5 th annual supply chain connections conference, winnipeg, february 11, 2009 inland terminals,...

TRANSCRIPT

55thth Annual Supply Chain Connections Conference, Annual Supply Chain Connections Conference, Winnipeg, February 11, 2009Winnipeg, February 11, 2009

Inland Terminals, Logistic Clusters Inland Terminals, Logistic Clusters and Global Commodity Chains: and Global Commodity Chains: Looking Into the Eye of the StormLooking Into the Eye of the Storm

Jean-Paul Rodrigue

Associate Professor, Dept. of Global Studies & Geography, Hofstra University, New York, USA

Van Horne Researcher in Transportation and Logistics, University of Calgary, Alberta, Canada

Inland Terminals: The Eye of the StormInland Terminals: The Eye of the Storm

Containerized Containerized TradeTrade

Questioning growth prospects.Questioning growth prospects.Paradigm shift (forecasting…).Paradigm shift (forecasting…).

Trade Trade ImbalancesImbalances

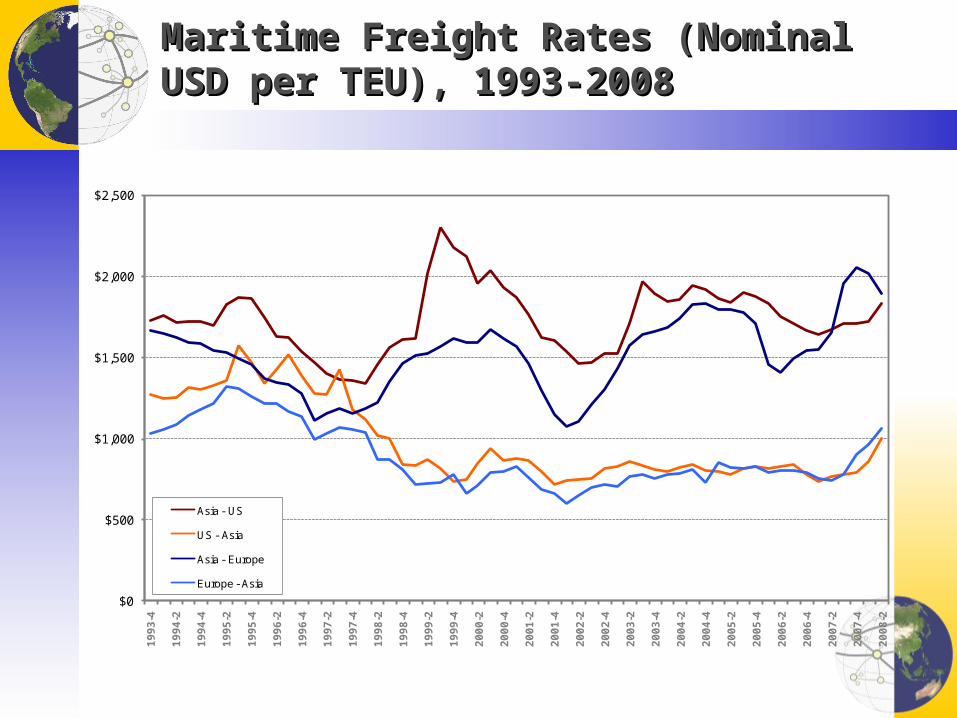

Imbalanced flows and shipping rates.Imbalanced flows and shipping rates.Load centers for empties on backhauls Load centers for empties on backhauls to ports.to ports.

TerminalizationTerminalization Integrating inland terminals, corridors Integrating inland terminals, corridors and commodity chains.and commodity chains.

GovernanceGovernanceIncluding inland terminals within public Including inland terminals within public policy and regional planning.policy and regional planning.Value capture.Value capture.

Global Containerized Trade: Prepare to be Global Containerized Trade: Prepare to be DisappointedDisappointed

Potential Divergence: The First Crisis ofPotential Divergence: The First Crisis ofGlobalizationGlobalization

Container yard, Port of Yantian, ChinaContainer yard, Port of Yantian, China

Impact of Recessions on Consumption and Freight Impact of Recessions on Consumption and Freight RatesRates

Value of GoodsLow HighNone

Significant

Decline

A – Basic GoodsB – Discretionary GoodsC – Durable GoodsD – Capital EquipmentE – Luxury Goods

ConsumptionConsumption

None

Significant

Decline

1 – Futures Indexes2 – Income and Spending3 – Container Volumes4 – Value of Trade

Trade and Freight RatesTrade and Freight Rates

SeveritySeverity

Sequence

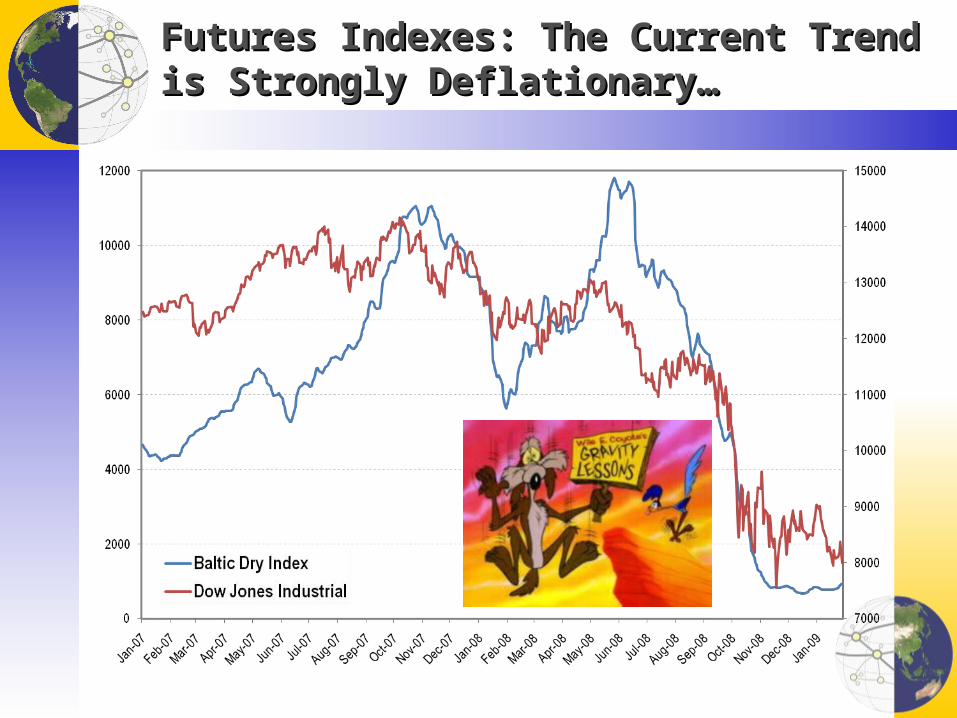

Futures Indexes: The Current Trend is Strongly Futures Indexes: The Current Trend is Strongly Deflationary…Deflationary…

