6-1 thoughts on budgeting acct7320 fall 2011 bailey

TRANSCRIPT

6-1

Thoughts on Budgeting ACCT7320 Fall 2011 Bailey

Purposes of Budgeting

6-2

Stimulate concern for the futureProvide a framework for delegation of

authority & responsibilityA financial model to test plans againstA communication device

- to relay top management’s style & authority- establish organizational climate- the dialogue is what’s important

Motivation?

Purposes of Budgeting

6-3

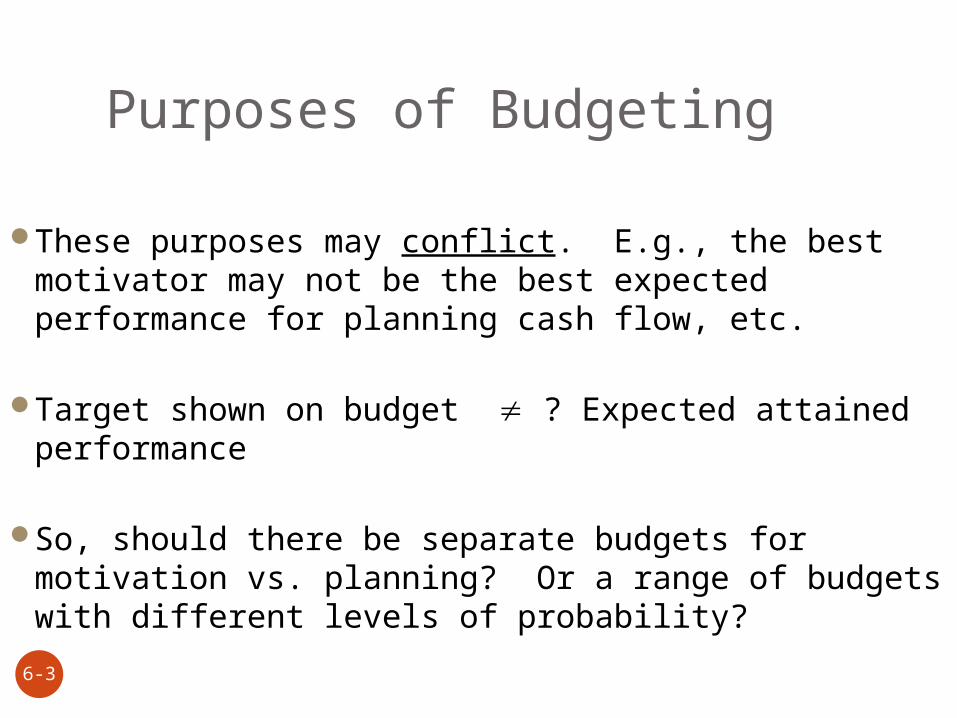

These purposes may conflict. E.g., the best motivator may not be the best expected performance for planning cash flow, etc.

Target shown on budget ? Expected attained performance

So, should there be separate budgets for motivation vs. planning? Or a range of budgets with different levels of probability?

Attitudes

6-4

Attitudes toward budgets tend to be negative.

Chris Argyris, The Impact of Budgets on People, 1952

Neg. attitudes towards accountants and budgets

Recommended participation in the budgeting process as a cure; generally supported by later research

Research on “Participation”

6-5

Participation represents a spectrum

Studies show greater likelihood that managers will carry out their “own” plans, than imposed plans.

open process of

group decision making

Consultation only; centralized decision

making

Participation

6-6

But care is needed in generalizing from the research studies

E.g., Some studies involved a change from authoritarianism to some participation - May not generalize to a change from some to much participation

Current research approach is to consider the underlying processes & conditions

Effects are more complicated

6-7

Participation

Improved groupcohesiveness

Better productivity?Worse productivity?

Prevailing Group Attitudes

Effectiveness

6-8

Additionally, the effectiveness of participation may depend upon:

NationalityEthnical attitudesPersonality types of workers, supervisorsAccess to information (centralized, dispersed)Type of decision (e.g., close down plant)

Forecasting of Revenues, Costs

6-9

Sales The key figure!

Determines: production level plant needs (expand?) selling & admin

expense

Methods of sales forecasting

1. Judgmental estimates by key executives, sales force

2. Trend analysisa) “we've been growing 10% per year”

b) Mathematical time seriesSales example, Dept. store:

Qtr Sales = f(St-1,St-4) Details are

complicated

Methods

6-11

3. Correlation (regression) analysis (Not in time series.

Just a correlation.)

#Refrig. Sold = y

x = # Housing starts in previous yeary = a + bx

...

. .. .

..

... .

..

.. .

.

....

Methods

6-12

4. Multiple regression

y = a + b1x1 + b2x2 + b3x3 etc.

E.g., y = tire sales by Uniroyalx1 = new cars to be manufactured

x2 = new cars made 3 years ago

x3 = GNP (or DPI)

Methods

6-13

5. Market share analysis(co's % of mkt) x (total industry forecast)

E.g.: pharmaceutical firm has 20% of market;

all legitimate drug sales = 1% of DPI 20% x 1% x DPI forecast = our sales

forecast

Budgeting, continued…

6-14

Discuss “Corporate Budgeting Is Broken”