No

Did this transfer result from a change in the classification of the transferee to that of a foreign corporation? Yes No

Indicate whether the transferor was required to recognize income under final and temporary Regulationssections 1.367(a)-4 through 1.367(a)-6 for any of the following:Tainted propertyDepreciation recaptureBranch loss recaptureAny other income recognition provision contained in the above-referenced regulations

Yes No Yes No Yes No Yes No

Did the transferor transfer assets which qualify for the trade or business exception under section 367(a)(3)? Yes No

Did the transferor transfer foreign goodwill or going concern value as defined in Temporary Regulationssection 1.367(a)-1T(d)(5)(iii)? Yes No If the answer to line 15a is "Yes," enter the amount of foreign goodwill or going concern valuetransferred

Was cash the only property transferred?

$

Yes No Was intangible property (within the meaning of section 936(h)(3)(B)) transferred as a result of thetransaction? Yes No If "Yes," describe the nature of the rights to the intangible property that was transferred as a result of thetransaction:

Form 926 (Rev. 12-2011)

JSA

2X2611 1.000

0.000000% 0.003211%

IRC SECTION 351

XXXX

X

XXXX

X

X

N/A

X

X

Public

PPPuubic

hts to the ints to the

Inspe

ction

ept

as defined in defined i

oodwill or goinwill or go

of section of sectio

Copy

nss

n under sen unde

Return by a U.S. Transferor of Propertyto a Foreign Corporation

926Form OMB No. 1545-0026(Rev. December 2011)

AttachmentSequence No. 128Department of the Treasury

Internal Revenue Service Attach to your income tax return for the year of the transfer or distribution.

U.S. Transferor Information (see instructions) Part I Name of transferor Identifying number (see instructions)

If the transferor was a corporation, complete questions 1a through 1d.If the transfer was a section 361(a) or (b) transfer, was the transferor controlled (under section 368(c)) by5 or fewer domestic corporations?Did the transferor remain in existence after the transfer?

1a

bYes No Yes No

If not, list the controlling shareholder(s) and their identifying number(s):

Controlling shareholder Identifying number

c If the transferor was a member of an affiliated group filing a consolidated return, was it the parentcorporation?If not, list the name and employer identification number (EIN) of the parent corporation:

Yes No

Name of parent corporation EIN of parent corporation

d Have basis adjustments under section 367(a)(5) been made? Yes No If the transferor was a partner in a partnership that was the actual transferor (but is not treated as such under section 367),complete questions 2a through 2d.

2

a List the name and EIN of the transferor's partnership:

Name of partnership EIN of partnership

bcd

Did the partner pick up its pro rata share of gain on the transfer of partnership assets?Is the partner disposing of its entire interest in the partnership?

Yes No Yes No

Is the partner disposing of an interest in a limited partnership that is regularly traded on an establishedsecurities market? NoYes

Transferee Foreign Corporation Information (see instructions) Part II 3 4 Identifying number, if anyName of transferee (foreign corporation)

5 Address (including country)

6 Country code of country of incorporation or organization (see instructions)

7 Foreign law characterization (see instructions)

8 Is the transferee foreign corporation a controlled foreign corporation? NoYes For Paperwork Reduction Act Notice, see separate instructions. Form 926 (Rev. 12-2011)

JSA2X2608 1.000

PACIFIC UNIVERSITY 93-0386892

KEYHAVEN CAPITAL PARTNERS II, LP 98-0539392XX

X

AMRA LEASING (JERSEY) LIMITED N/A-FOREIGN

LA MASURIER HOUSE, LA RUE LE MASURIER, ST. HELIER, JE JE2 4YE, CHANNEL ISLANDS

XC

CORPORATIONX

FIRST FLOOR,

PPPublblblic ership tship t

ror's partnersror's partner

tnershipership

RS IRS

Inspe

ction

on

ecns

peated return, wased return, w

f the parent core parent

been made?been made?

t wat

Copypy

CopC

Page 2Form 926 (Rev. 12-2011)

Information Regarding Transfer of Property (see instructions) Part III

Type ofproperty

(a)Date oftransfer

(b)Description of

property

(c)Fair market value on

date of transfer

(d)Cost or other

basis

(e)Gain recognized on

transfer

Cash

Stock andsecurities

Installmentobligations,accountreceivables orsimilar property

Foreign currencyor other propertydenominated inforeign currency

Inventory

Assets subject todepreciationrecapture (seeTemp. Regs. sec.1.367(a)-4T(b))

Tangible propertyused in trade orbusiness not listedunder anothercategory

Intangibleproperty

Property to be leased (as described in final and temp. Regs. sec.1.367(a)-4(c))

Property to besold (asdescribed inTemp. Regs. sec.1.367(a)-4T(d))

Transfers of oil andgas working interests(as described inTemp. Regs. sec.1.367(a)-4T(e))

Other property

Supplemental Information Required To Be Reported (see instructions):

Form 926 (Rev. 12-2011)

JSA2X2609 1.000

8/23/2012 LOAN NOTES 1,498

Public

icblic

blubPuPPuP

Inspe

ction

nontioctiececpespnsInI

n

sp

CopyypyopCopCoCC

Form 926 (Rev. 12-2011) Page 3

Additional Information Regarding Transfer of Property (see instructions) Part IV

9

10

11

12

13

14

15

16

17

Enter the transferor's interest in the foreign transferee corporation before and after the transfer:

(a) Before % (b) After %

Type of nonrecognition transaction (see instructions)

Indicate whether any transfer reported in Part III is subject to any of the following:Gain recognition under section 904(f)(3)Gain recognition under section 904(f)(5)(F)Recapture under section 1503(d)Exchange gain under section 987

abcd

abcd

a

b

a

b

Yes No Yes No Yes No Yes No

Did this transfer result from a change in the classification of the transferee to that of a foreign corporation? Yes No

Indicate whether the transferor was required to recognize income under final and temporary Regulationssections 1.367(a)-4 through 1.367(a)-6 for any of the following:Tainted propertyDepreciation recaptureBranch loss recaptureAny other income recognition provision contained in the above-referenced regulations

Yes No Yes No Yes No Yes No

Did the transferor transfer assets which qualify for the trade or business exception under section 367(a)(3)? Yes No

Did the transferor transfer foreign goodwill or going concern value as defined in Temporary Regulationssection 1.367(a)-1T(d)(5)(iii)? Yes No If the answer to line 15a is "Yes," enter the amount of foreign goodwill or going concern valuetransferred

Was cash the only property transferred?