Annual Light Vehicle Sales, United States, January Annual Light Vehicle Sales, United States, January 2008 – January 2009 (millions)2008 – January 2009 (millions)

-36.8%-36.8%

-42.3%-42.3%

-22.9%-22.9%

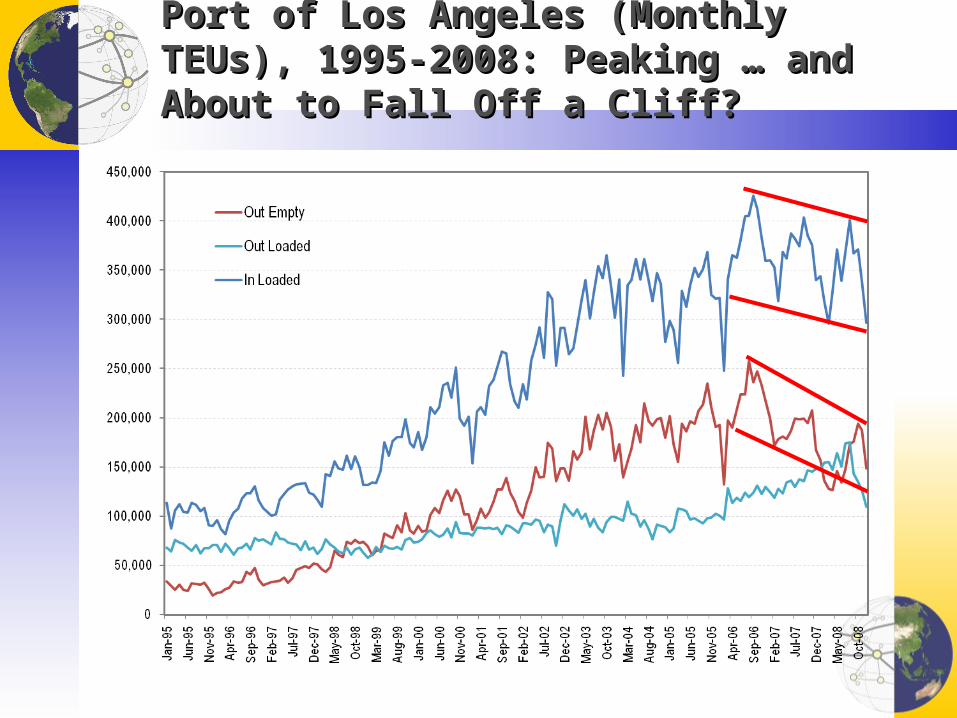

Port of Los Angeles (Monthly TEUs), 1995-2008: Port of Los Angeles (Monthly TEUs), 1995-2008: Peaking … and About to Fall Off a Cliff?Peaking … and About to Fall Off a Cliff?

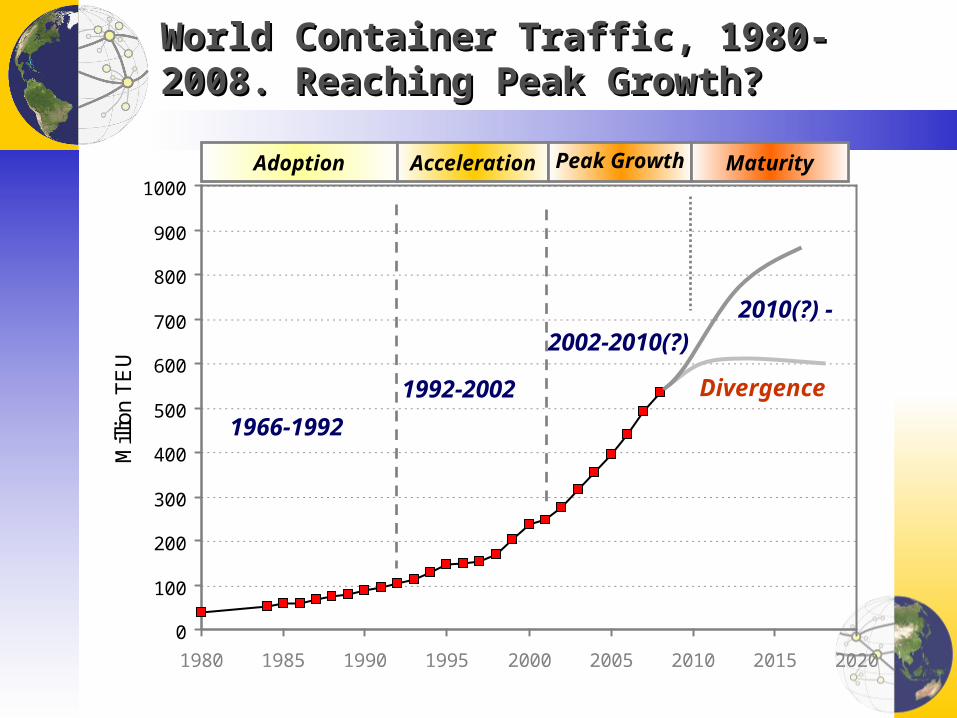

World Container Traffic, 1980-2008. Reaching Peak World Container Traffic, 1980-2008. Reaching Peak Growth?Growth?

