9 - 1 © 1998 the dryden press chapter 9 the cost of capital cost of capital components debt...

TRANSCRIPT

9 - 1

© 1998 The Dryden Press

CHAPTER 9The Cost of Capital

Cost of Capital ComponentsDebtPreferredCommon Equity

WACCMCCIOS

9 - 2

© 1998 The Dryden Press

What types of long-term capital do firms use?

Long-term debt

Preferred stock

Common equity:

Retained earnings

New common stock

9 - 3

© 1998 The Dryden Press

Should we focus on before-tax or after-tax capital costs?

Stockholders focus on A-T CFs.Thus, focus on A-T capital costs,i.e., use A-T costs in WACC. Onlykd needs adjustment.

9 - 4

© 1998 The Dryden Press

Should we focus on historical (embedded) costs or new (marginal)

costs?

The cost of capital is used primarily to make decisions which involve raising new capital. So, focus on today’s marginal costs (for WACC).

9 - 5

© 1998 The Dryden Press

A 15-year, 12% semiannual bond sells for $1,153.72. What’s kd?

60 60 + 1,00060

0 1 2 30i = ?

30 -1153.72 60 1000

5.0% x 2 = kd = 10%

N I/YR PV FVPMT

-1,153.72

...

INPUTS

OUTPUT

9 - 6

© 1998 The Dryden Press

Component Cost of Debt

Interest is tax deductible, so

kd AT = kd BT(1 - T)

= 10%(1 - 0.40) = 6%.Use nominal rate.Flotation costs small.

Ignore.

9 - 7

© 1998 The Dryden Press

What’s the cost of preferred stock? PP = $113.10; 10%Q; Par = $100; F = $2.

( )=−

= = =

0 1

10 00

100 090 9 0%.

. $100

$113. $2.

$10

$111.. .

k

D

Ppsps

Net

=

Use this formula:

9 - 8

© 1998 The Dryden Press

Picture of Preferred

( ) ( )kPer ps Nom= = = =$2.

$111.. ; .

50

102 25 2 25 4 9%. k

2.50 2.50

0 1 2kps = ?

-111.1

Ï

1111050

.$2.

.= =Dk k

Q

Per Per

...2.50

9 - 9

© 1998 The Dryden Press

Note:

Flotation costs for preferred are significant, so are reflected. Use net price.

Preferred dividends are not deductible, so no tax adjustment. Just kps.

Nominal kps is used.

9 - 10

© 1998 The Dryden Press

Is preferred stock more or less risky to investors than debt?

More risky; company not required to pay preferred dividend.

However, firms try to pay preferred dividend. Otherwise, (1) cannot pay common dividend, (2) difficult to raise additional funds, (3) preferred stockholders may gain control of firm.

9 - 11

© 1998 The Dryden Press

Why is yield on preferred lower than kd?

Corporations own most preferred stock, because 70% of preferred dividend are nontaxable to corporations.

Therefore, preferred often has a lower B-T yield than the B-T yield on debt.

The A-T yield to an investor, and the A-T cost to the issuer, are higher on preferred than on debt. Consistent with higher risk of preferred.

9 - 12

© 1998 The Dryden Press

Example:

kps = 8.84% kd = 10% T = 40%

kps, AT = kps - kps (1 - 0.7)(T)

= 8.84% - 8.84%(0.3)(0.4) = 7.78%

kd, AT = 10% - 10%(0.4) = 6.00%

A-T Risk Premium on Preferred = 1.78%

9 - 13

© 1998 The Dryden Press

Why is there a cost for retained earnings?

Earnings can be reinvested or paid out as dividends.

Investors could buy other securities, earn a return.

Thus, there is an opportunity cost if earnings are retained.

9 - 14

© 1998 The Dryden Press

Opportunity cost: The return stockholders could earn on alternative investments of equal risk.

They could buy similar stocks and earn ks, or company could repurchase its own stock and earn ks. So, ks is the cost of retained earnings.