$

Yes No Was intangible property (within the meaning of section 936(h)(3)(B)) transferred as a result of thetransaction? Yes No If "Yes," describe the nature of the rights to the intangible property that was transferred as a result of thetransaction:

Form 926 (Rev. 12-2011)

JSA

2X2611 1.000

0.000000% 0.006622%

N/A

XXXX

X

XXXX

X

X

N/A

X

X

Public

PPPuubic

hts to the ints to the

Inspe

ction

ept

as defined in defined i

oodwill or goinwill or go

of section of sectio

Copy

nss

n under sen unde

Return by a U.S. Transferor of Propertyto a Foreign Corporation

926Form OMB No. 1545-0026(Rev. December 2011)

AttachmentSequence No. 128Department of the Treasury

Internal Revenue Service Attach to your income tax return for the year of the transfer or distribution.

U.S. Transferor Information (see instructions) Part I Name of transferor Identifying number (see instructions)

If the transferor was a corporation, complete questions 1a through 1d.If the transfer was a section 361(a) or (b) transfer, was the transferor controlled (under section 368(c)) by5 or fewer domestic corporations?Did the transferor remain in existence after the transfer?

1a

bYes No Yes No

If not, list the controlling shareholder(s) and their identifying number(s):

Controlling shareholder Identifying number

c If the transferor was a member of an affiliated group filing a consolidated return, was it the parentcorporation?If not, list the name and employer identification number (EIN) of the parent corporation:

Yes No

Name of parent corporation EIN of parent corporation

d Have basis adjustments under section 367(a)(5) been made? Yes No If the transferor was a partner in a partnership that was the actual transferor (but is not treated as such under section 367),complete questions 2a through 2d.

2

a List the name and EIN of the transferor's partnership:

Name of partnership EIN of partnership

bcd

Did the partner pick up its pro rata share of gain on the transfer of partnership assets?Is the partner disposing of its entire interest in the partnership?

Yes No Yes No

Is the partner disposing of an interest in a limited partnership that is regularly traded on an establishedsecurities market? NoYes

Transferee Foreign Corporation Information (see instructions) Part II 3 4 Identifying number, if anyName of transferee (foreign corporation)

5 Address (including country)

6 Country code of country of incorporation or organization (see instructions)

7 Foreign law characterization (see instructions)

8 Is the transferee foreign corporation a controlled foreign corporation? NoYes For Paperwork Reduction Act Notice, see separate instructions. Form 926 (Rev. 12-2011)

JSA2X2608 1.000

PACIFIC UNIVERSITY 93-0386892

KEYHAVEN CAPITAL PARTNERS II, LP 98-0539392XX

X

AMRA LEASING (JERSEY) LIMITED N/A-FOREIGN

LA MASURIER HOUSE, LA RUE LE MASURIER, ST. HELIER, JE JE2 4YE, CHANNEL ISLANDS

XC

CORPORATIONX

FIRST FLOOR,

PPPublblblic ership tship t

ror's partnersror's partner

tnershipership

RS IRS

Inspe

ction

on

ecns

peated return, wased return, w

f the parent core parent

been made?been made?

t wat

Copypy

CopC

Page 2Form 926 (Rev. 12-2011)

Information Regarding Transfer of Property (see instructions) Part III

Type ofproperty

(a)Date oftransfer

(b)Description of

property

(c)Fair market value on

date of transfer

(d)Cost or other

basis

(e)Gain recognized on

transfer

Cash

Stock andsecurities

Installmentobligations,accountreceivables orsimilar property

Foreign currencyor other propertydenominated inforeign currency

Inventory

Assets subject todepreciationrecapture (seeTemp. Regs. sec.1.367(a)-4T(b))

Tangible propertyused in trade orbusiness not listedunder anothercategory

Intangibleproperty

Property to be leased (as described in final and temp. Regs. sec.1.367(a)-4(c))

Property to besold (asdescribed inTemp. Regs. sec.1.367(a)-4T(d))

Transfers of oil andgas working interests(as described inTemp. Regs. sec.1.367(a)-4T(e))

Other property

Supplemental Information Required To Be Reported (see instructions):

Form 926 (Rev. 12-2011)

JSA2X2609 1.000

8/23/2012 A SHARES 7

Public

icblic

blubPuPPuP

Inspe

ction

nontioctiececpespnsInI

n

sp

CopyypyopCopCoCC

Form 926 (Rev. 12-2011) Page 3

Additional Information Regarding Transfer of Property (see instructions) Part IV

9

10

11

12

13

14

15

16

17

Enter the transferor's interest in the foreign transferee corporation before and after the transfer:

(a) Before % (b) After %

Type of nonrecognition transaction (see instructions)

Indicate whether any transfer reported in Part III is subject to any of the following:Gain recognition under section 904(f)(3)Gain recognition under section 904(f)(5)(F)Recapture under section 1503(d)Exchange gain under section 987

abcd

abcd

a

b

a

b

Yes No Yes No Yes No Yes No

Did this transfer result from a change in the classification of the transferee to that of a foreign corporation? Yes No

Indicate whether the transferor was required to recognize income under final and temporary Regulationssections 1.367(a)-4 through 1.367(a)-6 for any of the following:Tainted propertyDepreciation recaptureBranch loss recaptureAny other income recognition provision contained in the above-referenced regulations

Yes No Yes No Yes No Yes No

Did the transferor transfer assets which qualify for the trade or business exception under section 367(a)(3)? Yes No

Did the transferor transfer foreign goodwill or going concern value as defined in Temporary Regulationssection 1.367(a)-1T(d)(5)(iii)? Yes No If the answer to line 15a is "Yes," enter the amount of foreign goodwill or going concern valuetransferred

Was cash the only property transferred?