0

100

200

300

400

500

600

700

800

900

1000

1980 1985 1990 1995 2000 2005 2010 2015 2020

Mill

ion

TE

U

Divergence

Adoption Acceleration Peak Growth Maturity

1966-1992

1992-2002

2002-2010(?)2010(?) -

Global Bulk and Container Fleet Partially Global Bulk and Container Fleet Partially Immobilized (Singapore, January 2009)Immobilized (Singapore, January 2009)

Cars Accumulating at the Long Beach Port Terminal, Cars Accumulating at the Long Beach Port Terminal, December 2008December 2008

Trade Imbalances: Coping with DistortionsTrade Imbalances: Coping with Distortions

Transport FlowsTransport FlowsTransport RatesTransport Rates

Inland Terminals and RepositioningInland Terminals and Repositioning

NS Rutherford Inland Terminal, PennsylvaniaNS Rutherford Inland Terminal, Pennsylvania

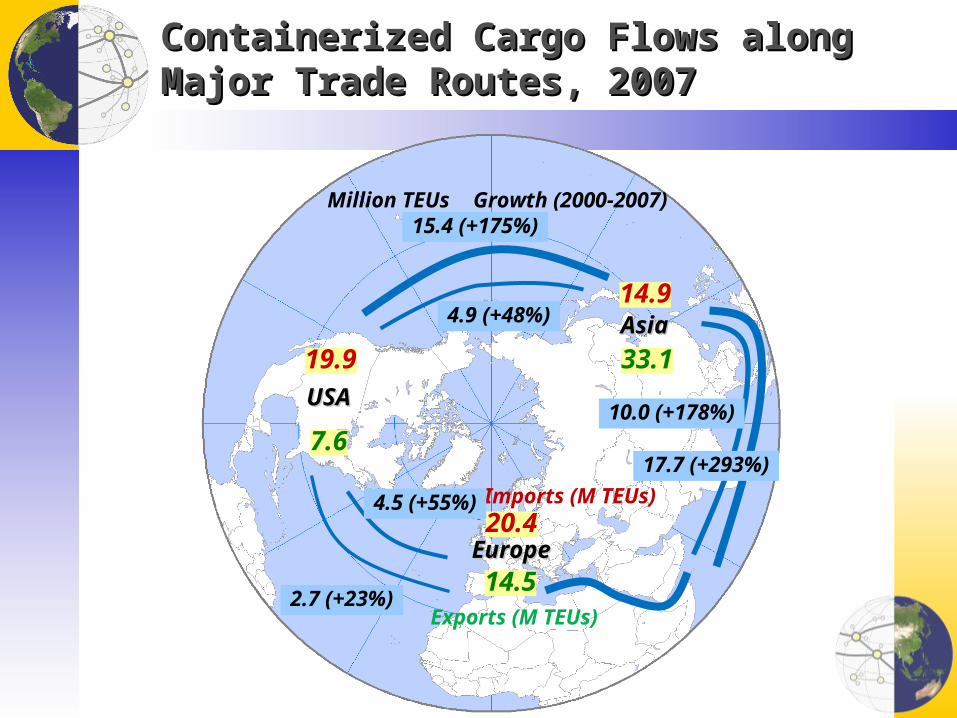

Containerized Cargo Flows along Major Trade Containerized Cargo Flows along Major Trade Routes, 1995-2007 (in millions of TEUs)Routes, 1995-2007 (in millions of TEUs)

4.0

5.2

5.6

7.2

8.8

10.2

12.4

12.4

15.0

15.4

3.5

3.3

3.3

3.9

3.9

4.1

4.2

4.4

4.7

4.9

2.8

3.5

4.5

5.9

6.1

7.3

8.9

10.8

15.3

17.7

2.3

2.7

3.6

4.0

4.2

4.9

5.2

5.5

9.1

10.0

1.2

1.3

2.2

2.7

1.5

1.7

1.7

2.1

2.5

2.7

1.4

1.7

2.9

3.6

2.6

2.9

3.2

3.8

4.4

4.5

0 10 20 30 40 50 60

1995

1998

2000

2001

2002

2003

2004

2005

2006

2007

Asia-USA

USA-Asia

Asia-Europe

Europe-Asia

USA-Europe

Europe-USA

Containerized Cargo Flows along Major Trade Containerized Cargo Flows along Major Trade Routes, 2007Routes, 2007

USAUSA

7.6

AsiaAsia

33.1

14.5

19.9

20.4

14.9

EuropeEurope

15.4 (+175%)

4.9 (+48%)

Million TEUs Growth (2000-2007)

Imports (M TEUs)

Exports (M TEUs)2.7 (+23%)

4.5 (+55%)

10.0 (+178%)

17.7 (+293%)

Maritime Freight Rates (Nominal USD per TEU), 1993-Maritime Freight Rates (Nominal USD per TEU), 1993-20082008