9 - 15

© 1998 The Dryden Press

Three ways to determine cost of retained earnings, ks:

1. CAPM: ks = kRF + (kM - kRF)b.

2. DCF: ks = D1/P0 + g.

3. Own-Bond-Yield-Plus-Risk Premium:

ks = kd + RP.

9 - 16

© 1998 The Dryden Press

What’s the cost of retained earnings based on the CAPM?

kRF = 7%, MRP = 6%, b = 1.2.

ks = kRF + (kM - kRF )b.

= 7.0% + (6.0%)1.2 = 14.2%.

9 - 17

© 1998 The Dryden Press

What’s the DCF cost of retained earnings, ks? Given: D0 = $4.19;

P0 = $50; g = 5%.

( )k

D

Pg

D g

Pgs = + =

++1

0

0

0

1

( )= +

= +

=

$4. .

$50.

. .

.

19 1050 05

0 088 0 05

13 8%.

9 - 18

© 1998 The Dryden Press

Suppose the company has been earning 15% on equity (ROE = 15%) and retaining 35% (dividend payout = 65%), and this situation is expected to continue.

What’s the expected future g?

9 - 19

© 1998 The Dryden Press

Retention growth rate:

g = b(ROE) = 0.35(15%) = 5.25%.

Here b = Fraction retained.

Close to g = 5% given earlier. Think of bank account paying 10% with b = 0, b = 1.0, and b = 0.5. What’s g?

9 - 20

© 1998 The Dryden Press

Could DCF methodology be applied if g is not constant?

YES, nonconstant g stocks are expected to have constant g at some point, generally in 5 to 10 years.

But calculations get complicated.

9 - 21

© 1998 The Dryden Press

Find ks using the own-bond-yield-plus-risk-premium method. (kd = 10%, RP = 4%.)

This RP = CAPM RP.Produces ballpark estimate of ks.

Useful check.

ks = kd + RP

= 10.0% + 4.0% = 14.0%

9 - 22

© 1998 The Dryden Press

What’s a reasonable final estimate of ks?

Method Estimate

CAPM 14.2%

DCF 13.8%

kd + RP 14.0%

Average 14.0%

9 - 23

© 1998 The Dryden Press

How do we find the cost of new common stock, ke?

Use DCF formula, but

adjust P0 for flotation cost.

End up with ke > ks.

9 - 24

© 1998 The Dryden Press

( )( )

kD g

P Fge =

+

−+0

0

1

1

New common, F = 15%:

( )( )

=−

+

= + =

$4. .

$50 ..

$4.

$42.. .

19 105

1 0 155 0%

40

505 0% 15 4%.