$

Yes No Was intangible property (within the meaning of section 936(h)(3)(B)) transferred as a result of thetransaction? Yes No If "Yes," describe the nature of the rights to the intangible property that was transferred as a result of thetransaction:

Form 926 (Rev. 12-2011)

JSA

2X2611 1.000

0.000000% 0.006622%

IRC SECTION 351

XXXX

X

XXXX

X

X

N/A

X

X

Public

PPPuubic

hts to the ints to the

Inspe

ction

ept

as defined in defined i

oodwill or goinwill or go

of section of sectio

Copy

nss

n under sen unde

Return by a U.S. Transferor of Propertyto a Foreign Corporation

926Form OMB No. 1545-0026(Rev. December 2011)

AttachmentSequence No. 128Department of the Treasury

Internal Revenue Service Attach to your income tax return for the year of the transfer or distribution.

U.S. Transferor Information (see instructions) Part I Name of transferor Identifying number (see instructions)

If the transferor was a corporation, complete questions 1a through 1d.If the transfer was a section 361(a) or (b) transfer, was the transferor controlled (under section 368(c)) by5 or fewer domestic corporations?Did the transferor remain in existence after the transfer?

1a

bYes No Yes No

If not, list the controlling shareholder(s) and their identifying number(s):

Controlling shareholder Identifying number

c If the transferor was a member of an affiliated group filing a consolidated return, was it the parentcorporation?If not, list the name and employer identification number (EIN) of the parent corporation:

Yes No

Name of parent corporation EIN of parent corporation

d Have basis adjustments under section 367(a)(5) been made? Yes No If the transferor was a partner in a partnership that was the actual transferor (but is not treated as such under section 367),complete questions 2a through 2d.

2

a List the name and EIN of the transferor's partnership:

Name of partnership EIN of partnership

bcd

Did the partner pick up its pro rata share of gain on the transfer of partnership assets?Is the partner disposing of its entire interest in the partnership?

Yes No Yes No

Is the partner disposing of an interest in a limited partnership that is regularly traded on an establishedsecurities market? NoYes

Transferee Foreign Corporation Information (see instructions) Part II 3 4 Identifying number, if anyName of transferee (foreign corporation)

5 Address (including country)

6 Country code of country of incorporation or organization (see instructions)

7 Foreign law characterization (see instructions)

8 Is the transferee foreign corporation a controlled foreign corporation? NoYes For Paperwork Reduction Act Notice, see separate instructions. Form 926 (Rev. 12-2011)

JSA2X2608 1.000

PACIFIC UNIVERSITY 93-0386892

KEYHAVEN CAPITAL PARTNERS II, LP 98-0539392XX

X

AUGUR FINANCIAL OPPORTUNITY SICAV N/A-FOREIGN

6, RUE DICKS, L-1417 LUXEMBOURG

LU

CORPORATIONX

PPPublblblic ership tship t

ror's partnersror's partner

tnershipership

RS IRS

Inspe

ction

on

ecns

peated return, wased return, w

f the parent core parent

been made?been made?

t wat

Copypy

CopC

Page 2Form 926 (Rev. 12-2011)

Information Regarding Transfer of Property (see instructions) Part III

Type ofproperty

(a)Date oftransfer

(b)Description of

property

(c)Fair market value on

date of transfer

(d)Cost or other

basis

(e)Gain recognized on

transfer

Cash

Stock andsecurities

Installmentobligations,accountreceivables orsimilar property

Foreign currencyor other propertydenominated inforeign currency

Inventory

Assets subject todepreciationrecapture (seeTemp. Regs. sec.1.367(a)-4T(b))

Tangible propertyused in trade orbusiness not listedunder anothercategory

Intangibleproperty

Property to be leased (as described in final and temp. Regs. sec.1.367(a)-4(c))

Property to besold (asdescribed inTemp. Regs. sec.1.367(a)-4T(d))

Transfers of oil andgas working interests(as described inTemp. Regs. sec.1.367(a)-4T(e))

Other property

Supplemental Information Required To Be Reported (see instructions):

Form 926 (Rev. 12-2011)

JSA2X2609 1.000

10/19/2012 B SHARES 3,131

Public

icblic

blubPuPPuP

Inspe

ction

nontioctiececpespnsInI

n

sp

CopyypyopCopCoCC

Form 926 (Rev. 12-2011) Page 3

Additional Information Regarding Transfer of Property (see instructions) Part IV

9

10

11

12

13

14

15

16

17

Enter the transferor's interest in the foreign transferee corporation before and after the transfer:

(a) Before % (b) After %

Type of nonrecognition transaction (see instructions)

Indicate whether any transfer reported in Part III is subject to any of the following:Gain recognition under section 904(f)(3)Gain recognition under section 904(f)(5)(F)Recapture under section 1503(d)Exchange gain under section 987

abcd

abcd

a

b

a

b

Yes No Yes No Yes No Yes No

Did this transfer result from a change in the classification of the transferee to that of a foreign corporation? Yes No

Indicate whether the transferor was required to recognize income under final and temporary Regulationssections 1.367(a)-4 through 1.367(a)-6 for any of the following:Tainted propertyDepreciation recaptureBranch loss recaptureAny other income recognition provision contained in the above-referenced regulations

Yes No Yes No Yes No Yes No

Did the transferor transfer assets which qualify for the trade or business exception under section 367(a)(3)? Yes No

Did the transferor transfer foreign goodwill or going concern value as defined in Temporary Regulationssection 1.367(a)-1T(d)(5)(iii)? Yes No If the answer to line 15a is "Yes," enter the amount of foreign goodwill or going concern valuetransferred

Was cash the only property transferred?