$0

$500

$1,000

$1,500

$2,000

$2,500

1993-4

1994-2

1994-4

1995-2

1995-4

1996-2

1996-4

1997-2

1997-4

1998-2

1998-4

1999-2

1999-4

2000-2

2000-4

2001-2

2001-4

2002-2

2002-4

2003-2

2003-4

2004-2

2004-4

2005-2

2005-4

2006-2

2006-4

2007-2

2007-4

2008-2

Asia - US

US - Asia

Asia - Europe

Europe - Asia

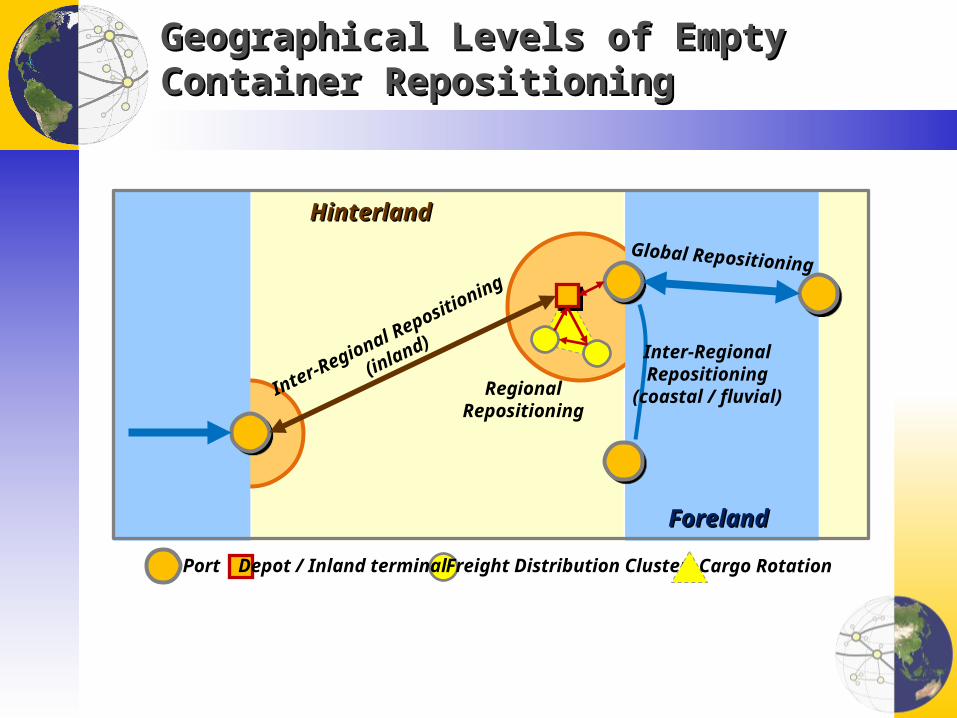

Geographical Levels of Empty Container Geographical Levels of Empty Container Repositioning Repositioning

HinterlandHinterland

ForelandForeland

Inter-Regional Repositioning

(inland)

Global Repositioning

Inter-RegionalRepositioning

(coastal / fluvial)

Port Depot / Inland terminal Freight Distribution Cluster

RegionalRepositioning

Cargo Rotation

Main North American Trade Corridors and Main North American Trade Corridors and Metropolitan Freight CentersMetropolitan Freight Centers

1) Efficient repositioning2) Cargo rotation3) Export market

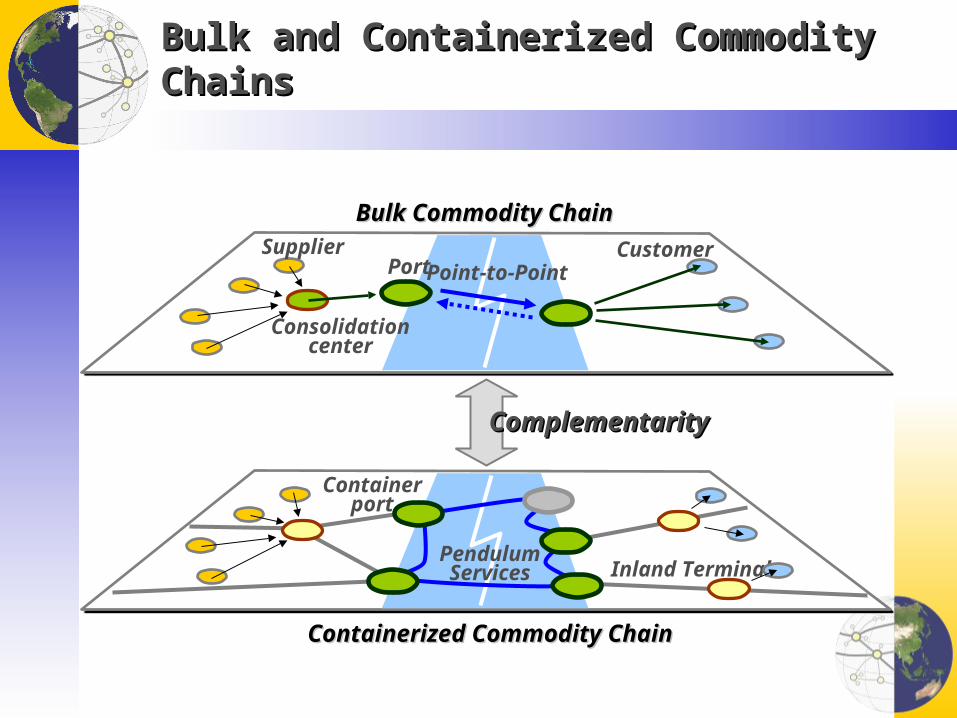

Bulk and Containerized Commodity ChainsBulk and Containerized Commodity Chains

Bulk Commodity ChainBulk Commodity Chain

Containerized Commodity ChainContainerized Commodity Chain

Consolidationcenter

PortSupplier Customer

Inland Terminal

Containerport

PendulumServices

Point-to-Point

ComplementarityComplementarity

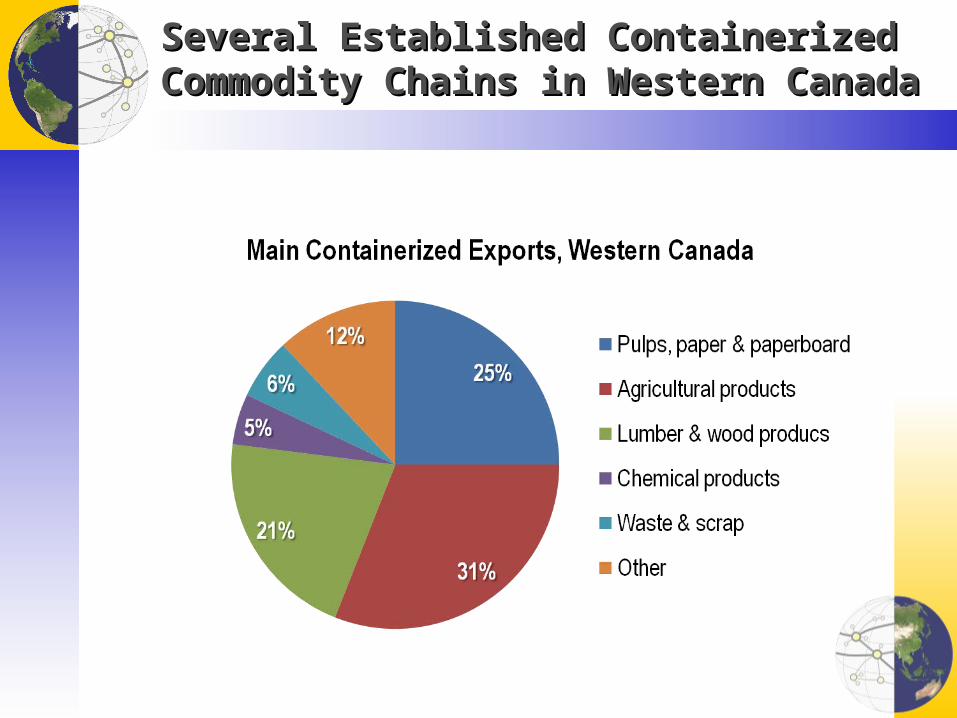

Several Established Containerized Commodity Several Established Containerized Commodity Chains in Western CanadaChains in Western Canada

Terminalization and Inland TerminalsTerminalization and Inland Terminals

Trimodal Container Terminal, Willebroek, BelgiumTrimodal Container Terminal, Willebroek, Belgium

Economies of Scale: A Hard Pill to SwallowEconomies of Scale: A Hard Pill to SwallowTerminalization and Supply ChainsTerminalization and Supply Chains

Extended Distribution CentersExtended Distribution Centers

Type and Function of Inland TerminalsType and Function of Inland Terminals

Satelliteterminal

Load center

Transmodalterminal

Type Function

Satellite terminal Close to a port facility. Accommodate additional traffic and serve functions that have become too expensive at the port. Container transloading.