9 - 25

© 1998 The Dryden Press

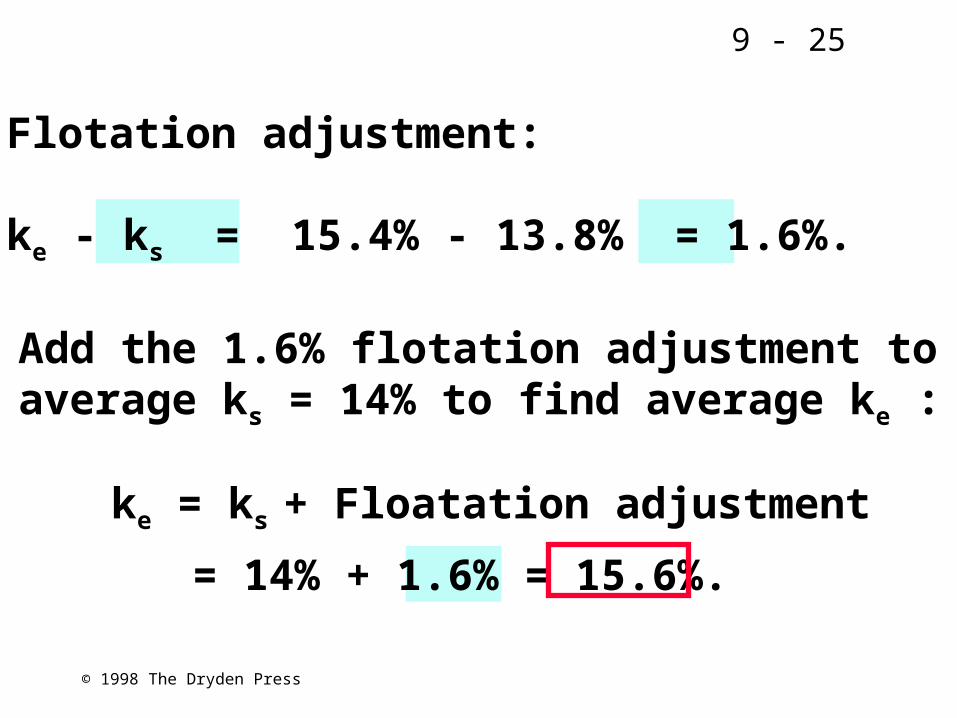

Flotation adjustment:

ke - ks = 15.4% - 13.8% = 1.6%.

Add the 1.6% flotation adjustment toaverage ks = 14% to find average ke :

ke = ks + Floatation adjustment

= 14% + 1.6% = 15.6%.

9 - 26

© 1998 The Dryden Press

Why is ke > ks?

1. Investors expect to earn ks.

2. Company gets money as retained earnings; earns ks; everything’s O.K.

3. But investors put up money to buy new stock; F pulled out; so net money must earn > ks to provide ks on money investors put up.

9 - 27

© 1998 The Dryden Press

Example

1. ks = D1/P0 + g = 10%; F = 20%.2. Investors put up $100, expect EPS

= DPS = 0.1($100) = $10.3. But company nets only $80.

4. If earn ks = 10% on $80, EPS = DPS = 0.10($80) = $8. Too low. Price falls.

5. Need to earn ke = 10% /0.8 = 12.5%.6. Then EPS = 0.125($80) = $10.

Conclusion: ke = 12.5% > ks = 10.0%.

9 - 28

© 1998 The Dryden Press

What’s WACC using only retained earnings for equity component of

WACC1?

WACC1 = wdkd(1 - T) + wpskps + wceks

= 0.3(10%)(0.6) + 0.1(9%) + 0.6(14%)

= 1.8% + 0.9% + 8.4% = 11.1%.

= Cost per $1 until retained earnings used up.

9 - 29

© 1998 The Dryden Press

WACC with New CS

F = 15%

WACC2 = wdkd(1 - T) + wpskps + wceke

= 0.3(10%)(0.6) + 0.1(9%) + 0.6(15.6%)

= 1.8% + 0.9% + 9.4% = 12.1%.

9 - 30

© 1998 The Dryden Press

Summary to this Point

ke or ks WACC

Debt + Pfd + RE: 14.0% 11.1%

Debt + Pfd + F = 15% 15.6% 12.1%

WACC rises because equity cost is rising.

9 - 31

© 1998 The Dryden Press

MCC Schedule Definition

MCC shows cost of each dollar raised.

Each dollar consists of $0.30 of debt, $0.10 of Preferred and $0.60 of equity (retained earnings or new common stock).

First dollars cost WACC1 = 11.1%, then WACC2 = 12.1%.

9 - 32

© 1998 The Dryden Press

How large will capital budget be before must issue new CS?

Capital Budget = Capital Raised

Debt = 0.3 Capital Raised Preferred = 0.1 Capital Raised Equity = 0.6 Capital Raised

= 1.0 Total Capital

Equity = RE = 0.6 Capital Raised, so Capital Raised = RE/0.6.

9 - 33

© 1998 The Dryden Press

Find Retained Earnings Break Point

Dollars of REFraction of equity

= = $500,000.

$500,000 total can be financed with retained earnings, debt, and preferred.