$

Yes No Was intangible property (within the meaning of section 936(h)(3)(B)) transferred as a result of thetransaction? Yes No If "Yes," describe the nature of the rights to the intangible property that was transferred as a result of thetransaction:

Form 926 (Rev. 12-2011)

JSA

2X2611 1.000

0.031782% 0.031782%

IRC SECTION 351

XXXX

X

XXXX

X

X

N/A

X

X

Public

PPPuubic

hts to the ints to the

Inspe

ction

ept

as defined in defined i

oodwill or goinwill or go

of section of sectio

Copy

nss

n under sen unde

Return by a U.S. Transferor of Propertyto a Foreign Corporation

926Form OMB No. 1545-0026(Rev. December 2011)

AttachmentSequence No. 128Department of the Treasury

Internal Revenue Service Attach to your income tax return for the year of the transfer or distribution.

U.S. Transferor Information (see instructions) Part I Name of transferor Identifying number (see instructions)

If the transferor was a corporation, complete questions 1a through 1d.If the transfer was a section 361(a) or (b) transfer, was the transferor controlled (under section 368(c)) by5 or fewer domestic corporations?Did the transferor remain in existence after the transfer?

1a

bYes No Yes No

If not, list the controlling shareholder(s) and their identifying number(s):

Controlling shareholder Identifying number

c If the transferor was a member of an affiliated group filing a consolidated return, was it the parentcorporation?If not, list the name and employer identification number (EIN) of the parent corporation:

Yes No

Name of parent corporation EIN of parent corporation

d Have basis adjustments under section 367(a)(5) been made? Yes No If the transferor was a partner in a partnership that was the actual transferor (but is not treated as such under section 367),complete questions 2a through 2d.

2

a List the name and EIN of the transferor's partnership:

Name of partnership EIN of partnership

bcd

Did the partner pick up its pro rata share of gain on the transfer of partnership assets?Is the partner disposing of its entire interest in the partnership?

Yes No Yes No

Is the partner disposing of an interest in a limited partnership that is regularly traded on an establishedsecurities market? NoYes

Transferee Foreign Corporation Information (see instructions) Part II 3 4 Identifying number, if anyName of transferee (foreign corporation)

5 Address (including country)

6 Country code of country of incorporation or organization (see instructions)

7 Foreign law characterization (see instructions)

8 Is the transferee foreign corporation a controlled foreign corporation? NoYes For Paperwork Reduction Act Notice, see separate instructions. Form 926 (Rev. 12-2011)

JSA2X2608 1.000

PACIFIC UNIVERSITY 93-0386892

KEYHAVEN CAPITAL PARTNERS II, LP 98-0539392XX

X

AUGUR FINANCIAL OPPORTUNITIES II SICAV N/A-FOREIGN

6, RUE DICKS, L-1417 LUXEMBOURG

LU

CORPORATIONX

PPPublblblic ership tship t

ror's partnersror's partner

tnershipership

RS IRS

Inspe

ction

on

ecns

peated return, wased return, w

f the parent core parent

been made?been made?

t wat

Copypy

CopC

Page 2Form 926 (Rev. 12-2011)

Information Regarding Transfer of Property (see instructions) Part III

Type ofproperty

(a)Date oftransfer

(b)Description of

property

(c)Fair market value on

date of transfer

(d)Cost or other

basis

(e)Gain recognized on

transfer

Cash

Stock andsecurities

Installmentobligations,accountreceivables orsimilar property

Foreign currencyor other propertydenominated inforeign currency

Inventory

Assets subject todepreciationrecapture (seeTemp. Regs. sec.1.367(a)-4T(b))

Tangible propertyused in trade orbusiness not listedunder anothercategory

Intangibleproperty

Property to be leased (as described in final and temp. Regs. sec.1.367(a)-4(c))

Property to besold (asdescribed inTemp. Regs. sec.1.367(a)-4T(d))

Transfers of oil andgas working interests(as described inTemp. Regs. sec.1.367(a)-4T(e))

Other property

Supplemental Information Required To Be Reported (see instructions):

Form 926 (Rev. 12-2011)

JSA2X2609 1.000

3/13/2012 B SHARES 1,26112/31/2012 B SHARES 293

Public

icblic

blubPuPPuP

Inspe

ction

nontioctiececpespnsInI

n

sp

CopyypyopCopCoCC

Form 926 (Rev. 12-2011) Page 3

Additional Information Regarding Transfer of Property (see instructions) Part IV

9

10

11

12

13

14

15

16

17

Enter the transferor's interest in the foreign transferee corporation before and after the transfer:

(a) Before % (b) After %

Type of nonrecognition transaction (see instructions)

Indicate whether any transfer reported in Part III is subject to any of the following:Gain recognition under section 904(f)(3)Gain recognition under section 904(f)(5)(F)Recapture under section 1503(d)Exchange gain under section 987

abcd

abcd

a

b

a

b

Yes No Yes No Yes No Yes No

Did this transfer result from a change in the classification of the transferee to that of a foreign corporation? Yes No

Indicate whether the transferor was required to recognize income under final and temporary Regulationssections 1.367(a)-4 through 1.367(a)-6 for any of the following:Tainted propertyDepreciation recaptureBranch loss recaptureAny other income recognition provision contained in the above-referenced regulations

Yes No Yes No Yes No Yes No

Did the transferor transfer assets which qualify for the trade or business exception under section 367(a)(3)? Yes No

Did the transferor transfer foreign goodwill or going concern value as defined in Temporary Regulationssection 1.367(a)-1T(d)(5)(iii)? Yes No If the answer to line 15a is "Yes," enter the amount of foreign goodwill or going concern valuetransferred

Was cash the only property transferred?