Freight distribution cluster / load center

Access regional markets (production and consumption). Intermodal, warehousing, and logistics functions. Linked with logistics parks and free trade zones.

Intermodal / Transmodal facility

Link large systems of freight circulation either through the same mode (e.g. rail-to-rail) or through intermodalism (e.g. rail-to-truck).

Corridor

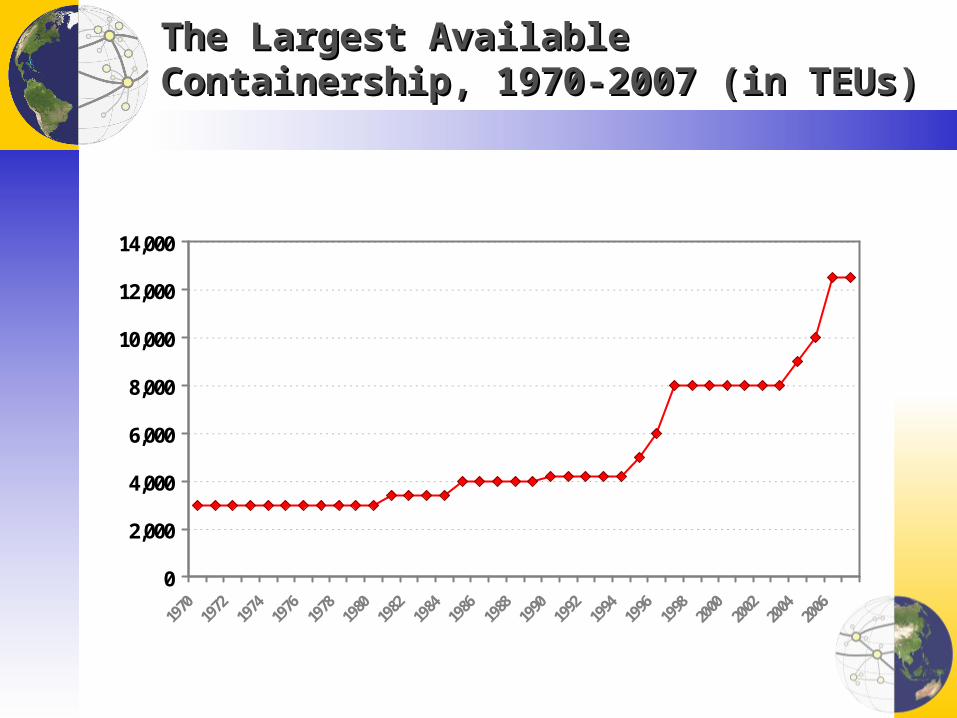

The Largest Available Containership, 1970-2007 (in The Largest Available Containership, 1970-2007 (in TEUs)TEUs)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

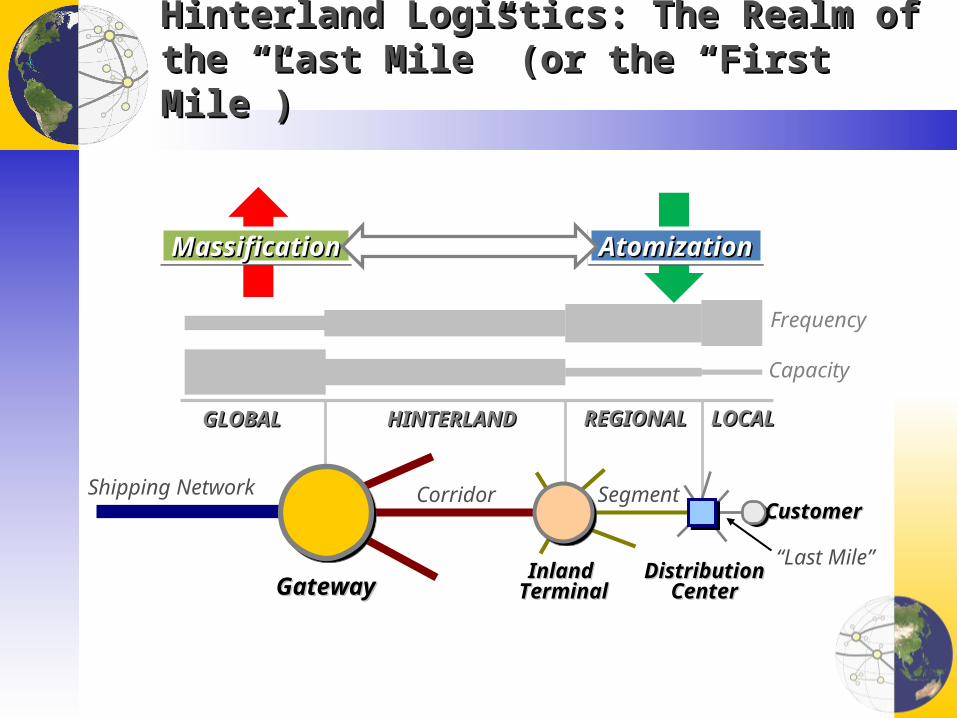

Hinterland Logistics: The Realm of the “Last Mile” Hinterland Logistics: The Realm of the “Last Mile” (or the “First Mile”)(or the “First Mile”)

GatewayGatewayInland Inland

TerminalTerminalDistributionDistribution

CenterCenter

Capacity

Frequency

CorridorCustomerCustomer

“Last Mile”