BPRE =

$300,0000.60

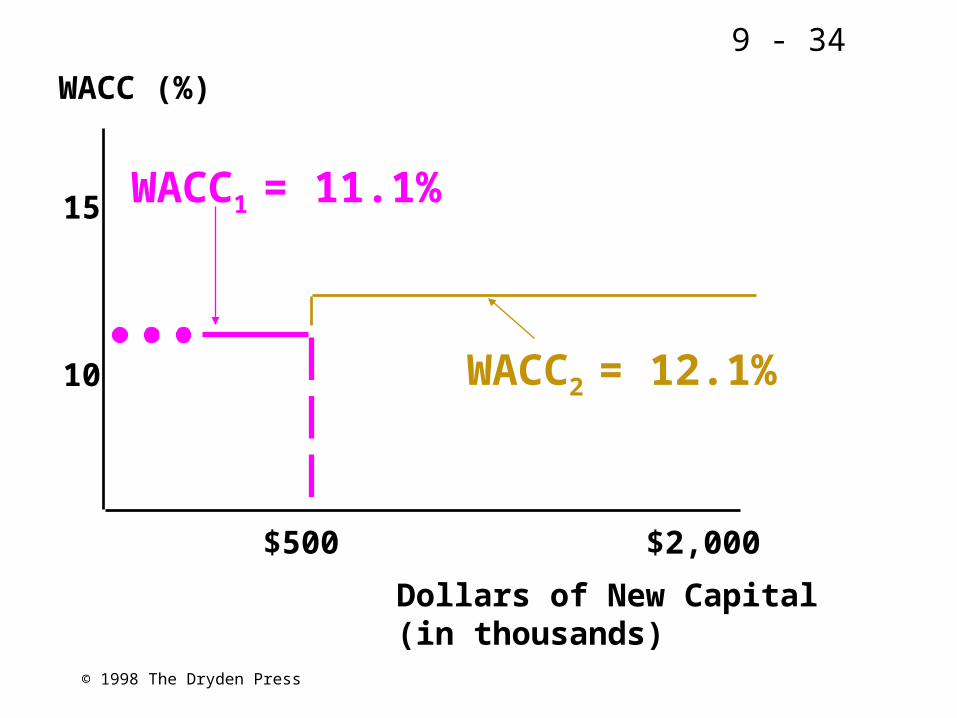

9 - 34

© 1998 The Dryden Press

WACC (%)

Dollars of New Capital(in thousands)