$

Yes No Was intangible property (within the meaning of section 936(h)(3)(B)) transferred as a result of thetransaction? Yes No If "Yes," describe the nature of the rights to the intangible property that was transferred as a result of thetransaction:

Form 926 (Rev. 12-2011)

JSA

2X2611 1.000

0.006974% 0.006974%

IRC SECTION 351

XXXX

X

XXXX

X

X

N/A

X

X

Public

PPPuubic

hts to the ints to the

Inspe

ction

ept

as defined in defined i

oodwill or goinwill or go

of section of sectio

Copy

nss

n under sen unde

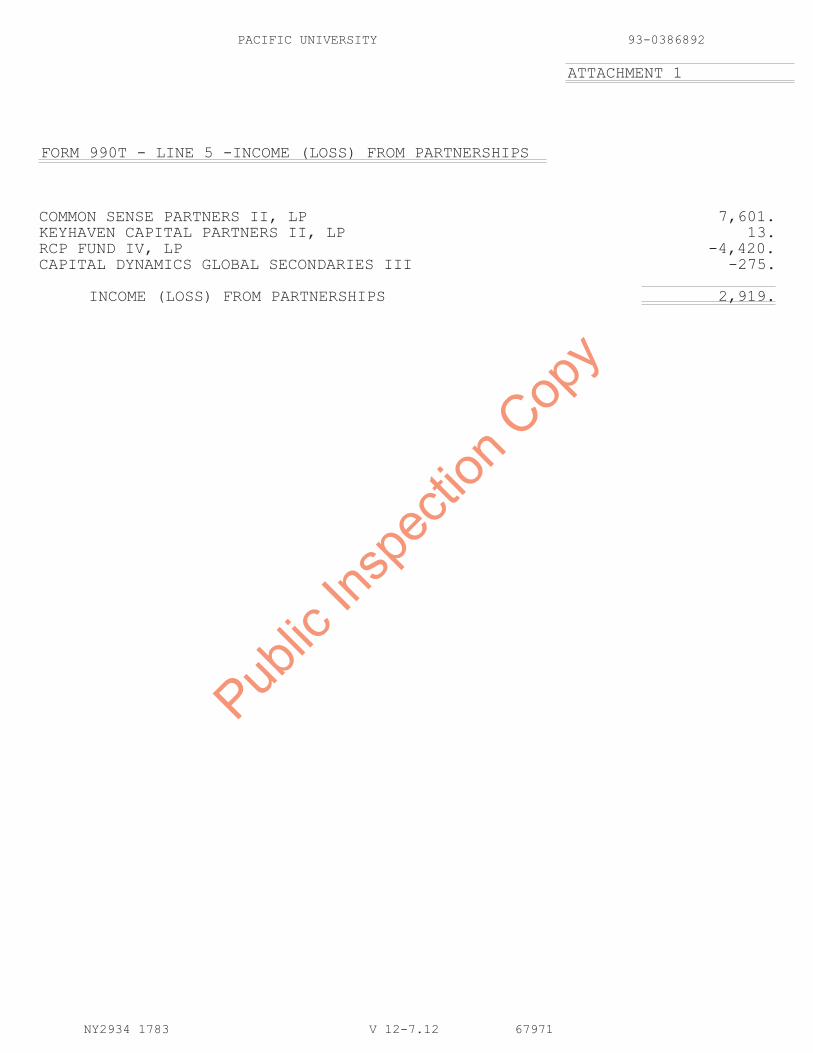

PACIFIC UNIVERSITY 93-0386892

ATTACHMENT 1

FORM 990T - LINE 5 -INCOME (LOSS) FROM PARTNERSHIPS

COMMON SENSE PARTNERS II, LP 7,601.KEYHAVEN CAPITAL PARTNERS II, LP 13.RCP FUND IV, LP -4,420.CAPITAL DYNAMICS GLOBAL SECONDARIES III -275.

INCOME (LOSS) FROM PARTNERSHIPS 2,919.

NY2934 1783 V 12-7.12 67971

Public

Insp

ectio

n Cop

y

PACIFIC UNIVERSITY 93-0386892

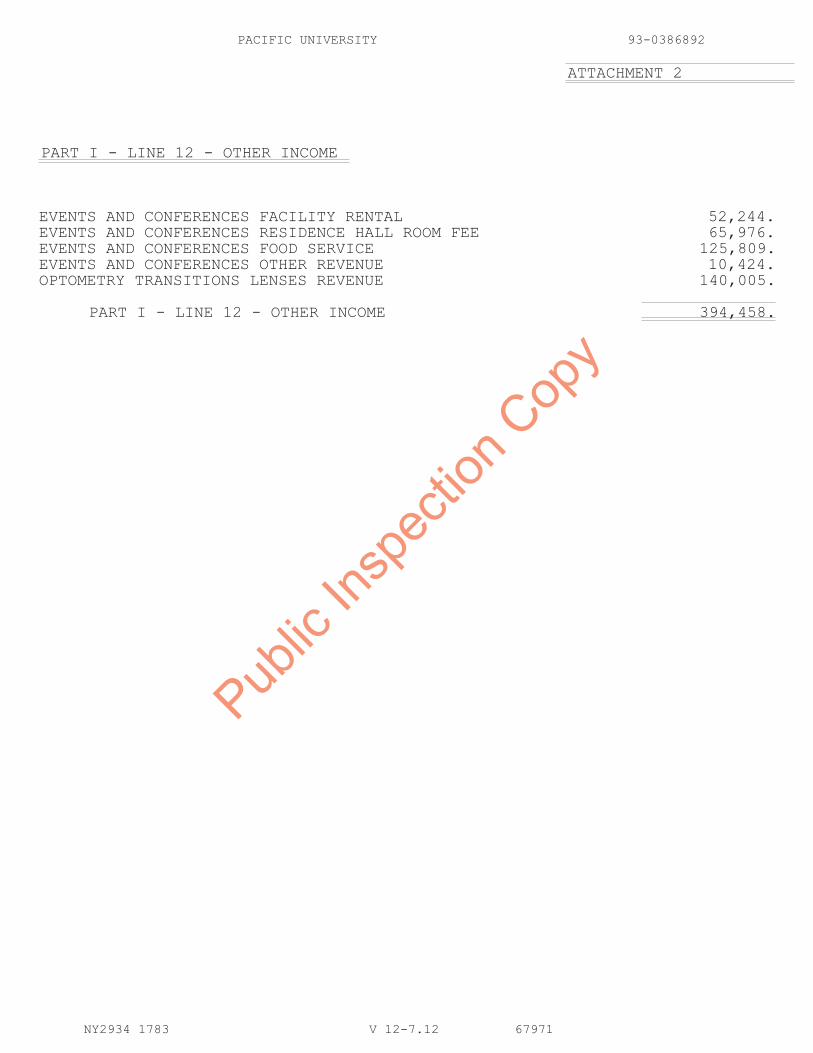

ATTACHMENT 2

PART I - LINE 12 - OTHER INCOME

EVENTS AND CONFERENCES FACILITY RENTAL 52,244.EVENTS AND CONFERENCES RESIDENCE HALL ROOM FEE 65,976.EVENTS AND CONFERENCES FOOD SERVICE 125,809.EVENTS AND CONFERENCES OTHER REVENUE 10,424.OPTOMETRY TRANSITIONS LENSES REVENUE 140,005.