Segment

GLOBALGLOBAL HINTERLANDHINTERLAND REGIONALREGIONAL LOCALLOCAL

Shipping Network

MassificationMassificationMassificationMassification AtomizationAtomizationAtomizationAtomization

Massification of Inland Terminals: Automated Massification of Inland Terminals: Automated Transfer Management SystemsTransfer Management Systems

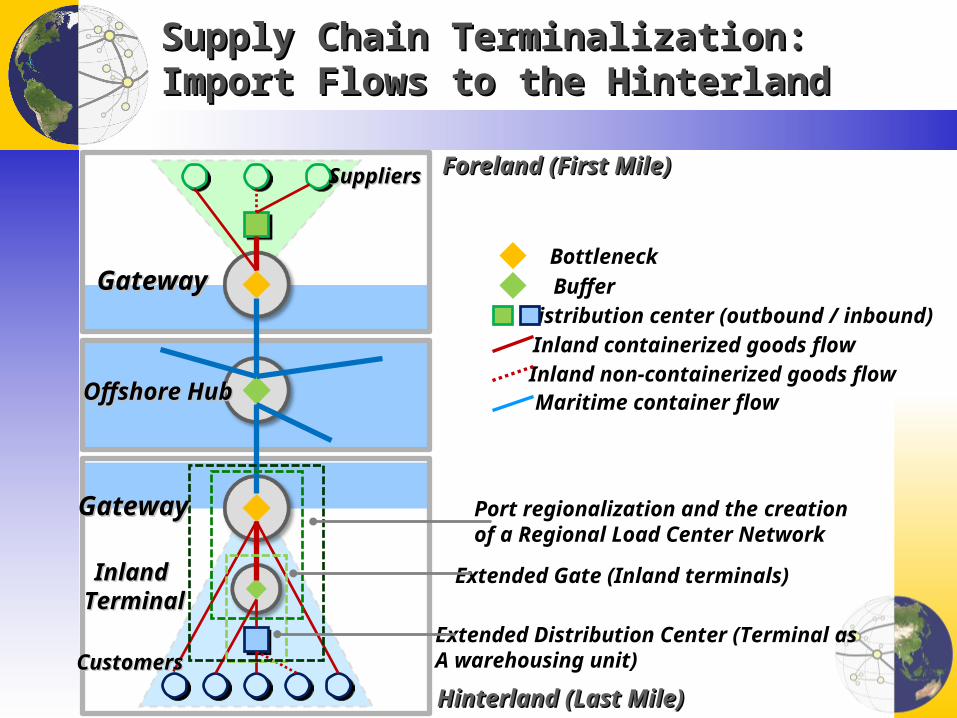

Supply Chain Terminalization: Import Flows to the Supply Chain Terminalization: Import Flows to the HinterlandHinterland

GatewayGateway

Offshore HubOffshore Hub

BottleneckBufferDistribution center (outbound / inbound)Inland containerized goods flowInland non-containerized goods flowMaritime container flow

Foreland (First Mile)Foreland (First Mile)

Hinterland (Last Mile)Hinterland (Last Mile)

GatewayGateway

SuppliersSuppliers

CustomersCustomersExtended Distribution Center (Terminal asA warehousing unit)

Extended Gate (Inland terminals)

Port regionalization and the creation of a Regional Load Center Network

Inland Inland TerminalTerminal

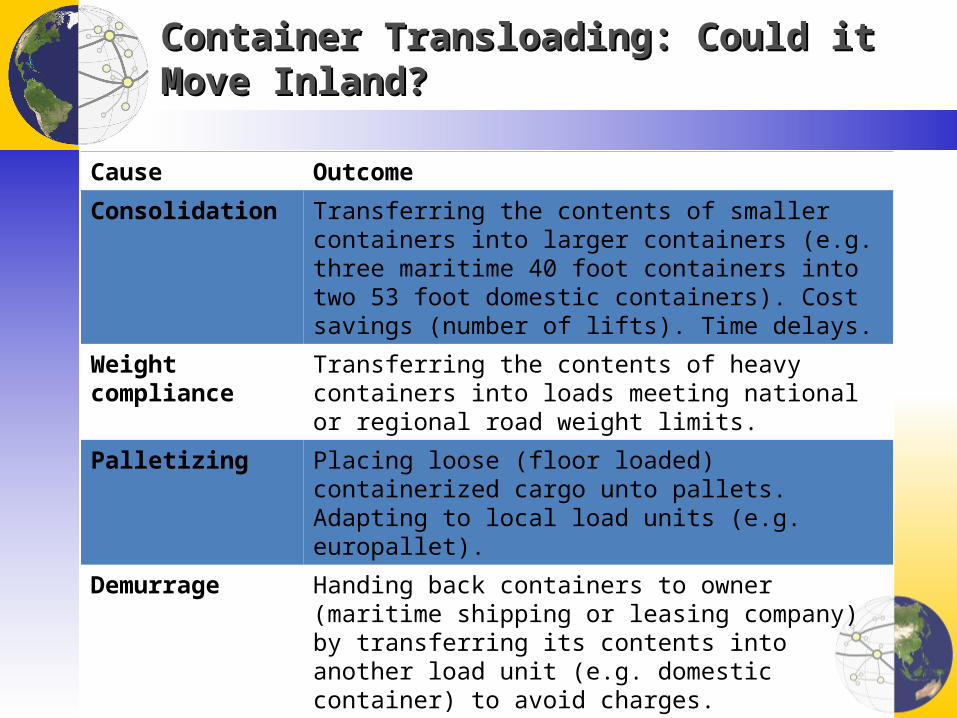

Container Transloading: Could it Move Inland?Container Transloading: Could it Move Inland?

Cause Outcome

Consolidation Transferring the contents of smaller containers into larger containers (e.g. three maritime 40 foot containers into two 53 foot domestic containers). Cost savings (number of lifts). Time delays.

Weight compliance Transferring the contents of heavy containers into loads meeting national or regional road weight limits.

Palletizing Placing loose (floor loaded) containerized cargo unto pallets. Adapting to local load units (e.g. europallet).

Demurrage Handing back containers to owner (maritime shipping or leasing company) by transferring its contents into another load unit (e.g. domestic container) to avoid charges.