15

10

$500 $2,000

WACC1 = 11.1%

WACC2 = 12.1%

9 - 35

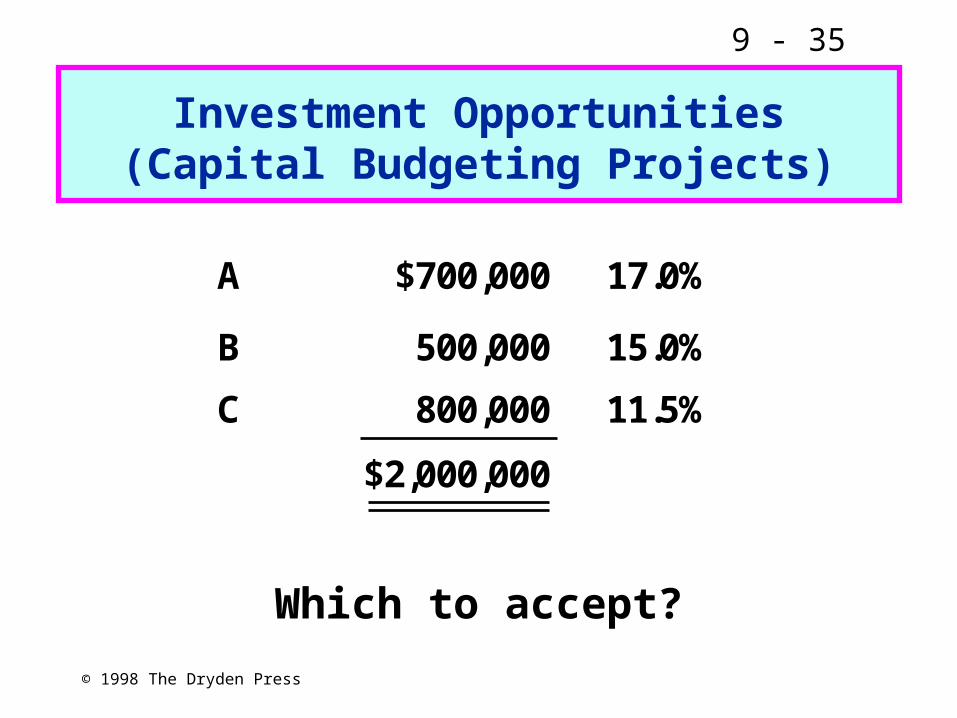

© 1998 The Dryden Press

Investment Opportunities(Capital Budgeting Projects)

A $700,000 17.0%

B 500,000 15.0%

C 800,000 11.5%

$2,000,000

Which to accept?

9 - 36

© 1998 The Dryden Press

A = 17B = 15

11.1

12.1

IOS

MCC

%

500 1,200 2,000 $

Optimal Capital Budget

C = 11.5

9 - 37

© 1998 The Dryden Press

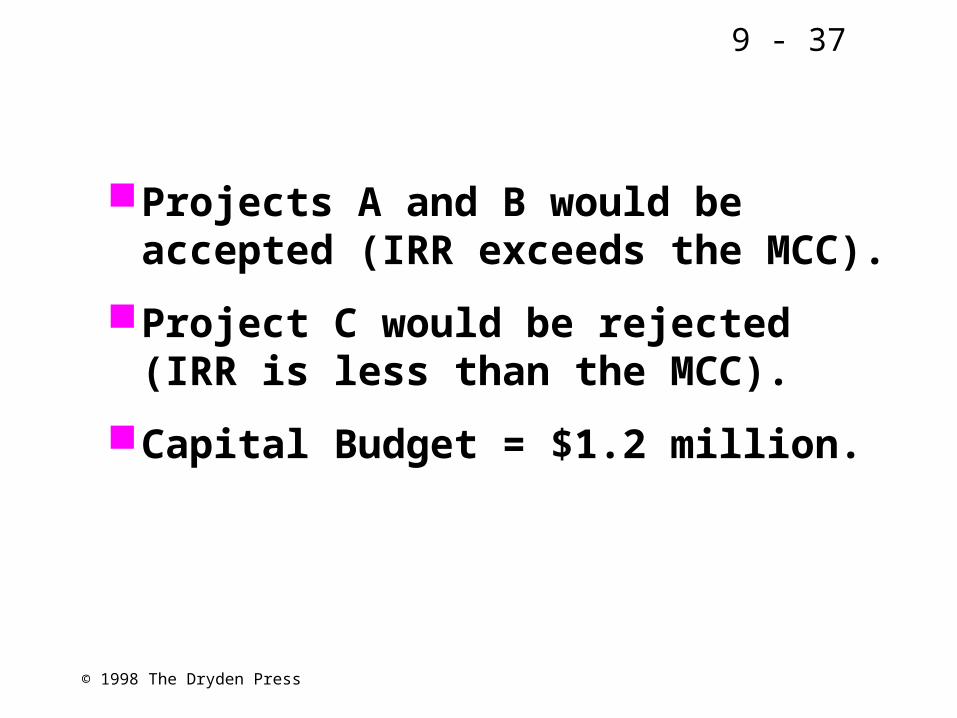

Projects A and B would be accepted (IRR exceeds the MCC).

Project C would be rejected (IRR is less than the MCC).

Capital Budget = $1.2 million.

9 - 38

© 1998 The Dryden Press

Would the MCC remain constant beyond $2 million?

No. WACC would eventually rise above 12.1%.

Costs of debt, preferred stock would rise.

Large increases in capital budget may also increase the perceived risk of the firm, increasing WACC.