PART I - LINE 12 - OTHER INCOME 394,458.

NY2934 1783 V 12-7.12 67971

Public

Insp

ectio

n Cop

y

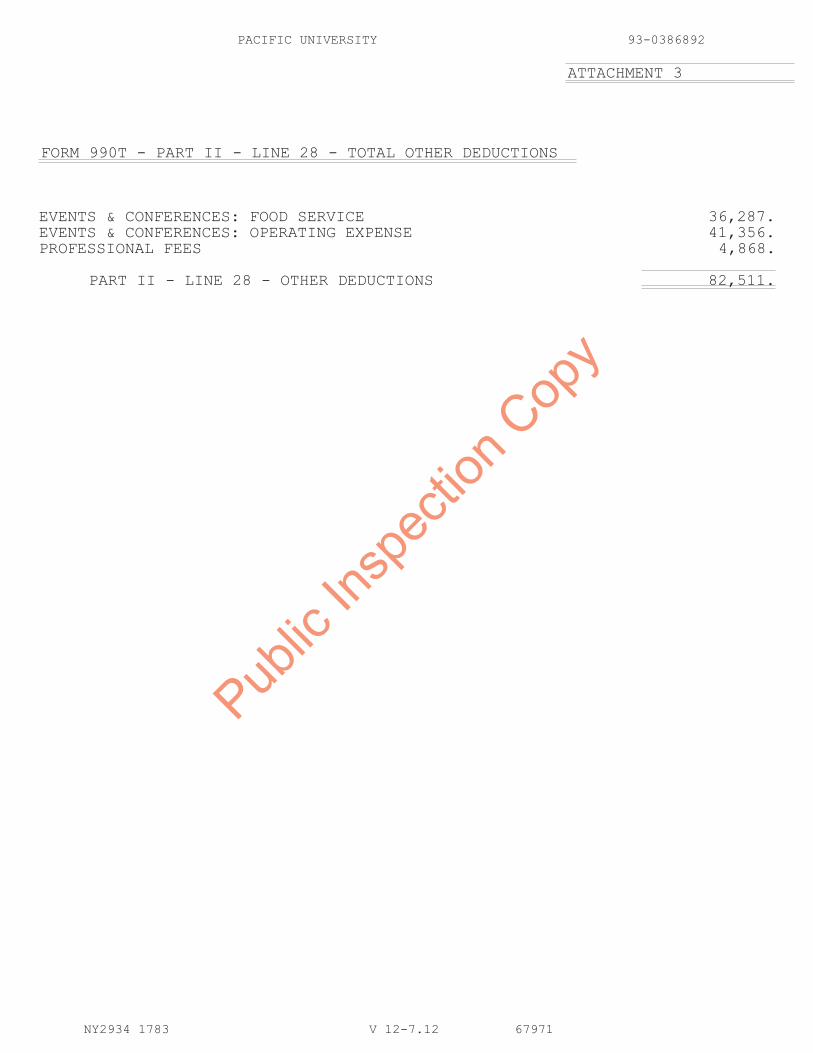

PACIFIC UNIVERSITY 93-0386892

ATTACHMENT 3

FORM 990T - PART II - LINE 28 - TOTAL OTHER DEDUCTIONS

EVENTS & CONFERENCES: FOOD SERVICE 36,287.EVENTS & CONFERENCES: OPERATING EXPENSE 41,356.PROFESSIONAL FEES 4,868.

PART II - LINE 28 - OTHER DEDUCTIONS 82,511.