Equipment availability

Making maritime containers available for exports and domestic containers available for imports. Trade facilitation.

Supply chain management

Terminal and transloading facility as a buffer. Delay decision to route freight to better fulfill regional demands. Perform some added value activities (packaging, labeling, final assembly, etc.)

Governance and Inland TerminalsGovernance and Inland Terminals

Terminal Operators and Value CaptureTerminal Operators and Value CaptureRegional Integration as Logistics ClustersRegional Integration as Logistics Clusters

Uiwang Inland Container Depot, South KoreaUiwang Inland Container Depot, South Korea

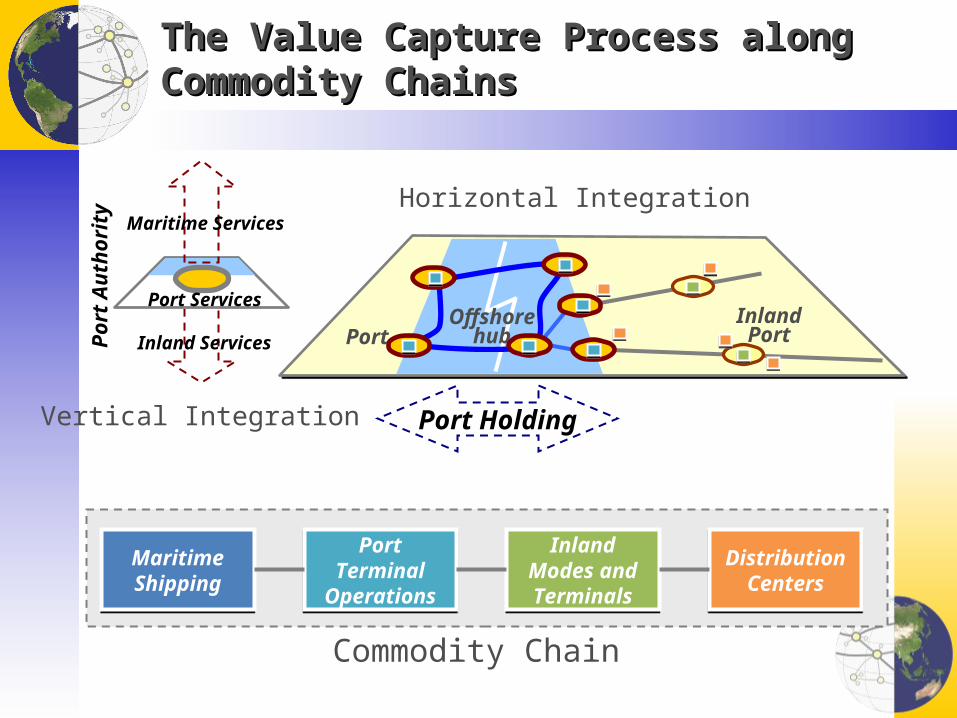

Commodity Chain

The Value Capture Process along Commodity ChainsThe Value Capture Process along Commodity Chains

Port Holding

Port

Aut

horit

y Maritime Services

Inland Services

Port Services

Horizontal Integration

Vertical Integration

Maritime ShippingMaritime Shipping

Port Terminal Operations

Port Terminal Operations

Inland Modes and TerminalsInland Modes and Terminals

Distribution Centers

Distribution Centers

Offshorehub

InlandPortPort

Inland Terminals: Operations and Added ValueInland Terminals: Operations and Added Value

CoreCore(Operations)(Operations)

InfrastructureInfrastructure Modal access (dock, siding, road), unloading areas

EquipmentEquipment Intermodal lifting equipment, storing equipment

StorageStorage Yard for empty and loaded containers

ManagementManagement Administration, maintenance, access (gates), information systems

AncillaryAncillary(Added (Added Value)Value)

Trade facilitationTrade facilitation Free trade zone, logistical services

Distribution Distribution centerscenters

Transloading, cross-docking, warehousing, light manufacturing, temperature controlled facilities (cold chain)

Storage depotStorage depot Container depot, bulk storage

Container servicesContainer services Washing, preparation, repair, worthiness certification

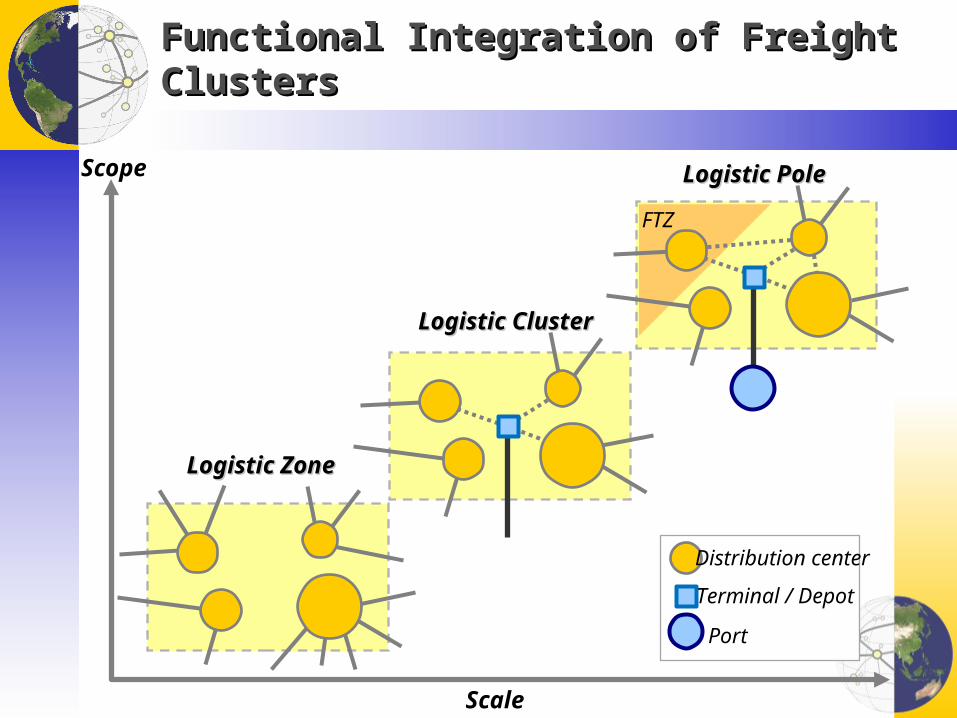

Functional Integration of Freight ClustersFunctional Integration of Freight Clusters