NY2934 1783 V 12-7.12 67971

Public

Insp

ectio

n Cop

y

PACIFIC UNIVERSITY

93-0386892

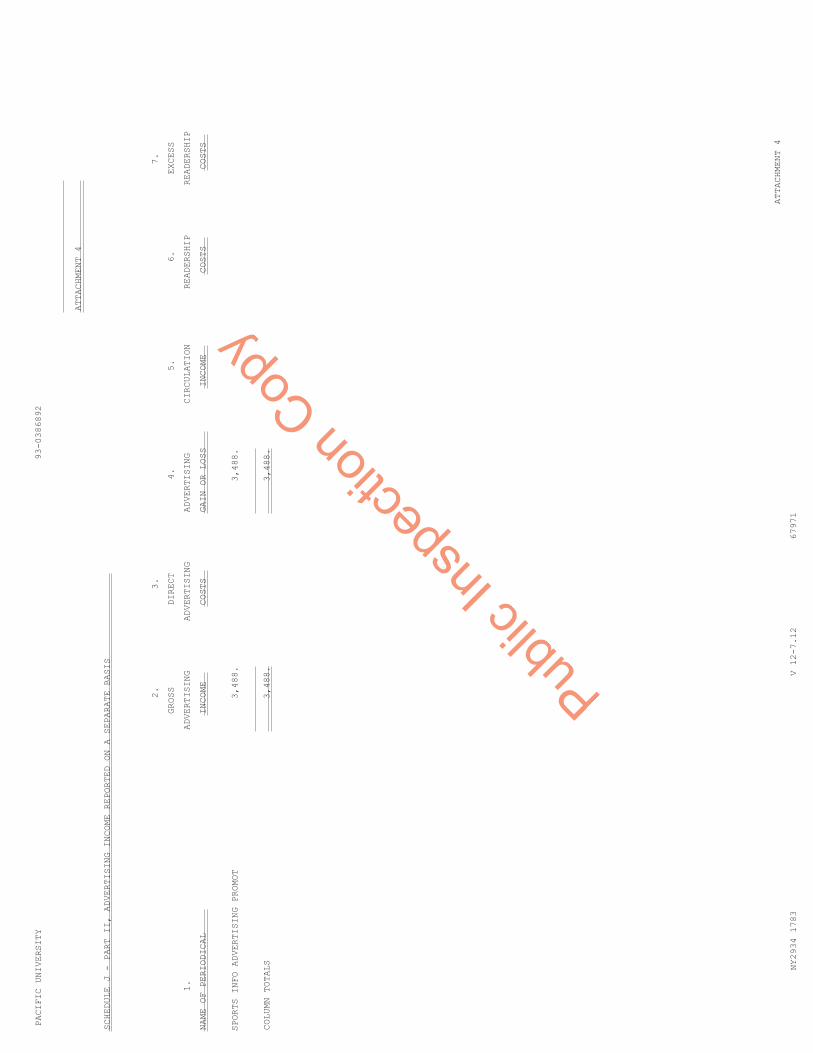

ATTACHMENT 4

SCHEDULE J - PART II, ADVERTISING INCOME REPORTED ON A SEPARATE BASIS

2.

3.

7.

GROSS

DIRECT

4.

5.

6.

EXCESS

1.

ADVERTISING

ADVERTISING

ADVERTISING

CIRCULATION

READERSHIP

READERSHIP

NAME OF PERIODICAL

INCOME

COSTS

GAIN OR LOSS

INCOME

COSTS

COSTS

SPORTS INFO ADVERTISING PROMOT

3,488.

3,488.

COLUMN TOTALS

3,488.

3,488.

ATTACHMENT 4

NY2934 1783

V 12-7.12

67971

Public

Insp

ectio

n Cop

y

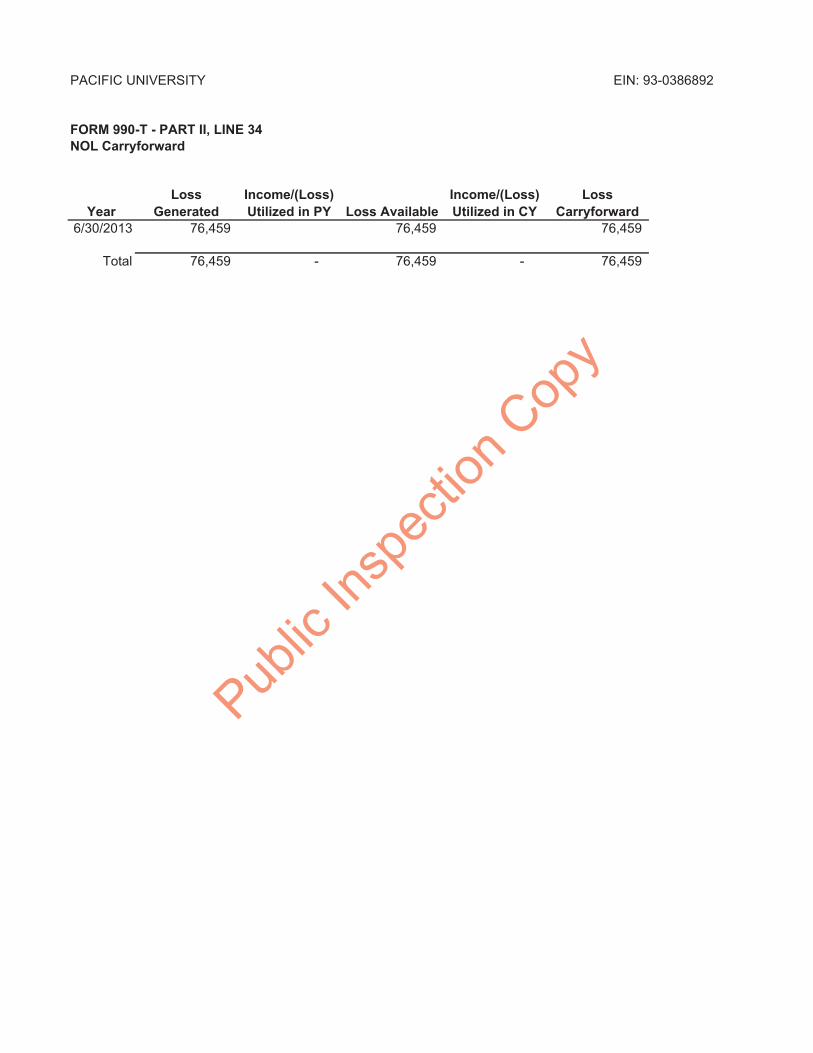

PACIFIC UNIVERSITY EIN: 93-0386892

FORM 990-T - PART II, LINE 34NOL Carryforward

YearLoss

GeneratedIncome/(Loss)Utilized in PY Loss Available

Income/(Loss)Utilized in CY

LossCarryforward

6/30/2013 76,459 76,459 76,459

Total 76,459 - 76,459 - 76,459

Public

Insp

ectio

n Cop

y

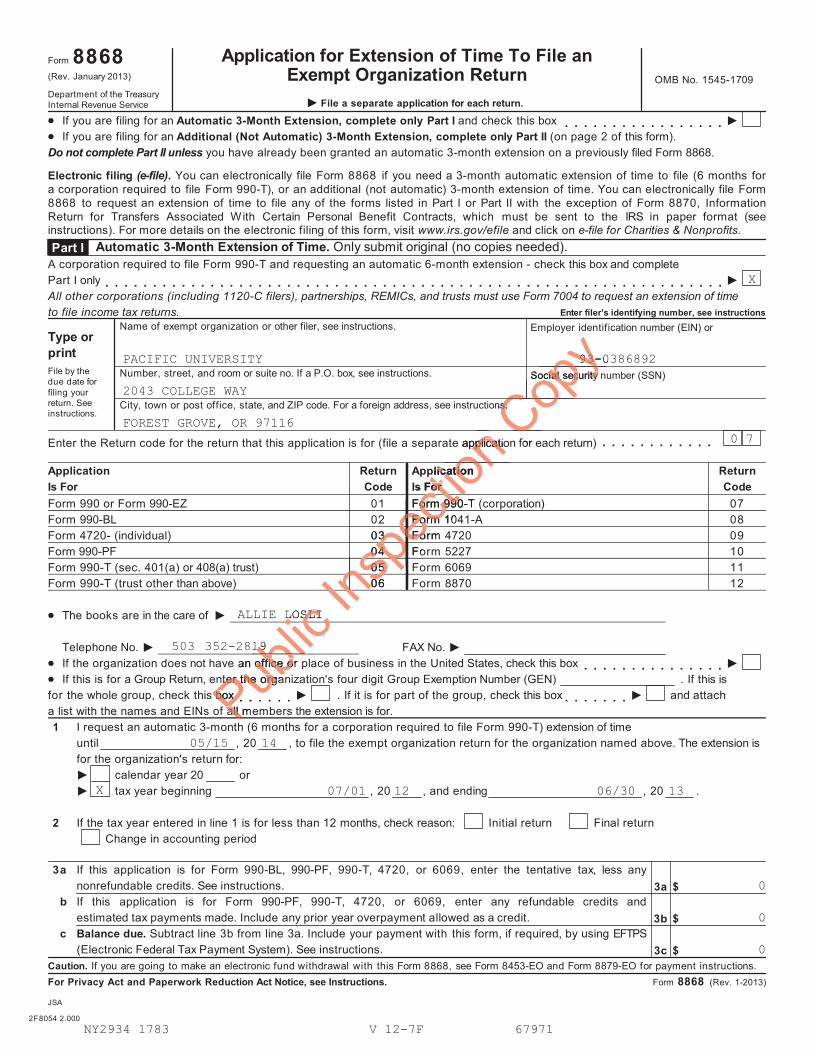

Application for Extension of Time To File anExempt Organization Return

Form 8868(Rev. January 2013) OMB No. 1545-1709Department of the TreasuryInternal Revenue Service File a separate application for each return.

If you are filing for an Automatic 3-Month Extension, complete only Part I and check this boxIf you are filing for an Additional (Not Automatic) 3-Month Extension, complete only Part II (on page 2 of this form).

Do not complete Part II unless you have already been granted an automatic 3-month extension on a previously filed Form 8868.

Electronic filing (e-file). You can electronically file Form 8868 if you need a 3-month automatic extension of time to file (6 months fora corporation required to file Form 990-T), or an additional (not automatic) 3-month extension of time. You can electronically file Form8868 to request an extension of time to file any of the forms listed in Part I or Part II with the exception of Form 8870, InformationReturn for Transfers Associated With Certain Personal Benefit Contracts, which must be sent to the IRS in paper format (seeinstructions). For more details on the electronic filing of this form, visit www.irs.gov/efile and click on e-file for Charities & Nonprofits.

Automatic 3-Month Extension of Time. Only submit original (no copies needed).Part I A corporation required to file Form 990-T and requesting an automatic 6-month extension - check this box and completePart I only All other corporations (including 1120-C filers), partnerships, REMICs, and trusts must use Form 7004 to request an extension of timeto file income tax returns. Enter filer's identifying number, see instructions

Name of exempt organization or other filer, see instructions. Employer identification number (EIN) orType orprintFile by thedue date forfiling yourreturn. Seeinstructions.

Number, street, and room or suite no. If a P.O. box, see instructions.

City, town or post office, state, and ZIP code. For a foreign address, see instructions.

Social security number (SSN)

Enter the Return code for the return that this application is for (file a separate application for each return)

ApplicationIs For

ReturnCode

ApplicationIs For

ReturnCode

Form 990 or Form 990-EZForm 990-BLForm 4720- (individual)Form 990-PFForm 990-T (sec. 401(a) or 408(a) trust)Form 990-T (trust other than above)

010203040506

Form 990-T (corporation)Form 1041-AForm 4720Form 5227Form 6069Form 8870

070809101112

The books are in the care of

Telephone No. FAX No.

If the organization does not have an office or place of business in the United States, check this boxIf this is for a Group Return, enter the organization's four digit Group Exemption Number (GEN)

. If this is

for the whole group, check this box . If it is for part of the group, check this box and attach a list with the names and EINs of all members the extension is for.1 I request an automatic 3-month (6 months for a corporation required to file Form 990-T) extension of time

until , 20 , to file the exempt organization return for the organization named above. The extension isfor the organization's return for:

calendar year 20 ortax year beginning , 20 , and ending , 20 .

2 If the tax year entered in line 1 is for less than 12 months, check reason: Initial return Final returnChange in accounting period

3a If this application is for Form 990-BL, 990-PF, 990-T, 4720, or 6069, enter the tentative tax, less anynonrefundable credits. See instructions. 3a

3b

3c

$

$

$

b If this application is for Form 990-PF, 990-T, 4720, or 6069, enter any refundable credits andestimated tax payments made. Include any prior year overpayment allowed as a credit.

c Balance due. Subtract line 3b from line 3a. Include your payment with this form, if required, by using EFTPS(Electronic Federal Tax Payment System). See instructions.

Caution. If you are going to make an electronic fund withdrawal with this Form 8868, see Form 8453-EO and Form 8879-EO for payment instructions.For Privacy Act and Paperwork Reduction Act Notice, see Instructions. Form 8868 (Rev. 1-2013)

JSA

2F8054 2.000

X

PACIFIC UNIVERSITY 93-0386892

2043 COLLEGE WAY

FOREST GROVE, OR 971160 7

ALLIE LOSLI

503 352-2819

05/15 14

X 07/01 12 06/30 13

0

0

0

NY2934 1783 V 12-7F 67971

PPPublic

icblan office or office onter the organter the orgaboxbox

all mall

cLOSLISLI

1919

Inspe

cti

Inpe

Innssppeee

cction

cti

one applicatiopplicatio

plicationplicatios Foror

203304040505060

Form 990-Torm 990Form 10Form FormFoFo

Copy

CCopypy

Cor i

ns.s.

Social security nocial security

for

93-093-