Logistic PoleLogistic Pole

Logistic ZoneLogistic Zone

Scale

Scope

Logistic ClusterLogistic Cluster

FTZ

Terminal / Depot

Distribution center

Port

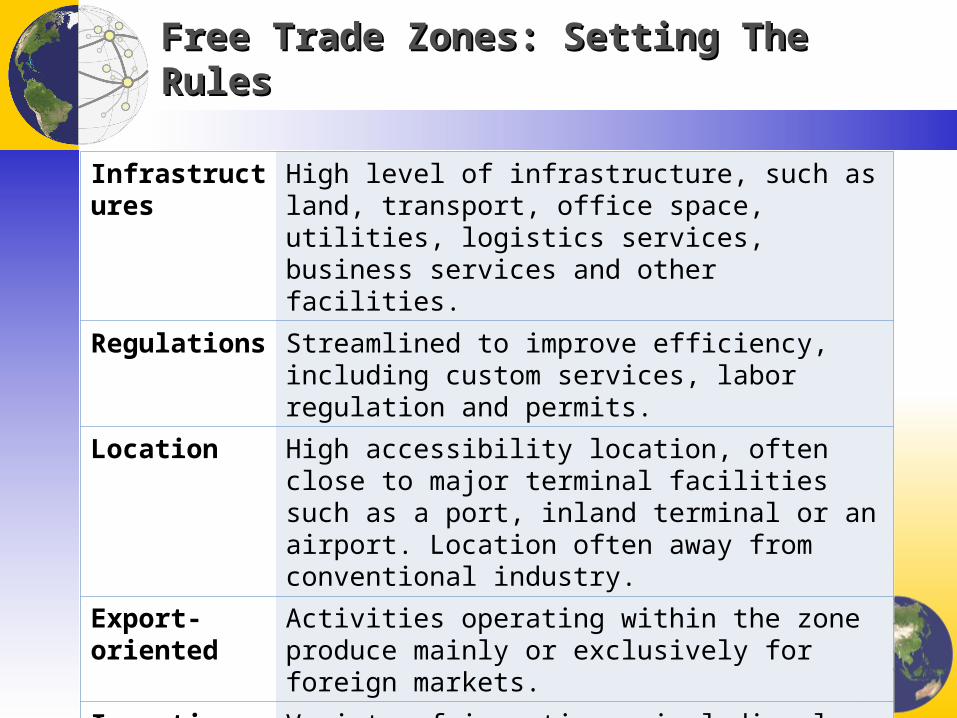

Free Trade Zones: Setting The RulesFree Trade Zones: Setting The Rules

Infrastructures High level of infrastructure, such as land, transport, office space, utilities, logistics services, business services and other facilities.

Regulations Streamlined to improve efficiency, including custom services, labor regulation and permits.

Location High accessibility location, often close to major terminal facilities such as a port, inland terminal or an airport. Location often away from conventional industry.

Export-oriented Activities operating within the zone produce mainly or exclusively for foreign markets.

Incentives Variety of incentives, including low cost land, infrastructures, tax and duty exemptions or various subsidies.

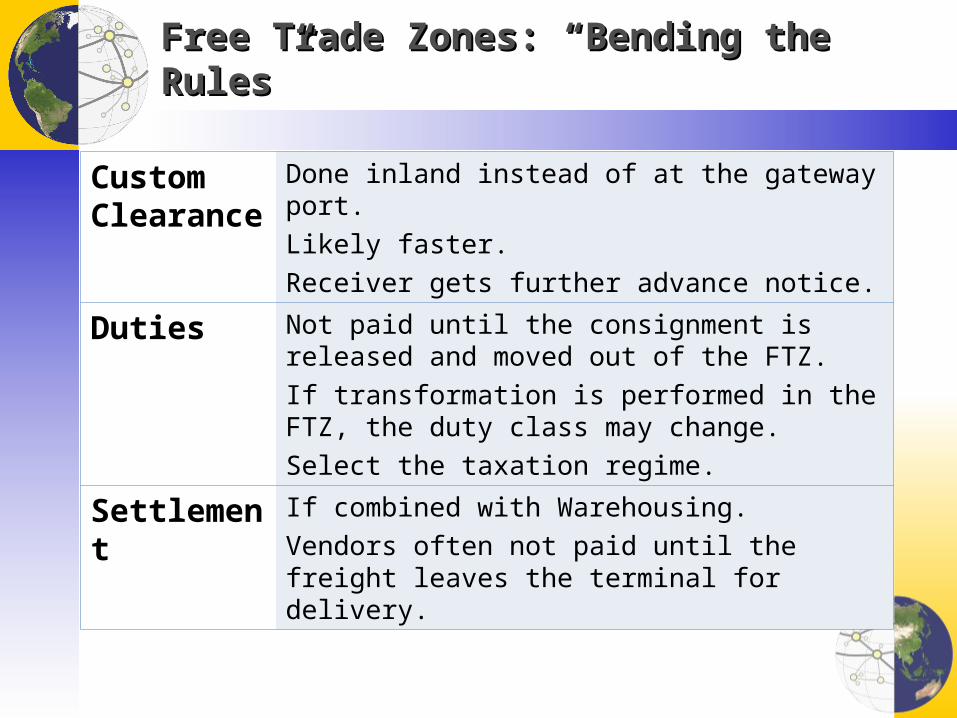

Free Trade Zones: “Bending the Rules”Free Trade Zones: “Bending the Rules”

Custom Clearance

Done inland instead of at the gateway port.Likely faster.Receiver gets further advance notice.

Duties Not paid until the consignment is released and moved out of the FTZ.If transformation is performed in the FTZ, the duty class may change.Select the taxation regime.

Settlement If combined with Warehousing.Vendors often not paid until the freight leaves the terminal for delivery.

Inland Terminals: The Calm after the Storm (lessons Inland Terminals: The Calm after the Storm (lessons to be learned)to be learned)

Rebalancing of the global economyRebalancing of the global economy

Repositioning strategiesRepositioning strategies

Terminalization (intermodal integration)Terminalization (intermodal integration)

Logistics cluster (regional integration)Logistics cluster (regional integration)